chemical group mid-winter conference -- mergers and ... · with imc global) • borealis...

TRANSCRIPT

Presentation to:

Mergers & Acquisitions in the Chemical Industry

Tim WildingManaging DirectorCIBC World Markets

2

Tim Wilding

> Mr. Wilding joined CIBC World Markets from Salomon Smith Barney to lead the firm’s coverage of the chemicals, plastics and packaging industries

> Mr. Wilding has over 16 years of experience covering the global chemicals industry, with significant M&A and capital raising transaction experience across all sectors of the industry (specialty chemicals, fine chemicals, petrochemicals, fertilizers, paints and coatings, plastics, and packaging)

> A native of Great Britain, he started his career in London with Chase Manhattan and was a member of their chemical group for 6 years before joining Salomon Smith Barney, where he spent 9 years

> Mr. Wilding has a BSc. with joint honors in Management and Chemicals Sciences and prior to his career in banking worked for Courtaulds plc in their coatings division

Selected Transaction History

• Huntsman Packaging ($1.065 billion sale to JPM Chase Capital Partners)

• ARCO Chemical ($6.5 billion sale to Lyondell)

• Lyondell Petrochemical ($410 million acquisition of Alathon from Occidental)

• Lyondell Petrochemical ($4.5 billion M&A formation of Equistar)

• IMC Global ($1.4 billion acquisition of Harris Chemical)

• Freeport-McMoRan ($1.2 billion merger with IMC Global)

• Borealis (acquisition of PCD Polymere)• Geo Specialty Chemicals (acquisition

and financing of Hercules peroxides business)

• Kemira ($430 million sale of TiO2)• ICI (sale of Flex Products)• Cambrex Corp. (buy side advisory)• Polymer Group ($295 million initial

public offering)• Engelhard ($566 million equity offering,

$120 million bond offering)• FMC Corp. ($300 million initial public

offering carve-out)• Great Lakes Chemical ($100 million

initial public offering carve-out)• Orica Ltd. ($225 million private

placement) • Huntsman (HMP Equity Holdings) senior

discount notes with warrants ($423 million)

• Rohm & Haas ($2.0 billion bond offering)

• Resolution Performance Polymers ($800 million bank and high yield offering)

• Terra Industries ($200 million high yield offering)

• Potash Corp. ($600 million bond offering)

• PolyOne ($200 million high yield offering)

• Hexcel Corporation $240 million high yield offering

• RPM, Inc. ($100 million bond offering)• Ecolab ($300 million bond offering) • Great Lakes Chemical ($400 million

bond offering)

3

Agenda

> General M&A Trends

> Chemical M&A Trends & Considerations

General M&A Trends

5

General M&A Trends

Summary of Current M&A Environment

M&A Rebound in 2005

> Worldwide announced M&A volume soared to over $2.8 trillion in 2005

> 31% increase from 2004’s total of $2.1 trillion, the best year for M&A since 2000, and the third-best year ever

> Aided by easy access to capital and a record amount of private equity funds

> Significant dry powder

> Recent raising of mega-funds (Carlyle, CVC, Goldman Sachs, Warburg, Apollo, Blackstone)

> Blockbuster going-private transactions (Toys “R” Us, SunGard, Neiman-Marcus)

> Transaction multiples continue to climb

> Debt markets remain accessible

Financial Sponsor Activity at All-time

High

Recent Surge in Hostile Activity

> 3.8% of 2005 transactions were hostile or unsolicited

> Significant growth in hedge funds in recent years – intrigued by M&A and activism opportunities

> 2006 has continued this trend

6

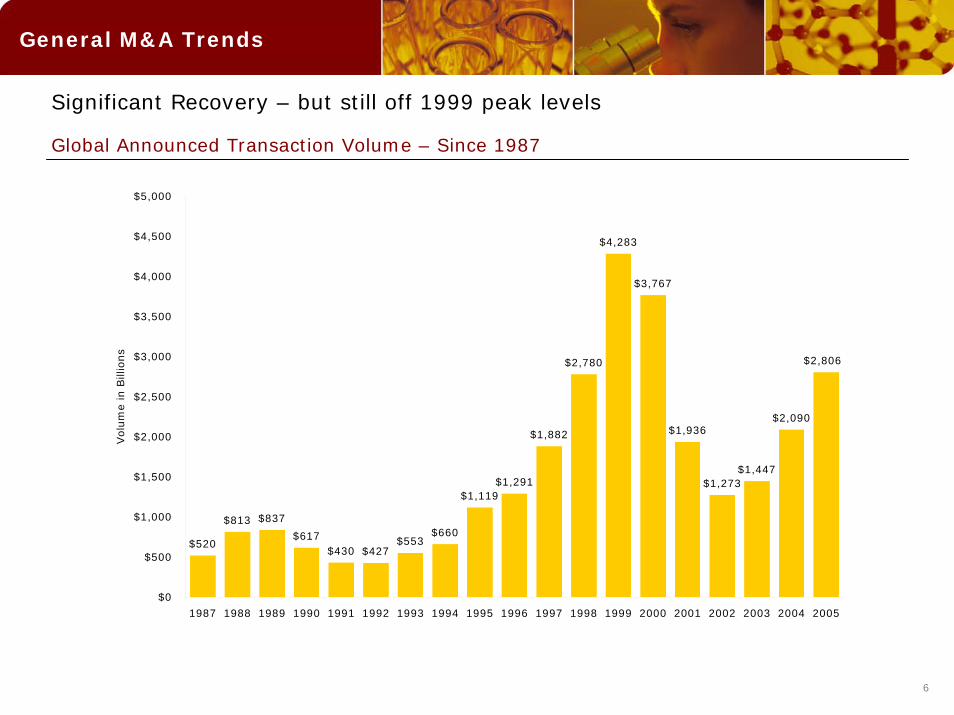

General M&A Trends

Significant Recovery – but still off 1999 peak levels

Global Announced Transaction Volume – Since 1987

$520

$813 $837

$617$430 $427

$553$660

$1,119$1,291

$1,882

$2,780

$4,283

$3,767

$1,936

$1,273$1,447

$2,090

$2,806

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Volu

me

in B

illio

ns

7

General M&A Trends

Growth in Private Equity Capital has fueled this recovery…

Buyout/Mezzanine and Venture Capital Raising

Increasingly Larger Pools of Capital

> Carlyle Group–$10 billion> CVC Capital Partners–$7.2 billion > Goldman Sachs Capital Partners–$8 billion > Warburg Pincus–$8 billion > Apollo Management LP–$10 billion > Blackstone Group–$12.5 billion

$46,690

$30,017

$51,661 $54,057

$76,436

$26,092

$10,649

$106,734

$3,862$16,987 $17,370

$37,782

$0

$30,000

$60,000

$90,000

$120,000

2000 2001 2002 2003 2004 Q1-Q3 2005

Buyout & Mezzanine ($M) Venture Capital ($M)

158

637

120309

86

172

91

141

130187

122130

“Mega-funds”

> Hertz Corp. sold to Clayton, Dubilier & Rice, Carlyle Group and Merrill Lynch Global Private Equity for $15 billion

> SunGard Data Systems sold to Silver Lake Partners and six other private equity firms for $11.3 billion

2005 Saw the Two Largest LBOs Since

RJR Nabisco in 1989

8

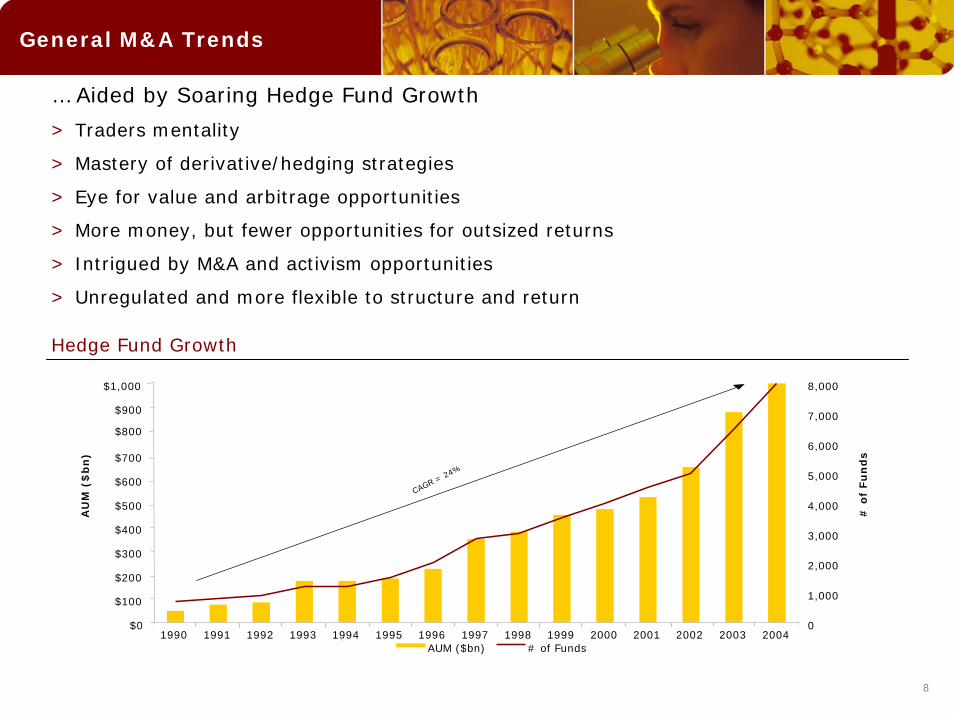

General M&A Trends

… Aided by Soaring Hedge Fund Growth

> Traders mentality

> Mastery of derivative/hedging strategies

> Eye for value and arbitrage opportunities

> More money, but fewer opportunities for outsized returns

> Intrigued by M&A and activism opportunities

> Unregulated and more flexible to structure and return

Hedge Fund Growth

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

AU

M (

$b

n)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

# o

f Fu

nd

s

AUM ($bn) # of Funds

CAGR = 24%

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

AU

M (

$b

n)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

# o

f Fu

nd

s

AUM ($bn) # of Funds

CAGR = 24%

9

General M&A Trends

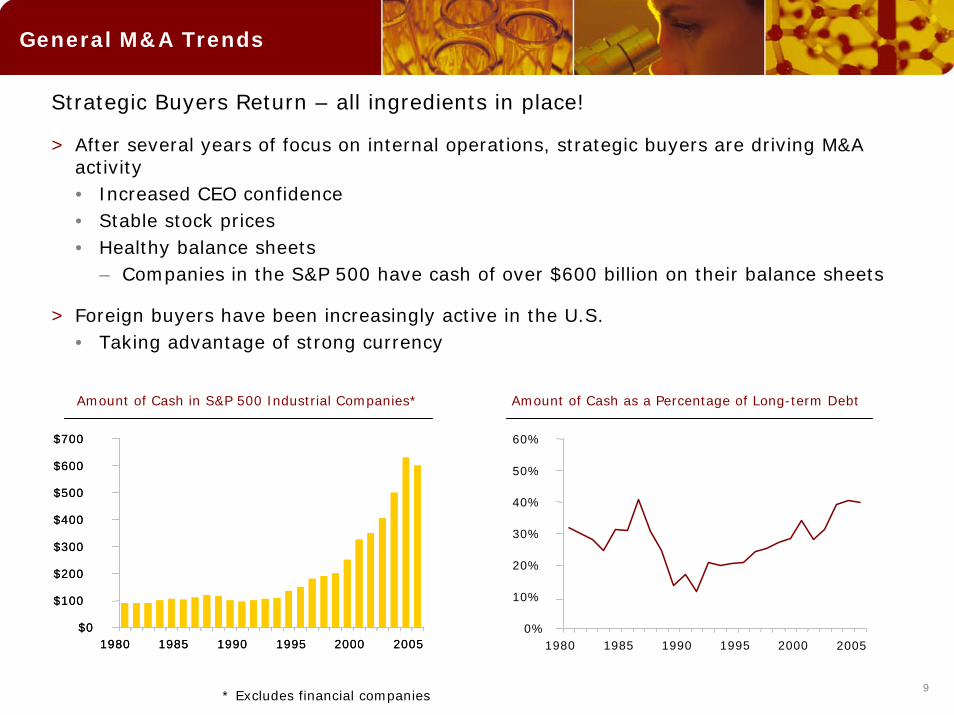

Strategic Buyers Return – all ingredients in place!

> After several years of focus on internal operations, strategic buyers are driving M&A activity• Increased CEO confidence• Stable stock prices• Healthy balance sheets

– Companies in the S&P 500 have cash of over $600 billion on their balance sheets

> Foreign buyers have been increasingly active in the U.S.• Taking advantage of strong currency

Amount of Cash in S&P 500 Industrial Companies* Amount of Cash as a Percentage of Long-term Debt

$0

$100

$200

$300

$400

$500

$600

$700

1980 1985 1990 1995 2000 2005$0

$100

$200

$300

$400

$500

$600

$700

1980 1985 1990 1995 2000 20050%

10%

20%

30%

40%

50%

60%

1980 1985 1990 1995 2000 2005

* Excludes financial companies

10

General M&A Trends

A predictable Consequence – A Surge in Hostile Activity

> Strategic raids: Hostile approaches deployed by blue-chip strategic buyers

> Availability of equity capital: Over $80 billion of private equity funds available for deployment and capital raising continues for mega-funds

> Cheap financing: Debt financing still remains very attractive by historical standards

> Deleveraging: Companies have accumulated cash and paid down debt – buyers can use target’s balance sheet to fund acquisitions

> CEO confidence: Studies indicate that CEO confidence is relatively high

> Sarbanes-Oxley effects: Less risk that public target will contain a significant undisclosed accounting or other problem

> Activism to remove takeover defenses: Activists are forcing companies to remove takeover defenses

> Impact of momentum investors: Momentum in favor of bidders is difficult to reverse when event-driven funds enter a target’s stock

> Boardroom jitters: Directors are nervous about being second-guessed if they reject a takeover proposal

11

General M&A Trends

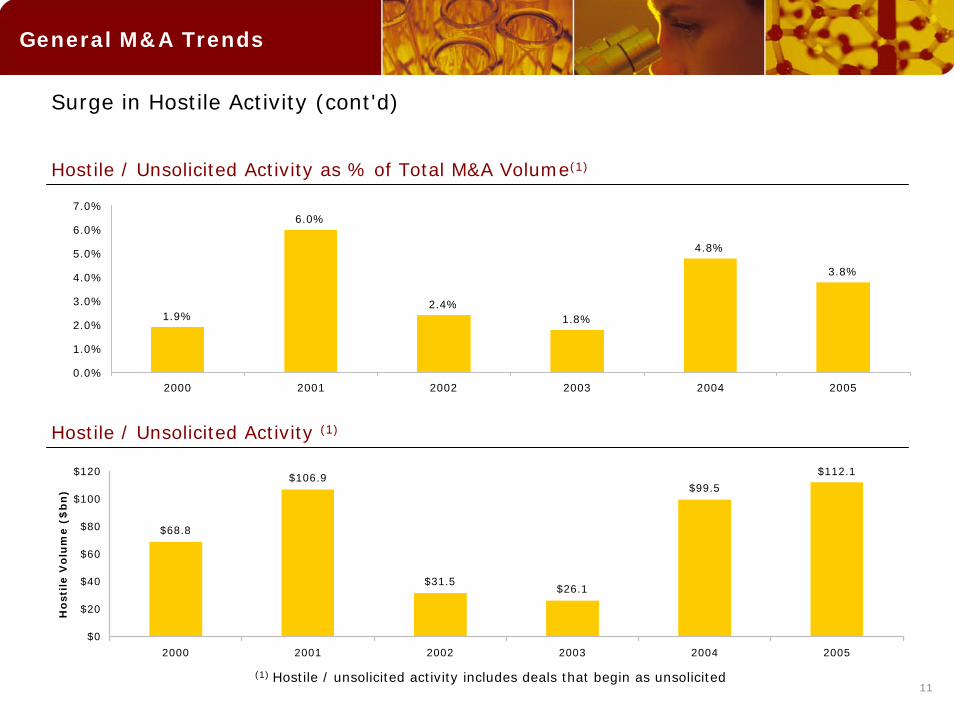

Surge in Hostile Activity (cont'd)

Hostile / Unsolicited Activity as % of Total M&A Volume(1)

1.9%

6.0%

2.4%1.8%

4.8%

3.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2000 2001 2002 2003 2004 2005

Hostile / Unsolicited Activity (1)

$68.8

$106.9

$31.5$26.1

$99.5

$112.1

$0

$20

$40

$60

$80

$100

$120

2000 2001 2002 2003 2004 2005

Ho

stil

e V

olu

me (

$b

n)

(1) Hostile / unsolicited activity includes deals that begin as unsolicited

Chemical M&A Trends & Considerations

13

Chemical M&A Trends & Considerations

What are the Key Ingredients in Making M&A Deals Happen?

> Willing buyer

> Willing seller

> Meeting of the minds

• Valuation

• Social issues

> Cycle Timing

• Economy

• Capital markets

14

Chemical M&A Trends & Considerations

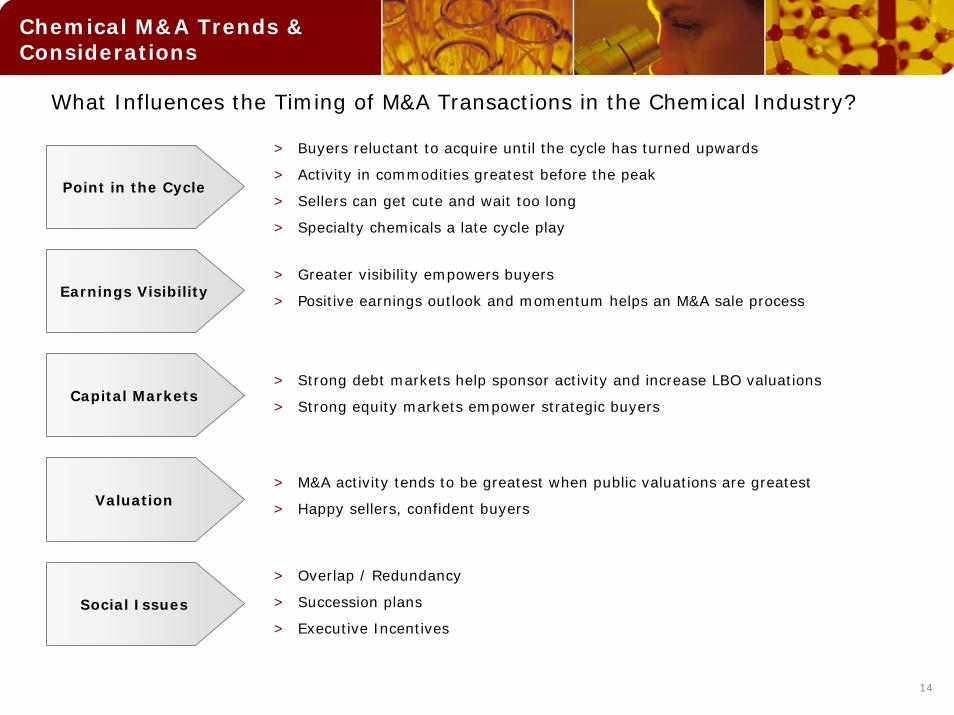

What Influences the Timing of M&A Transactions in the Chemical Industry?

> Buyers reluctant to acquire until the cycle has turned upwards

> Activity in commodities greatest before the peak

> Sellers can get cute and wait too long

> Specialty chemicals a late cycle play

Point in the Cycle

Earnings Visibility> Greater visibility empowers buyers

> Positive earnings outlook and momentum helps an M&A sale process

Capital Markets> Strong debt markets help sponsor activity and increase LBO valuations

> Strong equity markets empower strategic buyers

Valuation> M&A activity tends to be greatest when public valuations are greatest

> Happy sellers, confident buyers

Social Issues

> Overlap / Redundancy

> Succession plans

> Executive Incentives

15

Chemical M&A Trends & Considerations

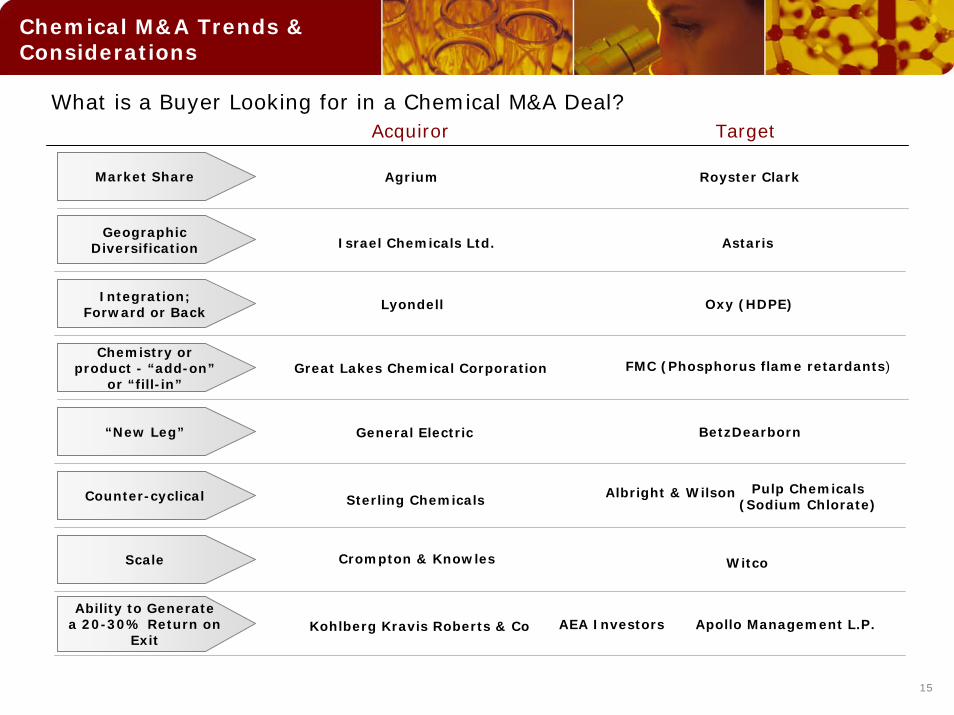

What is a Buyer Looking for in a Chemical M&A Deal?Acquiror Target

Market Share Agrium Royster Clark

“New Leg”

Counter-cyclical

Integration; Forward or Back

Chemistry or product - “add-on”

or “fill-in”

Scale

Ability to Generate a 20-30% Return on

Exit

Geographic Diversification Israel Chemicals Ltd. Astaris

Oxy (HDPE)Lyondell

FMC (Phosphorus flame retardants)Great Lakes Chemical Corporation

BetzDearbornGeneral Electric

Pulp Chemicals(Sodium Chlorate)

Albright & WilsonSterling Chemicals

Crompton & Knowles Witco

Kohlberg Kravis Roberts & Co Apollo Management L.P.AEA Investors

16

Chemical M&A Trends & Considerations

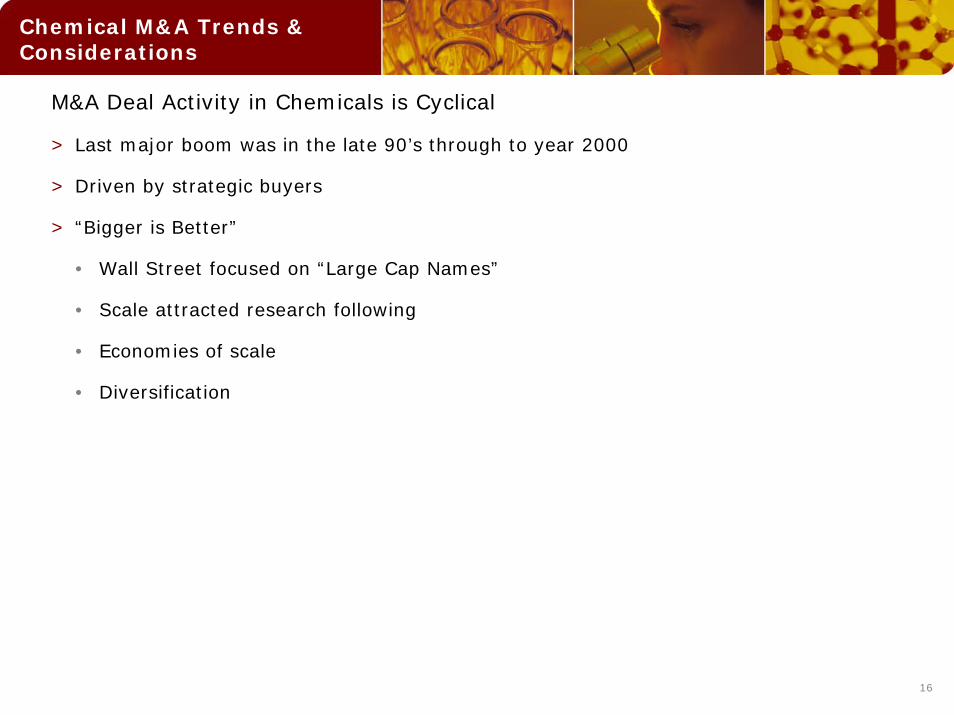

M&A Deal Activity in Chemicals is Cyclical

> Last major boom was in the late 90’s through to year 2000

> Driven by strategic buyers

> “Bigger is Better”

• Wall Street focused on “Large Cap Names”

• Scale attracted research following

• Economies of scale

• Diversification

17

Chemical M&A Trends & Considerations

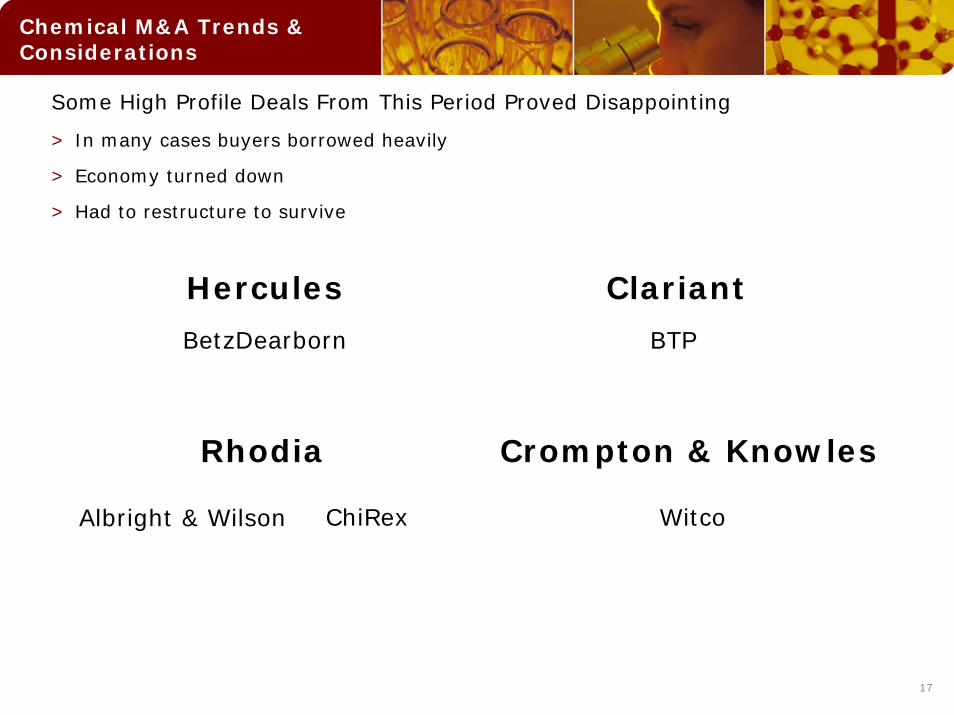

Some High Profile Deals From This Period Proved Disappointing

> In many cases buyers borrowed heavily

> Economy turned down

> Had to restructure to survive

Hercules Clariant

BetzDearborn BTP

Crompton & KnowlesRhodia

ChiRex WitcoAlbright & Wilson

18

Chemical M&A Trends & Considerations

The Perfect Storm 2001-2003

> M&A deal-making by strategics put on hold

> Chemical Industry’s Perfect Storm

• Economic downturn

• Over capacity

• High feedstock prices

• Commoditization

• Asian competition

> Investors reward cash and Balance Sheet strength

> As well as non-cyclicality (eg. Personal care, industrial gases)

> Buyer’s market

> Financial sponsors picked up the slack

> Hindsight is 20/20 – but this period proved a great time to buy!

19

Chemical M&A Trends & Considerations

Financial Sponsors Became the Most Active Class of Buyers of Chemical Assets

Financial Sponsor PurchaseDeal Activity (2001 – 2003) Target Price($mm)

Noveon(Goodrich Performance Material)

Cognis(from Henkel Group)

H&R(from Bayer)

$1,400

$2,237

$468

$1,679

$1,000

$4,350

$2,284

$610

AEA Investors Deutsche Bank DLJ

Goldman Sachs Permira

Apollo Management LP

EQT

Bain Capital

Apollo Management LP The Blackstone Group Goldman Sachs

The Blackstone Group

Apollo Management LP

Compass Minerals Group(IMC Global Salt Business)

SigmaKalon(from Totalfinaelf)

Ondeo Nalco(from Suez)

Celanese

United Agri Products(from ConAgra)

20

Chemical M&A Trends & Considerations

Why Sponsors Like Chemicals

> Track record of value creation

> Leverageable assets

> Requires industry knowledge, historically limiting competition

> Significant deal flow – industry continues to re-structure

> Willing to diligence complex situations which may not be understood in public markets

> Ability to work on lengthy “carve-out” processes

> Opportunity to capitalize on industry synergies via acquisitions

> Ability to buy diversified businesses in their entirety

> Can be quasi-strategic if acquired through an existing chemical investment platform

> Ability to exploit timing of cycles

> Consolidation and “add-on” acquisition opportunities

21

Chemical M&A Trends & Considerations

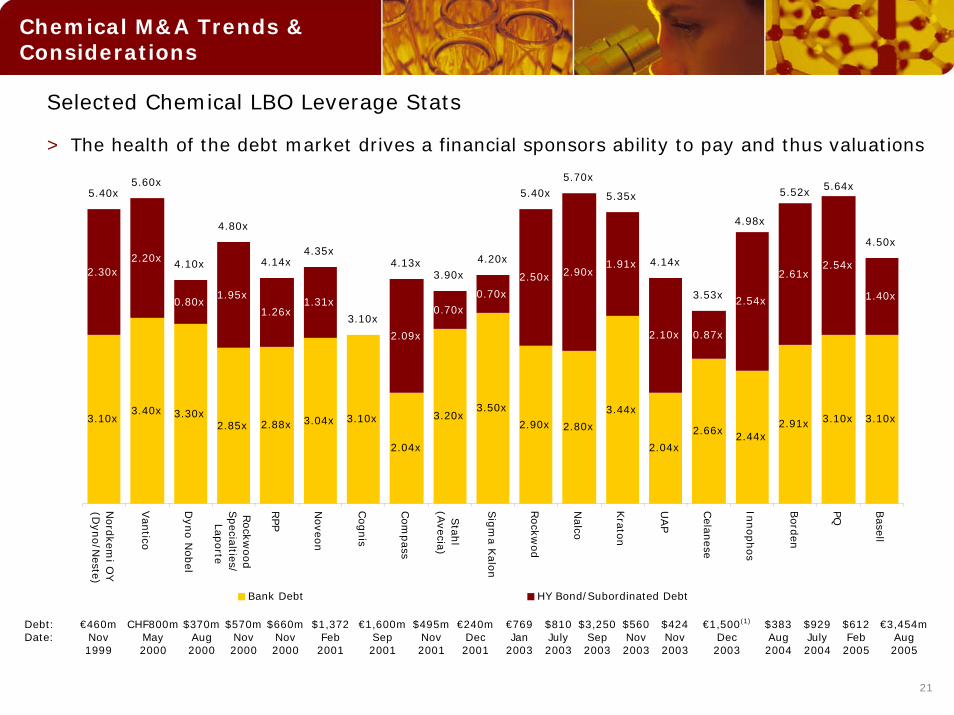

Selected Chemical LBO Leverage Stats

> The health of the debt market drives a financial sponsors ability to pay and thus valuations

3.10x3.40x 3.30x

2.85x 2.88x 3.04x 3.10x

2.04x

3.20x3.50x

2.90x 2.80x

3.44x

2.04x

2.66x 2.44x2.91x 3.10x 3.10x

2.30x2.20x

0.80x1.95x

1.26x1.31x

2.09x

0.70x0.70x

2.50x 2.90x1.91x

2.10x 0.87x

2.54x

2.61x2.54x

1.40x

5.40x5.60x

4.10x

4.80x

4.14x4.35x

3.10x

4.13x3.90x

4.20x

5.40x5.70x

5.35x

4.14x

3.53x

4.50x

5.64x

4.98x

5.52x

Nord

kemiO

Y

(Dyn

o/N

este)

Van

tico

Dyn

oN

obel

Rockw

ood

Specia

lties/ Lap

orte

RPP

Noveo

n

Cognis

Com

pass

Stah

l (A

vecia)

Sig

ma K

alon

Rockw

od

Nalco

Krato

n

UAP

Cela

nese

Innophos

Bord

en

PQ Basell

Bank Debt HY Bond/Subordinated Debt

Debt: €460m CHF800m $370m $570m $660m $1,372 €1,600m $495m €240m €769 $810 $3,250 $560 $424 €1,500(1) $383 $929 $612 €3,454m Date: Nov May Aug Nov Nov Feb Sep Nov Dec Jan July Sep Nov Nov Dec Aug July Feb Aug 1999 2000 2000 2000 2000 2001 2001 2001 2001 2003 2003 2003 2003 2003 2003 2004 2004 2005 2005

22

Chemical M&A Trends & Considerations

Case Study – Hexion, the creation by Apollo Management of a new industry major

> Industrial Logic – to consolidate the coating resins industry

> Filed with the SEC to pursue a U.S. IPO

Hexion Specialty Chemicals

Borden Resolution Specialty Materials Resolution Performance Products

Date: 8/2004 Price: $1,200 million

Date: 8/2004 Price: $215 million

Date: 11/2000 Price: $901 million

Bakelite AG

Date: 4/2005 Price: $246 million

23

Chemical M&A Trends & Considerations

Public to Private Transactions Have Substantially Increased

> We are likely to see this trend impact the chemical industry

Total Public-to-Private LBO Transaction Volume

$15

$10$9

$6$5

$8

$23

$50

$0B

$10B

$20B

$30B

$40B

$50B

1998 1999 2000 2001 2002 2003 2004 2005

24

12/1/94 2/26/97 5/25/99 8/21/01 11/17/03 2/13/0630405060708090

100110

Rela

tive P

rice

Relative - S&P 500 Index (Reported Basis) Specialty Chemicals Commodity Chemicals

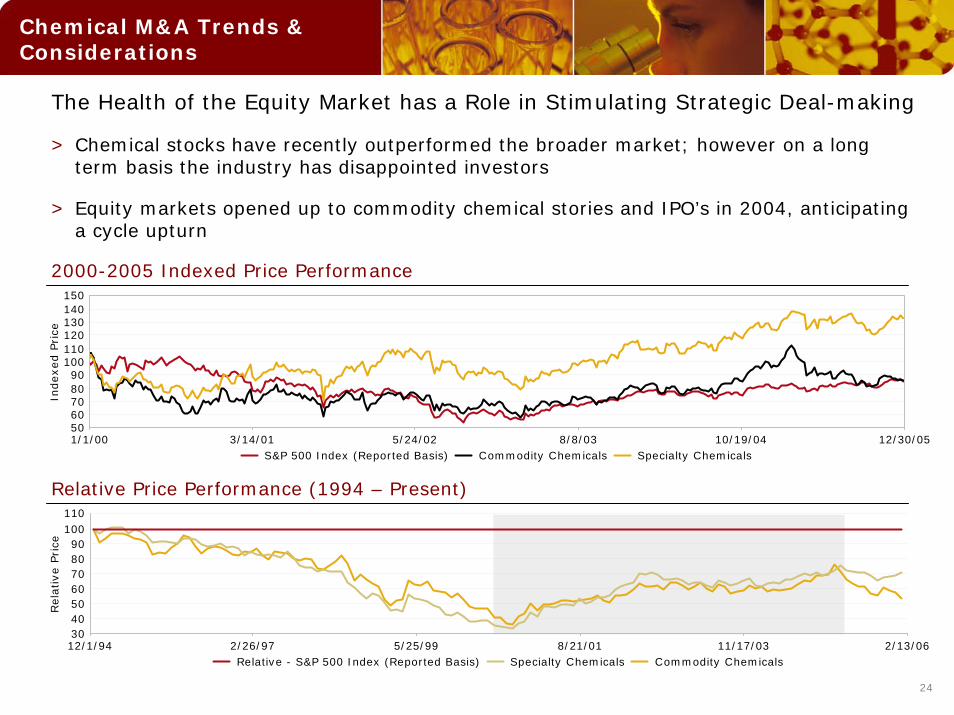

The Health of the Equity Market has a Role in Stimulating Strategic Deal-making

> Chemical stocks have recently outperformed the broader market; however on a long term basis the industry has disappointed investors

> Equity markets opened up to commodity chemical stories and IPO’s in 2004, anticipating a cycle upturn

Chemical M&A Trends & Considerations

1/1/00 3/14/01 5/24/02 8/8/03 10/19/04 12/30/055060708090

100110120130140150

Indexed P

rice

S&P 500 Index (Reported Basis) Commodity Chemicals Specialty Chemicals

2000-2005 Indexed Price Performance

Relative Price Performance (1994 – Present)

25

Chemical M&A Trends & Considerations

Why is the health of the equity market important for M&A deal-making?

> Renewed enthusiasm for chemical companies in the public equity markets is important in stimulating M&A activity for a number of reasons

• Market values reflect positive earnings growth and overall outlook

• Public valuations are a key valuation methodology

• Helps buyers make accretive transactions

• Helps public sellers realize value expectations

• Provides financial sponsors with a credible public equity market exit (IPO)

26

Chemical M&A Trends & Considerations

2005/2006 Return of the Strategic Buyer

> Valuation Multiples moving back to historical levels

> The stock market is rewarding acquirors

> Hostiles, historically a rarity in the chemical industry, have made an appearance

BASF + Engelhard Ineos + Innovene

OxyChem + Vulcan ChemicalsKemira + Finnish Chemicals

Cytec + UCB (Coating Resins) Henkel + Sovereign Specialty Chemicals

Lubrizol + NoveonLyondell + Milenium Chemicals

Albemarle + Akzo Nobel (Refining Catalysts) Crompton + Great Lakes Chemical Corp.

27

Chemical M&A Trends & ConsiderationsChemical M&A Trends & Considerations

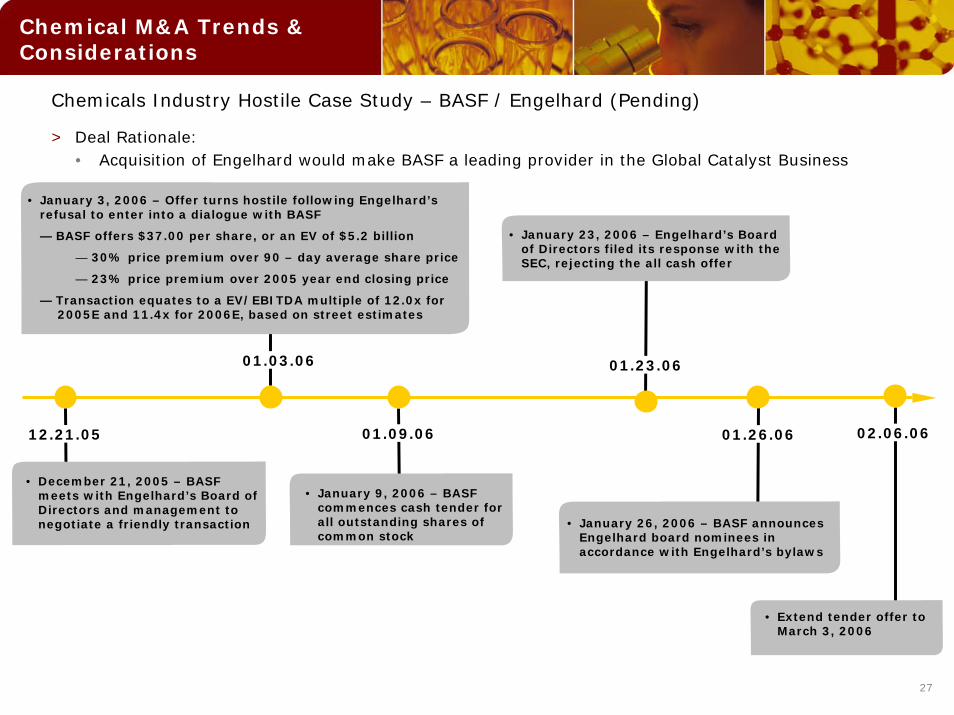

Chemicals Industry Hostile Case Study – BASF / Engelhard (Pending)

> Deal Rationale:• Acquisition of Engelhard would make BASF a leading provider in the Global Catalyst Business

01.03.06

• December 21, 2005 – BASF meets with Engelhard’s Board of Directors and management to negotiate a friendly transaction

12.21.05

• January 26, 2006 – BASF announces Engelhard board nominees in accordance with Engelhard’s bylaws

01.26.06

• January 23, 2006 – Engelhard’s Board of Directors filed its response with the SEC, rejecting the all cash offer

01.23.06

• January 9, 2006 – BASF commences cash tender for all outstanding shares of common stock

01.09.06 02.06.06

• Extend tender offer to March 3, 2006

• January 3, 2006 – Offer turns hostile following Engelhard’s refusal to enter into a dialogue with BASF

— BASF offers $37.00 per share, or an EV of $5.2 billion

— 30% price premium over 90 – day average share price

— 23% price premium over 2005 year end closing price

— Transaction equates to a EV/EBITDA multiple of 12.0x for 2005E and 11.4x for 2006E, based on street estimates

28

Chemical M&A Trends & Considerations

Chemical Issuers Took Advantage of Positive Equity Markets

> Unprecedented chemical equity issuance in 2004/2005 reflects investors renewed interest

> IPO’s can be an alternative to M&A sales

> Time has arguably passed for petrochemical IPOs given cycle peak

2004/2006 Chemical Equity Activity Transaction Size($mm)

Arkema Pending Spin-off TBD

Hexion Filed S-1 11/21/05 IPO $696

Innovene Filed S-1 9/12/05 (subsequently sold) IPO / Sale $1,000

Koppers 01/31/06 IPO $160

Tronox 11/22/05 IPO $245

Rockwood 08/16/05 IPO $408

Canexus 08/09/05 Income Trust IPO C$318

CF 08/05/05 IPO $660

Royster Clark 07/22/05 IDS IPO C$325

Huntsman 02/11/05 IPO $1,385

Lanxess 01/31/05 IPO / Spin-off €1,150

Celanses 01/20/05 IPO $800

29

Chemical M&A Trends & Considerations

Significant Recent Chemical Equity Activity (cont’d)

> Westlake launched the window for petrochemical IPOs

United Agra Products

11/22/04 IPO $504

Nalco 11/11/04 IPO $667

Kemira 10/04/04 IPO / Spin-off €98

Braskem 09/22/04 Common Stock $245

Westlake 08/11/04 IPO $171

Borden 07/15/04 IPO / Sale $1,200

Compass Minerals Group

07/09/04 Common Stock $138

Noveon 06/03/04 IPO / Sale $920

Rhodia 05/05/04 Rights Offering €471

Clariant 04/21/04 Rights Offering CHF 920

Yara 03/25/04 IPO / Spin-off $380

2004/2006 Chemical Equity Activity Transaction Size($mm)

30

Chemical M&A Trends & Considerations

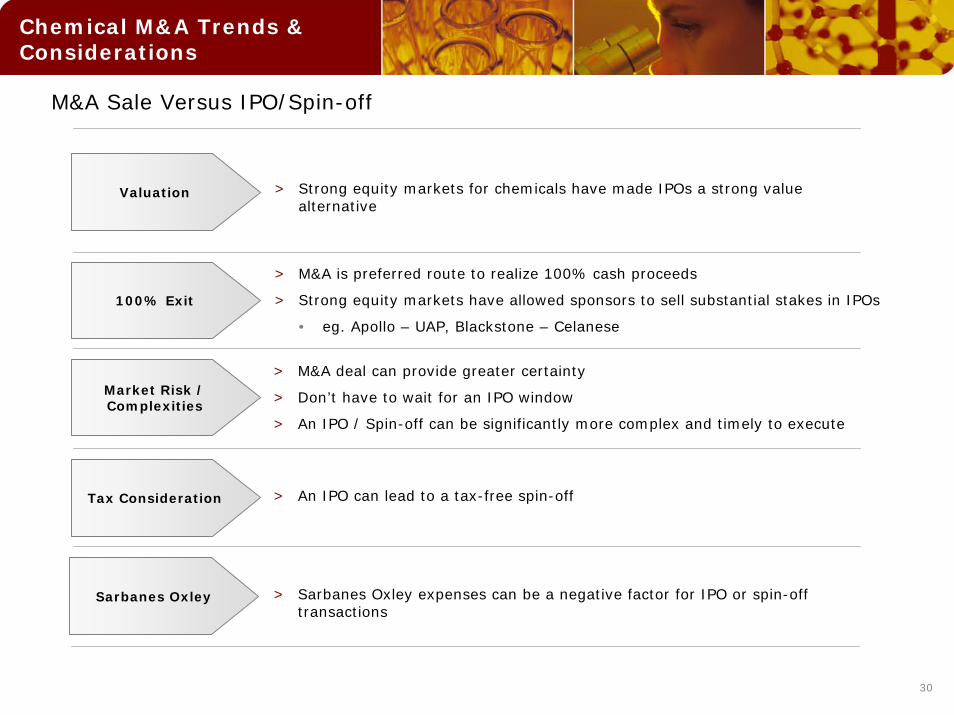

M&A Sale Versus IPO/Spin-off

Valuation > Strong equity markets for chemicals have made IPOs a strong value alternative

100% Exit

> M&A is preferred route to realize 100% cash proceeds

> Strong equity markets have allowed sponsors to sell substantial stakes in IPOs

• eg. Apollo – UAP, Blackstone – Celanese

Market Risk / Complexities

> M&A deal can provide greater certainty

> Don’t have to wait for an IPO window

> An IPO / Spin-off can be significantly more complex and timely to execute

Tax Consideration > An IPO can lead to a tax-free spin-off

Sarbanes Oxley > Sarbanes Oxley expenses can be a negative factor for IPO or spin-off transactions

31

Chemical M&A Trends & Considerations

M&A vs. IPO / Spin-off

Company IPO M&A Sale

KerrMcGee Tronox

Noveon

Canexus

Innovene

Royster Clark

32

Chemical M&A Trends & Considerations

M&A vs. IPO / Spin-off Case Study: Canexus

Income Trust IPO

August 2005

C$317,500,000

Joint Book-Runner with respect to this transaction

Income Trust IPOIncome Trust IPO

August 2005

C$317,500,000

Joint Book-Runner with respect to this transaction

Income Trust IPO

> In 2004, Nexen, a Canadian oil and gas provider, announced it would divest non-core assets, including its Nexen Chemicals division, a leading producer of sodium chlorate and chlor-alkali

> Nexen management decided to pursue a dual-track sale process, working towards an income trust IPO while simultaneously exploring an M&A sale

> CIBC World Markets was engaged as both joint M&A sell-side advisor and joint book-runner on the income trust IPO

> On August 9th, 2005, Nexen Chemicals, renamed Canexus, priced a $300 million income trust IPO with an offering yield of 8.75%

> The offering had been upsized late in the marketing process from $200 million and the yield was revised from an earlier range of 9-10%

> Following full exercise of a 5.8% Greenshoe, Nexen Inc. retained 61.4% of outstanding income trust units

(C$ in thousands)

At IPOTrust Units O/S 82.3 Unit Price $10.00Market Value $822.9Total Debt $200.0Enterprise Value $1,022.9

Adjusted LTM EBITDA(1) $103.8EV/Adjusted LTM EBITDA 9.9x (1) Adjusted for plant shutdown costs and other non-recurring

expenses

Dual Process Summary

Income Trust Valuation

Canexus

CIBC World Markets

33

Chemical M&A Trends & Considerations

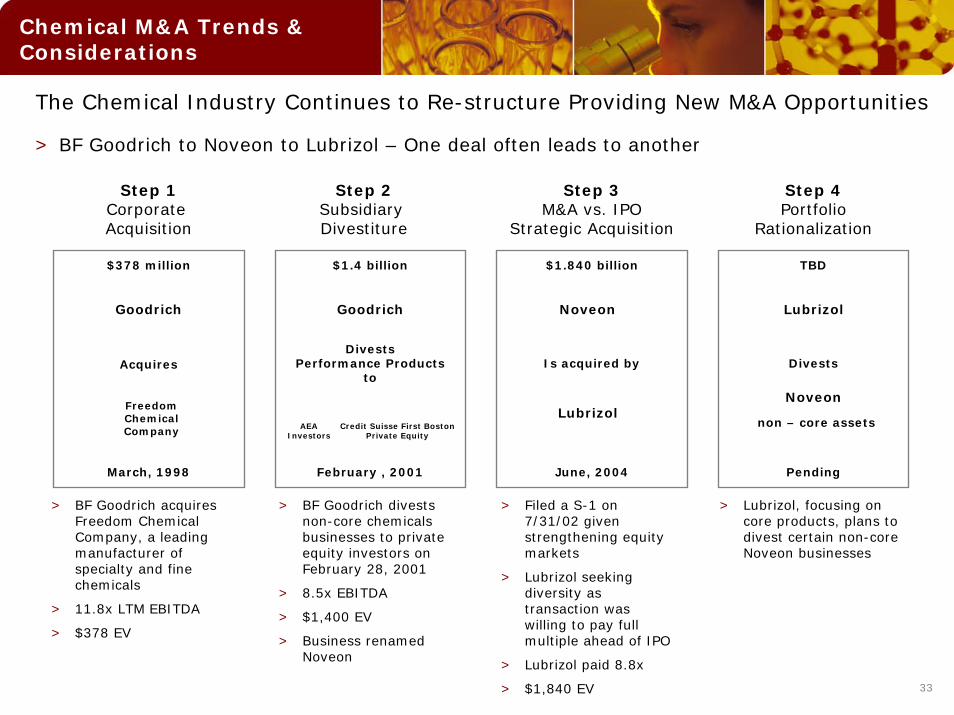

The Chemical Industry Continues to Re-structure Providing New M&A Opportunities

> BF Goodrich to Noveon to Lubrizol – One deal often leads to another

Step 1Corporate Acquisition

Step 2Subsidiary Divestiture

Step 3M&A vs. IPO

Strategic Acquisition

Step 4Portfolio

Rationalization

$378 million

Acquires

March, 1998

$1.840 billion

Is acquired by

June, 2004

$1.4 billion

Divests Performance Products

to

February , 2001

FreedomChemicalCompany

Goodrich Goodrich Noveon

LubrizolAEA

InvestorsCredit Suisse First Boston

Private Equity

TBD

Divests

Pending

non – core assets

Lubrizol

Noveon

> BF Goodrich acquires Freedom Chemical Company, a leading manufacturer of specialty and fine chemicals

> 11.8x LTM EBITDA

> $378 EV

> Filed a S-1 on 7/31/02 given strengthening equity markets

> Lubrizol seeking diversity as transaction was willing to pay full multiple ahead of IPO

> Lubrizol paid 8.8x

> $1,840 EV

> BF Goodrich divests non-core chemicals businesses to private equity investors on February 28, 2001

> 8.5x EBITDA

> $1,400 EV

> Business renamed Noveon

> Lubrizol, focusing on core products, plans to divest certain non-core Noveon businesses

34

Chemical M&A Trends & Considerations

Looking to the Future - Industry Consolidators, Some New Names

> The next wave of industry consolidation could involve some new names

> Access recently acquired Basell; Ineos recently acquired Innovene

Sabic Ineos

Hexion

Access Industries Reliance Chemicals

35

Chemical M&A Trends & Considerations

Closing Remarks

> The global chemical industry will continue to re-structure

> New companies will be born as non-chemical parents continue to spin-off assets

> The biggest companies will continue to get bigger

> M&A is back in fashion with strategic buyers

> Expect to see emerging strategic buyers make a big impact

> Financial buyers still very interested in the sector

> Expect to see renewed interest in “going-private” activity by small-cap public chemical companies