chapter 1 introduction - welcome to edwards school … painter/businessplans... · web viewchapter...

TRANSCRIPT

Sinochem Feasibility Study

Chapter 1: Introduction1.1 Background

This report constitutes a feasibility study for Sinochem1 to evaluate a fertilizer investment

opportunity in south east China. The hypothetical acquisition is between two companies:

Sinochem Group-China largest fertilizer company and ABC Fertilizer Company2- a mid-sized

fertilizer company which is located in Fujian Province of China. In 2001, ABC Company

proposed with Sinochem to use their one fertilizer production line as the capital to build a joint

venture (JV).

The feasibility study is based on the 200,000 tons/year synthetic fertilizer equipment which

ABC Company has completed the construction in year 2000. The product is a kind of granulated

compound fertilizer which contains essential nutrient for plant to grow. These nutrients include

Nitrogen, Phosphate and Potash (this kind of compound fertilizer is also named as NPK

fertilizer).3

After bilateral negotiations, Sinochem and ABC Company have signed a Letter of Intent in

2002 which includes the main principles for the future JV. A confidentiality clause was also

included. The letter pledged to exchange each party's commercial data for non-third party usage.

In 2002, the Investment Department of Sinochem Fertilizer Company had not enough

human resource to handle this project at that time; thus Sinochem had to temporary halt the

feasibility research of that project. In Dec 2003, Changfeng Liu--employee from Sinochem

Investment Department, now is assigned to U of S to study the one year MBA program--

contacted to Sinochem and ABC Company to express the willing to work on this project. Both of

them were pleased and agreed the request.

1 See more information about Sinochem at page 22 See more information about ABC company at page 43 See Figure A in Appendix 1

Changfeng Liu College of Commerce, University of Saskatchewan 1

Sinochem Feasibility Study

1.2 Parties Introduction

1.2.1 Sinochem Group

Sinochem Group, ranking among Fortune Global 500 companies for 14 consecutive years,

is one of the national foreign trade companies established immediately after the founding of P.R.

China, and has been ranked on top of the list of China’s largest import and export enterprises for

many years. It was one of the earliest Chinese companies entering Fortune Global 500 and has

enjoyed a sound reputation in the international petrochemical industry.

Triggered by factors both inside and outside, Sinochem faced a pressing challenge like

many other foreign trade companies operating mainly as an import and export agent. To make

foreign trade enterprises operating in socialist market economy fundamentally, Sinochem has

made great efforts to push forward market-oriented strategy and implement management

improvement project since 1998. It continued to nurture market-oriented core competitiveness,

extend core businesses into downstream and upstream sectors both at home and abroad, and set

up three pillar businesses including energy, agricultural inputs and chemicals. Sinochem is

striving to transform from a foreign trade agent into a commodity and service provider, and

eventually into a comprehensive player in the industries.

By extending into upstream (capital investment on resource-based projects) and

downstream (set up own logistic centers and distribution channels), Sinochem has formed an

integrated industrial chain and maintained a leading position in import and export volume.

Sinochem has also implemented Enterprise Resource Plan System (ERP) and Distribution

Management System (DMS) among its headquarters and all subsidiaries since 2000.

For fertilizer business unit, while further strengthening the position as the major fertilizer

importer and distributor, Sinochem actively participates in the restructuring of national

phosphate resources. It has built up a production capacity of 2.5 million tons of phosphate and

NPK at home and abroad, making Sinochem the largest fertilizer manufacturer in China.

Moreover, Sinochem has established a fertilizer distribution network covering 14 major

agricultural provinces.

Changfeng Liu College of Commerce, University of Saskatchewan 2

Sinochem Feasibility Study

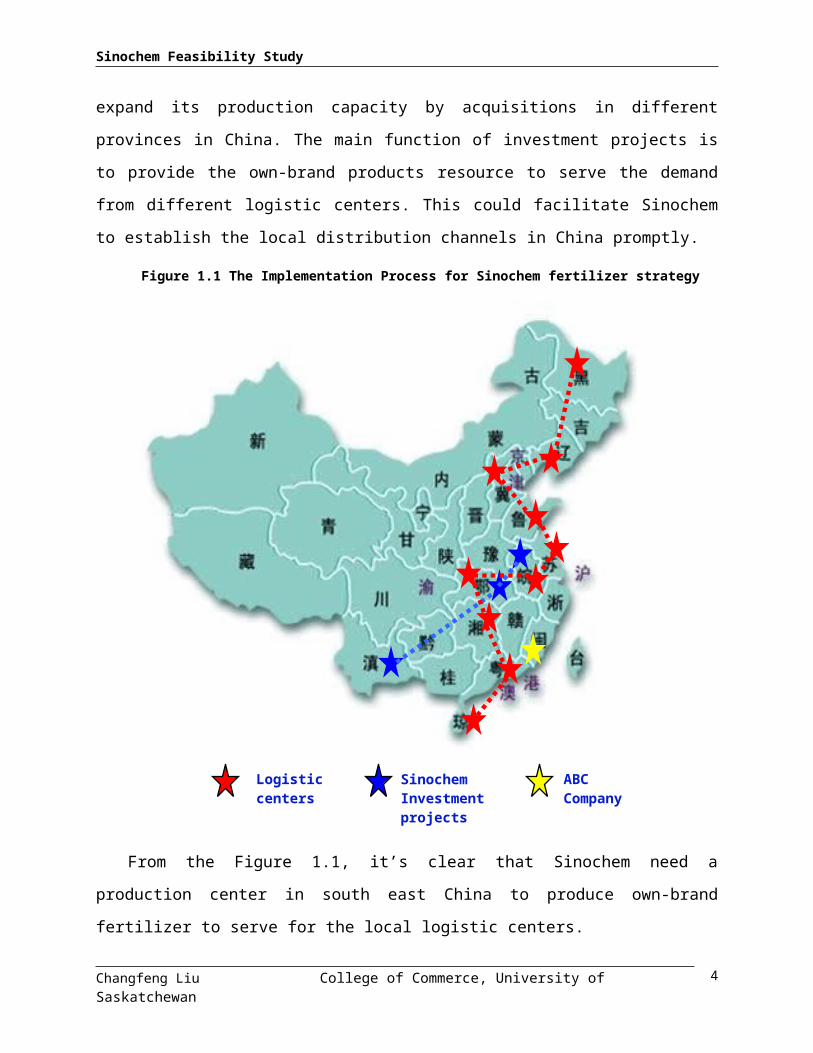

According to Sinochem’s five-year fertilizer strategy, the company wants to develop and

maintain as the largest phosphate and compound fertilizer producer and distributor in China.

Consequently, Sinochem is seeking the investment opportunities to expand its production

capacity by acquisitions in different provinces in China. The main function of investment

projects is to provide the own-brand products resource to serve the demand from different

logistic centers. This could facilitate Sinochem to establish the local distribution channels in

China promptly.

Figure 1.1 The Implementation Process for Sinochem fertilizer strategy

From the Figure 1.1, it’s clear that Sinochem need a production center in south east China to

produce own-brand fertilizer to serve for the local logistic centers.

Overall, Sinochem has four distinct strengths in fertilizer field:

Changfeng Liu College of Commerce, University of Saskatchewan

Logistic centers

Sinochem Investment projects

ABC Company

3

Sinochem Feasibility Study

Brand: Sinochem has developed and cultivated its brand over fifty years. Every year,

Sinochem sells over 6 million tons own-brand fertilizer to China market. The amount accounts

for around 60% of total China fertilizer market. Nearly 80% of them are imported from IMC,

Cargill, PCS and other main international fertilizer producers. Consequently, Sinochem’s brand

enjoys a high reputation among Chinese farmers.

Distribution network: From 1998 to 2003, Sinochem has set up 14 logistic centers in east

China. Over 200 distribution network were built to sell imported and domestic fertilizer to China

farmers.

Technical Human Resource: In 1989, Sinochem has invested a phosphate fertilizer

company (US-Agrichem) in Florida, U.S. with the capacity of 1.2 million ton per year. For 15

years, Sinochem has developed a technical expert’s team with rich operational experience which

could solve most of problems during fertilizer production.

Capital: For 5 consecutive years, Sinochem’s profit is around CAN$140 million. This

allows Sinochem has ability to implement investment activities freely.

1.2.2 ABC Fertilizer Company

ABC Fertilizer Company is the only middle-scale nitrogen and compound fertilizer

producer in Fujian Province, which is located in south-east China. The annual production

capacity is 170,000 metric tons (Mt) urea and 200,000 Mt compound fertilizers (NPK).4

From 1998 to 2000, the company inputted CANS$10 million to construct a new NPK

production line. But, the NPK line has only achieved 20% capacity because the workers could

not master the complicated technique. Also its own brand was not cognized by local market.

This leads continuous loss to ABC Company for three years. The management hoped to

cooperate with Sinochem eagerly by the NPK line to establish a JV to help them change current

urgent condition.

1.2.3 The Joint Venture (Sinochem-ABC limited Company)

The JV will be set up by Sinochem and ABC Company.

4 see Figure B in Appendix 1

Changfeng Liu College of Commerce, University of Saskatchewan 4

Sinochem Feasibility Study

ABC Company is supposed to use the total equity of the NPK production line and extra

cash as their capital. And Sinochem plan to use pure cash to invest. The amount of cash that

Sinochem would invest would meet the total demand of the projected cash meanwhile Sinochem

could be the larger shareholder for JV.5 The JV would undertake the¥41,570,000 debt of NPK

line from ABC Company.

The J-V’s equity structure is as followed:

Figure 1.2 JV Equity Structure

The JV plans to produce 200,000 Mt compound fertilizer annually after de-bottlenecking.

Sinochem authorized J-V to use “Sinochem” brand to its product. Fujian Province is the target

market which the NPK market is dominated by several foreign brands now. By leveraging

Sinochem’s logistic center and distribution network, the J-V plans to use local products to

substitute the foreign products in this market.

5 The equity structure is described in detail in Financial Plan.

Changfeng Liu College of Commerce, University of Saskatchewan

53% 47%The Joint Venture

Total equity47,000,000

5

Sinochem Group

Equity capital investment

Cash 25,000,000

ABC Fertilizer Company

Urea Production Line

NPK Production LineCapital equity 11,600,000Cash 10,400,000

Sinochem Feasibility Study

Chapter 2: Operations Plan2.1. Production Introduction

Most producers of compound fertilizers in world are producing nitrate based mineral

compound fertilizers under the product name "NPK". These products contain nitrogen in

ammoniacal (NH4) and nitrate (NO3) form, phosphorus expressed as P2O5, and normally also

potassium expressed as K2O.

The product name "NPK" is normally followed by three numbers to indicate the percent of

N, P2O5 and K2O which the product contains, e.g. 24–6–12 indicates that this particular grade

contains 24% N (nitrogen compounds), 6% P2O5 (phosphorus compounds) and 12% K2O

(potassium compounds). In addition, the fertilizer may contain magnesium, boron, sulphur,

micronutrients, etc. The typical content of nutrients (N + P2O5 + K2O) will normally be in the

range of 40-60%.

Fertilizer industry has developed over one hundred years. It’s also a kind of “setting sun”

industry, but it’s an essential industry for agriculture. Because the production techniques have

been developed into mature period, there isn’t too much significant new high-tech involved into

fertilizer production. Consequently, the efficiency and stability are the two main targets for

investors to choose the production techniques.

Nowadays, NPK fertilizers can be produced in four, basically different, ways:

Ammonium phosphate/ammonium nitrate-based NPK fertilizers

Nitrophosphate-based NPK fertilizers (mixed acid route)

Nitrophosphate-based NPK fertilizers (ODDA-route)

Mechanical blending of single or multi-nutrient components

The four processes are based on different technologies, having different investment costs,

economic impact, and energy consumptions. To save capital, this project did not invest in

phosphate rock refinery. Because the commercial phosphate acid is available in Yunnan province

which is about 1000km from the plant, it’s convenient to purchase phosphate acid outside instead

of producing by itself.

Changfeng Liu College of Commerce, University of Saskatchewan 6

Sinochem Feasibility Study

This compound fertilizer project is based on a mixed acid (phosphate acid and sulphur acid)

route with a capacity of 200,000 Mt/y of NPK. This production capacity makes it possible to

produce 660 t/d of NPK 15-15-15.

This plan describes the principles for production, pollution prevention and control and

defines achievable levels for waste and emissions to air and water for the existing NPK plants.

The plan does not give a detailed description of all the processes in operation.

Emission figures and production rates in a specific production unit will depend on the

product grade, but the grade selected for this feasibility study can be considered an average

grade: NPK grade (15–15–15 / N–P2O5–K2O).

In this project, there will be two kinds of products which grade as 15-15-15 (K2SO4 as a raw

material for potash) and 18-10-12 (KCI as a resource for potash), respectively. These two

products are designed for the different demands from grain farmers and fruit farmers according

to the local soil and plant condition. This report assumes each of the products has equal capacity.

In really case, the production would depend on the market demand.

2.2. Production Processes

The selection of the basic techniques is based on several factors:

Target product range (N/P/K ratio)

Raw material basis

Quality parameters

Flexibility of process

Size of production plant

Integration with other processes

Economic factors

There are three basic techniques for granulation:

Granulation with a pipe reactor system

Drum granulation with ammonization

Changfeng Liu College of Commerce, University of Saskatchewan 7

Sinochem Feasibility Study

Mixed acid process with phosphate rock digestion

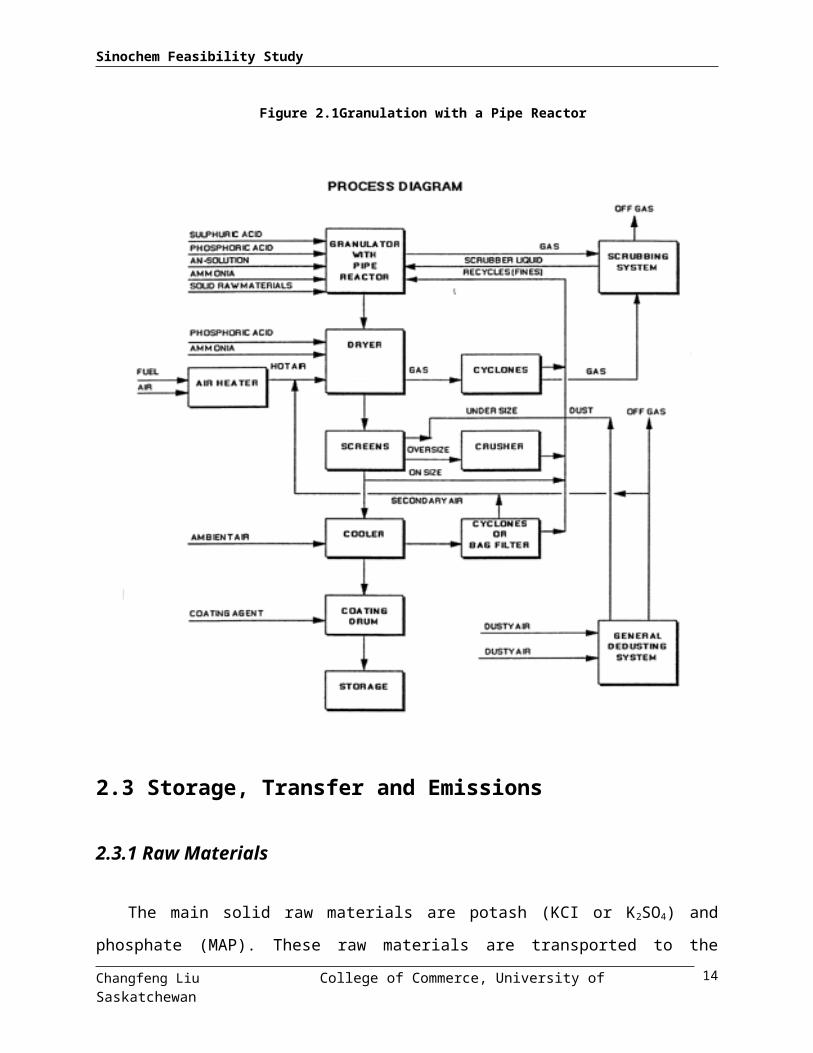

This project chooses the Granulation with a pipe reactor system as its technique in term of

its following characters:

Broad range of formulations

Direct neutralization of phosphoric and sulphuric acid in a pipe reactor

No phosphate rock digestion

Although high costs of raw materials (P2O5), it’s easy to purchase

Simple gas scrubbing

Low costs of labor and maintenance

Low cost of investment

The process works with a classical granulation loop but incorporates one pipe reactors. A

mixture of phosphoric and sulphuric acids (optional) is neutralized in the pipe reactors with

liquid ammonia. A wide range of grades, including ammonium phosphates, can be produced.

The process is flexible and easy to operate and the pipe reactors can be operated with a high turn-

down ratio.

2.2.1 Granulation and drying section

The required solid raw materials such as mono-ammonium phosphate (MAP), potassium

chloride (KCI), potassium sulphate (K2SO4), secondary nutrients, micronutrients and filler are

metered and fed into the granulator together with the recycle. The pipe reactor fitted in the

granulator is designed to receive phosphoric acid, part of the ammonia, and all other liquid feeds

such as sulphuric acid and recycled scrubber liquor.

Concentrated ammonium nitrate solution may be added directly into the granulator and

ammoniation rates in the pipe reactor vary according to the product. Further ammoniation may

be carried out in the granulator.

In the dryer The N/P mol ratio is 1.00 (essentially production of mono-ammonium

phosphate). The MAP produced consists of very fine particles and passes via the cyclones and

Changfeng Liu College of Commerce, University of Saskatchewan 8

Sinochem Feasibility Study

screens back to the granulation drum. The granules obtained are dried in a drying section using a

heated air stream.

2.2.2 Screening, crushing, cooling and coating

The dry granules are screened into three fractions. The over-size is removed and returned

via the crusher to the granulator, together with the fines. The product-sized fraction is removed

with the possibility of returning part of this fraction to the granulator to stabilize the recycle loop.

Finally the on-spec fraction is cooled in classical cooling equipment such as a fluidized bed

cooler. The cooled product is fed into a coating drum where a surface coating is applied to

prevent caking.

2.2.3 Gas scrubbing and dust removal

Gases from the granulator and the dryer are scrubbed in Venturi scrubbers with

recirculating ammonium phosphate or ammonium sulpho-phosphate solution. Make-up

phosphoric and sulphuric acid is added for pH control if necessary. The scrubber liquor which is

being recycled is fed to the pipe reactor in the granulator.

Finally, the gases are vented through cyclonic columns irrigated with an acidic solution.

The gases coming from the dryer are de-dusted in high efficiency cyclones to remove the

majority of the dust before scrubbing. The air coming from the cooling equipment is generally

recycled as secondary air to the dryer after de-dusting. General de-dusting equipment is installed

in the entire plant.

The layout of equipment is shown at the Appendix 1 as Figure C.

The main process steps are as followed:

Changfeng Liu College of Commerce, University of Saskatchewan 9

Sinochem Feasibility Study

Figure 2.1Granulation with a Pipe Reactor

2.3 Storage, Transfer and Emissions

2.3.1 Raw Materials

The main solid raw materials are potash (KCI or K2SO4) and phosphate (MAP). These raw

materials are transported to the production site by trains or trucks. They are tipped from wagons

and lorries into hoppers which feed the materials to conveyors. Belt conveyors are totally

Changfeng Liu College of Commerce, University of Saskatchewan 10

Sinochem Feasibility Study

enclosed in tunnels. Raw materials are stored in closed buildings or silos. Materials in storage are

handled by crane. The liquidized materials are H3PO4, Liquidized Urea and Liquidized ammonia.

H3PO4 will be stored into tanks and transferred to reactors. The other two would be transferred

directly to granulator by pipes from ABC Company’s storage tanks.

2.3.2 Products

Products are granulated fertilizers of different grades (the main product is 15-15-15, other

production of different grade products are determined by the demand of market). Belt conveyors

are placed in closed tunnels. Bulk storage is in closed buildings with walls to separate different

grades of product. Materials are handled by scraper. Fertilizers are hygroscopic and thus the

storage atmosphere is air-conditioned.

Fines and lumps must be screened out from the product after bulk storage for quality

reasons. The separated over- and under-sized material is recycled back to the NPK plant.

The entire final product is bagged in 50kg bags. Bagged products are normally stored under

cover.

2.3.3 Emissions

There is practically no emission to the environment from materials handling when this is

done correctly. There is no contaminated waste water and the only emission to air is the dust

collection air from the bagging plant and screening station. The average air volume through dust

filters is 4,000 Nm³.h-1 and the typical dust content after the filters is 30mg.Nm-3

2.4 Site plan

The production site has considered several factors:

Production flexibility

Production efficiency

Environmental impact

Changfeng Liu College of Commerce, University of Saskatchewan 11

Sinochem Feasibility Study

The NPK plant is adjacent to ABC Company’s urea plant where is located in Yong’an city,

Fujian Province. Therefore this could decrease the distance to transport liquidized ammonia and

urea from urea plant to NPK plant. Also, the inventory and final product building is near the

main highway. This could lower down the cost for transportation.

2.5 Supply Analysis6

N, P and K are three main materials for compounded fertilizer. Because Sinochem is the

only agent to sell imported potash, JV could get KCI and K2SO4 at a very competitive price.

ABC Company will offer urea and liquidized ammonia as the resource of N. In term of Yunnan

Province has the main phosphate rock storage in China, most of the NPK producers buy MAP

and H3PO4 from that province.

Table 2.1 Supply Analyses

Main Raw Material Price

(Per ton)

Annual Demand

(tons)

Buyer Seller

MAP

(N 10% -P2O5 50%)

132078 34100 JV Yunnan tri-circle phosphate company (by rail)

KCI (K2O 60%) 1100 60000 JV Sinochem fertilizer Co. (by rail)

K2SO4 (K2O 50%) 1460 40000 JV Sinochem fertilizer Co. (by rail)

Liquidized ammonia 1238 7320 JV ABC Company (by Pipes)

Liquidized urea

(N 46%)

940 44060 JV ABC Company (by Pipes)

H3PO4 (50%) 2780 13000 JV Yunnan tri-circle phosphate company (by rail tank)

H2SO4 (98%) (optional)

365 8160 JV Jiangxi Guixi Copper Co. (by rail tank)

6 All the currency in this feasibility study is RMB. The exchange ratio from CAN to RMB is around 6.1:1.7 All the Raw Material prices are before Value Added Tax (More introductions in Appendix 4 Financial Plan).8

Changfeng Liu College of Commerce, University of Saskatchewan 12

Sinochem Feasibility Study

2.6 Cost of Goods Manufactured

According to the nature of fertilizer manufacture, raw materials cover the most percentage

of cost for the final product. Traditional fertilizer plants are labor intensive. Because JV adapts

DCS system as its automatic production control system, the direct labor cost is rather low.

Consequently, direct materials account for 93.71% of total cost, while labor only has 0.71% for

final product.

Table 2.2 Cost of Goods Manufactured

NPK (K2SO4 based) NPK (KCI based) TotalPercenta

ge

Direct Materials¥122,348,1

00 Direct Materials¥95,168,47

6 ¥217,516,57

6 93.71%

Direct Labor Used ¥828,000 Direct Labor Used ¥828,000 ¥1,656,000 0.71%Manufacturing Overhead ¥6,474,976 Manufacturing Overhead ¥6,474,976 ¥12,949,952 5.58%Total Cost of Goods Manufactured

¥129,651,076

Total Cost of Goods Manufactured

¥102,471,452

¥232,122,528 100.00%

2.7 Capital Budget

2.7.1 Working Capital Plan

According to the <Letter of Intent>, Sinochem would invest ¥25,000,000 cash as well as

ABC invests ¥ 10,400,000 cash for JV. Meanwhile, the new company would borrow

¥20,000,000 from bank as short term liability. Therefore, the total increased cash for the JV is

¥55,400,000 at the beginning year.

After the JV sets up, the management would invest ¥8,604,700 into the construction of

new JV office building and NPK production De-bottlenecking. Consequently, the new long term

assets would be ¥61,774,700. The total working capital is ¥54,546,057 (See more detail on

Financial Plan).

Inventories

Changfeng Liu College of Commerce, University of Saskatchewan 13

Sinochem Feasibility Study

There are three kinds of inventories: raw materials, products under processing and final

products. To save cost, the final products are stored into bulk warehouse initially. When the

orders are coming, they are bagged and transported.

Figure 2.2 Average Collection Periods

10-45 days 5 days 45 days

Raw Material Processing Final Products

The total inventory periods are around 95 days.

Account Receivable

In nowadays China fertilizer market situation, credit policy only exists between companies

which had business each other over many years. Otherwise, the sellers only begin to transport

their products unless they have received buyers’ payment in advance. In this feasibility study, JV

will use 30 days as its average collection period, because most of their upstream and downstream

clients have been maintaining a good business relationship with Sinochem.

Average collection period: 30 days; recycle turnover: 360/30=12

Account receivable= total cost of sales/ recycle turnover

Account payable

Also, the average payment period is 30 days.

The total inventory, account receivable and account payable have been calculated in

Working Capital Plan.

2.7.2 Total Capital Cost

In the first year, the total capital costs will be ¥61,774,700. After the following years, JV

plan to input more money to maintains the equipments and increase the capacity. According to

Changfeng Liu College of Commerce, University of Saskatchewan 14

Sinochem Feasibility Study

the China Long term assets Depreciation Rules, the assets will be depreciated over twelve years.

The CCA rate is 8% and the salvage rate is 4%.

Table 2.3 Total Capital Cost

Description EstimatedCost ($)

Land (rental) ¥0Building Raw Material Warehouse ¥3,288,000 Products Warehouse ¥3,795,300 Bulk Warehouse ¥4,344,000 Main Production Building ¥8,723,000 Office Building ¥3,105,000 Landscaping ¥85,000 Total Cost ¥23,340,300Production Equipment: Pipe ¥740,000 Pipe Reactor ¥4,370,000 Screener ¥650,000 Pump ¥795,000 Storage Tanks ¥2,531,000 Granulator ¥3,127,000 Cooler ¥2,650,000 Bagging machine ¥400,000 Belt conveyer ¥2,120,000 Crusher ¥963,000 Dryer ¥2,542,400 Coating system ¥1,500,000 Tractor ¥1,382,000 Dust collector ¥870,000 Scrubber ¥1,204,000 Distributed Control System (DCS) ¥3,560,000 Design and Installation ¥8,580,000Office Equipment ¥450,000 Total Equipment Costs ¥38,434,400Total Capital Costs ¥61,774,700

Changfeng Liu College of Commerce, University of Saskatchewan 15

Sinochem Feasibility Study

2.8 Quality Control

From management perspective, total quality management (TQM) program and Activity

Based Management (ABM) is essential tools to help JV to improve product quality and decrease

cost in a shot time. In a long run, 6-Sigma program would set higher benchmark standard for

JV.

Because the location of plant site is near south sea, the Taiwan and south Asia markets

could be the promising target market for JV in future. Therefore, ISO registration ought to be

considered when the business is planning to export.

From a technique perspective, DCS system and de-bottlenecking plan are two crucial steps

for the new engineers to master the operation technique promptly

2.8.1 DCS system

To monitor and control day to day production, the NPK line has installed a new distributed

control system (DCS). DCS allows the plant to establish a common control room from which all

aspects of the production process could be monitored and controlled. Most of operation could be

done by computer. Thus, this decreased the probability of human mistake.

2.8.2 De-bottlenecking Plan

Because the former engineering team has not accumulated certain production experience,

the NPK line could not achieve its designed capacity steadily. By leveraging Sinochem’s

advantages, several senior engineer experts would help JV to diagnose and solve technique

problems. Also, they could train the main operation staff shifts by shifts.

2.9 Capacity Plan

Table 2.4 Capacity Expansion Plan (100%)Y1 50% Y7 115%Y2 75% Y8 120%Y3 100% Y9 125%Y4 100% Y10 125%

Changfeng Liu College of Commerce, University of Saskatchewan 16

Sinochem Feasibility Study

Y5 105% Y11 125%Y6 110% Y12 125%

The capacity expansion will fit the demand of local market demands. JV would invest more

capital every year according to the expansion plan.

Changfeng Liu College of Commerce, University of Saskatchewan 17

Sinochem Feasibility Study

Chapter 3: Human Resource Plan3.1 The period of feasibility research

3.1.1 Shareholder’s agreements

After bilateral negotiations, Sinochem and ABC Company have signed a Letter of Intent in

2002 which including the main principles for the future JV. The core content is as followed:

Company Name: Sinochem-ABC Fertilizer Company

Brand: Sinochem authorized JV to use its brand and logo—

Board of directors: the board of directors is made up of 5 people. Three come from

Sinochem and the other two will be assigned from ABC Company. Sinochem will recommend

the directors.

Management: Sinochem will recommend the candidates of CEO and chief sale officer to

the board. ABC Company will suggest the candidates of vice CEO, financial officer and

production officer to the board.

3.1.2 Project team and timetable

The Project Team consists of the personnel from two parties:

Sinochem: Financial Staff, Engineer, Lawyer and Marketing Staff.

ABC Company: Vice President and financial staff.

The project Manger should take responsibility to each part and lead the team to complete

the feasibility study during budget time.

See Appendix 2, Table A: Sinochem-ABC Company Feasibility Study Timetable.

Changfeng Liu College of Commerce, University of Saskatchewan 18

Sinochem Feasibility Study

3.2 The period of Integration

3.2.1 Strategic human resource management plan

JV develops the vision that employees and the company should be able to grow together.

JV plans to set up an employee performance management system which links performance

with income, encourages employees to seek better performance, serves as a major tool for

managers to evaluate the capacities of employees and helps raise the value of both the company

and the work force.

JV will launch the motivation system to balance the relationship between the management

and employees. The management will integrate physical and spiritual, short-term and long-term

motivations together so that employees feel their valuable work is recognized and well paid. JV

also plans to set up a sound welfare system to offer employees more benefits.

The JV’s value and culture should keep same with Sinochem’s, which is: Personality-

Honest, Cooperative, and Keen on Learning; Job Attitude- Serious, Creative, and striving for the

Top.

The purpose for strategic human resource management is: Establish strict reasonable and

effective rules; Cultivate excellent loyal and happy employees.

In the beginning period, JV needs more advanced personnel to join the company. The

recruitment channels could be: Key position-business relationship, HR company and creditable

recommendation; Common position-large scale recruitment, local HR centre and

recommendation.

3.2.2 Organizational chart

See Appendix 2; Figure A, Sinochem-ABC Company Feasibility Study Timetable

Changfeng Liu College of Commerce, University of Saskatchewan 19

Sinochem Feasibility Study

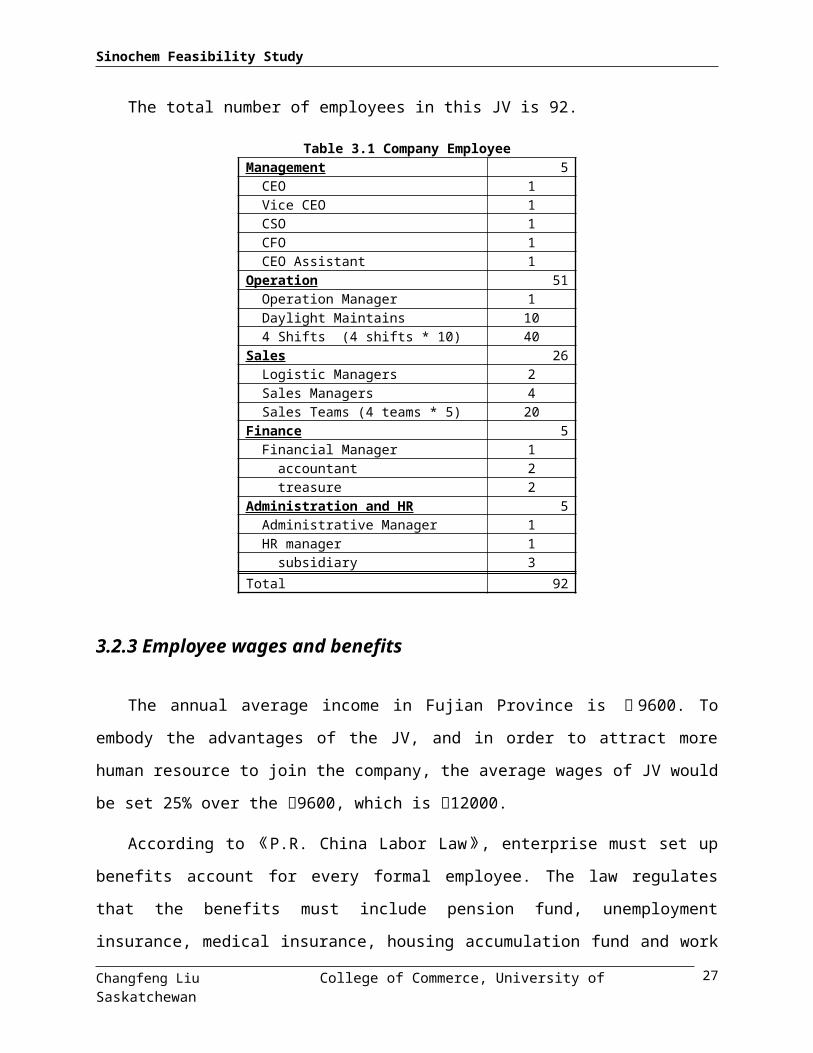

The total number of employees in this JV is 92.

Table 3.1 Company EmployeeManagement 5 CEO 1 Vice CEO 1 CSO 1 CFO 1 CEO Assistant 1Operation 51 Operation Manager 1 Daylight Maintains 10 4 Shifts (4 shifts * 10) 40Sales 26 Logistic Managers 2 Sales Managers 4 Sales Teams (4 teams * 5) 20Finance 5 Financial Manager 1 accountant 2 treasure 2Administration and HR 5 Administrative Manager 1 HR manager 1 subsidiary 3Total 92

3.2.3 Employee wages and benefits

The annual average income in Fujian Province is ¥9600. To embody the advantages of the

JV, and in order to attract more human resource to join the company, the average wages of JV

would be set 25% over the ¥9600, which is ¥12000.

According to 《P.R. China Labor Law》, enterprise must set up benefits account for every

formal employee. The law regulates that the benefits must include pension fund, unemployment

insurance, medical insurance, housing accumulation fund and work injury insurance. The

optional benefits could include family treasure insurance and maternity insurance and personal

insurance. The JV plans to pay the Compulsory and optional benefit for all the employees.

The benefits proportion to wage is shown below:

Changfeng Liu College of Commerce, University of Saskatchewan 20

Sinochem Feasibility Study

Table 3.2 Benefits proportion to wage

Items Pensio

n fund

Unemploymen

t insurance

Medical

insuranc

e

housing accumulation fund

work injury

insurance

maternity

insurance

Family

treasure

insurance

personal

insuranc

e

Total

Individual

Undertaking

Proportion

8% 0.5% 2% 8% ------ ----- ------ ----- 18.5%

Enterprise

undertaking

Proportion

20% 1.5% 10% 8% 0.4% 0.1% 3% 7% 50%

The total benefit that enterprise should undertake is 50% out of wages. Consequently, the

average human capital is ¥12000 * 150%=¥18000.

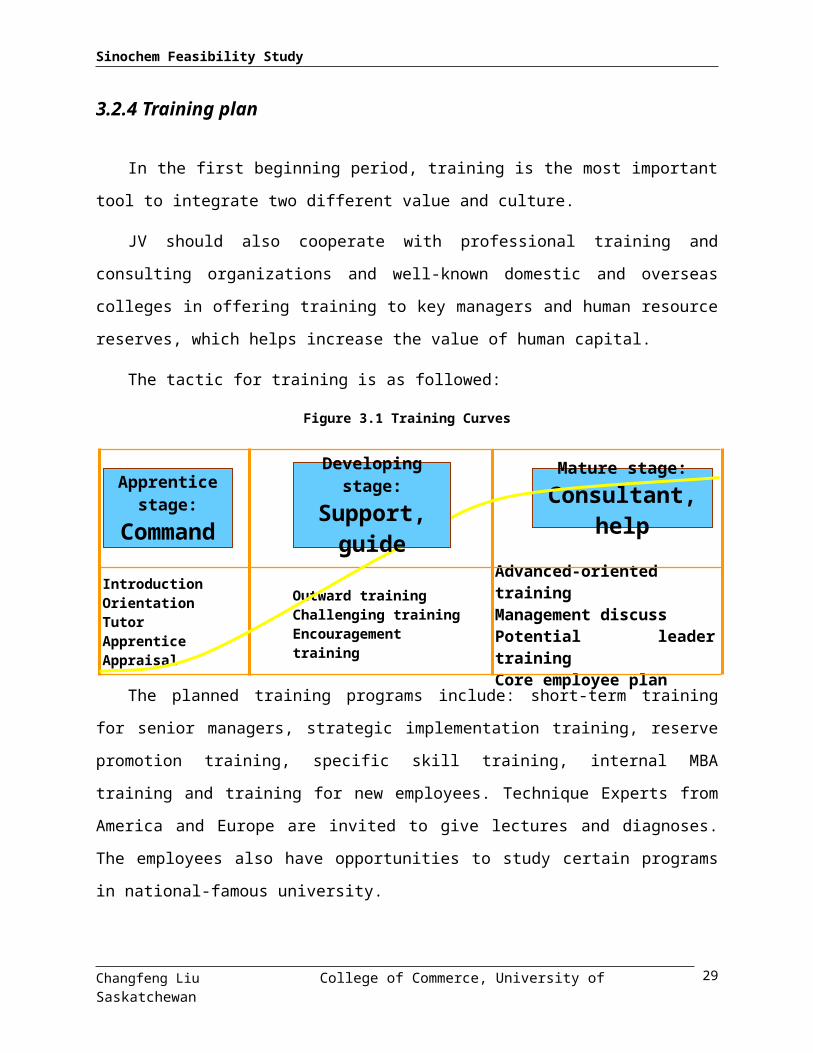

3.2.4 Training plan

In the first beginning period, training is the most important tool to integrate two different

value and culture.

JV should also cooperate with professional training and consulting organizations and well-

known domestic and overseas colleges in offering training to key managers and human resource

reserves, which helps increase the value of human capital.

The tactic for training is as followed:

Figure 3.1 Training Curves

Changfeng Liu College of Commerce, University of Saskatchewan

IntroductionOrientationTutorApprentice Appraisal

Mature stage:Consultant, help

Outward trainingChallenging trainingEncouragement training

Advanced-oriented trainingManagement discussPotential leader training Core employee plan

Developing stage:Support, guide

Apprentice stage:

Command

21

Sinochem Feasibility Study

The planned training programs include: short-term training for senior managers, strategic

implementation training, reserve promotion training, specific skill training, internal MBA

training and training for new employees. Technique Experts from America and Europe are

invited to give lectures and diagnoses. The employees also have opportunities to study certain

programs in national-famous university.

Changfeng Liu College of Commerce, University of Saskatchewan 22

Sinochem Feasibility Study

Chapter 4: Marketing Plan4.1 Compound Fertilizer Market Analysis and Sales Forecast

4.1.1 China Compound Fertilizer Market

China’s high-grade compound fertilizer industry developed very quickly in recent years.

The production capacities developed fast; output increased. Many new projects especially high-

grade NPK started. The proportion of the output of high-grade compound fertilizer in China’s

total phosphate and compound fertilizer output increased rapidly.

4.1.1.1 The General Situation of China’s Fertilizer Industry

After 50 years of development, the technology in China’s fertilizer industry has reached a

certain level. The product diversity has been improved. The structure has turned to be

reasonable. The production capacity has much increased. By the end of 2002, there were around

1200 fertilizer enterprises in China, among which there were 644 nitrogen fertilizer enterprises,

524 phosphate fertilizer enterprises and 41 potash fertilizer enterprises.

Figure 4.1The Structure of China’s Fertilizer Industry

In 2002, China’s fertilizer output reached 33.965 Million metric tones (Mt), up 5.9% over

2001, among which the nitrogen fertilizer, the phosphate fertilizer and the potash fertilizer

Changfeng Liu College of Commerce, University of Saskatchewan 23

Sinochem Feasibility Study

outputs reached 25.267 Mt, 7.394 Mt and 1.304 Mt, making up 74.39%, 21.77% and 3.84% of

the total and increasing by 4.75%, 8.72% and 13.55% against 2001 respectively.

Figure 4.2The Structure of China’s Fertilizer Production in 2002

In 2002, on nitrogen fertilizer, the urea output reached 14.548 Mt, accounting for 58% of

China’s total nitrogen fertilizer output. However, facing intensive competition and further

development of restructuring and product mix adjustment, some producers will face bankruptcy.

Therefore, the output in total nitrogen fertilizer production has continued to decline year-on-year.

Meanwhile, the production capacities and outputs of the high-analysis phosphate and

compound fertilizers have been growing steadily in China. As a result, ammonia consumption

has been increasing accordingly. For example, ammonia consumption for the production of

DAP/MAP and chemically-produced compound fertilizers reached nearly 1.50 Mt, and

accounted for 6% of the total ammonia output.

In 2002, Chinese phosphate fertilizer output was 7.394 Mt, among which the high-analysis

phosphate and compound fertilizers output was 2.958 Mt, up 11.92% over 2001 and accounting

for 40% of Chinese total phosphate fertilizer production ; the low-analysis phosphate fertilizers

output was 4.436 Mt, accounting for 60%.

At present, there are more than 300 NPK producers that have production licenses, and most

of the product is low concentration NPK (25-30%) and the average operation rate is low. There

are 109 enterprises that produce high-analysis phosphate and compound fertilizers in China,

among which 47 enterprises are producing MAP only, 8 enterprises producing DAP only, 4

Changfeng Liu College of Commerce, University of Saskatchewan 24

Sinochem Feasibility Study

enterprises producing TSP only, 15 enterprises producing NPK only ; and the remaining 35

enterprises are able to produce both MAP/DAP and NPK.

According to the preliminary statistics, the production capacity for chemically produced

NPK amounted to 10.32 million tons per year at the end of 2002. The outputs of DAP, MAP and

NPK increased by 39.29%, 12.49% and 20.19% over 2001, respectively.

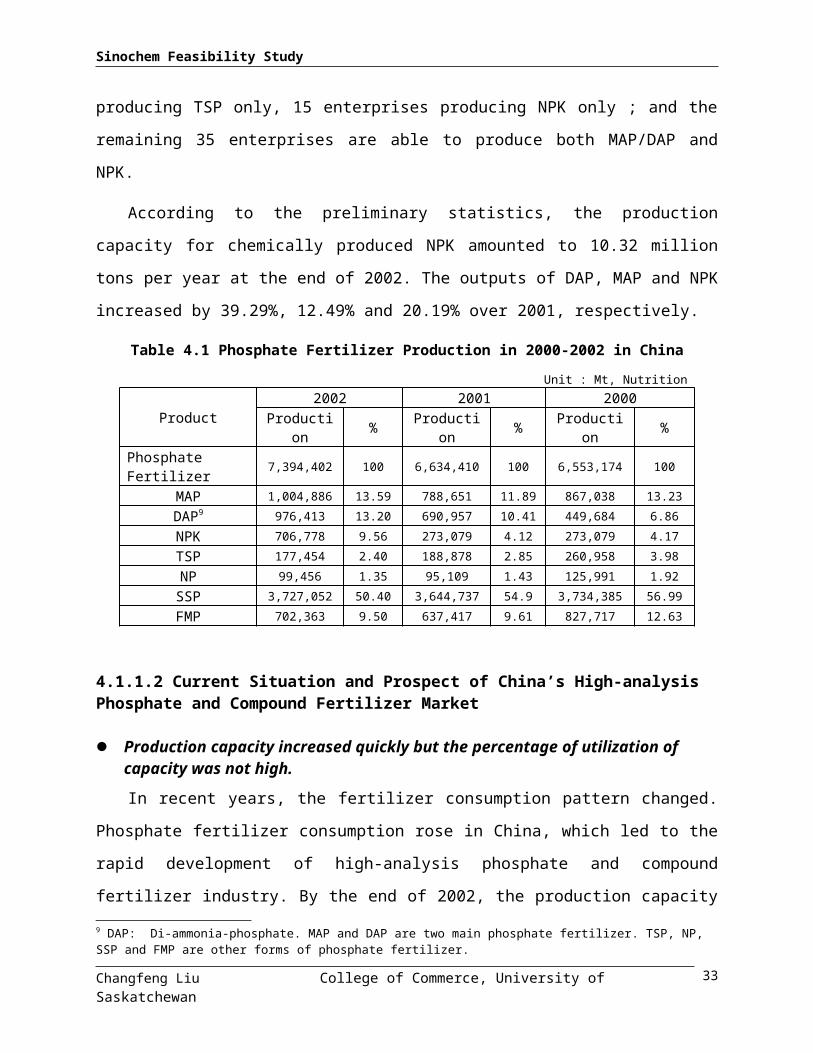

Table 4.1 Phosphate Fertilizer Production in 2000-2002 in China

Unit : Mt, Nutrition

Product 2002 2001 2000

Production % Production % Production % Phosphate Fertilizer 7,394,402 100 6,634,410 100 6,553,174 100

MAP 1,004,886 13.59 788,651 11.89 867,038 13.23

DAP9 976,413 13.20 690,957 10.41 449,684 6.86

NPK 706,778 9.56 273,079 4.12 273,079 4.17

TSP 177,454 2.40 188,878 2.85 260,958 3.98

NP 99,456 1.35 95,109 1.43 125,991 1.92

SSP 3,727,052 50.40 3,644,737 54.9 3,734,385 56.99

FMP 702,363 9.50 637,417 9.61 827,717 12.63

4.1.1.2 Current Situation and Prospect of China’s High-analysis Phosphate and Compound Fertilizer Market

Production capacity increased quickly but the percentage of utilization of capacity was not high.

In recent years, the fertilizer consumption pattern changed. Phosphate fertilizer

consumption rose in China, which led to the rapid development of high-analysis phosphate and

compound fertilizer industry. By the end of 2002, the production capacity of chemically-

produced phosphate and compound fertilizer reached 17.30 Mt. The proportion of the production

capacity of high-analysis phosphate and compound fertilizer in total phosphate fertilizer capacity

went up to 48% from 10% ten years ago.

The increases of MAP/DAP and NPK capacities contributed largely to the increase of

Chinese phosphate and compound fertilizer capacity. During the period of 1991 to 2001,

MAP/DAP capacity rose at an average annual increase rate of 17.7%. The production capacity of

9 DAP: Di-ammonia-phosphate. MAP and DAP are two main phosphate fertilizer. TSP, NP, SSP and FMP are other forms of phosphate fertilizer.

Changfeng Liu College of Commerce, University of Saskatchewan 25

Sinochem Feasibility Study

chemically-produced NPK reached 1.26 Mt, growing at an average annual rate of 35.5% (see

Figure 3).

Figure 4.3The Production Capacity of Chemically Produced NPK in 1995-2001 in China

The production capacity of high-analysis phosphate and compound fertilizers increased

notably in the past two years. The production capacity of chemically-produced NPK rose by

54%. The main additional production capacities are listed in Table 4.2.

Changfeng Liu College of Commerce, University of Saskatchewan 26

Sinochem Feasibility Study

Table 4.2The main additional production capacities

Province Enterprises Additional Capacity (1000t of product) Product

Hebei Sino-Arab Chemical Fertilizers Co Ltd 700 NPK Jiangsu Jiangsu Ruihe Fertilizer Co Ltd 40 MAP

Anhui Xuanzhou Sulfuric Acid Plant 40 MAP Hefei Sifang Phosphate and Compound Fertilizer Co Ltd 20 MAP Anhui Liuguo Chemical Industry Stock Co Ltd 240 DAP

Shandong

Laizhou Jinxing Chemical Co Ltd 100 SOP-NPK Qingdao Changhua Group 100 SOP-NPK Tianli Biochemical Industry Co Ltd 100 SOP-NPK Zibo Bofeng Compound Plant 100 SOP-NPK Anqiu Aobao Chemical Co Ltd 100 SOP-NPK

Hubei Hubei Xiangyun Chemical Holding Co 80 MAP Xiangfan Inorganic Chemical Plant General 30 MAP

Chongqing

Qijiang Fertilizer Plant General 20 MAP Fuling Chemical Holding Co Ltd 20 MAP Win-win Group Nanchuan Weifeng Chemical Plant General 40 MAP

Sichuan

Sichuan Shihua Holding Co Ltd 50 MAP Sichuan Hongda Holding Co Ltd Shihua Co 60 MAP Sichuan Longmang Phosphate Product Holding Co 20 MAP

Sichuan Shifang Yingfeng Industry Co Ltd 50 MAP 20 SOP-NPK

Sichuan Sulfuric Acid Plant 60 MAP Jinhe Phosphate Mine Chemical Plant 30 MAP Gongxian Zhongzheng Chemical Industry Co Ltd 20 MAP

Guizhou Guizhou Xiyang Fertilizer Industry Co Ltd 40 SOP-NPK

Yunnan Yunnan Phosphate Fertilizer Plant

30 MAP 50 TSP

Jianglin Group Holding Co Ltd 20 MAP Yunnan Tree-Circle Sinochem Cargill Fertilizer Co 600 DAP

Changfeng Liu College of Commerce, University of Saskatchewan 27

Sinochem Feasibility Study

Figure 4.4 Capacity Distribution of Chemically Produced NPK in China by Province in 2002(%)

The proportion of capacity utilization is not high, although the capacity of phosphate and

compound fertilizers increased rapidly in China. The production of chemically-produced

phosphate and compound fertilizers only accounted for 56.3% of its total capacity.

Table 4.3 Production and Capacity of Chemically Produced Phosphate and Compound Fertilizers in 2002 in China

Unit : 1000t of product

MAP DAP NPK TSP NP Total Capacity 3630 2760 8510 1450 1050 17400

Production 2193 2134 4204 396 863 9790 Proportion of the production in capacity(%) 60.4 77.3 49.4 27.3 82.2 56.3

The utilization of NPK production plants is relatively low. Most of NPK plants are small

scale and, their technique is simple and could only produce low concentrated NPK. These small

scale plants have to cease production soon.

China’s Imports of NPK

The top importers over the years were Guangdong, Shandong, Fujian and Zhejiang

provinces. Guangdong province and Beijing imported the largest fertilizer volume. The main

complex fertilizer import ports were Jiulong, Qingdao, Shanghai, Ningbo and Nanjing ports.

Over the years, NPK imports to China have largely been carried out from Russia, Norway,

Finland, Belgium, Greece and the Netherlands.

The largest foreign NPK suppliers to China are Acron (Russia), Rossosh (Russia), Norsk

Hydro (Norway), Kemira (Finland), BASF (Belgium).

Changfeng Liu College of Commerce, University of Saskatchewan 28

Sinochem Feasibility Study

In 2002, Acron exported around 1.5 million tons of NPK from Russia to China, which

accounts for more than 50% of the total NPK imports to China.

NPK consumption in China

With the development of China’s phosphate and compound fertilizer industry and the

improvement of the farmers’ living standard and knowledge level, the usage of compound

fertilizer is rising continuously. According to the statistics from the National Bureau of Statistics

of China, the usage of compound fertilizer amounted to 10.462 million tons (nutrient) in China

by 2002, rising by 6.3% as compared with that of 9.840 million tons in 2001. In the last three

years, increases in compound fertilizer usage remained at this level.

Figure 4.5 Compound Fertilizer Usages in China, 1995-2002

Distribution system in China

Since the late 1990s, China started to launch a Fertilizer Circulation System Reform. Up to

1999, two state-owned companies (one is Sinochem) and its local branches were entitled to

distribute and market fertilizers in the domestic market. From early 1999, local fertilizer

producers and agricultural service stations gained access to China’s domestic market.

Competition between more players is supposed to reduce fertilizer distribution costs.

Foreign companies and foreign investment companies are still not entitled to distribute

fertilizers in China. They are not allowed to set up companies for handling wholesale or retail

trade on the Chinese territory. Foreign companies will be entitled to do that by December 11,

2006, at the latest (i.e. 5 years after PRC entering into WTO).

Changfeng Liu College of Commerce, University of Saskatchewan 29

Sinochem Feasibility Study

The potential is great in China’s phosphate and compound fertilizer market

The forecast on phosphate and compound fertilizer needs in China can be made on the basis

of both the practical consumption for several previous years and its consumption by main crops.

However, because China lacks a nationwide and systematic follow-up on the fertilizer

consumption by main crops, the difference is big between the relative statistic data of phosphate

fertilizer consumption and the apparent consumption of phosphate fertilizer in China. It is not

scientific to use them in evaluating China’s phosphate market potential.

At present, Chinese plowland is still in serious shortage of phosphorus. According to related

research in 2000, the equilibrium nutrient can get guarantee only when the fast effective

phosphorus (FEP for short) content reaches 20mg/kg in the plowland. It could be seen from

Table 4 that the FEP content in 83.6% of Chinese plowland is lower than that standard.

According to the calculation made by Chinese specialists in the agricultural sector, 2.30 Mt of

P2O5 should be added into the plowland annually regardless of losses and uptake of phosphorus

in plowland in order to ensure that China’s 129.2 million hectares of plowland meet the standard

within the next ten years. Meanwhile, the FEP content in plowland will show a downward

movement in the future. In order to maintain the current FEP content of 12.9mg/kg, close to 2.53

Mt of P2O5 should be added into the soil annually regardless of phosphorus uptake by crops that

needs to be compensated with 8.49 Mt of P2O5 annually (more crops, more uptake of

phosphorus).

Based on the calculation above, it is projected that at least 13.32 Mt of P2O5 will be needed

in 2005 in China.

Table 4.4 Phosphate Fertilizer Demand in Raising FEP Content in Plowland, 2000-2010 in ChinaFEP content Sample Proportion Average FEP content Plowland area Demand(%

P2O5)(mg/kg) number (%) (mg/kg) (million hectares) (1000t)

>40 46 3.37 55.16 4.35 0

25~40 86 6.30 31.74 8.14 0

20~25 92 6.74 22.79 8.71 0

15~20 172 12.60 17.79 16.28 892

10~15 319 23.37 12.51 30.19 4562

5~10 427 31.28 7.32 40.41 10377

<5 223 16.34 3.18 21.11 7188

Total 1365 100 12.93 129.2 23020

Changfeng Liu College of Commerce, University of Saskatchewan 30

Sinochem Feasibility Study

Analyzing China’s current phosphoric resources, it is found around 3.00 Mt of P2O5 that are

returned to soil in forms of organic fertilizers annually. In 2005, assuming that China’s

phosphate fertilizer demand is 13.30 Mt P2O5, then the amount of P2O5 to be provided by

chemical fertilizers will be 10.30 Mt ; if the proportion of phosphate and compound fertilizer

production in total phosphate fertilizer production is estimated at 60%, then P2O5 provided by

phosphate and compound fertilizers will be 6.18 Mt ; the import volume of phosphate fertilizer

will be around 1.64 Mt P2O5 ; the home-made high-analysis phosphate and compound fertilizer

supply in the domestic market will be around 4.54 Mt P2O5, taking up 90% of the total high-

analysis phosphate and compound fertilizer output. Meanwhile, 500,000 t of phosphate and

compound fertilizers will likely be exported to abroad, making up 10% of the total output. In the

domestic market, the home-made high-analysis phosphate and compound fertilizers accounted

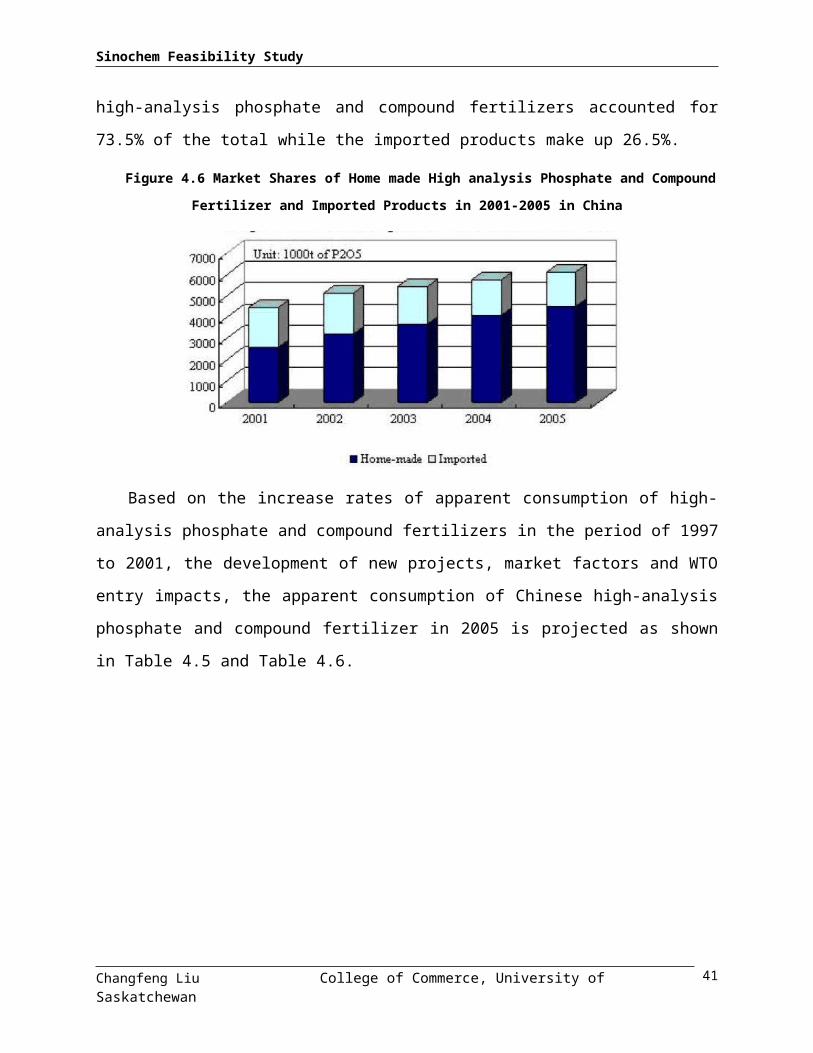

for 73.5% of the total while the imported products make up 26.5%.

Figure 4.6 Market Shares of Home made High analysis Phosphate and Compound Fertilizer and

Imported Products in 2001-2005 in China

Based on the increase rates of apparent consumption of high-analysis phosphate and

compound fertilizers in the period of 1997 to 2001, the development of new projects, market

factors and WTO entry impacts, the apparent consumption of Chinese high-analysis phosphate

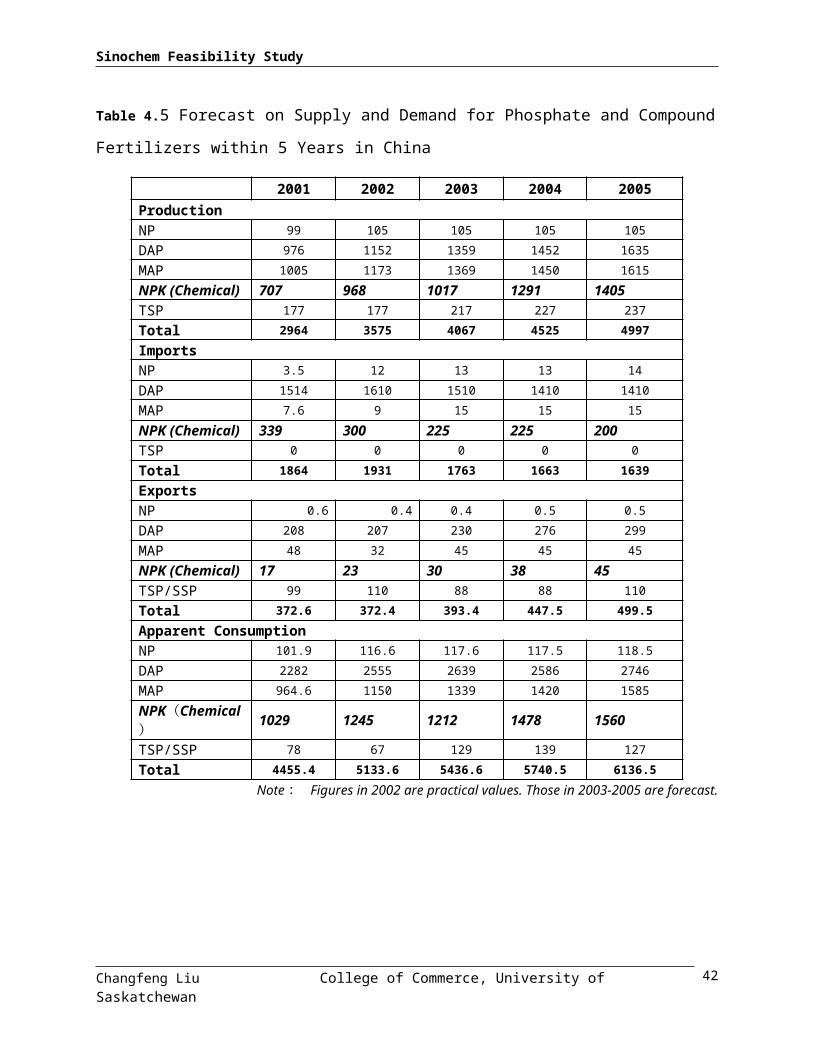

and compound fertilizer in 2005 is projected as shown in Table 4.5 and Table 4.6.

Changfeng Liu College of Commerce, University of Saskatchewan 31

Sinochem Feasibility Study

Table 4.5 Forecast on Supply and Demand for Phosphate and Compound Fertilizers within 5

Years in China

2001 2002 2003 2004 2005 Production NP 99 105 105 105 105

DAP 976 1152 1359 1452 1635

MAP 1005 1173 1369 1450 1615

NPK (Chemical) 707 968 1017 1291 1405 TSP 177 177 217 227 237

Total 2964 3575 4067 4525 4997

Imports NP 3.5 12 13 13 14

DAP 1514 1610 1510 1410 1410

MAP 7.6 9 15 15 15

NPK (Chemical) 339 300 225 225 200 TSP 0 0 0 0 0

Total 1864 1931 1763 1663 1639

Exports NP 0.6 0.4 0.4 0.5 0.5

DAP 208 207 230 276 299

MAP 48 32 45 45 45

NPK (Chemical) 17 23 30 38 45 TSP/SSP 99 110 88 88 110

Total 372.6 372.4 393.4 447.5 499.5

Apparent Consumption NP 101.9 116.6 117.6 117.5 118.5

DAP 2282 2555 2639 2586 2746

MAP 964.6 1150 1339 1420 1585

NPK(Chemical) 1029 1245 1212 1478 1560

TSP/SSP 78 67 129 139 127

Total 4455.4 5133.6 5436.6 5740.5 6136.5

Note : Figures in 2002 are practical values. Those in 2003-2005 are forecast.

Changfeng Liu College of Commerce, University of Saskatchewan 32

Sinochem Feasibility Study

Figure 4.7 Phosphate and compound Fertilizer Supplies in 2001-2005 in China

Table 4.6 Estimated Figures for Chinese Phosphate Fertilizer Demand and Supply in 2005

Unit: 1000t of P2O5Demand for raising FEP content in soil 2302

Demand for keeping reasonable FEP content in soil 2530

Demand for complementing crops’ uptake 8490

Total demand 13300

Supply from organic fertilizers 3000

Supply from chemical fertilizers 10300

Supply from phosphate and compound fertilizers, of which : 6180

Supply from home-made phosphates and compounds 4540

Supply from imported phosphates and compounds 1640

4.1.1.3 Conclusion

The production capacity of high-analysis phosphate and compound fertilizers will continue to increase in the next 5-10 years in China.

Because a lot of phosphate and compound fertilizer projects are under construction recently

in China, it is forecasted that Chinese production capacity of phosphate and compound fertilizers

will rise very fast before 2005, which can be reflected from the rapid development of capacity

expansion and new projects in Yunnan, Guizhou and Hubei provinces, which are the main

sources of domestic phosphate rock. By the end of 2010, only Yunnan province is scheduled to

add an additional capacity of 2.20 Mt P2O5 of phosphate and compound fertilizers or 2.80 Mt if

the market is bullish.

Changfeng Liu College of Commerce, University of Saskatchewan 33

Sinochem Feasibility Study

The current phosphate and compound fertilizer supply cannot meet the requirement from China’s agricultural sector.

China needs at least 6.18 Mt P2O5 of high-analysis phosphate and compound fertilizers in

2005. The current phosphate and compound fertilizer production capacity can only meet 47% of

that total requirement. There is still a large room for the development of high-analysis phosphate

and compound fertilizer industry. China will raise not only the capacity but also the production

of high-analysis phosphate and compound fertilizers. China still needs to import high-analysis

phosphate and compound fertilizers for a long period of time.

The main destination for home-made phosphate and compound fertilizers is the domestic

market although there exist opportunities for Chinese product export. Therefore, the

development of China’s phosphate and compound fertilizer industry will still focus on domestic

market and the competitiveness of the products.

NPK has promising prospects in China

At this stage, the compound fertilizer consumption rate and science fertilization level of

chemical fertilizer use in China is also lower. The compound fertilizer consumption rate is about

24%; it has a big gap between the world average level (about 30%) and a developed country’s

level (about 50%). As to the high concentration compound fertilizer in particular, China needs to

import large quantities of DAP and NPK from the international fertilizer market to meet the

needs of agriculture production.

From now on, the direction of China chemical fertilizer development is to further adjust the

nitrogen fertilizer/phosphate fertilizer proportion maladjustment, to boost the high concentration

compound fertilizer proportion, to heighten the compound fertilizer rate in phosphate fertilizer

production and consumption and enhance the service of fertilizer use in agriculture.

NPK consumption is a development trend in China. The fertilizer market has shown that the

urea, ammonium bicarbonate and SSP markets are worse than those for DAP and high

concentrated NPK. NPK production and consumption go up fast. However, because the demand

increases too fast, imports remain at the high level. The current NPK complex fertilizer imports

have reached 3 million tons per year. NPK has great potential market prospects and phosphate

fertilizer development is confronted with a severe challenge.

Changfeng Liu College of Commerce, University of Saskatchewan 34

Sinochem Feasibility Study

It is forecasted that by 2005 phosphate fertilizer output will reach 8,000 to 9,000 kt 10 (100%

P2O5), whereas NPK compound fertilizer output 10,500 kt (nutrient N+ P2O5+K2O) and NPK

complex fertilizer output 4,000 kt (nutrient N+ P2O5+K2O). With the current agriculture

development rates, the demand for fertilizer will reach 46,500 kt (nutrient) by 2005. Along with

further NPK recognition by farmers and development of economic crops, the ratio of NPK to the

total will be 30% by 2005. That is to say, the demand for NPK compound fertilizer will be

13,950 kt (nutrient N+ P2O5+K2O) and NPK complex fertilizer 6,000 kt (nutrient N+

P2O5+K2O). Therefore, high concentrated NPK fertilizer needs further development.

4.1.2 Compound Fertilizer Market in Fujian Province

4.1.2.1 General Background

Fujian Province is located in China’s southeast coastal region between north latitudes 23°33′

to 28°19′, and east longitudes 115°50′ to 120°40′, bordering Zhejiang Province on the north,

Jiangxi Province on the west and Guangdong Province on the south, respectively; on the east, the

Province faces the Taiwan Straits which separate it from Taiwan Province.

Figure 4.8 Fujian Province Geographical Location

10 Kt means 1000 Mt.

Changfeng Liu College of Commerce, University of Saskatchewan 35

Sinochem Feasibility Study

Fujian has a total area of 121,400 km2. Total population stood at 34.4 million based on

China’s 2002 population census. With a 3,324-km coastline, it has many ports, the biggest being

Fuzhou and Xiamen which are open to foreign trade and investment. Fujian is one of provinces

that China first opened to foreign investment. The Southeast Fujian area, which comprises five

cities and counties -- Fuzhou, Xiamen, Putian, Quanzhou and Zhangzhou, is the economic hub of

Fujian, accounting for 78.5% of the province’s GDP in 2002.

4.1.2.2 Infrastructure

Water Transport The coastal ports in Fujian have a combined annual throughput of over

69 million tons. Fuzhou's Mawei(馬尾) , Xiamen's Dongdu(東渡) and Meizhou(湄州)Bay are the most important harbours, with berths which can accommodate ships in the

10,000-to-50,000-ton-class.

Railways Fujian is well connected to northern and central China by railways. The province

is connected to the Beijing-Kowloon railway via the 500-km Yingtan-Xiamen railway. In the

near future, two new railways will be built -- the Wenfu Railway(溫福鐵路)and Ganglong

Railway(贛龍鐵路)- connecting with Zhejiang Province and Jiangxi Province.

Roadways Major arterial highways include those linking Fuzhou-Kunming (福州-昆明) , Beijing-Fuzhou, Xiamen-Chengdu(廈門-成都) , and Fuzhou-Lanzhou(福州-蘭州) . The first class roadway within the province is Fuzhou-Quangzhou-Xiamen-Zhangzhou

(福州-泉州-廈門-漳州) . Three new roadways are under construction; they are the

Wenzhou-Fuzhou highway, Zhangzhou-Longyan highway as well as the state highway that links

Beijing and Fuzhou.

Air Transport The Changle International Airport (長樂國際機場) in Fuzhou, the

Xiamen International Airport and the airport in Wuyishan(武夷山) operate more than 90

domestic and international routes, linking the province with more than 40 domestic cities, as well

as Hong Kong, Japan and the Philippines.

Electricity Fujian has abundant hydroelectric resources, with total electricity capacity

estimated at over 4.04 million kWh a year. The major power stations are located at Shuikou(水Changfeng Liu College of Commerce, University of Saskatchewan 36

Sinochem Feasibility Study

口), Shaxikou(沙溪口), Fuzhou, Zhangping(漳平)and Yong'an(永安). In Xiamen, a

power plant is being built at Songyu(嵩嶼).

4.1.2.3 Agriculture Industry

In 2002 the proportion of the three major industrial sectors (agriculture, industrial and

service) in the Fujian province has been readjusted to 14.2:46.1:39.7. In Agriculture, Fujian is in

transition from individual to industrial scale. During this 10th Five-Year Plan period, priority

will be given to the growth of three major industries in the province.

Fujian's food grain includes mainly rice, sweet potatoes and wheat, and cash crops mainly

sugar-cane, peanuts, rapeseed and tobacco. Fujian is one of China's major sugar-cane and tea

growers. The Wuyi Mountain Area is famous for its tea. Tangerines, Longans, lichees, bananas,

loquats and pineapples are the major fruit of Fujian.

The province has ample supplies of subtropical products such as sugar cane, peanuts and

oranges, but also has remarkably varied output. Other products include: rice, wheat, sweet

potatoes, rape seed, soybeans, sesame, tea, lychees, pineapples, pomelos, loquats, bananas, lotus

seeds, bamboo shoots, mushrooms, silver fungus, jute, tobacco, rosin, medicinal herbs, tea oil,

tung oil and Chinese tallow tree.

The principal types of land cover are rice, vegetables, and commercialized trees (orchards

and bananas), bare soil, urban areas. The known average crop cycle turnover is 2.3 per year.

4.1.2.4 Local Fertilizer Demand and Supply

Almost all the plants and fruits need fertilizer. But not all the farmer use fertilizer to

improve the growth. With the increasing of farmer’s income, more and more farmers began to

use NPK to help them to raise the yield of plant and fruit.

From the statistic data (See table 4.7), the local supply capacity only meet half of market

demand. Most of fertilizer, especially potash and NPK are highly relied on the products from

import and other provinces. Fujian Province is a big agriculture region; the annual fertilizer

demand is huge and steady. In recent years, the farmers began to realize the advantages of NPK.

Therefore, the demand for NPK is increasing quickly. But there isn’t any NPK plant in province

until ABC Company set up a NPK line in 2002. Still, the supply capacity couldn’t meet the

demand level.

Changfeng Liu College of Commerce, University of Saskatchewan 37

Sinochem Feasibility Study

Table 4.7 Annual Fertilizer Demand and Supply in Fujian Province from 1998—2002

Unit:Nutrition 1000 Mt

Year Total N P K NPK1999 Demand 1180.8 554.2 165.7 225.9 235

Supply 614.3 544.2 70.1 -- --2000 Demand 1243.3 567.3 172.4 240.7 262.9

Supply 604 520.6 83.4 -- --2001 Demand 1233.3 556.6 168.3 237.7 270.7

Supply 609.2 510.2 99 -- --2002 Demand 1244.9 562.3 153.2 239.1 290.3

Supply 636 530.7 85.3 -- 20

4.1.2.5 Local Fertilizer Market Situation and Main Competitors

Imported fertilizer owns over 50% of local market shares (See table 4.8). According to

Chinese WTO regulation, foreign fertilizer producers are not allowed to enter domestic

distribution chain in China until 2006. Now, most of foreign producers ask Sinochem as their

agent to sell their fertilizer to Chinese consumer. Because there is no local NPK manufacture in

Fujian province, all the NPK products are supplied by imported producers or neighborhood

provinces.

Considering setting up its own brand before the fertilizer market is totally opened to foreign

competitors in 2006, Sinochem need to establish a local plant to cultivate and extend its own

brand instead of foreign brands. Therefore, Sinochem could change the foreign brands’ sale

direction to other provinces so as to help its own brand could seize market share quickly.

Changfeng Liu College of Commerce, University of Saskatchewan 38

Sinochem Feasibility Study

Table 4.8The Main NPK Brands and Sales in Fujian Province in 2002

From Brand Sales (000 Mt) Price (per Mt)Russia

(Sinochem as agent)

AcronK2SO4 – based NPK (15-15-15) 170 1600

Norway(Sinochem as

agent)

HYDROK2SO4 – based NPK (15-15-15) 50 1750

Hebei ProvinceSacf

KCI – based NPK (15-15-15) 20 1300

Finland(Sinochem as

agent)

KEMIRAK2SO4 – based NPK (15-15-15) 15 1800

Shandong Province

YanyangtianKCI – based NPK (15-15-15) 14 1320

4.1.3 JV Sales Forecast

Sinochem want its target market share achieve 40% of Fujian Province NPK market in three

years. The total demand of this market is around 500,000 Mt. Therefore, the annual capacity of

JV should no less than 200,000 Mt.

4.2 JV Marketing Plan

4.2.1 Poisoning

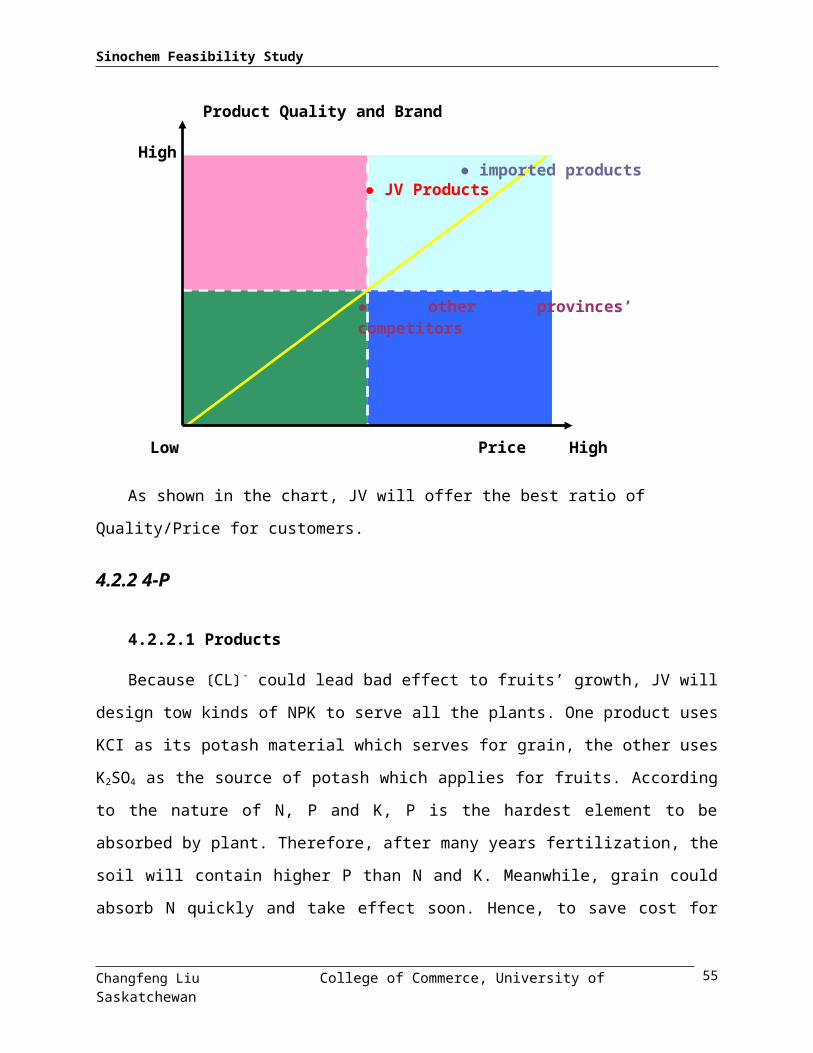

Sinochem orientates its brand as a quality leader. If Sinochem sets up the plant in Fujian

Province to meet the local demand, the JV will benefit from lower freight cost compared with the

competitors outside from Fujian Province, especially imported products. Meanwhile, Sinochem

and ABC Company could provide competitive potash and nitrogen material to JV. JV’ products

cost must be lower than other competitors. Therefore, JV positions its products as high quality,

famous brand but low price. The poisoning strategy could help JV to seize market share

promptly.

Changfeng Liu College of Commerce, University of Saskatchewan 39

Sinochem Feasibility Study

The relationship between quality and price could be described as followed:

Figure 4.9 JV Positioning

As shown in the chart, JV will offer the best ratio of Quality/Price for customers.

4.2.2 4-P

4.2.2.1 Products

Because 〔CL〕- could lead bad effect to fruits’ growth, JV will design tow kinds of NPK to

serve all the plants. One product uses KCI as its potash material which serves for grain, the other

uses K2SO4 as the source of potash which applies for fruits. According to the nature of N, P and

K, P is the hardest element to be absorbed by plant. Therefore, after many years fertilization, the

soil will contain higher P than N and K. Meanwhile, grain could absorb N quickly and take effect

soon. Hence, to save cost for farmers, JV will design higher N and lower P products for grain,

and design K2SO4 – based NPK for the demand of fruits.

The grades are as followed:

KCI – based NPK (18-10-12) K2SO4 – based NPK (15-15-15)

Changfeng Liu College of Commerce, University of Saskatchewan

P 价格

Product Quality and Brand

Low

● JV Products

● other provinces’ competitors

Price

● imported productsHigh

High

40

Sinochem Feasibility Study

Each product’s capacity will be 100,000 Mt.

4.2.2.2`Price

According to poisoning strategy, JV offers high quality but low price product, the price will

at the same range of domestic products.

KCI – based NPK (18-10-12) 1250/Mt (Price after tax but not includes freight)

K2SO4 – based NPK (15-15-15) 1450/Mt (Price after tax but not includes freight)

(Because the price of K2SO4 is higher than KCI, usually the price of S-based NPK is higher

than CI-based NPK too)

4.2.2.3 Promotion

JV will offer the same value added service for farmers as Sinochem does, including inviting

agricultural experts teach local farmers how to use fertilizer scientifically, how specific plant

needs certain content nutrition.

4.2.2.4 Place (Target Market)

Sinochem will set up its own distribution channel to cover the whole Fujian market. Each

village will have a direct sale store. This is the best way to control prices and channels.

According to the geographical distribution of plants, JV’s Target market could be mainly

defined as three market area: tea area, grain area and fruit area (See table 4.9 and figure 4.10).

Table 4.9 JV Target Plant and its UsageUnit:000 Mt Nutrition

Segment Market NPK Theoretical Need

Actual Usage Tactic

Grain CI- based 340 1301、 High quality, low

price

2、 Good branding image with own distribution channels

Fast-grow Forest CI- based 280 20Bamboo CI- based 270 20Fruits S-based 350 170Vegetable S-based 250 150Tea S-based 50 30Flower and grass S-based 10 3

Changfeng Liu College of Commerce, University of Saskatchewan 41

Sinochem Feasibility Study

Figure 4.10 JV Target Market

4.2.3 Freight Analysis

The three main materials for fertilizer are N, P and K. ABC Company will transfer urea to

JV by pipe directly. Sinochem will provide imported potash from Xiamen port which the freight

to JV is only 18/Mt, this freight is the lowest price compared with other domestic producers

because most of their location are far from port.

For final product, the freight in Fujian Province is much lower than outside competitors.

Consequently, the location of JV is one of main advantage to lower down selling price.

Changfeng Liu College of Commerce, University of Saskatchewan 42

Tea area

Grain area

Fruit and flower area

Sinochem Feasibility Study

Figure 4.11 JV Freight Map

4.2.4 Projections of Revenues and Marketing Expenses

Table 4.10 JV Projection of RevenuesSale Price (After value added tax) Revenues

NPK (K2SO4) RMB/Mt ¥1,450 ¥145,000,000 NPK (KCI) RMB/Mt ¥1,250 ¥125,000,000

Total ¥270,000,000

Setting up its own distribution channel is a key strategy for Sinochem. Therefore, Sinochem

will plan its marketing expense as they did in other province. The marketing expense includes

direct sale store constructions expenses, advertising, brochures, experts’ wages, web page, travel

Changfeng Liu College of Commerce, University of Saskatchewan 43

JJVV

¥4545//MtMt

¥1818//MtMt

¥2323//MtMt

¥105105//MtMt

¥4646//MtMt

¥4141//MtMt

¥5252//MtMt

Sinochem Feasibility Study

expenses and trade show. JV will take 5% of sales as marketing expenses to Sinochem.

Sinochem will undertake total selling job. Therefore, JV won’t have the burden of sale.

Changfeng Liu College of Commerce, University of Saskatchewan 44

Sinochem Feasibility Study

Chapter 5: Financial Plan5.1 Capital Costs

Before the JV set up, the total assets of NPK line is ¥ 53,170,000. ABC Company has

inputted ¥ 11,600,000 and loaned ¥ 41,570,000 from China Construction Bank. After the

investment, the two shareholders will contribute the new increasing equity cash ¥35,400,000 for

the JV. And the JV plan to undertake the debt and borrow a new short term bank loan

¥20,000,000.

At the time JV set up, the total assets will achieve from ¥53,170,000 to ¥108,570,000.

This value covers all operating costs for the first year and all capital expenditures.

Table 5.1 Opening Balance Sheet

Before Investment After InvestmentABC NPK line JV

ABC Company Equity 11,600,000 JV Equity 47,000,000 Sinochem (cash) 25,000,000 ABC Company 22,000,000 ABC capital 11,600,000 ABC (cash) 10,400,000 Liability 41,570,000 Liability 61,570,000 long term bank loan 41,570,000 long term bank loan 41,570,000 short term bank loan (new) 20,000,000 Total equity and liability ¥53,170,000 Total equity and liability ¥108,570,000 Current Assets Current Assets 46,795,300 Cash Cash Accounts Receivables Accounts Receivables Inventories Inventories Account Payables Account Payables Long term assets 53,170,000 Long term assets 61,774,700 Property, plant and equipment 53,170,000 Property, plant and equipment 61,774,700 Land usage fee 4,945,300 * Building 15,804,400 Building 23,340,300 Equipment 32,420,300 Equipment 38,434,400 Other Assets Other Assets Total Asset ¥53,170,000 Total Asset ¥108,570,000

After JV sets up, Sinochem will become the largest shareholder which holds 53% equity of the JV.

Table 5.2 JV Equity Structure

Changfeng Liu College of Commerce, University of Saskatchewan 45

Sinochem Feasibility Study

Sinochem 53%ABC Company 47%

In the first year, the total capital costs will be ¥61,774,700.

Table 5.3 Total Capital CostsLand (rental) 0Building ¥23,340,300Equipment ¥38,434,400

Total Capital Costs ¥61,774,700

5.2 Loan Amortization

JV will undertake former long term debt and borrow new short term debt from China

Construction Bank. The long term debt and short term debt are ¥41,570,000 and ¥21,000,000,

respectively. The total loan of ¥61,570,000 will be amortized over twelve years.

The bank would like to lend money to the company who has good credit history. Therefore,

to earn interest, the bank does not want the JV to pay off in a short time. Consequently, JV could

judge when and how much to pay the principle is the best situation according to the cash flow

requirement and the reasonable debt ratio. From the income projections this payment plan can

be covered each year by cash flow. See more detail in Appendix 4, Financial Model.

Changfeng Liu College of Commerce, University of Saskatchewan 46

Sinochem Feasibility Study

Table 5.4 Amortization Schedule

Y1 Y2 Y3 Y4 Y5 Y6

Long term debt41,570,00

041,570,00

041,570,00

041,570,00

041,570,00

041,570,00

0principal payment (input) 0 0 0 0 0 0interest payment 2,319,606 2,319,606 2,319,606 2,319,606 2,319,606 2,319,606

Balance41,570,00

041,570,00

041,570,00

041,570,00

041,570,00

041,570,00

0payment 2,319,606 2,319,606 2,319,606 2,319,606 2,319,606 2,319,606 Short term debt

20,000,000

20,000,000

20,000,000

20,000,000

20,000,000

20,000,000

principal payment (input) 0 0 0 0 0 0interest payment 1,098,000 1,098,000 1,098,000 1,098,000 1,098,000 1,098,000

Balance20,000,00

020,000,00

020,000,00

020,000,00

020,000,00

020,000,00

0payment 1,098,000 1,098,000 1,098,000 1,098,000 1,098,000 1,098,000Debt Ratio 57% 54% 50% 48% 47% 43%

Total Liability Balance61,570,00

061,570,00

061,570,00

061,570,00

061,570,00

061,570,00

0Interest 3,417,606 3,417,606 3,417,606 3,417,606 3,417,606 3,417,606Total Principal and Interest paid 3,417,606 3,417,606 3,417,606 3,417,606 3,417,606 3,417,606 Y7 Y8 Y9 Y10 Y11 Y12

Long term debt41,570,00

041,570,00

041,570,00

034,000,00

034,000,00

034,000,00

0principal payment (input) 0 0 7,570,000 0 0 0interest payment 2,319,606 2,319,606 2,319,606 1,897,200 1,897,200 1,897,200

Balance41,570,00

041,570,00

034,000,00

034,000,00

034,000,00

034,000,00

0payment 2,319,606 2,319,606 9,889,606 1,897,200 1,897,200 1,897,200 Short term debt

20,000,000

20,000,000

20,000,000

15,000,000

15,000,000

15,000,000

principal payment (input) 0 0 5,000,000 0 0 0interest payment 1,098,000 1,098,000 1,098,000 823,500 823,500 823,500

Balance20,000,00

020,000,00

015,000,00

015,000,00

015,000,00

015,000,00

0payment 1,098,000 1,098,000 6,098,000 823,500 823,500 823,500Debt Ratio 43% 43% 43% 37% 38% 38%

Total Liability Balance61,570,00

061,570,00

061,570,00

049,000,00

049,000,00

049,000,00

0Interest 3,417,606 3,417,606 3,417,606 2,720,700 2,720,700 2,720,700

Total Principal and Interest paid 3,417,606 3,417,60615,987,60

6 2,720,700 2,720,700 2,720,700Long term interest Rate 5.58%Short term interest Rate 5.49%

Changfeng Liu College of Commerce, University of Saskatchewan 47

Sinochem Feasibility Study

5.3 Dividend Policy

The dividends policy that JV implemented is based on cash flow condition. Sinochem

believes it’s a safe range that the debt ratio is kept around 40-50%. To keep this ratio, excess

cash flow will be applied to pay off the debt. Meanwhile, Sinochem also emphasizes on the

regular and steady dividend from the investment. Hence, JV will carry out the dividend policy

which gives attention to both healthy cash flow and ROE. According to the financial model, the

JV has structured a dividend and financing policy to match and balance from shareholder and

management’s requirements.

Table 5.5 Dividends Paid

Dividend Paid

Y1 Y2 Y3 Y4 Y5 Y6¥0 ¥0 ¥0 ¥6,000,000 ¥6,000,000 ¥0

Y7 Y8 Y9 Y10 Y11 Y12¥10,000,00

0¥12,000,00

0¥13,000,00

0¥14,000,00

0¥14,000,00

0¥15,000,00

0

Using the current dividend policy, JV could achieve an ERR on equity investment to

13.91%.

5.4 Cost Analysis

Raw Material is the main components of total cost. Therefore, how to decrease the purchase

price is a key factor to build JV’s cost advantage. In fact, Sinochem could supply the most

competitive potash to JV as well as ABC Company could provide nitrogen. These two materials

will account for 54% of total cost.

Table 5.6 Unit Cost

Unit Cost N P K AccessoryManufacturing

OverheadNPK (K2SO4) 252 406 438 136 65 NPK (KCI) 319 271 220 131 65

Figure 5.1 Unit Cost

Changfeng Liu College of Commerce, University of Saskatchewan 48

Sinochem Feasibility Study

5.5 Ratio Analysis

The projected performance ratios for JV show a successful business over the twelve year

business model. These results are depicted in Table 5.7. The fertilizer production is a business

with high capital start up costs and few variable manufacturing costs. Therefore profits will be

sensitive to business cycles in the early years because of high depreciation and high debt

servicing costs, and very little variable costs that can follow output.

Table 5.7 Ratio Analysis Y1 Y2 Y3 Y4 Y5 Y6 Y7 Y8Cash Conversion Cycle 65 65 65 65 65 65 65 65 Liquidity Ratios Current Ratio 2.53 3.03 3.65 4.05 4.44 5.07 5.36 5.58 Activity and Operating Ratios Total Asset Turnover 1.22 1.72 2.10 2.04 2.07 2.00 2.06 2.14 Inventory Turnover 3.30 4.11 4.88 5.00 4.96 4.97 4.98 4.98 Average Days Inventory 111 89 75 73 74 73 73 73 Leverage Ratios Debt Ratio 57% 54% 50% 48% 47% 43% 43% 43%Debt to Equity 1.32 1.16 0.99 0.93 0.87 0.76 0.74 0.74 Profitability Ratios Gross Profit Margin

14.03%

14.03%

14.03%

14.03%

14.03%

14.03%

14.03%

14.03%

Net Profit Margin 0.39% 3.42% 3.71% 3.71% 3.75% 3.79% 3.83% 3.86%Return on Total Assets 0.47% 5.88% 7.81% 7.57% 7.76% 7.58% 7.89% 8.27%

Return on Equity 1.10%12.72

%15.54

%14.63

%14.55

%13.34

%13.77

%14.40

%

Changfeng Liu College of Commerce, University of Saskatchewan 49

Sinochem Feasibility Study

The current ratio gives information on the liquidity of the company by showing its ability to

meet expenses out of cash flow. The current ratio defined as current assets (cash, inventory,

accounts receivable) over current liabilities (wages payable, current portion of long term debt).

This shows the ability of the company to make payments out of cash. Judging by the current

ratios this business could generate adequate cash flows to meet expenses. With the capacity

increase continuously, the total value of inventory goes up quickly. Hence, the current ratio is

higher than average industry level in future years.

The debt ratio shows the total liabilities over total assets. This shows how highly the

company is leveraged against its total assets. JV has a low debt ratio which means that JV has

adequate equity cash flow. This indicates JV does leave much room for restructuring debt and

leveraging total assets. The debt to equity ratio shows the amount of debt compared to the

amount of investor equity in the business. In this project, the debt ratio would be controlled at a

low risk level.

The return on assets (ROA) ratio is the total return of the business. In summary, ROA is the

return that both the lender and the business are generating from the assets. The ROA has to be

positive and higher than the cost of debt. Return on Equity is the net income over the total

shareholder’s equity. This ratio shows the returns that the business is generating on the money

that shareholders have invested. The gross margin is the net income over the cost of goods sold

before taxes. Gross margin shows the profits over the total costs. A large margin would indicate