ch22_liquidity_mngmt_efs_e3.ppt

TRANSCRIPT

© Prentice Hall, 2004

2222

Corporate Financial Management 3e

Emery Finnerty Stowe

Liquidity Management

Working Capital Management

Working capital = current assets – current liabilities

Working capital management refers to choosing the levels and mix of: cash, marketable securities, receivables and

inventories. different types of short-term financing.

Considerations in Working Capital Management

Sales impact

Liquidity

Relations with stakeholders suppliers customers

Short-term financing mix profitability risk considerations

Working Capital Management

Maturity matching approach

Conservative approach

Aggressive approach

Maturity Matching Approach

Hedge risk by matching the maturities of assets and liabilities.

Permanent current assets are financed with long-term financing, while temporary current assets are financed with short-term financing.

There are no excess funds.

Maturity Matching Approach

Temporary Current Assets

Time

$

Permanent Current Assets

Fixed AssetsLong Term

Financing

Short Term Financing

Conservative Approach

Long-term funds are used to finance both permanent as well as some temporary short-term assets.

When there are excess funds, they are invested in marketable securities.

Conservative Approach

Temporary Current Assets

Time

$

Permanent Current Assets

Fixed Assets

Marketable securitiesLong Term

Financing

Short Term Financing

Aggressive Approach

Use less long-term and more short-term financing than the conservative approach.

Aggressive Approach

Temporary Current Assets

Time

$

Permanent Current Assets

Fixed Assets Long Term

Financing

Short Term Financing

Cost and Risk Considerations

Yield curve is usually upward sloping.

Short-term rates are more volatile than long-term rates.

Firm's ability to obtain needed short-term financing.

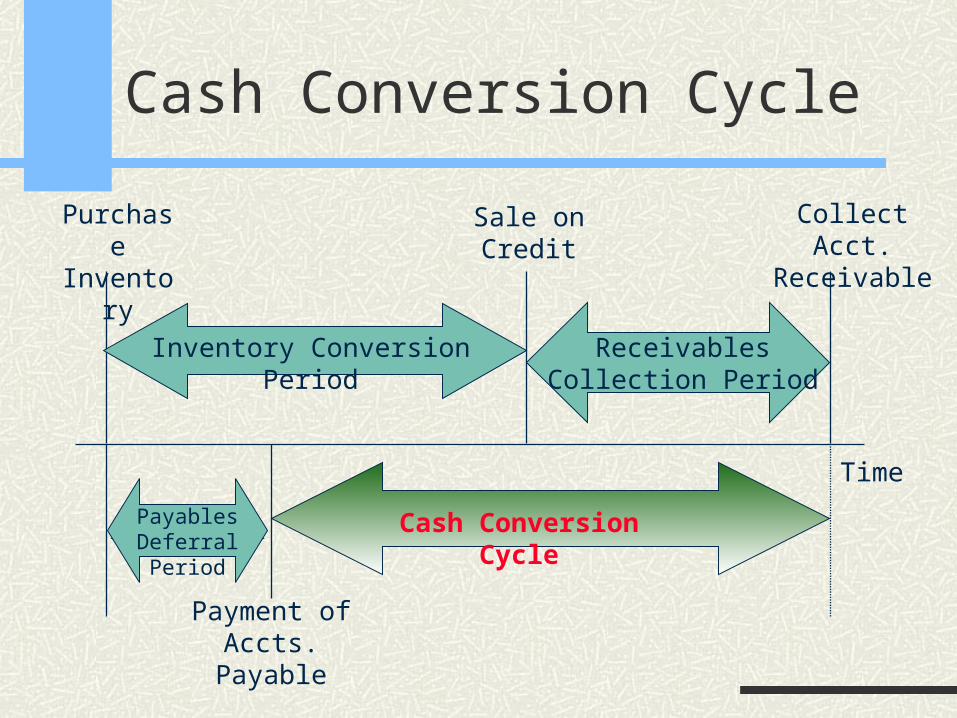

Cash Conversion Cycle

The cash conversion cycle is the length of time between payment of accounts payable and the receipt of cash from accounts receivable.

Cash Conversion Cycle

Purchase Inventory

Sale on Credit

Collect Acct. Receivable

Payment of Accts. Payable

Inventory Conversion Period

Cash Conversion Cycle

Time

Payables Deferral Period

Receivables Collection Period

Cash Conversion Cycle

period

deferral

Payables

period

collection

sReceivable

period

conversion

Inventory

cycle

conversion

Cash

Inventory Conversion Period

The inventory conversion period is the length of time from the purchase of inventory to the time the sales are made on credit.

turnoverInventory

365

Sales/365 ofCost

Inventory

period

conversion

Inventory

Receivables Collection Period

The receivables collection period is the average number of days it takes to collect on accounts receivable. Equal to days sales outstanding (DSO)

turnoversReceivable

365

Sales/365

sReceivable

period

collection

sReceivable

Payables Deferral Period

The payables deferral period is the average length of time between the purchase of materials and labor and the payment of cash for the same.

365expenses)/ tiveadministra and general Selling,sales of(Cost

payable taxespayroll benefits,Wages,payable Accounts

period

deferral

Payables

Cash Conversion Cycle

Given the following information about Vision Opticals, compute the firm’s cash conversion cycle.

InventoryAccounts ReceivableAccounts PayableWages, Benefits, Payroll Taxes

SalesCost of SalesSelling & Other Expenses

$19,000$21,000

$5,600$9,000

$227,000$93,000$22,000

Inventory Conversion Period

turnoverInventory

365

Sales/365 ofCost

Inventory

period

conversion

Inventory

days 74.575$93,000/36

$19,000

period

conversion

Inventory

Receivables Collection Period

turnoversReceivable

365

Sales/365

sReceivable

period

collection

sReceivable

days 77.3365$227,000/3

$21,000

period

collection

sReceivable

Payables Deferral Period

days 34.46365/)000,22$000,93($

000,9$600,5$

365expenses)/ tiveadministra and general Selling,sales of(Cost

payable taxespayroll benefits,Wages,payable Accounts

period

deferral

Payables

Cash Conversion Cycle

period

deferral

Payables

period

collection

sReceivable

period

conversion

Inventory

cycle

conversion

Cash

days 34.46days 77.33days 57.74

cycle

conversion

Cash

days 62

Cash Management

How much liquidity (cash plus marketable securities) should the firm have?

What should be the relative proportions of cash and marketable securities?

Demands for Cash

Transactions demand

Precautionary demand

Speculative demand

Compensating balances

Short-Term Investment Alternatives

U.S. Treasury securities T-bills, T-notes, and T-bonds

U.S. federal agency securities

Negotiable certificates of deposit

Short-term tax-exempt municipals

Bankers acceptances

Commercial paper

Preferred stock & money market preferred stock

Other Factors in Cash Management

Compensating balance requirements

Optimal amount of marketable securities transaction costs maturity risk yield

Special tax situations

Float

Float is the difference between the available (or collected) balance at the bank and the firm’s book or ledger balance.

Disbursement float occurs when the firm writes a check but the check has not yet cleared the banking system.

Collection float occurs when a check has been deposited but the funds are not yet credited to the firm’s bank account.

Float Management Techniques

Wire transfers

Zero balance accounts (ZBAs)

Controlled disbursing

Centralized processing of payables

Lockboxes

Lockbox Systems

Discount Music Stores is evaluating a lockbox system which will reduce float by 3 days. The lockbox system costs $15,000 per year. The firm’s daily collections average $150,000, and its opportunity cost of funds is 6% per year.

Should the firm utilize this lockbox system?

Lockbox Systems

Funds freed up due to a reduction in float = (3 days)($150,000 per day) or $450,000.

Annual value of float reduction = $450,000(6%) = $27,000.

After deducting the $15,000 cost of the lockbox system, the firm nets $12,000 before taxes.

Short-Term Financing

Trade Credit

Secured and Unsecured Bank Loans

Commercial Paper

Cost of Trade Credit

Discount Music Stores buys its inventory on “3/10, net 30” terms. What is the cost of not taking the discount?

0 10 30

+$970,000 –$1,000,000

Suppose DMS buys $1,000,000 worth of inventory; if they forgo the 3% discount to pay on day 30 they are borrowing $970,000 for 20 days and paying $30,000 interest:

Cost of Trade Credit: APY vs. APR

1%Discount %100

%Discount 1

PeriodDiscount Period Total

365

APY

PeriodDiscount -Period Total

365

%Discount %100

%Discount APR

Cost of Trade Credit: APR

0 10 30

+$970,000 –$1,000,000

days 20

365

000,970$

$30,000APR

%44.56APR

Cost of Trade Credit: APY

36520)1(

000,000,1$000,970$

r

970$

000,1$)1( 36520 r

%35.747435.01970$

000,1$ 20

365

r

0 10 30

+$970,000 –$1,000,000

Effective Use of Trade Credit

Advantages: Readily available Informal Flexible Stretching payments

Disadvantages High cost of discounts foregone Stretching of payments can hurt reputation

Bank Loans

Short-term unsecured loans Transaction loan Line of credit Revolving credit agreement

Term loans Bullet maturity Balloon payment

Cost of Bank Loans

Prime rate + “spread”

LIBOR + “spread”

Compensating balances

Compensating Balance Requirements

Let P = amount of loan f = loan term r = interest rate on loan B = incremental cash balance as a result of

compensating balance requirements y = interest earned (if any) on compensating balances

Interest charges = rPf

Interest received = yBf

Compensating Balance Requirements

f-

-APR

1

balance ngcompensati amount Loan

receivedInterest chargesInterest

fBP

yBfrPf 1

Compensating Balance Requirements

Custom Controls is considering a 1-year loan of $150,000 at an interest rate of 14%. Due to compensating balance requirements, Custom Controls will have to maintain a deposit balance of $20,000 which it would not have otherwise maintained at the lending bank. The deposit will earn 6% per year.

What is the APR of this loan?

Compensating Balance Requirements

Without the 6% yield on the compensating balance, the APR = 16.15%

fBP

yBfrPfAPR

1

1

1

000,20$000,150$

000,20$06.0000,150$14.0APR

= 15.23%

Discount Loans

The interest charge is deducted in advance for discount loans.

Let r = interest rate on the loan

f = the term of the loan

P = the principal amount

The APR of a discount loan is given by:

fr

r

frPfP

rPfAPR

1

1

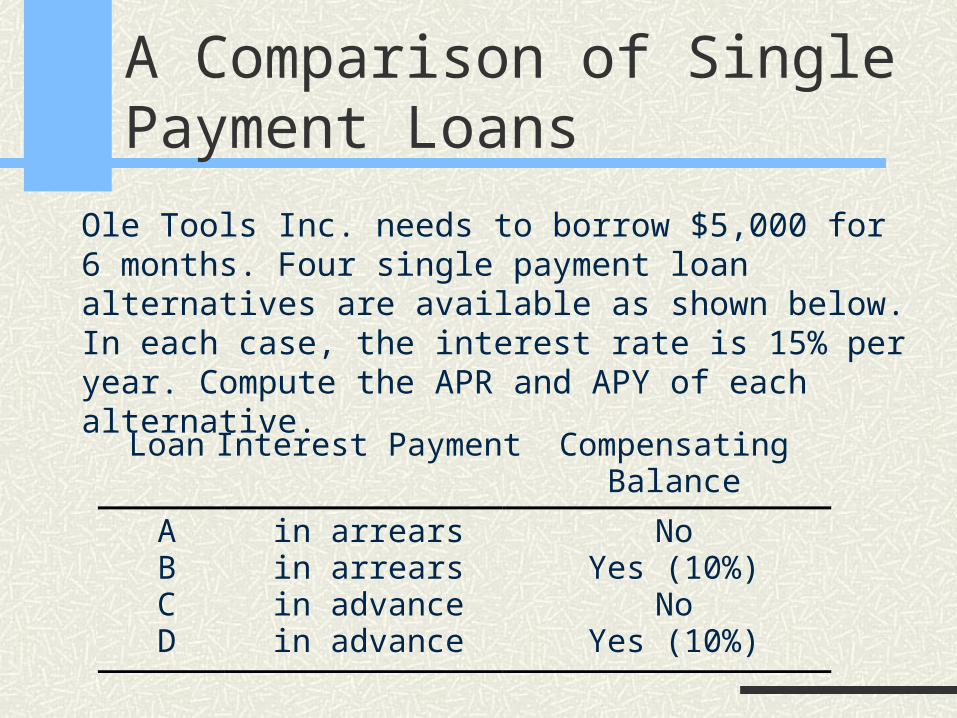

A Comparison of Single Payment Loans

Ole Tools Inc. needs to borrow $5,000 for 6 months. Four single payment loan alternatives are available as shown below. In each case, the interest rate is 15% per year. Compute the APR and APY of each alternative.

Loan Interest Payment CompensatingBalance

ABCD

in arrearsin arrears

in advancein advance

NoYes (10%)

NoYes (10%)

A Comparison of Single Payment Loans

Interest charge on the loan is $5,000× (.15) ×(0.5 years) or $375.

For loans A & B, this amount is added to the repayment at loan maturity.

For discount loans (loans C & D), this amount is deducted from the loan amount at loan initiation.

Compensating balances (for loans B & D), is $5,000×0.10 = $500.

A Comparison of Single Payment Loans

A

B

C

D

$5,000

$4,500

$4,625

$4,125

($5,375)

($4,875)

($5,000)

($4,500)

%22.165.

1

625,4$

375$

APR

Loan CF0 CF1 APR

%155.

1

000,5$

375

APR

%67.165.

1

500,4$

375

APR

%18.185.

1

125,4$

375$

APR

A Comparison of Single Payment Loans

A

B

C

D

$5,000

$4,500

$4,625

$4,125

($5,375)

($4,875)

($5,000)

($4,500)

Loan CF0 CF1 APR

15.00%

16.67%

16.22%

18.18%

APY

15.56%

17.36%

16.87%

19.01%

1000,5$

375,5$2

1500,4$

875,4$2

1625,4$

000,5$2

1125,4$

500,4$2

Discounted Installment Loans

Sheridan Systems borrows $12,000 for 3 months at 15%. The interest is paid in advance, and Sheridan will pay the loan in 3 monthly installments of $3,000 at the end of the first two months and $6,000 at the end of the third month.

Compute the APY and APR of this loan.

Discounted Installment Loans

The interest cost of this loan is ($12,000)(15%)(3/12 years) or $450.

Since the interest is deducted in advance, Sheridan will get $12,000 - $450 or $11,550 at loan initiation.

Discounted Installment Loans

0 1 3

–$6,000

32 )1(

000,6$

)1(

000,3$

1

000,3$550,11$

rrr

monthper %72.1r

2

–$3,000+$11,550 –$3,000

%6.200172.012 APR

%68.221)0172.1( 12 APY

Commercial Paper

Commercial paper is a negotiable business IOU note.

It is sold by the largest, most creditworthy firms on a discount basis.

Maturity is set to less than 270 days. Registration with the SEC is not required.

40% of commercial paper is sold through dealers. Commission of about 0.125% on an annualized basis.

Factors Affecting the Short-Term Financing Mix

Cost of each source of funds / incl’g options

Desired level of current assets

Seasonal component of current assets

Extent of maturity-matching

Flotation costs

Restricted access to long-term capital

Bankruptcy costs

Firm's choice of risk level