chapter 3 · web viewchapter 13 governance role of public shareholders overview theories of the...

TRANSCRIPT

Chapter 13 Governance Role of ShareholdersOutline

Chapter 13 Governance Role of Public ShareholdersA. OverviewB. Theories of the Firm

1. The Berle – Means Corporationo separation of ownership and controlo "management control"o law should be control device

2. The “Nexus of Contracts” Corporationo management-shareholder contracto mediated by markets: capital, control, employment, and chartering marketso law enforces implicit bargains

3. The “Political Product” Corporationo mandatory vs. enabling terms / fiduciary principleso anti-takeover legislationo law should be efficiency-minded

4. The “Team Production” Corporationo managers seek protection from institutional controlo banks, mutual funds, pension funds systematically weakened

C. The Dynamics of Shareholder Voting1. Shareholder voting rights

o voting by proxy state law: conditions

2. Federal proxy regulationo federal law: disclosure in public corporations

3. The proxy mechanism4. the collective action problem

o rational passivity o reasons

information costs free-rider problems prisoners' dilemma

o overcome: large, organized investors5. Institutional investors

o Types of institutional investors,trend in ownership; concentration in public companies

o constraints on institutional activism government regulation

SEC proxy rules insider trading rules 5% voting group disclosure

incentives / conflicts private pension funds - who manages?

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

1

mutual funds - where get information to beat market? insurance companies - what relation to corp. management? banks - what is main business with corporations?

D. Federal Regulation of Proxy Solicitations1. Management solicitations

o Securities Exchange Act of 1934 - § 14(a) "reporting companies" - § 12

equity securities listed on exchange 500 shareholders + $10 million assets

scope of SEC regulatory authority2. “Proxy solicitation”

o Long Island Lighting Company v. Barbasho SEC proxy rules

proxy card - Rule 14a- proxy statement - Rule 14a-

when prepare? filing obligation? nature of disclosure?

proxy "solicitation" - Rules 14a-1, 14a-2 definition / part of "continuous plan"

3. Shareholder communicationso 1992 Amendments

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

2

E. Shareholder Proposals1. Evolution of the shareholder proposal rule2. Rule 14a-8 in operation

o Lovenheim v. Iroquios Brands, LTD3. Measuring the success of shareholder proposals

o American Foundation of State County v. American International Group

Class Notes

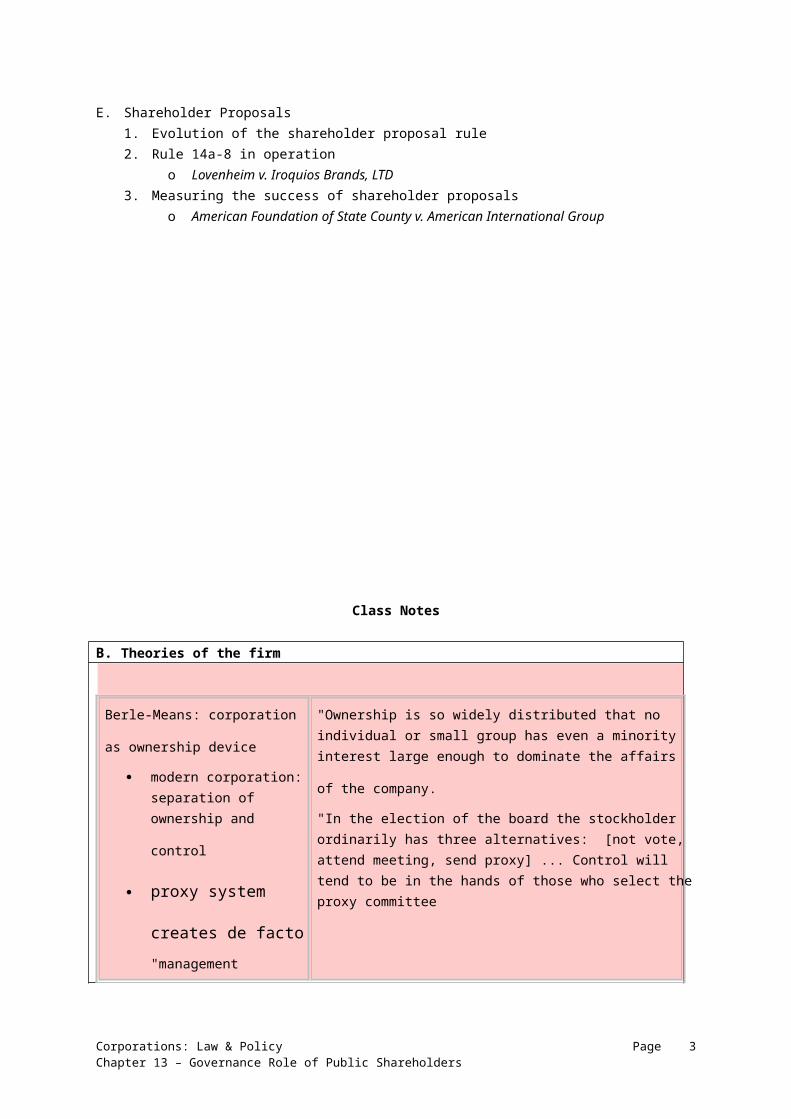

B. Theories of the firm

Berle-Means: corporation as

ownership device modern corporation:

separation of ownership

and control proxy system creates

de facto "management control"

law should be control

device

"Ownership is so widely distributed that no individual or small group has even a minority interest large enough to dominate

the affairs of the company. "In the election of the board the stockholder ordinarily has three alternatives: [not vote, attend meeting, send proxy] ... Control will tend to be in the hands of those who select the proxy committee

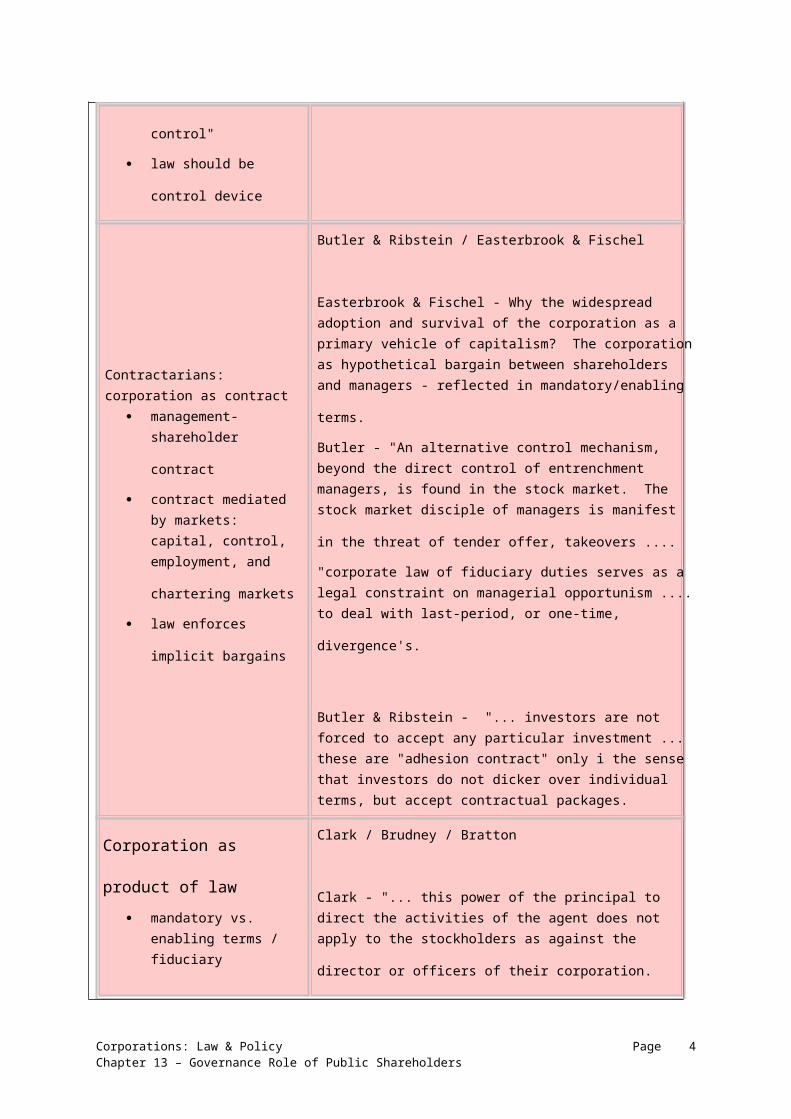

Contractarians: corporation as

contract management-shareholder

contract

Butler & Ribstein / Easterbrook & Fischel Easterbrook & Fischel - Why the widespread adoption and survival of the corporation as a primary vehicle of capitalism?

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

3

contract mediated by markets: capital, control, employment, and

chartering markets law enforces implicit

bargains

The corporation as hypothetical bargain between shareholders

and managers - reflected in mandatory/enabling terms. Butler - "An alternative control mechanism, beyond the direct control of entrenchment managers, is found in the stock market. The stock market disciple of managers is manifest in

the threat of tender offer, takeovers .... "corporate law of fiduciary duties serves as a legal constraint on managerial opportunism .... to deal with last-period, or one-

time, divergence's. Butler & Ribstein - "... investors are not forced to accept any particular investment ... these are "adhesion contract" only i the sense that investors do not dicker over individual terms, but accept contractual packages.

Corporation as product of law

mandatory vs. enabling terms / fiduciary

principles case in point: anti-

takeover legislation law should be regulatory,

efficiency-minded

Clark / Brudney / Bratton Clark - "... this power of the principal to direct the activities of the agent does not apply to the stockholders as against the

director or officers of their corporation. "most of the particular rules that make up the legal relationships among corporate officers, directors and stockholders .... are not the product of actual contracts made by persons subject to

them .... " ... if its intuitively plausible that there are "standard presumptions" adopted to fit the normal case. .... Some corporate law rules cannot be bargained around .... Basic

fiduciary duties fall in this category ... Brudney - "... the traditional fiduciary concept ... forbids or substantially curtails opportunistic behavior by management .... that the contract notion permits.. Moreover traditional fiduciary doctrine permits "consent" to departure from those principles

only in limited transactions "... courts, aided by commentators, have substantially diluted

fiduciary obligations of corporate management Bratton - " .... why do shareholder rationally vote to approve an

amendment that decrease value to them?" ".... developments begun in the late 1980s in response to takeover are prompting the nexus-of-contracts corporation's subsequent departure ... state legislatures came down emphatically on the side of defending managers.

Corporation as product of Roe

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

4

politics managers seek protection

from institutional

shareholder control banks, mutual funds,

pension funds

systematically weakened

"Disperse individuals would hold stock ... Institutions would neither hold nor vote big blocks or stock. Banks held none for their own account. Insurers rarely held stock.. Mutual funds and pensions have only recently become an important

economic phenomenon. " ... contractarians [and regulators] tend to look at state corporate law -- particularly Delaware's -- to find how law

governs the relationship between shareholder and managers. "Politics and the organization of financial intermediaries cannot be left out of the equation. ... American law and politics

deliberately diminished the power of financial institutions "The Darwinian survival of the fittest in law and economics fails to explain some important phenomenon -- [chaos, suited for

environment at time, path dependence] "We developed high-quality securities markets which allowed firms to raise capital in a national market, to remedy the absence of truly national financial institutions. ... Weak

intermediaries ... led to strong managers. " .... although Germany and Japan started with relatively strong intermediaries, they developed comparatively weak boards."

C. The Dynamics of Shareholder Voting

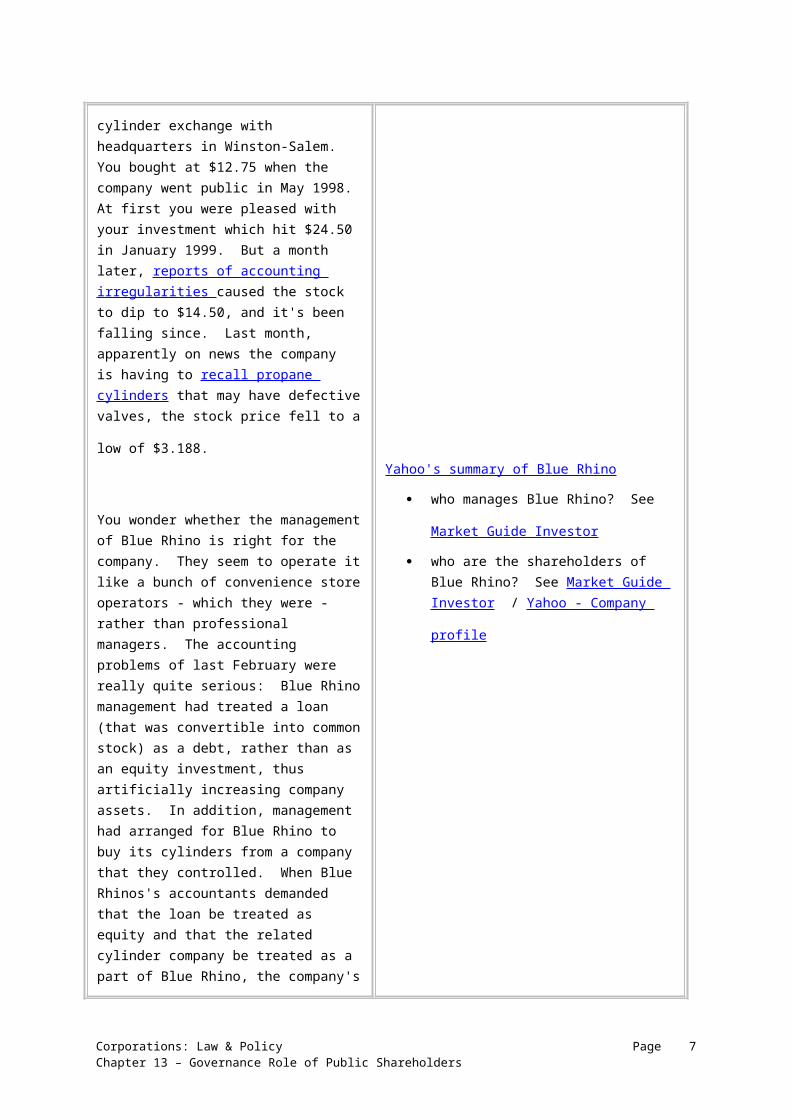

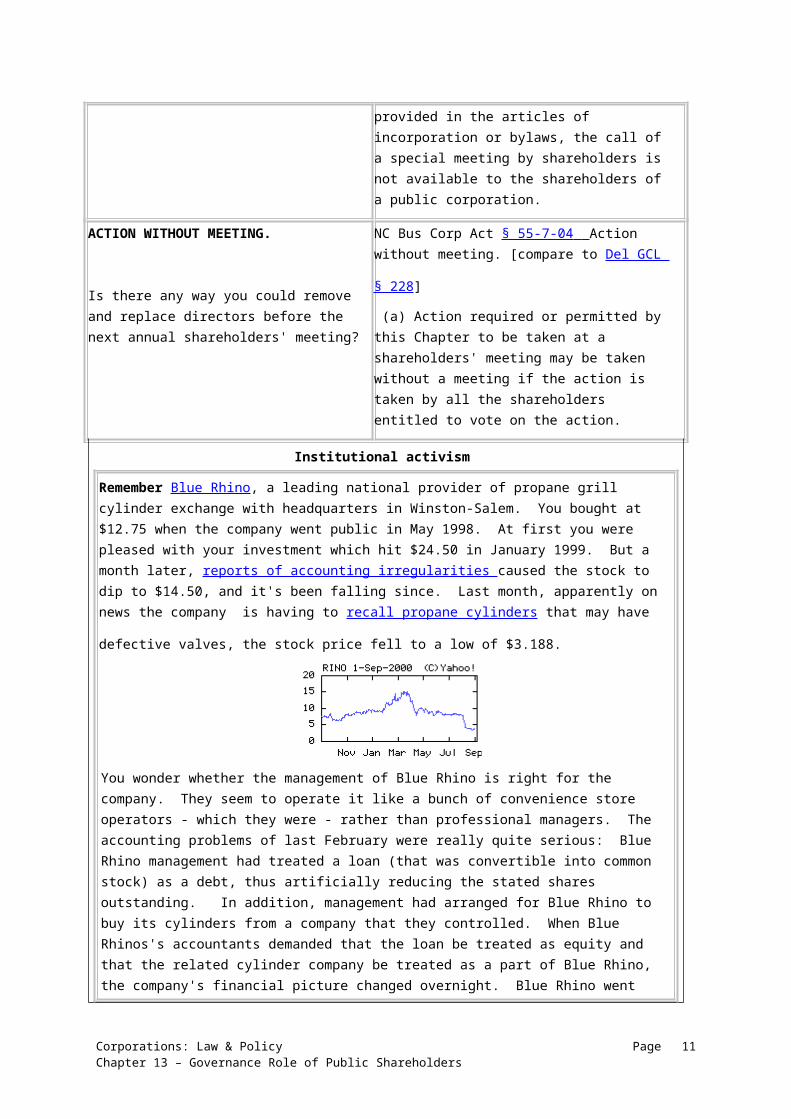

Impediments to "shareholder democracy" Some background. You own stock in Blue Rhino, a leading national provider of propane grill cylinder exchange with headquarters in Winston-Salem. You bought at $12.75 when the company went public in May 1998. At first you were pleased with your investment which hit $24.50 in January 1999. But a month later, reports of accounting irregularities caused the stock to dip to $14.50, and it's been falling since. Last month, apparently on news the company is having to recall propane cylinders that may have defective valves, the stock price fell to a

low of $3.188.

You would like to organize fellow shareholders to replace current management. A lot if information about U.S. companies is available on the Internet. For example, check Yahoo's summary

of Blue Rhino who manages Blue Rhino? See Market

Guide Investor who are the shareholders of Blue Rhino?

See Market Guide Investor / Yahoo -

Company profile

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

5

You wonder whether the management of Blue Rhino is right for the company. They seem to operate it like a bunch of convenience store operators - which they were - rather than professional managers. The accounting problems of last February were really quite serious: Blue Rhino management had treated a loan (that was convertible into common stock) as a debt, rather than as an equity investment, thus artificially increasing company assets. In addition, management had arranged for Blue Rhino to buy its cylinders from a company that they controlled. When Blue Rhinos's accountants demanded that the loan be treated as equity and that the related cylinder company be treated as a part of Blue Rhino, the company's financial picture changed overnight. Blue Rhino went from reporting $442,000 in positive earnings to $70,000 in

losses. The recall has not helped.

Organizing shareholder revolt. Assume you own 10,000 shares of Blue Rhino, worth about $30,000 and representing 0.108% of the total shares outstanding. Assume further that Blue Rhino's stock might double in price if professional management

were installed. Is it worth the trouble for you to work

toward replacing management? How much should you willing to

spend on this effort? Do the math. What are your alternatives?

Traditional view of passive shareholders

[Apple lambastes IBM in "best

commercial" ever]

Prisoner's dilemma You have been arrested, along with somebody said to be your partner in crime. The police take you to an interrogation room and lay out your options.

If you confess (and the other person does not) -- you will be sentenced to 2

years in prison. If you confess (and the other person does too) -- you will both be sentenced

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

6

to 6 years. If you do not confess (and the other person does) -- you will be sentenced

to 10 years. If you do not confess (and the other person does not either) -- you know

that you're both off!

You cannot cooperate with the other person. What do you do?

YOUR MISSION: KICK OUT THE BOARD! BOARD COMPOSITION. You consider the composition of the Blue Rhino board. How long will it take you to replace a majority of the board under a system of classified voting? Why would shareholders buy stock in a company with a staggered board?

How many any directors are on the Blue Rhino board? See Blue Rhino's articles of incorporation [Seventh - 1] and Bylaws

[Article II - Board of Directors] . How are they elected? What is the

meaning of a "classified board"? How does this affect your plans to replace the board? See Blue Rhino's articles of

incorporation [Seventh - 2] Who are the current directors? Who are

outside directors and who are inside directors? Look at company's 1999 Annual Report. / 1999 Proxy Statement [Def 14A

- Board of Directors]

SHAREHOLDERS' MEETING. Consider replacing the board. When does the company have its annual shareholders' meeting? See Blue Rhino bylaws [Article I - Stockholders Meetings].

According to Delaware law, when must the company hold its next annual shareholders' meeting? See Del GCL § 211. Blue Rhino - 1999 Proxy Statement. What if Blue Rhino were incorporated in North Carolina?

NC Bus Corp Act § 55-7-01 Annual meeting.

[Compare Del GCL § 211] (a) A corporation shall hold a meeting of shareholders annually at a time stated in or fixed in

accordance with the bylaws.

NC Bus Corp Act § 55-7-03 Court-ordered

meeting. (a) The superior court ... may, after notice is given to the corporation, summarily order a

meeting to be held: (1) On application of any shareholder if an annual meeting of the shareholders was not held within 15 months after the corporation's last annual meeting; or

NC Bus Corp Act § 55-7-02 Special meeting.

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

7

[Compare Del GCL § 211(d)] (a) A corporation shall hold a special meeting of

shareholders: (1) On call of its board of directors or the person or persons authorized to do so by the articles of

incorporation or bylaws; or (2) Within 30 days after the holders of at least ten percent (10%) of all the votes entitled to be cast on any issue proposed to be considered at the proposed special meeting sign, date, and deliver to the corporation's secretary one or more written demands for the meeting describing the purpose or purposes for which it is to be held; except however that, unless otherwise provided in the articles of incorporation or bylaws, the call of a special meeting by shareholders is not available to the shareholders of a public corporation.

ACTION WITHOUT MEETING. Is there any way you could remove and replace directors before the next annual shareholders' meeting?

NC Bus Corp Act § 55-7-04 Action without

meeting. [compare to Del GCL § 228] (a) Action required or permitted by this Chapter to be taken at a shareholders' meeting may be taken without a meeting if the action is taken by all the shareholders entitled to vote on the action.

Institutional activism

Remember Blue Rhino, a leading national provider of propane grill cylinder exchange with headquarters in Winston-Salem. You bought at $12.75 when the company went public in May 1998. At first you were pleased with your investment which hit $24.50 in January 1999. But a month later, reports of accounting irregularities caused the stock to dip to $14.50, and it's been falling since. Last month, apparently on news the company is having to recall propane cylinders

that may have defective valves, the stock price fell to a low of $3.188.

You wonder whether the management of Blue Rhino is right for the company. They seem to operate it like a bunch of convenience store operators - which they were - rather than professional managers. The accounting problems of last February were really quite serious: Blue Rhino management had treated a loan (that was convertible into common stock) as a debt, thus artificially reducing the stated shares outstanding. In addition, management had arranged for Blue Rhino to buy its cylinders from a company that they controlled. When Blue Rhinos's

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

8

accountants demanded that the loan be treated as equity and that the related cylinder company be treated as a part of Blue Rhino, the company's financial picture changed overnight. Blue Rhino went from reporting $442,000 in positive earnings to $70,000 in losses. The recall has not

helped. Assume that you are Safeco Asset Management (a mutual fund group in Seattle, Washington) which owns 771,200 shares of Blue Rhino, worth about $6.2 million and representing 8.37% of Blue Rhino's stock. If new management would double the price of Blue Rhino, is it worth the effort? How much should Safeco be willing to spend on a shareholder insurgency? Do the math. What are Safeco's alternatives? Consider the ownership structure of a typical U.S. public

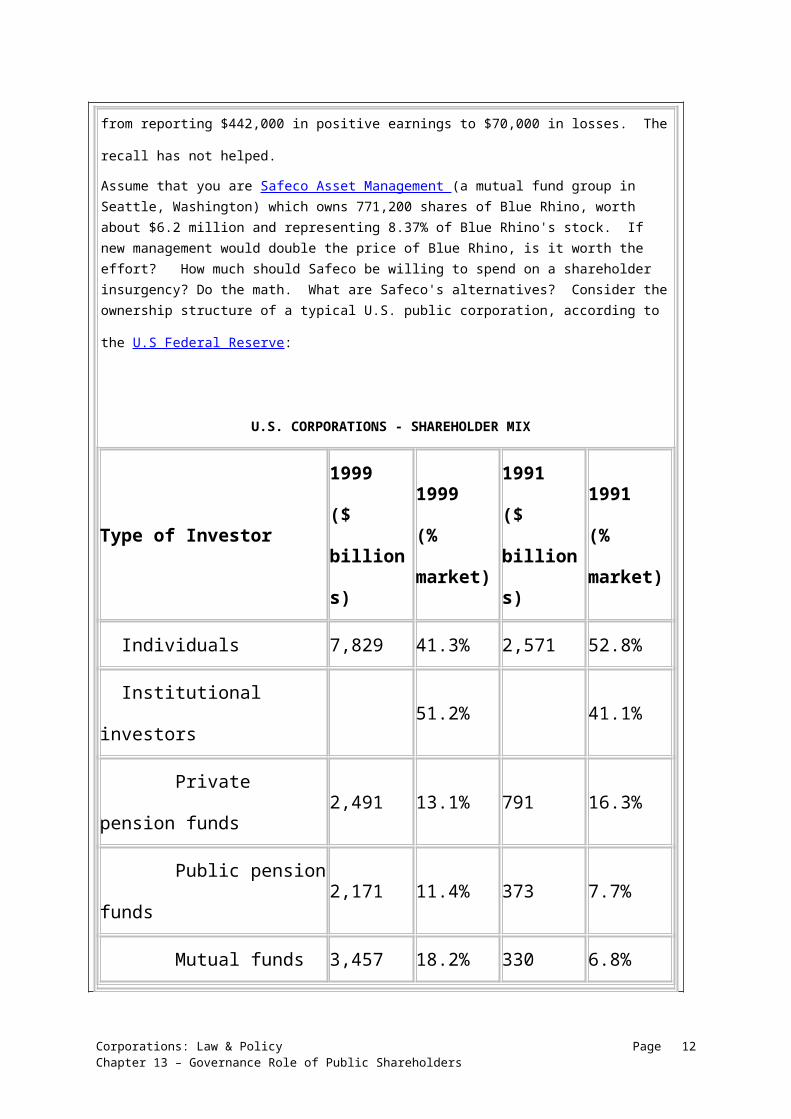

corporation, according to the U.S Federal Reserve:

U.S. CORPORATIONS - SHAREHOLDER MIX

Type of Investor1999 ($ billions)

1999 (% market)

1991 ($ billions)

1991 (% market)

Individuals 7,829 41.3% 2,571 52.8% Institutional investors 51.2% 41.1% Private pension funds 2,491 13.1% 791 16.3% Public pension funds 2,171 11.4% 373 7.7% Mutual funds 3,457 18.2% 330 6.8% Bank trust departments 358 1.9% 244 5.0% Insurance companies 1,174 6.2% 230 4.7% Foundations 181 1.0% 29 0.6% Foreign investors 1,315 6.9% 299 6.1% Total corporate equities 18,976 100% 4,867 100%

Regulatory impediments

You want to begin to contact other Blue Rhino investors. What if you agree to work together to change the board composition: Any

regulatory requirements? Who will be interested in your agreement to pool your voting resources? Who must you tell? What would be the effect of disclosure?

Securities Exchange Act § 13(d) (1) Any person who, after acquiring directly or indirectly the beneficial ownership of any equity security of a class which is registered pursuant to Section 12 of this title, ... is directly or indirectly the beneficial owner of more than 5 per centum of such class shall, within ten days after such acquisition, send to the issuer of the security at its principal executive office, by registered or certified mail, send to each exchange where the security is traded, and file with the Commission, a statement containing such of the following information, and such additional information, as the Commission may by rules

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

9

and regulations prescribe as necessary or appropriate in the

public interest or for the protection of investors-- (A) The background, and identity, residence, and citizenship of, and the nature of such beneficial ownership by, such person and all other persons by whom or on whose behalf the purchases have been

or are to be effected; (B) the source and amount of the funds or other consideration used or to be used in making the

purchases, ... (C) if the purpose of the purchases or prospective purchases is to acquire control of the business of the issuer of the securities, any plans or proposals which such persons may have to liquidate such issuer, to sell its assets to or merge it with any other persons, or to make any other major change in its

business or corporate structure; (D) the number of shares of such security which are beneficially owned, and the number of shares concerning which there is a right to acquire, directly or indirectly, by (i) such person, and (ii) by each associate of such person, giving the background, identity, residence and citizenship of each such

associate; and (E) information as to any contracts, arrangements,

or understandings with any person with respect to

any securities of the issuer, ... (2) When two or more persons act as a partnership, limited partnership, syndicate, or other group for the purpose of acquiring, holding, or disposing of securities of an issuer, such syndicate or group shall be deemed a "person" for the purposes of this subsection.

What if you and your group hold together more than 10% of Blue Rhino's stock and you work together to vote out the current board? If you fail, could you then sell your stock? What would be the

effect of selling your stock? What if your group puts some of your representatives on the board?

Securities Exchange Act § 16(b) [Any] profit realized by a [director, officer or 10% shareholder of a reporting company] from any purchase and sale, or any sale and purchase, of any equity security of such issuer .... within any period of less than six months, ... shall inure to and be recoverable by the issuer, irrespective of any intention on the part of such beneficial owner, director, or officer in entering into such transaction ... Suit to recover such profit may be instituted at law or in equity in any court of competent jurisdiction by the issuer, or by the owner of

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

10

any security of the issuer in the name and in behalf of the

issuer ...

Rule 16a-1 -- Definition of Terms Terms defined in this rule shall apply solely to section 16 of the Act and the rules thereunder. These terms shall not be limited to section 16(a) of the Act but also shall apply to all

other subsections under section 16 of the Act. (a) The term beneficial owner shall have the

following applications: (1) Solely for purposes of determining whether a person is a beneficial owner of more than ten percent of any class of equity securities registered pursuant to section 12 of the Act, the term "beneficial owner" shall mean any person who is deemed a beneficial owner pursuant to section 13(d) of the Act and the rules thereunder ...

D. Federal Regulation of Proxy Solicitations

Assume you are a shareholder in General Electric. You want to participate in the company's corporate governance. How will

this happen? You might want to browse important GE information. GE's website, like that of nearly all public corporations, provides "corporate information" which invariably has links to "investors relations" . For example,

from GE's website you can find links to -- GE's SEC filings GE's annual reports (for the last 5

years) proxy statements (for the 2004

annual meeting Investor presentations

General Electric's annual shareholders' meeting is to be held on the last day of April this year. GE's management is happy with the current directors, and all 16 directors are up for election. Who are they? How will they be elected? see GE 2003

Annual Report - Board of Directors What kinds of people are on the GE board? How

many of each? Outside Execs Former Execs Academics Ex-Govt lawyers bankers Insiders

PROXY REGULATION

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

11

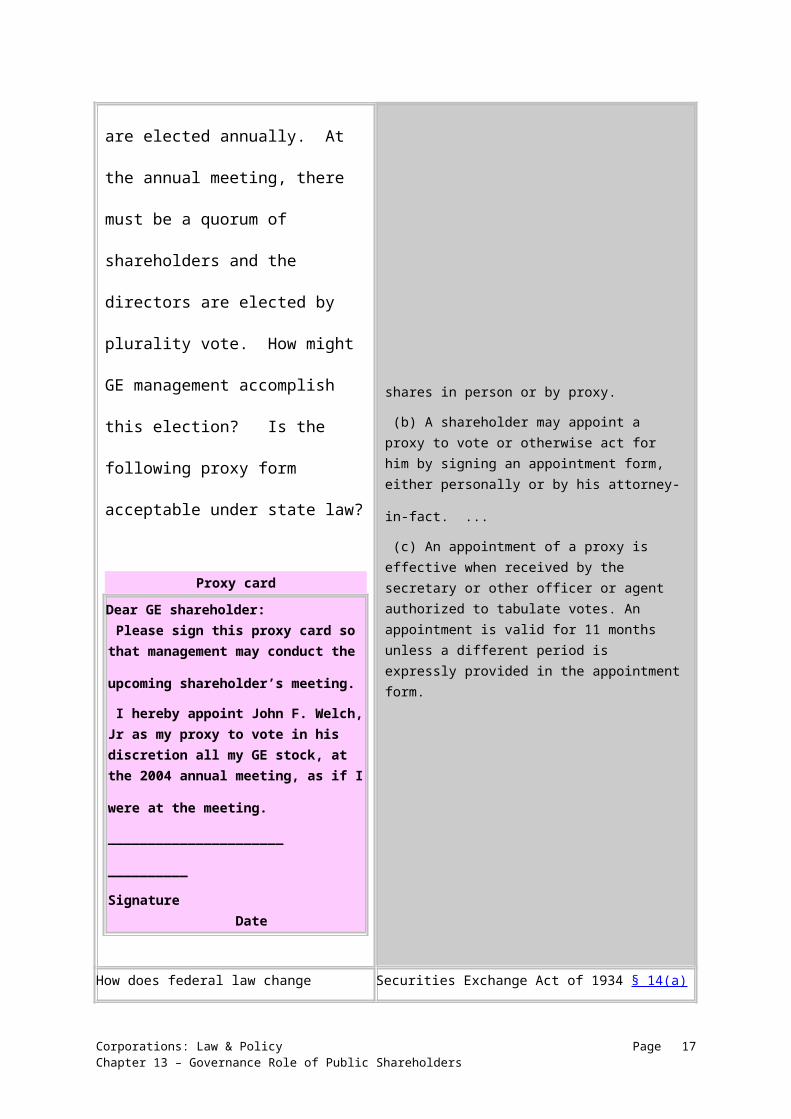

Under state law, directors are elected annually. At the annual meeting, there must be a quorum of shareholders and the directors are elected by plurality vote. How might GE management accomplish this election? Is the following proxy form acceptable under state law?

Proxy card

Dear GE shareholder: Please sign this proxy card so that management may conduct the upcoming shareholder’s meeting. I hereby appoint John F. Welch, Jr as my proxy to vote in his discretion all my GE stock, at the 2004 annual meeting, as if I were at the meeting. ______________________ __________

Signature Date

NC Bus Corp Act § 55-7-22 Proxies. (a) A shareholder may vote his shares in person or

by proxy. (b) A shareholder may appoint a proxy to vote or otherwise act for him by signing an appointment

form, either personally or by his attorney-in-fact. ...

(c) An appointment of a proxy is effective when received by the secretary or other officer or agent authorized to tabulate votes. An appointment is valid for 11 months unless a different period is expressly provided in the appointment form.

How does federal law change this? What are the purposes of Section 14 of the Securities Exchange Act of 1934? What companies are regulated by the federal proxy regime?

Securities Exchange Act of 1934 § 14(a) (a) Solicitation of proxies in violation of rules and regulations. It shall be unlawful for any person, by the use of the mails or by any means or instrumentality of interstate commerce or of any facility of a national securities exchange or otherwise, in contravention of such rules and regulations as the Commission may prescribe as necessary or appropriate in the public interest or for the protection of investors, to solicit or to permit the use of his name to solicit any proxy or consent or authorization in respect of any security (other than an exempted security) registered pursuant to section 12 of this title.

"Reporting company" - See Securities Exchange Act

of 1934 § 12(a) [companies listed on a US stock exchange]

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

12

§ 12(g) [big publicly-traded companies - 500 record Shs + $10 million assets]

Section 14 [synopsis]

It shall be unlawful for any person .. in contravention of such rules and

regulations as the Commission may

prescribe ... to solicit ... any proxy or consent or

authorization in respect of any security (other than an exempted security) of a

reporting company.

SEC REQUIREMENTS

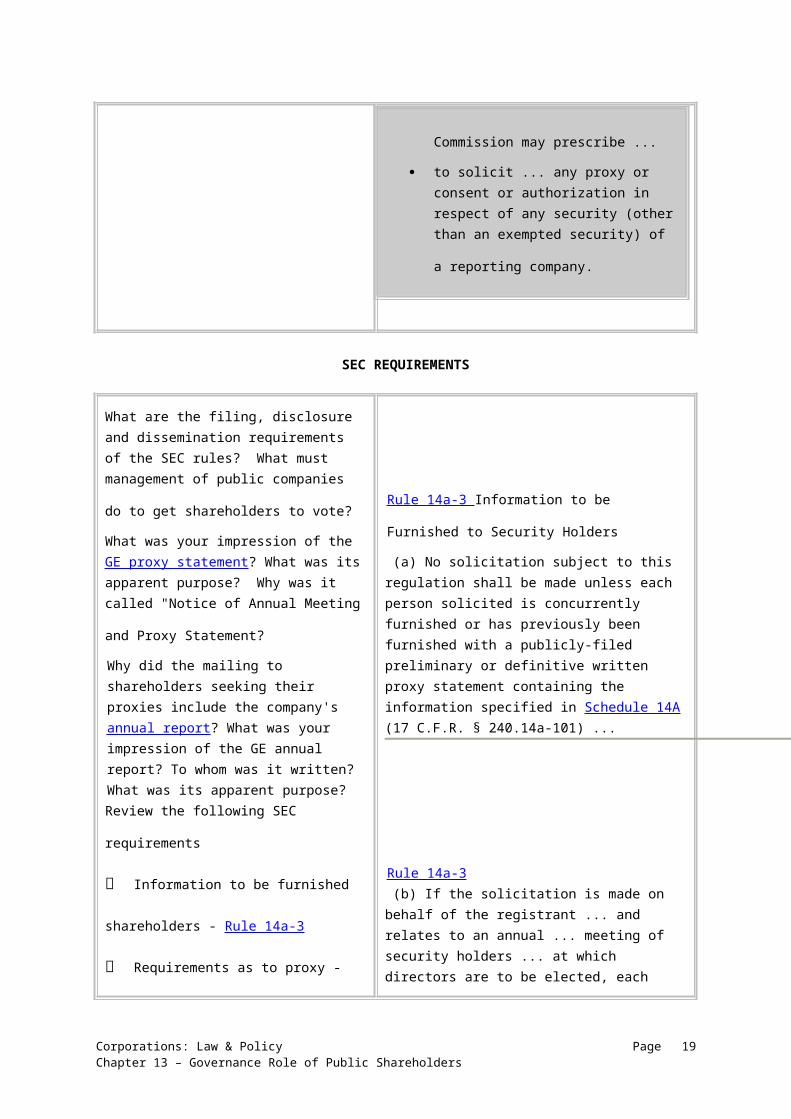

What are the filing, disclosure and dissemination requirements of the SEC rules? What must management of public

companies do to get shareholders to vote? What was your impression of the GE proxy statement? What was its apparent purpose? Why was it called "Notice of

Annual Meeting and Proxy Statement? Why did the mailing to shareholders seeking their proxies include the company's annual report? What was your impression of the GE annual report? To whom was it written? What was its apparent purpose?Review the following SEC requirements Information to be furnished shareholders - Rule 14a-3 Requirements as to proxy - Rule 14a-4 Information to be presented in proxy statement - Rule 14a-5 Filing of proxy statement - Rule 14a-6

Rule 14a-3 Information to be Furnished to Security

Holders (a) No solicitation subject to this regulation shall be made unless each person solicited is concurrently furnished or has previously been furnished with a publicly-filed preliminary or definitive written proxy statement containing the information specified in Schedule 14A (17 C.F.R. § 240.14a-101) ...

Rule 14a-3 (b) If the solicitation is made on behalf of the registrant ... and relates to an annual ... meeting of security holders ... at which directors are to be elected, each proxy statement furnished pursuant to paragraph (a) of this section shall be accompanied or preceded by an annual report to security holders ...

What's wrong with the following Rule 14a-4 Requirements as to proxy.

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

13

proxy card?

Proxy card

Dear GE shareholder: Please sign this proxy card so that management may conduct the upcoming shareholder’s meeting. I hereby appoint John F. Welch, Jr. as my proxy to vote in his discretion all my GE stock, at the 2004 annual meeting, as if I were at the meeting. ______________________ __________

Signature Date

(a) The form of proxy (1) shall indicate in bold-face type whether or not the proxy is solicited on behalf of the registrant's

board of directors ... (2) Shall provide a specifically designated blank

space for dating the proxy card; and (3) Shall identify clearly and impartially each separate matter intended to be acted upon ...(b) (1) Means shall be provided in the form of proxy whereby the person solicited is afforded an opportunity to specify by boxes a choice between approval or disapproval of, or abstention with

respect to each separate matter ... (2) A form of proxy which provides for the election of directors shall set forth the names of persons nominated for election as directors. Such form of proxy shall clearly provide any of the following means for security holders to withhold authority to vote for each nominee: (c) A proxy may confer discretionary authority to

vote with respect to any of the following matters: (1) Matters which the persons making the solicitation do not know, a reasonable time before the solicitation, are to be presented at the meeting, if a specific statement to that effect is made in the proxy statement or form of proxy; (d) No proxy shall confer authority. (1) To vote for the election of any person to any office for which a bona fide nominee is not named

in the proxy statement, (2) To vote at any annual meeting other than the next annual meeting (or any adjournment

thereof) ... (3) To vote with respect to more than one meeting (and any adjournment thereof) or more than one consent solicitation or

Shareholder communications

Long Island Lighting v. Barbash (2d Cir.

1985) Rule 14a-3 (a) No solicitation subject to this regulation shall

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

14

What is a proxy fight? What do the SEC proxy rules require of a dissident who seeks the proxies of other shareholders? What communications are permitted? Isn't this prior restraint forbidden by the 1st

Amendment? LILCO's shareholders (and customers) are steamed. Management is committed to building a nuclear power plant (Shoreham), and the utility took its time to get power back after Hurricane Gloria. Matthews, a holder of 100 shares, started a proxy fight.

What does the SEC require he do? In addition, a "Steering Committee of Citizens to Replace LILCO" formed. Who was on the committee? What did the committee want? What did it do? What was LILCO management's contention? What did the Second Circuit decide? What will LILCO management have to show on remand?

Advertisement in Newsday and N.Y. radio station

More LILCO mismanagement: the utility wants to pass on to ratepayers the needless costs of building the Shoreham nuclear power plant. There's an alternative: sell LILCO to a public power authority. The utility would not have to pay dividends to shareholders. A Long Island Power Authority could buy cheap hydropower, reducing rates to

be made unless each person solicited is concurrently furnished ... with a publicly-filed preliminary or definitive written proxy statement containing the information specified in Schedule 14A ... [Before 1993, the SEC rules had a separate form

for non-management proxy solicitations]

Rule 14a-9 False or misleading statements. (a) No solicitation subject to this regulation shall be made by means of any ... communication, written or oral, containing any statement which ... is false or misleading with respect to any material fact ...

Rule 14a-1 Definitions (l) Solicitation. (1) The terms "solicit" and "solicitation" include: (i) Any request for a proxy whether or not

accompanied by or included in a form of proxy: (ii) Any request to execute or not to execute, or to

revoke, a proxy; or (iii) The furnishing of a form of proxy or other communication to security holders under circumstances reasonably calculated to result in the procurement, withholding or revocation of a proxy.

Second Circuit: The question in every case is whether the challenged communication ... is "reasonably

calculated" to influence the shareholders' votes. Because discovery here was so abbreviated and the district court [was mistaken as to] what constitute a proxy

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

15

LILCO ratepayers by up to 50%. State law guarantees the right to replace LILCO! Citizens to Replace LILCO

solicitation .... the case must be remanded ...

First Amendment concerns:

Judge Winter [of "Race to Top" fame]

... the issues the ad addresses are quintessential matters of public political debate, namely whether a public power authority would provide cheaper electricity than LILCO. .... the ad was published in the middle of an election campaign in which LILCO's future was an issue. ... LILCO's claim raises a constitutional issue of the first magnitude. It asks

nothing less than that a federal court act as a censor I would construe federal proxy regulation as inapplicable, whatever the motives of those who purchase them.

SEC SHAREHOLDER COMMUNICATIONS RULES

What is the effect of the LILCO decision? Would the case have come out the same under the new "shareholder communication" amendments to the proxy

rules?

Rule 14a-2 (b) Rules 14a-3 to 14a-6 ... do not apply to the following: (1) Any solicitation by ... any person who does not ... seek ... the power to act as proxy for a security holder and does not furnish or otherwise request ... a form of revocation, abstention, consent or authorization.

Rule 14a-3 (f) The [proxy statement delivery requirements] shall not apply to a communication made by means of speeches in public forums, press releases, published or broadcast opinions, statements, or advertisements appearing in a broadcast media, newspaper, magazine or other bona fide publication disseminated on a regular

basis, provided that: (1) No form of proxy, consent or authorization or means to execute the same is provided to a security holder in connection

with the communication; and (2) At the time the communication is made, a definitive proxy statement is on file with the Commission pursuant to § 240.14a-6(b).

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

16

HYPOTHETICAL Concerned Shareholders of LILCO places an ad. Is it

OK? "We support the proxy fight of John W. Matthews. It's time to abandon the Shoreham project! We'll vote the green card. So should you!"

Rule 14a-1(l)(2) The terms [solicitation and solicit] do not apply to - A communication by a security holder who does not otherwise engage in a proxy solicitation ... stating how the security holder

intends to vote and the reasons therefor, provided (A) Is made by means of ... advertisements appearing in a broadcast media ....

E. Shareholder proposals

A SHAREHOLDER'S CAUSEYou believe that how we treat animals is a measure of our humanity. See Seven Laws of Noah, statutes of Mass. Bay Colony and all 50 states, ASPCA and Humane Society. You are appalled by forced geese feeding. In France geese are forcibly fed to produce more pate. The bird's body and wings are placed in a metal brace and its neck stretched. Through a funnel inserted 10-12 inches down its throat, a machine pumps corn-based mash into its stomach. An elastic band around the goose's throat prevents regurgitation. Feeding is repeated two to four times a day for 28 days, until the animal's liver has been enlarged six times -- from a normal 1/4 pound to 2

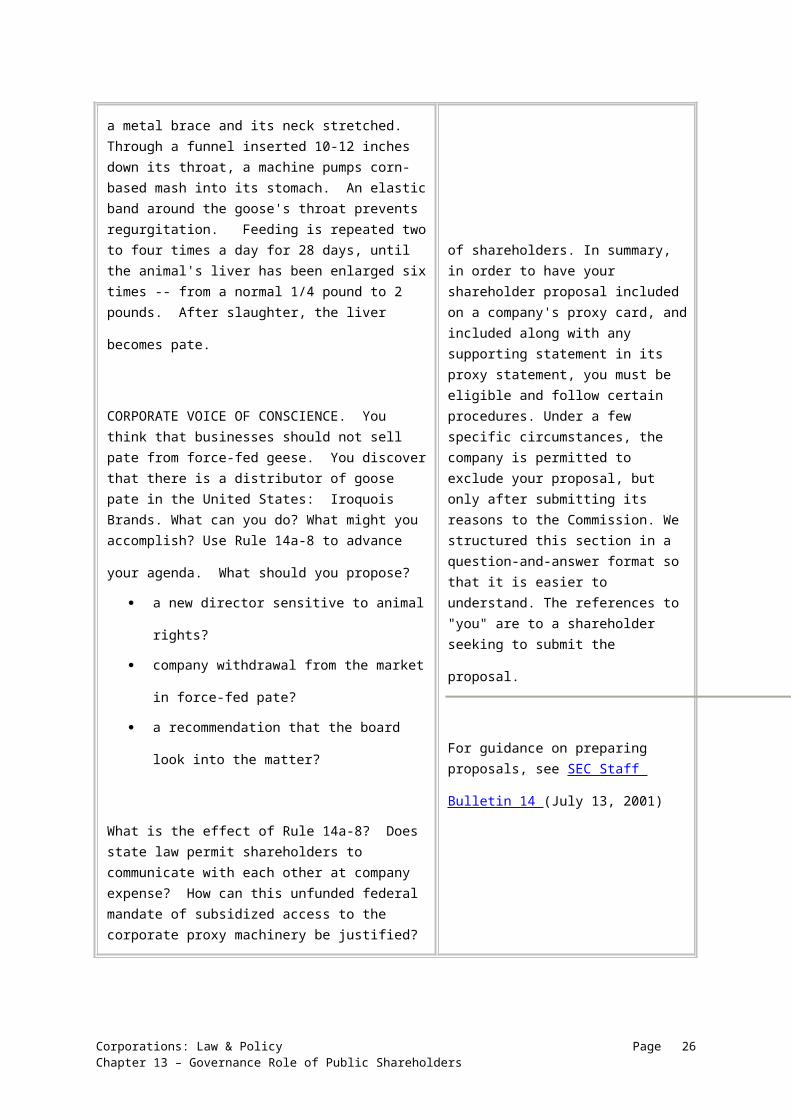

pounds. After slaughter, the liver becomes pate. CORPORATE VOICE OF CONSCIENCE. You think that businesses should not sell pate from force-fed geese. You discover that there is a distributor of goose pate in the United States: Iroquois Brands. What can you do? What might you accomplish? Use Rule 14a-8 to advance your agenda. What should

you propose? a new director sensitive to animal rights? company withdrawal from the market in force-

fed pate? a recommendation that the board look into the

matter?

Rule 14a-8 Shareholder Proposals. This section addresses when a company must include a shareholder's proposal in its proxy statement and identify the proposal in its form of proxy when the company holds an annual or special meeting of shareholders. In summary, in order to have your shareholder proposal included on a company's proxy card, and included along with any supporting statement in its proxy statement, you must be eligible and follow certain procedures. Under a few specific circumstances, the company is permitted to exclude your proposal, but only after submitting its reasons to the Commission. We structured this section in a question-and-answer format so that it is easier to understand. The references to "you" are to a shareholder seeking to submit the

proposal.

For guidance on preparing proposals, see SEC Staff Bulletin 14 (July 13,

2001)

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

17

What is the effect of Rule 14a-8? Does state law permit shareholders to communicate with each other at company expense? How can this unfunded federal mandate of subsidized access to the corporate proxy machinery be justified?

(a) Question 1: What is a proposal?

A shareholder proposal is your recommendation or requirement that the company and/or its board of directors take action, which you intend to present at a meeting of the company's shareholders. Your proposal should state as clearly as possible the course of action that you believe the company should follow. If your proposal is placed on the company's proxy card, the company must also provide in the form of proxy means for shareholders to specify by boxes a choice between approval or disapproval, or abstention. Unless otherwise indicated, the word "proposal" as used in this section refers both to your proposal, and to your corresponding statement in support of your proposal (if any).

(b) Question 2: Who is eligible to submit a proposal, and how do I demonstrate to the company that I am eligible?

(1 ) In order to be eligible to submit a proposal, you must have continuously held at least $2,000 in market value, or I %, of the company's securities entitled to be voted on the proposal at the meeting for at least one year by the date you submit the proposal. You must continue to hold those

securities through the date of the meeting. (2) If you are the registered holder of your securities, which means that your name appears in the company's records as a shareholder, the company can verify your eligibility on its own, although you will still have to provide the company with a written statement that you intend to continue to hold the securities through the date of the meeting of shareholders. However, if like many shareholders you are not a registered holder, the company likely does not know that you are a shareholder, or how many shares you own. In this case, at the time you submit your proposal, you must

prove your eligibility to the company in one of two ways: (i) The first way is to submit to the company a written statement from the "record" holder of your securities (usually a broker or bank) verifying that, at the time you submitted your proposal, you continuously held the securities for at least one year. You must also include your

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

18

own written statement that you intend to continue to hold the securities through the date of the meeting of

shareholders; or (ii) The second way to prove ownership applies only if you have filed a Schedule 1 3D, Schedule 1 3G, Form 3, Form 4 and/or Form 5, or amendments to those documents or updated forms, reflecting your ownership of the shares as of or before the date on which the one-year eligibility period begins. If you have filed one of these documents with the SEC, you may demonstrate your eligibility by submitting to

the company: (A) A copy of the schedule and/or form, and any subsequent amendments reporting a change in your

ownership level; (B) Your written statement that you continuously held the required number of shares for the one-year

period as of the date of the statement; and (C) Your written statement that you intend to continue ownership of the shares through the date of the company's annual or special meeting.

(c) Question 3: How many proposals may I submit?

Each shareholder may submit no more than one proposal to a company for a particular shareholders' meeting.

(d) Question 4: How long can my proposal be?

The proposal, including any accompanying supporting

statement, may not exceed 500 words.

Templeton Dragon Fund, (June 15, 1998)1998 SEC No-Act LEXIS 664; shareholder's supporting statement indicated that the proponent was limited by federal law to 500 words and that readers should go the proponent's Web site for more information. The SEC staff permitted the company to exclude the reference to the proponent's web site because (1) this undercuts the 500 word limitation and (2) the proponent is able to continually change the contents of its web site.

(e) Question 5: What is the deadline for submitting a proposal?

( 1) If you are submitting your proposal for the company's annual meeting, you can in most cases find the deadline in last year's proxy statement. However, if the company did not

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

19

hold an annual meeting last year, or has changed the date of its meeting for this year more than 30 days from last year's meeting, you can usually find the deadline in one of the company's quarterly reports on Form 10-Q or 10-QSB, or in shareholder reports of investment companies under § 270.30d- 1 of this chapter of the Investment Company Act of 1940. In order to avoid controversy, shareholders should submit their proposals by means, including electronic

means, that permit them to prove the date of delivery. (2) The deadline is calculated in the following manner if the proposal is submitted for a regularly scheduled annual meeting. The proposal must be received at the company's principal executive officers not less than 120 calendar days before the date of the company's proxy statement released to shareholders in connection with the previous year's annual meeting. However, if the company did not hold an annual meeting the previous year, or if the date of this year's annual meeting has been changed by more than 30 days from the date of the previous year's meeting, then the deadline is a reasonable time before the company begins to print and mail its proxy materials.

Lovenheim v. Iroquois Brands (D. D.C. 1985)

BE IT RESOLVED: that in order to assure that the Corporation is not inadvertently promoting cruelty to animals and does not risk damaging its reputation as a distributor of wholesome foods, the shareholders request that the Directors form a committee to study the methods by which its French supplier produces pate de foie gras, and report to the shareholders its findings, together with its opinion, based on expert consultation, as to whether or not this production method causes undue distress, pain, or suffering to the animals involved and, if so, whether future distribution of this product should be discontinued until a more humane production method is developed.You represent Iroquois Brands' management, fine people who believe in running a company that complies with the law and makes a return for its shareholders. How do you respond to Lovenheim's moralistic tantrum? Does the company have to include it in its proxy statement? Why

D.C. District Court: ... it seems clear based on the history of the rule that the meaning of "significantly related" is not

limited to economic significance ... ... in light of the ethical and social significance of plaintiff's proposal and the fact that it implicates significant levels of sales, plaintiff has shown a likelihood of prevailing on the merits ...

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

20

bother excluding it? What's wrong with the Lovenheim proposal? If you want to exclude it, what do you have to do? What is the SEC's role? How does the SEC respond?

See no-action correspondence. If Lovenheim sues, what is the court's role? (What court can he sue in?) What did the federal district court decide?

(f) Question 6: What if I fail to follow one of the eligibility or procedural requirements explained in answers to Questions 1 through 4 of this section?

Rule 14a-8 Shareholder Proposals. (1) The company may exclude your proposal, but only after it has notified you of the problem, and you have failed adequately to correct it. Within 14 calendar days of receiving your proposal, the company must notify you in writing of any procedural or eligibility deficiencies, as well as of the time frame for your response. Your response must be postmarked, or transmitted electronically, no later than 14 days from the date you received the company's notification. A company need not provide you such notice of a deficiency if the deficiency cannot be remedied, such as if you fail to submit a proposal by the company's properly determined deadline. If the company intends to exclude the proposal, it will later have to make a submission under Rule 14a-8 and provide you with a copy under Question

10 below, Rule 14a-8(j). (2) If you fail in your promise to hold the required number of securities through the date of the meeting of shareholders, then the company will be permitted to exclude all of your proposals from its proxy materials for any meeting held in the following two calendar years.

(i) Question 9: If I have complied with the procedural requirements, on what other bases may a company rely to exclude my proposal?

(1) Improper under state law: If the proposal is not a proper subject for action by shareholders under the laws

of the jurisdiction of the company's organization; Note to paragraph (i)(l): Depending on the subject matter, some proposals are not considered proper under state law if they would be binding on the company if approved by shareholders. In our experience, most proposals that are cast as recommendations or requests that the board of directors take specified action are proper under state law. Accordingly, we will assume that a proposal drafted as a recommendation or suggestion

is proper unless the company demonstrates otherwise.

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

21

(5) Relevance: If the proposal relates to operations which account for less than 5 percent of the company's total assets at the end of its most recent fiscal year, and for less than 5 percent of its net earnings and gross sales for its most recent fiscal year, and is not otherwise

significantly related to the company's business; (7) Management functions: If the proposal deals with a matter relating to the company's ordinary business operations;

SEC Review of Shareholder Proposals How do SEC staff and federal judge have the gall to say what SHs should and shouldn't hear? How do shareholders use Rule 14a-8? What has been the SEC response?

Proposals "excluded" by management

2001-02Type of proposal

Governance1981-821991-

92 26.5% 35.4% 47.3%

Operational 44.6% 30.2% 33.1%

Social/political 28.9% 34.4% 19.6%

TOTAL 100 % 100 % 100 %

Governance proposals: structure and composition of board, poison pills, share issuances Operational: executive compensation, production/business matters, company communications Social/political: environmental, political, military, labor Proposals found "includable" by SEC

Type of proposal 1981-82 1991-92 2001-02

Governance 18.2% 41.2% 55.7%

Operational 18.9% 3.4% 49.0%

Social/political 37.5% 18.2% 41.4%

AVERAGE 24.1 % 21.9% 48.7%

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

22

Research note: Search Lexis SEC no-

action correspondence o [Lexis search] o [Securities topical

index] o [SEC no-action

database] Search Westlaw SEC no-

action correspondence [Westlaw search]

Online voting For an example of proxy voting online, including a proposal that pension fund (CREF), disclose how it votes

on social responsibility proposals: CREF's proxy statement Internet voting service ID: 29088184385904 SEC rulemaking Curtis C. Verschoor

Legal effect of no-action letter What is a "no-action" letter? What is its legal effect? Are the parties bound? Are courts bound by them as statements of regulatory policy?

Wal-Mart District Court: No-action letters can provide insight into the meaning of [SEC rules] because they address specific issues and build upon the SEC's "vast experience of daily contact

with the practical working of this rule. "... ad hoc nature of these letters means that courts cannot place them on a presidential par with formal rulemaking or adjudication.

Can management respond to a troublesome shareholder proposal simply by making its own similar proposal and claim the company’s proposal preempts the shareholder’s proposal? See Rule 14a-8(i)(9).

The SEC staff has said yes. Gyrodyne Company of America Inc., SEC No-Action Letter, avail. 10/31/05) (accepting argument that company proposal that would permit special meetings to be called upon the request of shareholders owning not less than 30 percent of the stock was “inconsistent with” and thus preempted shareholder proposal requesting that the bylaws be amended to provide that a special meeting of shareholders could be called if requested by shareholders owning at least 15 percent of company’s stock).

Do Mutual Funds Back CEO Pay?Study Finds Firms Failed to Use Voting Power in Favor of Linking Compensation to PerformanceBy JENNIFER LEVITZMarch 28, 2006; Page C1

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

23

Mutual funds usually back executive-pay plans and oppose shareholder attempts to rein them in, according to a broad study of how money managers vote at the annual meetings of companies whose stock they own. In a study scheduled to be released today, two groups that have been critical of executive-pay levels say large mutual-fund companies -- which represent millions of investors through their stock holdings -- have voted in favor of management-pay plans 75.6% of the time. And when shareholder proposals seeking to rein in executive pay are up for vote, funds supported them only 27.6% of the time. The study, sponsored by the American Federation of State, County and Municipal Employees labor union in Washington and Corporate Library, a corporate-governance research group in Portland, Maine, said big fund groups, in general, "are enabling executive-compensation excesses" and "have not used their voting power" to tie pay more closely to company performance. The study reached no conclusions on the reasons behind the votes. One explanation, of course, is that the fund companies believe that executive pay is fair and aligned with shareholder interests. The study sponsors and a number of fund analysts said another explanation is that fund companies and their affiliates are often trying to get corporate management to buy their services -- in investment banking, and retirement-plan administration, for instance -- posing a potential conflict of interest when deciding whether to oppose top executives. The fund group that sided with management most often was Morgan Stanley, which backed company proposals on executive compensation 95% of the time and against shareholder proposals 84.3% of the time. The next most favorable to management was AIM Investments of Houston, which sided with management on compensation 90% of the time, and backed shareholder resolutions in 10% of cases. Morgan Stanley spokesman Chad Peterson said the company hadn't seen the study and wasn't prepared to discuss its findings. He said Morgan Stanley has a policy to vote "solely based on its fiduciary obligations to its clients" and with the "objective of maximizing long-term investment returns." The study also found exceptions to the pattern of support for management-pay plans, suggesting the fund industry is far from monolithic on the issue. It identified a few fund complexes, including Kansas City-based American Century Investment, and educator-retirement group TIAA-CREF of New York, as "pay constrainers" that often voted to curb the compensation of managers. American Century voted against management proposal on pay in 36.7% of cases and was for shareholder proposals 43.1% of the time. TIAA-CREF voted against management proposal 25.6% of the time and was the most likely to support the 362 shareholder resolutions to curb compensation that were examined in the study. It was in favor 53.4% of the time.

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

24

Ward Stouffer, corporate counsel for American Century, said, "We want to vote proxies to maximize shareholder values." A spokesman for TIAA-CREF, which supported shareholders 53% of the time, said it's active on compensation issues, because "executive pay is a window into the boardroom," and excessive pay can indicate that a company's priorities are not aligned with shareholders. The study looked at 37,966 votes cast by mutual funds on compensation questions at 1,603 companies in the year ended June 30. The sponsoring organizations said it was the first to zero in on compensation proposals since the Securities and Exchange Commission mandated, beginning in 2004, that mutual funds publicly disclose how they voted in proxies of the shares they owned. At the time, the fund industry was bitterly opposed to the new regulation, saying it could politicize the voting process and also trigger added paperwork. Indeed, also today, Co-Op America, a Washington nonprofit, is expected to deliver more than 35,000 petitions to Fidelity Investments, American Funds, and Vanguard Group after a study by Ceres, a coalition of investor groups, showed that big shareholders failed to vote on global-warming resolutions filed last year. The study's authors acknowledge that the study leaves out some big mutual-fund companies. The study included 18 of the 25 largest fund groups, leaving out seven, they said, because the proxy-voting forms filed by the fund companies were in a format that was incompatible with Corporate Library's database. The authors couldn't find a way to electronically extract the votes, and say each filing can be cumbersome, perhaps hundreds of pages long with hundreds of votes. The Corporate Library and union are, as part of today's study, calling for voting records to be presented to the public in a more digestible way. Other fund companies that mostly voted with management on compensation were Dreyfus Corp., AllianceBernstein, and OppenheimerFunds. The companies declined to comment, and referred questions to voting proxy policies posted on their Web sites. AIM's policy statement, typical of the proxies, said the company "believes in supporting the management of companies in which it invests." Federated Investors Inc. bucked management pay proposals 61% of the time. The other fund companies most likely to vote against management on executive compensation were Janus Capital Group and Vanguard Group, the study said. Fidelity Investments, the largest mutual-fund manager, came up as "the absolute worst," the study said, in supporting shareholder resolutions, voting for only 2% of them. Fidelity spokesman Vincent Loporchio said the company analyzes all shareholder proposals, but prefers to vote with its feet, by selling shares if it's unhappy with a company.

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

25

However, Boston-based Fidelity was "fairly aggressive" in another respect, the study found, voting against 32% of management's compensation proposals. Fidelity was one of only three mutual-fund companies -- along with Federated and Putnam Investments -- to vote against management's long-term equity compensation proposal in 2005 at Home Depot Inc., where CEO Robert Nardelli earned $27 million-plus last year while the company's stock lagged behind rival Lowe's Cos. Nell Minow of Corporate Library said voting records can point to significant philosophical differences between mutual-fund companies, and can indicate to investors "which mutual funds are truly committed to shareholder value." Don Phillips, managing director of the Chicago research firm, Morningstar Inc., said the study supports a thesis that financial-services companies' desire to solicit business from corporations is influencing votes. "At the end of the day, most asset managers are reluctant to pick fights with management because these big corporations are the ones who can write big checks to money-management firms for business," he said.

Write to Jennifer Levitz at [email protected]

Corporations: Law & Policy Page Chapter 13 – Governance Role of Public Shareholders

26