chapter 9: finance - robertleecannon.com€¦ · • how do financial managers evaluate capital...

TRANSCRIPT

© 2009 South-Western, a division of Cengage Learning

1

Chapter 9: FINANCE

Using Funds To Maximize Value

© 2009 South-Western, a division of Cengage Learning

2

LOOKING AHEAD

• How does maximizing financial value relate to social responsibility?

• How do financial managers use key ratios?

• How do financial managers use cash budgets?

• Why is working capital management important?

• How do financial managers evaluate capital budgeting proposals?

• How do financial managers determine the firm’s capital structure?

© 2009 South-Western, a division of Cengage Learning

3

WHAT MOTIVATES FINANCIAL DECISIONS

• What types of assets do we need to achieve goals?

• How do we get the funds we need?

• Evaluate financial performance

• Plan financial resources

• Manage working capital

• Evaluate investment opportunities

• Determine appropriate strategy

© 2009 South-Western, a division of Cengage Learning

4

%

EVALUATING PERFORMANCE: WHERE DO WE STAND?

• Financial ratios provide insight into financial strengths and weaknesses

• Use financial data from balance sheet and income statement

• Companies can compare their ratios with other businesses

© 2009 South-Western, a division of Cengage Learning

5

KEY FINANCIAL RATIOS

RATIO TYPE HOW IT IS COMPUTED

Current Liquidity: ability to pay short-term liabilities.

Current Assets

Current Liabilities

Inventory

Turnover

Asset Management: how firm is using assets to generate revenue.

Cost of Good Sold

Average Inventory

Debt-to-equity Leverage: extent to which a firm relies on debt.

Total Debt

Total Owner’s Equity

© 2009 South-Western, a division of Cengage Learning

6

KEY FINANCIAL RATIOS

RATIO TYPE HOW IT IS COMPUTED

Debt-to-assets

Leverage: measures the extent to which a relies on debt

Total Debt

Total Assets

Return on equity

Profitability: compares the amount of profit compared to resources invested

Net Income – Preferred Div

Avg Common Stock Equity

Return on assets

Profitability: compares the amount of profit compared to resources invested

Net Income

Average Total Assets

Earnings per share

Profitability: compares the amount of profit compared to resources invested

Net Income – Pref Dividends

Avg # of Shares Out

© 2009 South-Western, a division of Cengage Learning

7

FINANCIAL PLANNING: PROVIDING A ROAD MAP FOR

• What assets must be obtained?

• How much additional financing is needed?

• How much can the firm generate Internally? Externally?

• When will external financing be required?

© 2009 South-Western, a division of Cengage Learning

8

BASIC PLANNING TOOLS

Pro Forma Income Statement – forecasts the sales,

expenses and net income

Pro Forma Balance Sheet – forecasts the types and amounts

of assets a firm will need to carry out plans.

Cash Budget – detailed projection of

cash flows to determine when cash shortages

and surpluses will occur.

© 2009 South-Western, a division of Cengage Learning

9

CASH BUDGET

© 2009 South-Western, a division of Cengage Learning

10

MANAGING WORKING CAPITAL: CURRENT EVENTS

• Net Working Capital:

– Difference between current assets and liabilities

• Working capital must be managed

– Appropriate level of current assets

– Current liabilities needed to finance activities

© 2009 South-Western, a division of Cengage Learning

11

MANAGING CASH

• Need cash to pay bills

• Cash does not earn returns

• Report cash equivalents as cash

– Commercial Paper

– T-Bills

– Money Market Mutual Funds

© 2009 South-Western, a division of Cengage Learning

12

CASH EQUIVALENTS

• Commercial Paper– Short-term unsecured promissory note (IOUs).

– Issued by major corporations with excellent credit rating

– Sold at a discount; price plus interest is paid when the paper comes due

• T-bills– Short-term IOUs issued by the U.S. government.

– T-Bills normal mature in 4, 13, or 26 weeks

– Sold at a discount; face value is paid at maturity

– Good market for T-Bills since they are backed by the government

• Money Market Mutual Funds– Pooled funds to purchase a portfolio of short-term, liquid securities

– Affordable way for small investors to get into the market

© 2009 South-Western, a division of Cengage Learning

13

MANAGING ACCOUNTS RECEIVABLE

• Set Credit Terms

• Establish Credit Standards

• Design Appropriate Collection Policy

Accounts Receivable - Money which is owed to a company by a customer for products and services provided on credit.

© 2009 South-Western, a division of Cengage Learning

14

SMALL LOANS MAKE A BIG DIFFERENCE

• Muhammad Yunus and the bank he founded won the Nobel Peace prize for his research and development of microcredit

• Grammen Bank provides small loans to poor entrepreneurs in third-world countries.

© 2009 South-Western, a division of Cengage Learning

15

SHORT-TERM FINANCING

• Spontaneous Financing

– Trade Credit

• Short-Term Bank Loans

– Line of Credit

– Revolving Credit

• Factoring

• Commercial Paper

© 2009 South-Western, a division of Cengage Learning

16

BORROWING MONEY

““

“If you want to know the value of

money, go and try to borrow some.”

- Benjamin Franklin

© 2009 South-Western, a division of Cengage Learning

17

CAPITAL BUDGETING: IN IT FOR THE LONG HAUL

• Replace machines and equipment

• New machines and equipment

• Build a new factory, warehouse or office

• Introduce a new product line

Capital Budgeting – a systematic evaluation of a firm’s major long-run

capital investment opportunities.

© 2009 South-Western, a division of Cengage Learning

18

COMPARING CASH FLOWS THAT OCCUR AT DIFFERENT

Managers must evaluate costs and benefits of investment that occur over a period of many years.

Time Value of Money – a dollar received today is worth more than a dollar received in the future.

Compounding – earning interest in the current period on interest from previous periods.

© 2009 South-Western, a division of Cengage Learning

19

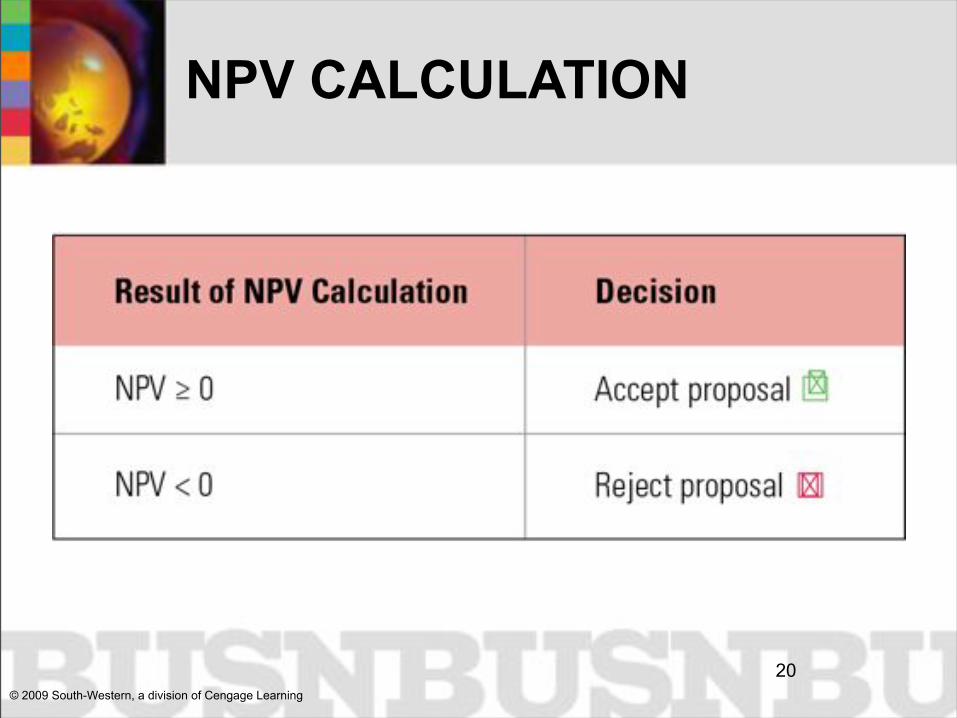

USING NET PRESENT VALUE TO EVALUATE CAPITAL

• Managers use the process of discounting to calculate the present value.

• Present value depends on the interest rate the invested money will earn.

• Net present value is the present value of all cash flows associated with an investment, including the initial (negative) cash flow of the investment.

Present Value – How much a given amount of cash received in a future period is worth today, given the time

value of money.

© 2009 South-Western, a division of Cengage Learning

20

NPV CALCULATION

© 2009 South-Western, a division of Cengage Learning

21

SOURCES OF LONG-TERM CAPITAL: LOANERS VS.

Capital Structure – the mix of equity and debt financing a firm uses for financing needs.

Debt Financing – creditors.

Equity Financing – owners.

© 2009 South-Western, a division of Cengage Learning

22

SOURCES OF DEBT FINANCING

• Long-term loans

• Private placements

• Issuing notes or bonds

© 2009 South-Western, a division of Cengage Learning

23

SOURCES OF EQUITY FINANCING

• Direct contributions by owners

– Owners directly contribute resources to unincorporated businesses

– Corporations raise equity capital by issuing stock

• Retained earnings

• Equity financing provides more flexibility than debt financing

© 2009 South-Western, a division of Cengage Learning

24

FINANCIAL LEVERAGE: USING DEBT TO MAGNIFY GAINS

• Heavy debt in capital structure

• Potential high returns to owners

• Increased risk

© 2009 South-Western, a division of Cengage Learning

25

FINANCING YOUR EDUCATION

• How are you currently financing your education?

• How leveraged are you?

• What are the sources of your equity financing?

• What are the advantages/disadvantages to your capital structure?

• What adjustments might you consider?

© 2009 South-Western, a division of Cengage Learning

26

LOOKING BACK

• How does maximizing financial value relate to social responsibility?

• How do financial managers use key ratios to evaluate the firm?

• How do financial managers use cash budgets?

• Why is working capital management important?

• How do financial managers evaluate capital budgeting proposals?

• How do financial managers determine the firm’s capital structure?