chapter - iii indian construction...

TRANSCRIPT

72

CHAPTER - III

INDIAN CONSTRUCTION INDUSTRY

Construction activity contributes to the economic development of a

country. The construction industry is the second largest economic activity

in India and plays an important role in the nation‟s economy. The

construction sector in India has an average annual investment of over

Rs.3billion. At present, the sector accounts for nearly 12 per cent of the

Indian GDP, making it the second biggest contributor after agriculture.

The sector is also the second biggest employer. Currently, it employs,

directly or indirectly, nearly 32 million workers or 14 per cent of the total

employable population of India. Further, construction industry is a

vanguard activity of several other key sectors of the economy whose

performance is dependent on the satisfactory performance of the

construction industry. For instance, the sector creates a multiplier effect

of between 1.8 and 2 percent on core industries such as steel, cement,

aluminum and petroleum.

The construction industry has been a significant contributor to

India‟s GDP growth of 8-10 per cent. Its present growth at 15-20 per

cent which seems to get stronger by the day, stems from rising demand

for quality infrastructure and real estate in residential and industrial

sector.

By 2020, it is expected that 47 percent of Indian‟s will be between

15 and 59 and India will have the world‟s largest population of workers

and consumers. Increased working – age population, coupled with higher

73

purchasing power and increased consumerism, will spur real estate

investments across all commercial, residential and retail sub-sectors.

According to a recent population analysis conducted by A. T.

Kearney, the middle and upper income population of India is expected to

rise at a CAGR of 14 percent from 51 million in 2000 to 373 million in

2015. Assuming that 25 per cent of this increasingly prosperous

population will require independent housing, there will be a demand for

about 20 million sq. ft. per annum of residential development, along with

the corresponding demand for retail, commercial and industrial

development (Nair, 2007)1.

Table 3.1

Construction activity in selected countries: year 1980

SL

No.

Countries Value added to

GDP ( per cent)

(percentage)

Share of gross

fixed capital

formation

(percentage)

Developed

countries

1. France 5 56

2. Italy 6 57

3. Japan 8 67

4. U.K 6 48

5. USA 4 55

Developing

countries

6. Kenya 5 48

7. South Korea 6 63

8. Mexico 5 57

9. Pakistan 5 60

10. India (approximate) 5 44

Source: Engineering News Record (ENR), Report (1993).

In Kerala, there is a huge unmet demand in the residential

construction sector. The coming into the scene of large number of

developers from outside has enlivened the sector in Kerala and this will

74

certainly augment the supply side of the business cycle. Because of high

returns, a large volume of funds flows into the sector. This naturally will

push the developmental activities of several other sectors and of several

related segments and the supply of both commercial and residential

properties.

The construction sector is a part of the service industry. The

services can broadly be classified into four segments: infrastructural,

industrial, residential and commercial. Nearly 54 percent of construction

activity is generated in various infrastructure sectors. This is followed by

other industrial activity (36 per cent), residential activity (5 per cent) and

commercial activity (5 per cent).

Major construction work includes setting up of road and highway

projects, powerplants, railway lines, mineral plants and dams,industry

irrigation and urban infrastructure projects.

Table No.3.2

India’s infrastructure development expenditure for the period

1990-91 to 1999-2005

Year Infrastructure expenditure (in billion Rs.)

1991-92 510954

1995-96 1073271

1999-2000 1761838

2000-01 1902999

2001-02 2081474

2002-03 2254888

2003-04 2519785

2004-05 2830465

Source: Infrastructure development report 2005

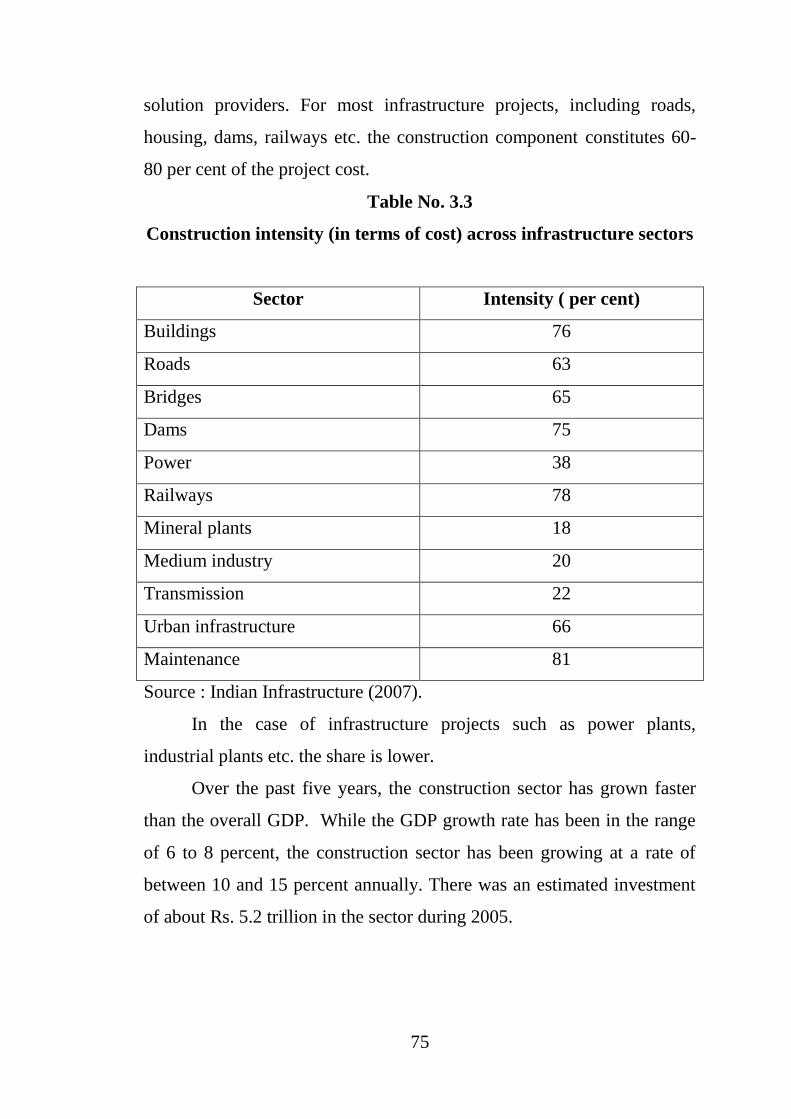

These works are undertaken through many entities including

construction contractors, equipment suppliers, material suppliers and

75

solution providers. For most infrastructure projects, including roads,

housing, dams, railways etc. the construction component constitutes 60-

80 per cent of the project cost.

Table No. 3.3

Construction intensity (in terms of cost) across infrastructure sectors

Sector Intensity ( per cent)

Buildings 76

Roads 63

Bridges 65

Dams 75

Power 38

Railways 78

Mineral plants 18

Medium industry 20

Transmission 22

Urban infrastructure 66

Maintenance 81

Source : Indian Infrastructure (2007).

In the case of infrastructure projects such as power plants,

industrial plants etc. the share is lower.

Over the past five years, the construction sector has grown faster

than the overall GDP. While the GDP growth rate has been in the range

of 6 to 8 percent, the construction sector has been growing at a rate of

between 10 and 15 percent annually. There was an estimated investment

of about Rs. 5.2 trillion in the sector during 2005.

1

76

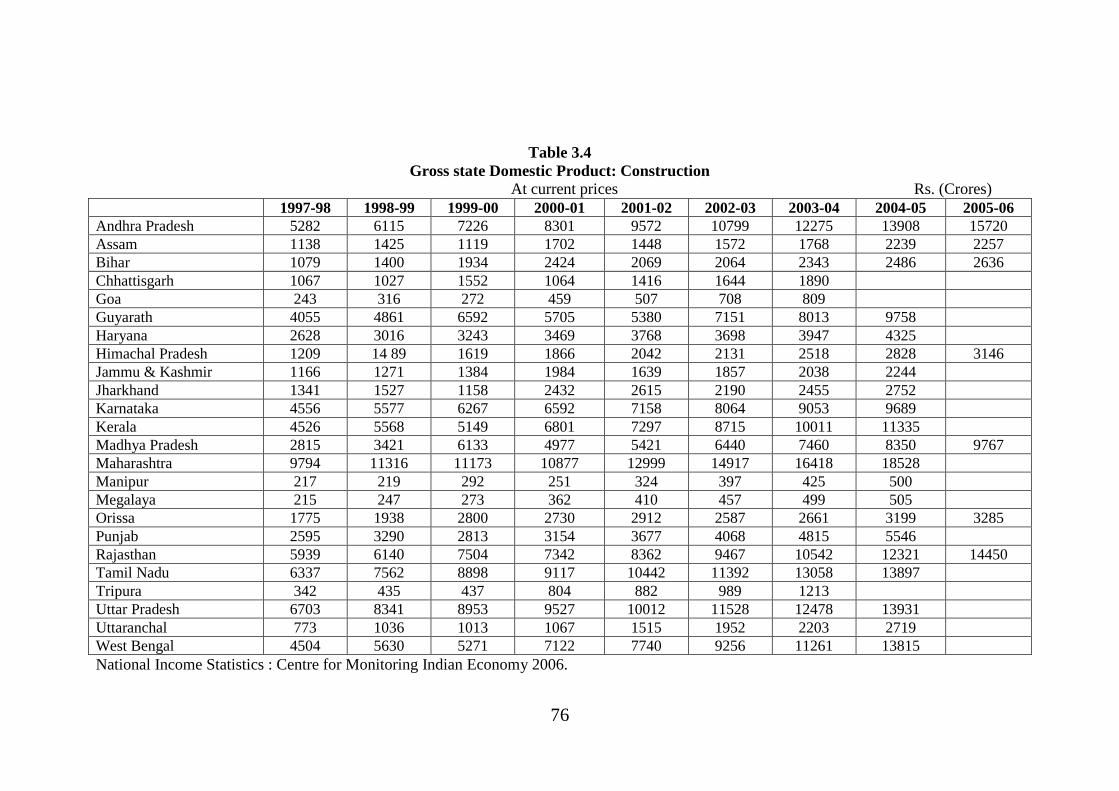

Table 3.4

Gross state Domestic Product: Construction

At current prices Rs. (Crores)

1997-98 1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

Andhra Pradesh 5282 6115 7226 8301 9572 10799 12275 13908 15720

Assam 1138 1425 1119 1702 1448 1572 1768 2239 2257

Bihar 1079 1400 1934 2424 2069 2064 2343 2486 2636

Chhattisgarh 1067 1027 1552 1064 1416 1644 1890

Goa 243 316 272 459 507 708 809

Guyarath 4055 4861 6592 5705 5380 7151 8013 9758

Haryana 2628 3016 3243 3469 3768 3698 3947 4325

Himachal Pradesh 1209 14 89 1619 1866 2042 2131 2518 2828 3146

Jammu & Kashmir 1166 1271 1384 1984 1639 1857 2038 2244

Jharkhand 1341 1527 1158 2432 2615 2190 2455 2752

Karnataka 4556 5577 6267 6592 7158 8064 9053 9689

Kerala 4526 5568 5149 6801 7297 8715 10011 11335

Madhya Pradesh 2815 3421 6133 4977 5421 6440 7460 8350 9767

Maharashtra 9794 11316 11173 10877 12999 14917 16418 18528

Manipur 217 219 292 251 324 397 425 500

Megalaya 215 247 273 362 410 457 499 505

Orissa 1775 1938 2800 2730 2912 2587 2661 3199 3285

Punjab 2595 3290 2813 3154 3677 4068 4815 5546

Rajasthan 5939 6140 7504 7342 8362 9467 10542 12321 14450

Tamil Nadu 6337 7562 8898 9117 10442 11392 13058 13897

Tripura 342 435 437 804 882 989 1213

Uttar Pradesh 6703 8341 8953 9527 10012 11528 12478 13931

Uttaranchal 773 1036 1013 1067 1515 1952 2203 2719

West Bengal 4504 5630 5271 7122 7740 9256 11261 13815

National Income Statistics : Centre for Monitoring Indian Economy 2006.

77

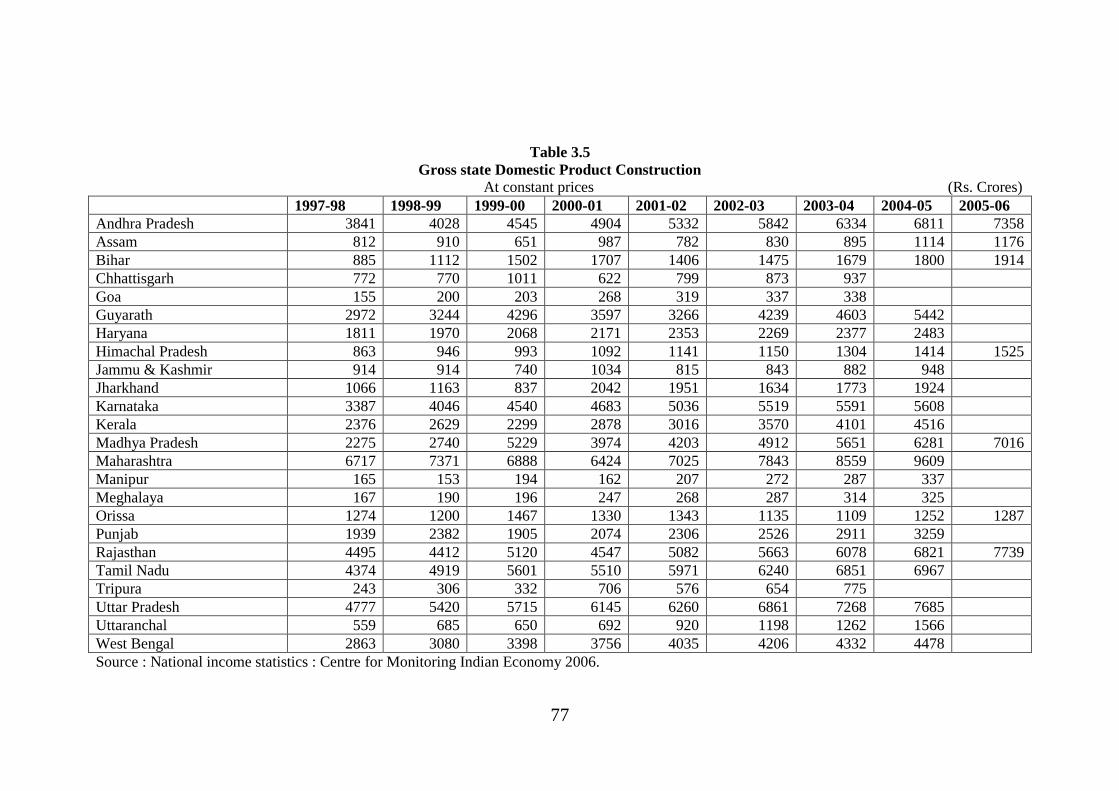

Table 3.5

Gross state Domestic Product Construction

At constant prices (Rs. Crores)

1997-98 1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

Andhra Pradesh 3841 4028 4545 4904 5332 5842 6334 6811 7358

Assam 812 910 651 987 782 830 895 1114 1176

Bihar 885 1112 1502 1707 1406 1475 1679 1800 1914

Chhattisgarh 772 770 1011 622 799 873 937

Goa 155 200 203 268 319 337 338

Guyarath 2972 3244 4296 3597 3266 4239 4603 5442

Haryana 1811 1970 2068 2171 2353 2269 2377 2483

Himachal Pradesh 863 946 993 1092 1141 1150 1304 1414 1525

Jammu & Kashmir 914 914 740 1034 815 843 882 948

Jharkhand 1066 1163 837 2042 1951 1634 1773 1924

Karnataka 3387 4046 4540 4683 5036 5519 5591 5608

Kerala 2376 2629 2299 2878 3016 3570 4101 4516

Madhya Pradesh 2275 2740 5229 3974 4203 4912 5651 6281 7016

Maharashtra 6717 7371 6888 6424 7025 7843 8559 9609

Manipur 165 153 194 162 207 272 287 337

Meghalaya 167 190 196 247 268 287 314 325

Orissa 1274 1200 1467 1330 1343 1135 1109 1252 1287

Punjab 1939 2382 1905 2074 2306 2526 2911 3259

Rajasthan 4495 4412 5120 4547 5082 5663 6078 6821 7739

Tamil Nadu 4374 4919 5601 5510 5971 6240 6851 6967

Tripura 243 306 332 706 576 654 775

Uttar Pradesh 4777 5420 5715 6145 6260 6861 7268 7685

Uttaranchal 559 685 650 692 920 1198 1262 1566

West Bengal 2863 3080 3398 3756 4035 4206 4332 4478

Source : National income statistics : Centre for Monitoring Indian Economy 2006.

78

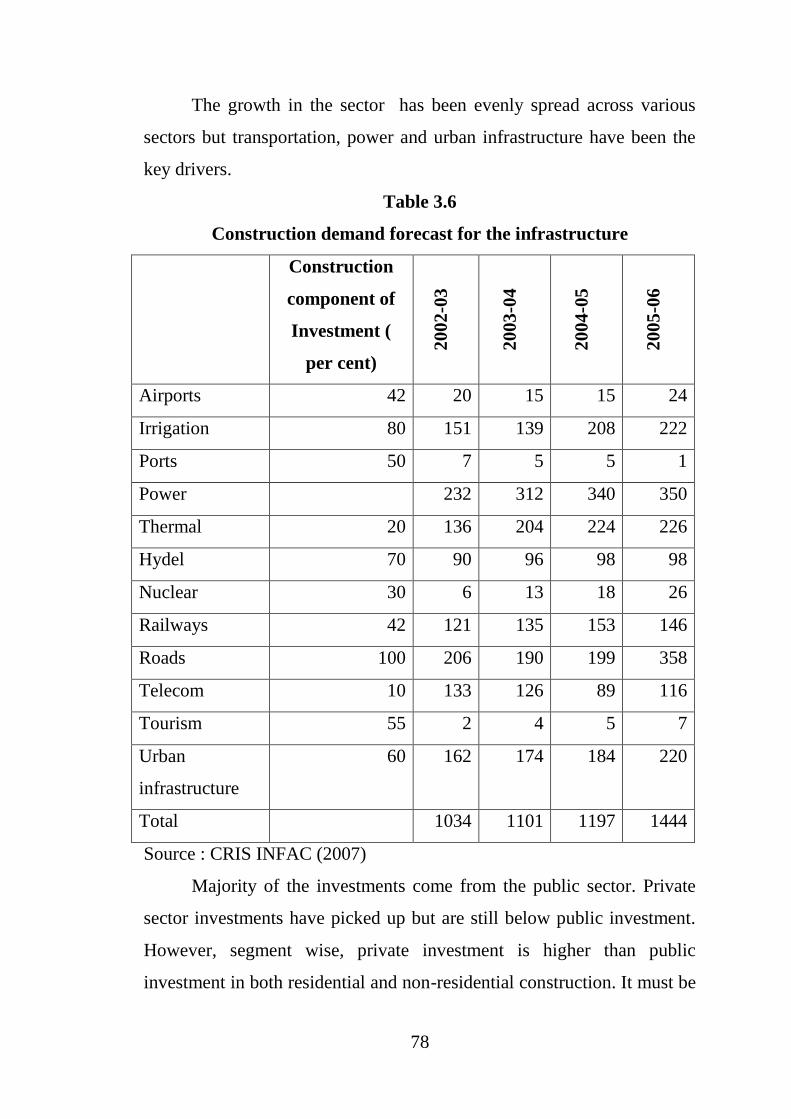

The growth in the sector has been evenly spread across various

sectors but transportation, power and urban infrastructure have been the

key drivers.

Table 3.6

Construction demand forecast for the infrastructure

Construction

component of

Investment (

per cent)

2002

-03

2003

-04

2004

-05

2005

-06

Airports 42 20 15 15 24

Irrigation 80 151 139 208 222

Ports 50 7 5 5 1

Power 232 312 340 350

Thermal 20 136 204 224 226

Hydel 70 90 96 98 98

Nuclear 30 6 13 18 26

Railways 42 121 135 153 146

Roads 100 206 190 199 358

Telecom 10 133 126 89 116

Tourism 55 2 4 5 7

Urban

infrastructure

60 162 174 184 220

Total 1034 1101 1197 1444

Source : CRIS INFAC (2007)

Majority of the investments come from the public sector. Private

sector investments have picked up but are still below public investment.

However, segment wise, private investment is higher than public

investment in both residential and non-residential construction. It must be

79

noted that the private sector contributed about 33 percent of the total

investment in construction in the year 2005.

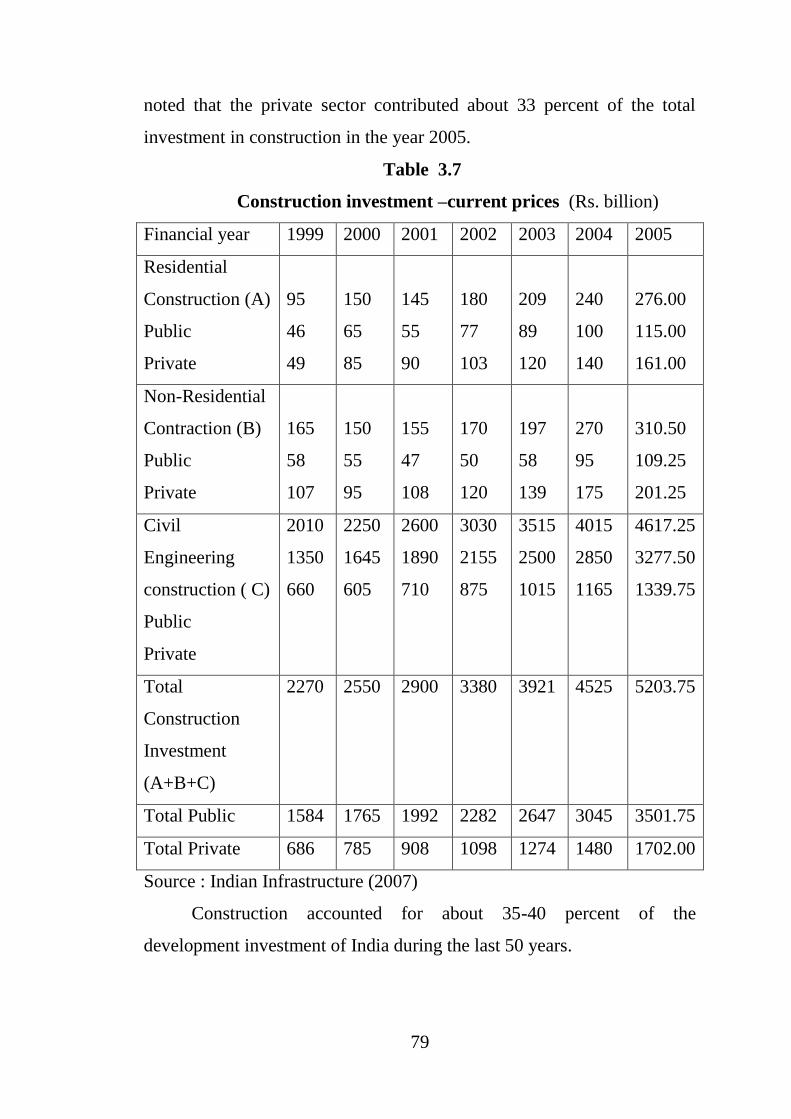

Table 3.7

Construction investment –current prices (Rs. billion)

Financial year 1999 2000 2001 2002 2003 2004 2005

Residential

Construction (A)

Public

Private

95

46

49

150

65

85

145

55

90

180

77

103

209

89

120

240

100

140

276.00

115.00

161.00

Non-Residential

Contraction (B)

Public

Private

165

58

107

150

55

95

155

47

108

170

50

120

197

58

139

270

95

175

310.50

109.25

201.25

Civil

Engineering

construction ( C)

Public

Private

2010

1350

660

2250

1645

605

2600

1890

710

3030

2155

875

3515

2500

1015

4015

2850

1165

4617.25

3277.50

1339.75

Total

Construction

Investment

(A+B+C)

2270 2550 2900 3380 3921 4525 5203.75

Total Public 1584 1765 1992 2282 2647 3045 3501.75

Total Private 686 785 908 1098 1274 1480 1702.00

Source : Indian Infrastructure (2007)

Construction accounted for about 35-40 percent of the

development investment of India during the last 50 years.

80

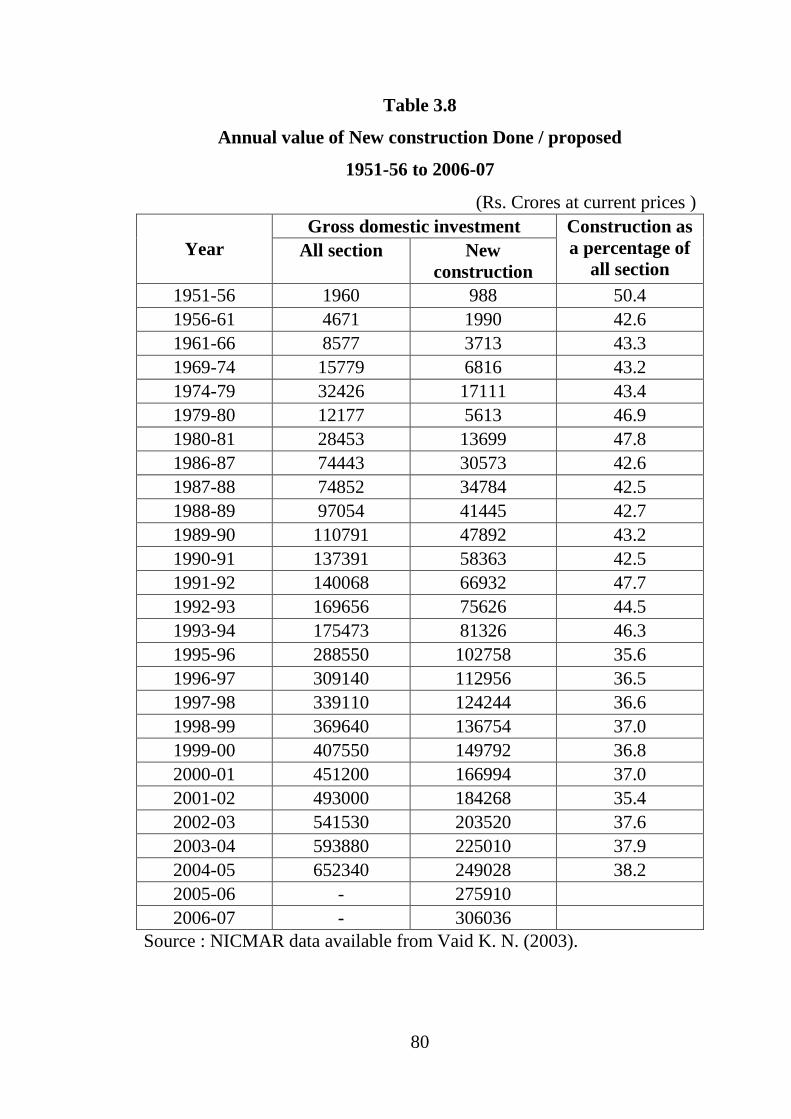

Table 3.8

Annual value of New construction Done / proposed

1951-56 to 2006-07

(Rs. Crores at current prices )

Year

Gross domestic investment Construction as

a percentage of

all section All section New

construction

1951-56 1960 988 50.4

1956-61 4671 1990 42.6

1961-66 8577 3713 43.3

1969-74 15779 6816 43.2

1974-79 32426 17111 43.4

1979-80 12177 5613 46.9

1980-81 28453 13699 47.8

1986-87 74443 30573 42.6

1987-88 74852 34784 42.5

1988-89 97054 41445 42.7

1989-90 110791 47892 43.2

1990-91 137391 58363 42.5

1991-92 140068 66932 47.7

1992-93 169656 75626 44.5

1993-94 175473 81326 46.3

1995-96 288550 102758 35.6

1996-97 309140 112956 36.5

1997-98 339110 124244 36.6

1998-99 369640 136754 37.0

1999-00 407550 149792 36.8

2000-01 451200 166994 37.0

2001-02 493000 184268 35.4

2002-03 541530 203520 37.6

2003-04 593880 225010 37.9

2004-05 652340 249028 38.2

2005-06 - 275910

2006-07 - 306036

Source : NICMAR data available from Vaid K. N. (2003).

81

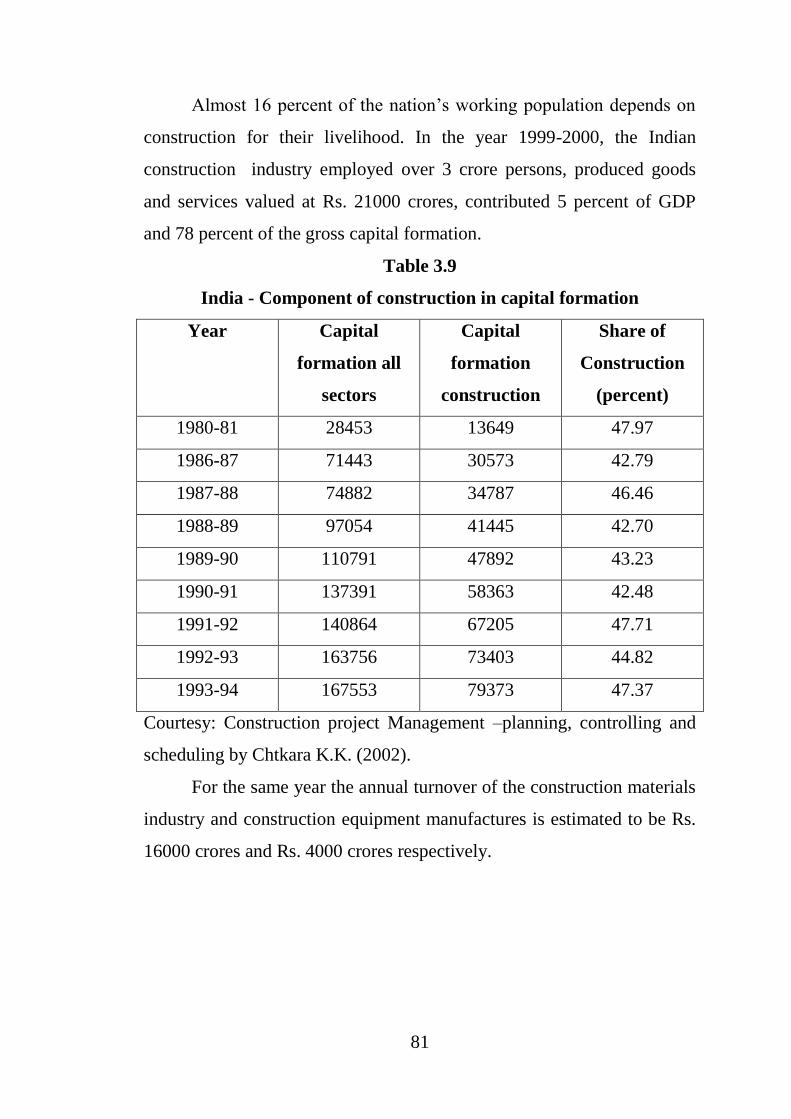

Almost 16 percent of the nation‟s working population depends on

construction for their livelihood. In the year 1999-2000, the Indian

construction industry employed over 3 crore persons, produced goods

and services valued at Rs. 21000 crores, contributed 5 percent of GDP

and 78 percent of the gross capital formation.

Table 3.9

India - Component of construction in capital formation

Year Capital

formation all

sectors

Capital

formation

construction

Share of

Construction

(percent)

1980-81 28453 13649 47.97

1986-87 71443 30573 42.79

1987-88 74882 34787 46.46

1988-89 97054 41445 42.70

1989-90 110791 47892 43.23

1990-91 137391 58363 42.48

1991-92 140864 67205 47.71

1992-93 163756 73403 44.82

1993-94 167553 79373 47.37

Courtesy: Construction project Management –planning, controlling and

scheduling by Chtkara K.K. (2002).

For the same year the annual turnover of the construction materials

industry and construction equipment manufactures is estimated to be Rs.

16000 crores and Rs. 4000 crores respectively.

82

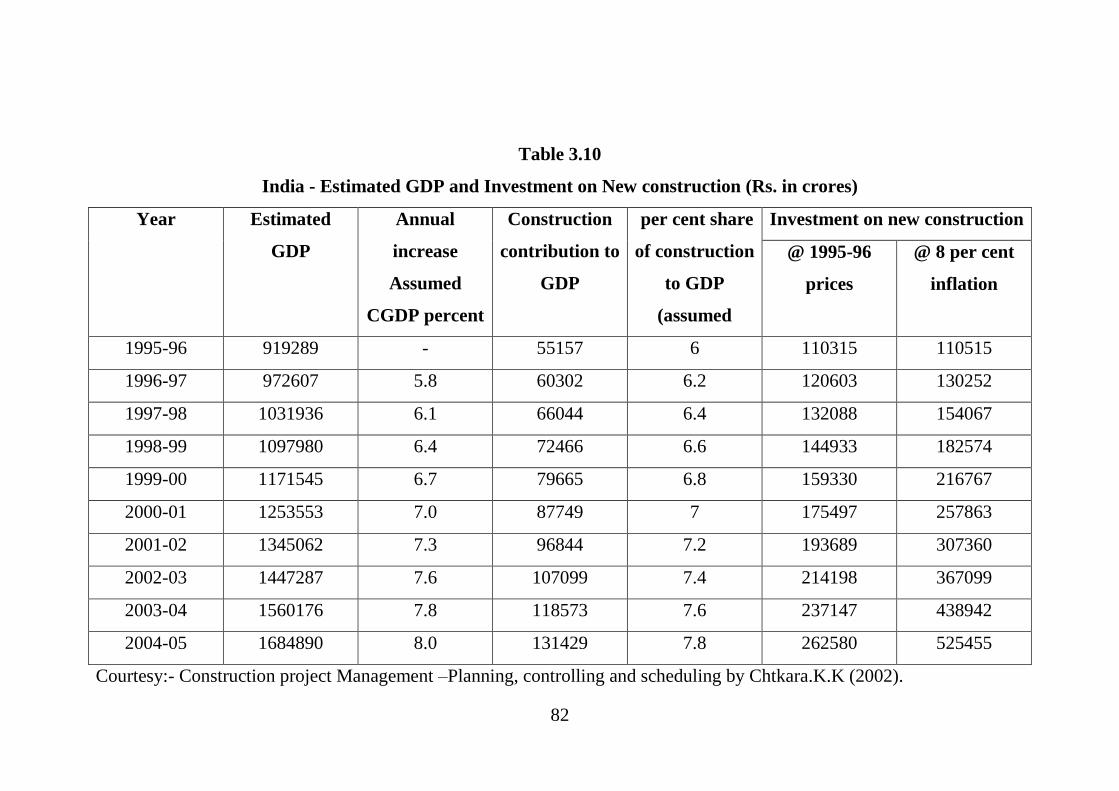

Table 3.10

India - Estimated GDP and Investment on New construction (Rs. in crores)

Year Estimated

GDP

Annual

increase

Assumed

CGDP percent

Construction

contribution to

GDP

per cent share

of construction

to GDP

(assumed

Investment on new construction

@ 1995-96

prices

@ 8 per cent

inflation

1995-96 919289 - 55157 6 110315 110515

1996-97 972607 5.8 60302 6.2 120603 130252

1997-98 1031936 6.1 66044 6.4 132088 154067

1998-99 1097980 6.4 72466 6.6 144933 182574

1999-00 1171545 6.7 79665 6.8 159330 216767

2000-01 1253553 7.0 87749 7 175497 257863

2001-02 1345062 7.3 96844 7.2 193689 307360

2002-03 1447287 7.6 107099 7.4 214198 367099

2003-04 1560176 7.8 118573 7.6 237147 438942

2004-05 1684890 8.0 131429 7.8 262580 525455

Courtesy:- Construction project Management –Planning, controlling and scheduling by Chtkara.K.K (2002).

83

The construction industry is an essential contributor to the process

of development. Roads, dams, irrigation works, schools, houses, hospitals

and other construction works are the physical foundations on which

development efforts and improved living standards are established. The

above mentioned products of the construction industry are investments or

capital goods, their value is high in relation to the income of the

purchaser. For the individual consumer, for example, the purchase of

house will usually entail the expenditure of several times of his annual

income. Similarly, the erection of a factory by a manufacturing firm will

be a large expenditure in relation to the running costs of production as

well as the annual income derived from it. Consequently, the products of

the construction industry, with the exception of repair and maintenance,

are paid for from savings i.e. the purchasing power which has accrued but

not used in the past. These savings may either belong to the ultimate

owner of the construction industry or borrowed from elsewhere. Thus,

construction industry thrives on the savings and investment of the

economy and has linkages with the rest of the economy in terms of

generation of output and employment.

The size of the construction industry is important to any nation as

changes in its output affect the size of the national product both directly

and indirectly. If the output of the industry is down, total investment in

the economy goes down. A change in the level of construction industry

output also affects the general employment levels and incomes of the

people. Governments influence construction industry both from demand

and supply sides. The Government is one of the biggest clients of

construction industry and as such it is the initiator of most of the

infrastructure development projects, civil and social services. A

Government uses investment in construction to regulate the economy as

well as to introduce the desired changes in it. The construction activity is

84

perhaps the first activity to be cut during a recession. A buoyancy in

construction can make the economy healthy. Thus, Government as client,

as a regulator of the industry and as initiator of economic changes

through construction, plays a significant role in this industry.

Fluctuations in the construction demand affect the economy in

many ways. It could lead either to a shrinkage or enhancement in both

backward and forward linkages; In fact, construction has been ranked

among the top four out of the twenty economic sectors in terms of inter

sectoral linkages.

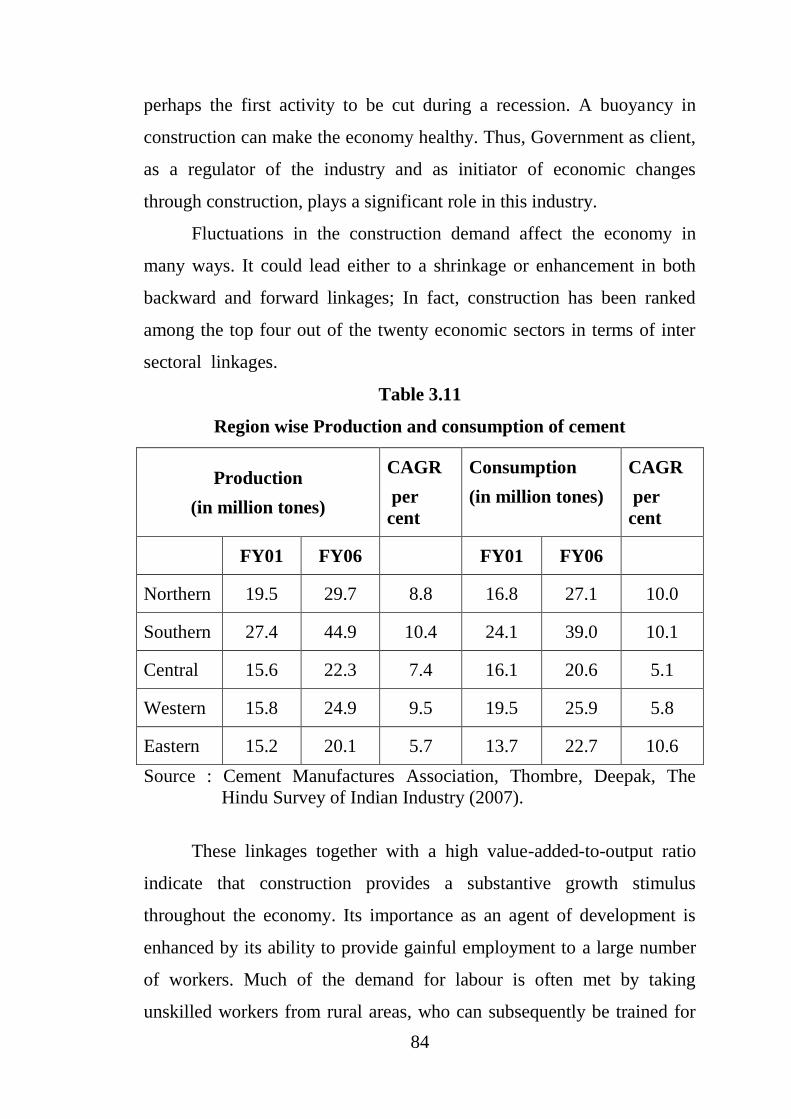

Table 3.11

Region wise Production and consumption of cement

Production

(in million tones)

CAGR

per

cent

Consumption

(in million tones)

CAGR

per

cent

FY01 FY06 FY01 FY06

Northern 19.5 29.7 8.8 16.8 27.1 10.0

Southern 27.4 44.9 10.4 24.1 39.0 10.1

Central 15.6 22.3 7.4 16.1 20.6 5.1

Western 15.8 24.9 9.5 19.5 25.9 5.8

Eastern 15.2 20.1 5.7 13.7 22.7 10.6

Source : Cement Manufactures Association, Thombre, Deepak, The

Hindu Survey of Indian Industry (2007).

These linkages together with a high value-added-to-output ratio

indicate that construction provides a substantive growth stimulus

throughout the economy. Its importance as an agent of development is

enhanced by its ability to provide gainful employment to a large number

of workers. Much of the demand for labour is often met by taking

unskilled workers from rural areas, who can subsequently be trained for

85

more demanding jobs. Construction is often the only significant

alternative for farm labour, particularly as it can adjust to the needs of

harvesting seasons to a larger degree than manufacturing.

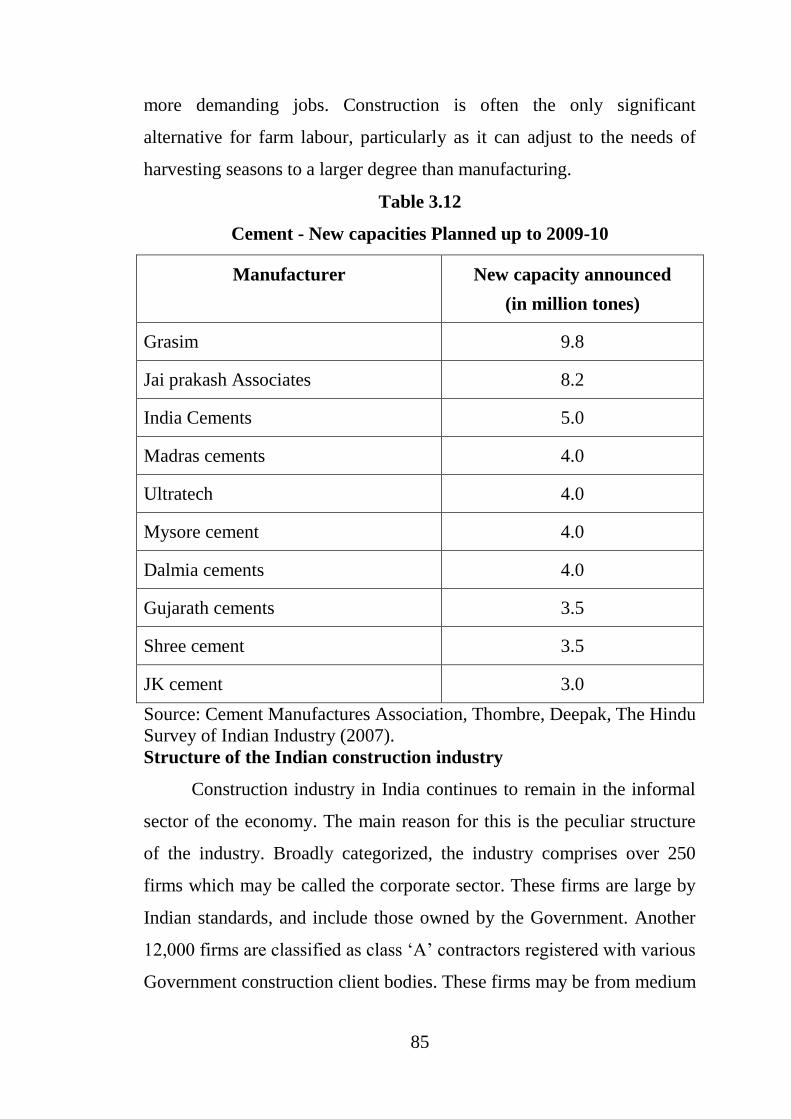

Table 3.12

Cement - New capacities Planned up to 2009-10

Manufacturer New capacity announced

(in million tones)

Grasim 9.8

Jai prakash Associates 8.2

India Cements 5.0

Madras cements 4.0

Ultratech 4.0

Mysore cement 4.0

Dalmia cements 4.0

Gujarath cements 3.5

Shree cement 3.5

JK cement 3.0

Source: Cement Manufactures Association, Thombre, Deepak, The Hindu

Survey of Indian Industry (2007).

Structure of the Indian construction industry

Construction industry in India continues to remain in the informal

sector of the economy. The main reason for this is the peculiar structure

of the industry. Broadly categorized, the industry comprises over 250

firms which may be called the corporate sector. These firms are large by

Indian standards, and include those owned by the Government. Another

12,000 firms are classified as class „A‟ contractors registered with various

Government construction client bodies. These firms may be from medium

86

to large size in terms of volume of business turnover. Then, there are six

hundred thousand small firms of contractors/sub-contractors who

compete for small jobs or work as sub-contractors of prime or other

contractors. Whereas there are numerous speciality contractors in this

category, most others work at low-end technology jobs of small value.

(Vaid, 2003)2.

Table 3.13

Steel Consumption in different regions of the world 2005-07

Million metric tones (mmt)

of finished steel

Change per year

per cent

2005 2006 2007 2005-06 2006-07

EU(15) 139.4 150.0 147.7 7.6 -1.5

EU(25) 158.8 171.5 169.6 8.0 -1.1

Other Europe 29.3 32.1 34.0 9.5 6.0

CIS 43.5 46.5 50.9 7.0 9.4

NAFTA 139.7 151.8 150.8 8.7 -0.7

South America 32.3 36.0 38.6 11.6 7.1

Africa 22.4 24.6 25.7 10.0 4.4

Middle East 34.0 37.3 40.6 9.6 8.9

Japan 78.0 78.6 80.8 0.8 2.8

India 38.1 41.9 45.7 10.0 9.1

Rest of Asia

(Excl, China)

117.8 118.5 121.8 -0.6 2.8

Australia New

Zealand

7.9 7.8 7.9 1.6 1.3

World

(excl. China)

701.8 746.7 766.4 6.4 2.6

China 327.0 374.0 413.0 14.4 10.4

World 1028.8 1120.7 1179.4 8.9 5.2

Source : International Iron & Steel Institute, Pye Darren, Hindu Survey of

Indian Industry (2007).

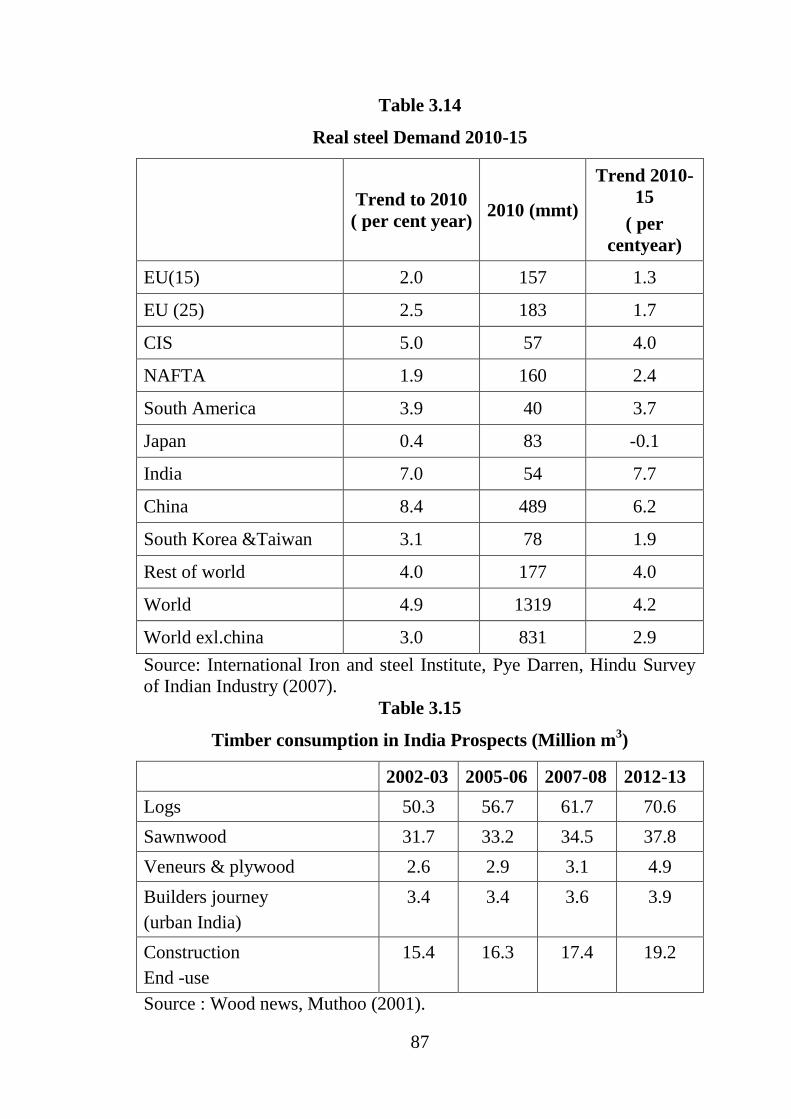

87

Table 3.14

Real steel Demand 2010-15

Trend to 2010

( per cent year) 2010 (mmt)

Trend 2010-

15

( per

centyear)

EU(15) 2.0 157 1.3

EU (25) 2.5 183 1.7

CIS 5.0 57 4.0

NAFTA 1.9 160 2.4

South America 3.9 40 3.7

Japan 0.4 83 -0.1

India 7.0 54 7.7

China 8.4 489 6.2

South Korea &Taiwan 3.1 78 1.9

Rest of world 4.0 177 4.0

World 4.9 1319 4.2

World exl.china 3.0 831 2.9

Source: International Iron and steel Institute, Pye Darren, Hindu Survey

of Indian Industry (2007).

Table 3.15

Timber consumption in India Prospects (Million m3)

2002-03 2005-06 2007-08 2012-13

Logs 50.3 56.7 61.7 70.6

Sawnwood 31.7 33.2 34.5 37.8

Veneurs & plywood 2.6 2.9 3.1 4.9

Builders journey

(urban India)

3.4 3.4 3.6 3.9

Construction

End -use

15.4 16.3 17.4 19.2

Source : Wood news, Muthoo (2001).

88

The near amorphous structure of the industry has both the positive

and negative implications. It stands in the way of skill development of the

construction labour force and technical upgradation of the construction

process. These problems could not have existed had the industry been

organized differently.

In practice, any construction activity in general or a building

construction activity in particular takes place in the following manner.

The construction industry (barring real estate developers) does not really

sell a tangible product, it sells a service. The services that it may provide

are determined by its clients and are performed at a time and place

specified by them. Contractors have little control on the demand for

construction services nor can they stimulate it. They do not even set rates

for their service as the same is done by clients. Further, contractors may

devise more efficient methods of building, but advances in materials and

machinery are out of their control. The financing of the construction

services is also outside the control of contractors. It is done by the client

who commissioned the service, and till recently the mode and periodicity

of payments were decided unilaterally by the client. Negotiated contract

terms are agreed upon in very limited number of projects. Thus a vast

majority of firms continue to operate in a product market where they have

no control over demand, technology, materials, workplace, finance and

labour supply. Consequently, their concern is to finish the job in hand and

not to bother about other things around them in the industry.

Consultants, workers and inputs industries are the other

participants in the construction industry. Architectural and engineering

consultant firms play an important role in construction process. Even

though there are thousands of consultants in our country, consulting firms

as formal organizations of appreciable size number to 2000. Construction

89

materials manufactures are also 4000 in the organized sector. The number

of construction equipment manufactures is 800. (Vaid, 2003)3.

Small size of firms is a handicap for skill formation and technology

upgradation in the construction industry. They lack a long term

perspective. As such they do not generally invest in plant and machinery

or Research and Development. They do not spend money on training their

workers because contractors fear that the workers would leave them on

the completion of the job. Small firms exhibit a very low level of

management ability. It may be admitted that the structure of the industry

is the direct result of the conditions prevailing in the market. It can also

be argued that the existence of a large number of small firms provides a

useful structural framework for its continuation.

History of Growth of construction

The Early Period

Shilpshastra or architecture was a highly developed profession in

ancient India. Rig-Veda contains many references about this subject.

Manusmriti contains the dos and donts in construction. Kautilya‟s

Arthashastra gives guidelines to kings and administrators regarding their

duties to people for the provision of civic infrastructure. Though the

formal relationship of client-consultant-contractor-input supplier in the

modern sense might not have existed, the parties to the construction

process were the same. The design and construction always remained a

specialists function to be hired for a fee. The Indus Valley Civilization

that flourished roughly between 3250 to 2750 B.C had very advanced

architectural city planning and construction capabilities.

The Muslim Period

The rich traditions of architecture, irrigation and roadways were

continued by the Muslim rulers of Delhi. King Feroze Tugluk is called

90

the „Father of irrigation‟. The Mughal emperors were great builders and

the accounts of their activities have been well chronicled.

The British period

Construction was a hectic activity during the British period. But

their priorities were different from the previous rulers. They required

dwellings and offices suitable to their life style, roads and transportations

for easy and fast movement of British officers and Indian raw materials to

ports for shipment. Administrative convenience, commercial interest and

mobilization of investments from local areas were the primary

considerations of the British East India company. Since construction was

primarily a department activity under British, private consultants and

contractors never grew (Vaid, 2003)4.

Independence and After

Construction continued to be a departmental activity for some more

years after independence. The role of the private sector was limited to

contracting only. Public sector consulting firms were established in the

late sixties.

Although construction contracting in the modern sense commenced

in India in 1860s, the British Government favoured only the British

contractors. Indian contractors were given some sub-contracting and low-

end jobs. The situation changed after independence.

The Builders Association of India (BAI) was formally incorporated

in 1944. From 1950 onwards, the Association has been lobbying with the

central and state governments for getting sanctions for many construction

related activities and aspects.

Realizing the importance of construction to national development,

the Planning Commission had set up a Construction Economics Division

within its organization at the start of the second Five year Plan. But it

continued till the mid-seventies.

91

Another significant development in the construction took place in

1976 when the BAI established the Overseas Construction Council of

India (OCCI) to facilitate construction project exports and render help to

project exporting firms. The OCCI was the designated export promotion

council for the construction sector and had a consultative status with

EXIM Bank, ECGC and the Ministry of Commerce. The formation,

structure and status of the OCCI was a step forward in ordering the

desired administrative and regulatory mechanism for the construction

sector.

The Government of India set up a Task Force on Project Exports

under the chairmanship of Dr. Abid Hussain in 1982, to recommend ways

and means of increasing India‟s share in the overseas construction

market. The Task force stressed the need for training in promoting

projects and consultancy export. It also suggested the establishment of an

institute at the national level. In pursuance of the recommendations, the

National Institute of Construction Management and Research (NICMAR)

was started. The initiative was taken by 26 leading construction

companies with the active encouragement of the Government of India.

Construction is a component of most development works.

As such, budgets and allocations of various ministries and

Government bodies have components on construction. These agencies

perceive construction in terms of their mainline activities: housing,

buildings, water, power, roads, rural development, hospitals, schools etc.

Till the inception of NICMAR there was no national level

construction platform. This platform began to be provided by the

NICMAR, and all those concerned with construction irrespective of their

sectoral organizations, came together on this platform. This construction

platform of the NICMAR was converted into Construction Industry

92

Development Council (CIDC) in 1996 and all roles and responsibilities of

the former were passed on to the latter.

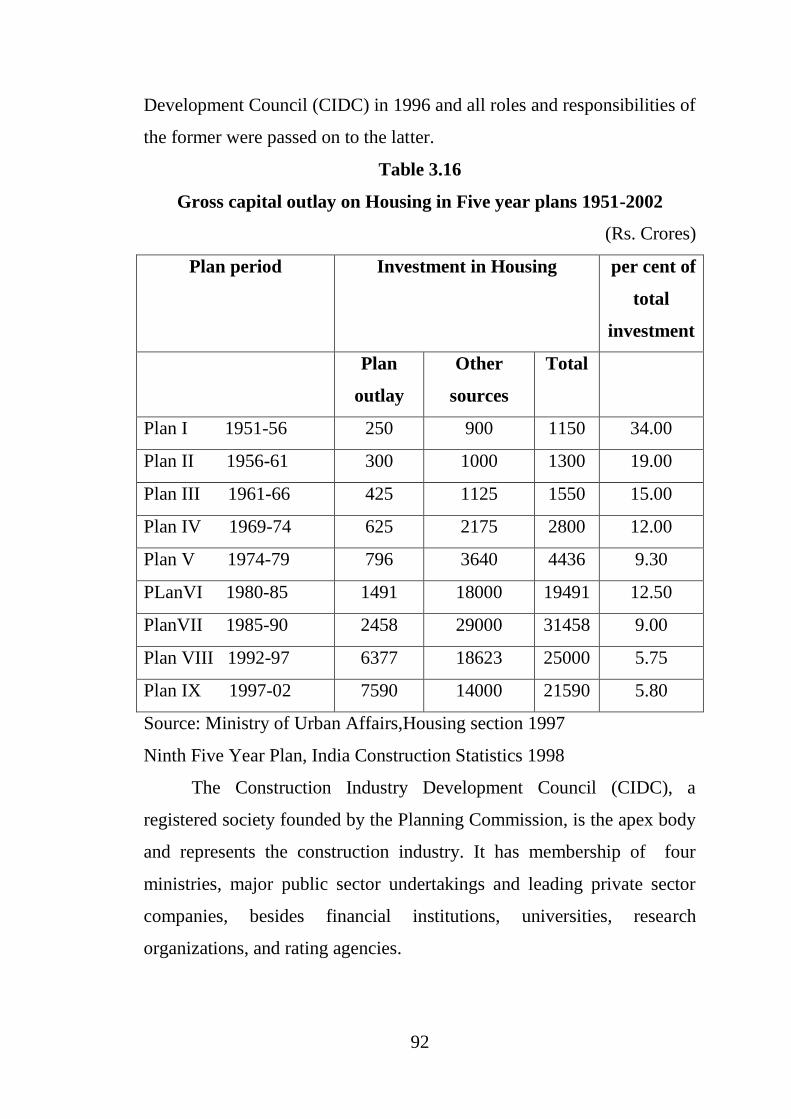

Table 3.16

Gross capital outlay on Housing in Five year plans 1951-2002

(Rs. Crores)

Plan period Investment in Housing per cent of

total

investment

Plan

outlay

Other

sources

Total

Plan I 1951-56 250 900 1150 34.00

Plan II 1956-61 300 1000 1300 19.00

Plan III 1961-66 425 1125 1550 15.00

Plan IV 1969-74 625 2175 2800 12.00

Plan V 1974-79 796 3640 4436 9.30

PLanVI 1980-85 1491 18000 19491 12.50

PlanVII 1985-90 2458 29000 31458 9.00

Plan VIII 1992-97 6377 18623 25000 5.75

Plan IX 1997-02 7590 14000 21590 5.80

Source: Ministry of Urban Affairs,Housing section 1997

Ninth Five Year Plan, India Construction Statistics 1998

The Construction Industry Development Council (CIDC), a

registered society founded by the Planning Commission, is the apex body

and represents the construction industry. It has membership of four

ministries, major public sector undertakings and leading private sector

companies, besides financial institutions, universities, research

organizations, and rating agencies.

93

Various central, state and municipal / local laws are applicable to

the construction industry. The laws relating to different aspects of the

sector fall under different categories. The various industry components

are regulated by different ministries, Government departments and

organizations like the Ministry of Environment and Forests, the Labour

Department, Pollution Control Board etc.

Many issues affect the smooth functioning of the sector. These

include contracting issues, financing issues, quality and technical issues

and manpower issues. Probably the biggest bottleneck facing the sector

today is the lack of skilled manpower. This is partly due to the lack of

demand for construction specific skills and partly due to lack of

institutions to help build the required skills.

The Construction Industry Development Council (CIDC) has

taken several steps to address the above problems. Some of the major

initiatives include devising a rating system to grade construction

companies, establishment of common lending norms to facilitate

financing, designing of quality assurance systems and several

programmes for upgrading worker skills.

The construction sector has started inducting the latest

development in IT and technology. Project design, development,

implementation and monitoring have been computerized. Major

initiatives include the establishment of a software development centre in

Hyderabad for the comprehensive incorporation of IT into every aspect of

construction and development of a wide network area-based system for

monitoring and control of projects across dispersed centres using IT.

The efforts of the Construction Industry Development Council

(CIDC) are laudable but they have not made a very marked difference;

their collective reach is still quite limited.

94

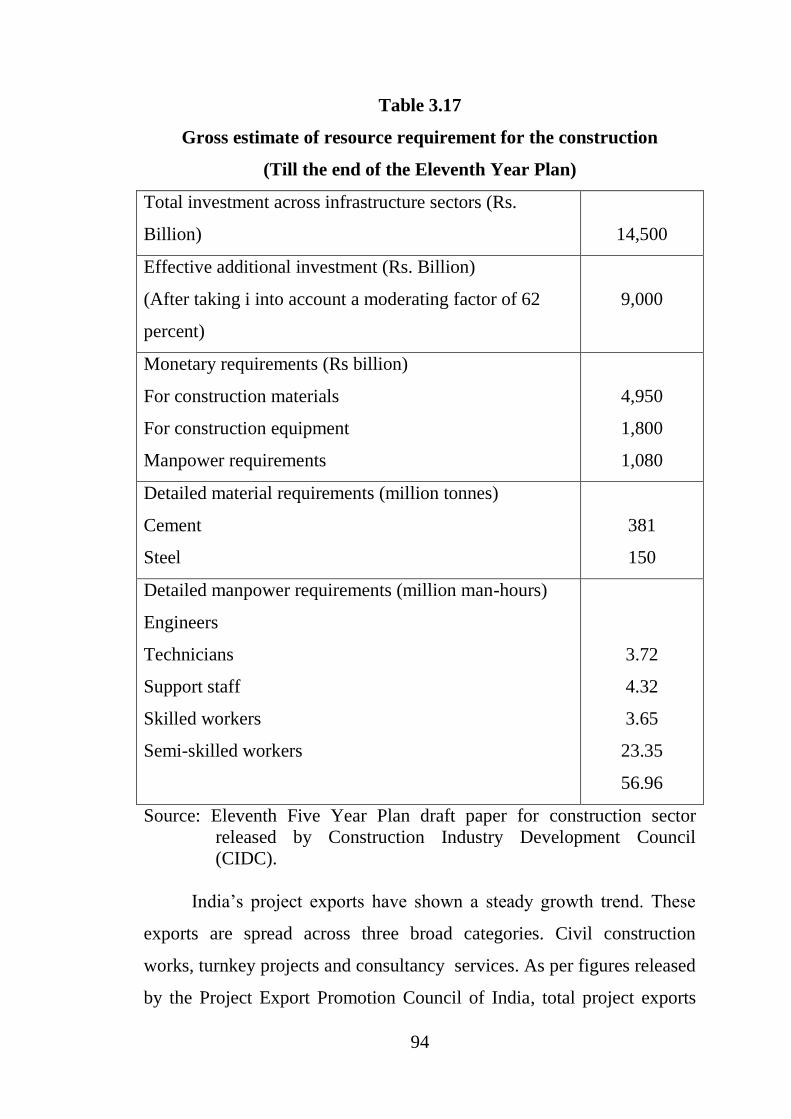

Table 3.17

Gross estimate of resource requirement for the construction

(Till the end of the Eleventh Year Plan)

Total investment across infrastructure sectors (Rs.

Billion)

14,500

Effective additional investment (Rs. Billion)

(After taking i into account a moderating factor of 62

percent)

9,000

Monetary requirements (Rs billion)

For construction materials

For construction equipment

Manpower requirements

4,950

1,800

1,080

Detailed material requirements (million tonnes)

Cement

Steel

381

150

Detailed manpower requirements (million man-hours)

Engineers

Technicians

Support staff

Skilled workers

Semi-skilled workers

3.72

4.32

3.65

23.35

56.96

Source: Eleventh Five Year Plan draft paper for construction sector

released by Construction Industry Development Council

(CIDC).

India‟s project exports have shown a steady growth trend. These

exports are spread across three broad categories. Civil construction

works, turnkey projects and consultancy services. As per figures released

by the Project Export Promotion Council of India, total project exports

95

(including the three categories given above) for 2005-06 were estimated

at Rs. 59.42 billion, a growth of nearly 29 percent over 2004-05. While

the Middle East has been the biggest market for project exports, major

projects have also been initiated in South East Asia, SAARC countries,

CIS countries, Africa and Latin America.

Currently, India is a small player in the global trade of construction

services. Many Indian companies do not have the technical and financial

strength to manage large turnkey projects. In most of the consultancy and

high-tech projects, it is the U.S.A which is dominating the world market

while Japan leads in the Asian market and South Korea in the Middle

East. It is to be noted that the use of modern and high-tech equipment in

the overseas construction has not percolated down to domestic

construction operations. As a result, construction activity within the

country remains low-tech and leisure-paced. Another impediment is the

lack of capital.

The Indian firms now have considerable exposure and expertise

and are well- equipped to face challenges in the international construction

market.

India has a large potential of expanding trade in construction and

allied services. The Government of India, the construction industry and

various organizational /associations in this sector need to take immediate

steps to make the Indian construction industry competitive at home and

abroad and to face the challenges and opportunities arising from trade

liberalization under GATS.

Construction Technology

Construction absorbs massive investments. Since construction is a

large activity anything done to improve its productivity must benefit, in

turn, the economy as a whole. Even a small improvement in productivity

level can lead to a large savings in time, cost and energy. For example, it

96

is estimated that completion of construction and commissioning of a

2000MW power station one month ahead of schedule would yield about

105 crores extra units of power which, if sold at Rs. 2 per unit, would

yield additional income of Rs. 210 crores and an ultimate increase in

GNP of Rs. 30000 crores (Vaid, 2003)5. Same is the case with building

construction where the benefits of productivity improvements and cost

savings are staggering.

Table No. 3.18

Construction Productivity

(Sq. meter per man-day)

1999 2000 2001 2002 20003 2004 2005

Physical

Measurement

Public

residential

0.50

0.50

0.50

0.50

0.50

0.50

0.51

Private

residential

0.50 0.50 0.50 0.50 0.50 0.50 0.51

Commercial 0.60 0.60 0.60 0.60 0.60 0.60 0.61

Industrial 0.70 0.70 0.70 0.70 0.70 0.70 0.71

Value added per

employee (no. of

units)

67,741

73,225

75,355

77,743

80,207

82,144

85,547

Source : Indian Infrastructure (2007)

But technology is managed by men and it is their capabilities and

motivations that make things happen.

Construction is an age old activity that has always used traditional

methods, techniques and materials. In India, for example, building

technology, which flourished in the Mughal period, had undergone a

revolutionary change with the establishment of Sultanate at Delhi in A.D.

1206.

97

In the pre-sultanate period, architecture progressed form rock-cut

technology to the Trabeate technique in which the pillars are placed

closely with stone blocks to support the heavy beam.

The Sultanate period brought the Arcuate system in which the vault

and the dome were used with lime and gypsum as mortars and this

enabled the use of fired bricks and rubble in complex constructions.

Although lime has been in use around 200 B.C in India and gypsum in

the Indus valley civilization, the two came to be used properly only after

the 13th

century.

However today‟s construction activity is not altogether traditional.

High rise buildings, complex designs, heavy reliance on concrete and new

materials, vertical transportations, pressure to finish projects quickly etc.

demand innovative work methods, new construction techniques,

mechanization of transportation and material handling systems and better

quality workmanship. At the same time, there are constraints on the

modernization of the construction activity. Some constraints are inherent

in the technology itself while some others exist due to social linkages of

technology. First, the current state of the construction industry does not

lend itself to mass production techniques. Limitations arise due to the

variations in the site conditions and owners‟ need to make their buildings

unique. Each facility has to be designed and produced to meet the

requirements of a given site as well as of the owner. Further, the site

operations must conform to local regulatory requirements of design and

building plans which may vary from one place to another.

Second, the efficiency of the construction work is affected by the

weather condition. Most of the work is done on sites exposed to

elements-inclement weather, rains etc. The intermittent and seasonal

nature of the construction activity leads to uneconomic and under

utilization of construction resources, and therefore, increased construction

98

costs. This is also one of the reasons for the low level of capital

investment by contractors.

Third, due to easy entry into the industry, small firms with scanty

resources and limited technical and financial capabilities proliferate.

Subcontracting and low labour wages justify the use of out-of-date

methods of construction. Low wages produce poverty on the one hand

and low productivity on the other. (Vaid, 2003)6.

Four, conditions of economic destitution and social backwardness

of construction workers are perpetuated along with lack of skills, poor

workmanship and low productivity.

Five, technological upgradation of the construction process,

improvement in the social quality of the workforce and economic size of

the firm must move hand in hand if efficiency and productivity are to be

improved. A contractor will have to hire high skill labour to mechanize

building operations. And as mechanization calls for the use of equipment,

the contractor needs to have financial resources to buy such equipment

and the technical capabilities in the firm to handle it.

Six, technology in the construction sector is related to a whole

spectrum of fields –materials machinery and equipments, process,

production systems, quality systems etc. The term technology denotes

much more than just the physical process of converting inputs into

outputs. It also signifies the procedural and organizational arrangements

for carrying out the transformation with economic benefits. New

materials play a major part in product and process innovations. But the

expenditure on technology is few and far between. In India, the public

capital outlay on Research and Development is 0.89 percent of the G N P

whereas the share comes to 3 per cent of the GNP in industrialized

countries. “Technology is not born. It is developed and made by human

99

beings through conscious planning and investment of money in machines

and man” (Bhaumik, 2001)7.

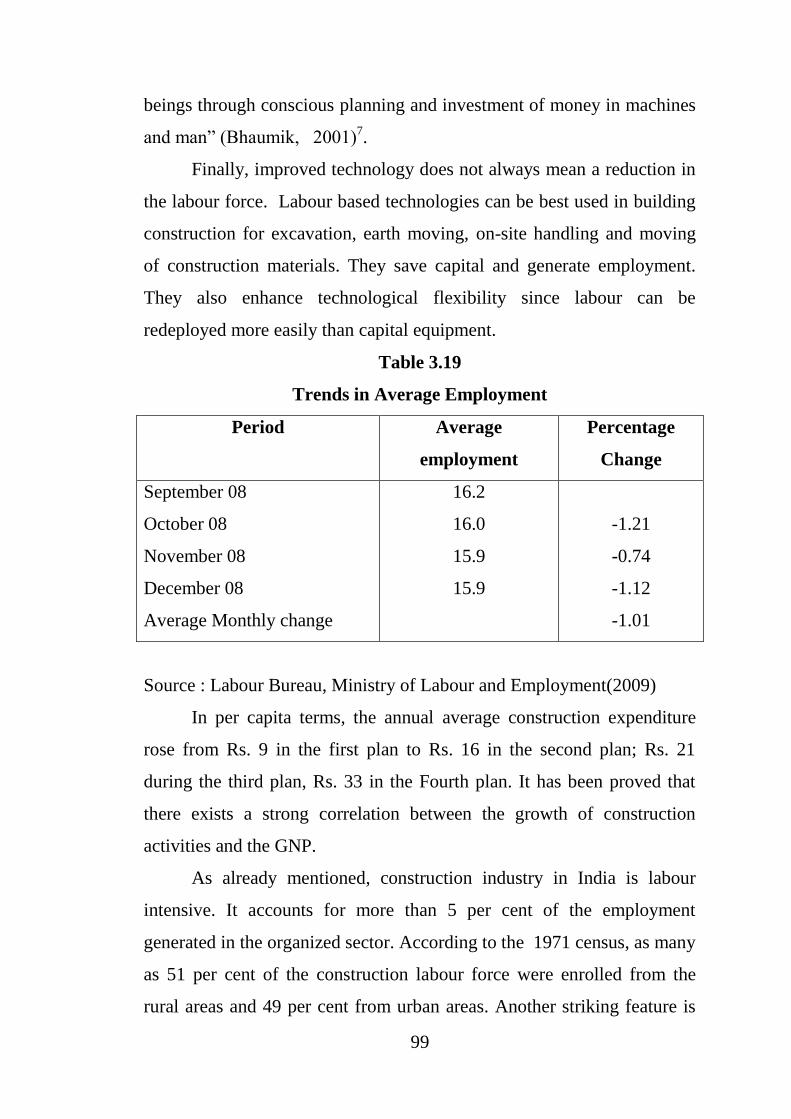

Finally, improved technology does not always mean a reduction in

the labour force. Labour based technologies can be best used in building

construction for excavation, earth moving, on-site handling and moving

of construction materials. They save capital and generate employment.

They also enhance technological flexibility since labour can be

redeployed more easily than capital equipment.

Table 3.19

Trends in Average Employment

Period Average

employment

Percentage

Change

September 08

October 08

November 08

December 08

Average Monthly change

16.2

16.0

15.9

15.9

-1.21

-0.74

-1.12

-1.01

Source : Labour Bureau, Ministry of Labour and Employment(2009)

In per capita terms, the annual average construction expenditure

rose from Rs. 9 in the first plan to Rs. 16 in the second plan; Rs. 21

during the third plan, Rs. 33 in the Fourth plan. It has been proved that

there exists a strong correlation between the growth of construction

activities and the GNP.

As already mentioned, construction industry in India is labour

intensive. It accounts for more than 5 per cent of the employment

generated in the organized sector. According to the 1971 census, as many

as 51 per cent of the construction labour force were enrolled from the

rural areas and 49 per cent from urban areas. Another striking feature is

100

that there has been a progressive increase in the member of women

absorbed in the construction activity. The National Building Organization

has estimated that every one million rupee worth of construction in India

generates an average employment of the order of 31800 man days of

unskilled and semi skilled, 30000 man days of skilled and about 13000

man days of managerial and technical personnel.

Workers in the construction industry are hired as and when

required and are retrenched on completion of the work. Due to temporary

nature of their jobs, workers remain idle till they find work at new

construction sites. In big constrictions firms, personnel at the supervisory

and managerial levels are employed on a permanent basis, but they have

to move from one project site to another. Construction labour, however, is

hired on a temporary basis and leads a migratory life, working on

different sites.

The economic condition of the construction labour is worst in our

country on account of their poor bargaining power due to lack of unions,

illiteracy and the temporary nature of their employment. Basic amenities

like shelter, drinking water, sanitary conveniences etc. are not adequately

provided to them at small construction sites. Nobody cares for the

education of their children.

Construction labour is the most disorganized sector in our country

and they do not enjoy the facilities which their counterparts in other

industries and organized sectors enjoy. Construction workers have no job

security and are the least trained. In many developed countries, there are

training institutes to train workers for particular trades such as mechanics,

wiremen, blacksmith operators, electricians etc. Although industrial

training institutes have been established in our country, their contribution

towards training of construction labour is not enough. Article 24 of the

constitution lays down that no child below the age of 14 years shall be

101

employed to work in any factory or sites, but still we have a large number

of child workers employed in our construction sites.

Construction workers are paid very low wages. There are two

methods of making wage payment to labour, namely the time rate system

and the piece rate system. Time rate is based on the actual time worked

and the piece rate system is based on the quantum of work carried out by

each labourer.

A number of trade unions are connected with the construction

industry (Gahlot and Dhir, 1991)8.

Indian construction-The changing face

Due to increase in outsourcing of labour through sub contractors,

the role of large construction companies has gradually changed from

physical construction to consultancy, management and co-ordination, and

a step forward to finding clients and marketing of products, which are in

turn produced by sub contractors. The top firms have moved to

international markets through mergers and acquisitions.

References

1 Op. Cit.

2 Op. Cit.

3 Op. Cit.

4 Op. Cit.

5 Op. Cit.

6 Op. Cit.

7 Bhaumik, Srimanta K. (2001) “Reforms in the real sector of the

industry”. The Hindu, December 9, 2003.

8 Op. Cit.