chapter 5 accounting for merchandising operations...

TRANSCRIPT

5-1

CHAPTER 5 Accounting for Merchandising Operations

ASSIGNMENT CLASSIFICATION TABLE

Study Objectives

Questions

Brief Exercises

Exercises

Problems Set A

Problems Set B

1. Describe the differences between a

service company and a merchandising company.

1, 2, 3, 4, 5 1

2. Explain and complete the entries for purchases under a perpetual inventory system.

6, 7 2, 4, 5 1, 3, 4, 5, 6

1, 2, 3, *9. *10

1, 2, 3, *9, *10

3. Explain and complete the entries for sales revenue under a perpetual inventory system.

7, 8, 9 3, 4, 5 2, 3, 4, 5 1, 2, 3, *9, *10

1, 2, 3, *9, *10

4. Explain and perform the steps in the accounting cycle for a merchandising company.

10, 11, 12 6, 7 6, 7 4, 5, *11 4, 5, *11

5. Distinguish between and be able to prepare both a multiple-step and a single-step income statement.

13, 14, 15, 16

8, 9, 10 7, 8, 9, 10 3, 4, 5, 6, 7, *10, *11

3, 4, 5, 6, 7, *10, *11

6. Explain the importance of and be able to calculate gross profit.

17 10, 11 10, 11 8 8

7. Calculate the inventory turnover and days sales in inventory ratios.

18, 19, 20 11 10, 11 8 8

*8. Describe and perform the accounting for sales taxes (Appendix 5A).

*21, *22 *12 *12 *9, *10 *9, *10

*9. Prepare a work sheet for a merchandising company (Appendix 5B).

*23 *13 *13 *11 *11

*Note: All asterisked Questions, Exercises, and Problems relate to material contained in the Appendices to each chapter.

5-2

ASSIGNMENT CHARACTERISTIC TABLE Problem Number

Description

Difficulty Level

Time Allotted (min.)

1A

Journalize and post inventory transactions. Moderate 30-40

2A

Journalize inventory transactions. Moderate 20-30

3A Journalize, post, and prepare partial income statement and balance sheet.

Moderate 60-70

4A Prepare financial statements and closing entries.

Moderate 30-40

5A Prepare financial statements, adjusting and closing entries.

Moderate 40-50

6A Classify the accounts of a merchandising company.

Simple 10-15

7A Prepare correct multiple-step and single-step income statements.

Complex 50-60

8A Calculate inventory ratios and comment.

Moderate 20-25

*9A Journalize inventory transactions with sales tax.

Moderate 40-50

*10A Journalize, post, and prepare trial balance and partial income statement, with sales taxes.

Moderate 70-80

*11A Complete work sheet, financial statements, adjusting and closing entries, and post-closing trial balance.

Moderate 50-60

1B Journalize and post inventory transactions.

Moderate 30-40

2B Journalize inventory transactions.

Moderate 20-30

3B Journalize, post, and prepare partial income statement and balance sheet.

Moderate 60-70

4B Prepare financial statements, adjusting entries, and closing entries.

Moderate 30-40

5B Prepare financial statements, adjusting entries and closing entries.

Moderate 40-50

6B Classify the accounts of a merchandising company.

Simple 10-15

7B Prepare correct multiple-step and single-step income statements.

Complex 50-60

8B Calculate inventory ratios and comment.

Moderate 20-25

*9B Journalize inventory transactions, with sales tax.

Moderate 40-50

*10B Journalize, post, and prepare trial balance and partial income statement, with sales taxes.

Moderate 70-80

*11B Complete work sheet, financial statements, adjusting and closing entries, and post-closing trial balance.

Moderate 50-60

5-3

BLOOM’S TAXONOMY TABLE Correlation Chart between Bloom’s Taxonomy, Study Objectives and End-of-Chapter Material

Study Objective Knowledge Comprehension Application Analysis Synthesis Evaluation 1. Describe the differences

between a service company and a merchandising company.

Q5-1 Q5-2 Q5-3

Q5-4 Q5-5

BE5-1

2. Explain and complete the entries for purchases under a perpetual inventory system.

Q5-6 Q5-7

BE5-2 BE5-4 BE5-5 E5-1 E5-3 E5-4 E5-6 P5-1A P5-2A

P5-3A *P5-9A *P5-10A P5-1B P5-2B P5-3B *P5-9B *P5-10B

E5-5

3. Explain and complete the entries for sales revenue under a perpetual inventory system.

Q5-8 Q5-7 Q5-9

BE5-3 BE5-4 BE5-5 E5-2 E5-3 E5-4 P5-1A P5-2A

P5-3A *P5-9A *P5-10A P5-1B P5-2B P5-3B *P5-9B *P5-10B

E5-5

4. Explain and perform the steps in the accounting cycle for a merchandising company.

Q5-12 Q5-10 Q5-11

BE5-6 BE5-7 E5-6 E5-7 P5-4A

P5-5A *P5-11A P5-4B P5-5B *P5-11B

5. Distinguish between and be able to prepare both a multiple-step and a single-step income statement.

Q5-14 P5-6A P5-6B

Q5-15 Q5-16

Q5-13 BE5-8 BE5-9 BE5-10 E5-7 E5-9 E-10 P5-3A P5-4A P5-5A

P5-7A *P5-10A *P5-11A P5-3B P5-4B P5-5B P5-7B *P5-10B *P5-11B

E5-8

6. Explain the importance of and be able to calculate gross profit.

Q5-17 BE5-10

BE5-11 E5-10

E5-11 P5-8A P5-8B

7. Calculate the inventory turnover and days sales in inventory ratios.

Q5-18 Q5-19 Q5-20

BE5-11 E5-10

E5-11 P5-8A P5-8B

*8. Describe and perform the accounting for sales taxes (Appendix 5A).

*Q5-21 *Q5-22 *BE5-12 *E5-12

*P5-9A *P5-10A *P5-9B *P5-10B

*9. Prepare a work sheet for a merchandising company (Appendix 5B).

*Q5-23 *BE5-13

*E5-13 *P5-11A *P5-10B *P5-11B

Broadening Your Perspective

BYP5-1 BYP 5-2 BYP5-3 BYP5-4 BYP5-5

BYP5-6 BYP5-7

5-4

ANSWERS TO QUESTIONS

1. The components of revenues and expenses differ as follows:

Merchandising

Service

Revenue

Sales

Service Revenue, Fees Earned, Rent Revenue, Interest Revenue, Investment Income, Gains

Other Revenue

Rent Revenue, Interest Revenue, Investment Income, Gains

Expenses Cost of Goods Sold, Operating Expenses

All expenses

Other Expense

Interest Expense, Losses

2. The income measurement process in a merchandising company can

be summarized as follows:

Sales

Revenues

Less

Cost of Goods Sold

Equals

Gross Profit

Less

Operating Expenses

Equals

Net

Income

3. The normal operating cycle for a merchandising company is likely to

be longer than for a service company because inventory must first be purchased and sold, and then the receivables must be collected.

4. Under a perpetual inventory system, inventory quantities and

amounts are updated continually. At any point in time, the Cost of Goods Sold and Inventory accounts represent what has been sold to date, and what remains.

Under a periodic inventory system, temporary accounts are used to accumulate purchases of inventory throughout the period. The cost of goods sold and inventory are determined only at the end of the period (annually for example).

5-5

Questions Chapter 5 (Continued)

5. Computer technology enables perpetual inventory systems to be

used by any company that requires timely information about the quantities of inventory on hand. It is more complex and costly to maintain a perpetual inventory record of costs, so companies with point of sale systems integrated with their inventory systems tend to be larger.

6. The reason for recording the purchase of merchandise for resale in a

separate account is to enable a company to determine its gross profit. This information is useful in setting prices.

7. The letters FOB mean free on board. FOB shipping point means that

the goods are placed free on board the carrier by the seller, and the buyer pays the freight costs. FOB shipping point will result in a debit to the Inventory account by the buyer.

FOB destination means that the goods are placed free on board to the buyer’s place of business, and the seller pays the freight. FOB destination will result in a debit to the Freight Out account by the seller.

8. (a) The primary source documents are:

(1) Cash sales—cash register tapes, (2) Credit sales—sales invoices, and (3) Sales returns and allowances—credit memoranda.

5-6

Questions Chapter 5 (Continued) 8. (b)

Seller Debit Credit Cash sales— Cash............................................... XXX

Sales........................................ XXX

Cost of Goods Sold ...................... XXX Merchandise Inventory.......... XXX

Credit sales— Accounts Receivable.................... XXX

Sales........................................ XXX Cost of Goods Sold ...................... XXX

Merchandise Inventory.......... XXX

Sales returns Sales Returns and Allowances.... XXX & allowances – Accounts Receivable or Cash XXX

Merchandise Inventory................. XXX Cost of Goods Sold................ XXX

Purchaser

Cash purchase— Merchandise Inventory............... XXX Cash........................................ XXX

Credit purchase— Merchandise Inventory............... XXX

Accounts Payable ................. XXX

Purchase returns Cash or Accounts Payable .......... XXX & allowances – Merchandise Inventory ......... XXX 9. Sales returns are not debited directly to the Sales account because

this would not provide information on the cost of the goods returned. This information can be useful in making decisions. Debiting returns directly to sales may also cause problems in comparing sales for different periods.

5-7

Questions Chapter 5 (Continued)

10. Disagree. The steps in the accounting cycle are the same for both a

merchandising company and a service enterprise.

11. A physical count is an important control feature. Using a perpetual inventory system a company knows what should be on hand. Performing a physical counts and checking it to the perpetual records is necessary to detect any errors in record keeping and/or shortages in stock.

12. Of the merchandising accounts, only Merchandise Inventory (ending)

will appear in the post-closing trial balance.

13. Gross profit ....................................................................... $580,000 Less: Net income ............................................................. 0300,000 Operating expenses.......................................................... $280,000 14. (a) The operating activities part of the income statement has three

sections: sales revenues, cost of goods sold, and operating expenses.

(b) The non-operating activities part consists of two sections: other revenues and gains, and other expenses and losses.

15. The functional groupings are selling and administrative. The problem

with functional groupings is that some expenses may relate to both, and have to be allocated between the functions.

16. The single-step income statement differs from the multiple-step

income statement in that (1) all data are classified into two categories: Revenues and expenses; and (2) only one step, subtracting total expenses from total revenues, is required in determining net income (or net loss).

5-8

Questions Chapter 5 (Continued)

17. Sales revenues.......................................................... $100,000 Cost of goods sold ................................................... 70,000 Gross profit ............................................................... 30,000 Operating expenses ................................................. 20,000 Net income ................................................................ $ 10,000 Gross profit margin = $30,000 ÷ $100,000 = 30% Profit margin = $10,000 ÷ $100,000 = 10%

18. Two ratios that help management determine whether or not there is sufficient inventory on hand are Inventory turnover and days sales in inventory

19. Managing inventory is critical to a company’s success. It is often the

largest current asset (inventory) and the largest expense (cost of goods sold) on the income statement. Companies must manage the quantity of inventory on hand to avoid excessive cost and to ensure they can meet demand.

20. An increase in days sales in inventory would be viewed as a

deterioration because it means there is more inventory on hand in relation to sales.

*21. Accounts Receivable.................................................... 1,053

Sales ..................................................................... 900 GST Payable......................................................... 63 PST Payable ......................................................... 90 Cost of Goods Sold ...................................................... 600 Merchandise Inventory ....................................... 600

*22. Office Furniture [$2,000 + (8% x $2,000)] .................... 2,160 GST Recoverable ($2,000 x 7%)................................... 140 Accounts Payable ............................................... 2,300

*23. (a) Merchandise inventory – Trial balance debit column; Adjusted

trial balance debit column; and Balance sheet debit column (b) Cost of goods sold – Trial balance debit column; Adjusted trial

balance debit column; and Income statement debit column

5-9

SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 5-1 (a) Cost of goods sold = $43,500 ($75,000 – $31,500)

Operating expenses = $20,700 ($31,500 – $10,800) (b) Gross profit = $38,000 ($108,000 – $70,000)

Operating expenses = $8,500 ($38,000 – $29,500) (c) Sales = $181,500 ($71,900 + $109,600)

Net income = $70,100 ($109,600 – $39,500) BRIEF EXERCISE 5-2 Rowen Company (a) March 2 Merchandise Inventory ................................. 900,000

Accounts Payable ................................... 900,000 (b) March 6 Accounts Payable ......................................... 130,000

Merchandise Inventory ........................... 130,000 (c) March 31 Accounts Payable ($900,000 – $130,000).... 770,000

Cash ......................................................... 770,000

5-10

BRIEF EXERCISE 5-3 Hunt Company (a) March 2 Accounts Receivable ................................... 900,000

Sales ...................................................... 900,000 Cost of Goods Sold...................................... 600,000

Merchandise Inventory......................... 600,000 (b) March 6 Sales Returns and Allowances ................... 130,000

Accounts Receivable............................ 130,000 Merchandise Inventory ................................ 90,000 Cost of Goods Sold .............................. 90,000 (c) March 31 Cash ($900,000 – $130,000) ......................... 770,000

Accounts Receivable............................ 770,000

BRIEF EXERCISE 5-4 Keo Company

Nov. 12 Merchandise Inventory ............................... 900 Cash ...................................................... 900

Mayo Company

Nov. 12 Cash.............................................................. 900 Sales...................................................... 900

Cost of Goods Sold..................................... 700 Merchandise Inventory........................ 700

5-11

BRIEF EXERCISE 5-5 March 3 Merchandise Inventory (20 X $25) ................. 500 Accounts Payable ................................ 500 March 6 Accounts Payable ........................................... 75 Merchandise Inventory (3 X $25) ........ 75 March 21 Accounts Receivable (15 X $45) .................... 675 Sales ...................................................... 675 Cost of Goods Sold (15 x $25) ....................... 375 Merchandise Inventory ........................ 375 Quantity: 20 – 3 – 15 = 2 units remaining Cost: $500 - $75 - $375 = $50 Proof: 2 units x $25 = $50 BRIEF EXERCISE 5-6 Aug. 31 Cost of Goods Sold (Inventory shrinkage) .. 900

Merchandise Inventory ($98,000 – $97,100) .............................. 900

BRIEF EXERCISE 5-7 July 31 Sales ................................................................. 180,000 Prasad, Capital ..................................... 180,000 Prasad, Capital................................................. 102,000 Sales Returns and Allowances ........... 2,000 Cost of Goods Sold.............................. 100,000 Ending capital balance (not required): $150,000 + $180,000 - $102,000 = $228,000 Merchandise Inventory is a balance sheet (permanent) account and is not closed.

5-12

BRIEF EXERCISE 5-8 HULDA COMPANY Income Statement (Partial) For the Month Ended October 31, 2003 Sales revenues

Sales ($300,000 + $100,000) .............................................. $400,000 Less: Sales returns and allowances ............................... 30,000 Net sales ............................................................................. $370,000

BRIEF EXERCISE 5-9 (1) Multiple-Step Income Statement

Item

Section

a.

Gain on sale of equipment

Other revenues and gains

b. Interest expense Other expenses and losses c.

d. Cost of goods sold Rent revenue

Cost of goods sold Other revenues and gains

(2) Single-Step Income Statement

Item

Section

a.

Gain on sale of equipment

Revenues

b. Interest expense Expenses c.

d. Cost of goods sold Rent revenue

Expenses Revenues

5-13

BRIEF EXERCISE 5-10 (a) Net sales = $485,000 ($500,000 – $15,000) (b) Gross profit = $145,000 ($485,000 – $340,000) (c) Net income = $35,000 ($145,000 - $70,000- $40,000) BRIEF EXERCISE 5-11 (a) Gross profit margin = 45% [($550,000 – $300,000) ÷ $550,000] (b) Inventory turnover = 12 times ($300,000 ÷ $25,000) (c) Days sales in inventory = 30 days (365 ÷ 12) *BRIEF EXERCISE 5-12 Merchandise Inventory................................................... 8,000 Supplies [$1,000 + ($1,000 X 10%)] ............................... 1,100 GST Recoverable [($8,000 + $1,000) X 7%]................... 630 Accounts Payable ................................................... 9,730 *BRIEF EXERCISE 5-13 (a) Cash: Trial balance debit column; Adjusted trial balance debit column;

Balance sheet debit column. (b) Merchandise Inventory: Trial balance debit column; Adjusted trial

balance debit column; Balance sheet debit column. (c) Sales: Trial balance credit column; Adjusted trial balance credit column;

Income statement credit column. (d) Cost of Goods Sold: Trial balance debit column; Adjusted trial balance

debit column; Income statement debit column.

5-14

SOLUTIONS TO EXERCISES EXERCISE 5-1 1. April 5 Merchandise Inventory.................................. 18,000

Accounts Payable ................................... 18,000 2. April 6 Merchandise Inventory.................................. 900

Cash.......................................................... 900 3. April 7 Equipment ...................................................... 26,000

Accounts Payable ................................... 26,000 4. April 8 Accounts Payable .......................................... 3,000

Merchandise Inventory ..................... ..... 3,000 5. May 2 Accounts Payable ($18,000 – $3,000)........... 15,000

Cash.......................................................... 15,000

5-15

EXERCISE 5-2 (a) Pippen Company 1. Dec. 3 Accounts Receivable................................ 400,000

Sales .................................................... 400,000 Cost of Goods Sold .................................. 320,000 Merchandise Inventory. .................... 320,000 2. Dec. 8 Sales Returns and Allowances................ 20,000

Accounts Receivable ......................... 20,000 3. Dec. 13 Cash ($400,000 – $20,000)........................ 380,000

Accounts Receivable ......................... 380,000 (b) Thomas Co. 1. Dec. 3 Merchandise Inventory............................. 400,000

Accounts Payable .............................. 400,000 2. Dec. 8 Accounts Payable ..................................... 20,000

Merchandise Inventory ...................... 20,000 3. Dec. 13 Accounts Payable ..................................... 380,000 Cash..................................................... 380,000

5-16

EXERCISE 5-3 Sept. 6 Merchandise Inventory (60 X $20) ......................... 1,200

Accounts Payable............................................ 1,200

10 Accounts Payable (2 X $20).................................... 40 Merchandise Inventory ................................... 40

12 Accounts Receivable (26 X $30) ............................ 780 Sales ................................................................. 780 Cost of Goods Sold (26 X $20) ............................... 520 Merchandise Inventory ................................... 520

14 Sales Returns and Allowances .............................. 30 Accounts Receivable ...................................... 30 Merchandise Inventory ........................................... 20 Cost of Goods Sold ......................................... 20

20 Accounts Receivable (30 X $30) ............................ 900 Sales ................................................................. 900 Cost of Goods Sold (30 X $20) ............................... 600 Merchandise Inventory ................................... 600

5-17

EXERCISE 5-4 Sept. 2 Merchandise Inventory (90 X $15) ......................... 1,350

Accounts Payable............................................ 1,350

5 Accounts Payable ................................................... 60 Merchandise Inventory ................................... 60

8 Accounts Receivable .............................................. 1,250 Sales (50 x $25)................................................ 1,250

Cost of Goods Sold................................................. 750 Merchandise Inventory (50 x $15) .................. 750

12 Accounts Receivable .............................................. 750 Sales (30 x $25)................................................ 750 Cost of Goods Sold................................................. 450 Merchandise Inventory (30 x $15) .................. 450 20 Merchandise Inventory (15 x $16).......................... 240 Accounts Payable............................................ 240

30 Cost of Goods Sold (Inventory Loss).................... 15* Merchandise Inventory ................................... 15 10 + 90 – 4 – 50 – 30 + 15 = 31 desk sets per records; 30 desk sets per count = 1 missing * Note: We assumed that the missing desk set had a cost of $15. It could also have been assumed to be $16, from the September 20 purchase.

5-18

EXERCISE 5-5 1. Sales Returns and Allowances......................................... 150

Sales............................................................................ 150 2. Supplies .............................................................................. 250

Cash .................................................................................... 250 Accounts Payable ...................................................... 250 Merchandise Inventory .............................................. 250

3. Sales.................................................................................... 50

Merchandise Inventory .............................................. 50 4. Cash .................................................................................... 270

Merchandise Inventory .............................................. 270

5-19

EXERCISE 5-6 (a) Jun. 10 Merchandise Inventory..................................... 5,000

Accounts Payable ..................................... 5,000

11 Merchandise Inventory..................................... 300 Cash............................................................ 300

12 Accounts Payable ............................................. 500 Merchandise Inventory ............................. 500

July 7 Accounts Payable ($5,000 – $500).................. 4,500

Cash............................................................ 4,500

15 Cash .................................................................. 8,500 Sales ........................................................... 8,500

15 Cost of Goods Sold ($5,000 + $300 - $500) .... 4,800 Merchandise Inventory ............................. 4,800

(b) July 31 Sales.................................................................. 8,500 Capital ........................................................ 8,500 31 Capital ............................................................... 4,800 Cost of Goods Sold................................... 4,800

5-20

EXERCISE 5-7 (a)

CECILIE COMPANY Income Statement (Partial) For the Year Ended October 31, 2003

Sales revenues Sales..................................................................................... $900,000 Less: Sales returns and allowances................................. 24,000 Net sales............................................................................... $876,000

Note: Freight Out is a selling expense.

(b) Closing entries: Oct. 31 Sales ........................................................... 900,000

Capital ................................................. 900,000

31 Capital......................................................... 36,000 Sales Returns and Allowances ......... 24,000 Freight Out .......................................... 12,000

5-21

EXERCISE 5-8 Natural

Cosmetics Mattar

Grocery Allied

Wholesalers Sales $90,000 (c) $100,000 $144,000 Less: Sales returns (a) 16,000 6,000 12,000 Net sales 74,000 94,000 (f) 132,000 Less: Cost of goods sold 64,000 (d) 72,000 (g) 108,000 Gross profit 10,000 22,000 24,000 Less: Operating expenses 6,000 (e) 12,000 18,000 Net income (b) $ 4,000 $ 10,000 (h) $ 6,000 (a) Sales.......................................................................... $90,000

*Sales returns ............................................................ (16,000) Net sales ................................................................... $74,000

(b) Gross profit .............................................................. $10,000

Operating expenses................................................. (6,000) *Net income .............................................................. $ 4,000

(c) *Sales ........................................................................ $100,000

Sales returns ............................................................ (6,000) Net sales ................................................................... $ 94,000

(d) Net sales ................................................................... $94,000

*Cost of goods sold ................................................. (72,000) Gross profit .............................................................. $22,000

(e) Gross profit .............................................................. $22,000

*Operating expenses ............................................... (12,000) Net income................................................................ $10,000

(f) Sales.......................................................................... $144,000

Sales returns ............................................................ (12,000) *Net sales.................................................................. $132,000

(g) Net sales ................................................................... $132,000

*Cost of goods sold ................................................. (108,000) Gross profit .............................................................. $ 24,000

(h) Gross profit .............................................................. $24,000 Operating expenses................................................. (18,000) *Net income .............................................................. $ 6,000

5-22

EXERCISE 5-9 (a)

CHEVALIER COMPANY Income Statement For the Year Ended December 31, 2002

Net sales...................................................................... $2,359,000 Cost of goods sold ..................................................... 00,989,000 Gross profit ................................................................. 1,370,000 Operating expenses

Selling expenses................................................. $690,000 Administrative expenses.................................... 0435,000

Total operating expenses ........................... 1,125,000 Income from operations............................................. 245,000 Other revenues and gains

Interest revenue .................................................. $45,000 Other expenses and losses

Interest expense..................................... $70,000 Loss on sale of equipment..................... 10,000 80,000 35,000

Net income .................................................................. $ 210,000 (b) CHEVALIER COMPANY Income Statement For the Year Ended December 31, 2002

Revenues Net sales.............................................................. $2,359,000 Interest revenue.................................................. 0 45,000 Total revenues.............................................. 2,404,000

Expenses Cost of goods sold ............................................. $989,000 Selling expenses ................................................ 690,000 Administrative expenses ................................... 435,000 Interest expense ................................................. 70,000 Loss on sale of equipment ................................ 0010,000 Total expenses ............................................ 2,194,000

Net income .................................................................. $ 210,000

5-23

EXERCISE 5-10 (a) JETFORM CORPORATION Income Statement For the Year Ended April 30, 2000 (in thousands)

Revenues Revenue from products and services................. $94,317 Interest revenue .................................................... 2,868 Gain on sale of assets .......................................... 1,813 Other income......................................................... 295 Total revenues................................................. $ 99,293

Expenses Cost of products and services ............................. $24,426 Sales and marketing expenses ............................ 45,097 General and administrative expenses ................. 26,485 Amortization expense ........................................... 10,300 Income tax expense .............................................. 1,086

Total expenses ................................................ 107,394 Net loss........................................................................... ($ 8,101)

5-24

EXERCISE 5-10 (Continued) (b) JETFORM CORPORATION Income Statement For the Year Ended April 30, 2000 (in thousands) Revenue from products and services....................... $ 94,317 Cost of products and services .................................. 00, 24,426 Gross profit ................................................................. 69,891 Operating expenses

Sales and marketing expenses.......................... $45,097 General and administrative expenses (including amortization expense) .............. 0 36,785

Total operating expenses ........................... 81,882 Loss from operations ................................................. (11,991) Other revenues and gains

Interest revenue.................................................. $2,868 Gain on sale of assets........................................ 1,813 Other income ...................................................... 295

4,976 Other expenses and losses

Income tax expense* ........................................... 1,086 3,890 Net loss......................................................................... ($ 8,101) *Note to Instructor: You may wish to explain that income tax expense is usually presented differently (following an income (or loss) before income taxes caption) in corporate income statements.

5-25

EXERCISE 5-10 (Continued)

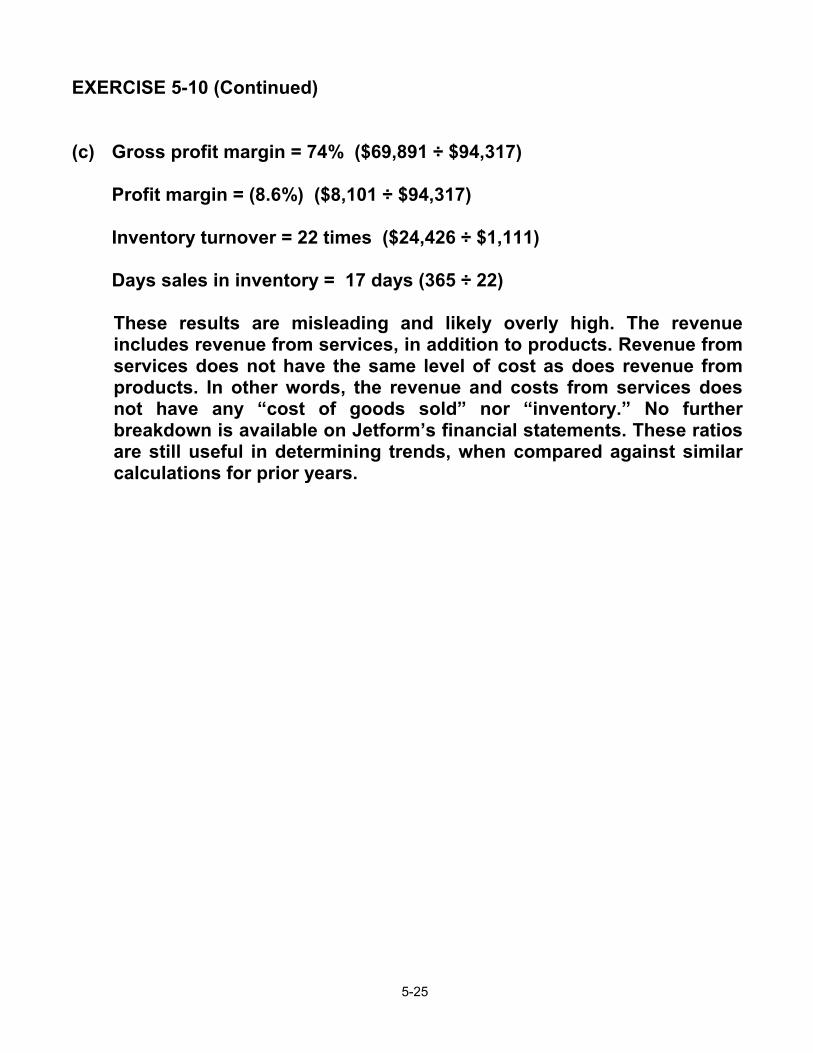

(c) Gross profit margin = 74% ($69,891 ÷ $94,317)

Profit margin = (8.6%) ($8,101 ÷ $94,317) Inventory turnover = 22 times ($24,426 ÷ $1,111) Days sales in inventory = 17 days (365 ÷ 22)

These results are misleading and likely overly high. The revenue includes revenue from services, in addition to products. Revenue from services does not have the same level of cost as does revenue from products. In other words, the revenue and costs from services does not have any “cost of goods sold” nor “inventory.” No further breakdown is available on Jetform’s financial statements. These ratios are still useful in determining trends, when compared against similar calculations for prior years.

5-26

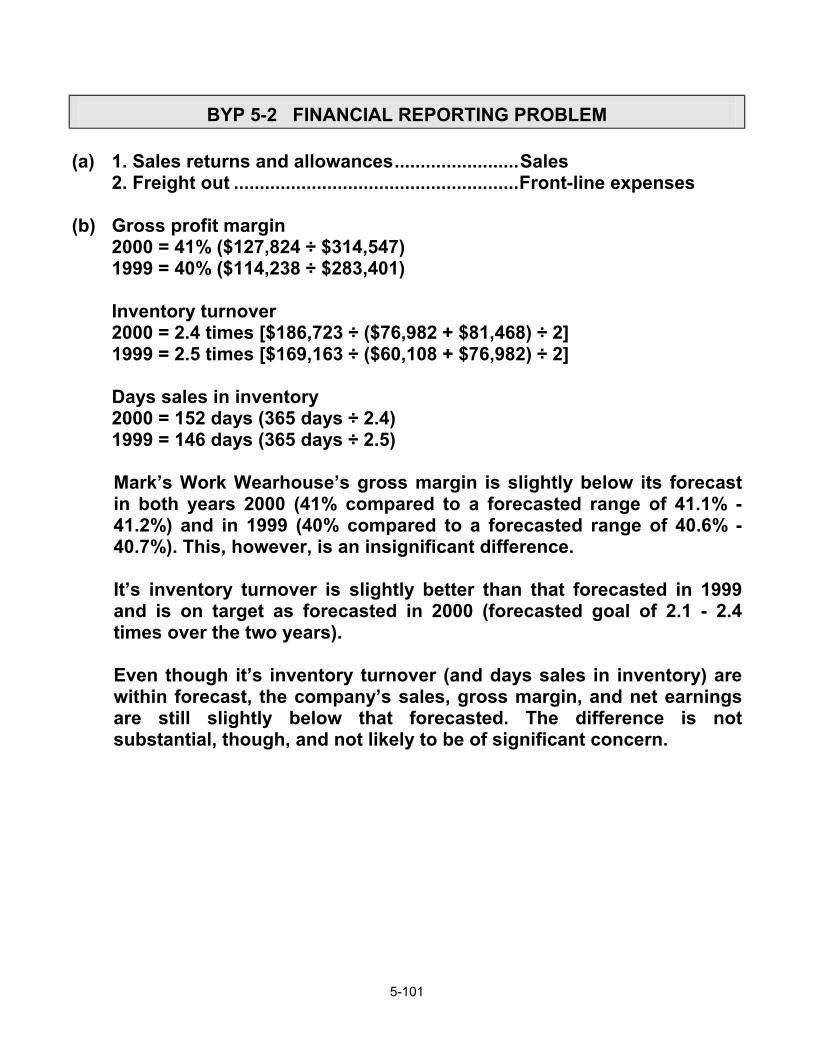

EXERCISE 5-11 Inventory turnover 2000 = 7.3 times [$1,298,606 ÷ ($193,831 + $160,092) ÷ 2] 1999 = 7.5 times [$1,546,723 ÷ ($160,092 + $254,690) ÷ 2] Days sales in inventory 2000 = 50 days (365 ÷ 7.3) 1999 = 49 days (365 ÷ 7.5) Gross profit margin 2000 = 23% [($1,683,142 - $1,298,606) ÷ $1,683,142] 1999 = 21% [($1,960,274 - $1,546,723) ÷ $1,960,274] The gross profit margin has improved, increasing from 21% in 1999 to 23% in 2000. The inventory turnover and days sales in inventory are basically unchanged from one year to the next.

5-27

*EXERCISE 5-12 Sept. 2 Merchandise Inventory (90 X $15) ............... 1,350.00 GST Recoverable ($1,350 x 7%) ................... 94.50

Accounts Payable.................................. 1,444.50

5 Accounts Payable ......................................... 64.20 Merchandise Inventory ......................... 60.00 GST Recoverable................................... 4.20

8 Accounts Receivable .................................... 1,337.50 Sales (50 x $25)...................................... 1250.00 GST Payable ($1,250 x 7%) ................... 87.50

Cost of Goods Sold....................................... 750.00 Merchandise Inventory (50 x $15) ........ 750.00

12 Accounts Receivable .................................... 802.50 Sales (30 x $25)...................................... 750.00 GST Payable ($750 x 7%) ...................... 52.50 Cost of Goods Sold....................................... 450.00 Merchandise Inventory (30 x $15) ........ 450.00 20 Merchandise Inventory (15 x $16)................ 240.00 GST Recoverable ($240 x 7%) ...................... 16.80 Accounts Payable.................................. 256.80 30 Cost of Goods Sold (Inventory Loss).......... 15.00* Merchandise Inventory ......................... 15.00 10 + 90 – 4 – 50 – 30 + 15 = 31 desk sets per records; 30 desk sets per count = 1 missing * Note: We assumed that the missing desk set had a cost of $15. It could also have been assumed to be $16, from the September 20 purchase. There is no GST effect of this loss.

5-28

*EXERCISE 5-13

(a)

Accounts

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Debit

Credit

Debit

Credit

Debit

Credit

Cash Merchandise Inven. Sales Sales Returns Cost of Goods Sold Rent Expense

9,000

80,000

10,000 250,000 42,000

450,000

10,000 250,000 42,000

450,000

9,000

80,000

(b) The accounts appearing in the post-closing trial balance are the balance

sheet accounts of Cash ($9,000) and Merchandise Inventory ($80,000).

5-29

SOLUTIONS TO PROBLEMS

PROBLEM 5-1A

(a) April 5 Merchandise Inventory–Custom Sedans (3 x $24,000)....................................................... 72,000

Accounts Payable ..................................... 72,000 13 Merchandise Inventory–Recreation Vehicles (2 x $28,000)....................................................... 56,000

Accounts Payable ..................................... 56,000

17 Accounts Receivable ........................................ 114,000 Sales (4 x $28,500)..................................... 114,000

Cost of Goods Sold (4 x $24,000) .................... 96,000 Merchandise Inventory–Custom Sedans 96,000 20 Merchandise Inventory–Convertibles (2 x $26,000)....................................................... 52,000

Accounts Payable ..................................... 52,000 22 Accounts Payable ............................................. 26,000

Merchandise Inventory–Convertibles ..... 26,000 24 Accounts Receivable ........................................ 102,000

Sales (3 x $34,000)..................................... 102,000 Cost of Goods Sold (3 x $28,000) .................... 84,000 Merchandise Inventory–Recreation Vehicles 84,000 28 Accounts Receivable ........................................ 31,000

Sales ........................................................... 31,000

Cost of Goods Sold........................................... 26,000 Merchandise Inventory–Convertibles ..... 26,000

5-30

PROBLEM 5-1A (Continued) (b)

Merchandise Inventory –Custom Sedans

Merchandise Inventory –Convertibles

Bal. 96,000 96,000 Bal. 78,000 26,000 72,000 52,000 26,000 72,000 78,000

Merchandise Inventory –Recreation Vehicles

Cost of Goods Sold Bal. 56,000 84,000 96,000

56,000 84,000 28,000 26,000

206,000

5-31

PROBLEM 5-2A

GENERAL JOURNAL Date Account Titles Ref. Debit Credit July 1

Merchandise Inventory (50 x $30) ........... Accounts Payable .............................

120 201

1,500

1,500 3 Accounts Receivable (40 x $50) ..............

Sales................................................... Cost of Goods Sold (40 x $30) ................. Merchandise Inventory .....................

112 401 505 120

2,000

1,200

2,000

1,200 9 Accounts Payable .....................................

Cash ................................................... 201 101

1,500 1,500

12 Cash ...........................................................

Accounts Receivable ........................ 101 112

2,000 2,000

17 Accounts Receivable (30 x $50) ..............

Sales................................................... Cost of Goods Sold (30 x $30) ................. Merchandise Inventory .....................

112 401 505 120

1,500

900

1,500

900 18 Merchandise Inventory ($1,700 + $100) ..

Accounts Payable ............................. Cash ...................................................

120 201 101

1,800 1,700 100

20 Accounts Payable ..................................... Merchandise Inventory .....................

201 120

300 300

21 Cash ...........................................................

Accounts Receivable ........................ 101 112

1,500 1,500

5-32

PROBLEM 5-2A (Continued) Date Account Titles Ref. Debit Credit July 22

Accounts Receivable (40 x $50) .............. Sales................................................... Cost of Goods Sold (40 x $30) ................. Merchandise Inventory .....................

112 401 505 120

2,000

1,200

2,000

1,200

30 Accounts Payable ($1,700 - $300) ........... Cash ...................................................

210 101

1,400 1,400

31 Sales Returns and Allowances................

Accounts Receivable ........................ Merchandise Inventory............................. Cost of Goods Sold ..........................

412 112 120 505

250

150

250

150

5-33

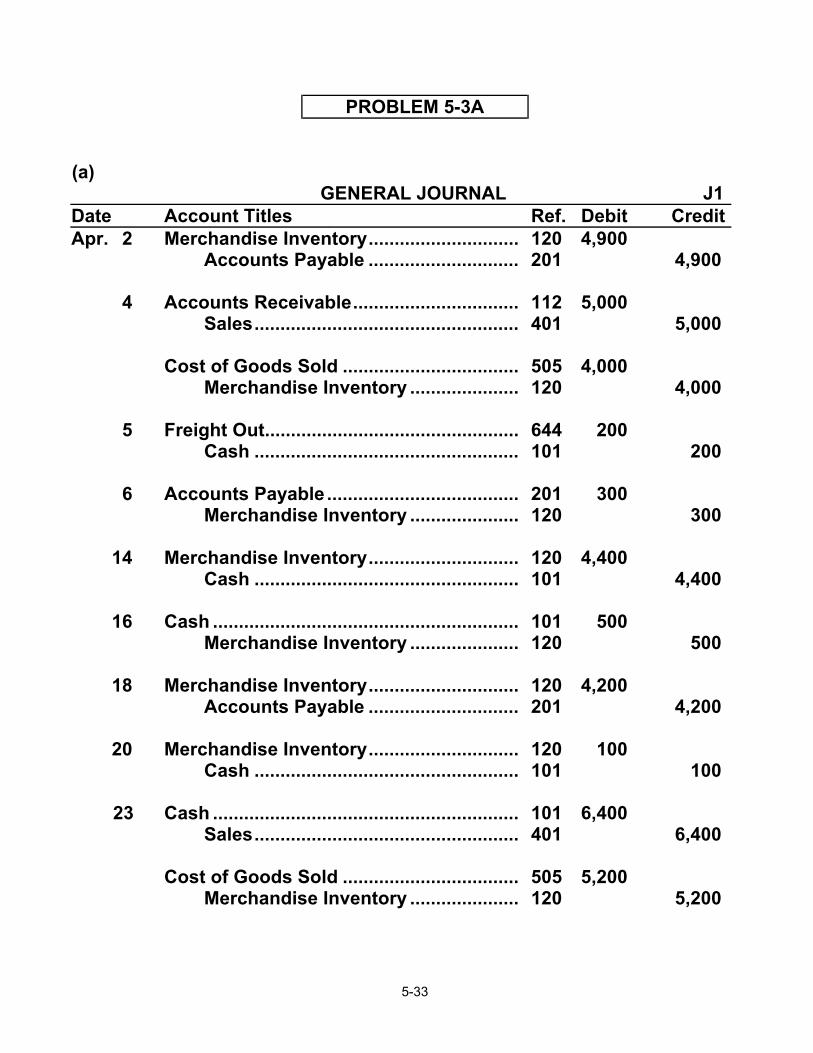

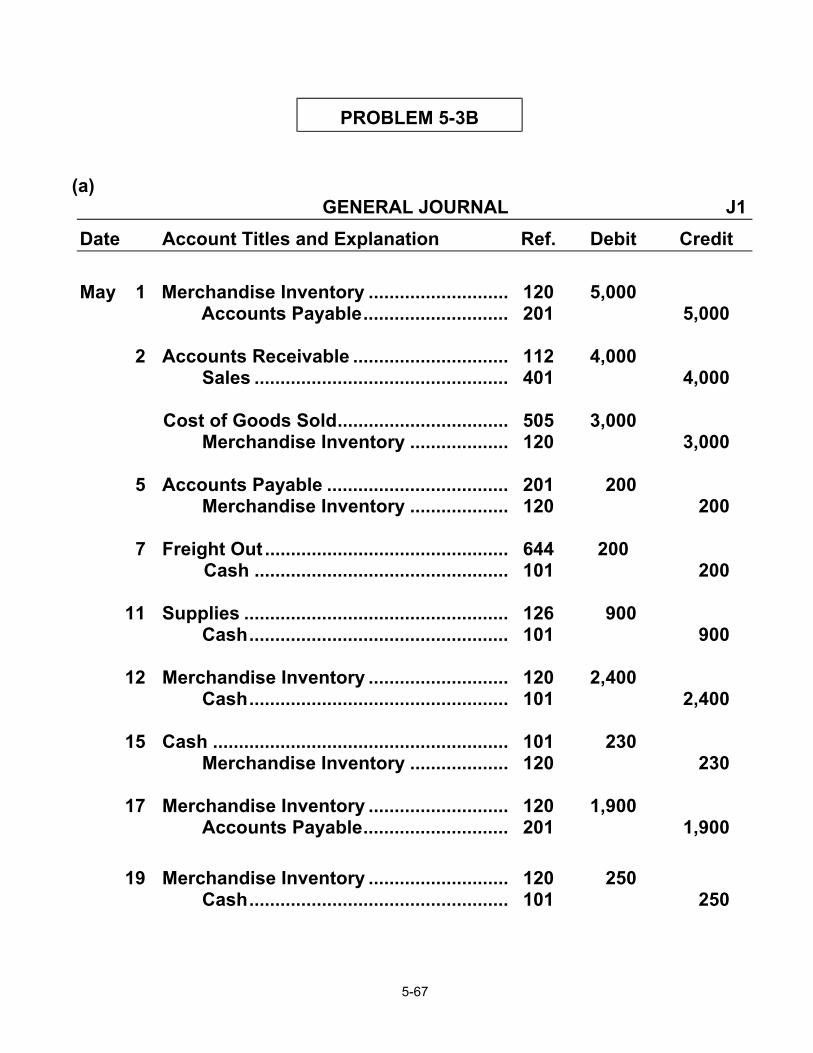

PROBLEM 5-3A

(a)

GENERAL JOURNAL J1 Date Account Titles Ref. Debit Credit Apr. 2 Merchandise Inventory.............................

Accounts Payable ............................. 120 201

4,900 4,900

4 Accounts Receivable................................

Sales................................................... Cost of Goods Sold .................................. Merchandise Inventory .....................

112 401 505 120

5,000

4,000

5,000

4,000 5 Freight Out.................................................

Cash ................................................... 644 101

200 200

6 Accounts Payable .....................................

Merchandise Inventory ..................... 201 120

300 300

14 Merchandise Inventory.............................

Cash ................................................... 120 101

4,400 4,400

16 Cash ...........................................................

Merchandise Inventory ..................... 101 120

500 500

18 Merchandise Inventory.............................

Accounts Payable ............................. 120 201

4,200 4,200

20 Merchandise Inventory.............................

Cash ................................................... 120 101

100 100

23 Cash ...........................................................

Sales................................................... Cost of Goods Sold .................................. Merchandise Inventory .....................

101 401 505 120

6,400

5,200

6,400

5,200

5-34

PROBLEM 5-3A (Continued) (a) (Continued)

J2

Date Account Titles Ref. Debit Credit Apr. 26 Merchandise Inventory .............................

Cash .................................................... 120 101

2,300 2,300

27 Accounts Payable ($4,900 - $300) ............

Cash .................................................... 201 101

4,600 4,600

28 Cash............................................................

Accounts Receivable......................... 101 112

5,000 5,000

29 Sales Returns and Allowances.................

Cash .................................................... Merchandise Inventory ............................. Cost of Goods Sold ...........................

412 101 120 505

90

60

90

60 30 Accounts Receivable ................................

Sales.................................................... Cost of Goods Sold ................................... Merchandise Inventory......................

112 401 505 120

3,700

3,000

3,700

3,000 (b)

Cash No. 101 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 1 5 14 16 20 23 26 27 28 29

Balance

J1 J1 J1 J1 J1 J2 J2 J2 J2

500

6,400

5,000

200 4,400

100

2,300 4,600

90

9,000 8,800 4,400 4,900 4,800

11,200 8,900 4,300 9,300 9,210

5-35

PROBLEM 5-3A (Continued) (b) (Continued)

Accounts Receivable No. 112 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 4 28 30

J1 J2 J2

5,000

3,700

5,000

5,000

0 3,700

Merchandise Inventory No. 120 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 2 4 6 14 16 18 20 23 26 29 30

J1 J1 J1 J1 J1 J1 J1 J1 J2 J2 J2

4,900

4,400

4,200 100

2,300

60

4,000 300

500

5,200

3,000

4,900

900 600

5,000 4,500 8,700 8,800 3,600 5,900 5,960 2,960

Accounts Payable No. 201 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 2 6 18 27

J1 J1 J1 J2

300

4,600

4,900

4,200

4,900 4,600 8,800 4,200

5-36

PROBLEM 5-3A (Continued) (b) (Continued)

M. Nisson, Capital No. 301 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 1

Balance

9,000

Sales No. 401 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 4 23 30

J1 J1 J2

5,000 6,400

3,700

5,000

11,400 15,100

Sales Returns and Allowances No. 412 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 29

J2

90

90

Cost of Goods Sold No. 505 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 4 23 29 30

J1 J1 J2 J2

4,000 5,200

3,000

60

4,000 9,200 9,140

12,140 Freight Out No. 644 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 5

J1

200

200

5-37

PROBLEM 5-3A (Continued) (c) NISSON DISTRIBUTING COMPANY Income Statement (Partial) For the Month Ended April 30, 2003 Sales revenues Sales................................................................................ $15,100 Less: Sales returns and allowances............................ 90 Net sales.......................................................................... 15,010 Cost of goods sold ................................................................ 12,140 Gross profit ............................................................................ $ 2,870 (d) NISSON DISTRIBUTING COMPANY Balance Sheet (Partial) April 30, 2003 Assets Current assets Cash................................................................................. $ 9,210 Accounts receivable....................................................... 3,700 Merchandise inventory .................................................. 2,960 Total current assets ............................................... 15,870

5-38

PROBLEM 5-4A

Adjusting entries—not required: Dec. 31 Insurance Expense .................................................. 800

Prepaid Insurance............................................. 800 Amortization Expense ............................................. 3,000 Accumulated Amortization—Store Equipment 3,000 Rent Expense ........................................................... 500 Rent Payable .................................................... 500 (a) WORLD ENTERPRISES Income Statement For the Year Ended December 31, 2002

Sales revenues Sales ......................................................................... $238,500 Less: Sales returns and allowances ..................... 4 4,600 Net sales ................................................................... 233,900

Cost of goods sold .......................................................... 177,000 Gross profit .................................................................... 56,900 Operating expenses

Salaries expense ..................................... $31,600 Amortization expense ............................. 3,000 Rent expense ($6,100 + $500)................. 6,600 Insurance expense ................................. 000800 Total operating expenses.................................. .. 42,000

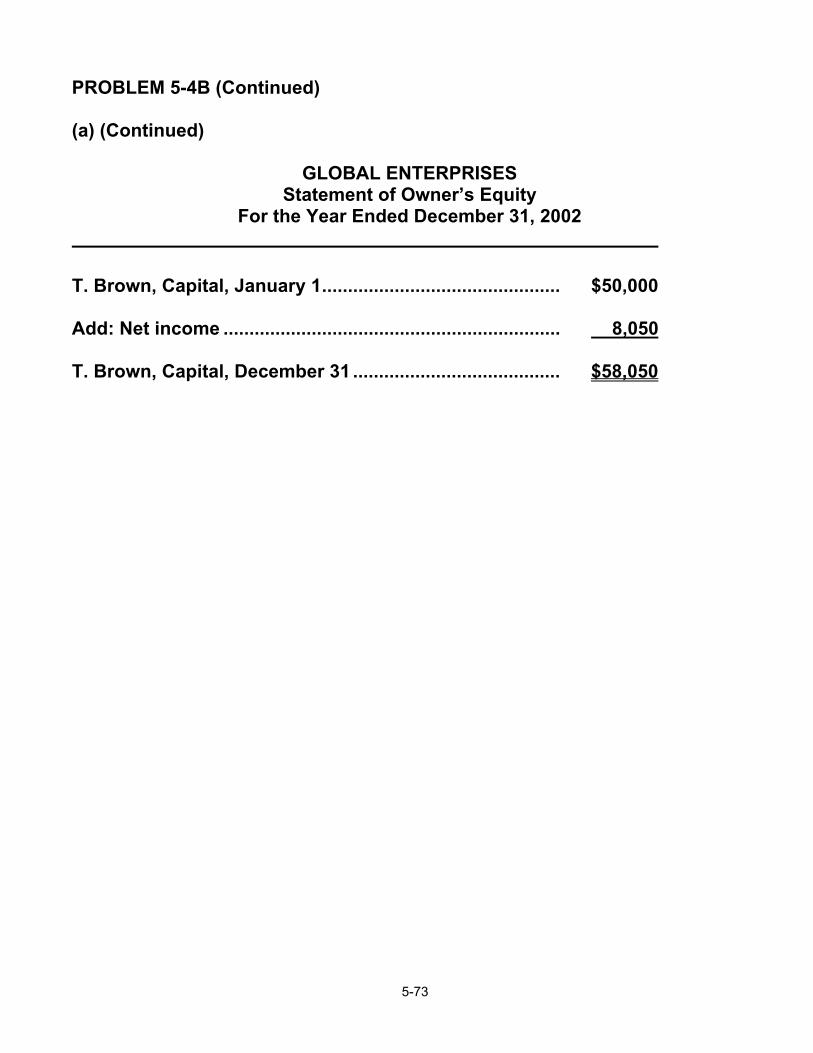

Net income ....................................................................... $14,900 WORLD ENTERPRISES Statement of Owner’s Equity For the Year Ended December 31, 2002

R. Roger, Capital, January 1 ........................................... $50,300 Add: Net income .............................................................. 14,900 R. Roger, Capital, December 31 ..................................... $65,200

5-39

PROBLEM 5-4A (Continued) (a) (Continued) WORLD ENTERPRISES Balance Sheet December 31, 2002 Assets Current assets

Cash .................................................................................. $ 14,000 Accounts receivable ....................................................... 30,600 Merchandise inventory.................................................... 27,500 Prepaid insurance ($1,800 – $800).................................. 1,000

Total current assets ................................................. 73,100 Capital assets

Equipment .......................................................... $42,000 Less: Accumulated amortization – Equipment 12,000 30,000

Total assets.............................................................. $103,100

Liabilities and Owner's Equity Current liabilities

Accounts payable ($34,400 + $500)................................ $ 34,900 Sales taxes payable ......................................................... 3,000 Total current liabilities..................................................... 37,900

Owner's equity

R. Roger, Capital .............................................................. 65,200

Total liabilities and owner's equity ......................... $103,100

5-40

PROBLEM 5-4A (Continued) (b) Dec. 31 Sales............................................................ 238,500

R. Roger, Capital ................................ 238,500

31 R. Roger, Capital ........................................ 223,600 Sales Returns and Allowances ......... 4,600 Cost of Goods Sold............................ 177,000 Salaries Expense................................ 31,600 Rent Expense...................................... 6,600 Insurance Expense............................. 800 Amortization Expense........................ 3,000

5-41

PROBLEM 5-5A

(a) DAIGLE DEPARTMENT STORE Income Statement For the Year Ended November 30, 2003

Sales revenues Sales........................................................................................ $850,000 Less: Sales returns and allowances ................................... 10,000 Net sales ................................................................................. 840,000

Cost of goods sold ........................................................................ 633,220 Gross profit .................................................................................. 206,780 Operating expenses

Selling expenses Salaries expense ($139,000 X 70%) $97,300 Sales commissions expense............ 12,750 Amortization expense—building 9,500 Delivery expense.............................. 8,200 Insurance expense ($9,000 x 50%) 4,500 Amortization expense— delivery equipment........................ 00 4,000

Total selling expenses ............. $136,250 Administrative expenses

Salaries expense ($139,000 X 30%) . $41,700 Utilities expense................................ 10,600 Insurance expense ($9,000 x 50%) .. 4,500 Property tax expense ........................ 3,500

Total administrative expenses . 0 60,300 Total operating expenses.. 196,550

Income from operations..................................................... 10,230 Other revenues and gains

Interest revenue .......................................................... $5,000 Other expenses and losses

Interest expense.......................................................... 8,000 000 3,000 Net income .......................................................................... $ 7,230

5-42

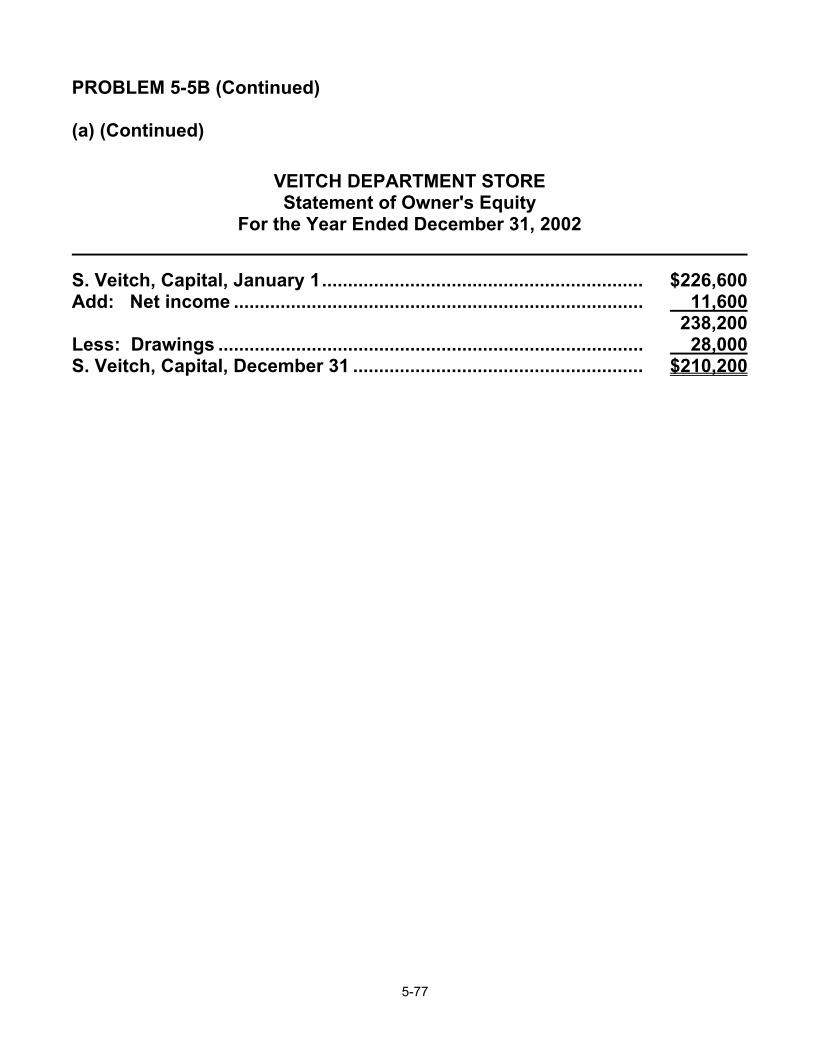

PROBLEM 5-5A (Continued) (a) (Continued) DAIGLE DEPARTMENT STORE Statement of Owner's Equity For the Year Ended November 30, 2003

B. Daigle, Capital, December 1, 2002 ................................................ $84,200 Add: Net income ............................................................................... 7,230 91,430 Less: Drawings .................................................................................. 012,000 B. Daigle, Capital, November 30, 2003.............................................. $79,430

5-43

PROBLEM 5-5A (Continued) (a) (Continued) DAIGLE DEPARTMENT STORE Balance Sheet November 30, 2003 Assets Current assets

Cash ............................................................................. $008,000 Accounts receivable ................................................... 11,770 Merchandise inventory............................................... 36,200 Prepaid insurance....................................................... 4,500

Total current assets ............................................ 60,470 Capital assets

Land ................................................... $50,000 Building.............................................. $125,000 Less: Accumulated amortization—

building ............................ 00 41,800 83,200 Delivery equipment........................... $57,000 Less: Accumulated amortization—

delivery equipment ............. 19,680 037,320 Total capital assets ................... 0170,520

Total assets................................................................... $230,990 Liabilities and Owner's Equity Current liabilities

Accounts payable ........................................................ $ 47,310 Property taxes payable................................................ 3,500 Sales commissions payable ....................................... 4,750 Current portion of mortgage....................................... 6,000

Total current liabilities ......................................... 61,560 Long-term liabilities

Mortgage payable ........................................................ 0 90,000 Total liabilities ...................................................... 151,560

Owner's equity B. Daigle, Capital.......................................................... 0 79,430 Total liabilities and owner's equity............................. $230,990

5-44

PROBLEM 5-5A (Continued) (b) Nov. 30 Amortization Expense–Delivery Equip ....... 4,000

Amortization Expense–Building .................. 9,500 Accum. Amortiz.–Delivery .................... 4,000 Accum. Amortiz.–Building.................... 9,500

30 Insurance Expense ....................................... 9,000 Prepaid Expense ................................... 9,000 30 Property Tax Expense .................................. 3,500 Property Tax Payable............................ 3,500 30 Sales Commissions Expense ...................... 4,750 Sales Commissions Payable................ 4,750

(c) Nov. 30 Sales............................................................... 850,000

Interest Revenue ........................................... 5,000 B. Daigle, Capital ................................... 855,000

Nov. 30 B. Daigle, Capital........................................... 847,770

Sales Returns and Allowances ............ 10,000 Cost of Goods Sold............................... 633,220 Salaries Expense................................... 139,000 Amortization Expense—Delivery Equipment........................................... 4,000 Delivery Expense................................... 8,200 Sales Commission Expense................. 12,750 Amortization Expense—Store Equipment........................................... 9,500 Insurance Expense................................ 9,000 Property Tax Expense........................... 3,500 Utilities Expense.................................... 10,600 Interest Expense.................................... 8,000

30 B. Daigle, Capital............................................ 12,000 B. Daigle, Drawings................................ 12,000

5-45

PROBLEM 5-6A Account Statement Classification Accounts Payable

Balance Sheet Current Liabilities

Accounts Receivable

Balance Sheet Current Assets

Accumulated Amortization –Office Building

Balance Sheet Capital Assets (Contra Account)

Accumulated Amortization –Store Equipment

Balance Sheet Capital Assets (Contra Account)

Advertising Expense

Income Statement Selling Expenses

Amortization Expense –Office Building

Income Statement Administrative Expenses

Amortization Expense –Store Equipment

Income Statement Selling Expenses

Cash

Balance Sheet Current Assets

Swirsky, Capital Balance Sheet Owner’s Equity Freight Out

Income Statement Selling Expenses

Swirsky, Drawings

Statement of Owner’s Equity

Drawings

Income Tax Expense

Income Statement Other Expenses

Income Tax Payable Insurance Expense

Balance Sheet Income Statement

Current Liabilities Administrative Expenses

Interest Expense

Income Statement Other Expenses

Interest Payable Balance Sheet Current Liabilities

5-46

Account Statement Classification

Land

Balance Sheet Capital Assets

Merchandise Inventory

Balance Sheet Current Assets

Mortgage Payable

Balance Sheet Long-Term Liability

Office Building

Balance Sheet Capital Assets

Prepaid Insurance

Balance Sheet Current Assets

Salaries Expense –Office Staff

Income Statement Administrative Expenses

Salaries Expense –Store Staff

Income Statement Selling Expenses

Salaries Payable

Balance Sheet Current Liabilities

Sales Returns and Allowances

Income Statement Contra Revenue

Store Equipment

Balance Sheet Capital Assets

Utilities Expense–Office

Income Statement Administrative Expenses

Utilities Expense–Store

Income Statement Selling Expenses

Wages Payable Balance Sheet Current Liabilities

5-47

PROBLEM 5-7A

(a)

MCGRATH COMPANY Income Statement

For the Year Ended December 31, 2002 Sales revenues Sales......................................................................... $800,000 Less: Sales returns and allowances .................... 30,000 Net sales .................................................................. 770,000 Cost of goods sold ......................................................... 555,000 Gross profit ..................................................................... 215,000 Operating expenses Selling expenses Sales salaries expense ($80,000 + $16,000) ........................... $96,000 Delivery expense............................... 30,000 Advertising expense ......................... 10,000 Sales commissions expense............ 6,000 $142,000 Administrative expenses Office salaries expense .................... $27,000 Rent expense..................................... 24,000 Utilities expense................................ 12,000 Amortization expense—office equip. 8,000 71,000 Total operating expenses....................................... 213,000 Income from operations................................................. 2,000 Other revenues and gains Rent revenue ........................................................... $40,000 Other expenses and losses Interest expense...................................................... 2,000 38,000 Net income ...................................................................... $ 40,000

5-48

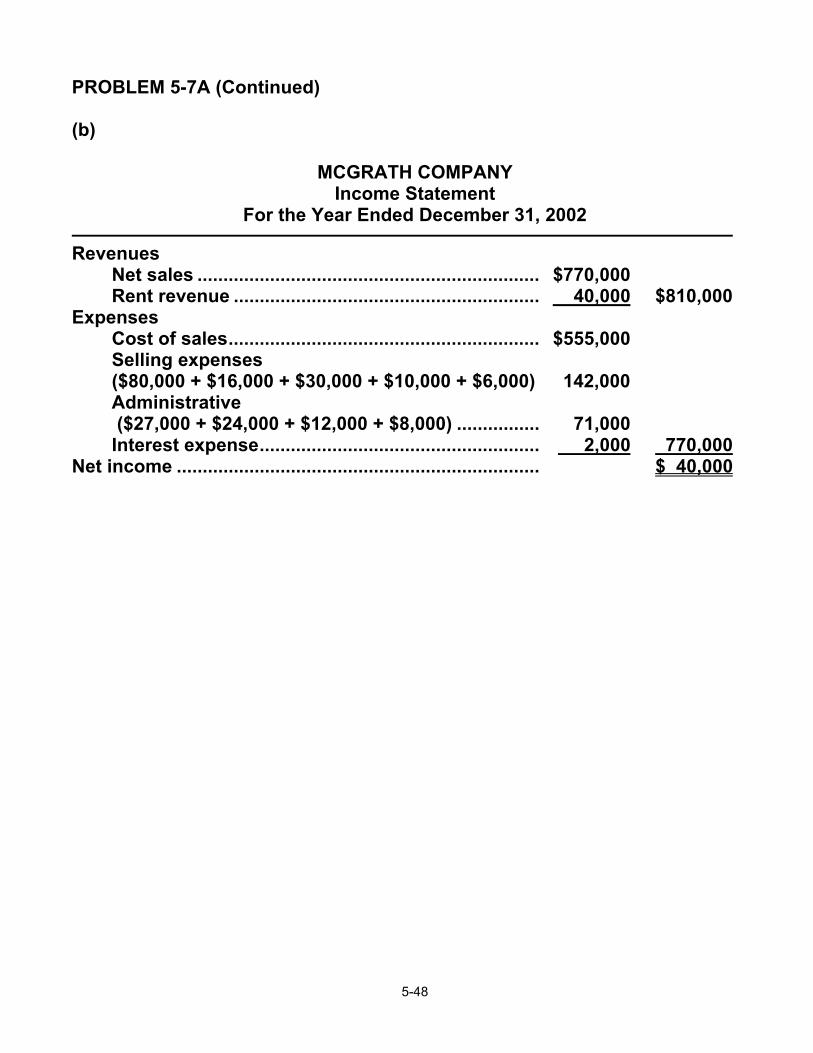

PROBLEM 5-7A (Continued) (b)

MCGRATH COMPANY

Income Statement For the Year Ended December 31, 2002

Revenues Net sales .................................................................. $770,000 Rent revenue ........................................................... 40,000 $810,000 Expenses Cost of sales............................................................ $555,000 Selling expenses ($80,000 + $16,000 + $30,000 + $10,000 + $6,000) 142,000 Administrative ($27,000 + $24,000 + $12,000 + $8,000) ................ 71,000 Interest expense...................................................... 2,000 770,000 Net income ...................................................................... $ 40,000

5-49

PROBLEM 5-8A

(a) 2000 1999 Gross profit margin

19.5% ($949,263 - $764,198) ÷ $949,263

23.8% ($808,251 – $615,827) ÷ $808,251

Inventory turnover

3.5 times $764,198 ÷ [($225,958 + $212,382) ÷ 2]

3.3 times $615,827 ÷ [($212,382 + $164,557) ÷ 2]

Days sales in inventory

104.3 days 365 days ÷ 3.5 times

110.6 days 365 days ÷ 3.3 times

(b) IPSCO’s gross profit margin declined in 2000. However, its management

of its inventories improved. It’s inventory turned over (sold) faster in 2000 and the number of days sales in inventory declined from 110.6 days to 104.3 days. This means that IPSCO is not holding its inventory for as long in 2000, as it did in 1999. The faster you sell your inventory, the faster the company will collect cash/receivables, the lower its carrying costs, and the reduced risk of inventory obsolescence.

5-50

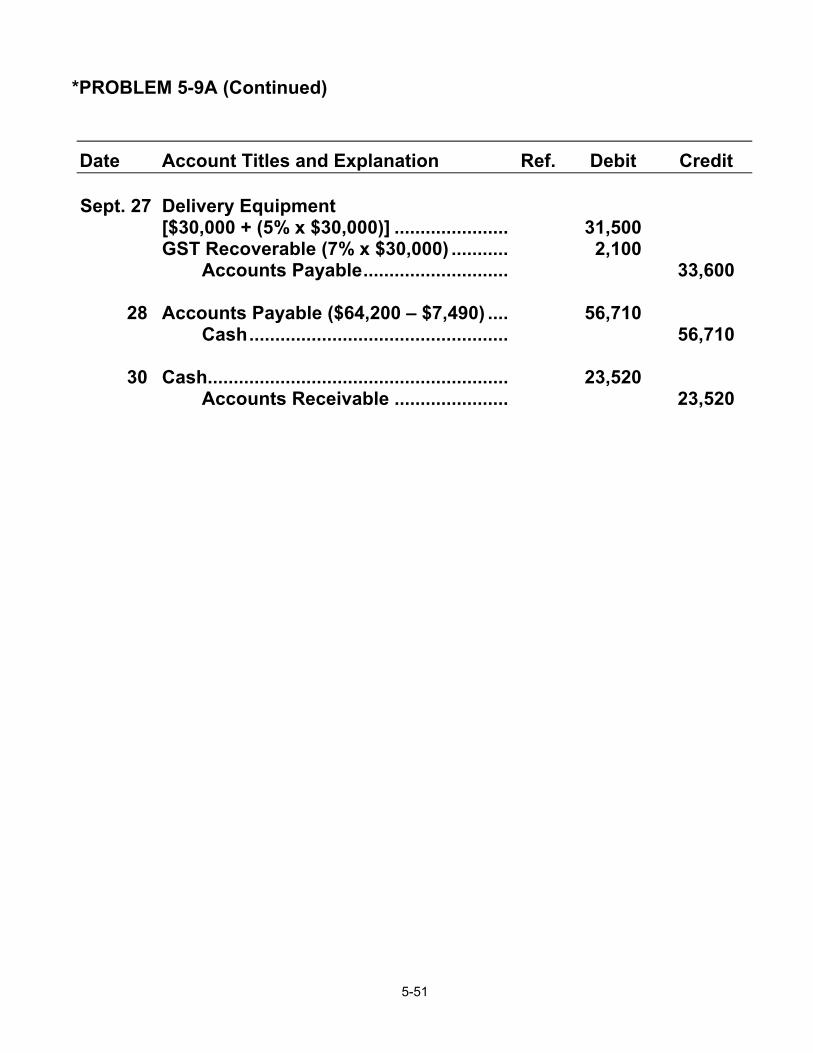

*PROBLEM 5-9A

GENERAL JOURNAL Date

Account Titles and Explanation

Ref.

Debit

Credit

Sept. 2

GST Recoverable.....................................Merchandise Inventory ...........................

Accounts Payable............................

4,200 60,000

64,200

4 Merchandise Inventory ...........................Cash..................................................

02,000 02,000

5 Accounts Payable ...................................Merchandise Inventory ...................GST Recoverable.............................

07,490 07,000 490

6 Accounts Receivable ..............................Sales .................................................GST Payable.....................................PST Payable .....................................

Cost of Goods Sold.................................Merchandise Inventory ...................

23,520

15,000

21,000 1,470 1,050

15,000

15 GST Recoverable.....................................Supplies [$4,000 + (5% x $4,000)] ..........

Cash..................................................

280 4,200

04,480

18 GST Recoverable.....................................Merchandise Inventory ...........................

Cash..................................................

420 6,000

06,420

22 Accounts Receivable ..............................Sales .................................................GST Payable (7% x $28,000) ...........PST Payable (5% x $28,000)............

Cost of Goods Sold.................................Merchandise Inventory ...................

31,360

20,000

28,000 1,960 1,400

20,000

5-51

*PROBLEM 5-9A (Continued)

Date

Account Titles and Explanation

Ref.

Debit

Credit

Sept. 27

Delivery Equipment [$30,000 + (5% x $30,000)] ......................GST Recoverable (7% x $30,000) ...........

Accounts Payable............................

31,500 2,100

33,600

28 Accounts Payable ($64,200 – $7,490) ....

Cash..................................................

56,710

0

56,710

30 Cash..........................................................Accounts Receivable ......................

23,520 00,

23,520

5-52

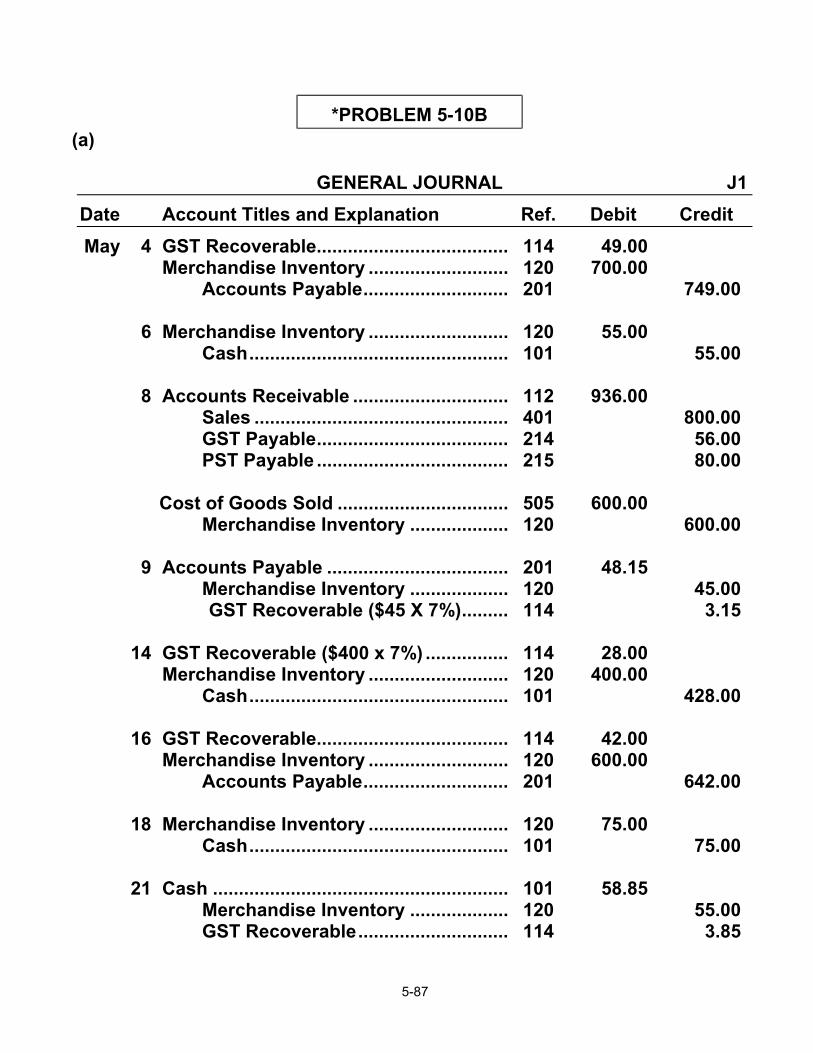

*PROBLEM 5-10A

(a) GENERAL JOURNAL J1 Date

Account Titles and Explanation

Ref.

Debit

Credit

April 4 GST Recoverable.................................... Merchandise Inventory ..........................

Accounts Payable...........................

114 120 201

42.00 600.00

642.00

6 Merchandise Inventory .......................... Cash.................................................

120 101

060.00 060.00

8 Accounts Receivable ............................. Sales ................................................ GST Payable.................................... PST Payable ....................................

Cost of Goods Sold ................................ Merchandise Inventory ..................

112 401 214 215

505 120

1,053.00

630.00

900.00 63.00 90.00

630.00

10 Accounts Payable .................................. Merchandise Inventory ..................

GST Recoverable ($40 X 7%)........

201 120 114

042.80 040.00 2.80

11 GST Recoverable.................................... Merchandise Inventory ..........................

Cash.................................................

114 120 101

21.00 300.00

321.00

14 GST Recoverable.................................... Merchandise Inventory ..........................

Accounts Payable...........................

114 120 201

49.00 700.00

749.00

15 Cash......................................................... Merchandise Inventory .................. GST Recoverable............................

101 120 114

053.50 050.00 3.50

17 Merchandise Inventory .......................... Cash.................................................

120 101

070.00 070.00

5-53

*PROBLEM 5-10A (Continued) (a) (Continued)

J2 Date

Account Titles and Explanation

Ref.

Debit

Credit

April 18

Accounts Receivable ..............................

Sales .................................................GST Payable.....................................PST Payable .....................................

Cost of Goods Sold................................. Merchandise Inventory ...................

112 401 214 215

505 120

936.00

560.00

800.00 56.00 80.00

560.00

20 Cash..........................................................Accounts Receivable ......................

101 112

500.00 500.00

27 GST Payable ............................................PST Payable.............................................Sales Returns and Allowances ..............

Accounts Receivable ......................

Merchandise Inventory .......................... Cost of Goods Sold .........................

214 215 412 112

120 505

2.10 3.00 30.00

25.00

035.10

25.00

29 Accounts Payable ...................................Cash..................................................

201 101

599.20 599.20

30 Accounts Receivable ..............................Sales .................................................GST Payable.....................................PST Payable .....................................

Cost of Goods Sold................................. Merchandise Inventory ...................

112 401 214 215

505 120

1,170.00

730.00

1,000.00

70.00 100.00

730.00

30 Cash..........................................................Accounts Receivable ......................

101 112

1,200.00 1,200.00

5-54

*PROBLEM 5-10A (Continued) (b) Cash No. 101 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 1 6 11 15 17 20 29 30

Balance

J1 J1 J1 J1 J2 J2 J2

053.50

500.00

1,200.00

060.00 321.00

070.00

599.20

2,500.00 2,440.00 2,119.00 2,172.50 2,102.50 2,602.50 2,003.30 3,203.30

Accounts Receivable No. 112

Explanation

Ref.

Debit

Credit Balance

Apr. 8 18 20 27 30 30

J1 J2 J2 J2 J2 J2

1,053.00 936.00

1,170.00

500.00 035.10

1,200.00

1,053.00 1,989.00 1,489.00 1,453.90 2,623.90 1,423.90

GST Recoverable No. 114 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 4 10 11 14 15

J1

J1 J1 J1 J1

42.00

21.00 49.00

2.80

3.50

42.00 39.20 60.20 109.20 105.70

5-55

*PROBLEM 5-10A (Continued) (b) (Continued) Merchandise Inventory No. 120 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 1 4 6 8 10 11 14 15 17 18 27 30

Balance

J1 J1 J1 J1 J1 J1 J1 J1 J2 J2 J2

600.00 60.00

300.00 700.00

70.00

25.00

630.00 40.00

50.00

560.00

730.00

3,500.00 4,100.00 4,160.00 3,530.00 3,490.00 3,790.00 4,490.00 4,440.00 4,510.00 3,950.00 3,975.00 3,245.00

Accounts Payable No. 201 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 4 10 14 29

J1 J1 J1 J2

42.80

599.20

642.00

749.00

642.00 599.20 1,348.20 749.00

GST Payable No. 214 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 8 18 27 30

J1 J2 J2 J2

2.10

63.00 56.00

70.00

63.00 119.00 116.90 186.90

5-56

*PROBLEM 5-10A (Continued) (b) (Continued) PST Payable No. 215 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 8 18 27 30

J1 J2 J2 J2

3.00

90.00 80.00

100.00

90.00 170.00 167.00 267.00

B. J. Evert, Capital No. 301 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 1

Balance

6,000.00

Sales No. 401 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 8 18 30

J1 J2 J2

900.00 800.00

1,000.00

0,900.00 1,700.00 2,700.00

Sales Returns and Allowances No. 412 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 27

J2

030.00

0,030.00

Cost of Goods Sold No. 505 Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 8 18 27 30

J1 J2 J2 J2

630.00 560.00

730.00

25.00

0,630.00 1,190.00 1,165.00 1,895.00

5-57

*PROBLEM 5-10A (Continued) (c)

B. J.'S TENNIS SHOP Trial Balance April 30, 2003

Debit

Credit

Cash ................................................................Accounts Receivable.....................................GST Recoverable ...........................................Merchandise Inventory..................................Accounts Payable ..........................................GST Payable ...................................................PST Payable ...................................................B. J. Evert, Capital .........................................Sales................................................................Sales Returns and Allowances.....................Cost of Goods Sold .......................................

$3,203.30

1,423.90 105.70 3,245.00

30.00 1,895.00 $9,902.90

$ 749.00 186.90 267.00 6,000.00 02,700.00

00000000 $9,902.90

(d)

B. J.'S TENNIS SHOP Income Statement (Partial) For the Month Ended April 30, 2003

Sales revenues

Sales........................................................................................ $2,700 Less: Sales returns and allowances.................................... 30 Net sales.................................................................................. 2,670

Cost of goods sold ........................................................................ 1,895 Gross profit .................................................................................... 775

5-58

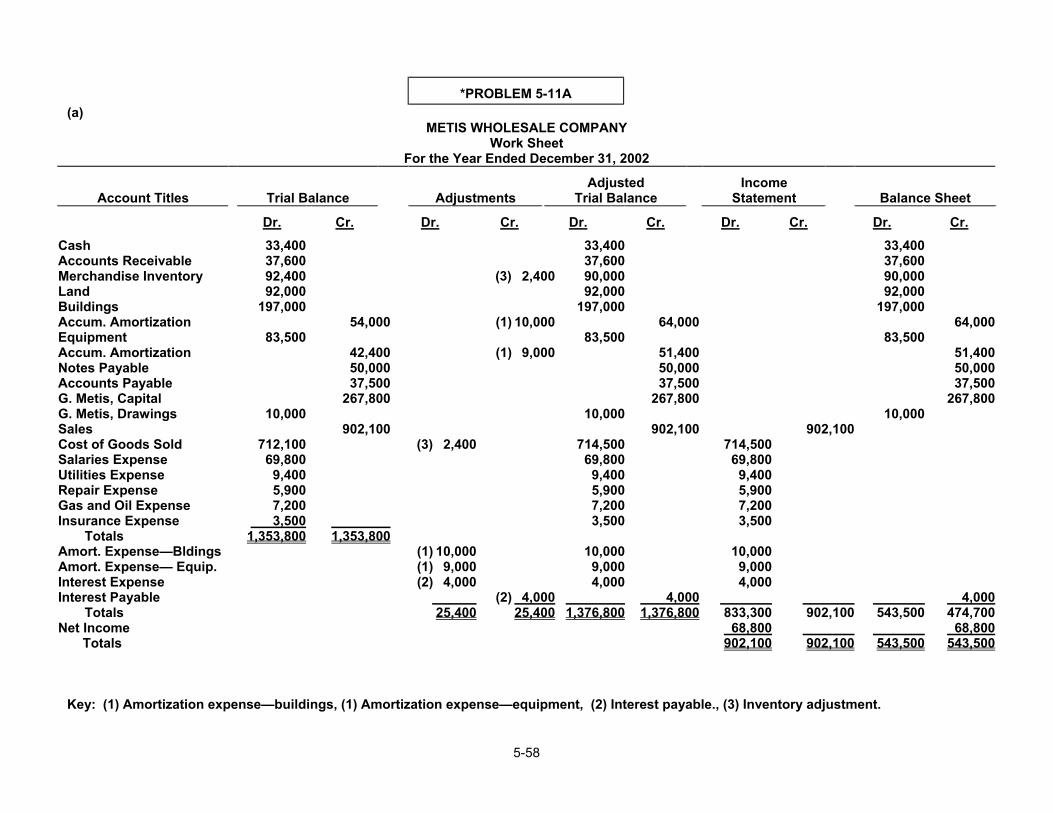

*PROBLEM 5-11A

(a) METIS WHOLESALE COMPANY

Work Sheet For the Year Ended December 31, 2002

Account Titles

Trial Balance

Adjustments

Adjusted Trial Balance

Income

Statement

Balance Sheet

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Cash Accounts Receivable Merchandise Inventory Land Buildings Accum. Amortization Equipment Accum. Amortization Notes Payable Accounts Payable G. Metis, Capital G. Metis, Drawings Sales Cost of Goods Sold Salaries Expense Utilities Expense Repair Expense Gas and Oil Expense Insurance Expense

Totals Amort. Expense—Bldings Amort. Expense— Equip. Interest Expense Interest Payable

Totals Net Income

Totals

33,400 37,600 92,400 92,000

197,000

83,500

10,000

712,100 69,800

9,400 5,900 7,200

0,00 3,500 1,353,800

54,000

42,400 50,000 37,500

267,800

902,100

00000000 1,353,800

(3) 2,400

(1) 10,000 (1) 9,000 (2) 4,000

000000 0025,400

(3) 2,400

(1) 10,000

(1) 9,000

(2) 04,000 25,400

33,400 37,600 90,000 92,000

197,000

83,500

10,000

714,500 69,800

9,400 5,900 7,200 3,500

10,000

9,000 4,000

00000000 1,376,800

64,000

51,400 50,000 37,500

267,800

902,100

0,004,000 1,376,800

714,500 69,800

9,400 5,900 7,200 3,500

10,000

9,000 4,000

0000000 0833,300

068,800 902,100

902,100

0000000 902,100

0000000 00902,100

33,400 37,600 90,000 92,000

197,000

83,500

10,000

0000000 543,500

0000000 543,500

64,000

51,400 50,000 37,500

267,800

004,000 474,700 068,800 543,500

Key: (1) Amortization expense—buildings, (1) Amortization expense—equipment, (2) Interest payable., (3) Inventory adjustment.

5-59

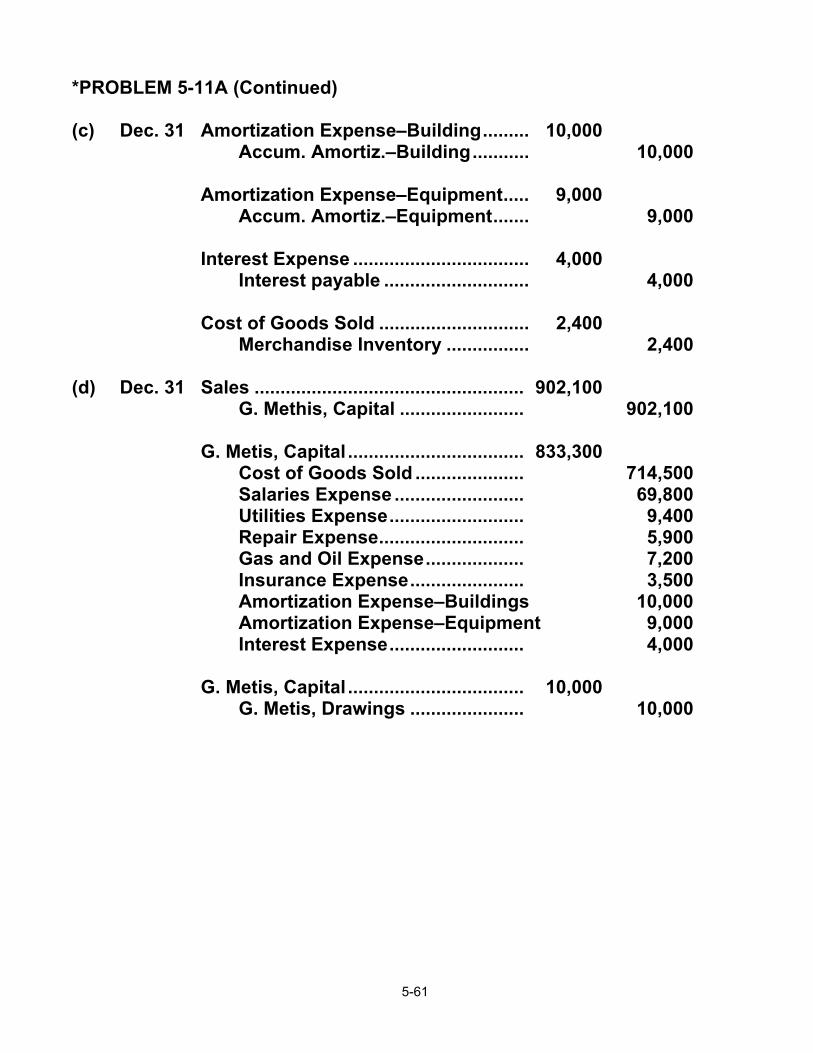

*PROBLEM 5-11A (Continued) (b)

METIS WHOLESALE COMPANY Income Statement

For the Year Ended December 31, 2002

Sales ..................................................................................................... $902,100 Cost of goods sold .............................................................................. 714,500 Gross profit ........................................................................................ 187,600 Operating expenses

Selling expenses Salaries expense ($69,800 X 80%) ..... $55,840 Gas and oil expense............................ 0007,200

Total selling expenses ................ $63,040 Administrative expenses

Salaries expense ($69,800 X 20%) ..... $13,960 Amortization expense—buildings ..... 10,000 Utilities expense.................................. 9,400 Amortization expense—equipment ... 9,000 Repair expense.................................... 5,900 Insurance expense .............................. 3,500

Total administrative expenses ... 00 51,760 Total operating expenses..................................... 0 114,800

Income from operations...................................................................... 72,800 Other expenses and losses

Interest expense .......................................................................... 00 4,000 Net income ........................................................................................... $ 68,800

METIS WHOLESALE COMPANY Statement of Owner’s Equity

For the Year Ended December 31, 2002

G. Metis, Capital January 1 ................................................................. $267,800 Add: Net income .................................................................................. 68,800 ............................................................................................................... 336,600 Less: Drawings .................................................................................... 10,000 G. Metis, Capital December 31 ........................................................... $326,600

5-60

*PROBLEM 5-11A (Continued) (b) (Continued)

METIS WHOLESALE COMPANY Balance Sheet

December 31, 2002

Assets Current assets Cash .............................................................................................. $ 33,400 Accounts receivable .................................................................... 37,600 Merchandise inventory ................................................................ 90,000 Total current assets.............................................................. 161,000 Capital assets Land............................................................ $ 92,000 Buildings.................................................... $197,000 Less: Accumulated amortization............. (64,000) 133,000 Equipment.................................................. 83,500 Less: Accumulated amortization............. (51,400) 32,100 257,100 Total assets .......................................................................... $418,100 Liabilities and Owner’s Equity Current liabilities Notes payable............................................................................... $ 50,000 Accounts payable ........................................................................ 37,500 Interest payable............................................................................ 4,000 Total liabilities ...................................................................... 91,500 Owner’s Equity G. Metis Capital ............................................................................ 326,600 Total liabilities and owner’s equity.................................... $418,100

5-61

*PROBLEM 5-11A (Continued) (c) Dec. 31 Amortization Expense–Building......... 10,000 Accum. Amortiz.–Building........... 10,000 Amortization Expense–Equipment..... 9,000 Accum. Amortiz.–Equipment....... 9,000 Interest Expense .................................. 4,000 Interest payable ............................ 4,000 Cost of Goods Sold ............................. 2,400 Merchandise Inventory ................ 2,400 (d) Dec. 31 Sales .................................................... 902,100 G. Methis, Capital ........................ 902,100 G. Metis, Capital .................................. 833,300 Cost of Goods Sold ..................... 714,500 Salaries Expense ......................... 69,800 Utilities Expense.......................... 9,400 Repair Expense............................ 5,900 Gas and Oil Expense................... 7,200 Insurance Expense...................... 3,500 Amortization Expense–Buildings 10,000 Amortization Expense–Equipment 9,000 Interest Expense.......................... 4,000 G. Metis, Capital .................................. 10,000 G. Metis, Drawings ...................... 10,000

5-62

*PROBLEM 5-11A (Continued) (e)

METIS WHOLESALE COMPANY Post-Closing Trial Balance

December 31, 2002

Debit Credit Cash .............................................................. $ 33,400 Accounts Receivable ................................... 37,600 Merchandise Inventory ................................ 90,000 Land............................................................... 92,000 Buildings....................................................... 197,000 Accumulated Amortization—Buildings...... $ 64,000 Equipment..................................................... 83,500 Accumulated Amortization—Equipment.... 51,400 Notes Payable............................................... 50,000 Accounts Payable ........................................ 37,500 Interest Payable............................................ 4,000 G. Metis, Capital ........................................... 00000 00 326,600

Totals $533,500 $533,500

5-63

PROBLEM 5-1B

(a) June 5 Merchandise Inventory–Jet Runners (2 x $22,000)................................................... 44,000