chapter 7 engineering economic analysis time value of money

Post on 21-Dec-2015

238 views

TRANSCRIPT

Chapter 7

Engineering Economic AnalysisTime Value of Money

Definitions

P – Principal or Present Value (of an investment)

Fn – Future Value (of an investment)

n – Years ( or other time unit) between P and F i – Interest Rate (based on time interval for n) per anum

Basis premise: Money when invested earns money

$1 today is worth more than $1 in the Future

Interest

Simple Interest – Annual Basis Simple Interest – Annual Basis Interest paid in any year = Interest paid in any year = PiPis s

PiPiss – Fraction of investment paid as – Fraction of investment paid as

interest per year interest per year

After After nn years total interest paid = years total interest paid = PiPissn n Total investment is worth = Total investment is worth = PP + + PiPissnn

Could earn interest on earned interest Could earn interest on earned interest

Interest

Compound Interest Compound Interest At time 0 we have P At time 0 we have P

At the end of Year 1, we have At the end of Year 1, we have FF11 = = PP (1 + (1 + ii) )

At the end of Year 2, we have At the end of Year 2, we have FF22 = = PP (1 + (1 + ii))2 2

At the end of Year n, we have At the end of Year n, we have FFnn = = PP (1 + (1 + ii))n n

or or PP = = FFnn / (1 + / (1 + ii))n n

Example

How much would i need to invest at 8 % How much would i need to invest at 8 % p.a. to yield $5000 in 10 years p.a. to yield $5000 in 10 years

97.2315$

08.01

5000

5000

10

08.0

10

10

P

F

n

i

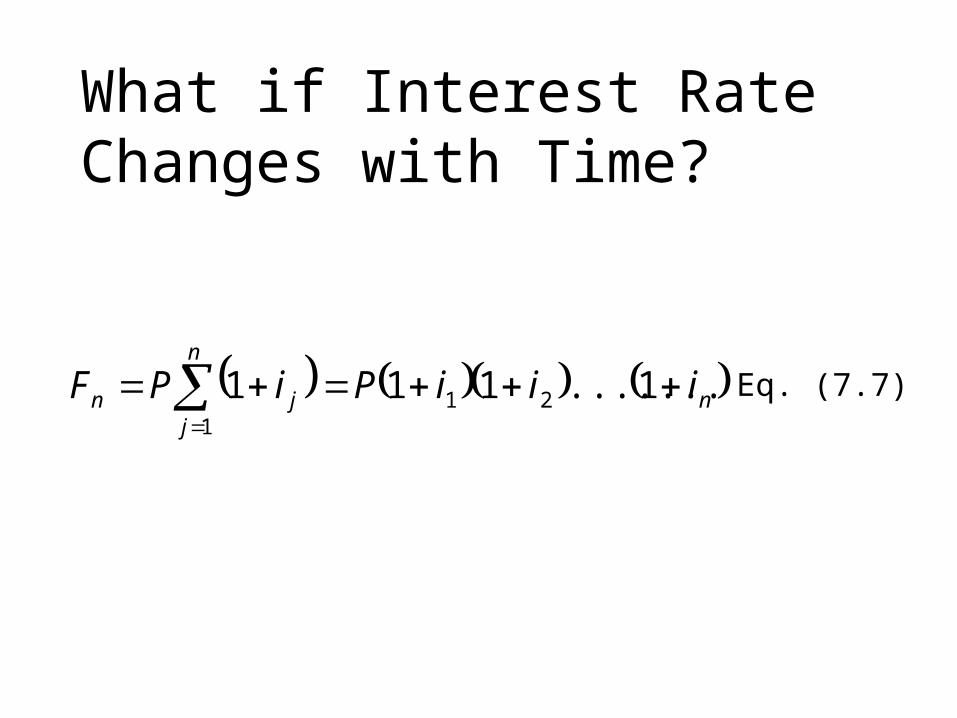

What if Interest Rate Changes with Time?

n

n

jjn iiiPiPF

1.......111 211

Eq. (7.7)

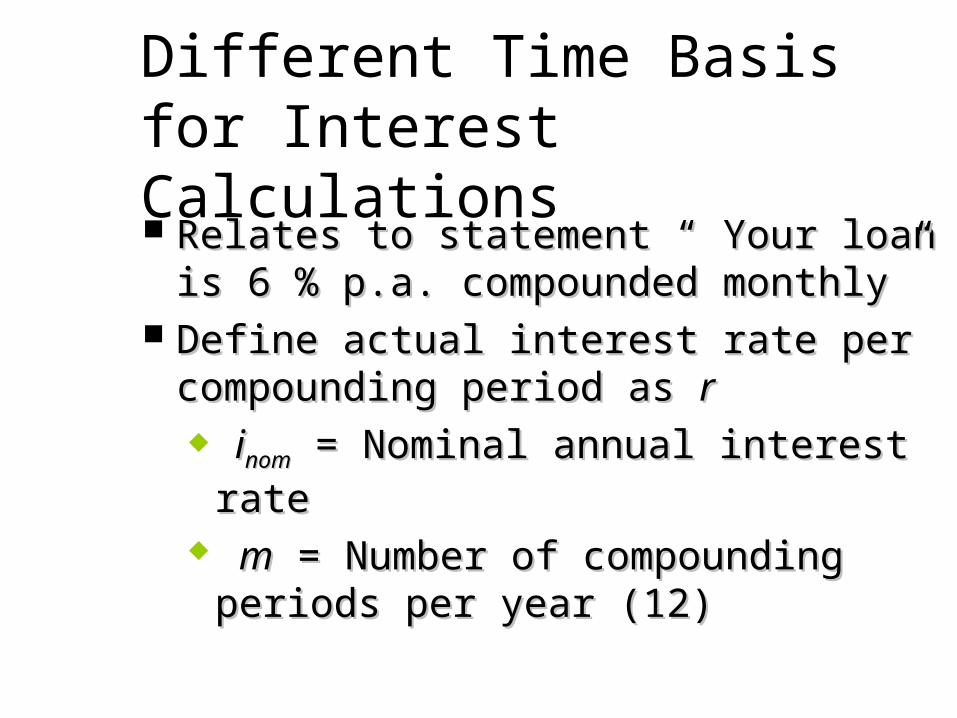

Different Time Basis for Interest Calculations Relates to statement “ Your loan is 6 % p.a. Relates to statement “ Your loan is 6 % p.a.

compounded monthly” compounded monthly” Define actual interest rate per compounding Define actual interest rate per compounding

period as period as rriinomnom = Nominal annual interest rate = Nominal annual interest rate mm = Number of compounding periods = Number of compounding periods

per year (12)per year (12)

Different Time Basis for Interest Calculations cont.

iieffeff = Effective annual interest rate = Effective annual interest rate

Look at condition after 1 yearLook at condition after 1 year

m

ir nom

effiPF 11

11

mnom

eff m

ii

Example

Invest $1000 at 10 % p.a. compounded Invest $1000 at 10 % p.a. compounded monthly. How much do I have in 1 year, 10 monthly. How much do I have in 1 year, 10 years?years?

04.2707$1

1047.0112

10.01

71.1104$12

10.0110001

1010

12

12

1

eff

eff

m

nom

iPF

i

m

iPF

Example cont.

As m decreases As m decreases iieffeff increases increases

Is there a limit as Is there a limit as mm goes to infinity goes to infinity Yes – continuously compounded Yes – continuously compounded

interest interest Derivation – pp. 229-230 Derivation – pp. 229-230 iieffeff (continuous) = e (continuous) = eiinom nom – 1– 1

Cash Flow Diagrams

Represent timings and approximate Represent timings and approximate magnitude of investment on a cfd magnitude of investment on a cfd xx-axis is time and -axis is time and yy-axis is magnitude -axis is magnitude both positive and negative investments both positive and negative investments

are possible. are possible. In order to determine direction (sign) of In order to determine direction (sign) of

cash flows, we must define what system is cash flows, we must define what system is being considered. being considered.

Consider a Discrete Cash Flow Diagram

Discrete refers to individual cfds that are Discrete refers to individual cfds that are plottedplotted

Example

I borrow $20 K for a car and repay as a I borrow $20 K for a car and repay as a $400 monthly payment for 5 years.$400 monthly payment for 5 years.

For Bank For Me

1 2 3

$400

60321

$2000

60

$400

$2000

Cumulative CFD

Cumulative CFD

Annuities

1 2 3 n

Uniform series of equally spaced – equal value cash flows

Annuities

What is future value What is future value FFnn = ? = ?

Geometric progressionGeometric progression

AiAiAF nnn .....11 21

i

iASF

n

nn

11

Calculations with Cash Flow Diagrams

Invest 5K, 1K, 2K at End of Years 0, 1, 3, Invest 5K, 1K, 2K at End of Years 0, 1, 3,

and take 3K at End of Year 4and take 3K at End of Year 4

0

$3000

$2000$1000

$5000

3

74

1

Example 1

How much in account at end of Year 7 if i = How much in account at end of Year 7 if i = 8% p.a. 8% p.a.

What would investment be at Year 0 be to get What would investment be at Year 0 be to get

this amount at Year 7 this amount at Year 7

84.9097$

08.013000

08.01200008.01100008.01000,5

7

3

4677

F

F

50.5308

08.1

84.90977

P

Example 2

What should my annual monthly car What should my annual monthly car payment be if interest rate is 8% p.a. payment be if interest rate is 8% p.a. compounded monthly?compounded monthly?

$20,000

A

Example 2 cont. Compare at Compare at nn = 60 = 60

53.405$

090.2979647.73

90.2979612

08.01000,20

47.73

1208.0

11208.0

1

60

60

60

60

A

A

F

AAF

Discount Factors

Just a shorthand symbol for a formula in Just a shorthand symbol for a formula in ii and and nn

n

n

n

nn

ii

ini

F

PPA

iFni

F

PFP

ini

F

P

i

FP

1

11,,

1

1,,

1

1,,

1

Table 7.1

Depreciation

Total Capital Investment = Fixed Capital + Total Capital Investment = Fixed Capital + Working Capital Working Capital Fixed Capital – All costs associated with Fixed Capital – All costs associated with

new construction, but new construction, but LandLand cannot be cannot be depreciated depreciated

Working Capital – Float of material to Working Capital – Float of material to start operations cannot depreciatestart operations cannot depreciate

WCLandFCITCI L

Definitions

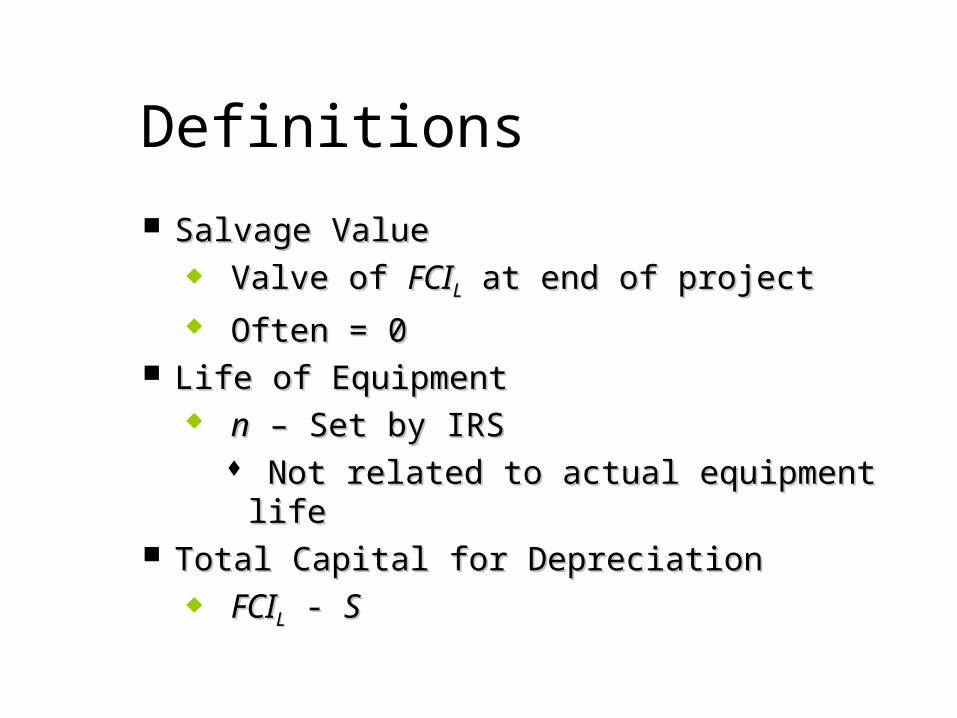

Salvage Value Salvage Value Valve of Valve of FCIFCILL at end of project at end of project Often = 0 Often = 0

Life of Equipment Life of Equipment nn – Set by IRS – Set by IRS

Not related to actual equipment life Not related to actual equipment life Total Capital for Depreciation Total Capital for Depreciation

FCIFCILL - - SS

3 Basic Methods for Depreciation

Straight Line Straight Line Sum of Years Digits (SOYD) Sum of Years Digits (SOYD) Double Deruning Balance (DDB)Double Deruning Balance (DDB)

Straight Line

n

SFCId LSL

k

n = # of years

Sum of Years Digits (SOYD)

1

2

11

nn

SFCIknd LSOYD

k

SOYD

Double Declining Balance (DDB)

1

0

2 k

jjL

DDBk dFCI

nd

Example 7.21

207

10150

1

7

1010$

10150$6

6

SL

st

L

d

Year

n

S

FCI

Same for Years 1-7

Example 7.21 (cont’d)

6.309.421507

2

9.421507

2

301015028

610150

872

1217

351015028

710150

872

1117

2

1

2

1

DDB

DDB

SOYD

SOYD

d

d

d

d

Taxation, Cash Flow, and Profit

Tables 7.3 – 7.4 Tables 7.3 – 7.4 Expenses = Expenses = COMCOMdd + + ddk k

Income Tax = (Income Tax = (RR – – COMCOMdd - - ddkk))t t After Tax (net)Profit = After Tax (net)Profit =

((RR – – COMCOMdd – –ddkk)(1 – )(1 – tt) ) After Tax Cash Flow = After Tax Cash Flow =

((RR – – COMCOMdd – – ddkk)(1 – )(1 – tt) + ) + ddk k

Inflation

$ Now Net Worth vs. $ Next Year $ Now Net Worth vs. $ Next Year

jCEPCIfnjCEPCI n 1

Inflation

Purchasing Power vs time Purchasing Power vs time

ff = Average inflation rate between Years = Average inflation rate between Years jj and and nn

fi

fifii

'

1

' 1 '1

nn

n

F iF P P i

fi f

Homework

• Problems 7.1- 7.8 – 7.9 – 7.19 – 7.20 – 7.21 – 7.22