chapter 14 equilibrium and efficiency copyright © 2014 mcgraw-hill education. all rights reserved....

TRANSCRIPT

chapter 14

Equilibrium and Efficiency

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-2

Learning Objectives• Identify the factors that make a market perfectly

competitive.• Determine the short- and long-run market demand

and supply.• Analyze changes in market equilibrium due to changes

in market conditions in the short and long run.• Explain how perfectly competitive markets can be

considered “efficient” for society.• Measure aggregate surplus, consumer surplus, and

producer surplus using market supply and demand curves.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-3

Overview

• What makes a market competitive, so that individuals and firms behave as price takers?

• We will aggregate the individual demand and supply curves we already know into market demand and supply curves

• We will analyze the short-run and long-run dynamics and equilibria of competitive markets

• We will show that the equilibrium outcome in competitive markets is efficient, maximizing aggregate surplus

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-4

Characteristics of a Perfectly Competitive Market

1. Buyers and sellers face no transaction costs2. Products are homogeneous, identical in the eyes of

the consumer3. There are many buyers and sellers, each accounting

for a small fraction of the overall demand or supply of the good

4. In a perfectly competitive market, buyers and sellers are price takers, taking the market price as given (unaffected by their actions) in deciding how much to buy or sell

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-5

Market Demand

• Market demand: sum of the demands of all the individual consumers

• Market demand curve: horizontal sum of the individual demand curves

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-6

Individual and Market Demand Curves

E

J

E J+

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-7

Market Supply

• Market supply: sum of the supply of all the individual sellers

• Market supply curve: horizontal sum of the individual supply curves

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-8

Individual and Market Supply Curves

A A R

R

+

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-9

Short-Run vs. Long-Run Market Supply

• Market supply curves– Short-run supply: Add up the short-run supply

curves of all currently active firms– Long-run supply: Add up the long-run supply

curves of all potential suppliers

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

The Long -Run Market Supply Curve with Free Entry

Free entry: when technology is freely available to anyone who wishes to start a firm, and entry is unrestricted. In that case, the number of potential firms is unlimited.

14-10Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-11

Competitive Equilibrium

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

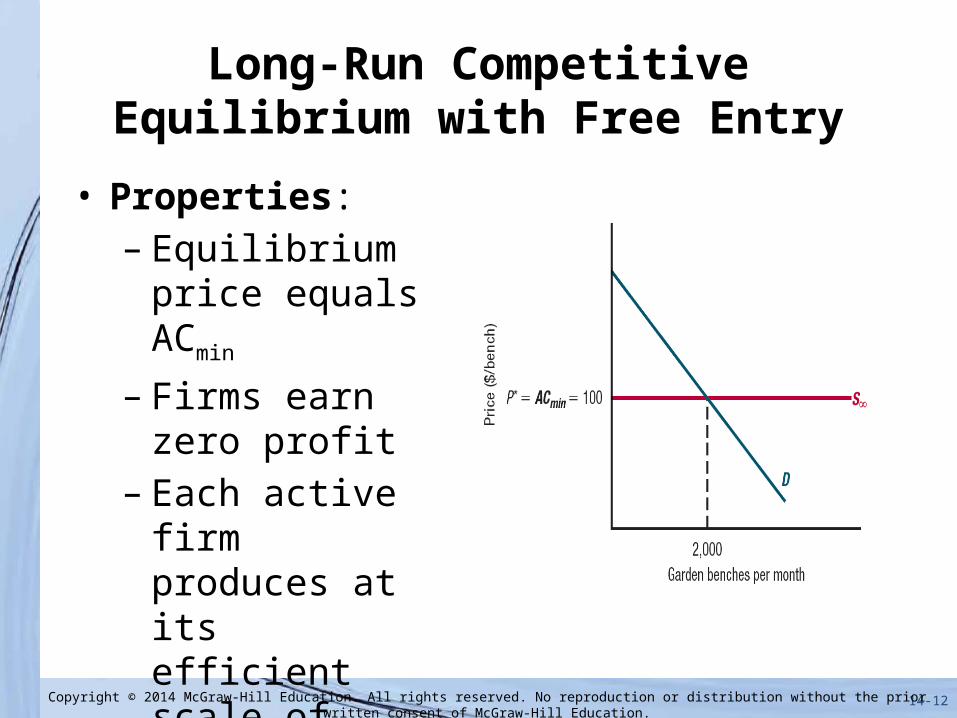

Long-Run Competitive Equilibrium with Free Entry

• Properties:– Equilibrium price

equals ACmin

– Firms earn zero profit

– Each active firm produces at its efficient scale of production

14-12Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-13

D’

S10

AS∞

D

Garden benches per month

Pric

e ($

/ben

ch)

2,000

P*= ACmin

= 100

(b) Demand decrease

C

1,000

Short-Run and Long-Run Responses to Demand Change

Garden benches per month

Pric

e ($

/ben

ch)

2,000

A

D’D

S∞P*= ACmin

= 100

(a) Demand increase

4,000

C

S10

B

QSR

PSR

BPSR

QSR

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-14

Price Changes in the Long-Run

Garden benches per month2,000

Pric

e ($

/ben

ch)

(a) Increasing input cost

AACmin= 100

S∞

DD’ D’

S10

ACmin= 110 Ŝ∞

ACmin= 90Ŝ∞

4,000

C

S10

A

Garden benches per month2,000

Pric

e ($

/ben

ch)

(b) Decreasing input cost

ACmin= 100

S∞

D

4,000

C

B

E

QLR

E

QLR

B

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-15

Aggregate Surplus

• Aggregate surplus: captures the net benefit created by the production and consumption of a good

• Aggregate surplus = Total benefit from consumption (total

willingness to pay) – Total avoidable cost of production

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-16

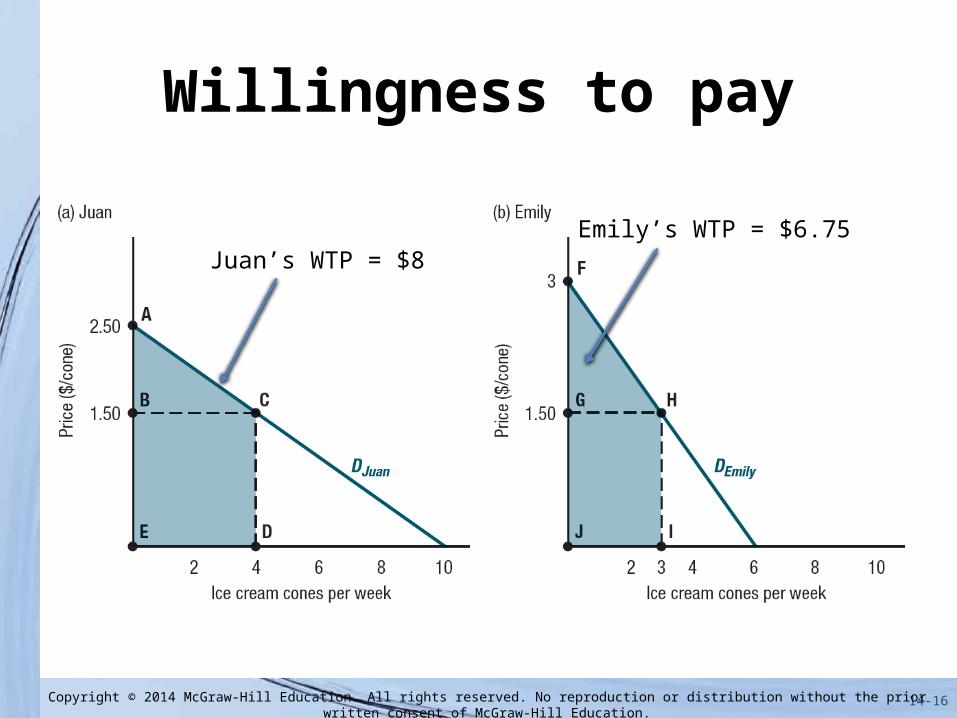

Willingness to pay

Juan’s WTP = $8Emily’s WTP = $6.75

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-17

Avoidable Cost of Production

Anitra’s ACP = $5

Robert’s ACP = $3

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-18

Competitive Equilibrium Maximizes Aggregate Surplus

• Pareto efficient (or Pareto optimal): an economic outcome at which it is impossible to make anyone better off without making someone else worse off

• Any change in who consumes the good, which firms produce it, or the amount that is produced and consumed, must lower aggregate surplus, making someone worse off in the process

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Effects of Change in Who Consumes Good

Transferring one ice cream cone from Juan to Emily results in lower aggregate surplus (Juan’s WTP(3) > Emily’s WTP(4))

14-19Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Effects of Change in Who Produces Good

Transferring production of one ice cream cone from Anitra to Robert results in lower aggregate surplus (Anitra’s ACP(3) < Robert’s ACP(4))

14-20Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Effects of an Increase in Goods Produced and Consumed

Robert’s cost of producing an additional ice cream cone exceeds Juan’s willingness to pay for that ice cream cone, lowering aggregate surplus

14-21Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Using Market Demand as a Measure of Willingness to Pay

• Whenever the units of a good are consumed by those individuals with the highest willingness to pay for them, we can measure consumers’ total willingness to pay for the units they consume by the area under the market demand curve up to that quantity.

14-22Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Using Supply Curves to Measure Total Avoidable Cost

• Whenever the units of a good are produced by the firms with the lowest avoidable cost of producing them, we can measure firms’ total avoidable cost for the units they produce by the area under the market supply curve up to that quantity.

14-23Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Measuring Consumer and Producer Surplus

14-24Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Deadweight Loss• Deadweight Loss: a reduction in aggregate surplus

below its maximum possible valueCompetitive equilibrium:

- Maximum surplus- Zero DWL

14-25Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-26

Consumer and Producer Surplus

• Consumer surplus: sum of consumers’ total willingness to pay minus their total expenditure

• Producer surplus: sum of firms’ revenue minus their avoidable costs

• Aggregate surplus = Consumer surplus + Producer surplus

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-27

Review

• A market is perfectly competitive when buyers and sellers face no transaction costs, products are homogeneous, and there are many buyers and sellers.

• In a long-run competitive equilibrium with free entry the equilibrium price equals ACmin, firms earn zero profit, and each active firm produces at its efficient scale of production.

• Aggregate surplus equals the sum of consumer surplus and producer surplus

• Competitive markets are Pareto efficient, maximizing aggregate surplus

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

14-28

Looking Forward

• Today we focused on competitive markets and how they maximize aggregate surplus

• Next we will analyze what happens when governments intervene in competitive markets using taxes, subsidies, price controls, tariffs, or other types of market intervention

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.