cffizens utilities company form 10-k annual … glossy/1990/citizens 1990 10-k.pdf · form 10-k...

TRANSCRIPT

I

,

•

CffiZENS UTILITIES COMPANY

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECuRITIEs EXCHANGE ACf OF 1934

FOR THE YEAR ENDED DECEMBER 31. 1990

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31. 1990 Commission ftle number 0-1291

CITIZENS UTILITIES COMPANY (Exact name of registrant as specified in its charter)

Delaware 06-0619596 (State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

High Ridge Park P.O. Box 3801

Stamford. Connecticut (Address of principal executive offices)

06905 (Zip Code)

Registrant's telephone number, including area code ______ --~,(=.20~34)~3::;:::2~9~-88=00~--------

Securities registered pursuant to Section 12(b) of the Act:

NONE

Securities registered pursuant to Section 12(g) of the Act:

Common Stock Series A, par value $.25 per share Common Stock Series B. par value $.25 per share

(Title of class)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding twelve months (or for such shorter period that the registrant was required to ftle such reports), and (2) has been subject to such filing requirements for the past ninety days.

Yes_x_ No_

State the aggregate market value of the voting stock held by nonaffiliates of the registrant as of February 28, 1991: $1,402,134,652.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of February 28, 1991.

Common Stock Series A Common Stock Series B

38,417,884 12,030,394

DOCUMENTS INCORPORATED BY REFERENCE

The Proxy Statement for the registrant's 1991 Annual Meeting of Stockholders is incorporated by reference into Part III of this Report.

-1-

PART I

Item 1. Description of Business (a) General Development of Business

The "Company" includes Citizens Utilities Company (the "parent company") and its subsidiaries (all subsidiaries are wholly-owned) except where the context or statement indicates otherwise. The Company was incorporated in Delaware in 1935 to acquire the assets and business of a predecessor public utility corporation. Since then the Company has grown as a result of investment in owned utility operations and numerous acquisitions of additional utility operations. It continues to consider business expansion by significant acquisitions or joint ventures in traditional public utility and related fields including telecommunications services.

On December 4, 1990, Louisiana General Services, Inc., (LGS) was merged with and into the Company. LGS is principally engaged in residential, commercial and industrial gas operations in Louisiana. LOS's 1990 operating revenues were $144.6 million and total assets were $186.7 million. The Company issued 4,182,387 Series B shares to effect the merger.

The Company directly, or through subsidiaries or partnerships, provides telecommunications (including cellular and paging), electric, gas and water /wastewater services in areas of thirteen states: Arizona, California, Colorado, Hawaii, Idaho, Illinois, Indiana, Louisiana, Nevada, Ohio, Pennsylvania, Utah and Vermont. Other than the LGS merger, discussed elsewhere herein, there have not been any material changes in the business of the Company during the past fiscal year. The Company emphasizes business expansion in service areas with growth potential, diversification by operating in multiple states and public utility services, including telecommunication services and having strong financial resources and consistent operating performance to enable it to make the investments and conduct the operations necessary to serve these growing areas and to make acquisitions consistent with this business expansion plan.

(b) Financial Information about Industry Segments Note 10 of the Notes to Consolidated Financial Statements included herein sets forth financial

information about industry segments of the Company for the last three fiscal years.

(c) Narrative Description of Business The Company is a diversified operating public utility providing telecommunications, electric, gas

and water /wastewater services to more than 750,000 customers in thirteen states.

Telecommunications The Company provides telephone services in Arizona, California and Pennsylvania to 123,953

telephone access lines served as of December 31, 1990. Subsidiaries of the Company provide radio paging services in Arizona, California and Utah to 36,431 pagers in service. A subsidiary of the Company, through its subsidiaries, is a limited partner in two metropolitan mobile cellular systems operating in California and Nevada and in seven rural mobile cellular systems holding operating rights in Arizona, California, Nevada and Pennsylvania. A portion of the Company's telecommunication services and rates are subject to the jurisdiction of Federal, state and local regulatory agencies. Also, the Company is a party to agreements with interconnecting telecommunications companies that govern the sharing of revenues for services jointly provided. Such agre~ments have provisions authorizing adjustments of estimated payments made under the revenue sharing provisions. Orders proposing changes by the Public Utility Commission of the State of California (the "CPUC") in response to changes in available technology and the marketplace generally call for, among other things, the investigations of: revised regulatory frameworks for intra-lATA telecommunications; alternative regulatory framework for local exchange carriers; less regulation of radio telephone utilities; and other similar proceedings relating to the telecommunications business in California. H some or all of the proposed policy changes are implemented as initially proposed, the Company's California telephone business could be adversely affected due to reduced revenues received under joint service agreements and tariff changes. However, the increased competition expected by the CPUC to result if it adopts

-2-

fmal decisions consistent with the initial orders would present new business opportunities to the Company as well as increased competition from other service providers.

Electric Operating divisions of the Company provide electric services to 90,684 residential, commercial and

industrial customers in Arizona, Hawaii, Idaho and Vermont as of December 31, 1990. The provision of services and rates charged is subject to the jurisdiction of Federal, state and local agencies. In response to regulatory initiatives, the Company's electric divisions are all proceeding with demand-side management programs and integrated resource planning techniques to identify ways customers may conserve energy usage, to assist in controlling peak demand for electrical service and to mitigate price increases to customers. The Company purchases the majority of needed electric supplies, the supply of which is believed to be adequate to meet current demands and to provide for additional sales to new customers. As a whole, the Company's electric segment does not experience material seasonal fluctuations.

Gas Operating divisions of the Company provide gas transmission and distribution services to

residential, commercial and industrial customers in Arizona, Colorado and now Louisiana. The acquisition of LGS (discussed elsewhere herein) significantly increased the Company's geographic and service diversification. Total number of gas customers served as of December 31, 1990 was 251,813 (including 234,711 LGS customers). The Company purchases all needed gas supplies, the supply of which is believed to be adequate to meet current demands and to provide for additional sales to new customers. The gas industry is subject to seasonal demand, with the peak demand occurring during the heating season of November 1 through March 31.

~ater/wastewater The Company provides water and/ or wastewater services to 238,494 customer connections in

Arizona, California, Idaho, Illinois, Indiana, Ohio and Pennsylvania as of December 31, 1990. The provision of these services and rates charged are subject to regulation by a wide variety of Federal, state and local agencies. A significant portion of the Company's water /wastewater construction expenditures necessary to serve new customers is generally made under agreements with land developers who generally advance construction costs to the Company, a portion of which costs are later refunded as new customers are added in their developments. ~ ater /wastewater public utility property of the Company from time to time has been subjected

to condemnation proceedings initiated by municipalities or utility districts seeking to acquire and take over the operation of such property. At January 1, 1990, one small operation in California, was subject to such proceedings. The condemnation is being contested by the Company before the California Superior Court.

Pursuant to the Federal ~ater Pollution Control Act Amendments of 1972 to the Clean ~ater Act, National Pollutant Discharge Elimination System (NPDES) permits are required for wastewater treatment facilities which discharge to surface waters. Permit conditions for two of the Company's facilities in Illinois and one of the Company's facilities in Ohio are presently being contested by the Company. ~ith respect to both of the Illinois facilities, the Illinois State Appellate Court had reversed Lower Court decisions that were adverse to the Company, and both matters were sent back to the Illinois Pollution Control Board. ~ith respect to one of those matters, that Board has issued another Order the Company considers unlawful and the United States Environmental Protection Agency has also issued a Compliance Order applicable to this facility; the Company has appealed the Order to the Illinois State Appellate Court. The other matter is still under consideration by the Illinois Pollution Control Board. ~ith respect to the Ohio facility, the Ohio EPA has proposed an NPDES permit which contains requirements that the Company believes are unlawful. The Company is presently contesting those permit requirements before the Ohio Environmental Board of Review. Compliance with the contested permit conditions for the two Illinois facilities would result in capital expenditures estimated at $7 5 million, and compliance with the contested permit conditions for the Ohio facility would result in capital expenditures estimated at $2 million. These expenditures, if made, would not have any material effect on the Company; additionally, these expenditures would become

-3-

part of the investment for rate-making purposes on which the Company would be entitled to earn a fair rate of return. The Company's water operations are subject to the Federal Safe Drinking Water Act and National Primary Drinking Water Regulations enacted thereunder by the United States Environmental Protection Agency. These regulations became effective June 24, 1977 and have been subsequently amended. The Company's water operations are in substantial compliance with the National Primary Drinking Water Regulations.

General The Company's public utility operations are conducted primarily in small communities and in

suburban and rural areas. No material part of the Company's business is dependent upon a single customer or upon a small group of customers, the loss of one or more of which would have a material adverse effect. .As a result of its diversification, the Company is not dependent upon any single geographic area for its revenues, nor is the Company dependent upon any one type of utility service. Because of this diversity, no single regulatory body regulates a utility service of the Company accounting for more than 21% of its 1990 revenues.

Usual competitive considerations and conditions are not applicable to the public utility business. The Company is subject to regulation by certain city and state Public Utility Commissions and the Federal Energy Regulatory Commission with respect to rates, issuance of securities and other matters. The Company is not subject to the Public Utility Holding Company Act.

Order backlog is not a significant consideration in the Company's business, and the Company has no contracts or subcontracts which may be subject to renegotiation of profits or termination at the election of the Federal government. The Company holds franchises and certificates of convenience and necessity from numerous governmental bodies, some perpetual and others of varying durations. The Company has no special working capital practices. The Company's research and development activities are not material. There are no patents, trademarks, licenses or concessions held by the Company that are material.

The Company employed 2,231 full time and 63 part time employees at December 31, 1990.

(d) The Company does not have any foreign operations or material export sales.

-4-

Item 2. Description of Property The administrative offices of the Company are located at High Ridge Park, Stamford, Connecticut,

06905, and are leased. The Company owns property including: telephone outside plant, central office, microwave radio and fiber-optic facilities; electric generation, transmission and distribution facilities; gas central office, transmission and distribution facilities; water production, treatment, storage, transmission and distribution facilities; wastewater treatment, transmission, collection and discharge facilities; and paging radio transmission and receiving facilities, all as necessary to provide services at locations listed below.

~ Service(s) Provided

Arizona Electric, Gas, Telephone Water, Wastewater, Paging

California Telephone, Water, Paging

Colorado Gas

Hawaii Electric

Idaho Electric, Water

Dlinois Water, Wastewater

Indiana Water

Louisiana Gas

Ohio Water, Wastewater

Pennsylvania Telephone, Water

Utah Paging

Vermont Electric

V arlo us public utility properties and the securities of certain subsidiaries are subject to the lien or the provisions of the Company's primary mortgage indenture. Certain public utility properties are also subject to the lien of other mortgage indentures.

Item 3. LeKal Proceedings None

Item 4. Submission of Matters to Vote of Security Holders The Registrant held a special meeting of stockholders on November 30, 1990 where the

stockholders approved an Amendment to the Restated Certificate of Incorporation of the Company (i) providing for an increase in the number of authorized shares of capital stock of the Company to a total of 280,000,000 shares, consisting of 100,000,000 shares of Common Stock Series A of the par value of Twenty-Five Cents ($.25) each, 130,000,000 shares of Common Stock Series B of the par value of Twenty-Five Cents ($.25) each (together representing an aggregate increase of 143,000,000 shares of the Company's Common Stock) and 50,000,000 shares of the par value of One Cent ($.01) each, of a new class of Preferred Stock, and (ii) authorizing the Board of Directors to issue the Preferred Stock in one or more series without further approval by the stockholders of the Company and permitting the Board of Directors of the Company to establish the attributes of any series of Preferred Stock prior to the issuance of any such series.

-5-

Executive Officers

Information as to Executive Officers of the Company as of March 15, 1991, follows:

Leonard Tow Daryl A. Ferguson Hampton D. Graham, Jr. James P. Avery David E. Chardavoyne J. Michael Love Robert L. O'Brien Donald K. Roberton James W. Swenson

62 52 46 34 42 39 48 49 58

Current Position and Office

Chairman of the Board and Chief Executive Officer President and Chief Operating Officer Vice President, Treasurer and Chief Financial Officer Assistant Vice President, {Acting Vice President) Electric Operations Vice President, Water and Wastewater Vice President, Corporate Planning Vice President, Revenue Requirements Vice President, Telecommunications Vice President, Gas

There is no family relationship between any of the officers of the Registrant. The term of office of each of the foregoing officers of the Registrant will continue until the next annual meeting of the Board of Directors and until a successor has been elected and qualified.

LEONARD TOW has been associated with the Registrant since April1989 as a Director. In June 1990, he was elected Chairman of the Board and Chief Executive Officer. He has also been a Director, Chief Executive Officer and Chief Financial Officer of Century Communications Corporation since its incorporation in 1973, and Chairman of its Board of Directors since October 1989.

DARYL A. FERGUSON has been associated with the Registrant since July 1989. He was Vice President, Administration from July 1989 through March 1990 and Senior Vice President, Operations and Engineering from March 1990 through June 1990. He has been President and Chief Operating Officer since June 1990. During the period April 1987 through July 1989, he was President and Chief Executive Officer of Microtecture Corporation. From 1985 through 1987 he taught at the University of Virginia Business School. From 1982 through 1985 he was President and Chief Operating Officer of Technicom.

HAMPTON D. GRAHAM, JR. has been associated with the Registrant since July 1979. He was Controller from June 1981 through June 1983 and Treasurer and Financial Administrative Officer from June 1983 through June 1989. He has been Vice President, Treasurer, and Chief Financial Officer since June 1989.

JAMES P. A VERY has been associated with the Registrant since August 1981. He was Project Manager, Electric through June 1988 and Assistant Vice President, Electric Operations from June 1988 through December 1990. He has been Acting Vice President, Electric Operations since December 1990.

DAVID E. CHARDAVOYNE has been associated with the Registrant since April 1978. He was Assistant Vice President, Water and Wastewater from June 1984 through June 1986 and Vice President, Water and Wastewater since June 1986.

-6-

J. MICHAEL LOVE has been associated with the Registrant since May 1990 and from November 1984 to January 1988. From December 1984 through June 1986, he was Executive Assistant to the President. From June 1986 through January 1988 he was Assistant Vice President, Regulatory Affairs and Community Relations. He left the Registrant in January 1988 to become President and General Counsel of Southern New Hampshire Water Company. He rejoined the Registrant in May 1990 and was Assistant Vice President, Corporate Planning from June 1990 through March 1991. He has been Vice President, Corporate Planning since March 1991.

ROBERT L. O'BRIEN has been associated with the Registrant since March 1975. He was Assistant Treasurer, Revenue Requirements from June 1978 through May 1979, Assistant Vice President and Assistant Treasurer, Revenue Requirements from June 1979 through May 1981 and has been Vice President, Revenue Requirements since June 1981.

DONALD K. ROBER TON has been associated with the Registrant since January 1991 and has been Vice President, Telecommunications since that date. Prior to joining the Registrant, he was Vice President, Western Operations at Henkels & McCoy from December 1989 through December 1990. From January 1984 through November 1989 he was a Vice President with Centel Communications Systems.

JAMES W. SWENSON has been associated with the Registrant since December 1990 as Vice President, Gas. He also serves as the Chief Executive Officer of the Registrant's Gas Division and Louisiana Gas Service Company. He was with Louisiana General Services, Inc. (LGS) from 1967 until LGS merged with the Registrant in December 1990. He served as Chairman of the Board of LGS from November 1985 and President and Chief Executive Officer from November 1982. He presently serves as Director of Impro Products, Inc., ltron, Inc. and Galaxy Cablevision.

-7-

PART II

Item 5. Market for the Registrant's Common Stock and Related Stockholder Matters

PRICE RANGE OF COMMON STOCK

The Company's Common Stock is traded on the over-the-counter markets as a National Market Issue under NASDAQ symbols CITUA for Series A and CITUB for Series B shares. The following table indicates the high and low prices per share as taken from the NASDAQ /NMS Monthly Statistical Report during the periods indicated. Prices are adjusted for stock dividends through 1990 to the nearest 1/8th. (See Note 7 of Notes to Consolidated Financial Statements.)

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter High Low High Low High Low High Low

1990 Series A 40-1/8 32-5/8 36-3/8 30-3/8 34-1/4 21-1/4 25-3/4 20

Series B 37-1/4 30-7/8 34-3/4 29-5/8 31-1/2 20-1/2 24-3/4 20-1/2

1989 Series A 40-1/4 35-3/4 44-3/4 37-1/4 44 38-3/4 43-5/8 39-5/8

Series B 34-3/4 26-3/4 37-3/4 30-1/2 39-5/8 33-3/4 40-1/8 35-3/8

The December 31, 1990 prices were: Series A 24 high, 23-1/4 low; Series B 24-1/4 high, 23-1/4low.

As of February 28, 1991, the approximate number of record security holders of the Company's Common Stock Series A and Series B was 23,265. This information was obtained from the Company's transfer agent.

DIVIDENDS

Quarterly stock dividends declared and issued on both Series A and B Common Stock were 1.33% for the first, second and third quarters of 1990 and 2.4% for the fourth quarter .of 1990. An annual dividend rate of $1.76 was considered by the Board in establishing the Series A and B stock dividends during 1990. Quarterly cash dividends declared and paid on Series B Common Stock were $.385 per share, totalling $1.54 during 1989. Semi-annual stock dividends of equivalent fair value, to the Series B cash dividend, declared on Series A Common Stock were 2.0% and 1.8% for the first and second half of 1989. (See Note 7 of Notes to Consolidated Financial Statements.)

-8-

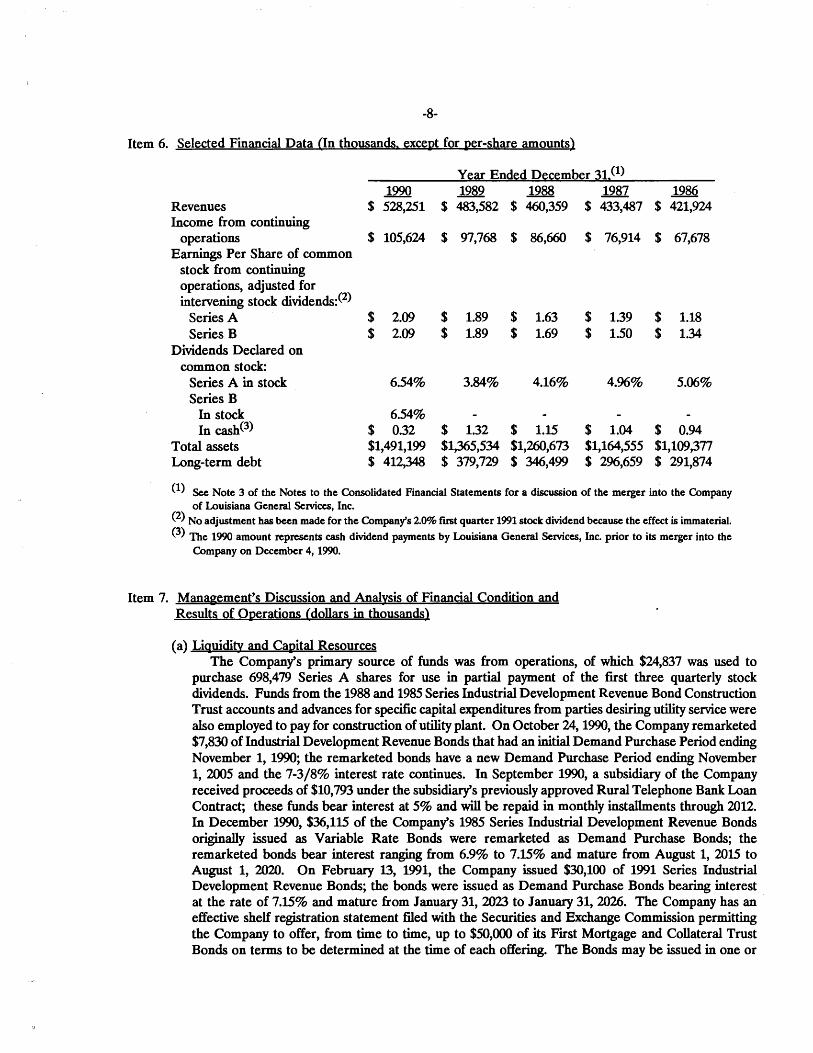

Item 6. Selected Financial Data (In thousands. except for per-share amounts)

Year Ended December 31.(1)

1990 1989 1988 1987 1986 Revenues $ 528,251 $ 483,582 $ 460,359 $ 433,487 $ 421,924 Income from continuing

operations $ 105,624 $ 97,768 $ 86,660 $ 76,914 $ 67,678 Earnings Per Share of common

stock from continuing operations, adjusted for intervening stock dividends:<2>

Series A $ 2.09 $ 1.89 $ 1.63 $ 1.39 $ 1.18 Series B $ 2.09 $ 1.89 $ 1.69 $ 1.50 $ 1.34

Dividends Declared on common stock:

Series A in stock 6.54% 3.84% 4.16% 4.96% 5.06% Series B

In stock 6.54% In cash<3) $ 0.32 $ 1.32 $ 1.15 $ 1.04 $ 0.94

Total assets $1,491,199 $1,365,534 $1,260,673 $1,164,555 $1,109,377 Long-term debt $ 412,348 $ 379,729 $ 346,499 $ 296,659 $ 291,874

(l) Sec Note 3 of the Notes to the Consolidated Financial Statements for a discussion of the merger into the Company of Louisiana General Services, Inc.

(2) No adjustment has been made for the Company's 2.0% first quarter 1991 stock dividend because the effect is immaterial.

(3) The 1990 amount represents cash dividend payments by Louisiana General Services, Inc. prior to its merger into the Company on December 4, 1990.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations (dollars in thousands)

(a) Liquidity and Capital Resources The Company's primary source of funds was from operations, of which $24,837 was used to

purchase 698,479 Series A shares for use in partial payment of the first three quarterly stock dividends. Funds from the 1988 and 1985 Series Industrial Development Revenue Bond Construction Trust accounts and advances for specific capital expenditures from parties desiring utility service were also employed to pay for construction of utility plant. On October 24, 1990, the Company remarketed $7,830 of Industrial Development Revenue Bonds that had an initial Demand Purchase Period ending November 1, 1990; the remarketed bonds have a new Demand Purchase Period ending November 1, 2005 and the 7-3/8% interest rate continues. In September 1990, a subsidiary of the Company received proceeds of $10,793 under the subsidiary's previously approved Rural Telephone Bank Loan Contract; these funds bear interest at 5% and will be repaid in monthly installments through 2012. In December 1990, $36,115 of the Company's 1985 Series Industrial Development Revenue Bonds originally issued as Variable Rate Bonds were remarketed as Demand Purchase Bonds; the remarketed bonds bear interest ranging from 6.9% to 7.15% and mature from August 1, 2015 to August 1, 2020. On February 13, 1991, the Company issued $30,100 of 1991 Series Industrial Development Revenue Bonds; the bonds were issued as Demand Purchase Bonds bearing interest at the rate of 7.15% and mature from January 31, 2023 to January 31, 2026. The Company has an · effective shelf registration statement filed with the Securities and Exchange Commission permitting the Company to offer, from time to time, up to $50,000 of its First Mortgage and Collateral Trust Bonds on terms to be determined at the time of each offering. The Bonds may be issued in one or

-9-

more series with the same or differing maturities. Proceeds of these bonds, when and if sold, will be used primarily to repay debt incurred and to reimburse the Company's treasury for funds spent on construction or acquisition of utility facilities.

From the reclassification of the outstanding common stock in 1956 only stock dividends have been paid on Series A and, through 1989, only cash dividends have been paid on Series B. During 1990, the Company declared the same stock dividend on its outstanding Series A and Series B common stock.

Capital expenditures for the years 1990, 1989 and 1988, respectively, were $147,158, $109,398 and $91,475, and for 1991 are expected to be approximately $U2,041. These expenditures were and in 1991 will be for public utility facilities and related property.

The Company anticipates that the funds necessary for its 1991 capital expenditures will be provided from operations, from 1988 and 1991 Series Industrial Development Revenue Bond proceeds, from commercial paper notes payable, from parties desiring utility service, from senior debt and other financing at appropriate times and, if deemed advantageous, from other borrowings including shortterm borrowings under bank credit lines. The Company has lines of credit With banks under which it may borrow up to $107,000.

On November 30, 1990, the Company's shareholders approved the Amendment to the Restated Certificate of Incorporation, increasing the authorized number of Series A and Series B shares and authorizing a new class of Preferred Stock. Authorized shares may be used for various corporate purposes, including stock dividends, stock splits and acquisitions.

On December 4, 1990, Louisiana General Services, Inc., (WS) was merged into the Company. As a result of the merger, each share of WS common stock was converted into .8 Series B shares. Approximately 4.2 million shares of Citizens' Series B Common Stock were issued in the merger, having an approximate market value as of the close of business on December 3, 1990 of $93,600. LGS is principally engaged in residential, commercial and industrial gas operations in Louisiana.

Regulatory proceedings before the Public Utility Commissions of Arizona, Hawaii and Vermont have reflected increasing public interest nationwide in examining the economic and environmental consequences of utility planning decisions. These commissions are actively promoting demand-side management programs to explore reductions to increasing electrical demand through conservation and load management. Recent orders proposing changes by the Public Utility Commission of the State of California (the "CPUC") in response to changes in available technology and the marketplace generally call for, among other things, the investigations of: revised regulatory frameworks for intralATA telecommunications; alternative regulatory framework for local exchange carriers; less regulation of radio telephone utilities; and other similar proceedings relating to the telecommunications business in California. If some or all of the proposed policy changes are implemented as initially proposed, the Company's California telephone business could be adversely affected due to reduced revenues under joint service agreements with interconnecting carriers and tariff changes. However, the increased competition expected by the CPUC to result if it adopts final decisions consistent with the initial orders would present new business opportunities to the Company as well as increased competition from other service providers. During the year ended December 31, 1990, the Company was authorized net increases in annual revenues for properties in Arizona, Colorado, California, Ohio, Pennsylvania and Vermont totalling $2,346.

The Financial Accounting Standards Board (FASB) has issued Statement of Financial Accounting Standards (SFAS) No. 103, "Accounting for Income Taxes- Deferral of the Effective Date of FASB Statement No. 96" which deferred the effective date of Financial Accounting Standards No. 96, "Accounting for Income Taxes", until fiscal years beginning after December 15, 1991. Adoption of SFAS No. 96 will affect the balance sheet presentation of deferred income taxes. The Company anticipates that there will be no material effect on net income upon the adoption of SFAS No. 96. In December 1990 the FASB issued SFAS No. 106, "Employers' Accounting for Postretirement Benefits Other than Pensions", effective for fiscal years beginning after December 15, 1992. Adoption of SFAS No. 106 will require accrual of the expected cost of providing postretirement benefits to an employee and the employee's beneficiaries and covered dependents, during the years

-10-

that the employee renders the necessary service. LGS' retired employees and a small number of the Company's retired employees have certain health care and life insurance benefits provided by the Company. The Company anticipates that there will be no material effect on the financial statements of the Company upon adoption of SFAS No. 106.

(b) Results of Operations Telecommunications revenues increased 21% in 1990 and 13% in 1989 primarily due to

increased toll revenues, adjustments to estimated toll revenue settlements and customer growth. Electric revenues increased 9% in 1990 and 11% in 1989 primarily due to customer growth and passons to customers of increases in purchased power and fuel oil costs. Pass-ons are required under tariff provisions and do not affect net income. Gas revenues decreased 1% in 1990 and 6% in 1989 primarily due to decreased sales volume to industrial customers in 1990 and decreased sales volume to residential and commercial customers in 1989 due to warmer weather conditions; the decrease in 1989 was partially offset by increased average revenue per MCF of gas sold to residential and industrial customers due to rate increase in 1989. Water/wastewater revenues increased 5% in 1990 and 7% in 1989 primarily due to customer growth and rate increases.

Electric energy and fuel oil purchased costs increased 12% in 1990 and 15% in 1989. Electric energy purchased costs for 1990 totalled $54,096, a 6% increase over the 1989 amount of $50,927, which was a 12% increase over the 1988 cost of $45,387. The increase in cost of electricity purchased was primarily due to higher supplier prices and increased volume purchased to satisfy increased customer growth in both 1990 and 1989. Fuel oil purchased in 1990 of $16,096 increased 38% from the 1989 amount of $11,653, and increased 27% in 1989 primarily due to higher supplier prices. Natural gas purchased decreased 3% in 1990 and 10% in 1989 primarily due to lower volume purchased due to decreased customer demand in 1990 and 1989, and decreased supplier prices charged in 1990. Under tariff provisions, changes in the Company's wholesale costs of electric energy, fuel oil and natural gas purchased are largely passed on to customers.

Operating expenses increased 23% in 1990 and 8% in 1989 primarily due to costs associated with the merged company, increased employee compensation and adjustments of inventory and accounts receivable of paging operation. Maintenance expenses increased 16% in 1990 and 9% in 1989 primarily due to telephone cable rearrangements in 1990 and increased amounts of plant in service in 1990 and 1989. Depreciation expense increased 4% in both 1990 and 1989, primarily due to increased investment in plant in service.

Taxes other than income increased by 12% in 1990 and 5% in 1989 primarily due to increased real estate, personal property and state sales taxes in 1990 and 1989. Income taxes increased 14% in 1989 primarily due to increased taxable income.

Interest expense increased 3% in 1990 and 19% in 1989 primarily due to additional Industrial Development Revenue Bond construction fund requisitions and the issuance of additional commercial paper notes payable to reimburse the treasury for construction expenditures.

Cost increases, including those due to inflation, are offset in due course by increases in revenues obtained under established regulatory procedures.

-11-

Item 8. Financial Statements and Supplementary Data

The following documents are filed as part of this Report:

1. Financial Statements: See Index on page F-1.

2. Supplementary Data: Quarterly Financial Data is included in the Financial Statements (see 1. above).

Item 9. Disagreements with Auditors on Accounting and Financial Disclosure

None PART ill

The Company intends to file with the Commission a definitive proxy statement for the 1991 Annual Meeting of Stockholders pursuant to Regulation 14A not later than 120 days after December 31, 1990. The information called for by this Part ill is incorporated by reference to that proxy statement.

PART IV

Item 14. Exhibits. Financial Statement Schedules and Reports on Form 8-K

Exhibit ~

3.1 3.2 3.2.1 3.2.2 3.2.3 3.2.4 3.2.5 3.2.6 3.3 3.4 3.4.1 3.4.2 4.1

4.2

(a) The following documents are filed as part of this Report:

1. The financial statements indexed on page F-1 of this Report.

2. The financial statement schedules required to be filed by Item 8 will be filed as a Form 8 amendment to this Report on or before April 30, 1991.

3. The Exhibits listed below:

Description

Certificate of Incorporation By-laws Amendment dated February 20, 1986, to the By-laws Amendment dated June 5, 1987, to the By-laws Amendment dated August 8, 1988, to the By-laws Amendment dated May 5, 1989, to the By-laws Amendment dated May 31, 1989, to the By-laws Amendment dated May 1, 1990, to the By-laws Certificate of Amendment of Restated Certificate of Incorporation, dated June 18, 1984 Certificate of Amendment of Restated Certificate of Incorporation, dated July 7, 1986 Certificate of Amendment of Restated Certificate of Incorporation, dated June 11, 1987 Certificate of Amendment of Restated Certificate of Incorporation, dated November 30, 1990 Copy of Indenture of Mortgage and Deed of Trust dated as of March 1, 1947 to The Marine Midland Trust Company of New York and Baldwin Maull, as Trustees (First Interstate Bank of California, Successor Corporate Trustee) Supplemental Indenture, dated April 22, 1947

Exhibit ~

4.3 4.4 4.5 4.6 4.7 4.8 4.9 4.10 4.11 4.U 4.13 4.14 4.15 4.16 4.17 4.18 4.19 4.20 4.21 4.22 4.23 4.24 4.25

4.26

-U-

Description

Second Supplemental Indenture, dated September 1, 1948 Third Supplemental Indenture, dated September 1, 1948 Fourth Supplemental Indenture, dated April1, 1949 Fifth Supplemental Indenture, dated April 30, 1950 Sixth Supplemental Indenture, dated May 1, 1950 Seventh Supplemental Indenture, dated October 1, 1952 Eighth Supplemental Indenture, dated December 1, 1954 Ninth Supplemental Indenture, dated December 1, 1955 Tenth Supplemental Indenture, dated May 1, 1960 Eleventh Supplemental Indenture, dated November 27, 1961 Twelfth Supplemental Indenture, dated September 11, 1962 Thirteenth Supplemental Indenture, dated October 1, 1962 Fourteenth Supplemental Indenture, dated November 1, 1970 Fifteenth Supplemental Indenture, dated November 1, 1974 Sixteenth Supplemental Indenture, dated March 1, 1975 Seventeenth Supplemental Indenture, dated April1, 1978 Instrument in Writing, dated January 14, 1952 appointing a Successor Individual Trustee Instrument in Writing, dated June 11, 1969 appointing a Successor Individual Trustee Instrument in Writing, dated November 1, 1972 appointing a Successor Individual Trustee Instrument in Writing, dated July 6, 1977 appointing a Successor Individual Trustee Instrument in Writing, dated February 14, 1983 appointing a Successor Individual Trustee Eighteenth Supplemental Indenture, dated April 15, 1986 Instrument in Writing, dated June 6, 1986 appointing a Successor Corporate Trustee and a Successor Individual Trustee Instrument in Writing, dated March 26, 1988 appointing a Successor Individual Trustee

The Company agrees to furnish to the Commission upon request copies of the Realty and Chattel Mortgage dated as of March 1, 1965 made by Citizens Utilities Rural Company, Inc. to the United States of America (the Rural Electrification Administration and Rural Telephone Bank) and the Mortgage Note which that mortgage secures; and the several subsequent supplemental Mortgages and Mortgage Notes; copies of the instruments governing the long-term debt of Ohio Utilities Company and Kauai Electric Company; and copies of separate loan agreements and indentures governing various Industrial Development Revenue Bonds.

10.1 Managerial Incentive Deferred Compensation Plan dated August, 1977; as Amended April7, 1978; June 8, 1979; and as of June 6, 1980

10.2 Senior Managerial Incentive Deferred Compensation Plan dated August 5, 1977; as Amended April 7, 1978; June 8, 1979; June 6, 1980; and as of January 16, 1981

10.3 Supplemental Benefits Agreement between Citizens Utilities Company and Ishler Jacobson dated August 5, 1977

10.3.1 Resolution dated May 19, 1989 10.3.2 Employment Agreement between Citizens Utilities Company and Ishler Jacobson, October 1, 1989 10.5 Employment Agreement effective January 1, 1981 10.5.1 Addendum dated as of January 1, 1989 10.6 Deferred Compensation Plans for Directors dated November 26, 1984 and December 10, 1984 10.6.1 Directors' Retirement Plan effective January 1, 1989 10.7 Amendment dated June 15, 1984, to the Managerial Incentive Deferred Compensation Plan

Exhibit ~

10.8 10.9 10.10 10.11 10.12 10.13 10.14 10.15 12.

22. 24. 25.

-13-

Description

Amendment dated June 15, 1984, to the Senior Managerial Incentive Deferred Compensation Plan Management Equity Incentive Plan effective June 22, 1990 LGS 1979 Option Incentive Plan, as amended LGS 1981 Incentive Option Plan, as amended LGS 1981 Stock Option Plan, as amended LGS Supplemental Executive Retirement Plan Letter agreement between LGS and James W. Swenson, dated May 18, 1979 Termination agreement dated March 14, 1986, between LGS and James W. Swenson Computation of ratio of earnings to fixed charges (this item is included herein for the sole purpose of incorporation by reference in the Company's Form S-3 No. 33-31880.) Subsidiaries of the Registrant Auditors' Consent Powers of Attorney

All items other than Exhibit Numbers 3.2.1, 3.2.2, 3.2.3, 3.2.4, 3.2.5, 3.2.6, 3.3, 3.4, 3.4.1, 3.4.2, 4.23, 4.24, 4.25, 4.26, 10.3.1, 103.2, 10.5.1, 10.6, 10.6.1, 10.7, 10.8, 10.9, 10.10, 10.11, 10.12, 10.13, 10.14, 10.15, 12, 22, 24 and 25 are incorporated by reference to Exhibits bearing the same designation in the Registrant's Annual Report on Form 10-K for the year ended December 31, 1980. Exhibit number 4.23 is incorporated by reference to the same exhibit designation in the Registrant's Annual Report on Form 10-K for the year ended December 31, 1983. Exhibit numbers 3.3, 10.6, 10.7 and 10.8 are incorporated by reference to the same exhibit designation in the Registrant's Annual Report on Form 10-K for the year ended December 31, 1984. Exhibit number 4.24 is incorporated by reference to the same exhibit designation in the Registrant's Form 8-K Current Report filed April, 1986. Exhibit number 4.25 is incorporated by reference to the same exhibit designation in the Registrant's Form S-3 No. 33-6455 filed June, 1986. Exhibit numbers 3.2.1 and 3.4 are incorporated by reference to the same exhibit designation in the Registrant's Annual Report on Form 10-K for the year ended December 31, 1986. Exhibit numbers 3.2.2 and 3.4.1 are incorporated by reference to the same exhibit designation in the Registrant's Annual Report on Form 10-K for the year ended December 31, 1987. Exhibit number 10.5.1 is incorporated by reference to the same exhibit designation in the Registrant's Form 8-K Current Report filed March, 1989. Exhibit numbers 3.2.3 and 4.26 are incorporated by reference to the same exhibit designation in the Registrant's Annual Report on Form 10-K for the year ended December 31, 1988. Exhibit numbers 3.2.4, 3.2.5, 103.1 and 10.6.1 are incorporated by reference to the same exhibit designation in the Registrant's Annual Report on Form 10-K for the year ended December 31, 1989. Exhibit number 10.9 is incorporated by reference to Appendix A to the Registrant's Proxy Statement dated May 14, 1990. Exhibit number 10.3.2 is incorporated by reference to the Registrant's Quarterly Report on Form 10-Q for the six months ended June 30, 1990. Exhibit number 3.4.2 is incorporated by reference to Exhibit number 4.2 to the Registrant's Form S-8 No. 33-39455. The Registrant's Annual Reports on Form 10-K and Form 8-K Current Reports bear SEC File Number Reference 0-1291.

(b) A report on Form 8-K was filed as of December 4, 1990, transmitting a press release announcing the merger of Louisiana General Services, Inc., with and into Citizens Utilities Company.

-14-

SIGNATURES

Pursuant to the requirements of Section 13 or 15( d) of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

cmZENS UTILITIES COMPANY (Registrant)

By. ________________________ _

Hampton D. Graham, Jr. Vice President; Treasurer, Chief Financial Officer and Principal

Accounting Officer March 28, 1991

Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of the registrant and in the capacities indicated on the 28th day of March 1991.

Signature

Leonard Tow* (Leonard Tow)

Norman I. Botwinik* (Norman I. Botwinik)

Aaron I. Fleischman* (Aaron I. Fleischman)

Andrew N. Heine* (Andrew N. Heine)

Elwood A. Rickless• (Elwood A. Rickless)

John L. Schroeder• (John L. Schroeder)

Robert D. Siff* (Robert D. Sift)

*By: _______________ _

(Hampton D. Graham, Jr.) Attorney-in-Fact

Chairman of the Board; Chief Executive Officer; Member, Executive Committee and Director

Member, Executive Committee and Director

Member, Executive Committee and Director

Director

Member, Executive Committee and Director

Director

Director

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES

Index to Financial Statements

Independent Auditors' Report Consolidated balance sheets as of December 31, 1990, 1989 and 1988 Consolidated statements of income for the three years ended

December 31, 1990 Consolidated statements of shareholders' equity for the three

years ended December 31, 1990 Consolidated statements of cash flows for the three years

ended December 31, 1990 Notes to consolidated financial statements

F-1

F-2 F-3

F-4

F-5

F-6 F-7- F-16

~Peat Marwick Certified Public Accountants

345 Park Avenue

New York, NY 10154

Independent Auditors' Report

The Board of Directors and Shareholders Citizens Utilities Company:

We have audited the consolidated financial statements of Citizens Utilities Company and subsidiaries as listed in the accompanying index. These consolidated financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with generally accepted auditing standards. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Citizens Utilities Company and subsidiaries at December 31, 1990, 1989 and 1988, and the results of their operations and their cash flows for the years then ended in conformity with generally accepted accounting principles.

New York, New York March 21, 1991

F-2

'-~9w··~l KPMG PEAT HARWICK

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS DECEMBER 31, 1990, 1989 AND 1988

(In thousands)

1990 1989 ASSETS

Current assets: Cash $ 28,118 $ 23,687 Accounts receivable:

Utility service 42,585 38,564 Other 13,973 12,469 Less allowance for doubtful accounts 410 482

562148 502551 Materials and supplies 10,232 9,087 Other current assets 32889 32900

982387 87,225

Property, plant and equipment 1,269,545 1,142,299 Less accumulated depreciation 3492820 3202987

9192725 8212312

Investments 395,629 370,742 Net assets of merged company's discontinued

oil and gas operations 12,583 20,121 Deferred debits and other assets 642875 662134

~114911199 ~113651534

LIABILITIES AND SHAREHOLDERS' EQUITY Current liabilities:

Accounts payable $ 72,581 $ 74,632 Income taxes accrued 27,6CJ3 15,553 Long-term debt due within one year 18,172 13,835 Customers' deposits 16,151 15,426 Interest accrued 7,258 7,649 Other current liabilities 352049 222743

1762904 1492838

Customer advances for construction 125,383 113,839 Contributions in aid of construction 36,581 34,173 Deferred income taxes 114,741 125,153 Deferred credits 19,013 21,484 Long-term debt 412,348 379,729 Shareholders' equity 6062229 5412318

$1A911199 !113651534

1988

$ 24,806

32,921 12,305

498 442728 8,603 22499

80,636

1,047,480 2902414 757,066

334,067

36,964 512940

~112601673

$ 73,023 20,428 4,851

14,417 7,560

152337 1352616

98,200 32,298

125,544 15,809

346,499 5062707

!112601673

The accompanying Notes are an integral part of these Consolidated Financial Statements.

F-3

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF INCOME

FOR THE THREE YEARS ENDED DECEMBER 31, 1990 (In thousands, except for per-share amounts)

1990 1989 1988 Revenues:

Telecommunications $176,427 $145,497 $128,456 Electric 136,242 124,897 112,472 Gas 155,574 156,431 165,561 Water /wastewater 56,991 54,100 50,427 Other 32017 22657 32443

5282251 4832582 4602359 Expenses:

Electric energy and fuel oil purchased 70,239 62,624 54,547 Natural gas purchased 87,411 90,278 100,262 Operating expenses 127,158 103,772 96,232 Maintenance expenses 31,842 27,540 25,360 Depreciation 45,262 43,347 41,545 Taxes other than income 29,183 26,153 24,839 Interest expense 312816 30,959 262087

4222911 3842673 368,872

Income from continuing operations before other income and income taxes 105,340 98,909 91,487

Interest and dividend income 32,218 32,929 26,914 Other income - net 92129 7,129 42515

Income from continuing operations before income taxes 146,687 1.38,967 122,916

Income taxes 412063 412199 362256

Income from continuing operations 1052624 972768 862660

Discontinued operations owned by merged company, net of tax provision:

Operating loss 0 (1,280) (2,327) Provision for discontinuance 0 (112372) 0

Net income $105.624 $85.116 $84.333

Earnings per share of common stock: From continuing operations

Series A $2.09 $1.89 $1.63

Series B $2.09 $1.89 $1.69

Net income Series A $2.09 $1.65 $1.58

Series B $2.09 ~ $1.64

The accompanying Notes are an integral part of these Consolidated Financial Statements.

F-4

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY

FOR THE THREE YEARS ENDED DECEMBER 31, 1990 (In thousands, except for per-share amounts)

Merged Com:Q!ny Unrealized ESOP Gain (Loss) Shares

Common Stock ($.25) On Purchased Series A Series B Additional Marketable With

Authorized 100,000 Authorized 130,000 Paid-in Retained Equity Guaranteed Issued Amount Issued Amount Capital Earning Securities Debt Total

Balance December 31, 1987 36,374 $9,094 11,796 $2,950 $307,930 $168,956 $ 20 ($2,078) $486,872

Net Income 84,333 84,333 Cash dividends:

Common Stock Series B, $1.34 per share (9,668) (9,668) Dividends of merged company (3,899) (3,899)

Stock dividends in shares of Common Stock Series A:

June@ 2.2% 21 5 (749) (23,891) (24,635) December @ 1.92% 19 5 (1,499) (23,943) (25,437)

Conversions of Series A to Series B (87) (22) 87 22 0 Transaction of merged company (33) (9) (404) (69) (557) 180 (859)

Balance December 31, 1988 36,327 $9,082 11,850 $2,963 $305,278 $191,819 ($537) ($1,898) $506,707 Net Income 85,116 85,116 Cash dividends:

Common Stock Series B, $1.54 per share (11,173) (11,173) Dividends of merged company (3,970) (3,970)

Stock dividends in shares of Common Stock Series A:

June@ 2.0% 239 60 7,033 (27,616) (20,523) December @ 1.8% 445 111 18,390 (27,876) (9,375)

Conversions of Series A to Series B (39) (10) 39 10 0 Transactions of merged company (327) (83) (5,756) (180) 660 (105) (5,464)

Balance December 31, 1989 36,972 $9,243 11,562 $2,890 $324,945 $206,120 $123 ($2,003) $541,318 Net Income 105,624 105,624 Cash dividends of merged company (3,942) (3,942) Stock dividends in shares of

Common Stock Series A and Series B: March @ 1.33% 147 37 97 24 5).67 (19,353) (14,025) June@ 1.33% 223 55 99 25 9,785 (19,483) (9,618) September @ 1.33% 267 67 100 25 10,222 (17,496) (7,182) December @ 2.4% 901 225 184 46 21,867 (22,138) 0

Conversions of Series A to Series B (80) (20) 80 20 0 Transactions of merged company (103) (25) (2,615) (313) (919) (2,074) (5,946)

Balance December 31, 1990 38.430 $9,607 12.019 $3.005 $369.471 $229.019 ($796) ~ $606.229

The accompanying Notes are an integral part of these Consolidated Fmancial Statements.

F-5

CITIZENS UTILffiES COMPANY AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE THREE YEARS ENDED DECEMBER 31, 1990 (In thousands)

1990 1989

Net cash provided by operating activities $130,758 $134,927

Cash flows from investing activities: Construction expenditures (134,575) (98,881) Customer advances for construction and

contributions in aid of construction 13,675 17,488 Securities purchases, net (25,590) (35,641) Change in net assets of merged company's

discontinued operations 72537 42191

(1382953) (1122843)

Cash flows from financing activities: Long-term debt borrowings 65,029 41,404 -Long-term debt principal payments (20,509) (7,476) Series A shares purchased for payment

of stock dividends (24,837) (35,886) Other (7205']) (212245)

122626 (232203)

Increase (decrease) in cash 4,431 (1,119) Cash at January 1, 232687 242806

Cash at December 31, s 28a118 S 23a687

The accompanying Notes are an integral part of these Consolidated Financial Statements.

F-6

1988

$138,326

(93,437)

8,763 (15,391)

(102382) (110z447)

53,817 (11,142)

(50,072) (142097)

(21z494)

6,385 182421

$ 24a806

CITIZENS UTILffiES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements

(In thousands, except for per-share amounts)

(1) Summazy of Significant AccountinK Policies: (a) Principles of Consolidation:

The consolidated financial statements include the accounts of Citizens Utilities Company and all subsidiaries after elimination of intercompany balances and transactions. Certain reclassifications of balances previously ~eported have been made to conform to current presentation.

(b) Property, Plant and Equipment: Property, plant and equipment are stated at original cost, including general overhead and an allowance for funds used during construction. Allowance for funds used during construction (AFUDC) represents the borrowing costs and a reasonable return on common equity of funds used to finance construction. AFUDC is capitalized as a component of additions to property, plant and equipment and is credited to income. AFUDC does not represent current cash earnings, however, under established regulatory rate making practices, after the construction project is placed in service, the Company is permitted to include in the rates charged for utility services a fair return on and depreciation of such AFUDC included in plant in service. The amount relating to equity is included in Other income ($6, 794, $5,886 and $4,303 for 1990, 1989 and 1988, respectively) and the amount relating to borrowings is a reduction of Interest expense ($1,698, $1,472 and $882 for 1990, 1989 and 1988, respectively). The weighted average rates used to calculate AFUDC were 14%, 13% and 12% in 1990, 1989 and 1988, respectively. Maintenance and repairs are charged to operating expenses as incurred. The cost, net of salvage, of ·routine property dispositions is charged against accumulated depreciation.

(c) Accumulated Depreciation: Depreciation expense, calculated using the straight-line method, is based upon estimated service lives of various classifications of property, plant and equipment and represented approximately 4% of the gross amounts of the property for 1990, 1989 and 1988.

(d) Deferred Income Taxes and Investment Tax Credits: Deferred income tax charges result from the use for income tax purposes of accelerated depreciation methods and certain other tax deductions in excess of charges to income for financial reporting purposes. The investment tax credits relating to utility properties, as defined by applicable regulatory authorities, have been deferred and are being amortized to income over the life of the related property. The preceding procedures are consistent with accepted rate-making procedures in many states where operations are conducted.

(e) Revenue: The Company recognizes revenues earned based on delivery of service to customers. Certain telephone toll and access service revenues are estimated under cost separation procedures that base revenues on current operating costs and investments in facilities to provide such services. Adjustments to these estimates are made when actual data for the interconnecting carriers becomes available.

(f) Earnings Per Share: Earnings per share is based on the period-end number of outstanding shares. Earnings per share is presented for each Series separately, with historical adjustment for stock dividends for each Series. The calculation is not adjusted for the 2% stock dividend declared on February 22, 1991 because its effect is immaterial. The effect on earnings per share of the exercise of dilutive options is immaterial.

F-7

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements (In thousands, except for per-share amounts)

(2) Property. Plant and Equipment: The components of property, plant and equipment at December 31, 1990, 1989 and 1988 are as follows:

Classification 1990 1989 1988 Transmission and distribution

facilities $882,501 $815,873 $755,774 Production facilities 175,192 146,711 131,145 Pumping, storage and purification

facilities 64,828 62,027 57,836 Intangibles 1,571 1,343 1,308 Other 114,078 89,842 80,066 Construction work in progress 31,375 26,503 21,351

(3) Merger: The Company issued 4,182 Series B shares effective December 4, 1990 in exchange for all the

outstanding shares of Louisiana General Services, Inc. (LGS), a company engaged in residential, commercial and industrial gas operations in the state of Louisiana. Each share of LGS' common stock was converted into .8 Series B shares. The acquisition was accounted for as a pooling of interests and, accordingly, the Company's consolidated financial statements include LGS' balance sheet (as of September 30) and related statements of income, cash flows and shareholders' equity (all for LGS' fiscal year ended September 30) for all periods presented.

Revenues and income from continuing operations included in the Consolidated Statements of Income are as follows:

.122.Q 1989 .12BB Revenues

Company $383,654 $338,655 $306,821 LGS 144.~97 144.927 153.538

Combined $528.251 $4§3.582 $460.359

Income from continuing OJ2erations Company $ 96,789 $ 88,705 $ 77,411 LGS 8.83~ 2.063 9.249

Combined ~1051624 ~ 971768 ~ 861660

( 4) Merged Companv's Discontinued Operations: In 1989, the Board of Directors of LGS (merged company) approved a plan of disposition relating to

the oil and gas exploration and production operation of LGS. Accordingly, the assets and operating results have been classified as discontinued operations in the consolidated financial statements.

Revenues from oil and gas operations and other income relating to the discontinued operations were $6,080, $5,962 and $6,043 for 1990, 1989 and 1988, respectively. The tax benefits of the discontinuance for 1990, 1989 and 1988 were $0, $824 and $1,299, respectively.

F-8

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements

(In thousands, except for per-share amounts)

( 4) Merged Company's Discontinued Operations: (continued) The net assets related to the discontinued oil and gas exploration and production operations, consisting

primarily of oil and gas properties, have been reduced to net realizable value. These net assets have been segregated in the consolidated balance sheets under the caption: "Net assets of merged company's discontinued oil and gas operations". A summary of these net assets follows:

Oil and gas property, net Accounts receivable and other assets Deferred credits and other payables

1990 $12,221

473 (111)

$12.583

September 30. 1989

$18,850 2,762

(1.491) $20.121

1988 $30,668 21,012

(14.716) $36.964

The estimated loss on disposal of the discontinued oil and gas exploration and production operations of $11,372, includes the direct costs of disposal. During fiscal1990, approximately $4,800 of cash proceeds were received from the sale of certain properties. The expected manner of disposition is by sale. The Company is continuing its efforts to obtain prospective buyers for the remaining oil and gas assets.

( 5) Investments Investments include higher grade, shorter-term fixed income securities and marketable equity securities,

held for additions and improvements to the Company's utility facilities, acquisitions and other corporate purposes. Fixed income securities are stated at cost, which approximates market. Marketable equity securities owned by LGS or its subsidiaries are stated at aggregate lower of cost or market except for marketable equity securities held by LGS' insurance subsidiary which are stated at market. Net unrealized gain (loss) on marketable equity securities owned by LGS is included in shareholders' equity.

The aggregate cost of marketable equity securities at September 30, 1990, 1989 and 1988 is $14,159, $17,298 and $14,415, respectively; aggregate market value is $13,389, $17,619 and $13,879, respectively.

Total gross unrealized gains were $1,563 and gross unrealized losses were $2,333 on marketable equity securities of LGS. Net realized gains included in the determination of net income for years 1990, 1989 and 1988, respectively, were $17, $490 and $85. The cost of securities sold was based on the actual cost of the shares of each security held at the time of sale.

F-9

CITIZENS UTILmES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements

(In thousands, except for per-share amounts)

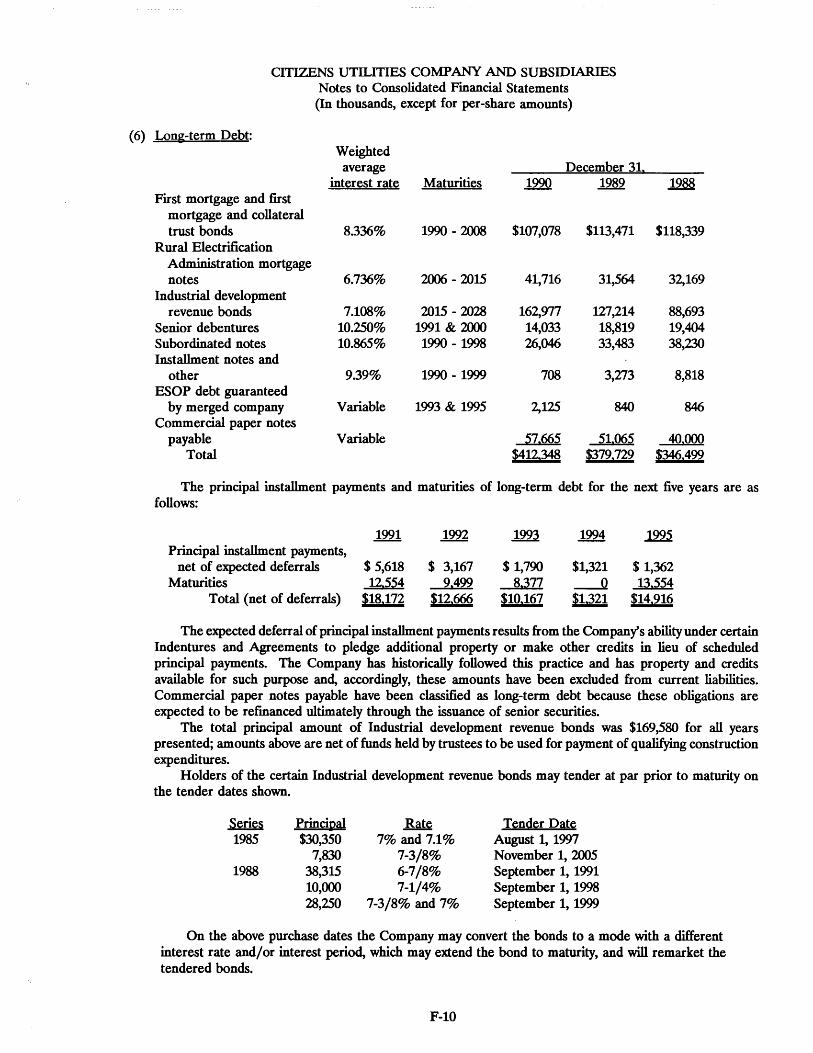

( 6} Long-term Debt: Weighted

average December 31a interest rate Maturities 1990 1989 1988

First mortgage and first mortgage and collateral trust bonds 8.336% 1990- 2008 $107,078 $113,471 $118,339

Rural Electrification Administration mortgage notes 6.736% 2006- 2015 41,716 31,564 32,169

Industrial development revenue bonds 7.108% 2015- 2028 162,977 127,214 88,693

Senior debentures 10.250% 1991 & 2000 14,033 18,819 19,404 Subordinated notes 10.865% 1990- 1998 26,046 33,483 38,230 Installment notes and

other 9.39% 1990- 1999 708 3,273 8,818 ESOP debt guaranteed

by merged company Variable 1993 & 1995 2,125 840 846 Commercial paper notes

payable Variable 'j7.665 51.065 40.000 Total $412.348 $379.729 $346.499

The principal installment payments and maturities of long-term debt for the next five years are as follows:

1991 1992 .!22l 1994 1995 Principal installment payments,

net of expected deferrals $ 5,618 $ 3,167 $ 1,790 $1,321 $ 1,362 Maturities 12.554 9.499 8.377 __ o 13.554

Total (net of deferrals) ~181172 ~12~666 ~101167 $1321 ~14a916

The expected deferral of principal installment payments results from the Company's ability under certain Indentures and Agreements to pledge additional property or make other credits in lieu of scheduled principal payments. The Company has historically followed this practice and has property and credits available for such purpose and, accordingly, these amounts have been excluded from current liabilities. Commercial paper notes payable have been classified as long-term debt because these obligations are expected to be refmanced ultimately through the issuance of senior securities.

The total principal amount of Industrial development revenue bonds was $169,580 for all years presented; amounts above are net of funds held by trustees to be used for payment of qualifying construction expenditures.

Holders of the certain Industrial development revenue bonds may tender at par prior to maturity on the tender dates shown.

~ Princi12al Rate Tender Date 1985 $30,350 7% and 7.1% August 1, 1997

7,830 7-3/8% November 1, 2005 1988 38,315 6-7/8% September 1, 1991

10,000 7-1/4% September 1, 1998 28,250 7-3/8% and 7% September 1, 1999

On the above purchase dates the Company may convert the bonds to a mode with a different interest rate and/ or interest period, which may extend the bond to maturity, and will remarket the tendered bonds.

F-10

CffiZENS UTILITIES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements

(In thousands, except for per-share amounts)

(6) Long-term Debt: (continued) The Company has available lines of credit with Banks totalling $107,000. $100,000 of the lines of credit

expire January 19, 1992 and $7,000, assumed in the merger with LOS, expire April 30, 1991. In the years 1990, 1989 and 1988, interest payments were $33,712, $31,958 and $25,889, respectively.

(7) Capital Stock: The common stock of the Company is in two Series, Series A and Series B. To the extent that cash

dividends are paid on the Series B, stock dividends with an equivalent fair value must be paid during the same calendar year on the Series A, unless cash dividends are declared on Series A shares at the same time and in an equal amount as on Series B shares. To the extent that stock dividends are declared on Series B, the same stock dividend must be declared on Series A. From the reclassification of the outstanding common stock in 1956 only stock dividends have been paid on Series A and, through 1989, only cash dividends have been paid on Series B. Under the provisions of the Tax Reform Act of 1969 {Section 421(b) (2)(A) }, there is no taxable income to Series A shareholders upon receipt of their stock dividends on Series A shares through December 31, 1990. During 1990, the Company declared the same stock dividend on its outstanding Series A and Series B Common Stock. Payment of the same stock dividend on both Series of shares is intended to preserve the nontaxable status of stock dividends when received on Series A shares, and now Series B shares, in 1991 and beyond.

Series A is convertible into Series B at all times except between the dates of declaration and record of dividends. Series B is not convertible into Series A. The shares of both Series have identical voting rights and participate ratably in liquidation.

The Company purchased Series A shares in the market from time to time for use in partial payment of the Series A stock dividend. No Series B shares were purchased for payment of the Series B stock dividend in any period. The table below shows the sources of Series A shares used for payment of the Series A stock dividend during the periods shown:

Purchased ....Q!§L Shares Issued Total

1990 $30,825 833 1,538 2,371 1989 $29,898 685 684 1,369 1988 $50,072 1,431 40 1,471

The Company has 50,000 authorized shares of preferred stock ($.01 par), none of which have been issued. The preferred stock may be issued by the Board of Directors (without actions by shareholders) in one or more series, having such attributes as may be designated by the Board of Directors at the time of issuance of the preferred shares.

The indenture securing long-term debt of the Company provides, among other things, that the Company will not declare or pay a cash dividend on the common stock if the aggregate amount declared or paid after December 31, 1946 shall exceed $613 plus the aggregate consolidated net earnings of the Company and its subsidiaries subsequent to December 31, 1946. At December 31, 1990, the entire retained earnings were free of such restrictions.

F-11

CmZENS UTILITIES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements (In thousands, except for per-share amounts)

(8) Stock Option Plan: On June 22, 1990, shareholders approved the Citizens Utilities Company Management Equity Incentive

Plan (the "Plan") effective June 22, 1990. Under the Plan, awards of the Company's Series A or Series B Common Stock may be granted to eligible officers and other management employees of the Company and its subsidiaries in the form of incentive stock options, non-qualified stock options, stock appreciation rights, or other stock based awards. The Plan will be administered by a Committee of the Board of Directors. The exercise price shall be equal to or greater than the fair market value of the underlying Common Stock on the date of grant. The maximum number of shares of Common Stock which may be issued pursuant to awards at any time will be 5% of the Company's Common Stock outstanding from time to time; provided that no more than 2,200 will be issued pursuant to incentive stock options under the Plan. No awards will be granted more than ten years after the effective date of the Plan.

In connection with the December 4, 1990 LGS merger, the Company assumed pre-existing LGS employee stock option plans and converted all options then outstanding under the LGS plans into options to acquire the Company's Series B shares.

· A summary of options granted under the plan follows:

Balance at January 1, 1990 Options granted Conversion of LGS plans

Balance at December 31, 1990 Options exercisable at end of year

(9) Income Taxes:

Shares Subject to Option

478 .m 122 231

Average Option Price per Share

$21-3/8 12-3/4 18-5/8 12-3/4

The provision for Federal and state income taxes includes amounts payable currently and amounts deferred for payment in future periods because of the timing of when income or expense is recognized for financial statement purposes and for income tax purposes. The Company and its subsidiaries are included in a consolidated Federal income tax return using a calendar year reporting period.

The provisions for Federal and state income taxes shown below reflect a combination of amounts for Citizens and its subsidiaries for calendar years and LGS and its subsidiaries for fiscal years ended September 30.

122Q 1989 1988 Current:

Federal $38,152 $34,664 $31,733 State 9.115 8.034 51943

47.'lfJ7 42.698 371676 Deferred:

Federal (3,167) 1,130 1,505 Investment Tax Credits (2,358) (2,489) (2,909) State (679) (14Q) ~)

(61204) (1.499) (1a420) Total $41.063 $41.199 ~361256

F-12

(9)

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements

(In thousands, except for per-share amounts)

Income Taxes: (continued) The following is a reconciliation of the provision for income taxes at Federal statutory rates to the

reported provision for income taxes: 1990 1989 1988

Consolidated tax provision at Federal statutory rate $49,874 34.0% $47,249 34.0% $41,972 34.0%

Allowance for funds used during construction {2,887) {2.0%) {2,502) {1.8%) {1,763) {1.4%)

Overhead expenses capitalized (765) (0.5%) {1,013) (0.7%) (974) (0.8%) Depreciation based on tax

service lives 712 0.5% 1,446 1.0% 1,648 1.3% Amortization of investment

tax credits {2,358) (1.6%) {2,489) (1.8%) {2,765) {2.2%) States income tax provision, net

of Federal income tax benefit 6,%9 4.7% 6,390 4.6% 4,812 3.9% Nontaxable interest and dividend

income {8,528) (5.8%) {7,893) (5.7%) {6,815) (5.5%) Nontaxable management fee (588) (0.4%) Dividend payments to Employee

Stock Ownership Plan {428) {0.3%) {369) (0.2%) {311) (0.3%) All other - net ____(2JB) ~) 380 ~ 452 0.4%

Total ~1a063 28.0% ~1a199 29.6% $36256 29.4%

For 1990,1989 and 1988, accumulated deferred income taxes amounted to $87,757,$95,616 and $93,978, respectively, and the unamortized deferred investment tax credits amounted to $26,984,$29,537 and $31,566, respectively. Income taxes paid during the year, which included balances due for prior years and estimated payments for the current year were $35,730, $46,196 and $28,045 for 1990, 1989 and 1988, respectively. At December 31, 1990, the cumulative amount of timing differences for which deferred income taxes have not been provided is $101,611.

The Company has not adopted the provisions of Financial Accounting Standards No. 96, "Accounting for Income Taxes", implementation of which is not required until 1992.

{10) Segment Information:

Year Ended December 311

.1220 1989 1988 Telecommunications:

Revenues $176,427 $145,497 $128,456 Assets 322,451 278,546 272,948 Depreciation 20,584 20,202 19,866 Capital expenditures 59,993 39,044 30,432 Operating income before

income taxes 78,807 66,073 57,163 Electric:

Revenues $136,242 $124,897 $112,472 Assets 252,439 211,930 177,178 Depreciation 8,281 7,741 6,799 Capital expenditures 46,954 33,583 24,886 Operating income before

income taxes 27,732 26,213 24,470

F-13

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements (In thousands, except for per-share amounts)

(10) Sement Information: (continued)

Year Ended December 31 .

.QM: Revenues $155,574 $156,431 $165,561 Assets 170,385 177,439 180,042 Depreciation 10,051 9,667 9,515 Capital expenditures 9,640 9,127 14,565 Operating income before

income taxes 14,870 19,017 19,422 W ilter Lwil§t~wat~r:

Revenues $ 56,991 $ 54,100 $ 50,427 Assets 290,715 275,102 238,974 Depreciation 6,284 5,680 5,320 Capital expenditures 28,338 26,524 20,771 Operating income before

income taxes 15,220 16,194 15,800

(11) Quarterly Fimmcial Datil (uniludited): The following presents information about operations of both the Company for the year ended

December 31, and LGS operations for the fiscal year ended September 30.

1990 In~Qm~ from ~ntinuing onerations

Earning§ P~r Share Revenues Amount Series A Series B

First Quarter $131.188 $22.420 $0.44 $0.44 Company 87,995 19,447 LGS 43,193 2,973

Second Quarter $139.080 S28.506 $0.56 $0.56 Company 88,455 23,265 LGS 50,625 5,241

Third Quarter S125.456 S27.862 $0.55 $0.55 Company 97,506 27,201 LGS 27,950 661

Fourth Quarter $132,527 $26,836 $0.53 $0.53

F-14

CffiZENS UTILITIES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements

(In thousands, except for per-share amounts)

(11) Quarterly Financial Data (unaudited): (continued)

(12)

Revenues First Quarter $117.362

Company 78,202 LOS 39,160

Second Quarter $132.170 Company 80,555 LOS 51,615

Third Quarter $121.059 Company 90,865 LOS 30,194

Fourth Quarter $112,991

Supplemental ~ash Flow InformiltiQn:

1989 Income from continuin" operations

Amount $19.297 17,093 2,204

$25.972 20,638 5,334

$26.064 24,392

1,672

$26,435

Earnings Per Share Series A Series B

$0.36 $0.38

$0.50 $0.50

$0.50 $0.51

$0.51 $0.51

Schedule of net cash provided by operating activities for the three years ended December 31,

1990 1989 1988 Net income $105,624 $85,116 $84,333 Adjustments to reconcile net income to

net cash provided by operating activities: Depreciation and amortization 45,262 43,347 41,545 Deferred income taxes and

amortization of investment tax credits (6,204) (2,196) (1,412) Allowance for equity funds used

during construction (6,794) (5,886) (4,303) Change in accounts receivable (5,596) (5,824) (8,872) Change in accounts payable (4,178) 1,413 14,522 Change in accrued taxes and

accrued interest 13,715 (4,315) 11,062 Loss from discontinued operations 1,280 2,327 Provision for discontinuance 11,372 Other (11.071) 10.620 (876)

~1301758 ~1341927 $138326

(13) Pension and Retirement Plans: The Company assumed LOS' employee benefit plans, as a result of the merger. The Company and

its subsidiaries have noncontributory pension plans covering all employees who have met certain service and age requirements. The benefits are based on years of service and final average pay or pay rate. Contributions are made in amounts sufficient to fund the plans' current service cost and to provide for benefits expected to be earned in the future. Plan assets are invested in a diversified portfolio of equity and fixed-income securities.

F-15

CITIZENS UTILITIES COMPANY AND SUBSIDIARIES Notes to Consolidated Financial Statements

(In thousands, except for per-share amounts)

(13) Pension and Retirement Plans: (continued) Pension costs for 1990, 1989 and 1988, based on measurements as of December 31, and June 30, for

the Company and LGS, respectively, amounted to:

1990 1989 1988 Com12an~ LGS ~om12an~ LGS ~OmJ2an~ LGS

Service cost $3,030 $ 649 $2,816 $ 502 $2,568 $ 526 Interest cost on projected

benefit obligation 1,659 1,640 1,415 1,522 1,194 1,422 Amortization of unfunded

prior service cost 349 (3,446) 349 2,006 606 (389) (Return) loss on plan assets ~) ...l.1QO -121.4) (3.486) ~) (916)

Net pension cost $3.695 $603 $3.606 $ 544 $3.834 $ 643

Service cost and interest cost on the projected benefit obligation were computed using an 8% discount rate for 1990, 1989 and 1988 (9% for LGS in 1988). The expected long-term rate of return was 9% (8% for LGS) for 1990 and 1989 and 8% for 1988.

The fair value of Company plan assets as of December 31, 1990, 1989 and 1988 was $36,105, $31,297 and $24,227, respectively. The actuarial present value of the accumulated benefit obligation for 1990, 1989 and 1988, respectively, was $20,494, $18,045 and $14,277 (Vested $19,496, $17,028 and $12,578). Total projected benefit obligation in 1990, 1989 and 1988, respectively, amounted to $39,081, $34,595 and $28,466, assuming an annual salary increase rate of 6% for all three years.

The fair value of LGS plan assets as of September 30, 1990, 1989 and 1988 was $19,592, $22,458 and $19,090, respectively. The actuarial present value of the accumulated benefit obligation for 199o, 1989 and 1988, respectively, was $23,549, $19,960 and $16,541 (Vested $23,468, $19,847 and $15,989). Total projected benefit obligation in 1990, 1989 and 1988, respectively, amounted to $24,963, $21,225 and $17,086, assuming an annual salary increase rate of 6% for all three years.

(14) Commitments: The Company has budgeted expenditures for facilities in 1991 of approximately $122,041 and

certain commitments have been entered into in connection therewith.

F-16