chapter 19 pricing concepts. introductionintroduction price: the exchange value of a good or service...

Post on 20-Dec-2015

215 views

TRANSCRIPT

Chapter 19Pricing Concepts

Chapter 19Pricing Concepts

IntroductionIntroduction• Price: the exchange value of a

good or service

some unit of value given up for something of value

Other TermsOther Terms

• Terms Used• Tuition• Fare• Fine• Tip• Bribe

Price CompetitionPrice Competition

CustomerNeeds

PriceCompetition

Slippery slope.

CustomerNeeds

ProductCompetition

PromotionCompetition

DistributionCompetition

Nonprice CompetitionNonprice Competition

Emphasize value and therefore increase quality

The Importance of Price to MarketersThe Importance of Price to Marketers• Manage demand

• Adapt to competitive environment

• Psychology of the consumer

• BOTTOMLINE issues

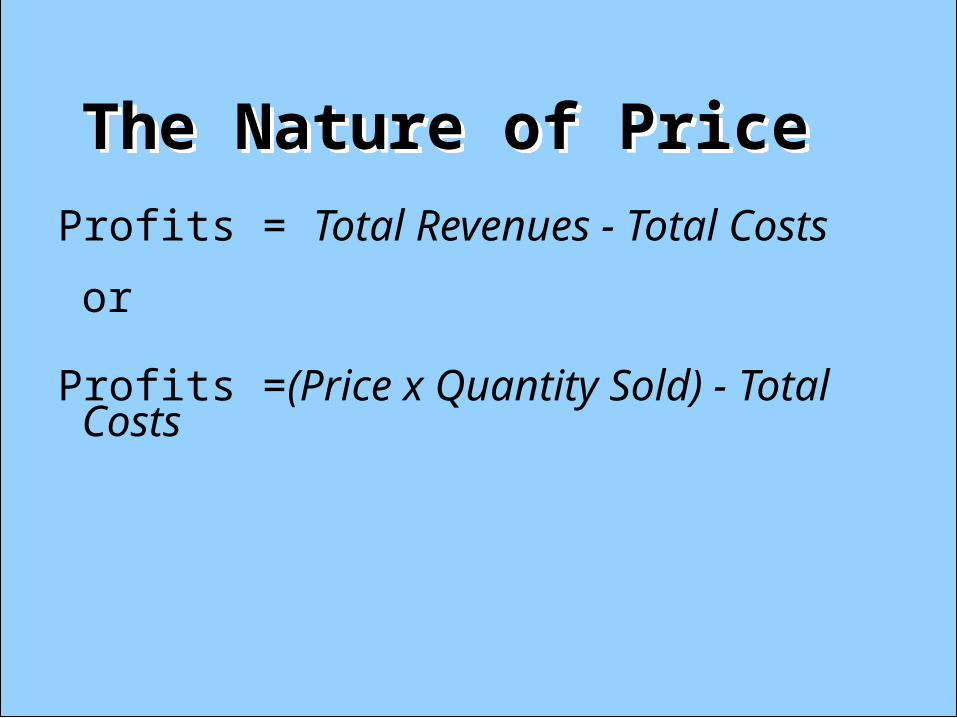

The Nature of PriceThe Nature of Price

Profits = Total Revenues - Total Costs

or

Profits =(Price x Quantity Sold) - Total Costs

Steps in Setting the Right PriceSteps in Setting the Right Price

Results lead to the right price

Fine tune with pricing tacticsFine tune with pricing tactics

Choose a price strategyChoose a price strategy

Estimate demand, costs, and profitsEstimate demand, costs, and profits

Establish pricing objectivesEstablish pricing objectives

Pricing ObjectivesPricing Objectives

Profit-orientedProfit-oriented• Profit Maximization:

• Target-Return Objectives:achieving a specified return on

either sales or investment

ROI = Net Profit after taxes Total assets

Pricing ObjectivesPricing Objectives

Profitability

Sales-orientedSales-oriented

• Sales maximization:

• Market-share objectives:for controlling a portion of the market

Price and Market SharePrice and Market Share

Pricing ObjectivesPricing Objectives

Meeting Competition

Meeting Competition

• Passive (status quo pricing)

• Value Pricing (starts with the customer, consider the competition and then sets the right price)

Profitability

Volume

Pricing ObjectivesPricing Objectives

Meeting Competition

PrestigePrestige

• Prestige Objectives: set at a relatively high level to help promote a high quality image

Profitability

Volume

PRICE DETERMINATION IN ECONOMIC THEORYPRICE DETERMINATION IN ECONOMIC THEORY

• Demand: schedule of the amounts of a firm’s good or service that consumers purchase at different prices during a specified period

• Supply: schedule of the amounts of a good or service that firms will offer for sale at different prices during a specified time period.

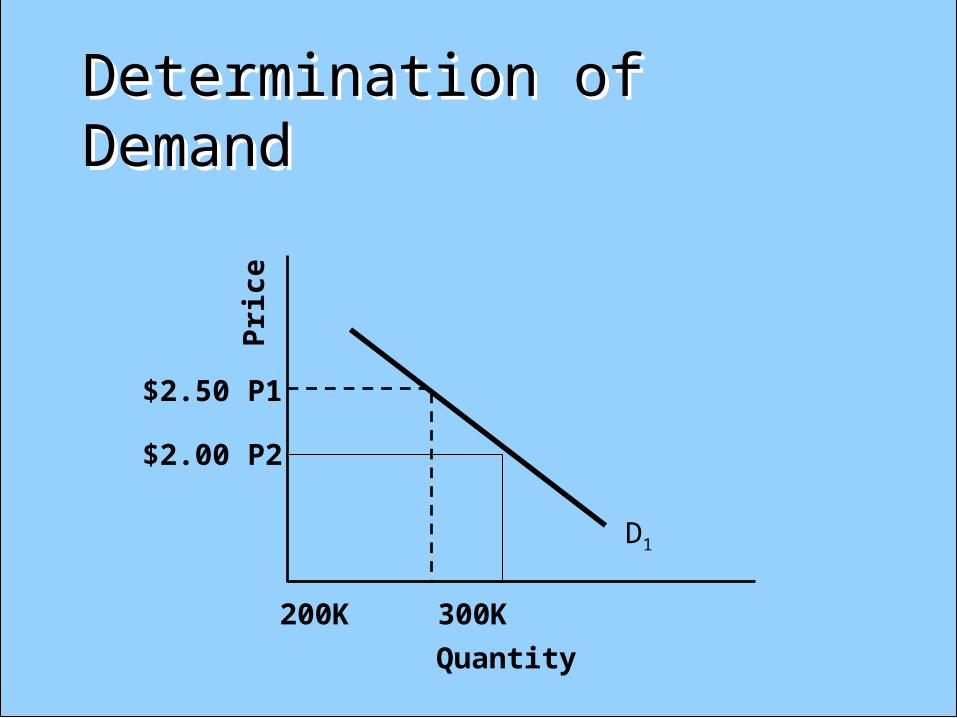

Determination of DemandThe Demand Curve Price/Quantity Relationship

Determination of DemandThe Demand Curve Price/Quantity Relationship

Q1 200K

Quantity

$2.50 P1

D1

Pri

ce

Determination of DemandDetermination of Demand

200K 300K

Quantity

$2.50 P1

D1

Pri

ce

$2.00 P2

Determination of DemandDetermination of Demand

200K 300K 400K

Quantity

$2.50 P1

D1

Pri

ce

$2.00 P2

$1.50 P3

The Concept Of Elasticity In Pricing StrategyThe Concept Of Elasticity In Pricing Strategy• Elasticity: measure of consumers

responsiveness to changes in price

Price Elasticity of Demand

% Change in Quantity Demanded

% Change in Price=

If Abs(elasticity) > 1 then DEMAND is ELASTIC

If Abs(elasticity) < 1 then DEMAND is INELASTIC

Determinants Of ElasticityDeterminants Of Elasticity

Availabilityof Substitutes

Luxury orNecessity

Portion ofBudget

Time

Determination of Demand - INELASTIC Determination of Demand - INELASTIC

Q2 Q1 Quantity

P1

P2

Pri

ce

Demand is not very sensitive to price increases

Determination of Demand - ELASTIC Determination of Demand - ELASTIC

Q2Quantity

P1

P2

Q1

Pri

ceDemand is very sensitive to price increases

Some Elasticity CalculationsSome Elasticity Calculations• % Change in Price = 10% (increase)• % Change in Quantity = -20% (decrease)• Abs(Elasticity) =

• Elastic?

Some Elasticity CalculationsSome Elasticity Calculations

• % Change in Price = +10% (increase)• % Change in Quantity = -5% (decrease)• Abs(Elasticity) =

• Elastic?

Elasticity and RevenuesElasticity and Revenues• Baseline Case• 100 units sold @ $ 10 each• Total Revenues = $ 10 * 100 units = $1000.

• Case I• Let us drop price to $8.• Demand increases to 110 units.• Revenue =• Abs(Elasticity) =

Elasticity and RevenuesElasticity and Revenues

• Case II• Let us drop price to $8.• Demand increases to 150 units.• Revenue = • Abs (Elasticity)=

Elasticity and RevenuesElasticity and Revenues

When Price DECREASES, Total Revenues INCREASE for __________ products

When Price DECREASES, Total Revenues DECREASE for _________ products

Elasticity and RevenuesElasticity and RevenuesPrice Goes...Price Goes... Revenue Goes...Revenue Goes... Demand is...

Down Up Elastic

Down Down Inelastic

Up Up Inelastic

Up Down Elastic

Careful : Revenues DO not equal profitability!

Analysis of Demand, Cost, and Profit RelationshipsAnalysis of Demand, Cost, and Profit Relationships•Fixed Costs – do not vary with # units produced

•Variable Costs – varies with # units produced

•Total Costs = Fixed Costs + Variable costs

Analysis of Demand, Cost, and Profit Relationships

Fixed CostsBreakeven Point = _______________________________

Per Unit Contribution to Fixed Costs

=Fixed Costs___________________

• (Price - Variable Costs) (per unit)!

Breakeven Analysis:

Evaluation of Breakeven AnalysisEvaluation of Breakeven Analysis

• Effective tool in assessing the sales required for covering costs and achieving specified levels of profit. Sensitivity analysis.

• Easily understood

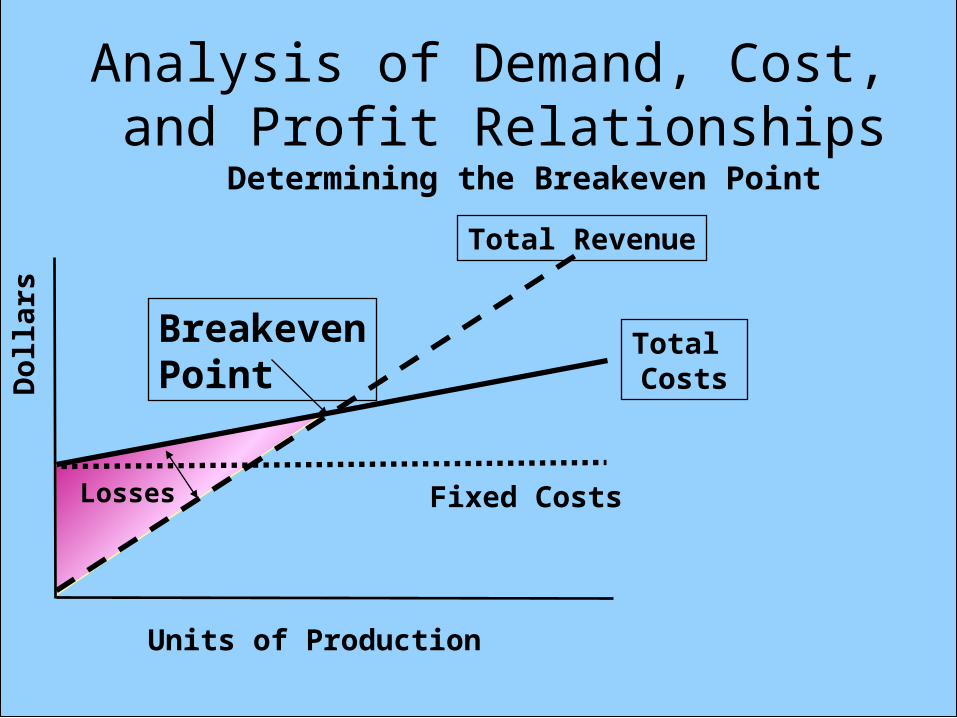

Analysis of Demand, Cost, and Profit Relationships

Determining the Breakeven Point

Quantity (Units of Production)

Fixed Costs

Total Revenue

Total Costs

BreakevenPointD

olla

rs

Analysis of Demand, Cost, and Profit Relationships

Determining the Breakeven Point

Units of Production

Fixed Costs

Total Revenue

Total Costs

BreakevenPointD

olla

rs

Losses

Analysis of Demand, Cost, and Profit Relationships

Determining the Breakeven Point

Units of Production

Fixed Costs

Total Revenue

Total Costs

BreakevenPoint

Profits

Do

llars

Breakeven AnalysisBreakeven Analysis

• Selling Price = $ 100 per unit• Variable costs = $ 50 per unit• Total Fixed Costs = $150, 000• Contribution =

Breakeven Point = _______________________________Per Unit Contribution to Fixed Costs

Fixed Costs

Breakeven (continued)Breakeven (continued)

• Breakeven point (in terms of unit sales) = _____ units

• Breakeven point (in terms of $ sales volume) = ____________ = $300,000

Factors that influence price:Product Life CycleFactors that influence price:Product Life Cycle

IntroductoryStage

GrowthStage

DeclineStage

$

High

$Stable

$Decrease

MaturityStage

$Decrease

Other factors that influence price:Other factors that influence price:

• Competition• Distribution Strategy• Promotion Strategy• Customer Power