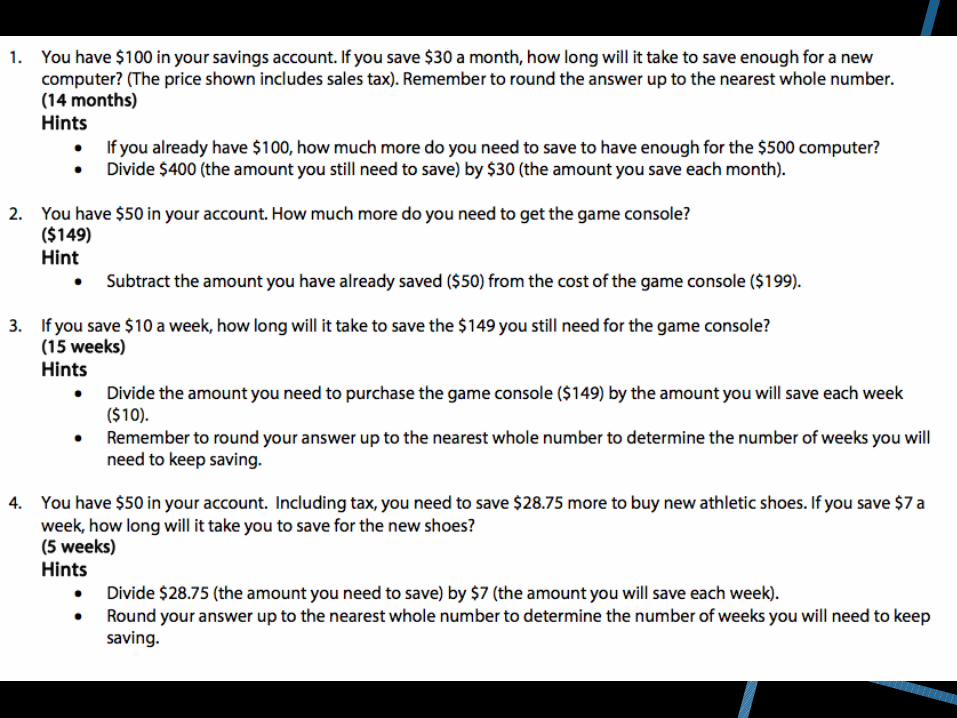

chapters 29 & 30 checking and savings accounts. thinking questions are you saving money for...

TRANSCRIPT

Chapters 29 & 30

Checking and Savings

Accounts

Thin

king

Quest

ions

Are you saving money

for something you want

or need? How do you

keep track of your money?

Savi

ngs

Acc

ounts

Saving: Putting money

aside for the future.Savings accounts:

bank accounts that give

interest for depositing

money in their accounts.

• Banks pay interest because they use that

money to make loans

to other customers.

Types

of

Inte

rest

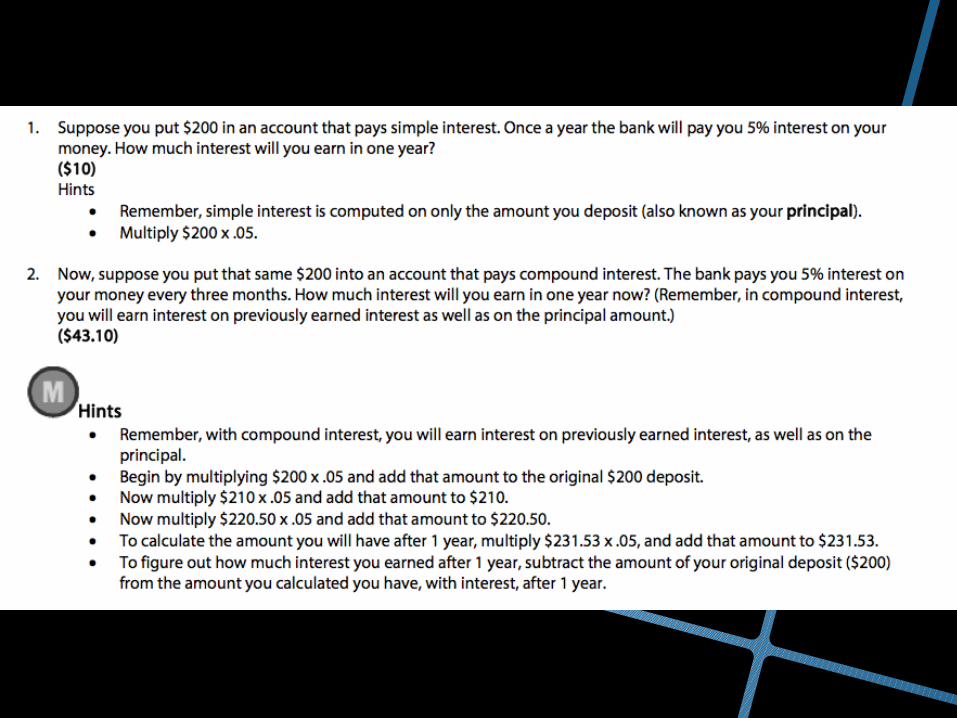

There are two basic kinds

of interest: Simple interest is calculated once in a given

period of time. Compound interest

allows the saver to earn

interest not only on the

amount that was deposited, called the

principal, but also on the

earned interest.

Types

of

savi

ngs

acc

ounts

Regular Savings Account

• Interest is paid monthly.

• The bank may require a minimum deposit. (This

means the amount of money you put into the

account each time.) • There may be limits on the number of deposits

and withdrawals you can make.

• Some banks charge fees.

Certificates of Deposit (CDs)

• Your money must remain in the account for a fixed

period of time, called the term.

• The more money you deposit, and the longer you

keep it in the account, the more interest you’ll

earn. • You’ll have to pay a penalty if you withdraw your

money before the term is completed.

Money Market Account • This type of savings account allows limited

checkwriting. • You may have limited withdrawals each month.

• Generally these accounts pay higher interest

rates than regular savings accounts.

• Interest is calculated at the end of a fixed time

period, for example, every month.

• Interest rate may change.

Deposit S

lips

To put money in your savings

account at the bank, you fill

out a deposit slip. A deposit

slip is a form used to record

the details of the transaction.

Once you’ve filled out the

deposit slip, you give it to the

bank teller, who will take care

of the rest.

With

dra

wal

Slip

s

If you withdraw money at the

bank, you’ll need to fill out a

withdrawal slip and have a

teller watch you sign it. Then

you must show the teller a

photo ID.

Keepin

g

Reco

rds

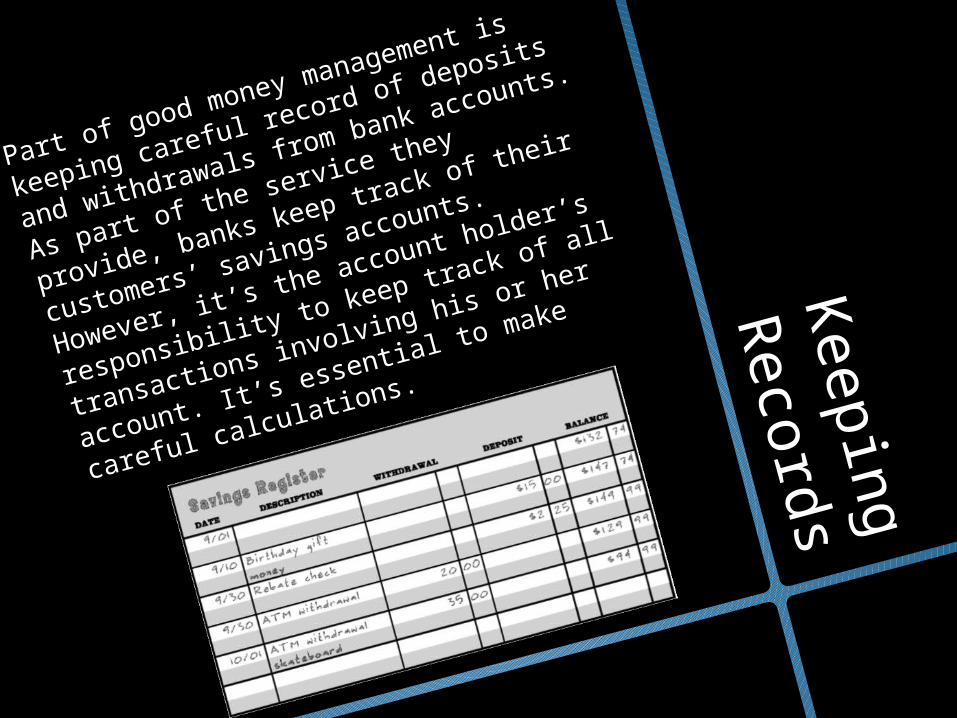

Part of good money management is

keeping careful record of deposits and

withdrawals from bank accounts. As

part of the service they provide,

banks keep track of their customers’

savings accounts. However, it’s the

account holder’s responsibility to keep

track of all transactions involving his

or her account. It’s essential to make

careful calculations.

Chapter 30:

Checking

Check

ing A

ccounts

Dis

cuss

ion Q

uest

ions

Describe other ways

people can pay for things besides paying in

cash.

When people write checks, why do stores

accept them? Isn’t a

check just a piece of

paper?

Check

ing

Acc

ounts

Checking accounts are very

similar to savings accounts. Both

types of accounts keep your

money safe, and both are very

easy to access if you need cash.

Checking accounts are designed

to be day-in and day-out money-

management tools, while

savings accounts are designed

for long-term money-

management. Unlike savings

accounts, banks expect people

to make frequent withdrawals

and deposits to checking

accounts.

Sim

ilari

ties

and

diff

ere

nce

s

An important difference between

checking and savings accounts is

that checking accounts come with

checks! A second important difference is

that most savings accounts earn

interest, while many checking

accounts do not. Checks can be used to make

purchases, just like cash, and they

help people pay bills or make

simple purchases without carrying

around cash or sending it through

the mail. People use checks for

rent, groceries, clothes.

Bad C

heck

s

In order to write a check,

there must be sufficient

funds in the checking

account to cover the

amount. Writing a check when you

know there is not enough

money in the account to

cover it is a violation of the

law. This is called writing a

“bad check.” Individuals

who write “bad checks”

may be fined or otherwise

punished.

Keepin

g R

eco

rds

When you write a check

or make a deposit to

your checking account,

it’s very important that

you immediately record

that transaction in your

check register. That way,

you will keep track of

how much money you

have available in your

account, and avoid writing a “bad check.”

What’

s on a

ch

eck

?