chapter 10 money and banking - phillipsburg school · pdf filechapter 10 money and banking 1....

TRANSCRIPT

Chapter 10 Money and Banking1. Money2. The History of American Banking3. Banking Today

How can you make the most of your money?

It’s been a hot day, and you have just gotten schooled at a game of basketball by Mr. Schenk. You arrived at a store to get a drink and you scramble for money in your short pockets but realize you have none. But wait! You forgot that you had a dollar bill in your wallet!

Great you can get that drink. Oops! I forgot about the tax! Darn it!

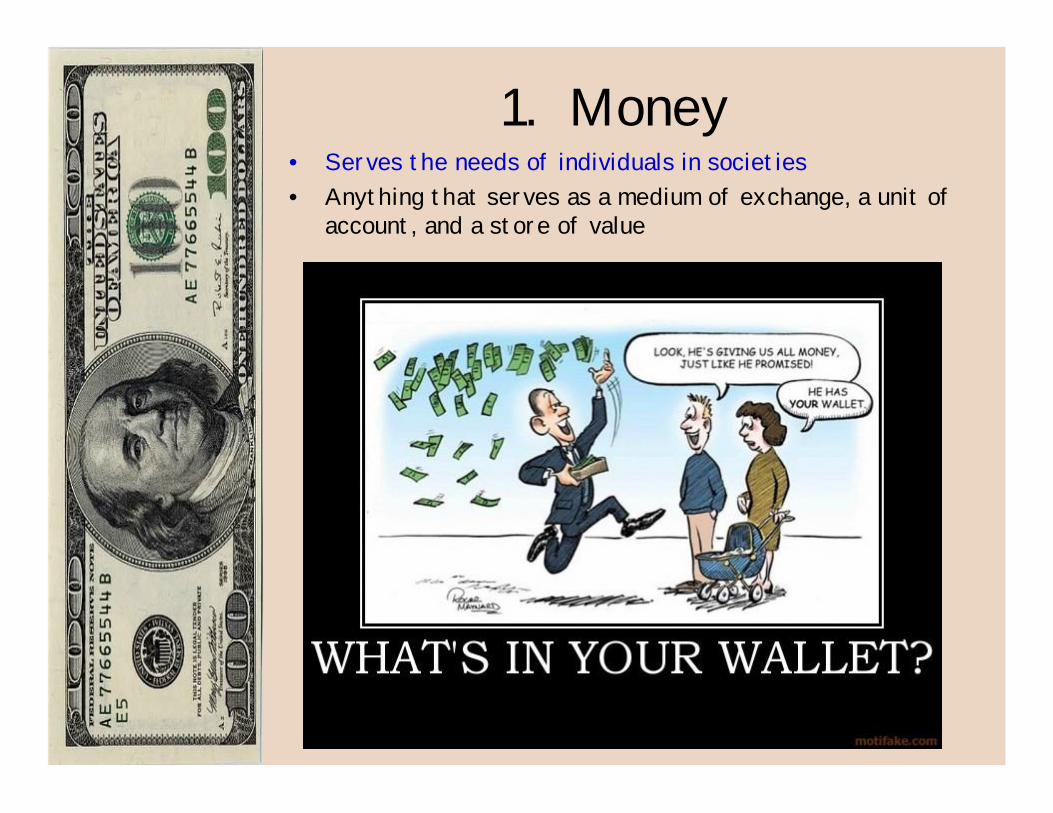

1. Money• Serves the needs of individuals in societies• Anything that serves as a medium of exchange, a unit of

account, and a store of value

The Three Uses of Money• Medium of Exchange -used to determine value during the

exchange of goods and services• Unit of Account -comparing the values of goods and

services• Store of Value -keeps its value if its stored rather than

spent

Uses of Money

Medium of Exchange Unit of Account Store of Value

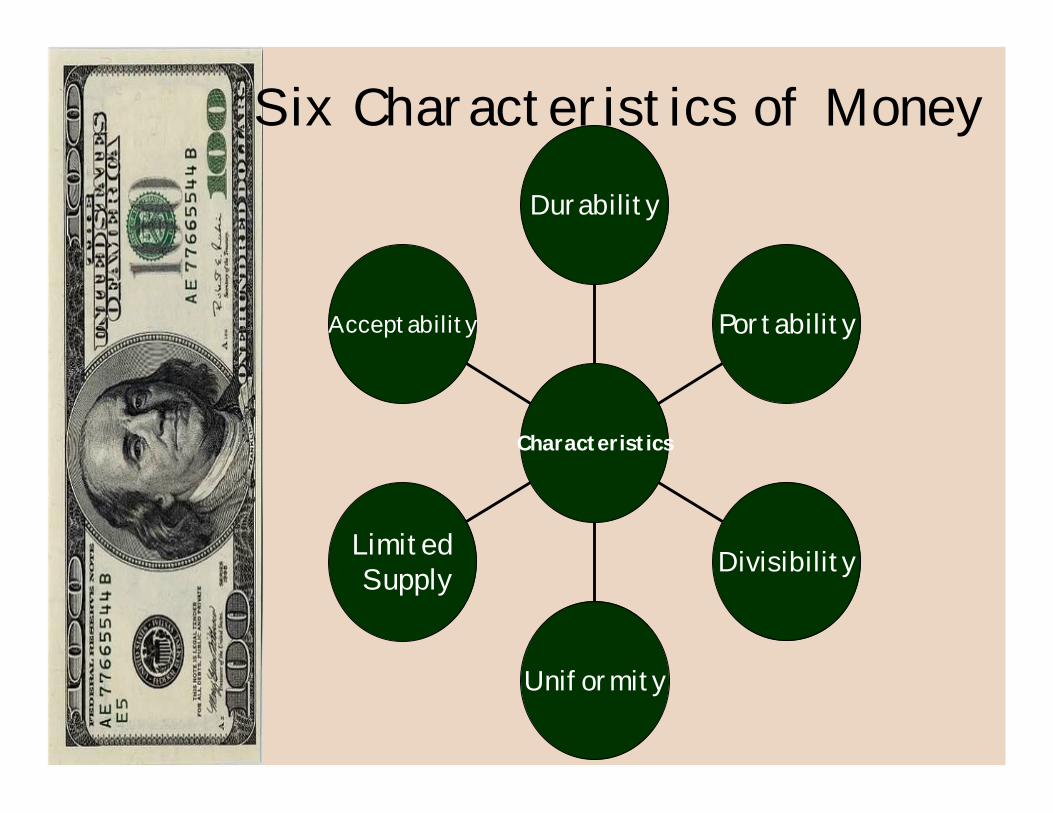

Six Characteristics of Money

Acceptability

LimitedSupply

Uniformity

Divisibility

Portability

Durability

Characteristics

Sources of Money’s Value

• Commodity Money –objects that have value and are used as money

• Representative Money -objects that have value because the holder can exchange them for something of value

• Fiat Money -objects that have value because government has decreed that they are an acceptable means of paying debt

Commodity

RepresentativeFiat

Money Sources

2. History of American Banking• Bank -an institute for receiving, keeping, and

lending money

This institution has led to many of arguments throughout the years of nation, even today! How!

120 South Third Street, Philadelphia

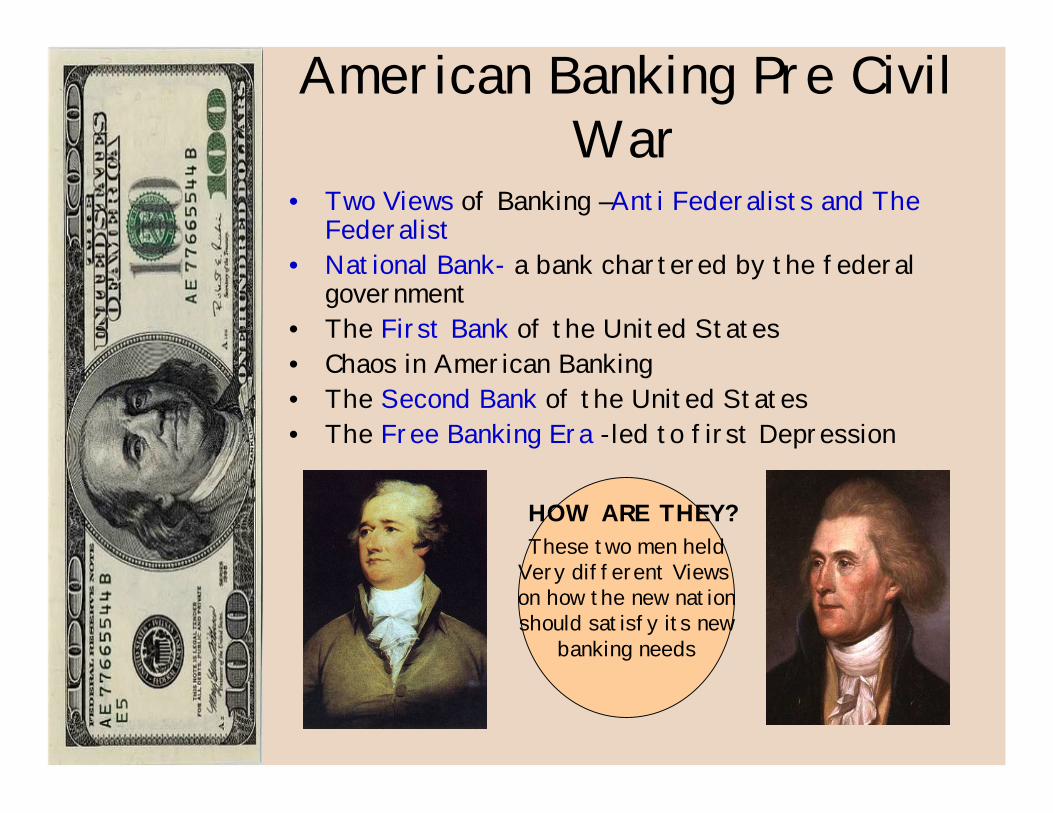

American Banking Pre Civil War

• Two Views of Banking –Anti Federalists and The Federalist

• National Bank- a bank chartered by the federal government

• The First Bank of the United States• Chaos in American Banking• The Second Bank of the United States• The Free Banking Era -led to first Depression

These two men heldVery different Views on how the new nationshould satisfy its new

banking needs

HOW ARE THEY?

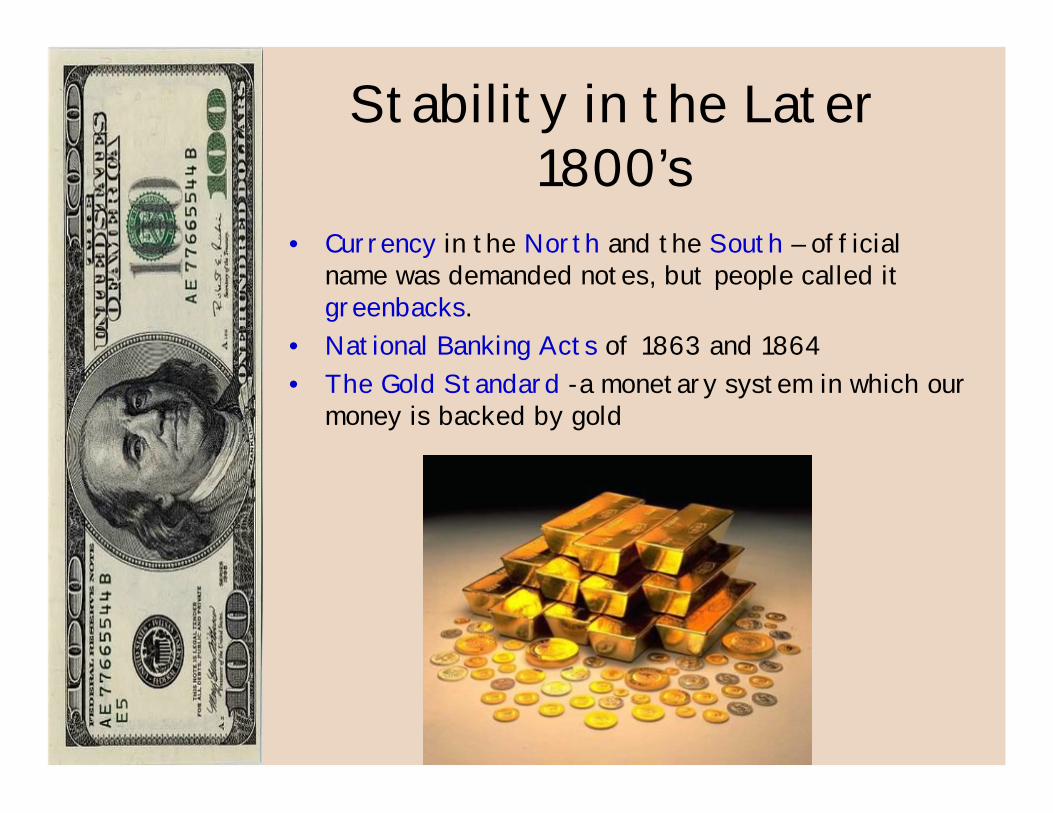

Stability in the Later 1800’s

• Currency in the North and the South – official name was demanded notes, but people called it greenbacks.

• National Banking Acts of 1863 and 1864• The Gold Standard -a monetary system in which our

money is backed by gold

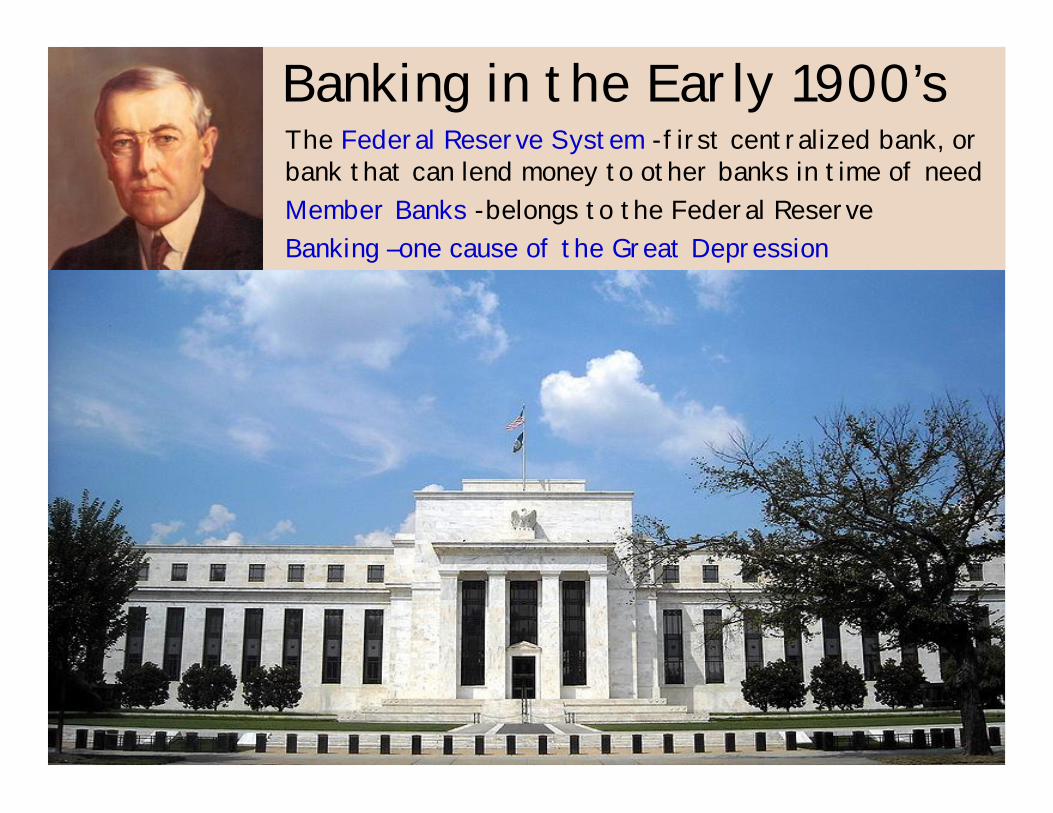

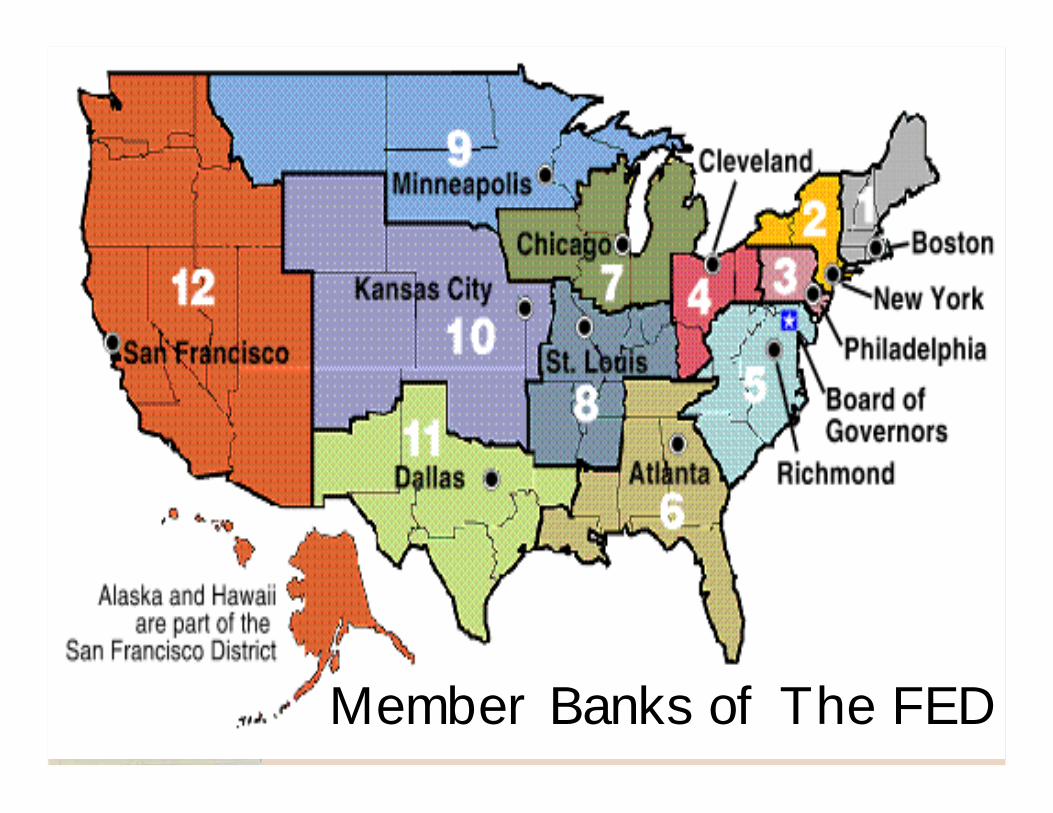

Banking in the Early 1900’s• The Federal Reserve System -first centralized bank, or

bank that can lend money to other banks in time of need• Member Banks -belongs to the Federal Reserve• Banking –one cause of the Great Depression

Member Banks of The FED

Two Crises For Banking• The Saving and Loans Crisis -Deregulation or to remove

restrictions on several industries that had ties to a class of banks known as S & L – long term loans at low rates

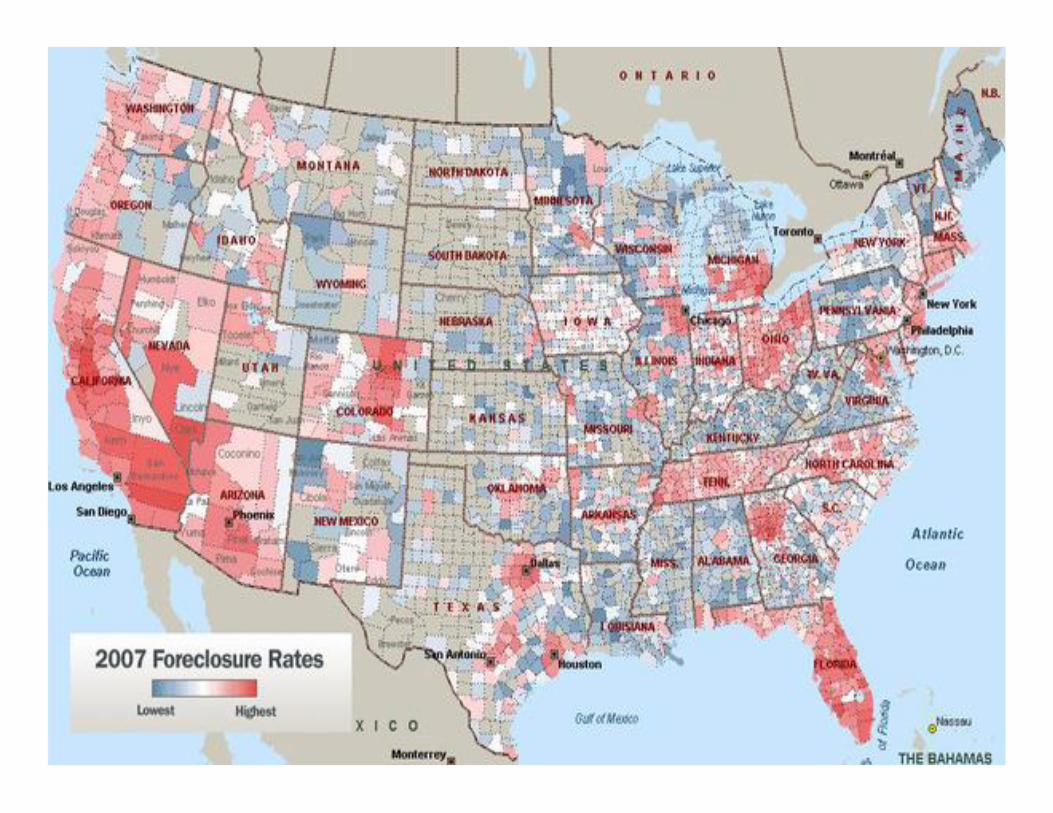

• In 2006, problems in the U.S. banking industries began to threaten the housing market and quickly spiraled us into a full-fledge crisis

• Foreclosures – a seizure of property from borrowers who are unable to repay their loans

Development in American Banking

In 2007, as a result of the subprime mortgage crisis is a sharp increase in the number of people who lose their homes because they can’t afford their mortgage.

2000s

Period of deregulation; saving and loans faced bankruptcies1980s

Period of regulation and long-term stability1940s-1960s

President Roosevelt helps restore confidence in the nation’s banks by establishing the FDIC

1933

The Great Depression Begins1929

President Wilson signs the Federal Reserve Act1913

National Banking Acts of 1863 and 1864 establish national banking system and uniform national currency

1863-1864

Civil War makes clear the need for a better monetary and bankingsystem

1861-1863

President Jackson vetoes re charter of Second Bank in 1832, giving rise to the Firs Banking Era

1830s-1860s

Second Bank of the United States reestablishes stability1816

Period of instability follows expiration of First Bank’s Charter1811-1816

First Bank of the United States is established.1791

The nation has no reliable medium of exchange. Federalists and Anti Federalists disagree

1780s

3. Banking Today• The Age of Electronic Banking - Good or Bad!!!

Measuring the Money Supply

• Money Supply – all the money available in the U.S. Economy

• M1 -money that people can gain access to easily and immediately to pay for goods and services– Liquidity -the ability to be used as cash– Demand deposit -money in checking account can

be used on demand• M2 -all assets in M1 plus several additional assets

(cant use directly)– Mutual funds -fund that pools money from small

savers to purchase short-term government and corporate securities

M1

$1,366.2Total M1 Money$6.7Traveler’s Checks$304.0Other Checkable Deposits$305.90Demand Deposits$749.60CurrencyBillionsM1 Components

Currency 55%

Demand Deposits 22%

Other CheckableDeposits 22.5%

Traveler's Check.005%

55%22.5%

22%

.5%

M2

$5,472.0Total M2$1,366.20Total M1

$398.7Small denomination time deposits

$805.0Retail Money Market Funds$2,902.10Saving DepositsBillionsM2 Components

Saving Deposit 53%

Retail Money Marketfunds 15%

Small demonination timedeposits 7%

Total M1 25%

53%7%

15%

25%

Functions of Financial Institutions• Storing Money -safe place for money• Saving Money -saving, checking, CD’s• Loans -personal, car, home improvements• Mortgages -loan to buy real estate• Credit Cards -buy goods and services and promise to pay it back with

interest• Simple and Compound Interest• Banks and Profits

$218.29$10.39$207.9015$171.04$8.14$162.9010$134.01$6.38$127.635$115.76$5.51$110.252

$110.25$5.25$105.001$105.00$5.00$100.00-

Principal at End of Year

Interest Earned at 5%

Principal Amount

End of Year

The chart at left shows the money earned on a $100 deposit when interest is compounded yearly at 5 percent. How many years does it take for the original deposit to double? After five years, what is the total interest that the deposit-holder will have earned?

Types of Financial Institutions• Commercial Banks -FDIC• Saving and Loans Associations -mostly homes• Savings Banks-small transaction banks• Credit Unions -cooperative lending associates• Finance Companies -installment loans to consumers

Money Enters Banks Money Leaves Bank

Bank retainsRequired services

Deposits from Customers

Interest from Borrowers

Fees for Services

Interest and WithdrawalsFrom Customers

Loans to borrowers

Bank Costs of Doing Business

Electronic Banking

• Automated Telling Machines ATM’s and Service Fees

• Debit Cards -a card to withdraw money with• Home Banking -Internet to conduct banking• Automated Clearing Houses• Stored-Valued Cards -college students

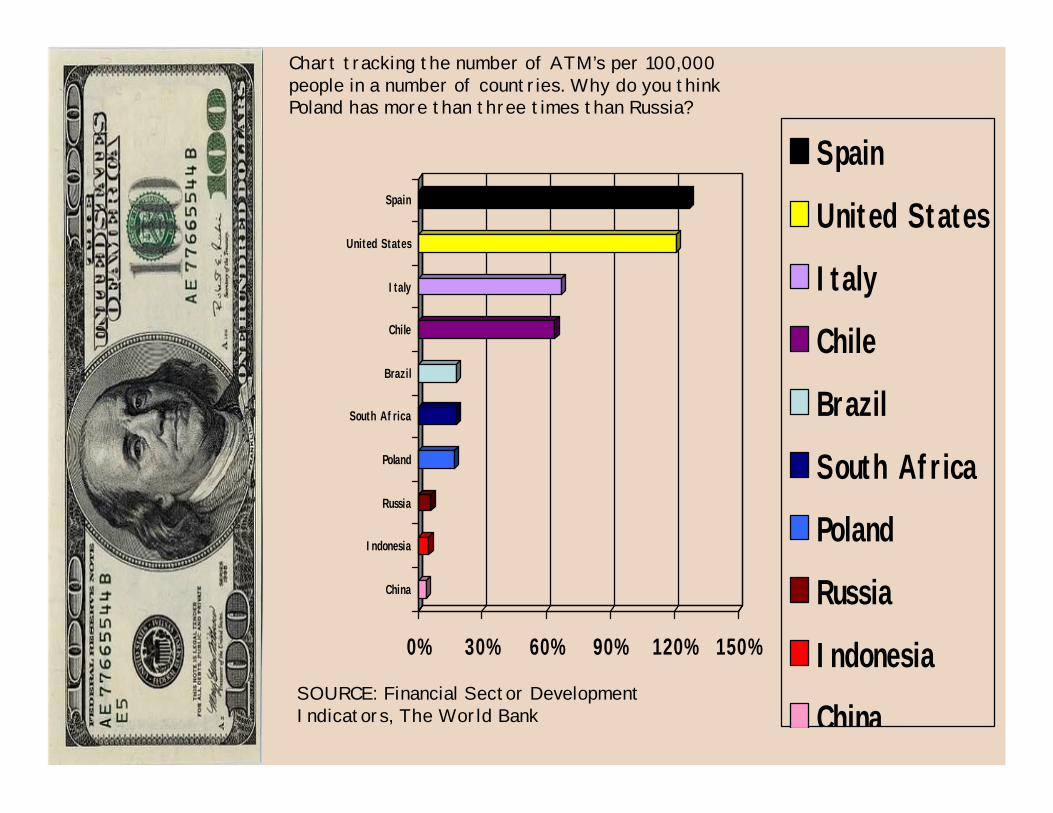

0% 30% 60% 90% 120% 150%

China

Indonesia

Russia

Poland

South Africa

Brazil

Chile

Italy

United States

Spain

Spain

United States

Italy

Chile

Brazil

South Africa

Poland

Russia

Indonesia

China

Chart tracking the number of ATM’s per 100,000 people in a number of countries. Why do you think Poland has more than three times than Russia?

SOURCE: Financial Sector Development Indicators, The World Bank

Development of U.S. Banking

1968Automatic teller machinesMaking deposits and withdrawals outside business hours

1909Development of credit unionsDifficult for people to get consumer credit

1946First bank issued credit cardNo convenient way of getting bank credit for small purchases

1933Federal Deposit Insurance Corporation

No insurance on saving deposits

1913Federal Reserve SystemNo central bank to monitor reserves

1913Federal Reserve SystemNo central decision making authority to regulate banks

1870sU.S. adopts gold standardGold did not support U.S. currency

1863, 1864National Banking ActsMany different currencies in U.S.

DateProblem Resolved byProblem