chapter 5 · consolidated financial statements are the financial statements of a group presented as...

TRANSCRIPT

Page 1 of 43

CHAPTER 5 IFRS 10 CONSOLIDATION OF PARENT AND SUBSIDIARY

DEFINITIONS

Consolidated financial statements are the financial statements of a group presented as those of a

single economic entity.

A group is a parent and all its subsidiaries

A parent is an entity that has one or more subsidiaries.

A subsidiary is an entity, including an unincorporated entity such as a partnership that is controlled by

another entity (known as the parent).

Investment entity an entity that: -

a) Obtains funds from one or more investors for the purpose of providing investors with investment

management services.

b) Commits to its investors that its business is to invest funds solely for returns from capital

appreciation, investment income or both, and

c) Measures and evaluates the performance of substantially all of its investments on a fair value

basis.

SCOPE

A parent, other than a parent exempt under this IAS, shall present consolidated financial statements in

which it consolidates its investments in subsidiaries in accordance with this Standard.

A parent need not present consolidated financial statements if and only if:

(a) the parent is itself a wholly-owned subsidiary, or is a partially-owned subsidiary of another entity

and its other owners, including those not otherwise entitled to vote, have been informed about,

and do not object to, the parent not presenting consolidated financial statements;

(b) the parent’s debt or equity instruments are not traded in a public market (a domestic or foreign

stock exchange or an over-the-counter market, including local and regional markets);

(c) the parent did not file, nor is it in the process of filing, its financial statements with a securities

commission or other regulatory organization for the purpose of issuing any class of instruments in

a public market; and

(d) the ultimate or any intermediate parent of the parent produces consolidated financial

statements available for public use that comply with International Financial Reporting Standards.

An entity is not required to consolidate it post employment benefit plans or other long-term employee

benefit plans to which IAS 19 applies.

An investment entity shall not consolidate its subsidiaries or apply IFRS 3, instead measure these

investments at fair value through profit or loss account.

CONSOLIDATION PROCEDURES

Consolidated financial statements:

(a) combine like items of assets, liabilities, equity, income, expenses and cash flows of the parent

with those of its subsidiaries.

(b) offset (eliminate) the carrying amount of the parent’s investment in each subsidiary and the

parent’s portion of equity of each subsidiary (IFRS 3 explains how to account for any related

goodwill).

(c) eliminate in full intra-group assets and liabilities, equity, income, expenses and cash flows relating

to transactions between entities of the group (profits or losses resulting from intra-group

transactions that are recognized in assets, such as inventory and fixed assets, are eliminated in

full). Intra-group losses may indicate an impairment that requires recognition in the consolidated

financial statements. IAS 12 Income Taxes applies to temporary differences that arise from the

elimination of profits and losses resulting from intra-group transactions.

Uniform accounting policies

If a member of the group uses accounting policies other than those adopted in the consolidated

financial statements for like transactions and events in similar circumstances, appropriate adjustments

are made to that group member’s financial statements in preparing the consolidated financial

statements to ensure conformity with the group’s accounting policies.

Page 2 of 43

Measurement of Assets and Liabilities and related Incomes and Expenses

An entity includes the income and expenses of a subsidiary in the consolidated financial statements

from the date it gains control until the date when the entity ceases to control the subsidiary. Income

and expenses of the subsidiary are based on the amounts of the assets and liabilities recognized in the

consolidated financial statements at the acquisition date.

For example, depreciation expense recognized in the consolidated statement of comprehensive

income after the acquisition date is based on the fair values of the related depreciable assets

recognized in the consolidated financial statements at the acquisition date.

Potential voting rights

When potential voting rights, or other derivatives containing potential voting rights, exist, the proportion

of profit or loss and changes in equity allocated to the parent and non-controlling interests in preparing

consolidated financial statements is determined solely on the basis of existing ownership interests and

does not reflect the possible exercise or conversion of potential voting rights and other derivatives,

unless paragraph B90 applies.

In some circumstances an entity has, in substance, an existing ownership interest as a result of a

transaction that currently gives the entity access to the returns associated with an ownership interest. In

such circumstances, the proportion allocated to the parent and non-controlling interests in preparing

consolidated financial statements is determined by taking into account the eventual exercise of those

potential voting rights and other derivatives that currently give the entity access to the returns.

Reporting date

The financial statements of the parent and its subsidiaries used in the preparation of the consolidated

financial statements shall have the same reporting date. When the end of the reporting period of the

parent is different from that of a subsidiary, the subsidiary prepares, for consolidation purposes,

additional financial information as of the same date as the financial statements of the parent to enable

the parent to consolidate the financial information of the subsidiary, unless it is impracticable to do so.

If it is impracticable to do so, the parent shall consolidate the financial information of the subsidiary

using the most recent financial statements of the subsidiary adjusted for the effects of significant

transactions or events that occur between the date of those financial statements and the date of the

consolidated financial statements. In any case, the difference between the date of the subsidiary’s

financial statements and that of the consolidated financial statements shall be no more than three

months, and the length of the reporting periods and any difference between the dates of the financial

statements shall be the same from period to period.

Non-controlling interests

An entity shall attribute the profit or loss and each component of other comprehensive income to the

owners of the parent and to the non-controlling interests. The entity shall also attribute total -

comprehensive income to the owners of the parent and to the non-controlling interests even if this

results in the non-controlling interests having a deficit balance.

If a subsidiary has outstanding cumulative preference shares that are classified as equity and are held

by non-controlling interests, the entity shall compute its share of profit or loss after adjusting for the

dividends on such shares, whether or not such dividends have been declared.

CONSOLIDATION PROCEDURE ILLUSTRATED

• Group has no books of account as a whole:

• Parent has its own books of accounts

• Subsidiary has its own books of accounts

• Each company prepares their own Financial Statements

In consolidation, we add up the financial statements of both companies

Reasons for consolidation:

⇒ Parent company controls the subsidiary hence they decide the subsidiary’s policies (stewardship

efficiencies, and inefficiencies)

⇒ Sales of financial instruments to ‘special purpose entities’ (IAS-39) e.g. factoring, assignment etc

⇒ Related party relationship may affect the financial statements of individual entities.

⇒ Decision to invest in group requires the detail of the performance of group as a whole.

METHOD OF CONSOLIDATION

Purchase method is based on the concept of single economic entity.

Single economic entity results in elimination of:

Page 3 of 43

⇒ Investment in subsidiary shown in parent company Financial Statements

⇒ Share Capital of subsidiary

⇒ Intra group balances – payables and receivables

⇒ Loans and advances between parent and subsidiary

⇒ Intra group trading – sale and purchase

⇒ Gain on Sale and purchase of fixed assets and inventory (opening and closing both), however,

losses on sale or purchase are assumed to be impairment losses and need not be eliminated.

⇒ Interest and dividend from S Co

⇒ The resultant deferred tax arising on temporary differences because of elimination of profits /

gains on intra-group transactions will be recognized.

⇒ The consolidated financial statements will be prepared using same accounting policies for like

transactions.

⇒ The purchase method of accounting has the following steps: -

Determination of cost

of investment

IFRS – 3 Date of

acquisition accounting

Calculation of goodwill

at date of acquisitionGroup Goodwill

Determination of Fair

value of net assets of

subsidiary company

Identification of date of

acquisition

Determination of value

of NCI at date of

acquisition, if partially

owned subsidiary

Full goodwill

NCI is recognized at

Fair Value

NCI is recognized at

proportionate share of

net assets DEALING WITH THE STATEMENT OF FINANCIAL POSITION

Consolidation Procedures for Basic Consolidation

1. Prepare the following working notes:

⇒ Working Note 1 for group structure, identification of percentage holding by the parent

company

⇒ Working Note 2 for cost of control (to calculate goodwill only group share of Goodwill)

⇒ Working Note 3 for Non-controlling Interest (if applicable i.e. where the holding by the parent

is less than 100% but more than 50% in subsidiary company)

⇒ Working Note 4 for Subsidiary Reserves by identifying Pre and Post acquisition reserves

⇒ Working Note 5 for Consolidated Reserves

Note separate working should be prepared for each reserve of subsidiary and parent

because similar reserve will be added with similar reserve.

2. Add all non-adjusting items line by line except cost of investment appearing in P. Co and share

capital of S. Co.

3. Make all necessary adjustments discussed on next pages.

4. Balance all working accounts and place the balances in the statement of financial position

1. Investment in subsidiary company

This balance is eliminated from statement of financial position and incorporated in the

calculation of goodwill.

Page 4 of 43

Entry:

Debit: Cost of control account

Credit: Investment in subsidiary

2. Share capital of subsidiary company

3. Subsidiary company reserves

First split reserves into post and pre acquisition reserves because both have different treatment,

and also before the following entries, make necessary adjustments to the both types of reserve.

Example 1 Acquisition of wholly owned subsidiary

On 31st December 20X1 P purchased the entire share capital of S for Rs. 40,000. The individual

statements of financial positions of P and S at that date were as follows: -

Statement of financial positions at 31 December 20X1

P S

Rs.000 Rs.000

Non-current assets 120 40

Investment in S at cost 40 -

Current assets 40 10

Total assets 200 50

Ordinary share capital (Rs.1 shares) 100 30

Retained earnings 50 10

Current liabilities 50 10

Total equity and liabilities 200 50

Required: Prepare consolidated statement of financial position as at December 31, 20X1?

Page 5 of 43

Example-2 Reserves (Pre-acquisition and post acquisition)

Statement of financial positions at 31 December 20X4

P S

Rs.000 Rs.000

Non-current assets 50 40

Investment in S at cost 70 -

Current assets 30 40

Total assets 150 80

Ordinary share capital (Rs.1 shares) 100 50

Retained earnings 30 20

Current liabilities 20 10

Total equity and liabilities 150 80

You are further informed that P acquired all the shares in S on 30 June 20X4 when the retained

earnings of S amounted to Rs.15,000.

Required: Prepare consolidated statement of financial position as at December 31, 20X4?

4 Treatment of impairment loss on goodwill

Example 3

Non-controlling interest

Statement of financial positions at 31 December 20X4

P S

Rs.000 Rs.000

Non-current assets 50 40

Investment in S at cost 70 -

Current assets 30 40

Total assets 150 80

Ordinary share capital (Rs.1 shares) 100 50

Retained earnings 30 20

Current liabilities 20 10

Total equity and liabilities 150 80

Required: -

P acquired 40,000 Rs.1 shares in S on 30 June 20X4 for Rs.70,000, when the retained earnings of S

amounted to Rs.15,000. The group has a policy of measuring non-controlling interest at

proportionate share of net assets at the date of acquisition. 20% of goodwill has impaired to

date?

Required: Prepare consolidated statement of financial position as at December 31, 20X4?

4. Fair values adjustments of subsidiary company assets/liabilities

If fair value differs at the date of acquisition and if not incorporated in group financial

statements then goodwill may include certain gains/losses of identifiable assets, which is not

permitted by definitions of goodwill as well as by IFRS – 3. The following is treatment of fair value

adjustments arising at the date of acquisition.

Page 6 of 43

Example 4

The summarized draft statement of financial positions of the companies in a group at 31 December

20X4 were

P S P S

Rs. Rs. Rs. Rs.

Sundry assets 86,000 24,500 Share capital (Rs.1 Ord.). 100,000 20,000

Investment in S (shares at cost) 27,000 - Retained earnings 22,000 6,500

Inventory 20,000 10,000 Payables 11,000 8,000

133,000 34,500 133,000 34,500

Prepare the consolidated statement of financial position at 31 December 20X4 for each of the following

alternatives.

a) P acquired all the shares in S on 1 January 20X4, when S had accumulated profits of Rs.6,000.

b) Facts as in (a) above, except that only 16,000 ordinary shares in S were purchased for Rs.27,000

c) Facts as in (a) above, except that only 16,000 ordinary shares in S were purchased for Rs.27,000

on 1 January 20X4. The subsidiary has not incorporated the fair values in its separate books and

fair value adjustments identified by the parent company at the date of acquisition are as

follows: -

Carrying value Fair value Exist on subsequent

Page 7 of 43

Rs. Rs. Reporting date

Property (Non-Depreciable) 10,000 12,000 Yes

Inventory 6,000 4,500 NO

The group has a policy of measuring non-controlling interest at proportionate share of net assets at the

date of acquisition. 20% of goodwill has impaired to date.

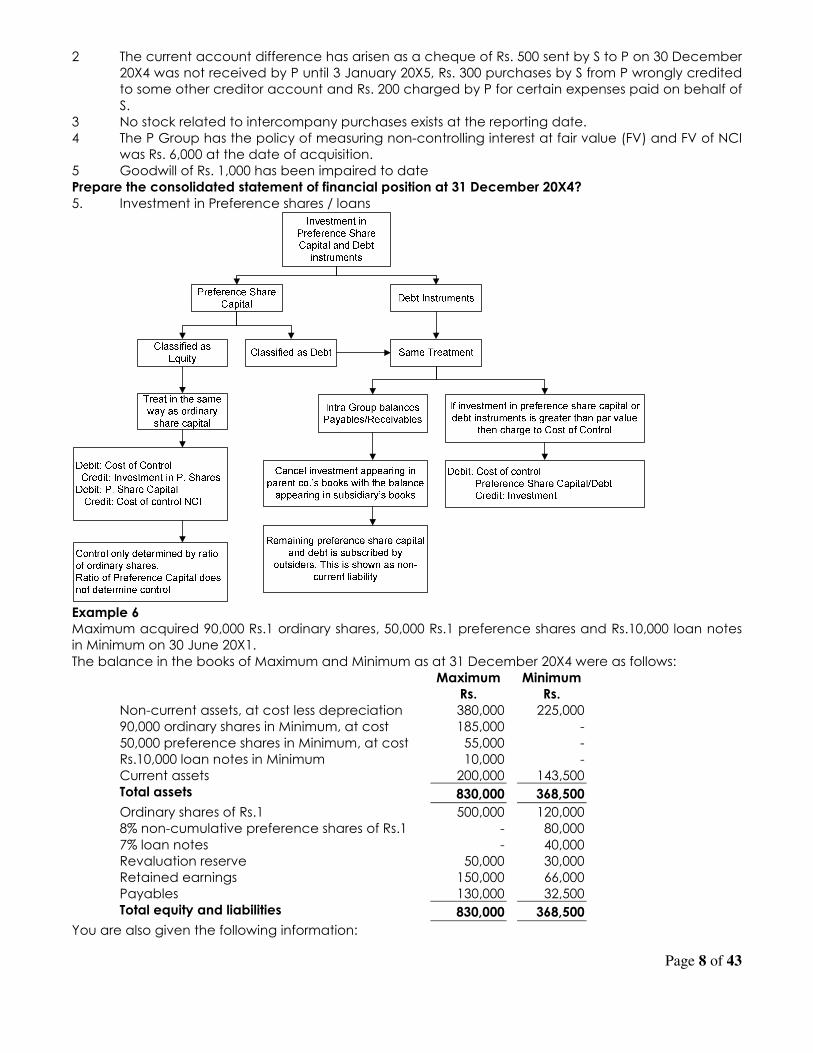

5 Intra group balances

Example 5

Statements of financial position at 31 December 20X4

P S

Rs. Rs.

Investment in S (at cost) 19,000 --

S current account 10,000 --

Cash at bank 20,000 28,000

Other sundry assets 41,000 16,000

Total assets 90,000 44,000

Share capital (Rs.1 Ord.) 50,000 10,000

Retained earnings 30,000 20,000

Current liabilities 10,000 5,000

P current account -- 9,000

Total equity and liabilities 90,000 44,000

1 P bought 7,500 shares in S on 1 January 20X4 when the balance on the retained earnings of S

was Rs.12,000.

Page 8 of 43

2 The current account difference has arisen as a cheque of Rs. 500 sent by S to P on 30 December

20X4 was not received by P until 3 January 20X5, Rs. 300 purchases by S from P wrongly credited

to some other creditor account and Rs. 200 charged by P for certain expenses paid on behalf of

S.

3 No stock related to intercompany purchases exists at the reporting date.

4 The P Group has the policy of measuring non-controlling interest at fair value (FV) and FV of NCI

was Rs. 6,000 at the date of acquisition.

5 Goodwill of Rs. 1,000 has been impaired to date

Prepare the consolidated statement of financial position at 31 December 20X4?

5. Investment in Preference shares / loans

Example 6

Maximum acquired 90,000 Rs.1 ordinary shares, 50,000 Rs.1 preference shares and Rs.10,000 loan notes

in Minimum on 30 June 20X1.

The balance in the books of Maximum and Minimum as at 31 December 20X4 were as follows:

Maximum Minimum

Rs. Rs.

Non-current assets, at cost less depreciation 380,000 225,000

90,000 ordinary shares in Minimum, at cost 185,000 -

50,000 preference shares in Minimum, at cost 55,000 -

Rs.10,000 loan notes in Minimum 10,000 -

Current assets 200,000 143,500

Total assets 830,000 368,500

Ordinary shares of Rs.1 500,000 120,000

8% non-cumulative preference shares of Rs.1 - 80,000

7% loan notes - 40,000

Revaluation reserve 50,000 30,000

Retained earnings 150,000 66,000

Payables 130,000 32,500

Total equity and liabilities 830,000 368,500

You are also given the following information:

Page 9 of 43

a) The revaluation reserve and retained earnings of Minimum as at 30 June 20X1 were Rs.12,000

and Rs.30,500 respectively.

b) The inventory of Minimum at 31 December 20X4 includes Rs.22,800 in respect of goods

purchased from Maximum. Maximum invoices Minimum at cost plus 20%.

c) Minimum owed Rs. 5,000 to Maximum included in its payables, which also agree with the

receivable balance in Maximum books.

d) Maximum has the policy of measuring NCI at proportionate share of net assets at the date of

acquisition.

e) The whole amount of goodwill has impaired by the current reporting date.

You are required to prepare the consolidated statement of financial position of Maximum and its

subsidiary Minimum as at 31 December 20X4.

6. Intra group trading and resultant stocks at the reporting date

Note: It may be possible that an item may be inventory for one entity and fixed asset for other entity

e.g. an item of inventory sold by parent company but recognized by subsidiary company as property,

plant and equipment. If this is the case then pass following adjusting entries while preparing

consolidated financial statements.

Debit Credit

Sales X (with sale price)

Cost of sales X (cost to the seller)

Property, plant and

equipment

X (Profit margin)

In other words it is just goods taken by an entity from inventory for use in the business.

Example-7

Intra-group profits on stocks

Statement of financial positions at 31 December 20X4

P S

Rs. Rs.

Investment in S (at cost) 75,000

Inventory 12,000 5,000

P current account 5,000

Other assets 83,000 90,000

Total assets 170,000 100,000

Page 10 of 43

Share capital (Rs. 1 ord.). 50,000 40,000

Retained earnings 100,000 55,000

Trade payables 20,000 5,000

Total equity and liabilities 170,000 100,000

1 P acquired 32,000 shares in S on 1 January 20X4 when the balance on the retained earnings of

S was Rs.50,000.

2 During the year S sold goods to P for Rs.80,000 making a standard mark up of 25%. At 31

December 20X4, P included in its inventory value Rs.5,000, being the price paid for goods

purchased from S.

3 Other than the goods in note no. 2 Rs. 5,000 goods are in transit not received by P till the

reporting date.

4 Except the goods in transit P has paid for the due amount to S before the year end.

Prepare the consolidated statement of financial position as at 31 December 20X4?

7 Dividends from subsidiary companies

a) Dividend Payable from subsidiary company and Dividend Receivable in parent company are

treated as intra-group balance.

b) Any amount of dividend payable to NCI is included in NCI.

c) If the dividend declared is greater than post-acquisition profit, then it was declared out of pre-

acquisition profits.

Possible situations:

1. Dividend declared / paid by subsidiary company and duly recorded by both companies.

Do nothing in group financial statements

2. Dividend declared by subsidiary company and no recording by both companies

Parent company Subsidiary company

Debit: Dividend Receivable Debit: SRE (Pre or Post)

Credit: CRE or P&L Credit: Dividend Payable

The dividend payable and receivable balances are cancelled.

3. Dividend declared by subsidiary company and no recording in parent’s accounts

Parent company

Debit: Dividend Receivable

Credit: CRE or P&L

The dividend payable and receivable balances are cancelled.

4. Dividend declared / paid by subsidiary and no recording in parent company

Parent company

Debit: Dividend Receivable

Credit: CRE or P&L

Debit: Cash in Transit

Page 11 of 43

Credit: Dividend Receivable

5. Dividend declared / paid by subsidiary and parent company has only recorded Dividend

Receivable

Parent company

Debit: Cash in Transit

Credit: Dividend Receivable

6. Dividend declared by subsidiary company from Pre-Acquisition profit and parent company

treated that as income.

Adjusting Entry

Debit: CRE or P&L

Credit: Cost of investment

Example 8

Up-minster acquired 80% of the ordinary share capital of Barking several years ago when the balance

on the accumulated profits of Barking was Rs.12,000. Their respective draft statement of financial

positions at 31 December 20X4 are as follows:

Up-minster Barking

Rs. Rs.

Non-current assets 100,000 92,000

Investment in Barking 55,000 -

Current assets 45,000 31,000

Total assets 200,000 123,000

Ordinary shares capital 100,000 50,000

Preference share capital - 10,000

Retained earnings 80,000 42,000

Proposed ordinary dividend (declared Dec 20X4) - 10,000

Sundry payables 20,000 11,000

Total equity and liabilities 200,000 123,000

Up-minster has not made any entry for the dividend receivable from Barking for the year. A proposed

preference dividend of Rs.2,000 by Barking (also declared in December 20X4) has not been accounted

for by either company. Up-minster purchased 30% of the preference shares for Rs.3,500 some years ago.

It’s the group policy to measure NCI at proportionate share of FV of net assets at the date of acquisition.

Prepare the consolidated statement of financial position at 31 December 20X4.

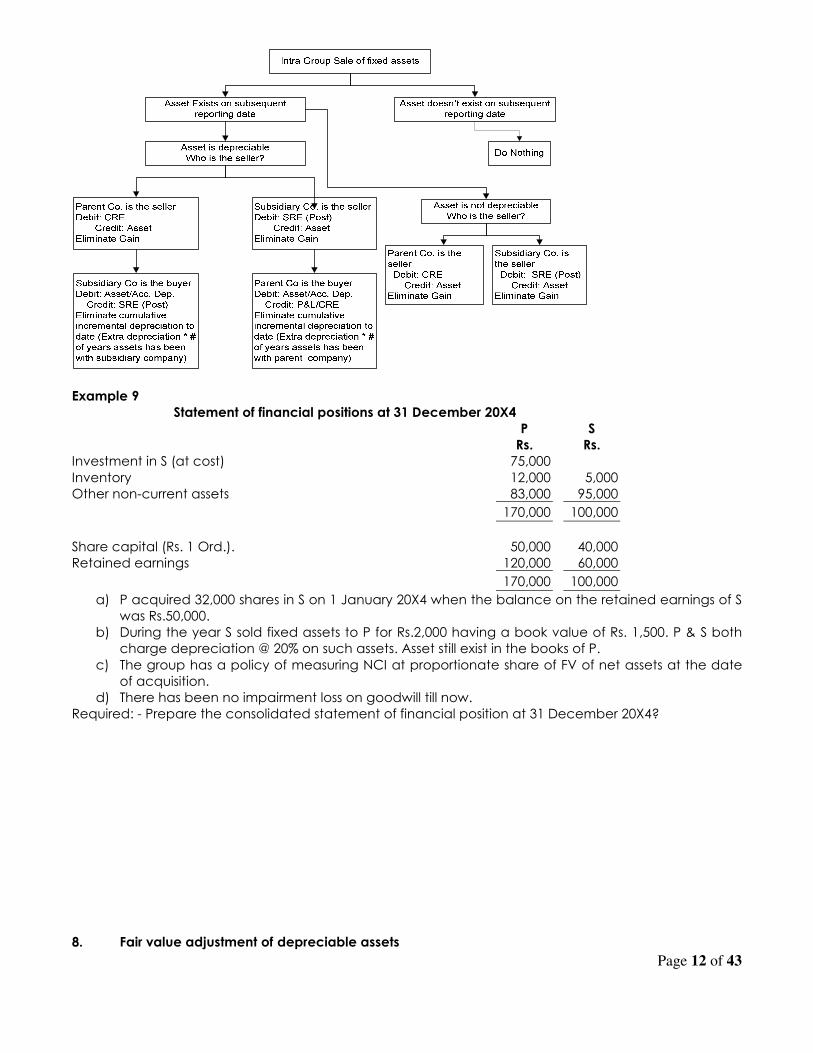

7. Intra group sale of fixed assets

Page 12 of 43

Example 9

Statement of financial positions at 31 December 20X4

P S

Rs. Rs.

Investment in S (at cost) 75,000

Inventory 12,000 5,000

Other non-current assets 83,000 95,000

170,000 100,000

Share capital (Rs. 1 Ord.). 50,000 40,000

Retained earnings 120,000 60,000

170,000 100,000

a) P acquired 32,000 shares in S on 1 January 20X4 when the balance on the retained earnings of S

was Rs.50,000.

b) During the year S sold fixed assets to P for Rs.2,000 having a book value of Rs. 1,500. P & S both

charge depreciation @ 20% on such assets. Asset still exist in the books of P.

c) The group has a policy of measuring NCI at proportionate share of FV of net assets at the date

of acquisition.

d) There has been no impairment loss on goodwill till now.

Required: - Prepare the consolidated statement of financial position at 31 December 20X4?

8. Fair value adjustment of depreciable assets

Page 13 of 43

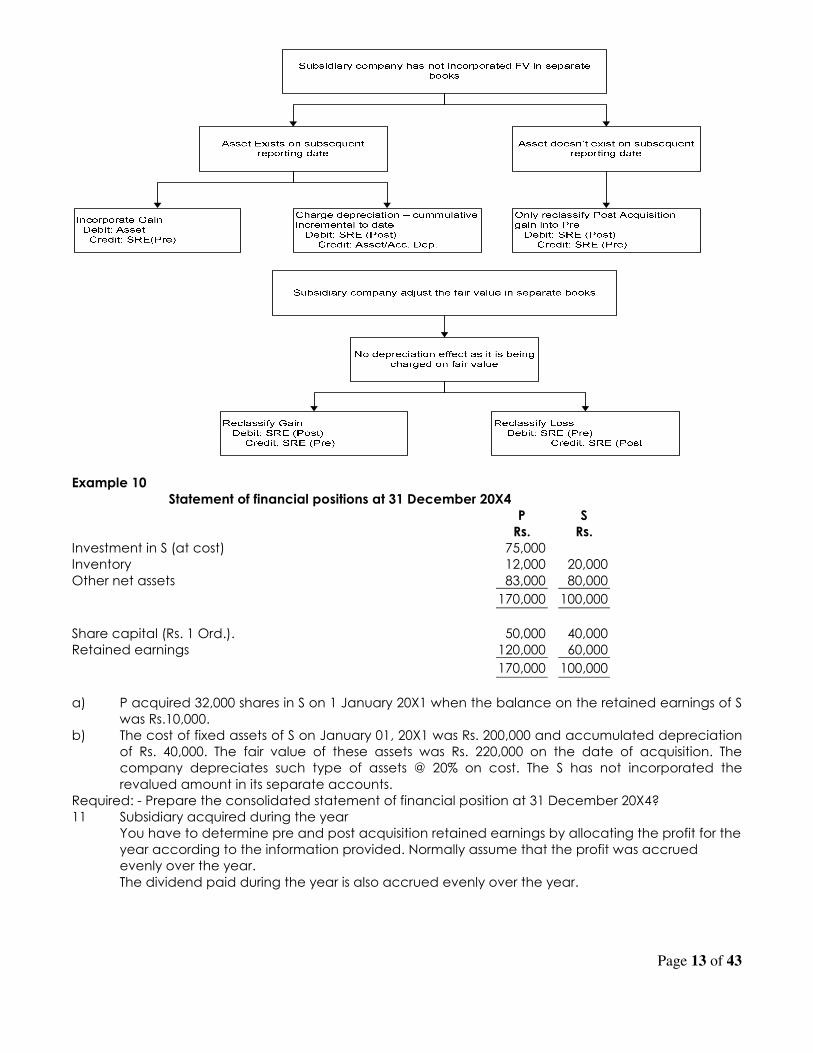

Example 10

Statement of financial positions at 31 December 20X4

P S

Rs. Rs.

Investment in S (at cost) 75,000

Inventory 12,000 20,000

Other net assets 83,000 80,000

170,000 100,000

Share capital (Rs. 1 Ord.). 50,000 40,000

Retained earnings 120,000 60,000

170,000 100,000

a) P acquired 32,000 shares in S on 1 January 20X1 when the balance on the retained earnings of S

was Rs.10,000.

b) The cost of fixed assets of S on January 01, 20X1 was Rs. 200,000 and accumulated depreciation

of Rs. 40,000. The fair value of these assets was Rs. 220,000 on the date of acquisition. The

company depreciates such type of assets @ 20% on cost. The S has not incorporated the

revalued amount in its separate accounts.

Required: - Prepare the consolidated statement of financial position at 31 December 20X4?

11 Subsidiary acquired during the year

You have to determine pre and post acquisition retained earnings by allocating the profit for the

year according to the information provided. Normally assume that the profit was accrued

evenly over the year.

The dividend paid during the year is also accrued evenly over the year.

Page 14 of 43

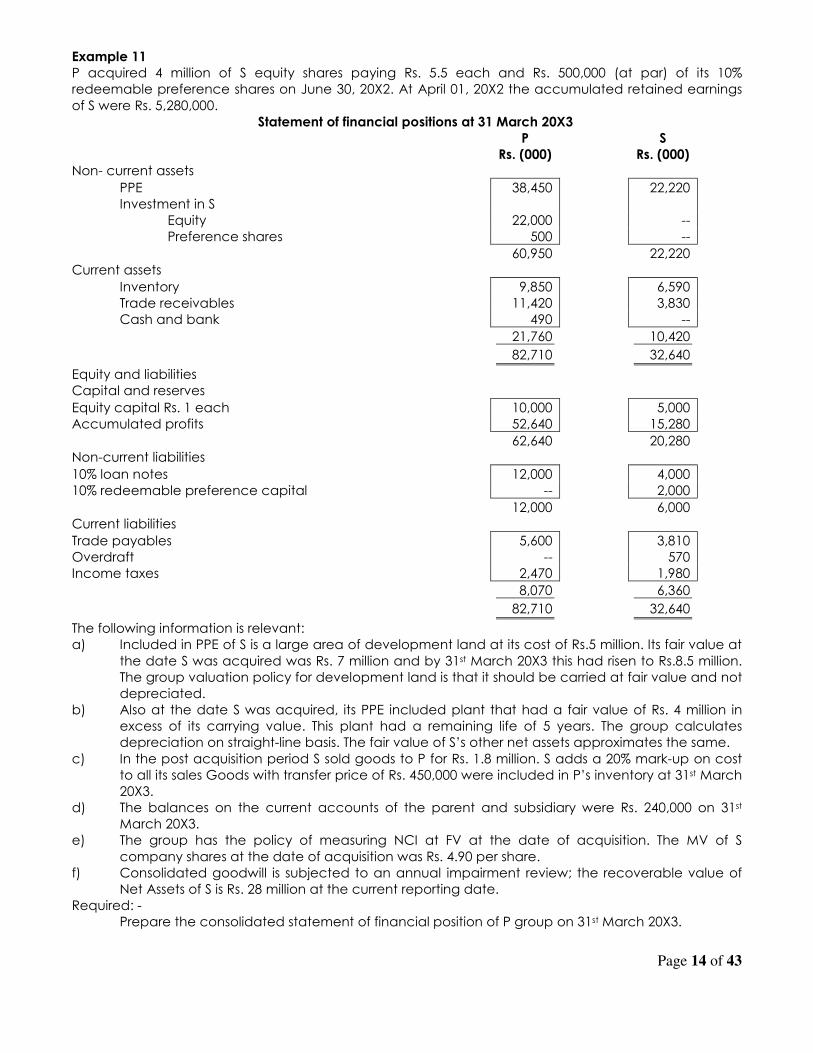

Example 11

P acquired 4 million of S equity shares paying Rs. 5.5 each and Rs. 500,000 (at par) of its 10%

redeemable preference shares on June 30, 20X2. At April 01, 20X2 the accumulated retained earnings

of S were Rs. 5,280,000.

Statement of financial positions at 31 March 20X3

P S

Rs. (000) Rs. (000)

Non- current assets

PPE 38,450 22,220

Investment in S

Equity 22,000 --

Preference shares 500 --

60,950 22,220

Current assets

Inventory 9,850 6,590

Trade receivables 11,420 3,830

Cash and bank 490 --

21,760 10,420

82,710 32,640

Equity and liabilities

Capital and reserves

Equity capital Rs. 1 each 10,000 5,000

Accumulated profits 52,640 15,280

62,640 20,280

Non-current liabilities

10% loan notes 12,000 4,000

10% redeemable preference capital -- 2,000

12,000 6,000

Current liabilities

Trade payables 5,600 3,810

Overdraft -- 570

Income taxes 2,470 1,980

8,070 6,360

82,710 32,640

The following information is relevant:

a) Included in PPE of S is a large area of development land at its cost of Rs.5 million. Its fair value at

the date S was acquired was Rs. 7 million and by 31st March 20X3 this had risen to Rs.8.5 million.

The group valuation policy for development land is that it should be carried at fair value and not

depreciated.

b) Also at the date S was acquired, its PPE included plant that had a fair value of Rs. 4 million in

excess of its carrying value. This plant had a remaining life of 5 years. The group calculates

depreciation on straight-line basis. The fair value of S’s other net assets approximates the same.

c) In the post acquisition period S sold goods to P for Rs. 1.8 million. S adds a 20% mark-up on cost

to all its sales Goods with transfer price of Rs. 450,000 were included in P’s inventory at 31st March

20X3.

d) The balances on the current accounts of the parent and subsidiary were Rs. 240,000 on 31st

March 20X3.

e) The group has the policy of measuring NCI at FV at the date of acquisition. The MV of S

company shares at the date of acquisition was Rs. 4.90 per share.

f) Consolidated goodwill is subjected to an annual impairment review; the recoverable value of

Net Assets of S is Rs. 28 million at the current reporting date.

Required: -

Prepare the consolidated statement of financial position of P group on 31st March 20X3.

Page 15 of 43

12 Expenses on acquisition

13 Other Fair Value Adjustments

Example 12

M/S Haseeb Limited acquired 75% M/S Saqib Limited on September 30, 2008 for Rs. 12 million by paying

immediately Rs. 10 million to the former owners and agreed to pay the balance amount after one year.

The discount rate Haseeb Limited uses for its present value calculation is 12%. The statements of financial

position for both the companies for the year ended December 31, 2008 is as follows: -

Haseeb Ltd. Saqib Ltd.

(Rs. 000) (Rs. 000)

Investment in Saqib Ltd 10,000 --

Property, plant and equipment 20,000 8,000

Current assets 15,000 6,000

45,000 14,000

Share capital 15,000 6,000

Retained earnings b / f 10,000 3,000

Profit for the year 6,000 1,200

31,000 10,200

Current liabilities 14,000 3,800

45,000 14,000

The following further information is also available: -

a) Haseeb Ltd only recorded the investment in Saqib Ltd at the amount of cash paid.

Page 16 of 43

b) The fair value of property, plant and equipment of Saqib Ltd at the date of acquisition was Rs.

1,000,000 more than its carrying value which results in extra depreciation of Rs. 45,000 in the post

acquisition period.

c) In the post acquisition period Saqib Ltd sold goods to Haseeb Ltd charging Rs. 100,000 as margin

on goods. 55% of the goods are still lying with Hasseeb Ltd.

d) All revenues and expenses have accrued evenly through the year.

e) The group has the policy of measuring NCI at the proportionate share of net assets at the date

of acquisition.

f) Saqib Ltd has a popular brand developed over many years in the past but has not been

recognized in its books, a professional firm of valuers placed a value of Rs. 200,000 at the date of

acquisition.

Required: -

a) Goodwill arising on acquisition

b) Consolidated balance sheet of Haseeb Ltd group

c) Statement of changes in equity of Haseeb Ltd Group

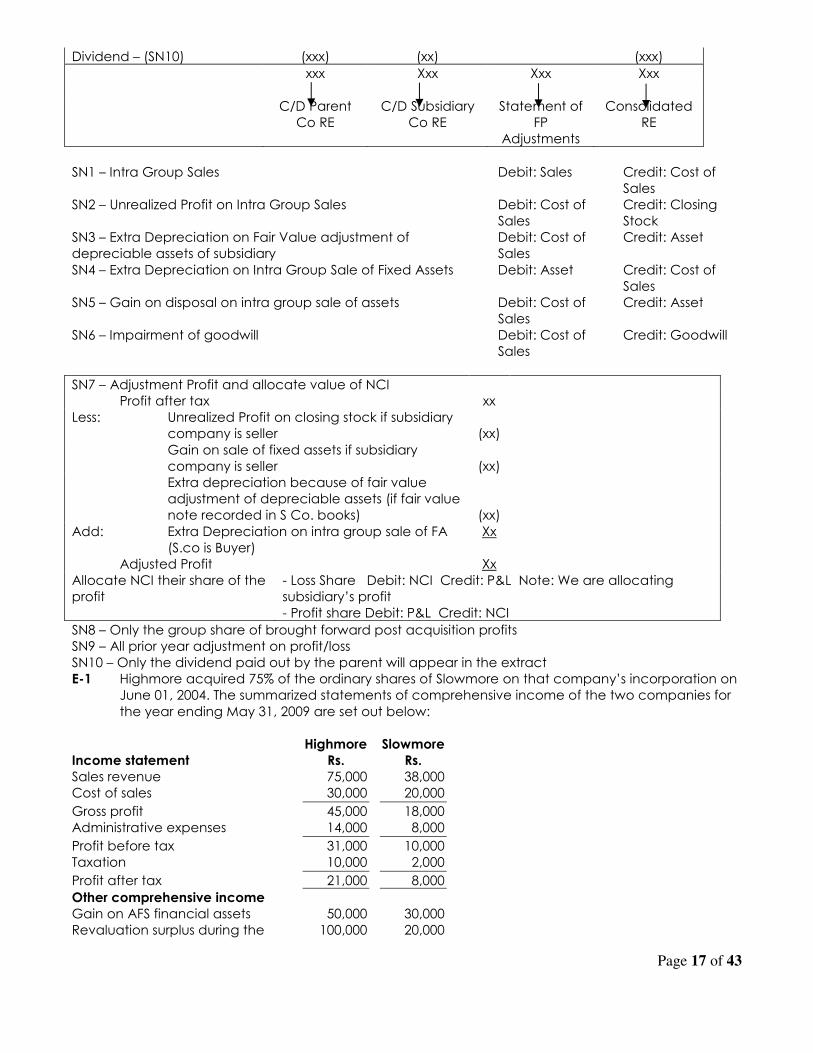

CONSOLIDATION OF STATEMENT OF COMPREHENSIVE INCOME

Working 1:

Parent Co- Subsidiary Co- Adjustments Consolidated

Current year Post Acquisition Figures

Sales Xxx Xxx SN1 xxx

Less: cost of sales (xxx) (xxx) SN1-5 (xxx)

Gross profit Xxx Xxx xxx

Selling and distribution (xxx) (xxx) - (xxx)

Administration (xxx) (xxx) SN6 (xxx)

Operating profit (xxx) (xxx)

Dividend Income – from subsidiary xxx (xxx) -

Interest income – from subsidiary xxx (xxx) -

Interest expense (xxx) (xxx) xxx (xxx)

Profit before tax Xxx Xxx (xxx) xxx

Tax expense (xxx) (xxx) (xxx)

Share of profit from associate - - xxx xxx

Non-controlling interest (SN 7) (x) x (xxx)

Profit attributable to group Xxx Xxx (xxx) xxx

Extended Working for the Retained Earnings Extract:

Parent Co- Subsidiary Co- Adjustments Consolidated

Current year Post Acquisition Figures

Profit attributable to group Xxx xxx (xxx)/xxx Xxx

Parent – profit B/F Xx - (xx) Xxx

Subsidiary – Profit B/F xxx SN9 (xxx)/xxx XN9 Xxx

Page 17 of 43

Dividend – (SN10) (xxx) (xx) (xxx)

xxx Xxx Xxx Xxx

C/D Parent

Co RE

C/D Subsidiary

Co RE

Statement of

FP

Adjustments

Consolidated

RE

SN1 – Intra Group Sales Debit: Sales Credit: Cost of

Sales

SN2 – Unrealized Profit on Intra Group Sales Debit: Cost of

Sales

Credit: Closing

Stock

SN3 – Extra Depreciation on Fair Value adjustment of

depreciable assets of subsidiary

Debit: Cost of

Sales

Credit: Asset

SN4 – Extra Depreciation on Intra Group Sale of Fixed Assets Debit: Asset Credit: Cost of

Sales

SN5 – Gain on disposal on intra group sale of assets Debit: Cost of

Sales

Credit: Asset

SN6 – Impairment of goodwill Debit: Cost of

Sales

Credit: Goodwill

SN7 – Adjustment Profit and allocate value of NCI

Profit after tax xx

Less: Unrealized Profit on closing stock if subsidiary

company is seller (xx)

Gain on sale of fixed assets if subsidiary

company is seller (xx)

Extra depreciation because of fair value

adjustment of depreciable assets (if fair value

note recorded in S Co. books)

(xx)

Add: Extra Depreciation on intra group sale of FA

(S.co is Buyer)

Xx

Adjusted Profit Xx

Allocate NCI their share of the

profit

- Loss Share Debit: NCI Credit: P&L Note: We are allocating

subsidiary’s profit

- Profit share Debit: P&L Credit: NCI

SN8 – Only the group share of brought forward post acquisition profits

SN9 – All prior year adjustment on profit/loss

SN10 – Only the dividend paid out by the parent will appear in the extract

E-1 Highmore acquired 75% of the ordinary shares of Slowmore on that company’s incorporation on

June 01, 2004. The summarized statements of comprehensive income of the two companies for

the year ending May 31, 2009 are set out below:

Highmore Slowmore

Income statement Rs. Rs.

Sales revenue 75,000 38,000

Cost of sales 30,000 20,000

Gross profit 45,000 18,000

Administrative expenses 14,000 8,000

Profit before tax 31,000 10,000

Taxation 10,000 2,000

Profit after tax 21,000 8,000

Other comprehensive income

Gain on AFS financial assets 50,000 30,000

Revaluation surplus during the 100,000 20,000

Page 18 of 43

year

150,000 50,000

Total comprehensive income 171,000 58,000

Required: Prepare consolidated statement of comprehensive income for the year ended May 31, 2009?

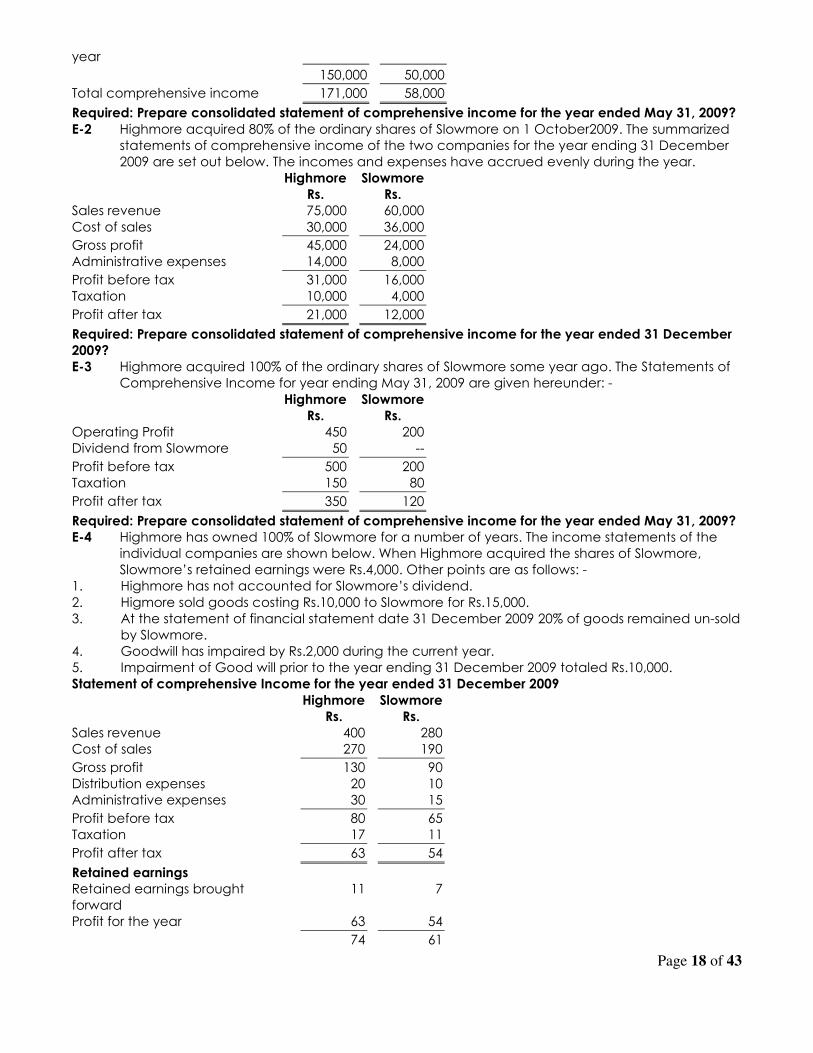

E-2 Highmore acquired 80% of the ordinary shares of Slowmore on 1 October2009. The summarized

statements of comprehensive income of the two companies for the year ending 31 December

2009 are set out below. The incomes and expenses have accrued evenly during the year.

Highmore Slowmore

Rs. Rs.

Sales revenue 75,000 60,000

Cost of sales 30,000 36,000

Gross profit 45,000 24,000

Administrative expenses 14,000 8,000

Profit before tax 31,000 16,000

Taxation 10,000 4,000

Profit after tax 21,000 12,000

Required: Prepare consolidated statement of comprehensive income for the year ended 31 December

2009?

E-3 Highmore acquired 100% of the ordinary shares of Slowmore some year ago. The Statements of

Comprehensive Income for year ending May 31, 2009 are given hereunder: -

Highmore Slowmore

Rs. Rs.

Operating Profit 450 200

Dividend from Slowmore 50 --

Profit before tax 500 200

Taxation 150 80

Profit after tax 350 120

Required: Prepare consolidated statement of comprehensive income for the year ended May 31, 2009?

E-4 Highmore has owned 100% of Slowmore for a number of years. The income statements of the

individual companies are shown below. When Highmore acquired the shares of Slowmore,

Slowmore’s retained earnings were Rs.4,000. Other points are as follows: -

1. Highmore has not accounted for Slowmore’s dividend.

2. Higmore sold goods costing Rs.10,000 to Slowmore for Rs.15,000.

3. At the statement of financial statement date 31 December 2009 20% of goods remained un-sold

by Slowmore.

4. Goodwill has impaired by Rs.2,000 during the current year.

5. Impairment of Good will prior to the year ending 31 December 2009 totaled Rs.10,000.

Statement of comprehensive Income for the year ended 31 December 2009

Highmore Slowmore

Rs. Rs.

Sales revenue 400 280

Cost of sales 270 190

Gross profit 130 90

Distribution expenses 20 10

Administrative expenses 30 15

Profit before tax 80 65

Taxation 17 11

Profit after tax 63 54

Retained earnings

Retained earnings brought

forward

11 7

Profit for the year 63 54

74 61

Page 19 of 43

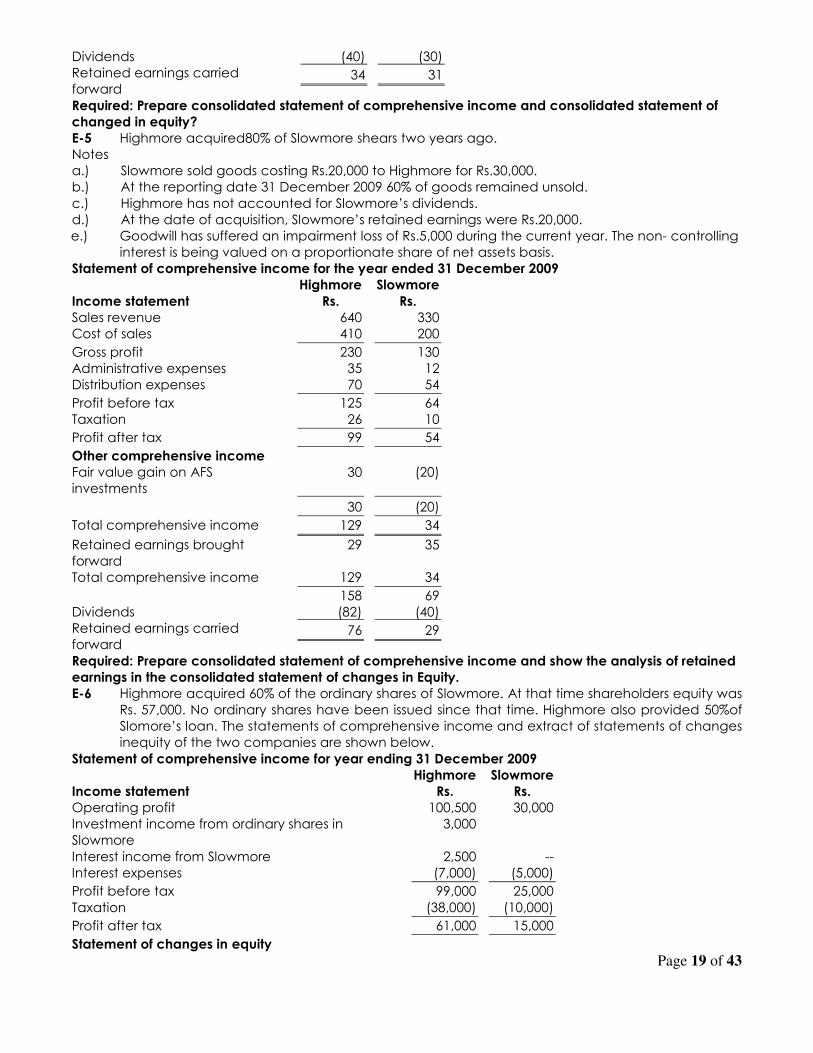

Dividends (40) (30)

Retained earnings carried

forward 34 31

Required: Prepare consolidated statement of comprehensive income and consolidated statement of

changed in equity?

E-5 Highmore acquired80% of Slowmore shears two years ago.

Notes

a.) Slowmore sold goods costing Rs.20,000 to Highmore for Rs.30,000.

b.) At the reporting date 31 December 2009 60% of goods remained unsold.

c.) Highmore has not accounted for Slowmore’s dividends.

d.) At the date of acquisition, Slowmore’s retained earnings were Rs.20,000.

e.) Goodwill has suffered an impairment loss of Rs.5,000 during the current year. The non- controlling

interest is being valued on a proportionate share of net assets basis.

Statement of comprehensive income for the year ended 31 December 2009

Highmore Slowmore

Income statement Rs. Rs.

Sales revenue 640 330

Cost of sales 410 200

Gross profit 230 130

Administrative expenses 35 12

Distribution expenses 70 54

Profit before tax 125 64

Taxation 26 10

Profit after tax 99 54

Other comprehensive income

Fair value gain on AFS

investments

30 (20)

30 (20)

Total comprehensive income 129 34

Retained earnings brought

forward

29 35

Total comprehensive income 129 34

158 69

Dividends (82) (40)

Retained earnings carried

forward 76 29

Required: Prepare consolidated statement of comprehensive income and show the analysis of retained

earnings in the consolidated statement of changes in Equity.

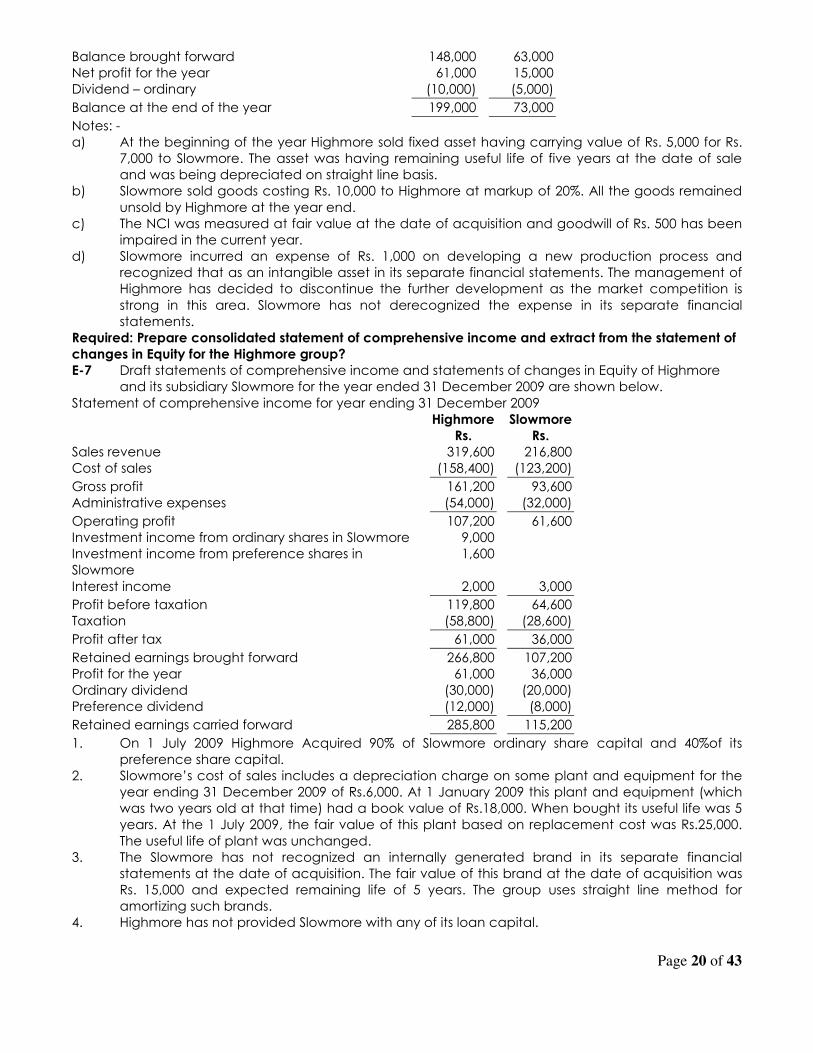

E-6 Highmore acquired 60% of the ordinary shares of Slowmore. At that time shareholders equity was

Rs. 57,000. No ordinary shares have been issued since that time. Highmore also provided 50%of

Slomore’s loan. The statements of comprehensive income and extract of statements of changes

inequity of the two companies are shown below.

Statement of comprehensive income for year ending 31 December 2009

Highmore Slowmore

Income statement Rs. Rs.

Operating profit 100,500 30,000

Investment income from ordinary shares in

Slowmore

3,000

Interest income from Slowmore 2,500 --

Interest expenses (7,000) (5,000)

Profit before tax 99,000 25,000

Taxation (38,000) (10,000)

Profit after tax 61,000 15,000

Statement of changes in equity

Page 20 of 43

Balance brought forward 148,000 63,000

Net profit for the year 61,000 15,000

Dividend – ordinary (10,000) (5,000)

Balance at the end of the year 199,000 73,000

Notes: -

a) At the beginning of the year Highmore sold fixed asset having carrying value of Rs. 5,000 for Rs.

7,000 to Slowmore. The asset was having remaining useful life of five years at the date of sale

and was being depreciated on straight line basis.

b) Slowmore sold goods costing Rs. 10,000 to Highmore at markup of 20%. All the goods remained

unsold by Highmore at the year end.

c) The NCI was measured at fair value at the date of acquisition and goodwill of Rs. 500 has been

impaired in the current year.

d) Slowmore incurred an expense of Rs. 1,000 on developing a new production process and

recognized that as an intangible asset in its separate financial statements. The management of

Highmore has decided to discontinue the further development as the market competition is

strong in this area. Slowmore has not derecognized the expense in its separate financial

statements.

Required: Prepare consolidated statement of comprehensive income and extract from the statement of

changes in Equity for the Highmore group?

E-7 Draft statements of comprehensive income and statements of changes in Equity of Highmore

and its subsidiary Slowmore for the year ended 31 December 2009 are shown below.

Statement of comprehensive income for year ending 31 December 2009

Highmore Slowmore

Rs. Rs.

Sales revenue 319,600 216,800

Cost of sales (158,400) (123,200)

Gross profit 161,200 93,600

Administrative expenses (54,000) (32,000)

Operating profit 107,200 61,600

Investment income from ordinary shares in Slowmore 9,000

Investment income from preference shares in

Slowmore

1,600

Interest income 2,000 3,000

Profit before taxation 119,800 64,600

Taxation (58,800) (28,600)

Profit after tax 61,000 36,000

Retained earnings brought forward 266,800 107,200

Profit for the year 61,000 36,000

Ordinary dividend (30,000) (20,000)

Preference dividend (12,000) (8,000)

Retained earnings carried forward 285,800 115,200

1. On 1 July 2009 Highmore Acquired 90% of Slowmore ordinary share capital and 40%of its

preference share capital.

2. Slowmore’s cost of sales includes a depreciation charge on some plant and equipment for the

year ending 31 December 2009 of Rs.6,000. At 1 January 2009 this plant and equipment (which

was two years old at that time) had a book value of Rs.18,000. When bought its useful life was 5

years. At the 1 July 2009, the fair value of this plant based on replacement cost was Rs.25,000.

The useful life of plant was unchanged.

3. The Slowmore has not recognized an internally generated brand in its separate financial

statements at the date of acquisition. The fair value of this brand at the date of acquisition was

Rs. 15,000 and expected remaining life of 5 years. The group uses straight line method for

amortizing such brands.

4. Highmore has not provided Slowmore with any of its loan capital.

Page 21 of 43

5. The revenue of Highmore includes Rs.38,000 in respect of goods sold to Slowmore at a price that

yielded a profit of 20 percent on selling price. These sales were made after acquisition. Rs.2,000

of these goods was in the closing inventory of Slowmore.

Required: Prepare consolidated statement of comprehensive income and extract from the statement of

changes in Equity for the Highmore group?

E-8 M/S Haseeb Limited acquired 75% M/S Saqib Limited on September 30, 2008 for Rs. 12 million by

paying immediately Rs. 10 million to the former owners and agreed to pay the balance amount

after one year. The discount rate Haseeb Limited uses for its present value calculation is 12%. The

profit and loss account for both the companies for the year ended December 31, 2008 is as

follows: -

Haseeb Ltd. Saqib Ltd.

(Rs. 000) (Rs. 000)

Revenue 10,000 5,000

Cost of sales (6,500) (4,000)

Gross profit 3,500 1,000

Operating cost (1,500) (400)

Operating profit 2,000 600

Tax expense (450) (200)

Profit after tax 1,550 400

Statement of changes in equity extract

Share capital 20,000 5,000

Retained earnings on January 01, 2008 15,000 7,500

The following further information is also available: -

a) The fair value of property, plant and equipment of Saqib Ltd at the date of acquisition was Rs.

1,000,000 more than its carrying value which results in extra depreciation of Rs. 45,000 in the post

acquisition period.

b) In the post acquisition period Saqib Ltd sold goods to Haseeb Ltd valuing Rs. 250,000 charging

Rs. 100,000 as margin on goods. 55% of the goods are still lying with Hasseeb Ltd.

c) All revenues and expenses have accrued evenly through the year.

d) The impairment loss on goodwill is 25% of the amount determined at the date of acquisition.

Required: -

a) Goodwill arising on acquisition

b) Consolidated Profit and loss account of Haseeb Ltd group

c) Statement of changes in equity of Haseeb Ltd Group

Page 22 of 43

ADDENDUM TO CHAPTER 5

GOODWILL IMPAIRMENT UNDER IAS 36 Introduction

In accordance with IFRS 3 (as revised in 2008), the acquirer measures and recognizes goodwill as of the

acquisition date as the excess of (a) over (b) below:

(a) the aggregate of:

(i) the consideration transferred measured in accordance with IFRS 3, which generally

requires acquisition-date fair value;

(ii) the amount of any non-controlling interest in the acquiree measured in accordance with

IFRS 3; and

(iii) in a business combination achieved in stages, the acquisition-date fair value of the

acquirer’s previously held equity interest in the acquiree.

(b) the net of the acquisition-date amounts of the identifiable assets acquired and liabilities

assumed measured in accordance with IFRS 3.

Allocation of goodwill

IAS 36 requires goodwill acquired in a business combination to be allocated to each of the acquirer’s

cash-generating units, or groups of cash-generating units, expected to benefit from the synergies of the

combination, irrespective of whether other assets or liabilities of the acquiree are assigned to those

units, or groups of units. It is possible that some of the synergies resulting from a business combination will

be allocated to a cash-generating unit in which the non-controlling interest does not have an interest.

Testing for impairment

Testing for impairment involves comparing the recoverable amount of a cash-generating unit with the

carrying amount of the cash-generating unit.

If an entity measures non-controlling interests as its proportionate interest in the net identifiable assets of

a subsidiary at the acquisition date, rather than at fair value, goodwill attributable to non-controlling

interests is included in the recoverable amount of the related cash-generating unit but is not recognized

in the parent’s consolidated financial statements. As a consequence, an entity shall gross up the

carrying amount of goodwill allocated to the unit to include the goodwill attributable to the non-

controlling interest. This adjusted carrying amount is then compared with the recoverable amount of the

unit to determine whether the cash-generating unit is impaired.

Allocating an impairment loss

IAS 36 requires any identified impairment loss to be allocated first to reduce the carrying amount of

goodwill allocated to the unit and then to the other assets of the unit pro rata on the basis of the

carrying amount of each asset in the unit.

If a subsidiary, or part of a subsidiary, with a non-controlling interest is itself a cash-generating unit, the

impairment loss is allocated between the parent and the non-controlling interest on the same basis as

that on which profit or loss is allocated.

If a subsidiary, or part of a subsidiary, with a non-controlling interest is part of a larger cash-generating

unit, goodwill impairment losses are allocated to the parts of the cash-generating unit that have a non-

controlling interest and the parts that do not. The impairment losses should be allocated to the parts of

the cash-generating unit on the basis of:

(a) to the extent that the impairment relates to goodwill in the cash-generating unit, the relative

carrying values of the goodwill of the parts before the impairment; and

(b) to the extent that the impairment relates to identifiable assets in the cash-generating unit, the

relative carrying values of the net identifiable assets of the parts before the impairment. Any

such impairment is allocated to the assets of the parts of each unit pro rata on the basis of the

carrying amount of each asset in the part.

In those parts that have a non-controlling interest, the impairment loss is allocated between the parent

and the non-controlling interest on the same basis as that on which profit or loss is allocated.

If an impairment loss attributable to a non-controlling interest relates to goodwill that is not recognized in

the parent’s consolidated financial statements, that impairment is not recognized as a goodwill

impairment loss. In such cases, only the impairment loss relating to the goodwill that is allocated to the

parent is recognized as a goodwill impairment loss.

Page 23 of 43

Example # 1

Parent acquires an 80 per cent ownership interest in Subsidiary for CU2,100 on 1 January 20X3. At that

date, Subsidiary’s net identifiable assets have a fair value of CU1,500. Parent chooses to measure the

non-controlling interests as the proportionate interest of Subsidiary’s net identifiable assets of CU300 (20%

of CU1,500). Goodwill of CU900 is the difference between the aggregate of the consideration

transferred and the amount of the non-controlling interests

(CU2,100 + CU300) and the net identifiable assets (CU1,500).

The assets of Subsidiary together are the smallest group of assets that generate cash inflows that are

largely independent of the cash inflows from other assets or groups of assets. Therefore Subsidiary is a

cash-generating unit. Because other cash-generating units of Parent are expected to benefit from the

synergies of the combination, the goodwill of CU500 related to those synergies has been allocated to

other cash-generating units within Parent. Because the cash-generating unit comprising Subsidiary

includes goodwill within its carrying amount, it must be tested for impairment annually, or more

frequently if there is an indication that it may be impaired (see paragraph 90 of IAS 36).

At the end of 20X3, Parent determines that the recoverable amount of cash-generating unit Subsidiary is

CU1,000. The carrying amount of the net assets of Subsidiary, excluding goodwill, is CU1,350.

Required: - Calculate and allocated impairment loss to goodwill and other assets, also identify the share

of loss of NCI and Group?

Example # 2

Parent acquires an 80 per cent ownership interest in Subsidiary for CU2,100 on 1 January 20X3. At that

date, Subsidiary’s net identifiable assets have a fair value of CU1,500. Parent chooses to measure the

non-controlling interests at fair value, which is CU350. Goodwill of CU950 is the difference between the

aggregate of the consideration transferred and the amount of the non-controlling interests (CU2,100 +

CU350) and the net identifiable assets (CU1,500).

The assets of Subsidiary together are the smallest group of assets that generate cash inflows that are

largely independent of the cash inflows from other assets or groups of assets. Therefore, Subsidiary is a

cash-generating unit. Because other cash-generating units of Parent are expected to benefit from the

synergies of the combination, the goodwill of CU500 related to those synergies has been allocated to

other cash-generating units within Parent. Because Subsidiary includes goodwill within its carrying

amount, it must be tested for impairment annually or more frequently if there is an indication that it

might be impaired.

Testing Subsidiary for impairment

At the end of 20X3, Parent determines that the recoverable amount of cash-generating unit Subsidiary is

CU1,650. The carrying amount of the net assets of Subsidiary, excluding goodwill, is CU1,350. Required: - Calculate and allocated impairment loss to goodwill and other assets, also identify the share of loss of

NCI and Group?

Past Papers On January 1, 2008, Misbah Holding Limited, dealing in textile goods, acquired 90% ownership interest in

Salman Limited (SL), a ginning company, against cash payment of Rs. 450 million. At that date, SL’s net

identifiable assets had a book value of Rs. 350 million and fair value of Rs. 400 million.

It is the policy of the company to measure the non-controlling interest at their proportionate share of

SL’s net identifiable assets.

During the year ended December 31, 2008, SL incurred a net loss of Rs. 150 million. The impairment

testing exercise carried out at the end of the year, by a firm of consultants, showed that the

recoverable amount of SL’s business is Rs. 200 million. However, the Board of Directors is inclined to take

a second opinion as they estimate that the recoverable amount is Rs. 390 million.

Required:

Based on each of the two valuations, compute the amounts to be reported in the consolidated

statement of financial position as of December 31, 2008 in respect of:

• Goodwill;

• Net identifiable assets, and

• Non-controlling interest. (15)

Page 24 of 43

CLASS ASSIGNMENT 1

Q-1

On 31 December 2009 P acquired all the shares of S for Rs.60,000. The statements of financial position of

the individual enterprises at that date were as follows:

Statement of financial position as at 31 December 2009 P S

Rs. Rs.

Total Assets

Non-current assets:

Property Plant & Equipment 120,000 40,000

Investment in shares of S 60,000 -

______ ______

180,000 40,000

Net Current Assets 20,000 10,000

______ ______

200,000 50,000

_______ ______

Equity and Liabilities

Capital and reserves:

Ordinary Shares of Rs 10.00 each 100,000 20,000

Retained Profits 100,000 30,000

_______ ______

200,000 50,000

Required:

Prepare the consolidated statement of financial position for the P Group on 31 December 2009.

Q-2

On 31 December 2008 Pacemaker acquired all the shares of Syclop for Rs. 60,000. At that time Syclop

accumulated profits were Rs. 30,000. The statements of financial position of the individual enterprises at

31 December 2009 were as follows:

Statements of financial position as at 31 December 2009 Pacemaker Syclop

Rs. Rs.

Total Assets

Non-current assets:

Property Plant & Equipment 160,000 50,000

Investment in shares of Syclop 60,000 -

_______ ______

220,000 50,000

Net Current Assets 30,000 10,000

______ ______

250,000 60,000

Equity and Liabilities

Capital and Reserves:

Ordinary shares of Rs. 10.00 each 100,000 20,000

Retained Profits 150,000 40,000

_______ ______

250,000 60,000

Consolidated Goodwill is subjected to an annual impairment review. No impairment has been

detected to date.

Required:

Prepare the consolidated statement of financial position for the pacemaker group on 31 December

2009.

Q-3

On 31 December 2009 Pedantic acquired 3,200 ordinary shares of Sophistic for Rs. 120,000. The

statements of financial position of the individual enterprises at 31 December 2009 were as follows:

Page 25 of 43

Statements of financial position as at 31 December 2009 Pedantic Sophistic

Rs. Rs.

Total Assets

Non-current assets:

Property Plant & Equipment 240,000 80,000

Investment in shares of Sophistic 120,000 -

_______ ______

360,000 80,000

Net Current Assets 40,000 20,000

_______ ______

400,000 100,000

Equity and Liabilities

Capital and Reserves:

Ordinary shares of Rs.10 each 200,000 40,000

Retained Profits 200,000 60,000

_______ ______

400,000 100,000

It is group policy to value non-controlling interest at its proportionate share of the subsidiary’s identifiable

net assets.

Required:

Prepare the Pedantic group’s consolidated statement of financial position at 31 December 20X1.

Q-4

On 31 December 20008, Patronic acquired 2,800 ordinary shares of Sardonic for Rs. 120,000. At that time

Sardonic accumulated profits were Rs. 60,000. The statements of financial position of the individual

enterprises at 31 December 2009 were as follows:

Statements of financial position as at 31 December 2009 Patronic Sardonic

Rs. Rs.

Total Assets

Non-current assets:

Property Plant & Equipment 320,000 100,000

Investment in shares of Sardonic 120,000 -

_______ _______

440,000 100,000

Net Current Assets

60,000 20,000

______ ______

500,000 120,000

Equity and Liabilities

Capital and Reserves:

Ordinary shares of Rs. 10 each 200,000 40,000

Retained Profits 300,000 80,000

______ ______

500,000 120,000

Note consolidated Goodwill is subjected to an annual impairment review. No impairment has been

detected to date. It is group policy to value non-controlling interest (NCI) at fair value; the fair value of

NCI was Rs. 35,600 at the date of acquisition.

Page 26 of 43

ASSIGNMENT # 2

Q-1

On 1 January 2009 PARVEZ acquired 1,800 ordinary shares of SAJID. At that time SAJID retained profits

were Rs. 16,000. The statements of financial position of the individual enterprises at 31 December 2009

are as follows:

Statements of financial position as at 31 December 2009 PARVEZ SAJID

Rs. Rs.

Total Assets

Non-current assets:

Property Plant & Equipment 120,000 40,000

Cost of Investment in shares of SAJID 40,000 -

_______ ______

160,000 40,000

Current Assets

Inventories 20,000 10,000

Receivables 40,000 30,000

Current A/c with SAJID 16,000 -

Cash 4,000 -

_______ ______

240,000 80,000

Equity and Liabilities

Capital and Reserves:

Ordinary shares of Rs. 10.00 each 100,000 24,000

Retained Profits 120,000 20,000

_______ ______

220,000 44,000

Current Liabilities:

Accounts payable 20,000 18,000

Current account with PARVEZ - 12,000

Bank Overdraft -

6,000 _______ ______

240,000 80,000

1. On 28th December 20X2 SAJID sent a cheque for Rs. 4,000 to PARVEZ. PERVEZ did not

account for this cheque until early January 20X3.

2. The group policy is to measure non-controlling interest at Fair value at the date of

acquisition. The fair value OF NCI was Rs. 15,000.

3. The fair value of Property, plant and equipment was Rs. 2,000 more than their carrying value

at the date of acquisition and those assets still exist in the statement of financial position of

the entity at the year end.

4. Consolidated goodwill is subject to an annual impairment review. The impairment loss

attributable to goodwill is Rs. 4,500.

Required: Prepare the PARVEZ group’s consolidated statement of financial position at 31 December

2009.

Q-2 The draft statement of financial position at 31 March 2002 of Window Limited and its 80%

subsidiary Glass Ltd, acquired on 30 September 2001, are as follows:

Window Glass

Limited Limited

Rs 000 Rs 000

Fixed assets

Intangible assets

Patents - 400

Goodwill - 550

Tangible assets 6,276 1,104

Page 27 of 43

Investments: Shares in Glass Ltd 180 -

6,456 2,054

Current assets

Stocks 1,854 806

Debtors 1,950 846

Suspense account 256 -

Cash 1,672 264

5,732 1,916

Creditors: amounts falling due within one year (3,428) (1,040)

Net current assets 2,304 876

Total assets less current liabilities 8,760 2,930

Capital and reserves

Called up share capital

Ordinary Rs 10 shares 4,000 1,400

Revaluation reserve 950 -

Profit and loss account 3,810 1,530

8,760 2,930

The following points are relevant.

(i) At acquisition the statement of financial position of Glass Ltd showed net assets with a

book value of Rs 2,530,000. Included in this total are freehold land with a book value of

Rs.500,000 (market value Rs 1,200,000), patents with a book value of Rs 400,000(market

value Rs 450,000) and goodwill (arising on the acquisition of an unincorporated business

some years ago) with a book value of Rs 600,000 (impairment loss of 50,000 has been

recognized in the post acquisition period by the acquiree). The fair values of all other

assets and liabilities are approximately equal to their book values. The above fair value

adjustments have not been incorporated in the separate books of Glass Limited.

(ii) The directors of Window Limited intend to restructure and reorganize Glass Ltd and wish

to provide for future losses and restructuring costs which are forecasted at Rs 116,000.

(iii) An investment in plant and machinery will be required to bring the remaining production

line of Glass Ltd up to date. This will amount to Rs 580,000 in the next 12 months.

(iv) The consideration comprised cash of Rs 180,000 and 80,000 shares of Window Limited

issued at a nominal value of Rs 10 and fair value of Rs 26 each. The shares have not yet

been reflected in the books of Window Limited.

(v) Professional fees to bankers and solicitors in respect of the acquisition amounted to Rs

150,000. In addition the directors of Window Limited estimate that the value of their time

spent on working the acquisition amounted to Rs 106,000.

(vi) Glass Ltd sells part of its output to Window Limited. Included in the stock of Window

Limited are goods valued at Rs 300,000 purchased from Glass Ltd at cost plus 25%.

(vii) Group policy is to measure full goodwill the fair value of NCI at the date of acquisition

was Rs. 20 per share.

Required:

(a) Calculate the value of goodwill if any arising on the acquisition of Glass Ltd.

(b) Show the Share Capital and Reserves on the consolidated statement of financial position of

Window Limited as at March 31 2002.

Page 28 of 43

ASSIGNMENT # 3

Q – 1

M/S Haneef Ltd purchased entire share capital of M/S Sajid Power Ltd at the date of its incorporation,

several years before. The shares were purchased at par value of Rs. 10 each. The total number of shares

issued by Sajid Power Ltd was 100 million. Following is the trial balance of both the companies for the

year ended June 30, 2009.

Haneef Ltd Sajid Ltd

Debit Credit Debit Credit

Rs. (m) Rs. (m) Rs. (m) Rs. (m)

Sales -- 12,000 -- 7,500

Cost of investment in Sajid Ltd 1,000 -- -- --

Cost of sales 6,500 -- 4,500 --

Operating expenses 3,500 -- 1,500 --

Closing stock 2,300 -- 2,000 --

Property, plant and

equipment

3,500 -- 1,200 --

Accumulated depreciation

b/f

-- 1,500 -- 700

Dividend income from Sajid

Ltd

-- 1,000 -- --

Ordinary share capital -- 3,000 -- 1,000

Retained earnings opening -- 2,500 -- 2,000

Creditors -- 500 -- 300

Due from Sajid Ltd 1,000 -- -- --

Debtors 2,500 -- 1,500 --

Cash and bank balance 200 -- 500 --

Due to Haneef Ltd -- -- -- 700

Dividend paid -- -- 1,000 --

20,500 20,500 12,200 12,200

Further, the following intra group transactions took place.

a) Haneef Ltd sold goods worth Rs. 500 million to Sajid Ltd during the year of which 1/5th are still in

the inventory of Sajid Ltd. Haneef Ltd charges 20% margin on all goods it sells to associated

companies.

b) The intra group balances are not reconciled because of a cheque in transit of Rs. 200 million

sent by Sajid Ltd to Haneef Ltd and Rs. 100 million management fee charged by Haneef Ltd to

Sajid Ltd.

c) The depreciation for the year is not charged in the above balances, the group uses 20%

depreciation rate for all its property, plant and equipment on reducing balance basis. The

depreciation is to be charged in cost of sales.

Required: - Prepare consolidated statement of financial position as on June 30, 2009, statement of

comprehensive income and consolidated statement of changes in equity for the year ended June 30,

2009?

Q – 2

M/S Haneef Ltd purchased entire share capital of M/S Sajid Ltd on July 01, 2008 by paying Rs. 12 per

share and issued one share for every five shares of Sajid Ltd. The par value per share of Sajid Ltd is Rs. 10.

Following is the trial balance of both the companies for the year ended June 30, 2009. The market value

of Haneef Ltd shares at the date of acquisition was Rs. 20 each.

Haneef Ltd Sajid Ltd

Debit Credit Debit Credit

Rs. (m) Rs. (m) Rs. (m) Rs. (m)

Sales -- 12,000 -- 7,500

Cost of investment in Sajid Ltd 1,200 -- -- --

Cost of sales 6,500 -- 4,500 --

Operating expenses 3,500 -- 1,500 --

Page 29 of 43

Closing stock 2,300 -- 2,000 --

Property, plant and

equipment

3,300 -- 1,200 --

Accumulated depreciation

b/f

-- 1,500 -- 700

Dividend income from Sajid

Ltd

-- 500 -- --

Ordinary share capital -- 3,000 -- 1,000

Retained earnings opening -- 2,500 -- 500

Creditors -- 500 -- 1,300

Due from Sajid Ltd 1,000 -- -- --

Debtors 2,000 -- 1,500 --

Cash and bank balance 200 -- 500 --

Due to Haneef Ltd -- -- -- 700

Dividend paid -- -- 500 --

20,000 20,000 11,700 11,700

Further, the following intra group transactions took place.

a) Haneef Ltd sold goods worth Rs. 500 million to Sajid Ltd during the year of which 1/5th are still in

the inventory of Sajid Ltd. Haneef Ltd charges 20% margin on all goods it sells to associated

companies.

b) The intra group balances are not reconciled because of a cheque in transit of Rs. 200 million

sent by Sajid Ltd to Haneef Ltd and Rs. 100 million management fee charged by Haneef Ltd to

Sajid Ltd.

c) The depreciation for the year is not charged in the above balances, the group uses 20%

depreciation rate for all its property, plant and equipment on reducing balance basis. The

depreciation is to be charged in cost of sales.

Required: - Prepare consolidated statement of financial position as at June 30, 2009, statement of

comprehensive income and consolidated statement of changes in equity for the year ended June 30,

2009?

PAST PAPERS

Q – 1

Following is the summarised trial balance of Faisal Limited (FL) and its subsidiaries, Saqib Limited (SL) and

Ayaz Industries Limited (AIL) for the year ended December 31, 2007:

FL SL AIL

Rs. (m) Rs. (m) Rs. (m)

Cash and bank balances 4,920 660 2,700

Accounts receivable 6,240 2,460 6,580

Stocks in trade – closing 14,460 4,200 5,680

Investment in subsidiaries – at cost

SL 9,000

AIL 10,500

Other investments 11,100

Property, plant and equipment 22,500 3,480 5,940

Cost of sales 49,200 18,000 21,000

Operating expenses 3,600 2,100 5,400

Accumulated depreciation (5,760) (420) (1,260)

Ordinary share capital (Rs. 10 each (30,000) (12,000) (6,000)

Retained earnings – opening (33,780) (4,800)

Sales (57,600) (16,500) (33,800)

Accounts payable (2,760) (1,980) (1,440)

Gain on sale of fixed assets (540)

Dividend income (1,080)

Following additional information is also available: -

Page 30 of 43

i) On January 01, 2007, FL acquired 480 million shares of AIL from its major shareholders for Rs.

10,500 million.

ii) SL was incorporated on February 01, 2007. 75% of the shares were acquired by FL at par value

on the same date.

iii) The following intercompany sales were made during the year 2007: -

Sales Included in

buyer’s closing

stocks in trade

Amount

receivable /

payable at year

end

Gross profit %

on sales

Rs. (m) Rs. (m) Rs. (m) Rs. (m)

FL to AIL 2400 900 20

SL to AIL 1800 600 800 10

AIL to FL 3600 1200 30

FL and its subsidiaries value stock in trade at the lower of cost or net realizable value. While

valuing FL’s stock in trade, the stock purchased from AIL has been written down by Rs. 100

million.

iv) On July 01, 2007, FL sold certain plants and machines to SL. Detail of the transaction are as

follows: -

Rs. (m)

Sale value 144

Less: cost of plant and machineries 150

Accumulated depreciation (60)

Net book value 90

Gain on sale of plants 54

The plants and machineries were purchased on January 01, 2005, and were being depreciated

on straight line method over a period of five years. SL computed depreciation thereon using

the same method based on the remaining useful life.

FL billed Rs. 100 million to each subsidiary for management services provided during the year

2007 and credited it to operating expenses. The invoices were paid on December 15, 2007.

v) Details of cash are as follows:-

Dividend

Date of declaration Date of payment %

FL Nov 25, 2007 Jan 5, 2008 20

AIL Oct 15, 2007 Nov 20, 2007 10

Required: -

Prepare consolidated balance sheet and profit and loss account of FL and its subsidiaries for the year

ended December 31, 2007. Ignore tax and corresponding figures.

Q – 2

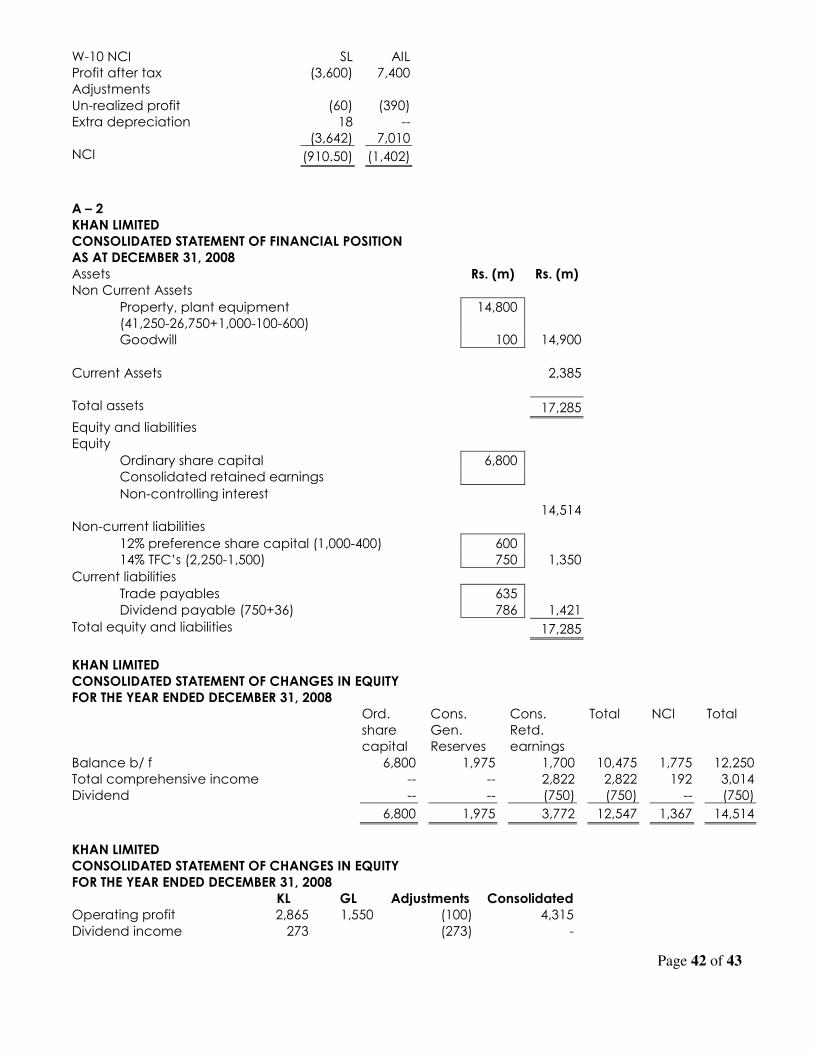

On January 1, 2002, Khan Limited (KL) acquired 375 million ordinary shares and 40 million preference

shares in Gul Limited (GL) whose general reserve and retained earnings on the date of acquisition,

stood at Rs. 200 million and Rs. 1,000 million respectively.

The following balances were extracted from the records of KL and its subsidiary on December 31, 2008:

KL GL

Debit Credit Debit Credit

Rs. (m) Rs. (m) Rs. (m) Rs. (m)

Ordinary share capital (Rs. 10 each) 6,800 5,000

12% Preference share capital (Rs. 10 each) 1,000

General reserve 1,750 500

Retained earnings 2,000 1,200

Loan from KL at 15% rate of interest 2,000

14% Term Finance Certificates (TFCs) (Rs. 100

each)

2,250

Page 31 of 43

Accounts payable 445 190

Dividend payable – preference shares 60

Dividend payable – ordinary shares 750 300

Property, plant and equipment - at cost 16,250 25,000

Property, plant and equipment - acc.

depreciation

9,750 17,000

Investment in ordinary shares of GL 5,500

Investment in preference shares of GL 400

Loan to GL at 15% rate of interest 2,000

Investment in KL's TFCs (purchased at par value) 1,500

Profit before tax, interest and dividend 2,865 1,550

Dividend income 273

Interest income 300 210

Dividend receivable 249

Current assets 1,069 1,316

Interest on TFCs 315

Interest on loan from KL 300

Taxation 650 474

Preference dividend 120

Ordinary dividend – interim 750 300

27,183 27,183 29,010 29,010

Following relevant information is available: -

i) At the date of acquisition the fair value of buildings included in property, plant and equipment

of GL was assessed at Rs. 1000 million above its carrying value. All other identifiable assets and

liabilities were considered to be fairly valued. GL provided for depreciation on building at 10%

on the straight line basis.

ii) GL purchased the TFC in KL on January 01, 2008.

iii) The non controlling interest is measured at their proportionate share of the GL’s identifiable net

assets.

iv) There is no impairment in the value of goodwill since its acquisition.

v) There are no components of other comprehensive income.

Required: -

Prepare the following in accordance with the requirement of International Financial Reporting

Standards: -

(a) Consolidated statement of financial position as at December 31, 2008.

(b) Consolidated statement of comprehensive income for the year ended December 31, 2008.

(c) Consolidated statement of retained earnings for the year ended December 31, 2008.

Note:

Ignore deferred tax and corresponding figures.

Notes to the above statements are not required. However, show workings wherever it is necessary.

Page 32 of 43

ANSWERS TO ASSIGNMENTS

Assignment # 1

A-1

P Group

Consolidated statement of financial position

As at December 31, 2009

Rs. Rs.

Assets

Non-current assets

Property, plant and equipment 160,000

Goodwill 10,000

170,000

Current assets

Net current assets 30,000

200,000

Equity

Ordinary share capital 100,000

Consolidated retrained earnings 100,000 200,000

W-1 Group structure %

Group 100

NCI --

100

W-2 Cost of control account Debit Credit

Investment 60,000

Share capital 20,000

Pre-acquisition retained earnings 30,000

Goodwill 10,000

60,000 60,000

A-2

Pacemaker Group

Consolidated statement of financial position

As at December 31, 2009

Rs. Rs.

Assets

Non-current assets

Property, plant and equipment 210,000

Goodwill 10,000

220,000

Current assets

Net current assets 40,000

260,000

Equity

Ordinary share capital 100,000

Consolidated retrained earnings

(150,000+10,000)

160,000 260,000

W-1 Group structure %

Group 100

NCI --

100

Page 33 of 43

W-2 Cost of control account Debit Credit

Investment 60,000

Share capital 20,000

Pre-acquisition retained earnings 30,000

Goodwill 10,000

60,000 60,000

A-3

Pedantic Group

Consolidated statement of financial position

As at December 31, 2009

Rs. Rs.

Assets

Non-current assets

Property, plant and equipment 320,000

Goodwill 40,000

360,000

Current assets

Net current assets 60,000

420,000

Equity

Ordinary share capital 200,000

Consolidated retrained earnings 200,000 400,000

NCI 20,000

420,000

W-1 Group structure %

Group 80

NCI 20

100

W-2 Cost of control account Debit Credit

Investment 120,000

Share capital 32,000

Pre-acquisition retained earnings

(60,000x0.80)

48,000

Goodwill 40,000

120,000 120,000

W-3 NCI

Share capital 8,000

SRE-pre 12,000

C/ d 20,000

20,000 20,000

A-4

Patronic Group

Consolidated statement of financial position

As at December 31, 2009

Rs. Rs.

Assets

Non-current assets

Property, plant and equipment 420,000

Goodwill (50,000+5,600) 55,600

475,600

Current assets

Net current assets 80,000

Page 34 of 43

555,600

Equity

Ordinary share capital 200,000

Consolidated retrained earnings

(300,000+14,000)

314,000 514,000

NCI 41,600

555,600

W-1 Group structure %

Group 70

NCI 30

100

W-2 Cost of control account Debit Credit

Investment 120,000

Share capital (40,000 x 0.70) 28,000

Pre-acquisition retained earnings (60,000x0.70) 42,000

Goodwill 50,000

120,000 120,000

W-3 NCI

Share capital 12,000

SRE-pre 18,000

SRE-post (20,000x0.30) 6,000

Goodwill 5,600

C/ d 41,600

41,600 41,600

W-4 NCI goodwill

Fair value of NCI 35,600

Share capital 12,000

SRE-pre 18,000

Goodwill 5,600

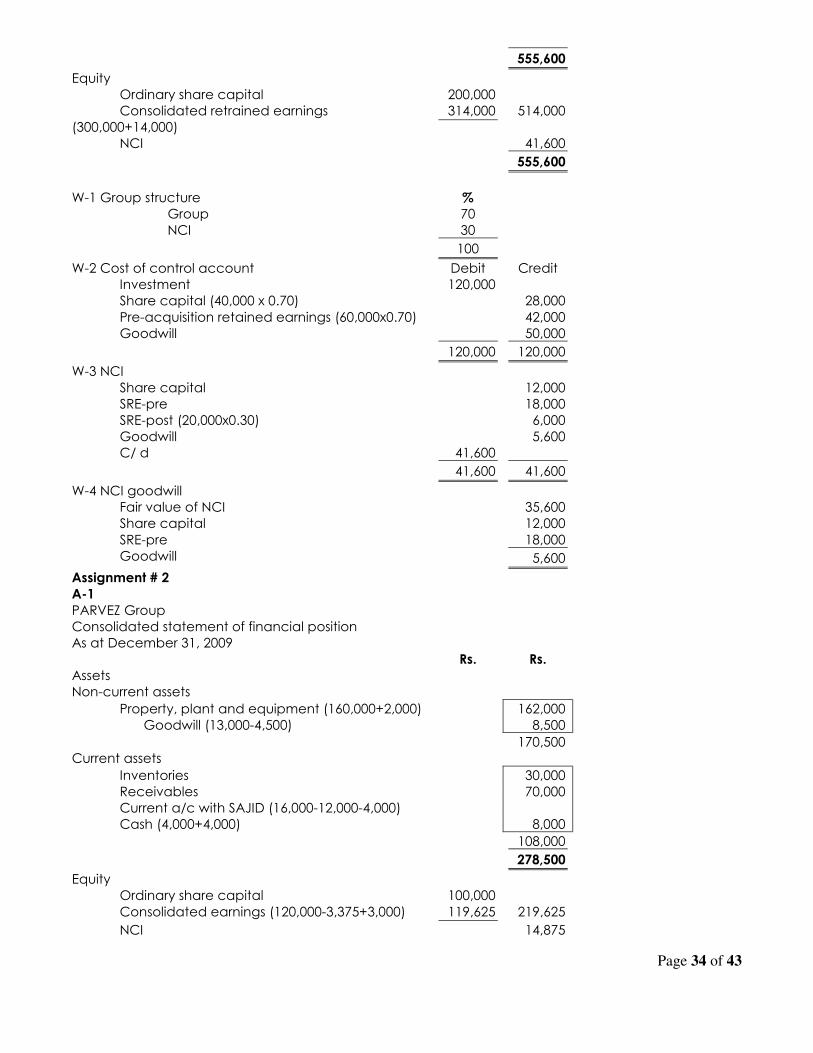

Assignment # 2

A-1

PARVEZ Group

Consolidated statement of financial position

As at December 31, 2009

Rs. Rs.

Assets

Non-current assets

Property, plant and equipment (160,000+2,000) 162,000

Goodwill (13,000-4,500) 8,500

170,500

Current assets

Inventories 30,000

Receivables 70,000

Current a/c with SAJID (16,000-12,000-4,000)

Cash (4,000+4,000) 8,000

108,000

278,500

Equity

Ordinary share capital 100,000

Consolidated earnings (120,000-3,375+3,000) 119,625 219,625

NCI 14,875

Page 35 of 43

234,500

Current liabilities

Accounts payable 38,000

Bank overdraft 6,000

44,000

278,500

W-1 Group structure %

Group 75

NCI 25

100

W-2 Cost of control account Debit Credit

Investment 40,000

Share capital (24,000x.75) 18,000

Pre-acquisition retained earnings (18,000x.75) 13,500

Goodwill 8,500

40,000 40,000

W-3 NCI

Share capital 6,000

SRE-pre 4,500

SRE-post (4,000x.25) 1,000

Goodwill 4,500

Impairment loss 1,125

C/ d 14,875

16,000 16,000

W-4 NCI goodwill

Fair value of NCI 15,000

Share capital (6,000)

SRE-pre (4,500)

Goodwill 4,500

W-5 Subsidiary Retained Earnings

At reporting date 20,000

Fair value gain (pre) 2,000

Pre-acquisition (18,000)

Post acquisition 4,000

A – 2

WINDO LIMITED

CONSOLIDATED STATEMENT OF FINANCIAL STATEMENT

AS AT MARCH 31, 2001

Rs. (000) Rs. (000)

FIXED ASSETS

Intangible assets

Patents (400+50) 450

Goodwill 140

Tangible assets (7,380+700) 8,080 8,670

CURRENT ASSETS

Stocks (2,660-60) 2,600

Debtors 2,796

Cash 1,936 7,332

16,002

EQUITY AND LIABILITIES

Page 36 of 43

Equity

Ordinary share capital

(4,000+800)

4,800

Share premium 1,280

Revaluation reserve 950

Retained earnings 3,866 10,896

NCI 638

11,534

Current liabilities

Creditors 4,468

16,002

Workings

W-1

Group retained earnings (Parent co.) 3,810

Suspense account (256)

Share of post acquisition profits 312

3,866

W-2 Dr. Cr.

Subsidiary retained earnings

Balance 1,530

Fair value gain (700+50) 750

Goodwill 550