chapter 7 - mgmt-026 | uc merced - 2 c omponents of a ccounting s ystems c1 •keyboards •scanners...

TRANSCRIPT

PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 7

ACCOUNTING INFORMATION SYSTEMS

7 - 2

COMPONENTS OF ACCOUNTING SYSTEMS C1

•Keyboards •Scanners •Modems •Bar-Code Reader

•Hardware •Software •Professional Judgment

Increasingly, source documents are electronic files creating a “paperless”

system.

7 - 3

COMPONENTS OF ACCOUNTING SYSTEMS C1

•CD/DVD •Hard Drive •Tape •Paper Document

•Printer •Monitor •Projectors •Web communications

7 - 4

SPECIAL JOURNALS IN ACCOUNTING C2

7 - 5

SUBSIDIARY LEDGERS

Subsidiary ledgers are a listing of individual accounts with common characteristics.

Characteristic Controlling Account Subsidiary Ledger

Amounts due from customers

Accounts Receivable

Accounts Receivable Ledger

Amounts owed to creditors

Accounts Payable

Accounts Payable Ledger

C3

7 - 6

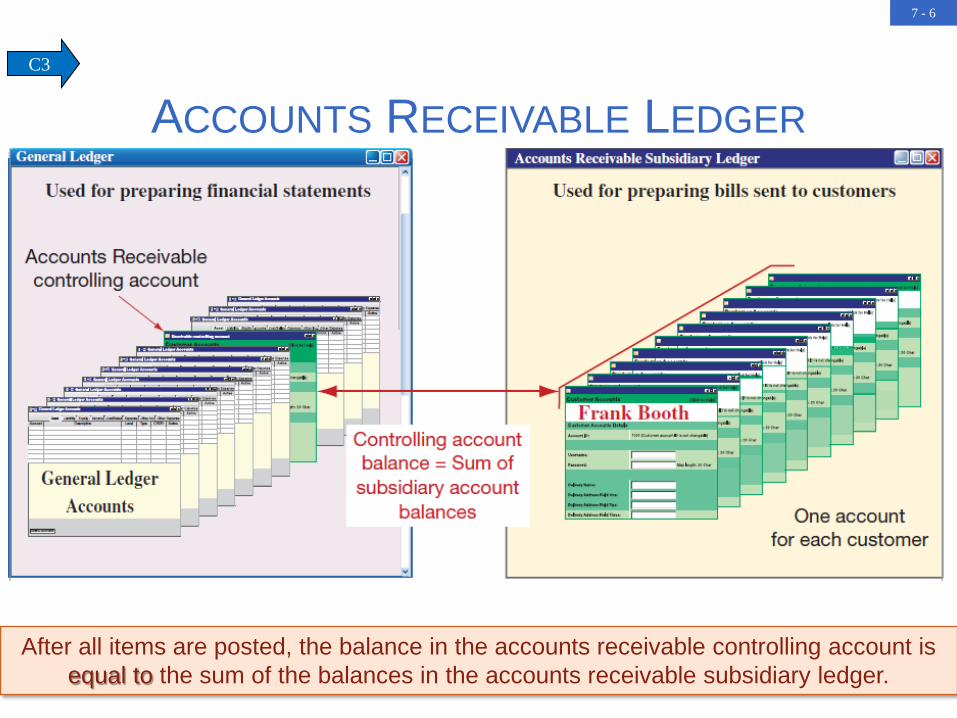

ACCOUNTS RECEIVABLE LEDGER

After all items are posted, the balance in the accounts receivable controlling account is equal to the sum of the balances in the accounts receivable subsidiary ledger.

C3

7 - 7

SALES JOURNAL P1

7 - 8

PROVING THE LEDGERS P2

The balance of the Accounts Receivable controlling account in the general ledger should equal the accounts

in the accounts receivable subsidiary ledger.

A schedule of accounts receivable lists each customer

and the balance owed.

7 - 9

SALES TAXES P1

Governmental agencies often require sellers to collect sales taxes from customers and to periodically send these taxes

to the appropriate agency.

7 - 10

P1

Cash Receipts Types 1. Cash from credit

customers 2. Cash from cash

sales 3. Cash from other

sources

7 - 11

FOOTING, CROSSFOOTING, AND POSTING P1

7 - 12

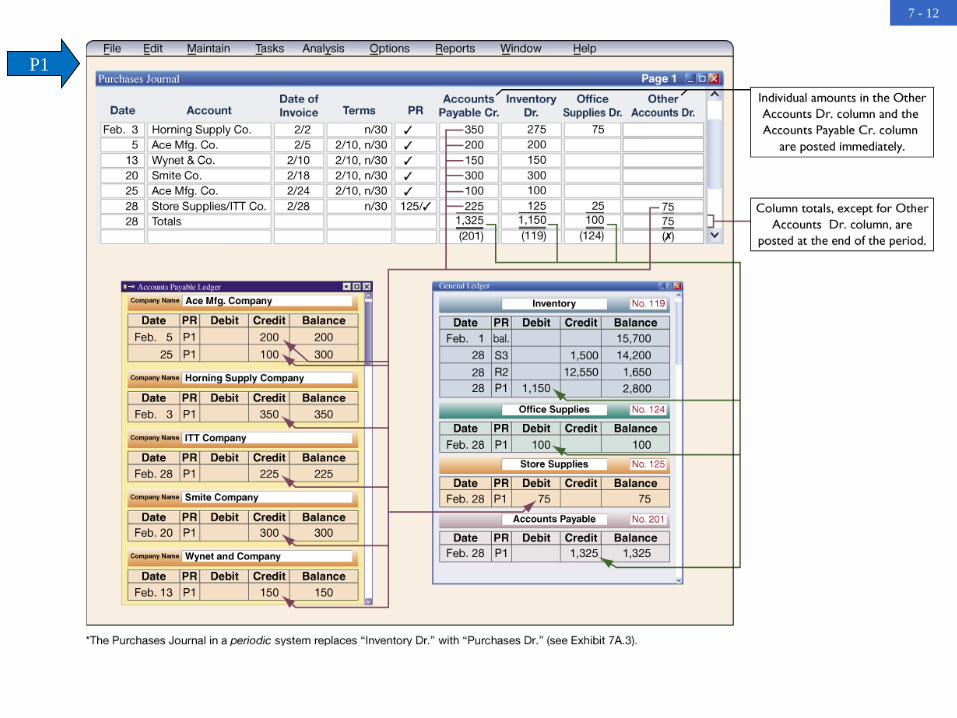

P1

7 - 13

PROVING THE LEDGER P2

The balance of the Accounts Payable controlling account in the general ledger should equal the

accounts in the accounts payable subsidiary ledger.

A schedule of accounts payable lists each supplier and the balance owed to them.

7 - 14

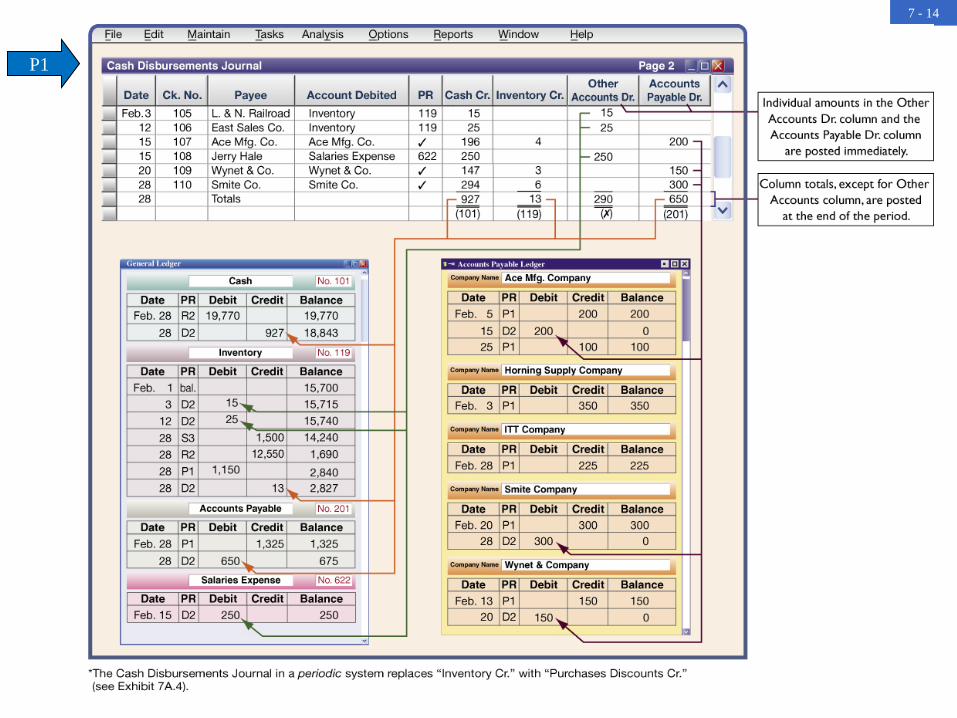

P1

7 - 15

GENERAL JOURNAL TRANSACTIONS Adjusting Entries

Purchase Returns &

Allowances

Closing Entries

P1

Sales Returns & Allowances

7 - 16

END OF CHAPTER 7