chapter 3 interest and equivalence -...

TRANSCRIPT

Engineering Economics ECIV 5245

Chapter 3

Interest and Equivalence

2

Cash Flow Diagrams (CFD)

Used to model the positive and negative cash flows.

At each time at which cash flow will occur, a vertical

arrow is added, point down for costs and up for

revenues.

Cash flow are drawn to relative scale

Rent and insurance are beginning-of-period cash

flows; i.e. just put an arrow in where it occurs.

O&M, salvages, and revenues are assumed to be end-

of-period cash flows.

3

Example 3-1Purchase a new $30,000 mixing machine. The machine

may be paid for in one of two ways

A. Pay the full price now minus a 3% discount

B. Pay $5000 now, $8000 at the end of 1st yr, and $6000 at

end of each following year

List the alternatives in the form of a table of cash flows

4

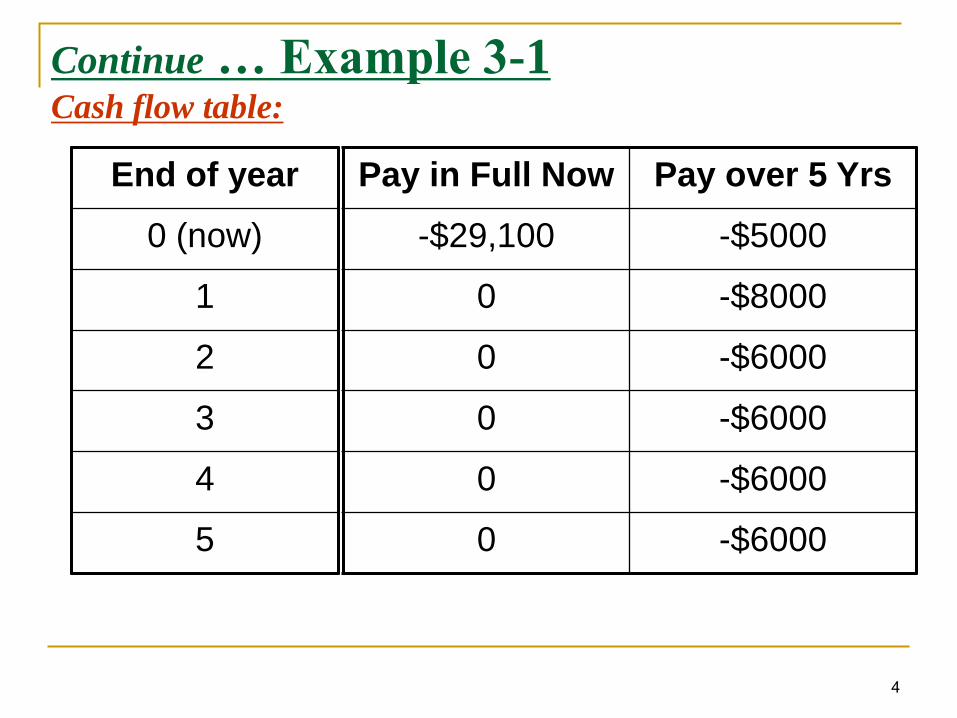

Continue … Example 3-1

End of year

0 (now)

1

2

3

4

5

Pay in Full Now Pay over 5 Yrs

-$29,100 -$5000

0 -$8000

0 -$6000

0 -$6000

0 -$6000

0 -$6000

Cash flow table:

5

Example 3-2A man borrowed $1000 from a bank at 8% interest.

At the end of 1st yr: Pay half of the $1000 principal amount

plus the interest.

At the end of 2nd yr: Pay the remaining half of the principal

amount plus the interest for the second year.

Compute the borrower’s cash flow

End of Year Cash Flows

0 (Now) +$1000

1 -580

2 -540

6

Time Value of Money

If monetary consequences occur in a short period of

time → Simply add the various sums of money

What if time span is greater?

$100 cash today vs. $100 cash a year from now?

Money is rented. The rent is called the interest

If you put $100 in the bank today, and interest rate is

9% → $109 a year from now

7

Interest

Simple Interest

Compound interest

8

Simple Interest

Interest that is computed only on the original sum and

not on accrued interest.

e.g. if you loaned someone the amount of P at a simple

interest rate of i for a period of n years:

Total interest earned = P× i× n = P i n

The amount of money due after n years:

F = P + P i n

Or F = P(1+ i n)

9

Example 3-3You loaned a friend $5000 for 5 years at a simple

interest rate of 8% per year.

How much interest you receive from the loan?

How much will your friend pay you at the end of 5 yrs.

Total interest earned = P i n = (5000)(0.08)(5) = $2000

Amount due at the end of loan = P + P i n = 5000 + 2000

= $7000

10

Compound Interest

This is the interest normally used in real life

Interest on top of interest

Next year’s interest is calculated based on the unpaid

balance due, which includes the unpaid interest from

the preceding period.

11

Example 3-4

12

… Compound Interest

Compound interest is interest that is charged on the original sum and un-paid interest.

You put $500 in a bank for 3 years at 6% compound interestper year.

At the end of year 1 you have (1.06) 500 = $530.

At the end of year 2 you have (1.06) 530 = $561.80.

At the end of year 3 you have (1.06) $561.80 = $595.51.

Note:

$595.51 = (1.06) 561.80

= (1.06) (1.06) 530

= (1.06) (1.06) (1.06) 500 = 500 (1.06)3

13

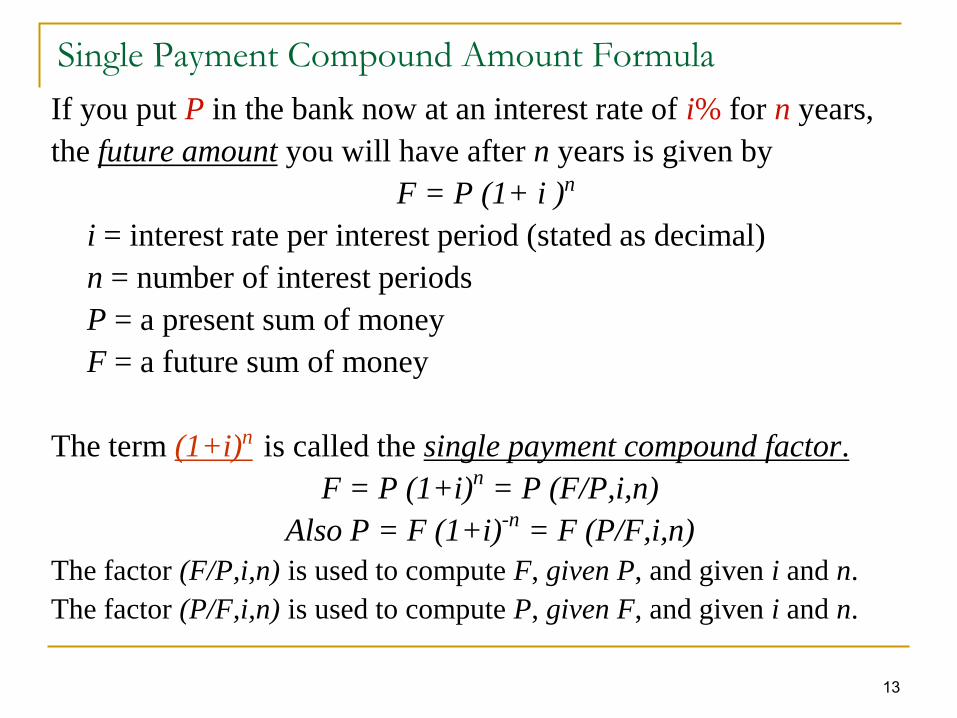

Single Payment Compound Amount Formula

If you put P in the bank now at an interest rate of i% for n years,

the future amount you will have after n years is given by

F = P (1+ i )n

i = interest rate per interest period (stated as decimal)

n = number of interest periods

P = a present sum of money

F = a future sum of money

The term (1+i)n is called the single payment compound factor.

F = P (1+i)n = P (F/P,i,n)

Also P = F (1+i)-n = F (P/F,i,n)

The factor (F/P,i,n) is used to compute F, given P, and given i and n.

The factor (P/F,i,n) is used to compute P, given F, and given i and n.

14

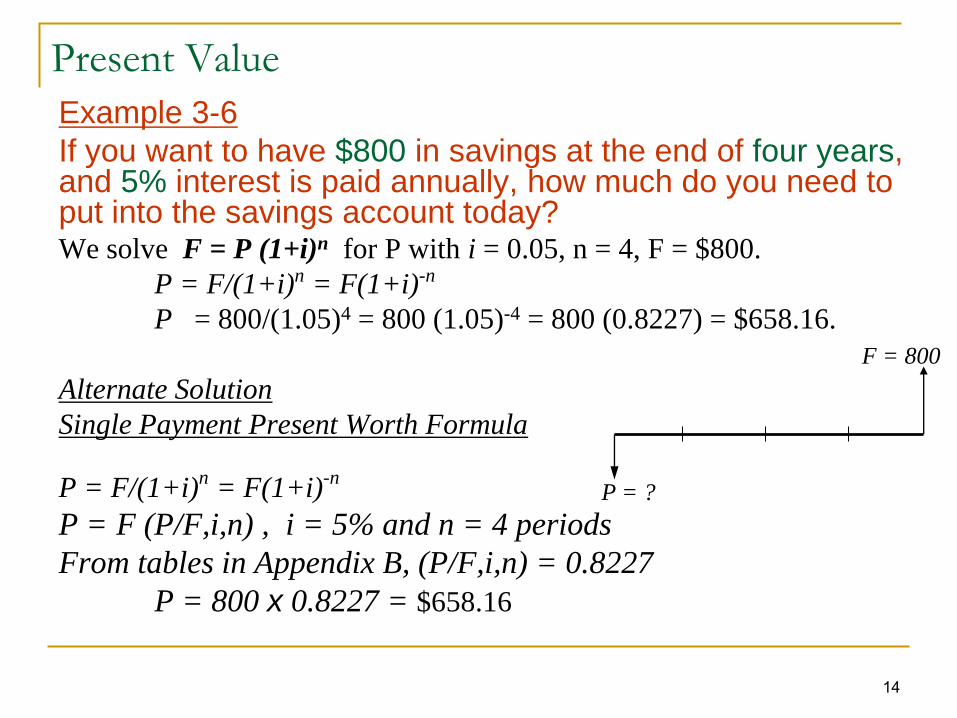

Present Value

Example 3-6

If you want to have $800 in savings at the end of four years, and 5% interest is paid annually, how much do you need to put into the savings account today?We solve F = P (1+i)n for P with i = 0.05, n = 4, F = $800.

P = F/(1+i)n = F(1+i)-n

P = 800/(1.05)4 = 800 (1.05)-4 = 800 (0.8227) = $658.16.

Alternate Solution

Single Payment Present Worth Formula

P = F/(1+i)n = F(1+i)-n

P = F (P/F,i,n) , i = 5% and n = 4 periods

From tables in Appendix B, (P/F,i,n) = 0.8227

P = 800 x 0.8227 = $658.16

F = 800

P = ?

15

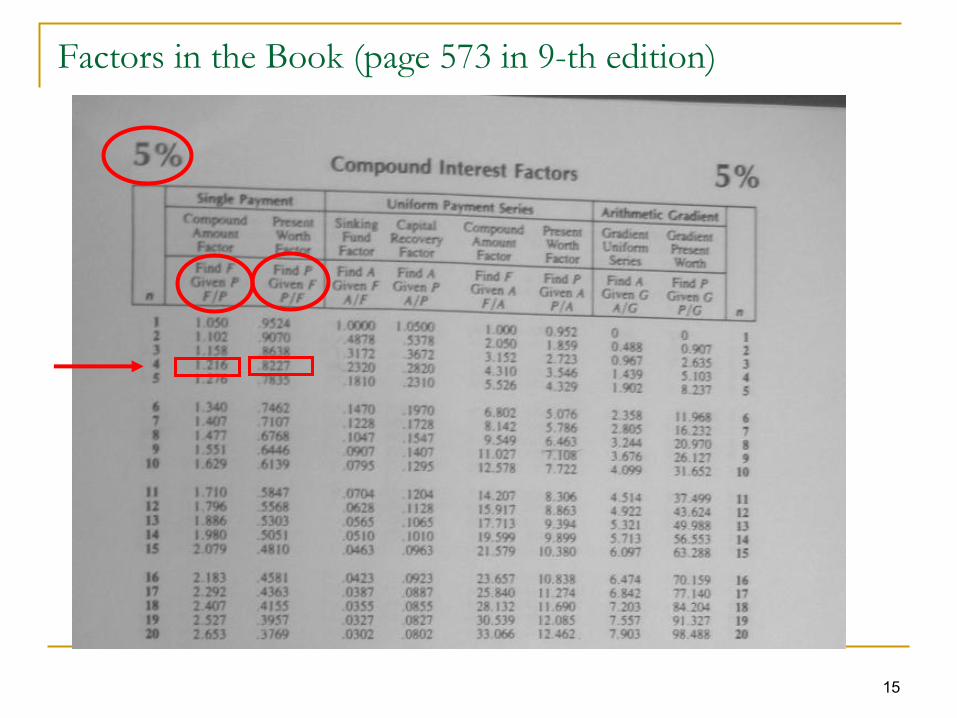

Factors in the Book (page 573 in 9-th edition)

16

Present ValueExample: You borrowed $5,000 from a bank at 8%

interest rate and you have to pay it back in 5 years. The debt can be repaid in many ways.

Plan A: At end of each year pay $1,000 principal

plus interest due.

Plan B: Pay interest due at end of each year and

principal at end of five years.

Plan C: Pay in five end-of-year payments.

Plan D: Pay principal and interest in one payment

at end of five years.

17

…Example (cont’d)You borrowed $5,000 from a bank at 8% interest rate and you have to pay

it back in 5 years.

Plan A: At end of each year pay $1,000 principal plus interest due.

a b c d e f

Year Amnt.

Owed

Int. Owed Total OwedPrincip.

Payment

Total

Paymentint*b b+c

1 5,000 400 5,400 1,000 1,400

2 4,000 320 4,320 1,000 1,320

3 3,000 240 3,240 1,000 1,240

4 2,000 160 2,160 1,000 1,160

5 1,000 80 1,080 1,000 1,080

SUM 1,200 5,000 6,200

18

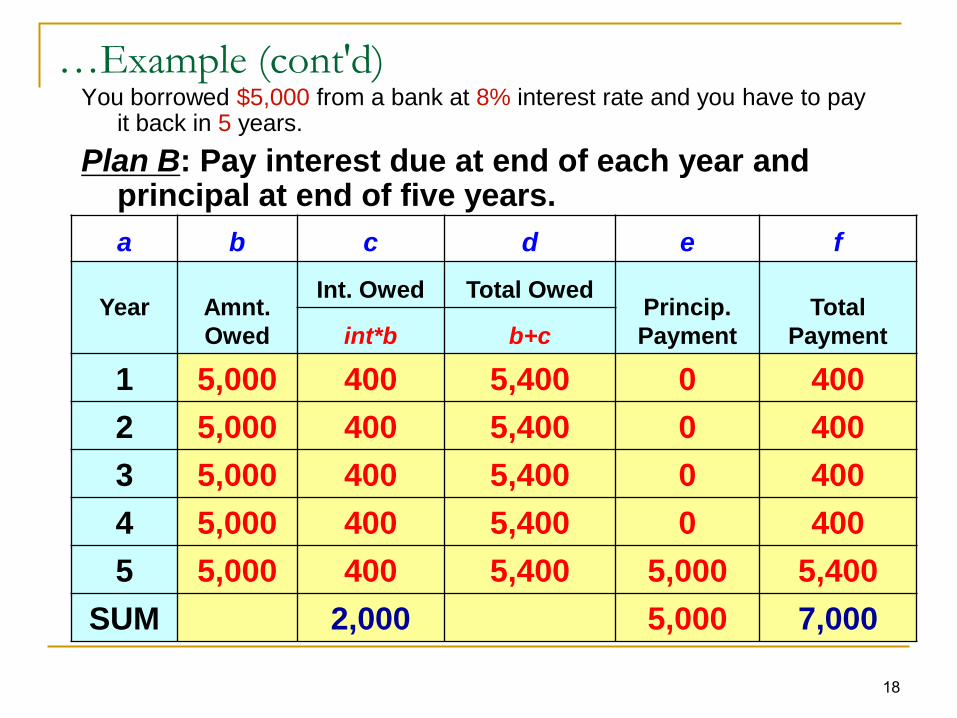

…Example (cont'd)You borrowed $5,000 from a bank at 8% interest rate and you have to pay

it back in 5 years.

Plan B: Pay interest due at end of each year and principal at end of five years.

a b c d e f

Year Amnt.

Owed

Int. Owed Total OwedPrincip.

Payment

Total

Paymentint*b b+c

1 5,000 400 5,400 0 400

2 5,000 400 5,400 0 400

3 5,000 400 5,400 0 400

4 5,000 400 5,400 0 400

5 5,000 400 5,400 5,000 5,400

SUM 2,000 5,000 7,000

19

… Example (cont'd)You borrowed $5,000 from a bank at 8% interest rate and you have to pay

it back in 5 years.

Plan C: Pay in five equal end-of-year payments.

a b c d e f

Year Amnt.

Owed

Int. Owed Total OwedPrincip.

Payment

Total

Paymentint*b b+c

1 5,000 400 5,400 852 1,252

2 4,148 332 4,480 920 1,252

3 3,227 258 3,485 994 1,252

4 2,233 179 2,412 1,074 1,252

5 1,160 93 1,252 1,160 1,252

SUM 1,261 5,000 6,261

20

… Example (cont'd)You borrowed $5,000 from a bank at 8% interest rate and you have to pay

it back in 5 years.

Plan D: Pay principal and interest in one payment at end of five years.

a b c d e f

Year Amnt.

Owed

Int. Owed Total OwedPrincip.

Payment

Total

Paymentint*b b+c

1 5,000 400 5,400 0 0

2 5,400 432 5,832 0 0

3 5,832 467 6,299 0 0

4 6,299 504 6,802 0 0

5 6,802 544 7,347 5,000 7,347

SUM 2,347 5,000 7,347

21

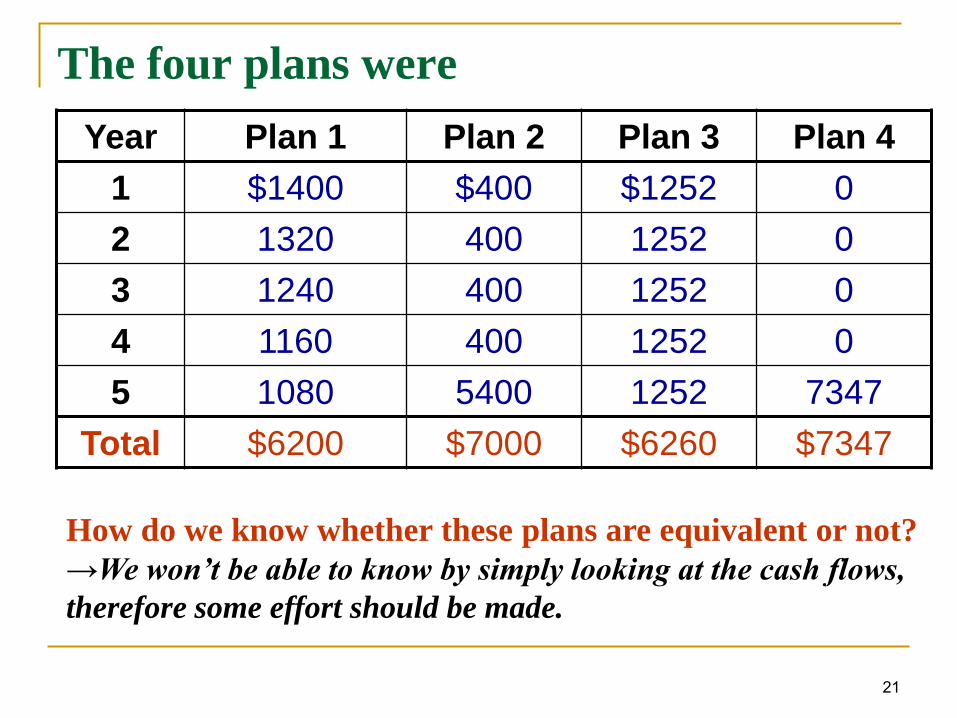

The four plans were

Year Plan 1 Plan 2 Plan 3 Plan 4

1 $1400 $400 $1252 0

2 1320 400 1252 0

3 1240 400 1252 0

4 1160 400 1252 0

5 1080 5400 1252 7347

Total $6200 $7000 $6260 $7347

How do we know whether these plans are equivalent or not?

→We won’t be able to know by simply looking at the cash flows,

therefore some effort should be made.

22

Equivalence

In the previous example, four payment plans were

described.

The four plans were used to accomplish the task of

repaying a debt of $5000 with interest at 8%.

All four plans are equivalent to $5000 now.

i.e. all four plans are said to be equivalent to each

other and to $5000 now.

23

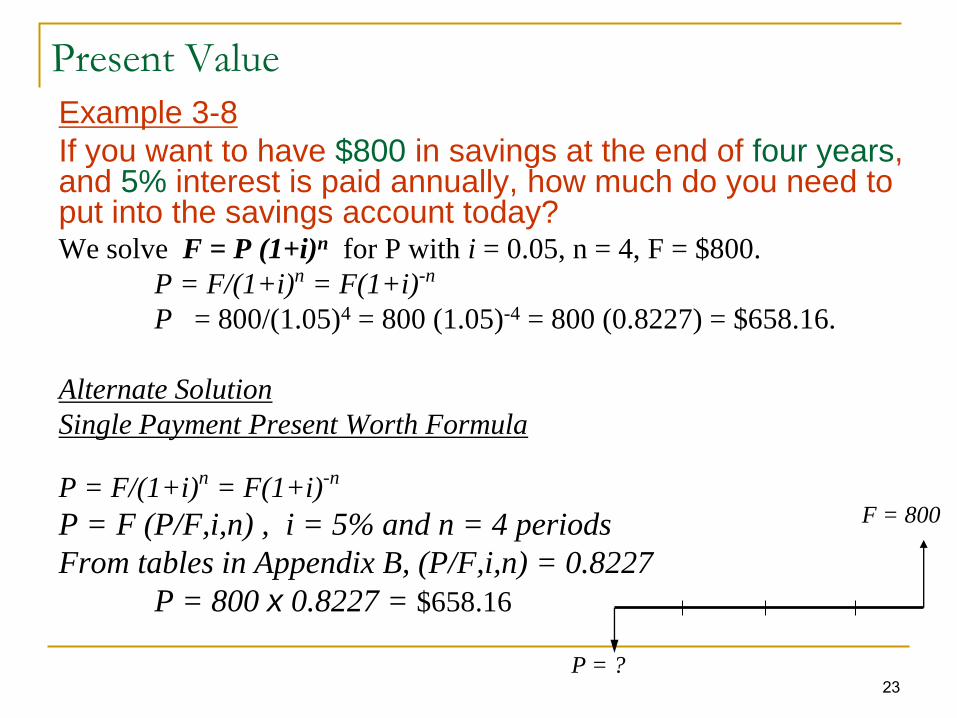

Present Value

Example 3-8

If you want to have $800 in savings at the end of four years, and 5% interest is paid annually, how much do you need to put into the savings account today?We solve F = P (1+i)n for P with i = 0.05, n = 4, F = $800.

P = F/(1+i)n = F(1+i)-n

P = 800/(1.05)4 = 800 (1.05)-4 = 800 (0.8227) = $658.16.

Alternate Solution

Single Payment Present Worth Formula

P = F/(1+i)n = F(1+i)-n

P = F (P/F,i,n) , i = 5% and n = 4 periods

From tables in Appendix B, (P/F,i,n) = 0.8227

P = 800 x 0.8227 = $658.16

F = 800

P = ?

24

In 3 years, you need $400 to pay a debt. In two more years, you need $600 more to pay a second debt. How much should you put in the bank today to meet these two needs if the bank pays 12% per year?

Interest is compounded yearly

P = 400(P/F,12%,3) + 600(P/F,12%,5)

= 400 (0.7118) + 600 (0.5674)

= 284.72 + 340.44 = $625.16

$400

0 1 2 3 4 5

$600

Alternate Solution

P = F(1+i)-n

P = 400(1+0.12)-3

+ 600(1+0.12)-5

P = $625.17

Example 3-8

P

25

In 3 years, you need $400 to pay a debt. In two more years, you need $600 more to pay a second debt. How much should you put in the bank today to meet these two needs if the bank pays 12% compounded monthly?

Interest is compounded yearly

P = 400(P/F,12%,3) + 600(P/F,12%,5)

= 400 (0.7118) + 600 (0.5674)

= 284.72 + 340.44 = $625.16

$400

0 1 2 3 4 5

$600

Interest is compounded monthly

P = 400(P/F,12%/12,3*12) + 600(P/F,12%/12,5*12)

= 400(P/F,1%,36) + 600(P/F,1%,60)

= 400 (0.6989) + 600 (0.5504)

= 279.56 + 330.24 = $609.80

Example 3-8 (Interest Compounded monthly)

P

26

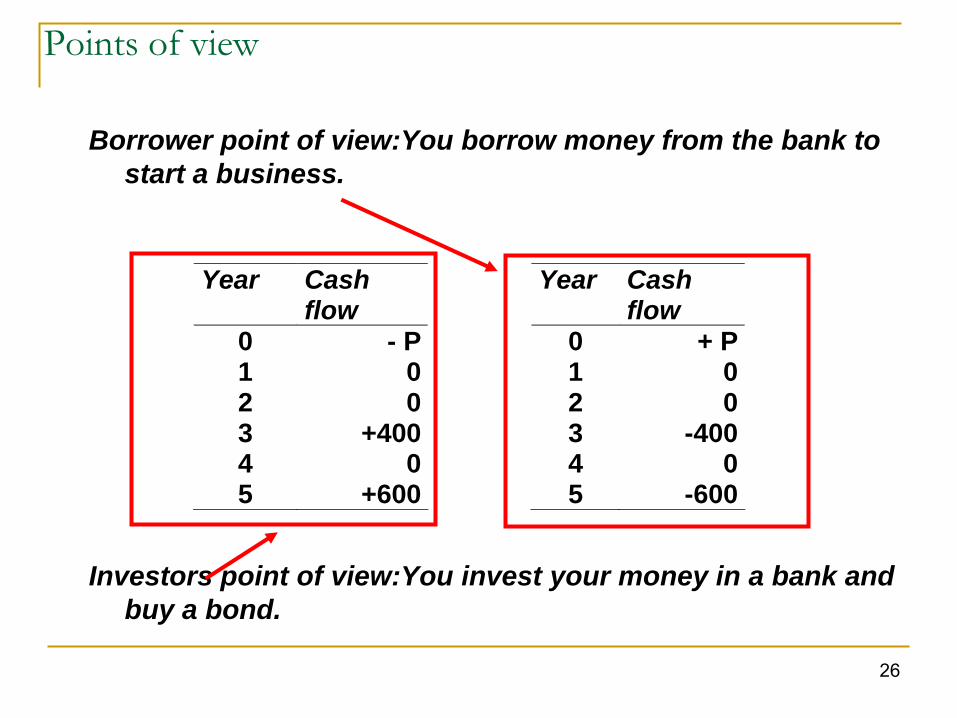

Borrower point of view:You borrow money from the bank to

start a business.

Investors point of view:You invest your money in a bank and

buy a bond.

Year Cash flow

0 - P 1 0 2 0 3 +400 4 0 5 +600

Year Cash flow

0 + P 1 0 2 0 3 -400 4 0 5 -600

Points of view

27

Appendix B in the text book tabulate:

Compound Amount Factor

(F/P,i,n) = (1+i)n

Present Worth Factor

(P/F,i,n) = (1+i)-n

These terms are in columns 2 and 3, identified as

Compound Amount Factor: “Find F Given P: F/P”

Present Worth Factor: “Find P Given F: P/F”

Concluding Remarks