chapter: 2: industry overview - information...

TRANSCRIPT

17

CHAPTER: 2:

INDUSTRY OVERVIEW

18

CHAPTER: 2: INDUSTRY OVERVIEW

2.1 Introduction: The mutual fund industries is lot a like the shining film stars of the finance sector.

Though it is possible the minimum segments of the finance industries, it is also

noticeable that the most sensational and glamorous industry where the rules of

the games are change everyday, and there are constant shifts and upheavals.

Now a days lots of new investments avenues innovated in the financial market.

Stupendous growth of wealth management industry has unleashed immense

opportunities and prospects for the financial intermediaries. The industry has a

tremendous growth from the past two decades. The industry gives many more

new benchmarks in the financial market.

This chapter provides the information about the history and inception of the

mutual fund; it also contains general overview related to global and Indian mutual

fund industry. In the later part, concern with the status of the different players in

the market as well as mutual fund industry contribution to the economy. Now, the

integral part of this chapter is role of mutual fund in economic development.

2.2 History of Mutual Fund:

the various types of investors. Mutual fund is considered as to be the most

attractive and adorable investment vehicle. From the same investment horizon

mutual fund investors has got the tremendous record break returns. The concept

of collecting the money from small investors and invested those money in various

types assets bundle. It is also called as mutual fund. In 18th century the initially

19

this idea was developed in Netherlands, and the current position of mutual fund

industry as a rising star of the financial market. Only in united state a trillion of

dollars invested in various mutual funds schemes among the globe. Mutual funds

are not an American invention. The first was started in the Netherlands in 1822,

and the second in Scotland in the 1880's. During 18th century the concept of risk

investment avenues.

2.2(A) Mutual Fund The Era Begins:

The different kind of thoughts was available among the historians about inception

of the concept of mutual fund. Some history writers found that the first closed

ended investment companies established during 1822 in Netherlands by King

William and it was considered as first mutual funds, while other historian

identified that Adriaan Van Ketwich; a Dutch trader or merchant who established

an investment trust in 1774 and given this idea to the king William. Ketwich also

developed the theory of diversification which would directly appeal to the

investors to invest their funds with a minimum capital. Initially Ketwich fund called

he next investment trust launched in 1849 in Switzerland, and the

same kind of Investment Avenue was established in the 1880s.

The idea of polling capital and spreading risk among the various assets with the

help of close ended investment avenues were very popular in France and Grate

Britain. In 1890 the United States also adopted this close ended investment

vehicle. The first close ended trust was formed in 1893 in U.S. named The

20

Boston Personal Property Trust. In 1907 the Alexander fund was launched in

Philadelphia, this was the most important step toward the evolution of modern

mutual funds. The Alexander funds have a various types of features like

investors can withdraw their funds on demand, semi annual issues and partial

payment options.

2.2(B) The Arrival of Modern Investment Vehicle Mutual Fund:

The concept starts with the new developments and innovations in mutual fund

segment. In 1924 modern mutual fund was arrived with the formation of the

Massachusetts investors trust in Boston. Actual fund was launched in the public

in 1928, and ultimately the outcome was mutual fund firm business called as a

MFS investment management. State investors trust act as a custodian for of

Massachusetts Investors' Trust, later on in 1924 state investors trust launched

their own funds with Richard Saltonstall, Paul Cabot and Richard Paine. In 1928

the first no load fund was jointly launched by the promoters of State investors

trust and Stevens, Saltonstall and Clark. A era has started in the history of

mutual fund in 1928, the mutual fund was consider as modern investment vehicle

when the Wellington fund was arrived in the abroad market. Wellington Fund was

a durable fund with the elements of common stock and bonds. Another

interesting fact about fund was that it opposed the traditional methods of

investment in trade and business.

The first index fund was established in 1971 by John Mcquown and William

Fouse under the banner of well Fargo bank. The concept of index fund would

nicely utilize by John Bogle and established a Vanguard Group. The concept of

21

mutual fund again renamed with the lower cost index fund. The initial concept of

no load fund was developed in 1970 but at that time it was not so popular and

attractive. This new concept of running a business had given a huge impact in

the business of mutual fund and provided extra contribution in financial market or

industry. The fund managers became a hero during 1980s to 1990s because the

secondary market was in bullish mode. The front line fund managers Michael

Price, Peter Lynch and Max Heine performed very well among the market

competitors. The maximum money and fund collected from the retail household

investors and applied in the investment trust. During this time period the recent

stories came out with scandals associated with mutual fund firms, which resulted

in attractiveness of the mutual fund investment, giant reputed names involved in

the scams and most of the investors withdraw their fund from the mutual funds.

Still today, the funds are evolving and improving in order to offer people much

wider choices and better advantages for fulfillment of their various investment

needs and financial objectives.

2.2(C) Inception of Mutual fund in India:

The mutual fund concept was introduced in India with the establishment of Unit

trust of India in 1963. in 1964 unit trust of India was launched a first scheme

called UNIT-64 which is now less popular among the investors. UTI enjoyed the

sole market leader in mutual fund until 1987, when Life insurance Corporation of

India, General Insurance Corporation of India and some public sector banks

established mutual fund organizations. From 1993 onward major foreign private

players were also allowed to set up the mutual fund in India. Today more than 32

22

mutual funds Corporation jointly manage Rs. 6713575.19 Cr. under lots of

various schemes.

The evolution has been started in 1963 when government of India started unit

trust of India. During the period of 1964 to 87 the mutual fund industry was in a

starting phase. The mutual funds directly control under the reserve bank of India

and other administrative and regulatory bodies and also functioned as per the

direction of reserve bank of India. UTI was disconnected with the RBI in 1978

and acquired the management and control by IDBI (Industrial development bank

of India). The first scheme UNIT- 64 was introduced in 1964 and UTI had

collected Rs. 6700 Cr. of Assets under management up to 1988.

After 1987 onwards entry of public sector mutual funds and non UTI organization

collectively set up mutual fund with life insurance Corporation of India, general

Insurance Corporation of India and public sector banks. In June 1987 the first

non UTI mutual fund was set up by SBI Mutual fund with the collaboration of

State bank of India followed by the other nationalized bank like Canbank mutual

fund in 1987, Punjab National bank mutual fund in August 1989, Indian Bank

Mutual Fund in November 1989, Bank of India mutual fund in June 1990, Bank of

Baroda Mutual Fund in October 1992. Life insurance corporation was also

launched their own mutual fund in June 1989, while in December 1990 general

insurance corporation had established mutual fund. Asset under management in

Indian mutual fund sector was Rs. 47004 Cr in 1993.

The journey was continued; in 1993 the doors are opened for private players in

the mutual fund sectors. A new chapter has started in the mutual fund sector;

23

most of the private players give a variety of funds among the different sectors.

During 1993 mutual fund regulations came into existence through the

government of India and all mutual fund has to be fulfilled the norms as per these

regulation except UTI. In July 1993 the first private sector mutual fund registered

called as Kothari Pioneer; now it is called as a Franklin Templeton.

The mutual fund regulation was revised in 1996 against the 1993 Mutual fund

regulation which was established by SEBI. The primary norms were similar but

some strict norms were imposed in 1993 Regulations. Form 1993 onward all the

mutual fund organization functioning under the 1993 regulations.

The number of mutual fund houses was sensibly increased, with abroad mutual

fund organizations. Foreign financial institutions were set up the new mutual

funds in India, also foreign players and India payers jointly set up the mutual

funds in Indian market. Total 33 mutual funds are working in the environment till

January 2003 and the assets value of Rs. 121805 Cr. The UTI secured the first

position with the fund value of Rs 44541Cr among the other market participant in

the Indian mutual fund industry.

nd august 1995 a

non profit organization was incorporated by SEBI and Government of India called

Association of Mutual fund in India (AMFI) for monitoring the activities of mutual

fund organizations.

AMFI is an apex and governing body for all Asset Management companies which

has been registered with securities exchange board of India. Till today all the

24

Asset management companies and mutual fund organizations are members of

the AMFI. The basic functions of AMFI are to provide the direction and assist the

Asset management companies.

The governing body AMFI has laid down the mutual fund industry to become

more professional and wealthy market with the optimal ethical standards. This

enhances the value of mutual fund industry in Indian financial system. It always

concern with the promoting and protecting the interest of the unit holders as well

as mutual funds.

The next step shows the major reform in the Indian mutual fund industry and it

was started from 2003 still its going on. In February 2003, the unit trust of India

act-1963 was restructured and divided into two individual separate entities. The

January 2003, US-64 and various other schemes and the second one is Unit

Trust of India which has not come under the purview of Mutual fund regulation.

The UTI is directly functioning under the Government of India and other

governing bodies. The central government liberalized the policies in 1992-93 and

the many of the private and foreign players now entered in the Indian financial

market, the effect of this decision creates earthquake in the Indian primary and

secondary market. It shows tremendous growth in the India mutual fund

segment.

UTI has collaborate with the nationalized banks like state bank of India, Punjab

national bank, bank of baroda and Life insurance of India and through the various

mutual fund products in the market. All of the mutual funds functioned under the

25

guidelines of mutual fund regulation 1996 and registered with securities

exchange board of India. at the end of March 2000, UTI has collectively acquired

Rs. 76000Cr asset under management from various mutual fund. Many of the

period of 2000 the Indian mutual fund industry was in the consolidation and

growth phase.

(Figure: 2.1 Growth in the asset under management)

(Source: http://www.amfiindia.com/showhtml.aspx?page=mfindustry)

The above figure (2.1) indicates the road map of asset management companies

from March 1965 to March 2011. Imagine the percentage change in the asset

under management, its unbelievable growth during the period of 2003 and its

steady increase up to the march 2008, heavy recession was going on in the year

26

of 2008-

growth for AMC, then some strict rules & regulation are implemented by SEBI in

the year 2010-2011, it shows a small decreased in the growth of AMC.

2.3 The organization of the mutual funds:

Institutions and individuals invest their money in mutual fund schemes by

purchasing units and shares issued by the mutual fund schemes, through the

sales of units or shares mutual fund acquires the cash and those cash fund

directly invest in stock market with bundle of securities. Bundle securities

comprise the stocks, bonds and other liquid investment. Mutual fund having

several advantages such as diversification, money market fund accounts, extra

privileges, asset allocation programme and money market fund accounts.

A mutual fund organization is formed under the state law either as a business or

corporation; sometimes is called as a statutory trust. Mutual fund organizations

have their own directors and officers, if the organization formed as a corporation

or business and in case of organization formed as business trust then trustees of

the individual trust enjoy the right of directors and officers like Google and Exxon.

In this method mutual funds are likely to be considered as a other operating

company. The managing board of the funds plays a crucial role in the operation

of funds.

As a traditional vie

organization has no employees in traditional view. The MF organization ware

27

relies on the service providers and third parties which either considered as

individual contractor or affiliated organization to perform the business activities.

The below diagram (chart: 2.2 Organization chart of mutual fund) depict the major

service providers generally relied upon by the any specific fund.

As per prescribe guidelines in mutual fund regulation1996, the fund have their

own written compliance program at the time of establishment. As individual

person appointed and designated as a Chief compliance officer. The compliance

program includes details about the standard procedures and internal control

manual which is related to minimum standard mention in the rules and

regulations.

(Figure: 2.2 Organization chart of mutual funds)

(Source: Investment Company Fact Book 2011, 51st Edition)

28

(I) Shareholders

Mutual fund unit holders have specific voting right just like share holders of any

corporate or companies. These rights are similar to the company act-1956. The

unit holders have a right to appoint or remove the directors for any specific

mutual fund organization, Call the directors for meeting when its needed,

Conduct a meeting for a specific reason. The extra right like material changes in

terms of agreement and contract with its investment or merchant adviser. The

general identical view about the fund management fees and fundamental polices

on the same subject matter.

(II) Sponsors

To establishing a mutual fund is a quite complicated and difficult process

performed by the fund sponsors, which is generally called as a investment or

merchant advisor. The fund sponsors have a various kind of roles and

responsibility. Generally the sponsors bring together all the third parties and

concern parties at the time of launching the mutual fund. The primary duty of

sponsors is right to describe the operations and management of the funds among

the investors. The sponsor gives the direction to affiliated directors and officers to

look after the fund operations and also appoint the unaffiliated individual act as a

independent director.

Some of the most important stages in the process of starting a mutual fund with

respect to organizing the fund under state rules and regulations as either a

corporation or business trust, as investment company under the Investment

29

company act 1940 and also registering the fund with the SEC (security and

exchange commission). The investment companies have to registering the fund

shares/units for sale and purchase to the general public and investors under the

Securities Act of 1933, Unless otherwise it exempt from doing same. The

investment company must also make documentation and pay prescribed fees to

general public or investors. As per investment Company Act in United States

requires to deposit the fund of $100,000 for each new fund before distributing its

shares and units among the shareholders or unit holders. This fund is generally

contributed by the adviser or sponsor in the form of an initial investment.

(III) Advisers

Investment advisers have a primary responsibility for operating and directing the

funds overall investment and managing its internal as well as external business

activities. Investment advisers can appoint their own staff for smooth operations.

It includes professionals who carried out the investment activities, construction of

portfolio and diversification of portfolio on behalf of fund holders or unit holders.

Professionals have also assigned the duty by investment advisors that invest the

money according to the objectives and policy schemes. The additional task given

to the investment advisor; to become act as administrator and also providing

different types of back office services, it has also observed from past track record

the deposit the initial money and create the fund.

30

staff are subject to followed some legal restriction and standards. It includes

restriction on the various transactions that may affect the shareholders interest.

In case of investment advisors have their own written compliance program and

manuals, which are monitoring by the chief compliance officer and design the

comprehensive norms and procedures for internal control subject to all

regulations and applicable laws.

(IV) Administrators

Most of the back office operations and functions perform by the administrator of

the specific fund. The role of the administrator includes clerical work, book

keeping, fund management accounts & audits, tax aspects, data processing,

preparation of reports for tax authority, shareholder and other concern parties.

The substitute responsibility of fund administrator is to help maintain and assist in

internal control and compliance procedures, subject to oversight by the fund

management board.

(V) Principal Underwriters

Investors purchase and redeem fund unit or share either directly or indirectly

through the principle underwriter. The principle underwriter is also called as fund

distributor. All of the principle underwriters are registered as brokers or dealers

under Securities Exchange Act -1934. The primary roles and duties of the

underwriter to strictly follow the rules prescribe under this act for sell and offer the

fund management that first purchase the shares from the fund management then

31

resell these securities among the general investors. Prior permission has been

taken from the independent directors and other concern parties with respect to

the agreement with principle under writers.

(VI) Transfer Agents

Share holders, unit holders and mutual fund organization depend on the services

of the transfer agent. For the purpose of maintain the records, client accounts,

calculation of tax, capital gain, dividend distribution, distribution of the relevant

statements to share holders and other necessary documents an investment

banker appoint the person called transfer agents. On behalf the mutual fund

organization transfer agents perform their day to day activities. Transfer agents

are the communication bridge between share holders/ unit holders and mutual

fund organization.

(VII) Auditors

Auditors. and responsibility is described with the

detail description in the offer/prospects documents, after understanding all the

terms & conditions the auditors are issuing the certificate relevant to the

disclosers.

2.4 Significance of Mutual Fund in the Investment Decision:

Mutual fund is the most appropriate and popular investment vehicle for the

individual investors, those are belongs from small size and medium size income

groups. Mutual fund gives an opportunity to invest the money in well diversified

and professionally managed basket of securities at a relatively low cost. The

32

primary objective of an investment proposal would fit into one or a combination of

two broad categories, income and capital gains. These two objectives can be

achieved through investment in mutual fund. Mutual funds have played a most

significant role as financial intermediaries in the capita

concern with the growth of the corporate sector. Mutual funds are attractive

investment avenues among the investors because its have a various advantage

over other investment avenues. Particularly for the investors who has a limited

resources and intends low risks.

The following points show the advantages of mutual fund in the investment

decision:

Professional Expertise:

Investment needs expertise. It requires a continuous study and research of the

fundamental dynamics of the primary and secondary market. Any investors have

a surplus funds or capital to be invested in various securities and those

investments would be able to generate a handsome return then its called person

having a sound investment skills towards the choice of investment vehicles

Mutual fund organizations appoint the qualified fund managers for better

performance of any mutual fund schemes, on the other side small inventors have

a lack of the sound skills so they are depend on the expertise of fund managers

and invest their money in specific funds.

The essential qualification to become a fund managers are globally authorized

chartered finance analysis and MBA. The person has a sound analytical skill and

33

minimum experience as research analysts can appoint as a fund manager. The

fund manager can also assist in the fund operation management process.

Diversification:

A sound investment policy based on the principle of diversification, which is the

idea of not serving all the foods in single plate by investing in many assets and

companies stock the mutual fund, can protect themselves from the unexpected

drop in the value of some shares. The small investors cannot do broad

diversification on his own because of various reasons; when investors have fund

constraints. Mutual fund is one of the largest associations of small investors.

Maximum number of small investors can largely participate in the various

company stocks under the one banner.

Safety of Investment:

Investors in mutual funds receive adequate protection from regulatory agencies.

Mutual funds submit several reports to these agencies and also are required to

publish details of their operations for the public information.

Liquidity:

Mutual funds are highly liquid investments, unless any specific schemes have

identical lock in time period. Your funds are ready to available whenever you

require. Generally it would take the settlement time duration for getting cash from

the mutual fund investment. Mutual funds are directly or indirectly connected with

the stock market and banking system. Most of the mutual funds directly send

34

Low Operating Cost:

The mutual fund investors are divided in to the large number of units with a small

value of investment. The total investment of any single mutual fund scheme

divided among the million of investors, that means total operating cost of the fund

is also divided in to million of investors. Mutual fund organizations are also able

to reducing the operating cost with the help of economies of scales th

they offer very low cost products for investors.

Low level of Risk:

Mutual fund investment is the safest investment in the current environment.

When fund manager construct a portfolio from the pool of fund they always

concern with risk factors. The larger number of securities in the portfolio the level

of risk factor should be diversified among the maximum number of securities. It

could be generate a maximum return with a lower level of risk.

Switching

All the mutual fund schemes are generally treaded in the listed stock exchange,

which means investors are having a good opportunity to shift form one fund to

another fund to buy or sell the mutual fund units in the open market.

Tax saving

Many mutual funds provide tax shelter. In India equity linked mutual fund

schemes allowed tax rebate under section 88 and tax exemption of mutual fund

dividend under section 80(L). A fixed income and salary holders investors are

easily availed the benefits of tax exemption and also generate the high return

from the mutual fund investment.

35

Well regulated

In India mutual funds are monitored and regulated by the securities and

exchange board of India (SEBI), which tries to save the interests of the individual

investors. As per guidelines of SEBI mutual fund provide the regular information

to investors about their fund value and investments. Subsidiary disclosers

requirement describe by AMFI for investors perspective like specific investment,

assets class, unit value and present status.

2.5 Mutual funds in developed countries:

The developed countries of UK, Japan & USA presented three different

classification of the working of the mutual fund industry with the same operational

ideology to provide the maximum possible return with risk.

2.5(A) Mutual funds in United Kingdom:

There are two unique organizations in the UK, investment trust and unit trust

which has offer the diversified portfolio investment services to individual investors

in UK. Unit trusts are open ended fund and collect the unlimited funds from the

individual investors, issue units and invest the funds in capital market

instruments. It operates under the auspices of the Finance Service Act-1986 and

the securities and investment board overseas operation.

Unit trust in UK can be categorized according to the investment objective-

General Trust which provide capital growth and reasonable income

Capital trust which provides maximum capital growth

Income trust which provides high income

36

In UK the most flourishing unit trust are among the general category. By the end

of 1995 the total assets of 1132, unit trust stood at 1, 09,996 million GBP under

19.80 billion GBP, which accounted for 18% of the total industry.

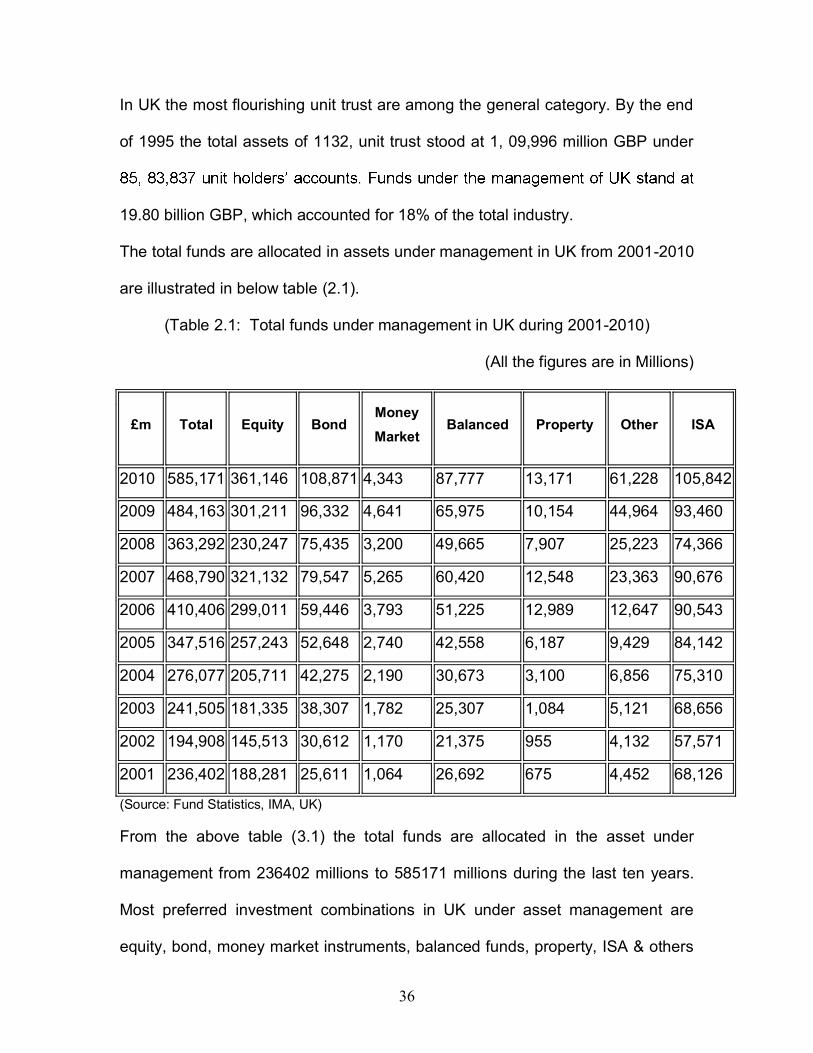

The total funds are allocated in assets under management in UK from 2001-2010

are illustrated in below table (2.1).

(Table 2.1: Total funds under management in UK during 2001-2010)

(All the figures are in Millions)

£m Total Equity Bond Money Market

Balanced Property Other ISA

2010 585,171 361,146 108,871 4,343 87,777 13,171 61,228 105,842

2009 484,163 301,211 96,332 4,641 65,975 10,154 44,964 93,460

2008 363,292 230,247 75,435 3,200 49,665 7,907 25,223 74,366

2007 468,790 321,132 79,547 5,265 60,420 12,548 23,363 90,676

2006 410,406 299,011 59,446 3,793 51,225 12,989 12,647 90,543

2005 347,516 257,243 52,648 2,740 42,558 6,187 9,429 84,142

2004 276,077 205,711 42,275 2,190 30,673 3,100 6,856 75,310

2003 241,505 181,335 38,307 1,782 25,307 1,084 5,121 68,656

2002 194,908 145,513 30,612 1,170 21,375 955 4,132 57,571

2001 236,402 188,281 25,611 1,064 26,692 675 4,452 68,126

(Source: Fund Statistics, IMA, UK)

From the above table (3.1) the total funds are allocated in the asset under

management from 236402 millions to 585171 millions during the last ten years.

Most preferred investment combinations in UK under asset management are

equity, bond, money market instruments, balanced funds, property, ISA & others

37

etc, the table also indicates 60% growth rate in UK under asset management

from the last decade.

2.5(B) Mutual funds in Japan:

Mutual funds in the Japan are known as Investment trust, but they differ from

investment trust of UK. Investment trust in Japan was set up under the securities

investment Law-1951. In Japan investment trusts are bifurcated into two

categories knows as a stock investment trust & bond investment trust. Mainly two

kinds are investment trusts are working in economy of Japan first one is unit type

& second is open type. In case of unit type investment trust is no continuous

capital flow while in case of open type capital flow is continuous.

In Japan some of the mutual funds are acclaimed as international best

performers among the other world wide mutual funds in 2010. It was also

observed that the same mutual funds were quite strong in recession period.

indicates that Japan would be top performer in next future, among the developed

economies.

In Japan on an average 5.9% fund value fall in 2010, it was better then the

stock funds had been declined by 13.3% in 2010. in second quarter world stock

exchanges declined by 11% and also European fund were declined by 14%,

while Japan stock fund after leading in first quarter it was slump in second

quarter by 6.8 % in 2010.

38

In the beginning of 2010 the Japanese economy performed very well then

optimistic estimation was made in 2009 by the research experts. The general

perc

negative return.

The value of the mutual funds in Japan falls 4.6% to 803 billion in 2010 because

of the currency deprecation (yen) and the security market stock market collapse.

In Asia pacific mutual fund market acquired second position after

Australia. Due to size and market participant worlds other stock market brokers

compare to the worlds 16th largest economy Netherlands

fund market players are more actively participate in the world economy.

2.5(C) Mutual funds in USA:

The USA is the pacemaker in the world wide mutual fund industry. The first

investors trust was set up in 1924. The growth of

the mutual funds was retarded due to the stock market crash of 1929 & the

outbreak of the Second World War. The period of boom for the industry was

lion.

A mutual fund in USA is describes as a management company, which may be

diversified or non diversified. A diversified management company has at least

75% of its assets in cash & cash items, government securities and securities of

other investment companies. A non diversified company is not subject to the

above limitations. Open ended management companies are called mutual funds.

In the United states a mutual fund is registered with the securities and exchange

39

commissions (SEC) is equivalent to SEBI and is overseen by a board of directors

or board of trustee. The basic purpose of to establish regulatory bodies are

management companies.

The following table (3.2) contains the total net assets allocated under assets

management in USA during 2001 to 2010.

(Table 2.2: Total net Assets under management in USA for the period of

2001-2010)

(All figures are in $ billions)

Year Total Equity funds

Hybrid funds

Bond funds

Money market funds

2001 6,974.91 3,419.61 344.87 925.12 2,285.31

2002 6,383.48 2,664.01 323.95 1,130.45 2,265.08

2003 7,402.42 3,686.30 428.33 1,247.77 2,040.02

2004 8,095.08 4,386.67 516.60 1,290.48 1,901.34

2005 8,891.11 4,942.65 564.35 1,357.28 2,026.82

2006 10,397.94 5,914.10 650.31 1,495.07 2,338.45

2007 12,002.28 6,518.76 716.73 1,681.03 3,085.76

2008 9,603.60 3,705.55 498.28 1,567.54 3,832.24

2009 11,120.20 4,957.04 639.15 2,208.11 3,315.89

2010 11,820.68 5,667.40 741.07 2,608.29 2,803.92

(Source: 2011 investment company fact book)

The total net assets are allocated in the various funds like equity funds, hybrid

funds, bond funds, money market instrument funds etc, in USA. From the above

40

statistics increased in the net assets are approximately 40% from 2001 to 2010.

The table also depicts the most preferred investment funds are equity and bond

funds during this period.

2.6 Role of the mutual fund industry in the economic development:

The financial system of a country frequently influences its economy. The

relationship between economic development and economic financial structure of

the country is depicted in the present institutional arrangement, intermediation

process and delivery system. A certain level of financial development denotes

more mature way of mobilization of the funds, a shift from self financing and then

to indirect financing.

Mutual funds are active financial institutions, which play crucial role in an

economic by mobilizing saving and investing them in the capital market. Large

numbers of market participant are belongs to the mutual fund industry. The

activity of mutual funds have both short term and long term impact on the

financial market and house hold saving, and economy of any country. in the

national economy mutual funds provide the help in process of financial

intermediation and deepening. They mobilize funds in the saving market and act

as a complementary to banking. Stock market movements are also significantly

associated with mutual fund operators.

Mutual funds are financial intermediaries in the investment business. They collect

t increases

41

liquidity in the money market. The scope of efficiency of mutual funds are

influenced by over all economic fundamentals and principles; the interconnection

between the real sector and financial sector, the structure of development always

concern with capital market movement, market participant, institutional financial

arrangement and general government policy.

The Indian financial institutional have played a dominant role in the assets

preparation and contributed significantly in macroeconomic growth of our

country. In this process, Indian mutual fund sector have emerged as strong

financial intermediaries and are playing a very vital role in brining stability and

constancy to the economy and financial system.

Mutual funds are also called as institutional device for the economic

development. The growth of the economy is directly related to the specific sector

of the financial market, generally financial intermediaries are played a vital role

for the economic development. Mutual funds are potentially sound investment

2.7 World market of the mutual fund industry:

2.7(A) Global view of Mutual funds:

From 1990 onward the tremendous growth in mutual fund sector in the whole

world, during the1990

gives steady return and safety. This was happened particularly in the US where

the total net assets value of mutual fund was grew from $ 1.6 trillion in 1992 to $

42

5.5 trillion in 1998. During this time period compounded and equivalent annual

average growth rate was 22.4%. The same growth rate remains constants and

increased till 2005 in the word. It was also noticeable that large number of

investors was willingly to invest their money in various foreign mutual funds

schemes.

The member countries of the EU (European Union) has provided the significant

evidence of the growth of total mutual fund assets value from $ 1 trillion in 1992

to 2.6 trillion in 1998 with annual average growth rate of 17.7%. Among the

member countries of EU, Greece showed record break growth rate of 78%,

significantly followed by Italy at 48% and the rest of the member countries of

European Union countries shows average growth of 35%. Some developing

countries of EU like Morocco, achieved a higher growth rate, but it has started

from the small compositions.

over this period and also shows magnificent growth in the house hold ownership

of the mutual funds. Research estimates reported in US by Investment Company

Institute (ICI-2002) depict that the ratio of US house holds owning mutual funds

increased from 6% in 1990 to 27% in1992 and 44% in 1998.

It is also significant to note that this growth in the financial market and mutual

fund sector run by various economic factors such as high market capitalization in

market, uses of internet connected system and innovative techniques. During the

43

period of 2000, in US market capitalization of publicly treaded stocks through the

internet was predicted to be $ 1.3 trillions as compare to normal stocks valuation

of $ 843 billion in June 2000. From 1991 to 1999 the growth rate of market

capitalization was increased by more then 300% in US, concern with the initial

benchmark of 68% in 1991. It was also noticeable that from 1991 to 1999 the

GDP growth rate increased by 180% in US economy. the general trend shown

from the historical data that various factors contributed in the growth of mutual

fund sector across the globe, awareness level of investors towards the equity

market and their performance, availability of attractive mutual fund products

among the investors.

The European fund and asset management association (EFAMA) released and

published the international statistics about the mutual funds and asset

management industry. Highlights about the facts and figures had given below for

2011.

Investment fund assets worldwide remained steady during the second quarter to

stand at EURO 19.49 trillion at end June 2011. In terms of US dollar currency,

global investment fund assets value increased 1.7 percent during the quarter to

US $ 28.17 trillion. Total net inflows into investment funds increased during the

quarter to EURO 147 billion, compared to total net fund inflows of EURO 102

billion in the last quarter. This increase came on the back of increased net inflows

into long-term funds, coupled with reduced net withdrawals from money market

funds. Net inflows to long-term funds (Except money market mutual funds)

44

increased during the quarter to EURO 206 billion, up from EUR 176 billion of net

inflows in the first quarter. Bond funds enjoyed a steep increase in net inflows

during the quarter to register EURO 70 billion of net fund inflows, compared to

EURO 42 billion in the last quarter. Equity funds continued to record net inflows

amounting to EURO 16 billion, although at a reduced rate compared to the last

quarter when net inflows amounted to EURO 45 billion. Balanced/mixed funds

also enjoyed increased net sales during the quarter to register inflows of EURO

40 billion.Net inflows into long-term funds in Europe increased to EURO 48 billion

during the quarter, whereas net inflows in the United States remained steady at

EURO 98 billion. The information presented in the below graph (2.3) was

complied by investment company Institute (US) and EFAMA on behalf of an

organization of national investment fund associations and the international funds

association,. The collection of the statistics up to for the year of 2011 contains

from the 45 countries.

(Chart: 2.3: Worldwide investment fund Assets)

(Source: International statistics release, 2011)

45

From the above graph (2.3) it has clearly indicate that from 2008 to 2011 the

global investment fund assets significantly increased by 16.70%, since from first

quarter of 2009 to second quarter of 2011 the investment fund assets shows

continuous increasing trend.

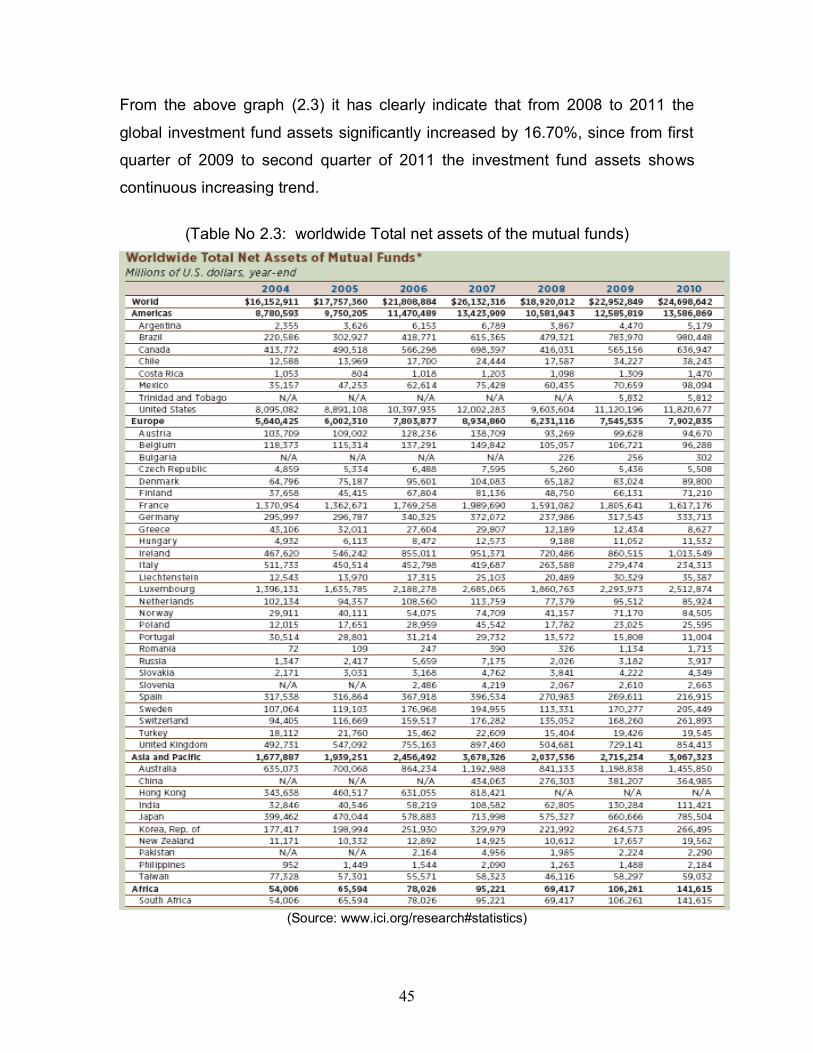

(Table No 2.3: worldwide Total net assets of the mutual funds)

(Source: www.ici.org/research#statistics)

46

According to the investment company institute (ICI) world wide total net assets of

the mutual funds from the period of 2004 to 2010, during this time period total net

assets has increased in each and every country. The above table (2.3) shows the

exact figures of total net assets of mutual funds.

As compared to the European & Asian pacific countries growth of the total net

assets has increased in double figures in America and their associated region.

Now from the above statistics it clearly indicates that potential net assets have

increased in the low population region form the respective countries. In the year

2010 maximum investment in the mutual funds assets has coming from brazil,

united states, Ireland, Luxembourg, Germany, Australia, united kingdom, china

etc. growth of the mutual fund industry has continuous increased from 2004

onwards. Approximately every year 10% average growth in total net assets

worldwide.

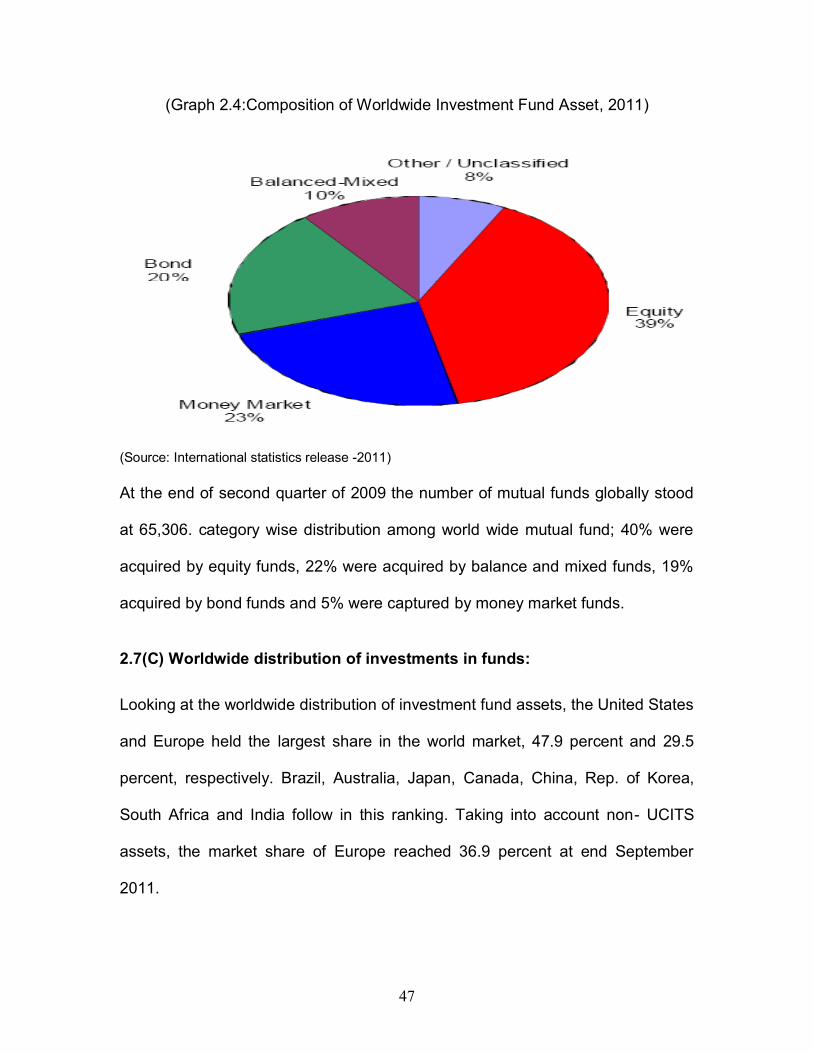

2.7(B) Worldwide composition of investments in funds:

Hear the below graph (2.4) represents the world wide total compositions of

various investment funds. Fourth quarter ending of 2009, 39% of global

investment fund assets were only held in equity funds. The fund asset acquired

20% of bond funds and the fund asset captured 10% of balanced/mixed fund. At

last Money market fund assets acquired 23% of the worldwide total. From this

statistics its clearly indicates that the first preference has given by the equity fund

& the second preference has given money market funds by investors.

47

(Graph 2.4:Composition of Worldwide Investment Fund Asset, 2011)

(Source: International statistics release -2011)

At the end of second quarter of 2009 the number of mutual funds globally stood

at 65,306. category wise distribution among world wide mutual fund; 40% were

acquired by equity funds, 22% were acquired by balance and mixed funds, 19%

acquired by bond funds and 5% were captured by money market funds.

2.7(C) Worldwide distribution of investments in funds:

Looking at the worldwide distribution of investment fund assets, the United States

and Europe held the largest share in the world market, 47.9 percent and 29.5

percent, respectively. Brazil, Australia, Japan, Canada, China, Rep. of Korea,

South Africa and India follow in this ranking. Taking into account non- UCITS

assets, the market share of Europe reached 36.9 percent at end September

2011.

48

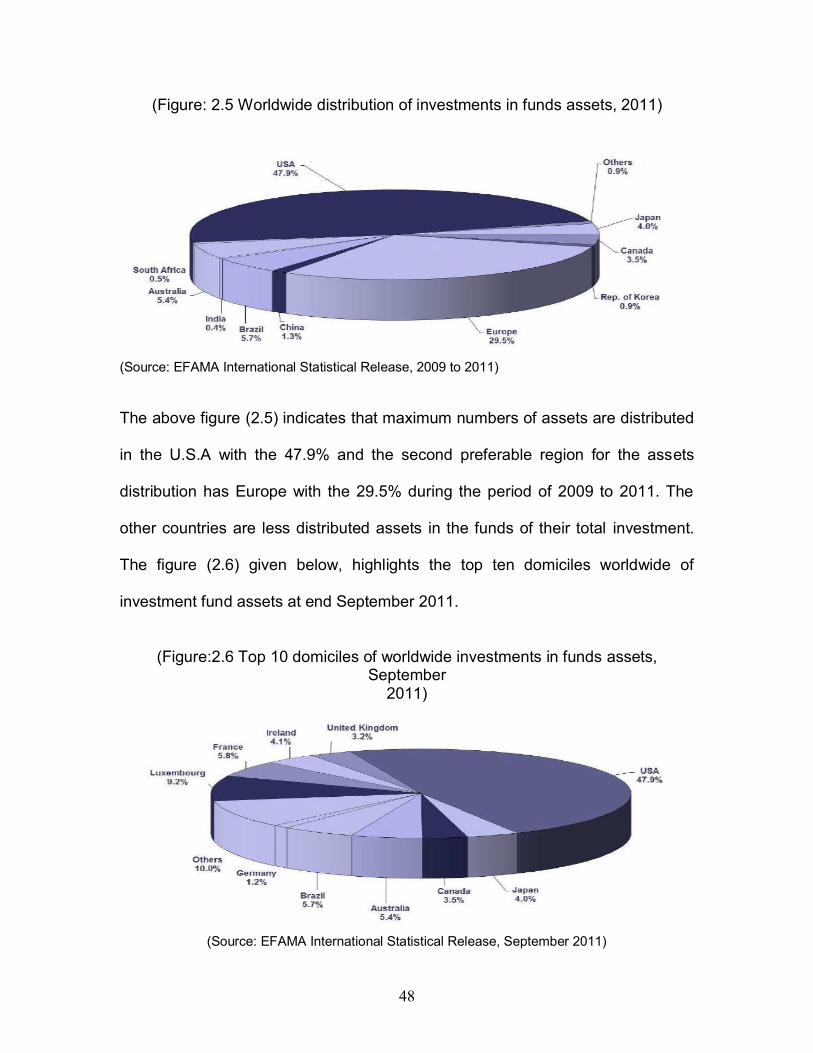

(Figure: 2.5 Worldwide distribution of investments in funds assets, 2011)

(Source: EFAMA International Statistical Release, 2009 to 2011)

The above figure (2.5) indicates that maximum numbers of assets are distributed

in the U.S.A with the 47.9% and the second preferable region for the assets

distribution has Europe with the 29.5% during the period of 2009 to 2011. The

other countries are less distributed assets in the funds of their total investment.

The figure (2.6) given below, highlights the top ten domiciles worldwide of

investment fund assets at end September 2011.

(Figure:2.6 Top 10 domiciles of worldwide investments in funds assets, September

2011)

(Source: EFAMA International Statistical Release, September 2011)

49

The first domicile is USA acquiring with the maximum 47.9% of investment in the

funds followed by the other countries with the remaining percentage but the

highest percentage has only acquired by USA that means the higher awareness

level in the USA among the market participants.

2.7(D) Worldwide fund sponsors:

In 2010, there were 669 financial firms from around the world that competed in

the U.S. market to provide investment management services to fund investors.

Historically, low barriers to entry have attracted a large number of investment

company sponsors to the fund marketplace in the United States and other

countries. These low barriers to entry led to a rapid increase in the number of

fund sponsors in the 1980s and 1990s. However, competitions among these

sponsors and pressure from other financial products have reversed this trend

over the past decade. From year-end 2000 to year-end 2010, 502 fund sponsors

left the fund business. In the same time, 379 new firms entered (Chart 2.7). The

overall effect has been a net reduction of 16 percent in the number of industry

firms serving investors. The decrease in the number of advisers has occurred

with larger fund sponsors acquiring some smaller fund families and with some

fund advisers liquidating funds and leaving the fund business. In addition, several

other large sponsors of funds sold their fund advisory businesses. The portion of

fund companies that have been able to retain assets in addition to attracting new

investments has been generally lower in this decade than during the 1990s. Two

bear markets leading to outflows from stock funds and other competitive

50

pressures affected the profitability of fund sponsors and contributed to the

decline in their number over the past 10 years.

(Chart 2.7: Number of Fund Sponsors during the period of 2000 to 2010)

(Source: A Review of Trends and Activity in the Investment Company Industry, Fact Book 2011)

The decline in the number of fund sponsors has been concentrated primarily

among those advising mutual funds, and their exit from the industry has caused

the growth in the number of mutual funds to slow in recent years and to decline

over the past two years. Competitive dynamics also affect the number of funds

offered in any given year by the fund advisers that remain. In particular, fund

sponsors create new funds to meet investor demand, and they merge or liquidate

funds that do not attract sufficient investor interest. The pace of newly opened

funds continued to slow in 2010 to its lowest level since 1996. Nevertheless, the

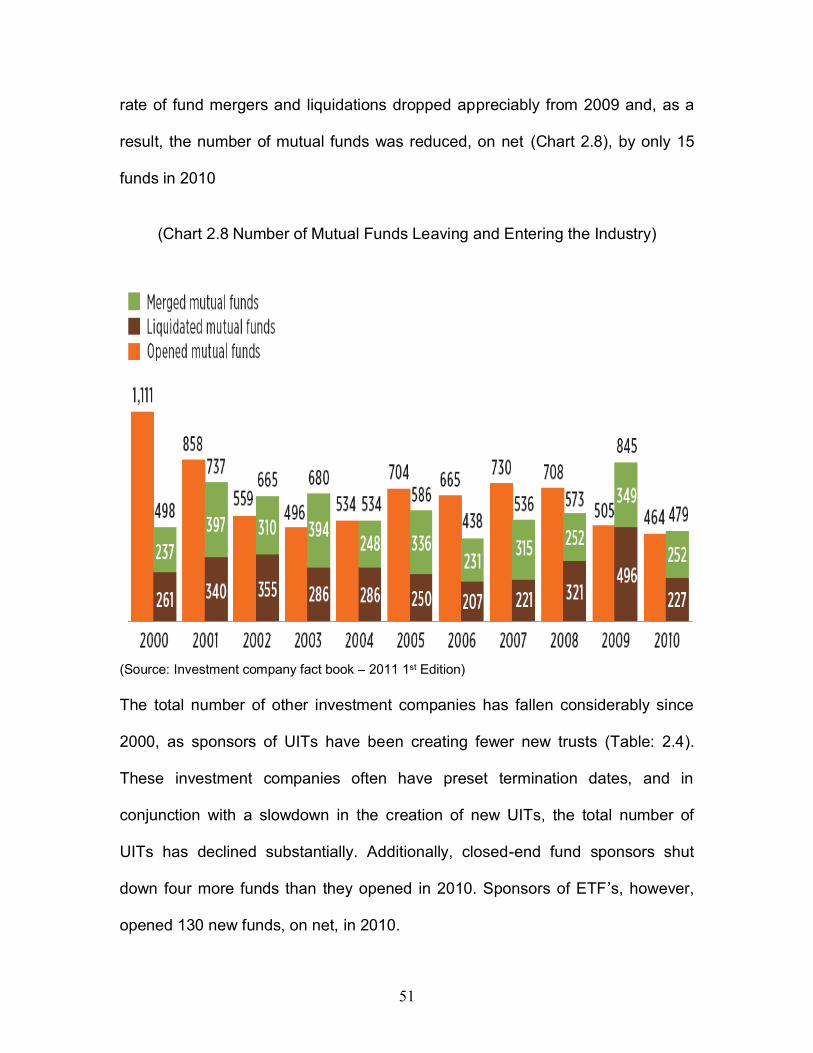

51

rate of fund mergers and liquidations dropped appreciably from 2009 and, as a

result, the number of mutual funds was reduced, on net (Chart 2.8), by only 15

funds in 2010

(Chart 2.8 Number of Mutual Funds Leaving and Entering the Industry)

(Source: Investment company fact book 2011 1st Edition)

The total number of other investment companies has fallen considerably since

2000, as sponsors of UITs have been creating fewer new trusts (Table: 2.4).

These investment companies often have preset termination dates, and in

conjunction with a slowdown in the creation of new UITs, the total number of

UITs has declined substantially. Additionally, closed-end fund sponsors shut

down four more funds than they opened in 2010. Sponsors of ETF s, however,

opened 130 new funds, on net, in 2010.

52

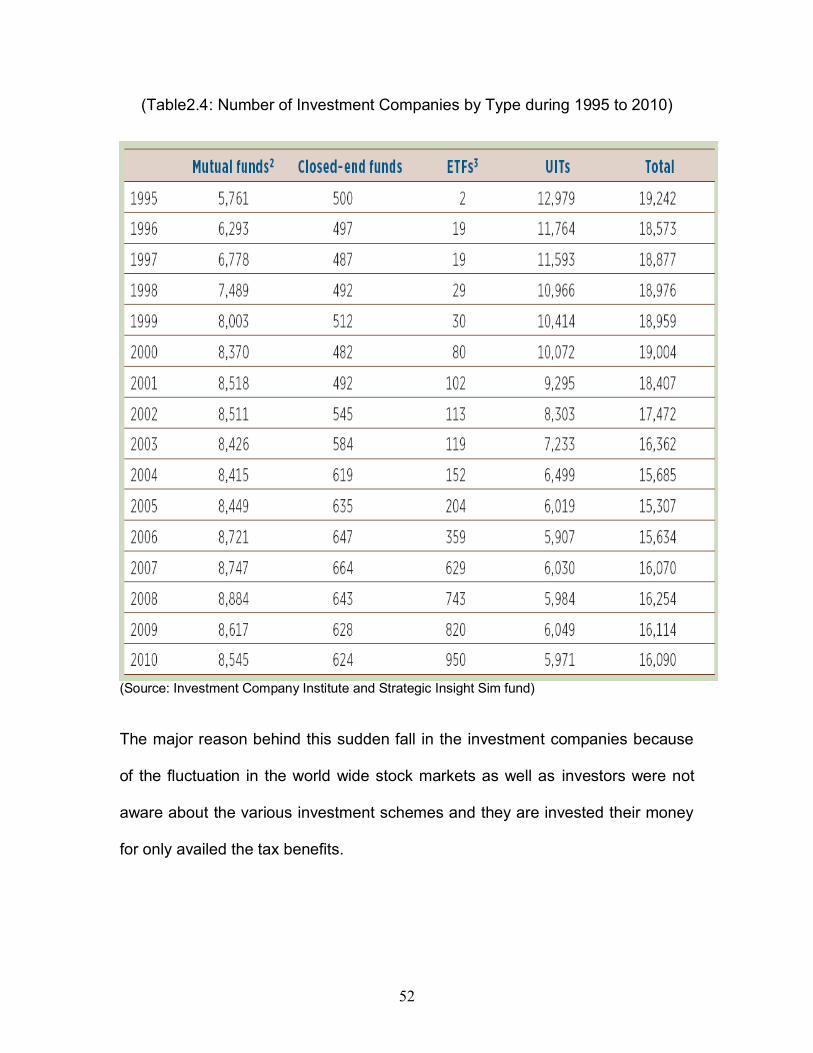

(Table2.4: Number of Investment Companies by Type during 1995 to 2010)

(Source: Investment Company Institute and Strategic Insight Sim fund)

The major reason behind this sudden fall in the investment companies because

of the fluctuation in the world wide stock markets as well as investors were not

aware about the various investment schemes and they are invested their money

for only availed the tax benefits.

53

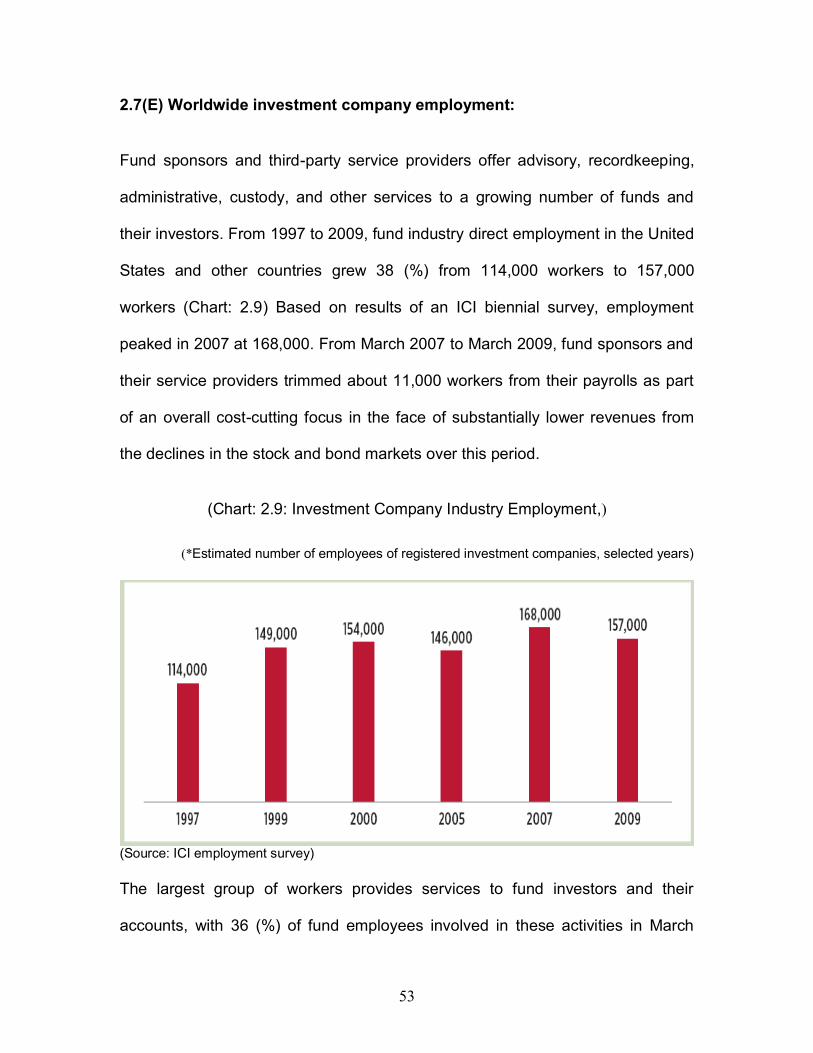

2.7(E) Worldwide investment company employment:

Fund sponsors and third-party service providers offer advisory, recordkeeping,

administrative, custody, and other services to a growing number of funds and

their investors. From 1997 to 2009, fund industry direct employment in the United

States and other countries grew 38 (%) from 114,000 workers to 157,000

workers (Chart: 2.9) Based on results of an ICI biennial survey, employment

peaked in 2007 at 168,000. From March 2007 to March 2009, fund sponsors and

their service providers trimmed about 11,000 workers from their payrolls as part

of an overall cost-cutting focus in the face of substantially lower revenues from

the declines in the stock and bond markets over this period.

(Chart: 2.9: Investment Company Industry Employment,)

(*Estimated number of employees of registered investment companies, selected years)

(Source: ICI employment survey)

The largest group of workers provides services to fund investors and their

accounts, with 36 (%) of fund employees involved in these activities in March

54

2009 (Chart: 2.10). Shareholder account servicing encompasses a wide range of

activities to help investors monitor and update their accounts. These employees

work in call centers and help shareholders and their financial advisers with

questions about investor accounts. They also process applications for account

openings and closings. Other services include retirement plan transaction

processing, retirement plan participant education, participant enrollment, and

plan compliance.

At the same time, 28 (%)

investment adviser or a third-party service provider in support of portfolio

management functions such as investment research, trading and security

settlement, information systems and technology, and other corporate

management functions.

Jobs related to fund administration, including financial and portfolio accounting

and regulatory compliance duties, accounted for 11 (%) of industry employment.

Personnel involved with distribution services (e.g., marketing, product

development and design, investor communications) represented 16 percent of

the workforce. Sales-force employees including registered representatives and

sales support staff where at least 50 (%)

from fund sales and fund supermarket representatives accounted for 9 percent

of fund industry jobs.

55

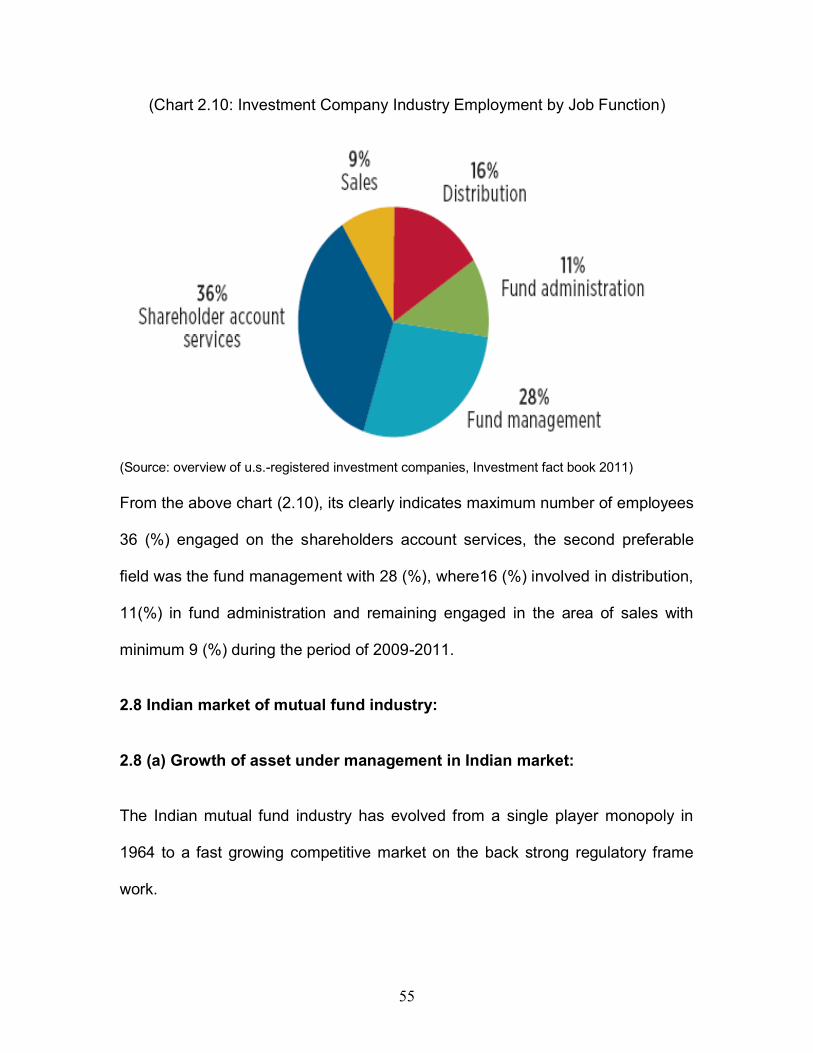

(Chart 2.10: Investment Company Industry Employment by Job Function)

(Source: overview of u.s.-registered investment companies, Investment fact book 2011)

From the above chart (2.10), its clearly indicates maximum number of employees

36 (%) engaged on the shareholders account services, the second preferable

field was the fund management with 28 (%), where16 (%) involved in distribution,

11(%) in fund administration and remaining engaged in the area of sales with

minimum 9 (%) during the period of 2009-2011.

2.8 Indian market of mutual fund industry:

2.8 (a) Growth of asset under management in Indian market:

The Indian mutual fund industry has evolved from a single player monopoly in

1964 to a fast growing competitive market on the back strong regulatory frame

work.

56

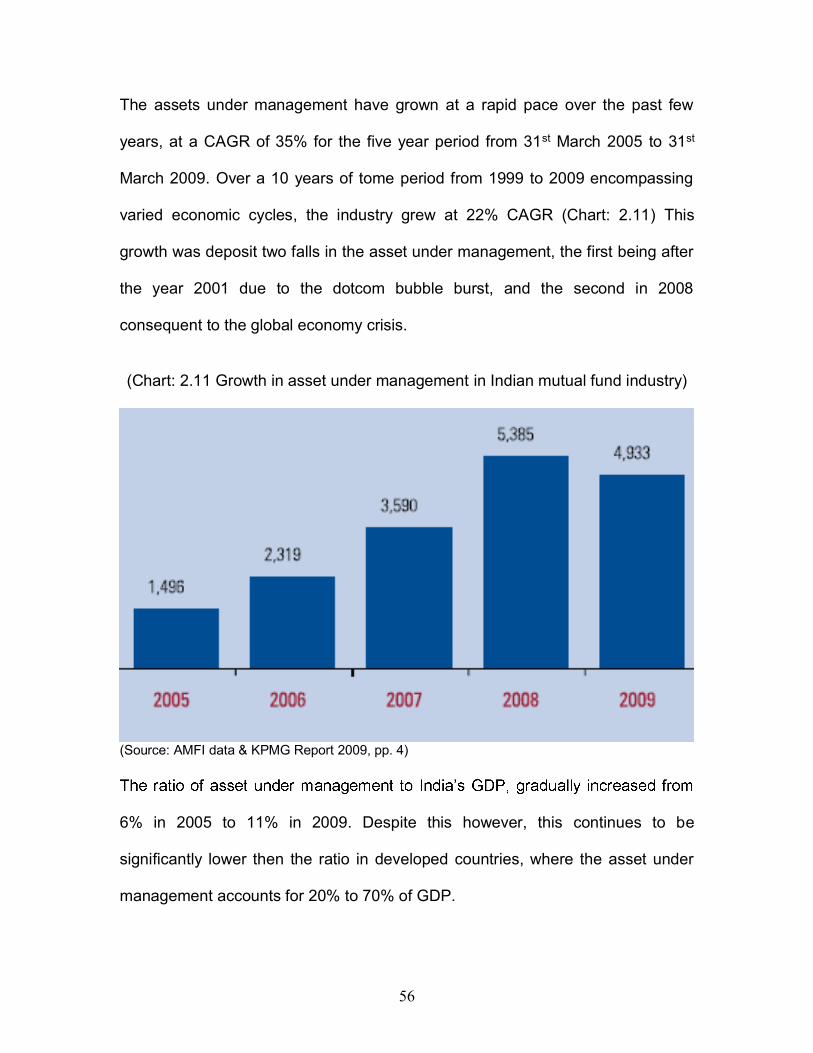

The assets under management have grown at a rapid pace over the past few

years, at a CAGR of 35% for the five year period from 31st March 2005 to 31st

March 2009. Over a 10 years of tome period from 1999 to 2009 encompassing

varied economic cycles, the industry grew at 22% CAGR (Chart: 2.11) This

growth was deposit two falls in the asset under management, the first being after

the year 2001 due to the dotcom bubble burst, and the second in 2008

consequent to the global economy crisis.

(Chart: 2.11 Growth in asset under management in Indian mutual fund industry)

(Source: AMFI data & KPMG Report 2009, pp. 4)

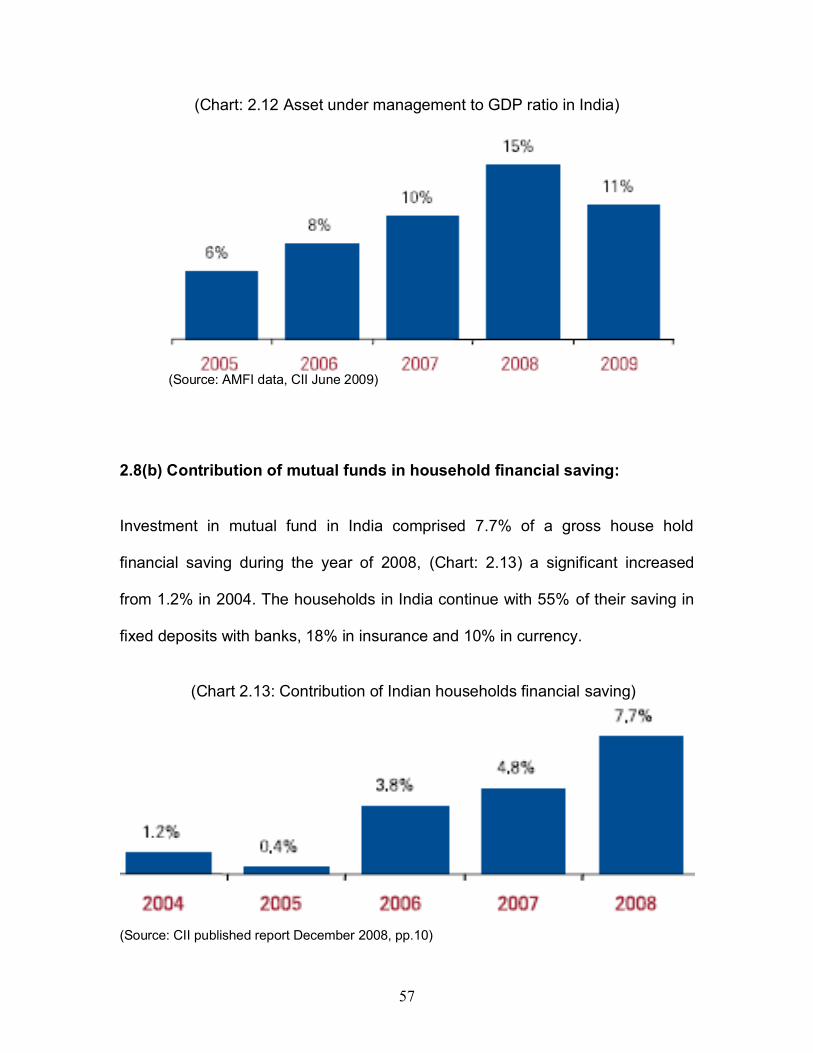

6% in 2005 to 11% in 2009. Despite this however, this continues to be

significantly lower then the ratio in developed countries, where the asset under

management accounts for 20% to 70% of GDP.

57

(Chart: 2.12 Asset under management to GDP ratio in India)

(Source: AMFI data, CII June 2009)

2.8(b) Contribution of mutual funds in household financial saving:

Investment in mutual fund in India comprised 7.7% of a gross house hold

financial saving during the year of 2008, (Chart: 2.13) a significant increased

from 1.2% in 2004. The households in India continue with 55% of their saving in

fixed deposits with banks, 18% in insurance and 10% in currency.

(Chart 2.13: Contribution of Indian households financial saving)

(Source: CII published report December 2008, pp.10)

58

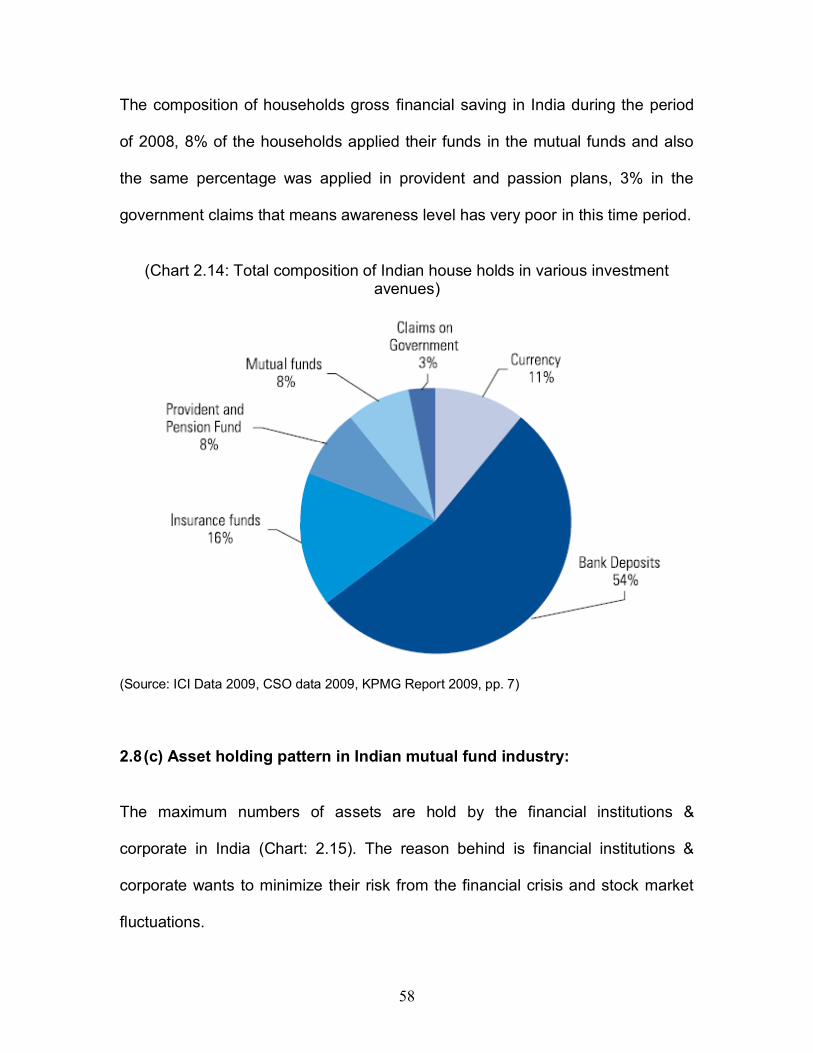

The composition of households gross financial saving in India during the period

of 2008, 8% of the households applied their funds in the mutual funds and also

the same percentage was applied in provident and passion plans, 3% in the

government claims that means awareness level has very poor in this time period.

(Chart 2.14: Total composition of Indian house holds in various investment avenues)

(Source: ICI Data 2009, CSO data 2009, KPMG Report 2009, pp. 7)

2.8 (c) Asset holding pattern in Indian mutual fund industry:

The maximum numbers of assets are hold by the financial institutions &

corporate in India (Chart: 2.15). The reason behind is financial institutions &

corporate wants to minimize their risk from the financial crisis and stock market

fluctuations.

59

(Chart 2.15: Investment Holding Pattern in India)

(Source: SEBI, SBI Handbook, 2009)

The investor-wise pattern of asset-holding as well as investors accounts reveals

that individual investors account for almost 96.75% of total investors account and

contribute Rs 1552.8 Bn which is 37.0% of the total net assets as on March 31,

2009. The comparatively lower share of net assets of individual investors in total

net assets is mainly because of lower penetration of mutual fund as an

investment instrument among working population (age group 18-59 years). A

majority of investors in the age group 18-59 years are not aware of mutual funds

or of investing in mutual funds through Systematic Investment Plan (SIP).

However, take up of mutual fund as an investment opportunity by individual

investors, particularly in Tier 2 and Tier 3 towns, is expected to increase in the

near future.

Corporate/institutions sector on the other hand, though account for only 1.2% of

60

as much as 56.3% to the total net assets of the industry as on March 31, 2009.

Despite a rise in net FII inflows in the domestic mutual funds, FII s constitute a

bn to the total net assets (1% of total net assets of the Indian Mutual fund

industry as on March 31, 2009).

2.8 (d) Key resource drivers of Indian mutual fund industry:

There are lots of key resources divers in the mutual fund industry, these drivers

are considerably pushed to the Indian mutual fund industry. Investment pattern

continuous changing from the early 1990s as result of the LPG policy

announcement. Many of the foreign direct investors & foreign institutional

investors are interested to invest their funds in Indian mutual funds with the back

pool of regularities. Several new asset management companies has established

during this time period with a new products and services, now from this era

onwards lots of new investment avenues were available for the investors with a

different type of characteristics. The only attractive things have begun.

(I) Awareness Level:

The most important driver of growth in the mutual industry is awareness level.

Investors are more aware about the newly introduce financial avenues. Choose

the best fitted investment vehicles among from the available opportunities by

investors. During the period of 2000 to 2005 various kinds of awareness

programme conducted by SEBI (Securities exchange board of India) and AMFI

(Association of mutual funds in India)

61

investors are aware about the mutual funds and also attract toward them. SEBI

(Securities exchange board of

India) also concern with investors wealth and principle. The overall credit goes to

SEBI (Securities exchange board of India) & AMFI (Association of mutual funds

in India) related to awareness programme.

(II) Growth of the financial market:

During the period of 2002 to 2008 tremendous growth shown in the Indian

financial market, because of FII (Foreign institutional investors) & FDI (Foreign

direct investors) has invested huge amount in the Indian stock market. Mutual

fund is relay on subject to the market movement. Indian financial market has

reached at the level of 30% premium during this time period, where the

financial market.

(III) Reserve bank

Most of the investors are planning their future investment plan according to the

re not the

attractive investments for investors. Here the investors are trying to search new

attractive investment avenues, from the available options mutual fund is the best

option; where the investors can generate secured minimum return from their

62

investors. Policy of RBI is the major factor concern with growth of the mutual fund

industry.

(IV) Innovation in distribution channels and availability of the products:

Newly established distribution channels are more effective and efficient to reach

the target base investors with respect to the mutual fund products. Innovation in

distribution channels are expected to raise 2% to 3% from the present market

penetration specifically in rural and semi urban areas. Mutual fund products are

available everywhere. Generally mutual fund products are benefited for the lower

income groups; from the lower income group most of the investors belong from

the ruler area and middle class cities. Now a day in India financial distributors

and other channels are provided various kinds of products towards the

requirement of the investors, so the investors can choose the need based

product as per their needs.

(V) Demographics factors:

The most significant growth driver is demographics factors for mutual fund

industry. Increased in the disposable incomes and saving from the household

saving may result the house holds seeking the Due to urbanization of Indian

rural areas male and female are working and generate some income; also

provide some contribution towards the economy. More young people (Age

between 21 to 39 years) are taking more risk and also demands more returns.

People coming from the rural and semi urban areas are more conservative about

their investment and future security. Form the general trend from the house hold

63

sect

investment. Generally husband and wife both are generating a successive level

of income and they are more conscious about their saving.

(VI) Financial Planning:

Now a day investors are more attentive about their future financial needs, which

means they are always take the help of their financial assistant or financial

advisor. Majority of the investors are generally concern with the secured and

constant return with a safety of principle. Financial planner or assistant will

provide all the possible help to the investors for choosing the investment

avenues. In current scenario most probably all the financial institutions related to

service sector provide this kind of services to their investors. Most of the

investors want to satisfy their needs with the several other advantages. This is

also another important driver of growth in the mutual fund industry.

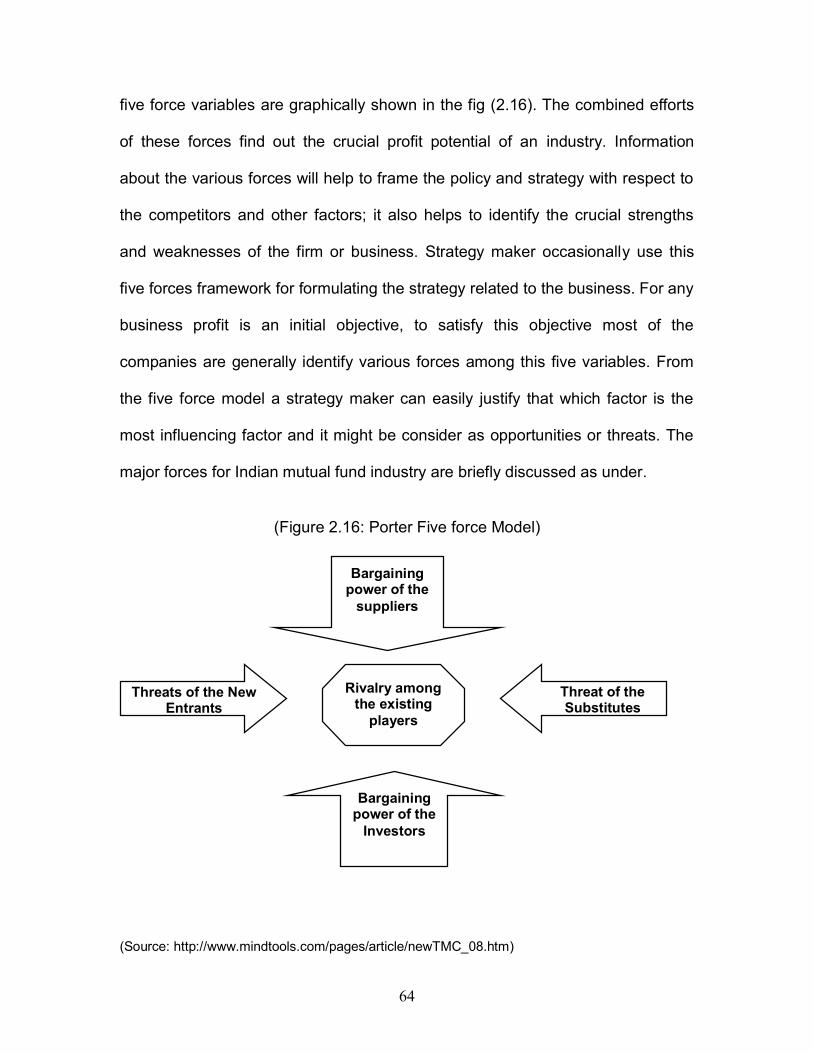

2.8 (e) Porter five forces model for Indian mutual fund industry:

This model was developed by Michael. E. Porter of Harvard business school in

1979. It has provided a frame work for business strategy and industry analysis.

This model concern with the pure competition in the market, where it implies that

risk adjusted rates of return should be steady across industry or firm, hear the

specific factors. Most of the industries depend on the five basic forces as threats

of the new entrants, threat of the substitutes, bargaining power of the suppliers,

bargaining power of the investors and rivalry among the existing players. This

64

five force variables are graphically shown in the fig (2.16). The combined efforts

of these forces find out the crucial profit potential of an industry. Information

about the various forces will help to frame the policy and strategy with respect to

the competitors and other factors; it also helps to identify the crucial strengths

and weaknesses of the firm or business. Strategy maker occasionally use this

five forces framework for formulating the strategy related to the business. For any

business profit is an initial objective, to satisfy this objective most of the

companies are generally identify various forces among this five variables. From

the five force model a strategy maker can easily justify that which factor is the

most influencing factor and it might be consider as opportunities or threats. The

major forces for Indian mutual fund industry are briefly discussed as under.

(Figure 2.16: Porter Five force Model)

(Source: http://www.mindtools.com/pages/article/newTMC_08.htm)

Threats of the New Entrants

Threat of the Substitutes

Bargaining power of the

Investors

Bargaining power of the

suppliers

Rivalry among the existing

players

65

(A) Threats of the new Entrants:

SEBI (Securities board of India) and AMFI (Association of Mutual funds in India)

considerable laid out rules & regulations for new entrants in mutual fund industry.

playing very well in the industry. For new entrants the significant amount of

investment & complicated process for taking the permission from the SEBI &

institutions have been tie up with banks and other financial corporations to

establish a new AMC (Assets management Companies). It is a bright hope for

potential new entrants.

(B) Threats of the substitutes:

Substitute products & services are those which are different but satisfy the same

needs of the investors. Among th

various kind of financial products are easily available from the present players.

On the other side various similar kinds of products are also available in the

financial market. The major alternative of mutual funds products are insurance

schemes, derivative contracts, option contracts, future contracts, forward

contracts, gold mini contracts and many more. Every day at least one new

product launch with a different type of characteristics. Now a day mutual funds

are not limited to traditional open ended & close ended schemes, there are lots of

66

choices are available in the financial basket for the purpose of investment. Most

of the investors are largely depends on the advice of market makers & stock

brokers, that means many of the substitute products & services are affected by

the market makers & stock brokers. In the mutual fund industry availability of

substitutes are very high.

(C) Bargaining power of the suppliers:

In India mutual fund industry governed by SEBI (Securities exchange board of

India) & AMFI (Association of Mutual funds in India), these two prime governing

bodies are having an authority to provide guidelines for mutual funds. Suppliers

of the mutual funds industry are financial institutions, major collaborative banks

and asset management companies. The common objectives of the suppliers are

to down sizing risk and at least generates moderate or higher amount of return.

The general ideas related to the market players are to provide a batter products

& services to the investors. At the inception time of mutual fund industry in India

very limited numbers of players are available, but from the fourth growth phase

onwards various private players are also jump in this industry. So the quality of

the services has increased year by year. In Indian mutual fund industry

bargaining power of the suppliers are low.

(D) Bargaining power of the investors:

The bargaining powers of the investors are very high. The wide ranges of

financial products are available. The marketers have segmented the market in to

67

been observed that those assets management companies are not having sound

marketing strategies have facing a various kind of problems. Cost of switching

from one scheme to other scheme is very low, so investors can easily shift from

one to another. Fund manager have not performing very well then existing

investors withdrawal their money and invest else where.

(E) Rivalry among the existing players:

Rivalries among the existing players are very high, because most of the asset

management companies are provided homogeneous kind of products & services.

Hear the main reason is high market growth. India is one of the largest market

place and overall potential economic growth of country is high as compared to

other developing countries. Another main reason for strong competition is

undifferentiated services which can be provided by all the assets management

companies. Most of the mutual fund investors are not loyal towards their mutual

fund schemes, because the same kind of investment avenues are provided

higher amount of return, that means clients acquisition is the major competitive

factor among the existing players.

2.9 Market share of the Indian Mutual fund industry:

During the period of 2000 to 2009, 38 mutual fund players have been given the

regulatory approval by SEBI (Securities exchange board of India). The drastic

changed in the mutual fund industry from 2001 to 2009, investors has shifted

from public players to private sector players and also increased the contribution

of private sector players towards the industry. The sudden fall in the market

68

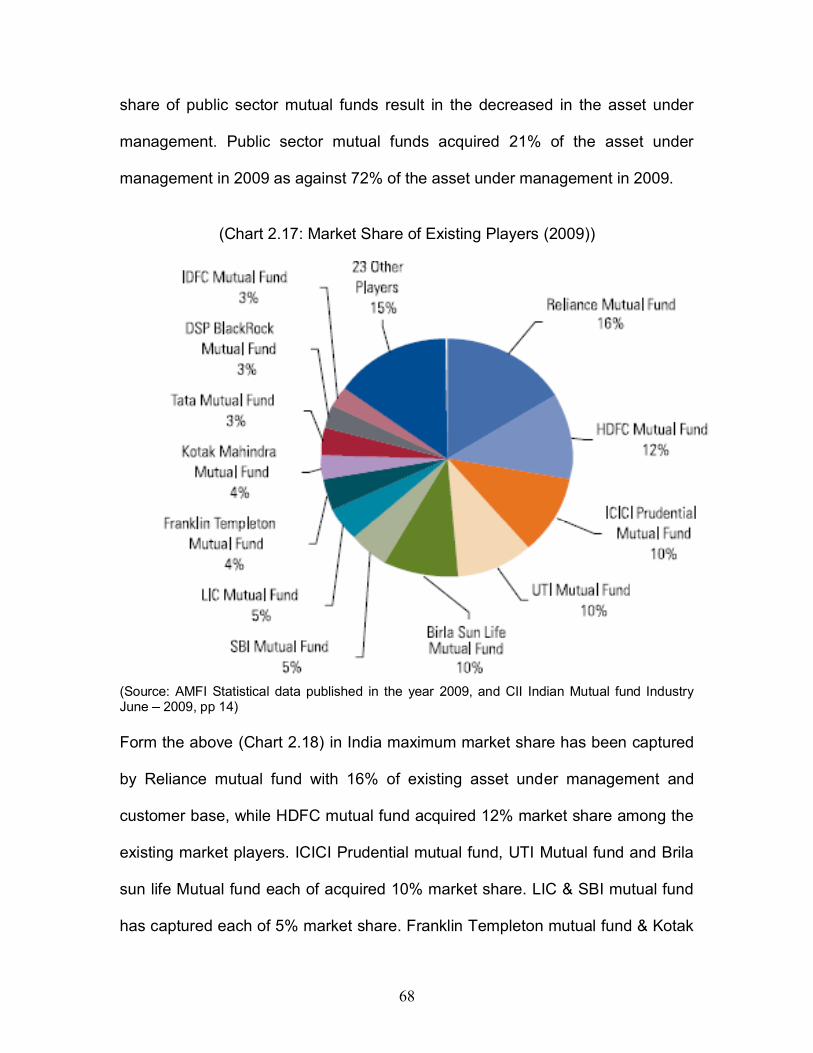

share of public sector mutual funds result in the decreased in the asset under

management. Public sector mutual funds acquired 21% of the asset under

management in 2009 as against 72% of the asset under management in 2009.

(Chart 2.17: Market Share of Existing Players (2009))

(Source: AMFI Statistical data published in the year 2009, and CII Indian Mutual fund Industry June 2009, pp 14)

Form the above (Chart 2.18) in India maximum market share has been captured

by Reliance mutual fund with 16% of existing asset under management and

customer base, while HDFC mutual fund acquired 12% market share among the

existing market players. ICICI Prudential mutual fund, UTI Mutual fund and Brila

sun life Mutual fund each of acquired 10% market share. LIC & SBI mutual fund

has captured each of 5% market share. Franklin Templeton mutual fund & Kotak

69

mahindra mutual fund gain each of 4% market share. IDFC mutual fund and DSP

Black rock mutual fund has acquired each of 3% market share and remaining

15% market share has been adopted by local and 23 other players. The

conclusion drawn from the present situation has more than 58% market share

achieved by top 5 major market players.

The Indian mutual fund industry has been witnessed during the period of 2005 to

2008; top 5 players jointly acquired more than 50% of industry asset under

management, however it has constantly increased up to March 2009 with 58% as

against the 38% in the US. In India major top 10 players has consistently been

gained 75% of market share in asset under management.

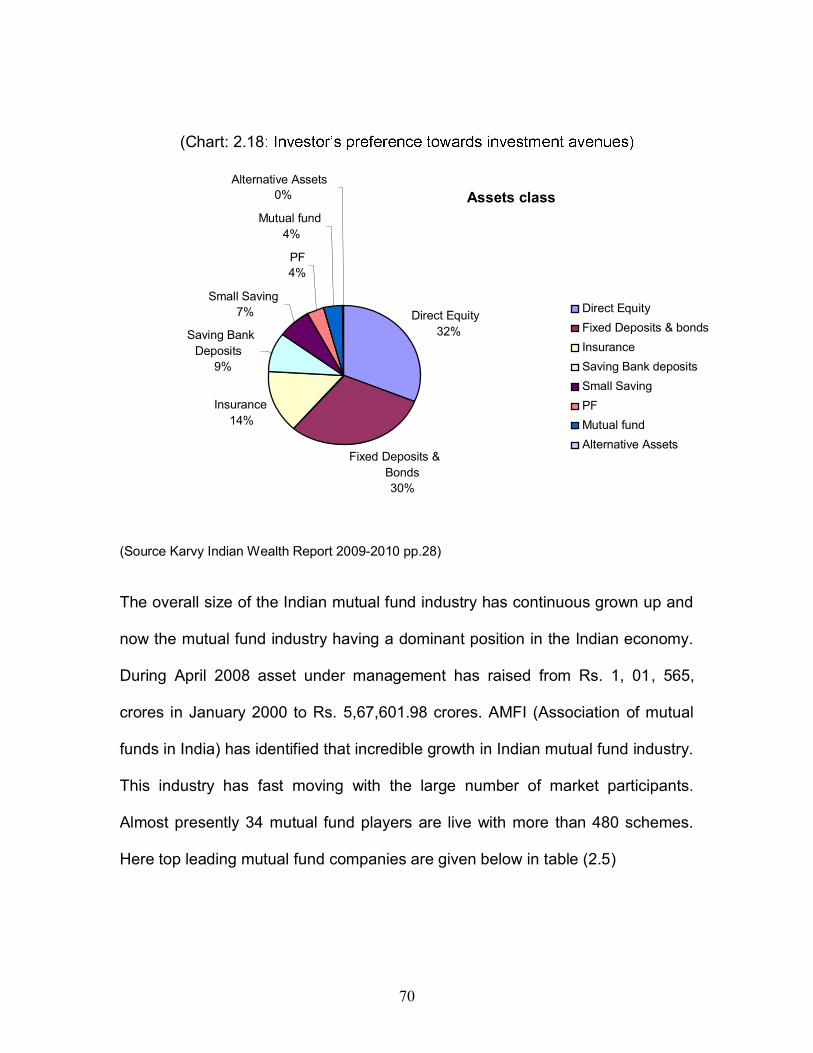

Hear from the below pie chart (Chart 2.18) asset break up of individual wealth in

India. From the several assets 32% investors preferred to invest as a assets in a

equity, while 30% of investors preferred fixed deposits and bonds, 14% investors

are interested in the insurance sector, 9% belongs to the saving banks deposits,

7% from the small saving assets avenues. 4% of each is in mutual fund and

provident funds.

Its clearly depict from the above pie chart and statistics only 4% investors are

invested their money in mutual funds that means still a huge untapped market

available for the mutual fund companies and asset under management.

70

(Chart: 2.18

(Source Karvy Indian Wealth Report 2009-2010 pp.28)

The overall size of the Indian mutual fund industry has continuous grown up and

now the mutual fund industry having a dominant position in the Indian economy.

During April 2008 asset under management has raised from Rs. 1, 01, 565,

crores in January 2000 to Rs. 5,67,601.98 crores. AMFI (Association of mutual

funds in India) has identified that incredible growth in Indian mutual fund industry.

This industry has fast moving with the large number of market participants.

Almost presently 34 mutual fund players are live with more than 480 schemes.

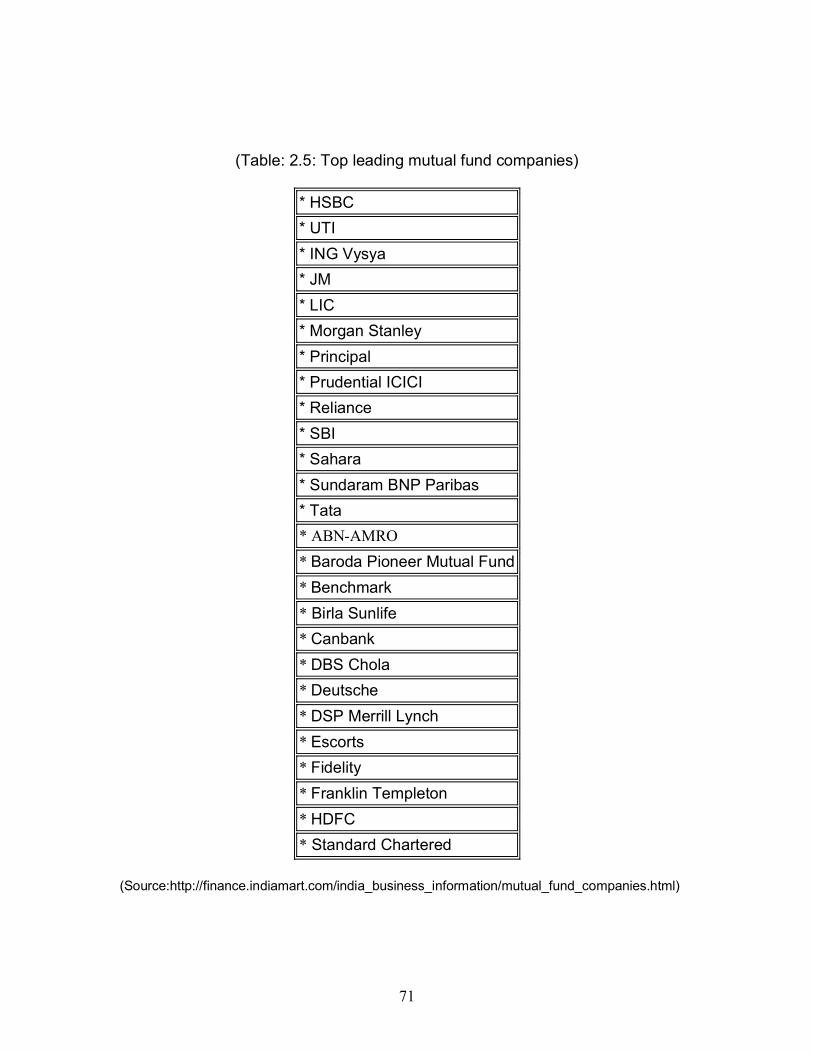

Here top leading mutual fund companies are given below in table (2.5)

Assets class

Direct Equity 32%

Fixed Deposits & Bonds 30%

Insurance 14%

Saving Bank Deposits

9%

Small Saving 7%

PF 4%

Mutual fund 4%

Alternative Assets 0%

Direct Equity Fixed Deposits & bonds Insurance Saving Bank deposits Small Saving PF Mutual fund Alternative Assets

71

(Table: 2.5: Top leading mutual fund companies)

* HSBC * UTI * ING Vysya * JM * LIC * Morgan Stanley * Principal * Prudential ICICI * Reliance * SBI * Sahara * Sundaram BNP Paribas * Tata * ABN-AMRO * Baroda Pioneer Mutual Fund * Benchmark * Birla Sunlife * Canbank * DBS Chola * Deutsche * DSP Merrill Lynch * Escorts * Fidelity * Franklin Templeton * HDFC * Standard Chartered

(Source:http://finance.indiamart.com/india_business_information/mutual_fund_companies.html)

72

As compare to other develop countries economy penetration level is very low in

India. The world industry has grown in terms of size and total assets under

management of more than 30,351million USD. From the various sector, the

domestic private players plays vital role in the growth mutual fund industry. The

total accounts approximately 91% of the resources has mobilized showing their

overwhelming dominance in the market. Individual contributes 98.04% of their

savings; 56.16% out of 98.04% invested their funds assets under management.

2.10 Challenges in the Indian Mutual fund industry:

Indian mutual fund industry has grown with positive growth rate from the past few

years; the major challenge face by mutual industry that during the period of

financial crisis investors are move away from the financial market as well as

financial products. Economic reforms regulatory amendments are the again

important challenges in the mutual funds industry. Some of the challenges are

listed below;

2.10 (a) Heavy burden on margin:

Most of the fund houses facing maximum burden on margin. Due to the heavy

burden of the margin cost structure of the fund houses are not behave in

effective & efficient manner. Increase in the area of cost means less

attractiveness of the various mutual products. Regulatory compliance is one of

the reasons for increase in the cost structure for fund houses. Local distribution

channels are also influencing the cost structure for mutual fund houses.

73

2.10 (b) Market competitions:

mutual fund industry. It is very difficult to survive for s

competitive market. Valuable efforts put by regulatory bodies through the

mergers and acquisitions in the mutual fund industry for reducing competition.

Looking forward to the future prospects heavy market competition is the

challenges in the mutual fund industry.

2.10 (c) Structural reforms in the economy:

From 2008 to 2011 Indian economy has facing lots of financial problems; to cope

up with these difficulties government & RBI (Reserve Bank of India) take some

precautionary steps for stability in the economy. Most of the financial sector has

facing the problem of financial crisis. Mutual fund is the one of the segments

where investors are loosing their trust toward the mutual fund products due to the

financial crisis even though this sector has not affecting very much by financial

crisis. Regulatory reforms are most significant challenge in the mutual fund

industry.

2.10 (d) Availability of resources:

The major challenge is the availability of proper resource persons in the mutual

fund houses. The fund manager is not capable enough to manage the portfolio of

various funds then performance of the scheme in terms of return or NAV (Net

assets value) is reducing and these mutual fund products are less attractive.

74

Shortage of the talented resource person is the drawback of Indian mutual fund

industry.

2.10(e) Market stability:

As we know very well mutual funds are subject to the market risk that means

return of funds is totally depends on the market movement. Due to the huge

scams in the Indian financial market investors are loose their confidence in the

mutual fund products even though they reduce their tax obligation. Market

fluctuation is the challenge in the Indian mutual fund industry.

2.11 Future outlook of mutual fund industry:

Mutual fund is capable enough to attract the Indian capital market. Mutual fund is

a more trustworthy investment avenue as compared to the other investment

vehicle in financial market. Mutual fund is quite risky investment but on the other

side it gives many more benefits. Mutual fund industry has shows significant

growth in last decades.

From the mutual fund sector limited share has been kept by households. Now

higher number of households interested to invest their money in less risky & high

yield funds. Due to urbanization, financial awareness and young population with

a increased risk appetite mutual fund industry have a tremendous potential

untapped market in the various demographic regions.

75

The innovative & extraordinary distribution channel plays a significant role

especially in class II and Class III cities or towns; which are having a potential

future mutual market. This will enhance to reach of mutual funds to the rural

population. Domestic collaboration and joint venture are also helpful for

accelerating the growth in the mutual fund industry in future.

Entry of the global players, huge competition in the local mutual market is

expected to increase. Due to market competition asset management companies

develop new marketing strategies and it will result to increase in the potential

percentage of investment in mutual fund segment.

As per the general observation of Indian economy have a more concentric saving

approach as compare to rest of the world. Indian investors are expected to

increase their investments in mutual funds to gain the several advantages.

Right now Indian economy passing through very critical condition; probably

growth of all the sectors are in a negative mode. Based on the estimation of

KPMG (Klynveld Peat Marwick Goerdeler) and CII (Confederation of Indian

Industry) asset under management of mutual funds will increase in the range of

15% to 25% by 2015. The estimation also indicates that profitability of fund

houses will be reducing due to various economic factors. As per new research

create a new benchmark of USD 300 billion by 2015. In future SEBI (securities

exchange board of India) and AMFI (Association of Mutual funds) will conduct

76

more awareness programme with the help of NISM (National Institute of Stock

Market); it will indicate dynamic future growth in mutual fund industry. Some

more regulatory amendments will create more transparency in mutual fund

industry that means more numbers of investors are attract towards mutual fund

products in future.