chapter 9 investing in long-term debt (bonds). characteristics of all bonds interest - coupon rate...

TRANSCRIPT

Chapter 9

Investing in Long-Term Debt (Bonds)

Characteristics of All Bonds

• Interest - coupon rate

• Principal amount

• Maturity date

Characteristics of All Bonds

• The indenture

• The trustee

• Yield– Current yield– Yield to maturity

Risk to Bondholders

• Default - failure to meet the terms of the indenture

• Fluctuations in interest rates

• Reinvestment rate risk

• Loss of purchasing power

Importance of Ratings

• Investment grade - triple B or better

• Non-investment grade (high-yield bonds)

• Moody’s and Standard & Poor’s ratings

Importance of Ratings

• Similarity of ratings

• Ratings do change

Types of Corporate Bonds

• Mortgage bonds

• Equipment trust certificates

• Debentures

• Subordinated debentures

• Income and revenue bonds

Types of Corporate Bonds

• Convertible bonds

• Variable interest rates bonds

• Zero coupon and discount bonds

• Eurobonds

High-yield (Junk) Bonds

• Non-investment grade

• Poor quality increases the yields over investment grade bonds

Bonds are Issued as

• Bearer bond

• Registered bond

• Book-entry bond

Price of a Bond

• The present value of the cash flows

• Interest and principal are discounted back to the present at the going rate of interest on comparable debt

Comparable Debt

• Same term to maturity

• Same risk class

Comparable Debt

• Comparable bonds

–can have different coupons

–can have different prices

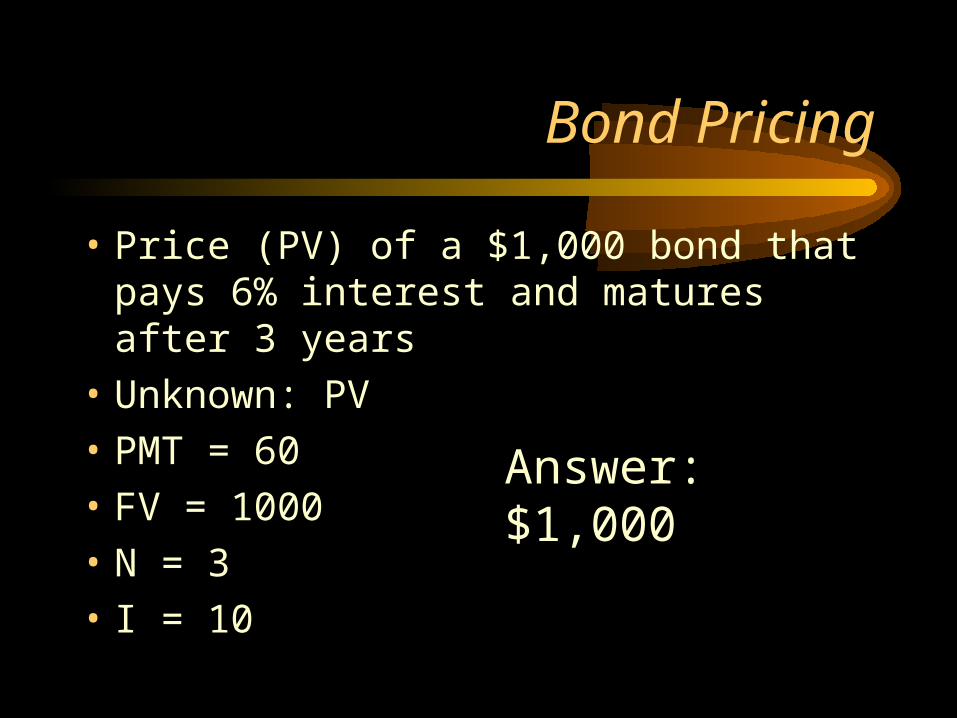

Bond Pricing

• Price (PV) of a $1,000 bond that pays 6% interest and matures after 3 years

• Unknown: PV

• PMT = 60

• FV = 1000

• N = 3

• I = 10

Answer: $1,000

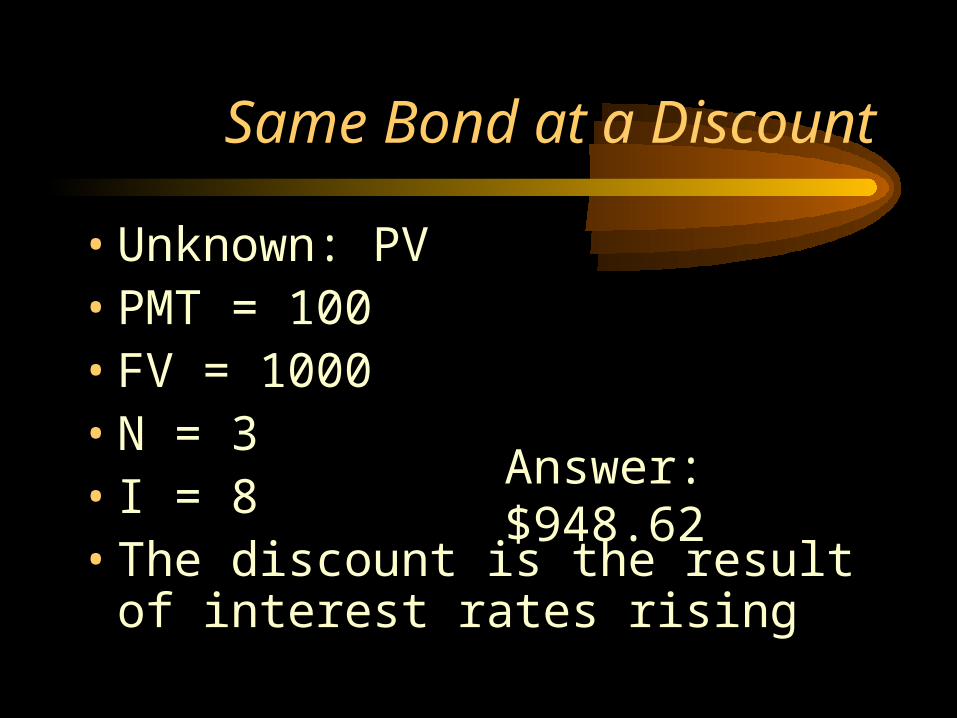

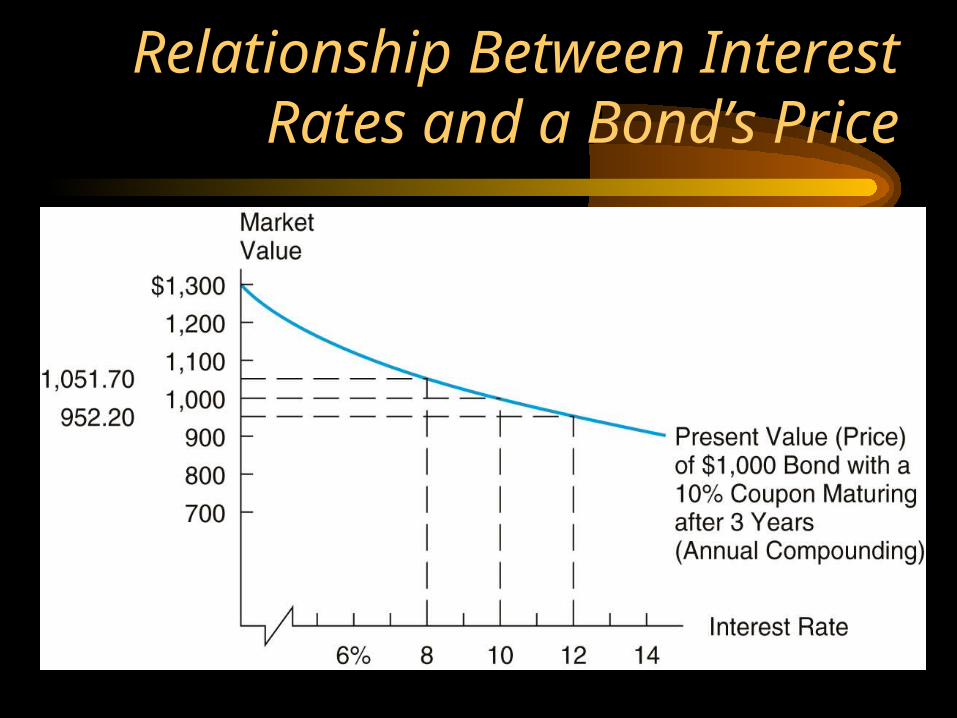

Same Bond at a Discount

• Unknown: PV• PMT = 100• FV = 1000• N = 3• I = 8• The discount is the result of interest

rates rising

Answer: $948.62

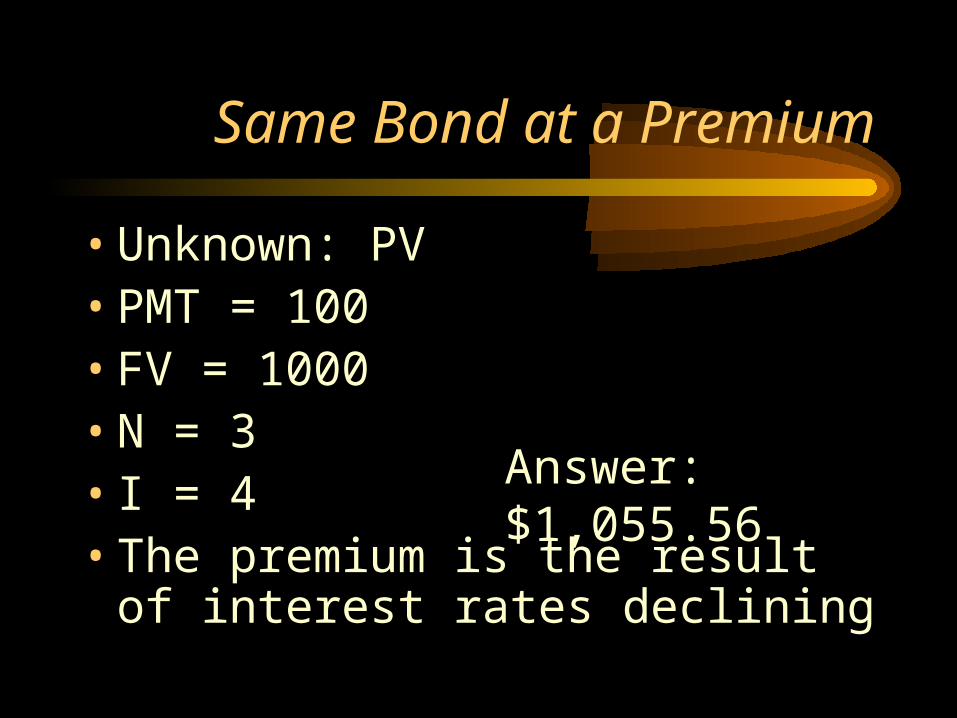

Same Bond at a Premium

• Unknown: PV• PMT = 100• FV = 1000• N = 3• I = 4• The premium is the result of

interest rates declining

Answer: $1,055.56

Relationship

• The inverse relationship between

–Bond prices and

–Interest rates

• Interest rate risk–Higher rates cause bond prices to

decline

Relationship Between Interest Rates and a Bond’s Price

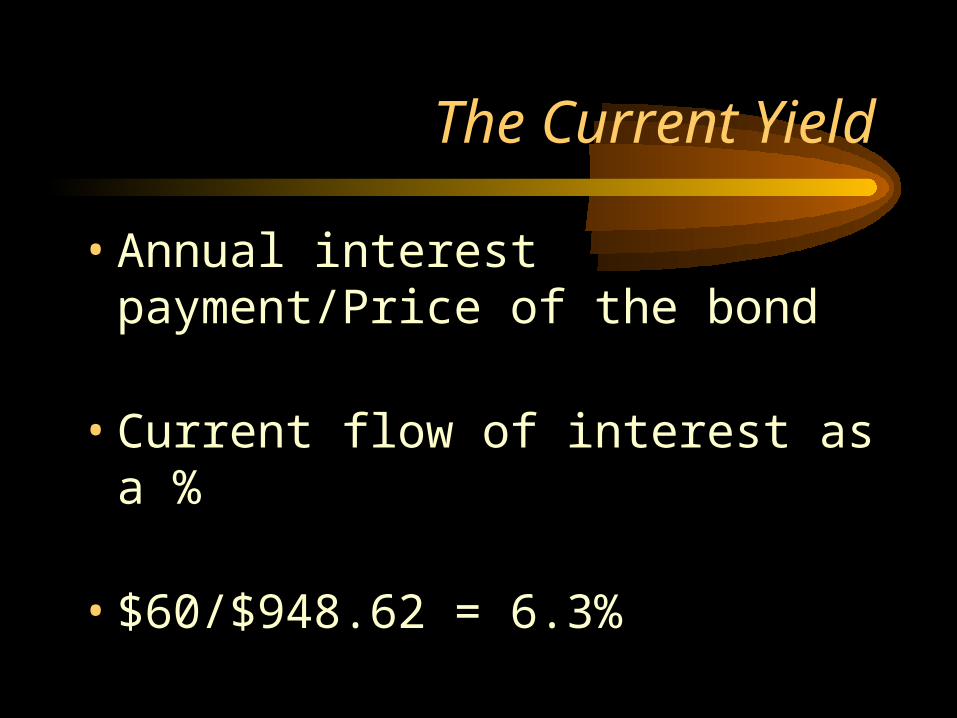

The Current Yield

• Annual interest payment/Price of the bond

• Current flow of interest as a %

• $60/$948.62 = 6.3%

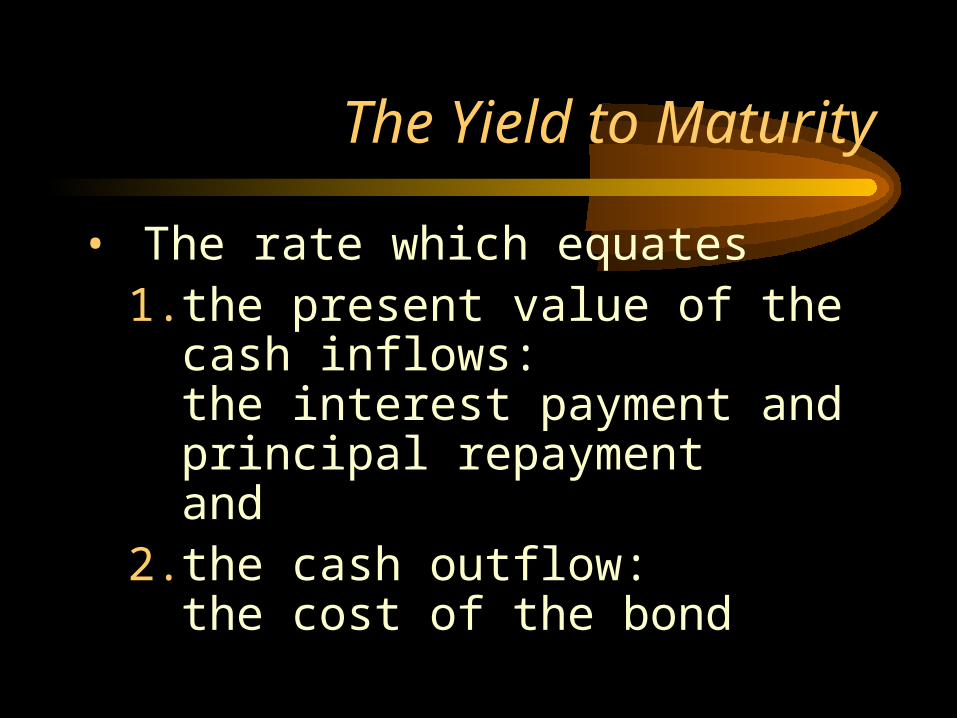

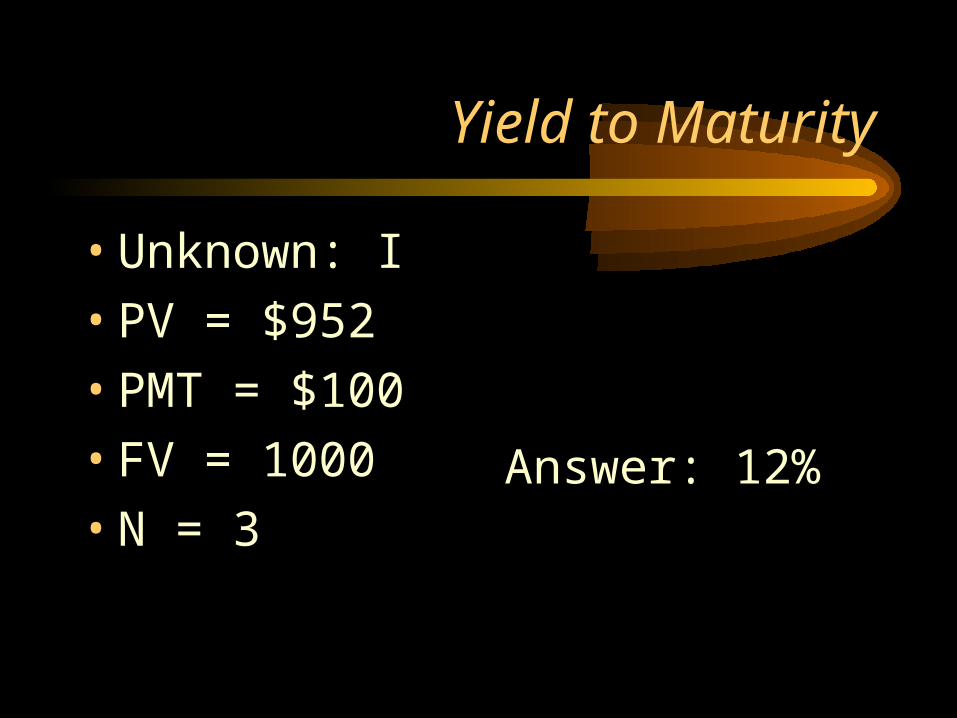

The Yield to Maturity

• The rate which equates 1. the present value of the cash

inflows:the interest payment and principal repayment and

2. the cash outflow:the cost of the bond

Yield to Maturity

• Unknown: I

• PV = $952

• PMT = $100

• FV = 1000

• N = 3Answer: 12%

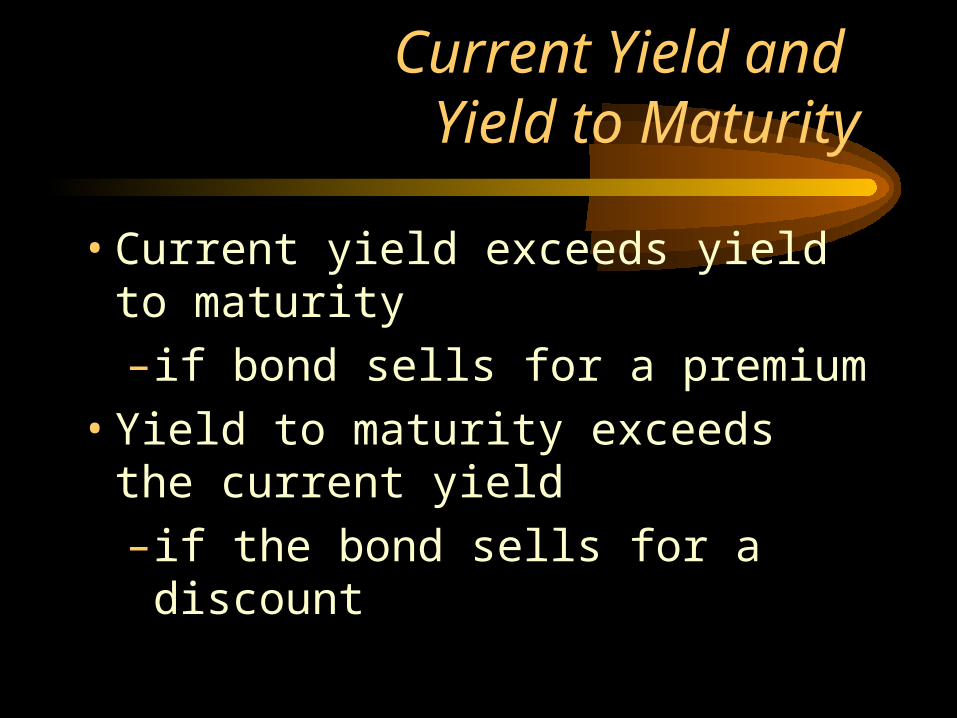

Current Yield and Yield to Maturity

• Current yield exceeds yield to maturity

–if bond sells for a premium

• Yield to maturity exceeds the current yield

–if the bond sells for a discount

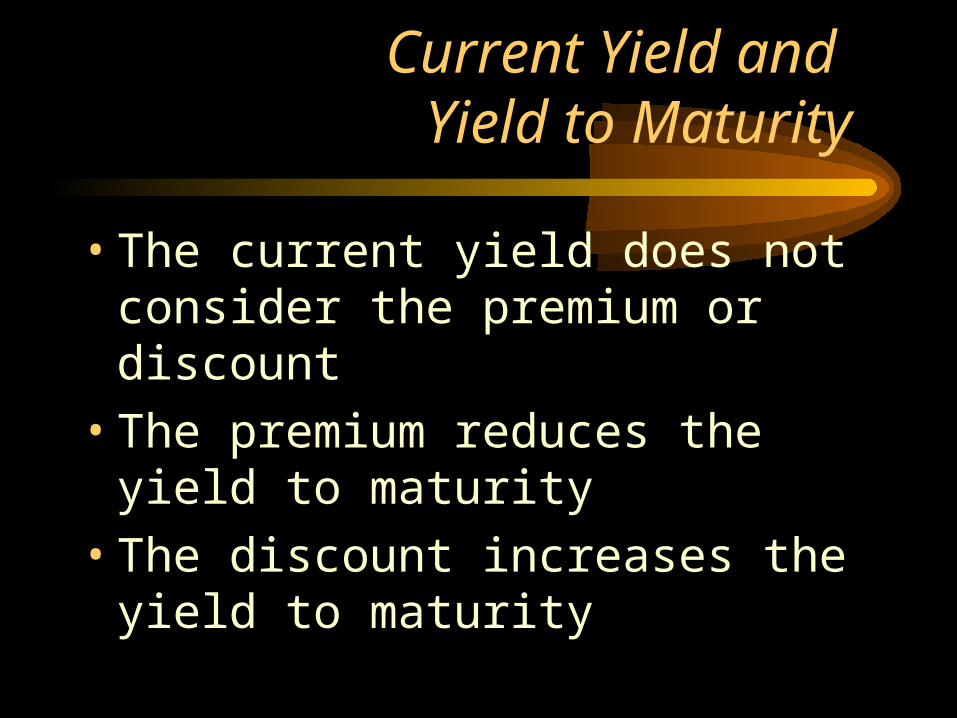

Current Yield and Yield to Maturity

• The current yield does not consider the premium or discount

• The premium reduces the yield to maturity

• The discount increases the yield to maturity

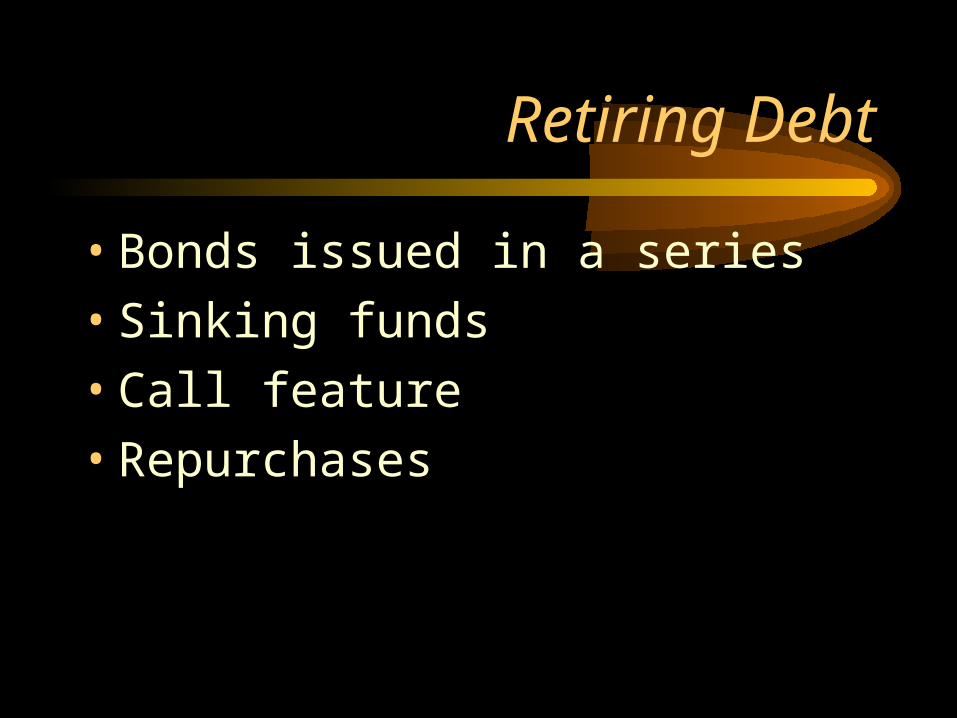

Retiring Debt

• Bonds issued in a series

• Sinking funds

• Call feature

• Repurchases

Features of Convertible Bonds

• Convertible into common stock at the holder's option

• Interest (coupon)

• Maturity date

• Call feature

Convertible Bonds

• The three possible outcomes

–conversion

–retirement at maturity

–default

Convertible Bonds

• Number of shares into which the bond may be converted

• Face value divided by the conversion price

• $1000 / $20 = 50 shares

Convertible Bonds

• Conversion Price– Face value dividend by the number of

shares into which the bond may be converted

– $1000 / 50 shares = $20

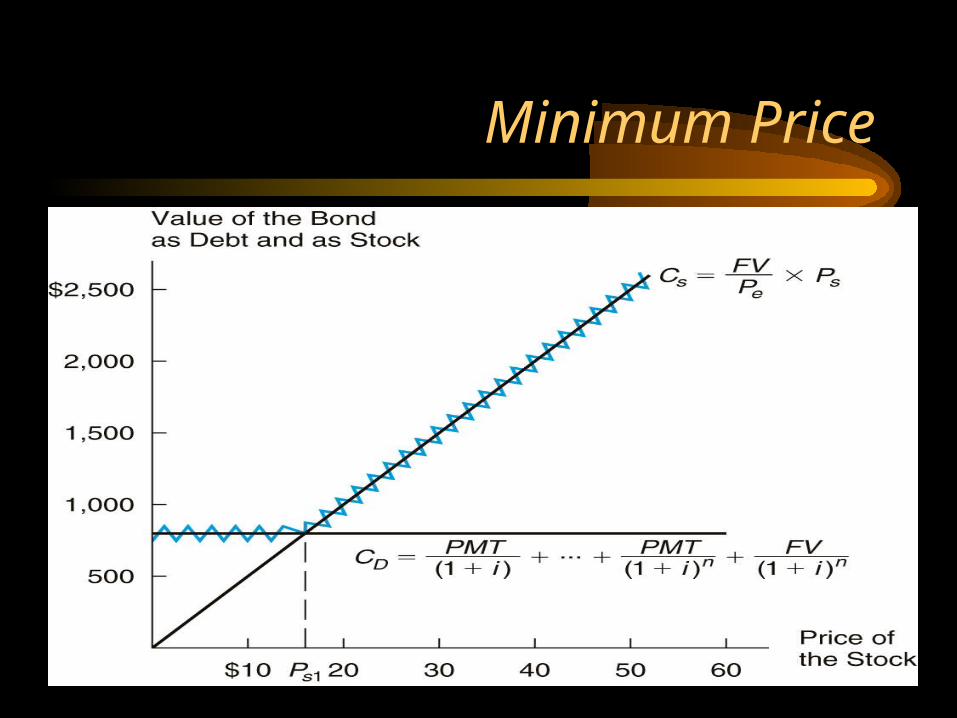

A Convertible Bond's Value as Stock

• The number of shares times the price of the stock

• 50 shares x $10 = $500

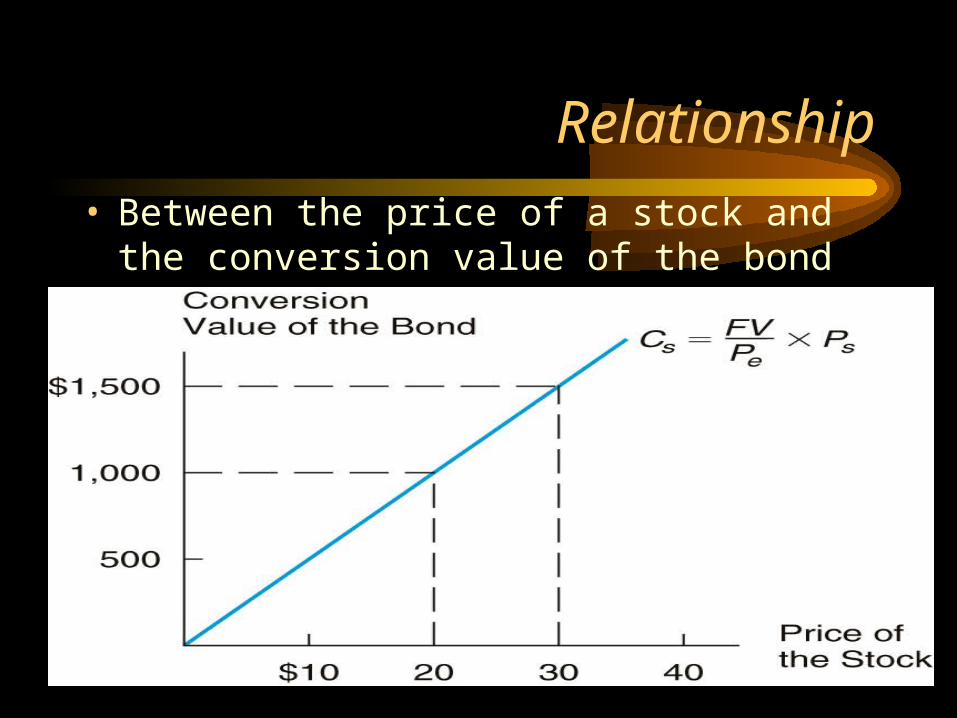

Relationship• Between the price of a stock and the

conversion value of the bond

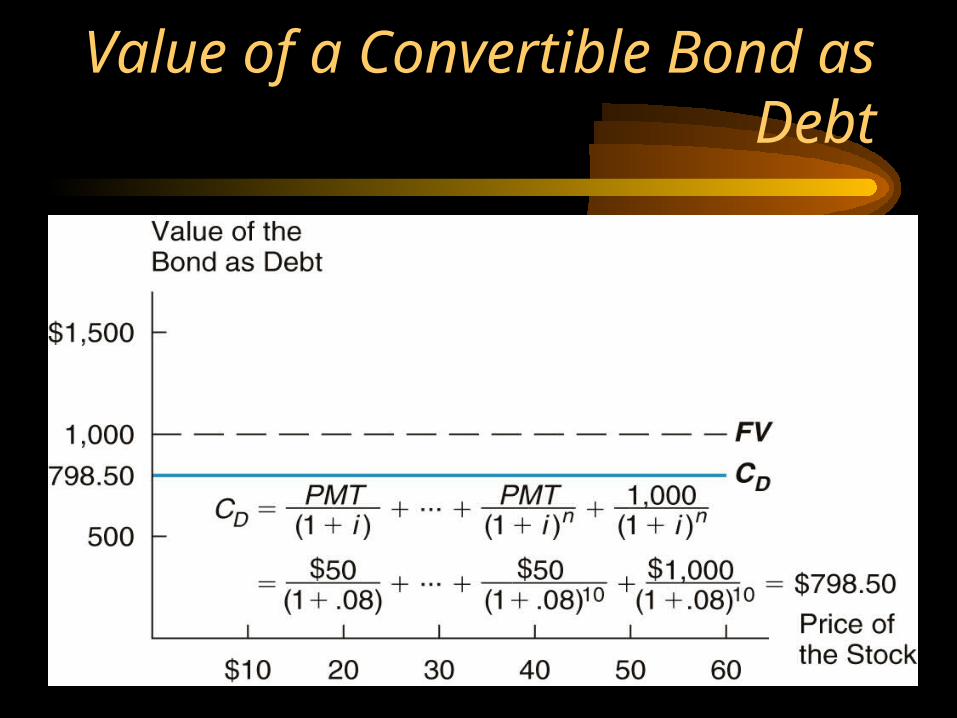

Value of a Convertible Bond as Debt

• Model for the pricing of a bond applies

• Present value of the

–Interest payment

–Principal repayment

Value of a Convertible Bond as Debt

Minimum Price

• Minimum price of the bond combines

–the value of the bond as stock and

–the value as debt

Minimum Price

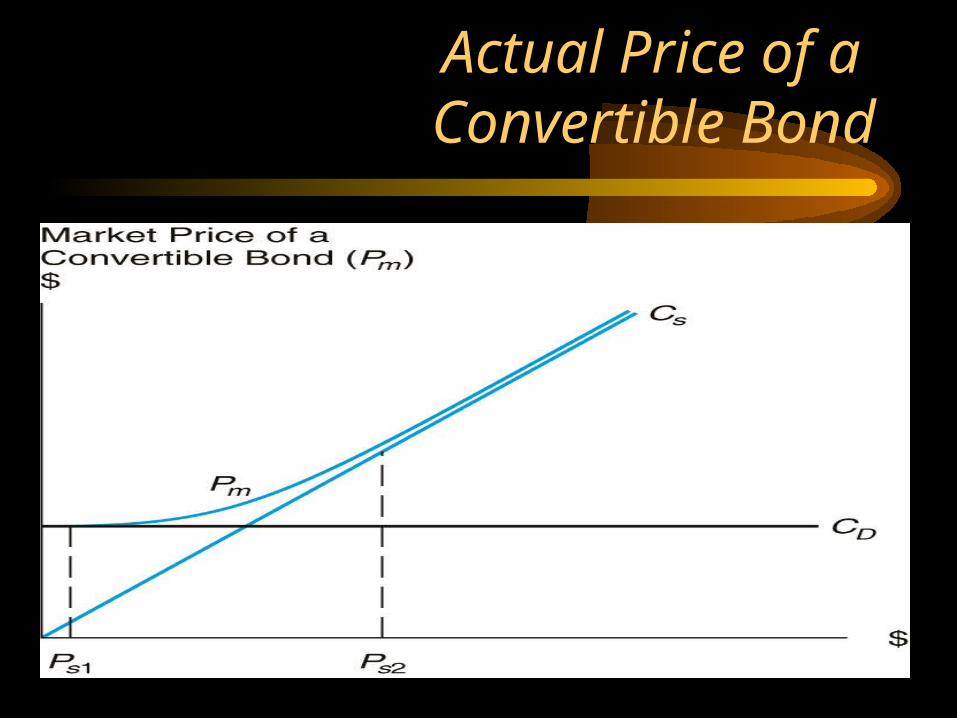

Actual Price of a Convertible Bond

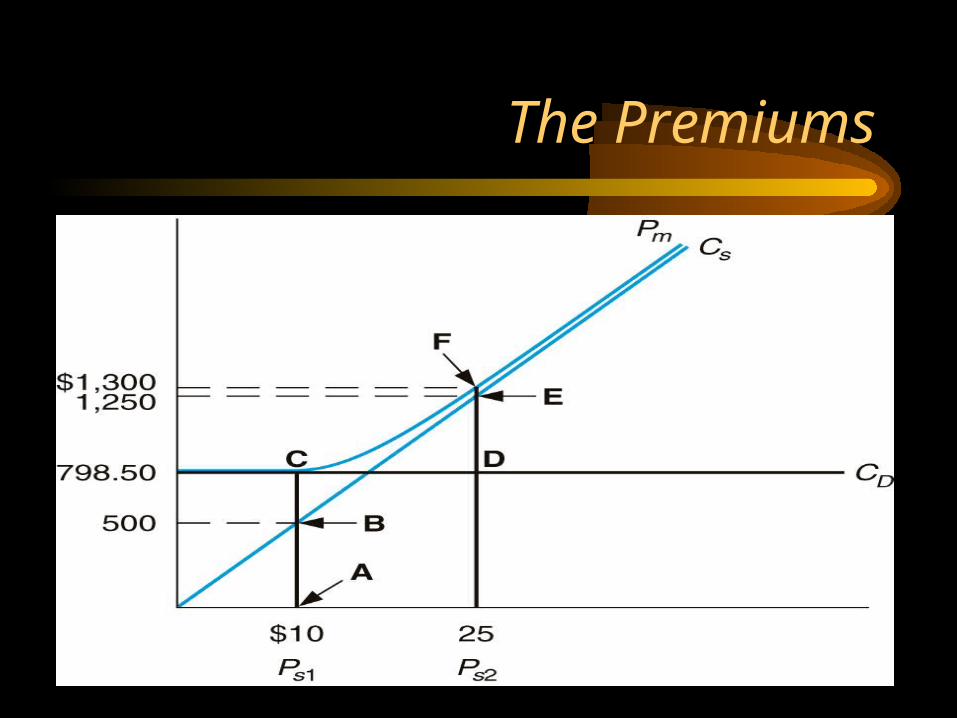

The Premiums

• The premiums paid over

–The bond's value as stock

–The bond's value as debt

The Premiums

Importance of the Call Feature

• Company may call the bond

• Forced conversion

• Price of stock exceeds conversion price

Failure to Convert

• Lose price appreciation

• Receive face value

Convertible Preferred Stock

• The features associated with convertible bonds apply to convertible preferred stock

• Except –the instrument is equity–lacks the safety associated with

debt

Federal Government Securities

• Nonmarketble federal government debt

–Series EE (“patriot”) bond

Federal Government Securities

• Marketable federal government debt

–Treasury bills

–Treasury notes and bonds

–Zero coupon bonds

Federal Debt

• Amount of federal debt in existence primarily consists of

–Treasury bills

–Intermediate - term debt

–Bonds

• Emphasis on short-term debt

Federal Debt and Risk

• Safe from default

• Risk from price fluctuations

• Purchasing power risk

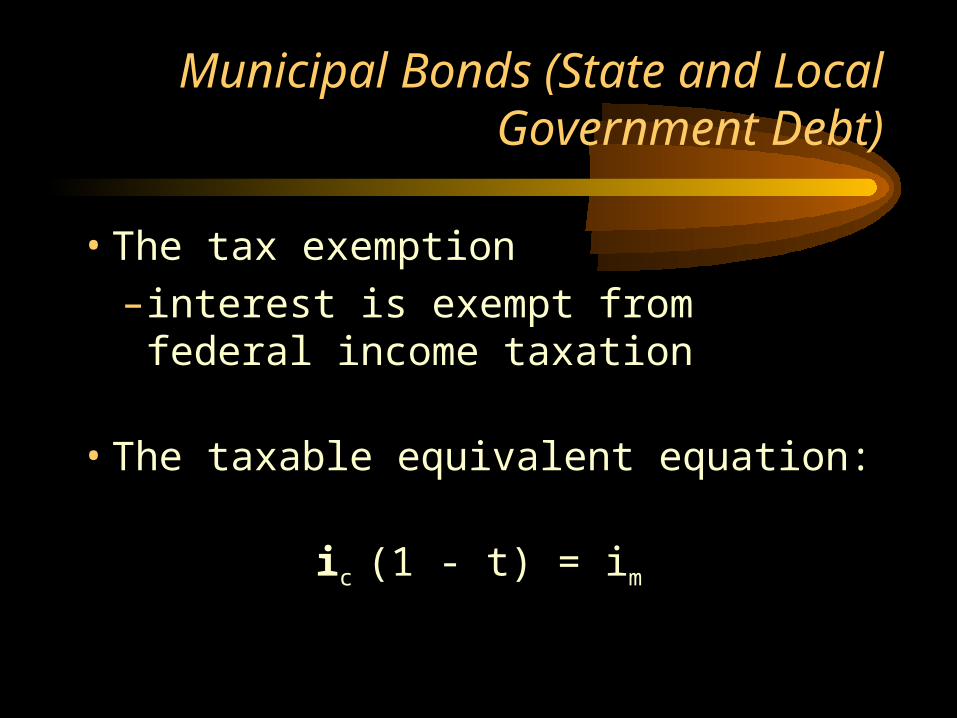

Municipal Bonds (State and Local Government Debt)

• The tax exemption– interest is exempt from federal

income taxation

• The taxable equivalent equation:

ic (1 - t) = im

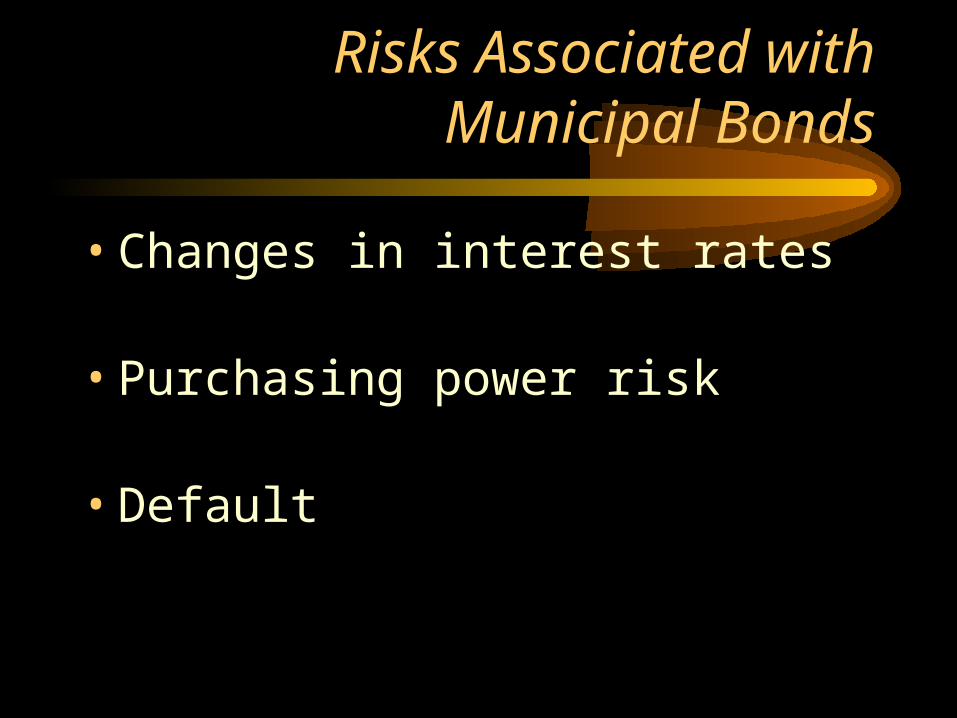

Risks Associated with Municipal Bonds

• Changes in interest rates

• Purchasing power risk

• Default