cb insights asia-tech-investment-report

TRANSCRIPT

THE ASIA TECH INVESTMENT REPORTA comprehensive, data-driven look at technology investment trends, top deals,

active investors and strategic activity in Asia.

May 23, 2017

The technology market intelligence platform.

CB Insights software lets you predict, discuss, and

communicate emerging technology trends using data in ways that are beyond human cognition.

www.cbinsights.com 2

www.cbinsights.com 3See what other customers have to say at http://www.cbinsights.com/customer-love

The most publicly reference-able customers of anyone in the industry

A FEW OF OUR HAPPY CUSTOMERS

Kate Barrett

Director, New Enterprise Associates

“With CB Insights we can quickly and reliably aggregate data across the investing landscape, from sector trends to financing activity. The intuitive user interface and robust set of features have made it a go-to resource for our team, and the customer support is second to none...”

www.cbinsights.com 4

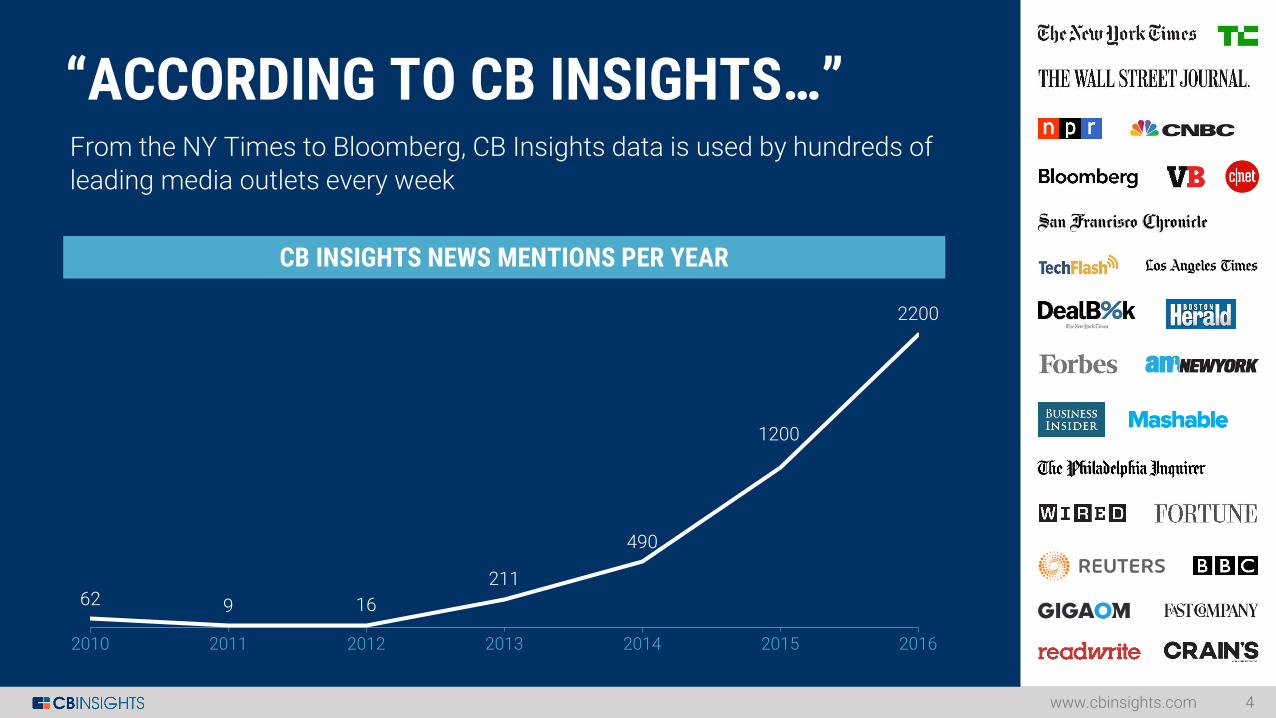

From the NY Times to Bloomberg, CB Insights data is used by hundreds of

leading media outlets every week

“ACCORDING TO CB INSIGHTS…”

CB INSIGHTS NEWS MENTIONS PER YEAR

62 9 16

211

490

1200

2200

2010 2011 2012 2013 2014 2015 2016

www.cbinsights.com 5

TABLE OF CONTENTS

Asia Financing Trends

China Financing Trends

India Financing Trends

Southeast Asia Financing Trends

8

32

40

47

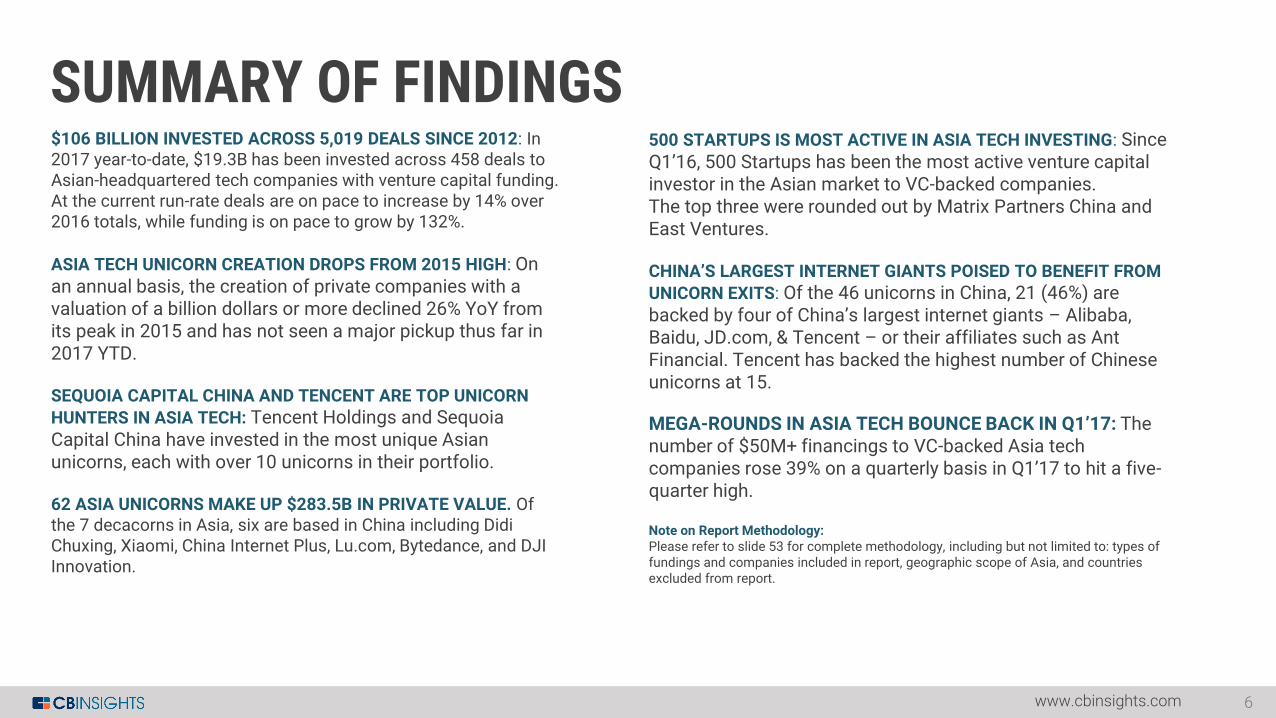

SUMMARY OF FINDINGS

6www.cbinsights.com

500 STARTUPS IS MOST ACTIVE IN ASIA TECH INVESTING: Since Q1’16, 500 Startups has been the most active venture capital investor in the Asian market to VC-backed companies. The top three were rounded out by Matrix Partners China and East Ventures.

CHINA’S LARGEST INTERNET GIANTS POISED TO BENEFIT FROM

UNICORN EXITS: Of the 46 unicorns in China, 21 (46%) are backed by four of China’s largest internet giants – Alibaba, Baidu, JD.com, & Tencent – or their affiliates such as Ant Financial. Tencent has backed the highest number of Chinese unicorns at 15.

MEGA-ROUNDS IN ASIA TECH BOUNCE BACK IN Q1’17: The number of $50M+ financings to VC-backed Asia tech companies rose 39% on a quarterly basis in Q1’17 to hit a five-quarter high.

Note on Report Methodology:Please refer to slide 53 for complete methodology, including but not limited to: types of fundings and companies included in report, geographic scope of Asia, and countries excluded from report.

$106 BILLION INVESTED ACROSS 5,019 DEALS SINCE 2012: In 2017 year-to-date, $19.3B has been invested across 458 deals to Asian-headquartered tech companies with venture capital funding. At the current run-rate deals are on pace to increase by 14% over 2016 totals, while funding is on pace to grow by 132%.

ASIA TECH UNICORN CREATION DROPS FROM 2015 HIGH: On an annual basis, the creation of private companies with a valuation of a billion dollars or more declined 26% YoY from its peak in 2015 and has not seen a major pickup thus far in 2017 YTD.

SEQUOIA CAPITAL CHINA AND TENCENT ARE TOP UNICORN

HUNTERS IN ASIA TECH: Tencent Holdings and Sequoia Capital China have invested in the most unique Asian unicorns, each with over 10 unicorns in their portfolio.

62 ASIA UNICORNS MAKE UP $283.5B IN PRIVATE VALUE. Of the 7 decacorns in Asia, six are based in China including Didi Chuxing, Xiaomi, China Internet Plus, Lu.com, Bytedance, and DJI Innovation.

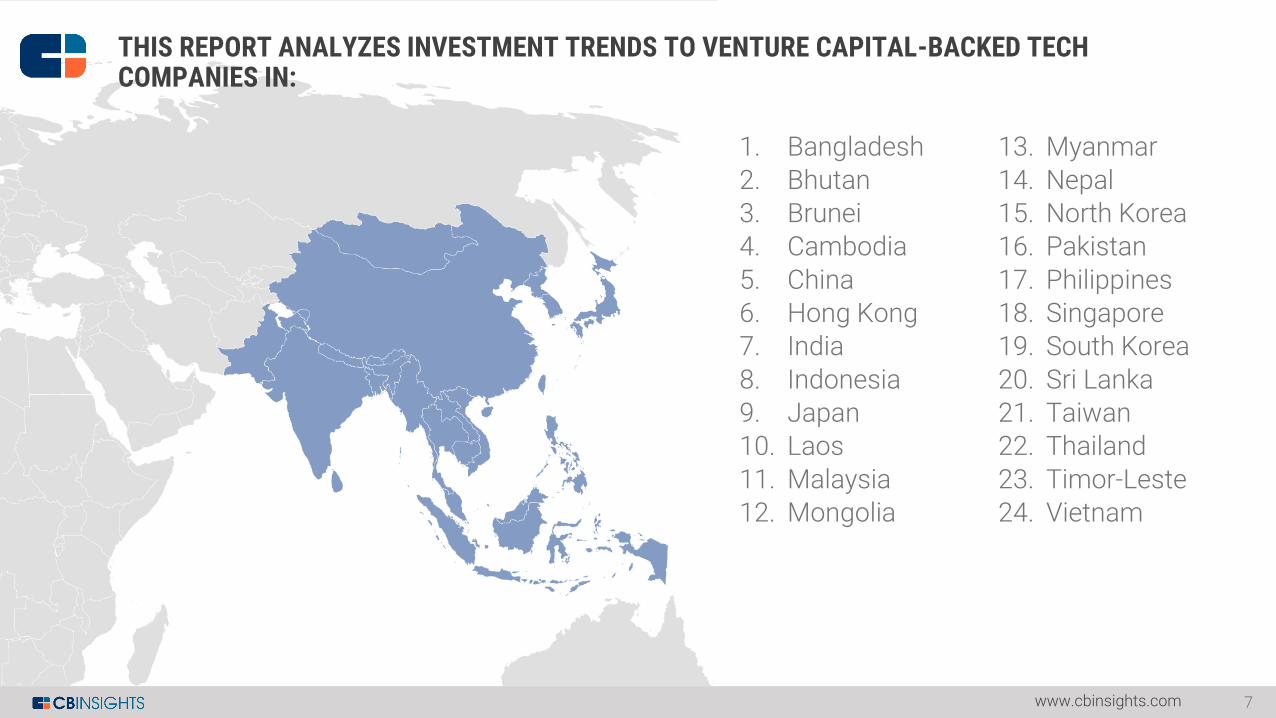

THIS REPORT ANALYZES INVESTMENT TRENDS TO VENTURE CAPITAL-BACKED TECH COMPANIES IN:

7www.cbinsights.com

1. Bangladesh

2. Bhutan3. Brunei4. Cambodia

5. China6. Hong Kong7. India

8. Indonesia9. Japan10. Laos

11. Malaysia12. Mongolia

13. Myanmar

14. Nepal15. North Korea16. Pakistan

17. Philippines18. Singapore19. South Korea

20. Sri Lanka21. Taiwan22. Thailand

23. Timor-Leste24. Vietnam

ASIATECH INVESTMENT TRENDS

www.cbinsights.com 8

Since 2012, VC-backed Asia tech startups have raised:

$106.2 BILLIONacross

5,019 DEALSwww.cbinsights.com 9

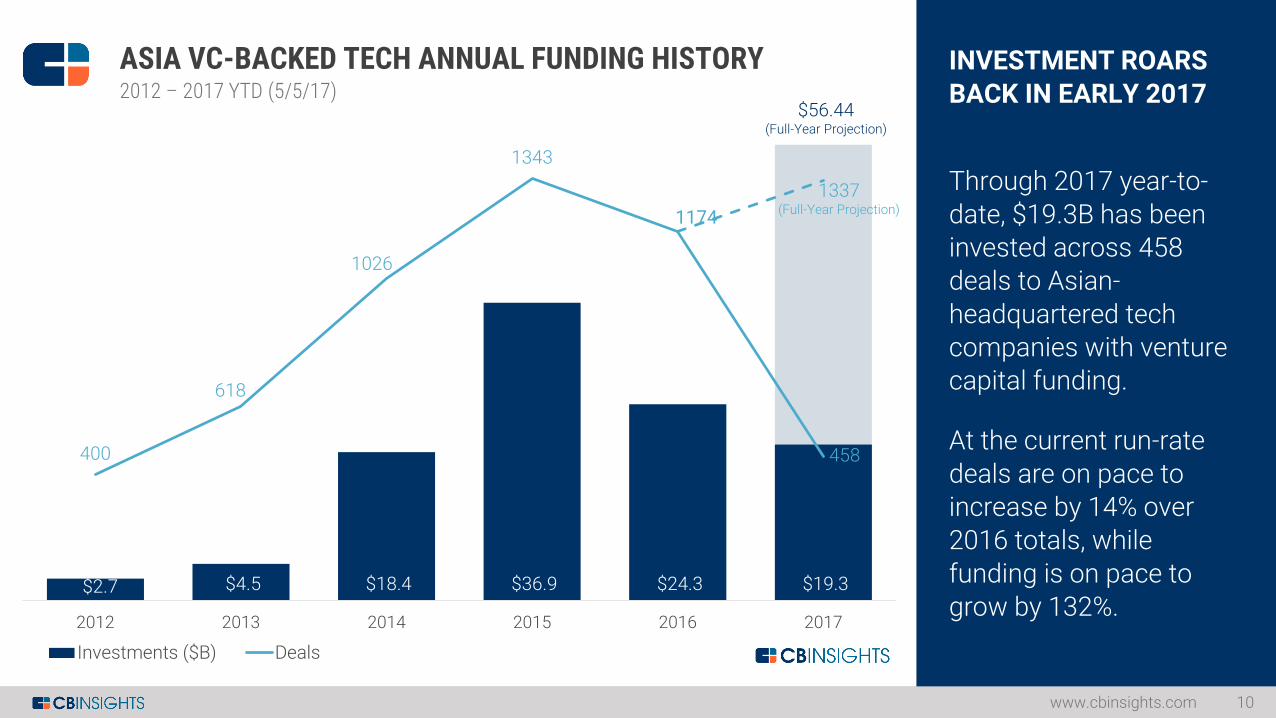

ASIA VC-BACKED TECH ANNUAL FUNDING HISTORY INVESTMENT ROARS

BACK IN EARLY 2017

Through 2017 year-to-

date, $19.3B has been invested across 458 deals to Asian-

headquartered tech companies with venture capital funding.

At the current run-rate

deals are on pace to increase by 14% over 2016 totals, while

funding is on pace to grow by 132%.

www.cbinsights.com 10

2012 – 2017 YTD (5/5/17)

$2.7 $4.5 $18.4 $36.9 $24.3 $19.3

400

618

1026

1343

1174

458

2012 2013 2014 2015 2016 2017

Investments ($B) Deals

$56.44(Full-Year Projection)

1337(Full-Year Projection)

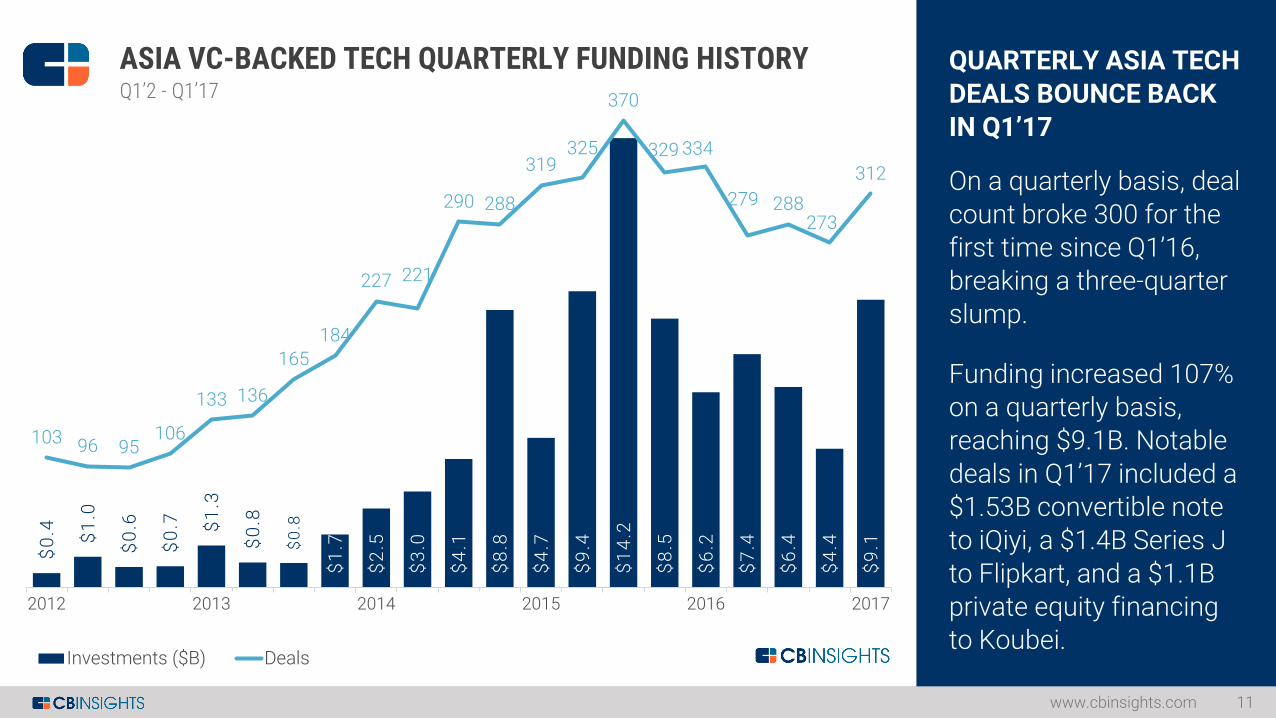

QUARTERLY ASIA TECH

DEALS BOUNCE BACK IN Q1’17

On a quarterly basis, deal

count broke 300 for the first time since Q1’16, breaking a three-quarter

slump.

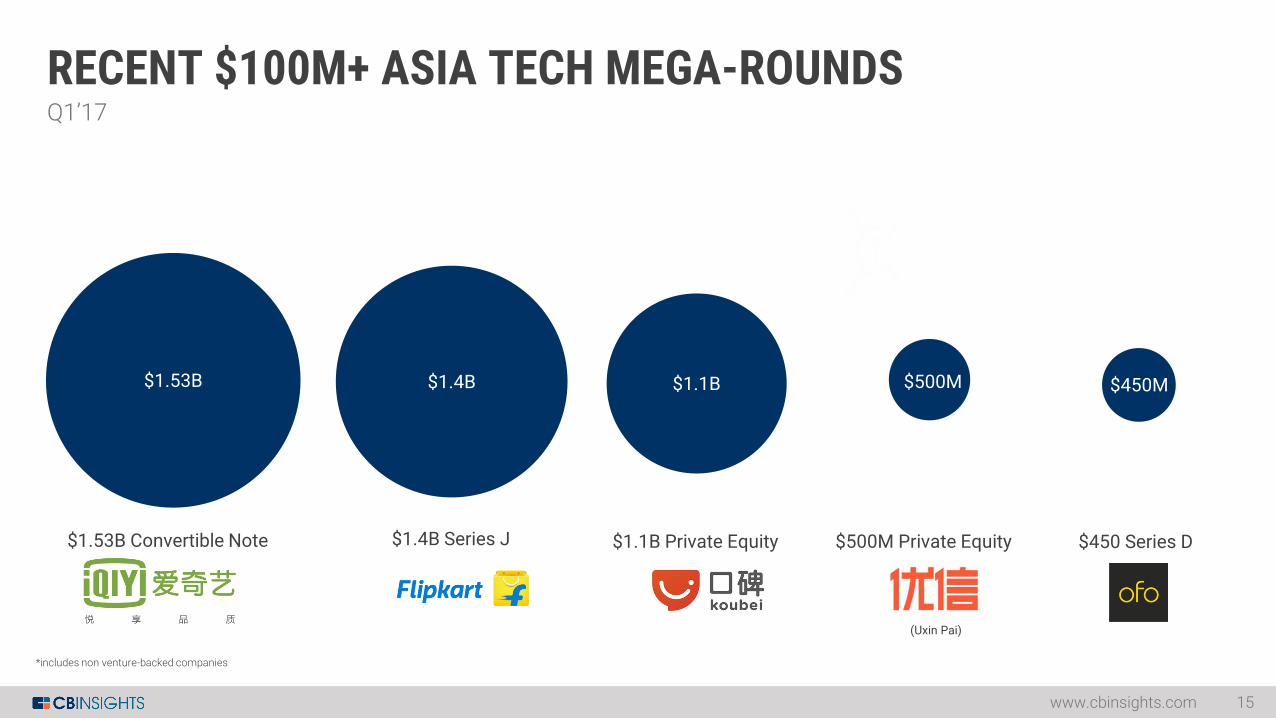

Funding increased 107% on a quarterly basis, reaching $9.1B. Notable

deals in Q1’17 included a $1.53B convertible note to iQiyi, a $1.4B Series J

to Flipkart, and a $1.1B private equity financing to Koubei.

www.cbinsights.com 11

ASIA VC-BACKED TECH QUARTERLY FUNDING HISTORYQ1’2 - Q1’17

$0

.4

$1

.0

$0

.6

$0

.7

$1

.3

$0

.8

$0

.8

$1

.7

$2

.5

$3

.0

$4

.1

$8

.8

$4

.7

$9

.4

$1

4.2

$8

.5

$6

.2

$7

.4

$6

.4

$4

.4

$9

.1

103 96 95106

133 136

165

184

227 221

290 288

319325

370

329 334

279 288273

312

2012 2013 2014 2015 2016 2017

Investments ($B) Deals

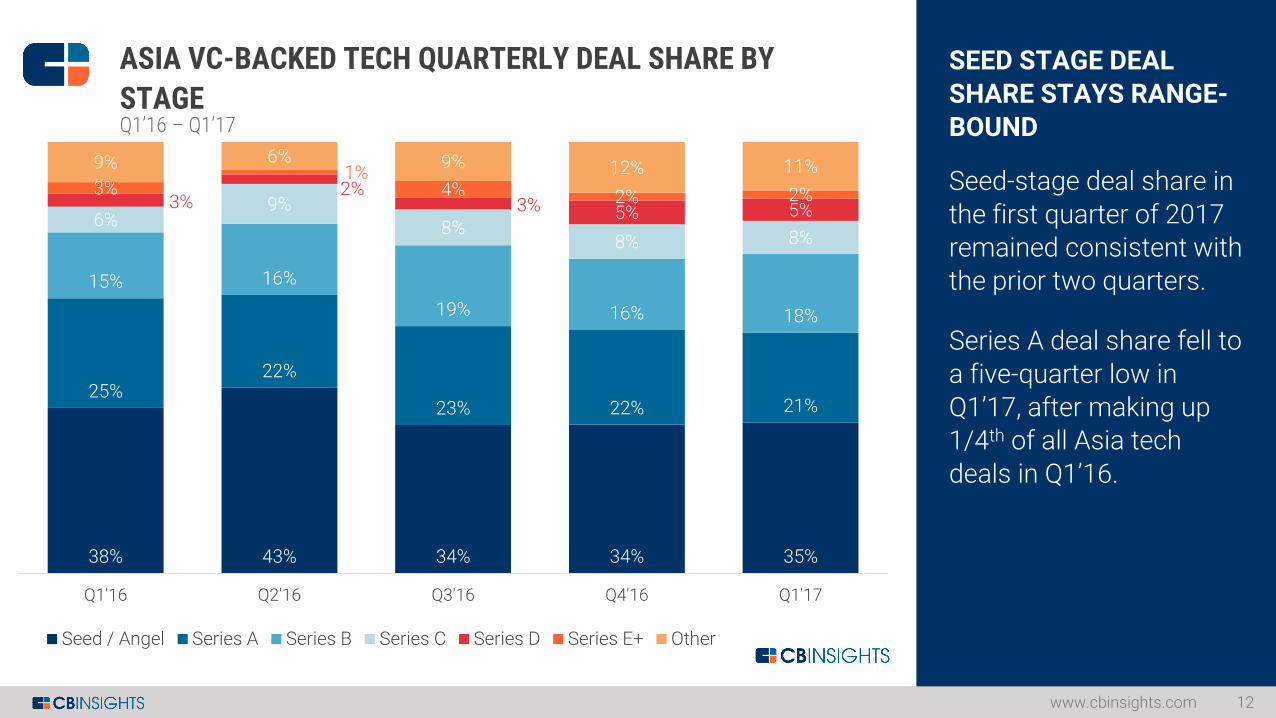

38% 43% 34% 34% 35%

25%22%

23% 22% 21%

15% 16%

19% 16% 18%

6%9%

8%8% 8%

3%2%

3% 5% 5%3%

1%4% 2% 2%

9% 6% 9% 12% 11%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Seed / Angel Series A Series B Series C Series D Series E+ Other

SEED STAGE DEAL

SHARE STAYS RANGE-BOUND

Seed-stage deal share in

the first quarter of 2017 remained consistent with the prior two quarters.

Series A deal share fell to

a five-quarter low in Q1’17, after making up 1/4th of all Asia tech

deals in Q1’16.

www.cbinsights.com 12

ASIA VC-BACKED TECH QUARTERLY DEAL SHARE BY

STAGEQ1’16 – Q1’17

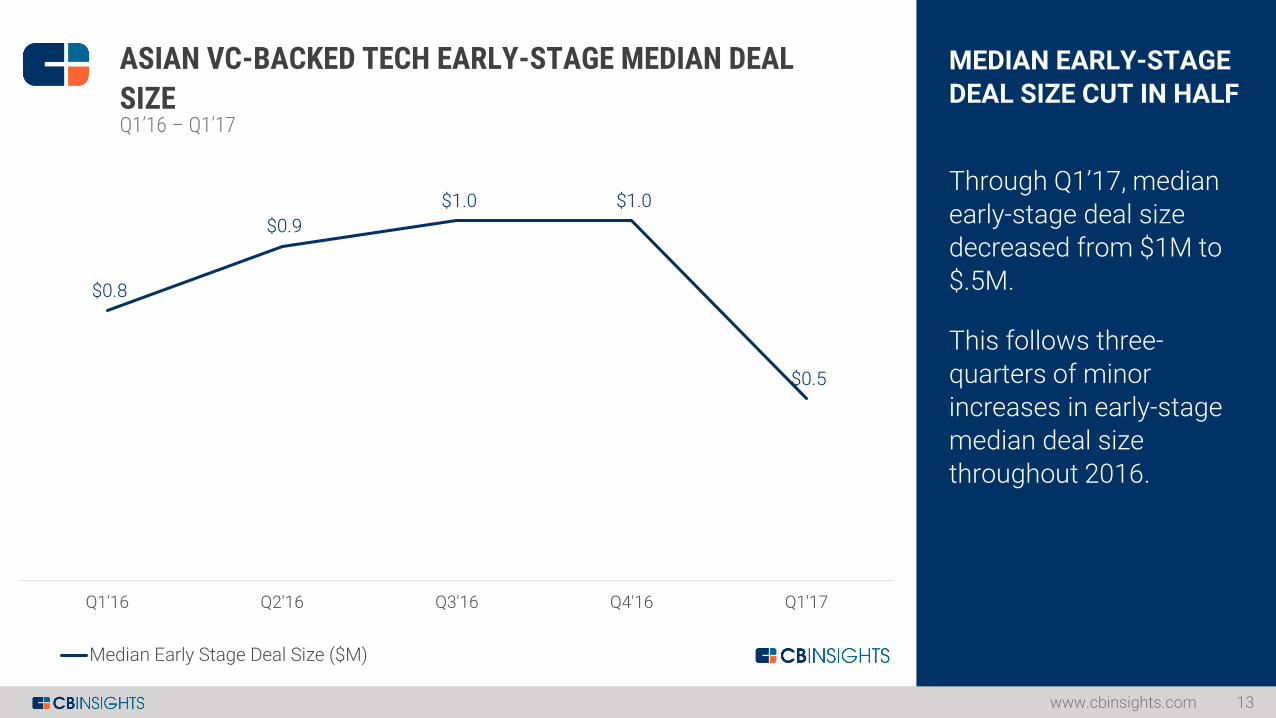

$0.8

$0.9

$1.0 $1.0

$0.5

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Median Early Stage Deal Size ($M)

MEDIAN EARLY-STAGE

DEAL SIZE CUT IN HALF

Through Q1’17, median

early-stage deal size decreased from $1M to $.5M.

This follows three-

quarters of minor increases in early-stage median deal size

throughout 2016.

www.cbinsights.com 13

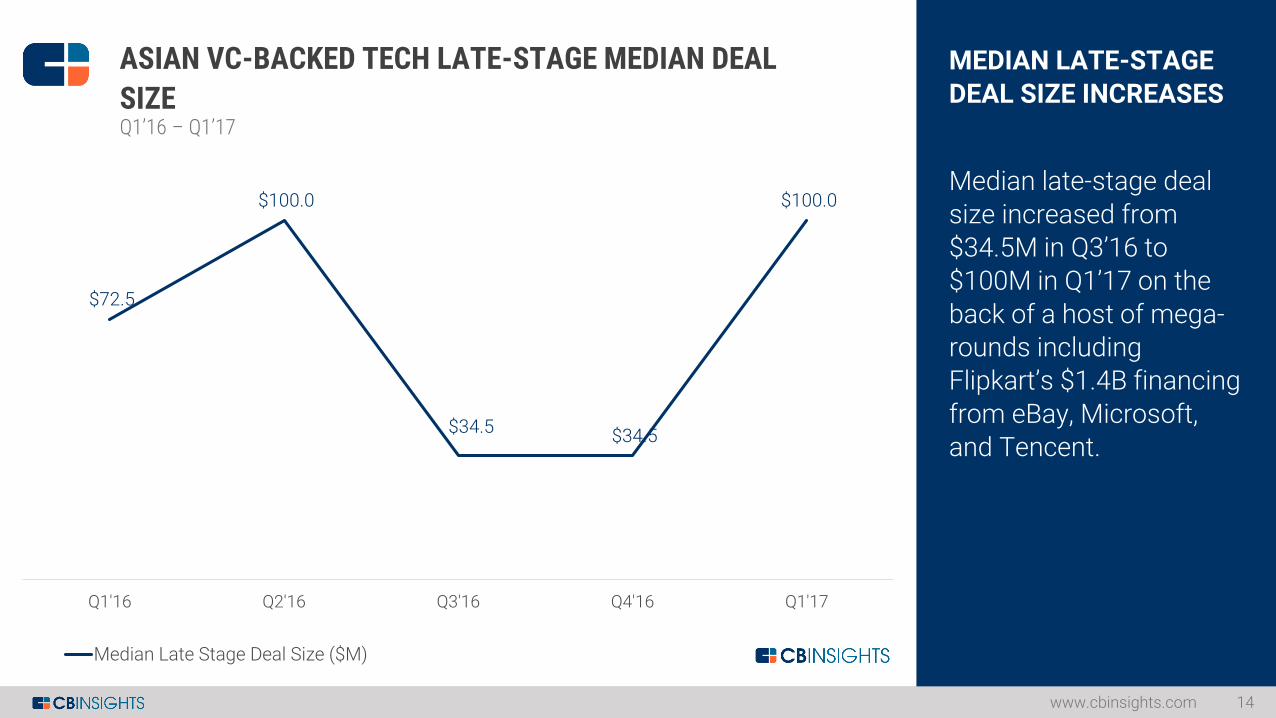

ASIAN VC-BACKED TECH EARLY-STAGE MEDIAN DEAL

SIZEQ1’16 – Q1’17

$72.5

$100.0

$34.5 $34.5

$100.0

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Median Late Stage Deal Size ($M)

MEDIAN LATE-STAGE

DEAL SIZE INCREASES

Median late-stage deal

size increased from $34.5M in Q3’16 to $100M in Q1’17 on the

back of a host of mega-rounds including Flipkart’s $1.4B financing

from eBay, Microsoft, and Tencent.

www.cbinsights.com 14

ASIAN VC-BACKED TECH LATE-STAGE MEDIAN DEAL

SIZEQ1’16 – Q1’17

RECENT $100M+ ASIA TECH MEGA-ROUNDS

www.cbinsights.com 15

Q1’17

450Series D

$1.53B

$1.53B Convertible Note

$1.4B

$1.4B Series J

$1.1B

$1.1B Private Equity $500M Private Equity $450 Series D

(Uxin Pai)

$500M $450M

*includes non venture-backed companies

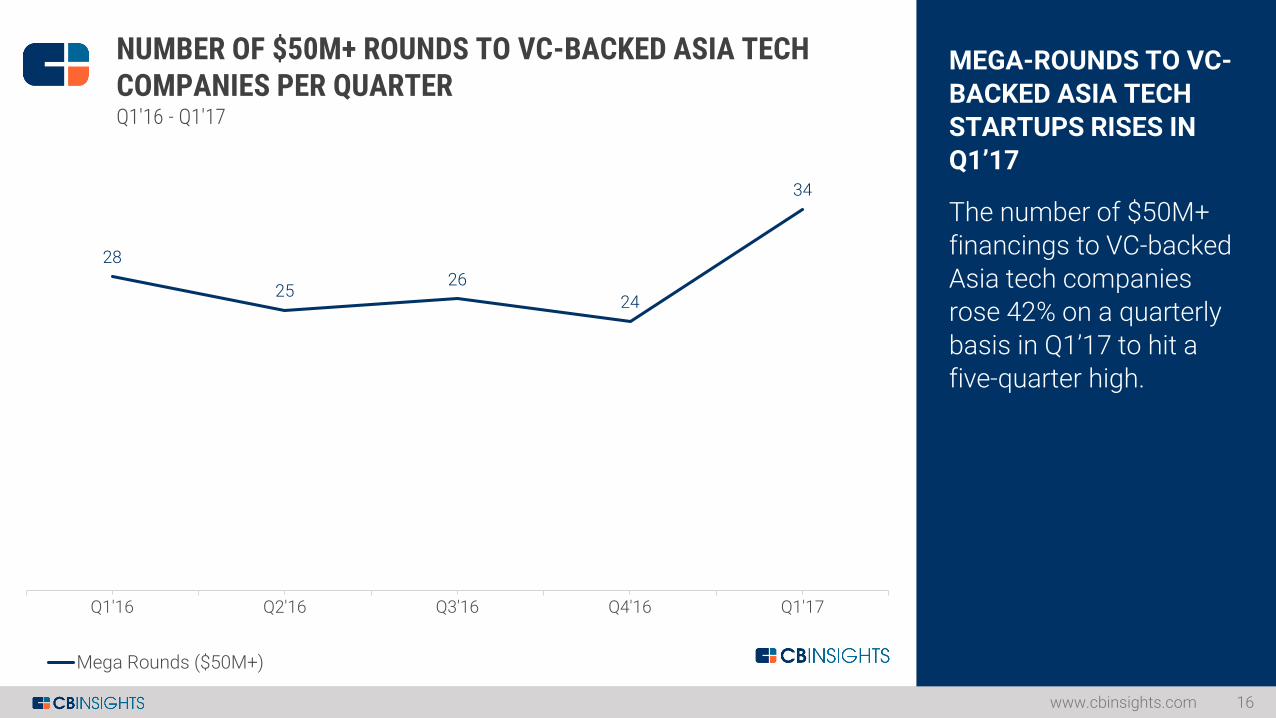

MEGA-ROUNDS TO VC-

BACKED ASIA TECH STARTUPS RISES IN Q1’17

The number of $50M+

financings to VC-backed Asia tech companies rose 42% on a quarterly

basis in Q1’17 to hit a five-quarter high.

www.cbinsights.com 16

28

2526

24

34

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

NUMBER OF $50M+ ROUNDS TO VC-BACKED ASIA TECH COMPANIES PER QUARTERQ1'16 - Q1'17

Mega Rounds ($50M+)

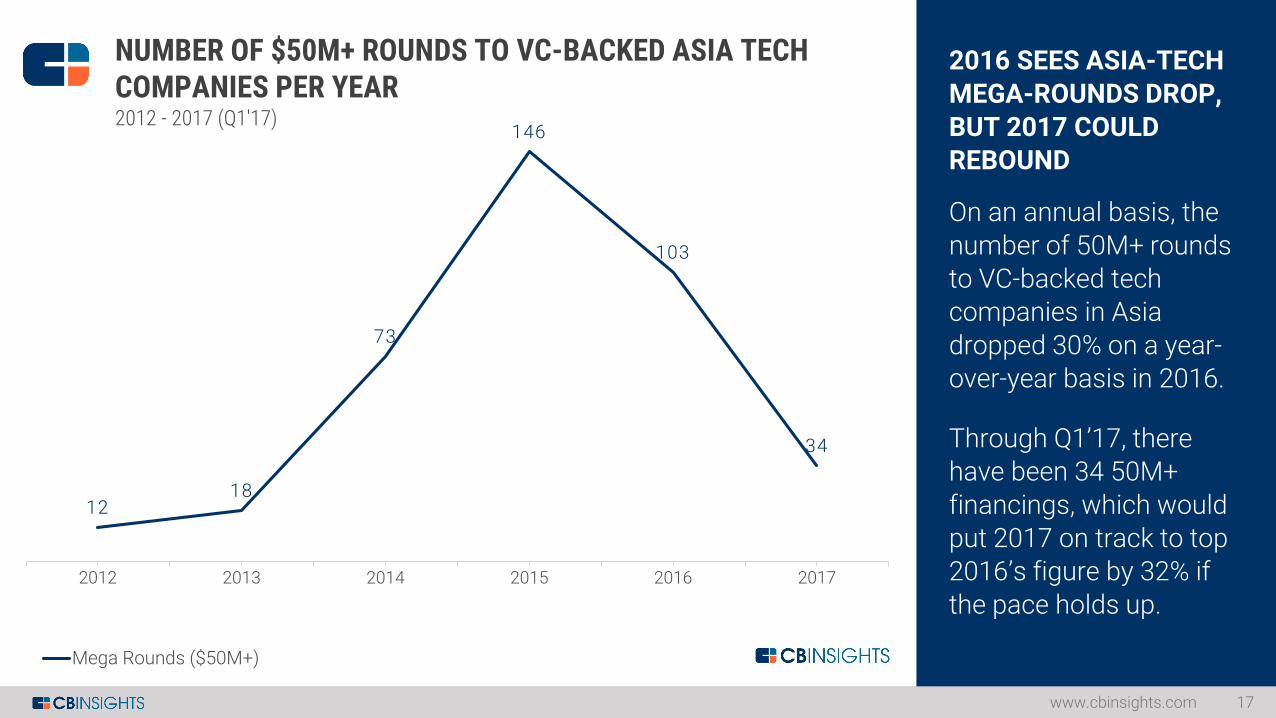

2016 SEES ASIA-TECH

MEGA-ROUNDS DROP, BUT 2017 COULD REBOUND

On an annual basis, the

number of 50M+ rounds to VC-backed tech companies in Asia

dropped 30% on a year-over-year basis in 2016.

Through Q1’17, there have been 34 50M+

financings, which would put 2017 on track to top 2016’s figure by 32% if

the pace holds up.

www.cbinsights.com 17

1218

73

146

103

34

2012 2013 2014 2015 2016 2017

NUMBER OF $50M+ ROUNDS TO VC-BACKED ASIA TECH COMPANIES PER YEAR2012 - 2017 (Q1'17)

Mega Rounds ($50M+)

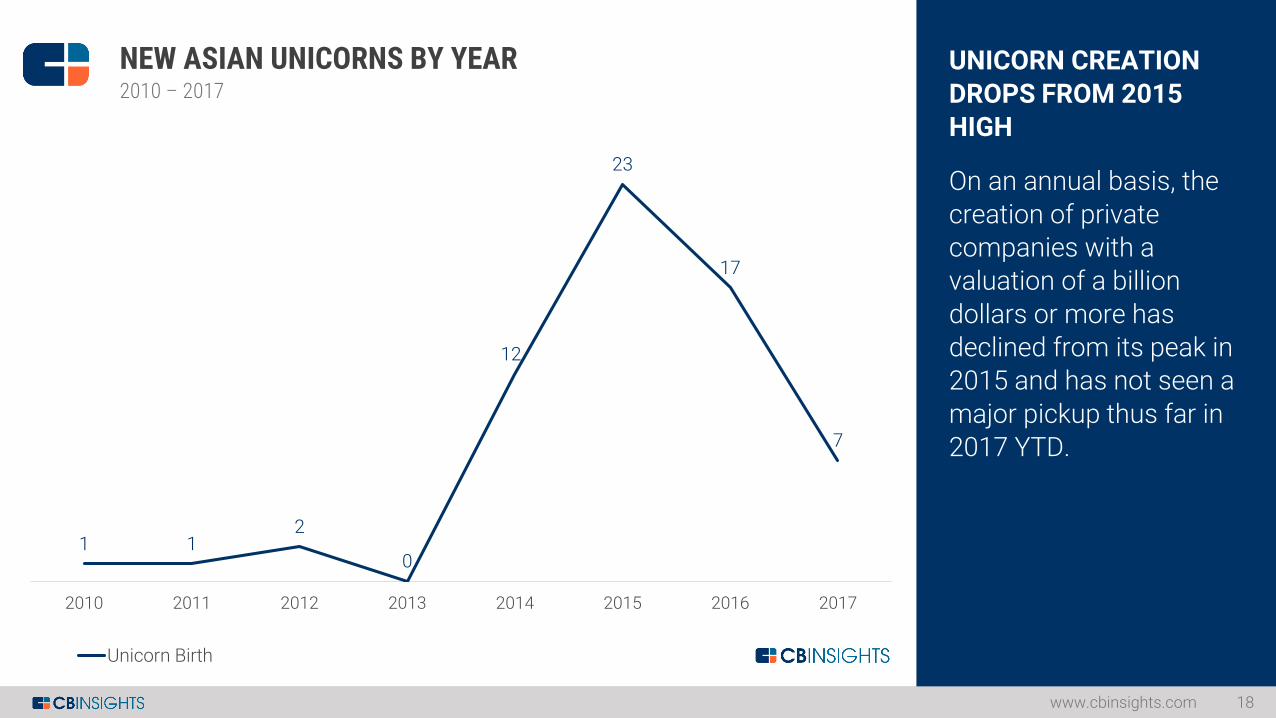

UNICORN CREATION

DROPS FROM 2015 HIGH

On an annual basis, the

creation of private companies with a valuation of a billion

dollars or more has declined from its peak in 2015 and has not seen a

major pickup thus far in 2017 YTD.

www.cbinsights.com 18

NEW ASIAN UNICORNS BY YEAR 2010 – 2017

1 12

0

12

23

17

7

2010 2011 2012 2013 2014 2015 2016 2017

Unicorn Birth

$5

0.0

$4

6.0

$2

0.0

$1

8.5

$1

1.6

$1

1.0

$1

0.0

$8

.0

$7

.0

$5

.9

$5

.8

$5

.0 $

4.6

$4

.5

$4

.0

$3

.8

$3

.5

$3

.0

$3

.0

$3

.0

$3

.0

$3

.0

$2

.9

$2

.0

$2

.0

$2

.0

$2

.0

$1

.8

$1

.6

$1

.5

$1

.5

$1

.4

$1

.4

$1

.2

$1

.1

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

$1

.0

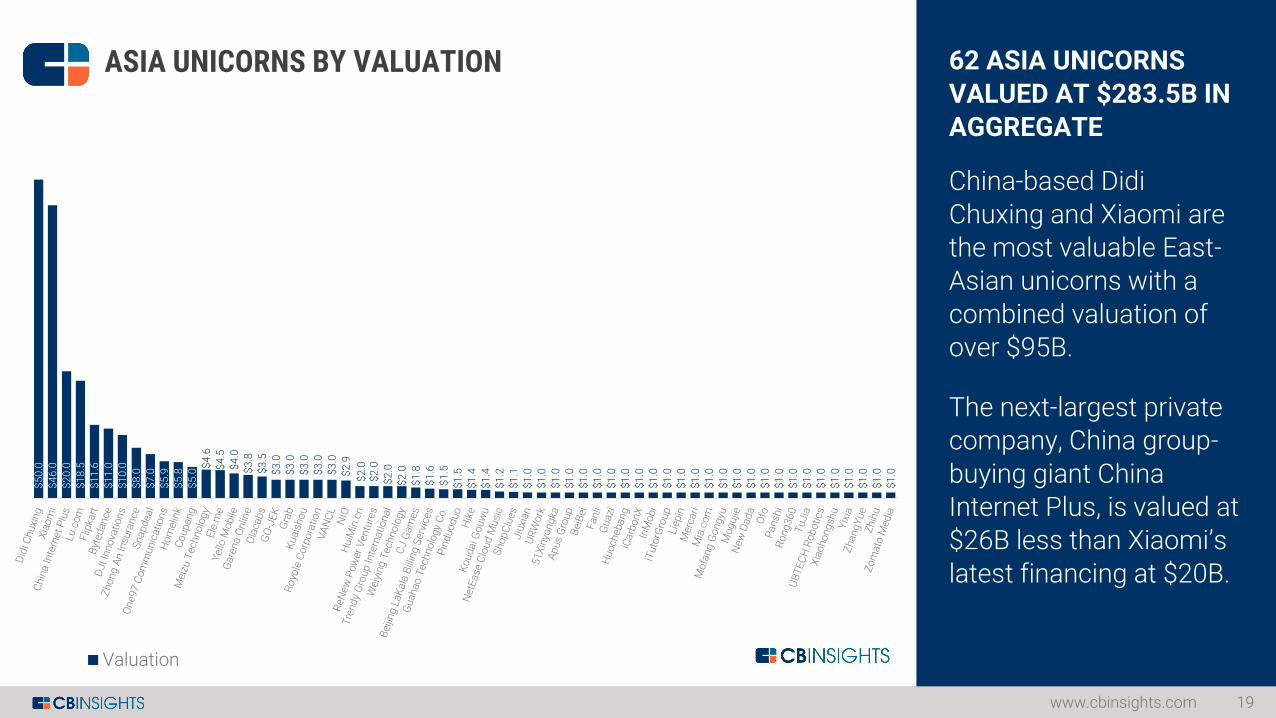

ASIA UNICORNS BY VALUATION

Valuation

62 ASIA UNICORNS

VALUED AT $283.5B IN AGGREGATE

China-based Didi

Chuxing and Xiaomi are the most valuable East-Asian unicorns with a

combined valuation of over $95B.

The next-largest private company, China group-

buying giant China Internet Plus, is valued at $26B less than Xiaomi’s

latest financing at $20B.

www.cbinsights.com 19

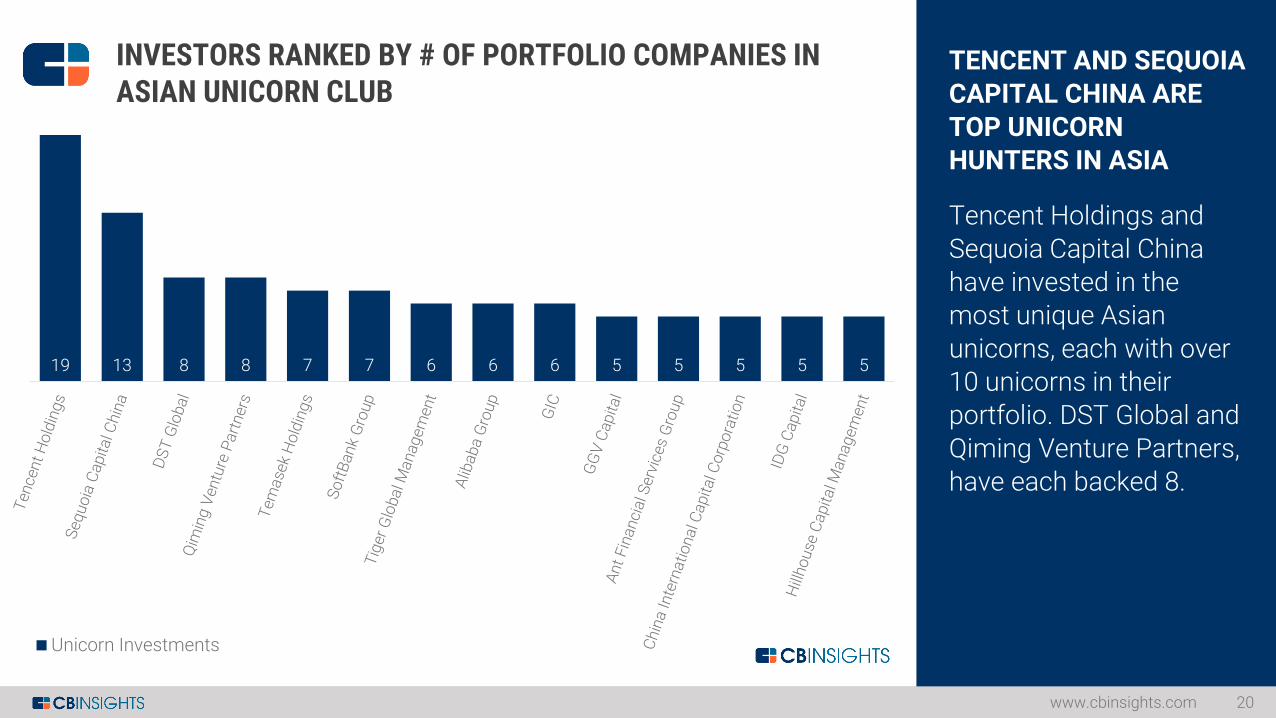

TENCENT AND SEQUOIA

CAPITAL CHINA ARE TOP UNICORN HUNTERS IN ASIA

Tencent Holdings and

Sequoia Capital China have invested in the most unique Asian

unicorns, each with over 10 unicorns in their portfolio. DST Global and

Qiming Venture Partners, have each backed 8.

www.cbinsights.com 20

19 13 8 8 7 7 6 6 6 5 5 5 5 5

INVESTORS RANKED BY # OF PORTFOLIO COMPANIES IN ASIAN UNICORN CLUB

Unicorn Investments

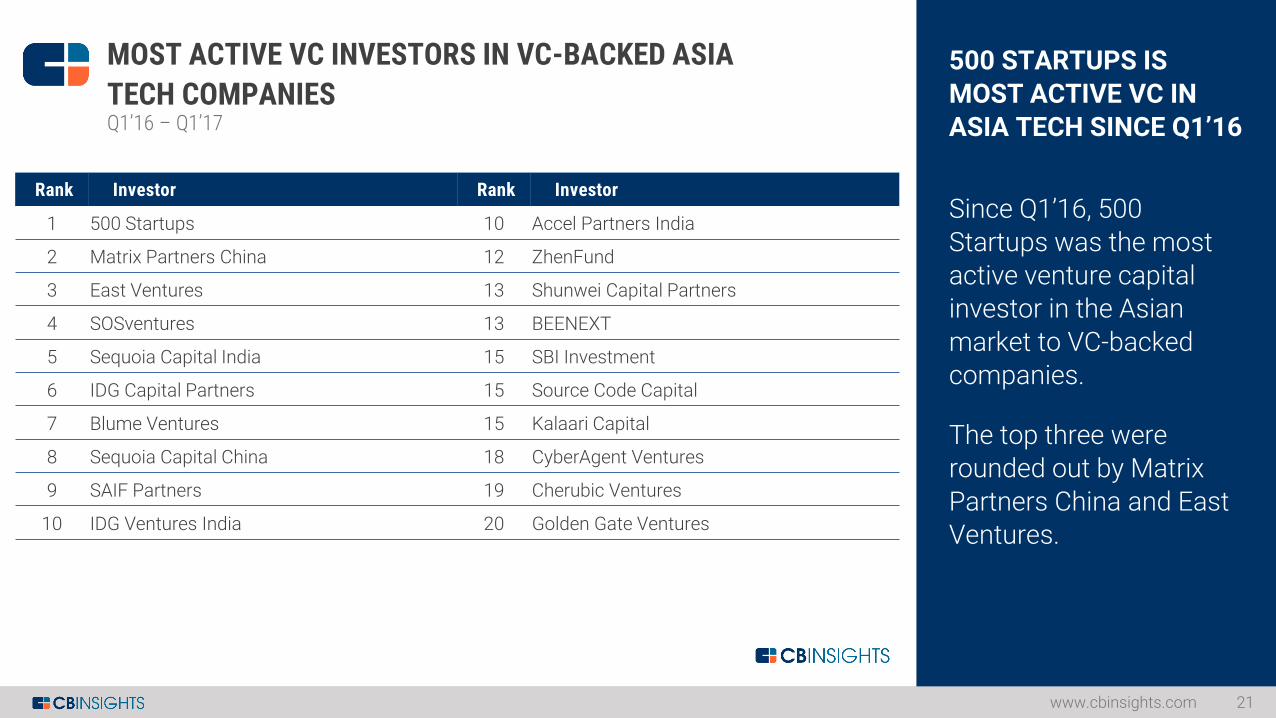

500 STARTUPS IS

MOST ACTIVE VC IN ASIA TECH SINCE Q1’16

Since Q1’16, 500

Startups was the most active venture capital investor in the Asian

market to VC-backed companies.

The top three were rounded out by Matrix

Partners China and East Ventures.

www.cbinsights.com 21

MOST ACTIVE VC INVESTORS IN VC-BACKED ASIA

TECH COMPANIESQ1’16 – Q1’17

Rank Investor Rank Investor

1 500 Startups 10 Accel Partners India

2 Matrix Partners China 12 ZhenFund

3 East Ventures 13 Shunwei Capital Partners

4 SOSventures 13 BEENEXT

5 Sequoia Capital India 15 SBI Investment

6 IDG Capital Partners 15 Source Code Capital

7 Blume Ventures 15 Kalaari Capital

8 Sequoia Capital China 18 CyberAgent Ventures

9 SAIF Partners 19 Cherubic Ventures

10 IDG Ventures India 20 Golden Gate Ventures

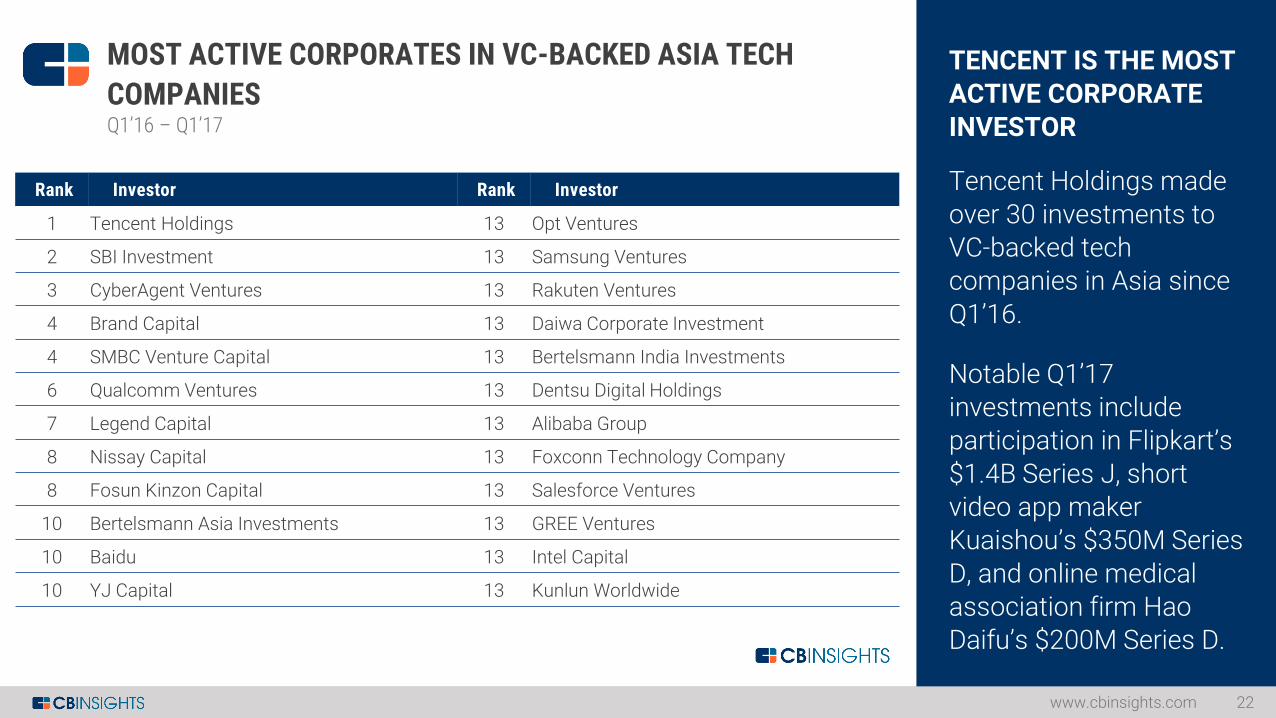

TENCENT IS THE MOST

ACTIVE CORPORATE INVESTOR

Tencent Holdings made

over 30 investments to VC-backed tech companies in Asia since

Q1’16.

Notable Q1’17 investments include participation in Flipkart’s

$1.4B Series J, short video app maker Kuaishou’s $350M Series

D, and online medical association firm Hao Daifu’s $200M Series D.

www.cbinsights.com 22

MOST ACTIVE CORPORATES IN VC-BACKED ASIA TECH

COMPANIESQ1’16 – Q1’17

Rank Investor Rank Investor

1 Tencent Holdings 13 Opt Ventures

2 SBI Investment 13 Samsung Ventures

3 CyberAgent Ventures 13 Rakuten Ventures

4 Brand Capital 13 Daiwa Corporate Investment

4 SMBC Venture Capital 13 Bertelsmann India Investments

6 Qualcomm Ventures 13 Dentsu Digital Holdings

7 Legend Capital 13 Alibaba Group

8 Nissay Capital 13 Foxconn Technology Company

8 Fosun Kinzon Capital 13 Salesforce Ventures

10 Bertelsmann Asia Investments 13 GREE Ventures

10 Baidu 13 Intel Capital

10 YJ Capital 13 Kunlun Worldwide

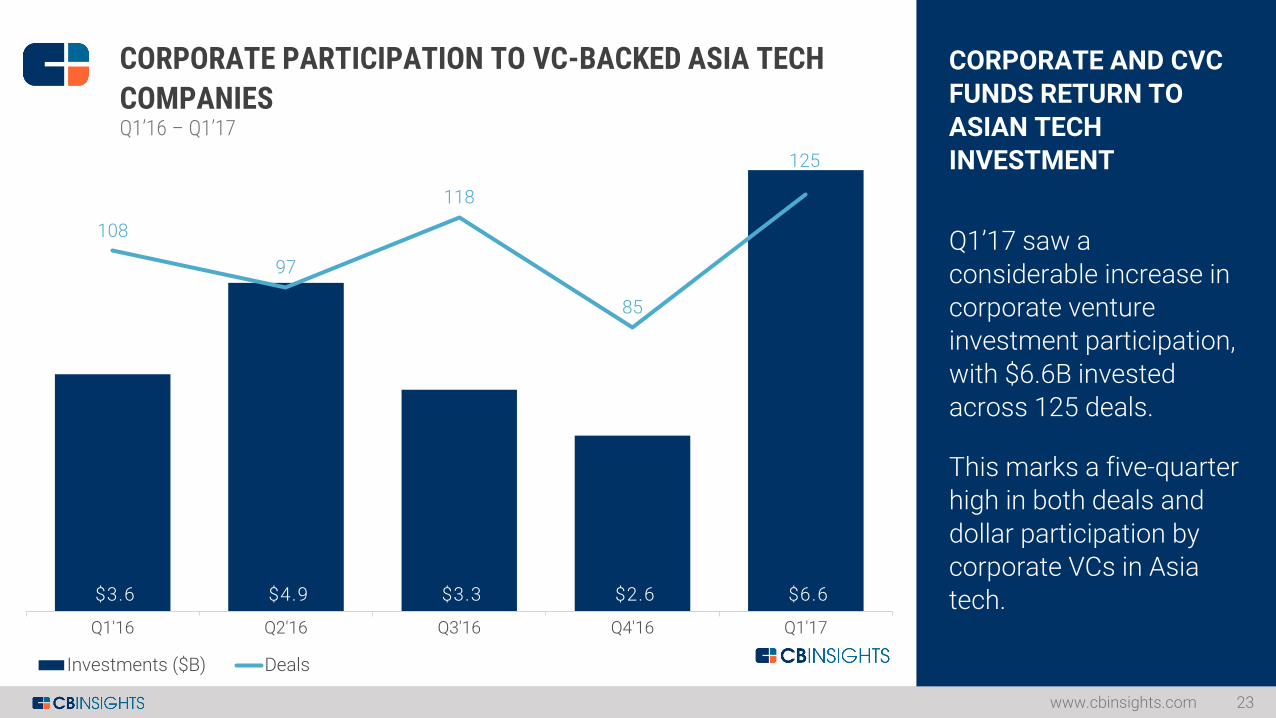

CORPORATE AND CVC

FUNDS RETURN TO ASIAN TECH INVESTMENT

Q1’17 saw a

considerable increase in corporate venture investment participation,

with $6.6B invested across 125 deals.

This marks a five-quarter high in both deals and

dollar participation by corporate VCs in Asia tech.

www.cbinsights.com 23

CORPORATE PARTICIPATION TO VC-BACKED ASIA TECH

COMPANIESQ1’16 – Q1’17

$3.6 $4.9 $3.3 $2.6 $6.6

108

97

118

85

125

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Investments ($B) Deals

68% 65% 59% 69% 60%

32%35%

41%

31%

40%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Other Investors Corp / CVC Deal Participation

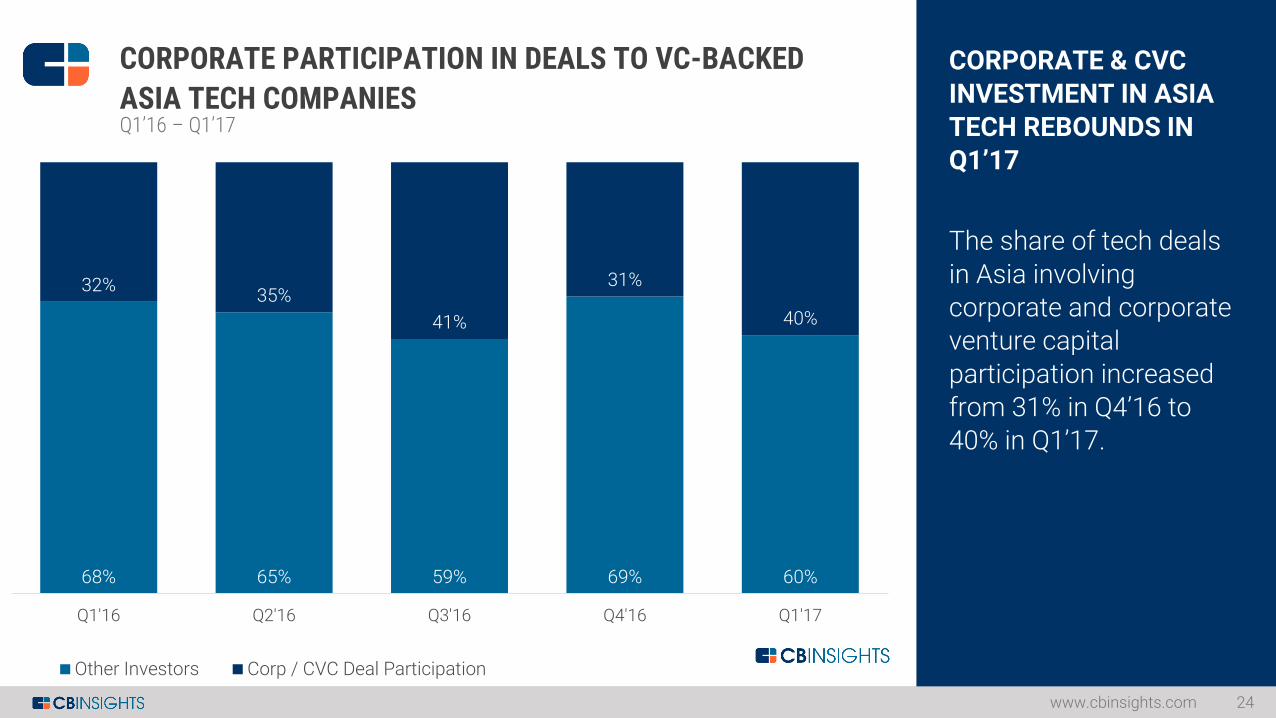

CORPORATE & CVC

INVESTMENT IN ASIATECH REBOUNDS IN Q1’17

The share of tech deals

in Asia involving corporate and corporate venture capital

participation increased from 31% in Q4’16 to 40% in Q1’17.

www.cbinsights.com 24

CORPORATE PARTICIPATION IN DEALS TO VC-BACKED

ASIA TECH COMPANIESQ1’16 – Q1’17

105

89

100

95

101

112

9192

98

89

65

4953

3138

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

China India Southeast Asia

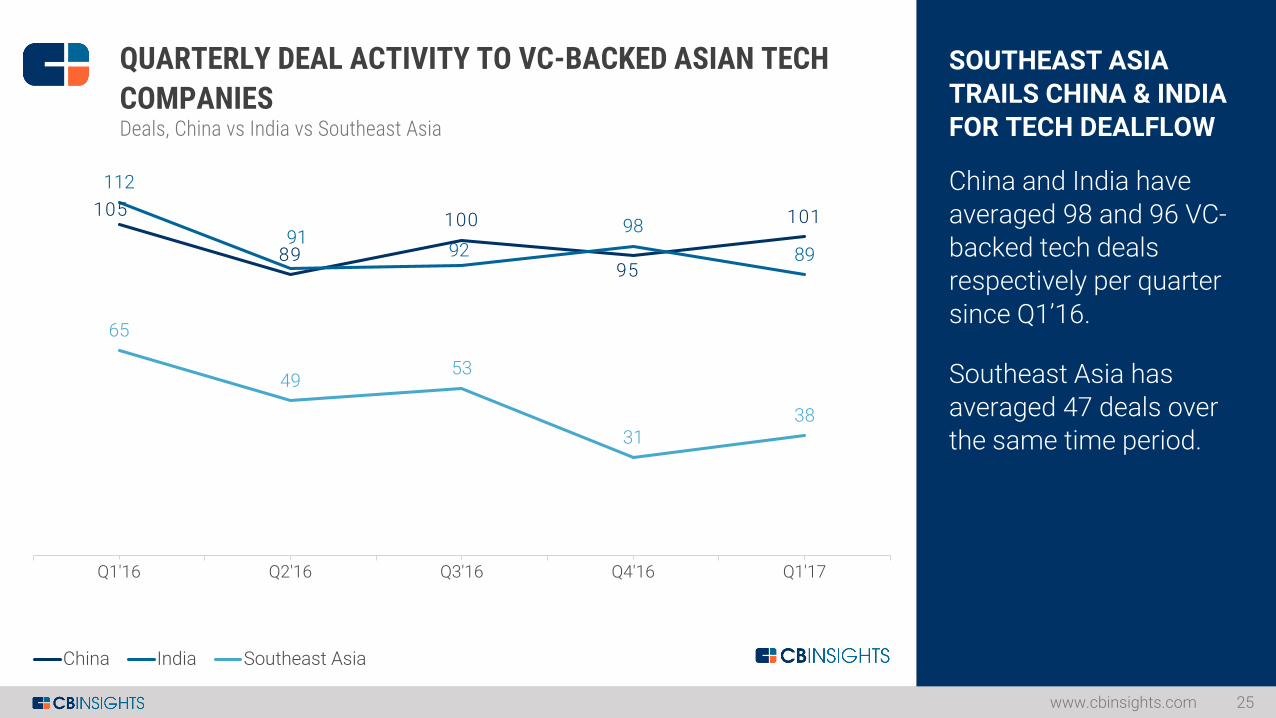

SOUTHEAST ASIA

TRAILS CHINA & INDIAFOR TECH DEALFLOW

China and India have

averaged 98 and 96 VC-backed tech deals respectively per quarter

since Q1’16.

Southeast Asia has averaged 47 deals over the same time period.

www.cbinsights.com 25

QUARTERLY DEAL ACTIVITY TO VC-BACKED ASIAN TECH

COMPANIESDeals, China vs India vs Southeast Asia

$4.3 $6.4 $3.8 $3.6 $6.0 $1.1 $0.5 $0.8 $0.4 $2.6 $0.3 $0.2

$1.5 $0.1 $0.2

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

China India Southeast Asia

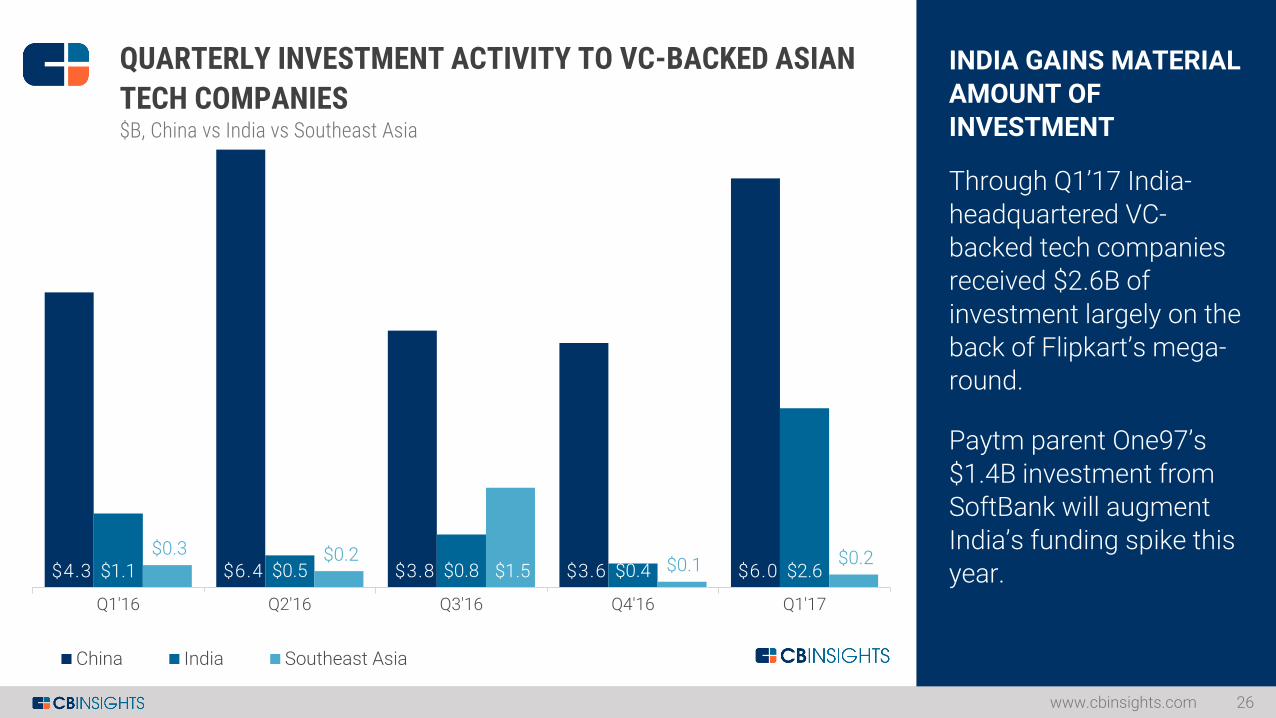

INDIA GAINS MATERIAL

AMOUNT OF INVESTMENT

Through Q1’17 India-

headquartered VC-backed tech companies received $2.6B of

investment largely on the back of Flipkart’s mega-round.

Paytm parent One97’s

$1.4B investment from SoftBank will augment India’s funding spike this

year.

www.cbinsights.com 26

QUARTERLY INVESTMENT ACTIVITY TO VC-BACKED ASIAN

TECH COMPANIES$B, China vs India vs Southeast Asia

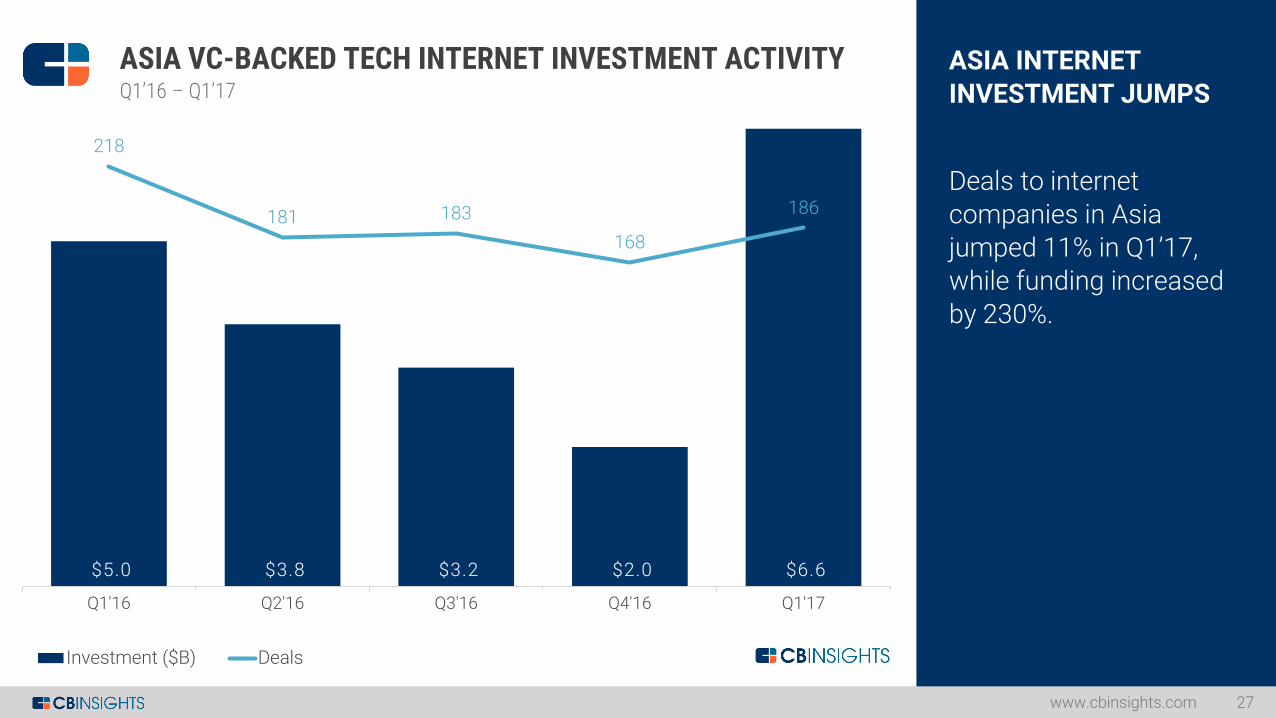

ASIA INTERNET

INVESTMENT JUMPS

Deals to internet

companies in Asia jumped 11% in Q1’17, while funding increased

by 230%.

www.cbinsights.com 27

ASIA VC-BACKED TECH INTERNET INVESTMENT ACTIVITYQ1’16 – Q1’17

$5.0 $3.8 $3.2 $2.0 $6.6

218

181 183

168

186

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Investment ($B) Deals

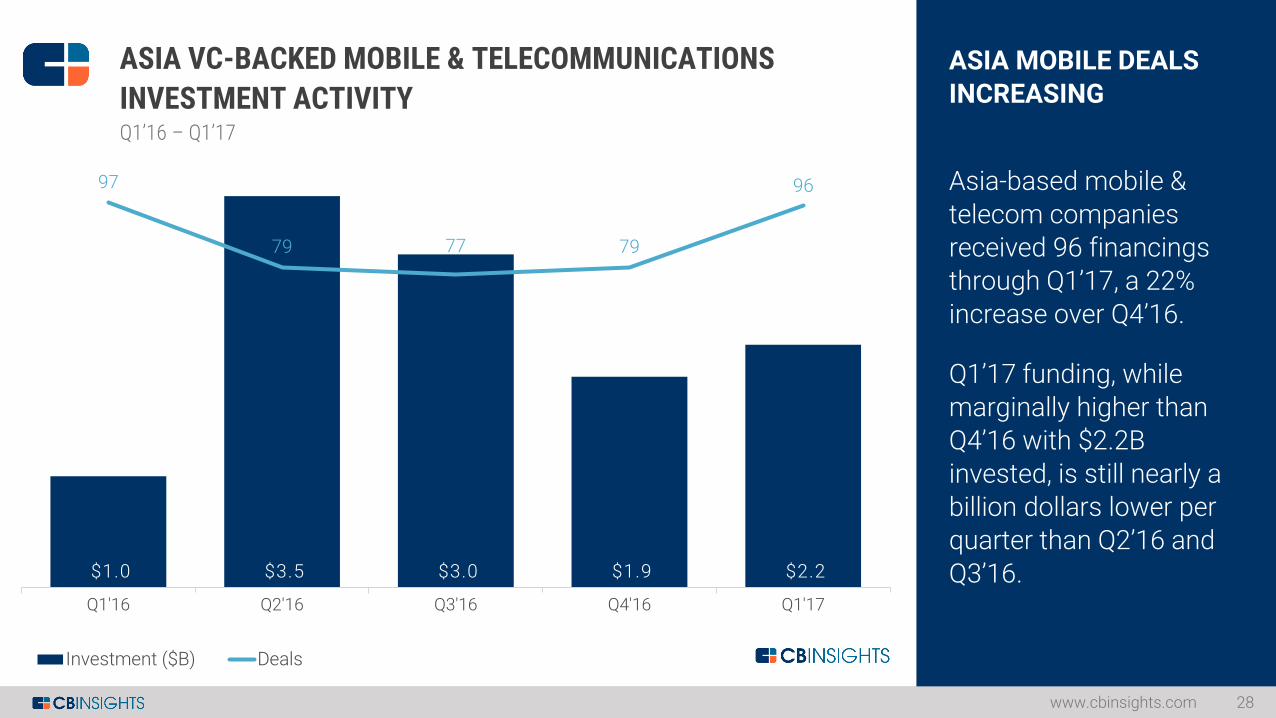

ASIA MOBILE DEALS

INCREASING

Asia-based mobile &

telecom companies received 96 financings through Q1’17, a 22%

increase over Q4’16.

Q1’17 funding, while marginally higher than Q4’16 with $2.2B

invested, is still nearly a billion dollars lower per quarter than Q2’16 and

Q3’16.

www.cbinsights.com 28

ASIA VC-BACKED MOBILE & TELECOMMUNICATIONS

INVESTMENT ACTIVITYQ1’16 – Q1’17

$1.0 $3.5 $3.0 $1.9 $2.2

97

79 77 79

96

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Investment ($B) Deals

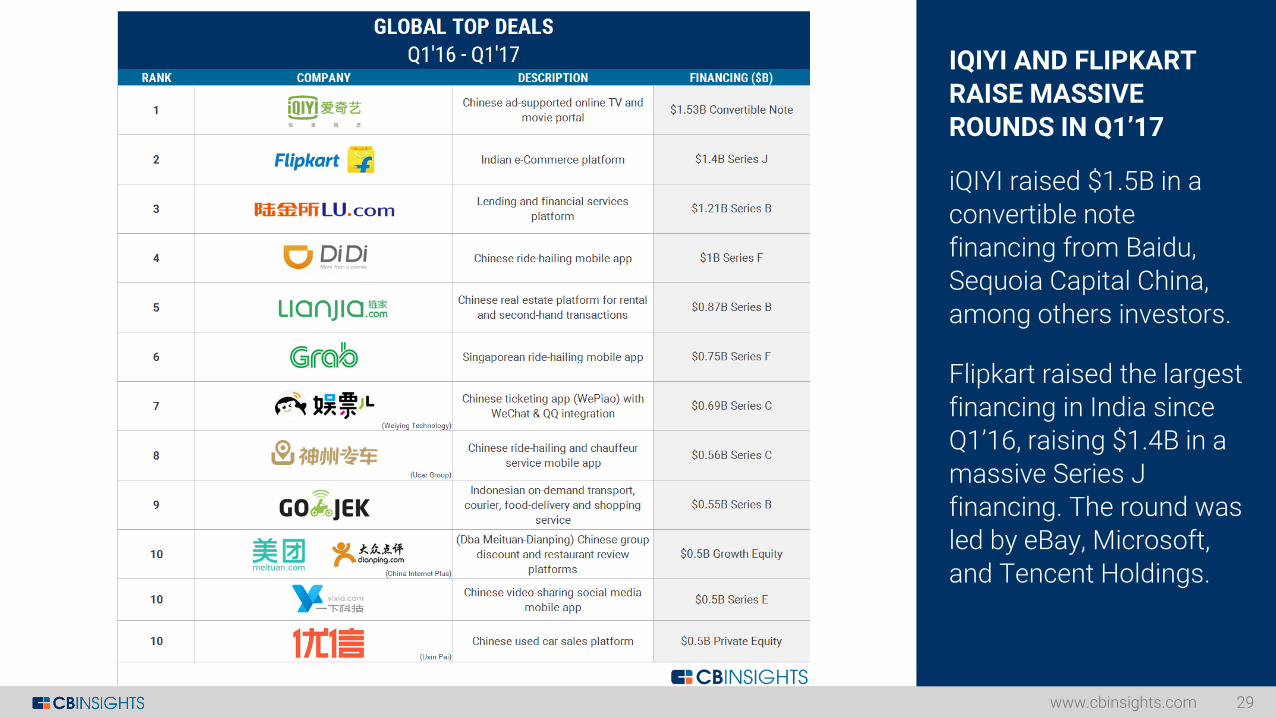

IQIYI AND FLIPKART

RAISE MASSIVE ROUNDS IN Q1’17

iQIYI raised $1.5B in a

convertible note financing from Baidu, Sequoia Capital China,

among others investors.

Flipkart raised the largest financing in India since Q1’16, raising $1.4B in a

massive Series J financing. The round was led by eBay, Microsoft,

and Tencent Holdings.

www.cbinsights.com 29

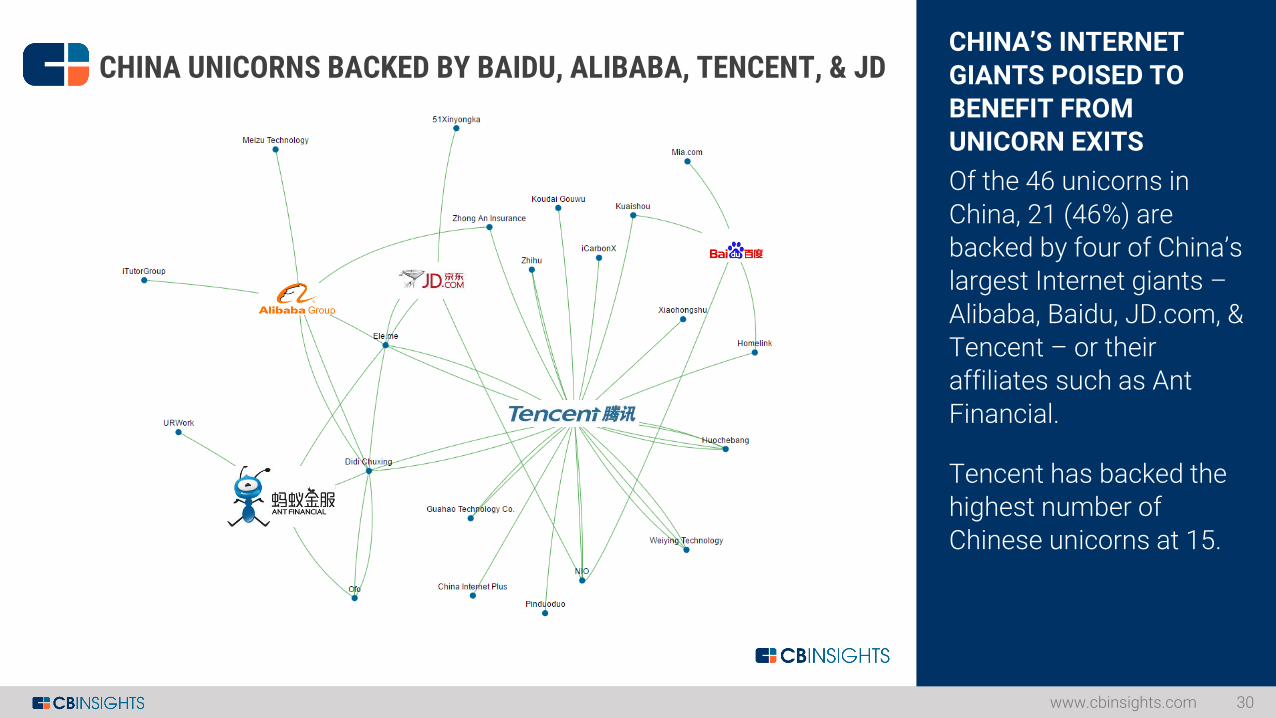

CHINA’S INTERNET

GIANTS POISED TO BENEFIT FROM UNICORN EXITS

Of the 46 unicorns in

China, 21 (46%) are backed by four of China’s largest Internet giants –

Alibaba, Baidu, JD.com, & Tencent – or their affiliates such as Ant

Financial.

Tencent has backed the highest number of Chinese unicorns at 15.

www.cbinsights.com 30

CHINA UNICORNS BACKED BY BAIDU, ALIBABA, TENCENT, & JD

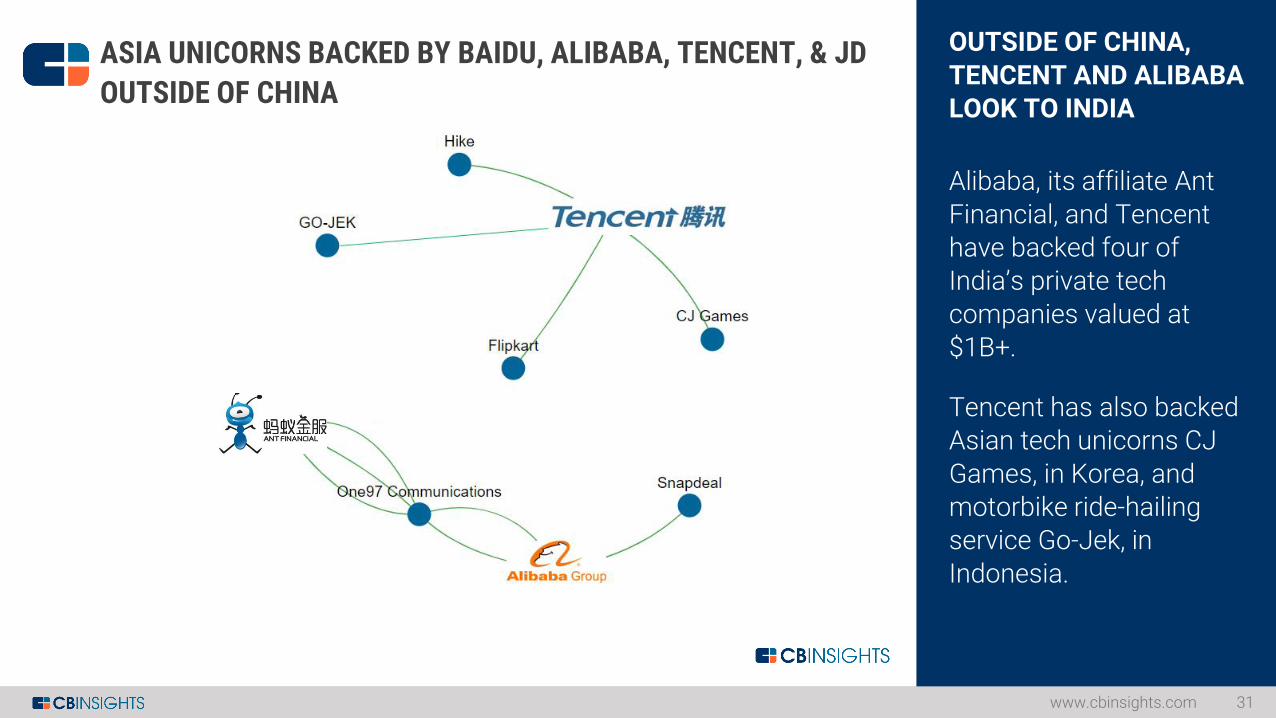

OUTSIDE OF CHINA,

TENCENT AND ALIBABA LOOK TO INDIA

Alibaba, its affiliate Ant

Financial, and Tencent have backed four of India’s private tech

companies valued at $1B+.

Tencent has also backed Asian tech unicorns CJ

Games, in Korea, and motorbike ride-hailing service Go-Jek, in

Indonesia.

www.cbinsights.com 31

ASIA UNICORNS BACKED BY BAIDU, ALIBABA, TENCENT, & JD

OUTSIDE OF CHINA

CHINAFINANCING TRENDS

www.cbinsights.com 32

$4.3 $6.4 $3.8 $3.6 $6.0

105

89

10095

101

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Investments ($B) Deals

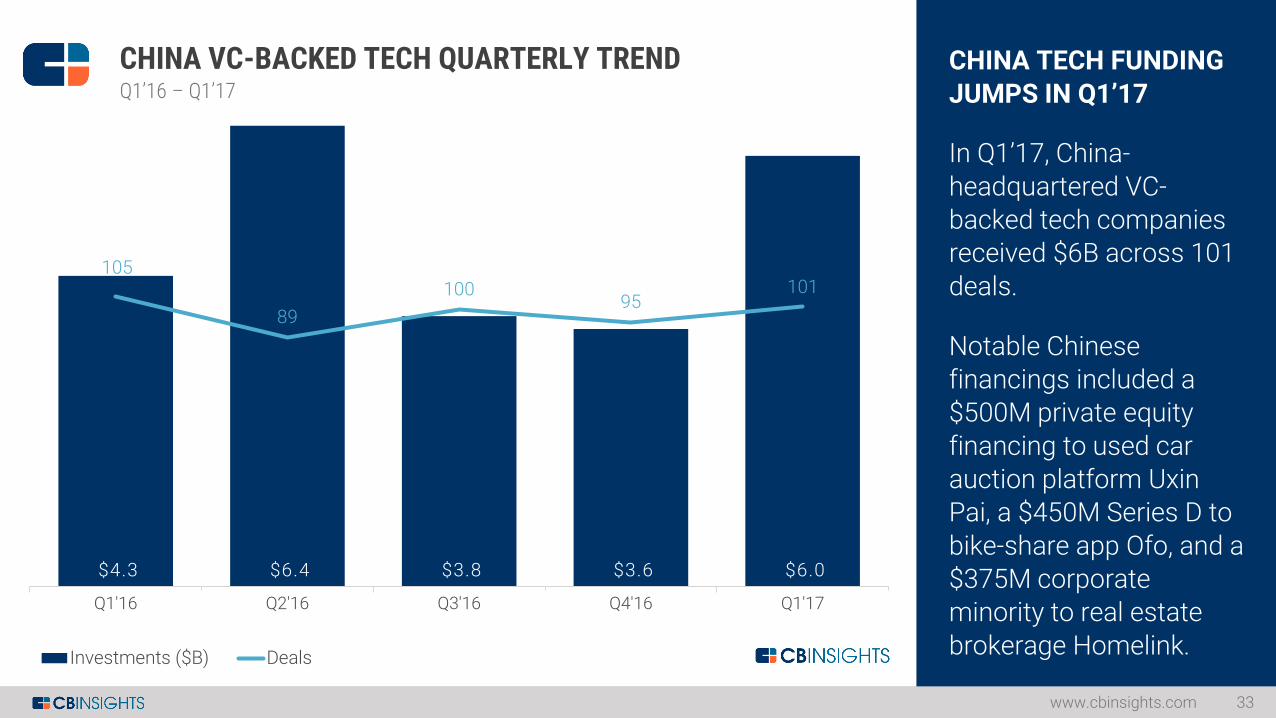

CHINA TECH FUNDING

JUMPS IN Q1’17

In Q1’17, China-

headquartered VC-backed tech companies received $6B across 101

deals.

Notable Chinese financings included a $500M private equity

financing to used car auction platform UxinPai, a $450M Series D to

bike-share app Ofo, and a $375M corporate minority to real estate

brokerage Homelink.

www.cbinsights.com 33

CHINA VC-BACKED TECH QUARTERLY TRENDQ1’16 – Q1’17

7% 11% 15% 13% 7%

32%27%

20%18%

26%

30% 27%26%

26% 29%

12%20%

18%15%

16%

5%

6%

3%

8%

13%

5%1%

3%3%

2%

10% 8%15% 17%

8%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Seed / Angel Series A Series B Series C Series D Series E+ Other

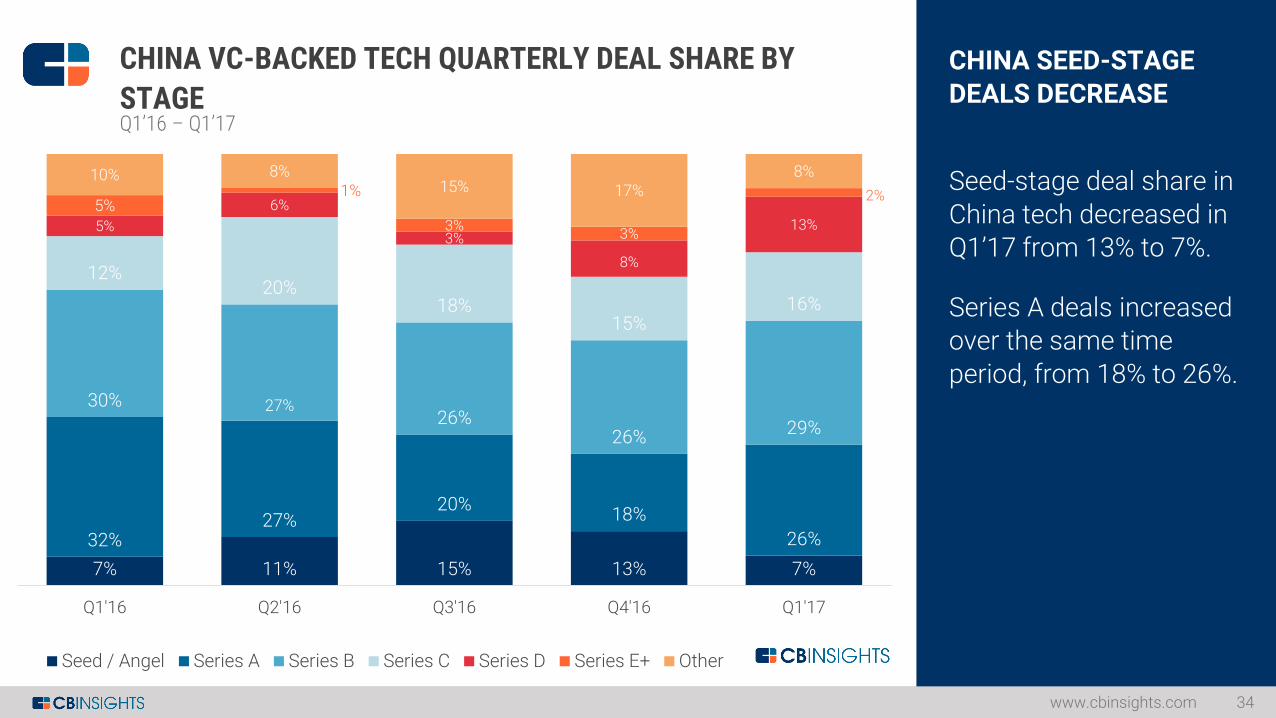

CHINA SEED-STAGE

DEALS DECREASE

Seed-stage deal share in

China tech decreased in Q1’17 from 13% to 7%.

Series A deals increased over the same time

period, from 18% to 26%.

www.cbinsights.com 34

CHINA VC-BACKED TECH QUARTERLY DEAL SHARE BY

STAGEQ1’16 – Q1’17

63% 58% 50% 52% 55%

30%34%

34% 32%31%

3% 3%

7% 6%6%

2% 2%

4% 4% 3%

2% 2%5% 6% 5%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Internet Mobile & TelecommunicationsSoftware (non-internet/mobile) Computer Hardware & ServicesElectronics

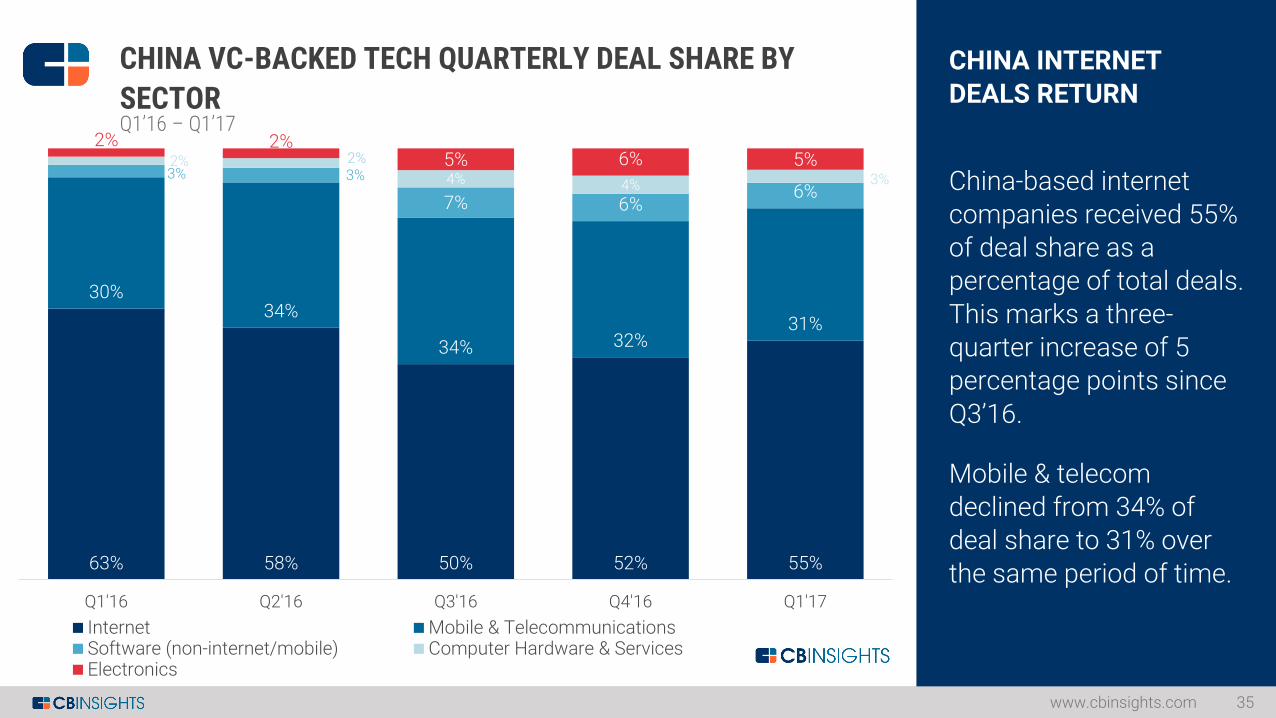

CHINA INTERNET

DEALS RETURN

China-based internet

companies received 55% of deal share as a percentage of total deals.

This marks a three-quarter increase of 5 percentage points since

Q3’16.

Mobile & telecom declined from 34% of deal share to 31% over

the same period of time.

www.cbinsights.com 35

CHINA VC-BACKED TECH QUARTERLY DEAL SHARE BY

SECTORQ1’16 – Q1’17

IQIYI, LU.COM, DIDI

CHUXING RAISE BILLION-DOLLAR ROUNDS

iQIYI, P2P lender Lu.com,

and ride-share giant DidiChuxing all raised billion dollar+ rounds since

Q1’16.

Other top deals over the past five quarters to VC-backed China tech

companies include a $450M round to bike-share app Ofo and a

$690M financing to Chinese ticketing app Weiying.

www.cbinsights.com 36

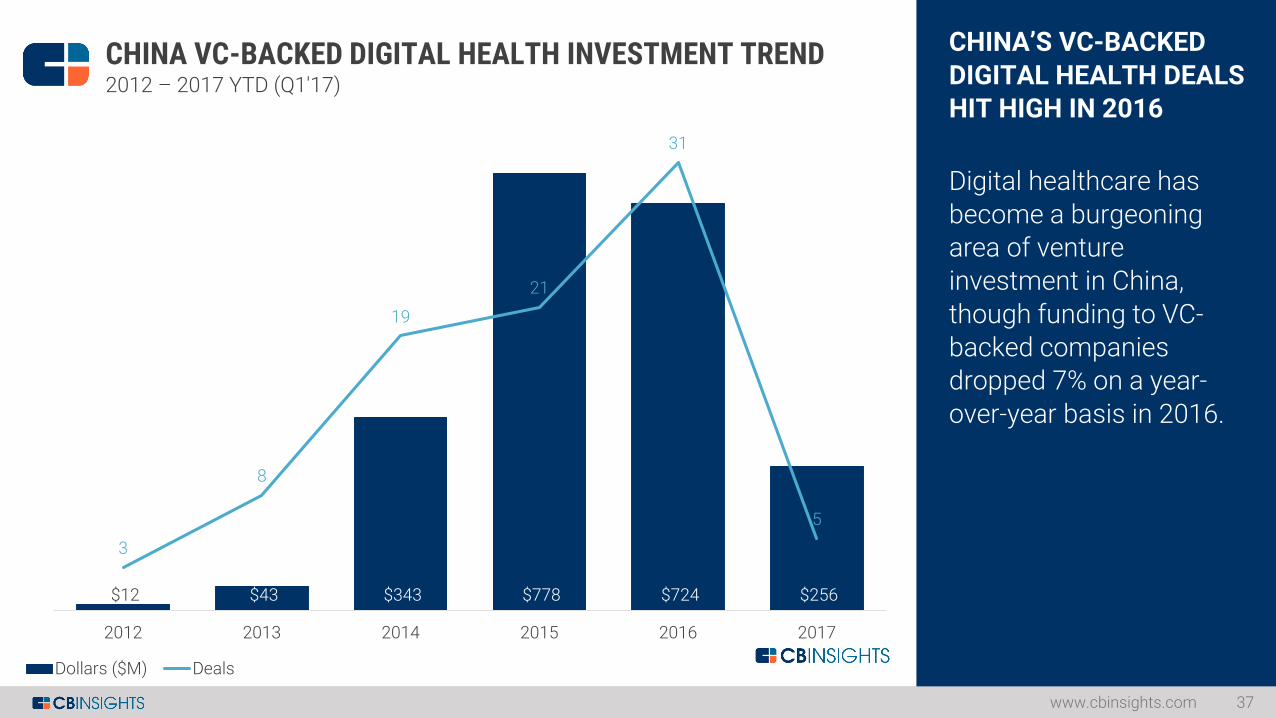

CHINA’S VC-BACKED

DIGITAL HEALTH DEALS HIT HIGH IN 2016

Digital healthcare has

become a burgeoning area of venture investment in China,

though funding to VC-backed companies dropped 7% on a year-

over-year basis in 2016.

www.cbinsights.com 37

$12 $43 $343 $778 $724 $256

3

8

19

21

31

5

0

5

10

15

20

25

30

35

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

2012 2013 2014 2015 2016 2017

CHINA VC-BACKED DIGITAL HEALTH INVESTMENT TREND2012 – 2017 YTD (Q1'17)

Dollars ($M) Deals

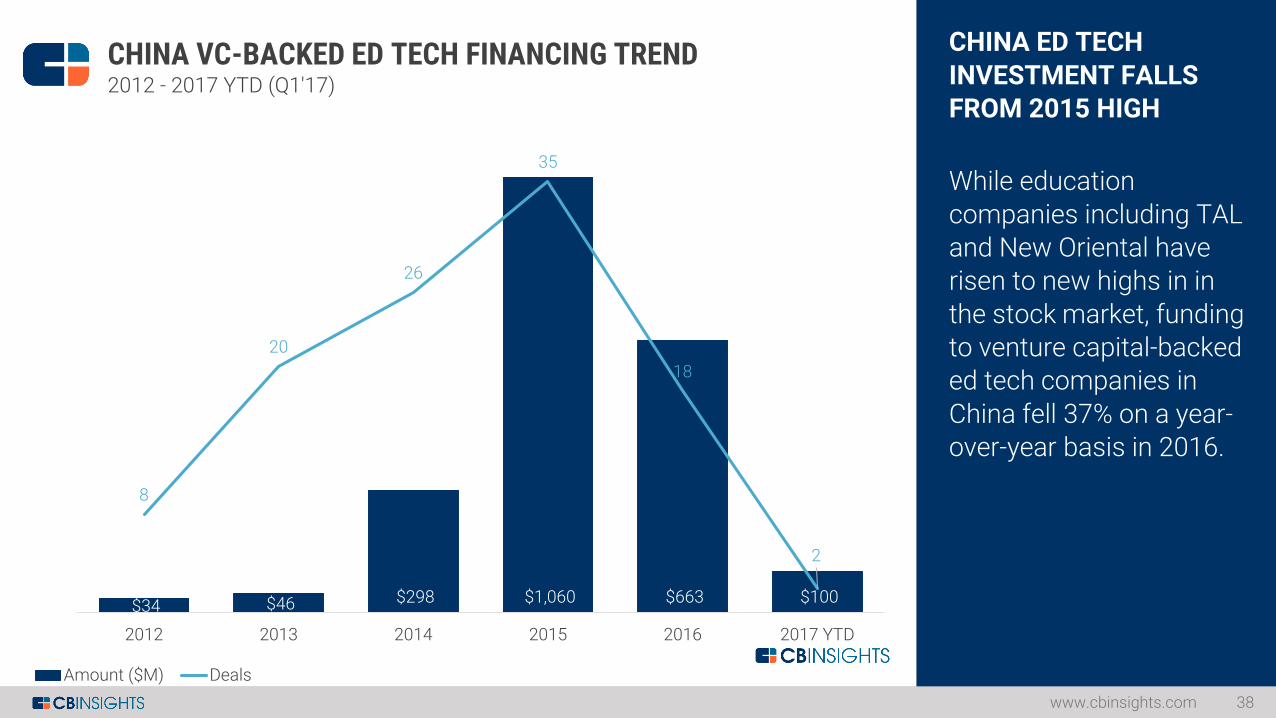

CHINA ED TECH

INVESTMENT FALLS FROM 2015 HIGH

While education

companies including TAL and New Oriental have risen to new highs in in

the stock market, funding to venture capital-backed ed tech companies in

China fell 37% on a year-over-year basis in 2016.

www.cbinsights.com 38

$34 $46 $298 $1,060 $663 $100

8

20

26

35

18

2

0

5

10

15

20

25

30

35

40

$-

$200

$400

$600

$800

$1,000

$1,200

2012 2013 2014 2015 2016 2017 YTD

CHINA VC-BACKED ED TECH FINANCING TREND2012 - 2017 YTD (Q1'17)

Amount ($M) Deals

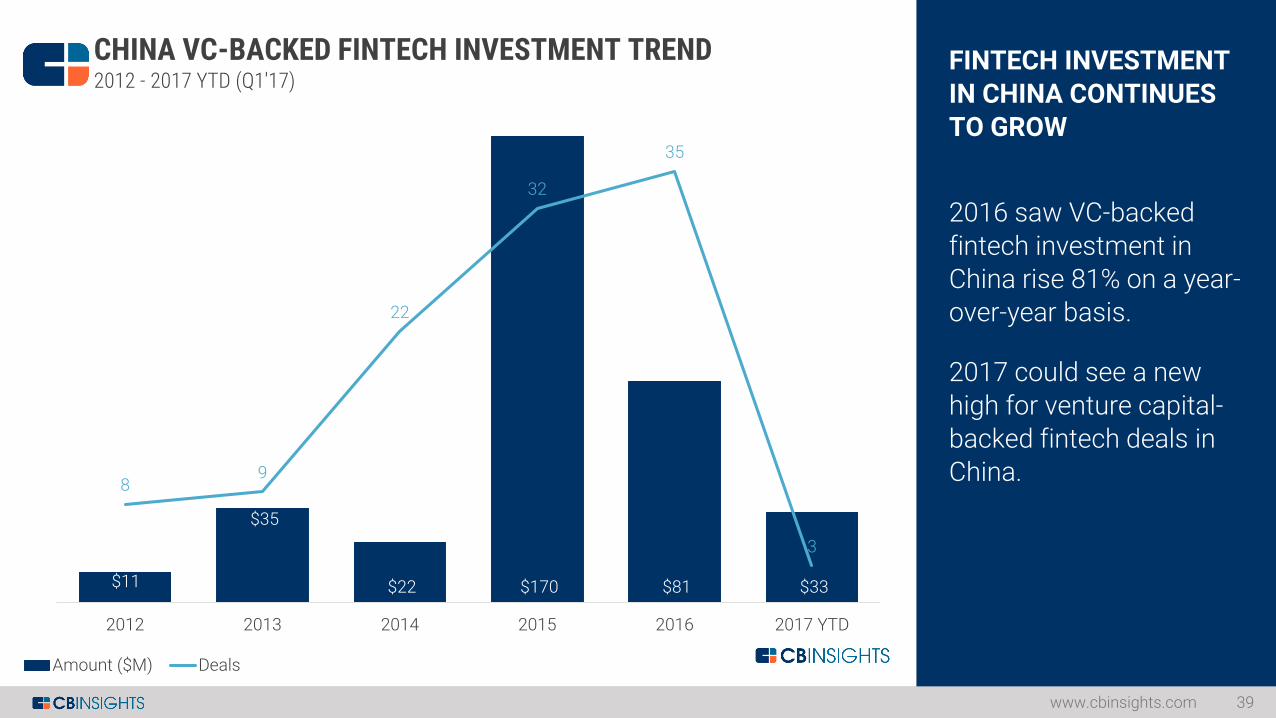

FINTECH INVESTMENT

IN CHINA CONTINUES TO GROW

2016 saw VC-backed

fintech investment in China rise 81% on a year-over-year basis.

2017 could see a new

high for venture capital-backed fintech deals in China.

www.cbinsights.com 39

$11

$35

$22 $170 $81 $33

89

22

32

35

3

0

5

10

15

20

25

30

35

40

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

2012 2013 2014 2015 2016 2017 YTD

CHINA VC-BACKED FINTECH INVESTMENT TREND2012 - 2017 YTD (Q1'17)

Amount ($M) Deals

INDIAFINANCING TRENDS

www.cbinsights.com 40

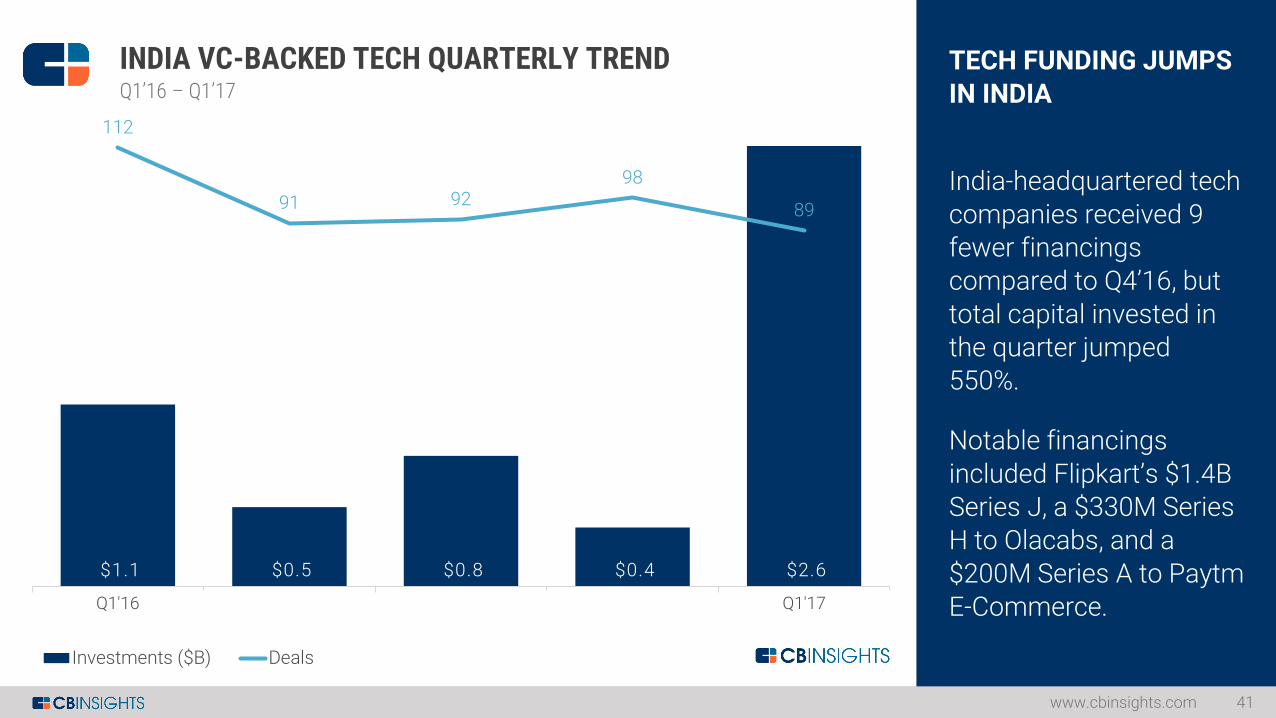

$1.1 $0.5 $0.8 $0.4 $2.6

112

91 9298

89

Q1'16 Q1'17

Investments ($B) Deals

TECH FUNDING JUMPS

IN INDIA

India-headquartered tech

companies received 9 fewer financings compared to Q4’16, but

total capital invested in the quarter jumped 550%.

Notable financings

included Flipkart’s $1.4B Series J, a $330M Series H to Olacabs, and a

$200M Series A to Paytm E-Commerce.

www.cbinsights.com 41

INDIA VC-BACKED TECH QUARTERLY TRENDQ1’16 – Q1’17

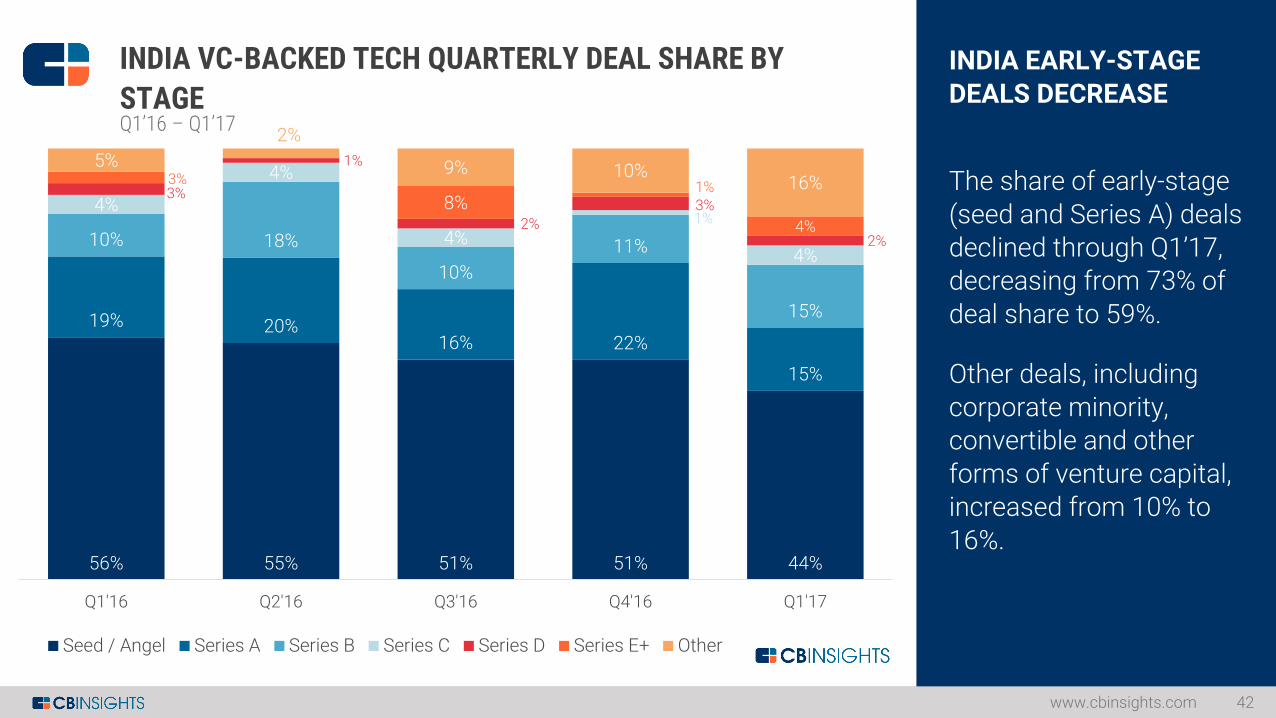

56% 55% 51% 51% 44%

19% 20%16% 22%

15%

10% 18%

10%

11%

15%

4%

4%

4%1%

4%

3%

1%

2%

3%

2%

3%

8%1%

4%

5%

2%

9% 10%16%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Seed / Angel Series A Series B Series C Series D Series E+ Other

INDIA EARLY-STAGE

DEALS DECREASE

The share of early-stage

(seed and Series A) deals declined through Q1’17, decreasing from 73% of

deal share to 59%.

Other deals, including corporate minority, convertible and other

forms of venture capital, increased from 10% to 16%.

www.cbinsights.com 42

INDIA VC-BACKED TECH QUARTERLY DEAL SHARE BY

STAGEQ1’16 – Q1’17

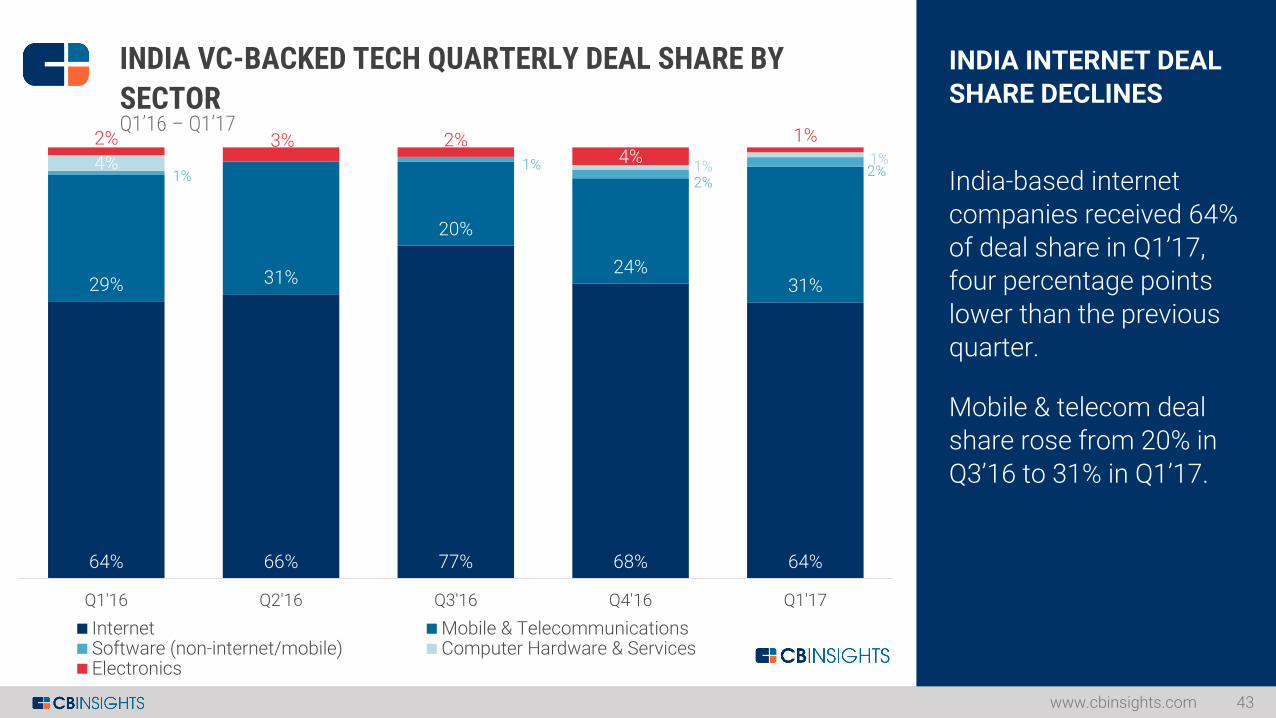

64% 66% 77% 68% 64%

29% 31%

20%

24%31%

1%1%

2%2%4% 1%1%

2% 3% 2%4%

1%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Internet Mobile & TelecommunicationsSoftware (non-internet/mobile) Computer Hardware & ServicesElectronics

INDIA INTERNET DEAL

SHARE DECLINES

India-based internet

companies received 64% of deal share in Q1’17, four percentage points

lower than the previous quarter.

Mobile & telecom deal share rose from 20% in

Q3’16 to 31% in Q1’17.

www.cbinsights.com 43

INDIA VC-BACKED TECH QUARTERLY DEAL SHARE BY

SECTORQ1’16 – Q1’17

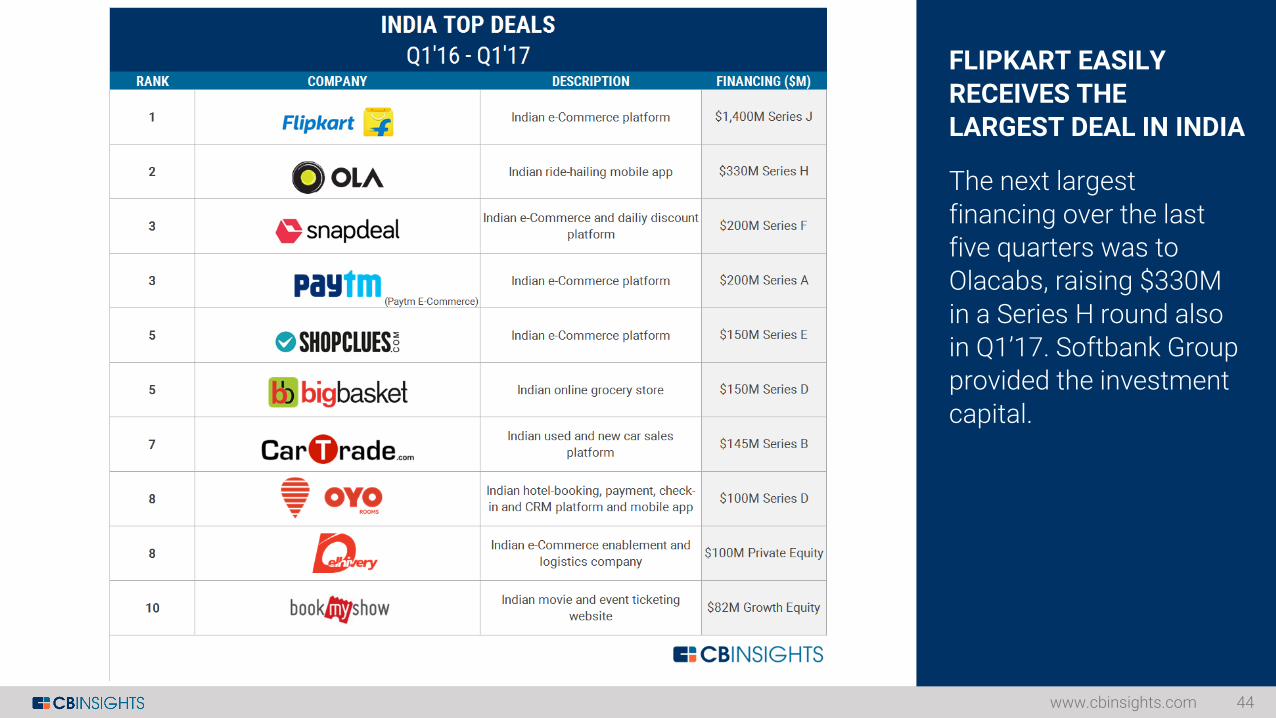

FLIPKART EASILY

RECEIVES THE LARGEST DEAL IN INDIA

The next largest

financing over the last five quarters was to Olacabs, raising $330M

in a Series H round also in Q1’17. Softbank Group provided the investment

capital.

www.cbinsights.com 44

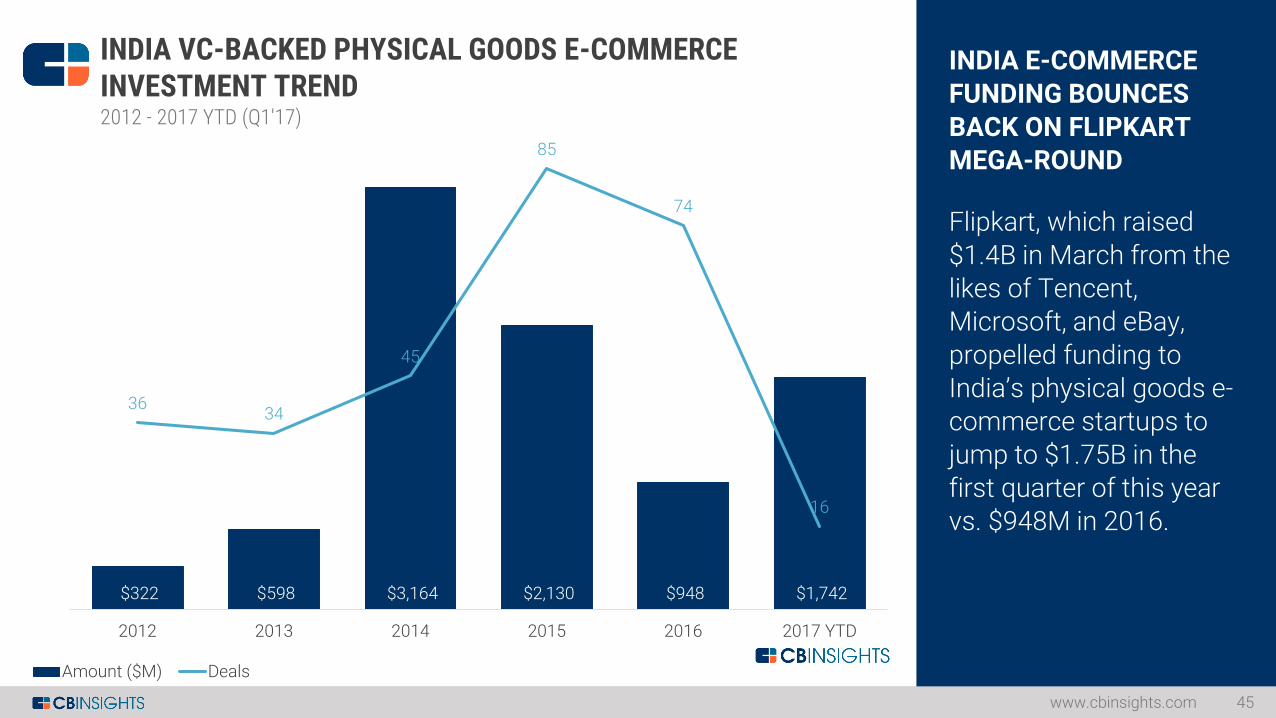

INDIA E-COMMERCE

FUNDING BOUNCES BACK ON FLIPKART MEGA-ROUND

Flipkart, which raised

$1.4B in March from the likes of Tencent, Microsoft, and eBay,

propelled funding to India’s physical goods e-commerce startups to

jump to $1.75B in the first quarter of this year vs. $948M in 2016.

www.cbinsights.com 45

$322 $598 $3,164 $2,130 $948 $1,742

3634

45

85

74

16

0

10

20

30

40

50

60

70

80

90

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2012 2013 2014 2015 2016 2017 YTD

INDIA VC-BACKED PHYSICAL GOODS E-COMMERCE INVESTMENT TREND2012 - 2017 YTD (Q1'17)

Amount ($M) Deals

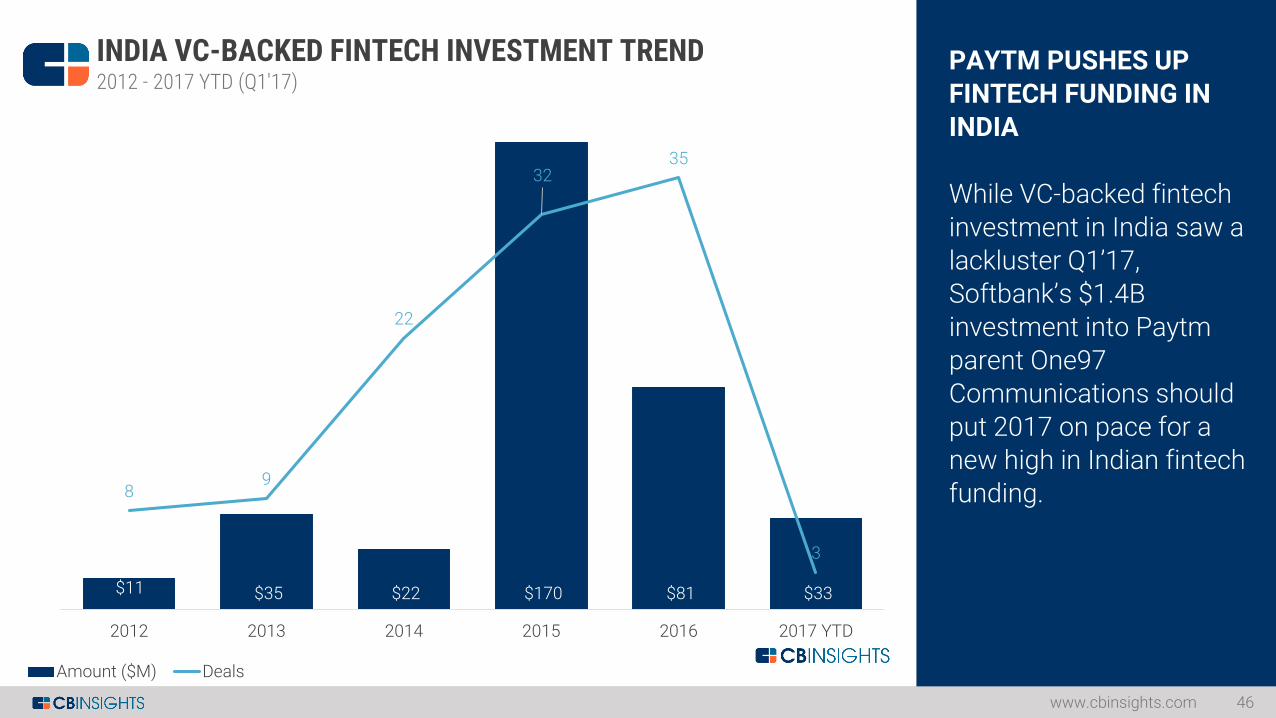

PAYTM PUSHES UP

FINTECH FUNDING IN INDIA

While VC-backed fintech

investment in India saw a lackluster Q1’17, Softbank’s $1.4B

investment into Paytm parent One97 Communications should

put 2017 on pace for a new high in Indian fintech funding.

www.cbinsights.com 46

$11 $35 $22 $170 $81 $33

89

22

3235

3

0

5

10

15

20

25

30

35

40

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

2012 2013 2014 2015 2016 2017 YTD

INDIA VC-BACKED FINTECH INVESTMENT TREND2012 - 2017 YTD (Q1'17)

Amount ($M) Deals

SOUTHEAST ASIAFINANCING TRENDS

www.cbinsights.com 47

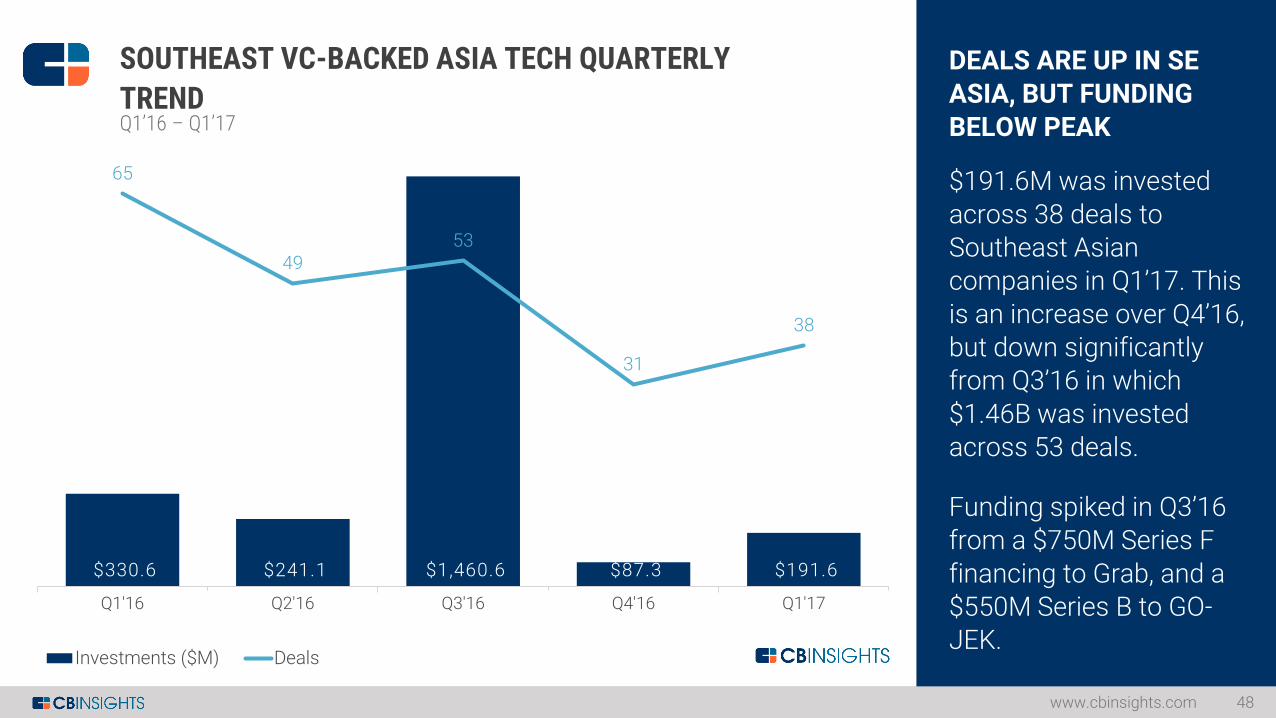

$330.6 $241.1 $1,460.6 $87.3 $191.6

65

4953

31

38

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Investments ($M) Deals

DEALS ARE UP IN SE

ASIA, BUT FUNDING BELOW PEAK

$191.6M was invested

across 38 deals to Southeast Asian companies in Q1’17. This

is an increase over Q4’16, but down significantly from Q3’16 in which

$1.46B was invested across 53 deals.

Funding spiked in Q3’16 from a $750M Series F

financing to Grab, and a $550M Series B to GO-JEK.

www.cbinsights.com 48

SOUTHEAST VC-BACKED ASIA TECH QUARTERLY

TRENDQ1’16 – Q1’17

57% 65% 38% 52% 55%

26%

22%

32%

23%21%

6%4%

23% 3%

11%

2% 2%

6%

5%2%

6%

2% 2%9%4%

2%

10% 8%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Seed / Angel Series A Series B Series C Series D Series E+ Other

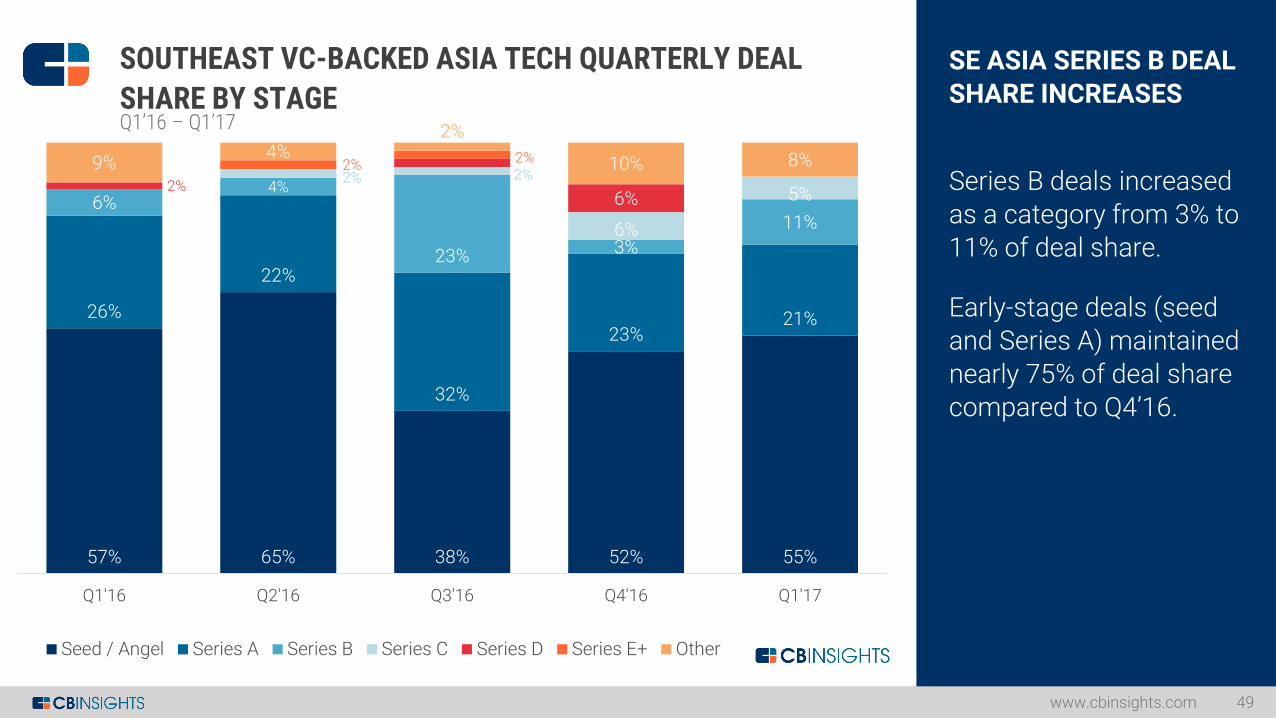

SE ASIA SERIES B DEAL

SHARE INCREASES

Series B deals increased

as a category from 3% to 11% of deal share.

Early-stage deals (seed and Series A) maintained

nearly 75% of deal share compared to Q4’16.

www.cbinsights.com 49

SOUTHEAST VC-BACKED ASIA TECH QUARTERLY DEAL

SHARE BY STAGEQ1’16 – Q1’17

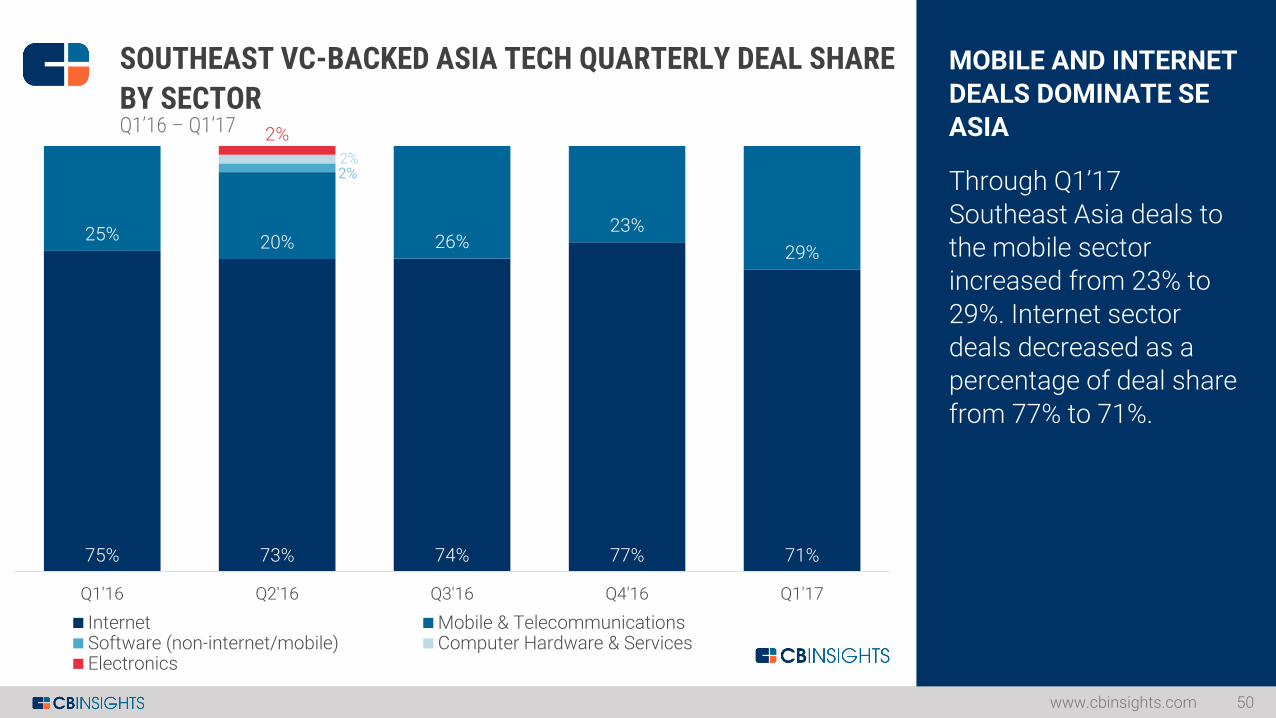

75% 73% 74% 77% 71%

25% 20% 26%23%

29%

0%

2%

0% 0% 0%

2%

2%

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17

Internet Mobile & TelecommunicationsSoftware (non-internet/mobile) Computer Hardware & ServicesElectronics

MOBILE AND INTERNET

DEALS DOMINATE SE ASIA

Through Q1’17

Southeast Asia deals to the mobile sector increased from 23% to

29%. Internet sector deals decreased as a percentage of deal share

from 77% to 71%.

www.cbinsights.com 50

SOUTHEAST VC-BACKED ASIA TECH QUARTERLY DEAL SHARE

BY SECTORQ1’16 – Q1’17

GRAB AND GO-JEK

LARGEST DEALS IN SE ASIA

Singapore-based ride-

hailing company Grab and Indonesia-based hyperlocal transport

startup GO-JEK both received massive financings in Q3’16.

The next largest funding

went to Sea Group (fkaGarena), the Singapore-based online gaming, e-

commerce and digital financial services company.

www.cbinsights.com 51

RANK DESCRIPTION

1 Singaporean ride-hailing mobile app

2

Indonesian on-demand transport,

courier, food-delivery and shopping

service

3

Singaporean digital entertainment, e-

Commerce and digital financing

services company

4 Indonesian e-Commerce platform

5Malaysian internet TV and movie

platform

6Malaysian internet TV and movie

platform

7Singaporean consumer-to-consumer e-

Commerce platform

8Singaporean dating and social media

mobile app

9Singaporean e-Commerce delivery and

logistics company

9Indonesian peer-to-peer lending

platform

$30M Series B

$30M Series A

$147M Series E

$90M Series B

$45M Corporate

Minority

$35M Series B

$32.5M Series D

SOUTHEAST ASIA TOP DEALS

Q1'16 - Q1'17FINANCING ($M)

$750M Series F

$550M Series B

$170M Series D

COMPANY

SOUTHEAST ASIA

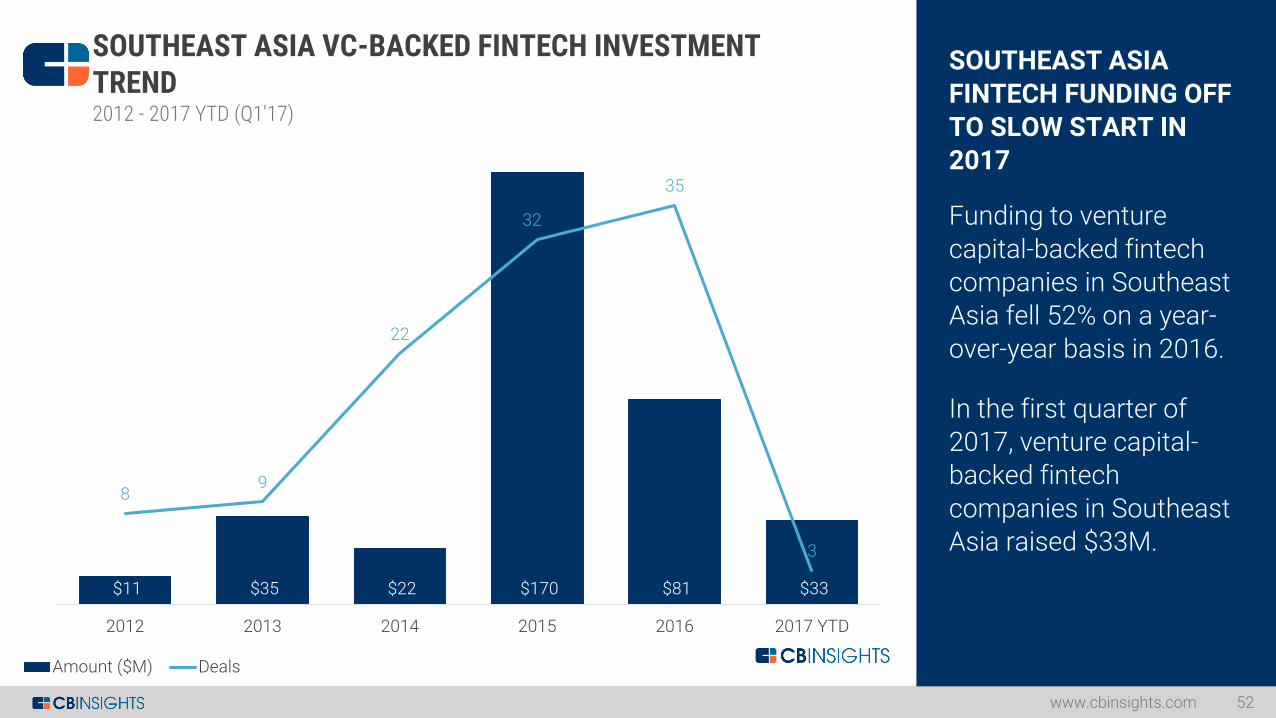

FINTECH FUNDING OFF TO SLOW START IN 2017

Funding to venture

capital-backed fintech companies in Southeast Asia fell 52% on a year-

over-year basis in 2016.

In the first quarter of 2017, venture capital-backed fintech

companies in Southeast Asia raised $33M.

www.cbinsights.com 52

$11 $35 $22 $170 $81 $33

89

22

32

35

3

0

5

10

15

20

25

30

35

40

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

2012 2013 2014 2015 2016 2017 YTD

SOUTHEAST ASIA VC-BACKED FINTECH INVESTMENT TREND2012 - 2017 YTD (Q1'17)

Amount ($M) Deals

CB Insights (cbinsights.com) encourages you to review the methodology and definitions employed to better understand the numbers presented in this report. If you have any questions about the definitions or methodological principles used, we encourage you to reach out to CB Insights directly. Additionally, if you feel your firm has been underrepresented, please send an email to [email protected] and we can work together to ensure your firm’s investment data is up-to-date.

NOTES ON METHODOLOGY

www.cbinsights.com 53

What is included: What is excluded:

– Equity financings into emerging companies. Fundings must come from VC-backed companies, which are defined as companies who have received funding at any point from either: venture capital firms, corporate venture group or super angel investors.

– Fundings of only private companies. Funding rounds raised by public companies of any kind on any exchange (including Pink Sheets) are excluded from our numbers, even if they received investment by a venture firm(s).

– Only includes the investment made in the quarter for tranched investments. If a company does a second closing of its Series B round for $5M and previously had closed $2M in a prior quarter, only the $5M is reflected in our results.

– Round numbers reflect what has closed – not what is intended. If a company indicates the closing of $5M out of a desired raise of $15M, our numbers reflect only the amount which has closed.

– Only verifiable fundings are included. Fundings are verified via (1) various federal and state regulatory filings; (2) direct confirmation with firm or investor; (3) press release; or (4) credible media sources.

– Equity fundings to joint ventures and spinoffs/spinouts are included, given that they meet the VC-backed criteria.

– “Asia” includes the following countries: Bangladesh, Bhutan, Brunei, Cambodia, China, Hong Kong, India, Indonesia, Japan, Laos, Malaysia, Mongolia, Myanmar, Nepal, North Korea, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, Timor-Leste, Vietnam.

– “Southeast Asia” includes the following countries: Brunei, Cambodia, Indonesia, Malaysia, Myanmar, Philippines, Singapore, Thailand, Timor-Leste, Vietnam.

– No contingent funding. If a company receives a commitment for $20M subject to hitting certain milestones but first gets $8M, only the $8M is included in our data.

– No business development / R&D arrangements whether transferable into equity now, later or never. If a company signs a $300M R&D partnership with a larger corporation, this is not equity financing nor is it from venture capital firms. As a result, it is not included.

– No buyouts, consolidations or recapitalizations. All three of these transaction types are commonly employed by private equity firms and are tracked by CB Insights. However, they are excluded for the purposes of this report.

– No private placements. These investments, also known as PIPEs (Private Investment in Public Equities), even if made by a venture capital firm(s).

– No debt / loans of any kind (except convertible notes). Venture debt or any kind of debt / loan issued to emerging, startup companies, even if included as an additional part of an equity financing, is not included. If a company receives $3M with $2M from venture investors and $1M in debt, only the $2M is included in these statistics.

– No government funding. Grants, loans or equity financings by the federal government, state agencies, or public-private partnerships to emerging, startup companies are not included.

– Fundings and unicorns from the following countries are not included: Afghanistan, Armenia, Azerbaijan, Bahrain, Cyprus, Georgia, Iran, Iraq, Israel, Jordan, Kazakhstan, Kuwait, Kyrgyzstan, Lebanon, Maldives, Oman, Palestine, Qatar, Russian Federation, Saudi Arabia, Syrian Arab Republic, Tajikistan, Turkey, Turkmenistan, United Arab Emirates, Uzbekistan, Yemen.