chapter one 1.0 introduction. 1.1 background … law governs procurement and disposal at the central...

TRANSCRIPT

CHAPTER ONE

1.0 INTRODUCTION.

The research was about the effective implementation of the Procurement and Disposal Authority

guidelines in secondary schools a case study of Lunyo Hill Secondary school. The researcher

was motivated by the fact that effective implementation of public procurement and disposal

guidelines is largely ignored in Secondary schools and Lunyo Hill S.S has not been exceptional.

This has necessitated the need for research to establish how this can be addressed.

1.1 Background to the study.

The government of Uganda has reformed its Procurement and Disposal system. A key milestone

in this reform was the enactment of the Public Procurement and Disposal of Public Assets

(PPDA) Act. This law governs Procurement and Disposal at the central as well as the local

government levels. Procurement and Disposal activities in schools that fall under Ministry of

Education and sports (MOES) as well as District Administration through Decentralization are

accordingly regulated through this new law. (PPDA Act 2003).

Further, section 97 of the PPDA Act 1/2003, provides that the Authority May issue guidelines

from time to time which shall be laid down before parliament and shall be gazetted for better

carrying out of the objectives and functions under the Act.

The procurement decision – making system that existed in the secondary schools revolved

around Board of Governors, School Management Committee, PTA, Head Teachers and the

Bursar. Each of these school structures had its own specific functions; the procurement was

incidental to those main functions. There was no clear-cut demarcation between roles,

responsibilities and functions relating to procurement. While guidance may have been sought

from Central Tender Board (CTB) and Ministry of Education and Sports for big procurement,

the bulk of procurement was localized at the school level.

With the PPDA Act in force and the decentralization process underway, the moment to proceed

with the procurement reform at the institution level is at hand. Thus it is important to identify the

unique circumstances of schools in implementing the rules and regulations introduced by the

Act.

The Public procurement and disposal guideline for schools in Uganda, lays down procurement

and disposal rules and regulation for goods, works and services in schools.

It customizes the Act, the regulations and guidelines to school setting. The Guidelines is a desk

book guide to procurement and disposal operations. While care has been taken to incorporate all

the rules and procedures deemed necessary for procurement and disposal function in schools, it

is important to point out that it is not intended to replace the Act or the regulation and guidelines.

According to the PPDA guideline 2005 for schools in Uganda, the guideline draws from the Act

and the regulations. The Act and regulations contains all the details of the legal provisions

relating to principles, structures, relating relationships, documentations, delegation, type of

contracts and payments.

Therefore users of the guidelines are advised to consult the Act and regulations frequently so as

not to miss the detailed provisions when required. These guidelines may therefore be referred to

as the procurement and disposal guidelines for schools in Uganda. It applies to all public

procurement and disposal activities in schools subject to the provisions of the Act and

regulations in consultations with the Authority for interpretation and regulation.

Financial Performance.

According to Pandy (1999), Financial Performance means the ability to operate efficiently and

effectively. It further refers to profitability in terms of the organization that is, minimizing

expenses or expenditure and maximizing revenues of the organization as well as owners.

1.2 Statement of the problem.

Procurement and Disposal guideline is very important in every school for it enhances

accountability, transparency, service delivery, value for money and good financial performance.

However, this guiding tool has been flouted and ignored by managers in secondary schools and

has led to fraud, poor contract management, conflict of interest hence poor financial performance

and Lunyo Hill Secondary school has not been exceptional. This however has prompted the

researcher to assess the effects of effective implementation of the PPDA guidelines on financial

performance of this school.

1.3 General objectives.

The general objective of the study was to assess the effects of effective implementation of PPDA

guidelines on financial performance.

1.4 Specific objectives.

i. To find out how procurement planning affects financial performance of Lunyo Hill

Secondary School. ii. To establish how procurement controls affect financial

performance of Lunyo Hill Secondary School.

iii. To establish the relationship between contract monitoring and financial performance.

1.5 Research Questions.

i. How does procurement planning affect financial performance of Lunyo Hill Secondary

School?

ii. How does procurement control affect financial performance in the school?

iii. What is the relationship between contract monitoring and financial performance in lunyo

Hill Secondary School.

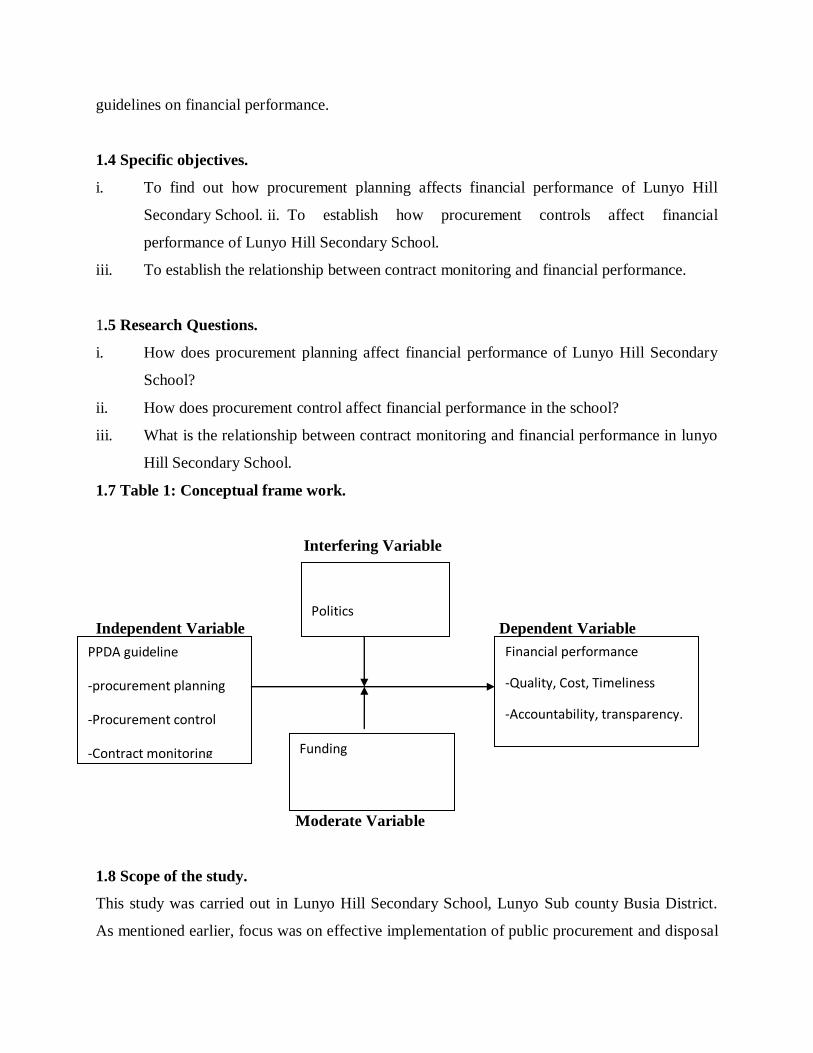

1.7 Table 1: Conceptual frame work.

Interfering Variable

Independent Variable Dependent Variable

Moderate Variable

1.8 Scope of the study.

This study was carried out in Lunyo Hill Secondary School, Lunyo Sub county Busia District.

As mentioned earlier, focus was on effective implementation of public procurement and disposal

Politics

Financial performance

-Quality, Cost, Timeliness

-Accountability, transparency.

PPDA guideline

-procurement planning

-Procurement control

-Contract monitoring Funding

guideline and financial performance of Lunyo Hill SS between the period 2008-2011 the

respondents were staffs of Lunyo Hill S.S.

1.9 Justification of the study.

The researcher carried out this particular research because he realized a problem of flouting

procurement guidelines and procedures which is against the PPDA Act 2003.

In Lunyo Hill Secondary School, the study was important because its results would help the

Directors, Administrators, Procurement Personnel, Accountants and Teachers to pay more

attention in the implementation of procurement guidelines and regulations to enhance good

Financial Performance.

The study will help policy markers and procurement cadres of the school to know more about the

importance of effective implementation of PPDA guideline to enhance Financial Performance.

The study will help the readers to add on the knowledge they have on procurement management

and financial performance.

1.10 Definition of key Terms.

PPDA Guideline;

Means directives issued by the Authority under section 97 of PPDA Act 2003

Procurement Planning;

Refers to aggregation of requirement to achieve lower unit cost.

Procurement Control;

Involves ensuring that procurement Act, Regulation and guidelines are followed.

Contract monitoring;

Is a regular process of evaluating agency performance based on measurable service deliverable

and verifying agency compliance with the terms and conditions of the contract.

CHAPTER TWO

LITERATURE REVIEW

2.0 INTRODUCTION.

This chapter reviews related literature to the topic under investigation. It involves a critical

review of what others have written on the subject of investigation. The source would be both

primary and secondary sources.

2.1 Procurement Planning.

Procurement planning is a process of determining the procurement needs of an entity and the

timing of their acquisition and their funding such that the entity’s operations are met as required

in an efficient way.

It is part of the procurement process of acquiring works, services and supplies that are required

to meet organizational needs. The Government of Uganda has made it mandatory for all

government institutions to have a procurement Plan, without it public procurement becomes

problematic for the Procurement and Disposal Entities and staff involved in the procurement

cycle.

According to public procurement and disposal of public Assets Act 2003, procurement planning

is done by the user department, procurement and disposal unit, Accounting officer, Board of

governors to mention but a few. The initiation of the requirement is done by the user departments

that prepare a multi- annual rolling work plan for procurement based on the approved budget.

Procurement planning is therefore integrated into annual and multi-annual sector expenditure

programme to enhance financial predictability, accounting and control over procurement. The

work plan therefore includes;

A detailed breakdown of activities of works, services or supplies to be procured, schedule of

procurement requirements, methods of procurement. All this is done to enhance good financial

performance in the organization.

Planning for a procurement activity takes into account the aggregation of requirements to

achieve lower unit cost, pre-qualification scheduling of available resources to process the

procurement requirement of the procurement and disposal entity.

Harold and Kootz (1990) observes that planning requires decision making that is choosing

among alternatives further course of action plans thus provide national approach to reselect

objectives and planning strongly implies managerial innovation.

Bashaka (2009), observes that procurement planning helps in achieving organizational goals/

objectives timely, minimizes emergencies, cost reduction, facilitating efficiency, controls cash

flows enables aggregation of various requirements and hence economies of scale. Bashaka also

affirms that procurement planning enhances team work, fraud detection, fosters harmony and

group working relationship, facilitates inventory management and increases productivity hence

enhancing good financial performance.

Bailey (1998), concurs with Bashaka (2009) that procurement planning helps in saving money

for the entity by obtaining price reduction through quantity discounts, enables consolidating of

requirements for greater economies and also providing sufficient time to obtain required

approval before submission of requisition. All these lead to good financial performance.

However Bashaka (2009) also observes that lack of procurement planning leads to high costs,

wastes, loss of advantages to buy in bulk, time wastage and conflict due to lack of role

differentiation.

PPDA Act (2003) section 34 (2) emphasizes due diligence and Regulation also requires the user

department to prepare a work plan for their procurement based on the approved budget as a key

aspect of procurement, it helps in testing consistency hence improving financial performance.

2.2 Procurement control effects on financial performance.

Procurement control involves following procurement cycle for efficiency and proper financial

performance since procurement activities take 70% of the organization budget. (PPDA act,

2003).

Controlling procurement related activities in the right way leads to good financial performance

for example if planning and budgeting is done, requirement requisitioned for , right prices quoted

paper specifications made, right deliveries and quality goods and services delivered this will lead

to achieving value for money and this helps in enhancing financial performance.

Zenz (1997) Observes that different organizations are setup for different purposes which include

achieving values for money, good service delivery to their customers and this can be achieved

through effective implementation of the procurement guideline that emphasizes control of

procurement activities whose quality goods and services be delivered to the customers in the

right quantity, quality and at the right time. Therefore by having proper procurement control

which discourages poor quality products, services, fraud in place, good financial performance

would be yielded.

Lysons (2000) observes that procurement control is very vital in an organization and that if well

managed financial performance would improve and organization will realize profits when proper

procedures are used.

Lysons further states that use of correct procurement process which entails specifications,

selection, ordering, monitoring and after sales service will enable the organization cut down a lot

of procurement related costs hence increasing profitability of the organization.

According to Baily (1998), procurement control performs several activities to ensure that the

organization performs well financially and delivers maximum value for money to the

organization for example, suppliers’ identification and selection, buying, negotiation and

measurement and improvement and purchasing system development. The accurate supplier’s

selection includes such factors as reliability, delivery dates, quality, reputation, financial status

and continuity of supplies.

Great care therefore must be taken over selection of every supplier as shortcut in this area would

lead to inefficiency and loss of profitability in the long run.

Zenz (1999), further affirms that procurement control involves maintenance of complete set of

records regarding the operation and activities of the department.

The information stored in these records include suppliers past performance and current prices of

goods and services required, copies of local purchase orders, contracts and agreements entered

into. This will lead to proper flow of information in the organization.

2.3 Relationship between contract monitoring and financial performance.

Lysons (2000), observes that there is a relationship between contract monitoring and financial

performance. Therefore supplier performance checks whether the supplier fall below predefined

performance rating during the course of purchasing, minimizes the amount of the final suppliers

that is to say contract monitoring takes into account the suppliers delivery performance after

supplier has been selected.

According to Bashaka (2009), the purpose of contract monitoring is to improve program

performance through early identification of questions and issue resolution, identify potential

problems that may require additional security evaluate agency performance controls to ensure

there is a reliable basis for validating source deliverables and to ensure that financial

documentation is adequate and accurate so that cost will not be questioned later on. By doing

this, best value for every pound spent will lead to good financial performance and this can also

be attributed to buying efficiently and wisely.

CHAPTER THREE.

METHODOLOGY

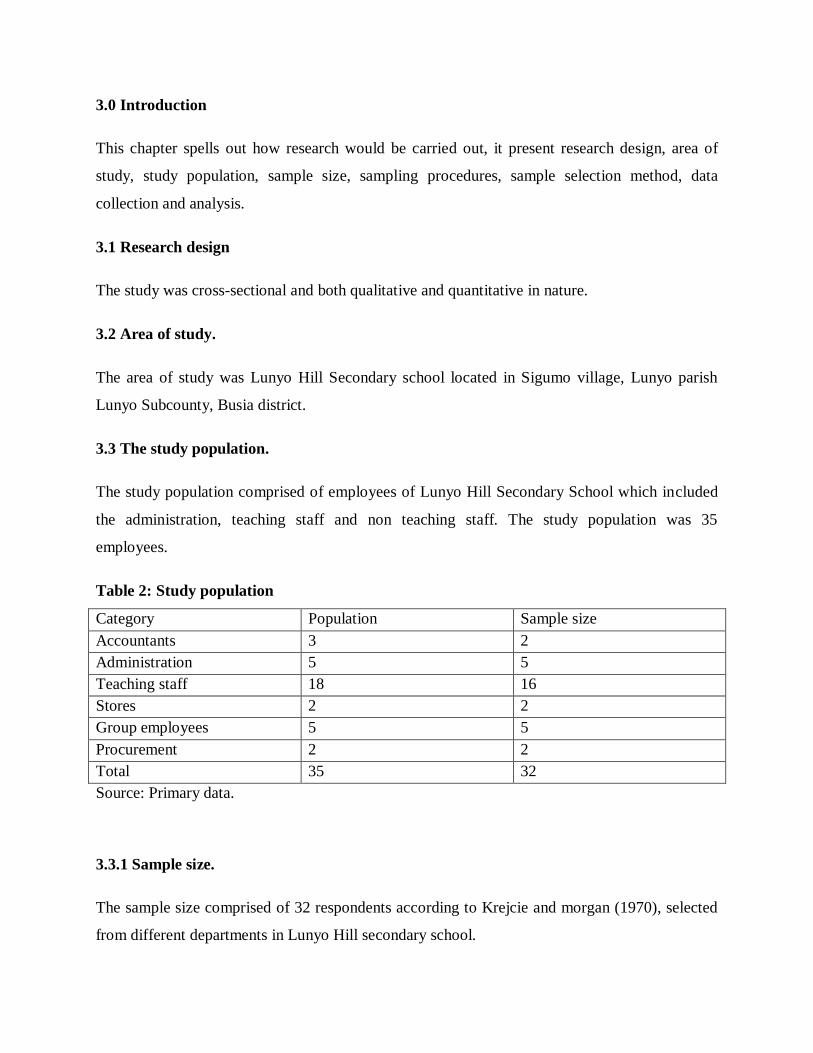

3.0 Introduction

This chapter spells out how research would be carried out, it present research design, area of

study, study population, sample size, sampling procedures, sample selection method, data

collection and analysis.

3.1 Research design

The study was cross-sectional and both qualitative and quantitative in nature.

3.2 Area of study.

The area of study was Lunyo Hill Secondary school located in Sigumo village, Lunyo parish

Lunyo Subcounty, Busia district.

3.3 The study population.

The study population comprised of employees of Lunyo Hill Secondary School which included

the administration, teaching staff and non teaching staff. The study population was 35

employees.

Table 2: Study population

Category Population Sample size

Accountants 3 2

Administration 5 5

Teaching staff 18 16

Stores 2 2

Group employees 5 5

Procurement 2 2

Total 35 32

Source: Primary data.

3.3.1 Sample size.

The sample size comprised of 32 respondents according to Krejcie and morgan (1970), selected

from different departments in Lunyo Hill secondary school.

This gave the researcher the opportunity to find out different information from respondents so as

to come up with logical conclusions.

3.3.2 Sampling techniques.

The researcher used stratified methods of sampling where the respondents would be picked from

the group and interviewed. This enabled the researcher to find out how effective implementation

of the procurement guideline affects financial performance in Lunyo Hill secondary school

3.4 Data collection method.

The researcher used the triangulation method of data collection which combines both qualitative

and quantitative methods of data collection; he used face to face interviews, observation,

questionnaire methods, and focus group discussions among others.

3.4.1 Data collection instruments.

The researcher used questionnaires list and interview guide because all the respondents would be

able to read and write.

3.5 Source of data.

3.5.1 Primary data.

The data was obtained through interviews with respondents and by self administered

questionnaires.

3.5.2 Secondary data.

This was got from Lunyo Hill secondary school review of procurement records, financial report

news paper, journal, PPDA guideline, regulation and the Act.

3.6 Data analysis.

The researcher analyzed the data using frequency distribution tables. This helped the researcher

to interpret data and draw conclusion and recommendations.

3.7. Anticipated research problems.

The cost involved in the research like transport costs to Lunyo, secretarial services,

telephone costs and stationary seemed to be high. However the researcher borrowed some

money from friends and relatives to meet the costs involved.

Limited time on the part of the researcher in order to meet the deadline of submission set

by the university. However, with this, the researcher dedicated some extra time on the

research work so as to finish.

CHAPTER FOUR.

4.0 PRESENTATION, INTERPRETATION AND ANALYSIS OF THE RESEARCH

FINDINGS.

4.1 Introduction.

This chapter involves presentation, interpretation and analysis of the research findings.

4.2 Background information.

The data was collected from the field using the methodology described in chapter three. During

the data collection, questionnaires and interviews were used basing on the objectives and

research questions and frequency tables used to analyze the data and then presented in form of

percentages. In analysis of data three objectives were tested to determine the effective

implementation of PPDA guideline on Financial Performance of Lunyo Hill Secondary school.

This part presents personal attributes of the respondents that were actively involved in the study.

It therefore shows the sex, age, educational level and the experience of the respondents in the

school

Table 3. Sex of the respondents.

Sex Frequency Percent Valid percent

Male 21 65.6 65.6

Female 11 34.4 34.4

Total 32 100.0 100.0

Source: primary data

In the table above, findings show that the highest number of respondents (65.6%) was males

while the least number (34.4%) represented the female. This therefore implies that the school

employees more males than females.

Table 4: Age of respondents.

Age Frequency Percent Valid percent

21-25 3 9.3 9.3

26-30 10 31.3 31.3

31-35 12 37.5 37.5

36-40 2 6.3 6.3

41-45 3 9.3 9.3

Above 46 2 6.3 6.3

Total 32 100.0 100.0

Source: Primary data.

From the above table, findings revealed that the highest number of the respondents 37.5% was

between 31-35 years, 31.3% were 26-30 years, 9.3% were between 41-45 and 21-25 respectively

6.3% were between (36-40) and 6.3% were above 46 years. This therefore implies that the

majority of Lunyo Hill SS employees were mature enough. Despite this they have failed to cope

up with effective implementation of procurement guidelines and this has contributed to poor

financial performance of the school.

Table 5: Responses showing the experience of the respondents.

Experience Frequency Percent Valid percent

Less than 1 year 3 9.4 9.4

2years 12 37.5 37.5

3-4years 8 25 25

More than 5years 9 28.1 28.1

Total 32 100.0 100.0

Source: primary data.

Findings from the above table revealed that the highest number of respondents 37.5% have

served the school for a period of 2 years, 28.1% have served for a period of 5years, 25% served

for a period between 3-4years and 9.4% for a period of less than 1 year.

This implies that the majority hard served the school for the period of 2years and this could be a

reason for ineffective implementation of the procurement guideline contributing to poor finance

performance.

Table 6: Education level of the respondents.

Education levels Frequency Percent Valid percent

Degree 6 18.7 18.7

Diploma 17 53.1 53.1

A’level 4 12.5 12.5

O’level 3 9.4 9.4

Primary 2 6.3 6.3

Total 32 100.0 100.0

Source: primary data.

53.1% of the respondents were Diploma holders, 18.7% University graduates, 12.5 finished

advanced levels, 9.4% attained ordinary level and 6.3% were of primary level.

The response implies that the highest number of respondents had degrees and diploma. Despite

this, procurement guidelines were not effectively implemented hence causing poor financial

performance.

4.3 Findings on the study variables.

Findings on the study variables were analyzed on specific objectives. Findings were therefore

presented in tables as below;

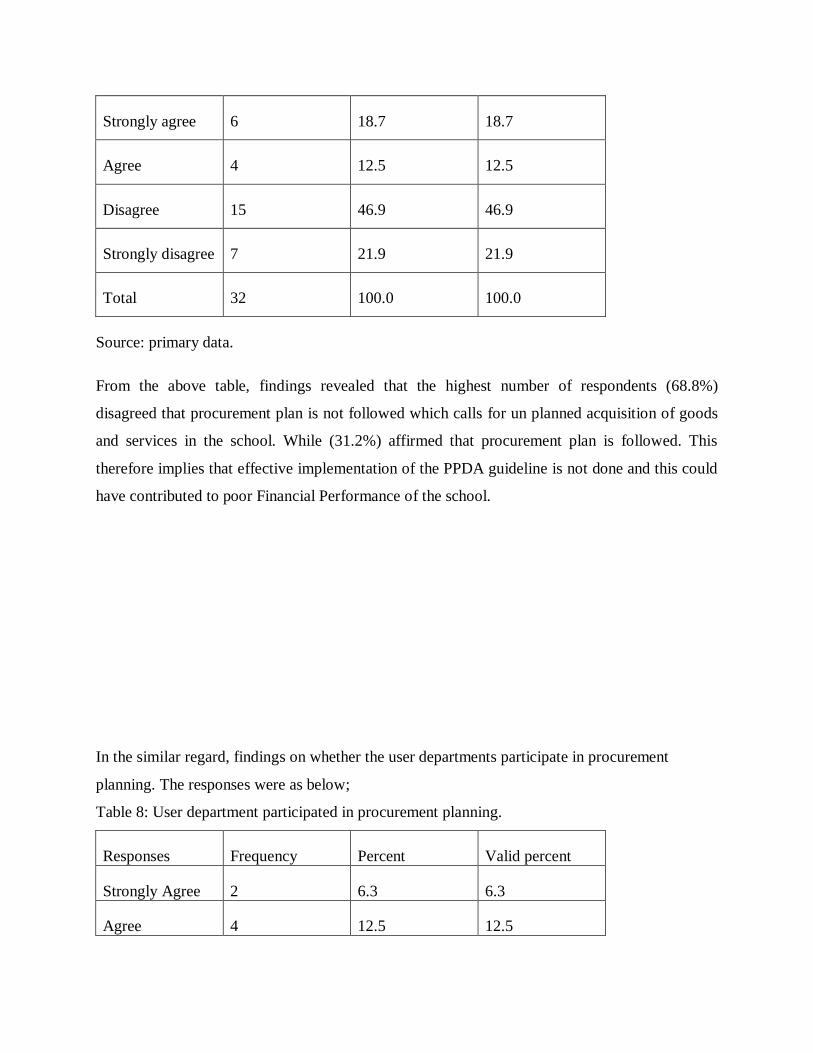

Table 7: Response on whether procurement planning is done effectively.

Responses Frequency Percent Valid percent

Strongly agree 6 18.7 18.7

Agree 4 12.5 12.5

Disagree 15 46.9 46.9

Strongly disagree 7 21.9 21.9

Total 32 100.0 100.0

Source: primary data.

From the above table, findings revealed that the highest number of respondents (68.8%)

disagreed that procurement plan is not followed which calls for un planned acquisition of goods

and services in the school. While (31.2%) affirmed that procurement plan is followed. This

therefore implies that effective implementation of the PPDA guideline is not done and this could

have contributed to poor Financial Performance of the school.

In the similar regard, findings on whether the user departments participate in procurement

planning. The responses were as below;

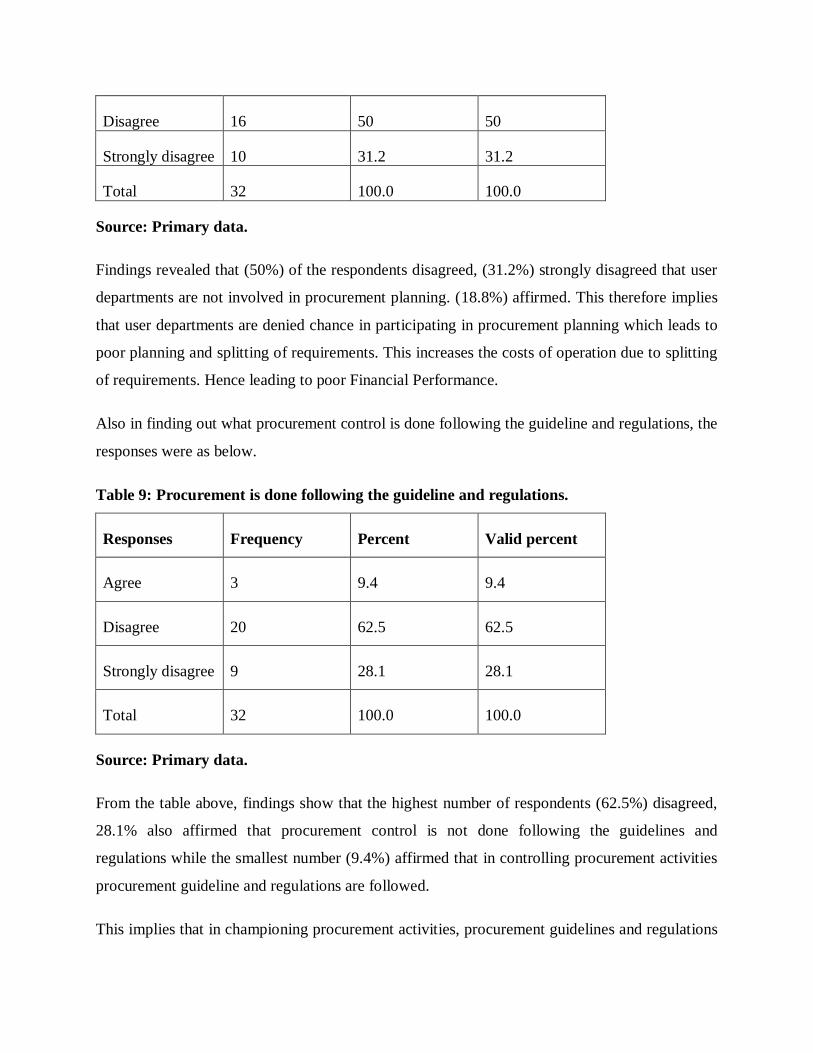

Table 8: User department participated in procurement planning.

Responses Frequency Percent Valid percent

Strongly Agree 2 6.3 6.3

Agree 4 12.5 12.5

Disagree 16 50 50

Strongly disagree 10 31.2 31.2

Total 32 100.0 100.0

Source: Primary data.

Findings revealed that (50%) of the respondents disagreed, (31.2%) strongly disagreed that user

departments are not involved in procurement planning. (18.8%) affirmed. This therefore implies

that user departments are denied chance in participating in procurement planning which leads to

poor planning and splitting of requirements. This increases the costs of operation due to splitting

of requirements. Hence leading to poor Financial Performance.

Also in finding out what procurement control is done following the guideline and regulations, the

responses were as below.

Table 9: Procurement is done following the guideline and regulations.

Responses Frequency Percent Valid percent

Agree 3 9.4 9.4

Disagree 20 62.5 62.5

Strongly disagree 9 28.1 28.1

Total 32 100.0 100.0

Source: Primary data.

From the table above, findings show that the highest number of respondents (62.5%) disagreed,

28.1% also affirmed that procurement control is not done following the guidelines and

regulations while the smallest number (9.4%) affirmed that in controlling procurement activities

procurement guideline and regulations are followed.

This implies that in championing procurement activities, procurement guidelines and regulations

are not followed which could have contributed a lot in cost cutting, right quantity and quality of

the goods and services procured. Due to these inefficiencies the school has experienced poor

performance problem which has retarded the growth and the expansion of the school

In analyzing whether procurement procedures are flouted, the responses were as seen below.

Table 10: procurement procedures are flouted.

Responses Frequency Percent Valid percent

Strongly agree 22 68.8 68.8

Agree 6 18.7 18.7

Disagree 4 12.5 12.5

Total 32 100.0 100.0

Source: primary data.

In the above table, findings revealed that (87.5%) of the respondents affirmed that procurement

procedures are flouted since procurement process is not followed in the acquisition of goods and

services. This therefore brings in inefficiencies in services delivery. Failure to honor the

procurement procedures ushers in discrimination, lack of transparency. This has affected the

financial performance of the school. Closely related to the above, in analyzing whether tenders

are awarded to the successful bidders Responses were as follows;

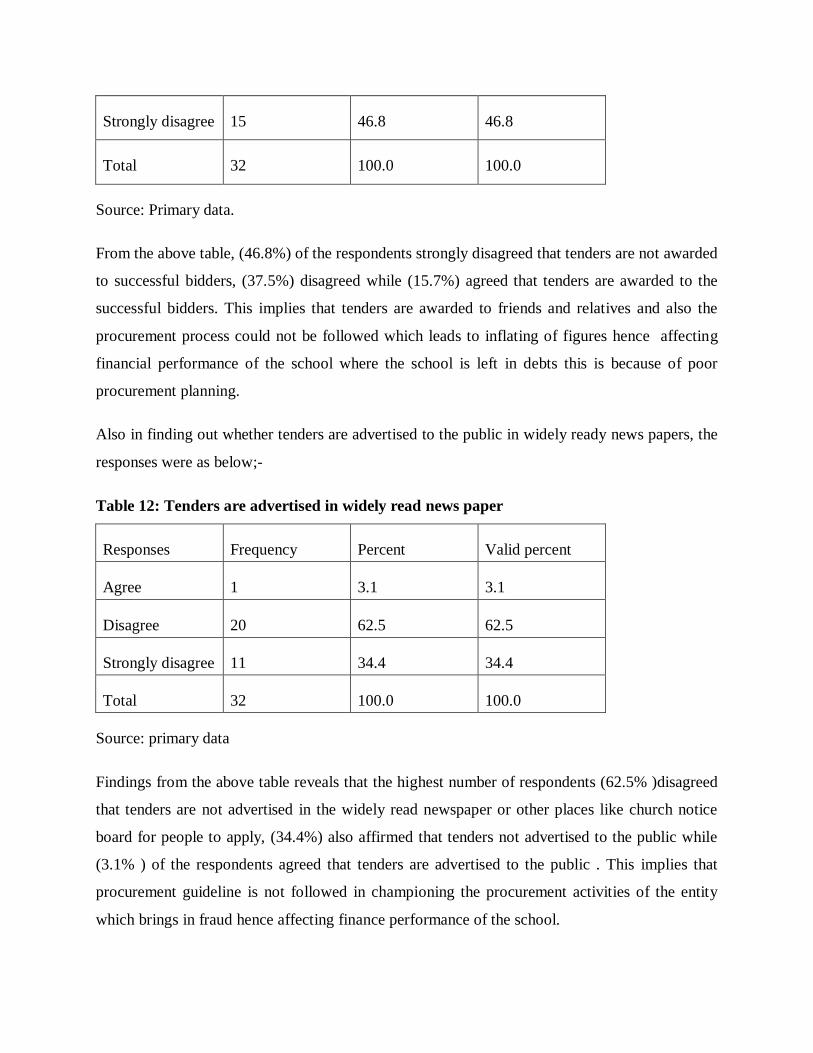

Table 11: Tenders are awarded to the successful bidders.

Responses Frequency Percent Valid percent

Strongly agree 2 6.3 6.3

Agree 3 9.4 9.4

Disagree 12 37.5 37.5

Strongly disagree 15 46.8 46.8

Total 32 100.0 100.0

Source: Primary data.

From the above table, (46.8%) of the respondents strongly disagreed that tenders are not awarded

to successful bidders, (37.5%) disagreed while (15.7%) agreed that tenders are awarded to the

successful bidders. This implies that tenders are awarded to friends and relatives and also the

procurement process could not be followed which leads to inflating of figures hence affecting

financial performance of the school where the school is left in debts this is because of poor

procurement planning.

Also in finding out whether tenders are advertised to the public in widely ready news papers, the

responses were as below;-

Table 12: Tenders are advertised in widely read news paper

Responses Frequency Percent Valid percent

Agree 1 3.1 3.1

Disagree 20 62.5 62.5

Strongly disagree 11 34.4 34.4

Total 32 100.0 100.0

Source: primary data

Findings from the above table reveals that the highest number of respondents (62.5% )disagreed

that tenders are not advertised in the widely read newspaper or other places like church notice

board for people to apply, (34.4%) also affirmed that tenders not advertised to the public while

(3.1% ) of the respondents agreed that tenders are advertised to the public . This implies that

procurement guideline is not followed in championing the procurement activities of the entity

which brings in fraud hence affecting finance performance of the school.

Findings whether the school has a contract committee in place, the responses were as below;

Table 13: The school has a contract committee.

Responses Frequency Percent Valid percent

Strongly Agree 2 6.25 6.25

Agree 2 6.25 6.25

Disagree 28 87.5 87.5

Total 32 100.0 100.0

Source: primary data.

From the table above, the highest number of respondents (87.5%) disagreed that the contract

committee is not in place while (12.5%) representing the minority affirmed that the contract

committee is in place. Therefore following the majority respondents, it implies that the school

has no contract committee and as a result award of tenders to providers is done without proper

evaluation and scrutiny of the providers. Therefore the absence of such committees in place to

look at the procurement method and procedures used in the acquisition of goods contributes a lot

to manipulation of the figures hence charging the entity highly on the goods and services

supplied to the entity. Thus affecting the financial performance of the entity.

In relation to the above, in analyzing whether standard bidding documents are prepared and used

in the procurement process. The responses where given as here under;

Table 14: Standard bidding documents are used.

Responses Frequency Percent Valid percent

Agree 2 6.3 6.3

Disagree 9 28.1 28.1

Strongly Disagree 20 62.5 62.5

Neither Agree or disagree 1 3.1 3.1

Total 32 100.0 100.0

Source: Primary data

Findings reveals that (62.5%) of respondents strongly disagreed that standard bidding documents

are used in the procurement process, (28.1%) disagreed while the smallest number 6.3% agreed.

This implies that non use of standard bidding documents could have brought in many

inefficiencies hence leading to poor financial performance.

Table 15: Effective implementation of procurement guideline can help to improve financial

performance.

Responses Frequency Percent Valid percent

Agree 24 75 75

Strongly agree 8 25 28

Total 32 100 100

Source: primary data

Findings from the above table reveal that (75%) of the respondents affirmed that effective

implementation of the procurement guideline can improve finance performance of the school,

(25%) strongly affirmed. This therefore implies that effective implementation of procurement

guideline for example use of standard bidding documents, procurement plan, contracts

monitoring, award of tenders to the successful bidders coupled with proper prices and quality

and quantity can enhance value for money. As a result, Financial Performance shall be enhanced

and with Lysons who contends that proper implementation of the procurement guidelines lead to

acquire goods at a low cost hence saving a lot for the entity thus boosting the entity’s financial

performance.

CHAPTER FIVE

5.0 DISCUSION, SUMMARY, CONCLUSION AND RECOMMENDATIONS

5.1 Introduction.

This chapter involves discussion, summary, conclusion and recommendations.

5.2 Discussion of findings.

A considerable number of respondents in the field revealed that financial performance was still

poor due to ineffective implementation of the public procurement and disposal guideline. This is

in line with Bashaka (2009) where upon he states that procurement guideline should aim at

enhancing financial performance and this can be achieved through cutting down the costs

through effective negotiation.

Further findings revealed that there is a lot of inefficiencies in the way goods and services are

acquired for example no proper procedures followed, no contract committee in place, no

advertisement made to the public. All these inefficiencies affect the financial performance of the

institution. This is in line with Lysons (2000) where upon he argues that effective

implementation of the procurement guidelines would help in cutting the costs hence enjoying

value for money and this would enhance financial performance of the school if activities are

channeled in a proper way.

Findings also showed that contracts monitoring in the institution was poor. This was showed by

lack of procurement documents in place which is a sign of inefficiency and poor planning of the

procurement schedules. Bashaka (2009) affirms that poor record keeping brings in loopholes and

inefficiency in the institution and as a result financial performance is affected due to lack of

accountability.

Further responses from the study revealed that advertisement of tenders or invitation for bids is

not done by the institution and these calls for non transparency, wrong selection of providers

without any competition. This is totally against PPDA Act 2003 which encourages competitive

bidding for smooth running of procurement activities in the institution. Also to mention is that

non advertisement of bids calls in for discrimination which is against the PPDA regulation and

guidelines.

Findings also showed that there was no contracts committee in place yet it is a requirement for

every entity to have a contract committee which committee does the work of adjudication and

award of contract, approves the solicitation documents, evaluation committee and also

recommendations from the procurement and disposal unit of the entity. PPDA Act (2003).

The study findings also revealed that the procurement planning is not done effectively and this

can be showed by non involvement of the user departments in the planning of procurement

activities for example should be acquired at what time. PPDA Act, regulation and guideline

argues entities to carryout procurement planning for efficiency and effectiveness of the entity.

5.3 Summary of Findings.

There is poor financial performance due to ineffective implementation of procurement guideline

by the institution especially; there is poor procurement planning, poor record keeping, lack of

transparency, poor contract monitoring, ineffective internal control. All these inefficiencies in the

implementation of procurement guideline affect financial performance of the organization.

5.4 Conclusion.

The researcher during the study realized that there were a lot of inefficiencies in the financial

performance of the institution as a result of the ineffective implementation of the PPDA

guidelines.

There is a correlation between procurement guidelines and financial performance in the

institution. The relationship here is that procurement guidelines used by the institution affect its

Financial Performance. It is therefore evident that procurement guideline used by the institution

does not enable the institution to have financial discipline.

5.5 Recommendations.

The researcher through the study brings out the following recommendations.

The institution should effectively implement the PPDA guidelines to improve financial

performance.

The institution should emphasize procurement planning and control to enhance financial

performance and this can be achieved through effective implementation of the PPDA guidelines.

All contracts should be monitored by the concerned person and report to the contracts committee

for any departures from the terms and conditions of the contract.

5.6 Areas for further research.

It can not be claimed that the study to assess the effective implementation of the PPDA guideline

on finance performance was exhausted.

The researcher proposes the following as possible areas of further research in relation to the

study.

The impact of procurement ethics on financial performance of an organization.

The effect of monitoring and evaluation on financial performance of an organization.

REFERENCES

Baily P.J.H (1987). Purchasing and supply management 5th

Ed, International Thomson Business

press, London United Kingdom.

Baily P&Jessop D (1998). Purchasing principles and management 8th Ed, prentice Hall, Pearson

Education limited, Edinbwigh Gate, England.

Lysons, K. (2000), purchasing and supply Chain management, 15th Ed. Prentice Hall, Pearson

Education, Edinbwgh Gate, England.

Zenz, G.J (1994), Purchasing and the management of materials, 7th

Ed Published by John Willy

and Sons Inc, New York, U.S.A.

Jessop, D & Morrison; A, (1994) storage and supply of materials, 6th

Ed,Pitman Publishing

London, United Kingdom.

Bashaka, B, (2009). Procurement planning and management in the public and private sectors

Appendix

Questionnaire for selected staff of Lunyo Hill Secondary School.

Dear Respondents.

I am Wabwire Eridard a student of Makerere University carrying out a research study on the

Effect of Effective implementation of Public Procurement and Disposal Authority guidelines on

Financial Performance.

You are kindly requested to spare little of your precious time and fill this questionnaire.

Background information,

1. Sex

Female Male

2. Age of respondents.

21-25 26-30 31-35

36-40 41-45 Above 46

3. Experience of respondents

Less than 1year 2years 3-4years more than 5years

4. Education levels of the respondents

Degree Diploma A’level O’level

Primary

General Research Questions.

Statement Strongly

Agree

Agree Disagree Neither

Agree nor

Disagree

Strongly

disagree

5. Procurement planning is done

effectively

6. Procurement plan is followed

7. User departments participate

in procurement planning.

8. procurement is done

following guidelines and

regulations

9. Procurement procedures are

flouted

10. Tenders are awarded to the

successful bidders

11.Tenders are advertised

12. The school has a contract

committee in place

13. Standard bidding documents

are used

14.Procurement guideline can

help to improve financial

performance of the school