chapter 16

TRANSCRIPT

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-1

Week 11 - Quality Costs and Productivity:

Measurement, Reporting, and ControlChapter 16

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-2

Learning Objectives

1. Identify and describe the four types of quality costs.

2. Prepare a quality cost report and explain the difference between the conventional view of acceptable quality level and the view espoused by total quality control.

3. Explain why quality cost information is needed and how it is used.

4. Explain what productivity is and calculate the impact of productivity changes on profits.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-3

Quality Defined

Quality of Design: The degree of excellence, which is a function of a product’s specifications

– Example: Compare a Cadillac Seville with a Honda Civic. The Seville is a luxury car with specially designed features and the Civic is an economy car with standard features. Both are designed to provide transportation but the design quality are obviously different

Quality of Conformance: The degree of excellence, which is a measure of how well the product meets its requirements or specifications

– Example: If the Honda Civic does what it is designed to do and does it well, quality exists. If an economy car is designed to provide reliable, low-cost, low-maintenance transportation, the desired quality exists

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-4

Quality Dimensions

Performance consistently Aesthetics Serviceability Features or quality of design Reliability Durability Quality conformance Achievement of advertised functions

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-5

Measuring the Costs of Quality

Control activities Prevention costs Appraisal costs

Failure activities Internal failure costs External failure costs

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-6

Estimating Hidden Quality Costs

The Multiplier Method The Market Research Method

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-7

Examples of Quality Costs

Prevention costs Appraisal Costs

Quality engineering Inspection of raw materials

Quality training Packaging inspection

Quality planning Product acceptance

Quality audits Process acceptance

Design reviews Field testing

Quality circles Supplier verification

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-8

Internal failure costs External failure costs

Scrap Lost sales

Rework Returns/allowances

Downtime (defect related) Warranties

Reinspection Repair

Retesting Product liability

Design changes Complaint adjustment

Examples of Quality Costs

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-9

Reporting Quality Costs Quality Costs %of Sales

Prevention costs:

Quality training $35,000

Reliability engineering 80,000 $115,000 4.11

Appraisal costs:

Materials inspection $20,000

Product acceptance 10,000

Process acceptance 38,000 68,000 2.43

Internal failure costs:

Scrap 50,000

Rework 35,000 85,000 3.04

External failure costs:

Customer complaints 25,000

Warranty 25,000

Repair 15,000 65,000 2.32

Total quality costs $333,000 11.90%

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-10

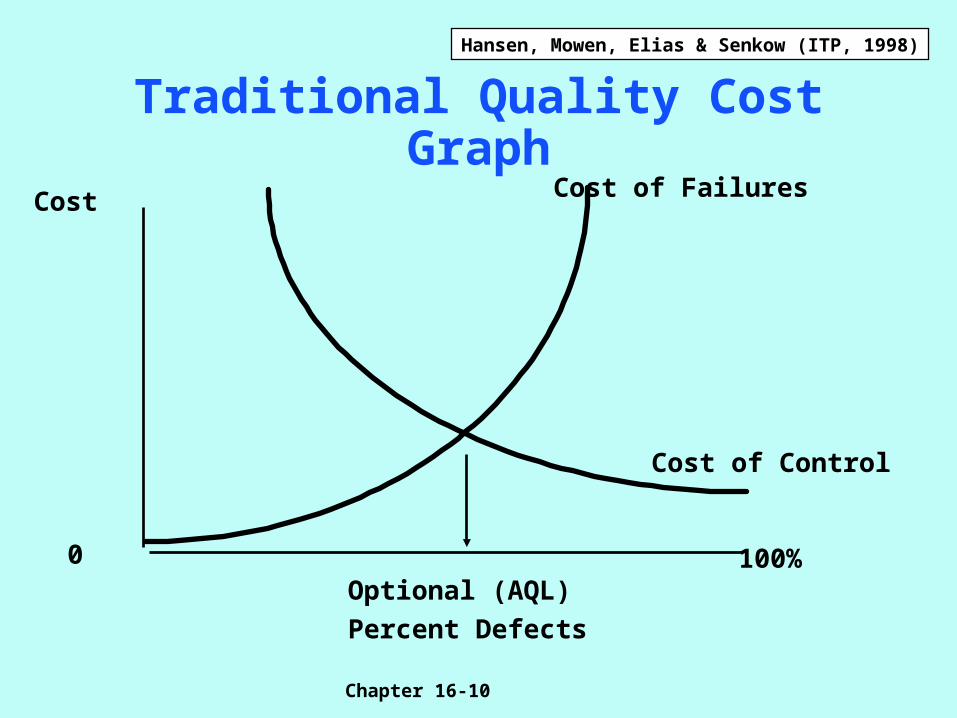

Traditional Quality Cost Graph

Cost

0Optional (AQL)

Percent Defects

100%

Cost of Failures

Cost of Control

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-11

ZERO-DEFECT GRAPH

Cost Total

Quality

Cost

0 100%

Percentage Defects

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-12

Types of Quality Performance Reports

Progress with respect to a current-period standard or goal.

Progress with respect to last year’s quality performance.

The progress trend since the inception of the quality improvement program.

Progress with respect to the long-range standard or goal.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-13

Prevention costs:

Quality training $35,000 $30,000 $5,000U

Reliability engineering 80,000 $115,000 80,000 $110,000 0 $5,000U

Appraisal costs:

Materials inspection $20,000 $28,000 $8,000F

Product acceptance 10,000 15,000 5,000F

Process acceptance 38,000 $68,000 35,000 $78,000 3,000U $10,000F

Internal failure costs:

Scrap 50,000 $44,000 6,000U

Rework 35,000 $85,000 36,500 $80,500 1,500F $4,500U

External failure costs:

Customer complaints 25,000 $25,000 $ 0

Warranty 25,000 20,000 5,000U

Repair 15,000 $65,000 17,500 $62,500 2,500F $2,500U

Total quality costs $333,000 $331,000 $2,000U

Cost Item Actual Costs Budgeted Costs Variance

Interim Quality Cost Report

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-14

Actual Costs Actual Costs

Cost Item 1998 1997 Variance

Quality Cost: One-year Trend

Prevention costs:

Quality training $35,000 $36,000 $1,000F

Reliability engineering 80,000 $115,000 120,000 $156,000 40,000F $41,000F

Appraisal costs:

Materials inspection $20,000 $33,600 $13,600F

Product acceptance 10,000 16,800 6,800F

Process acceptance 38,000 $68,000 $39,200 $89,600 1,200F $21,600F

Internal failure costs:

Scrap 50,000 $48,000 2,000U

Rework 35,000 $85,000 40,000 $88,000 5,000F $3,000F

External failure costs:

Customer complaints 25,000 $33,000 $8,000F

Warranty 25,000 23,000 2,000U

Repair 15,000 $65,000 16,400 $72,400 1,400F $7,400F

Total quality costs $333,000 $406,000 $73,000F

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-15

Multiple-Period Quality Costs

Quality Costs Actual Sales %of Sales

1994 $462,000 $2,200,000 21.0

1995 423,000 2,350,000 18.0

1996 412,500 2,750,000 15.0

1997 406,000 2,800,000 14.5

1998 333,000 2,800,000 11.9

Assume the following data:

Worksheet

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-16

Multiple-Period Total Quality Costs

0

5

10

15

20

25

1994 1995 1996 1997 1998

Total Quality Costs as a % of Sales

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-17

Multiple-Trend Analysis for Individual Quality Costs

Internal External

Prevention Appraisal Failure Failure

1994 6.0%1 4.5% 4.5% 6.0%

1995 6.0 4.0 3.5 4.5

1996 5.4 3.6 3.0 3.0

1997 5.6 3.2 3.1 2.6

1998 4.4 2.4 3.0 2.3

Assume the following quality cost data:

1Expressed as a % of sales

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-18

Quality Cost Information

For monitoring quality performance For understanding the relationship between

quality and costs For suggesting alternative programs For implementing new programs

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-19

Illustration of Productivity Improvement

Technical Efficiency: Condition where no more of any one input is used than necessary to produce a given output.

A. Technical efficiency improvement: using less input to produce the same output or producing more output using the same input.

B. Price efficiency improvement: using a less costly input mix to produce the same output.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-20

Partial Productivity Measures

I. Partial Productivity Measurement: measuring productivity for one input at a time.

Partial Measure = Output / Input

II. Operational Productivity Measure: partial measure where both input and output are expressed in physical terms.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-21

Productivity: Measurement and Control

Productivity Measurement Defined - Productivity is the

relationship between output and the inputs used to produce

the output.

Partial Productivity Ratio = Output/Input

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-22

Productivity Measurement

Assume the following data:

1995 1996

Number of heaters produced 110,000 110,000

Labour hours used 11,000 10,000

Material used (kgs.) 110,000 88,000

Unit selling price (heaters) $25 $25

Wages per labour hour $10 $10

Cost per pound of material $5 $5

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-23

Operational Productivity Measurements

1995a 1996b

Labour productivity ratio 10.00 11.00

Material productivity ratio 1.00 1.25

Ratios do not reveal the value of the improvement

labour: 110,000/11,000; Materials: 110,000/110,000bLabour: 110,000/10,000; Materials: 110,000/88,000

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-24

Profit-Linked Productivity Measurement

Profit-Linkage Rule: The measure of value of productivity changes

is the difference between costs of inputs that should be used

in the absence of any productivity change and the cost of inputs

actually used. The difference in costs is the amount by which profits

changed because of productivity changes.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

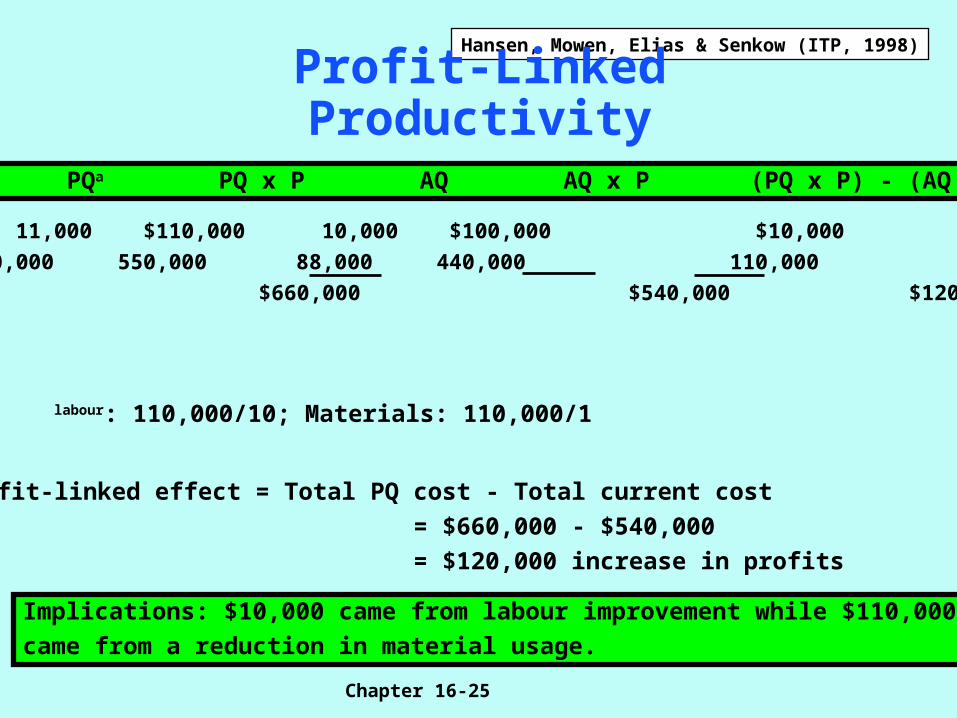

Chapter 16-25

Profit-Linked Productivity

Input PQa PQ x P AQ AQ x P (PQ x P) - (AQ x P)

Labour 11,000 $110,000 10,000 $100,000 $10,000

Materials 110,000 550,000 88,000 440,000 110,000

$660,000 $540,000 $120,000

labour: 110,000/10; Materials: 110,000/1

Profit-linked effect = Total PQ cost - Total current cost

= $660,000 - $540,000

= $120,000 increase in profits

Implications: $10,000 came from labour improvement while $110,000

came from a reduction in material usage.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-26

In-Class AssignmentPrevention

- quality engineering

- receiving inspection

- quality training

Appraisal

- product inspection

Internal failure

- scrap

- rework

External failure

- net cost of returned products

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-27

Cost of Quality Report Shortcomings

Information is not explicitly gathered Budgets are not prepared Quantitative measures are missing Responsibility not properly delegated

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-28

Numerical Questions from the Back of Chapter 16

W16-3, E16-3, E16-7,E16-13.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-29

Question E16-3

Please return to the textbook to read the question.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-30

Question E16-7

Please return to the textbook to read the question.

Hansen, Mowen, Elias & Senkow (ITP, 1998)

Chapter 16-31

Question E16-13

Please return to the textbook to read the question.