chapter 11 economic analysis of banking regulation © 2005 pearson education canada inc

TRANSCRIPT

Chapter 11

Economic Analysis of Banking Regulation

© 2005 Pearson Education Canada Inc.

© 2005 Pearson Education Canada Inc. 11-2

How Asymmetric InformationExplains Banking Regulation

1. Government Safety Net and Deposit Insurance

A. Prevents bank runs due to asymmetric information: depositors can’t tell good from bad banks

B. Creates moral hazard incentives for banks to take on too much risk

C. Creates adverse selection problem of crooks and risk-takers wanting to control banks

D. Too-Big-to-Fail increases moral hazard incentives for big banks

2. Restrictions on Asset Holdings

A. Reduces moral hazard of too much risk taking

© 2005 Pearson Education Canada Inc. 11-3

3. Bank Capital Requirements

A. Reduces moral hazard: banks have more to lose when have higher capital

B. Higher capital means more collateral for FDIC

4. Bank Supervision: Chartering and Examination

A. Reduces adverse selection problem of risk takers or crooks owning banks

B. Reduces moral hazard by preventing risky activities

5. New Trend: Assessment of Risk Management

6. Disclosure Requirements

A. Better information reduces asymmetric information problem

How Asymmetric InformationExplains Banking Regulation

© 2005 Pearson Education Canada Inc. 11-4

3. Bank Capital RequirementsA. Reduces moral hazard: banks have more to lose when have

higher capitalB. Higher capital means more collateral for CDIC

4. Bank Supervision: Chartering and ExaminationA. Reduces adverse selection problem of risk takers or crooks

owning banksB. Reduces moral hazard by preventing risky activitiesC. New trend: Assessment of risk management

5. Disclosure RequirementsA. Better information reduces asymmetric information problem

How Asymmetric InformationExplains Banking Regulation

© 2005 Pearson Education Canada Inc. 11-5

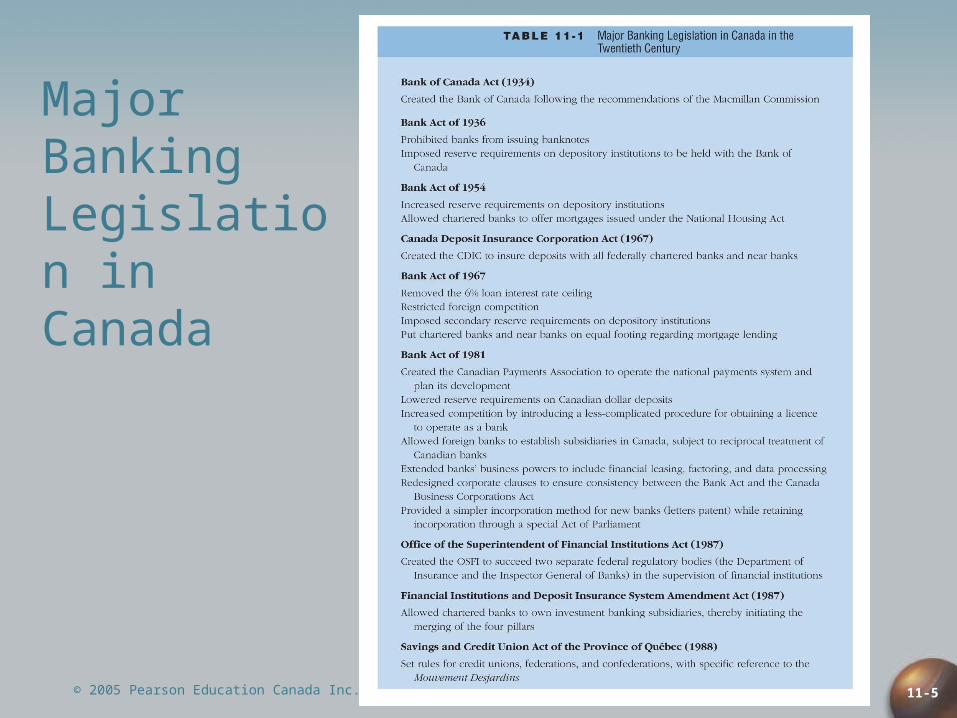

Major Banking Legislation in Canada

11-6

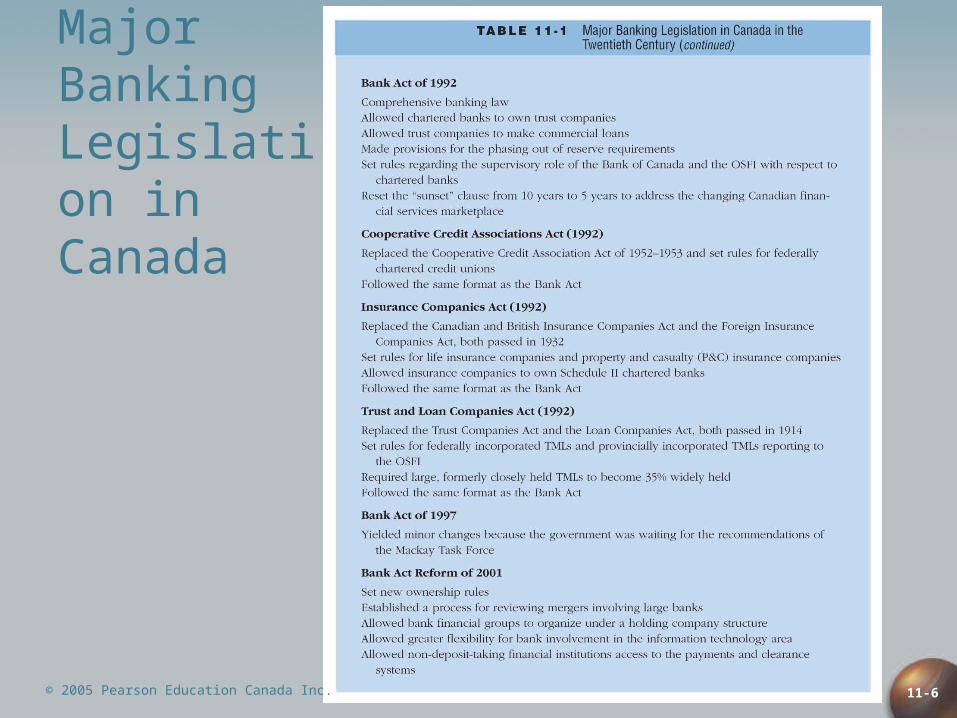

Major Banking Legislation in Canada

© 2005 Pearson Education Canada Inc.

© 2005 Pearson Education Canada Inc. 11-7

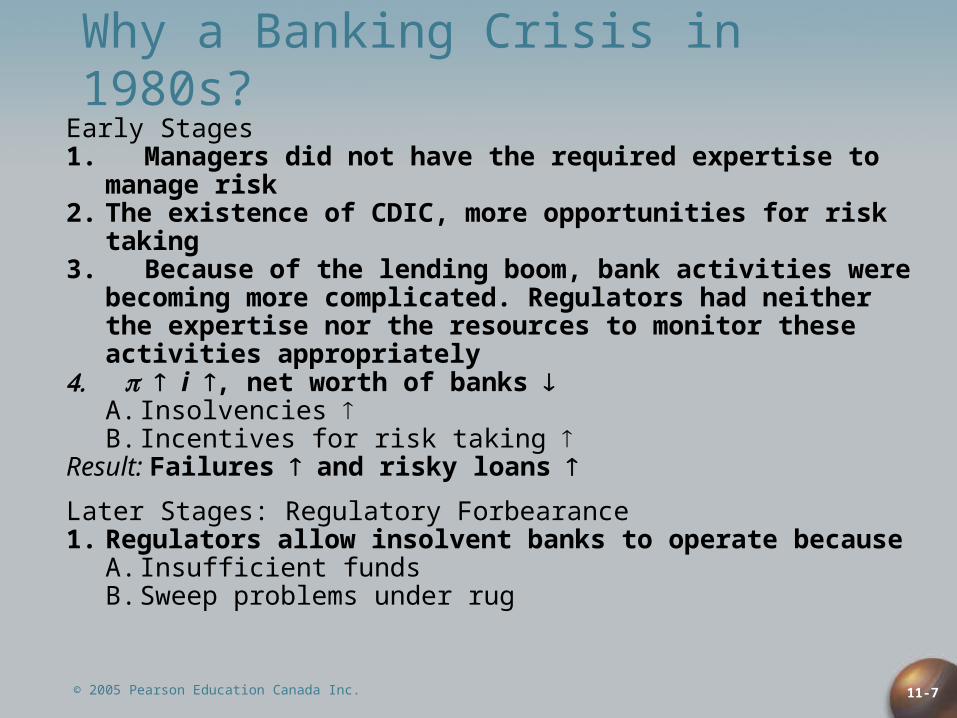

Why a Banking Crisis in 1980s?Early Stages1. Managers did not have the required expertise to manage risk2. The existence of CDIC, more opportunities for risk taking3. Because of the lending boom, bank activities were becoming

more complicated. Regulators had neither the expertise nor the resources to monitor these activities appropriately

i , net worth of banks A. Insolvencies B. Incentives for risk taking

Result: Failures and risky loans

Later Stages: Regulatory Forbearance1. Regulators allow insolvent banks to operate because

A. Insufficient funds B. Sweep problems under rug

© 2005 Pearson Education Canada Inc. 11-8

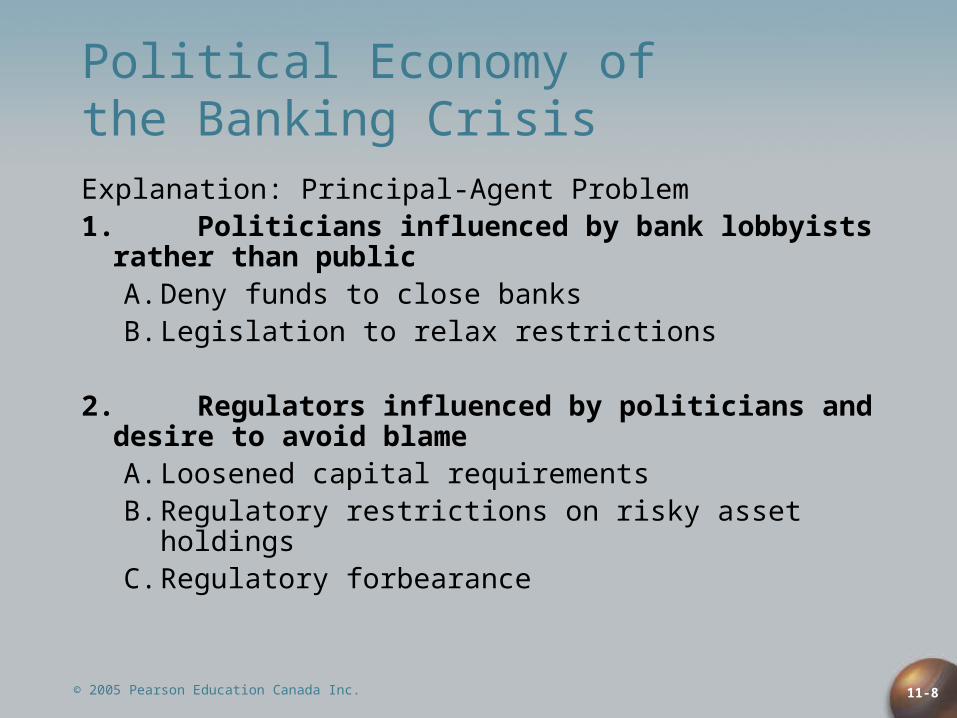

Political Economy ofthe Banking CrisisExplanation: Principal-Agent Problem1. Politicians influenced by bank lobbyists rather than

publicA. Deny funds to close banksB. Legislation to relax restrictions

2. Regulators influenced by politicians and desire to avoid blameA. Loosened capital requirementsB. Regulatory restrictions on risky asset holdingsC. Regulatory forbearance

© 2005 Pearson Education Canada Inc. 11-9

CDIC Developments

• CDIC insures each depositor at member institutions up to a loss of $60 000 per account

• All federally incorporated financial institutions and all provincially incorporated TMLs are members of the CDIC

• Insurance companies, credit unions, caisses populaires, and investment dealers are not eligible for CDIC membership

• QDIB insures provincially incorporated institutions in Québec and the other provinces have deposit insurance corporations that insure the deposits of credit unions in their jurisdiction

• CDIC insures only deposits in Canadian currency and payable in Canada; foreign currency deposits are not insured

• Not all deposits and investments offered by CDIC member institutions are insurable

© 2005 Pearson Education Canada Inc. 11-10

Not All Deposits Are Insurable

Insurable deposits include• Savings and chequing accounts• Term deposits with a maturity date < 5 years• Money orders and drafts, certified drafts and

cheques, and traveller’s chequesThe CDIC does not insure• Term deposits with an initial maturity date > 5 years• T-bills, bonds and debentures issued by governments

and corporations (including the chartered banks)• Investments in stocks, mutual funds, and mortgages.

© 2005 Pearson Education Canada Inc. 11-11

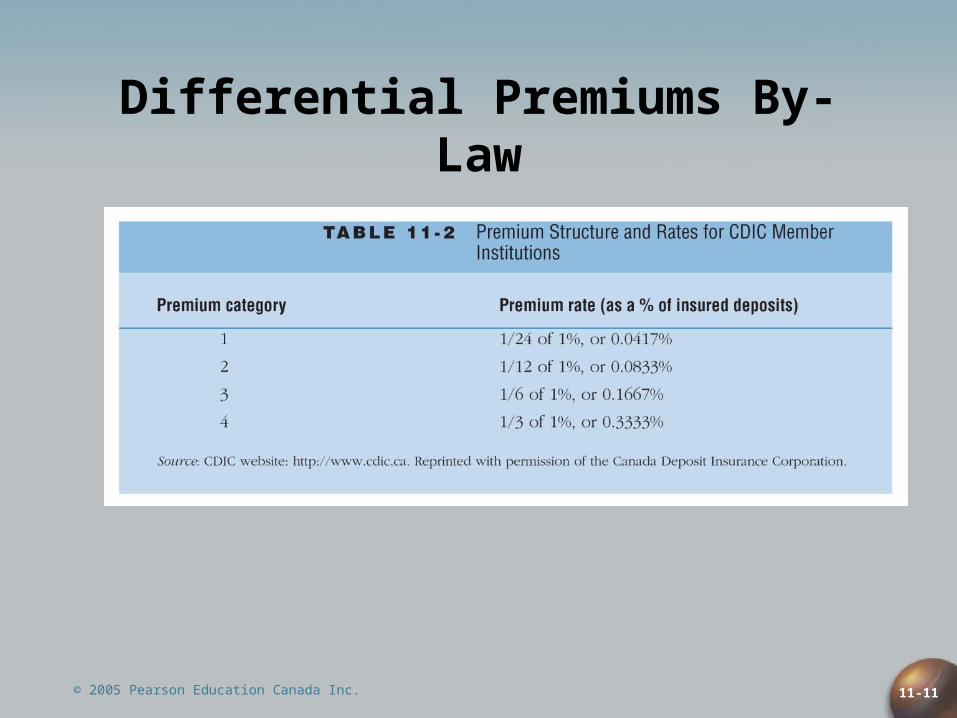

Differential Premiums By-Law

© 2005 Pearson Education Canada Inc. 11-12

Opting-Out By-Law

• Permits Schedule III banks, that accept primarily wholesale deposits (defined as $150 000 or more), to opt out of CDIC membership and therefore to operate without deposit insurance

• It requires, however, an opted-out bank to inform all depositors, by posting notices in its branches, that their deposits will not be protected by the CDIC, and not to charge any early withdrawal penalties for depositors who choose to withdraw

Implications:• Minimizes CDIC exposure to uninsured deposits• By compensating only the insured depositors rather than all

depositors, this legislation increases the incentives of uninsured depositors to monitor the risk-taking activities of banks, thereby reducing moral hazard risk

© 2005 Pearson Education Canada Inc. 11-13

Evaluating CDIC Limits on Scope of Deposit Insurance1. Eliminate deposit insurance entirely2. Lower limits on deposit insurance3. Eliminate too-big-to-fail4. Coinsurance

Prompt Corrective Action1. Critics believe too many loopholes2. However: accountability increased by mandatory review of

bank failure resolutions

Risk-based Insurance Premiums1. Hard to implement

Other Proposed Changes1. Regulatory consolidation2. Market-value accounting

© 2005 Pearson Education Canada Inc. 11-14

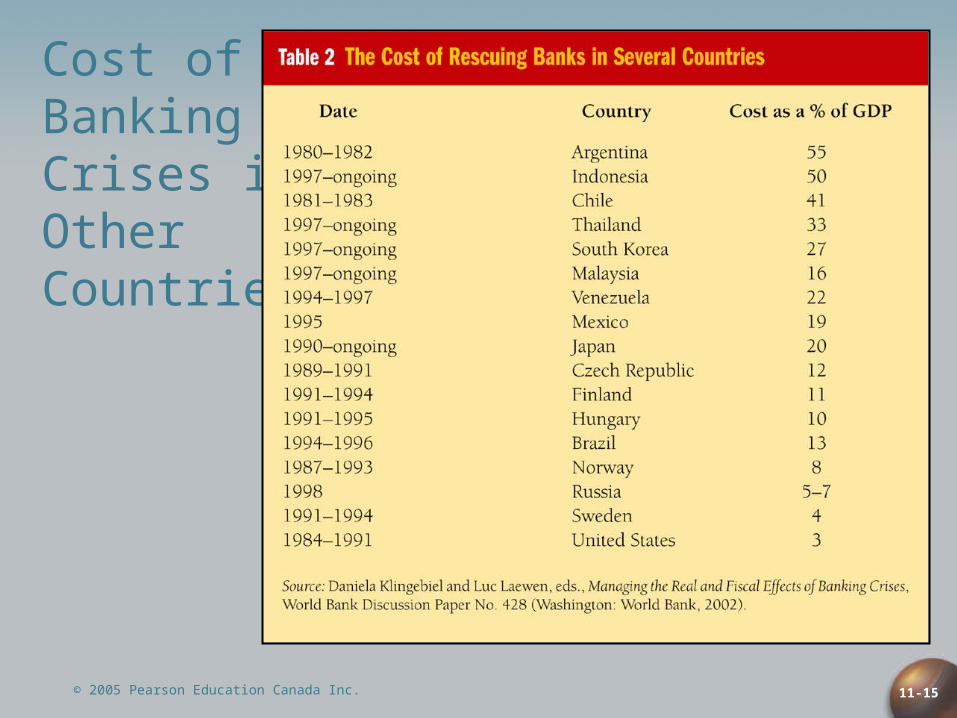

Banking Crises Worldwide

© 2005 Pearson Education Canada Inc. 11-15

Cost of Banking Crises in Other Countries