chapter 5 banking and interest rates. copyright ©2014 pearson education, inc. all rights...

TRANSCRIPT

Chapter 5

Banking and Interest Rates

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-2

Chapter Objectives

• Describe the types and functions of financial institutions

• Describe the banking services offered by financial institutions

• Identify the components of interest rates

• Explain why interest rates change over time

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-3

Types of Financial Institutions

• Depository institutions: Financial institutions that accept deposits from individuals and provide loans

– Commercial banks: financial institutions that accept deposits and use the funds to provide commercial and personal loans

• Deposits insured by Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-4

Types of Financial Institutions (cont’d)

– Savings institutions (or thrift institutions): financial institutions that accept deposits and provide mortgage and personal loans to individuals

– Credit unions: nonprofit depository institutions that serve members who have a common affiliation

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-5

Types of Financial Institutions (cont’d)

• Nondepository institutions: financial institutions that do not offer federally insured deposit accounts, but provide various other financial services

– Finance companies: nondepository institutions that specialize in providing personal loans to individuals

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-6

Types of Financial Institutions (cont’d)

– Securities firms: nondepository institutions that facilitate the purchase or sale of securities by providing investment banking and brokerage services

– Insurance companies: nondepository institutions that provide insurance to protect individuals or firms against possible adverse events

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-7

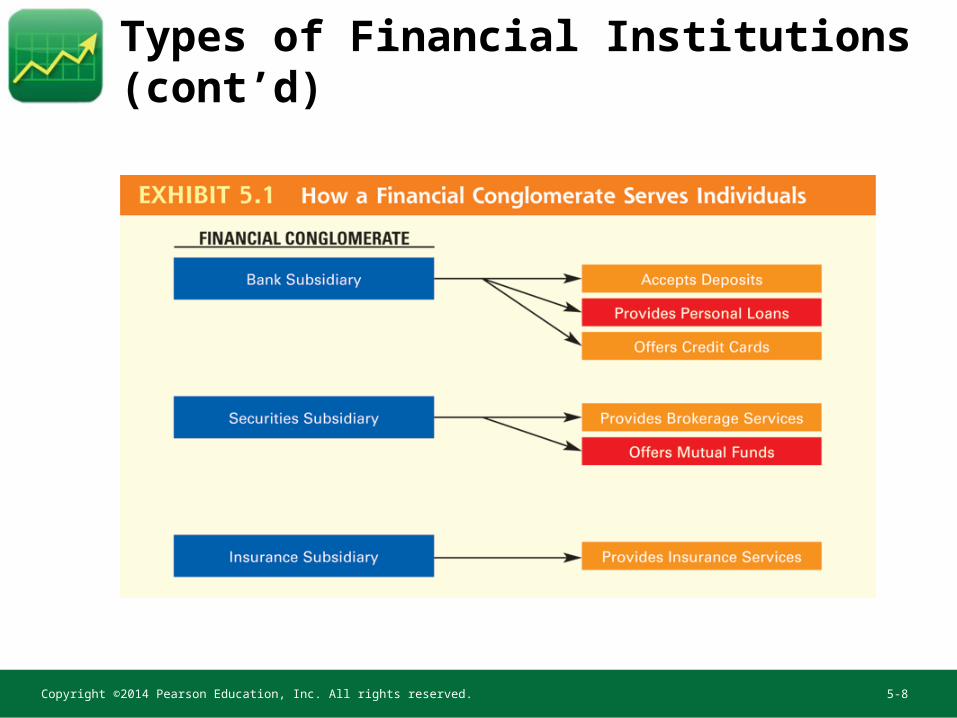

Types of Financial Institutions (cont’d)

– Investment companies: nondepository institutions that sell shares to individuals and use the proceeds to invest in securities to create mutual funds

• Financial conglomerates: financial institutions that offer a diverse set of financial services to individuals or firms– Examples include Bank of America and Citigroup

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-8

Types of Financial Institutions (cont’d)

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-9

Banking Services Offered by Financial Institutions

• Checking services

– Checking accounts allow you to draw on funds by writing checks

– Paying Bills on Time

• Fees are charged for

– Paying bills after the deadline

– Making loan payments after the deadline

– Ignoring the rules of a car lease contract, such as maximum mileage allowed

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-10

Banking Services Offered by Financial Institutions (cont’d)

– Monitoring Your Account Balance

• Record checks in your checkbook as you write them

– Reconciling Your Account Balance

• Make sure the bank statement agrees with your check register

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-11

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-12

Banking Services Offered by Financial Institutions (cont’d)

• Check float—the time from when you write a check until your checking account balance is reduced

– Check Clearing for the 21st Century Act (Oct. 2004) allows banks to transmit electronic images of checks, virtually eliminating float

– Electronic checking deters fraud

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-13

Banking Services Offered by Financial Institutions (cont’d)

• Credit card financing such as Visa and Mastercard

• Debit card: a card that is used to make purchases that are charged against a checking account

– Debit cards for Teenagers

• Convenient way for parents to transfer funds to children, but may encourage overspending

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-14

Additional Services Financial Institutions Offer

• Safety deposit box: a box at a financial institution where a customer can store documents, jewelry, or other valuables

• Automated teller machines (ATMs): a machine where individuals can deposit and withdraw funds any time of the day

– Fees can be charged for using another financial institution’s ATM

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-15

Additional Services Financial Institutions Offer (cont’d)

• Cashier’s check: a check that is written on behalf of a person to a specific payee and will be charged against a financial institution’s account

• Money order: a check that is written on behalf of a person for a fixed amount that is paid in advance

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-16

Additional Services Financial Institutions Offer (cont’d)

• Traveler’s check: a check that is written on behalf of an individual and will be charged against a large well-known financial institution or credit card sponsor’s account

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-17

Selecting a Financial Institution

• Criteria Used to Select a Financial Institution– Convenience

• Close to where you live or work, convenient ATM locations, online banking

– Paying bills online

– Deposit rates and insurance• Comparison shop for best interest rates

– Fees• Some consumers using Wal-Mart to avoid fees

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-18

Financial Planning Online

• Go to www.fdic.gov/bank/individual/online/

safe.html

• This Web site provides tips for safe banking over the Internet

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-19

Interest Rates on Deposits and Loans

• Interest rates on deposits and loans affect your cash inflows and outflows

• Certificate of deposit: an instrument that is issued by a depository institution and specifies a minimum investment, an interest rate, and a maturity

• Risk-free rate: a return on an investment that is guaranteed for a specified period

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-20

Interest Rates on Deposits and Loans (cont’d)

• Risk premium: an additional return beyond the risk-free rate that can be earned from a deposit guaranteed by the government

• Loan rate—financial institutions loan money at a rate higher than they pay depositors– Individuals with a poor credit history pay

higher rates

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-21

Interest Rates on Deposits and Loans (cont’d)

• Impact of the economy of the risk premium– When economic conditions weaken, firms issuing

securities must pay a higher risk premium to sell their securities, resulting in investors reluctance to purchase the securities for fear the firm might go bankrupt and not repay their debt

– Investors more willing to invest in a favorable economic climate

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-22

Financial Planning Online

• Go to dir.yahoo.com/business_and_economy/

finance_and_investment/banking

• This Web site provides information about individual financial institutions such as the services they offer and the interest rates they pay on deposits or charge on loans.

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-23

Interest Rates on Deposits and Loans (cont’d)

• Twisted perception of the risk premium– Some investors attracted to investments for the

wrong reasons– They pursue risky investments to make up for

limited income– This is faulty reasoning as those with limited

incomes can less afford losses

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-24

Interest Rates on Deposits and Loans (cont’d)

• Comparing interest rates and risks

– Choice depends on risk tolerance

• If you will need your money within a year, you should take no risk

• If you will need a portion of your money when your investment matures, you can afford to take some risk

• No choice is right for all investors

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-25

Financial Planning Online

• Go towww.bloomberg.com/markets/rates/

index.html

• This Web site provides updated quotations on key interest rates and charts showing recent movements in these rates

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-26

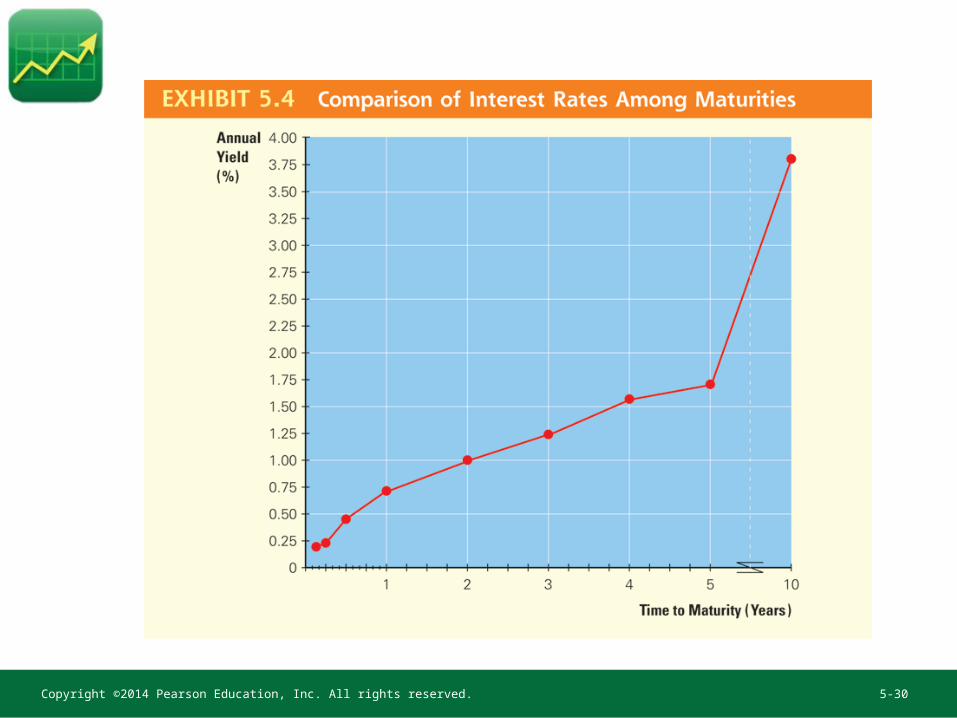

Interest Rates on Deposits and Loans (cont’d)

• Term structure of interest rates: the relationship between the maturities of risk-free debt securities and the annualized yields offered on those securities

– Often based on rates of return offered by U.S. Treasury securities with different maturities

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-27

Interest Rates on Deposits and Loans (cont’d)

• Shifts in the yield curve- Graphs such as the one on the previous slide

can be found in financial publications such as the Wall Street Journal and illustrate how returns change over time

• Loan Rates- Financial institutions obtain funds by accepting

deposits and providing loans to individuals and firms

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-28

Financial Planning Online

• Go to www.bankrate.com/finance/federal-reserve

• This Web site provides updated information about the Fed’s recent actions and upcoming meetings, as well as forecasts of future policy decisions and the potential impact of these decisions.

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-29

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-30

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-31

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-32

Why Interest Rates Change

• Monetary policy: the actions taken by the Federal Reserve to control the money supply

– Money supply: demand deposits (checking accounts) and currency held by the public

– Open market operations: the Fed’s buying and selling of Treasury securities

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-33

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-34

Why Interest Rates Change

• Shift in the government demand for funds– Any change in the government’s borrowing

behavior can affect the demand for funds and affect interest rates

• Shift in the business demand for funds– When firms adjust their borrowing and spending

plans, this affects demand and interest rates

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-35

Financial Planning Online

• Go to http://www.bloomberg.com/markets/rates/

index.html

• This Web site provides updated information about the Fed’s recent actions and upcoming meetings, as well as forecasts of future policy decisions and the potential impact of these decisions

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-36

How Banking Services Fit within Your Financial Plan

• The key banking decisions for your financial plan are:

– What banking service characteristics are most important to you?

– What financial institution provides the best banking service characteristic for you?

Copyright ©2014 Pearson Education, Inc. All rights reserved. 5-37