chapter 11 completing the audit “it ain’t over till it’s over.” – yogi berra, former...

TRANSCRIPT

Chapter 11

Completing the Audit

“It ain’t over till it’s over.”– Yogi Berra, former catcher for the New York Yankees

McGraw-Hill/Irwin

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Considerations in Completing the Audit

• Roll-forward work

• Revenue and expense accounts

• Attorney letters

• Management representations

• Going-concern assessment

• Adjusting entries

• Subsequent events

• Audit documentation review

• Subsequent discovery of facts

• Omitted audit procedures

• Management letter

• Communications with those charged with governance

11-2

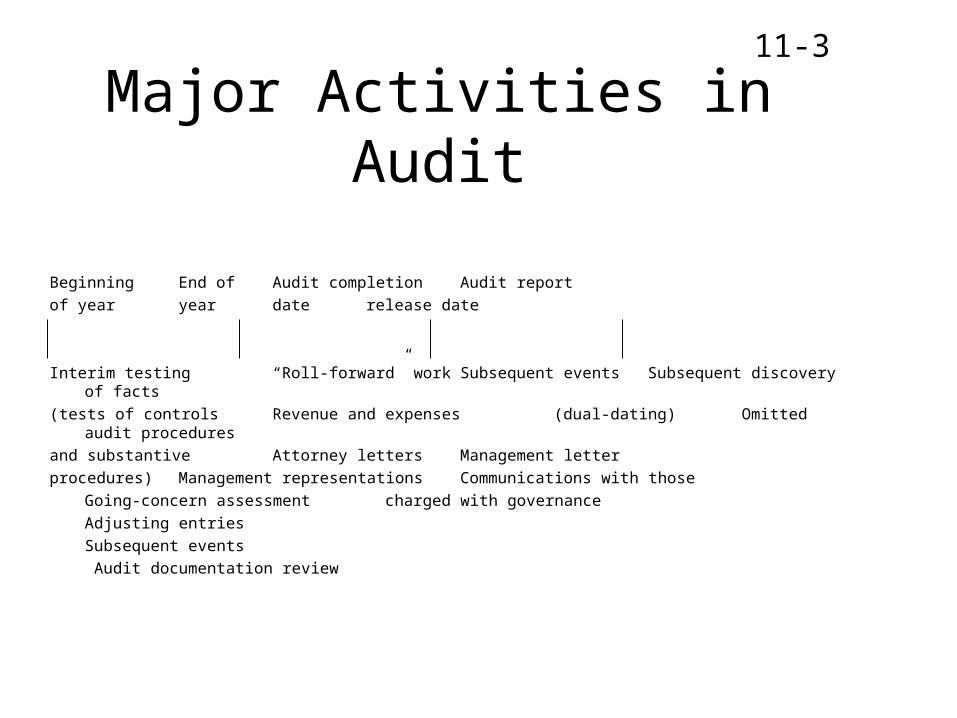

Major Activities in Audit

Beginning End of Audit completion Audit report

of year year date release date

Interim testing “Roll-forward” work Subsequent events Subsequent discovery of facts

(tests of controls Revenue and expenses (dual-dating) Omitted audit procedures

and substantive Attorney letters Management letter

procedures) Management representations Communications with those

Going-concern assessment charged with governance

Adjusting entries

Subsequent events

Audit documentation review

11-3

Activities Between End of Year and Audit Completion Date

• Revenue and expense accounts

• Attorney letters

• Management representations

• Subsequent events

• Audit documentation review

11-4

Revenue and Expense Accounts

• Substantive procedures for related balance sheet accounts

• Analytical procedures

• Scan accounts for large and unusual entries

• Be aware of “miscellaneous,” “other,” and “clearing” accounts – “earnings management”

11-5

Activities Between End of Year and Audit Completion Date

• Revenue and expense accounts

• Attorney letters

• Management representations

• Subsequent events

• Audit documentation review

11-6

Procedures for Litigation, Claims, and Assessments

• Inquiry of clients• Review minutes of meetings of stockholders,

directors, and committees• Review contracts, loan agreements, and

correspondence from taxing and governmental agencies

• Obtain information concerning guarantees from bank confirmations

• Review documentation related to legal services

11-7

Attorney Letters: Responsibilities

• Auditors– Initiate request for attorney letter

• Client– Prepare listing, description, and evaluation of litigation,

claims, and assessments for letter– Send letter to attorney including information related to

litigation, claims, and assessments• Attorney

– Respond to auditors regarding client’s description of litigation, claims, and assessments contained in attorney letter

11-8

Attorney Letters: Contents

• Listing of pending litigation, claims, and assessments

• Description of each item or case included in the listing

• Evaluation of the likelihood of an unfavorable outcome

• Estimate of the range of potential loss• Understanding regarding unasserted claims

11-9

Activities Between End of Year and Audit Completion Date

• Revenue and expense accounts

• Attorney letters

• Management representations

• Subsequent events

• Audit documentation review

11-10

Management Representations

• Provided by management to auditors• Dated using audit completion date• Broad purpose

– Impress upon management its primary responsibility for the financial statements

– May establish auditors’ defense if a question related to inquiries subsequently arises

• Qualify or disclaim an opinion if not provided by the client

11-11

Management Representations

• Required without regard to materiality:– Management responsibility for the fairness of the

financial statements

– Availability of all financial records and data

– Management responsibility for design and implementation of programs and controls related to fraud

– Disclosure of significant deficiencies in internal control

– Information concerning fraud involving the client

11-12

Representations Related to I/C

• If subject to requirements of AS 5– Management has performed as assessment of

I/C– Management’s conclusion with respect to the

operating effectiveness of its I/C– No subsequent changes in I/C that significantly

affect I/C– No control deficiencies from prior engagements

have not been properly resolved

11-13

Adjusting Journal Entries

• Accumulate proposed entries on “score sheet”• Consider pre tax and after tax effects• Require adjustment for all material entries• Require adjustment for proposed entries totaling a

material amount• Require adjustment for “qualitatively material”

entries• Recommend adjustment for all other items

11-14

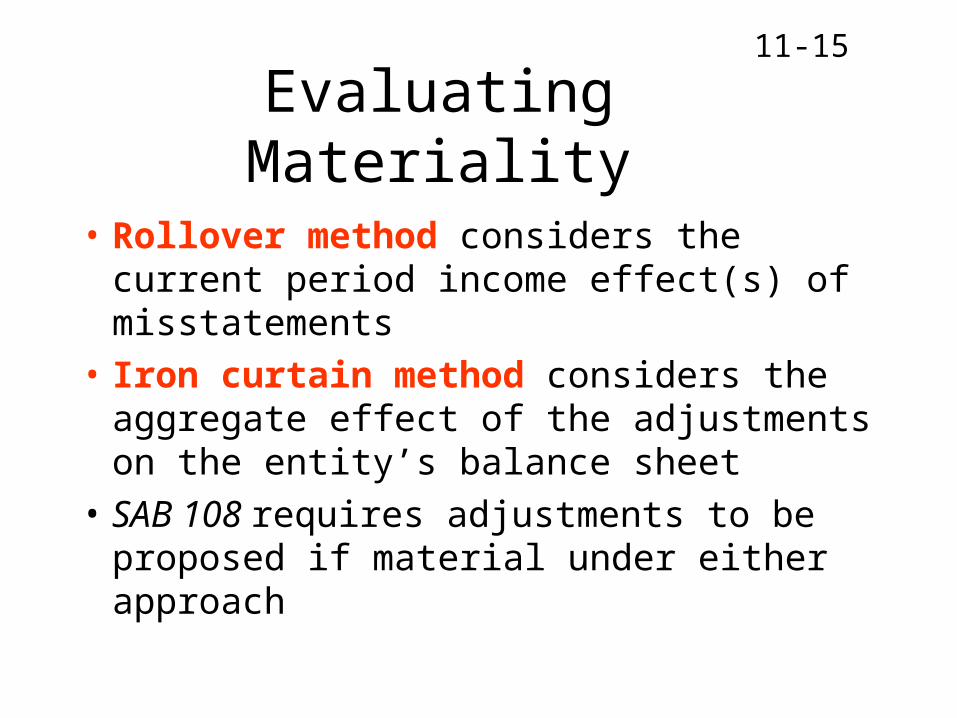

Evaluating Materiality

• Rollover method considers the current period income effect(s) of misstatements

• Iron curtain method considers the aggregate effect of the adjustments on the entity’s balance sheet

• SAB 108 requires adjustments to be proposed if material under either approach

11-15

Activities Between End of Year and Audit Completion Date

• Revenue and expense accounts

• Attorney letters

• Management representations

• Subsequent events

• Audit documentation review

11-16

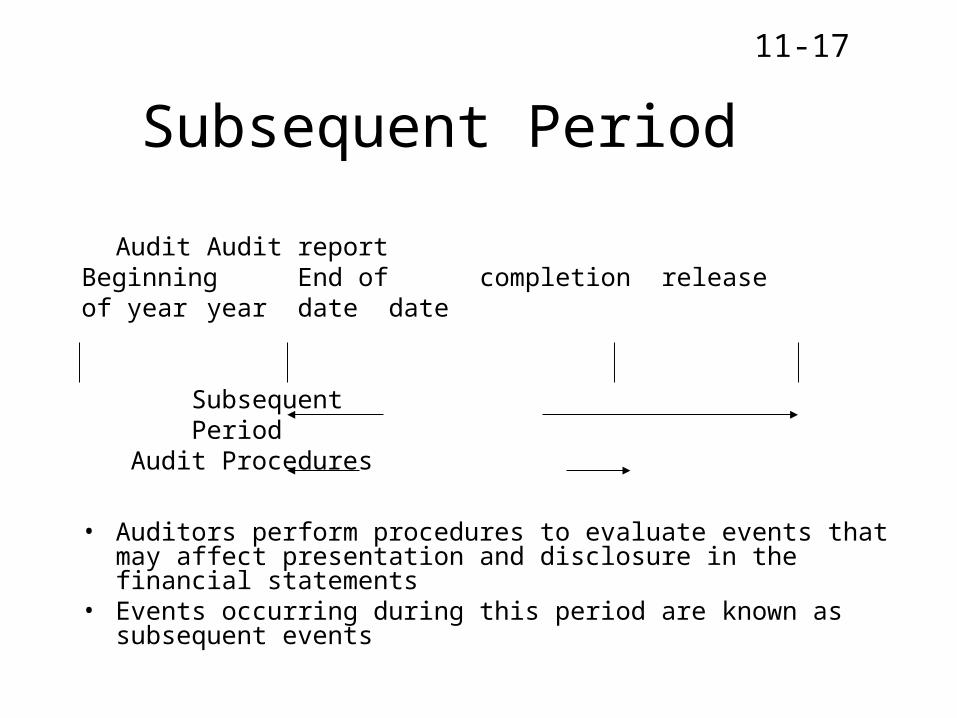

Subsequent Period

Audit Audit report

Beginning End of completion releaseof year year date date

Subsequent Period Audit Procedures

• Auditors perform procedures to evaluate events that may affect presentation and disclosure in the financial statements

• Events occurring during this period are known as subsequent events

11-17

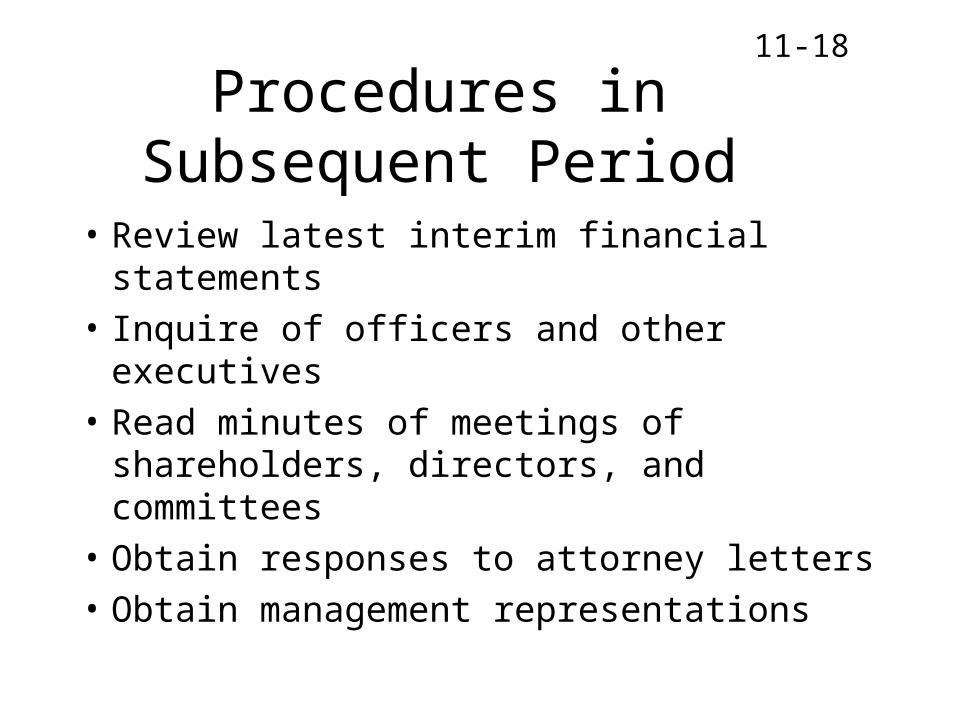

Procedures in Subsequent Period

• Review latest interim financial statements

• Inquire of officers and other executives

• Read minutes of meetings of shareholders, directors, and committees

• Obtain responses to attorney letters

• Obtain management representations

11-18

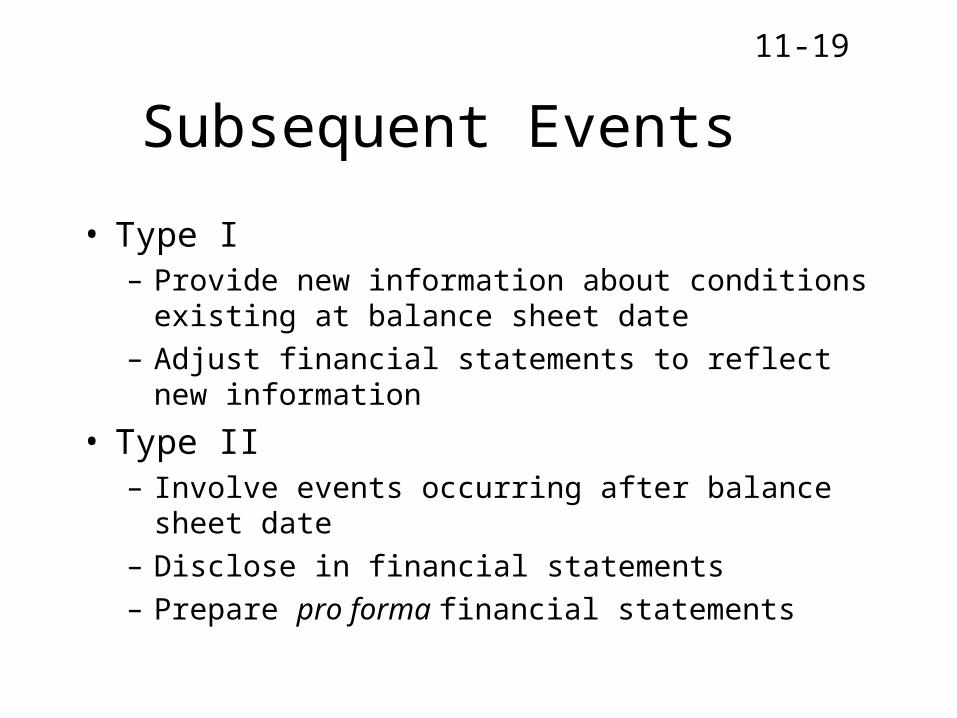

Subsequent Events

• Type I– Provide new information about conditions existing at

balance sheet date

– Adjust financial statements to reflect new information

• Type II– Involve events occurring after balance sheet date

– Disclose in financial statements

– Prepare pro forma financial statements

11-19

When are Subsequent Events Identified?

• Prior to audit completion date– Perform audit procedures and ensure proper

disclosure

• Following audit completion date but prior to audit report release date– Dual date audit report

• Following audit report release date – “Subsequent discovery of facts”

11-20

Activities Between End of Year and Audit Completion Date

• Revenue and expense accounts

• Attorney letters

• Management representations

• Subsequent events

• Audit documentation review

11-21

Audit Documentation Review

• Audit supervisor– Have all steps in audit program been performed?– Is referencing among documentation clear?– Are explanations understandable?

• Audit manager and partner– Is the overall scope of the audit adequate?– Do overall conclusions support the opinion?

• Reviewing partner– Are the quality of audit work and reporting consistent

with quality standards of the firm?

11-22

Activities Following Audit Report Release Date

• Subsequent discovery of facts

• Omitted procedures

• Communication with audit committee (or those charged with governance)

• Management letters

11-23

Subsequent Discovery of Facts

• Require disclosure of events if:– Facts are reliable and existed at report date

– Facts affect financial statements and auditors’ reports

– Persons are continuing to rely on financial statements and auditors’ reports

• If client refuses disclosure, auditors should inform board that he or she will notify regulatory agencies and others relying on the reports

11-24

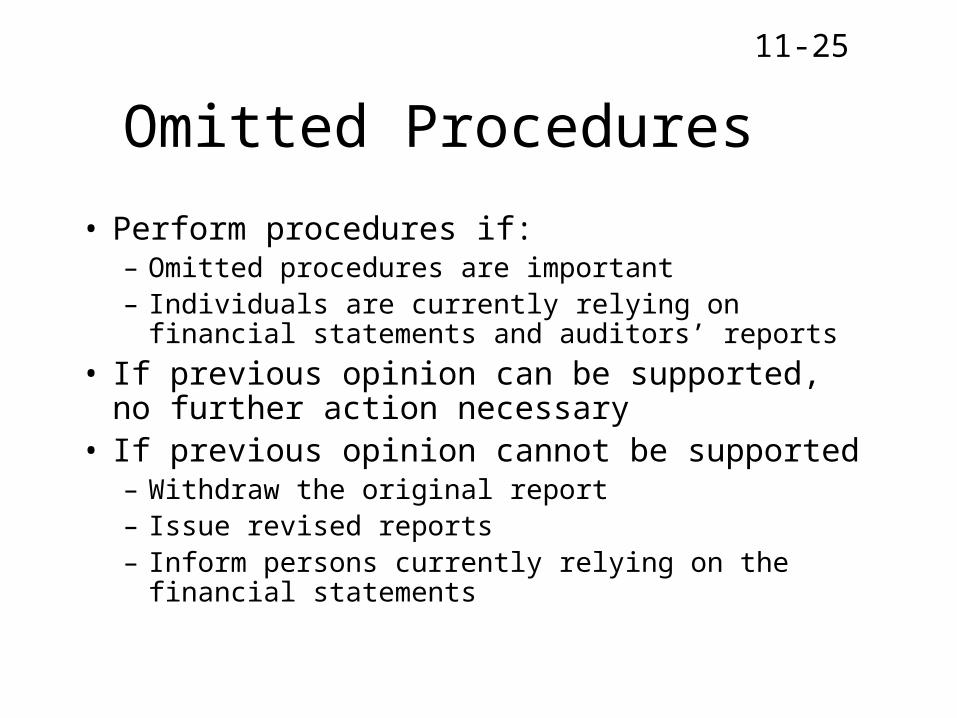

Omitted Procedures

• Perform procedures if:– Omitted procedures are important– Individuals are currently relying on financial statements and

auditors’ reports

• If previous opinion can be supported, no further action necessary

• If previous opinion cannot be supported– Withdraw the original report– Issue revised reports– Inform persons currently relying on the financial statements

11-25

Communication with Individuals Charged with Governance

• Auditors’ responsibility under GAAS

• Overview of planned scope and timing of audit

• Judgment about quality of accounting policies, estimates, and disclosures

• Significant difficulties encountered during audit

• Uncorrected misstatements• Disagreements with

management

• Material, uncorrected misstatements

• Representations requested from management

• Management consultations with other auditors

• Significant issues discussed with management

• Other findings or issues significant and relevant to those charged with governance

11-26

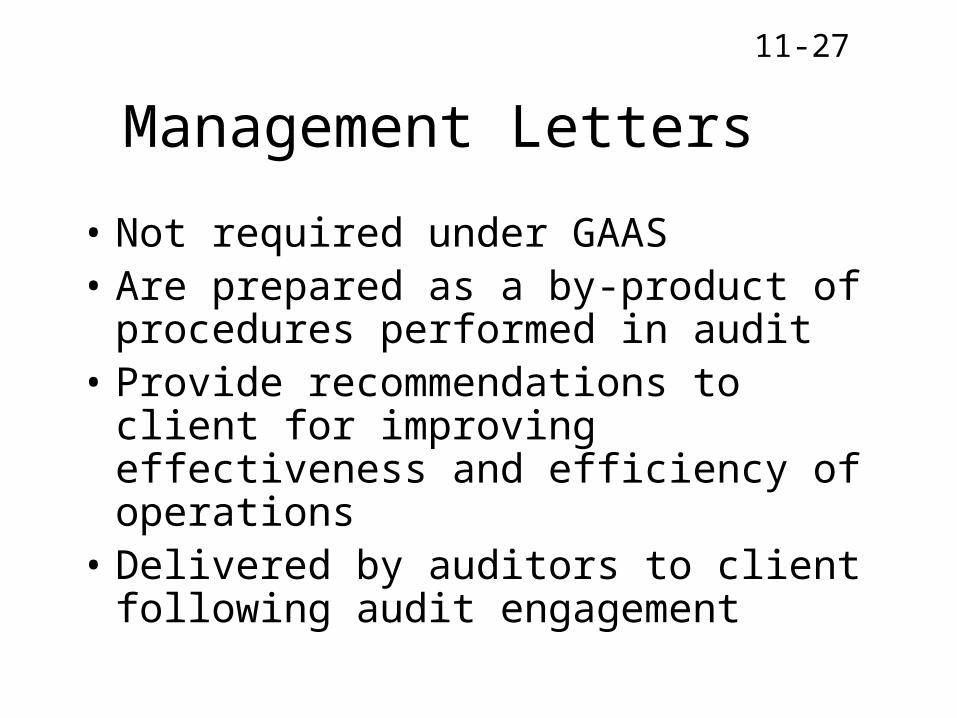

Management Letters

• Not required under GAAS• Are prepared as a by-product of procedures

performed in audit• Provide recommendations to client for

improving effectiveness and efficiency of operations

• Delivered by auditors to client following audit engagement

11-27

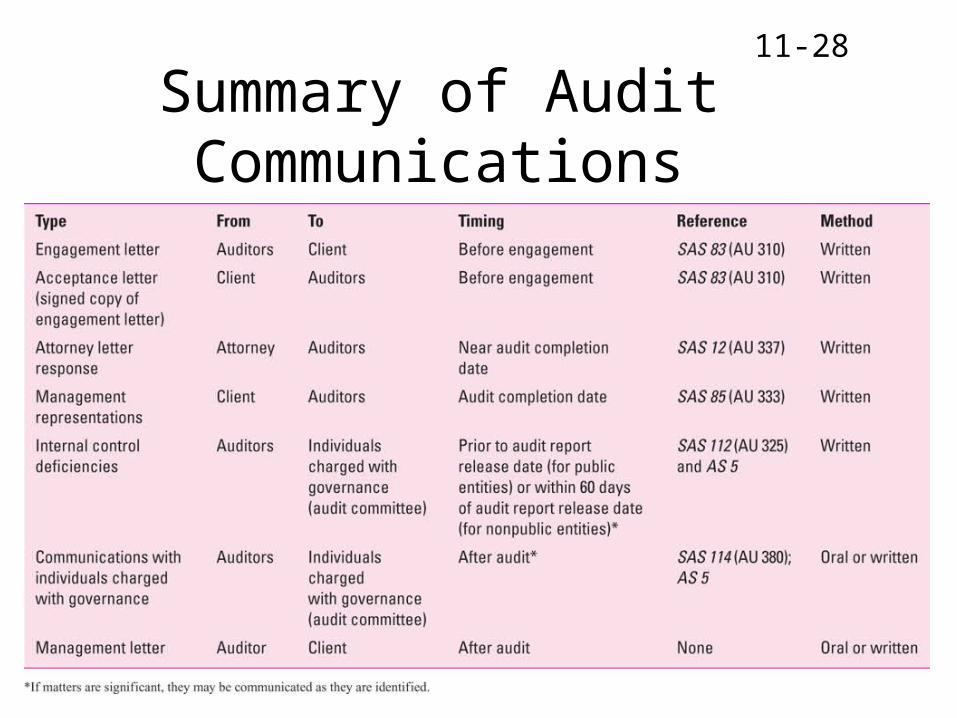

Summary of Audit Communications

11-28