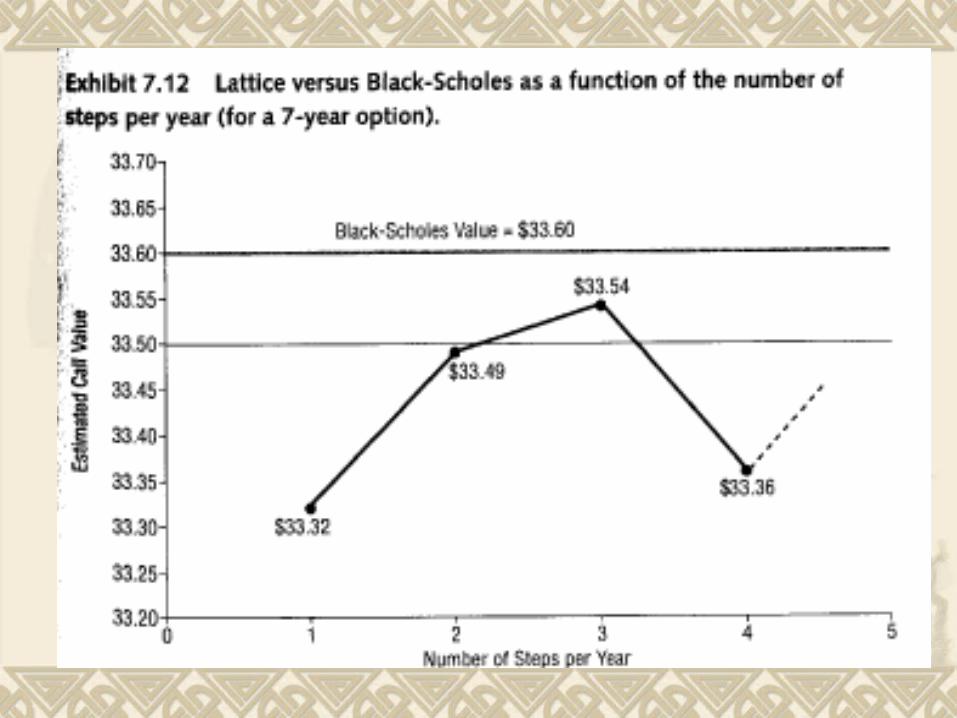

chap 7 going from one step per time period to many

TRANSCRIPT

Chap 7

Going from One Step Per Time Period to

Many

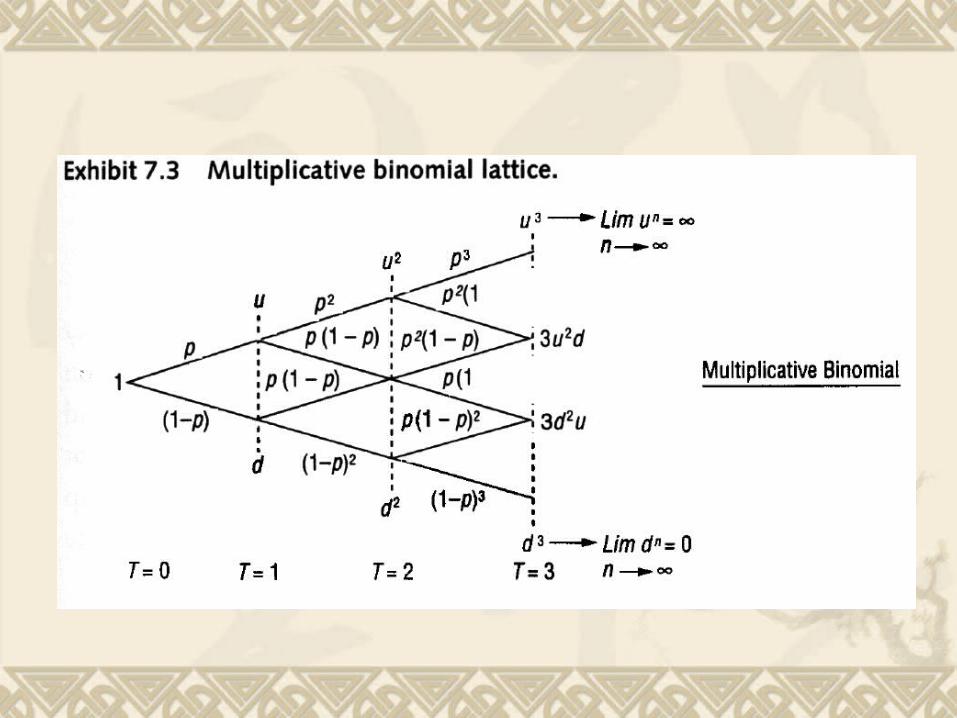

Pascal’s triangle – a building block( )E T n Tp

( , ) (1 )VAR n T p Tp p

Starting value is positive

du

drp f

)1(

du

rup f

)1(1

[ 1 ] (1 )u uu ud fC pC p C r

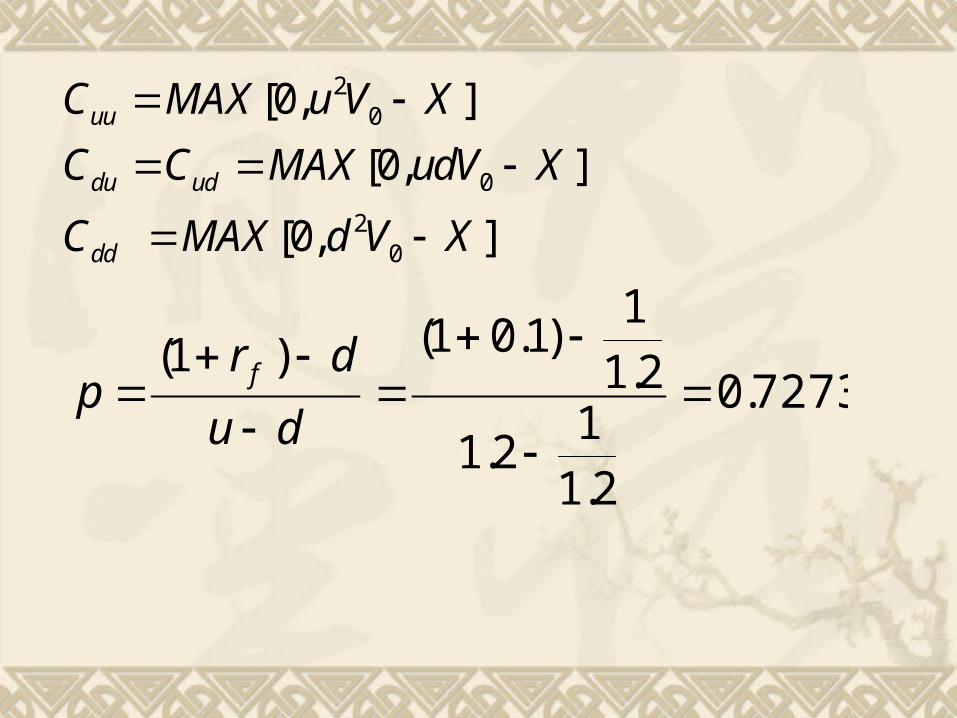

Assuming that V0 = $20, that u = 1.2, that X = $21, and that the risk-free rate equals 10 percent.

[ 1 ] (1 )u uu ud fC pC p C r

1 1 d ud dd fC pC p C r 0 1 1 u d fC pC p C r

2 20

2

[ (1 ) (1 ) (1 ) ]

(1 )

uu ud du dd

f

C p C p p C p pC p C

r

20

0

20

[0, ]

[0, ]

[0, ]

uu

du ud

dd

C MAX u V X

C C MAX udV X

C MAX d V X

7273.0

2.1

12.1

2.1

1)1.01()1(

du

drp f

2

0 2

1 0.2727

0.7273 (7.80)$3.41

1.1

p

C

0[0, ]

!( , ) (1 )

( )! !

n T n

n T n

MAX u d V X

TB n T p p p

T n n

-0 0

0

!(1 ) [0, ]

( )! !

(1 )

Tn T n n T n

n

Tf

TC p p MAX u d V X

T n n

r

0 0

!(1 ) [ ]

( )! !

(1 )

Tn T n n T n

n a

Tf

TC p p u d V X

T n n

r

All of the states of nature where n< a have zero payoffs because the call option will not be exercised.

-

0 0

!(1 )

( )! ! (1 )

!(1 ) (1 )

( )! !

n T nTn T n

Tn a f

TT n T n

fn a

T u dC V p p

T n n r

TX r p p

T n n

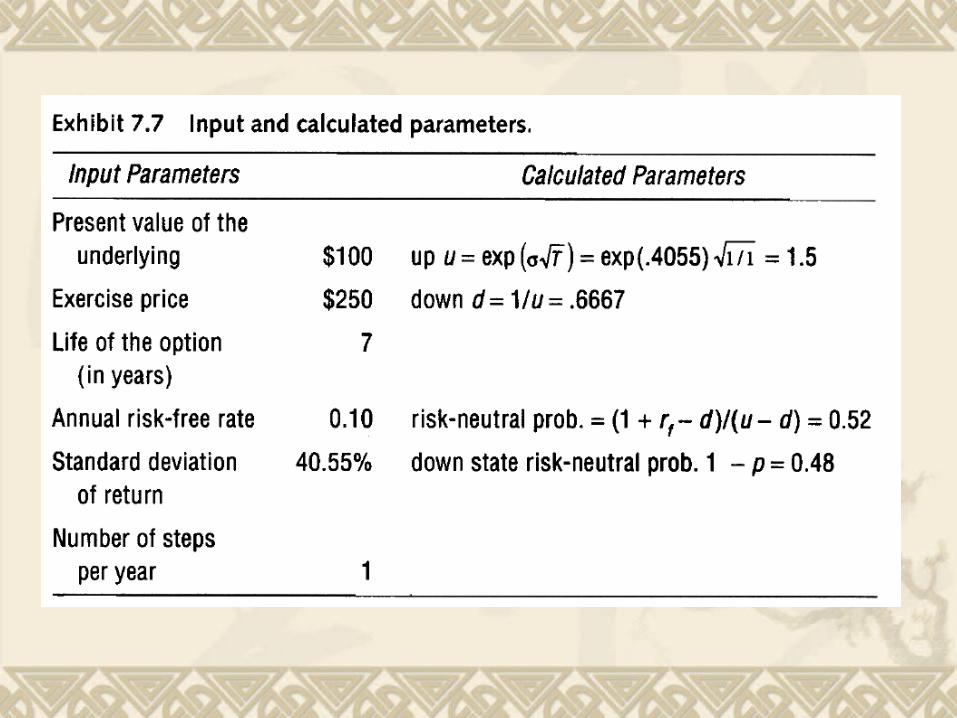

V0 equal $100, let u = 1.5 (i.e.,150% per year), the exercise price be $250, the life of the option be seven periods, and the annual risk-free rate equal 10 percent, we have the parameters of Exhibit7.6.

There are eight end states. The number of up movements ranges from zero to

seven. Given an exercise price of $250, the option is in the

money only for the three uppermost states where n, the number of up movements, is 5,6, or 7.

Therefore, the value of the border state, state a, is 5. The risk-neutral probability is p = (1.1-0.667)/(1.5-

0.667) = 0.52.

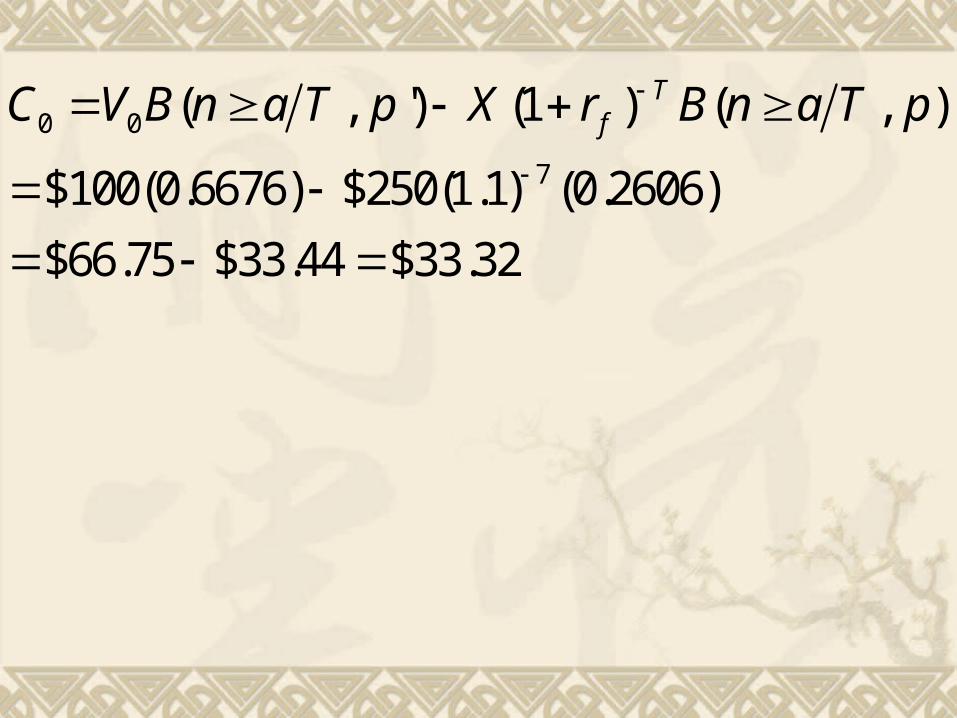

7(1 ) ( , ) 250(1.10) (0.260668) $33.44TfX r B n a T p

pr

up

f

)1('

)1()1(

'1 pr

dp

f

(1 )(1 )

(1 ) ( ') (1 ')(1 ) (1 )

n T nn T n

Tf

n T n

n T n

f f

u dp p

r

u dp p p p

r r

0 0 ( , ') (1 ) ( , )TfC V B n a T p X r B n a T p

du

drp f

)1(

pr

up

f

1'

7091.052.01.1

5.1

1'

p

r

up

f

2909.0)52.01(1.1

667.0)1(

1'1

p

r

dp

f

0 0

7

( , ') (1 ) ( , )

$100(0.6676) $250(1.1) (0.2606)

$66.75 $33.44 $33.32

TfC V B n a T p X r B n a T p

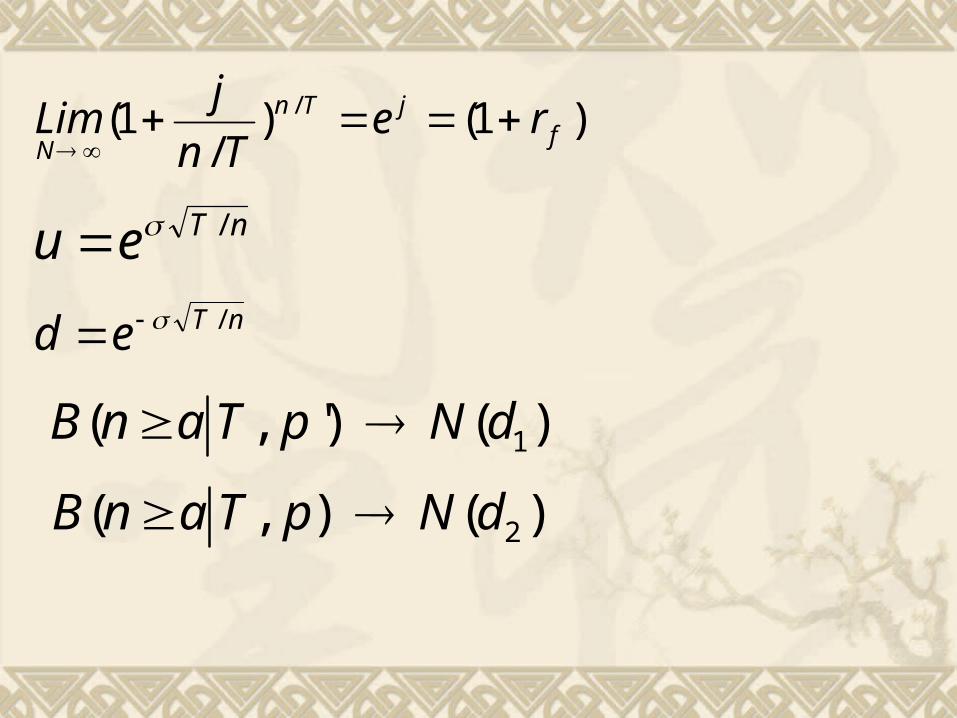

The limit of the binomial option pricing model is the Black-Scholes formula

0 0 ( , ') (1 ) ( , )TfC V B n a T p X r B n a T p

du

drp f

)1(

pr

up

f

1'

)1()/

1( /f

jTn

Nre

Tn

jLim

nTeu /nTed /

1( , ') ( )B n a T p N d

2( , ) ( )B n a T p N d

7

7)ln(

n

Tu

nTeu /

4055.0)5.1ln()ln( uj

f er 1

ln(1.1)

0.0953

j

j

TT

TrX

V

df

2

1ln

1

100ln 0.0953(7)

12500.4055 7

20.4055 70.9163 0.6672

0.5(0.53638)0.4055(2.646)

0.24910.53638 0.3042

1.0728

1( ) 0.5 0.1195 0.6195N d

2 1 0.3042 0.4055 7 0.7686d d T

2( ) 0.5 0.27894 0.22106N d

0 1 2

0.0953(7)

( ) ( )

100(0.6195) 250 (0.22106)

61.95 250(0.5132)(0.22106)

61.95 28.36 33.59

jTC VN d Xe N d

e

Step 1 defines the uppermost ending branch of the tree, the first of two seed cells.

Step 2 copies this cell down column I from cell I32 to cell I39.

Step 3 is the coding of the first cell, B32 as the value of the option if exercised.

Step 4 is to copy the cell across the first row up to but not including the last column (up to cell I31)

Step 5 defines a second seed cell, C33. It is coded as an “if statement.”

33 ( 12 "", "", (( 13 - $ $24),

(($ $26* 33 $ $27* 34) / $ $24))

C IF B MAX C D

I D I D I

($ $26* 33 $ $27* 34) / $ $24

0.51998(21.56) 0.48001(2.07)

1.111.09

I D I D I

Step 6 copies cell C33 across the columns up to

and including cell H33