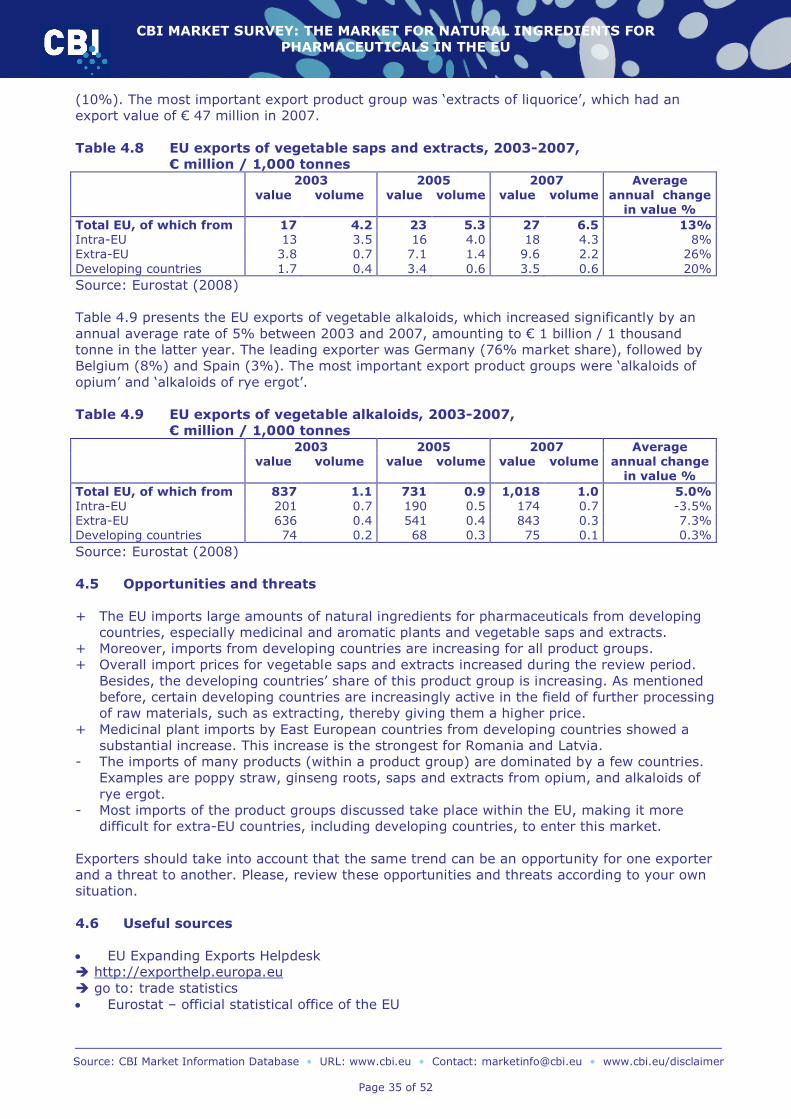

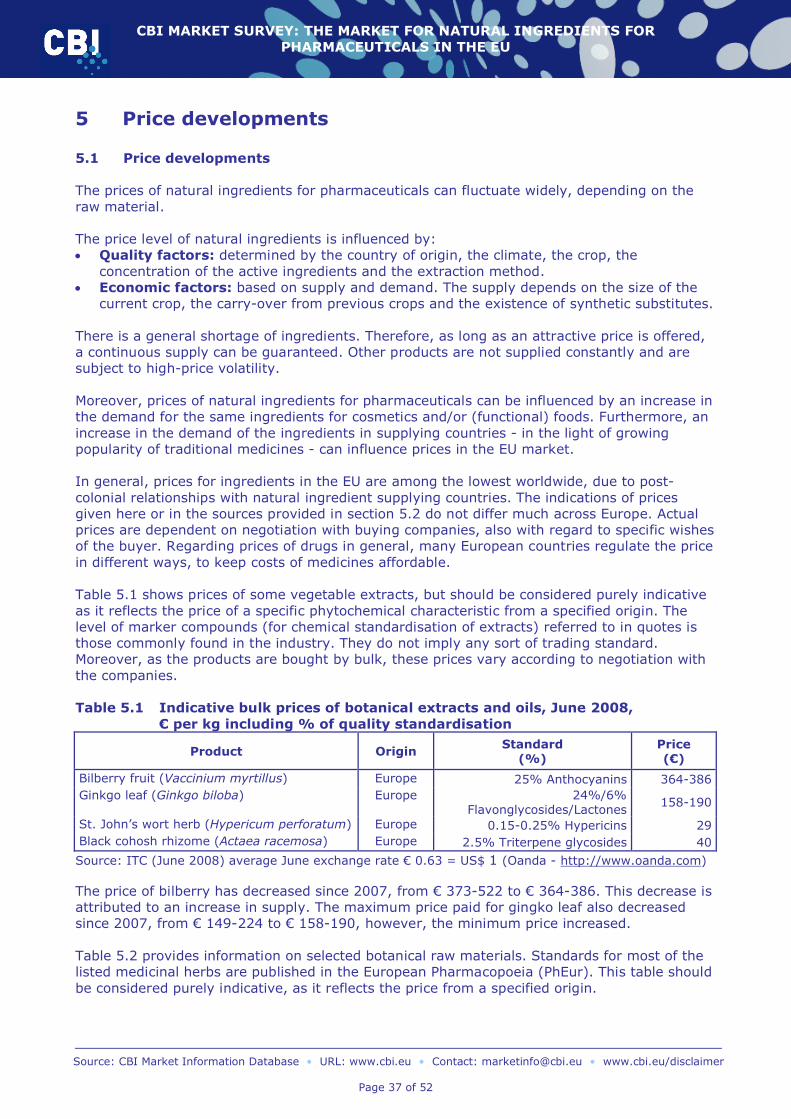

cbi market survey the market for natural … naturales... · this market survey provides exporters...

TRANSCRIPT

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 1 of 52

CBI MARKET SURVEY

THE MARKET FOR NATURAL INGREDIENTS FOR

PHARMACEUTICALS IN THE EUPublication date: October, 2008

CONTENTS

REPORT SUMMARY ..................................................................................................... 2

INTRODUCTION.......................................................................................................... 4

1 INDUSTRIAL DEMAND........................................................................................... 5

2 PRODUCTION...................................................................................................... 18

3 TRADE CHANNELS FOR MARKET ENTRY............................................................... 24

4 TRADE: IMPORTS AND EXPORTS ......................................................................... 29

5 PRICE DEVELOPMENTS........................................................................................ 37

6 MARKET ACCESS REQUIREMENTS ....................................................................... 40

7 OPPORTUNITY OR THREAT?................................................................................ 42

APPENDICES

APPENDIX A PRODUCT CHARACTERISTICS............................................................. 43

APPENDIX B INTRODUCTION TO THE EU MARKET .................................................. 47

APPENDIX C LIST OF DEVELOPING COUNTRIES ..................................................... 48

APPENDIX D LIST OF HERBS BASICALLY QUALIFIED FOR THE PREPARATION OF HERBAL MEDICINAL PRODUCTS ON THE EU MARKET......................... 50

APPENDIX E CULTIVATION VERSUS WILD COLLECTION......................................... 51

APPENDIX F REFERENCES ...................................................................................... 52

This survey was compiled for CBI by ProFound – Advisers In Developmentin collaboration with Klaus Dürbeck and Andrew Jones.

Disclaimer CBI market information tools: http://www.cbi.eu/disclaimer

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 2 of 52

Report summary

This market survey provides exporters of natural ingredients for pharmaceuticals with a wide range of facts, figures and information pertinent to the market in the European Union (EU). The market in individual EU countries is discussed further in separate market surveys. These market surveys can be downloaded at http://www.cbi.eu/marketinfo. The survey also includes a large number of references for additional research, primarily using the Internet.

The natural ingredients for pharmaceuticals in this survey fall into the following groups: Medicinal and aromatic plants; Vegetable saps and extracts; Vegetable alkaloids.

Industrial demand for natural ingredients for pharmaceuticalsNatural ingredients for pharmaceuticals are used in the conventional pharmaceutical industry and the herbal medicine market. Herbal medicines represent a range of product types, including products sold as raw herb (dried or fresh), and others, which are processed to varying degrees, including tinctures (an infusion of herbs in alcohol) and extracts (greater concentration of the active material of the plant with the aid of a solvent).

There certainly is a market for natural ingredients for pharmaceuticals in Europe. In 2007, total European sales of pharmaceutical products totalled € 176 billion, of which Germany, France and the United Kingdom had the largest market shares. The EU pharmaceutical market showed a growth of approximately 4% since 2005. This upward economic trend was reflected by growth figures in almost all EU countries. At the same time, East European countries, such as Poland, Romania and Slovakia, showed a strong growth between 2005 and 2007, generated mainly by a strong growth in non-prescription sales.

Furthermore, total pharmaceutical production in the EU amounted to approximately € 182 billion in 2006, or 35% of world’s production. France, the United Kingdom, Germany and Italy were the largest producers.

TrendsThe main trend taking place in the global trade of natural ingredients is the shift of further processing of raw plant material from Western countries to developing countries. It used to be rather challenging for exporters in developing countries to supply EU buyers with ready-to-use saps and extracts, because these were mostly processed within the EU. Nowadays, however, a limited but increasing number of suppliers in developing countries, most notably China and India, but also Brazil, Mexico and Malaysia, are able to supply processed ingredients. This shift was firstly related to lower-value saps but, as was notable at CPhI 2007, a major pharmaceuticals trade fair, this now also concerns further processed extracts. Nevertheless, industry sources indicate that EU companies remain competitive on the EU market, due to the very high quality demands and legislative requirements in the EU.

The use of natural ingredients for pharmaceuticals is expected to rise globally, both in conventional and herbal medicine. This upward trend is predicted not only because of general population growth, but also due to the increasing popularity of natural-based, environmentally-friendly products, which especially stimulates the consumption of herbal medicine. Next to these reasons, the demand for herbal medicines, and especially their renaissance in the EU, is driven by the following factors: Increasing costs of institutional, pharmaceutical-based health care; Interest of individuals, communities and national governments in greater self-reliance in

health care; Interest of communities and national governments in small and large-scale industrial

development based on local/national biodiversity resources;

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 3 of 52

Increasing success in validating the safety and efficacy of herbal remedies; Legislation improving the status of the herbal medicine industry; Renewed interest of companies in isolating useful compounds from plants; Search for new drugs and treatments of serious and drug-resistant diseases; Marketing strategies by the companies dealing in herbal medicine.

Production in the EUEurope's place in the production of medicinal and aromatic plants is of global importance. At least 2,000 medicinal and aromatic plants in Europe are used on a commercial basis, of which two-thirds are native to Europe. Of the 2,000 species, about 130 plant species are cultivated in the EU and less than 500 plant species are cultivated worldwide. Wild collection, especially in certain East European countries, plays a vital role in this. Nowadays, Eastern Europe is the most important region in Europe where medicinal plants are wild-collected. Bulgaria and Albania are important producers of medicinal plants in this region; and suppliers in Romania are specialized in the wild-collection of Arnica, which is widely used in Europe and the United States.

Trade structureEuropean-based companies and German companies in particular, dominate the global herbal supply industry. Manufacturers of herbal medicines used to acquire their raw materials from traders, but now some have their own plantations or have direct contact with producers.Besides, manufacturers of herbal products are increasingly interested in having direct relationships with producers of the required materials, in order to ensure a sustained source and/or to save costs (traceability). Furthermore, the capacity of many countries harbouring biological diversity to engage in value-adding research has expanded over the last decade. Companies are therefore increasingly open to collaboration with provider-country institutions, if they are confident of the quality and cost-effectiveness of the work of these institutions.

EU trade and developing countriesDeveloping countries accounted for a significant share in the EU market of natural ingredients for pharmaceuticals in 2007: 34% for medicinal and aromatic plants, 43% for vegetable saps and extracts and 22% for vegetable alkaloids. Especially the product group vegetable saps and extracts showed a strong average annual growth in imports from developing countries, corresponding with the trend that processing of raw plant material is increasingly taking place in developing countries.

In 2007, the leading developing country suppliers of medicinal and aromatic plants to the EU were China, India, Morocco, Egypt and Turkey. The leading suppliers of vegetable saps and extracts were Turkey, Iran and China, and of vegetable alkaloids were India, China, and Indonesia. China and India were the dominant developing country suppliers in this marketsegment.

Opportunities for exportersNext to general opportunities stemming from a growing demand for natural ingredients for pharmaceuticals, some more specific opportunities are discussed in this EU survey. First of all, next to certain ingredients and wild-collected ingredients mentioned in this survey, there are increasing opportunities for processed and value-added plant material. In the past, this appeared to be challenging for developing country suppliers, but this situation has somewhat improved. Moreover, natural ingredients not available within the EU, such as active ingredients from tropical fruits and vegetables, offer opportunities for developing country suppliers. Entering a niche market is also an interesting opportunity.

The registered growth of the production as well as consumption of (herbal) medicine in Central and East European countries also offer opportunities for developing-country producers of natural ingredients. For more information, see also the specific regular and compact country surveys of these countries.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 4 of 52

Introduction

This CBI market survey profiles the natural ingredients for pharmaceuticals market in the EU. The emphasis of this survey lies on those products, which are of importance to developing country suppliers. The role of and opportunities for developing countries are highlighted.

The natural ingredients discussed in this market survey fall under the following groups: Medicinal and aromatic plants (examples are ginseng roots, poppy straw and St John’s

Wort, but the variety is enormous, covering over 50,000 species used for medicinal purposes worldwide);

Vegetable saps and extracts (examples are liquorice extracts, aloe, hop extracts, agar-agar and guava, but here also the variety is very large);

Vegetable alkaloids (an alkaloid, strictly speaking, is a naturally-occurring amine produced by a plant. Examples are cinchona, opium and rye ergot).

For detailed information on the selected product groups, please consult appendix A. More information about the EU can be found in appendix B.

CBI market surveys covering the market in specific EU countries, specific product(group)s or documents on market access requirements can be downloaded from the CBI website. For information on how to make optimal use of the CBI market surveys and other CBI market information, please consult ‘From survey to success - export guidelines’. All information can be downloaded from http://www.cbi.eu/marketinfo go to ‘Search CBI database’ and select your market sector and the EU.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 5 of 52

1 Industrial demand

There is a general lack of information on the industrial demand for natural ingredients for pharmaceuticals. Therefore, this chapter on industrial demand will first discuss pharmaceutical consumption in general, then natural pharmaceutical and herbal medicine consumption. Afterwards, an overview of the pharmaceutical production in the EU will be presented. The developments of the pharmaceutical industry in the EU are interesting to understand in order to assess the needs of the market. The overall information given in this chapter will provide indicators of the industrial demand for natural ingredients for pharmaceuticals in the EU.

1.1 Market size

Pharmaceutical consumptionData from the Intercontinental Marketing Services (IMS Health) covering 90% of total pharmaceutical global sales, showed that global pharmaceutical sales increased by 6% to 7% in 2007. However, 2008 is expected to be a year of transition and global pharmaceutical sales are estimated to grow 5% to 6%, totalling € 460 billion. This small slow down on growth is expected to occur because of a decline in the cost of drug treatments, pricing and market access, among others. A shift in growth from the top seven markets to emerging markets is also expected.

Europe accounted for 31% of global pharmaceutical sales in 2007. Approximately 24% of sales of new medicines launched during the period 2002-2007 were generated on the European market (IMS, 2008). According to the European Self-Medication Association (AESGP)1, European sales of pharmaceutical products totalled € 176 billion in 2007, of which Germany, France and the United Kingdom had the largest share (together around 54%). These data are shown in Table 1.1, which also shows the total pharmaceutical market (non-prescription and prescription, excluding hospital sales) and the non-prescription (or Over-The-Counter, OTC) market.

The EU pharmaceutical market in 2007 showed a growth of approximately 4% in comparison to 2005. The upward economic trend is reflected by growth figures in almost all EU countries(except Italy). It is interesting to note that East European countries, such as Poland, Romania and Slovakia, showed a strong growth between 2005 and 2007, originating mainly in a strong growth in non-prescription sales.

Table 1.1 EU pharmaceutical market by country, excluding hospital sales, 2005-2007, in € million, share of non-prescription in % of value

Total Non-prescription% non-

prescript-ion drugs in 2007

2005€ mln

2006€ mln

2007€ mln

annual growth

2005€ mln

2006€ mln

2007€ mln

annual growth

EU Total* 163,063 167,828 175,733 4% 24,694 25,456 26,358 3% 15%Germany 35,085 35,100 36,600 2% 5,908 5,910 5,869 -0.3% 16%France 28,908 29,950 31,000 4% 5,668 5,840 5,921 2% 19%United Kingdom 25,204 25,944 26,617 3% 3,939 4,175 4,608 8% 17%Italy 19,431 19,185 19,053 -1% 2,195 2,044 2,139 -1% 11%Spain 12,841 13,454 14,032 5% 1,472 1,483 1,145 -12% 8%Poland 5,207 5,601 6,294 10% 1,309 1,427 1,663 13% 26%Greece 4,497 5,010 5,887 14% 350 364 435 11% 7%The Netherlands 5,119 5,347 5,585 4% 637 664 696 5% 12%Belgium 4,003 3,997 4,204 2% 595 619 634 3% 15%Austria 3,588 3,744 3,995 6% 326 323 339 2% 8%Sweden 3,541 3,712 3,968 6% 326 348 367 6% 9%

1 It should be noted that figures from IMS Health and AESGP cannot be compared, due to differing definitions of pharmaceuticals.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 6 of 52

Total Non-prescription% non-

prescript-ion drugs in 2007

2005€ mln

2006€ mln

2007€ mln

annual growth

2005€ mln

2006€ mln

2007€ mln

annual growth

Portugal 3,364 3,388 3,577 3% 238 284 267 6% 7%Denmark 2,239 2,441 2,706 10% 212 222 241 7% 9%Finland 2,367 2,361 2,509 3% 275 242 273 -0.4% 11%Hungary 2,015 2,131 2,072 1% 284 301 287 1% 14%Ireland 1,686 1,883 2,068 11% 263 292 330 12% 16%Romania 1,082 1,543 1,974 35% 166 364 458 66% 23%Czech Republic 1,526 1,488 1,881 11% 376 375 485 14% 26%Slovakia 920 1,081 1,224 15% 124 147 168 16% 14%Slovenia 440 468 487 5% 31 32 33 3% 7%Source: AESGP (2008)* Excluding: Bulgaria, Cyprus, Estonia, Latvia, Lithuania, Luxembourg and Malta.

Pharmaceutical products concern a broad range of products. However, in this market survey we will focus on the self-medication category and non-prescription market, as this includes the bulk of herbal medicine sales, which are an important destination for natural ingredients. Whereas non-prescription pharmaceuticals include all medicines which are available without a prescription from a physician, self-medication specifically relates to products which are directly available on shelf space in pharmacies, drugstores and supermarkets.

Table 1.2 shows expenditure on pharmaceutical, non-prescription and self-medication products in the European Union. Both the non-prescription and the self-medication market show growth between 2005 and 2007. In 2007, the European self-medication market amounted to € 25.4 billion, 70% of the total non-prescription market. The continuous growth of especially the self-medication sector can be explained by continuous product development, innovation and more products being available on the market. Several sub-markets can be distinguished within the self-medication market. The largest sub-markets are cough and cold medicaments, followed by analgesics and digestive products. Of the largest sub-markets, only analgesics and skin products exceeded the overall growth of the self-medication market.

Table 1.2 Pharmaceutical market in the EU, in € million2005€ mln

2006€ mln

2007€ mln

2005-2007% change

Total 163,063 167,828 175,733 4% Non-prescription 24,694 25,456 26,358 3%

Self-medication 17,110 17,566 18,568 4%Cough & cold 3,906 4,178 3,964 1%Analgesics 3,109 3,128 3,545 7%Digestives 2,625 2,627 2,712 2%Skin products 1,870 1,998 2,090 6%Vitamins and minerals 2,141 2,184 2,217 2%

Source: AESGP (2008)

Natural pharmaceuticals and herbal medicine consumptionDuring the last three decades, the herbal medicine market grew substantially around the world. At present, 80% of the population in developing countries relies on plant-based drugs for their healthcare needs, as these drugs are more widely available and more affordable.Moreover, their use is firmly embedded within wider belief systems, and local expertise is involved. In many developed countries, popular use of herbal medicine is fuelled by concern about the adverse effects of chemical drugs, but also by greater public access to health information (WHO, 2005). At present, herbal medicines have a global market share of approximately 30% (FNR, Agency of Renewable Resources, 2007).

Estimates of the overall value of natural pharmaceuticals vary considerably, also because of the use of different definitions. According to the Development Center for Biotechnology, the global market value for herbal medicines totalled € 19 billion in 2006 and it is expected to

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 7 of 52

surpass € 26 billion in 2011 (China Post, 2007). In Europe, herbal or phyto medicines have a relatively strong position compared to other markets, due to traditional acceptance and the high share in the reimbursement system for drugs. In 2003, the biggest markets for phyto-pharmaceuticals within the EU were Germany and France, comprising two thirds of the European market of around € 6 billion. Germany accounted for 39% of the market, while France accounted for 29%. Italy, Poland, the UK and Spain accounted for 7%, 6%, 6% and 4% of the market, respectively. Imports were significant, as domestic production only met a small proportion of demand (i.e. 5-10% in Germany, 30% in France) (IENICA, 2004).

Next to natural pharmaceuticals, strong growth is seen in the area of functional food. It is estimated that sales of extracts to the food industry, for use in functional foods, are growing by around 20% per year (Nutraingredients Europe - online newsletter, 2006), while the number of consumers of functional foods is growing between 6% and 7% annually. The major growth sectors are digestive health and functional food for the immune system (Foodtechnology - magazine, 2005).

EU production of (natural) pharmaceuticals Total pharmaceutical production in the EU amounted to approximately € 182 billion in 2006, or 35% of the world’s production. France, the United Kingdom, Germany and Italy were the largest producers, representing 19%, 14%, 13% and 12% of the total EU production, respectively.

Table 1.3 Pharmaceutical industry in the EU*, in € million1990 2000 2005 2006 2007**

Production 63,010 123,282 172,098 182,339 190,000

R&D expenditure 7,766 17,849 21,778 24,759 26,000* Data relate to EU-27, Norway and Switzerland since 2005**EstimationSource: EFPIA (2008)

Moreover, in 2006, the pharmaceutical industry invested about € 25 billion in Research & Development (R&D) in Europe. Compared to the North American and Asian regions, Europe is a relatively less attractive R&D investment location in terms of market conditions and incentives for the creation of new biopharmaceutical companies. R&D spending in the US grows more than twice as fast as in Europe (IMS, 2007).

Next to West European well-established pharmaceutical industries, Central and East European countries (mainly Poland, Hungary and the Czech Republic) are becoming increasingly important hotspots for pharmaceutical research. These countries offer low-cost manufacturing, and well-qualified medical practitioners are available to conduct clinical research.

The growing interest of the pharmaceutical industry in East and Central European countries also becomes visible in the manufacturing of natural pharmaceuticals. In Chapter 2 on the Production of medicinal plants in Europe, it becomes clear that the East European region has a long tradition in the collection and cultivation of herbs and medicinal and aromatic plants. Next to the availability of raw material, the countries (especially the Czech Republic, Poland and the three Baltic states) show many developments in the field of product innovations. This is alsorelated to the fact that these countries have not fully harmonised their regulations with EU regulations on herbal medicine. Examples of product innovations are pharmaceutical applications of active ingredients from fruit and vegetables.

Next to East and Central European countries, the established processing industries in countries such as Germany, Switzerland, France and the United Kingdom retain a large share in EU production of natural pharmaceuticals.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 8 of 52

Industrial demand for natural ingredients for pharmaceuticals

Medicinal and aromatic plantsIn 2004, the Food and Agricultural Organisation (FAO) estimated that only up to 13% of flowering plant species was used medically worldwide, constituting over 50,000 species out of an estimated total of 420,000. In the period 1991-2003, the reported average annual global exports of medicinal and aromatic plant material amounted on average to 467,000 tonnes, or approximately € 1.06 billion (FAO, 2004).

The international trade was dominated by only a few countries: 80% of the worldwide imports was channelled to just 12 countries. Three international trade centres for botanicals could be recognised: the USA for North and South America, Hong Kong for Asia, and Germany for intra-European trade. Europe was responsible for one third of the annual global imports. Germany accounted for 12% of the total, and four other EU countries (France, Italy, the United Kingdom and Spain) were among the major importers. In these countries, the raw material was mainly processed in each country’s industry, and then sold as finished products either on the domestic market or exported (FAO, 2004).

A large part of the EU demand for raw plant material is sourced from within the European Union, especially since the accession of Romania and Bulgaria, both being important producers of raw plant material. However, a vast array of tropical and subtropical plant species cannot be sourced in the EU, mostly due to climatic reasons. In Chapter 4, it becomes apparent that the imports by EU countries of raw plant material are increasing, and that imports from developing countries are also increasing. Germany, with its large extraction industry, is the biggestmarket for raw plant materials, but France and Italy are also of importance. Moreover, there is a growing demand from East and Central European producers, which increasingly position themselves in the market for natural ingredients for pharmaceuticals.

Table 1.4 shows the most important medicinal plants on the European market. Echinacea has been on the list for a long time. Gingko, Valerian and St. John’s Wort are confirmed as important plants by European importers and manufacturers. They also mention having had continued success with Hawthorn, Chamomile, Goldenseal, Garlic and Devil’s Claw. Several South African plants are also becoming more popular in Europe, especially in functional food markets. These include the antibiotic Umckalaoba in Germany, but also fruit extracts from baobab and wild melon (Nutraingredients, 2006).

Table 1.4 Top ten ranked medicinal plants and medicinal herbs most commonly used in the United States and Europe

Species Use

Hypericum perforatum Anxiety, depression, insomniaEchinacea purpurea Immune stimulationGinkgo biloba Dementia, Alzheimer’s disease, tinnitusSabal serrulata Benign prostatic hyperplasiaTanacetum parthenium Migraine prophylaxisAllium sativum Lipid-lowering, antithrombotic, fibrinolytic, anti-hypertensive, anti-theroscleroticZingiber officinalis AntiemeticPanax ginseng Tonic, performance enhancer, “adaptogen”, mood enhancerValeriana officinalis Sedative, hypnotic, anxiolyticEphedra distachya Asthma, rhinitis, common cold, weight loss; enhancer of athletic performanceSource: “Medicinal Plant Biotechnology. From Basic Research to Industrial Applications” (2007)

The information given above, and in Table 2.2 in the production chapter, do not show much overlap. From this, it becomes clear that European importers of many medicinal plant ingredients depend on sourcing in countries outside the EU.

Within the natural ingredients trade, a dominance of certain preferred wild-collected species and quantities can be observed above cultivated species. The main reason for this is that

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 9 of 52

domestication of plant species is very costly in terms of investment, in terms of time (around 10 years) and human capacity (e.g. seed masters). In 2005, the total value of organic wild production worldwide was estimated at between € 530 and € 630 million at FOB prices, of which 19% was destined for food supplements and 14% for natural remedies. The EU accounted for 43% of this market. Of the total organic wild-collected species market, 22% was constituted by medicinal and aromatic plants (International Trade Centre - ITC, 2006).

For more information on wild-collection, please refer to Table 1.5 (under Section 1.3 in this chapter) which shows a list of medicinal plants and notes whether they are principally cultivated or wild-collected. The subsequent section on certification of natural ingredients also discusses certification of wild-collected plants. Moreover, the following chapter on EU production and the CBI market surveys covering the market in individual EU countries also discuss wild-collection taking place in the EU.

Vegetable saps and extracts Vegetable saps and extracts are not only used by the pharmaceutical and herbal medicine industry, but also in the cosmetics and the food sectors. Unfortunately, total demand figures for this product group are not available and it is also quite difficult to isolate the demand of the pharmaceutical industry.

In general, European - and especially German - companies play a vital role in the trade and processing of vegetable saps and extracts. The most important EU consumers are also located in Germany, where there are many extractions and processing companies active in the saps and extracts trade. Furthermore, the new and increasingly important position of China and India as suppliers is also interesting to note.

It used to be rather challenging for exporters in developing countries to supply EU buyers with ready-to-use saps and extracts because these were mostly processed within the EU, isolating active ingredients, or making them suit other buyer requirements necessitating complicated processing steps. Nowadays, however, a limited but increasing number of suppliers in developing countries, most notably China and India, but also Brazil, Mexico and Malaysia, are able to meet such demands. This shift was firstly related to lower-value saps but, as was notable at CPhI 2007, a major pharmaceutical trade fair, this now also concerns further processed extracts. Nevertheless, industry sources indicate that EU companies remain competitive on the EU market, due to the very high quality demands and legislative requirements in the EU.

Furthermore, fruit and vegetable extracts are increasingly in demand. For example, from research conducted by the Scottish Crop Research Institute (2007), it became clear that blackcurrant is far more nutritious than other more exotic fruits containing high anti-oxidant contents. Blackcurrant is used in the food and pharmaceutical industries as well as in the intervening nutraceutical sector. At CPhI 2007, interest was also expressed for dried fruit powders of fruits with high contents of interesting ingredients, such as vitamins and anti-oxidants. The most evident example was the sales of cranberry powder.

Vegetable alkaloidsNo European market data is available for most of the products described here and therefore information is provided only on global demand. It is important to note that alkaloids predominately come from cultivated sources and have well established supply chains.

The six opium alkaloids which occur naturally in large amounts are morphine, narcotine, codeine, thebaine, papaverine and narceine. Of these, morphine, codeine, and thebaine are under international control. They are all three used in the drug industry, thebaine usually for conversion into some derivative which is more useful medically. They are all heavily regulated. Papaverine is also economically significant.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 10 of 52

A variety of actors is involved in the manufacture of opium-based products, ranging from government departments, which oversee licensed opium production schemes, to subsidiary companies of a small number of larger companies, among which are Europe’s Sanofi-Aventis, Bayer and Glaxo Smith Kline. They have numerous subsidiaries and partners and most of them operate in a number of different countries. In many cases, it is these subsidiaries which actually manufacture and market the opium-based medicines. In 2003, the global exports of licit opiates consisted of almost 500 tonnes opium (The Senlis Council, 2004). Currently, the global market for opiates shows upward trends, mostly due to an increased demand in Asia.

Cinchona alkaloid is another important alkaloid, widely used in the pharmaceutical and chemical industry. The most popular compound Quinine is a valuable anti-malarial agent and muscle relaxant. The commercial quinine market today is difficult to calculate. It is estimated that around 300-500 metric tons of quinine alkaloids are extracted annually from 5,000-10,000 metric tons of harvested bark. Nearly half of the harvested raw material is directed to the food industry for the production of quinine water, tonic water, and as an FDA-approved bitter food additive. The remainder is used in the manufacture of pharmaceutical products. Quinine is also used for a variety of ailments in European herbal medicine. Furthermore, natural quinine extracted from Cinchona bark is making a come-back in the treatment of malaria.

1.2 Market segmentation

The market for natural ingredients for pharmaceuticals can be segmented into ingredients required by the pharmaceutical industry, and those by the herbal medicine industry. Making an assessment of the size of each of these segments is not possible, but the earlier described market information has given us an idea of the end-market sizes.

Ingredients required by the pharmaceutical industry Around 80% of the conventional drugs on the market is plant-based, for which pharmaceutical companies are constantly looking for sources. Some well-known examples are morphine from opium poppy, atropine from belladonna, quinine from cinchona bark and benzyl penicillin.

Traditionally, pharmaceutical companies are large, vertically integrated corporations, which conduct the full range of activities, from creating libraries of compounds to marketing the drugs which emerge from their pipelines. However, since the 1980s the number of small pharmaceutical biotech companies has grown.

Ingredients required by the herbal medicine industryThe WHO “Global Atlas of Traditional, Complementary and Alternative Medicine” gives information on the status of this diverse and expanding field of medicine around the world.Several movements can be distinguished within the traditional herbal medicine industry, of which important on the European market are:

Traditional Chinese Medicine (TCM): is a range of traditional medical practices used in China which have developed over the course of several thousand years.

Ayurveda or ayurvedic medicine: is a 2,000-year-old comprehensive system of medicine, based on a holistic approach rooted in the ancient Indian Vedic culture.

Unani medicines: is a comprehensive system encompassing virtually all of the known healing systems of the world.

Western Traditional Herbal Medicine: the term 'Western' THM encompasses a number of similar, but unique and separate systems of herbal medicine. Western Herbal Medicine is also known as Phytotherapy, Phytomedicine and Botanical/Plant Medicine.

Homeopathy: is one type of alternative medicine, being particularly popular in Europe and India. Homeopathy rests on the premise of treating sick persons with therapeutic agents (drugs, remedies), which are deemed to produce in a healthy person, symptoms similar to those of the illness.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 11 of 52

Herbal medicines represent a range of product types. These include products sold as raw herb (dried or fresh), and others which are processed to varying degrees, including tinctures (an infusion of herbs in alcohol) and extracts (greater concentration of the active material of the plant with the aid of a solvent). Herbal medicines are part of larger markets, referred to in the USA, for example, as the ‘dietary supplement’ market. Dietary supplements encompass vitamins, minerals, herbs/botanicals, and other natural medicines.

1.3 Trends

Trends in (natural) pharmaceutical consumption and productionResearch shows that better health is what Europeans feel would most improve the quality of their lives. The search for a healthier life style increases the focus on healthcare issues and expenditure in new niche markets. In addition, rising healthcare demand is driven by a combination of socio-economic factors (e.g. population growth and ageing), rising health care expectations (people want to live healthier and longer lives), and technological progress (more diseases are being diagnosed and more diseases are being effectively treated).

Another more general trend concerns the production and innovation of pharmaceuticals in the European Union. Historically, European companies used to develop and produce the majority of new pharmaceuticals in the world. Recently, however, the pharmaceutical sector's centre of gravity has been steadily shifting from Europe to the USA. Whereas in Europe innovation is sometimes perceived as a threat to healthcare systems, US patients are better informed and more willing to embrace innovations (EFPIA, European Federation of Pharmaceutical Industries and Associations, 2007).

In contrast to the trend-sensitive cosmetic and food sectors, the pharmaceutical sector does not show the same pace of trends. As a matter of fact, the statement ‘natural’ is of less use for regular medicine than for food and cosmetic products. Since medicines are consumed as a result of, to some extent, urgent need, they are less sensitive to trends. Moreover, the herbal medicine market is a relative small market on its own, not much supported by the regular pharmaceutical industry as happens in the cosmetic industry. There, and in the food industry, the term ‘natural’ is used as a means of marketing, while in the pharmaceutical industry this is of less importance. Besides, publications showing negative outcomes of the use of natural medicines strongly influence the natural pharmaceutical market. Examples include the ban of Kava Kava on the EU market. This root, with relaxing and anti-depressive properties, was banned in the EU after reports linked it to some cases of liver damage. Moreover, the European pharmaceutical industry is in the hands of a few large players who, for a large part,define developments in the market.

Nevertheless, the general trend towards a preference for natural products is also influencing the herbal medicine market, enforced by the blurring of borders between pharmaceuticals and cosmetics (cosmeceuticals) and food (functional and health food).

The herbal medicine market is a relatively small market, but its significance is expected to rise globally. This upward trend is a result of the increasing popularity of natural-based, environmentally friendly products. The demand for herbal remedies, and especially their renaissance in the developed countries, is driven by the following factors (FAO, 2004): Increasing costs of institutional, pharmaceutical-based health care; Interest of consumers and national governments in greater self-reliance in health care; Interest of communities and national governments in small and large-scale industrial

development, based on local/national biodiversity resources; Increasing success in validating the safety and efficacy of herbal remedies; Legislation improving the status of the herbal medicine industry; Renewed interest of companies in isolating useful compounds from plants; Search for new drugs and treatments of serious and drug-resistant diseases; Marketing strategies by the companies dealing in herbal medicine.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 12 of 52

Other trends which have an impact on demand for botanical medicines and, consequently, the demand for natural pharmaceutical ingredients are the following: The entry of large pharmaceutical OTC companies has placed botanical medicines more

strongly on the mass market, thanks to increased advertising budgets. In December 2003, the EU parliament adopted new legislation that makes it easier for

traditional medicine producers to demonstrate efficacy in the European countries. Regarding limited therapeutic indications and in the absence of adequate clinical data, companies have to demonstrate safe use of a ‘traditional medicinal herbal product’ for 15 years within Europe and for 30 years in its community of origin. This enables the entry of new products into the EU market and has a positive effect on the demand for ingredients.

Consumers seek an alternative or complement to pharmaceutical drugs and modern healthcare, related to the “green” consumption movement. The entrance to the market of 'alternative' medicine from other cultures, such as Chinese herbal remedies and Ayurvedic medicines, has strengthened the positioning of herbal medicine.

Herbal remedies are sought by ageing populations afflicted by chronic diseases, for which modern medicine has few satisfactory treatments, or entails severe side effects.

Increasingly, consumers are turning to the Internet for self-diagnosis and to find healthcare solutions. There is, however, still a lack of knowledge about complementary treatments and many consumers indicate that they do not know enough about complementary medicines.

Research into rain forest biodiversity and other natural environments, by initiatives such as the Biotrade-programme of UNCTAD (United Nations Conference on Trade and Development), and publications such as “Amazon Your Business” help the development of natural medicines. The conventional pharmaceutical industry takes a more sceptical stance, seeing fewer truly significant contributions coming from these natural products.

Increased emphasis on safety, efficacy and quality has resulted in more research and development, a shift towards standardised products, and requirements for high-quality raw materials. This expanded research and development has improved the legitimacy of natural medicines. However, at a global level, government re-imbursement of natural medicines is decreasing.

Furthermore, an interesting upcoming trend in the market for natural pharmaceuticals is the growing demand for natural medicines for veterinary use. This trend is related to the growing demand for organic products and supports organic farming.

Trends in natural ingredientsTrends in the markets for pharmaceutical ingredients are dominated by the shift and increase of extract production in wealthy countries outside the traditional extract producer markets (e.g. Europe, North America and Japan). Regarding the demand for natural ingredients, this would signify an even more increasing demand for further processed ingredients from countries such as China, India and Brazil, but also Mexico, South Africa and Malaysia. Also, in the EU market this increase in the demand for natural ingredients is perceived, as East and Central European companies are increasingly taking over processing of raw materials into ingredients or even final products.

Most herbal medicines have a long history of traditional use, which confirms safety and efficacy, and their documentation is used in many regulatory systems to guide the approval of commercial products. This is, for instance, the case in the EU Directive Traditional Herbal Medicinal Products Directive (2004/24/EC). Moreover, driven by the increasing demand for active ingredients, more and more scientific research is being carried out on active ingredients of plant materials.

A future driver of growth in the demand for natural ingredients could be the increasing attention paid to products aimed at stimulating cognitive functions. Products launched in this sector have increased dramatically in the last five years. Products often featured were gingko biloba, ginseng (linked to improved memory), soy lecithin (linked to slowing down the progression of Parkinson’s) and St. Johns wort (combating depression) (Nutraingredients Europe, 2006).

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 13 of 52

Currently, a lot of research is conducted in the field of plant-based anti-cancer medicine and it is estimated that cancer drugs will become the largest category of herbal medicine, surpassing those for respiratory diseases. Green tea (extract) is mentioned several times as a popular ingredient but also coffee, pectin and other fruit and vegetable extracts, such as broccoli. Moreover, there are also examples of anti-cancer natural products derived from vinca alkaloids, extracted from Catharanthus roseus (Madagascar Periwinkle).

The following natural ingredients for pharmaceuticals have been spotted as being increasingly popular and used in product innovations:

Blackcurrant and other anthocyanin compounds causing the red and blue colour of berries and other fruits, containing high anti-oxidant levels and used for supplements;

Echinacea, to prevent common colds and flues; Green tea extract, used for a broad range of medicines; Southern African plants, such as Namibian Devil's Claw, treating arthritis, look set to

come in vogue. In general, the demand for products that treat or mitigate stress, fatigue and a feeling of life running too fast - remains strong;

Artemisia annua has been mentioned by the industry for anti-malaria treatment. The alkaloid quinine has also been mentioned by the industry as a popular natural

ingredient for pharmaceuticals; There is also a growing demand for natural vitamins, as a result of growing concern

about the use of chemically composed vitamins.

In general, EU companies are reporting a shortage of raw plant material, specifically for non-cultivated plant species. Several reasons explain this shortage (Klaus Duerbeck and ProFound, 2007):

There is an increasing demand from the herbal and pharmaceutical industry in the producing countries themselves, due to increasing popularity and purchasing power of the consumers (especially in China and India);

On the other hand, the sector for natural ingredients for the pharmaceutical is facing competition from the growing attention to bio-fuels, making production of oil crops more interesting for farmers;

During recent years, the downward price spiral for raw materials made it increasingly unattractive for raw plant material producers and ingredient suppliers to market their products to European counterparts;

The trend to go for sustainable production and certification has promoted value addition activities in the countries of origin;

Collectors are moving out of the collection business, due to alternative income opportunities;

Destruction of the natural habitat is affecting an increasing number of species.

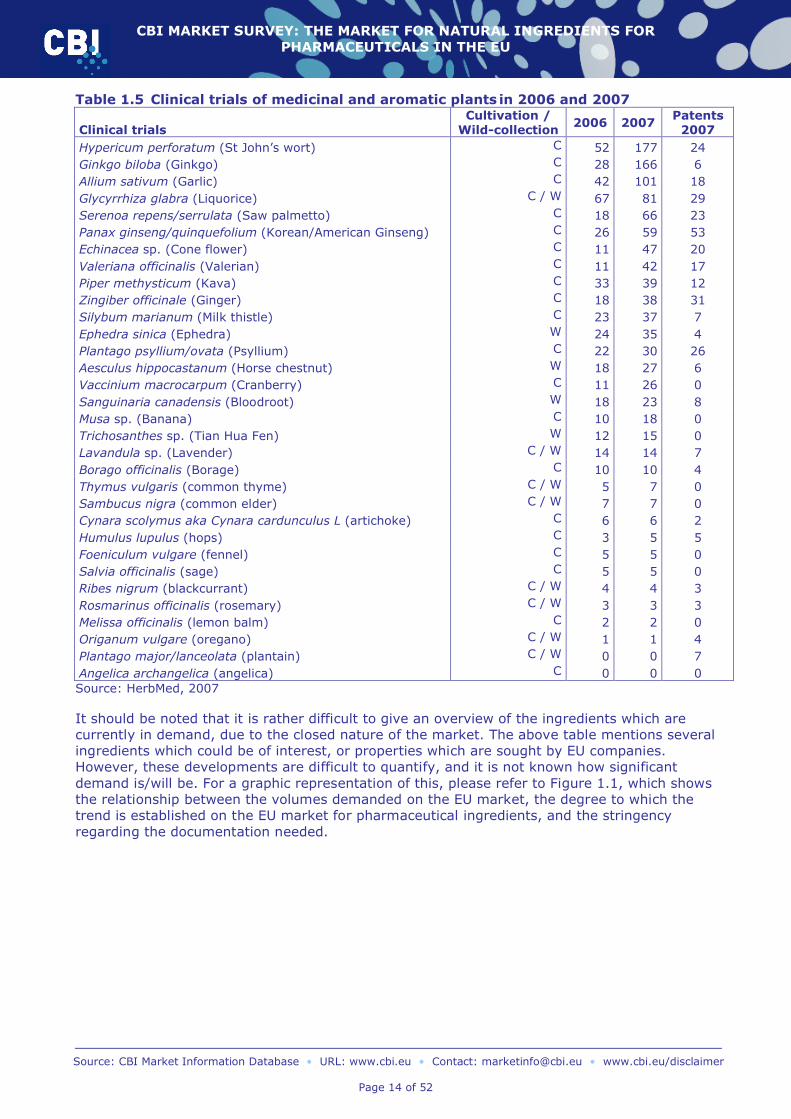

Clinical trialsClinical trials which are being conducted are a good indication of emerging product developments and species interesting for the medicinal industry. Globally, 748 clinical trials were conducted in 2007 on 96 plant species or their combination formulas. Hypericum perforatum (St John’s wort) topped the list with 177 clinical trials.

Furthermore, the number of patents is often a good indication of innovation concerning a product, including active ingredients and applicants. The table below presents the clinical trials until 2006, compared to the trials until 2007, as well as the number of patents in that same year.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 14 of 52

Table 1.5 Clinical trials of medicinal and aromatic plants in 2006 and 2007

Clinical trialsCultivation /

Wild-collection 2006 2007Patents

2007Hypericum perforatum (St John’s wort) C 52 177 24Ginkgo biloba (Ginkgo) C 28 166 6Allium sativum (Garlic) C 42 101 18Glycyrrhiza glabra (Liquorice) C / W 67 81 29Serenoa repens/serrulata (Saw palmetto) C 18 66 23Panax ginseng/quinquefolium (Korean/American Ginseng) C 26 59 53Echinacea sp. (Cone flower) C 11 47 20Valeriana officinalis (Valerian) C 11 42 17Piper methysticum (Kava) C 33 39 12Zingiber officinale (Ginger) C 18 38 31Silybum marianum (Milk thistle) C 23 37 7Ephedra sinica (Ephedra) W 24 35 4Plantago psyllium/ovata (Psyllium) C 22 30 26Aesculus hippocastanum (Horse chestnut) W 18 27 6Vaccinium macrocarpum (Cranberry) C 11 26 0Sanguinaria canadensis (Bloodroot) W 18 23 8Musa sp. (Banana) C 10 18 0Trichosanthes sp. (Tian Hua Fen) W 12 15 0Lavandula sp. (Lavender) C / W 14 14 7Borago officinalis (Borage) C 10 10 4Thymus vulgaris (common thyme) C / W 5 7 0Sambucus nigra (common elder) C / W 7 7 0Cynara scolymus aka Cynara cardunculus L (artichoke) C 6 6 2Humulus lupulus (hops) C 3 5 5Foeniculum vulgare (fennel) C 5 5 0Salvia officinalis (sage) C 5 5 0Ribes nigrum (blackcurrant) C / W 4 4 3Rosmarinus officinalis (rosemary) C / W 3 3 3Melissa officinalis (lemon balm) C 2 2 0Origanum vulgare (oregano) C / W 1 1 4Plantago major/lanceolata (plantain) C / W 0 0 7Angelica archangelica (angelica) C 0 0 0Source: HerbMed, 2007

It should be noted that it is rather difficult to give an overview of the ingredients which are currently in demand, due to the closed nature of the market. The above table mentions several ingredients which could be of interest, or properties which are sought by EU companies. However, these developments are difficult to quantify, and it is not known how significant demand is/will be. For a graphic representation of this, please refer to Figure 1.1, which shows the relationship between the volumes demanded on the EU market, the degree to which the trend is established on the EU market for pharmaceutical ingredients, and the stringency regarding the documentation needed.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 15 of 52

Figure 1.1 Representation of the natural trend in the market for pharmaceutical ingredients

Source: Adapted from Andrew Jones and Klaus Duerbeck, 2007

Corporate Social Responsibility (CSR)There is an increasing interest in social and environmental aspects when doing business in the EU market, especially when the final product is natural and/or organic. It should be noted that, for a product to be certified, detailed documentation over the organic and/or Fair Trade chain is needed for traceability purposes. Despite the fact that there is still CSR certification, social responsibility increasingly finds a way to the market. Various schemes focus on different areas along the supply chain for production, processing, trade, manufacturing and marketing:

Product quality certification - such as the legislative GMP (Good Manufacturing Practices), also GACP (Good Agricultural and Collection Practices). For more information please check http://www.who.int

Organic certification - organically certified raw materials and value-added products are increasingly being requested by European companies on the phyto-pharmaceutical market. This is, for example, used for the development of new products. The organic certification also serves as a guarantee for quality. For more information, please check the International Federation of Organic Agriculture Movements (IFOAM) - http://www.ifoam.org

Natural ingredients collected in the wild2 - are also increasingly organically certified. Currently, the following schemes have been developed: Organic Wild Collection (ISSC-MAP) - http://www.floraweb.de/map-pro; and FairWild - http://www.fairwild.org

Forest management certification – which supports the conservation of forests. For more information, visit the website from the Forest Stewardship Council (FSC) -http://www.fsc.org

Social certification - of which the most prominent is Fair Trade - http://www.fairtrade.net –although it is less interesting for pharmaceutical ingredients.

For CSR specifically, an interesting certification body is the Global Reporting Initiative (GRI) -http://www.globalreporting.org - which has developed a sustainability reporting framework. This framework sets out the principles and indicators that organizations can use to measure and report their economic, environmental and social performance.

1.4 Opportunities and threats

+ As became clear from this section, the pharmaceutical, especially the non-prescription market, as well as the natural pharmaceutical market, showed a growing demand during the review period. As a result, the European production of (natural) pharmaceuticals also

2 Appendix E provides an overview of advantages and disadvantages of wild collection as opposed to cultivation.

degree of establishment of trend

raw material from cultivation / wild-collection

CSR

certification

documented use in traditional medicine

natural ingredients

Ascending documentation

needed

Ascending volumes

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 16 of 52

showed some growth. Both consumption and production growth indicated opportunities for suppliers of natural ingredients for pharmaceuticals. Within the EU, the East and Central European pharmaceutical markets showed the highest market growth.

- On the other hand, East and Central European countries are also developing their (natural) pharmaceutical ingredient sectors in order to further process the raw materials, thereby posing a threat to suppliers in developing countries who want to enter the EU market.

- Moreover, Europe seems to offer fewer opportunities for innovation and a shift of pharmaceutical research and development is observed from the EU to the USA. This could pose a threat to developing country suppliers to EU pharmaceutical companies.

+ Natural ingredients not available within the EU, such as active ingredients from tropical fruits and vegetables, offer good opportunities for developing country suppliers. Moreover, since the process of domestication of wild-collected raw plant material is expensive, there is a solid demand for certain wild-collected plant species. Next to certain ingredients and wild-collected ingredients, there are increasing opportunities for processed and value-added plant material. In the past, this appeared to be more challenging for developing country suppliers; however suppliers from larger developing countries (i.e. China and India) have entered the market for processed ingredients.

+/- However, it should be stressed, that in almost all cases, the EU buyer will ask for well-documented ingredients, at least meeting GMP standards. Traceability and transparency in the supply chain is increasingly important in the global trade of natural ingredients, posing a threat to some suppliers.

+ In that sense, different kinds of certification standards, such as organic certification, could signify an opportunity. Regarding pharmaceuticals, certification is not so much used for actual marketing of the end-product, but as a proof of traceability. This could add value to the quality of the ingredient offered. Organic production is particularly attractive for growers in developing countries, since much of their production is already organic, although not certified (‘organic by default’).

+ The indicated clinical trials can also offer an opportunity, as they indicate new products and new applications for the medicinal industry. Plants which could be an opportunity are for example St Johns wort and Ginkgo which have undergone a large amount of clinical trials and, moreover, the trials have increased strongly since 2006. An increasing number of trials is an indication of possible growth in future demand for a product.

1.5 Useful sources

(Natural) pharmaceutical associations and other sector-related organisations offering market information are: The European Federation of Pharmaceutical Industries and Associations (EFPIA) -

http://www.efpia.org - provides information, national codes of practice and links to national associations.

The European Self-Medication Industry (AESGP) - http://www.aesgp.be - provides facts and figures on the European pharmaceutical, self-medication, and non-prescription market.

European Medicines Agency (EMEA) - http://www.emea.europa.eu European Herbal & Traditional Medicine Practitioners Association (EHTPA) -

http://www.ehpa.eu European Health Product Manufacturers (EHPM) - http://www.ehpm.org Interactive European Network for Industrial Crops and their Applications (IENICA) -

http://www.ienica.net - provides reports on commercial-industrial crops in the EU. The European Scientific Cooperative on Phytotherapy (ESCOP) - http://www.escop.com

Furthermore, Herb World - http://www.herbnet.com/associations_p1.htm - provides links to national associations of herbs and health product manufacturers in the European Union.

Also of interest are further market research organisations, especially those focusing on the pharmaceutical industries, which provide reports on a large number of industries. Examples are:

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 17 of 52

IMS Retail Drug Monitor - http://www.imshealth.com - published every month under ‘Press Room’ and ‘Top-line Industry Data’; it tracks monthly sales of medicinal products by retail pharmacy outlets in 13 key markets worldwide.

Piribo - http://www.piribo.com – is a reliable source of information for the global biotechnology, healthcare and pharmaceutical industries.

Espicom - http://www.espicom.com – is an interesting and reliable source of information for the pharmaceutical and medical devices market.

Useful trade press links providing market information are the following: Nutraingredients - http://www.nutraingredients.com/news - an interesting site with new

developments on consumption, companies and production. Nutraceuticals International - http://www.marketletter.com/nutra.htm - gives information

and tendencies for the nutraceuticals market CABI - http://www.cabi.org - is a non-profit organization specialized in scientific publishing,

research and communication. American Botanical Council - http://abc.herbalgram.org Nutrition Business Journal - http://nutritionbusinessjournal.com Pharma Marketing Service - http://www.fachzeitung.com Zeitschrift für Arznei- und Gewürzpflanzen - http://www.zag-info.de Agro Food Industry Hi-tech - http://www.teknoscienze.com Fitoterapia Journal - http://www.indena.com/pages/fitoterapia.php

Furthermore, Herb World - http://www.herbnet.com/press_p5.htm - is an interesting source of magazines in the field of medicinal herbs.

Three other interesting sources for market information are: Herbmed - http://www.herbmed.org - an interactive, electronic herbal database which

provides access to the scientific data underlying the use of herbs for health. Amazon Your Business - http://www.amazonyourbusiness.nl - an interesting new

publication on business opportunities for products from the Amazon, including medicines. PhytoLab - http://www.phytolab.com - an officially recognized laboratory for the testing of

plant-based products in Germany.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 18 of 52

2 Production

2.1 Size of production

Medicinal and aromatic plants (MAP) IntroductionWorldwide, between 50,000 and 70,000 plant species are used in traditional and modern medicinal systems (Federal Agency for Nature Conservation, 2007). Medicinal and aromatic plant (MAP) material is obtained both from plants growing in the wild and from cultivation. Worldwide, about 80% of the species used is harvested in the wild. Unfortunately, around4,000 species are endangered by over-collection (WWF, 2007).

Traditionally, production of most herbs and spices has been concentrated in the temperate and semi-tropical regions of the world. This follows from the low wage rates of the labour intensive production and climatic considerations. The processing of medicinal herbs and spices remains concentrated in Europe, particularly in Germany and France, and in Asia (especially China and Korea). Other significant processing areas include Yugoslavia, Bulgaria and Hungary.

According to the wildlife trade monitoring network Traffic, the largest quantities wild-collected in the following countries are the MAP species: sage in Albania and Bosnia-Herzegovina; juniper in Bosnia-Herzegovina; dog-rose in Bulgaria; nettle in Croatia; field shave-grass (Equisetum arvense) in Croatia; and bilberry and raspberry in Romania. Furthermore, species like Yellow Gentian (Gentiana lutea) and Mountain Tea (Sideritis raeseri) have become endangered in the Balkans (Traffic, 2005).

The trade in former East European countries has changed in recent years from strictly organised, state-controlled systems, to free and diversified markets with an increasing number of competing private companies. This has also had negative effects on the sustainability and conservation of MAPs, because previous quotas and controls are now largely ignored (IENICA, 2005). Furthermore, in some East European countries, the production of medicinal herbs is stimulated through, for example, EU subsidies in Bulgaria (SAPARD - Special accession programme for agriculture and rural development, 2007) and a rural development programme in Hungary (MARD - Ministry of Agriculture and Rural Development, 2007).

Wild collection in the EUWild collection plays a vital role in the use of, and trade in, MAPs in Europe, since cultivation has not proved to be manageable and profitable for the majority of the plants traded. At least 2,000 medicinal and aromatic plants in Europe are used on a commercial basis, of which two-thirds (1,200-1,300 species) are native to Europe (Planta Europa – a network of independent organisations, 2007). Of the 2,000 species, about 130 plant species are cultivated in the EU and less than 500 plant species are cultivated worldwide (Duerbeck, 2005).

Nowadays, Eastern Europe is the most important region in Europe where medicinal plants are wild-collected (Kathe, 2006). Bulgaria and Albania are important producers of medicinal plants in this region; and suppliers in Romania are specialized in the wild-collection of Arnica, which is widely used in Europe and the United States.

The deregulation of state-controlled commerce of MAPs in new EU countries has resulted in an increase in wild-collection, which is becoming a problem for the environment. In Estonia, most herbs for health products are collected in the wild; in Hungary, approximately 25% of total production (120 plant species) is collected, with an output of 10,000-15,000 tonnes of dried plant material each year; in Romania around 155 varieties of medicinal and aromatic plants are collected in the wild (750-850 tonnes/year) (IENICA, 2005).

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 19 of 52

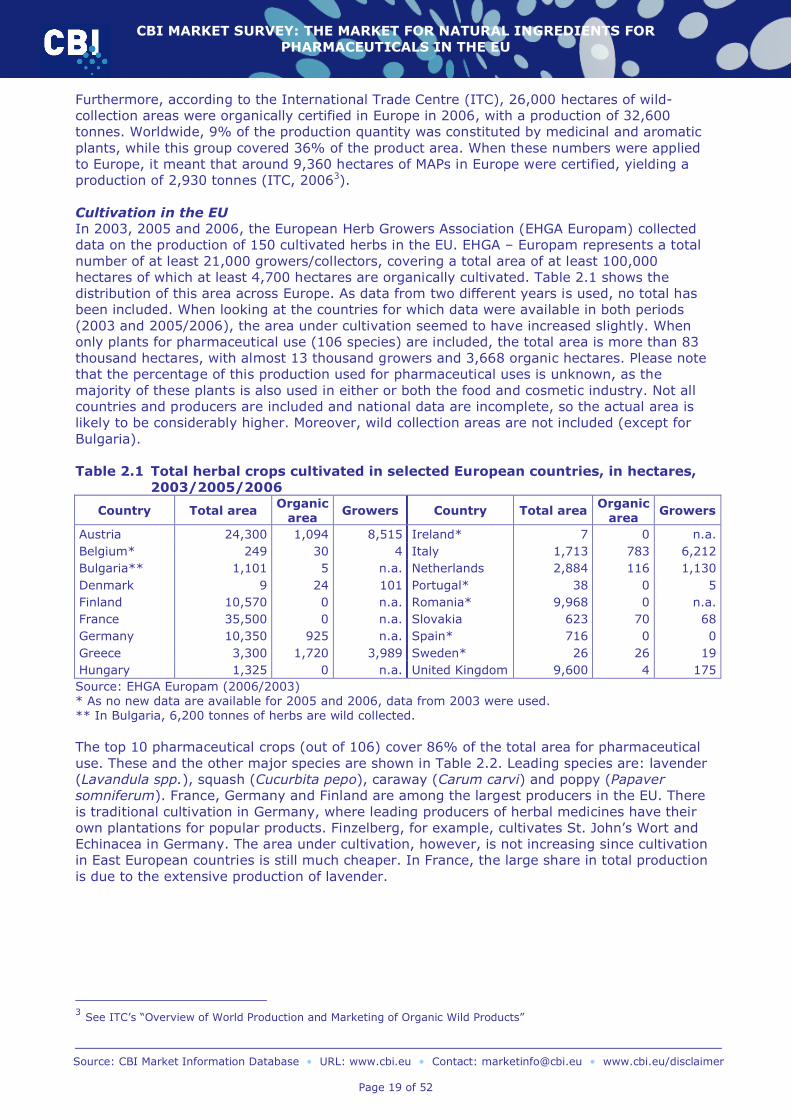

Furthermore, according to the International Trade Centre (ITC), 26,000 hectares of wild-collection areas were organically certified in Europe in 2006, with a production of 32,600 tonnes. Worldwide, 9% of the production quantity was constituted by medicinal and aromatic plants, while this group covered 36% of the product area. When these numbers were applied to Europe, it meant that around 9,360 hectares of MAPs in Europe were certified, yielding a production of 2,930 tonnes (ITC, 20063).

Cultivation in the EUIn 2003, 2005 and 2006, the European Herb Growers Association (EHGA Europam) collected data on the production of 150 cultivated herbs in the EU. EHGA – Europam represents a total number of at least 21,000 growers/collectors, covering a total area of at least 100,000 hectares of which at least 4,700 hectares are organically cultivated. Table 2.1 shows the distribution of this area across Europe. As data from two different years is used, no total has been included. When looking at the countries for which data were available in both periods (2003 and 2005/2006), the area under cultivation seemed to have increased slightly. When only plants for pharmaceutical use (106 species) are included, the total area is more than 83 thousand hectares, with almost 13 thousand growers and 3,668 organic hectares. Please note that the percentage of this production used for pharmaceutical uses is unknown, as the majority of these plants is also used in either or both the food and cosmetic industry. Not all countries and producers are included and national data are incomplete, so the actual area is likely to be considerably higher. Moreover, wild collection areas are not included (except for Bulgaria).

Table 2.1 Total herbal crops cultivated in selected European countries, in hectares, 2003/2005/2006

Country Total area Organicarea

Growers Country Total area Organicarea

Growers

Austria 24,300 1,094 8,515 Ireland* 7 0 n.a.Belgium* 249 30 4 Italy 1,713 783 6,212Bulgaria** 1,101 5 n.a. Netherlands 2,884 116 1,130Denmark 9 24 101 Portugal* 38 0 5Finland 10,570 0 n.a. Romania* 9,968 0 n.a.France 35,500 0 n.a. Slovakia 623 70 68Germany 10,350 925 n.a. Spain* 716 0 0Greece 3,300 1,720 3,989 Sweden* 26 26 19Hungary 1,325 0 n.a. United Kingdom 9,600 4 175Source: EHGA Europam (2006/2003)* As no new data are available for 2005 and 2006, data from 2003 were used.** In Bulgaria, 6,200 tonnes of herbs are wild collected.

The top 10 pharmaceutical crops (out of 106) cover 86% of the total area for pharmaceutical use. These and the other major species are shown in Table 2.2. Leading species are: lavender (Lavandula spp.), squash (Cucurbita pepo), caraway (Carum carvi) and poppy (Papaver somniferum). France, Germany and Finland are among the largest producers in the EU. There is traditional cultivation in Germany, where leading producers of herbal medicines have their own plantations for popular products. Finzelberg, for example, cultivates St. John’s Wort and Echinacea in Germany. The area under cultivation, however, is not increasing since cultivation in East European countries is still much cheaper. In France, the large share in total production is due to the extensive production of lavender.

3 See ITC’s “Overview of World Production and Marketing of Organic Wild Products”

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 20 of 52

Table 2.2 Top herbal crops with pharmaceutical use cultivated in Europe, in hectares, 2003/2005

Scientific name

Common name

Totalarea

Growers Organicarea

Scientific name

Common name

Totalarea

Growers Organicarea

Total pharm.l used herbs

-- 83,112 12,781 3,668 Chamaemelum nobile

Chamomile 241 5 1

Lavendula spp, Lavender 21,410 86 108 Melissa officinalis

Lemon balm 234 134 74

Cucurbita pepo Squash 15,100 5,000 300 Hippophae rhamnoides

Sea Buckthorn

206 50 20

Carum carvi Caraway 13,536 623 66 Fraxinus ornus Ash 200 110 0Papaver somniferum

Poppy 11,300 850 50 Hypericum perforatum

St Johns Wort

197 68 27

Borago officinalis

Borage 2,719 31 2 Oenothera biennis

Evening primrose

192 5 7

Silybum marianum

St Marys thistle

2,527 343 7 Nasturtium officinale

Watercress 179 1 0

Humulus lupulus

Hops (10% med./ 90% arom.)

2,133 275 13 Sambucus nigra

Common elder

172 42 31

Chamomilla recutita

German chamomile

1,809 110 258 Digitalis lanata Woolly foxglove

165 27 0

Salvia sclarea Clary sage 1,045 20 7 Rosmarinus officinalis

Rosemary 158 99 17

Mentha piperita Peppermint 967 153 40 Echinacea spp Echinacea 156 73 62Ocimum basilicum

Basil 834 1,505 20 Plantago lanceolata

Plantain 131 40 20

Foeniculum vulgare

Fennel 651 138 198 Fagopyrum esculentum

Buckwheat 131 75 35

Crocus sativus Saffron crocus

645 1,120 1,724 Helianthus tuberosus

Jerusalem artichoke

116 20 10

Thymus vulgaris

Common thyme

624 134 44 Melilotus officinalis

Yellow melilot

106 12 13

Origanum vulgare hirtum

Greek oregano

579 251 0 Cynara scolymus

Globe artichoke

92 6 5

Origanum marjorana

Marjoram 558 25 20 Anisum vulgare

Aniseed 83 15 69

Cannabis sativa Hemp 450 203 49 Plantago scabra

Plantain 82 0 0

Ribes nigrum Blackcurrant 446 12 9 Origanum vulgare

Wild oregano

81 60 14

Gingko biloba Maidenhair tree

430 0 0 Papaver somniferum

Opium poppy

76 11 0

Aromacia rusticana

Horseradish 380 180 7 Angelica archangelica

Angelica 75 4 0

Salvia officinalis Sage 289 156 58 Glycyrrhizaglabra

Liquorice 75 9 71

Valeriana officinalis

Valerian 281 51 16 Gentiana lutea Great yellow gentian

72 11 2

Mentha spp Mint 271 32 20 Plantago psillium

Ispagula 59 9 22

Allium sativum Garlic 263 295 5 Salix spp Willow 58 16 1

Source: EHGA Europam (2005)Please note that this table only includes data from 2005 (in which information was not provided for several of the countries included in Table 2.1 in which information from 2003 has been included). Therefore these tables cannot be compared.

Vegetable saps and extractsThe processing of medicinal herbs is concentrated in countries with strong herbal and traditional medicine. Significant production areas in Europe include France, Balkan countries, Germany, Poland and Hungary. Germany has a very large medicinal and aromatic plant extraction industry and the largest percentage of medicinal herbs is brokered through that country. The United Kingdom is one of the major centres of research and development in the field of tropical commodities and extracts, while China and Korea are the two major producers in the Asian region.

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 21 of 52

Vegetable alkaloidsAccording to our sources, there is no production of cinchona or rye ergot in Europe. There are, however, companies such as Buchler GmbH - http://www.quinine-buchler.com - which process and trade these products. Germany, France and the United Kingdom, are important alkaloids extraction countries. Trading houses in Germany include Buchler GmbH and Henry Lamotte -http://www.lamotte.de; in the United Kingdom they include StanChem International -http://www.stanchem.co.uk. Alkaloids of opium are mostly produced in the UK and Germany. Production of opium is strictly regulated.

2.2 Trends

As mentioned before, trends in the market of pharmaceutical ingredients are dominated by the shift and increase of extract production in resource-rich countries outside the traditional extract producer markets. Recent trade shows an important shift of the extract manufacturers to the increasing dominance of manufacturers in China, India and Brazil, but also countries such as Mexico, South Africa and Malaysia are emerging as well-functioning sourcing networks. The availability of natural resources and raw material is an advantage in this. These new producing countries are not only producing for the Western markets, but also for the increasingly important local and regional markets, where consumers have found new interest in local therapies.

The same trend can be observed within the EU: East European countries are increasingly taking a more dominant position in the processing and manufacturing of (natural) pharmaceuticals. The fact that they are also the largest producers of raw plant material in the EU is adding value to this position. Established Western companies, however, retain a dominant position regarding the trading of (natural) ingredients and the marketing of end-products.

Cultivation and wild-harvestingSince the demand for cultivated plant material started competing with the demand for wild-harvested ingredients, various trends were triggered. No clear statement can be made as to which of the two is preferred on the EU market. In general, in all countries, the industry remains dependent on wild-collected plant material, particularly since wild-collected plant material can be procured from certified (organic) wild collection (Duerbeck, 2005). Other reasons for this are the high costs of domestication and cultivation (Bundesamt für Naturschutz - BfN, 2007). Moreover, cultivation is not necessarily the most beneficial production system for MAP species. Furthermore, wild-collection provides the main income forrural households, especially in lower income countries (BfN, 2007).

There is, however, a group of companies, focusing especially on the mass-market, which prefer cultivated material. Cultivated materials of important species provide: a reliable supply and volume, at an agreed price, guaranteed over time; quality control can be better assured (e.g. species authentication, unadulterated material,

known input of pesticides, fertilizers, good post-harvest handling); the active compound content can be standardized; and material can be certified organic or biodynamic.

For example, Weleda AG - http://www.weleda.com - in Germany cultivates around 250 species on its property, and seeks to bring more into cultivation. This production is conducted within the company, using its own investments. Outsourcing is less common and it is a slow development, with very limited numbers of species taken into cultivation each year. Moreover, production of more specialist plants is increasing, using organic or bio-dynamic cultivation techniques.

Smaller herbalist-based companies in Europe, which consume limited quantities of raw material (often wild-harvested species), also find it difficult to maintain direct sourcing

CBI MARKET SURVEY: THE MARKET FOR NATURAL INGREDIENTS FOR PHARMACEUTICALS IN THE EU

Source: CBI Market Information Database • URL: www.cbi.eu • Contact: [email protected] • www.cbi.eu/disclaimer

Page 22 of 52

relationships for species outside their geographic area, given the costs involved in building these relationships and tracking the materials. Therefore, they prefer to source their raw material from the same region where they process pharmaceuticals.

Wild collection standardsOver-harvesting of medicinal and aromatic plants, land conversion and habitat loss threaten around 4,000 species worldwide. For these reasons, approaches to wild MAP collection, which balance the needs of local, regional, and international markets with the need for conservation and sustainable use, are urgently needed. It is essential, regarding any wild-collected source, to work towards developing sustainable sources.

In recent years, a number of initiatives has been launched to achieve a better framework for the sustainable use of biological diversity. These have been discussed in the previous section.

Other trendsOther trends in the production of medicinal plants are (Foster, 2006): increased attention to Good Agricultural and Collection Practices (GACP); increased attention to traceability; supplier and manufacturer accountability; and increasing opportunity for socially responsible direct farmer/supplier relationships (i.e.

consumers in rich countries want to “feel good” about the products they use).

Furthermore, EU companies are increasingly producing both conventional and organic product lines, and are offering ingredients destined for the cosmetic, food, OTC healthcare and pharmaceutical sectors. They are diversifying their product range to enter different sectors in the EU, although, of course, some companies still only offer ingredients to a specific sector. This shows the need for developing country suppliers to carry out more market research, to target the right company, or right division in a company, and to pay close attention to the sectors in which they are interested, before contacting companies in the EU.

2.3 Opportunities and threats

+ Due to climatic conditions, many raw materials for natural ingredients for pharmaceuticals, especially non-temperate, cannot be grown in the EU, and have to be imported from elsewhere. Moreover, many raw materials require considerable labour input and can therefore be grown/collected more cheaply in developing countries. Taking only the competition from EU production into account, developing country exporters may find the best opportunities in the supply of exotic ingredients, or their (semi-processed) raw materials, for which the production conditions are not favourable in the EU. In contrast, exporters of temperate products or further processed products are threatened by EU producers. Moreover, production of further processed natural ingredients, such as saps and extracts, can lie outside of the scope of many developing country producers, but should nevertheless be explored. Increasingly, countries such as India and China are able to supply processed ingredients.

+/- Traceability of ingredients is increasingly required by companies and ingredient processors in the EU. Suppliers in developing countries, who have a system of tracing and tracking supported by documentation, have a competitive advantage in dealing with EU importers.