chapter no.2 conceptual frame work of npa...

TRANSCRIPT

45

Chapter No.2

Conceptual frame work of NPA management

1. Introduction

2. Meaning and definition of NPA

3. Factors contributing to NPA

4. Reasons for NPA

5. Early warning signals for NPA

6. Impact of NPA

7. Management of NPA

8. Remedies Available for NPA

9. Recommendations of the Narsimham Committee

10. RBI Guidelines for NPA Recognition

11. Why and How does an account become an NPA?

12. Treatment of account as NPA

Record of Recovery

Treatment of NPA- Borrower wise and not facility- wise

Agricultural Advance – default in repayment due to natural calamities

Housing loan to staff

Credit facilities Guaranteed by central / state Government

Project financing

Other Advances

Recognition of Income on Investment treated as NPA

NPA Reporting to Reserve Bank

Concept of commencement of commercial production and

Restructuring to loan account

Basic Consideration

Advances Granted under Rehabilitation packages Approved by

BIFRT/ Term lending Institutions

Internal System for classification of assets as NPA

13. Income Recognition

Income Recognition – policy

Reversal of Income on account becoming NPA

Booking of Income on investment in share & Bonds

Partial Recovery of NPA

Interest Application

14. Provisioning norms for NPA

15. conclusion

46

1. Introduction:

The word NPA is not something new to the bankers. It is regular but disguised

loan asset. As everyone knows, a portion of assets may become NPA .An asset

becomes non-performing when it ceases to generate income for the bank. The

serenity of the incidence of nonperforming assets in Indian public sector banks, noted

in the early 1990s, raised a severe hue and cry in various quarters. In fact the problem

started much earlier , which became evident from continued recapitalization of many

PSBs since 1985-86.chaterer by the root cause, malfunctioning of the PSBs increased

by the end of the 1980s.This led to the setting up of the Narasimbham Committee

(1991) which in fact identified NPA as one of the possible cause of the

malfunctioning of the PSBs .In order to quantify the NPA problem, Narasimham

committee (1991) made it mandatory on the part of the banks to publish annually the

magnitude of NPA. NPA are those categories of assets (advances, bills discounted ,

overdraft, cash credit etc.) For which any amount remains due for a period of 180

days. Accordingly, as from the march, 31st 2004, NPA is an advance where:

Interest and/or instalment of principal remain overdue for a period of

more than 90 days in respect of term loans.

The account remains out of order for a period or more than 90 days, in

respect of an overdraft/ cash credit(OD/CC)

The bill remains overdue for a period of more than 90 days ,in case of

bills purchased and discounted.

Interest and/or instalment of principal remain overdue for two harvest

seasons but for a period not exceeding two half years in the case of an

advance granted for agricultural purpose and

Any amount to be received remains overdue for a period of more than

90 days.

47

TABLE 1.1 : overview of NPA classification in india

Standard Asset It does not create any problem while paying interest/

instalments of the principal. It usually carries more

than normal risk attached to the business.

Sub- standard asset NPA for a period less than or equal to 12 months.

Doubtful Asset NPA for a period exceeding 12 months.

Loss Asset An asset where loss has been identified by the bank

or internal or external auditors or by the RBI

inspection.

2. Meaning and definition of NPA:

In a simple word ,an asset which, ceases to generate income for the

bank is called a non- performing asset (NPA). When a borrower could not pay

interest and/or instalment on a loan, which remain overdue for more than 180

days then it becomes non- performing. The basic factor to determine whether

an account is NPA or the record of recovery and not the availability of

security. The period of non- performance of 180 days has been reduced to 90

days with effect from March 31st, 2004.

Non Performing Asset means an asset or account of borrower, which

has been classified by a bank or financial institution as sub-standard, doubtful

or loss asset in accordance with the directions or guidance relating to asset

classification issued by The Reserve Banks of India.

According to S. Ramaswami (Accounting world Feb. 2008) “Non-

Performing Assets (NPA) have been a great worry for Indian Banks, with the

countdown started for the adoption of Based 2 norms, fear of breaching the

minimum level of capital adequacy looms large for some of banks.”

According to Dr.Ch. Rajesham and Dr.K.Rajender, “Non-Performing

Assets are those assets that cease to generate income for banks.”

In line with the international practices and as per the recommendations

made by the committee on Financial System (Chairman Shri M. Narsimham),

the Reserve Bank of India has introduced, in a phased manner, prudential

48

norms for income recognition, asset classification and provisioning for the

advances portfolio of the banks so as to move towards greater consistency and

transparency in the published accounts.

The securitization and Reconstruction of Financial Assets and

Reconstruction of Financial Assets and Enforcement of Security Interest

(SARFAESI) Act, 2002 defined non-performing assets as, “an asset or account

of a borrower, which has been classified by a bank or financial institution as

sub standard, doubtful or loss assets in accordance with the direction and

guidelines relating to asset classification issued by the RBI.”

3. Factors contributing to NPA:

According to a recent study conducted by the RBI, the underlying

reasons for NPA in India can be classified into two heads, namely:

I. Internal Factors

II. External Factors

Internal Factors

The following internal factors contribute to NPA in the order of prominence:

o Diversion of funds for expansion / diversification/ modernisation or for

taking up new projects.

o No satisfaction regarding credit worthiness of borrowers.

o Non- compliance to lending norms

o Lack of post credit supervision .

o Lack of appropriate margins

o In adequacy of documents.

o Excessive overdraft lending.

External Factors:

The external factors that contribute to NPA’s are the following:

o Recession in the economy as a whole

o Input or power shortage

o Price escalation of inputs

o Exchange rate fluctuation

49

o Accidents and natural calamities

o Changes in government policies relating to excise and import duties,

o Government loan waiver scheme

Other Factors:

Apart from the above factors, there are certain other factors which are

responsible for standard assets becoming NPA. They are the following:

(a) Liberalisation of the economy and the consequent pressures from

Liberalisation like severe competition , reduction of tariffs, removal of

restriction, etc.

(b) Poor monitoring of credits and the failure to recognise early warning

signals shown by standard assets.

(c) Promoters’ over optimism in setting up large projects.

(d) Sudden crashing of capital markets and the failure to raise adequate funds.

(e) Granting of loans for certain sectors on the basis of government’s

directives rather than commercial imperatives.

(f) Mismatch of funding i.e., using loans granted for long – term

transactions.

(g) High leveraging and high cost of borrowing.

(h) Commitment of wilful defaults sensing that the recourse available to

collect debts is very slow.

4. Reasons for NPA:

In priority Sector Advances:

i. Directed and pre-approved natures of loans sanctioned under

sponsored programmes.

ii. Mis- utilisation of loan and subsidies.

iii. Diversion of funds.

iv. Absence of security.

v. Lack of effective follow – up ( post- sanction supervision &

control).

vi. Absence of bankruptcy and fore - closure laws.

vii. Dicripit legal system.

viii. Cost in effective legal recovery measures.

50

ix. Difficulty in execution of decrees obtained.

x. Lack of marketing support.

In Non- priority Sector Advances:

Improper& inadequate credit appraisal

i. Demand recession.

ii. Frequent changes in govt. policies.

iii. Industrial sickness and labour problems.

iv. Antiquated legal & judicial system.

v. Lack of legal reform(bankruptcy, foreclosure laws. )

vi. Diversion of funds.Wilful default.

vii. Technology obsolescence.

viii. Incompetence- management failure(s).

ix. Fear psychosis among banks and lack of effective follow up

(policing of assets by banks).

x. Political compulsion and corruption.

While lenders have been making every possible effort for recovery of

NPA, it is the Indian legal system , which has failed them, as it is more geared

to protect borrowers and not lenders. Whereas borrowers can use hundred and

one tactics to delay the recovery process , the creditors have practically no

right(s). As a result, there was nothing that a bank or F1 could do after the

money was disbursed to the borrowers. It is often said ,”In India, one can see

sick companies and closed factories, but not sick promoters.”

5. Early Warning Signals:

The Early Warning Signals (EWS) are those which clearly indicate or

show some signs of credit deterioration in the loan account. They indicate the

potential problems involved in the accounts so that remedial action can be

initiated immediately. In fact most banks have EWS for identification of

potential NPA.

(a) Financial Signals

(b) Operational Signals

(c) Banking Signals

51

(d) Managerial Signals

(e) External Signals

Financial Warning Signals

Some of the financial warning signals are:

(a) Default in repayment

(b) Continuous irregularity in the account

(c) Devolvement of L/C or invocation of guarantees.

(d) Deterioration in working capital position or in liquidity

(e) Declining sales compared to precious period

(f) Substantial increase in long – term debts in relation to equal

(g) Raising sales but falling profits

(h) Incurring operating losses or net losses

(i) Raising level of bad debt losses

Operational Warning Signals

The operational warning signals are:

(a) Underutilisation of plant capacity

(b) Non-payment of electricity, wages, etc.

(c) Frequent labour problems

(d) Poor diversification and frequent changes in plane for expansion or

diversification or modernisation

(e) Evidence of overstocking and aged inventory

(f) Loss of important customers

Managerial Warning Signals

The managerial warning signals relate to:

(a) Diversion of funds and poor financial controls

(b) Lack of co operation from key personnel

(c) Change in management or ownership pattern or key personnel

(d) Undertaking of undue risks

(e) Fudging of financial statements

52

Banking Signals

Banking related warning signals are:

(a) Frequent request for further loans

(b) Delays in servicing of interest

(c) Reduction of operations in the accounts or reduction of bank

balances

(d) Opening of accounts with other banks

(e) Dishonour of cheques or return of bills sent for collection

(f) Not routing sales transactions through the account

(g) Delays in submitting stock statement and other data or non- submission

of periodical statements

(h) Frequent excesses in the account

External Warning Signals

Signals relating to external factors are:

(a) Economic recession

(b) Introduction of new technology

(c) Changes in government policies

(d) Emergence of new competition

(e) Natural calamities

(f) Weakening of industry characteristics

6. Impact of NPA :

Impact of NPA on Banking Operations :

The efficiency of a bank is not reflected only by the size of its balance

sheet but also by the level of return on its assets. The NPA do not generate

interest income for banks. At the same time, banks are required to provide

provisions for NPA from their current profits. The NPA have deleterious

impact on the return on assets in the following ways:

1. The interest income of banks will fall and it is to be accounted only on

receipt basis.

53

2. Banks profitability is affected adversely because of the providing of

doubtful debts and consequent to writing it off as bad debts.

3. Return on investments (ROI) is reduced.

4. The capital adequacy ratio is disturbed as NPA enter into its calculation.

5. The cost of capital will go up.

6. Asset and liability mismatch will widen.

7. It limits recycling of the funds.

7. Management of NPA:

The size of the NPA portfolio in the Indian banking industry was

increase .However, due to the active steps taken by the regulatory authorities

and the banks, the gross NPA level has reduced. To ensure long-term

profitability, banks have to manage NPA effectively by adopting the following

techniques:

(a) Ensuring that loans are diversified across several customer segments.

(b) Introducing robust risk scoring techniques to ensure better quality of

loans.

(c) Improving the quality of credit monitoring system by designating a

separate credit manager or relationship manager for that purpose.

(d) Raising the share of non- fund income by increasing service product

offering by better use of technology.

(e) Reducing operating expenses by upgrading the banking technology.

(f) Monitoring early warning signals and taking immediate appropriate

action.

(g) Adopting credit rating system to identify, measure and moniter the

credit rate of individual proposal.

(h) Putting certain borrow able accounts which exhibit certain distress

signals under watch list and paying a close and special attention so that

they may not become an NPA.

(i) Reducing the impact of operational risks by measure them and

mitigating insuring them.

(j) Knowing a clients profile thoroughly and preparing a credit report by

paying frequent visit to the client and his business unit.

54

(k) Appraising credit proposals professionally and insisting on timely

delivery of credit.

8. Remedies Available for NPA :

In spite of better credit management in terms of appraising and

monitoring of loan assets, NPA do occur. In such cases, various remedial

measures are available to deal with such NPA. The remedies may be broadly

divided into two namely.

(I) Non- legal remedies

(II) Legal remedies

Non- legal Remedies

Non- legal remedies may be in the form of compromise, mergers and

take-overs. The goods pledged or hypothecated may be sold without the

intervention of the court. The debts can be assigned in favour of an agency

which may come forward to collect debts for a service charge.

Legal Remedies

The RBI has advised lenders to initiate legal measure including

criminal action. Some of the important legal measurea available are:

(a) Filing of civil suits for the recovery of debts or for the enforcement of the

security.

(b) Filing of suits under State Recovery Act for the recovery f debts.

(c) Referring cases to Lokadalats constituted under the Legal Services

Authorities Act, 1987 which help in resolving disputes between the parties

by conciliation, mediation, compromise, or amicable settlement. Every

award of the Lokadalat shall be deemed to be a decree of a civil court.

(d) Resolving large loans via debt recovery mechanisms , most notably the

Corporate Debt Restructuring(CDR) mechanism. One time settlement

schemes have been tried with good results.

(e) Proceeding against the default borrower under the securitisation and

Reconstruction of Financial Assets and Enforcement of Security Interest

55

Act, 2002 which came into effect on June 21, 2002. Under the Act, banks

and financial institutions are allowed to issue demand notices to defaulting

borrowers and to take possession of the secured asset without the

intervention of the courts, if the dues are not paid within 60 days from the

date of such notice. The provisions of this Act are applicable to unsecured

loans or loans below Rs. 1,00,000 or loans due is less than 20% of the

principal amount and interest thereon.

Recently on April 8, 2004 the Supreme Court has upheld the validity

of the Seuritisation Act by giving one major relief to the borrower- litigant.

The earlier provision that the borrower will have to deposit 75% of the

disputed amount before appealing has been scrapped. With the implementation

of the SRFAESI Act , many lenders have commenced their recovery action

against recalcitrant debtors. Since the Supreme Court has upheld the

constitutional validity of the Act , it will go a long way in managing NPA

successfully. This Act also provides the formal legal basis for setting up Asset

Reconstruction Companies (ARCs) in India.

9. Recommendations of the Narsimham Committee:

Institutions would be given a period of three years to move towards the

above In regard to income recognition the committee recommends that in

respect of banks and financial institutions which are the following the accrual

system of accounting, no income should be recognized in the accounts in

respect of non-performing assets. An asset would be considered non-

performing if interest on such assets remains past due for a period exceeding

180 days at the balance sheet date. The committee further recommends that

banks and financial norms in a phased manner beginning with that current

year.

Provisioning / Asset Management:

For the purpose of provisioning, the Committee recommends that, using the

health code classification which is already in vogue in banks and financial

institutions, the assets should be classified into four categories namely,

Standard, Sub- standard, Doubtful and Loss Assets. In regard to Sub-Standard

56

Assets, a general provision should be created equal to 10 percent of the total

outstanding under this category.

In respect of Doubtful Debts, provision should be created to the extent of 100

percent of the security shortfall. In respect of the secured portion of some

Doubtful Debts, further provision should be created, ranging from 20 percent to

50 percent, depending on the period for which such assets remain in the doubtful

category. Loss Assets should either be fully written off or provision is created to

the extent of 100 percent.

The Committee is of the view that a period of four years should be given to the

banks and financial institution to conform to these provisioning requirements.

The movement towards these norms should be done in a phased manner

beginning with the current year. However, it is necessary for banks and financial

institutions to ensure that in respect of doubtful debts 100 percent of the security

shortfall is fully provided fir in the shortest possible time.

The Committee believes that the balance sheets of banks and financial

institutions should be made transparent and full disclosures made in the balance

sheets as recommended by the International Accounting Standards Committee.

This should be done in a phased manner commencing with the current year. The

Reserve Bank, however, may defer implementation of such parts of the

standards as it considers appropriate during the transitional period until the

norms regarding income recognition and provisioning are fully implemented.

The Committee suggests that the criteria recommended for non-performing

assets and provisioning requirements should be given due recognition by the tax

authorities. For this purpose, the Committee recommends that the guidelines to

be issued by the Reserve Bank of India under Section 43 D of the Income Tax

Act should be in line with our recommendations for determination of non-

performing assets.

57

Also, the specific provisions made by the banks and institutions in line with our

recommendations should be made permissible deductions under the Income Tax

Act.

The Committee further suggests that in regard to general provisions, instead of

deductions under Section 36 (1) (VIII) being restricted to 5 percent of total

income and 2 percent of the aggregate average advances by rural branches, it

should be restricted to 0.5 percent of the aggregate average non-agricultural

advance and 2 percent of the aggregate average advances by rural branches. This

exemption should also be available to banks having operations outside India in

respect of their Indian assets, in addition to the deductions available under

Section 36 (1) (viii).

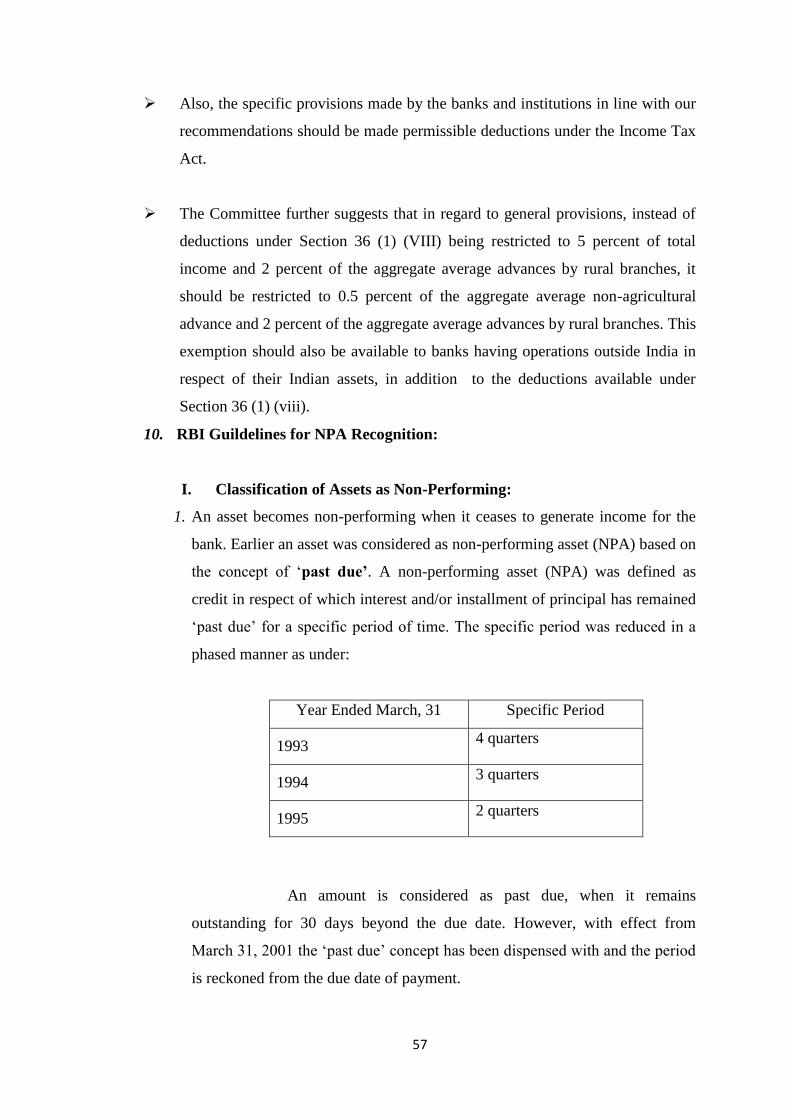

10. RBI Guildelines for NPA Recognition:

I. Classification of Assets as Non-Performing:

1. An asset becomes non-performing when it ceases to generate income for the

bank. Earlier an asset was considered as non-performing asset (NPA) based on

the concept of ‘past due’. A non-performing asset (NPA) was defined as

credit in respect of which interest and/or installment of principal has remained

‘past due’ for a specific period of time. The specific period was reduced in a

phased manner as under:

Year Ended March, 31 Specific Period

1993 4 quarters

1994 3 quarters

1995 2 quarters

An amount is considered as past due, when it remains

outstanding for 30 days beyond the due date. However, with effect from

March 31, 2001 the ‘past due’ concept has been dispensed with and the period

is reckoned from the due date of payment.

58

2. With a view to moving towards international best practices and to

ensure greater transparency, ’90 days’ overdue norms for identification of

NPA have been made applicable as below.

From 31st

March, 2004 an asset is considered to have gone bad when

the borrower has defaulted on principal and interest repayment for more then

one quarter or 90 days.

As per RBI guidelines NPA consist of sub-standard assets, doubtful

assets and loss assets. Any assets generally turn into NPA when they fail to

yield income during certain period. As a result, doubtful assets find its way

from sub-standard assets after 18 months in Indian context against 12 months

under the international norms and finally when it is found irrecoverable then it

moves to loss assets category. Banks are allowed to make full provision for

such assets i.e. 100 percent of unsecured portion of doubtful assets plus 20-50

per cent of secured portion (depending on the period for which the account is

doubtful) and a general 10 per cent (20 per cent under the international norms)

of the outstanding balance in respect of sub standard assets. The central bank

is in favors of implementing the time limit of 90 days from April, 2004 so that

the banks would remain competitive in the context of their international

exposure.

With effect from March 31, 2005, banks will have to classify assets as

‘doubtful’, if they remained under the sub-standard category for 12 months.

To help banks to overcome extra provisioning because of changes in assets

classification, the central bank has allowed a phased provisioning; a minimum

of 20 percent each year over four years.

In the light of the Narsimham Committee recommendations, from time

to time RBI has issued the guidelines in respect of recognition of NPA, their

classification and provisioning, which is summarized as under.

The following are the RBI guidelines for NPA classification and

provisioning.

59

Standard Assets:

Standard Assets, which are not NPA, but involve business risks,

require a minimum of 0.25 percent provision on global portfolio but not on

domestic portfolio.

Sub Standard Assets:

From 31.3.2001, these are those accounts which have been classified

as NPA for a period less than or equal to 18 months. The general provision of

10 percent of total outstanding interest should be made on sub-standard assets.

Doubtful Assets:

From 31.3.2001 these are those accounts which have remained as NPA

for a period exceeding 18 months. On these assets the banks are required to

provide 100 percent for the unsecured portion and an additional provision of

20 to 50 percent advances, if doubtful for 3 and above 3 years.

Loss Assets:

Loss assets are those NPA accounts which are last by the bank or

auditors or by RBI on inspection 100 percent provision for the amount

outstanding must be made.

Standard assets are treated as performing assets and the remaining

categories of sub-standard, doubtful and loss assets are known as NPA both on

gross and net basis. It is general practice to NPA in terms of percentage.

Tier I Bank (Unit banks i.e. banks having a single branch/ HO with

deposits upto Rs. 100 crores and banks having multiple branches within a

single district with deposits upto 100 crores) have been permitted to classify

loan accounts including gold loans and small loan upto Rs 1 lack as NPA

based on 180 days delinquency norm instead of the extant 90 days norm. This

relaxation will be in force upto March 31, 2008. The deposits base of Rs. 100

crores for the above will be determined on the basis of average of the

fortnightly Net Demand and Time Liabilities in the financial year concerned.

60

For the above category of banks, an account would be classified as Non

Performing Asset if the:

(I) Interest and/or installment of principal remain overdue for a period of

more than 180 days in respect of a Term Loan.

(II) The account remains ‘Out of Order’ for a period of more than 180 days, in

respect of an Overdraft/Cash Credit (OD/CC).

(III) The bill remains overdue for a period of more than 180 days, in the case of

bills purchased and discounted.

(IV) Any amount to be received remains overdue for a period of more than 180

days in respect of other accounts.

Tables including provisioning norms for the two different type of Co-

operative bank named tier I and Tier II Co-operative bank is as below.

Table no. 1.2 provision of tier I capital adequate

Period for which the advance has

remained in ‘doubtful’ category

Provision requirement

Up to one year 20 percent

One to three years 30percent

More than three years (D-III)

(I) Out standing stock of NPA as on

March 31, 2010

(II) Advances classified as ‘doubtful for

more than three years’ on or after

April 1, 2010

-50 percent as on March 31, 2010

-60 percent with effect from March

31,2011

-75 percent with effect from March 31,

2012

- 100 percent with effect from March 31,

2013

-100 percent

(Source: Master circular on income recognition, asset classification, Provisioning &

other Related Matters by RBI.)

61

Tier II bank (all UCBs other than those referred to at Para 2.1.3) shall classify

their loan accounts as NPA as per 90 day norm as hitherto.

Period for which the advance has remain

in doubtful category

Provision requirement

Upto 1 year 20 percent

1to 3 years 30 percent

More than 3 years

- Outstanding stock of NPA as on

March 31, 2009.

- Advances classified as doubtful for

more than 3 years on or after April

1, 2007

- 50 percent as on march 31, 2007

- 60 percent with effect from

March 31, 2008.

- 75 percent with effect from

March 31, 2009

- 100 percent with effect from

March 31, 2010.

- 100 percent

(Source: Master circular on income recognition, asset classification, Provisioning &

other Related Matters by RBI.)

11. Why And How Does an Account Become an NPA?

An account does not become an NPA overnight. It gives signals

sufficiently in advance that steps can be taken to prevent the slippage of the

account into NPA due to causes attributable to the borrower the lender and for

reasons beyond the control of both.

The following is a list of factors attributable to the borrower, which could

account for the borrowers accounts becoming non-performing assets:

Financial losses for two years consecutively.

Poor management and marketing strategy, poor assessment of demand,

over capacity for the product, lack of commitment entering a declining

market, price war, etc.

Diversion of funds within and outside the business or project, Sometimes

funds are diverted for another project.

62

Differences and disputes among promoters/directors.

The bandwagon effect – People with little experience in the field enter a

profession just because others have succeeded recently. This is common

in the construction, real estate and hospitality industries.

High cost base evidenced by labor costs , low productivity, distribution

costs, raw material cost, lugh recoganization cost.

Inadequate financial control demonstrated by poor debt

management/structure.

Inadequate information which is demonstrated by the following poorly

prepared budgets or no budgets, no costing/unit costs, limited

analysis/planning for stocks, capital expenditure not planned/budgeted.

Time and cost overrun due to poor supervision and control over the

project by the promoters.

Increasing low margin sales, debtor provisions, currency losses, creditor

pressure and short term debt. Emphasis on cash sales with little regard for

profit.

Borrowing to pay operational expenses like electricity, wages etc.

Recurrence of problems previously resolved.

Maintenance of expensive offices/keeping premises in a continuous state

of neglect.

Short term loans /Ad hoc loans/Excess over limits continuing beyond due

date.

Qualified audit opinion.

Unable to comply with loan covenants.

Liquidity ratios reveal deteriorating trends.

Increase in creditors days outstanding.

Speculative investments.

However, there are also external factors over also external factors over which

the borrower has no control and these could also lead to non performing assets.

These external factors could include:

Delay in financial closure.

Delay in realization of receivables.

63

Exchange rate fluctuation.

Depressed capital market.

General recession in the particular industry.

Changes in personal habits of promoters / key people.

Fraud is also a contributory factor to cases of NPA. The following are all signs

of fraud that need to be recognized in order to prevent NPA.

Sales / inventory / assets overstated, liabilities understated.

Audits cease.

Abnormally large fund transfers.

Significant cash balances in non-interest earning accounts.

Management overrides internal controls.

Sale of assets to related parties.

Unusual supplier relationships.

Staff working unusually long working hours.

Any sign of deceit, in appropriate attitude and reaction to questions

12. Treatment of Accounts as NPA:

1. Record of recovery:

I) The treatment of an asset as NPA should be based on the record of

recovery. Banks should not treat an advance as NPA merely due to

existence of some deficiencies which are of temporary in nature such as

non-availability of adequate drawing power, balance outstanding

exceeding the limit, non-submission of stock statements and the renewal of

the limits on the due date, etc. where there is a threat of loss, or the

recoverability of the advances is in doubt, the asset should be treated as

NPA.

II) A credit facility should be treated as NPA as per norms given below.

However, where the accounts of the borrowers have been regularized by

repayment of overdue amounts through genuine sources (not by sanction

64

of additional facilities or transfer of funds between accounts), the accounts

need not be treated as NPA. In such cases, it should, however, be ensured

that the accounts remain in order subsequently and a solitary credit entry

made in an account on or before the balance sheet date which extinguishes

the overdue amount of interest or installment of principal is not reckoned

as the sole criteria for treatment the account as a standard asset.

2. Treatment of NPA – Borrower-wise and not Facility-wise:

I) In respect of a borrower having more than one facility with a bank, all the

facilities granted by the bank will have to be treated as NPA and not the

particular facility or part thereof which has become irregular.

II) However, in respect of consortium advances or financing under multiple

banking arrangements, each bank may classify the borrowal accounts

according to its own record of recovery and other aspects having a bearing

on the recoverability of the advances.

3. Agricultural Advances – default in repayment due to natural calamities:

I) Where natural calamities impair the repaying capacity of agricultural

borrowers, primary (urban) Co-operative banks, as a relief measure may

decide on their own to:

(a) Convert the short-term production loan into a term loan or re-schedule

the repayment period, and

(b) Sanction fresh short-term loans

II) In such cases of conversion or re-shedulement, the term loan as well as

fresh short-term loan may be treated as current dues and need not be

classified as non performing asset (NPA). The asset classification of these

loans would, therefore, be governed by the revised terms and conditions

and these would be treated as NPA under the extant norms applicable for

classifying agricultural advances as NPA.

65

4. Housing loan to Staff:

In the case of housing loan or similar advances granted to staff

members where interest is payable after recovery of principal, interest need

not be considered as overdue from the first quarter onwards. Such loans/

advances should be classified as NPA only when there is a default in

repayment of installment of principal or payment of interest on the respective

due dates.

5. Credit Facilities Guaranteed by Central/ state Government:

(I) The credit facilities backed by guarantee of the Central Government

though overdue should not be treated as NPA.

(II) This exemption from classification of government guaranteed advances as

NPA is not for the purpose of recognition of income.

(III) From the year ended March 31, 2006, State Government guaranteed

advance and investment in State Government guaranteed securities would

attract asset classification and provisioning norms, if interest and/or

principal or any other amount due to the bank remains overdue for more

than 90 days irrespective of the fact whether the guarantee have been

invoked or not.

6. Project Financing:

In The case of bank finance given for industrial projects where

moratorium is available payment of interest, payment of interest becomes due

only after the moratorium or gestation period is over. Therefore, such amounts

of interest do not become overdue and hence NPA, with reference to the date

of debit of interest. They become overdue after due date for payment of

interest, if uncollected.

7. Other Advances:

(I) Advances against term deposits, NSCs eligible for surrender, IVPs, KVPs``A

and Life policies need not be treated as NPA although interest thereon may not

have been paid for more than 90 days provided adequate margin is available in

the accounts.

66

(II) Primary (urban) Co-operative banks should fix monthly/quarterly instalments

for repayments for repayment of gold loans for non-agricultural purposes

taking into account the pattern of income generation and repayment capacity

of the borrowers and such gold loan accounts may be treated as NPA if

instalments of principal and/or interest become overdue after due date.

(III) As regards gold loans granted for agricultural purpose, interest is

required to be charged as per Supreme Court judgment at yearly intervals and

payment should coincide with the harvesting of crops. Accordingly, such

advances will be treated as NPA only if installments of principal and/or

interest become overdue after due date.

8. Recognition of Income on Investment Treated as NPA:

The investments are also subject to the prudential norms on income

recognition. Banks should not book income on accrual basis in respect of any

security irrespective of the category in which it is included, where the

interest/principal is in arrears for more than 90 days.

9. NPA Reporting to Reserve Bank:

The primary (urban) Co-operative banks should report the figures of

NPA to the Regional Office of thee Reserve Bank at the end of each year

within two months from the close of the year in the prescribed proforma given

in the above table.

10. Project Financing:

In the case of bank finance given for industrial projects where

moratorium is available for payment of interest becomes due only after the

moratorium or gestation period is over. Therefore, such amounts of interest do

not become overdue and hence NPA, with reference to the date of debit of

interest. They become overdue after due date for payment of interest, if

uncollected.

67

11. Concept of Commencement of Commercial Production and

Restructuring of Loan Account:

Where a unit commences commercial production, but the level and

volume of production reached immediately after the date of completion of the

project is not adequate to generate the required cash floe to service the loan, it

may be necessary to re-fix the repayment schedule.

13. Guideline for Classification of Assets:

1. Basic Considerations:

(I) Broadly speaking, classification of assets into above categories should be

done taking into account the degree of well defined credit weaknesses and

extent of dependence on collateral security for realization of dues.

(II) In respect of accounts where there are potential threats to recovery on

account erosion in the value of security and existence of other factors such

as, frauds committed by borrowers, it will not be prudent for the banks to

classify them first as sub-standard and then as doubtful after expiry of 12

months from the date the account has become NPA. Such accounts should

be straight away classified as doubtful asset or loss asset, as appropriate,

irrespective of the period for which it has remained as NPA.

2. Advances Granted under Rehabilitation Packages Approved by

BIFRT/Term Lending Institutions:

(I) Banks are not permitted to upgrade the classification of any advance in

respect of which the terms have been re-negotiated unless the package of

re-negotiated terms has worked satisfactorily for a period of one year.

While the existing credit facilities sanctioned to a unit under rehabilitation

packages approved by BIFR/term lending institutions will continue to be

classified as sub-standard or doubtful as the case may be in respect of

additional facilities sanctioned under the rehabilitation packages the

income recognition and asset classification norms will become applicable

after a period of one year from the date of disbursement.

68

(II) A similar relaxation must be made in respect of SSI units which are

identified as sick by banks themselves and where rehabilitation

packages/nursing programmes have been drawn by the banks themselves

or under consortium arrangements.

3. Internal System for Classification of Assets as NPA:

(I) Banks should establish appropriate internal systems to eliminate the

tendency to delay or postpone the identification of NPA, especially in

respect of high value accounts. The banks may fix a minimum cut-off

point to decide what would constitute a high value account depending

upon their respective business levels. The cut-off point should be valid for

the entire accounting year.

(II) Responsibility and validation levels for ensuring proper assets

classification may be fixed by the bank.

(III) The system should ensure that doubts in asset classification due to any

reason are settled through specified internal channels within one month

from the date on which the account would have been classified as NPA as

per extent guidelines.

(IV) RBI would continue to identify the divergences arising due to non-

compliance, for fixing accountability. Where there is willful non-

compliance by the official responsible for classification and is well

documented, RBI would initiate deterrent action including imposition of

monetary penalties.

14. Income Recognition:

1. Income Recognition – Policy:

(I) The policy of income recognition has to be objective and based on the

record of recovery. Income from non-performing assets (NPA) is not

recognized on accrual basis but is booked as income only when it is

actually received. Therefore, banks should not take to income account

interest on non-performing assets on accrual basis.

69

(II) However, interest on advances against term deposits, NSCs, IVPs, KVPs

and Life policies may be taken to income account on the due date,

provided adequate margin is available in the accounts.

(III) Fees and commissions earned by the banks as a result of re-

negotiations or rescheduling of outstanding debts should be recognized on

an accrual basis over the period of time covered by the re-negotiated or

rescheduled or rescheduled extension of credit.

(IV) If Government guaranteed advances become ‘overdue’ and thereby

NPA, the interest on such advances should not be taken to income account

unless the interest has been realized.

2. Reversal of Income on Accounts Becoming NPA:

(I) If any advance including bills purchased and discounted becomes NPA as

at the close of any year, interest accrued and credited to income account in

the corresponding previous year, should be reversed or provided for if the

same is not realized. This will apply to Government guaranteed accounts

also.

(II) If interest income from assets in respect of a borrower becomes subject to

non-accrual, fees, commission and similar income with respect to same

borrower that have been accrued should ceased to accrue in the current

period and should be reversed or provided for with respect to past periods,

if uncollected.

(III) Banks undertaking equipment leasing should follow prudential

accounting standards. Lease rentals comprise two elements – a finance

charge (i.e. interest charge) and a charge towards recovery of the cost of

the asset. The interest component alone should be taken to income

account. Such income taken to income account, before the asset became

NPA, and remained unrealized should be reversed or provided for in the

current accounting period.

3. Booking of Income on Investments in Shares & Bonds:

(I) As a prudent practice and in order to bring about uniform accounting

practice among banks for booking of income on units of UTI and equity of

70

All India Financial Institutions, such income should be booked on cash

basis and not on accrual basis.

(II) However, in respect of income from Government securities/bonds of

public sector undertaking and All India Financial Institutions, where

interest rates on the instruments are predetermined, income may be booked

on accrual basis, provided interest is serviced regularly and is not in

arrears.

4. Partial Recovery of NPA: Interest Application:

(I) In case of NPA where interest has not been received for 90 days or more,

as a prudential norm, there is no use in debiting the said account by

interest accrued in subsequent quarters and taking this accrued interest

amount as income of the bank as the said interest is not being received. It

is simultaneously desirable to show such accrued interest separately or

park in a separate account so that receivable on such NPA account is

computed and shown as such, though not accounted as income of the

bank for the period.

(II) The interest accrued in respect of performing assets may be taken to

income account as the interest is reasonably expected to be received.

However, if interest is not actually received for any reason in these cases

and the account is to be treated as an NPA at the close of subsequent year

as per the guidelines, then the amount of interest so taken to income in the

corresponding previous year should be reversed or should be provided for

in full.

(III) With a view to ensuring uniformity in accounting the accrued interest of

both the performing and non-performing assets, the following guidelines

may be adopted notwithstanding the existing provisions in the respective

State Co-operative Societies Act;

(i) Interest accrued in respect of non-performing advances should not be

debited to borrowal accounts but shown separately under ‘Interest

Receivable Account’ on the ‘Property and Assets’ side of balance sheet

and corresponding amount shown under ‘Overdue Interest Reserve

Account’ on the ‘Capital and Liabilities’ side of the balances sheet.

71

(ii) In respect of borrowal accounts, which are treated as performing assets,

accrued interest can alternatively be debited to debit to the borrowal

account and credited to Interest account and taken to income account. In

case the accrued interest in respect of the borrowal account is not actually

realized and the account has become NPA as at the close of subsequent

year, should be reversed or provided for.

(iii) The illustrative accounting entries to be passed in respect of accrued

interest on both the performing and non-performing advances are

indicated in the Annex 3.

(iv) In the above context, it may be clarified that overdue interest reserve is

not created out of the real or earned income received by the bank and as

such, the amounts held in the Overdue Interest Reserve Account can

regarded as ‘reserve’ or a part of owned funds of the banks. It will also be

observed that the Balance Sheet format prescribed under the Third

Schedule to the Banking Regulation Act, 1949 (As Applicable to Co-

operative Societies) specifically requires the banks to show ‘Overdue

Interest Reserve’ as a distinct item on the ‘Capital and Liabilities’ side

vide item 8 thereof.

15. Provisioning Norms For NPA:

In conformity with the prudential norms, provision should be made on

the non-performing assets on the basis of classification of assets into

prescribed categories as detailed in paragraph III above.

(i) Taking into account the time lag between an account becoming doubtful of

recovery, its recognition as such, the realization of the security and the erosion

over time in the value of security charged to the bank, the banks should make

provision against assets, doubtful assets and sub-standard assets as below.

a) Loss assets:

1. he entire assets should be written off after obtaining necessary approval from

the competent authority and as per the provision of the Co-operative Societies

Act, /rules. If the assets are permitted to remain in the books for any reason,

100 % of the outstanding should be provided for.

72

2. In respect of an asset identified as a loss asset, full provision at 100 % should

be made if the expected salvage value of the security is negligible.

b) Doubtful assets:

1. Provisions should be for 100 % of the extent to which the advances is not

covered by the realizable value of the security to which the bank has a

valid resource should be made and realizable value is estimated on a

realistic basis.

2. In regard to the secured portion, provision may be made on the following

basis, at the rates ranging from 20 % to 100 % of the secured portion

depending upon the period for which the asset has remained doubtful.

16. Conclusion:

The Indian banking sector is facing a serious problem of NPA. The

extent of NPA is comparatively higher in Public sector banks. To improve the

efficiency and profitability, the bank has to be scheduled. Various steps have

been taken by government to reduce the NPA . IT is highly impossible to have

zero percentage NPA. But at least Indian banks can try competing with

foreign banks to maintain international standard .

NPA is a double- edged weapon , which affects bank profitability due

to interest income not being recognized on NPA accounts and loan loss

previously to be created from profit earned. The bank must adopy structured

NPA management policy for elimination or reducing the NPA in the banks. In

general the trend of NPA in CBE are increasing trend on the same time the

CBA has been adopted a very good techniques to contrel over the NPA.

73

References:

1. Vasant Desai, “ Banks and institutional Management, Re- Oriented Second

Edition 2010, Himalaya Publishing House.

2. Dr. K. Natarajan & Prof. E. Gordon, “ Banking Theory , Law and Practice

Twenty Second Revised Edition 2010, Himalaya Publishing House

3. Dr. Falguni C. Shastri, “ Asset Quality and Management of NPA” Book

Enclave, Jaipur India .

4. K. Rajender, “ Management of Non- Performing Assets in Public sector

Banks” an article published in the Indian Journal of Commerce, Vol.62 Jan-

March,2009.

5. H. Rajesham and K. Rajender-2007, Management of NPA in Indian Scheduled

Commercial Banks, The Chartered Accountants of India, 55(12) june,1952-

1960.

6. K. Rajender and S. Suresh. 2007. Management of NPA in Indian banking. A

case study of State Bank of Hyderabad. The management Accountant,42(9)

septemmber 740-749.

7. Money and Banking Centre for Monitoring Indian Economy,2007-08.

8. Rajiv Rajan and Sarat Chandra Dhal, “ Non- Performing Loans and terms of

Credit of Public Sector Banks in India: An empirical assessment. Reserve

Bank of India, Occasional Papers,24 (3) winter:8-121.

9. Santi Gopal Maji and Soma Cley,2003, “ Management of NPA in Urban Co-

Operative Bank”- A Case Study of the Khatra Peoples Co-Operative Banks

LTD. The Management Accountant, March pp.195-207.

10. Suplipta Ghosh,2006. NPA Management in District Central Co- Operative

Study of MCCBL and TGCCBL. The management Accountant, 31(2)

February,54-58.

11. Kajal Chaudhary and Monika Sharma, “ Performance of Indian Public Sector

Banks and private Sector Banks: A Comparative Study in International Journal

of Innovation Management and Technology.Vol.2 No.3 June 2011.

12. Dr. Vibha Jain: “ Non- Performing Assets in Commercial Banks: Regal

publication, New Delhi,,1st Edition 2007 P.78-79.

74

13. Hallinan, Joseph T. 2003, “ Bigger Banks, Better deals ?” Wall Street Journal-

Eastern Edition. Vol. 242, issue 84, PP.D1-D3.

14. RBI , Master circular on Prudential Norms on Income Recognition, Asset

classification and Provisioning.

15. Subramanium, K.1997. Banking Reforms in India. TMH Publishing Co. LTD

New Delhi.

16. Sagar R. Dave, Performance evalution in Indian Banking.

17. Wells Fargo & co. (2003) , “ Big Banks Report Strong gains , Led by wells

Fargo, Bank One.” Wall Street Journal- Eastern Edition, Vol.242, Issue 80,

P.c5.

18. Mohit Kakkar (2008) , “ comparative Analysis on Non-Performing Assets” ,

an article in International journal of Research in Commerce & management,

Volume No. 2 , Issue No. 7 July.

19. Dr. A. Shyamala, “ NPA in Indian Banking Sector: Impact on Profitability” an

article published in Indian Streams Research Journal, Vol.1 june 2012.pp 1-4 .

20. Bhattcharya H. (2001) , “ Banking strategy, Credit Appraisal & zLending

Decisions, Oxford Universith Press, New Delhi.

21. Jansen D. & Baye M. (1999) : Money, Banking & financial Markets- An

Economic Approach; AITBS Publishers and Distributers, New Delhi.

22. Dr. Aroop kumar Mehapatra, “ NPA’s Side effect and it’s curative mantra” ,

an article published in international Journal of Research in Commerce &

Management Vol. No.2 July 2011.

23. Rajaraman , Bhaumik and N. Bhatia (1999), “ NPA variation Across Indian

Commercial Banks” ,Economic and political Weekly, Vol. 37 No. 3 .

24. I & G Vaishitha (2002) , “ Non- Performing Assets of Public Sector Banks” ,

Economic and Political Weekly, Vol.37 No.5.

25. Das A. and S. Ghosh (2005) , “ Size, Non- Performing loan , Capital and

Productivity change”, An article in Journal of Quantitative Economics, New

Series, Vol.3 No. 2.

26. Mukharjee, Paramita, (2003) , “ Dealing With NPA” Money and Finance, Vol.

12, March 2003.

27. Sharma Meena,(2002) , “ Managing NPA through Asset Reconstruction

Companies”, Ed.Book, Economic Reforms in India, Deep & Deep

Publications, New Delhi.

75

28. Sandeep Sharma & Rajesh Sharma , “ Performance of Indian Public Sector

Banks with Special reference to NPA” an Article Published in the Indian

Journal Of Commerce, Vol. 63. No. 3 July- Sept.2010.

29. Price water house loopers 2004, “Management of NPA by Indian Banks”. IBA

Bulletin, Special issue. January 67-68.

30. Ms. Kanika Goyal, “ Empirical Study of NPA Management of Indian Public

Sector Banks” An article Published in Shri Krishna International Research &

Educational consortium, Vol. 1 Oct.2010.

31. Dr. Suresh Patidar, “ Analysis of NPA in Priority sector Lending” An article

Published in Bauddhik, Vol.3 Jan.2010.

32. Dr. Hosmani A.P. “ Unearthing the Epidemic of NPA- A Study with reference

to Public Sector Banks in India,” An article published in International Journal

of Multididiplinary research Vol. 1, Dec. 2011.

33. Renu Jatana , “ Impact of NPA on Profitability of Banks” , an article published

in Indian Journal of Accounting , Vol. XXXIX (2) June 2009.