cg dec-17 dec-16 sep-17 change auto sales 476,015...

TRANSCRIPT

ICICI Securities Ltd. | Retail Equity Research

February 20, 2018

Earnings Wrap Q3FY18

Encouraging earnings recovery under way…

Sensex companies (ex-banks) posted a robust Q3FY18

performance partly due to low base due to demonetisation in base

quarter i.e. Q3FY17 and adapting of trading channel to the new

GST regime. Quarterly results are encouraging thereby depicting

upbeat domestic economic sentiment (also depicted by

November-December 2017 IIP numbers) thereby reinforcing our

view of a smart earnings recovery being under way. On topline

front, oil & gas, metals space continued to benefit from the surge in

commodity prices while capital goods, auto space saw strong

growth on bottomline front. In Q3FY18, net sales were at | 476,015

crore, up healthy 11.9% YoY (best in last four quarters). EBITDA for

the quarter was at | 103,944 crore with corresponding EBITDA

margins at 21.8% (highest in last eight quarters), up 100 bps YoY.

Companies continue to see pressure on gross margins (down 180

bps) on account of a rise in commodity prices, which was more

than compensated by operating leverage benefits (up 280 bps) on

account of better capacity utilisation levels (sweating of assets).

PAT in Q3FY18 was at | 50,548 crore, up a healthy 9.7% YoY

At a broader level, for the entire listed universe, double digit sales

& PAT growth on a YoY basis at 11.1% & 13.3%, respectively, is

encouraging. Critical analysis of the same depicts growth led by

large cap companies’ vis-à-vis small cap & midcap domain. It also

aids our belief to be cautious while investing in small & midcap

companies and sticking to more quality names that exhibit capital

efficiency and have sustainable growth prospects

On the sectoral front, in Q3FY18, the auto space continued the

positive momentum with overall 16% volume growth on a YoY

basis. The key surprise was upbeat M&HCV sales (up 37% YoY). In

the banking space, asset quality concerns surfaced with 20% YoY

growth in GNPA in the PSU banking space. Going forward, with

government’s focus on “ease of living”, thrust on augmenting farm

income and pick-up of investment cycle under way, we expect

Sensex earnings to record impressive 21.6% CAGR in FY18-20E

#Data based on 23 companies (excluding banks, NBFCs)

Exhibit 1: Sensex aggregate # (| crore)

Dec-17 Dec-16 Sep-17

YoY (%)

change

QoQ (%)

change

Sales 476,015 425,381 457,236 11.9 4.1

Total Expenses 372,070 336,641 358,835 10.5 3.7

Raw material 178,130 151,517 177,102 17.6 0.6

Employee 69,676 64,802 68,776 7.5 1.3

Other expenses 124,264 120,322 112,957 3.3 10.0

Expenses (% of sales)

Total Expenses 78.2 79.1 78.5 -98 bps -32 bps

Raw material 37.4 35.6 38.7 180 bps -131 bps

Employee 14.6 15.2 15.0 -60 bps -40 bps

Other expenses 26.1 28.3 24.7 -218 bps 140 bps

Operating Profit 103,944 88,739 98,402 17.1 5.6

OPM% 21.8 20.9 21.5 98 bps 32 bps

Other Income 11,131 12,508 12,590 -11.0 -11.6

Interest 12,732 10,860 13,038 17.2 -2.3

Depreciation 30,806 25,687 28,472 19.9 8.2

PAT 50,548 46,098 49,941 9.7 1.2

PAT margin % 10.6 10.8 10.9 -22 bps -30 bps

Source: Capitaline, ICICIdirect.com Research

BSE Sensex (ex-banks, NBFC)

| crore Dec-17 Dec-16 Sep-17

Sales 476,015 425,381 457,236

EBITDA 103,944 88,739 98,402

Net Profit 50,548 46,098 49,941

Indices performance (% return) in Q3FY18

9.4

6.8

8.0

8.9

9.7

9.7

10.1

10.6

11.4

13.4

15.5

19.3

26.3

29.2

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0

FMCG

Banks

Power

Sensex

Oil & Gas

Healthcare

Metals

Auto

CG

IT

Mid Cap

Small Cap

Real Estate

CD

(%)

CG: Capital Goods

CD: Consumer durables

Small Cap: BSE Small Cap

BSE Sensex – Heat Map (% Return) in Q3FY18

RILAirtel SBI Maruti M&M

22.0% 19.8%

HUL Infosys ONGC ICICI Bank

13.5%

17.9%

Sun Pharma

16.5% 15.8% 14.2%

36.0% 22.1%

13.5%

Tata Steel Wipro TCS Axis Bank L&T

NTPC

12.2%

Adani Ports Tata Motors Bajaj Auto

3.8%

10.2%

Cipla

10.9% 10.8%12.1%

7.7% 7.6% 7.2% 5.7%

-12.7%

2.4%3.7%

HDFC Bank Dr. Reddy Asian Paints ITC Kotak Bank

0.3% -1.8% -2.9% -5.0%

Hero Moto HDFC Coal India

0.8%

LupinPower Grid

1.9%3.7%

Aggregate Summary

Sales Net profit Sales Net profit

Nifty 7.7 8.8 12.6 15.6

BSE midcap 2.9 3.9 4.0 -1.0

BSE smallcap 6.0 172 12.6 2.2

All Co's (2246 cos) 5.6 11.1 11.1 13.3

QoQ growth (%) YoY growth (%)

Positive surprises & Buys

NRB Bearing

TCI Express

NCC

Sun TV

KEC International

Heidelberg Cement

Indian Hotel

Contact for feedback and comments

ICICI Securities Ltd. | Retail Equity Research

Page 2

Exhibit 2: Sensex EPS at | 322/share in Q3FY18

332

346 347

339

314

364

345

328

339

360

330

352

322

280

290

300

310

320

330

340

350

360

370

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

EPS

Source: Bloomberg, Reuters, ICICIdirect.com Research

@ for calculation of EPS we have considered standalone profit for Bajaj Auto, Cipla, HDFC, HDFC Bank, Hero

MotoCorp, Hindustan Unilever, ITC, L&T, M & M, Maruti Suzuki, NTPC, ONGC and Reliance Industries while for

the rest of the companies, consolidated profit has been considered

Exhibit 3: Sensex aggregate quarterly revenue, operating profit & net profit trend

420,121401,047

417,199 425,381

468,742

423,660457,236

476,015

88,127 86,140 88,437 88,739 88,083 86,564 98,402 103,944

49,421

43,619

47,359

46,098

49,590

46,545

49,94150,548

40,000

42,000

44,000

46,000

48,000

50,000

52,000

0

100000

200000

300000

400000

500000

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

| crore

| crore

Net Sales (LHS) Operating Profits (LHS) PAT (RHS)

Source: Capitaline, ICICIdirect.com Research

#Data is based on 23 companies (excluding banks, NBFCs)

Exhibit 4: Sensex aggregate quarterly revenue & profitability growth trend (%)

10.0

-11.3

8.4

1.23.9

-4.4

3.9

2.0

-9.6

7.9

-3.3

18.8

7.9

-2.7

6.9

-6.1

-15

-10

-5

0

5

10

15

20

25

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2016 2017 2018

(%

)

Sales growth QoQ (%) Net profit growth QoQ (%)

Source: Capitaline, ICICIdirect.com Research

#Data is based on 23 companies (excluding banks, NBFCs)

On a YoY basis, in Q3FY18, ex banks, the Sensex topline

increased convincingly at double digits at 11.9% YoY (highest

in recent past). EBITDA growth, for the quarter, came in at

17.1% YoY thereby exceeding topline growth primarily tracking

100 bps expansion in EBITDA margins to 21.8%. The margin

improvement was factoring in lower overhead costs mainly

employee (60 bps) and other expenses (220 bps), which was

partly compensated by an increase in raw material costs (180

bps) on account of an increase in commodity prices. PAT in

Q3FY18 was up a healthy 9.7% YoY

On a QoQ basis, carrying the positive current underway from

the last quarter the performance of Sensex companies was

largely flat. Sensex companies witnessed topline growth of

4.1% QoQ with EBITDA growth at 5.6% YoY with 30 bps

expansion in EBITDA margins (21.8% in Q3FY18 vs. 21.5% in

Q2FY18). PAT in Q3FY18 was up marginally 1.2% YoY. PAT

growth was a laggard following a decline in other income and

corresponding increase in depreciation on a sequential basis

EPS for the quarter i.e. Q3FY18 was at | 322/share, down

4.9% YoY (| 339/share in Q3FY17). Resurgent asset quality

concerns in the banking space (especially public sector banks)

weighted on overall index earnings with weighted average

Sensex EPS witnessing de-growth on a YoY basis despite ex-

banking space witnessing close to double digit growth (up

9.4% YoY)

On a YoY basis, in Q4FY16, ex banks and commodity space,

the Sensex topline increased 12.4% YoY to | 307583 crore in

Q4FY16 while EBITDA came in at | 63694 crore with

corresponding EBITDA margins at 20.7%. Margins came in

higher by 230 bps YoY on account of 78 bps savings in raw

material costs and 90 bps savings in other operating expenses

as companies realised operating leverage benefits. PAT for the

quarter was at | 35161 crore, up 27.9% YoY

During Q4FY16, the Sensex topline increased 9.5% QoQ while

the bottomline expanded 17.4% QoQ primarily on the back of a

136 bps increase in EBITDA margins largely on account of

lower raw material and employee costs

ICICI Securities Ltd. | Retail Equity Research

Page 3

Exhibit 5: Sensex aggregate quarterly EBITDA margin

21.0

21.5

21.2 20.9

18.8

20.4

21.5

21.8

17

18

19

20

21

22

23

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

%

EBITDA Margin

Source: Capitaline, ICICIdirect.com Research

#Data is based on 23 companies (excluding banks, NBFCs)

Industry wise revenue & profit movement

Exhibit 6: Industry wise aggregate revenue (Sensex companies) ( | crore)

Dec-17 Dec-16 Sep-17 YoY change (%) QoQ change (%)

Auto 118,692 103,324 119,584 14.9 -0.7

Capital goods 28,747 26,110 26,447 10.1 8.7

FMCG 18,362 16,953 18,623 8.3 -1.4

IT 62,367 60,696 61,531 2.8 1.4

Oil & Gas 122,806 99,422 110,446 23.5 11.2

Metals 55,090 48,152 50,612 14.4 8.8

Pharma 14,401 15,296 14,293 -5.8 0.8

Power 28,281 26,026 26,952 8.7 4.9

Others 27,268 29,401 28,748 -7.3 -5.1

Aggregate 476,015 425,381 457,236 11.9 4.1

Source: Capitaline, ICICIdirect.com Research

Topline growth for the quarter was again led by the commodity

space, which includes oil & gas (up 23.5% YoY) and metals (up

14.4% YoY) and consumer driven auto space (up 14.9% YoY). IT

and pharma continued their underperformance with topline growth

of 2.8% & -5.8% respectively. Bottomline growth, on the other

hand, witnessed a divergence. Growth was led by capital goods

(up 48% YoY, L&T) and metals (up 33% YoY) followed by auto (up

29% YoY, Tata Motors) and oil & gas (up 22% YoY). IT & pharma

reported de-growth at the PAT level

During the quarter, in the capital goods domain, all EPC companies

reported robust execution trends and record order inflows. In the

IT space, Tier-I companies reported a dollar revenue growth of

1.2% QoQ and 9% YoY. Constant currency (CC) revenues grew an

average of 1.5% QoQ in a seasonally weak quarter. In the pharma

space, the challenging environment in the US generic space

continues to impact pharma universe growth

Exhibit 7: Industry wise aggregate net profit (Sensex companies) (| crore)

Dec-17 Dec-16 Sep-17 YoY change (%) QoQ change (%)

Auto 6,048 4,688 8,522 29.0 -29.0

Capital goods 1,618 1,090 2,020 48.4 -19.9

FMCG 4,003 3,685 3,916 8.6 2.2

IT 12,172 12,637 12,376 -3.7 -1.6

Oil & Gas 14,460 11,876 13,228 21.8 9.3

Metals 4,141 3,115 1,387 32.9 198.6

Pharma 1,583 2,599 1,742 -39.1 -9.1

Power 4,402 4,399 4,580 0.1 -3.9

Others 2,122 2,008 2,172 5.7 -2.3

Aggregate 50,548 46,098 49,941 9.7 1.2

Source: Capitaline, ICICIdirect.com Research,

#Data is based on 23 companies (excluding banks, NBFCs)

In Q3FY18, EBITDA margins continued their uptrend largely

factoring in operating leverage benefits following better

capacity utilisation levels (sweating of assets). Margins for the

quarter were at 21.8%, up 30 bps QoQ & 100 bps YoY. Raw

material as a percentage of sales came in at 37.4% vs. 35.6%

in Q3FY17, up 180 bps while employee and other operating

expense was at 40.7% vs. 43.5% in Q3FY17

Interest costs increased ~32% YoY for Sensex companies in

Q2FY14. Interest cost as a percentage of EBITDA has also seen

an uptrend to 8.2% in Q2FY14 from 7.2% in Q2FY13 mainly due

to a sharp rise in interest outgo

Industry wise revenue contribution (%)

Dec-17 Dec-16 Sep-17

Auto 24.9 24.3 26.2

Capital goods 6.0 6.1 5.8

FMCG 3.9 4.0 4.1

IT 13.1 14.3 13.5

Oil & Gas 25.8 23.4 24.2

Metals 11.6 11.3 11.1

Pharma 3.0 3.6 3.1

Power 5.9 6.1 5.9

Others 5.7 6.9 6.3

Source: Capitaline, ICICIdirect.com Research

Industry wise net profit contribution (%)

Dec-17 Dec-16 Sep-17

Auto 12.0 10.2 17.1

Capital goods 3.2 2.4 4.0

FMCG 7.9 8.0 7.8

IT 24.1 27.4 24.8

Oil & Gas 28.6 25.8 26.5

Metals 8.2 6.8 2.8

Pharma 3.1 5.6 3.5

Power 8.7 9.5 9.2

Others 4.2 4.4 4.3

Source: Capitaline, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 4

Key notable surprises and stock calls

This section of Earnings Wrap includes the key surprises witnessed in the

earnings of coverage companies and our take post analysis of results.

The above companies posted a strong set of earnings in Q3FY18, which

we believe are more fundamental and sustainable in nature, going

forward. We have a positive view on these companies.

Exhibit 8: Key surprises and stock calls (Q3FY18)

CMP

(|)

NRB Bearing Positive

NRB Bearings reported stellar Q3FY18 numbers. Revenues, EBITDA and PAT grew 25.4%, 103.4% and

178.5%, respectively, led by growth in its key segments such as auto and exports. Going forward, its after-

market segment is also likely to pick up, given the GST related issues are almost over. Accordingly, we expect

all three segments – auto, after-markets and exports to grow at a healthy rate of 12.7%, 13.2%, 13.8%,

respectively. Accordingly, we estimate topline and bottomline growth of 13% and 22.8% CAGR over FY17-20E.

Given its inexpensive valuations in the peer set; we recommend BUY, valuing NRB at 21x FY20E earnings to

arrive at a target price of | 215 per share

160 215 Buy 34

TCI Express Positive

In addition to the seasonally strong quarter (Q3), TCI Express' margins pleasantly surprised us in the current

quarter. Revenues continued their growth momentum with growth of 22% YoY (12% QoQ) to | 229 crore.

However with a margin expansion of 270 bps YoY (up 82 bps QoQ) to 10.5%, absolute EBITDA grew 64% YoY

(up 22% QoQ) to | 24.1 crore. Higher utilisations on the back of improved tonnage coupled with improved

macro environment (GST and eway bill) provides growth visibility. Industry leading growth rates and return

ratios affirms our BUY rating on the company, assigning P/E of 30x on FY20E EPS of | 22

500 660 Buy 32

NCC Positive

NCC reported strong Q3FY18 results. NCC’s topline de-grew 2.8% YoY to | 1850.7 crore due to adjustment of

indirect taxes and GST. EBITDA margins expanded significantly by 460 bps YoY to 13.8% due to bonus claims

worth | 73 crore for UP expressway. Hence, PAT grew robustly by 72.2% YoY to | 100.4 crore. NCC has

witnessed healthy order inflows to the tune of | 21614 crore in 9MFY18, significantly exceeding its initial

FY18E guidance of | 12000 crore. Hence we expect a robust pick-up in execution leading to revenue growth

of 26.2% CAGR to | 12413 crore in FY18-20E. We have a BUY rating with TP of | 160

125 160 Buy 28

Sun TV Positive

Sun TV reported heathy ad and broadcasting revenues growth of 18.9% (core ad growth of 21.6% YoY) in

Q3FY18, reflecting the monetisation of improved share in Malayalam and Telugu markets. The subscription

growth was healthy owing to continued improvement in realisations. Going forward, we factor in 12.5% CAGR

in ad revenues in FY17-20E to | 1850 crore, driven by lower base and strong traction in non-Tamil markets.

Moreover likely digitisation in Tamil Nadu would provide much needed fillip to subscription growth. We expect

17.5% CAGR in subscription revenues over FY17-20E. We maintain our BUY recommendation with a target

price of | 1150, valuing it at 27x FY20E P/E

913 1150 Buy 26

KEC

International

Positive

KEC reported strong Q3FY18 results. The beat was in terms of order inflow & backlog, execution trend,

EBITDA margins and finance costs. The company is one of key beneficiaries of revival of domestic capex cycle

and is witnessing healthy order inflows. The order inflows of 9MFY18 were at |11,300 crore, up 31% YoY,

coupled with L1 status of |4,000 crore. Robust growth in order backlog backed by strong order wins, massive

scale up in new business, consistency in margin expansion and improvement in balance sheet matrices will

drive the ROCE of the business to 21.4% by FY20. This will be aided by 20% PAT CAGR over FY19E-20E. We

value the company at 18x FY20E EPS to arrive at a fair value of | 450/share and assign a BUY rating

380 450 Buy 18

Heidelberg

Cement

Positive

Heidelberg Cement reported strong Q3FY18 results. Revenues increased 24.8% YoY to | 483.9 crore on the

back of 16.5% YoY growth in volumes. Further, EBITDA/tonne increased 65.5% YoY to | 620/t led by decline in

power cost and operating leverage benefit. Going forward, with higher government spending and improved

availability of sand in the company’s area of operation we expect revenues to grow at a CAGR of 11.0% over

FY17-19E. Also, we expect the EBITDA margin to improve 290 bps in FY17-19E mainly led by operating

leverage benefit and cost efficiency. Further, steady cash flow is expected to help reduce debt in FY17-19E.

Hence, we have a BUY rating on the stock with a target price of | 180 (i.e. valuing at 12.5x FY19E EV/EBITDA,

$142/tonne on capacity of 5.4 MT)

157 180 Buy 15

Indian Hotels Positive

Indian Hotels reported strong Q3FY18 results. Consolidated revenues increased 5.8% YoY to | 1,197.3 crore

mainly led by 8.8% YoY increase in domestic revenue. In addition, the company’s domestic segment continues

to outperform in terms of margins (which increased 28 bps YoY to 30.3%). Going forward, we expect domestic

segment to continue to gain traction led by higher occupancy, limited capacity addition and rise in spending

by domestic travelers. In addition, debt reduction through rights issue and divestment or turnaround of loss

making international subsidiaries remain key positive triggers for the long term. Hence we have a BUY rating

on the stock with a target price of | 155/share (i.e. valuing at EV/room of | 2.5 crore/room)

138 155 Buy 12

Potential

Upside (%)Company Quarterly Performance & Outlook

Q3FY18

Result Rating

Target

Price (|)

Source: ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 5

Sector specific takeaways from quarter

Auto & auto ancillary

Overall auto volumes reported strong volume of 16% YoY mainly due

to the low base of last year, which was impacted by demonetisation. In

terms of segments, 2-W reported healthy growth of 16.6% YoY, driven

by both scooters & motorcycle that were up 20% YoY & 17% YoY

respectively. CV volumes witnessed a noteworthy pick-up (increased

29.6% YoY) driven by robust M&HCV volumes, up 36.8% YoY mainly

due to pre-buying on account of mandatory norm of air ventilation

system in trucks sold after December 31, 2017. On the flip side, PV

segment remained subdued up 3.2% YoY. MSIL, the market leader in

the PV space, continued to outperform, registering 11% YoY growth.

Thus, the overall revenue of I-direct auto universe (Ex Tata Motors -

TML) grew ~25% YoY, with OEM and ancillary revenue growth at

~23% and ~28% YoY, respectively

The EBITDA margin of our universe (ex-TML) declined 33 bps YoY to

~14.6% and was impacted by higher input cost & other expense.

Average prices of key input moved up – steel, aluminum, lead, rubber

increased 8.1%, 17.7%, 11.4%, 3.7% YoY, respectively. Thus, PAT of

the I-direct universe (ex-TML) increased 9% YoY, with OEM’s PAT up

11% YoY while ancillary PAT increased marginally by 2% YoY

Among our coverage OEM universe, TML’s results were below our

estimates, as a ramp up of Velar & Discovery volumes was offset by

run out of higher margin 17 Model Year Range Rover & Range Rover

Sport impacting JLR’s performance. Its domestic business witnessed a

significant turnaround. MSIL revenue and margin were in line with our

expectations. However, lower other income impacted PAT

On the ancillary front, Apollo Tyres and JK Tyre reported strong

volume driven revenue growth (post dumping duty on import of TBR

tyres) & reported QoQ margin expansion. Balkrishna Industries

margins were impacted by one-off events. The battery players, Exide &

Amara reported healthy revenue growth. However, the continued

escalation in lead price impacted their margins. The integration of PKC

group lifted Motherson Sumi’s revenue - up 35.8% YoY but the margin

across its businesses was impacted by higher input cost, start-up cost

& other expenses

We expect the growth momentum to continue in FY19E after 1) the

government’s focus on rural economy aids demand for 2-W players, 2)

A buoyant outlook on infrastructure spending & restriction on over-

loading may catalyse M&HCV growth & 3) positive consumer sentiment

& new launches will drive demand for the PV segment

Exhibit 9: Q3FY18 volume growth YoY (%)

Industry, 16

HMCL, 16

BAL, 18

TVS, 15

HMSI, 25

Maruti, 11

TML, 29

Hyundai, 2

ALL, 42

0 12

+ve

-ve

+ve

-ve

Source: Company, ICICIdirect.com Research

October 2017 was subdued but November & December

made up for the growth in Q3. The traditional year-end

discount/offers also resulted in higher demand for vehicles.

The 3-W saw strong demand revival as volumes grew

52.4% YoY, after domestic & export grew 51.2% YoY &

54.5% YoY, respectively

Further lower other income (due to lower yield on

investments) impacted the profitability of the companies.

Bajaj Auto’s margins were impacted by higher CSR spend

of | 28 crore resulting in higher other expense. Eicher

Motors’ PAT was impacted due to lower other income and

higher depreciation during the quarter. The results of Ashok

Leyland were largely in-line with our estimates.

Bharat Forge reported strong all-round performance.

Wabco’s revenue was driven by strong traction in exports

& domestic M&HCV volumes. However, higher input cost

impacted its margins.Bosch’s revenue & margin came in

above our estimates mainly driven by strong growth in its

mobility segment

The pace of electric vehicle (EV) adoption & BS VI

implementation by 2020 is expected to lead to huge

investments & partnership in R&D

ICICI Securities Ltd. | Retail Equity Research

Page 6

Banking

Asset quality witnessed pressure in Q3FY18 post seeing a fall in

slippages in Q2FY18. Absolute GNPA of PSU banks increased 20%

YoY (6% QoQ) to | 777,266 crore while that of private banks increased

2.1% QoQ to | 108,522 crore. The reasons for rise in slippages include

NPAs from second list referred to NCLT, NPA divergences largely by

SBI and recognition of a large telecom account in Q3FY18

Except for Axis Bank, most private banks saw a QoQ rise in GNPA.

Overall system GNPA & RA remained >12% of loans

Rise in slippages and G-sec yields entailed higher provisions in

Q3FY18, which increased 17% QoQ to | 76,618 crore. This was led by

PSU banks, which saw an increase of 23.9% QoQ to | 66,484 crore

Other income was subdued (down 16.7% YoY, 26.8% QoQ) as

treasury earnings were muted. A sustained rise in yields allowed lower

prospects for any trading gains

NII growth was healthy across banks at 14.8% YoY to | 85,714 crore

(13.7% YoY for PSU banks) mainly led improved traction in loans at

>10% YoY (albeit on a lower base last year due to demonetisation)

As two major line items in P&L (i.e. other income & provisions)

worsened, the sector saw a loss of | 6,943 crore led by PSU banks

Exhibit 10: Financial summary of PSU banks

(| Crore) Q3FY18 Q2FY18 Q1FY18 Q4FY17 Q3FY17 Q2FY17 Q1FY17 YoY (%) QoQ (%)

NII 53652 51860 43918 53983 47190 51816 49085 13.7 3.5

Growth YoY (%) 13.7 0.1 -10.5 10.3 -2.0 4.1 6.6

Other income 23291 35517 26342 32361 30641 28689 23448 -24.0 -34.4

Growth YoY (%) -24.0 23.8 12.3 16.8 61.5 47.9 48.7

Total operating exp. 40220 39206 33897 38931 40082 41115 36860 0.3 2.6

Staff cost 22560 21363 21560 20940 24283 23201 22003 -7.1 5.6

Operating profit 36723 48171 36362 47413 37749 39390 35673 -2.7 -23.8

Growth YoY (%) -2.7 22.3 1.9 26.3 21.4 11.3 14.2

Provision 66484 53678 36697 63115 37348 37589 38116 78.0 23.9

PBT -29760 -5507 -335 -15701 401 1801 -2443 NM NM

PAT -18097 -4284 -307 -10008 -191 308 -1926 NM NM

Growth YoY NM NM NM NM NM -95.9 NM

GNPA 777266 733974 733136 684733 646199 630320 592247 20.3 5.9

Growth YoY 20.3 16.4 23.8 26.8 59.7 100.6 113.3

NNPA 415705 397441 417175 383088 376792 370115 351576 10.3 4.6

Growth YoY 10.3 7.4 18.7 21.5 59.1 107.2 120.2

Source: Capitaline, ICICIdirect.com Research

Exhibit 11: Financial summary of private banks

(| Crore) Q3FY18 Q2FY18 Q1FY18 Q4FY17 Q3FY17 Q2FY17 Q1FY17 YoY (%) QoQ (%)

NII 32062 30948 29987 29780 27455 24132 23219 16.8 3.6

Growth YoY 16.8 28.2 29.1 7.0 15.0 31.6 4.7

Other income 14927 16672 15535 14678 15249 19098 13105 -2.1 -10.5

Growth YoY -2.1 -12.7 18.5 3.4 19.9 80.2 23.8

Total operating exp. 20942 20331 20156 19626 18683 15352 14274 12.1 3.0

Staff cost 7569 7725 7590 7028 7386 7319 6531 2.5 -2.0

Operating profit 26047 27290 25366 24833 24021 27878 22050 8.4 -4.6

Growth YoY 8.4 -2.1 15.0 29.7 11.3 48.3 20.1

Provision 10135 11843 8843 9513 9493 13144 7046 6.8 -14.4

PBT 15872 15407 16484 15283 14490 14701 14911 9.5 3.0

PAT 11154 10506 11683 10565 9651 10501 10314 15.6 6.2

Growth YoY 15.6 0.0 13.3 -2.7 -14.0 0.6 6.3

GNPA 108522 106275 96201 92102 86409 74524 61613 25.6 2.1

Growth YoY 25.6 42.6 56.1 77.4 92.8 103.0 77.0

NNPA 53573 55082 49838 47084 40894 36903 31208 31.0 -2.7

Growth YoY 31.0 49.3 59.7 89.6 103.6 142.2 117.3

Source: Capitaline, ICICIdirect.com Research

Around 16 out of the 21 PSU banks reported losses in Q3FY18.

Bank of India and SBI reported highest losses of | 2341 crore &

| 2416 crore, respectively

ICICI Securities Ltd. | Retail Equity Research

Page 7

Capital goods

On an overall basis, revenues for capital goods companies grew 12.4%

YoY in Q3YF18 backed by robust execution trends across all EPC

companies. EBITDA margins were flattish YoY at 10% given high input

costs were cushioned by a pick-up in execution. PAT for the coverage

universe grew 9.9% YoY

On the order inflow front, L&T announced order wins in to the tune of

| 48,000 crore with strong order wins in the domestic market. We

believe given a pick-up in tendering in the domestic market L&T will be

able to report positive YoY growth in order inflows for FY18E. In the

midcap space, KEC was key performer as order inflows for 9MFY18

were at ~| 11,300 crore mark coupled with strong revenue growth of

26% YoY and margin expansion of 20 bps. Kalpataru Power also

reported strong 9MFY18 order wins with a backlog of | 10,000 crore

thereby ensuring it can grow at a CAGR of >15% in FY18-20E

Bearing companies like SKF, Timken, NRB reported healthy topline,

EBITDA, PAT growth of 11.9% YoY, 38.7% and 35.2%, respectively.

Strong topline numbers were mostly due to improved demand across

user industries – auto, steel, cement, etc and pick-up in exports

Cement: healthy volume growth; high energy costs dent margins

Cement companies under our coverage reported healthy volume

growth of 21.3% YoY (ex-Ambuja) mainly led by low base in the last

year (due to demonetisation). Realisations for the quarter were up

3.6% YoY (down 1.4% QoQ). Consequently, total revenue of the sector

increased 25.7% YoY. In terms of margins, higher power cost (led by

ban on pet coke and sharp rise in pet coke prices) and freight cost (due

to increase in diesel prices and adherence to overloading in north

region) has led to fall in margins (down 190 bps to 16.2% in Q3FY18)

In Q3FY18, realisation for our coverage increased 3.6% YoY mainly

due to change in sales mix (from ex-factory to FOR) and better pricing

in the northern and central region. Players like Heidelberg, Shree

Cement and JK Lakshmi registered realisation growth of 7.1%, 10.1%

& 8.5%, respectively. On the volume front, ACC, Heidelberg reported

volume growth of 27.0%, 16.5%, respectively. UltraTech reported

volume growth of 33.2% YoY mainly led by merger of Jaypee

EBITDA/t in our coverage universe declined 6.9% YoY to | 763/t led by

rise in power and freight cost. Among the coverage universe, ACC and

Heidelberg reported an increase of 28.3% YoY and 65.5% YoY mainly

led by operating leverage benefit and low base last year

Overall, despite healthy revenue growth, profitability was impacted by

increase in cost. Key short-term concerns are RERA compliance, sand

mining, lack of private capex and subdued urban housing demand

Exhibit 12: Cement volumes & capacity utilisation trends

36.8

41.8 40.4

34.931.9

43.8 42.8

34.6

38.7

0.0

10.0

20.0

30.0

40.0

50.0

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

0.0

20.0

40.0

60.0

80.0

100.0

Cement Volumes (In MT) - LHS

Capacity Utilisation (%) - RHS

Source: Company, ICICIdirect.com Research

Exhibit 13: Realisations & margins trend

4,4

86

4,3

15

4,4

79

4,6

42

4,5

38

4,4

61

4,7

57

4,7

67

4,7

00

711

835

985

928

819

747

1008

912

763

0

1,000

2,000

3,000

4,000

5,000

6,000

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

0.0

5.0

10.0

15.0

20.0

25.0

Realisation/tonne - LHS EBITDA/tonne - LHS

Margin (%) - RHS

Source: Company, ICICIdirect.com Research

Product based companies saw robust margin expansion on

account of operating leverage and better product mix

On account of support to the EPC value chain, interest costs

were up 7.4% but lower than revenue growth of the universe,

which is commendable

Bhel also reported decent order wins to the tune of | 12,100

crore in Q3FY18 but management commentary suggests that

they will be able to clock orders more than that they did in

FY17. The key takeaway was the conversion of L1 orders into

final awards and 47% YoY growth in executable backlog

Thermax also maintained its consistency in wining orders as it

managed to bag orders to the tune of | 1,297 crore coupled

with improved management commentary in terms of bouncing

back to growth in FY19E

Other product companies like Grindwell and Greaves Cotton

also reported a healthy Q3FY18 performance

Excluding UltraTech (which had merged Jaypee in current

quarter) volume growth was up 14.8% YoY mainly led by

increase in government spending on infrastructure activities

and capacity expansion

In terms of regional performance, regions like Bihar, Tamil

Nadu and Kerala were impacted by sand availability issues

and poor demand while north and central regional players

witnessed healthy demand from infrastructure

Ramco Cement reported volume growth of 14.7% YoY

mainly led by higher sales in the eastern region. However,

India Cements reported 1.9% YoY decline in volumes mainly

led by sand mining issue in Tamil Nadu. JK Cement

reported volume growth of 20.4% YoY mainly led by 21.7%

YoY growth in grey cement.

However, Ramco reported EBITDA/t decline of 25.4% YoY

due to absence of low cost pet coke inventory in the current

quarter. Further, Mangalam and JK Cement reported 66.6%

YoY and 17.1% YoY in EBITDA/t due to a ban on pet coke in

the company’s area of operations

ICICI Securities Ltd. | Retail Equity Research

Page 8

Consumer Durables

I-direct consumer discretionary universe recorded sales growth in line

with our estimate of ~15% supported by same amount of volume

growth. Volume growth was largely on account of low base

(demonetisation), launch of new products and inventory build-up at

dealer’s level (prior to change in energy norms). As expected, piping

and air conditioner majors recorded strong volume growth of 21% (led

by Astral Poly Technik) and ~23% (led by Voltas) YoY, respectively

On the margin front, raw material prices such as titanium di-oxide and

copper prices witnessed northward movement (up 7% and 29%,

respectively), which put pressure on gross margin of paint companies

(down in the range of ~150 bps) and selective electrical goods

companies (remain flat in Q3FY18). However, the impact of flattish to

negative gross margin was largely negated by higher operating

leverage, which finally translated into a marginal increase in I-direct

universe EBITDA margin (up ~60 bps YoY)

With GST related issues subsiding, going forward, we believe the trade

channel across India would start building inventory at pre-GST level.

We believe organised players would also benefit from implementation

of GST in terms of gaining market share due to a shift in demand from

the unorganised to organised category

FMCG

FMCG companies witnessed strong growth in the December quarter

led by robust volume growth on account of the low base of the

corresponding quarter impacted by demonetisation. The previous two

quarters were impacted by GST related trade disruption mainly due to

large wholesale network de-stocking and difficulty in coping up with

the new indirect tax regime

However, in Q3FY18 except small de-growth in canteen store

department (CSD) most general trade has returned to normal. Our

coverage universe reported 5.7% growth in sales. However, on a

comparable basis (net of excise in base quarter), sales witnessed

double digit growth. With the further cut in GST rate on detergents,

malt based beverages and other FMCG products, companies have

passed on the benefits in terms of price cuts during the quarter

In our coverage universe, HUL, Dabur, GSK and Marico witnessed

17%, 18%, 20% & 15% comparable sales growth, respectively, led by

robust volume growth. Most companies have not taken any price

increase mainly due to anti profiteering clause under GST. However,

due to a sharp increase in copra prices, Marico has passed on some of

this increase in terms of price hikes

Our coverage universe has seen a 230 bps expansion in operating

margins. Led by higher EBITDA, net profit of our coverage universe

companies has seen healthy growth of 22%. FMCG behemoth HUL

and ITC have seen net profit growth of 27% & 17%, respectively

Despite a commodity price increase, FMCG companies have been able

to further expand their already elevated margins with the reduction in

advertisement expenditure due to a shift towards digital advertisement

and GST related input cost benefits

Quarterly sales growth (%)

10.5

5.0

-0.3

-1.0

0.6

4.9

6.46.1

0.7

5.1

2.6

5.4

6.2

-2

0

2

4

6

8

10

12

Q3FY15

Q4FY15

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

Source: Company, ICICIdirect.com Research

On the other hand, paint industry volume growth was largely

driven by Kansai Nerolac whereas Asian Paints volume

growth remains at lower single digit (~5% YoY). Though

selective counters witnessed realisation growth in Q3FY18

(due to a change in product mix), the I-direct CD realisation

growth remain muted

Under our coverage universe, Pidilite, Essel Propack and V-

Guard recorded an increase in EBITDA margin by 252 bps, 223

bps and 136 bps YoY, respectively

ICICI Securities Ltd. | Retail Equity Research

Page 9

Hotel: Improving occupancy, ARR keeps revenues buoyant

This being a seasonally strong quarter, occupancy and average room

revenues (ARR) improved in business and leisure destination.

Occupancy levels and ARR in business destination increased 2.0% and

1.0%, respectively, while occupancy and ARR in leisure destination

increased 1.0% and 2.0%, respectively

TajGVK reported a good set of Q3FY18 numbers. The key highlight of

the quarter was the turnaround in the company’s JV Taj Santacruz,

which reported a net profit of | 39 lakh for the first time since its

commissioning. Further, the company’s consolidated topline increased

14.4% YoY while margins improved 376 bps led by lower power cost

and operating leverage benefit

Indian Hotels (IHCL) reported a 5.8% YoY increase in consolidated

revenues mainly due to 8.8% YoY rise in domestic revenues. However,

IHCL’s EBITDA margin declined 16 bps YoY to 23.4% led by 174 bps

YoY decline in international margins at 11.4% while domestic margins

improved 28 bps YoY to 30.3%

Exhibit 12: Occupancy trend

73

77

6769

78

68

75

70

55

74

63

74

63

7370

55

76

61

77

60

40

50

60

70

80

90

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

(%

)

Business Destinations Leisure Destinations

Source: Company, ICICIdirect.com Research

Exhibit 13: ARR trend

8392

6635

6766 8083

8077

6944

6915

8163

8517

9108

5333

5910

9533

6850

5583

9825

8065

9636

0

2000

4000

6000

8000

10000

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

(|

)

Business Destinations Leisure Destinations

Source: Company, ICICIdirect.com Research

Information Technology

Tier-I IT companies reported dollar revenue growth of 1.2% QoQ and

9% YoY growth in Q3FY18. Constant currency (CC) revenues grew an

average of 1.5% QoQ in a seasonally weak quarter

Analysing growth trends across geographies suggests Europe leading

the growth for most Tier-I IT companies while US witnessed a

slowdown in momentum. Among verticals, energy saw good growth

while retail is witnessing early signs of a recovery. BFSI segment

continued to see pressure and is yet to see any recovery although

insurance is going steady. Digital offerings with 20-30% contribution to

overall revenues is witnessing healthy double digit growth

In terms of revenue outlook for FY18E, Infosys, HCL Tech maintained

its revenue guidance of 5.5-6.5% and 10.5-12.5% in CC terms with HCL

expecting to meet the lower end of the revenue guidance

For Tier-I companies, EBIT margins for the quarter were largely flat

sequentially. Wipro IT services margins declined 250 bps QoQ to

14.8% on account of one-off. However, barring a one-off, margins

were flat QoQ. In terms of EBIT margin trajectory for FY18E, Infosys

(23-25%) and HCL Tech (19.5-20.5%) retained their margin guidance

while TCS continues to target its EBIT margin band of 26-28% (in CC

terms) for FY18E but will be watchful on increased local hiring and

demand for investments in digital. Notably, for mid-tier IT companies,

a healthy recovery on EBITDA margins front was seen in the quarter

Dollar revenue growth trend

0.7

3.2

2.9

(1.4)

1.5

3.1

3.2

1.0

4.1 3.7 2.3

3.1

2.7

0.8

2.2

(0.7)

-5

0

5

10

Q4FY17

Q1FY18

Q2FY18

Q3FY18

%

Infosys TCS

HCL Tech Wipro

Source: Company, ICICIdirect.com Research,

EIH’s reported revenues were flat YoY but margins declined

282 bps YoY due to increase in employee cost

Management commentaries are indicative of a better FY19E

owing to better client commentary and in anticipation of a

better performance compared to FY18E

ICICI Securities Ltd. | Retail Equity Research

Page 10

Infrastructure, building material and real estate

Infrastructure

Our construction universe top line de-grew 3.8% YoY to | 4,532.2

crore mainly due to GST transition related issues. On the operational

front, there was a 240 bps YoY expansion in EBITDA margins to 11.1%

on account of exceptionally high margins for NCC. Consequently, the

bottomline of our universe grew robustly by 37.7% YoY to | 193.3

crore owing to 72.2% YoY PAT growth of NCC. Overall, with a strong

order book and anticipated improvement in working capital cycle and

debt reduction, execution our construction universe is expected to pick

up from FY19 onwards

Strong opportunities lie ahead with NHAI looking to bid out EPC and

HAM projects worth ~| 1.3 lakh crore over the next few months. Also,

strong awarding momentum should continue with the government

looking to construct 83,677 km of roads over the next five years with a

total outlay of | 6.92 lakh crore under the Bharatmala Pariyojana. We

believe this programme could provide a huge fillip to road awarding

activity over next few years benefiting our road & construction

universe companies

Building materials

Our building material coverage universe companies posted decent

performance across product categories given the low base as Q3FY17

was impacted by demonetisation. Also, de-stocking continued in the

first half of Q3FY18 as dealers maintained minimum inventory amid

possibilities of a GST rate cut from 28% to 18% for several building

material products. Now, with the GST rate cut across product

categories to 18%, we expect a faster unorganised to organised sector

shift, benefiting our building material universe companies

However, passage of the e-way bill would play a critical role for faster

movement of unorganised players to organised sector. The deferral of

e-way bill implementation may hinder their growth prospects in the

near term

In Q3FY18, our tiles universe posted volume growth of 8.4% YoY to

29.4 MSM. However, revenues grew 3% YoY to | 1046.8 crore as

realisations softened during the quarter

Further, EBITDA margins contracted 160 bps YoY to 13.3% due to

higher fuel costs. Hence, the bottomline of our tiles universe declined

significantly by 8.8% YoY to | 68.6 crore

The plywood segment reported strong numbers in Q3FY18. While

Greenply’s (GIL) plywood volumes grew 13.1%, Century Plyboards

(CPIL) reported volume growth of 3.8%. Consequently, the topline of

our plywood universe grew moderately by 16.0% YoY to | 909.2 crore

led by 20.6% YoY growth in CPIL’s revenues to | 509.9 crore as the

MDF division has started contributing to the topline

Real estate

The demand scenario in the real estate sector continued to remain

subdued in Q3FY18. Furthermore, new launches could pick up from

FY19E onwards with several companies planning to launch a few new

projects. Going forward, over the long term, with RERA

implementation, a consolidation in the industry is expected, which

would ultimately benefit organised players like Mahindra Lifespace,

Sobha, Oberoi Realty & Sunteck Realty of our coverage universe

On the volume front, Sobha’s volumes grew 8.4% QoQ to 9.33 lakh sq

ft (lsf) while Mahindra Lifespace’s sales volumes grew 13.6% QoQ to

2.5 lsf. However, Oberoi’s volumes de-grew 12.9% QoQ at 1.5 lakh sq

ft, given the absence of new launches and current market scenario

Tiles universe sales volume trend

15.9

19.3

16.4

17.4

17.6

11.2

15.6

9.3

12.5

11.8

4

8

12

16

20

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18E

(M

SM

)

Kajaria Ceramics Somany Ceramics

Source: Company, ICICIdirect.com Research,

On the road front, topline grew moderately by 3.0% YoY to

| 3,362.6 crore on account of moderate execution during the

quarter. Furthermore, EBITDA margins contracted 320 bps YoY

to 26.2%. However, the bottomline of our road universe

reported significant growth of 15.7% to | 412.0 crore due to

18.1% YoY growth in the PAT of PNC Infratech

Further, on operational front, EBITDA margins expanded 160

bps YoY to 16.5% led by 130 bps YoY expansion in CPIL’s

margins. Consequently, our plywood universe posted a robust

bottom-line growth of 35.0% YoY to | 82.7 crore

On the financial front, revenues of our real estate universe

grew 30.2% YoY to | 1394.3 crore mainly due to 144.0%

YoY growth in Sunteck’s topline (due to incremental

revenues from Sunteck City Avenue 1 & 2 at Goregaon

during Q3FY18). Consequently, the bottomline of universe

grew robustly at 51.6% YoY to | 245.3 crore

ICICI Securities Ltd. | Retail Equity Research

Page 11

Logistics

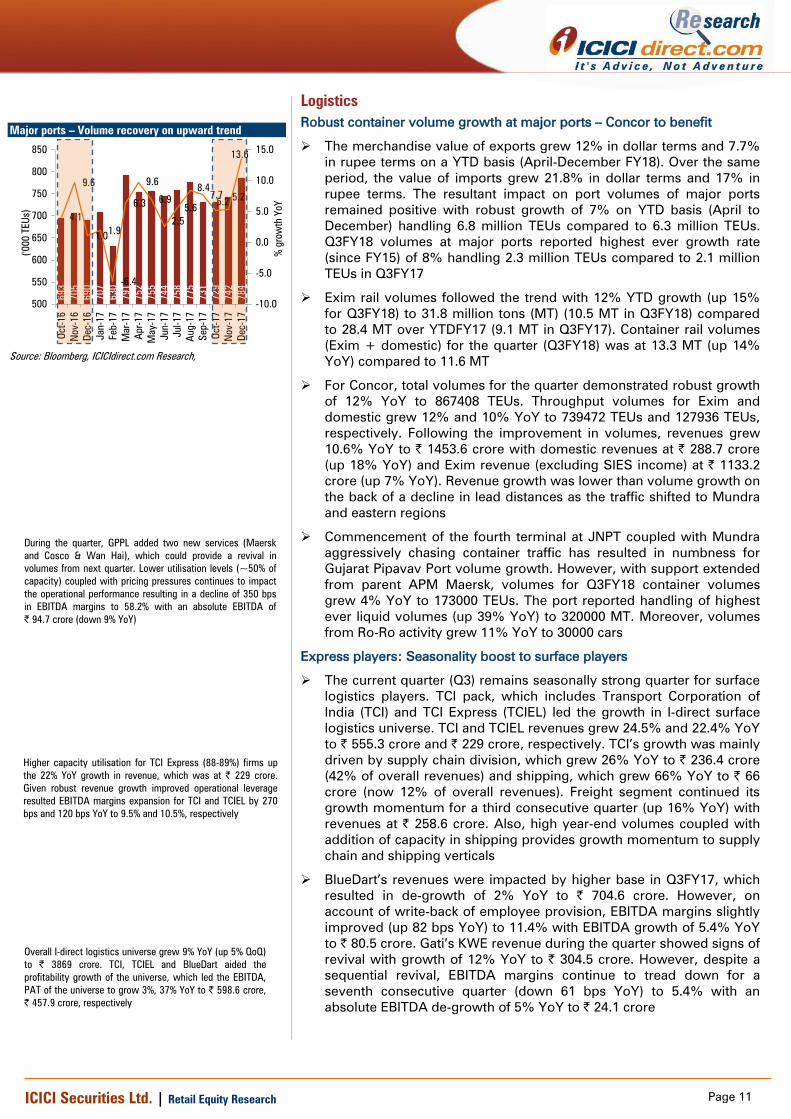

Robust container volume growth at major ports – Concor to benefit

The merchandise value of exports grew 12% in dollar terms and 7.7%

in rupee terms on a YTD basis (April-December FY18). Over the same

period, the value of imports grew 21.8% in dollar terms and 17% in

rupee terms. The resultant impact on port volumes of major ports

remained positive with robust growth of 7% on YTD basis (April to

December) handling 6.8 million TEUs compared to 6.3 million TEUs.

Q3FY18 volumes at major ports reported highest ever growth rate

(since FY15) of 8% handling 2.3 million TEUs compared to 2.1 million

TEUs in Q3FY17

Exim rail volumes followed the trend with 12% YTD growth (up 15%

for Q3FY18) to 31.8 million tons (MT) (10.5 MT in Q3FY18) compared

to 28.4 MT over YTDFY17 (9.1 MT in Q3FY17). Container rail volumes

(Exim + domestic) for the quarter (Q3FY18) was at 13.3 MT (up 14%

YoY) compared to 11.6 MT

For Concor, total volumes for the quarter demonstrated robust growth

of 12% YoY to 867408 TEUs. Throughput volumes for Exim and

domestic grew 12% and 10% YoY to 739472 TEUs and 127936 TEUs,

respectively. Following the improvement in volumes, revenues grew

10.6% YoY to | 1453.6 crore with domestic revenues at | 288.7 crore

(up 18% YoY) and Exim revenue (excluding SIES income) at | 1133.2

crore (up 7% YoY). Revenue growth was lower than volume growth on

the back of a decline in lead distances as the traffic shifted to Mundra

and eastern regions

Commencement of the fourth terminal at JNPT coupled with Mundra

aggressively chasing container traffic has resulted in numbness for

Gujarat Pipavav Port volume growth. However, with support extended

from parent APM Maersk, volumes for Q3FY18 container volumes

grew 4% YoY to 173000 TEUs. The port reported handling of highest

ever liquid volumes (up 39% YoY) to 320000 MT. Moreover, volumes

from Ro-Ro activity grew 11% YoY to 30000 cars

Express players: Seasonality boost to surface players

The current quarter (Q3) remains seasonally strong quarter for surface

logistics players. TCI pack, which includes Transport Corporation of

India (TCI) and TCI Express (TCIEL) led the growth in I-direct surface

logistics universe. TCI and TCIEL revenues grew 24.5% and 22.4% YoY

to | 555.3 crore and | 229 crore, respectively. TCI’s growth was mainly

driven by supply chain division, which grew 26% YoY to | 236.4 crore

(42% of overall revenues) and shipping, which grew 66% YoY to | 66

crore (now 12% of overall revenues). Freight segment continued its

growth momentum for a third consecutive quarter (up 16% YoY) with

revenues at | 258.6 crore. Also, high year-end volumes coupled with

addition of capacity in shipping provides growth momentum to supply

chain and shipping verticals

BlueDart’s revenues were impacted by higher base in Q3FY17, which

resulted in de-growth of 2% YoY to | 704.6 crore. However, on

account of write-back of employee provision, EBITDA margins slightly

improved (up 82 bps YoY) to 11.4% with EBITDA growth of 5.4% YoY

to | 80.5 crore. Gati’s KWE revenue during the quarter showed signs of

revival with growth of 12% YoY to | 304.5 crore. However, despite a

sequential revival, EBITDA margins continue to tread down for a

seventh consecutive quarter (down 61 bps YoY) to 5.4% with an

absolute EBITDA de-growth of 5% YoY to | 24.1 crore

Major ports – Volume recovery on upward trend

693

705

690

707

630

791

752

755

744

758

775

731

729

742

784

4.1

9.6

1.01.9

-6.4

6.3

9.6

6.9

2.5

5.6

8.4

7.75.2

5.2

13.6

500

550

600

650

700

750

800

850

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

('0

00 T

EU

s)

-10.0

-5.0

0.0

5.0

10.0

15.0

% g

row

th Y

oY

Source: Bloomberg, ICICIdirect.com Research,

During the quarter, GPPL added two new services (Maersk

and Cosco & Wan Hai), which could provide a revival in

volumes from next quarter. Lower utilisation levels (~50% of

capacity) coupled with pricing pressures continues to impact

the operational performance resulting in a decline of 350 bps

in EBITDA margins to 58.2% with an absolute EBITDA of

| 94.7 crore (down 9% YoY)

Higher capacity utilisation for TCI Express (88-89%) firms up

the 22% YoY growth in revenue, which was at | 229 crore.

Given robust revenue growth improved operational leverage

resulted EBITDA margins expansion for TCI and TCIEL by 270

bps and 120 bps YoY to 9.5% and 10.5%, respectively

Overall I-direct logistics universe grew 9% YoY (up 5% QoQ)

to | 3869 crore. TCI, TCIEL and BlueDart aided the

profitability growth of the universe, which led the EBITDA,

PAT of the universe to grow 3%, 37% YoY to | 598.6 crore,

| 457.9 crore, respectively

ICICI Securities Ltd. | Retail Equity Research

Page 12

Media

This quarter witnessed a strong revival in the broadcasting sector,

reflecting the waning impact of the after effects of GST and RERA. In

contrast, the print sector continued to suffer from these legislations and

their continued impact on the localised ad market, which is likely to take

some time to recover. Multiplexes continued to report strong ad growth

given the star studded movies slate. In the broadcasting segment,

subscription revenues continued it double digit growth run rate.

In broadcasting segment, the ad revenue growth (25.7% YoY for

Zee, ~21.6% for TV Today and 4% YoY for Sun TV) was strong on

account of strong volume numbers for FMCG companies (one of

the biggest clients for TV broadcasters). Subscription revenues for

Zee declined 15.5% YoY owing to exclusion of sports business. On

a like-to-like basis, domestic subscription grew 7.5% YoY.

Subscription revenues for Sun TV grew 16.5% YoY

Multiplex: Ad revenues for the quarter continued to report strong

numbers for multiplexes. Ad revenues for Inox grew 33.3% YoY

while that of PVR grew 10.6% YoY. On account of strong content

slate in the base (Dangal, MS Dhoni, Ae Dil Hai Mushkil) and

relatively weak content performance this quarter except Tiger

Zinda Hai and Golmaal Again, footfall for the quarter declined for

multiplexes (decline of 2.7% YoY for Inox and 2.8% YoY for PVR).

However, because of star studded movies, multiplexes could raise

ATPs and it grew 6% YoY for Inox and 6.6% YoY for PVR.

Consequently, on account of ATP growth, the box office

collections were relatively strong

Print: In the print segment, we witnessed a mixed set of numbers.

HMVL reported 5% YoY ad revenue growth while DB Corp and

Jagran reported 5.8% YoY and 3.8% YoY decline in ad revenues,

respectively. Circulation revenues grew 1.4%,6.1% YoY for Jagran

and DB Corp, respectively

In radio segment, ENIL reported 1.5% YoY de-growth in ad

revenues. However, adjusting for one client issue, ad revenues

would have grown 4.6% YoY, which was similar to peer’s ad

growth for the quarter

Metals

Q3FY18 for the metals and mining sector was marked by healthy

volume growth and strong realisations. The topline of the coverage

universe increased 20% YoY and 13% QoQ to | 86,154 crore. The

aggregate sector EBITDA was at | 22,219 crore registering growth of

25% YoY and 39% QoQ. Corresponding EBITDA margins came in at

25.8% (vs. Q3FY17: 24.7% and Q2FY18: 21%).

The ferrous space reported outperformance on the back of increased

volumes and strong realisations. JSW Steel’s domestic operations

reported healthy volume of 4.0 MT for the quarter. The company’s

consolidated topline increased 27.5% YoY, 6.2% QoQ to | 17,861

crore on the back of higher than anticipated realisations. Consolidated

EBITDA came in at | 3,851 crore (up 34.3% YoY, 26.8% QoQ).

Resultant consolidated EBITDA margin was at 21.6%. Standalone

operations reported a strong EBITDA/tonne of | 9,000/tonne

Graphite electrode majors reported another upbeat performance for

Q3FY18 driven by higher realisations. Graphite India (GIL) reported a

strong set of Q3FY18 numbers wherein the topline came in at | 933.1

crore (up 176.4%YoY, 102.0% QoQ). The EBITDA came in at | 518.6

crore (implying EBITDA margin of 55.6%). HEG reported a robust

performance for the quarter. The operating income came in at | 842.7

crore (up 256.2% YoY, 105.8% QoQ). The company reported EBITDA

of | 557.5 crore with strong EBITDA margin of 66.2%)

Footfalls – PVR & Inox

18.517.9 18.2

21.0

18.7

19.7

12.7 12.513.0

15.8

12.8

15.3

10

15

20

25

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

(m

illion)

PVR Inox

Source: Company, ICICIdirect.com Research

Going ahead, we expect broadcaster to continue with

strong ad growth momentum owing to budget 2018-19

emphasis on doubling rural income (augurs well for FMCG,

one of the biggest clients for TV segment). The momentum

of strong ad growth is expected to continue for Multiplexes

in the next quarter as well while Print is likely to witness a

rather gradual recovery vis-à-vis other mediums.

During Q3FY18, the entire non-ferrous pack witnessed a

healthy uptick both YoY and QoQ. During the quarter,

average zinc prices were up 28.6% YoY and 9.1% QoQ to

US$3232/tonne. Average lead prices were up 16.4% YoY

and 6.8% QoQ to US$2489/tonne. During the quarter,

aluminium prices increased 23.0% YoY and 4.7% QoQ to

US$2104/tonne while copper prices increased 29.3% YoY

and 7.4% QoQ to US$6822/tonne

On the back of healthy prices of non ferrous metals and

crude, Vedanta reported a steady performance for Q3FY18,

wherein the topline increased 25.5% YoY and 12.8% QoQ to

| 24,361 crore. The EBITDA grew 15% YoY, 19.3% QoQ to |

6,763 crore. The corresponding EBITDA margin stood at

27.8%. The company reported a PAT of | 2,173 crore.

ICICI Securities Ltd. | Retail Equity Research

Page 13

Oil & gas

Crude oil prices in Q3FY18 increased sharply QoQ by 19.1% to

US$61.6/bbl from US$51.7/bbl in Q2FY18. On account of the same,

realisations of upstream oil companies reported QoQ improvement

and were reflected in the topline, which was largely in line with our

estimates. However, oil & gas production numbers were slightly below

our estimates. While EBITDA increased ~20% QoQ, profitability

declined ~2% QoQ and came in below our estimates on higher

expenses related to exploratory costs and DD&A

Oil marketing companies reported a mixed performance on the

operational front with lower-than-expected operational GRMs. On the

marketing front, product sales were largely in line with our estimates

and reported an average growth indicating consistency despite

increased competition from private players. The profitability increased

~50% QoQ mainly on account of higher than estimated inventory gain

Pharmaceuticals

In line with expectations, the challenging environment in the US

generic space continues to impact the pharma universe growth.

Domestic formulations growth also came lower-than I-direct estimates

mainly due to slow recovery post GST implementation. Revenues of

the I-direct universe were at | 39,781 crore, growth of 2% YoY

US sales (select pack) declined 15% YoY to | 10,309 crore due to

persisting pricing pressure owing to client consolidation and increased

competition, lack of meaningful approvals and high base. Domestic

formulations grew 10% YoY to | 8,612 crore. Domestic inventory

holding period at distributor level has come down to 30-35 days

compared to historical level of 40-45 days. Management commentary

suggests inventory holding period is likely to remain at current level

On the revenues front, eight out of 19 companies under coverage

registered negative or muted growth during the quarter due to

continued pricing pressure in the US and slower-than-expected

domestic recovery in some companies after GST implementation and

changes in reporting pattern (new reporting norm ex-excise). Bucking

the trend, Jubilant Life registered 39% YoY growth (reported robust

growth across portfolio) while Cadila registered 38% YoY growth

mainly due to exclusivity for gLialda (ulcerative colitis)

EBITDA for the universe declined ~12% YoY to | 8,541 crore mainly

due to pricing pressure in the US. However, an improvement in

domestic margins, cost rationalisation and curb in R&D spending

restricted further fall in margins. Net profit declined 32% YoY to | 3900

crore due to lower operational performance, one-off

Impairment/amortisation charges and additional tax provisions due to

re-measurement of deferred tax assets post the change in US tax rate

Exhibit 14: Sharing of gross under-recoveries (| crore)

Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18

Upstream 0 0 0 0 0

Downstream 0 0 0 0 0

Government 4297 7604 6319 3239 7892

Total 4297 7604 6319 3239 7892

Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18

Upstream 0.0 0.0 0.0 0.0 0.0

Downstream 0.0 0.0 0.0 0.0 0.0

Government 100.0 100.0 100.0 100.0 100.0

Total 100.0 100.0 100.0 100.0 100.0

Sharing of gross under-recoveries (%)

Sharing of gross under-recoveries (| crore)

Source: Company, ICICIdirect.com Research

Sales from US & India (| crore)

(| crore) Q3FY18 Q3FY17 Var. (%) Q2FY18 Var. (%)

Ajanta 155.0 149.0 4.0 172.0 -9.9

Alembic 314.1 294.0 6.8 346.5 -9.4

Biocon 156.1 123.3 26.6 175.9 -11.3

Cadila 916.8 796.8 15.1 894.5 2.5

Glenmark 578.5 516.9 11.9 710.7 -18.6

Indoco 155.9 144.2 8.2 188.2 -17.2

Ipca 382.9 343.0 11.6 424.7 -9.9

Lupin 1,068.8 991.2 7.8 1,159.3 -7.8

Cipla 1,601.0 1,398.0 14.5 1,646.0 -2.7

Dr Reddy's 612.6 594.7 3.0 637.0 -3.8

Sun Pharma 2,085.0 1,969.4 5.9 2,221.0 -6.1

Torrent 586.0 503.0 16.5 607.0 -3.5

Total 8,612.7 7,823.4 10.1 9,182.8 -6.2

India

(| crore) Q3FY18 Q3FY17 Var. (%) Q2FY18 Var. (%)

Aurobindo 1,909.6 1,745.1 9.4 2,098.9 -9.0

Cadila 1,583.8 886.9 78.6 1,643.6 -3.6

Cipla 650.0 662.0 -1.8 617.3 5.3

Glenmark 735.9 1,230.8 -40.2 727.1 1.2

Lupin 1,432.1 2,175.5 -34.2 1,361.1 5.2

Dr Reddy's 1,607.3 1,659.5 -3.1 1,431.8 12.3

Sun Pharma 2,124.2 3,419.3 -37.9 1,986.2 6.9

Torrent 266.0 310.0 -14.2 255.0 4.3

Total 10,308.8 12,089.1 -14.7 10,121.0 1.9

US

Source: Company, ICICIdirect.com Research

Key parameters in Q3FY18

Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18

Singapore

GRMs ($/bbl) 6.7 6.4 6.7 8.3 7.4

Crude oil

($/bbl) 50.1 54.6 50.1 51.7 61.6

APM gas

(NCV)

($/mmbtu) 2.7 2.7 2.7 2.7 3.2

Source: Bloomberg, Reuters, ICICIdirect.com Research

On the gas utility companies front, the performance continued

to show QoQ and YoY improvement due to robust volume

growth with financials coming in line with our estimates. The

volume growth was mainly contributed by city gas distribution

sector with increased conversion of CNG vehicles and

additions of PNG houses. The relatively lower domestic APM

gas prices and suitable price hikes augured well for margins in

Q3FY18

ICICI Securities Ltd. | Retail Equity Research

Page 14

Power

Regulated utilities reported a below expected performance in terms of

revenue and profitability. However, the only silver lining was decent

capacity addition by both regulated utilities. NTPC reported ~4200 MW

of capacity addition in 9MFY18 while the target for FY19E seems

encouraging in terms of capacity addition. On the Q3FY18

performance, the generation growth at 10% YoY was in line but

EBIDTA was below estimates as higher employee expenses (non-pass

though portion) dented profitability

CESC reported of results as energy sold grew 12% YoY, in line with

estimates. However, higher cost of power purchase was a dampener.

Also, higher base of demonetisation in Q3FY17 impacted SSG growth

at Spencer’s Retail while PLFs of Chandrapur were soft QoQ at 37% on

account of lower sales in the spot market

Retail

Q3FY18 turned out to be a mixed quarter for retail companies wherein,

on the one hand, various branded players reported steady topline

growth, while on the other, margin profile for various players

enhanced significantly. The boost in profitability can be attributed to, a)

sustained efforts towards cost optimisation and b) benefit of input tax

credit kicking in. Revenues of our retail coverage universe grew 7.2%

while EBITDA grew robustly by 30% YoY in Q3FY18

Shoppers Stop’s departmental store reported LTL sales growth of

mere 1.4% YoY. The subdued LTL growth was on account of the

recent downward revision of GST rates on various non-apparel

categories (37% of revenues) leading to lower MRP. On the balance

sheet front, efforts to improve the liquidity resulted in a debt reduction

by ~| 300 crore (HyperCity stake disinvestment) to | 237 crore as on

December 31, 2017 (Debt Equity down from 0.8x in FY17 to 0.2x)

Among specialty retail, Titan reported moderate revenue growth of

8.3% in Q3FY18 despite Dussehra falling in September this year.

Primary sales for Tanishq had been lower due to advance stocking

requirements by franchisees, which happened during the end of

Q2FY18. Going forward, the management remained upbeat on the

growth outlook for the jewellery division.

Textiles

Despite cotton prices cooling down ~4-5% to | 107/kg vs. | 112/kg,

margins for textiles players continued to remain under pressure on

account of a) high cost cotton inventory, b) constant rupee

appreciation and c) reduction in duty drawbacks. EBITDA margins for

Arvind’s textile division declined sharply by 330 bps YoY to 14%, while

EBITDA margins for Vardhman Textiles declined 740 bps YoY to 13.7%

On the revenue front, the apparel coverage universe reported healthy

growth of 15% YoY in Q3FY18. The growth can be attributed to

favourable base effect of demonetisation and normalisation in trade

channels settling in gradually post GST disruptions

Arvind’s revenues increased 16% YoY driven by strong performance

in branded segment, which grew 24% YoY, while the textile segment

rose 9.4% YoY. Innerwear companies, Page and Rupa reported robust

revenue growth of 18% and 35%, respectively. Kewal Kiran Clothing

(KKCL) revenues remained flattish as it refrained from giving away

heavy discounts. The management believes it would result in a dilution

of its brand image and have a negative impact on its profitability

LTL sales growth for departmental stores

17.4

5.9

5.5

2.2

6.4

19.8

1.4

(5.5

)

(1.1

)

(20)

(10)

-

10

20

30

40

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

%

Blended Stores > 5 years Stores < 5 years

Source: Company, ICICIdirect.com Research

Power Grid also reported strong assets in 9MFY18, which was

in excess of | 19,500 crore and is well on track to achieve its

guidance of | 31,000 crore of asset capitalisation. Revenues

and PAT were below estimates on account of below expected

telecom and consultancy revenues

Vardhman Textiles reported double digit topline growth of

12.3% YoY after many quarters with revenues from textile

segment and acrylic fibre segment growing at 11% and 21%,

respectively. Revenues for Siyaram grew 15.6% YoY, with a

sharp recovery being witnessed in the fabric division (20%

growth) while garmenting segment continued on its strong

trajectory (21% growth).

Among branded apparel players, Arvind (brands & retail

segment), Siyaram and Page reported margin expansion of

350 bps, 50 bps and 200 bps YoY, respectively.

Revenues for Aditya Birla Fashion and Retail (ABFRL) grew 9%

YoY, mainly led by steady growth in lifestyle brands (8.2%

growth) and Pantaloons (12% growth)

Trent Ltd, sustained its healthy revenue trajectory with a

growth of 18% YoY (the results also included revenues from

Zudio that was acquired by the company with effect from

October 1, 2017)

ICICI Securities Ltd. | Retail Equity Research

Page 15

Telecom

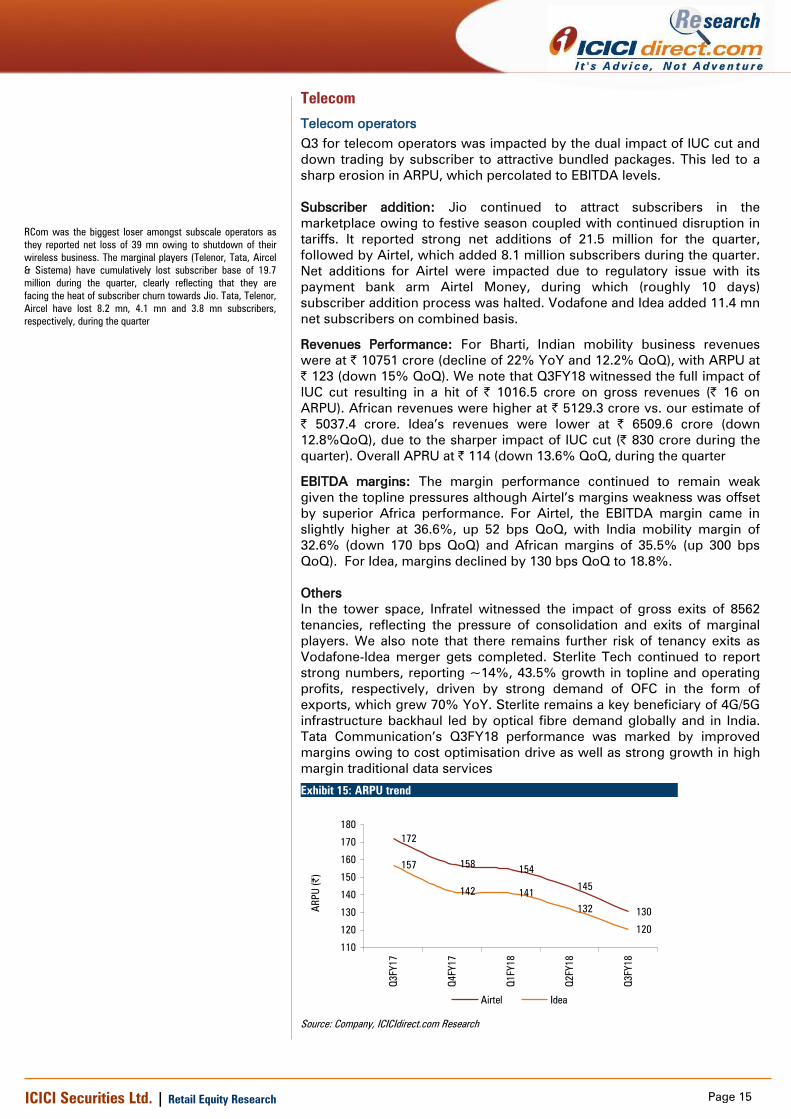

Telecom operators

Q3 for telecom operators was impacted by the dual impact of IUC cut and

down trading by subscriber to attractive bundled packages. This led to a

sharp erosion in ARPU, which percolated to EBITDA levels.

Subscriber addition: Jio continued to attract subscribers in the

marketplace owing to festive season coupled with continued disruption in

tariffs. It reported strong net additions of 21.5 million for the quarter,

followed by Airtel, which added 8.1 million subscribers during the quarter.

Net additions for Airtel were impacted due to regulatory issue with its

payment bank arm Airtel Money, during which (roughly 10 days)

subscriber addition process was halted. Vodafone and Idea added 11.4 mn

net subscribers on combined basis.

Revenues Performance: For Bharti, Indian mobility business revenues

were at | 10751 crore (decline of 22% YoY and 12.2% QoQ), with ARPU at

| 123 (down 15% QoQ). We note that Q3FY18 witnessed the full impact of

IUC cut resulting in a hit of | 1016.5 crore on gross revenues (| 16 on

ARPU). African revenues were higher at | 5129.3 crore vs. our estimate of

| 5037.4 crore. Idea’s revenues were lower at | 6509.6 crore (down

12.8%QoQ), due to the sharper impact of IUC cut (| 830 crore during the

quarter). Overall APRU at | 114 (down 13.6% QoQ, during the quarter

EBITDA margins: The margin performance continued to remain weak

given the topline pressures although Airtel’s margins weakness was offset

by superior Africa performance. For Airtel, the EBITDA margin came in

slightly higher at 36.6%, up 52 bps QoQ, with India mobility margin of

32.6% (down 170 bps QoQ) and African margins of 35.5% (up 300 bps

QoQ). For Idea, margins declined by 130 bps QoQ to 18.8%.

Others

In the tower space, Infratel witnessed the impact of gross exits of 8562

tenancies, reflecting the pressure of consolidation and exits of marginal

players. We also note that there remains further risk of tenancy exits as

Vodafone-Idea merger gets completed. Sterlite Tech continued to report

strong numbers, reporting ~14%, 43.5% growth in topline and operating

profits, respectively, driven by strong demand of OFC in the form of

exports, which grew 70% YoY. Sterlite remains a key beneficiary of 4G/5G

infrastructure backhaul led by optical fibre demand globally and in India.

Tata Communication’s Q3FY18 performance was marked by improved

margins owing to cost optimisation drive as well as strong growth in high

margin traditional data services

Exhibit 15: ARPU trend

172

158154

145

130

157

142 141

132

120

110

120

130

140

150

160

170

180

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

AR

PU

(|

)

Airtel Idea

Source: Company, ICICIdirect.com Research

RCom was the biggest loser amongst subscale operators as

they reported net loss of 39 mn owing to shutdown of their

wireless business. The marginal players (Telenor, Tata, Aircel

& Sistema) have cumulatively lost subscriber base of 19.7

million during the quarter, clearly reflecting that they are

facing the heat of subscriber churn towards Jio. Tata, Telenor,

Aircel have lost 8.2 mn, 4.1 mn and 3.8 mn subscribers,

respectively, during the quarter

Page 16 ICICI Securities Ltd | Retail Equity Research

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC

Andheri (East)

Mumbai – 400 093

Page 17 ICICI Securities Ltd | Retail Equity Research

Disclaimer ANALYST CERTIFICATION We /I, Pankaj Pandey Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the

subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI

Securities Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private

sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the

details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment

banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons

reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential

and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any

form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the

information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has

been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory

capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed.

This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or

other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as

customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or

appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions,

based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The

recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI

Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are

advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections.

Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other

assignment in the past twelve months.