checklist for review of audits of hud engagements (ending ... · pdf file7 fha-approved...

TRANSCRIPT

00-8 JAN 2014 Checklist for Review of Audits of HUD Engagements (Ending on or After December 15, 2012) 22,081

AICPA Peer Review Program Manual PRP §22,080

Section 22,080 Supplemental Checklist for Review of Audits of For-Profit Housing and Urban Development Engagements (For Financial Statements With Periods Ending on or After December 15, 2012)

Engagement No.:

Instructions for Use of the Supplemental Checklist for Review of Audits of Housing and Urban Development Engagements

Notice to Readers A separate section of the manual has been set aside for supplemental engagement checklists relating to reviews of audit engagements of entities subject to Government Accountability Office Government Auditing Standards. The checklist section numbers and titles are as follows:

Section Title

22,110 Supplemental Checklist for Review of Audit Engagements Performed in Accordance With Government Auditing Standards (Yellow Book) 2011 Revision

22,120 Supplemental Checklist for Review of Agreed Upon Procedures and Other Attestation Engagements Performed in Accordance With Government Auditing Standards (Yellow Book) 2011 Revision

Review of all for-profit U.S. Department of Housing and Urban Development audit engagements will require use of one or more of these peer review engagement checklists.

Overview and Instructions

This supplemental checklist was developed for use by reviewers of the U.S. Department of Housing and Urban Development (HUD) for-profit engagements. (It should not be used for review of not-for-profit entities or state and local government audit engagements.) It should be used in conjunction with the General Audit Engagement Checklist (PRP sec. 20,400) (audit checklist); the Financial Reporting and Disclosure Checklist (PRP sec. 22,300); the Supplemental Checklist for Review of Audit Engagements Performed in Accordance With Government Auditing Standards (Yellow Book) 2011 Revision (PRP sec. 22,110); and other guidance materials issued to implement the peer review program. Questions regarding these instructions or any other materials should be directed to the AICPA Peer Review at 919.402.4502.

This checklist is not intended to be an all-inclusive document containing all disclosures and audit procedures related to HUD programs. It is a summarization of commonly addressed key areas and related concepts or procedures. Therefore, it should be used in conjunction with various reference materials dealing with reporting, disclosure, and audit procedure issues in order to sufficiently evaluate HUD engagements. These additional materials include the Consolidated Audit Guide for Audits of HUD Programs IG 2000.04 REV-2 CHG-1 as amended by changes 217 (the HUD audit guide).

22,082 Engagement Checklist Supplements—System Reviews 00-8 JAN 2014

PRP §22,080 Copyright © 2014, American Institute of Certified Public Accountants, Inc.

Important Note to Reviewers Regarding Revisions to the HUD Audit Guide (www.hudoig.gov/reports-publications/audit-guides/consolidated-audit-guides) and the Effect on This Checklist (see the table on page 22,083 for the status of chapter updates as of the date of this checklist). At the time of the development of this checklist, HUD is in the process of updating the HUD audit guide on a chapter-by-chapter basis with various effective dates. Ultimately, when all chapters have been revised, the entire guide will be issued in its entirety. This approach by HUD has made it difficult to update this checklist. The status of each chapter is included in the following table, along with the related effective dates. In reviewing chapters that have been updated by HUD, reviewers should use this checklist in conjunction with the updated chapter from the HUD audit guide with consideration of the effective dates. Upon completion of the HUD audit guide overhaul, this checklist will be revised to be consistent with the guide.

Revisions to chapters 1, 2, 6, and 7 have been released since the prior version of this checklist. The following is an overview of the changes to those chapters:

Chapter 1, “General Audit Guidance,” applies to all entities required to undergo an audit under the HUD audit guide and is effective for audits of entities with year ends ending on or after June 30, 2013. The chapter revisions clarify the use and applicability of the HUD audit guide.

Chapter 2, “Reporting Requirements and Sample Reports,” includes revisions that were made to align the HUD guidance with the Government Auditing Standards—December 2011 Revision issued by the U.S. Government Accountability Office and generally accepted auditing standards issued by the AICPA. A significant change in the guidance is the elimination of separate reporting on compliance with respect to nonmajor HUD programs. The updated reports were released in March 2013.

Chapter 6, “Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance,” was revised in October 2011 to reflect changes to net worth, capital, and liquidity requirements and to provide new reporting formats to conform to the updated Ginnie Mae MBS Guide. The guidance was effective upon issuance with additional changes issued in April 2013.

Chapter 7, “FHA-Approved Lenders Audit Guidance,” was updated in December 2012 for guidance relating to institutions that participate in the Federal Housing Administration (FHA) insurance programs for Title I property improvement and manufactured housing loans and for Title II single family and multifamily mortgages. This revised chapter merged the content of the previous chapter 8 with chapter 7 and eliminated chapter 8 from the HUD audit guide. The requirements in chapter 7 apply to audits of profit-motivated FHA-approved lenders with fiscal years ending on or after December 31, 2012.

For detailed discussion regarding the recent revisions, refer to the Transmittal Letters for each revised chapter of the HUD audit guide or refer to the current news section of the GAQC HUD Resources webpage at www.aicpa.org/ InterestAreas/GovernmentalAuditQuality/Resources/HUDInformation/Pages/HUDInformationNews.aspx. Also refer to the HUD Real Estate Assessment Center website at http://portal.hud.gov/hudportal/HUD?src=/program_offices/ public_indian_housing/reac and the HUD Office of Inspector General website at www.hudoig.gov for the latest information about any new HUD financial reporting requirements.

The questions in this checklist emphasize reporting matters and general procedures ordinarily performed by an independent auditor in the audit of financial statements of HUD programs. All “no” answers must be thoroughly explained in the section provided in the applicable audit checklist.

For any questions related to the updated chapters, reviewers should answer “N/A” if the engagement year end was prior to the effective date of that chapter.

Note: This checklist has been updated through Statement on Auditing Standards No. 127, Omnibus Statement on Auditing Standards2013 (AICPA, Professional Standards), and AU-C section 935, Compliance Audits (AICPA, Professional Standards).

00-8 JAN 2014 Checklist for Review of Audits of HUD Engagements (Ending on or After December 15, 2012) 22,083

AICPA Peer Review Program Manual PRP §22,080

Chapter Description Updated Audit Period

Effective

1 Transmittal Letter 5/2013 Periods Ending on or After

June 30, 2013

1 General Audit Guidance 5/2013 Periods Ending on or After

June 30, 2013

2 Reporting Requirement and Sample Reports 3/2013 Periods Ending on or After

March 31, 2013

2 Transmittal Letter 3/2013 Periods Ending on or After

March 31, 2013

3 Transmittal Letter 7/21/2008 12/31/2008

3 HUD Multifamily Housing Programs 7/2008 12/31/2008

4 HUD Multifamily Hospital Program 7/2008* Upon Issuance

5 Transmittal Letter 3/23/2007 6/30/2007

5 Insured Development Cost Certification Audit Guidance 3/23/2007 6/30/2007

6 Transmittal Letter 5/2012 Upon Issuance

6 Transmittal Letter for REV-2, CHG-13 4/2013 Upon Issuance

6 Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance 5/2012 and

4/2013

Upon Issuance

7 Transmittal Letter 12/2012 Upon Issuance

7 FHA-Approved Lenders Audit Guidance 12/2012 Upon Issuance

Appendix HUD Regional Inspector Generals for Audit 3/2007 3/2007

*Chapter in process of being updated by HUD but not issued as of the date of this checklist.

Note to Reviewer: The AICPA established the Governmental Audit Quality Center (GAQC) (http://gaqc.aicpa.org) as a voluntary firm membership to enhance quality of audits performed under Government Auditing Standards (also referred to as the Yellow Book or governmental audits), including HUD engagements. GAQC firm members have agreed, as a condition of membership, to have employees of a GAQC member firm review the governmental engagements selected for its peer review. To avoid misunderstandings, it is advisable that team captains ensure that they include a GAQC firm member. This requirement can be met with a team captain or team member whose firm is a member of the GAQC.

22,084 Engagement Checklist Supplements—System Reviews 00-8 JAN 2014

PRP §22,080 Copyright © 2014, American Institute of Certified Public Accountants, Inc.

Contents

Section Page I. Report and Financial Statements (Supplement to section IV of the applicable General Audit Engagement Checklist) General ............................................................................................................................................. 22,085 Program Specific Requirements ....................................................................................................... 22,086 A. Chapter 3, “HUD Multifamily Housing Programs—Reporting Requirements” ....................... 22,086 B. Chapter 4, “HUD Multifamily Hospital Program—Reporting Requirements” ......................... 22,087 C. Chapter 5, “Insured Development Cost Certification Audit Guidance—Reporting Requirements” ....................................................................................................................... 22,088 D. Chapter 6, “Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance—Reporting Requirements”................................................................................... 22,088 E. Chapter 7, “FHA-Approved Lenders Audit Guidance” ............................................................ 22,089

II. Working Paper Areas—Housing and Urban Development Engagements (Supplement to section II of the applicable General Audit Engagement Checklist) General ............................................................................................................................................. 22,090 Specific Program Requirements ....................................................................................................... 22,090-1 A. Chapter 3, “HUD Multifamily Housing Programs” .................................................................. 22,090-2 B. Chapter 4, “HUD Multifamily Hospital Program” ................................................................... 22,090-3 C. Chapter 5, “Insured Development Cost Certification Audit Guidance” ................................... 22,090-3 D. Chapter 6, “Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance” .................. 22,090-4 E. Chapter 7, “FHA-Approved Lenders Audit Guidance” ............................................................ 22,090-4

Explanation of References:

AU-C Reference to section number for clarified Statements on Auditing Standards in AICPA Professional Standards

GAS Government Auditing StandardsDecember 2011 Revision, United States General Accounting Office (Yellow Book)

HUD Consolidated Audit Guide for Audits of HUD Programs, Handbook IG 200004 REV-2 CHG-1, December 2001, as amended by changes 2 through 17

AAG-SLA AICPA Audit Guide Government Auditing Standards and OMG Circular A-133 Audits, as of February 1, 2013

00-8 JAN 2014 Checklist for Review of Audits of HUD Engagements (Ending on or After December 15, 2012) 22,085

AICPA Peer Review Program Manual PRP §22,080

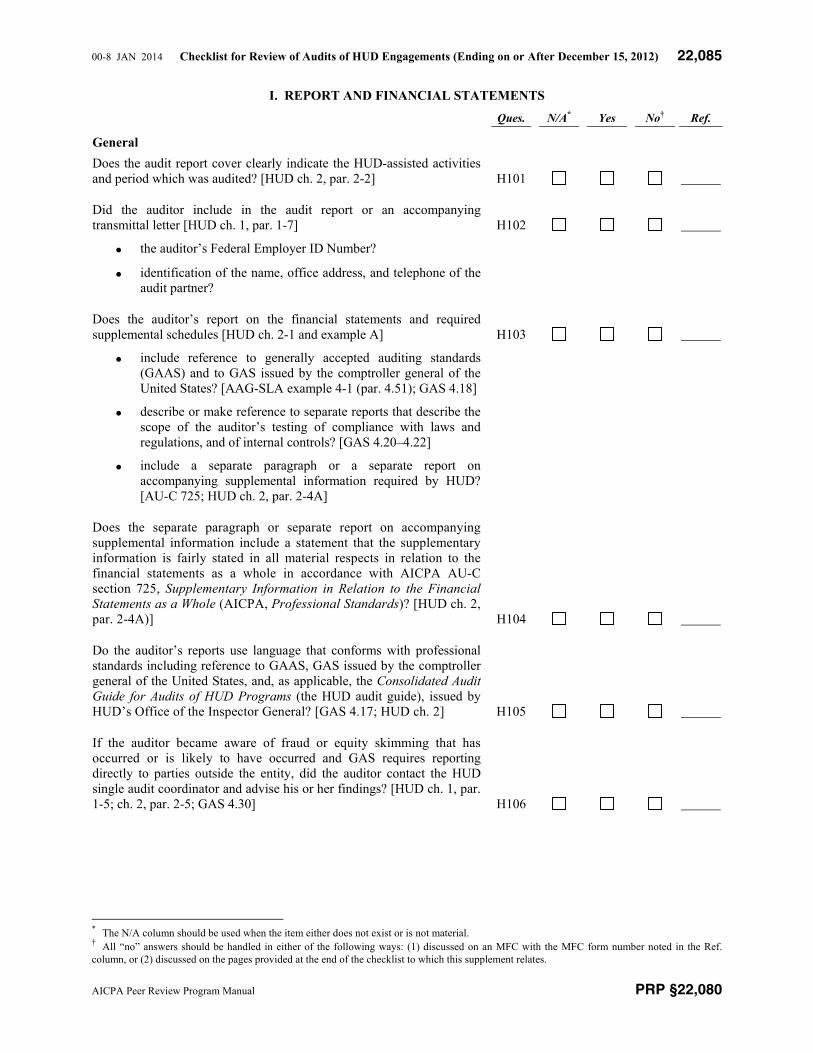

I. REPORT AND FINANCIAL STATEMENTS

Ques. N/A* Yes No† Ref.

General

Does the audit report cover clearly indicate the HUD-assisted activities and period which was audited? [HUD ch. 2, par. 2-2] H101

Did the auditor include in the audit report or an accompanying transmittal letter [HUD ch. 1, par. 1-7] H102

the auditor’s Federal Employer ID Number?

identification of the name, office address, and telephone of the audit partner?

Does the auditor’s report on the financial statements and required supplemental schedules [HUD ch. 2-1 and example A] H103

include reference to generally accepted auditing standards (GAAS) and to GAS issued by the comptroller general of the United States? [AAG-SLA example 4-1 (par. 4.51); GAS 4.18]

describe or make reference to separate reports that describe the scope of the auditor’s testing of compliance with laws and regulations, and of internal controls? [GAS 4.20–4.22]

include a separate paragraph or a separate report on accompanying supplemental information required by HUD? [AU-C 725; HUD ch. 2, par. 2-4A]

Does the separate paragraph or separate report on accompanying supplemental information include a statement that the supplementary information is fairly stated in all material respects in relation to thefinancial statements as a whole in accordance with AICPA AU-C section 725, Supplementary Information in Relation to the Financial Statements as a Whole (AICPA, Professional Standards)? [HUD ch. 2,par. 2-4A)] H104

Do the auditor’s reports use language that conforms with professional standards including reference to GAAS, GAS issued by the comptroller general of the United States, and, as applicable, the Consolidated Audit Guide for Audits of HUD Programs (the HUD audit guide), issued by HUD’s Office of the Inspector General? [GAS 4.17; HUD ch. 2] H105

If the auditor became aware of fraud or equity skimming that has occurred or is likely to have occurred and GAS requires reporting directly to parties outside the entity, did the auditor contact the HUD single audit coordinator and advise his or her findings? [HUD ch. 1, par. 1-5; ch. 2, par. 2-5; GAS 4.30] H106

* The N/A column should be used when the item either does not exist or is not material. † All “no” answers should be handled in either of the following ways: (1) discussed on an MFC with the MFC form number noted in the Ref. column, or (2) discussed on the pages provided at the end of the checklist to which this supplement relates.

22,086 Engagement Checklist Supplements—System Reviews 00-8 JAN 2014

PRP §22,080 Copyright © 2014, American Institute of Certified Public Accountants, Inc.

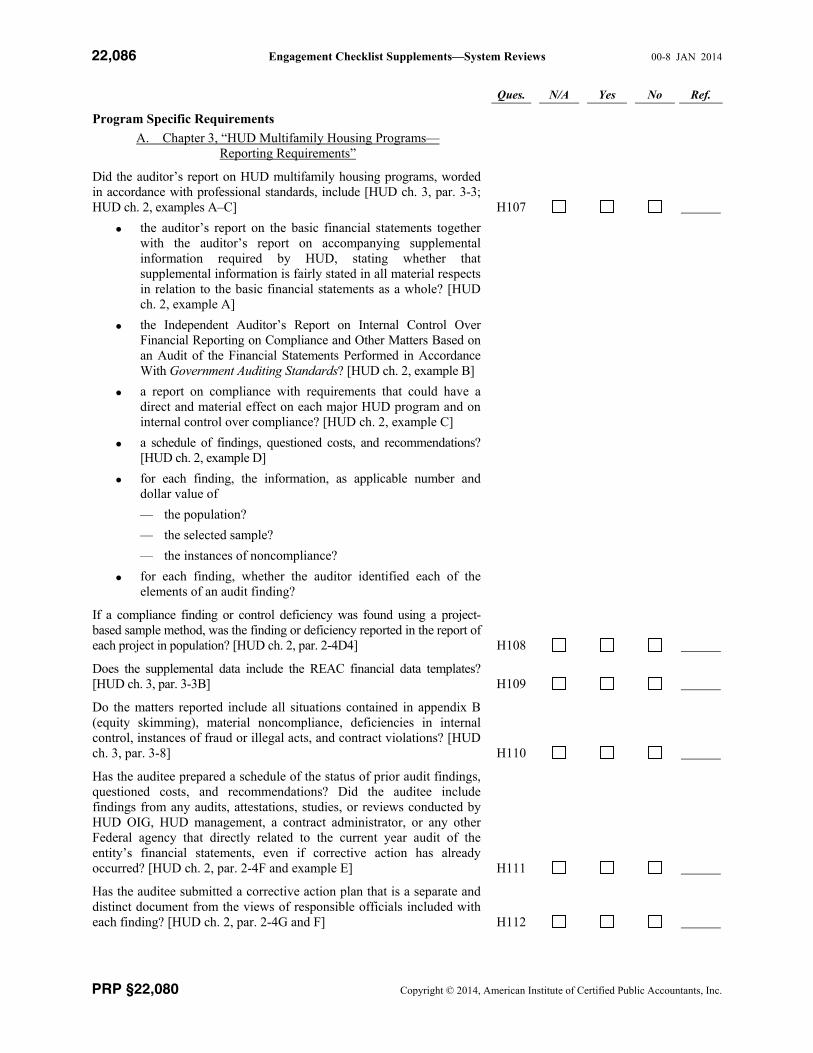

Ques. N/A Yes No Ref.

Program Specific Requirements

A. Chapter 3, “HUD Multifamily Housing Programs— Reporting Requirements”

Did the auditor’s report on HUD multifamily housing programs, wordedin accordance with professional standards, include [HUD ch. 3, par. 3-3; HUD ch. 2, examples A–C] H107

the auditor’s report on the basic financial statements together with the auditor’s report on accompanying supplemental information required by HUD, stating whether that supplemental information is fairly stated in all material respects in relation to the basic financial statements as a whole? [HUD ch. 2, example A]

the Independent Auditor’s Report on Internal Control Over Financial Reporting on Compliance and Other Matters Based on an Audit of the Financial Statements Performed in Accordance With Government Auditing Standards? [HUD ch. 2, example B]

a report on compliance with requirements that could have a direct and material effect on each major HUD program and on internal control over compliance? [HUD ch. 2, example C]

a schedule of findings, questioned costs, and recommendations? [HUD ch. 2, example D]

for each finding, the information, as applicable number and dollar value of

— the population?

— the selected sample?

— the instances of noncompliance?

for each finding, whether the auditor identified each of the elements of an audit finding?

If a compliance finding or control deficiency was found using a project-based sample method, was the finding or deficiency reported in the report of each project in population? [HUD ch. 2, par. 2-4D4] H108

Does the supplemental data include the REAC financial data templates?[HUD ch. 3, par. 3-3B] H109

Do the matters reported include all situations contained in appendix B (equity skimming), material noncompliance, deficiencies in internal control, instances of fraud or illegal acts, and contract violations? [HUD ch. 3, par. 3-8] H110

Has the auditee prepared a schedule of the status of prior audit findings, questioned costs, and recommendations? Did the auditee include findings from any audits, attestations, studies, or reviews conducted by HUD OIG, HUD management, a contract administrator, or any other Federal agency that directly related to the current year audit of the entity’s financial statements, even if corrective action has already occurred? [HUD ch. 2, par. 2-4F and example E] H111

Has the auditee submitted a corrective action plan that is a separate and distinct document from the views of responsible officials included with each finding? [HUD ch. 2, par. 2-4G and F]

H112

00-8 JAN 2014 Checklist for Review of Audits of HUD Engagements (Ending on or After December 15, 2012) 22,087

AICPA Peer Review Program Manual PRP §22,080

Ques. N/A Yes No Ref.

Has the auditor followed up on prior audit findings reported by the auditee, performed procedures to assess the reasonableness of the schedule, and reported as a current year finding when the auditor concludes that the schedule materially misrepresents the status of any prior audit finding? [HUD ch. 2, par. 2-4F] H113

Has the auditor compared the data prepared for electronic submission in the multifamily financial assessment subsystem to the hard copy annual audited financial statements and issued an agreed-upon procedures report on the results thereof? [HUD ch. 1, par. 1-5A5; ch. 3, par. 3-3C] H114

B. Chapter 4, “HUD Multifamily Hospital Program— Reporting Requirements”

Did the auditor’s report on HUD multifamily hospital program, worded in accordance with professional standards, include [HUD ch. 4, par. 2; HUD ch. 2, examples A–C] H115

the auditor’s report on the ownership entity’s financial statements together with the auditor’s report on accompanying supplemental information required by HUD, stating whether that supplemental information is fairly stated in all material respects in relation to the financial statements as a whole?

the Independent Auditor’s Report on Internal Control Over Financial Reporting on Compliance and Other Matters Based on an Audit of the Financial Statements Performed in Accordance With Government Auditing Standards? [HUD ch. 2, example B]

a report on compliance with requirements that could have a direct and material effect on each major HUD program and on internal control over compliance? [HUD ch. 2, example C]

the schedule of findings and questioned costs, if applicable?

for each finding, the information, as applicable number and dollar value of

— the population?

— the selected sample?

— the instances of noncompliance?

Do the matters reported include material noncompliance, deficiencies in internal control, instances of fraud or illegal acts, and contract violations? [HUD ch. 4, par. 4-4] H116

Has the auditee prepared a schedule of the status of prior audit findings, questioned costs, and recommendations? Did the auditee include findings from any audits, attestations, studies, or reviews conducted by HUD OIG, HUD management, a contract administrator, or any other Federal agency that directly related to the current year audit of the entity’s financial statements, even if corrective action has already occurred? [HUD ch. 2, par. 2-4F and example E]

H117

Has the auditee submitted a corrective action plan that is a separate and distinct document from the views of responsible officials included with each finding? [HUD ch.. 2, par. 2-4G]

H118

22,088 Engagement Checklist Supplements—System Reviews 00-8 JAN 2014

PRP §22,080 Copyright © 2014, American Institute of Certified Public Accountants, Inc.

Ques. N/A Yes No Ref.

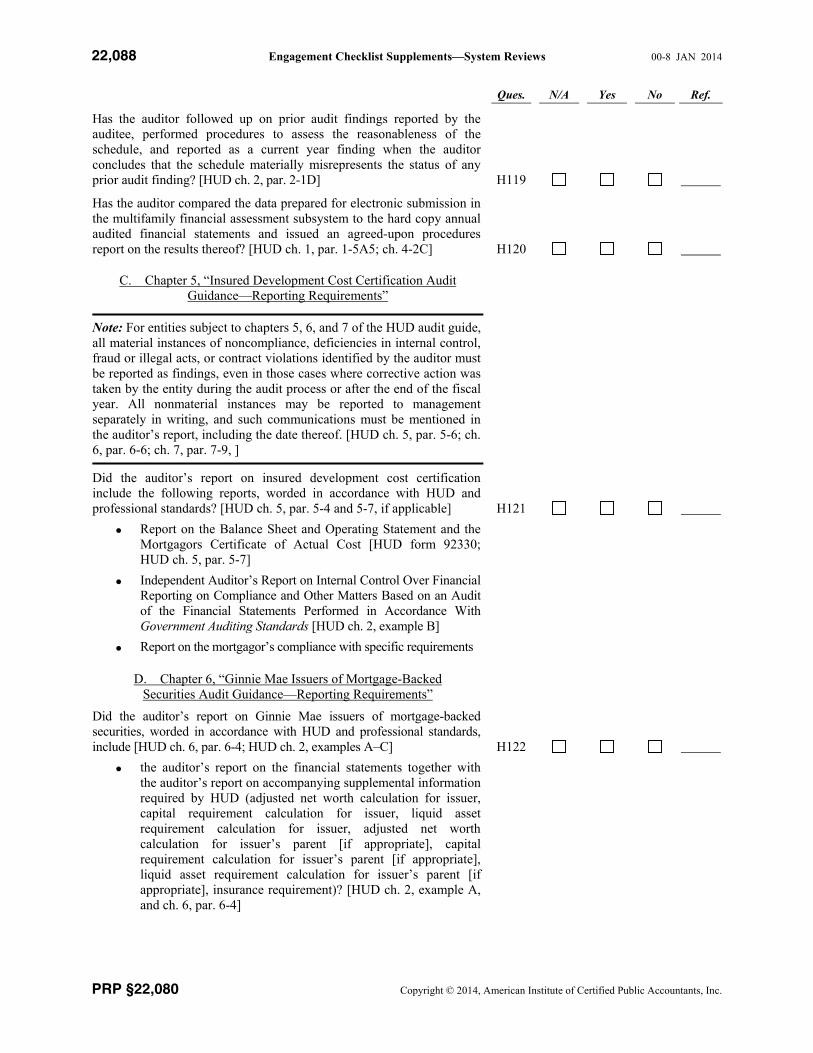

Has the auditor followed up on prior audit findings reported by the auditee, performed procedures to assess the reasonableness of the schedule, and reported as a current year finding when the auditor concludes that the schedule materially misrepresents the status of any prior audit finding? [HUD ch. 2, par. 2-1D] H119

Has the auditor compared the data prepared for electronic submission in the multifamily financial assessment subsystem to the hard copy annual audited financial statements and issued an agreed-upon procedures report on the results thereof? [HUD ch. 1, par. 1-5A5; ch. 4-2C] H120

C. Chapter 5, “Insured Development Cost Certification Audit Guidance—Reporting Requirements”

Note: For entities subject to chapters 5, 6, and 7 of the HUD audit guide, all material instances of noncompliance, deficiencies in internal control, fraud or illegal acts, or contract violations identified by the auditor must be reported as findings, even in those cases where corrective action was taken by the entity during the audit process or after the end of the fiscal year. All nonmaterial instances may be reported to management separately in writing, and such communications must be mentioned in the auditor’s report, including the date thereof. [HUD ch. 5, par. 5-6; ch. 6, par. 6-6; ch. 7, par. 7-9, ]

Did the auditor’s report on insured development cost certification include the following reports, worded in accordance with HUD and professional standards? [HUD ch. 5, par. 5-4 and 5-7, if applicable] H121

Report on the Balance Sheet and Operating Statement and the Mortgagors Certificate of Actual Cost [HUD form 92330;HUD ch. 5, par. 5-7]

Independent Auditor’s Report on Internal Control Over Financial Reporting on Compliance and Other Matters Based on an Audit of the Financial Statements Performed in Accordance With Government Auditing Standards [HUD ch. 2, example B]

Report on the mortgagor’s compliance with specific requirements

D. Chapter 6, “Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance—Reporting Requirements”

Did the auditor’s report on Ginnie Mae issuers of mortgage-backed securities, worded in accordance with HUD and professional standards, include [HUD ch. 6, par. 6-4; HUD ch. 2, examples A–C] H122

the auditor’s report on the financial statements together with the auditor’s report on accompanying supplemental information required by HUD (adjusted net worth calculation for issuer, capital requirement calculation for issuer, liquid asset requirement calculation for issuer, adjusted net worth calculation for issuer’s parent [if appropriate], capital requirement calculation for issuer’s parent [if appropriate], liquid asset requirement calculation for issuer’s parent [if appropriate], insurance requirement)? [HUD ch. 2, example A,and ch. 6, par. 6-4]

00-8 JAN 2014 Checklist for Review of Audits of HUD Engagements (Ending on or After December 15, 2012) 22,089

AICPA Peer Review Program Manual PRP §22,080

Ques. N/A Yes No Ref.

the Independent Auditor’s Report on Internal Control Over Financial Reporting on Compliance and Other Matters Based on an Audit of the Financial Statements Performed in Accordance With Government Auditing Standards? [HUD ch. 2, example B]

a report on compliance with requirements that could have a direct and material effect on each major HUD program and on internal control over compliance? [HUD ch. 2, example C]?

E. Chapter 7, “FHA-Approved Lenders Audit Guidance”

Note: Mortgagee Letter 2011-05. This mortgagee letter, titled Revised Audited Financial Statement Reporting Requirements for Supervised Lenders in Parent-Subsidiary Structures and New Financial ReportingRequirements for Multifamily Mortgagees (ML 2011-05), was issued on January 5, 2011, and is effective immediately. It clarifies that supervised mortgagees should be following all other requirements in the HUD audit guide for nonsupervised mortgagees (primarily found in chapter 7 of that guide) except for those modified in ML 2011-05. Note: Loan Correspondent Audits No Longer Required. On April 20, 2010, HUD issued a final rule that eliminated the audit requirement for loan correspondents (previously, loan correspondents were required to have a financial statement audit and a compliance audit under the HUD Consolidated Audit Guide).

Did the auditor’s report on supervised and nonsupervised lenders, worded in accordance with professional standards, include [HUD ch. 7,par. 7-3] H123

an appropriate level of financial statements and audited consolidating schedules depending on the parent or subsidiary structure (see chart HUD ch. 7, par. 7-3)? Note: Except for governmental (subject to A133) and small supervised lenders, all FHA-approved lenders are required to have an annual audit in accordance with this guide regardless of the number of loans originated or serviced. [HUD ch. 7, par. 7-3]

the auditor’s report on the financial statements together with the auditor’s report on accompanying supplemental information required by HUD? [HUD ch. 2, example A]

the auditor’s report that covers the lender’s computation of the adjusted net worth, the hardcopy of the electronic submission, and, if applicable, consolidating schedules as supplementary information in relation to the financial statements as a whole?[HUD ch. 7, par. 7-3A]

the Independent Auditor’s Report on Internal Control Over Financial Reporting on Compliance and Other Matters Based on an Audit of the Financial Statements Performed in Accordance With Government Auditing Standards? [HUD ch. 2, example B]

a report on compliance with requirements that could have a direct and material effect on each major HUD program and on internal control over compliance? [HUD ch. 2, example C]

an agreed-upon procedures report on the electronic submission (LASS Templates) in accordance with AICPA Statements on Standards for Attestation Engagements? [HUD ch. 7, par. 7-4A]

22,090 Engagement Checklist Supplements—System Reviews 00-8 JAN 2014

PRP §22,080 Copyright © 2014, American Institute of Certified Public Accountants, Inc.

II. WORKING PAPER AREAS—HOUSING AND URBAN DEVELOPMENT ENGAGEMENTS

Note: The instructions to section III of the applicable audit checklist should be used when completing this section of the supplement.

Ques. N/A* Yes No† Ref.

General

Does the engagement letter required by HUD specify H201

that the audit was to be performed in accordance with GAAS, GAS, and the consolidated audit guide for audits of HUD programs? [HUD ch. 1, par. 1-5]

the estimated date that the audit report will be delivered to the auditee? [HUD ch. 1, par. 1-5]

that the secretary of HUD, the HUD Inspector General, and GAO or their representatives have access to the working papers(hardcopy or electronic) and, upon request, photocopies or electronic access will be provided to them? [HUD ch. 1, par. 1-7]

that if the auditor becomes aware of noncompliance with provisions of laws, regulations, contracts, and grant agreementsor fraud that has occurred or is likely to occur, the auditor is required to bring such acts to the attention of the appropriate level of management? In addition, as required in chapter 2, of this audit guide, the auditor may be required to contact the HUD single audit coordinator to discuss matters related to fraud or equity skimming. Based on that discussion, the auditor may be requested to prepare a written report on all known or likely fraud that has occurred. Acceptance of the engagement letter grants the auditor permission to contact the HUD single audit coordinator and discuss the conditions noted. [HUD ch. 1,par. 1-5]

that if the program being audited requires electronic submission of the financial and compliance data to HUD, the responsibilities of the auditor and the client should be included as follows: [HUD ch. 1, par. 1-5]

— The client is responsible to make the electronic submissionto HUD

— The auditor under a separate agreed-upon procedure engagement is responsible for applying procedures to ensure that the data submitted agree with the auditee’s hardcopies of the supporting documentation.

a description of the scope of the planned audit and contents of

the report as set forth in chapter 2 of the HUD audit guide?[HUD ch. 1, par. 1-5]

permission for the auditor to review the prior auditors audit documentation files (working papers) supporting the prior audit and for the auditor to discuss matters with the prior auditor that may not be adequately explained or documented in the audit documentation or any preexisting condition the auditor notes in his or her review that was not in the prior audit report? [HUD ch. 1, par. 1-5]

* The N/A column should be used when the item either does not exist or is not material. † All “no” answers should be handled in either of the following ways: (1) discussed on an MFC with the MFC form number noted in the Ref. column, or (2) discussed on the pages provided at the end of the checklist to which this supplement relates.

00-8 JAN 2014 Checklist for Review of Audits of HUD Engagements (Ending on or After December 15, 2012) 22,090-1

AICPA Peer Review Program Manual PRP §22,080

Ques. N/A Yes No Ref.

a list of the information the auditor wants the auditee to provide for the audit and the requested delivery date of those items? [HUD ch. 1, par. 1-5]

that the auditor provided his or her most recent external peer review report to the audit client when requested? [GAS 3.106]

For HUD-insured and multifamily projects, did the auditor consider whether the firm’s independence was impaired by performing bookkeeping services? [HUD Handbook 4370.2 par. 3-1] H202

Did the auditor obtain a representation letter from management that includes matters concerning compliance with program laws and regulations that have a material effect on the financial statements, each HUD-assisted program, and all compliance violations or issues regardless of their materiality, as well as management’s responsibilities for establishing and maintaining effective control over financial reporting and internal control over compliance? [AU-C 935.23.24; HUD ch. 1, par. 1-5D] H203

Specific Program Requirements

The specific requirements for the following programs are contained in separate chapters of the HUD audit guide:

chapter 3, “HUD Multifamily Housing Programs Audit Guidance”

chapter 4, “HUD Multifamily Hospital Program”

chapter 5, “Insured Development Cost Certification Audit Guidance”

chapter 6, “Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance”

chapter 7, “FHA-Approved Lenders Audit Guidance”

Note: Although use of this guide is mandatory for audits of all for-profit participants, this guide is not intended to be a complete manual of audit procedures for the compliance audit. The audit guide is not intended to cover all situations that may exist or replace the auditor’s judgment of audit work required to meet GAAS or generally accepted government auditing standards. It is meant to supplement those standards with information specific to HUD program audits. Suggested audit procedures contained herein might not cover all circumstances or conditions encountered in a particular audit. The auditor should use professional judgment to tailor the procedures so that the audit objectives are met. However, auditors must address all compliance requirements in this guidethat could have a direct and material effect on a major HUD-assisted program. If the auditor determines that certain procedures for a compliance requirement will not be performed, the rationale for the exclusion must be explained and documented in the audit documentation in support of the auditor’s report. [HUD ch. 1, par. 1-1]

If the auditor decided not to perform detailed testing of a particular compliance requirement, were the reasons therefore appropriately explained and documented in the workpapers? [HUD ch. 1, par. 1-1] H204

22,090-2 Engagement Checklist Supplements—System Reviews 00-8 JAN 2014

PRP §22,080 Copyright © 2014, American Institute of Certified Public Accountants, Inc.

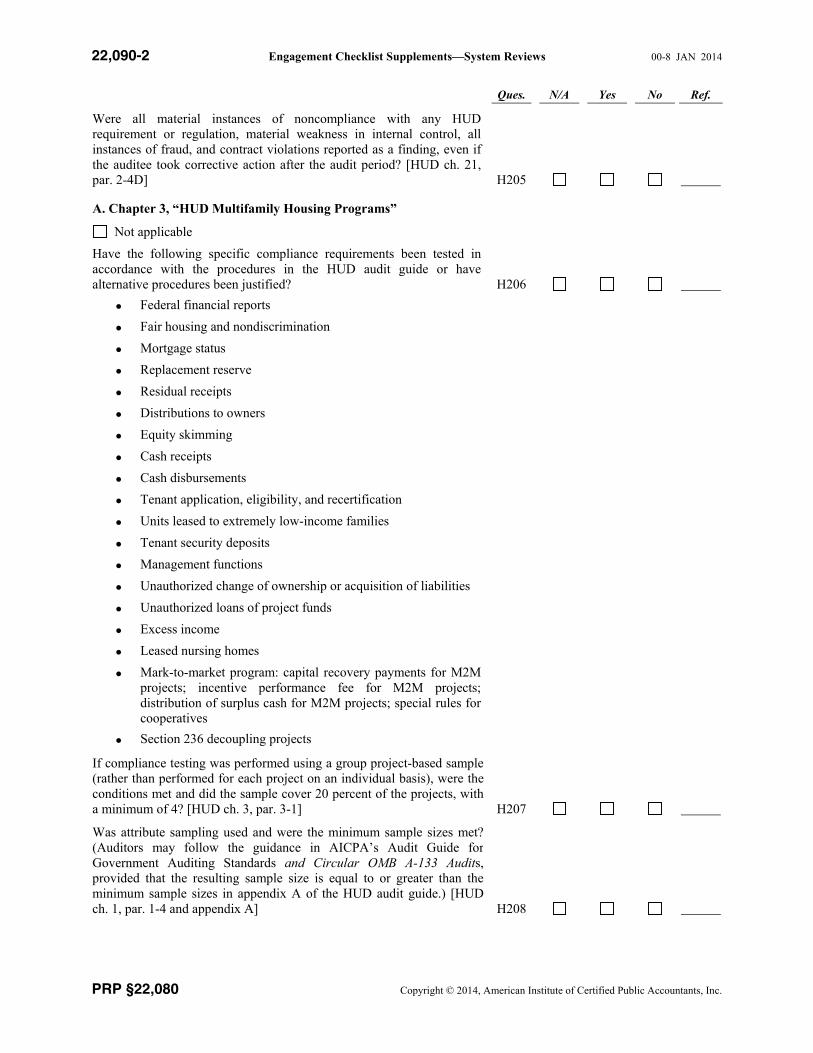

Ques. N/A Yes No Ref.

Were all material instances of noncompliance with any HUD requirement or regulation, material weakness in internal control, all instances of fraud, and contract violations reported as a finding, even if the auditee took corrective action after the audit period? [HUD ch. 21,par. 2-4D] H205

A. Chapter 3, “HUD Multifamily Housing Programs”

Not applicable

Have the following specific compliance requirements been tested in accordance with the procedures in the HUD audit guide or have alternative procedures been justified? H206

Federal financial reports

Fair housing and nondiscrimination

Mortgage status

Replacement reserve

Residual receipts

Distributions to owners

Equity skimming

Cash receipts

Cash disbursements

Tenant application, eligibility, and recertification

Units leased to extremely low-income families

Tenant security deposits

Management functions

Unauthorized change of ownership or acquisition of liabilities

Unauthorized loans of project funds

Excess income

Leased nursing homes

Mark-to-market program: capital recovery payments for M2M projects; incentive performance fee for M2M projects; distribution of surplus cash for M2M projects; special rules for cooperatives

Section 236 decoupling projects

If compliance testing was performed using a group project-based sample (rather than performed for each project on an individual basis), were theconditions met and did the sample cover 20 percent of the projects, witha minimum of 4? [HUD ch. 3, par. 3-1] H207

Was attribute sampling used and were the minimum sample sizes met?(Auditors may follow the guidance in AICPA’s Audit Guide forGovernment Auditing Standards and Circular OMB A-133 Audits,provided that the resulting sample size is equal to or greater than theminimum sample sizes in appendix A of the HUD audit guide.) [HUD ch. 1, par. 1-4 and appendix A] H208

00-8 JAN 2014 Checklist for Review of Audits of HUD Engagements (Ending on or After December 15, 2012) 22,090-3

AICPA Peer Review Program Manual PRP §22,080

Ques. N/A Yes No Ref.

B. Chapter 4, “HUD Multifamily Hospital Program”

Not applicable

Have the following specific compliance requirements been tested in accordance with the procedures in the HUD audit guide or have alternative procedures been justified? H209

Federal financial reports

Fair housing and nondiscrimination

Mortgage status

Replacement reserve

Residual receipts

Distributions to owners

Tenant application, eligibility, and recertification

Management functions

Unauthorized change of ownership or acquisition of liabilities

Unauthorized loans of project funds

Unauthorized transfer of beneficial interest

Electronic submission verification

Excess income

Was attribute sampling used and were the minimum sample sizes met?(Auditors may follow the guidance in AICPA’s Audit Guide for Government Auditing Standards and Circular OMB A-133 Audits,provided that the resulting sample size is equal to or greater than the minimum sample sizes in appendix A of the HUD audit guide.) [HUD ch. 1, par. 1-4 and appendix A] H210

C. Chapter 5, “Insured Development Cost Certification Audit Guidance”

Not applicable

Have the following specific compliance requirements been tested in accordance with the procedures in the HUD audit guide or have alternative procedures been justified? H211

Federal financial reports

Accounting system

Cut-off timing and eligibility of costs

Identity of interest

If applicable, was a contractor certificate of actual cost [Form HUD-92330A] together with an auditor’s opinion thereon (in accordance with Government Auditing Standards), included in the mortgagor’s reporting package? [HUD ch. 5, par. 5-4B] H212

Was attribute sampling used and were the minimum sample sizes met?(Auditors may follow the guidance in AICPA’s Audit Guide for Government Auditing Standards and Circular OMB A-133 Audits,provided that the resulting sample size is equal to or greater than the minimum sample sizes in appendix A of the HUD audit guide.) [HUD ch. 1, par. 1-4 and appendix A] H213

22,090-4 Engagement Checklist Supplements—System Reviews 00-8 JAN 2014

PRP §22,080 Copyright © 2014, American Institute of Certified Public Accountants, Inc.

Ques. N/A Yes No Ref.

D. Chapter 6, “Ginnie Mae Issuers of Mortgage-Backed Securities Audit Guidance”

Not applicable

Have the following specific compliance requirements been tested in accordance with the procedures in the HUD audit guide or have alternative procedures been justified? H214

Federal financial reports

Eligibility to issue mortgage-backed securities

Review of custodial documents

Issuer’s administration of pooled mortgages

Review of monthly accounting reports and quarterly submissions

Securities marketing and trading practices

Adjusted net worth (required for all Ginnie Mae issuers, even if there are no securities or commitments outstanding at fiscal yearend)

Did the auditor address the required supplemental data as listed in the HUD audit guide (insurer’s adjusted net worth, issuer’s capital requirement, issuer’s liquid asset requirement, parent’s adjusted net worth, capital requirement and liquid asset requirements [if appropriate],and insurance requirement in the formats required? [HUD ch. 6, par. 6-4, attachments B–H] H215

Has a corrective action plan been submitted? [HUD ch. 6, par. 6-4] H216

Was attribute sampling used and were the minimum sample sizes met?(Auditors may follow the guidance in AICPA’s Audit Guide for Government Auditing Standards and Circular OMB A-133 Audits, provided that the resulting sample size is equal to or greater than the minimum sample sizes in appendix A of the HUD audit guide.) [HUD ch. 1, par. 1-4 and appendix A] H217

E. Chapter 7, “FHA-Approved Lenders Audit Guidance”

(Note: Mortgagee Letter 2011-05. This mortgagee letter, titled Revised Audited Financial Statement Reporting Requirements for Supervised Lenders in Parent-Subsidiary Structures and New Financial Reporting Requirements for Multifamily Mortgagees (ML 2011-05), was issued on January 5, 2011, and is effective immediately. It clarifies that supervised mortgagees should be following all other requirements in the HUD audit guide for nonsupervised mortgagees (primarily found in chapter 7 of that guide) except for those modified in ML 2011-05. Note: Loan Correspondent Audits No Longer Required. On April 20, 2010, HUD issued a final rule that eliminated the audit requirement for loan correspondents (previously, loan correspondents were required to have a financial statement audit and a compliance audit under the HUD Consolidated Audit Guide).

Not applicable

Have the following specific compliance requirements been tested in accordance with the procedures in the HUD audit guide or have alternative procedures been justified? H218

00-8 JAN 2014 Checklist for Review of Audits of HUD Engagements (Ending on or After December 15, 2012) 22,090-5

AICPA Peer Review Program Manual PRP §22,080

Ques. N/A Yes No Ref.

Compliance Requirements and Suggested Audit Procedures Applicable to Both Title I and Title II Lenders

Quality control plan

Sponsor responsibility for third-party originators

Branch office operations

Loan origination

Loan servicing

Federal financial and activity reports

Lender annual recertification, adjusted net worth, liquidity, andlicensing

Compliance Requirements and Suggested Audit Procedures Applicable to Title I Lenders

Loan disbursement

Eligible fees and charges

Compliance Requirements and Suggested Audit Procedures Applicable to Title II Lenders

Loan settlement

Escrow accounts

Kickbacks

Multifamily Insured Loans Reporting Requirement

Loan fees for multifamily mortgages

Did the auditor report on the required supplemental data as listed in the HUD audit guide, including adjusted net worth, in the format required? [HUD ch. 7, par. 7-4, attachments A–D] H219

Was attribute sampling used and were the minimum sample sizes met?(Auditors may follow the guidance in AICPA’s Audit Guide for Government Auditing Standards and Circular OMB A-133 Audits, provided that the resulting sample size is equal to or greater than the minimum sample sizes in appendix A of the HUD audit guide.) [HUD ch. 1, par. 1-4 and appendix A] H220

[The next page is 22,080A-1.]