chapter 13 relevant costs for decision making - garrison

DESCRIPTION

Relevant costingDifferential AnalysisTRANSCRIPT

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-5

True/False Questions

1. Sunk costs are costs that have proven to be unproductive.

Ans: False AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Medium

2. All costs are avoidable in a decision except sunk costs and future costs that do not

differ between the alternatives at hand.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Easy

3. Consistency demands that a cost that is relevant in one decision be regarded as

relevant in other decisions as well.

Ans: False AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Medium

4. A cost may be relevant for one decision making situation but irrelevant for another

situation.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Easy

5. A future cost that does not vary among alternatives under consideration is irrelevant.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Easy

6. Opportunity costs represent economic benefits that are forgone as a result of pursuing

some course of action.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Easy

7. An existing asset should not be replaced until its original cost has been fully

recovered.

Ans: False AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Medium

Chapter 13 Relevant Costs for Decision Making

13-6 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

8. Fixed costs are irrelevant in decisions about whether a product line should be dropped.

Ans: False AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Easy

9. In a special order situation, any fixed cost associated with the order would be

irrelevant.

Ans: False AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 4 Level: Medium

10. When a company has a production constraint, total contribution margin will be

maximized by emphasizing the products with the highest contribution margin per unit

of the constrained resource.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Easy

11. Eliminating nonproductive time is particularly important in a bottleneck operation.

Ans: True AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Medium

12. One way to increase the effective utilization of a bottleneck is to reduce the number of

defective units.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Easy

13. As a general guide, it is profitable to continue processing joint products after the split-

off point if their total revenues exceed the joint costs.

Ans: False AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 6 Level: Medium

14. Joint costs are irrelevant in the decision of whether to sell a joint product at the split-

off point or process it further and then sell it.

Ans: True AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 6 Level: Easy

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-7

15. A key advantage of using activity-based costing is that any cost that is assigned to a

product is also a relevant cost in any decision involving that product.

Ans: False AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Easy

Multiple Choice Questions

16. Costs which can be eliminated in whole or in part if a particular business segment is

discontinued are called:

A) sunk costs.

B) opportunity costs.

C) avoidable costs.

D) irrelevant costs.

Ans: C AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Easy

17. Consider the following statements:

I. Assemble all costs associated with each alternative being considered.

II. Eliminate those costs that are sunk.

III. Eliminate those costs that differ between alternatives.

Which of the above statements does not represent a step in identifying the relevant

costs in a decision problem?

A) Only I

B) Only II

C) Only III

D) Only I and III

Ans: C AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Easy

Chapter 13 Relevant Costs for Decision Making

13-8 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

18. Which of the following cash flows is relevant in a decision about accepting

Alternative X or Alternative Y?

A) a cash inflow for Alternative X that is not a cash inflow for Alternative Y.

B) a cash inflow that is lost if Alternative X is accepted and is not lost if

Alternative Y is accepted.

C) a cash outflow that is avoided if Alternative X is accepted and is not avoided if

Alternative Y is accepted.

D) all of the above.

Ans: D AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Medium

19. Which of the following best describes an opportunity cost:

A) it is a relevant cost in decision making, but is not part of the traditional

accounting records.

B) it is not a relevant cost in decision making, but is part of the traditional

accounting records.

C) it is a relevant cost in decision making, and is part of the traditional accounting

records.

D) it is not a relevant cost in decision making, and is not part of the traditional

accounting records.

Ans: A AACSB: Reflective Thinking AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Medium

Source: CPA, adapted

20. Consider the following statements:

I. A division's net operating income, after deducting both traceable and allocated

common corporate costs, is negative.

II. The division's avoidable fixed costs exceed its contribution margin.

III. The division's traceable fixed costs plus its allocated common corporate costs

exceed its contribution margin.

Which of the above statements give an economic reason for eliminating the division?

A) Only I

B) Only II

C) Only III

D) Only I and II

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Easy

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-9

21. The Jabba Company manufactures the “Snack Buster” which consists of a wooden

snack chip bowl with an attached porcelain dip bowl. Which of the following would

be relevant in Jabba's decision to make the dip bowls or buy them from an outside

supplier?

Fixed overhead cost The variable

that can be eliminated if selling

the bowls are purchased cost of the

from the outside supplier Snack Buster

A) Yes Yes

B) Yes No

C) No Yes

D) No No

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

22. The acceptance of a special order will improve overall net operating income so long as

the revenue from the special order exceeds:

A) the contribution margin on the order.

B) the incremental costs associated with the order.

C) the variable costs associated with the order.

D) the sunk costs associated with the order.

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 4 Level: Medium

23. Kinsi Corporation manufactures five different products. All five of these products

must pass through a stamping machine in its fabrication department. This machine is

Kinsi's constrained resource. Kinsi would make the most profit if it produces the

product that:

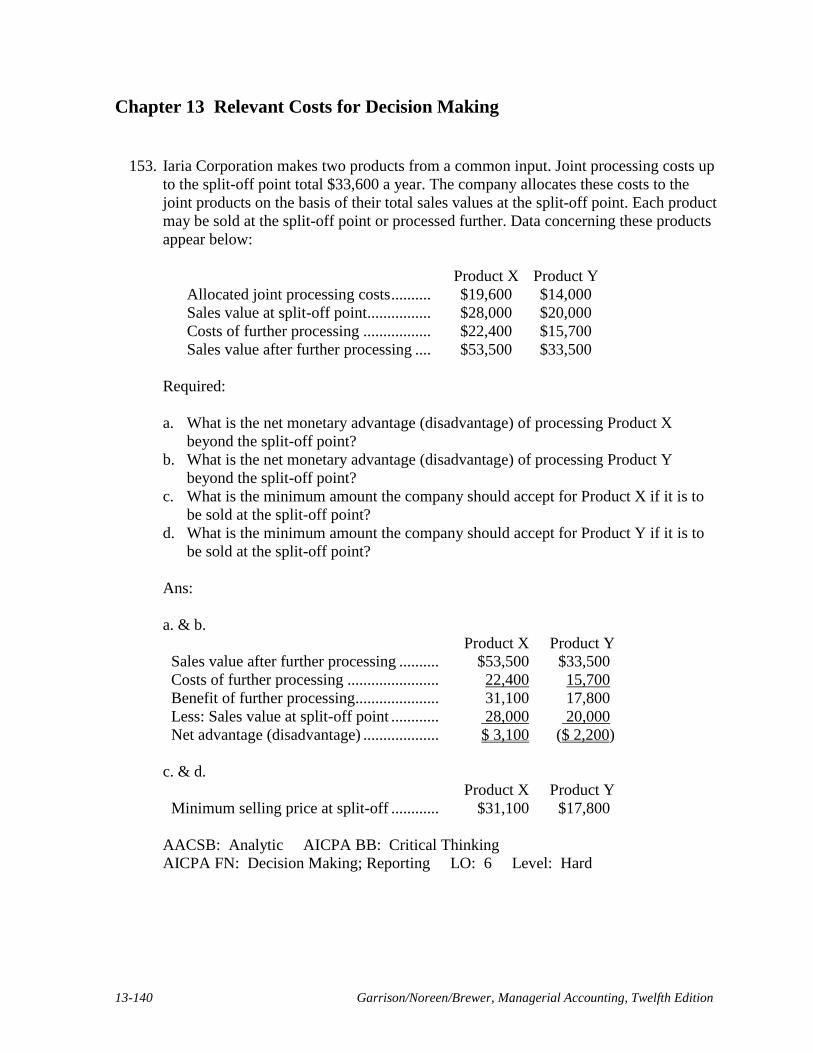

A) uses the lowest number of stamping machine hours.

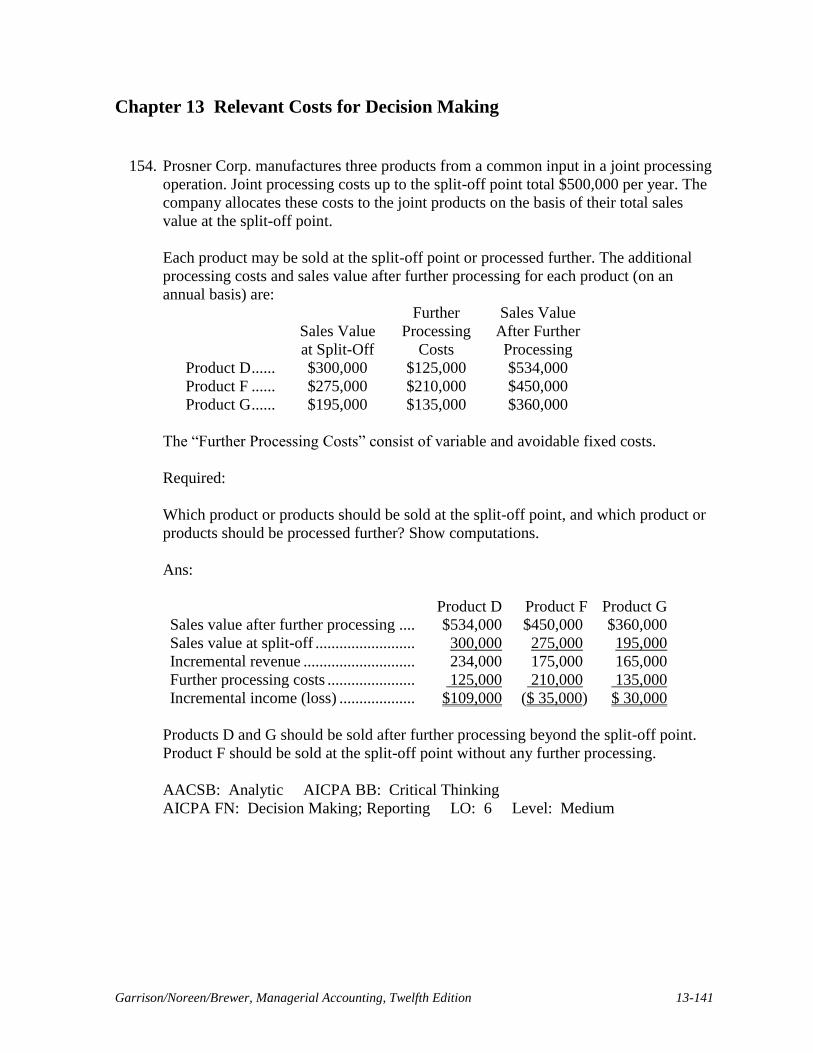

B) generates the highest contribution margin per unit.

C) generates the highest contribution margin ratio.

D) generates the highest contribution margin per stamping machine hour.

Ans: D AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Medium

Chapter 13 Relevant Costs for Decision Making

13-10 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

24. In a sell or process further decision, consider the following costs:

I. A variable production cost incurred prior to split-off.

II. A variable production cost incurred after split-off.

III. An avoidable fixed production cost incurred after split-off.

Which of the above costs is (are) not relevant in a decision regarding whether the

product should be processed further?

A) Only I

B) Only III

C) Only I and II

D) Only I and III

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 6 Level: Easy

25. Gandy Company has 5,000 obsolete desk lamps that are carried in inventory at a

manufacturing cost of $50,000. If the lamps are reworked for $20,000, they could be

sold for $35,000. Alternatively, the lamps could be sold for $8,000 for scrap. In a

decision model analyzing these alternatives, the sunk cost would be:

A) $8,000

B) $15,000

C) $20,000

D) $50,000

Ans: D AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Easy

Source: CPA, adapted

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-11

26. Hodge Inc. has some material that originally cost $74,600. The material has a scrap

value of $57,400 as is, but if reworked at a cost of $1,500, it could be sold for

$54,400. What would be the incremental effect on the company's overall profit of

reworking and selling the material rather than selling it as is as scrap?

A) -$79,100

B) -$21,700

C) -$4,500

D) $52,900

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Medium

Source: CIMA, adapted

Solution:

Incremental revenue from reworking ($54,400 − $1,500) $52,900

Less incremental revenue from selling as scrap ................ 57,400

Net loss from reworking .................................................... ($ 4,500)

27. Milford Corporation has in stock 16,100 kilograms of material R that it bought five

years ago for $5.75 per kilogram. This raw material was purchased to use in a product

line that has been discontinued. Material R can be sold as is for scrap for $3.91 per

kilogram. An alternative would be to use material R in one of the company's current

products, S88Y, which currently requires 2 kilograms of a raw material that is

available for $7.60 per kilogram. Material R can be modified at a cost of $0.77 per

kilogram so that it can be used as a substitute for this material in the production of

product S88Y. However, after modification, 4 kilograms of material R is required for

every unit of product S88Y that is produced. Milford Corporation has now received a

request from a company that could use material R in its production process. Assuming

that Milford Corporation could use all of its stock of material R to make product S88Y

or the company could sell all of its stock of the material at the current scrap price of

$3.91 per kilogram, what is the minimum acceptable selling price of material R to the

company that could use material R in its own production process?

A) $0.88

B) $3.03

C) $4.57

D) $3.91

Ans: D AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Hard

Source: CIMA, adapted

Chapter 13 Relevant Costs for Decision Making

13-12 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Solution:

Product S88Y:

Current cost (2 kg @ $7.60): $15.20

If material R were used, 4 kilograms would be needed. It currently costs $15.20 for

Product S88Y; to maintain this same cost, material R would need to cost $3.03 per

kilogram [($15.20 ÷ 4 kg) − $0.77]. The company should sell material R for $3.91 per

kilogram.

28. Otool Inc. is considering using stocks of an old raw material in a special project. The

special project would require all 240 kilograms of the raw material that are in stock

and that originally cost the company $2,112 in total. If the company were to buy new

supplies of this raw material on the open market, it would cost $9.25 per kilogram.

However, the company has no other use for this raw material and would sell it at the

discounted price of $8.35 per kilogram if it were not used in the special project. The

sale of the raw material would involve delivery to the purchaser at a total cost of

$71.00 for all 240 kilograms. What is the relevant cost of the 240 kilograms of the raw

material when deciding whether to proceed with the special project?

A) $1,933

B) $2,004

C) $2,220

D) $2,112

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Hard

Source: CIMA, adapted

Solution:

Opportunity cost of sales foregone if special project is

undertaken ($8.35 × 240) .............................................. $2,004

Less: delivery cost ............................................................. 71

Relevant cost of 240 kilograms of raw material ............... $1,933

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-13

29. Hamby Corporation is preparing a bid for a special order that would require 780 liters

of material W34C. The company already has 640 liters of this raw material in stock

that originally cost $8.30 per liter. Material W34C is used in the company's main

product and is replenished on a periodic basis. The resale value of the existing stock of

the material is $7.60 per liter. New stocks of the material can be readily purchased for

$8.35 per liter. What is the relevant cost of the 780 liters of the raw material when

deciding how much to bid on the special order?

A) $6,481

B) $6,376

C) $6,513

D) $5,928

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Hard

Source: CIMA, adapted

Solution:

Relevant cost = $8.35 per liter × 780 liters = $6,513

30. Schickel Inc. regularly uses material B39U and currently has in stock 460 liters of the

material for which it paid $3,128 several weeks ago. If this were to be sold as is on the

open market as surplus material, it would fetch $5.95 per liter. New stocks of the

material can be purchased on the open market for $6.45 per liter, but it must be

purchased in lots of 1,000 liters. You have been asked to determine the relevant cost of

760 liters of the material to be used in a job for a customer. The relevant cost of the

760 liters of material B39U is:

A) $4,902

B) $4,672

C) $4,522

D) $6,450

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Hard

Source: CIMA, adapted

Solution:

Relevant cost = $6.45 per liter × 760 liters = $4,902

Chapter 13 Relevant Costs for Decision Making

13-14 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

31. Munafo Corporation is a specialty component manufacturer with idle capacity.

Management would like to use its extra capacity to generate additional profits. A

potential customer has offered to buy 6,500 units of component VGI. Each unit of

VGI requires 1 unit of material I57 and 5 units of material M97. Data concerning these

two materials follow:

Material

Units in

Stock

Original

Cost Per

Unit

Current

Market

Price

Per Unit

Disposal

Value

Per Unit

I57 ....... 2,400 $9.10 $9.40 $8.95

M97 ..... 33,960 $4.70 $4.70 $3.50

Material I57 is in use in many of the company's products and is routinely replenished.

Material M97 is no longer used by the company in any of its normal products and

existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials, in total, for purposes of determining

a minimum acceptable price for the order for product VGI?

A) $174,850

B) $213,130

C) $213,850

D) $171,925

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Hard

Source: CIMA, adapted

Solution:

Material

# Required

per unit

Relevant

price Total

I57 ............... 1 × $9.40 = $ 9.40

M97 ............. 5 × $3.50 = 17.50

Total per unit relevant cost ...................... $26.90

Minimum acceptable price for 6,500 units of VGI =

$26.90 per unit × 6,500 units = $174,850

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-15

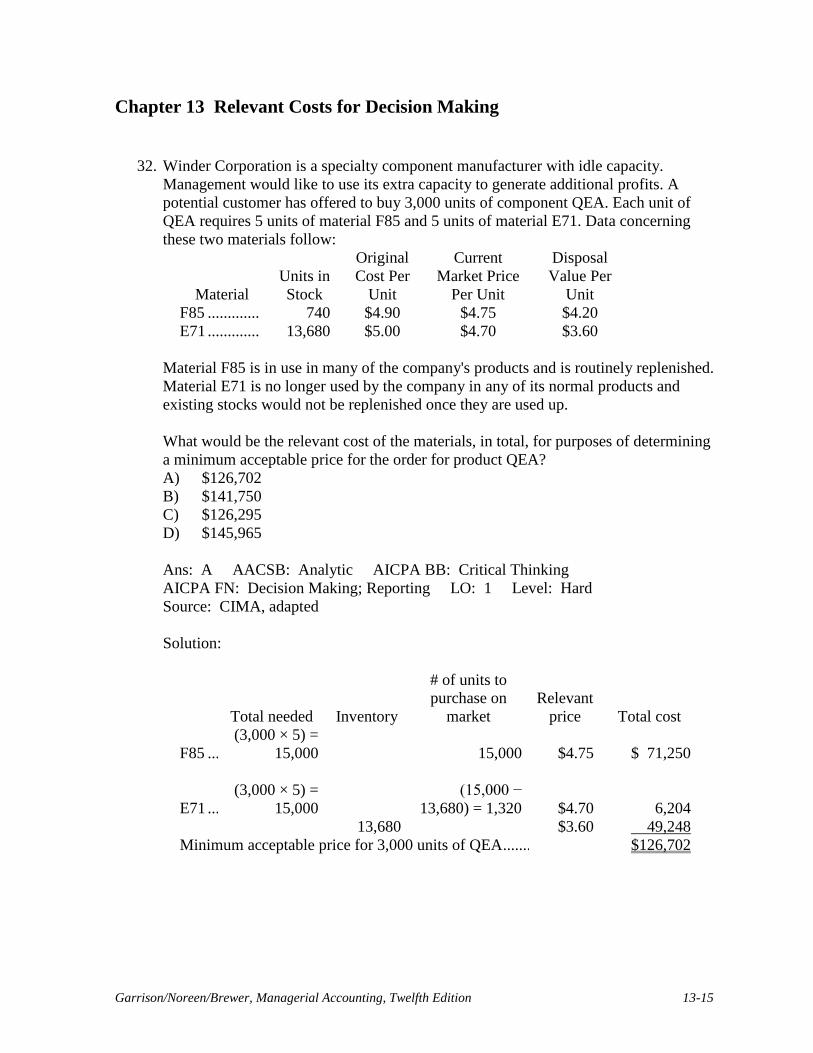

32. Winder Corporation is a specialty component manufacturer with idle capacity.

Management would like to use its extra capacity to generate additional profits. A

potential customer has offered to buy 3,000 units of component QEA. Each unit of

QEA requires 5 units of material F85 and 5 units of material E71. Data concerning

these two materials follow:

Material

Units in

Stock

Original

Cost Per

Unit

Current

Market Price

Per Unit

Disposal

Value Per

Unit

F85 ............. 740 $4.90 $4.75 $4.20

E71 ............. 13,680 $5.00 $4.70 $3.60

Material F85 is in use in many of the company's products and is routinely replenished.

Material E71 is no longer used by the company in any of its normal products and

existing stocks would not be replenished once they are used up.

What would be the relevant cost of the materials, in total, for purposes of determining

a minimum acceptable price for the order for product QEA?

A) $126,702

B) $141,750

C) $126,295

D) $145,965

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 1 Level: Hard

Source: CIMA, adapted

Solution:

Total needed Inventory

# of units to

purchase on

market

Relevant

price Total cost

F85 .............

(3,000 × 5) =

15,000 15,000 $4.75 $ 71,250

E71 .............

(3,000 × 5) =

15,000

(15,000 −

13,680) = 1,320 $4.70 6,204

13,680 $3.60 49,248

Minimum acceptable price for 3,000 units of QEA ........... $126,702

Chapter 13 Relevant Costs for Decision Making

13-16 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

33. Rice Corporation currently operates two divisions which had operating results last

year as follows:

West Troy

Division Division

Sales .......................................................... $600,000 $300,000

Variable costs ............................................ 310,000 200,000

Contribution margin .................................. 290,000 100,000

Traceable fixed costs ................................. 110,000 70,000

Allocated common corporate costs ........... 90,000 45,000

Net operating income (loss) ...................... $ 90,000 ($ 15,000)

Since the Troy Division also sustained an operating loss in the prior year, Rice's

president is considering the elimination of this division. Troy Division's traceable

fixed costs could be avoided if the division were eliminated. The total common

corporate costs would be unaffected by the decision. If the Troy Division had been

eliminated at the beginning of last year, Rice Corporation's operating income for last

year would have been:

A) $15,000 higher

B) $30,000 lower

C) $45,000 lower

D) $60,000 higher

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Medium

Source: CPA, adapted

Solution:

Troy Division:

Contribution margin .......................................................... $100,000

Less: traceable fixed costs ................................................. 70,000

Segment margin of Troy Division .................................... $ 30,000

Rice Corporation’s operating income would have been $30,000 less without the

segment margin contributed by the Troy Division.

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-17

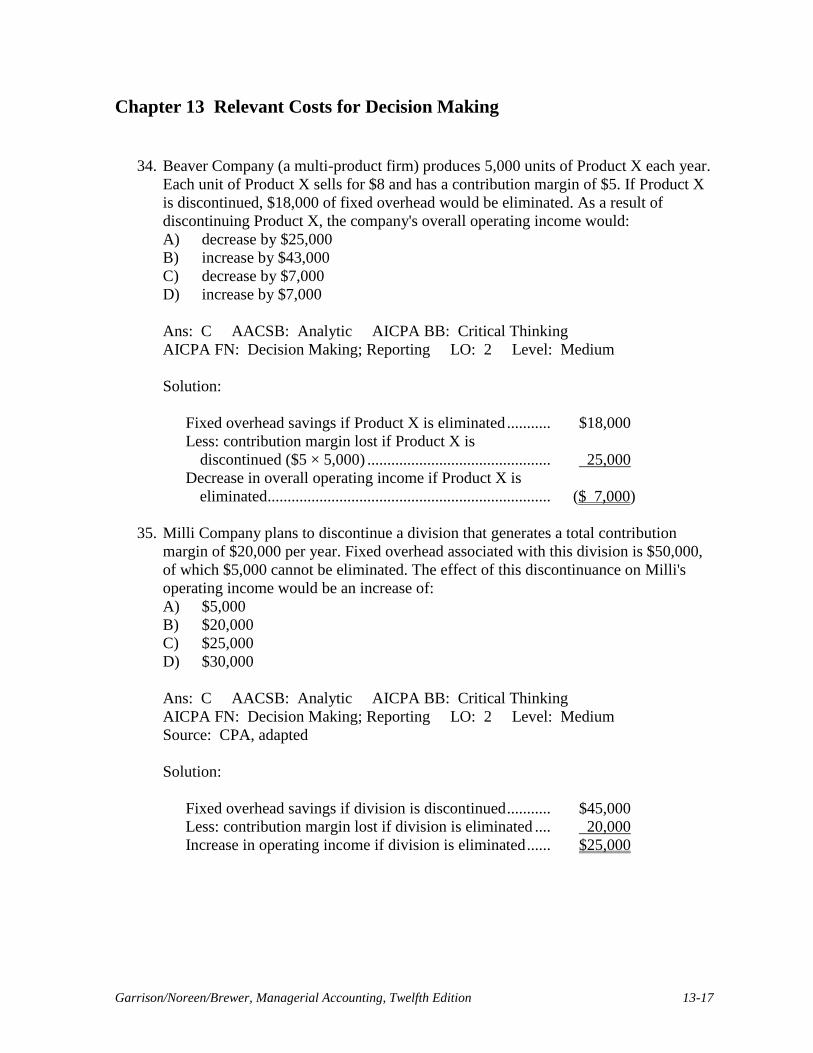

34. Beaver Company (a multi-product firm) produces 5,000 units of Product X each year.

Each unit of Product X sells for $8 and has a contribution margin of $5. If Product X

is discontinued, $18,000 of fixed overhead would be eliminated. As a result of

discontinuing Product X, the company's overall operating income would:

A) decrease by $25,000

B) increase by $43,000

C) decrease by $7,000

D) increase by $7,000

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Medium

Solution:

Fixed overhead savings if Product X is eliminated ........... $18,000

Less: contribution margin lost if Product X is

discontinued ($5 × 5,000) .............................................. 25,000

Decrease in overall operating income if Product X is

eliminated ....................................................................... ($ 7,000)

35. Milli Company plans to discontinue a division that generates a total contribution

margin of $20,000 per year. Fixed overhead associated with this division is $50,000,

of which $5,000 cannot be eliminated. The effect of this discontinuance on Milli's

operating income would be an increase of:

A) $5,000

B) $20,000

C) $25,000

D) $30,000

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Medium

Source: CPA, adapted

Solution:

Fixed overhead savings if division is discontinued ........... $45,000

Less: contribution margin lost if division is eliminated .... 20,000

Increase in operating income if division is eliminated ...... $25,000

Chapter 13 Relevant Costs for Decision Making

13-18 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

36. ABD Realty manages five apartment complexes in its region. Shown below are

summary income statements for each apartment complex:

U V W X Y

Rental income .......... $1,000 $1,210 $2,347 $1,878 $1,065

Expenses ................... 800 1,300 2,600 2,400 1,300

Operating income ..... $ 200 ($ 90) ($ 253) ($ 522) ($ 235)

Included in the expenses is $1,200 of common corporate expenses that have been

allocated to the apartment complexes based on rental income. These common

corporate expenses would have to be incurred regardless of how many apartment

complexes ABD Realty manages. The apartment complex(es) that ABD Realty should

consider dropping is (are):

A) V, W, X, Y

B) W, X, Y

C) X, Y

D) X

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Hard

Source: CMA, adapted

Solution:

Total rental income = $1,000 + $1,210 + $2,347 + $1,878 + $1,065 = $7,500

U V W X Y

Rental income .......... $1,000 $1,210 $2,347 $1,878 $1,065

Less expenses ........... 800 1,300 2,600 2,400 1,300

Add back proportional

share of common

expenses [(Rental

income in each

column ÷ Total

rental income of

$7,500) × $1,200]* 160 194 376 300 170

Apartment complex

margin $ 360 $ 104 $ 123 ($222) ($ 65)

*expenses rounded to nearest whole dollar

Since complexes X and Y have negative margins, ABD Realty should consider

dropping those two divisions.

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-19

37. The following information relates to next year's projected operating results of the

Children's Division of Grunge Clothing Corporation:

Contribution margin .......... $200,000

Fixed expenses .................. 500,000

Net operating loss .............. ($300,000)

If Children's Division is dropped, half of the fixed costs above can be eliminated.

What will be the effect on Grunge's profit next year if Children's Division is dropped

instead of being kept?

A) $50,000 increase

B) $250,000 increase

C) $250,000 decrease

D) $550,000 increase

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Medium

Solution:

Keep the

Division

Drop the

Division Difference

Contribution margin ...................... $200,000 $ 0 ($200,000)

Fixed expenses .............................. 500,000 250,000 250,000

Net operating income (loss) .......... ($300,000) ($250,000) ($ 50,000)

Net operating income would increase by $50,000 if the Children’s Division were

dropped. Therefore, the division should be dropped.

Chapter 13 Relevant Costs for Decision Making

13-20 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

38. The management of Furrow Corporation is considering dropping product L07E. Data

from the company's accounting system appear below:

Sales ...................................................................... $830,000

Variable expenses ................................................. $365,000

Fixed manufacturing expenses .............................. $291,000

Fixed selling and administrative expenses ............ $166,000

In the company's accounting system all fixed expenses of the company are fully

allocated to products. Further investigation has revealed that $186,000 of the fixed

manufacturing expenses and $106,000 of the fixed selling and administrative expenses

are avoidable if product L07E is discontinued. What would be the effect on the

company's overall net operating income if product L07E were dropped?

A) Overall net operating income would increase by $8,000.

B) Overall net operating income would decrease by $173,000.

C) Overall net operating income would decrease by $8,000.

D) Overall net operating income would increase by $173,000.

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Easy

Solution:

Keep the

Product

Drop the

Product Difference

Sales .............................................. $830,000 $ 0 ($830,000)

Variable expenses ......................... 365,000 0 365,000

Contribution margin ...................... 465,000 0 (465,000)

Fixed expenses:

Fixed manufacturing expenses ... 291,000 *105,000 186,000

Fixed selling and administrative

expenses.................................. 166,000 **60,000 106,000

Total fixed expenses ...................... 457,000 165,000 292,000

Net operating income (loss) .......... $ 8,000 ($165,000) ($173,000)

Net operating income would decline by $173,000 if product L07E were dropped.

Therefore, the product should not be dropped.

*$291,000 − $186,000 = $105,000

**$166,000 − $106,000 = $60,000

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-21

39. Product U23N has been considered a drag on profits at Jinkerson Corporation for

some time and management is considering discontinuing the product altogether. Data

from the company's accounting system appear below:

Sales ....................................................................... $730,000

Variable expenses .................................................. $350,000

Fixed manufacturing expenses .............................. $234,000

Fixed selling and administrative expenses ............ $161,000

In the company's accounting system all fixed expenses of the company are fully

allocated to products. Further investigation has revealed that $144,000 of the fixed

manufacturing expenses and $93,000 of the fixed selling and administrative expenses

are avoidable if product U23N is discontinued. What would be the effect on the

company's overall net operating income if product U23N were dropped?

A) Overall net operating income would increase by $15,000.

B) Overall net operating income would increase by $143,000.

C) Overall net operating income would decrease by $143,000.

D) Overall net operating income would decrease by $15,000.

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 2 Level: Easy

Solution:

Keep the

Product

Drop the

Product Difference

Sales ............................................... $730,000 $ 0 ($730,000)

Variable expenses .......................... 350,000 0 350,000

Contribution margin ...................... 380,000 0 ( 380,000)

Fixed expenses:

Fixed manufacturing expenses ... 234,000 *90,000 144,000

Fixed selling and administrative

expenses .................................. 161,000 **68,000 93,000

Total fixed expenses ...................... 395,000 158,000 237,000

Net operating income (loss) .......... ($ 15,000) ($ 158,000) ($143,000)

Net operating income would decline by $143,000 if product U23N were dropped.

Therefore, the product should not be dropped.

*$234,000 − $144,000 = $90,000

**$161,000 − $93,000 = $68,000

Chapter 13 Relevant Costs for Decision Making

13-22 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

40. Supler Company produces a part used in the manufacture of one of its products. The

unit product cost is $18, computed as follows:

Direct materials ......................................... $ 8

Direct labor ............................................... 4

Variable manufacturing overhead ............. 1

Fixed manufacturing overhead .................. 5

Unit product cost ....................................... $18

An outside supplier has offered to provide the annual requirement of 4,000 of the parts

for only $14 each. It is estimated that 60 percent of the fixed overhead cost above

could be eliminated if the parts are purchased from the outside supplier. Based on

these data, the per-unit dollar advantage or disadvantage of purchasing from the

outside supplier would be:

A) $1 disadvantage

B) $1 advantage

C) $2 advantage

D) $4 disadvantage

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

Solution:

Relevant cost per unit:

Direct materials ............................................... $ 8

Direct labor ..................................................... 4

Variable manufacturing overhead ................... 1

Fixed manufacturing overhead ($5 × 0.60) ..... 3

Relevant manufacturing cost ........................... $16

Net advantage (disadvantage):

Relevant manufacturing cost savings ........ $16

Less: cost from outside supplier ................ 14

Net advantage ............................................ $ 2

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-23

41. Sharp Company produces 8,000 parts each year, which are used in the production of

one of its products. The unit product cost of a part is $36, computed as follows:

Variable production costs ........ $16

Fixed production costs ............. 20

Unit product cost ..................... $36

The parts can be purchased from an outside supplier for only $28 each. The space in

which the parts are now produced would be idle and fixed production costs would be

reduced by one-fourth. If the parts are purchased from the outside supplier, the annual

impact on the company's operating income will be:

A) $24,000 increase

B) $24,000 decrease

C) $56,000 increase

D) $56,000 decrease

Ans: D AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

Solution:

Relevant cost per unit:

Variable production costs ................................ $16

Fixed manufacturing overhead ($20 × 0.25) ... 5

Relevant manufacturing cost ........................... $21

Relevant manufacturing cost savings ($21 × 8,000) ............ $168,000

Less: cost to purchase from outside supplier ($28 × 8,000) . 224,000

Net disadvantage of purchasing from outside supplier ........ ($ 56,000)

Chapter 13 Relevant Costs for Decision Making

13-24 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

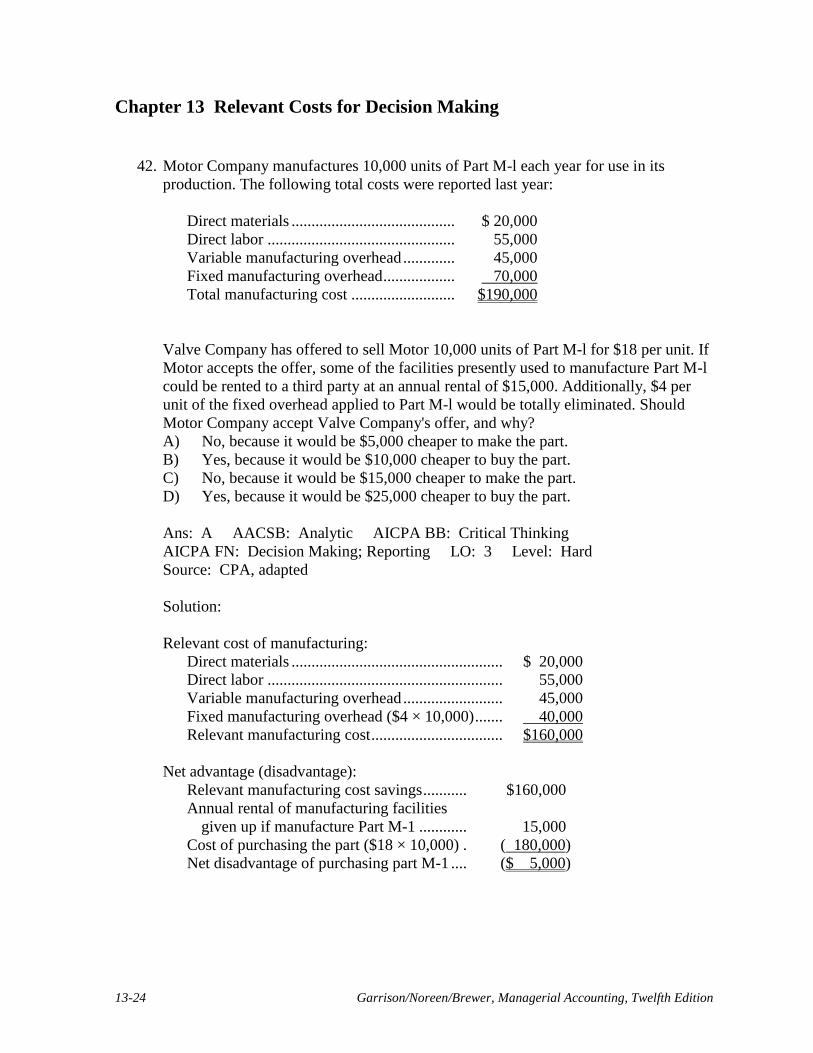

42. Motor Company manufactures 10,000 units of Part M-l each year for use in its

production. The following total costs were reported last year:

Direct materials ......................................... $ 20,000

Direct labor ............................................... 55,000

Variable manufacturing overhead ............. 45,000

Fixed manufacturing overhead .................. 70,000

Total manufacturing cost .......................... $190,000

Valve Company has offered to sell Motor 10,000 units of Part M-l for $18 per unit. If

Motor accepts the offer, some of the facilities presently used to manufacture Part M-l

could be rented to a third party at an annual rental of $15,000. Additionally, $4 per

unit of the fixed overhead applied to Part M-l would be totally eliminated. Should

Motor Company accept Valve Company's offer, and why?

A) No, because it would be $5,000 cheaper to make the part.

B) Yes, because it would be $10,000 cheaper to buy the part.

C) No, because it would be $15,000 cheaper to make the part.

D) Yes, because it would be $25,000 cheaper to buy the part.

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Hard

Source: CPA, adapted

Solution:

Relevant cost of manufacturing:

Direct materials ..................................................... $ 20,000

Direct labor ........................................................... 55,000

Variable manufacturing overhead ......................... 45,000

Fixed manufacturing overhead ($4 × 10,000) ....... 40,000

Relevant manufacturing cost ................................. $160,000

Net advantage (disadvantage):

Relevant manufacturing cost savings ........... $160,000

Annual rental of manufacturing facilities

given up if manufacture Part M-1 ............ 15,000

Cost of purchasing the part ($18 × 10,000) . ( 180,000)

Net disadvantage of purchasing part M-1 .... ($ 5,000)

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-25

43. Kingston Company needs 10,000 units of a certain part to be used in its production

cycle. The following information is available concerning Kingston's unit product cost:

Direct materials ......................................... $ 6

Direct labor ................................................ 24

Variable manufacturing overhead ............. 12

Fixed manufacturing overhead .................. 15

Unit product cost ....................................... $57

Utica Company has offered to supply Kingston's entire annual requirements of the part

for $53 each. If Kingston buys the part from Utica instead of making it, Kingston

would have no other use for the facilities and 60 percent of the fixed manufacturing

overhead would continue. In deciding whether to make or buy the part, the total

relevant costs to make the part internally are:

A) $342,000

B) $480,000

C) $530,000

D) $570,000

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

Source: CPA, adapted

Solution:

Relevant cost per unit:

Direct materials ............................................... $ 6

Direct labor ...................................................... 24

Variable manufacturing overhead ................... 12

Fixed manufacturing overhead ($15 × 0.40) ... 6

Relevant manufacturing cost ........................... $48

Total relevant costs to make the part internally ($48 × 10,000) = $480,000

Chapter 13 Relevant Costs for Decision Making

13-26 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

44. The following standard costs pertain to a component part manufactured by Bor

Company:

Direct materials ....................... $ 4

Direct labor ............................. 10

Manufacturing overhead ......... 40

Standard cost per unit .............. $54

An outside supplier has offered to supply all of the parts needed by Bor Company for

$50 each. The 60% of the manufacturing overhead cost that is fixed would be

unaffected by this decision. In the decision to “make or buy,” what is the relevant unit

cost to make the part internally?

A) $54

B) $38

C) $30

D) $5

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

Source: CPA, adapted

Solution:

Relevant cost per unit:

Direct materials ......................................... $ 4

Direct labor ............................................... 10

Manufacturing overhead ($40 × 0.40) ...... 16

Relevant manufacturing cost ..................... $30

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-27

45. Gordon Company produces 1,000 units of a part per year which are used in the

assembly of one of its products. The unit cost of producing these parts is:

Variable manufacturing cost ......... $15

Fixed manufacturing cost .............. 12

Total manufacturing cost ............... $27

The part can be purchased from an outside supplier at $20 per unit. If the part is

purchased from the outside supplier, two thirds of the total fixed costs incurred in

producing the part can be eliminated. The annual increase or decrease on the

company's operating incomes as a result of buying the part from the outside supplier

would be:

A) $3,000 increase

B) $1,000 decrease

C) $7,000 increase

D) $5,000 decrease

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

Solution:

Relevant cost per unit:

Variable production costs ................................ $15

Fixed manufacturing overhead ($12 × 2/3) ..... 8

Relevant manufacturing cost ........................... $23

Net advantage (disadvantage) per unit:

Manufacturing cost savings ....................... $23

Cost of purchasing the part ........................ 20

Net advantage (disadvantage) ................... $ 3

Total = $3 × 1,000 units = $3000 increase

Chapter 13 Relevant Costs for Decision Making

13-28 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

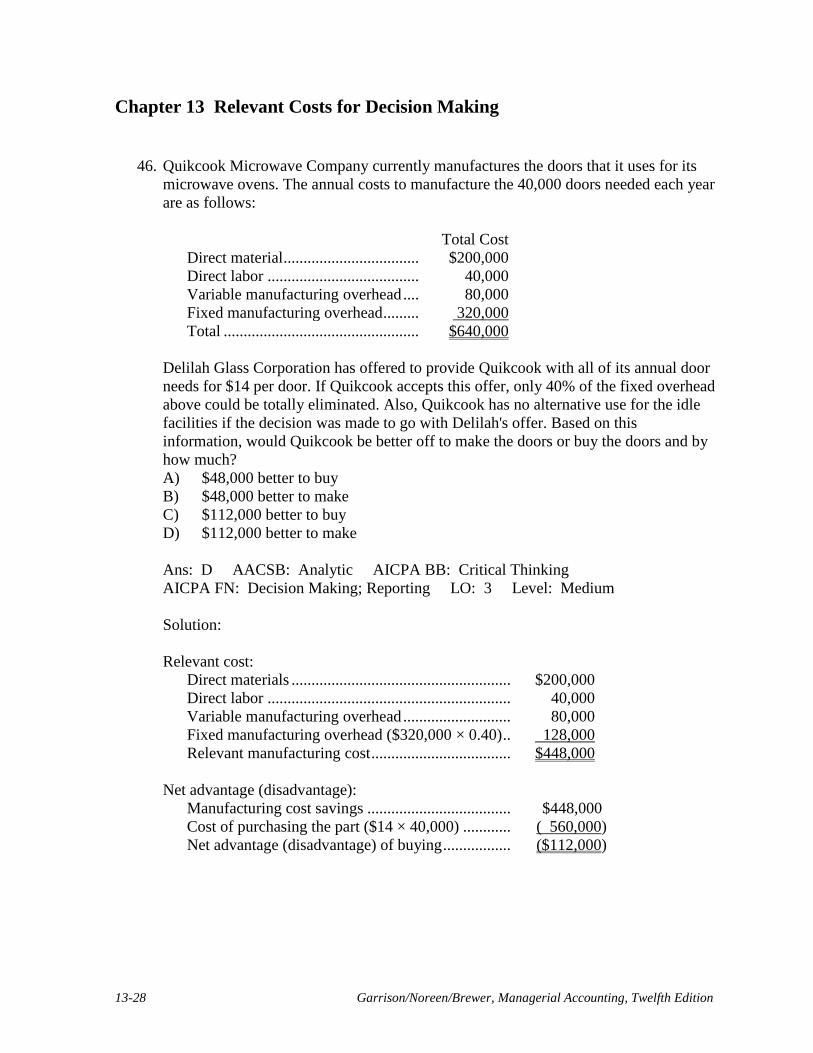

46. Quikcook Microwave Company currently manufactures the doors that it uses for its

microwave ovens. The annual costs to manufacture the 40,000 doors needed each year

are as follows:

Total Cost

Direct material .................................. $200,000

Direct labor ...................................... 40,000

Variable manufacturing overhead .... 80,000

Fixed manufacturing overhead ......... 320,000

Total ................................................. $640,000

Delilah Glass Corporation has offered to provide Quikcook with all of its annual door

needs for $14 per door. If Quikcook accepts this offer, only 40% of the fixed overhead

above could be totally eliminated. Also, Quikcook has no alternative use for the idle

facilities if the decision was made to go with Delilah's offer. Based on this

information, would Quikcook be better off to make the doors or buy the doors and by

how much?

A) $48,000 better to buy

B) $48,000 better to make

C) $112,000 better to buy

D) $112,000 better to make

Ans: D AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

Solution:

Relevant cost:

Direct materials ....................................................... $200,000

Direct labor ............................................................. 40,000

Variable manufacturing overhead ........................... 80,000

Fixed manufacturing overhead ($320,000 × 0.40) .. 128,000

Relevant manufacturing cost ................................... $448,000

Net advantage (disadvantage):

Manufacturing cost savings .................................... $448,000

Cost of purchasing the part ($14 × 40,000) ............ ( 560,000)

Net advantage (disadvantage) of buying ................. ($112,000)

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-29

47. Sardi Inc. is considering whether to continue to make a component or to buy it from an

outside supplier. The company uses 17,000 of the components each year. The unit

product cost of the component according to the company's cost accounting system is

given as follows:

Direct materials ......................................... $ 8.20

Direct labor ................................................ 8.30

Variable manufacturing overhead ............. 1.20

Fixed manufacturing overhead .................. 4.30

Unit product cost ....................................... $22.00

Assume that direct labor is a variable cost. Of the fixed manufacturing overhead, 70%

is avoidable if the component were bought from the outside supplier. In addition,

making the component uses 2 minutes on the machine that is the company's current

constraint. If the component were bought, this machine time would be freed up for use

on another product that requires 4 minutes on the constraining machine and that has a

contribution margin of $7.00 per unit.

When deciding whether to make or buy the component, what cost of making the

component should be compared to the price of buying the component?

A) $24.21

B) $25.50

C) $20.71

D) $22.00

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Hard

Source: CIMA, adapted

Solution:

Relevant cost per unit:

Direct materials .................................................. $ 8.20

Direct labor ......................................................... 8.30

Variable manufacturing overhead ...................... 1.20

Fixed manufacturing overhead ($4.30 × 0.70) ... 3.01

Relevant manufacturing cost .............................. $20.71

Add contribution margin lost* ........................... 3.50

$24.21

*$7.00 ÷ 4 minutes = $1.75 per minute; $1.75 per minute × 2 minutes = $3.50

Chapter 13 Relevant Costs for Decision Making

13-30 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

48. Part S51 is used in one of Haberkorn Corporation's products. The company makes

12,000 units of this part each year. The company's Accounting Department reports the

following costs of producing the part at this level of activity:

Per Unit

Direct materials ......................................... $6.30

Direct labor ............................................... $5.70

Variable manufacturing overhead ............. $4.80

Supervisor’s salary .................................... $7.00

Depreciation of special equipment ............ $8.60

Allocated general overhead ....................... $7.20

An outside supplier has offered to produce this part and sell it to the company for

$37.70 each. If this offer is accepted, the supervisor's salary and all of the variable

costs, including direct labor, can be avoided. The special equipment used to make the

part was purchased many years ago and has no salvage value or other use. The

allocated general overhead represents fixed costs of the entire company. If the outside

supplier's offer were accepted, only $17,000 of these allocated general overhead costs

would be avoided.

If management decides to buy part S51 from the outside supplier rather than to

continue making the part, what would be the annual impact on the company's overall

net operating income?

A) Net operating income would decline by $5,800 per year.

B) Net operating income would decline by $22,800 per year.

C) Net operating income would decline by $149,800 per year.

D) Net operating income would decline by $39,800 per year.

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Easy

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-31

Solution:

Make Buy

Direct materials (12,000 units @ $6.30 per unit) ..... $ 75,600

Direct labor (12,000 units @ $5.70 per unit) ........... 68,400

Variable overhead (12,000 units @ $4.80 per unit) . 57,600

Supervisor’s salary (12,000 units @ $7.00 per unit) 84,000

Depreciation of special equipment (not relevant) .... 0

Allocated general overhead (avoidable only) ........... 17,000

Outside purchase price (12,000 units @ $37.70 per

unit) ....................................................................... $452,400

Total cost .................................................................. $302,600 $452,400

The total cost of the make alternative is lower by $149,800 ($302,600 − $452,400).

Thus, net operating income would decline by $149,800 if the offer from the supplier

were accepted. Therefore, the company should continue to make the part itself.

Chapter 13 Relevant Costs for Decision Making

13-32 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

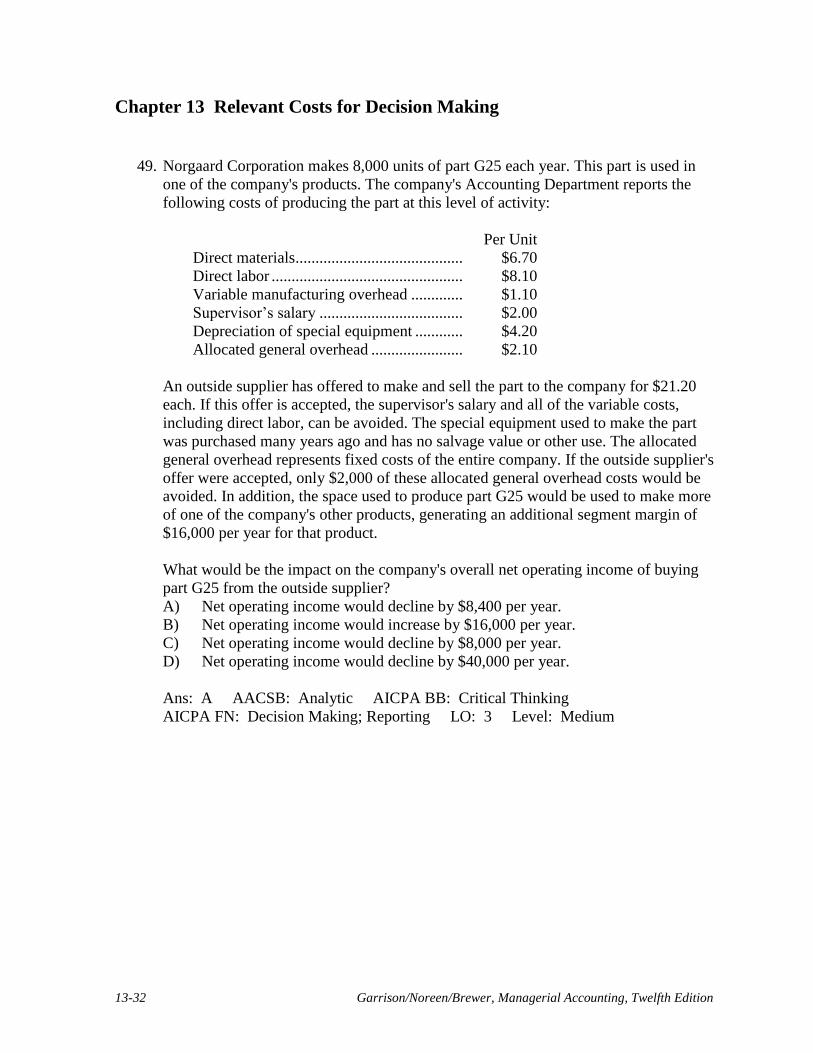

49. Norgaard Corporation makes 8,000 units of part G25 each year. This part is used in

one of the company's products. The company's Accounting Department reports the

following costs of producing the part at this level of activity:

Per Unit

Direct materials.......................................... $6.70

Direct labor ................................................ $8.10

Variable manufacturing overhead ............. $1.10

Supervisor’s salary .................................... $2.00

Depreciation of special equipment ............ $4.20

Allocated general overhead ....................... $2.10

An outside supplier has offered to make and sell the part to the company for $21.20

each. If this offer is accepted, the supervisor's salary and all of the variable costs,

including direct labor, can be avoided. The special equipment used to make the part

was purchased many years ago and has no salvage value or other use. The allocated

general overhead represents fixed costs of the entire company. If the outside supplier's

offer were accepted, only $2,000 of these allocated general overhead costs would be

avoided. In addition, the space used to produce part G25 would be used to make more

of one of the company's other products, generating an additional segment margin of

$16,000 per year for that product.

What would be the impact on the company's overall net operating income of buying

part G25 from the outside supplier?

A) Net operating income would decline by $8,400 per year.

B) Net operating income would increase by $16,000 per year.

C) Net operating income would decline by $8,000 per year.

D) Net operating income would decline by $40,000 per year.

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-33

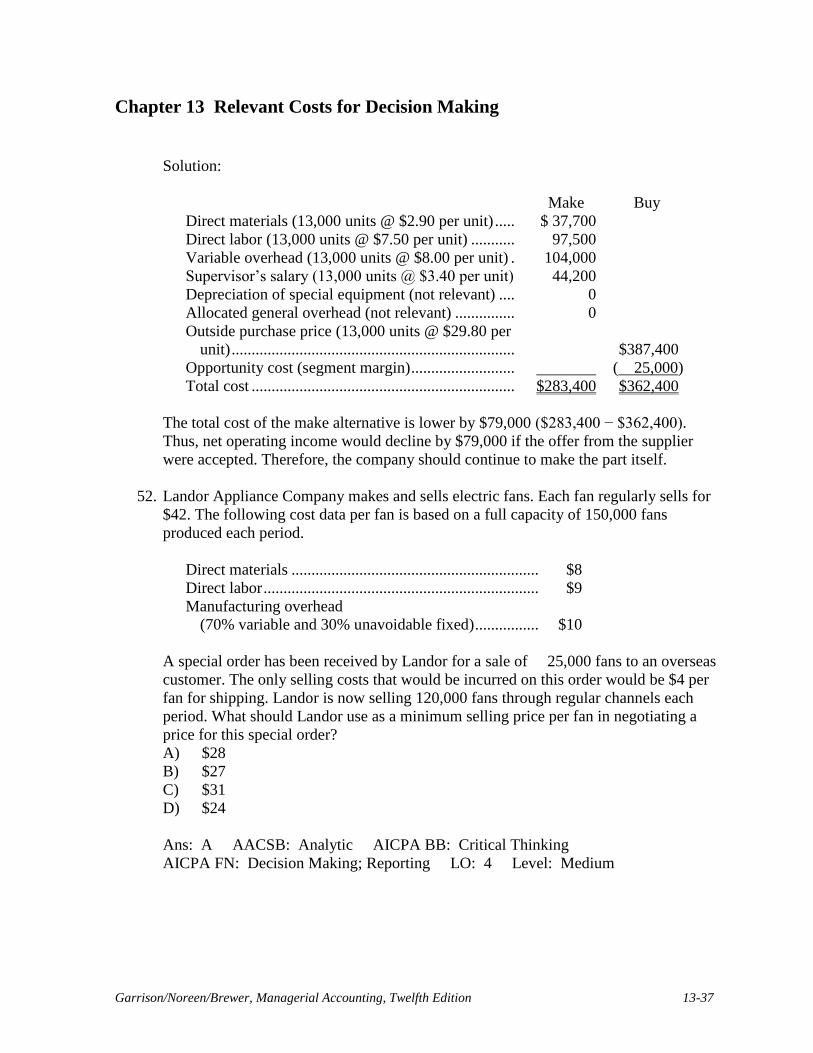

Solution:

Make Buy

Direct materials (8,000 units @ $6.70 per unit) ....... $ 53,600

Direct labor (8,000 units @ $8.10 per unit) ............. 64,800

Variable overhead (8,000 units @ $1.10 per unit) ... 8,800

Supervisor’s salary (8,000 units @ $2.00 per unit) .. 16,000

Depreciation of special equipment (not relevant) .... 0

Allocated general overhead (avoidable only) ........... 2,000

Outside purchase price (8,000 units @ $21.20 per

unit) ....................................................................... $169,600

Opportunity cost ....................................................... ( 16,000)

Total cost .................................................................. $145,200 $153,600

The total cost of the make alternative is lower by $8,400 ($145,200 − $153,600).

Thus, net operating income would decline by $8,400 if the offer from the supplier

were accepted. Therefore, the company should continue to make the part itself.

Chapter 13 Relevant Costs for Decision Making

13-34 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

50. Rebelo Corporation is presently making part E07 that is used in one of its products. A

total of 17,000 units of this part are produced and used every year. The company's

Accounting Department reports the following costs of producing the part at this level

of activity:

Per Unit

Direct materials ......................................... $3.80

Direct labor ............................................... $3.80

Variable manufacturing overhead ............. $1.10

Supervisor’s salary .................................... $2.50

Depreciation of special equipment ............ $1.40

Allocated general overhead ....................... $8.60

An outside supplier has offered to make and sell the part to the company for $20.80

each. If this offer is accepted, the supervisor's salary and all of the variable costs can

be avoided. The special equipment used to make the part was purchased many years

ago and has no salvage value or other use. The allocated general overhead represents

fixed costs of the entire company, none of which would be avoided if the part were

purchased instead of produced internally. If management decides to buy part E07 from

the outside supplier rather than to continue making the part, what would be the annual

impact on the company's overall net operating income?

A) Net operating income would decline by $6,800 per year.

B) Net operating income would decline by $163,200 per year.

C) Net operating income would increase by $163,200 per year.

D) Net operating income would increase by $6,800 per year.

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Easy

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-35

Solution:

Make Buy

Direct materials (17,000 units @ $3.80 per unit) ....... $ 64,600

Direct labor (17,000 units @ $3.80 per unit) ............. 64,600

Variable overhead (17,000 units @ $1.10 per unit) ... 18,700

Supervisor’s salary (17,000 units @ $2.50 per unit) .. 42,500

Depreciation of special equipment (not relevant) ...... 0

Allocated general overhead (not relevant) ................. 0

Outside purchase price (17,000 units @ $20.80 per

unit) ......................................................................... $353,600

Total cost .................................................................... $190,400 $353,600

The total cost of the make alternative is lower by $163,200 ($353,600 − $190,400).

Thus, net operating income would decline by $163,200 if the offer from the supplier

were accepted. Therefore, the company should continue to make the part itself.

Chapter 13 Relevant Costs for Decision Making

13-36 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

51. Part U16 is used by Mcvean Corporation to make one of its products. A total of

13,000 units of this part are produced and used every year. The company's Accounting

Department reports the following costs of producing the part at this level of activity:

Per Unit

Direct materials ......................................... $2.90

Direct labor ............................................... $7.50

Variable manufacturing overhead ............. $8.00

Supervisor’s salary .................................... $3.40

Depreciation of special equipment ............ $1.80

Allocated general overhead ....................... $7.00

An outside supplier has offered to make the part and sell it to the company for $29.80

each. If this offer is accepted, the supervisor's salary and all of the variable costs,

including the direct labor, can be avoided. The special equipment used to make the

part was purchased many years ago and has no salvage value or other use. The

allocated general overhead represents fixed costs of the entire company, none of which

would be avoided if the part were purchased instead of produced internally. In

addition, the space used to make part U16 could be used to make more of one of the

company's other products, generating an additional segment margin of $25,000 per

year for that product. What would be the impact on the company's overall net

operating income of buying part U16 from the outside supplier?

A) Net operating income would increase by $25,000 per year.

B) Net operating income would decline by $79,000 per year.

C) Net operating income would decline by $35,400 per year.

D) Net operating income would increase by $14,600 per year.

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 3 Level: Medium

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-37

Solution:

Make Buy

Direct materials (13,000 units @ $2.90 per unit) ..... $ 37,700

Direct labor (13,000 units @ $7.50 per unit) ........... 97,500

Variable overhead (13,000 units @ $8.00 per unit) . 104,000

Supervisor’s salary (13,000 units @ $3.40 per unit) 44,200

Depreciation of special equipment (not relevant) .... 0

Allocated general overhead (not relevant) ............... 0

Outside purchase price (13,000 units @ $29.80 per

unit) ....................................................................... $387,400

Opportunity cost (segment margin) .......................... ( 25,000)

Total cost .................................................................. $283,400 $362,400

The total cost of the make alternative is lower by $79,000 ($283,400 − $362,400).

Thus, net operating income would decline by $79,000 if the offer from the supplier

were accepted. Therefore, the company should continue to make the part itself.

52. Landor Appliance Company makes and sells electric fans. Each fan regularly sells for

$42. The following cost data per fan is based on a full capacity of 150,000 fans

produced each period.

Direct materials .............................................................. $8

Direct labor ..................................................................... $9

Manufacturing overhead

(70% variable and 30% unavoidable fixed) ................ $10

A special order has been received by Landor for a sale of 25,000 fans to an overseas

customer. The only selling costs that would be incurred on this order would be $4 per

fan for shipping. Landor is now selling 120,000 fans through regular channels each

period. What should Landor use as a minimum selling price per fan in negotiating a

price for this special order?

A) $28

B) $27

C) $31

D) $24

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 4 Level: Medium

Chapter 13 Relevant Costs for Decision Making

13-38 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

Solution:

Direct materials ................................................. $ 8

Direct labor ....................................................... 9

Variable manufacturing overhead ($10 × 0.70) 7

Variable selling cost .......................................... 4

Minimum selling price ...................................... $28

53. Ignace Timekeepers, Inc. manufactures and sells wrist watches. Ignace has the

capacity to manufacture and sell 20,000 watches each year but is currently only

manufacturing and selling 15,000. The following costs relate to annual operations at

15,000 watches:

Total Cost

Variable manufacturing cost ..................... $150,000

Fixed manufacturing cost .......................... $120,000

Variable selling and administrative cost ... $90,000

Fixed selling and administrative cost ........ $180,000

Ignace normally sells its watches for $42 each. A discount chain is interesting in

purchasing Ignace's excess capacity of 5,000 watches. This special order would not

affect regular sales or the cost structure above. Ignace's profits for the year will

increase as long as the price on this special order exceeds:

A) $12.00

B) $13.50

C) $16.00

D) $31.00

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 4 Level: Medium

Solution:

Total relevant costs:

Variable manufacturing cost .............................. $150,000

Variable selling and administrative cost ............ 90,000

Total relevant costs ............................................... $240,000

Divided by 15,000 watches ...................................

÷

15,000

Minimum selling price for special order ............... $16

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-39

54. Gallerani Corporation has received a request for a special order of 6,000 units of

product A90 for $21.20 each. Product A90's unit product cost is $16.20, determined as

follows:

Direct materials ......................................... $ 6.10

Direct labor ................................................ 4.20

Variable manufacturing overhead ............. 2.30

Fixed manufacturing overhead .................. 3.60

Unit product cost ....................................... $16.20

Direct labor is a variable cost. The special order would have no effect on the

company's total fixed manufacturing overhead costs. The customer would like

modifications made to product A90 that would increase the variable costs by $4.20 per

unit and that would require an investment of $21,000 in special molds that would have

no salvage value.

This special order would have no effect on the company's other sales. The company

has ample spare capacity for producing the special order. If the special order is

accepted, the company's overall net operating income would increase (decrease) by:

A) ($18,600)

B) ($16,200)

C) $30,000

D) $5,400

Answer:

D

Ans: D AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 4 Level: Easy

Solution:

Incremental revenue (6,000 units @ $21.20 per unit) ...................... $127,200

Less incremental costs:

Direct materials (6,000 units @ $6.10 per unit) ............................ 36,600

Direct labor (6,000 units @ $4.20 per unit) .................................. 25,200

Variable manufacturing overhead (6,000 units @ $2.30 per unit) 13,800

Modifications (6,000 units @ $4.20 per unit) ............................... 25,200

Special molds ................................................................................ 21,000

Total incremental cost ...................................................................... 121,800

Incremental net operating income .................................................... $ 5,400

Chapter 13 Relevant Costs for Decision Making

13-40 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

55. A customer has requested that Lewelling Corporation fill a special order for 9,000

units of product S47 for $20.50 a unit. While the product would be modified slightly

for the special order, product S47's normal unit product cost is $14.40:

Direct materials ......................................... $ 3.10

Direct labor ............................................... 1.50

Variable manufacturing overhead ............. 6.40

Fixed manufacturing overhead .................. 3.40

Unit product cost ....................................... $14.40

Direct labor is a variable cost. The special order would have no effect on the

company's total fixed manufacturing overhead costs. The customer would like

modifications made to product S47 that would increase the variable costs by $5.00 per

unit and that would require an investment of $36,000 in special molds that would have

no salvage value.

This special order would have no effect on the company's other sales. The company

has ample spare capacity for producing the special order. If the special order is

accepted, the company's overall net operating income would increase (decrease) by:

A) ($9,900)

B) $4,500

C) $54,900

D) ($26,100)

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 4 Level: Easy

Solution:

Incremental revenue (9,000 units @ $20.50 per unit) ..................... $184,500

Less incremental costs:

Direct materials (9,000 units @ $3.10 per unit) ........................... 27,900

Direct labor (9,000 units @ $1.50 per unit) .................................. 13,500

Variable manufacturing overhead (9,000 units @ $6.40 per unit) 57,600

Modifications (9,000 units @ $5.00 per unit) ............................... 45,000

Special molds ................................................................................ 36,000

Total incremental cost ...................................................................... 180,000

Incremental net operating income .................................................... $ 4,500

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-41

56. Holden Company produces three products, with costs and selling prices as follows:

Product A Product B Product C

Selling price per unit ............... $30 100% $20 100% $15 100%

Variable costs per unit ............. 18 60% 15 75% 6 40%

Contribution margin per unit ... $12 40% $ 5 25% $ 9 60%

A particular machine is a bottleneck. On that machine, 3 machine hours are required to

produce each unit of Product A, 1 hour is required to produce each unit of Product B,

and 2 hours are required to produce each unit of Product C. In which order should it

produce its products?

A) C, A, B

B) A, C, B

C) B, C, A

D) The order of production doesn't matter.

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Medium

Solution:

Product A Product B Product C

Contribution margin per unit ............... $12 $5 $9

Machine-hours per unit ........................ 3 1 2

Contribution margin per hour .............. $4.00 $5.00 $4.50

Rank in terms of profitability .............. 3 1 2

Chapter 13 Relevant Costs for Decision Making

13-42 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

57. Wood Carving Corporation manufactures three products. Because of a recent lack of

skilled wood carvers, the corporation has had a shortage of available labor hours. The

following per unit data relates to the three products of the corporation:

Letter Openers Elvis Statues Candle Holders

Sales price ................... $30 $80 $42

Variable costs .............. $20 $40 $20

Labor hours required ... 1 6 2

Assume that Wood Carving only has 1,800 labor hours available next month. Also

assume that Wood Carving can only sell 800 units of each product in a given month.

What is the maximum amount of contribution margin that Wood Carving can generate

next month given this labor hour shortage?

A) $12,000

B) $19,000

C) $19,600

D) $19,800

Ans: C AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Hard

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-43

Solution:

Demand for wood carvers:

Letter Openers Elvis Statues Candle Holders

Labor-hours per unit .......... 1 6 2

Monthly demand in units ... 800 800 800

Total hours required ........... 800 4,800 1,600

Total time required for all products: 7,200

Optimal production plan:

Letter Openers Elvis Statues Candle Holders

Selling price per unit ............................ $30.00 $80.00 $42.00

Variable cost per unit ........................... $20.00 $40.00 $20.00

Contribution margin per unit ............... $10.00 $40.00 $22.00

Labor-hours per unit ............................ 1 6 2

Contribution margin per hour .............. $10.00 $6.67 $11.00

Rank in terms of profitability .............. 2 3 1

Optimal production .............................. 200 0 800

Total hours available ........................................................................ 1,800

Less: hours required for 800 Candle Holders (800 × 2) ................... 1,600

Hours remaining ............................................................................... 200

Divided by hours required per Letter Opener .................................. ÷ 1

Number of Letter Openers to produce .............................................. 200

Maximum contribution margin:

Candle Holders (800 × $22).......................................................... $17,600

Letter Openers (200 × $10) ........................................................... 2,000

Maximum contribution margin ........................................................ $19,600

Chapter 13 Relevant Costs for Decision Making

13-44 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

58. Banfield Corporation makes three products that use compound W, the current

constrained resource. Data concerning those products appear below:

VP YI WX

Selling price per unit ..................... $248.04 $230.66 $505.44

Variable cost per unit .................... $190.71 $172.14 $388.80

Centiliters of compound W ........... 3.90 3.80 8.10

Rank the products in order of their current profitability from most profitable to least

profitable. In other words, rank the products in the order in which they should be

emphasized.

A) WX, VP, YI

B) YI, VP, WX

C) WX, YI, VP

D) VP, WX, YI

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Easy

Solution:

Optimal production plan:

VP YI WX

Selling price per unit ........................... $248.04 $230.66 $505.44

Variable cost per unit .......................... 190.71 172.14 388.80

Contribution margin per unit ............... $57.33 $58.52 $116.64

Centiliters per unit ............................... 3.90 3.80 8.10

Contribution margin per centiliter ....... $14.70 $15.40 $14.40

Rank in terms of profitability .............. 2 1 3

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-45

59. An automated turning machine is the current constraint at Jordison Corporation. Three

products use this constrained resource. Data concerning those products appear below:

LN JQ RQ

Selling price per unit ..................... $165.88 $313.11 $494.52

Variable cost per unit .................... $118.30 $239.61 $381.42

Minutes on the constraint .............. 2.60 4.90 7.80

Rank the products in order of their current profitability from most profitable to least

profitable. In other words, rank the products in the order in which they should be

emphasized.

A) LN, JQ, RQ

B) RQ, LN, JQ

C) RQ, JQ, LN

D) JQ, RQ, LN

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Easy

Solution:

Optimal production plan:

LN JQ RQ

Selling price per unit ........................... $165.88 $313.11 $494.52

Variable selling cost per unit ............... 118.30 239.61 381.42

Contribution margin per unit ............... $47.58 $73.50 $113.10

Machine minutes per unit .................... 2.60 4.90 7.80

Contribution margin per minute .......... $18.30 $15.00 $14.50

Rank in terms of profitability .............. 1 2 3

Chapter 13 Relevant Costs for Decision Making

13-46 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

60. The constraint at Rauchwerger Corporation is time on a particular machine. The

company makes three products that use this machine. Data concerning those products

appear below:

WX KD FS

Selling price per unit ..................... $192.00 $542.66 $222.84

Variable cost per unit .................... $158.72 $420.54 $167.76

Minutes on the constraint .............. 3.20 8.60 3.60

Assume that sufficient time is available on the constrained machine to satisfy demand

for all but the least profitable product. Up to how much should the company be willing

to pay to acquire more of the constrained resource?

A) $33.28 per unit

B) $10.40 per minute

C) $122.12 per unit

D) $15.30 per minute

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 5 Level: Medium

Solution:

WX KD FS

Selling price per unit ........................... $192.00 $542.66 $222.84

Variable cost per unit .......................... 158.72 420.54 167.76

Contribution margin per unit ............... $33.28 $122.12 $55.08

Machine minutes per unit .................... 3.20 8.60 3.60

Contribution margin per minute .......... $10.40 $14.20 $15.30

Rank in terms of profitability .............. 3 2 1

The company should be willing to pay up to the contribution margin per minute for

the least profitable job, which is $10.40.

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-47

61. The Freed Company produces three products, X, Y, Z, from a single raw material

input. Product Y can be sold at the splitoff point for total revenues of $50,000, or it

can be processed further at a total cost of $16,000 and then sold for $68,000. Product

Y:

A) should be sold at the split-off point, rather than processed further.

B) would increase the company's overall net operating income by $18,000 if

processed further and then sold.

C) would increase the company's overall net operating income by $68,000 if

processed further and then sold.

D) would increase the company's overall net operating income by $2,000 if

processed further and then sold.

Ans: D AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 6 Level: Easy

Solution:

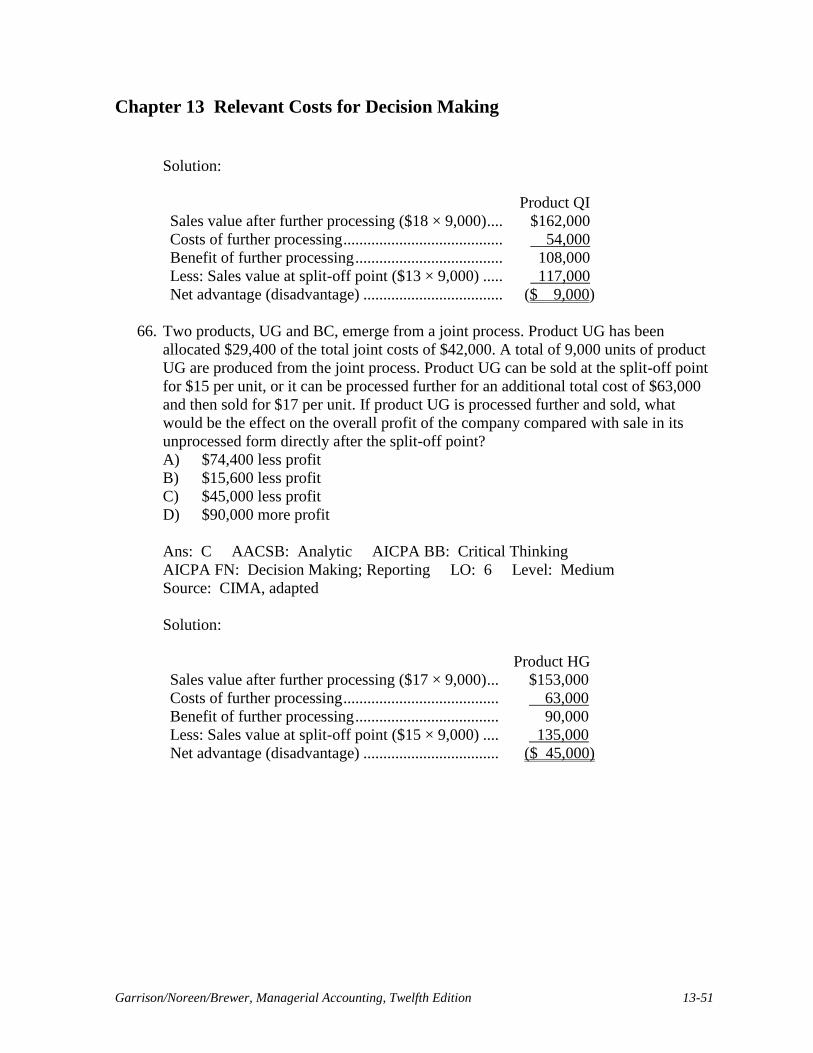

Product Y

Sales value after further processing .......... $68,000

Costs of further processing ........................ 16,000

Benefit of further processing ..................... 52,000

Less: Sales value at split-off point ............ 50,000

Net advantage ............................................ $ 2,000

Chapter 13 Relevant Costs for Decision Making

13-48 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

62. Pendall Company manufactures products Dee and Eff from a joint process. Product

Dee has been allocated $2,500 of the $20,000 in total joint costs associated with the

production of 1,000 units each of Dee and Eff each year. Dee can be sold at the split-

off point for $3 per unit, or it can be processed further with additional costs of $1,000

and sold for $5 per unit. If Dee is processed further and sold, the result would be:

A) A break-even situation.

B) An additional gain of $1,000 from further processing.

C) A loss of $1,000 from further processing.

D) An additional gain of $2,000 from further processing.

Ans: B AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 6 Level: Medium

Source: CPA, adapted

Solution:

Dee

Sales value after further processing ($5 × 1,000) . $5,000

Costs of further processing ................................... 1,000

Benefit of further processing................................. 4,000

Less: Sales value at split-off point ($3 × 1,000) ... 3,000

Net advantage ........................................................ $1,000

Chapter 13 Relevant Costs for Decision Making

Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition 13-49

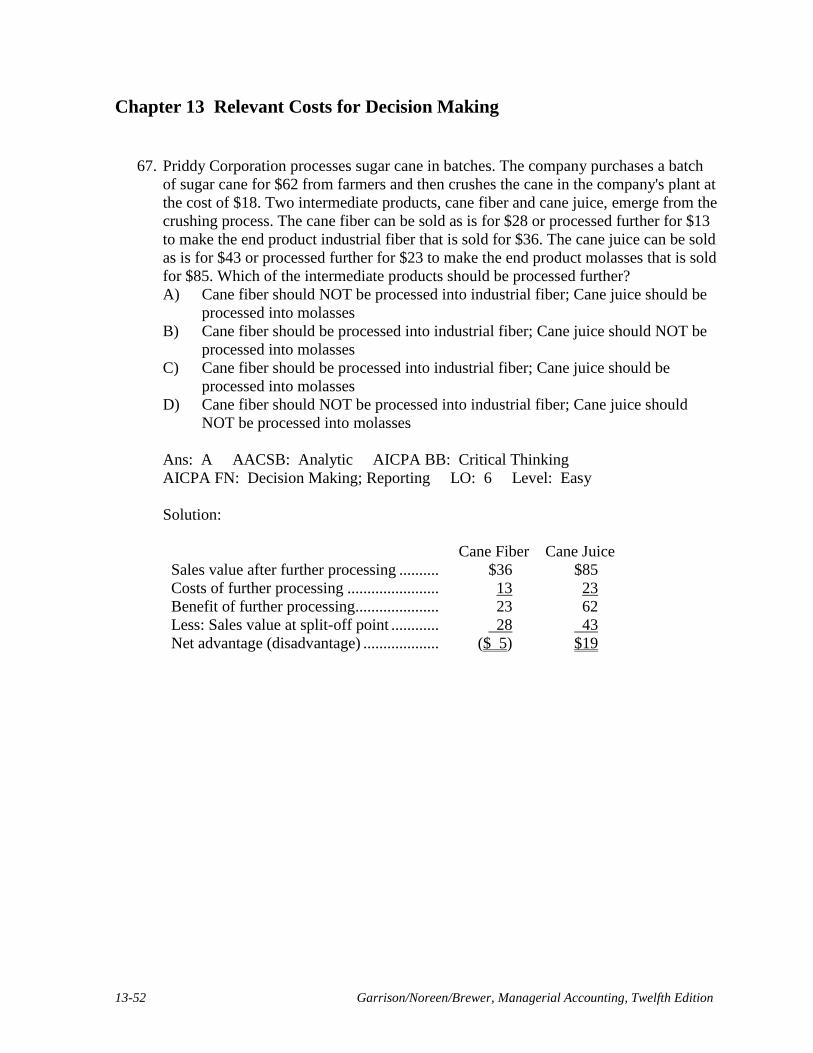

63. Faustina Chemical Company manufactures three chemicals (TX14, NJ35, and KS63)

from a joint process. The three chemicals are in industrial grade form at the split-off

point. They can either be sold at that point or processed further into premium grade.

Costs related to each batch of this chemical process is as follows:

TX14 NJ35 KS63

Sales value at split-off point ...................... $16,000 $12,000 $5,000

Allocated joint costs .................................. $6,000 $6,000 $6,000

Sales value after further processing ........... $20,000 $18,000 $9,000

Cost of further processing ......................... $5,000 $3,000 $2,000

For which product(s) above would it be more profitable for Faustina to sell at the split-

off point rather than process further?

A) TX14 only

B) KS63 only

C) TX14 and KS63 only

D) NJ35 and KS63 only

Ans: A AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Decision Making; Reporting LO: 6 Level: Hard

Solution:

TX14 NJ35 KS63

Sales value after further processing .... $20,000 $18,000 $9,000

Sales value at split-off ......................... 16,000 12,000 5,000

Incremental revenue ............................ 4,000 6,000 4,000

Further processing costs ...................... 5,000 3,000 2,000

Incremental income (loss) ................... ($1,000) $ 3,000 $2,000

Product TX14 should be sold at the split-off point without any further processing.

Products NJ35 and KS63 should be sold after further processing beyond the split-off

point.

Chapter 13 Relevant Costs for Decision Making

13-50 Garrison/Noreen/Brewer, Managerial Accounting, Twelfth Edition

64. Khiem, Inc. manufactures baseball gloves that normally sell for $55 each. Khiem

currently has 400 defective gloves in inventory that have $35 of materials, labor, and

overhead assigned to each glove. The defective gloves can either be completely

repaired at a cost of $25 per glove or sold as is at a reduced price of $18 per glove.

Khiem would be better off by: