ch.1 the nature of accounting - wordpress.com€¦ · 1 ch.1 the nature of accounting ......

TRANSCRIPT

12/13/13

1

Ch.1 The Nature of Accounting

J. Wu 1

• What is accounting?

• Why do we need accounting?

• Elements of accounting and accounting

equation

• What is business transaction and how to record

them?

• Financial statements overview

• Ethics issues

12/13/13

2

• Accounting is the process of recording, summarizing, analyzing, and interpreting financial activities to permit individuals and organizations to make informed judgments and decisions.

• Accounting combines recording, summarizing, analyzing, and interpreting into a single process and applies this process to financial activities.

J. Wu 2

12/13/13

3

• Individuals

• Owners

• Managers

• Investors

• Banks and other lending institutions

• Governments

• Tax authorities

J. Wu 3

12/13/13

4

J. Wu 4

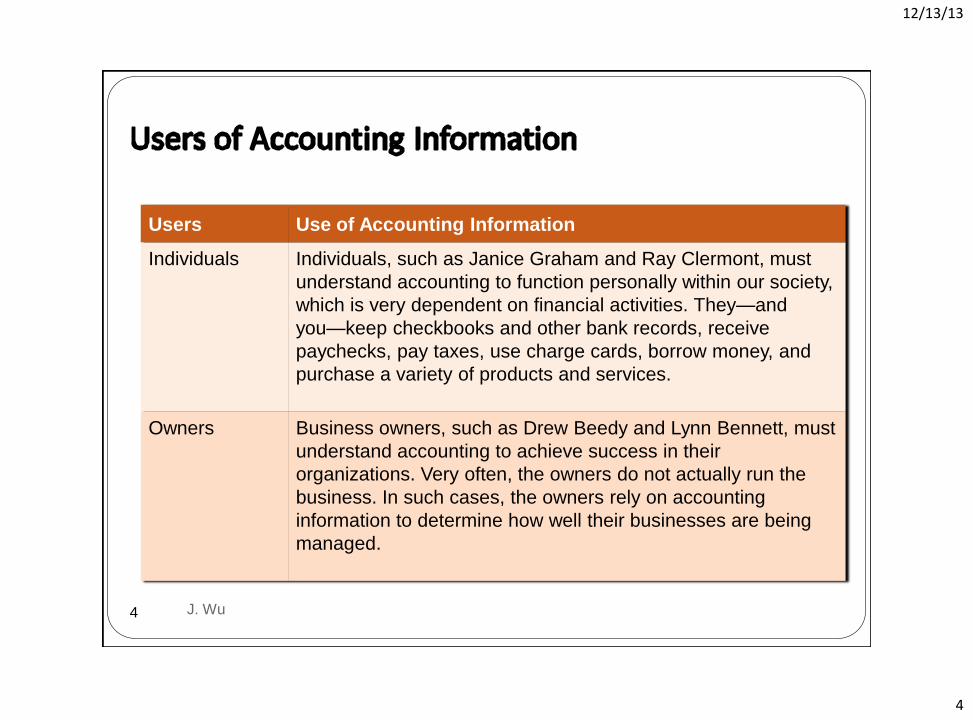

Users Use of Accounting Information

Individuals Individuals, such as Janice Graham and Ray Clermont, must

understand accounting to function personally within our society,

which is very dependent on financial activities. They—and

you—keep checkbooks and other bank records, receive

paychecks, pay taxes, use charge cards, borrow money, and

purchase a variety of products and services.

Owners Business owners, such as Drew Beedy and Lynn Bennett, must

understand accounting to achieve success in their

organizations. Very often, the owners do not actually run the

business. In such cases, the owners rely on accounting

information to determine how well their businesses are being

managed.

12/13/13

5

J. Wu 5

Users Use of Accounting Information

Managers Managers use accounting data extensively in deciding on

alternatives, such as what to sell, how to price, and when to

expand the product line.

Investors Investors use accounting data for insights on the financial

condition of potential investments when deciding whether to

invest in a business.

Banks and

other lending

institutions

Lenders, such as banks, use accounting data in deciding

whether to approve a loan.

12/13/13

6

J. Wu 6

Users Use of Accounting Information

Governments Governmental units (federal, state, and local) also record,

summarize, analyze, and interpret financial events to operate

with limited resources.

Tax authorities Tax authorities use accounting data reported to the government

in deciding whether a business is complying with tax rules and

regulations. Since our country has an extensive taxing system,

this is a major use of accounting data.

12/13/13

7

• Sole

Proprietorship

A business

owned by one

person

• Partnership

A business co-

owned by two

or more

persons

J. Wu 7

12/13/13

8

• Corporation

•A business that is owned by investors called •stockholders

• Limited Liability Company (LLC)

•A business that combines features of a corporation •and those of proprietorships and partnerships

J. Wu 8

12/13/13

9

• Service Business

Performs services for customers to earn a profit

• Merchandising Business

Purchases goods produced by others and then sells these goods to customers

• Manufacturing Business

Produces a product to sell to its customers

J. Wu 9

12/13/13

10

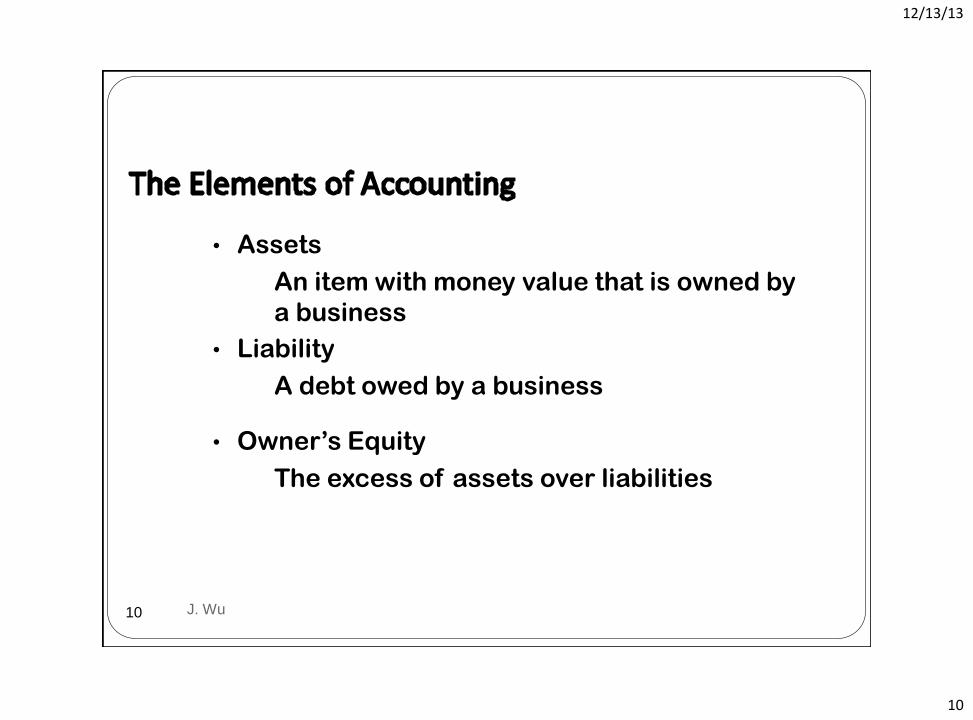

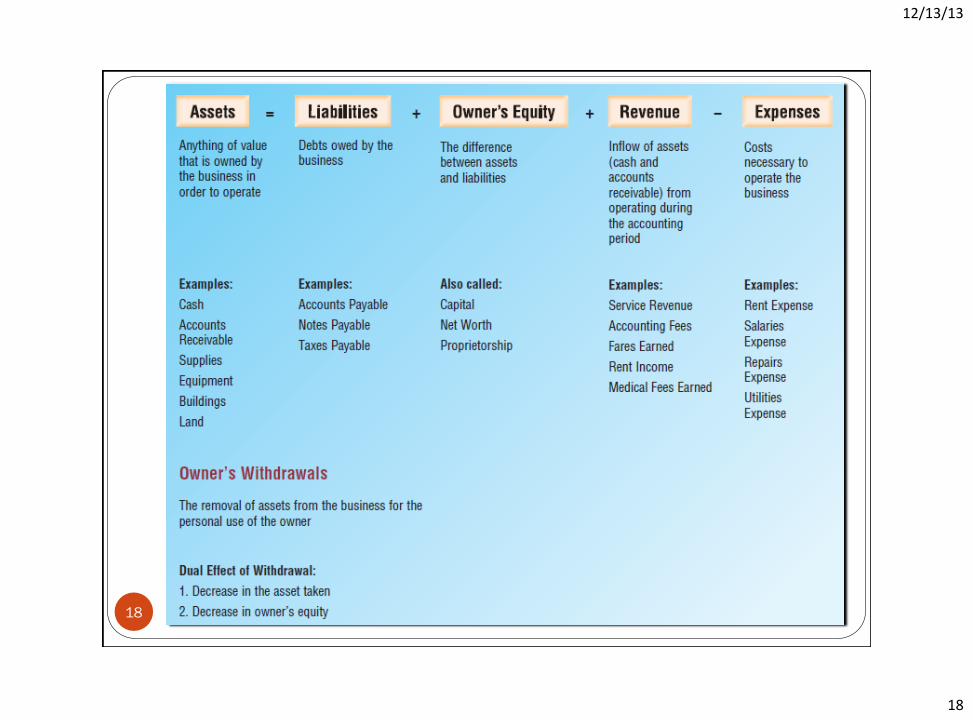

• Assets

An item with money value that is owned by

a business

• Liability

A debt owed by a business

• Owner’s Equity

The excess of assets over liabilities

J. Wu 10

12/13/13

11

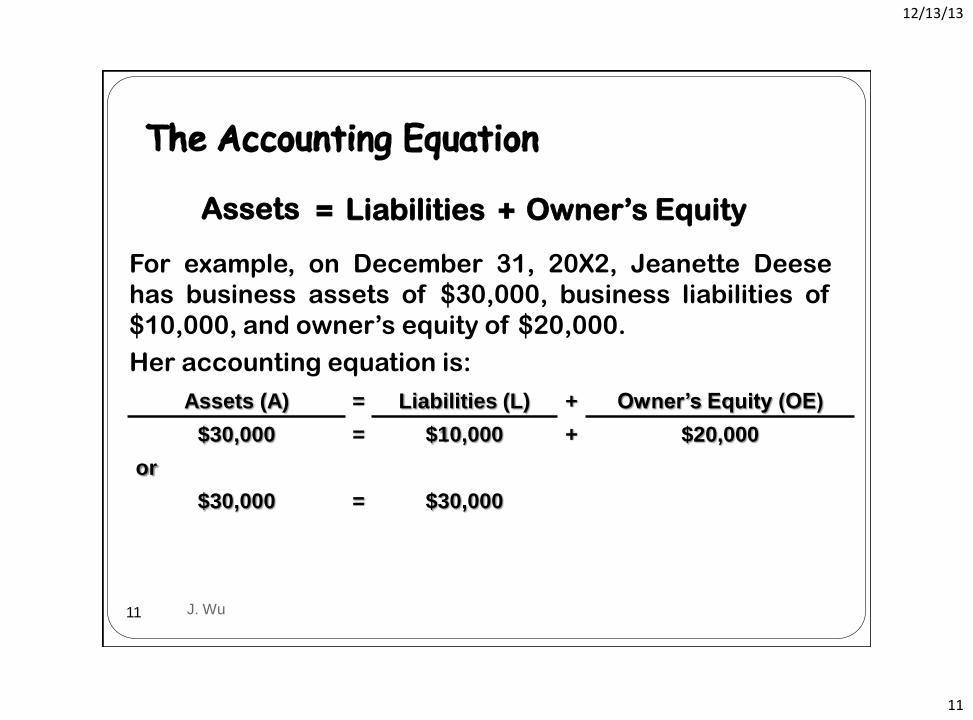

For example, on December 31, 20X2, Jeanette Deese

has business assets of $30,000, business liabilities of

$10,000, and owner’s equity of $20,000.

Her accounting equation is:

J. Wu 11

Assets (A) = Liabilities (L) + Owner’s Equity (OE)

$30,000 = $10,000 + $20,000

or

$30,000 = $30,000

Assets = Liabilities + Owner’s Equity

12/13/13

12

Any activity that changes the value of a firm’s assets, liabilities, or owner’s equity is called a transaction.

Purchase of equipment on credit

Cash payment to a creditor

Receipt of cash for services rendered to a customer

Purchase of supplies for cash

Payment of rent for the month

Payment of utility bill

Receipt of a bill to be paid later

Payment to employees for the payroll

Owner investment of cash in the business J. Wu 12

12/13/13

13

i. Total assets must always equal liabilities plus

owner’s equity.

ii. To maintain this balance, transactions are recorded

as having a dual effect on the basic accounting

elements.

iii. Every business transaction has at least two effects

on the accounting equation.

J. Wu 13

12/13/13

14

• Owner investments increase owner’s equity.

• Revenue increases owner’s equity.

• Expenses decrease owner’s equity.

• Owner withdrawals decrease owner’s equity.

J. Wu 14

12/13/13

15

• Summaries of financial activities • Used to communicate important accounting information to

users • Income Statement

A summary of a business’s revenue and expenses for a specific period of time, such as a month or year

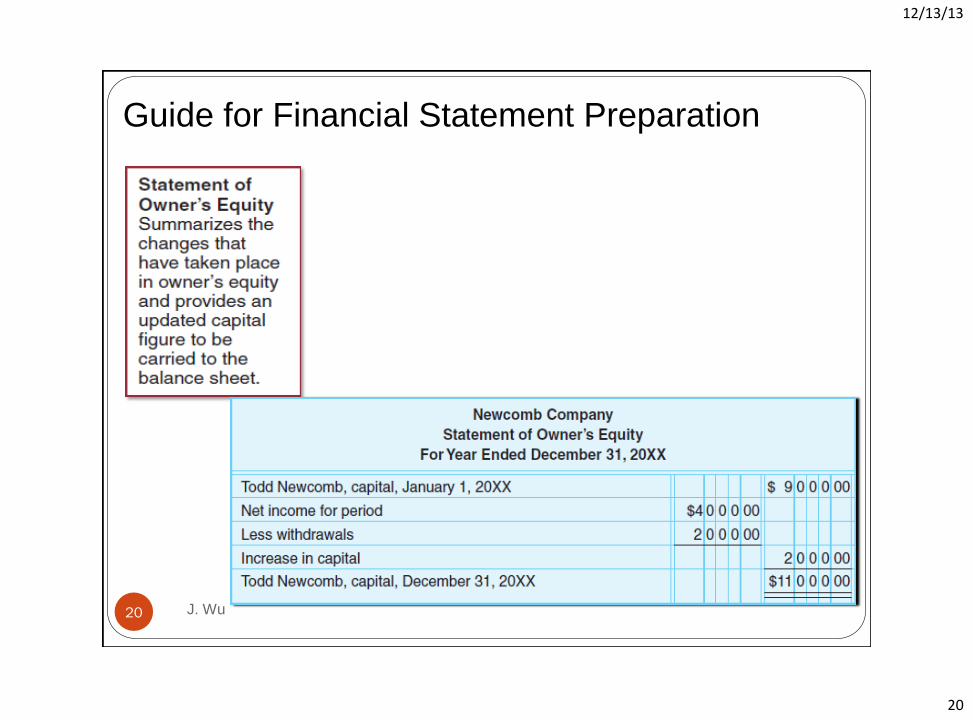

• Statement of Owner’s Equity A summary of the changes that have occurred in owner’s equity during a specific period of time

• Balance Sheet A listing of a firm’s assets, liabilities, and owner’s equity at a specific point in time

J. Wu 15

12/13/13

16

• Income Statement

• Prepared first

• To determine a firm’s net income

• Net Income

• Is shown on the statement of owner’s

equity

• Part of determining ending owner’s equity

• Ending Owner’s Equity

• Shown on the balance sheet

J. Wu 16

12/13/13

17

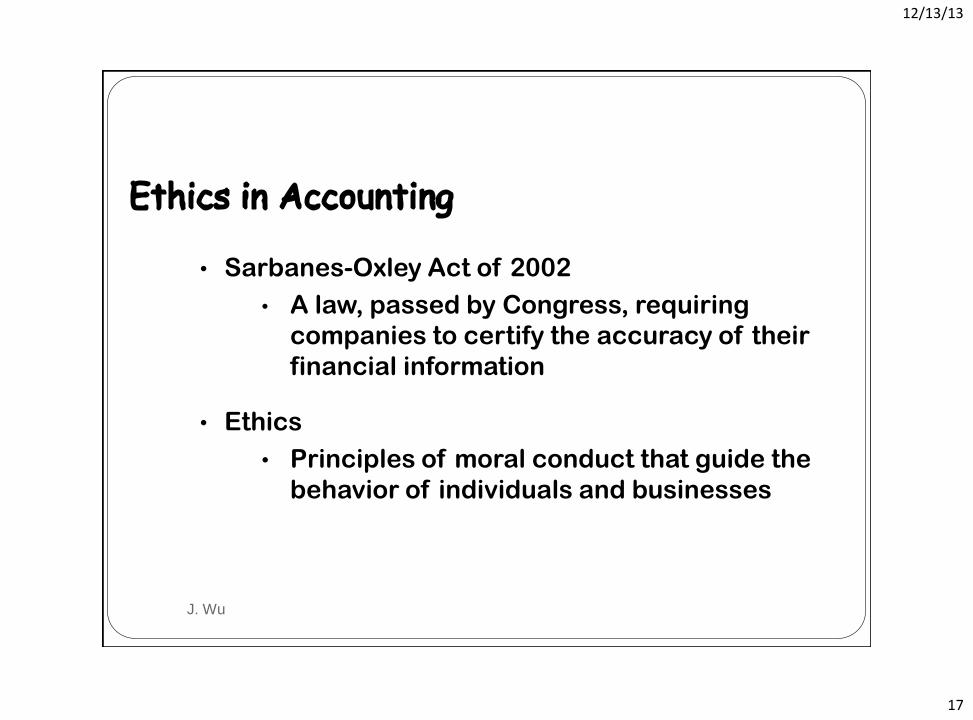

• Sarbanes-Oxley Act of 2002

• A law, passed by Congress, requiring

companies to certify the accuracy of their

financial information

• Ethics

• Principles of moral conduct that guide the

behavior of individuals and businesses

J. Wu 17

12/13/13

18

J. Wu 18

12/13/13

19

J. Wu 19

Guide for Financial Statement Preparation

12/13/13

20

J. Wu 20

Guide for Financial Statement Preparation

12/13/13

21

J. Wu 21

Guide for Financial Statement Preparation