casey research perpetual income report

TRANSCRIPT

CASEY RESEARCH PERPETUAL INCOME REPORT

BY NICK GIAMBRUNO

2

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

Dear Investor,

Unfortunately, I have to confirm your suspicions…

The American middle class is dying.

In 2015, it dipped below 50% of the population for the first time since data collection started on this issue. It’s now an official minority group.

Meanwhile, nearly half of Americans don’t have enough money to cover a surprise $400 expense. Many are living paycheck to paycheck, with little to no cushion. And US homes are less affordable than they’ve been in decades – possibly ever.

In this report, I’ll tell you why this is happening, and how it will lead to a genuine crisis… likely soon.

I’ll also show you how to secure your spot among the “haves” as this all plays out. It includes owning the two investment recommendations I’m sharing with you today.

You’ll find all the details in the pages below.

Regards,

Nick Giambruno Chief Analyst, The Casey Report

3

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

LIST OF INVESTMENTSInvestment No. 1 .................................................................................... Walmart (WMT)

Buy Walmart up to $110 per share. Use a 50% trailing stop loss.

Investment No. 2 ............................................................................... ExxonMobil (XOM)

Buy ExxonMobil up to $100 per share. Use a 50% trailing stop loss.

4

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

THE LARGEST MIDDLE CLASS IN WORLD HISTORYThe late 1950s was the golden age of America’s middle class.

This isn’t nostalgia talking. The US really did have robust main streets and thriving small businesses.

Back then, the US produced three-quarters of the world’s cars and airplanes. Americans produced most of the world’s steel and built the majority of the world’s skyscrapers.

Plus, the US stock market held the bulk of the world’s total stock market capitalization.

All this productivity gave the average American an unusually high standard of living.

Around then, a husband could support his family on an average income. He and his wife likely owned their home as well as their car. They had multiple children – and didn’t think much of the cost of having more. Plus, they had money to save.

THE BLEAK SITUATION TODAYCompare that to the average family today. Both spouses likely have to work – whether they want to or not – just to afford the same basic lifestyle.

Plus, it now costs well over $200,000 to raise a child, on average. And that doesn’t even include college costs. Back in 1960, it cost roughly $25,000.

This hefty price tag is one of the main reasons middle class families are having fewer children… or none at all.

In short, the average American’s standard of living has taken a huge hit over the past generation or so.

Consider a typical school teacher’s financial situation, for example.

In 1959, the median annual salary for a US high school teacher was $5,276, according to the Department of Labor. Meanwhile, the median US home value was $9,627, according to the US Census Bureau.

That means a teacher made enough money each year to cover over half of the price of a middle-class home. Or 55%, to be exact.

Take a minute and think… how does your annual income compare to the price of your home? I’d bet many people make far less than 55%.

Today, the median purchase price of a US home is $241,700. To maintain the 1959 income-to-home price ratio, a high school teacher would need to make $132,935 annually.

5

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

Of course, the average high school teacher doesn’t make nearly that much. Not even close. He or she makes around $48,290 – or just enough to cover 36% of the median home price.

IT ALL WENT DOWNHILL IN THE ’70SThe school teacher’s predicament is only one example of a broader trend. In fact, circumstances are actually worse than it lets on.

As you can see in the chart below, the median income-to-home price ratio is just a hair above 20% now. That’s a historical low. And a far cry from the 58% peak it hit in the late 1950s.

Notice that the downtrend starts in the 1970s. More on that shortly…

Clearly, home prices have risen much faster than income levels since 1970.

Of course, Americans haven’t stopped buying homes. They’ve just gone deeper and deeper into debt to do it.

That debt has helped hide the slump in the average person’s standard of living.

Cars are another large expense for Americans. Debt has helped camouflage a big price increase here, too.

Americans now owe over $1.1 trillion in auto debt. This figure has skyrocketed 2,954% since 1971.

Americans have also racked up more than $1 trillion in credit card debt. This debt explosion also started in the early 1970s. Credit card debt is up 14,281% since 1971.

6

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

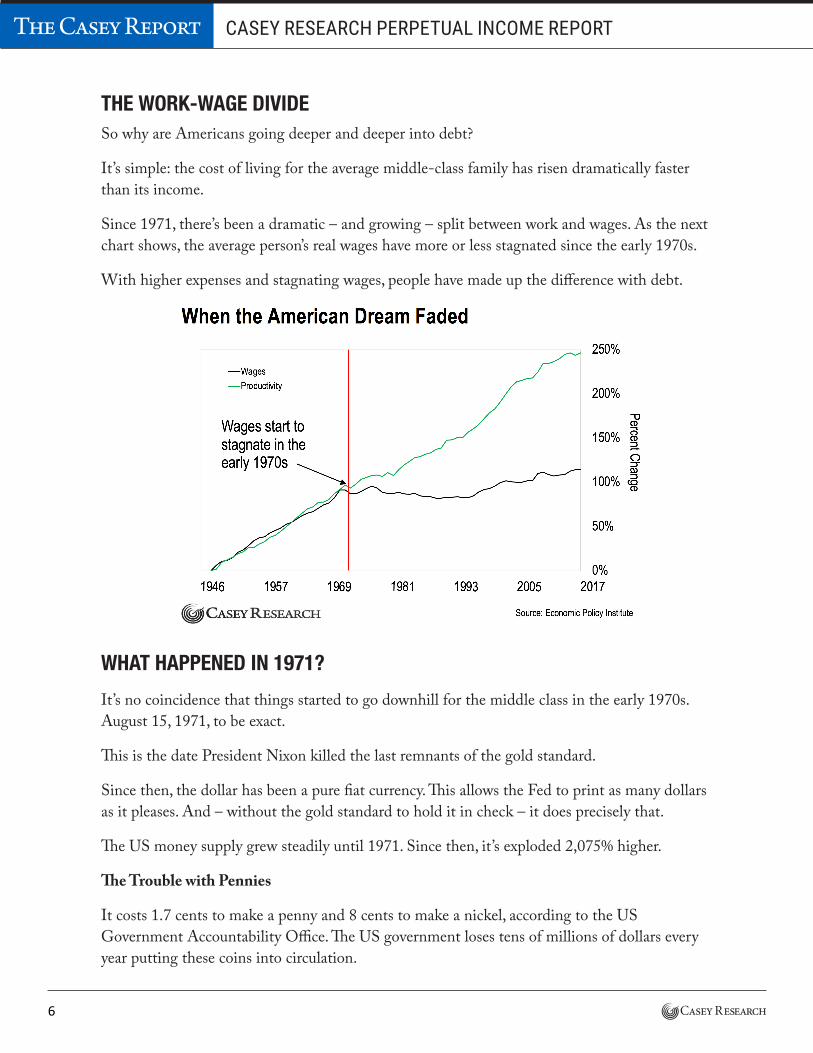

THE WORK-WAGE DIVIDESo why are Americans going deeper and deeper into debt?

It’s simple: the cost of living for the average middle-class family has risen dramatically faster than its income.

Since 1971, there’s been a dramatic – and growing – split between work and wages. As the next chart shows, the average person’s real wages have more or less stagnated since the early 1970s.

With higher expenses and stagnating wages, people have made up the difference with debt.

WHAT HAPPENED IN 1971?

It’s no coincidence that things started to go downhill for the middle class in the early 1970s. August 15, 1971, to be exact.

This is the date President Nixon killed the last remnants of the gold standard.

Since then, the dollar has been a pure fiat currency. This allows the Fed to print as many dollars as it pleases. And – without the gold standard to hold it in check – it does precisely that.

The US money supply grew steadily until 1971. Since then, it’s exploded 2,075% higher.

The Trouble with Pennies

It costs 1.7 cents to make a penny and 8 cents to make a nickel, according to the US Government Accountability Office. The US government loses tens of millions of dollars every year putting these coins into circulation.

7

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

Why bother? Because phasing out the penny and nickel would mean acknowledging currency debasement. And no government wants to do that.

It would reveal the government’s incompetence and make it harder to hide its role in killing the middle class through inflation. This helps the government deny the problem even exists.

Nevertheless, the problem is very real: Federal Reserve has devalued the dollar over 80% since 1969.

There’s an important lesson here: The Federal Reserve and fiat money are mortal enemies of the common man.

Think of the Fed as a colony of termites eating away at the American dream. It’s the main culprit in the death of the middle class.

The Four Tenets of Lasting Wealth

I think this trend will lead to a genuine crisis… and likely soon. Unfortunately, it won’t be pretty.

In the meantime, a perfect storm of economic pressures will further hollow out the middle class. Tens of millions of Americans will be kicked down the ladder.

As Doug Casey puts it:

Most middle-class people will end up joining either the upper or lower class – mostly the lower – and that’ll be a moral disaster for the country.

If you want to firmly establish yourself in the world of the “rich,” I recommend…

• Owning hard assets like physical gold, silver, and certain real estate.

• Owning the highest-quality elite businesses. Think businesses with attractive dividend yields. Even better if you buy these standouts at bargain prices.

• Holding some speculative investments. They can leapfrog your wealth. Think transformative technologies like cryptocurrency and blockchain, the cannabis industry, and natural resource stocks.

• Protecting what you’ve earned from taxation, inflation, and other forms of confiscation by internationalizing your assets. This reduces the threat any one particular government poses to your wealth.

These are the four keys to lasting wealth. They’re time-tested strategies. And they work.

In this report, we’re focusing on the second key: owning the highest-quality elite businesses.

That means Dividend Aristocrats…

8

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

DIVIDEND ARISTOCRATS – HOW TO SECURE YOUR PERPETUAL INCOME STREAMOne of the keys to building lasting wealth has been the same for centuries: owning enduring, high-quality businesses. Think Standard Oil, McDonald’s, Disney, Starbucks, Nestlé, or Coca-Cola.

This isn’t going to change. Enduring, high-quality businesses built the fortunes of Rockefeller, Rothschild, Steve Jobs, and Bill Gates.

The easiest and fastest way to find the highest quality, most elite businesses is to look for Dividend Aristocrats. They’re the safest and strongest companies in the world.

A Dividend Aristocrat is a company that’s increased its dividend for at least 25 consecutive years. A business has to have a strong and sustainable advantage over its competitors to be able to do that. It also shows that a company can manage the ups and downs of the business cycle.

These companies are also better able to pass on price increases. That makes them great inflation hedges. This is especially important for preserving your wealth.

A Dividend Aristocrat is usually a “best of breed” industry dominator with a powerful brand. It’s the kind of company Warren Buffett would put money in… the sort you’d buy for the long-term. Think retirement holdings.

A Dividend Aristocrat is a goose that lays an ever-increasing number of golden eggs. So… they’re rarely cheap. After all, everyone knows they’re the best.

At The Casey Report, we welcome the opportunity to buy Dividend Aristocrats at bargain levels. It’s hard to think of a better investment.

The Dividend Aristocrat Radar is our treasure map…

We use it to find elite businesses at bargain valuations. Owning these companies will help you build your personal financial empire.

Without question, dividends are the single best indicator of true value. Earnings can be unreliable. Flexible accounting rules allow companies to stretch the truth. The right fictions can easily pump up a company’s earnings.

Dividends, on the other hand, are actual cash payments landing in your pocket. You can’t fake that.

So how do we know when a Dividend Aristocrat is cheap enough?

The best way is to compare its current dividend yield to its historical dividend yield. The higher the current yield is, relatively speaking, the more attractive the valuation. Our “sweet spot” is circled in the chart below.

9

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

(Keep in mind, this chart is just an example. We continually update it to find the best dividend payouts.)

The Dividend Aristocrat Radar has helped us pinpoint two outstanding ways to protect and grow your wealth, even during a crisis.

DIVIDEND ARISTOCRAT #1 – WALMART (WMT)Walmart is the world’s biggest retailer. It has over 11,700 locations spanning five continents. It also has a growing online presence.

Walmart is perhaps the only retailer capable of seriously competing with Amazon in the e-commerce space.

Here’s why…

Online sales still only account for less than 10% of all US retail purchases. That means physical stores account for over 90%.

While most traditional retailers (Walmart included) are trying to catch up with Amazon in the online space, Amazon is trying catch up with Walmart’s brick-and-mortar stores. It’s part of the reason Amazon acquired Whole Foods.

I expect Walmart to gradually grow its online presence to better compete with Amazon. But it’s questionable whether Amazon could ever build anything comparable to Walmart’s physical presence.

10

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

Walmart’s physical stores give it a key competitive advantage. Amazon couldn’t even dream of matching it for many years, if ever.

Walmart will thrive in the e-commerce era because of its dominant physical presence and its growing online presence.

Walmart is the Biggest Grocer in the US

Groceries matter. To companies that sell consumers food on a regular basis, it’s an opportunity to upsell and boost their margins. After all, most people buy groceries at least once a week.

Unfortunately for online retailers like Amazon, less than 5% of groceries are sold online. Compare this to roughly 70% of entertainment and books.

Amazon knows this is a problem. Just look at its Whole Foods acquisition and its AmazonFresh service.

But consider this…

With 5,358 US storefronts, Walmart has more physical locations than any other retailer in the country. Meanwhile, Amazon has only 470 stores if you include Whole Foods.

In the US, nearly 90% of the population lives within 10 miles of a Walmart or Sam's Club store. (Walmart owns Sam’s Club.)

It took Walmart many decades and enormous amounts of capital to build out this dense network of stores. This network is how the company dominates the US food retail market. It gives Walmart a remarkable competitive advantage.

But can’t Amazon do the same by simply boosting online grocery sales? Well, that’s easier said than done.

To start, most people still prefer to buy their groceries in person. Aside from habit, there are practical reasons for this. If you need eggs for breakfast, you’re not going to wait a day or two to have them delivered. Plus, you probably like to see things like fish and produce before committing.

Second, Amazon needs a much heavier physical presence to increase its grocery sales. This missing link is one of the reasons AmazonFresh has had problems with late or missed deliveries.

Walmart’s tremendous store density gives it a key advantage over Amazon in the same-day order space. But it’s not all only about groceries…

The Rise of the “Omni-Shopper”

Most people use a mixed shopping strategy. Known as omni-shoppers, they shop in-store and online simultaneously. It’s rapidly becoming the dominant form of retail shopping.

11

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

Amazon knows this. That’s why it’s working to expand its network of physical stores.

However, with its wide physical footprint, Walmart is already in a unique position to move to the front of the omni-shopping trend.

Here are some examples of what it’s doing:

• Walmart bought e-commerce company Jet.com in 2016. This gave it access to a large group of younger, wealthier, urban shoppers. It also marked a significant shift in how the retailer approaches e-commerce. Lastly, Jet’s co-founder Marc Lore, one of the sharpest minds in e-commerce, became the head of Walmart's e-commerce division.

• Walmart started offering discounts to customers who pick up their online orders at a Walmart store (instead of having them shipped).

• Walmart is installing self-service kiosks (pickup towers) in some stores. This makes in-store pickups easier. Customers don’t have to interact with a cashier.

• For home deliveries, Walmart started offering free, two-day shipping on orders $35 and up.

• Walmart added Mobile Express Returns. It allows customers to receive a refund for returned merchandise in less than a minute.

• The company introduced faster checkout processes. Customers at Sam’s Club, for instance, can shop via the Scan & Go app and avoid long check-out lines.

These changes are still new. But they represent multiple avenues for sustained growth.

Remember, 81% of shoppers who collect their online orders at the store end up buying more stuff, according to the International Council of Shopping Centers. Walmart is well-placed to get a boost from these shoppers.

Survival of the Fittest

Amazon dominates e-commerce. It handles about 40% of all online purchases in the US. Walmart is a distant second, for now anyway. It handles 15% of all online transactions.

But whatever Amazon can do, Walmart can emulate. In other words, Walmart has a better shot at becoming Amazon than the other way around.

With its $3.3 billion takeover of Jet.com, Walmart has already made a big move into online retail. But it’s not stopping there.

Since the Jet.com deal, Walmart has dumped billions of dollars into acquisitions – both at home and abroad. It purchased e-commerce businesses such as ShoeBuy (a Zappos competitor in the footwear space), Moosejaw (outdoor retailer), and ModCloth (online women's clothing retailer), among others.

12

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

In an effort to better compete with Amazon, Walmart has also acquired Parcel, a same-day delivery startup.

Aside from e-commerce, Walmart is solidifying its physical store advantage in another key market: China. In 2018, it ranked fifth among leading retail chains in the massive, upwardly mobile country.

Amazon isn’t doing anything close to that in China. In fact, it only has around 1% of China’s online retail market.

By contrast, JD.com (a company Walmart holds a 10% stake in) is the No. 2 online retailer in China. It’s second only to Alibaba. With $67.2 billion in revenue in 2018, it dwarfs Amazon’s tiny market share.

Walmart’s name has also become synonymous with innovation in China.

The company has developed a big online grocery delivery business there. It’s capable of delivering fresh produce to homes within an hour. I expect this to help it build similar capabilities in the US.

Meanwhile, Walmart’s partner JD.com is one of the biggest technology and artificial intelligence-driven delivery companies in China. It has everything from self-driving cars to robots. And it’s building 150 drone airports.

In short, Walmart is light-years ahead of Amazon in China. I expect it to take the lead in key countries like Japan and India, too.

Walmart has partnered with Japanese e-commerce giant Rakuten to launch a grocery delivery service in Japan. The deal also gives Walmart the exclusive rights to sell a line of tablet e-readers from Rakuten Kobo, its Canadian subsidiary. It’s a direct shot at Amazon's Kindle line. Walmart’s subsidiary Seiyu GK and Rakuten have recently opened the first Walmart eCommerce store in the country.

In India, Walmart acquired a majority stake in Flipkart, the country’s leading online retailer.

Amazon is a strong player in India. But it’s still No. 2 to Flipkart in sales. And with only about 2% of India’s retail sales currently happening online, this was the right time to get in.

Planning for the future is essential, but Walmart’s efforts are already bearing fruit. Its domestic online sales grew 43% in the final quarter of 2018. Analysts expect e-commerce to continue to grow this year.

The next chart tracks Walmart’s revenue over the past couple of decades.

13

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

I expect Walmart’s share of the e-commerce market to continue to grow as it chips away at Amazon’s dominance. Meanwhile, the company is set to dominate the omni-channel retail space through its low-cost price model, innovation and strong brick-and-mortar presence.

The company has certainly wiped out a major competitor before…

KMART VS. WALMARTRemember Kmart?

The first Kmart store opened in 1962. In the two decades that followed, Kmart came to dominate retail. It was where young couples bought their first dinette sets and suburban lawn chairs.

But nobody cares about Kmart anymore.

As the story goes, Walmart founder Sam Walton developed the model for his stores by visiting Kmart stores and looking at what he could improve. Walton quickly realized he could defeat his competitor in the low-price game, which Kmart was known for.

Before long, Walmart devised thousands of ways to lower its costs. Then, it passed on those savings to its customers.

Walmart also created a hyper-efficient logistics system, built increasingly larger stores, and squeezed every penny out of every square inch of shelf space. Plus, its sheer volume gave it bargaining power with its suppliers.

Unlike Kmart, Walmart accurately predicted future trends. Embracing technology was a crucial part of this (as it is today).

14

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

Sam Walton wasn’t a computer guy. But he trusted his IT advisers. He also understood the importance of supply chain excellence. Successfully fusing the two was key to Walmart’s eventual victory over Kmart.

Before Walmart came along, most retailers did weekly, manual inventory checks. It was time and labor intensive. It was also prone to error.

Walmart revolutionized this practice. It automatically logged everything customers bought and ordered any necessary new inventory that night.

This seems like the obvious way to do things now. But Walmart’s computerized inventory system was a game-changer when the company introduced it.

It also allowed Walmart to track buying habits and build predictive models of shopping behavior. This gave it an important edge over the competition, Kmart in particular.

Meanwhile, Kmart rested on its laurels. Its shelves were often empty, and its work practices outdated.

This all meant one thing: Walmart sold more and more, while Kmart sold less and less. This went on for decades.

Once a formidable, fast-growing retailer, Kmart filed for bankruptcy in 2002. It was the largest retail bankruptcy case in history. The company later became a unit of Sears Holdings. It’s slipped further into oblivion ever since.

Ultimately, Walmart beat out Kmart – and a lot of other competition. That experience gives it a significant edge in the battle against Amazon.

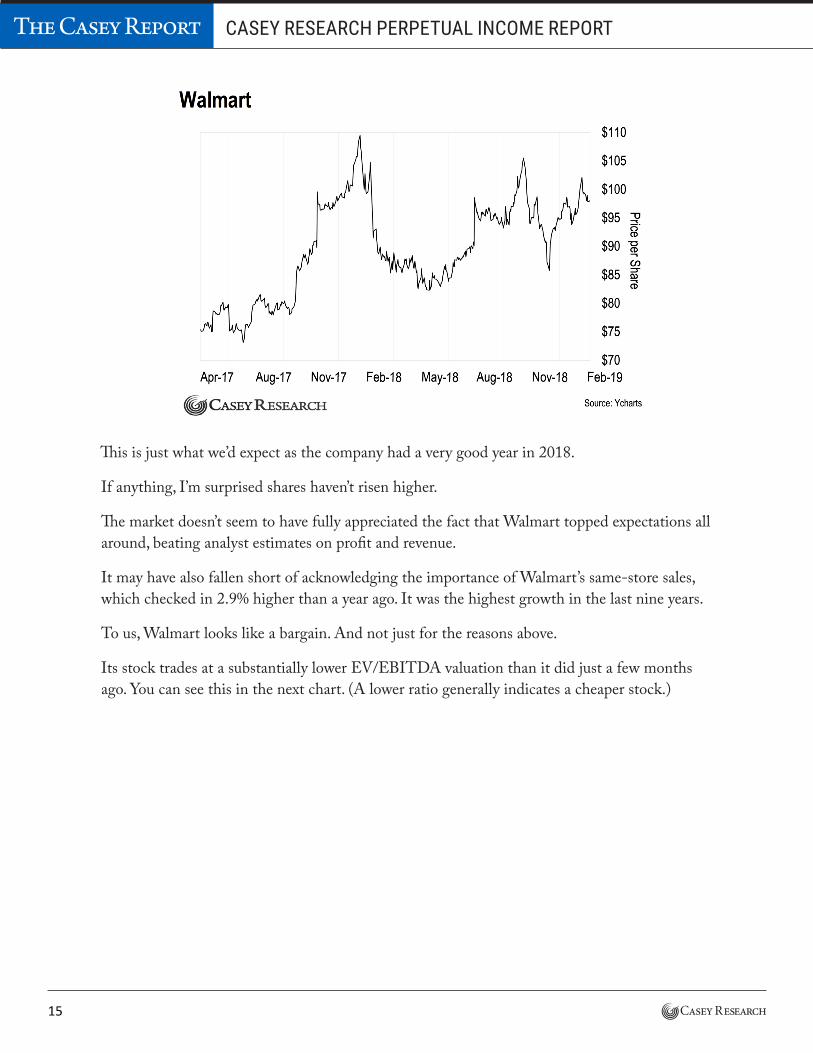

Valuation

The chart below shows Walmart’s stock performance. It’s been in an uptrend for the past year.

15

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

This is just what we’d expect as the company had a very good year in 2018.

If anything, I’m surprised shares haven’t risen higher.

The market doesn’t seem to have fully appreciated the fact that Walmart topped expectations all around, beating analyst estimates on profit and revenue.

It may have also fallen short of acknowledging the importance of Walmart’s same-store sales, which checked in 2.9% higher than a year ago. It was the highest growth in the last nine years.

To us, Walmart looks like a bargain. And not just for the reasons above.

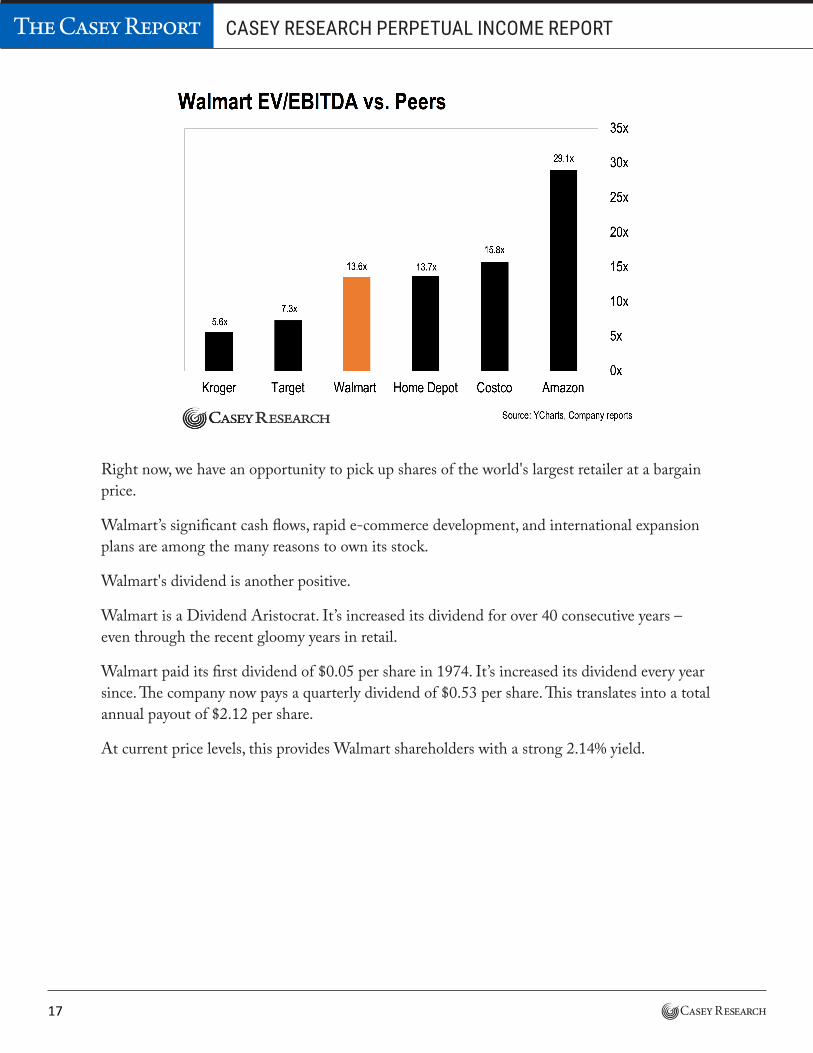

Its stock trades at a substantially lower EV/EBITDA valuation than it did just a few months ago. You can see this in the next chart. (A lower ratio generally indicates a cheaper stock.)

16

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

One Sign of a Cheap Stock

EV stands for “economic value.” It represents the sum of the market value of a company’s debt and equity, less its cash.

EBITDA refers to “earnings before interest, taxes, depreciation, and amortization.”

The ratio of the two, EV/EBITDA, is useful for comparing a company to its peers. All else being equal, a lower ratio indicates a cheaper stock.

The next chart shows EV/EBITDA for Walmart and other large US retail companies, including Amazon.

17

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

Right now, we have an opportunity to pick up shares of the world's largest retailer at a bargain price.

Walmart’s significant cash flows, rapid e-commerce development, and international expansion plans are among the many reasons to own its stock.

Walmart's dividend is another positive.

Walmart is a Dividend Aristocrat. It’s increased its dividend for over 40 consecutive years – even through the recent gloomy years in retail.

Walmart paid its first dividend of $0.05 per share in 1974. It’s increased its dividend every year since. The company now pays a quarterly dividend of $0.53 per share. This translates into a total annual payout of $2.12 per share.

At current price levels, this provides Walmart shareholders with a strong 2.14% yield.

18

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

Risks

The grocery business is generally recession-proof. But grocery sales make up only half of Walmart’s revenue. It also sells consumer goods, home décor and furniture, and many other items. As such, Walmart isn’t immune to economic risk. An economic downturn could hurt sales.

Increasing competition in the retail space is a potential risk to Walmart’s core business. The company’s escalating war with Amazon is the big theme to watch.

We’re also closely watching Walmart’s progress in e-commerce and omni-shopping. This is crucial. Poor performance here would make us re-examine our investment thesis.

Recommendation

Owning Walmart at bargain prices is a key piece to building lasting wealth.

We also like Walmart’s family-business element. As significant shareholders, the Walton heirs have a lot of skin in the game. This means their interests are aligned with those of shareholders.

Buy Walmart (WMT) up to $110 per share. Use a 50% trailing stop loss on the position.

Plan on holding shares for at least a year, potentially much longer depending on how successful the company is with e-commerce and omni-shopping.

19

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

DIVIDEND ARISTOCRAT #2 – EXXONMOBIL (XOM)ExxonMobil is one of the largest oil and gas producers in the world that's not partially or completely owned by a government. It’s also the largest direct descendant of John D. Rockefeller's Standard Oil Company.

ExxonMobil operates on five continents. It produces oil and gas from conventional, unconventional, and deep-water operations. The company also refines much of its own production into a wide range of fuels and chemicals.

Why We Like ExxonMobil

ExxonMobil has a market capitalization of $339 billion. It produces around four million barrels of oil per day. The company has operational centers all over the world and spends millions of dollars every year unlocking new reserves.

ExxonMobil reported a 23% jump in reserves last year. Given the company’s sheer size, it's remarkable that it’s continuing to grow.

Its size also gives it enormous leverage when it negotiates with governments and other players in the oil industry, such as drilling operators.

Resilience

ExxonMobil is an integrated oil company. That means it’s also in the natural gas, coal, and electric power business. Plus, it controls pipelines, transportation, oil refining, and retail service stations.

This is one of the reasons it’s so successful. The stronger-performing segments can offset the weaker ones.

The company’s size and diversified operations give it a wide margin of safety. It has so much access to capital, so many assets, such high production volumes, and such great credit that it would likely survive any crisis that could put many of its peers out of business.

Ability to Acquire Other Companies

ExxonMobil has over $3 billion in cash. Plus, it can easily access the debt and equity markets if it wants to buy something.

If the market begins to turn sour, ExxonMobil has the ability to purchase refineries and oil blocks for pennies on the dollar.

Dividend

ExxonMobil is one of the best-run companies in the world. Its Dividend Aristocrat status attests to this.

20

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

The company has been paying dividends for over a century. And it’s increased them for a big part of that.

The next chart shows how ExxonMobil’s dividend yield compares to those of its peers.

You likely noticed that Total, Royal Dutch Shell, and BP all have higher current dividend yields. But those yields also come with more risk.

None of those companies can match ExxonMobil’s much longer and more consistent track record of dividend growth.

ExxonMobil has raised its dividend for 36 consecutive years. It’s also paid dividends uninterrupted for more than one hundred years.

The company’s dividend has also nearly quadrupled over the last 18 years alone, as you can see in the chart below. The company’s strong revenue stream and reliable multibillion-dollar earnings made that possible.

21

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

ExxonMobil has shown that during tough times, it’s still able to increase payouts. For example, it increased its dividend by 20% during the 2008–2009 recession.

When the price of oil tumbled below $30 per barrel in 2016, many oil companies couldn’t even pay out their dividends, let alone grow them. But not ExxonMobil.

That’s why ExxonMobil is rarely cheap. After all, everyone knows it’s the best.

However, now is one of those rare moments…

Take a look at the next chart on the following page. The red line shows ExxonMobil’s current dividend yield. The black line shows its historical dividend yield.

22

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

The company’s current dividend yield is 4.1%. Note that it hasn’t been this consistently high since the 1990s.

A 4.1% yield from an elite company like ExxonMobil is nothing to sneeze at. It’s more than double that of the S&P 500.

At the very least, we can expect ExxonMobil’s dividend yield to continue to gradually grow. If turmoil develops in the Middle East, as I expect it to, it could rocket even higher.

Price

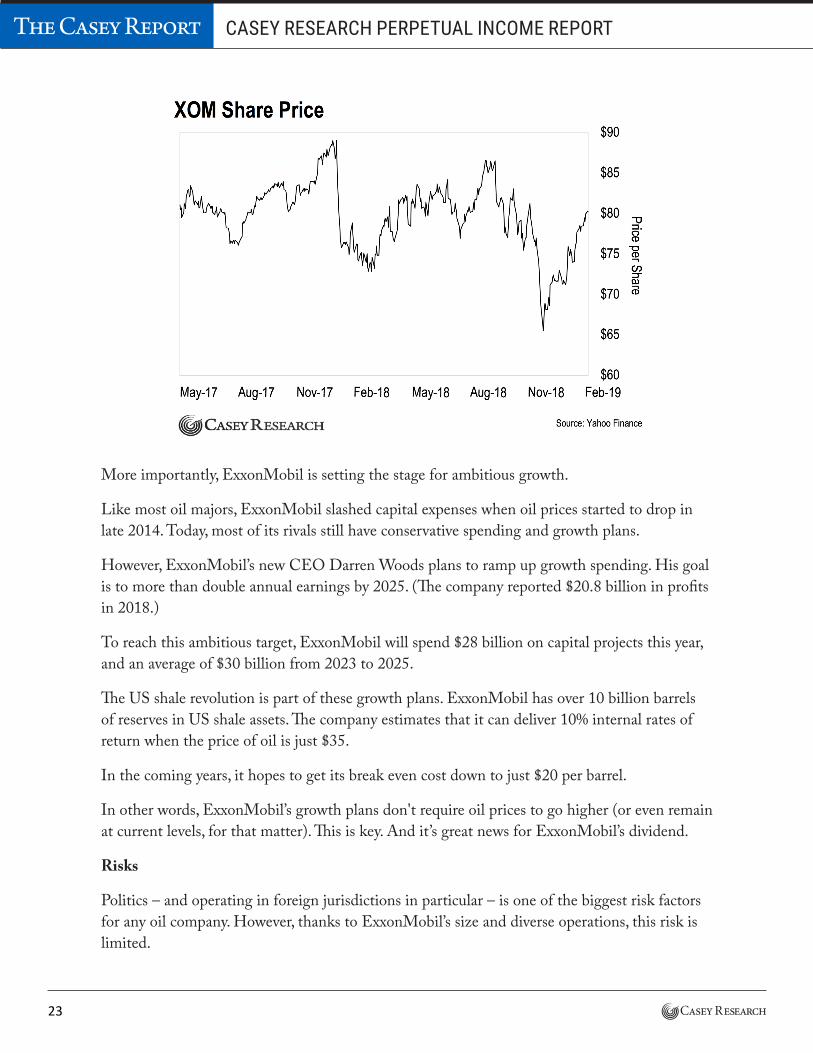

The market has noticed ExxonMobil’s positive operating results. Its share price is up roughly 15% since January 2019, as of this writing. However, it’s still relatively low compared to recent past highs, as you can see in the chart below on the following page.

23

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

More importantly, ExxonMobil is setting the stage for ambitious growth.

Like most oil majors, ExxonMobil slashed capital expenses when oil prices started to drop in late 2014. Today, most of its rivals still have conservative spending and growth plans.

However, ExxonMobil’s new CEO Darren Woods plans to ramp up growth spending. His goal is to more than double annual earnings by 2025. (The company reported $20.8 billion in profits in 2018.)

To reach this ambitious target, ExxonMobil will spend $28 billion on capital projects this year, and an average of $30 billion from 2023 to 2025.

The US shale revolution is part of these growth plans. ExxonMobil has over 10 billion barrels of reserves in US shale assets. The company estimates that it can deliver 10% internal rates of return when the price of oil is just $35.

In the coming years, it hopes to get its break even cost down to just $20 per barrel.

In other words, ExxonMobil’s growth plans don't require oil prices to go higher (or even remain at current levels, for that matter). This is key. And it’s great news for ExxonMobil’s dividend.

Risks

Politics – and operating in foreign jurisdictions in particular – is one of the biggest risk factors for any oil company. However, thanks to ExxonMobil’s size and diverse operations, this risk is limited.

24

CASEY RESEARCH PERPETUAL INCOME REPORTThe Casey Report

To contact us, call toll free Domestic/International: 1-888-512-2739, Mon-Fri: 9am-7pm ET, or email us here.

© 2019 Casey Research, 455 NE 5th Ave, Suite D317, Delray Beach, FL 33483, USA. All rights reserved. Any reproduction, copying, or redistribution, in whole or in part, is prohibited without written permission from the publisher.

Information contained herein is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your personal situation—we are not financial advisors nor do we give personalized advice. The opinions expressed herein are those of the publisher and are subject to change without notice. It may become outdated and there is no obligation to update any such information.

Recommendations in Casey Research publications should be made only after consulting with your advisor and only after reviewing the prospectus or financial statements of the company in question. You shouldn’t make any decision based solely on what you read here.

Casey Research writers and publications do not take compensation in any form for covering those securities or commodities.

Casey Research expressly forbids its writers from owning or having an interest in any security that they recommend to their readers. Furthermore, all other employees and agents of Casey Research and its affiliate companies must wait 24 hours before following an initial recommendation published on the Internet, or 72 hours after a printed publication is mailed.

The company’s operations are spread across five continents. A revolution, war, nationalization, or militant attack in any given country could cripple smaller companies. But these things are often no more than a pinch to ExxonMobil.

Because of its size and diversification, ExxonMobil can do business in risky jurisdictions… and often it pays off very well for shareholders.

Another risk factor comes from electric cars. Faster than expected adoption rates could hurt the oil industry.

I’m watching this situation closely. But I don’t think it poses an imminent risk to ExxonMobil or its dividend.

In any case, ExxonMobil is also a major producer of natural gas. And higher electricity use would increase demand for natural gas.

There is also the risk of another major downturn in oil prices. But given the rising tensions we see in the Middle East, I think this is unlikely.

Even so, if oil prices did fall drastically, ExxonMobil could lean on its diversified downstream operations to help weather the storm, just as it’s done in the past.

ExxonMobil’s current price is giving us a great entry point into one of the most elite businesses in the world. We’re also locking in a yield that’s more than double that of the S&P 500 – and is set to grow much higher.

Recommendation

Buy ExxonMobil (XOM) up to $100 per share. Use a 50% trailing stop loss on the position.

Plan on holding shares for at least a year, potentially much longer.