chapter 15 corporate capital gains - … · chapter 15 corporate capital gains this chapter...

TRANSCRIPT

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 159 FA 2015

CHAPTER 15

CORPORATE CAPITAL GAINS

This chapter explains how companies pay corporation tax on capital gains, covering in particular:– how we calculate the gain chargeable;– what relief is available against a capital gain.

15.1 Introduction

A company pays corporation tax on capital gains arising on the disposal of chargeable assets. Most capital assets are chargeable with a number of minor exceptions, e.g. cars. The definition of a car does not extend to vans and other commercial vehicles, which may give rise to chargeable gains where they are sold at a profit.

Individuals pay capital gains tax (CGT) at a flat rate of 18% or 28% depending on the level of their total taxable income, whereas companies include the gains as part of their TTP and so pay corporation tax on gains.

The rules for computing gains for companies are similar to the rules that apply to individuals. However, companies can claim indexation allowance whereas individuals can’t. Also, companies are not entitled to an annual exemption and are not eligible for many of the reliefs that individuals can claim, e.g. entrepreneurs' relief.

15.2 Computation of Gains

The proforma for computing gains for a company is shown below. We start with sale proceeds from which we can deduct any incidental costs of sale, such as solicitor's or surveyor's fees, etc.

We deduct the cost of the asset which will also include any enhancement expenditure and other incidental costs of acquisition, including legal fees and stamp duty paid. That gives us the unindexed gain.

We then deduct indexation allowance, which is an allowance for inflation, to give the indexed gain. It is this indexed gain that is subject to corporation tax.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 160 FA 2015

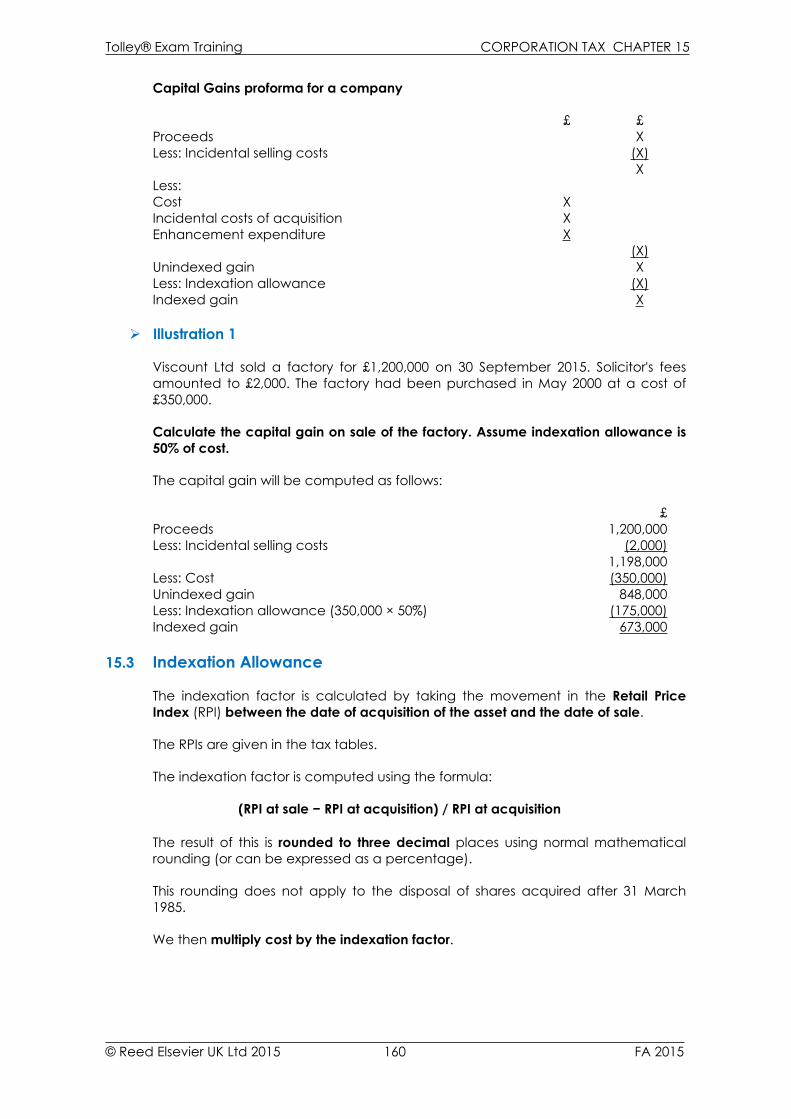

Capital Gains proforma for a company

£ £Proceeds XLess: Incidental selling costs (X)

XLess:Cost XIncidental costs of acquisition XEnhancement expenditure X

(X)Unindexed gain XLess: Indexation allowance (X)Indexed gain X

Illustration 1

Viscount Ltd sold a factory for £1,200,000 on 30 September 2015. Solicitor's fees amounted to £2,000. The factory had been purchased in May 2000 at a cost of £350,000.

Calculate the capital gain on sale of the factory. Assume indexation allowance is 50% of cost.

The capital gain will be computed as follows:

£Proceeds 1,200,000Less: Incidental selling costs (2,000)

1,198,000Less: Cost (350,000)Unindexed gain 848,000Less: Indexation allowance (350,000 × 50%) (175,000)Indexed gain 673,000

15.3 Indexation Allowance

The indexation factor is calculated by taking the movement in the Retail Price Index (RPI) between the date of acquisition of the asset and the date of sale.

The RPIs are given in the tax tables.

The indexation factor is computed using the formula:

(RPI at sale − RPI at acquisition) / RPI at acquisition The result of this is rounded to three decimal places using normal mathematical rounding (or can be expressed as a percentage).

This rounding does not apply to the disposal of shares acquired after 31 March 1985.

We then multiply cost by the indexation factor.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 161 FA 2015

Illustration 2

In the previous illustration, Viscount Ltd, we assumed the indexation factor was 50%.

Recalculate the capital gain on sale of the factory using the correct indexation factor.

The correct indexation factor for May 2000 to September 2015 is:

(257.8 – 170.7)/170.7 = 0.510252 = 0.510 or 51.0%

The correct gain is therefore:

£Unindexed gain 848,000Less: Indexation allowance (350,000 × 0.510) (178,500)Indexed gain 669,500 If the value of the RPI has fallen between acquisition and disposal, then indexation allowance is nil.

15.4 Enhancement Expenditure

Enhancement expenditure is added to the “base cost”, or allowable cost, of the asset. It may need to be indexed separately if the enhancement occurs at a different date to that of the acquisition of the asset.

Illustration 3

Assume in the Viscount Ltd illustration that the factory was extended in October 2001 at a cost of £200,000. Ignore the incidental selling costs, so that proceeds are £1,200,000 and original cost is £350,000.

Calculate the capital gains on sale of the factory, taking into account the enhancement expenditure in October 2001.

£Proceeds (Sept 2015) 1,200,000Less: Cost (May 2000) (350,000)Less: Enhancement (Oct 2001) (200,000)Unindexed gain 650,000Less: Indexation on costMay 2000 to Sept 2015(257.8 – 170.7)/170.7 = 0.510 × 350,000 (178,500)Less: Indexation on enhancementOct 2001 to Sept 2015(257.8 – 174.3)/174.3 = 0.479 × 200,000 (95,800)Indexed gain 375,700

15.5 Capital Losses

Capital losses are computed in the same way as capital gains, except that indexation cannot create or increase a capital loss, it can only reduce a gain to zero.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 162 FA 2015

Illustration 4

Using the Viscount Ltd illustration again, but this time, let's assume that the asset was actually sold for just £400,000. So, Viscount Ltd sells a factory for £400,000 on 30 September 2015 and had originally purchased the factory in May 2000 at a cost of £350,000.

Calculate the gain or loss on sale of the factory.

£Proceeds 400,000Less: Cost (350,000)Unindexed gain 50,000Less: Indexation allowance350,000 × 0.510 = 178,500 (restricted) (50,000)Indexed gain Nil Indexation allowance is claimed, but restricted to the amount of the unindexed gain as it cannot create a loss. Hence, the indexed gain, after the indexation allowance, is nil.

Illustration 5

Assume now that the asset was actually sold by Viscount Ltd for just £250,000. The original acquisition cost is still £350,000.

Calculate the gain or loss on sale of the factory.

£Proceeds 250,000Less: Cost (350,000)Allowable capital loss (100,000) No indexation is claimable as it cannot increase this loss.

Capital losses must be set against current period chargeable gains, and then carried forward against future capital gains. The chargeable gains figure included in TTP is net of current year capital losses and brought forward capital losses as shown below: TCGA 1992 s.2

£Chargeable gains XLess: Current year capital losses (X)Less: Brought forward capital losses (X)Net chargeable gains included in TTP X

15.6 Assets Purchased Before 31 March 1982

Where the asset was originally acquired before 31 March 1982, we are required to do an additional calculation to compute the capital gains and losses for the company.

The additional calculation starts in the same place i.e. with sales proceeds. However, instead of deducting original cost, we deduct the value of the asset as at 31 March 1982.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 163 FA 2015

In effect we are pretending that we bought the asset on 31 March 1982 for its value at that date. This gives us the gross gain from which we can deduct indexation allowance to arrive at the indexed gain.

We compare this calculation based on the value of the asset at 31 March 1982 with the normal capital gain calculation based on cost. Consequently, if the value of the asset has risen from the time of purchase to March 1982, it will be advantageous to use the March 1982 value.

We will prepare two calculations; one based on cost and one based on the March 1982 value.

Where this produces two gains, we take the lower gain.

If this gives us two losses, we take the lower loss.

Where this produces one gain and one loss, the answer will be nil.

Indexation allowance runs from March 1982 and is based on the higher of the cost or March 1982 value in both calculations. A full proforma is shown at the end of the chapter.

It is possible for companies to make a “global rebasing election”. A global rebasing election means that the company will elect for all capital gains on pre 1982 assets to be calculated by reference to the March 1982 value instead of cost. TCGA 1992, s.35

This means that only one calculation will be performed – that being the one using March 1982 value.

A global rebasing election is irrevocable and applies to all assets held by the company at 31 March 1982. The election must be in writing and the time limit for the election is the two years from the end of the first chargeable accounting period in which a pre 1982 asset is sold. For most companies this time limit is likely to have already been passed.

The main advantage of making a global rebasing election is for administrative convenience – i.e. it takes away the need for the company to ascertain the original acquisition cost. A rebasing election can also give a company access to higher capital losses.

Illustration 6

Ventura Limited purchased a factory in June 1970 for £80,000. It was worth £160,000 on 31 March 1982. The factory is sold in September 2015 for £550,000.

Calculate the chargeable gain on sale of the factory.

Cost March 1982£ £

Proceeds 550,000 550,000Less: Cost/March 1982 value (80,000) (160,000)Unindexed gain 470,000 390,000Less: Indexation allowanceMarch 1982 to September 2015On higher of cost or March 1982 value(257.8 – 79.44)/79.44 = 2.245 × 160,000 (359,200) (359,200)Indexed gain 110,800 30,800

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 164 FA 2015

Indexation will run from March 1982 to September 2015 (date of sale) on the 31 March 1982 value of £160,000, being the higher of cost or March 1982 value, for both calculations.

As the two columns both produce capital gains, the lower gain is taken i.e. £30,800. This will be included in Ventura Limited's TTP and charged to corporation tax.

Illustration 7

Using the Ventura Limited illustration again, let's now assume that instead the asset was sold for £450,000. Original cost is still £80,000 and the value at 31 March 1982 is £160,000.

Calculate the chargeable gain on sale of the factory.

Cost March 1982£ £

Proceeds 450,000 450,000Less: Cost (80,000) (160,000)Unindexed gain 370,000 290,000Less: Indexation (2.245 × 160,000) (359,200) *(290,000)Indexed gain 10,800 Nil * The indexation is restricted so as not to produce a loss.

The lower amount is taken, i.e. nil.

15.7 Rollover Relief — Introduction

Where a company sells one qualifying asset and purchases another qualifying asset (or assets), within a specified period, the gain on the sale of asset 1 can be deducted from the base cost of asset 2 upon the company making an election. This will ensure that the company does not pay corporation tax on the gain arising at the time of the sale of the first asset. TCGA 1992, s.152

The effect of the rollover relief claim is to defer the gain on the sale of asset 1. By reducing the base cost of asset 2, a larger gain will arise on its subsequent sale.

These rules only apply when the company is selling assets used for the purposes of a trade. If only part of the asset is used in the trade, or for part of the period of ownership it is used for non-trade purposes, apportionments are made. The Government is keen to encourage companies to reinvest in their trading activities without having to pay corporation tax on gains along the way. TCGA 1992 s.152(1)

Eligible assets include:

i. Land and buildings; TCGA 1992, s.155 ii. Goodwill acquired or created prior to April 2002; iii. Fixed plant and machinery - “Fixed” means bolted to the floor or building. Goodwill bought or wholly created after 1 April 2002 is not within the capital gains regime because it is an intangible fixed asset.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 165 FA 2015

The specified period during which asset 2 must be purchased is one year before the disposal of asset 1 to three years afterwards. TCGA 1992, s.152(3)

The company must claim within 4 years of the end of the chargeable accounting period of the disposal of asset 1, or the chargeable accounting period in which asset 2 is acquired (whichever is later).

Illustration 8

Hugh Ltd acquired a freehold factory on 1 January 2007 for £500,000. Three of the five floors of the factory were used in the trade of the company, and the other floors were rented out. Hugh Ltd has a 31 December year end.

The factory (factory 1) was sold in August 2016 for £750,000. The company had moved into a smaller freehold factory (factory 2), which it had acquired in June 2016 for £490,000.

There will be a gain on the disposal of factory 1. However, as this is a qualifying asset that was 60% used in the trade of the company, and a new qualifying asset which will be used in the trade (factory 2) was acquired within 1 year before and 3 years after the disposal, 60% of the gain can potentially be rolled over.

When looking at proceeds reinvested, we again need to consider the trade use of the assets. So in this illustration, of the £750,000 proceeds 60% related to the trade use of factory 1, so £450,000 needs to be reinvested for full rollover relief. In this case, £490,000 has been reinvested, so rollover relief is available in full.

Disposal of factory 1 £

Proceeds (Aug 16) 750,000Less: Cost (Jan 07) (500,000)Less: Indexation allowance(260.0 - 201.6)/201.6 = 0.290 × 500,000 (145,000)Indexed gain 105,000Non trade use – immediately chargeable40% × £105,000 (42,000)Eligible for rollover relief 63,000Less: Rollover relief (63,000)Chargeable now (full proceeds reinvested) Nil The base cost of factory 2 is £490,000 less rollover relief of £63,000, so £427,000 .

£42,000 of the gain is chargeable in the accounting period of disposal of factory 1, so year ended 31 December 2016. A rollover relief claim must be made by 31 December 2020.

15.8 Rollover Relief - Proceeds Not Fully Reinvested

Illustration 9

Assume Hamster Ltd sells a business asset for £200,000 realising a chargeable gain of £80,000. Hamster Ltd uses the money to buy a replacement asset which costs £180,000. Therefore Hamster Ltd has not fully reinvested the proceeds of sale. TCGA 1992, s.153

Cash retained = 200,000 − 180,000 = £20,000

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 166 FA 2015

Where the company does not spend all of the sale proceeds, the amount of cash retained (£20,000) is immediately chargeable to corporation tax. This amount is the gain. This means that having made a chargeable gain of £80,000, the company is immediately charged on £20,000. The balance, here being £60,000, is the rollover relief that the company can claim.

Show the chargeable gain on the sale of the old asset, after claiming rollover relief and the base cost of the new asset.

£Proceeds 200,000Less: Cost + indexation (120,000)Gain 80,000Less: Rollover relief (60,000)Gain (200,000 − 180,000) 20,000 The £60,000 will be rolled over and reduces the base cost of the new asset.

£Cost 180,000Less: Rolled over gain (60,000)Base cost of new asset 120,000

Illustration 10

Assume Gerbil Ltd sells a business asset for £200,000, realising a chargeable gain of £80,000. It uses part of the sale proceeds to buy a replacement asset. The new building is considerably smaller and costs £110,000.

Calculate the chargeable gain on the sale of the old asset, after claiming all available reliefs and show the base cost of the new asset.

Where a company has not fully reinvested its proceeds of sale, we must identify the amount of cash retained.

Cash retained = 200,000 − 110,000 = £90,000 However, it is not possible for HMRC to charge Gerbil Ltd on a gain of £90,000, as its actual gain is only £80,000. Therefore the whole of this gain of £80,000 will be immediately charged to tax, and no rollover relief will be available. The base cost of the new asset will remain at £110,000.

This demonstrates that when the cash retained by the company exceeds the chargeable gain, the whole of the gain is chargeable and no rollover relief can be claimed.

£Proceeds 200,000Less: Cost + indexation (120,000)Gain 80,000Less: Rollover relief NilGain 80,000

Base cost of new asset 110,000

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 167 FA 2015

15.9 Rollover Relief - Depreciating Assets

A depreciating asset for chargeable gains purposes is similar to a “wasting asset”. A “wasting asset” is an asset with a useful life of not more than 50 years. A depreciating asset is either a wasting asset, or an asset which will become a wasting asset within the next 10 years. Therefore a depreciating asset is an asset with a useful life not exceeding 60 years. TCGA 1992, s.154(7)

Plant and machinery is always regarded as having a useful life not exceeding 60 years, and is therefore a depreciating asset. The other common type of depreciating asset is a lease of not more than 60 years on land and buildings used in the business.

Where the asset being purchased is a depreciating asset, we do not take the gain on the original asset and roll it over against the base cost of the replacement. If the replacement asset is a depreciating asset, relief is given by freezing the gain on the old asset for a certain period of time. TCGA 1992, s.154(2)

Illustration 11

A Ltd sells a building in July 2015. Proceeds are £200,000, giving rise to a gain of £80,000. The building is replaced with fixed plant and machinery bought in May 2015 for £180,000.

Calculate the chargeable gain on the sale of the building and state the base cost of the fixed plant and machinery.

All of the conditions for rollover relief have been satisfied. Both assets are used in the trade, both assets are on the list of qualifying assets, and the reinvestment takes place within the four year time window.

However the way in which we defer the chargeable gain in this instance is slightly different, because the replacement asset, i.e. the asset purchased, is a depreciating asset. As not all of the sale proceeds have been reinvested in the replacement asset, A Ltd will have a gain of £20,000 which is immediately chargeable to corporation tax, whilst the remaining £60,000 will be deferred.

£Proceeds 200,000Less: Cost + indexation (120,000)Gain 80,000Less: Deferred gain (60,000)Gain chargeable (200,000 − 180,000) 20,000

Where the replacement asset is a depreciating asset, the deferred gain is not rolled over. The base cost of the plant and machinery remains at £180,000.

Instead of reducing the base cost of the replacement asset, the £60,000 is “frozen”.

The frozen gain crystallises on the earliest of three events: TCGA 1992, s.154(2)

i. The frozen gain will become chargeable if the depreciating asset, i.e. the plant and machinery, is sold by A Ltd.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 168 FA 2015

ii. If A Ltd stops using the plant and machinery within its trade, for example the machine starts being used for a non-business purpose, this will also crystallise the frozen gain.

iii. If neither of these two events happens, the frozen gain will automatically

crystallise 10 years after the acquisition of the depreciating asset. In the example, the plant and machinery was purchased in May 2015. Therefore the frozen gain of £60,000 will “unfreeze” in May 2025 at the latest.

Illustration 12

In the previous illustration, the frozen gain was £60,000. This gain was frozen when the original building was sold in July 2015. A Ltd bought plant and machinery in May 2015 and the base cost of this plant and machinery is £180,000.

Assume that A Ltd sells the machinery in June 2016 for £195,000.

Calculate the chargeable gains arising on the sale of the fixed plant and machinery.

A gain will arise on the sale as follows:

June 2016 £Proceeds 195,000Less: Cost (180,000)Less: Indexation (0.009 × 180,000) (1,620)Gain 13,380 The sale of the depreciating asset will also lead to the crystallisation of the frozen gain.

The chargeable gain which crystallises in June 2016 is £60,000. We add this to the gain on the sale of the plant and machinery:

£Gain 13,380Add: Frozen gain crystallising 60,000Total chargeable gains 73,380

15.10 Rollover Relief - the 50% Rule

The “50% rule” is a slightly strange rule introduced in 1988, as a means of giving rebasing relief for assets acquired before March 1982 for which rollover relief is claimed as rebasing was not introduced until April 1988. The “50% rule” applies if three specific conditions have been satisfied: TCGA 1992, Sch 4

1. The company must have acquired an asset before 31 March 1982. TCGA 1992, Sch 4 para 2

2. The asset must have been sold by the company between 31 March 1982 and 5

April 1988. 3. Having made the disposal, the company must have claimed rollover relief, so

that all or part of the original gain is rolled over and reduces the base cost of the replacement asset.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 169 FA 2015

If all three conditions are satisfied, the gain rolled over against the base cost of the replacement asset is not the whole of the original gain, but is only 50% of that gain. By rolling over a smaller amount, we are increasing the base cost of the replacement asset and thereby reducing the eventual capital gain when the replacement asset is sold.

Illustration 13

A company bought a building for £20,000 in June 1980. The company sells the building for £50,000 in May 1986. The gain is calculated by taking proceeds less cost less indexation allowance. Indexation accrues between March 1982 and the date of sale in May 1986. Remember, in calculating this capital gain we do not do a calculation using the March 1982 value instead of cost, because the rebasing rules were not introduced until April 1988, and this disposal was in May 1986.

£Proceeds 50,000Less: Cost (20,000)Less: Indexation allowance(March 1982 to May 1986)20,000 × 0.232 (4,640)Gain 25,360 In June 1986, the company reinvested the sales proceeds in acquiring a replacement building costing £80,000. The whole of the sales proceeds from the first disposal have been reinvested in acquiring a replacement asset, so the whole of the gain of £25,360 can be rolled over.

However, because we have a pre-1982 asset, which was sold between 1982 and 1988 and a rollover relief claim has been made, what is rolled over is not all of the gain of £25,360, but only 50% of it.

£Cost 80,000Less: 50% of rolled-over gain (12,680)Base cost of replacement asset 67,320 Building number 2 is sold for £200,000 in September 2015. Building number 2 is treated as having been bought in June 1986 for its revised base cost of £67,320. Indexation runs from June 1986 until September 2015, giving a gain of:

£Proceeds 200,000Less: Cost (67,320)Less: Indexation allowance(257.8 – 97.79)/97.79 = 1.636 × 67,320 (110,136)Gain 22,544 This “50% rule” can be difficult to spot. Only 50% of the gain will be rolled over, where:

i. a pre-1982 asset; ii. is sold between 1982 and 1988; and iii. the gain is deferred.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 170 FA 2015

15.11 Shares and Securities

Before we examine the treatment of shares, we will consider why we need special rules in the first place.

Consider A Ltd which has been buying shares in a quoted company called XYZ plc for a number of years. The share purchases have been as follows:

Date Shares Cost£

June 1986 3,000 9,000September 1990 2,000 8,000December 2005 4,000 20,000Total 9,000 37,000 A Ltd currently has 9,000 shares, which have been acquired in three tranches between 1986 and 2005 at various costs. The total cost of A Ltd's shareholding is £37,000.

In August 2015, A Ltd sells 6,000 of the XYZ plc shares for £36,000. The capital gain calculation will therefore be:

£Proceeds 36,000Less: Base cost (?)Capital gain X In order to calculate the chargeable gain arising on the sale of these 6,000 shares, we need to identify their base cost. To calculate the base cost, we need to identify which shares A Ltd has sold.

The share “matching” rules determine the order in which shares are deemed to have been sold. The “matching” rules we are about to study apply for companies only. There are different matching rules for disposals of shares by individuals.

Also note that the “matching” rules only apply to shares in the same class in the same company. We should never mix up different types of shares or different companies. Indeed, with shares of different types there is no need for matching rules because there is not the same difficulty telling them apart.

The matching rules for companies is as follows:

1. First, the company is deemed to have sold any shares it acquired on the same day. TCGA 1992, s.105

2. The next shares deemed to have been sold are those acquired in the previous

9 days, on a first in first out basis. No indexation allowance is given on these shares. TCGA 1992, s.107(3)

3. Then the disposal will be matched with share acquisitions from 1 April 1982 to 9

days before the disposal, which are “pooled” together and form one asset for capital gains purposes. This asset is called the “Section 104 pool”. This is an indexed pool. TCGA 1992, s.107(8)

To calculate the indexation allowance, you take any acquisitions from 1 April 1982 to 31 March 1985, index each acquisition up to March 1985 and include

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 171 FA 2015

them in the pool. From 1 April 1985, indexation is calculated on the pool as a whole, and is not rounded to 3 decimal places.

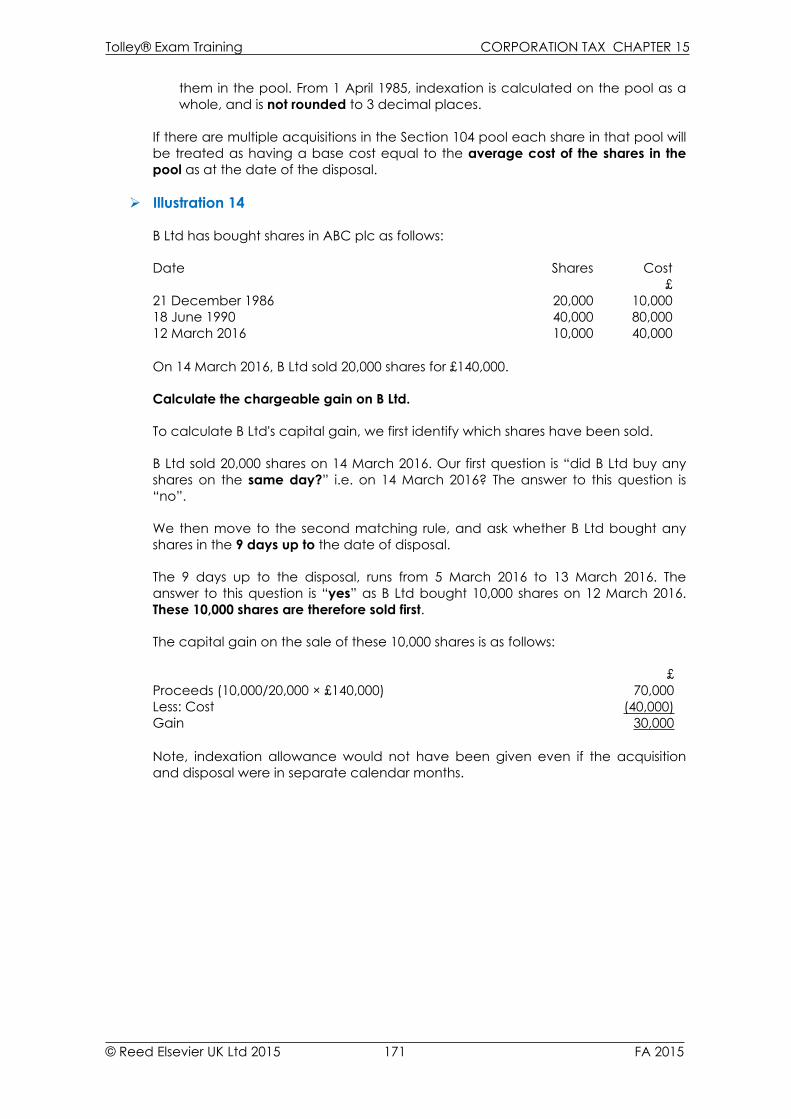

If there are multiple acquisitions in the Section 104 pool each share in that pool will be treated as having a base cost equal to the average cost of the shares in the pool as at the date of the disposal.

Illustration 14

B Ltd has bought shares in ABC plc as follows:

Date Shares Cost£

21 December 1986 20,000 10,00018 June 1990 40,000 80,00012 March 2016 10,000 40,000 On 14 March 2016, B Ltd sold 20,000 shares for £140,000.

Calculate the chargeable gain on B Ltd.

To calculate B Ltd's capital gain, we first identify which shares have been sold.

B Ltd sold 20,000 shares on 14 March 2016. Our first question is “did B Ltd buy any shares on the same day?” i.e. on 14 March 2016? The answer to this question is “no”.

We then move to the second matching rule, and ask whether B Ltd bought any shares in the 9 days up to the date of disposal.

The 9 days up to the disposal, runs from 5 March 2016 to 13 March 2016. The answer to this question is “yes” as B Ltd bought 10,000 shares on 12 March 2016. These 10,000 shares are therefore sold first.

The capital gain on the sale of these 10,000 shares is as follows:

£Proceeds (10,000/20,000 × £140,000) 70,000Less: Cost (40,000)Gain 30,000 Note, indexation allowance would not have been given even if the acquisition and disposal were in separate calendar months.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 172 FA 2015

We next look at the Section 104 pool. The remaining acquisitions were all made between 1 April 1982 and 5 March 2016 and so form the Section 104 pool. The remaining 10,000 shares sold will be sold from the 60,000 shares in the Section 104 pool holding.

ABC plc shares No. Cost Indexed cost

£ £Dec 1986 Acquisition 20,000 10,000 10,000

June 1990 Indexation: Dec 86 to June 90[(126.7 − 99.62)/99.62] × 10,000 2,718Acquisition 40,000 80,000 80,000

60,000 90,000 92,718Mar 2016 Indexation: June 90 to Mar 16

[(259.1 − 126.7)/126.7] × 92,718 96,889189,607

Disposal (10,000/60,000) (10,000) (15,000) (31,601)Balance C/fwd 50,000 75,000 158,006 A Ltd's capital gain will therefore be:

£Proceeds (10,000/20,000 × 140,000) 70,000Less: Cost (15,000)Unindexed gain 55,000Less: Indexation (31,601 − 15,000) (16,601)Capital gain 38,399 B Ltd has therefore sold 2 assets:

1. 10,000 shares bought on 12 March 2016; and 2. 10,000 shares from the Section 104 holding The total gain on sale is:

£Gain on shares acquired March 2016 30,000Gain on shares in Section 104 holding 38,399Net chargeable gain 68,399

15.12 Disposal of Substantial Shareholding

Disposals by a company of “substantial shareholdings” in other companies are exempt from tax. Consequently, gains are not taxable and losses are not allowable when dealing with disposals of substantial shareholdings. The rules apply to shareholdings in both UK resident and non resident companies.

A substantial shareholding is defined as 10% or more of a company's ordinary share capital. The ordinary shares held must also give entitlement to at least 10% of the company's distributable profits and 10% of assets on a winding up. For these purposes, the holdings of other group members are taken into account. TCGA 1992, Sch 7AC para 8

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 173 FA 2015

To qualify:

i. A substantial shareholding must have been held throughout a 12 month period beginning not more than two years before the sale takes place; TCGA 1992, Sch 7AC para 7

ii. the investing company must either be a sole trading company or a member of

a trading group; iii. the shares must be in a qualifying company, which is defined as a trading

company or the holding company of a trading group; Conditions (ii) and (iii) must apply in the latest 12 month period in which the substantial shareholding test has been satisfied and ending with the time of the disposal, AND immediately following the disposal. TCGA 1992, Sch 7AC paras 18 & 19

15.13 Loss on Sale of Corporate Venturing Scheme (CVS) Shares

Prior to 1 April 2010, companies investing in CVS companies (small unquoted trading companies) received tax relief by way of a tax reducer. The tax reducer was usually 20% of the amount invested (or a lower amount if the tax relief reduced the CT liability to zero). There was no upper limit.

Where a capital loss is made on disposal of CVS shares, it is reduced by the amount of any CVS tax reducer that was originally given.

If a company sells shares in a qualifying CVS company and makes a loss on the sale, the interaction with the substantial shareholdings rules must be considered. If the CVS holding qualifies under the substantial shareholdings rules, no capital loss is allowable.

However, if the holding is not a substantial shareholding, there are two things the company can do with the capital loss. It may:

1. set the loss against chargeable gains in the same chargeable accounting period and carry forward any remaining losses against future chargeable gains; or

2. elect to deduct the loss from its other income, before deductions for qualifying

charitable donations, in the same chargeable accounting period and then from any income in the preceding 12 months. FA 2000, Sch 15 para 68

Any allowable loss is reduced by the corporation tax relief already obtained.

Illustration 15

Williams plc, a UK quoted company with a 31 March year end, invested £500,000 in shares in Orange Ltd, a qualifying CVS company, in June 2007 and obtained maximum relief. The holding was not a substantial shareholding.

Williams plc sold the Orange Ltd shares in September 2015 for £320,000. It had other profits for the year ended 31 March 2016 of £1.9m.

Assuming all relevant claims are made, calculate the corporation tax liability of Williams plc for the year ended 31 March 2016.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 174 FA 2015

In its year ended 31 March 2008, Williams plc would have received corporation tax relief of:

500,000 × 20% = £100,000

As the holding was not a substantial shareholding, the capital loss on the sale of the shares in September 2015 is calculated as follows:

£Proceeds 320,000Less:Cost 500,000CVS relief received in y/e 31.3.08 (100,000)

(400,000)Allowable capital loss (80,000) Williams plc can elect to set this loss against its other income in the year ended 31 March 2016 (the CAP in which the loss was actually made).

The corporation tax computation for the year ended 31 March 2016 will be:

£Profits before loss relief 1,900,000Less: CVS loss relief (80,000)TTP 1,820,000

CT @ 20% 364,000

15.14 Paper for Paper Exchanges

The rules for companies are essentially the same as for individuals. Where shares or non-qualifying corporate bonds are received we use the no disposal fiction. If cash is received as well as securities then there will be a disposal and indexation will be available. TCGA 1992, s.116(10)

Where shares are replaced by QCBs in a reorganisation, the shares are treated as though they had been disposed of at market value and the resulting gain or loss is then deferred and only recognised on the disposal of the QCBs. In the meantime, the QCBs are subject to the normal loan relationship rules. TCGA 1992, s.116 (10)

However, where under a s.135 TCGA 1992 or s.136 TCGA 1992 reorganisation, a QCB (i.e. a loan relationship) is replaced by shares or other QCBs, then there is no deferral of the gain or loss and there is an immediate recognition. The gain or loss is brought into the loan relationship provisions. TCGA 1992, s.116 (8A)

The assumption made in s.127 TCGA 1992 of there being no disposal and the new holding being treated as the acquisition of the old holding is not applied. The new asset of shares or securities is treated as being effectively acquired at market value.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 175 FA 2015

EXAMPLES

Example 1

Cresta Ltd purchased a warehouse in May 1991 for £425,000 and incurred solicitor's and surveyor's fees on this purchase amounting to £2,000. Stamp Duty Land Tax was charged at 3% on the purchase price and this was payable by Cresta Ltd. The warehouse was sold in January 2016 for £1.5 million and solicitor's fees of £3,000 were incurred.

You are required to calculate the indexed chargeable gain.

Example 2

Burrow Ltd has a 31 December year end and bought a warehouse in May 2011 for £80,000. The warehouse was sold in October 2015 for £200,000. Assume the indexation allowance between May 2011 and October 2015 is £8,000.

Burrow Ltd bought an office block in August 2016 for £170,000. Both buildings were used wholly for trade purposes.

a. Assuming all relevant claims are made calculate Burrow Ltd's chargeable gains in year ended 31 December 2015 and show the base cost of the office block. State the date by which the claim must be made.

b. Explain how your answer would be different if instead of an office block,

Burrow Ltd purchased fixed plant and machinery in August 2016.

Example 3

ABC Ltd had the following share transactions in DEF plc:

Date Event No. Cost Proceeds£ £

1.3.16 Buy 10,000 15,00017.3.16 Buy 6,000 10,00021.3.16 Sell 8,000 16,00021.3.16 Buy 4,000 10,00028.3.16 Buy 6,000 18,000 Calculate ABC Ltd's gain/(loss) on the sale in March 2016.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 176 FA 2015

Example 4

Regan plc has one wholly owned subsidiary and prepares accounts to 31 December each year.

In November 2006, Regan plc subscribed for £120,000 of shares in Waterman Ltd, an unquoted trading company. This represented an 8% holding in Waterman Ltd. CVS relief was available on the subscription.

On 29 December 2015, Regan plc sold its shares in Waterman Ltd for £75,000.

Its results for the year ended 31 December 2015 were as follows:

£Trade profit 148,000Non-trading profit (LR) 47,000Cash donation paid to charity (8,000)Dividend received from ICI plc 13,500 Assuming all relevant claims are made, calculate the TTP for Regan plc for the year ended 31 December 2015.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 177 FA 2015

ANSWERS

Answer 1

£ £Proceeds 1,500,000Less: Incidental costs (3,000)Net sale proceeds 1,497,000Less:Cost 425,000Incidental costs 2,000Stamp duty land tax (425,000 × 3%) 12,750

(439,750)Unindexed gain 1,057,250Less: Indexation allowanceMay 1991 to January 2016(258.6 – 133.5)/133.5 = 0.937 × 439,750 (412,046)Indexed gain 645,204

Answer 2

a) Y/e 31 Dec 2015 £

Warehouse:Proceeds 200,000Less: Cost (80,000)Unindexed gain 120,000Less: Indexation allowance (8,000)Gain before rollover 112,000Less: Rollover relief (82,000)Gain (200,000 - 170,000) 30,000

Office block:Cost 170,000Less: Rolled over gain (82,000)Base cost of new asset 88,000 The rollover relief claim would need to be made by 31 December 2020, 4 years from the end of the accounting period of the purchase of the office block (as this is in a later accounting period than the disposal).

b)

If Burrow Ltd had purchased fixed plant and machinery, the gain on the warehouse and the amount of the rollover relief would remain the same.

However, fixed plant and machinery is a depreciating asset and therefore its base cost would remain unchanged at £170,000.

The £82,000 of rolled over gain is instead frozen and crystallises on the earliest of:

• the subsequent sale of the fixed plant and machinery, • the date the fixed plant and machinery ceases to be used in the trade, and

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 178 FA 2015

• 10 years after the acquisition of the fixed plant and machinery.

Answer 3

8,000 shares sold 21.3.16

Same day? Yes 4,000 bought 21.3.16Previous 9 days Yes 4,000 out of 6,000 bought 17.3.16

8,000 Disposal 1 – sale of 4,000 shares bought 21.3.16 £ £Proceeds16,000 × (4,000/8,000) 8,000Less: Cost (21.3.16) (10,000)Loss (2,000) (2,000) Disposal 2 – sale of 4,000 shares bought 17.3.16Proceeds16,000 × (4,000/8,000) 8,000Less: Cost (17.3.16)10,000 × (4,000/6,000) (6,667)Gain 1,333 1,333

Net loss (667) Note:

No indexation is available when disposing of shares acquired in the previous 9 days, whether in same month as disposal or not.

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 179 FA 2015

Answer 4

Tax relief originally given in y/e 31.12.06 = 120,000 × 20% = £24,000

As the holding is only 8% it is not a substantial shareholding and so there is an allowable loss on the disposal.

Loss relief on sale of Waterman Ltd shares can be claimed against other income for the CAP in which the loss was made. Allowable loss is:

£Proceeds 75,000Less:Cost 120,000Less: CVS relief received in y/e 31.12.06 (24,000)

(96,000)Allowable loss (21,000) The corporation tax computation will therefore be:

£Trade profit 148,000Non-trading profit (LR) 47,000

195,000Less: CVS loss relief(deducted before qualifying charitable donations) (21,000)

174,000Less: Qualifying charitable donation – cash donation paid

(8,000)

TTP 166,000