chapter seven portfolio analysis. the efficient set theorem n the theorem an investor will choose...

TRANSCRIPT

CHAPTER SEVEN

PORTFOLIO ANALYSIS

THE EFFICIENT SET THEOREM THE THEOREM

•An investor will choose his optimal portfolio from the set of portfolios that offermaximum expected returns for varying

levels of risk, andminimum risk for varying levels of

returns

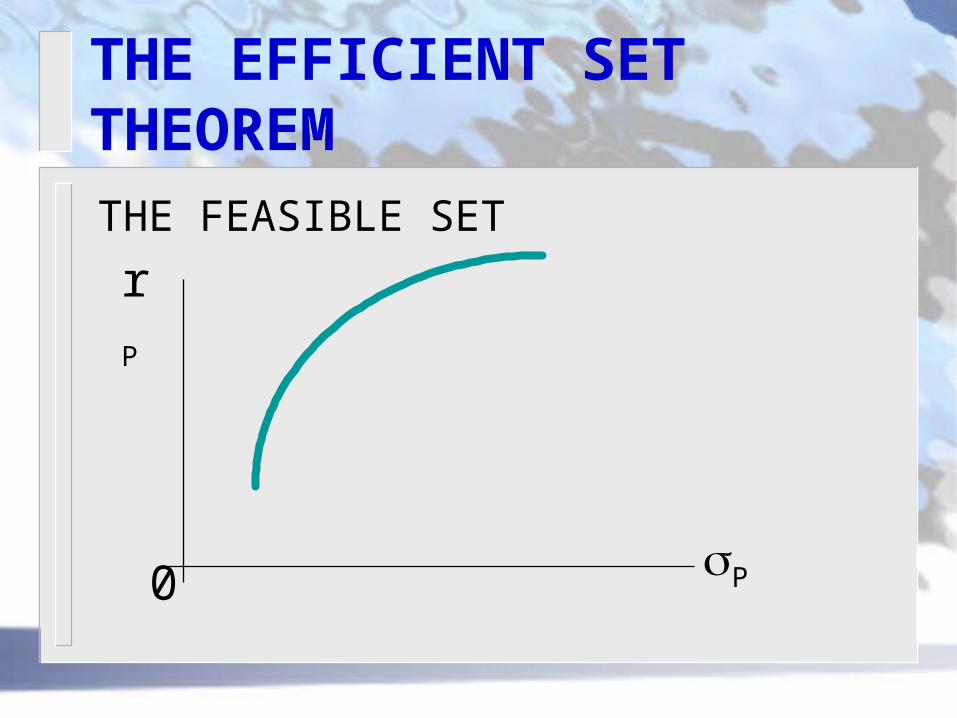

THE EFFICIENT SET THEOREM THE FEASIBLE SET

•DEFINITION: represents all portfolios that could be formed from a group of N securities

THE EFFICIENT SET THEOREMTHE FEASIBLE SET

rP

P0

THE EFFICIENT SET THEOREM EFFICIENT SET THEOREM APPLIED TO

THE FEASIBLE SET•Apply the efficient set theorem to the

feasible setthe set of portfolios that meet first conditions of

efficient set theorem must be identifiedconsider 2nd condition set offering minimum risk

for varying levels of expected return lies on the “western” boundary

remember both conditions: “northwest” set meets the requirements

THE EFFICIENT SET THEOREM THE EFFICIENT SET

•where the investor plots indifference curves and chooses the one that is furthest “northwest”

•the point of tangency at point E

THE EFFICIENT SET THEOREMTHE OPTIMAL PORTFOLIO

E

rP

P0

CONCAVITY OF THE EFFICIENT SET WHY IS THE EFFICIENT SET

CONCAVE?•BOUNDS ON THE LOCATION OF

PORFOLIOS

•EXAMPLE:Consider two securities

– Ark Shipping Company• E(r) = 5% = 20%

– Gold Jewelry Company• E(r) = 15% = 40%

CONCAVITY OF THE EFFICIENT SET

P

rP

A

G

rA = 5

A=20

rG=15

G=40

CONCAVITY OF THE EFFICIENT SET ALL POSSIBLE COMBINATIONS RELIE

ON THE WEIGHTS (X1 , X 2)

X 2 = 1 - X 1

Consider 7 weighting combinations

using the formula

22111

rXrXrXrN

iiiP

CONCAVITY OF THE EFFICIENT SETPortfolio return

A 5B 6.7C 8.3D 10E 11.7F 13.3G 15

CONCAVITY OF THE EFFICIENT SET USING THE FORMULA

we can derive the following:

2/1

1 1

N

i

N

jijjiP XX

CONCAVITY OF THE EFFICIENT SET

rP P=+1 P=-1

A 5 20 20B6.7 10 23.33C8.3 0 26.67D10 10 30.00E 11.7 20 33.33F 13.3 30 36.67G15 40 40.00

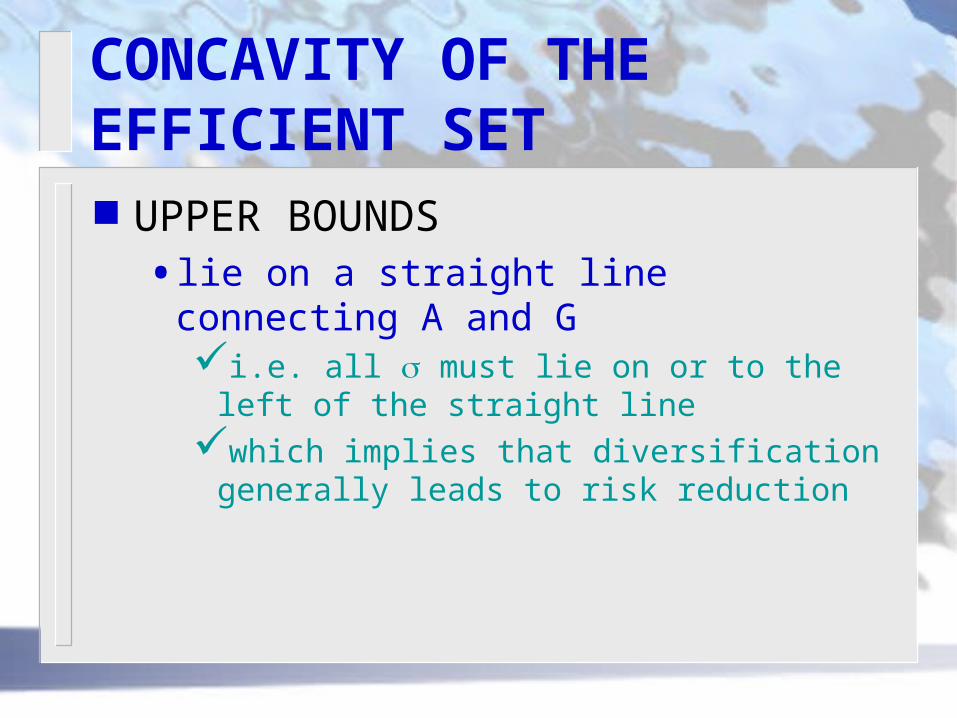

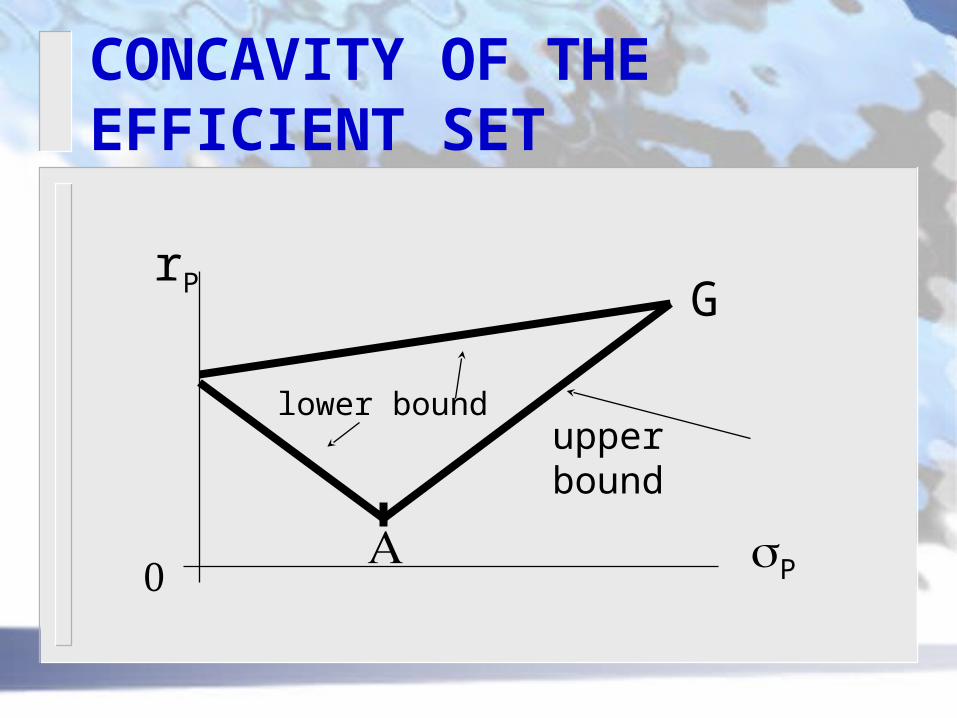

CONCAVITY OF THE EFFICIENT SET UPPER BOUNDS

•lie on a straight line connecting A and Gi.e. all must lie on or to the left of the

straight linewhich implies that diversification

generally leads to risk reduction

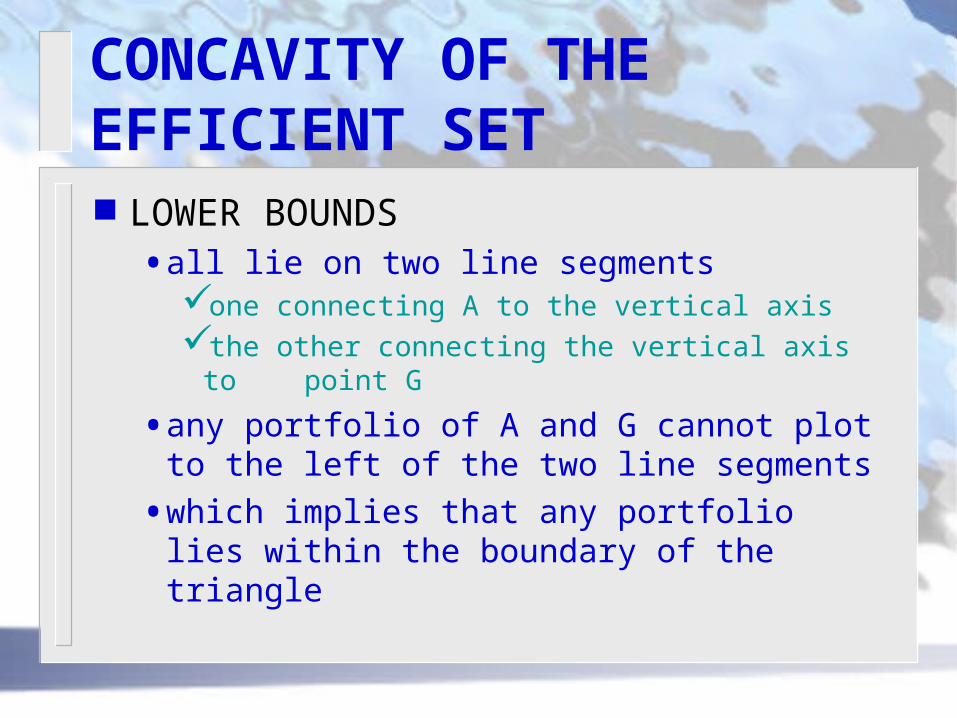

CONCAVITY OF THE EFFICIENT SET LOWER BOUNDS

•all lie on two line segmentsone connecting A to the vertical axisthe other connecting the vertical axis to

point G

•any portfolio of A and G cannot plot to the left of the two line segments

•which implies that any portfolio lies within the boundary of the triangle

CONCAVITY OF THE EFFICIENT SET

G

upper bound

lower bound

rP

P

CONCAVITY OF THE EFFICIENT SET ACTUAL LOCATIONS OF THE

PORTFOLIO•What if correlation coefficient (ij ) is

zero?

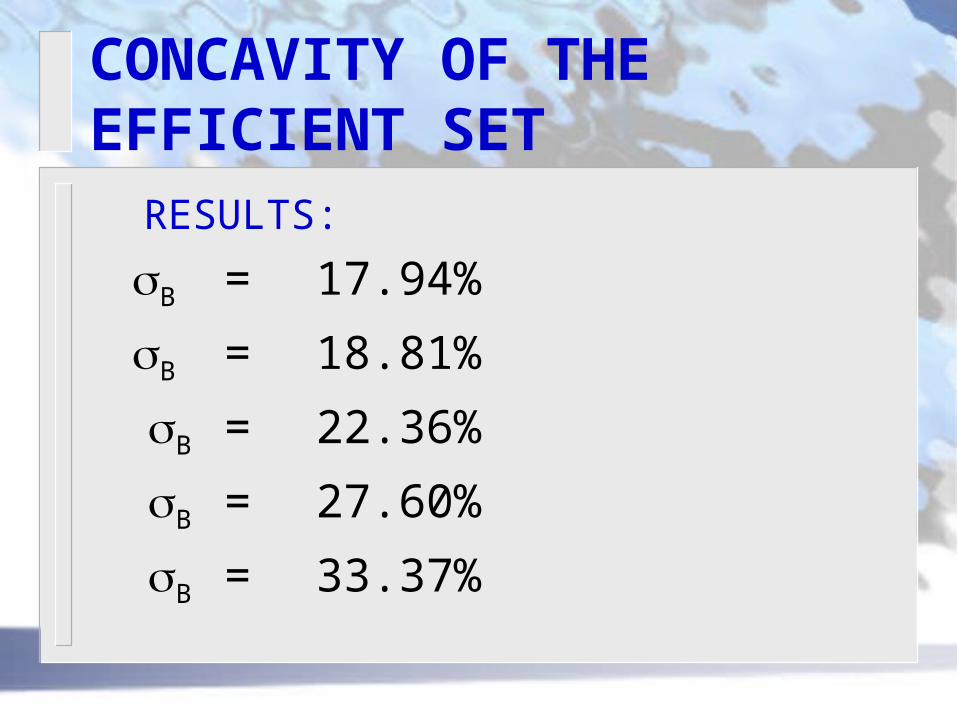

CONCAVITY OF THE EFFICIENT SET

RESULTS:

B = 17.94%

B = 18.81%

B = 22.36%

B = 27.60%

B = 33.37%

CONCAVITY OF THE EFFICIENT SETACTUAL PORTFOLIO LOCATIONS

CD

F

CONCAVITY OF THE EFFICIENT SET IMPLICATION:

•If ij < 0 line curves more to left

•If ij = 0 line curves to left

•If ij > 0 line curves less to left

CONCAVITY OF THE EFFICIENT SET KEY POINT

•As long as -1 < the portfolio line curves to the left and the northwest portion is concave

•i.e. the efficient set is concave

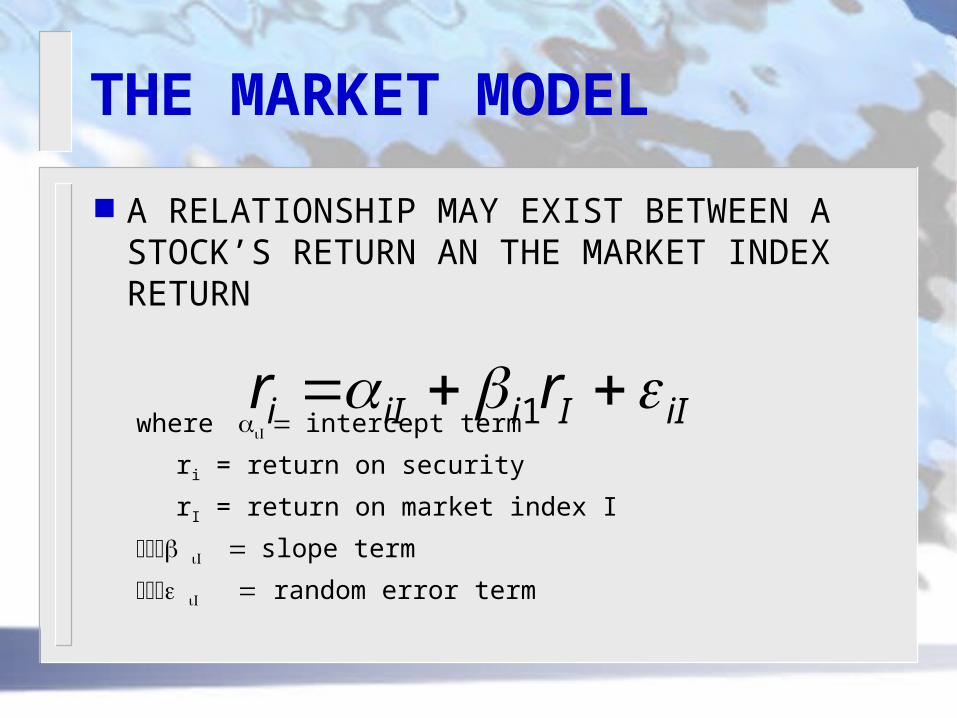

THE MARKET MODEL

A RELATIONSHIP MAY EXIST BETWEEN A STOCK’S RETURN AN THE MARKET INDEX RETURN

where intercept term

ri = return on security

rI = return on market index I

slope term

random error term

iIIiiIi rr 1

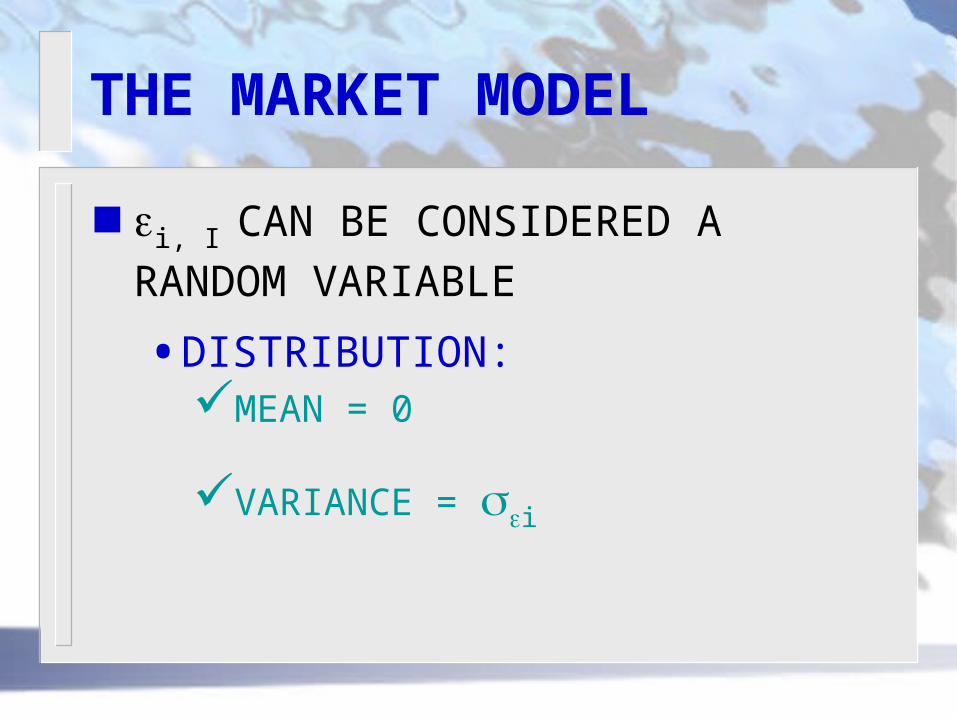

THE MARKET MODEL

THE RANDOM ERROR TERMS i, I

•shows that the market model cannot explain perfectly

•the difference between what the actual return value is and

•what the model expects it to be is attributable to i, I

THE MARKET MODEL

i, I CAN BE CONSIDERED A RANDOM VARIABLE

•DISTRIBUTION:MEAN = 0

VARIANCE = i

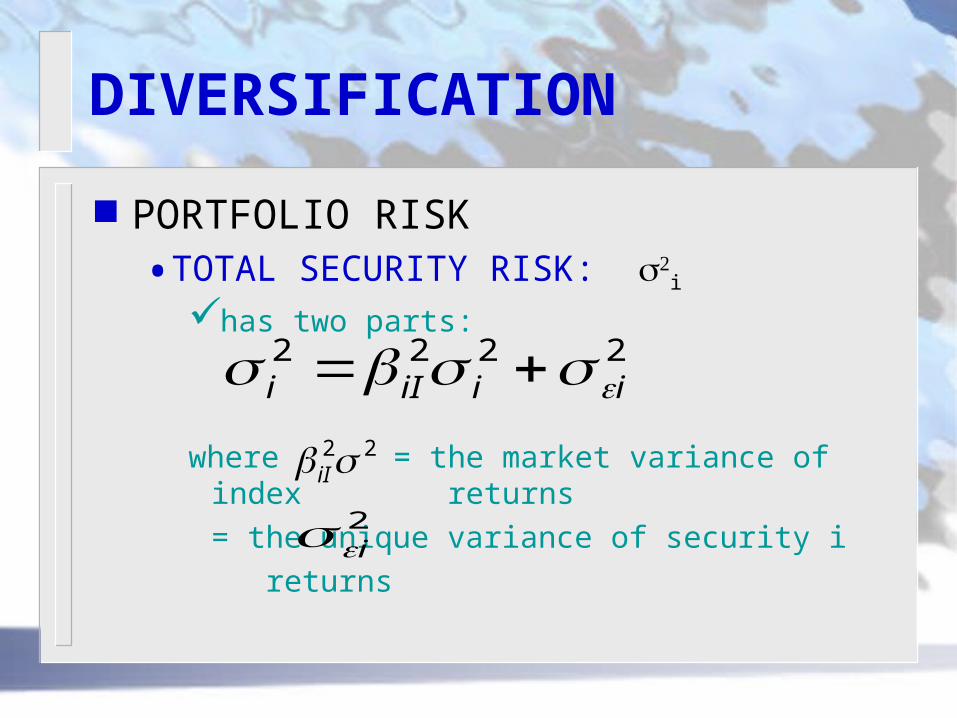

DIVERSIFICATION

PORTFOLIO RISK•TOTAL SECURITY RISK:

i

has two parts:

where = the market variance of index returns

= the unique variance of security i

returns

2222iiiIi

22 iI2i

DIVERSIFICATION

TOTAL PORTFOLIO RISK•also has two parts: market and

uniqueMarket Risk

– diversification leads to an averaging of market risk

Unique Risk– as a portfolio becomes more diversified, the

smaller will be its unique risk

DIVERSIFICATION

Unique Risk– mathematically can be expressed as

N

iiP N1

22

2 1

NNN

222

21 ...1

END OF CHAPTER 7