ceo quarterly market review q2 2017/18 - mosl · 1 mosl ceo quarterly market review q2 2017/18. ......

TRANSCRIPT

CEO Quarterly Market ReviewQ2 2017/18

5committees established

3working groups

established

1market code

dispute

2.7m supply points

planned settlement runs

corrective settlement runs

over

61,000 services switched

cost of

£1.1m to operate the market per month

Financial settlement of around

3.5m transactions1

code changes considered by the Panel15

15

21

1 Transactions relate to all interactions by trading parties with the central system (CMOS), e.g. switches, meter readings, etc.

£210ma month

Market to Date

1 self-supply retailer

22 national retailers

12 regional retailers

35retailers

in the market

25wholesalers

Contents

Foreword 1

Review of the second quarter 3

– The market landscape 3

– Switching 3

– Settlement and data quality 9

– Market change 10

Looking forward 11

1 Transactions relate to all interactions by trading parties with the central system (CMOS), e.g. switches, meter readings, etc.

Welcome to our second Quarterly Market Review, reflecting on non-household retail water market activity from July to September 2017.

The new open water market continues to offer 1.2 million business customers the opportunity

to shop around for the best deal. Six months since full market opening on 1 April 2017 there are seven more parties progressing through market entry assurance and an additional self -supply retailer has achieved its market entry certification. We have seen more than 61,000 switches and a significant increase in the number of transactions processed by the central marketing operating system (CMOS) compared to the previous quarter.

CMOS

We have improved the functionality of CMOS at an operational level following the release of version 3.0 on 30 September. This improved functionality covers:

A new volume transfer process

Changes to trade effluent

Tariffing updates

Cross border meters.

CMOS 3.0 is the first release focused on new functionality rather than defect resolutions and is part of our cycle of two major releases a year. We are sensitive to the demands that our releases place upon member IT services and are planning to reduce the frequency of releases in 2018/19.

MOSL changes

There has also been significant change within MOSL. On 1 September Jim Keohane officially took up his responsibilities as MOSL Chair and on 27 September we welcomed Mel Karam, Chief Executive of Bristol Water, as our new Wholesaler Director on the MOSL Board for a two-year term. I would like to express my sincere thanks to Peter Simpson, our outgoing Wholesaler Director, for his dedication and hard work on the MOSL Board and during the Open Water programme. Peter has played a leading role throughout the creation of the market and the establishment of MOSL.

Member engagement

Jim will join me at an event on Wednesday 25 October to meet with the CEOs and senior leaders of our members. The event will be an opportunity to review member feedback from the CEO survey, provide an update on the progress of the Strategic Review and discuss the upcoming Business Plan 2018/19.

We launched our monthly User Forum in September to provide opportunities for trading parties to meet, discuss key market issues and get involved with improvement activities. Live video streaming was available for members to join the discussions online, which received positive feedback, particularly from those members unable to travel.

Foreword

MOSL CEO Quarterly Market Review Q2 2017/181

We are committed to ensuring all companies have access to key market forums and groups regardless of their type, size or geographical location.

We have also been exploring how we can introduce innovation to improve the efficiency of the market, especially through digital; and would like to explore some early ideas and some potential initiatives with our members. We are consulting with members on our plans to create a new Digital Strategy Committee, in place of the former CIO Forum. This new committee will be available to advise the Panel on technology matters and as the market matures, it will support MOSL in the development of its digital strategy and technology implementation.

Next steps

In line with our commitment to provide transparent and insightful information about the market, we are also working to develop our market reporting capabilities. You will see the early fruits of this work in the next Quarterly Review.

In summary it’s been a busy few months, with lots more to come. I look forward to continuing discussions with all of our members and stakeholders on how we can work together to improve and evolve the market.

Chris Scoggins

Chief Executive Officer, Market Operator Services Limited (MOSL)

We have improved the functionality of CMOS at an operational level following the release of version 3.0 on 30 September.

MOSL CEO Quarterly Market Review Q2 2017/18 2

The market landscape

In this quarter several retailers have announced their intent to enter into joint ventures or mergers to consolidate their market shares. Currently the largest five national retailers, which include two new entrant retailers, serve around 75 per cent of all supply points in the market.

One new national retailer has entered the market during the quarter, bringing the current number of retailers to 35. One national retailer with no supply points in the English market has exited during the quarter and one large regional retailer has announced its intention to exit the market. This will again change the market dynamics.

Switching

Switching has continued at a steady rate during the quarter with an additional 25,010 switches bringing the total so far since market opening to 61,311. This represents 2.3 per cent of the 2.7 million supply points in the market.

Review of the second quarter

Transaction Date, Week Commencing (2017)

Num

ber o

f Sup

ply

Poi

nts

Cumulative Switching of ServiceAs at 1st October

Total Switching

Water Services

Sewerage Services

0

10k

20k

30k

40k

50k

60k

70k

03 A

pril

10 A

pril

17 A

pril

24 A

pril

01 M

ay

08 M

ay

15 M

ay

22 M

ay

29 M

ay

05 Ju

ne

12 Ju

ne

19 Ju

ne

26 Ju

ne

03 Ju

ly

10 Ju

ly

17 Ju

ly

24 Ju

ly

31 Ju

ly

07 A

ugus

t

14 A

ugus

t

21 A

ugus

t

28 A

ugus

t

04 S

eptem

ber

11 S

eptem

ber

18 S

eptem

ber

25 S

eptem

ber

Cumulative Switching of Service As at 1 October 2017

MOSL CEO Quarterly Market Review Q2 2017/183

As in Quarter 1, the number of switches has continued to fluctuate around 1,000 to 2,000 a week.

Transaction Date, Week Commencing (2017)

Num

ber o

f Sup

ply

Poi

nts

Sw

itche

d

0

1k

2k

3k

4k

6k

5k

Total

03 A

pril

10 A

pril

17 A

pril

24 A

pril

01 M

ay

08 M

ay

15 M

ay

22 M

ay

29 M

ay

05 Ju

ne

12 Ju

ne

19 Ju

ne

26 Ju

ne

03 Ju

ly

10 Ju

ly

17 Ju

ly

24 Ju

ly

31 Ju

ly

07 A

ugus

t

14 A

ugus

t

21 A

ugus

t

28 A

ugus

t

04 S

eptem

ber

11 S

eptem

ber

18 S

eptem

ber

25 S

eptem

ber

Weekly Switching Rate As at 1 October 2017

MOSL CEO Quarterly Market Review Q2 2017/18 4

There is a continued customer preference to have one retailer providing both their water and sewerage retail services.

Switching Behaviours As at 1 October 2017

Services switched with no associated service

4%Water and sewerage both switched to a new retailer from two different retailers

14%

Water retailer acquired sewerage service

17%

Water and sewerage both switched to a new retailer from a single retailer

58%Sewerage retailer

acquired water service

5%

Water and/or sewerage switched as individual services

2%

MOSL CEO Quarterly Market Review Q2 2017/185

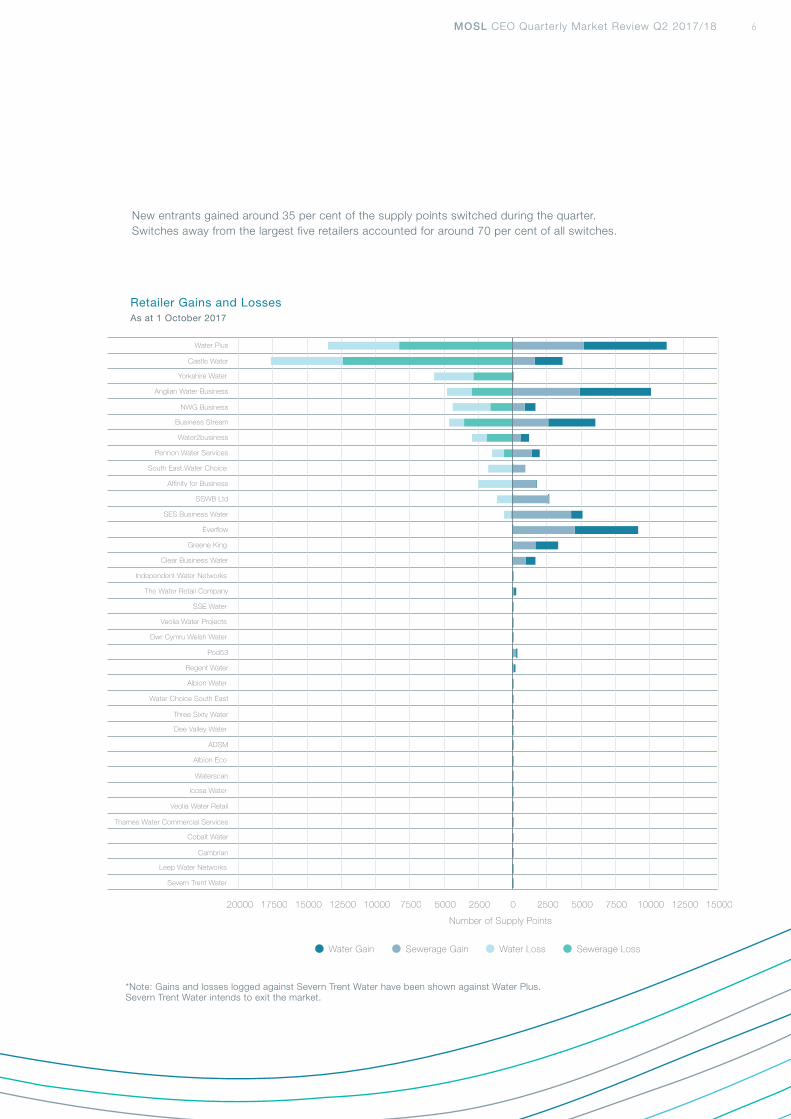

New entrants gained around 35 per cent of the supply points switched during the quarter. Switches away from the largest five retailers accounted for around 70 per cent of all switches.

Number of Supply Points

As at 01 October

Water Gain Sewerage Gain Water Loss Sewerage Loss

20000 10000 0 1000017500 15000 12500 7500 5000 2500 2500 5000 7500 12500 15000

Icosa Water

Severn Trent Water

Albion Eco

Dee Valley Water

Leep Water Networks

Albion Water

Dwr Cymru Welsh Water

Veolia Water Projects

SSE Water

Independent Water Networks

Greene King

South East Water Choice

Yorkshire Water

Cambrian

Cobalt Water

Thames Water Commercial Services

Veolia Water Retail

Waterscan

ADSM

Three Sixty Water

Water Choice South East

Regent Water

Pod53

The Water Retail Company

Clear Business Water

Everflow

SES Business Water

SSWB Ltd

Affinity for Business

Pennon Water Services

Water2business

Business Stream

NWG Business

Anglian Water Business

Castle Water

Water Plus

Retailer Gains and Losses As at 1 October 2017

*Note: Gains and losses logged against Severn Trent Water have been shown against Water Plus. Severn Trent Water intends to exit the market.

MOSL CEO Quarterly Market Review Q2 2017/18 6

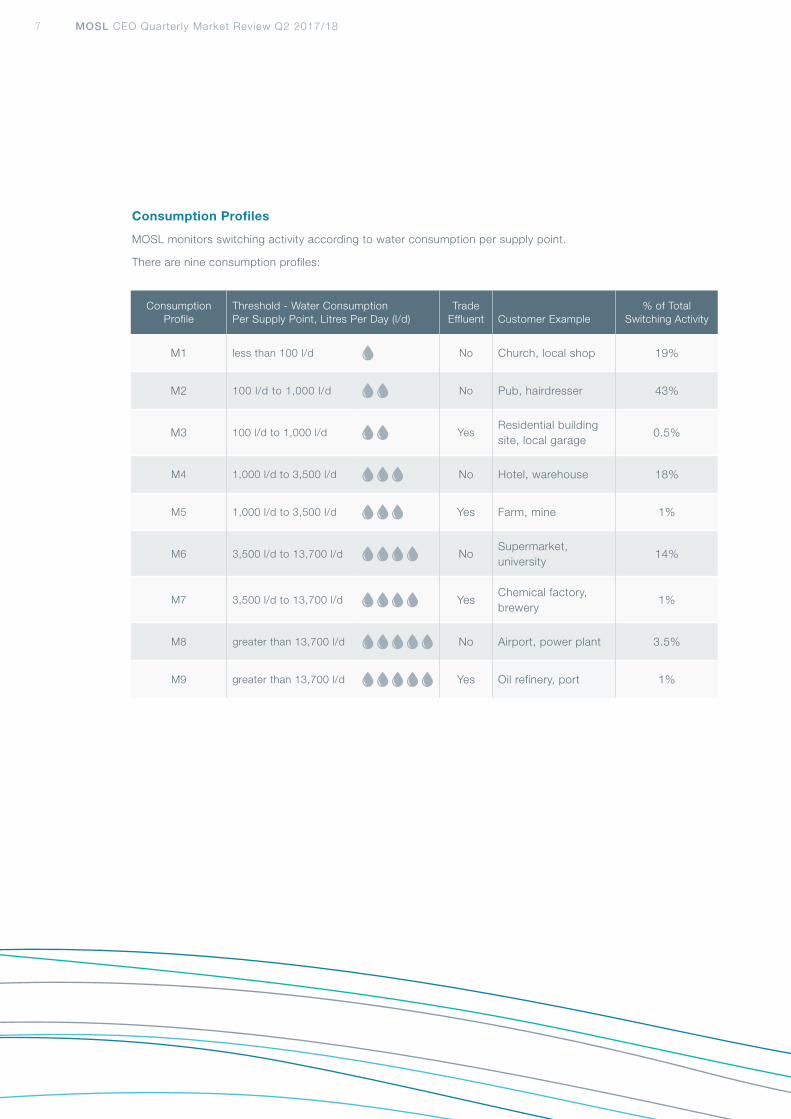

Consumption Profiles

MOSL monitors switching activity according to water consumption per supply point.

There are nine consumption profiles:

Consumption Profile

Threshold - Water Consumption Per Supply Point, Litres Per Day (l/d)

Trade Effluent Customer Example

% of Total Switching Activity

M1 less than 100 l/d No Church, local shop 19%

M2 100 l/d to 1,000 l/d No Pub, hairdresser 43%

M3 100 l/d to 1,000 l/d YesResidential building site, local garage

0.5%

M4 1,000 l/d to 3,500 l/d No Hotel, warehouse 18%

M5 1,000 l/d to 3,500 l/d Yes Farm, mine 1%

M6 3,500 l/d to 13,700 l/d NoSupermarket, university

14%

M7 3,500 l/d to 13,700 l/d YesChemical factory, brewery

1%

M8 greater than 13,700 l/d No Airport, power plant 3.5%

M9 greater than 13,700 l/d Yes Oil refinery, port 1%

MOSL CEO Quarterly Market Review Q2 2017/187

Switching has continued in all customer segments. There has been sustained growth in the level of switching of supply points with associated trade effluent.

0.4%

0.8%0.9%

1.2%

1.1%

1.9%

2.2%

3.4%

3.9%

3.7%

6.8%

6.4%

1.4%

2.0%

2.2%

3.5%

3.1%

3.0%

5.6%

5.3%

3.4%

3.8%

3.6%

4.8%

6.2%

5.8%

4.2%

3.8%

4.1%

4.2%

3.3%

4.1%

3.9%

3.6%

6.8%

6.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1.0%

3.0%

5.0%

7.0%

9.0%

12.0%

14.0%

11.0%

13.0%

15.0%

Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2

M1 M2 M3 M4 M5 M6 M7 M8 M9

Sewerage %Water %

Per

cent

age

of S

uppl

y P

oint

s S

witc

hed

with

in S

egm

ent

Consumption Profile

Proportion of Supply Points Switched within Segment Total Supply Points as at 1 October 2017: 2,669,733

MOSL CEO Quarterly Market Review Q2 2017/18 8

Settlement and data quality

Settlement is most significantly affected by missing or incomplete data (user exceptions) and the accuracy of meter reads.

We have seen the completeness of data improve, with a significant reduction in the number of supply points with user exceptions over the quarter.

Supply points which are not currently settling are missing data owned by the wholesalers. The majority of these supply points are either missing data on the type of service being provided, the associated wholesale tariff or meter details.

Inaccurate retailer meter reads have caused the largest variances in overall settlement. Nine unplanned settlement runs have been requested by trading parties during the quarter to correct inaccurate consumption information.

.

Apr May Jun Jul Aug Sep Oct

180M

190M

200M

210M

220M

230M

240M

P1 - Provisional monthly settlement report using forecast consumption information

R1 - First monthly settlement report including actual meter readings

GB

P

Aggregate Value of Settlement

Note: May and August R1 aggregate values include corrective adjustments

MOSL CEO Quarterly Market Review Q2 2017/189

Market change

The Panel has considered 15 change proposals in the first six months of the market, with four raised during the last quarter. These covered a broad range of topics from the composition of a committee through to negotiating alternative eligible credit support.

Of these change proposals, 11 have been recommended for approval by the Panel, two have been recommended for rejection and two still remain in the process.

Since market opening, seven code changes have been implemented and, as at 1 October, a further four are awaiting decision from Ofwat.

In addition, 15 changes approved by Ofwat prior to market opening, were implemented within CMOS as part of release 3.0.

To enable continued improvements to the market codes, the Panel has created five committees and three working groups since market opening. This includes the recently established Trade Effluent Issues Committee which will offer expertise to the Panel on matters relating to trade effluent.

MOSL CEO Quarterly Market Review Q2 2017/18 10

Business Plan for 2018/19

On 25 October, we will be hosting an event for the CEOs of our wholesaler and retailer members where we will present the principles of our draft Business Plan for the year 2018/19.

The Business Plan is focused on stabilising the market, providing a high quality service, capitalising on innovation, effective engagement and ensuring good governance.

The MOSL Board will put the final version of the Business Plan to members at a general meeting on 15 December.

Digital initiatives

We have been engaging with members on how we can use digital tools to the benefit of the overall market. This engagement included the Digital Innovation Workshop which we hosted on 29 August. Key areas of opportunities raised included:

Additional reporting

Automation of processes

Data quality improvement

Alternate transactional submission process to augment the current portal (low volume interface).

We will be implementing early pilots this year and plan to develop innovative solutions next year. These digital initiatives will reduce costs, improve transparency and reduce overall friction in the market.

To support these initiatives, we are consulting with members on establishing a Digital Strategy Committee which will be chaired by the market and sponsored by MOSL. This committee will look at and inform our digital strategy for the development of tools for trading parties.

Market performance

One key area of focus for the next quarter will be how we measure market performance.

The Market Performance Committee will conclude its review into the Market Performance Standards and Operational Performance Standards and the associated charging mechanisms. This is likely to result in material changes to the overall market performance framework.

How we report on our own performance is important to the market. We will be starting to publish information on our own compliance against around 1,150 market operator obligations under the market codes.

We will expand our focus for market reporting. The months to date have been focused on assessing whether the market is working. Moving forwards, we will be monitoring how the market is behaving and identifying areas of improvement for the market. You can expect to see much more of our market performance team over the rest of this year and moving forward.

Looking forward

MOSL CEO Quarterly Market Review Q2 2017/1811

Market change

Looking forward, there is a continuous pipeline of change for the Panel and its Committees to consider. The focus for the coming months includes:

Data protection and the General Data Protection Regulation (GDPR)

Performance standards for the market

Market entry process.

As requested by the Panel, we will be considering self-supply, SPID versioning and the current suspension of developer services (Part A of the Operational Terms).

Code governance itself will be an area of focus over the next quarter. In December the Panel will be conducting a review of its processes and operating practices. We are also reviewing the provisions for urgent change proposals to enable market critical changes to be considered and addressed in a timely manner.

Market audit

The market auditor will be publishing its half-yearly report in November which we expect to highlight opportunities for all parties in the market to improve.

The market auditor has gathered information using a market wide questionnaire and site visits. Initial feedback from the questionnaire highlights that key areas of challenge for the market include data quality, the interactions between wholesalers and retailers, and clarity in industry processes.

The market auditor will continue its engagement with the market and MOSL during the next quarter.

One key area of focus for the next quarter will be how we measure market performance.

MOSL CEO Quarterly Market Review Q2 2017/18 12

16 High Holborn, Holborn,London, WC1V 6BX

Tel: 020 8616 7444

Email: [email protected]

www.mosl.co.uk

© MOSL 2017

All information in this document including text, data and images, is protected by copyright. Information may not be copied, reproduced or republished without: accrediting MOSL as the data source; referencing the MOSL publication date; and including a link to the original data source on the MOSL website. For more information please see the CEO Quarterly Review Data Publication Guidance via the MOSL website.