china china infrastructure -...

TRANSCRIPT

Deutsche Bank Markets Research

Asia

China

Transportation

Infrastructure

Industry

China Infrastructure

Date

3 March 2017

Forecast Change

PPP story continues, upgrading 2017-2018 infra FAI; Buy CCC/CSCI

Reiterating positive view on constructors in 2017

________________________________________________________________________________________________________________

Deutsche Bank AG/Hong Kong

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016.

Phyllis Wang

Research Analyst

(-) - -

Key Changes

Company Target Price Rating

1800.HK 12.08 to 13.71(HKD)

-

3311.HK 14.97 to 16.06(HKD)

-

1186.HK 11.84 to 13.36(HKD)

-

0390.HK 6.93 to 7.92(HKD) -

Source: Deutsche Bank

Top picks

China Comms Construct (1800.HK),HKD10.78

Buy

CSCI (3311.HK),HKD13.40 Buy

Source: Deutsche Bank

Companies Featured

China Comms Construct (1800.HK),HKD10.78

Buy

2015A 2016E 2017E

P/E (x) 8.9 9.4 7.9

EV/EBITDA (x) 8.8 9.3 8.9

Price/book (x) 0.7 1.1 1.0

CSCI (3311.HK),HKD13.40 Buy

2015A 2016E 2017E

P/E(x) 11.8 13.6 10.2

EV/EBITDA(x) 11.5 11.0 8.4

Price/book(x) 2.6 2.0 1.8

China Rail Construction (1186.HK),HKD11.20

Buy

2015A 2016E 2017E

P/E (x) 9.4 9.4 8.1

EV/EBITDA (x) 5.0 4.9 4.4

Price/book (x) 0.9 1.1 1.0

China Railway Group (0390.HK),HKD7.16 Buy

2015A 2016E 2017E

P/E (x) 11.6 10.8 9.3

EV/EBITDA (x) 8.6 7.7 6.9

Price/book (x) 0.9 1.1 1.0

Source: Deutsche Bank

We reiterate our positive view on the construction sector for the rest of this year after our recent trip and analysis of PPP projects. Domestic orders for infrastructure projects are still healthy in Jan 2017. We believe healthy momentum in the coming months will continue, supported by the accelerating development of PPP projects (mainly highway and municipal projects). Management guidance on new orders in 2017 looks stronger than expectation. We raise our estimate on infrastructure spending in China by 2-4% in 2017-2018, on our base case analysis of PPP projects. We still like constructors on the back of healthy earnings and order outlook. CCC and CSCI are top picks.

Positive message from recent tour: healthy new orders growth to continue Our trip last week to Beijing, Shangdong, Jiangsu, Hubei and Hunan in relation to the infrastructure construction sector gave us the impression that sentiment in the infrastructure industry remains strong. Progress on the PPP model (especially from highway, subway and municipal projects) is ahead of our expectation, which should support infra spending in 2017-19. In addition, all the constructors expect positive new order growth this year after the strong growth in 2016. Accordingly, we raise our new orders estimates for the constructors by 8-23% in 2017.

Lifting infra FAI in China, due to accelerating development of PPP projects We lift China infra spending (including railway, road and municipal projects) forecasts by 2-4% for 2017-18 on a base-case scenario, mainly due to higher assumption on highway and subway investment. Thus, we now forecast infra FAI in China to grow 5% CAGR in 2016-2018 (vs. previous 3.5%), among which we expect investment via the PPP financial model to account for 20% of total in 2018 (vs. previous 15%). We estimate the market size for PPP projects (mainly including transportation and municipal projects) will be more than Rmb2trn in 2017-18 (vs. our previous estimate of Rmb1.65trn), representing a 35% CAGR over 2016-2018. Our blue sky scenario implies 2% and 9% potential upside from our current estimates for infra FAI and investment for PPP projects, respectively; we believe this would enhance constructors’ earnings by 5-10% on the back of higher construction volume and better margin expansion led by a rising portion from high-margin PPP projects.

Upgrade earnings/TP; consensus estimates conservative; top pick: CCC/CSCI We raise CRCC, CRG, CCC and CSCI’s 2016-2018 earnings by 4-7% on higher infra spending assumption. Our revised 2017-2018 earnings forecasts are 3-16% ahead of market consensus. CCC is our top pick as it is likely a medium-term beneficiary of the OBOR initiative and has more attractive valuations then peers. It has the highest exposure to PPP projects among the big three names and strong capability to control projects. Potential SOE reforms may benefit its B/S. CCC trades at 7.9x 2017E PE (3%/15% discount to CRCC/CRG’s). We also like CSCI for its potential to be the biggest beneficiary of the PPP model promotion given its high exposure to the domestic infra investment business.

Valuing Chinese railway companies on DCF; risks Our preferred valuation methodology for railway names is one-year forward FY17E DCF (WACC: 7.4% for CRG, 7.0% for CRCC, 8.0% for CCC, and 8.5% for CSCI). Risks: government spending and political risk for overseas projects. In this report we change estimates and TPs for companies under coverage. Please see Figure 18-19 on page 9 for details.

Distributed on: 02/03/2017 21:03:35 GMT

3 March 2017

Infrastructure

China Infrastructure

Page 2 Deutsche Bank AG/Hong Kong

PPP story continues

Positive message on constructors from our recent trip

We took a trip last week to gain further insight into the infrastructure sector.

We covered five regions in China (Beijing, Shangdong, Jiangsu, Hubei and

Hunan) and visited infrastructure constructors (MCC, CSCEC, Gezhouba, and

JSTI group), Jinan Development and Reform Commission and industry expert

from China Railway Construction (CRC).

The trip gave us the impression that sentiment in the infrastructure industry

remains strong. Progress on the Public-Private Partnership (PPP) model

(especially from highway, subway and municipal projects) is ahead of our

expectation, which should support infrastructure spending in 2017-19E. We

believe railway infrastructure spending (a key driver for infrastructure spending

growth in the past few years), will no longer be the catalyst in the next few

years, which is also in line with industry expert’s view (from CRC).

1) All the constructors we visited are positive on the outlook, given the

accelerating development of PPP models. As well, they cite the

continued healthy new orders growth from infrastructure projects in

January 2017 and expect this trend to remain for the rest of this year.

2) Jinan local government is aggressively pushing PPP project

developments. 32 projects are now in their project pool, among which

10 are in execution period. They have picked up 30 projects this year,

which will be put into the local governments’ PPP project pool.

3) The railway expert from CRC expects railway infrastructure to have no

growth in 2017. The development of PPP railway projects looks slow

due to low returns.

Good signals from PPP annual report

Expanding national PPP reserves, further accelerating implementation

The China Public Private Partnerships Center (CPPPC) recently released an

annual report on the MoF’s PPP project pool. The report notes improvement in

scale and quality of reserved PPP projects. At the end of 2016, total investment

from 11,260 reserved PPP projects amounted to RMB13.5tr, up 8.3% from

end-September 2016 and 66% from end-January 2016. Despite the expanding

scale, the contract signing rate in terms of project number and total

investment continued to rise; it jumped to 12.0% from 9.0% at end-September

and to 16.5% from 12.5% at end-September, respectively. By percentage

points, the 4Q16 contract signing rate enjoyed the fastest quarterly growth in

2016.

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 3

Figure 1: Contract signing rate for national PPP project

reserve by number of projects

Figure 2: Contract signing rate for national PPP project

reserve by investment

298 369

619

946

1,351

4.3% 4.8%6.7%

9.0%12.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

-

200

400

600

800

1,000

1,200

1,400

1,600

End-Jan 2016 End-Mar 2016 End-Jun 2016 End-Sep 2016 End-Dec 2016

Number of contracted projects Contract signing rate

# of projects

410 510

1,060

1,560

2,230

5.0% 5.8%

10.0%12.5%

16.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

-

500

1,000

1,500

2,000

2,500

End-Jan 2016 End-Mar 2016 End-Jun 2016 End-Sep 2016 End-Dec 2016

Contracted investment value Contract signing rate

Rmbbn

Source: CPPPC

Source: CPPPC

Regional and industrial distribution remains concentrated

Regional distribution of the PPP project pool is still concentrated. As of end-

2016, the top five provinces represented 48% of total number of projects and

42% of total project investments (with Guizhou and Shandong dominating both

rankings), reflecting the differentiated attitude of local governments towards

the PPP model. We note that active participants in PPP projects are mainly

from provinces that have a weaker fiscal situation to boost infrastructure

investment, as well as from provinces with larger population to underpin

projects’ operational profitability.

Figure 3: Regional distribution of national PPP project

reserve by number of projects at end-2016

Figure 4: Regional distribution of national PPP project

reserve by investment at end-2016

Guizhou, 16%

Shandong, 10%

Xinjiang, 8%

Sichuan, 8%

Inner Mongolia, 7%Henan, 7%Liaoning, 4%

Gansu, 4%

Hebei, 4%

Yunnan, 4%

Others, 29%

Guizhou, 12%

Shandong, 9%

Yunnan, 8%

Henan, 7%

Sichuan, 7%

Inner Mongolia, 5%Jiangsu, 5%Hebei, 5%

Gansu, 4%

Liaoning, 4%

Others, 34%

Source: CPPPC

Source: CPPPC

In terms of reserved project type, municipal (mainly subway), transportation

(mainly highway) and urban comprehensive development projects occupied

the top three of the reserved project number (jointly accounting for 54% of

total) and project investment (68% of total) at end-2016. Figure 5 and Figure 6

illustrate the overall rising trend of these three project types. Indeed, these are

the major businesses of the constructors under our coverage. Business

opportunities remain adequate, in our view, given the significant upside

potential in contract signing rate and the sizeable municipal, transportation and

urban development projects.

3 March 2017

Infrastructure

China Infrastructure

Page 4 Deutsche Bank AG/Hong Kong

Figure 5: Contribution from

transportation/municipal/urban development PPP

projects by number

Figure 6: Contribution from

transportation/municipal/urban development PPP

projects by investment

43.7%

52.7%53.1%

53.7%53.8%

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

60.0%

End-Jan 2016 End-Mar 2016 End-Jun 2016 End-Sep 2016 End-Dec 2016

63.9%

65.2%

67.2%

68.0% 67.7%

60.0%

62.0%

64.0%

66.0%

68.0%

70.0%

End-Jan 2016 End-Mar 2016 End-Jun 2016 End-Sep 2016 End-Dec 2016

Source: CPPPC

Source: CPPPC

Demonstration projects leading the way

Compared with the MoF’s entire PPP pool, the 743 demonstration PPP

projects, which have a total investment of RMB1.9tr, recorded a much higher

contract signing rate at end-2016 (i.e. 49%/50% in terms of number of

projects/total investment). We highlight that besides the high implementation

rate, there are much fewer projects in the initial recognition stage (4% of total)

compared with that in the MoF’ entire pool (62% of total). This will enable

smoother project negotiations and execution, in our view.

Figure 7: Contract signing rate by number of projects at

end-2016

Figure 8: Contract signing rate by investment at end-

2016

48.9%

12.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Demonstration projects National PPP reserve

50.4%

16.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Demonstration projects National PPP reserve

Source: CPPPC

Source: CPPPC

The first batch of demonstration projects, released in November 2014, is finally

100% contracted, in line with the MoF’s previous guidance. In the same

guidance, the MoF urged all the second and third batch of demonstration

projects to finish procurement (or to be contracted by definition) by end-March

2017 and end-September 2017. So far, the average execution period (time

between project release and being contracted) of the third batch of

demonstration projects (released in October 2016) has shortened by four

months to 11 months. If procurements could be achieved on time (which is

highly likely, in our view, given stronger administrative and financial support

and the need to better understand the PPP model from all related parties), the

implied average execution period could decline further, and could accelerate

the constructors’ revenue recognition from PPP projects in 2017.

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 5

Figure 9: Demonstration PPP projects released by the MoF

Announcement date # of projects Total investment (Rmbbn)

Deadline for finishing procurement

Implied period for full procurement

(month)

Contract signing rate by # of projects

First batch Nov-14 22 71 Dec-16 25.0 100%

Second batch Sep-15 205 627 Mar-17 18.0 62%

Third batch Oct-16 516 1,170 Sep-17 11.5 43%

Total 743 1,868 50% Source: MoF, CPPPC

Figure 10: Average execution period for demonstration projects at end-2016

15.015.6

11.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

First batch Second batch Third batch

Month

Source: CPPPC

Constructors’ new orders: raising our estimates; solid growth may continue in 2017-2018E

New contract growth strong in 4Q16, beating expectations

Despite having a high 4Q15 base, CRG and CRCC registered higher-than-

expected new orders growth of 25% and 38% in 4Q16, respectively. Expedited

rollout of PPP projects continued to drive solid growth in the urban transit and

municipal segments in 4Q16 and brought strong recovery in highway

construction orders too (+121% yoy for CRG and +110% for CRCC), which

helped offset a weaker railway bidding market during the same period (new

orders down 25%/26% for CRG/CRCC in 4Q16). In FY2016, CRG and CRCC’s

total new contract value rose 29% yoy to RMB1.24trn and 28% yoy to

RMB1.22trn, respectively (13% and 15% higher than our previous estimates for

CRG and CRCC). Newly-signed PPP contract value was RMB290bn and

RMB240bn for CRG and CRCC, respectively, of which RMB160bn/RMB200bn

was related to construction for CRG/CRCC, respectively.

CSCI’s 2016 new orders grew 19% yoy to HKD84bn, slightly above our

previous estimate of HKD82bn and its guidance of HKD83bn. Among CSCI’s

2016 new orders, HKD50bn+ would be related to PPP projects, based on our

estimate.

3 March 2017

Infrastructure

China Infrastructure

Page 6 Deutsche Bank AG/Hong Kong

CCC’s 2016 new orders grew 12% yoy to Rmb730bn, slightly above our

estimate. The solid growth was mainly driven by the investment (81% yoy) and

overseas segments (51% yoy). Total new contract value contributed by PPP

was around Rmb174bn, of which Rmb151bn was related to construction.

Management guidance on 2017 orders looks stronger than forecasts

All the constructors we visited witnessed continued healthy new orders growth

from infrastructure projects in January 2017. The constructors expect the trend

to continue for the rest of the year. During our Beijing conference in January

2017, CRCC guided for new orders to grow c. 10% yoy. CCC gave new orders

growth guidance on 28 February 2017, expecting new orders to rise more than

20% in 2017. The guidance provided by these companies is better than our

expectations.

Upgrading our new orders estimates for the constructors

Based on ytd performance and management guidance, we raise our new order

estimates by 18% on average for the constructors in 2017 and 23% in 2018.

Figure 11: CCC’s new orders growth Figure 12: CRCC’s new orders growth

608 650

731

900

994

12%

7%

12%

23%

10%

0%

5%

10%

15%

20%

25%

500

600

700

800

900

1,000

1,100

2014 2015 2016 2017E 2018E

Rmb bn

New contract value YoY chg

828 949

1,219

1,356

1,466

-3%

15%

28%

11%8%

-6%-3%0%3%6%9%12%15%18%21%24%27%30%

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

2014 2015 2016 2017E 2018E

Rmb bn

New contract value YoY chg

Source: Deutsche Bank, Company data

Source: Deutsche Bank, Company data

Figure 13: CRG’s new orders growth Figure 14: CSCI’s new orders growth

935 957

1,235 1,358

1,453

1% 2%

29%

10%7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

2014 2015 2016 2017E 2018E

Rmb bn

New contract value YoY chg

60 70

84 94

101 32%

16%20%

13%

7%

0%

5%

10%

15%

20%

25%

30%

35%

-

20

40

60

80

100

120

2014 2015 2016 2017E 2018E

HK$ bn

New contract value YoY chg

Source: Deutsche Bank, Company data

Source: Deutsche Bank, Company data

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 7

Lifting infra FAI estimates, mainly driven by higher PPP investment (mainly highway and municipal projects)

We believe the promotion of PPP projects should support infrastructure

investment, in turn helping to support China’s economic growth. We note that

municipal and transportation projects (the target market of CCC, CRCC, CRG

and CSCI) account for a high proportion of total investment for the national

reserve for PPP projects. Hence, the accelerating development of PPP projects

should benefit all the constructors under our coverage.

We lift China infrastructure spending (including railway, road and municipal

projects) estimate by 2-4% in 2017-2018 based on a base-case scenario (our

assumption: all the projects in the national PPP project reserve could enter

implementation period in the next three years). Consequently, we now forecast

infra FAI in China to register a 5% CAGR over 2016-2018 (vs. our previous

estimates of 3.5%), among which we expect investment via the investment

financing model to account for 17% of total in 2018 (vs. our previous forecast

of 15%). We estimate the market size for PPP projects (mainly including

transportation and municipal projects) will be more than Rmb2trn in 2017-18

(vs. our previous estimates of Rmb1.65trn), representing a 35% CAGR over

2016-2018.

Our blue sky scenario (our assumption: PPP projects could enter

implementation period in the next 2.5 years) suggests 2% and 9% potential

upside from our current estimates for infra FAI and investment for PPP

projects, respectively, which should enhance the constructors’ earnings by

5-10%.

In addition, there is upside risk to our estimates on infra investment as we

assume current reserved PPP projects (amounting to Rmb13.5trn) in the MoF’s

pool would enter implementation period and no additional PPP projects from

the beginning of this year.

Figure 15: DB assumption on China infrastructure spending (base case)

Rmbm 2013 2014 2015 2016E 2017E 2018E 2019E

Railway 532,770 622,300 659,638 676,129 676,129 608,516 547,664

yoy change 17% 6% 3% 0% -10% -10%

Road 1,369,220 1,546,094 1,651,330 1,778,740 1,912,146 2,007,753 2,007,753

yoy change 13% 7% 8% 8% 5% 0%

Water and others 184,097 171,057 190,770 189,396 189,396 189,396 189,396

yoy change -7% 12% -1% 0% 0% 0%

Municipal (including Urban transit)

2,383,950 2,335,990 2,303,220 2,455,211 2,633,032 2,829,656 3,018,318

yoy change -2% -1% 7% 7% 7% 7%

Total 4,285,940 4,675,441 4,804,958 5,099,476 5,410,703 5,635,320 5,763,131

yoy change 9.1% 2.8% 6.1% 6.1% 4.2% 2.3%

Investment business 342,875 420,790 480,496 626,588 905,280 1,146,145 1,300,681

yoy change 23% 14% 30% 44% 27% 13%

% of total 8% 9% 10% 12% 17% 20% 23%

Cash construction 3,943,065 4,254,652 4,324,462 4,472,888 4,505,423 4,489,176 4,462,450

yoy change 8% 2% 3% 0.7% -0.4% -1%

% of total 92% 91% 90% 88% 83% 80% 77%

Our assumption: PPP projects could be entered into implementation period in the next 3 years Source: Deutsche Bank. CRC, MoT, MOHURD

3 March 2017

Infrastructure

China Infrastructure

Page 8 Deutsche Bank AG/Hong Kong

Figure 16: DB assumption on China infrastructure spending (worst case)

Rmbm 2013 2014 2015 2016E 2017E 2018E 2019E

Railway 532,770 622,300 659,638 676,129 675,890 606,232 541,361

yoy change 17% 6% 3% 0% -10% -11%

Road 1,369,220 1,546,094 1,651,330 1,778,740 1,902,432 1,963,555 1,924,193

yoy change 13% 7% 8% 7% 3% -2%

Water and others 184,097 171,057 190,770 189,396 189,396 189,396 189,396

yoy change -7% 12% -1% 0% 0% 0%

Municipal (including Urban transit)

2,383,950 2,335,990 2,303,220 2,455,211 2,625,489 2,791,656 2,940,371

yoy change -2% -1% 7% 7% 6% 5%

Total 4,470,037 4,675,441 4,804,958 5,099,476 5,393,207 5,550,838 5,595,321

yoy change 4.6% 2.8% 6.1% 5.8% 2.9% 0.8%

Investment business 357,603 420,790 480,496 626,588 886,207 1,057,030 1,127,243

yoy change 18% 14% 30% 41% 19% 7%

% of total 8% 9% 10% 12% 16% 19% 20%

Cash construction 4,112,434 4,254,651 4,324,462 4,472,888 4,507,000 4,493,808 4,468,078

yoy change 3% 2% 3% 1% 0% -1%

% of total 92% 91% 90% 88% 84% 81% 80% Our assumption: PPP projects could be entered into implementation period in the next 3.5 years Source: Deutsche Bank, CRC, MoT, MOHURD

Figure 17: DB assumption on China infrastructure spending (best case)

Rmbm 2013 2014 2015 2016E 2017E 2018E 2019E

Railway 532,770 622,300 659,638 676,129 676,368 610,872 550,020

yoy change 17% 6% 3% 0% -10% -10%

Road 1,369,220 1,546,094 1,651,330 1,778,740 1,944,182 2,101,104 2,101,300

yoy change 13% 7% 8% 9% 8% 0%

Water and others 184,097 171,057 190,770 189,396 189,396 189,396 189,396

yoy change -7% 12% -1% 0% 0% 0%

Municipal (including Urban transit)

2,383,950 2,335,990 2,303,220 2,455,211 2,640,575 2,869,919 3,061,525

yoy change -2% -1% 7% 8% 9% 7%

Total 4,470,037 4,675,441 4,804,958 5,099,476 5,450,521 5,771,291 5,902,241

yoy change 4.6% 2.8% 6.1% 6.9% 5.9% 2.3%

Investment business 357,603 420,790 480,496 626,588 948,646 1,289,570 1,447,625

yoy change 18% 14% 30% 51% 36% 12%

% of total 8% 9% 10% 12% 17% 22% 25%

Cash construction 4,112,434 4,254,651 4,324,462 4,472,888 4,501,875 4,481,721 4,454,615

yoy change 3% 2% 3% 1% 0% -1%

% of total 92% 91% 90% 88% 83% 78% 75%

Our assumption: PPP projects could be entered into implementation period in the next 2.5 years Source: Deutsche Bank, CRC, MoT, MOHURD

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 9

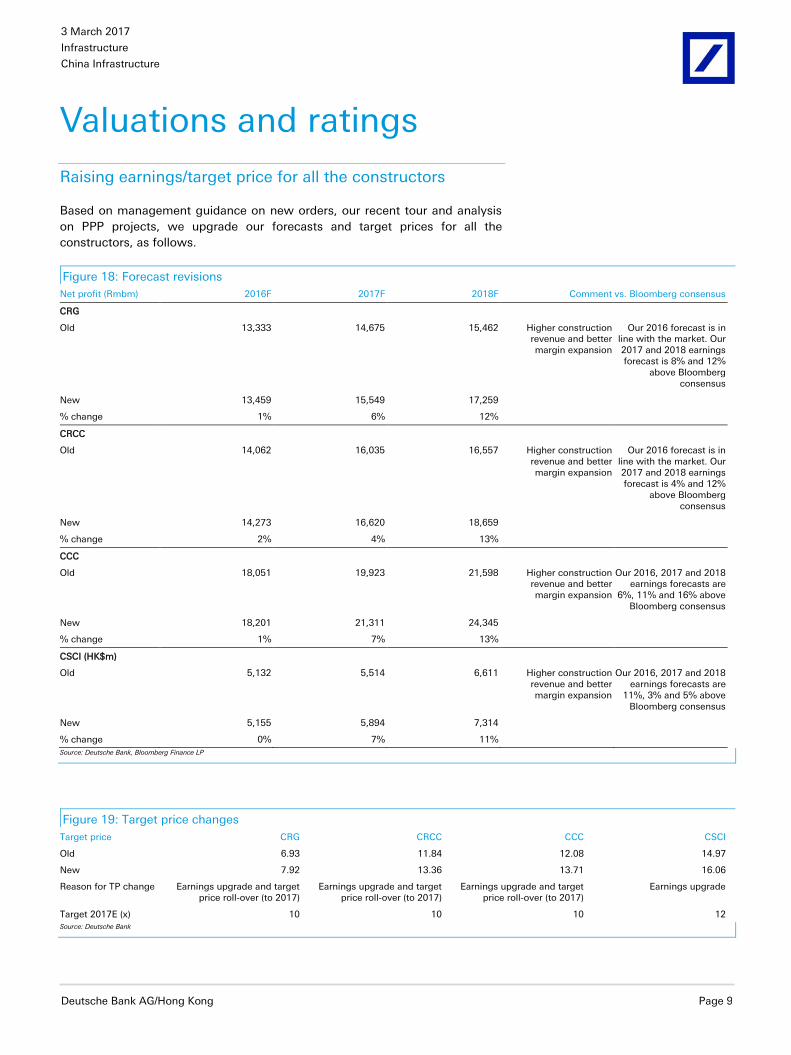

Valuations and ratings

Raising earnings/target price for all the constructors

Based on management guidance on new orders, our recent tour and analysis

on PPP projects, we upgrade our forecasts and target prices for all the

constructors, as follows.

Figure 18: Forecast revisions

Net profit (Rmbm) 2016F 2017F 2018F Comment vs. Bloomberg consensus

CRG

Old 13,333 14,675 15,462 Higher construction revenue and better margin expansion

Our 2016 forecast is in line with the market. Our 2017 and 2018 earnings forecast is 8% and 12%

above Bloomberg consensus

New 13,459 15,549 17,259

% change 1% 6% 12%

CRCC

Old 14,062 16,035 16,557 Higher construction revenue and better margin expansion

Our 2016 forecast is in line with the market. Our 2017 and 2018 earnings forecast is 4% and 12%

above Bloomberg consensus

New 14,273 16,620 18,659

% change 2% 4% 13%

CCC

Old 18,051 19,923 21,598 Higher construction revenue and better margin expansion

Our 2016, 2017 and 2018 earnings forecasts are

6%, 11% and 16% above Bloomberg consensus

New 18,201 21,311 24,345

% change 1% 7% 13%

CSCI (HK$m)

Old 5,132 5,514 6,611 Higher construction revenue and better margin expansion

Our 2016, 2017 and 2018 earnings forecasts are

11%, 3% and 5% above Bloomberg consensus

New 5,155 5,894 7,314

% change 0% 7% 11%

Source: Deutsche Bank, Bloomberg Finance LP

Figure 19: Target price changes

Target price CRG CRCC CCC CSCI

Old 6.93 11.84 12.08 14.97

New 7.92 13.36 13.71 16.06

Reason for TP change Earnings upgrade and target price roll-over (to 2017)

Earnings upgrade and target price roll-over (to 2017)

Earnings upgrade and target price roll-over (to 2017)

Earnings upgrade

Target 2017E (x) 10 10 10 12 Source: Deutsche Bank

3 March 2017

Infrastructure

China Infrastructure

Page 10 Deutsche Bank AG/Hong Kong

Figure 20: Valuation comparables

Stock name Stock code Rating TP (HK$)

Price (March 1)

Upside to TP

P/E (x) EPS growth

P/B (x) ROE (%)

Dividend yield (%)

new new old HK$ % FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY17E

CCC 1800.HK Buy 13.71 12.08 10.80 27% 9.4 7.9 6% 19% 1.0 0.9 11.3% 12.8% 2.6%

CSCI 3311.HK Buy 16.06 14.97 13.20 22% 13.4 10.1 -4% 34% 2.0 1.8 20.3% 18.6% 3.0%

CRCC 1186.HK Buy 13.36 11.84 11.36 18% 9.6 8.2 7% 16% 1.1 1.0 12.1% 12.7% 1.9%

CRG 390.HK Buy 7.94 6.93 7.11 12% 10.7 9.3 11% 15% 1.1 1.0 11.0% 11.7% 1.8%

Source: Deutsche Bank, Bloomberg Finance LP, Company data

2016 earnings preview

All the construction companies under our coverage are scheduled to release

2016 results in mid- to end-March 2017. We forecast CRG, CCC, CRCC and

CSCI’s 2016 core earnings to increase 15%, 15%, 13% and 1% yoy,

respectively. Our earnings estimate for CCC and CSCI is 6% and 11% ahead of

market consensus. Our forecasts for the other two names are largely in line

with market expectations.

Figure 21: 2016 earnings calendar

Ticker 2016 result date

CRG 390.HK 30-Mar-2017

CRCC 1186.HK 30-Mar-2017

CCC 1800.HK 28-Mar-2017

CSCI 3311.HK 21-Mar-2017 Source: Company data

Our top picks – CCC and CSCI

CCC (1800.HK, Buy, target price HK$13.71)

Investment thesis

CCC is a leading state-owned company, engaged primarily in infrastructure

construction (mainly ports, roads, bridges, and railways), dredging, port

machinery, and road/bridge/port design. CCC is our top pick in the sector

mainly due to the following reasons.

1) In our opinion, CCC is the largest prospective beneficiary from the

OBOR plan in the medium term.

2) It has the highest exposure to investment business among big three

constructors. PPP projects account for 21% of CCC’s new orders in

2016, vs. 14-17% for CRG and CRCC.

3) It has strong capability to control overseas and investment-business

projects considering its good track record.

4) Potential SOE reforms may benefit its B/S. We believe it is possible for

CCC to introduce forecast strategic investors and optimize its business

this year.

5) CCC is trading at 8x 2017E PE, at a 4% and 15% discount to CRCC

and CRG’s, respectively.

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 11

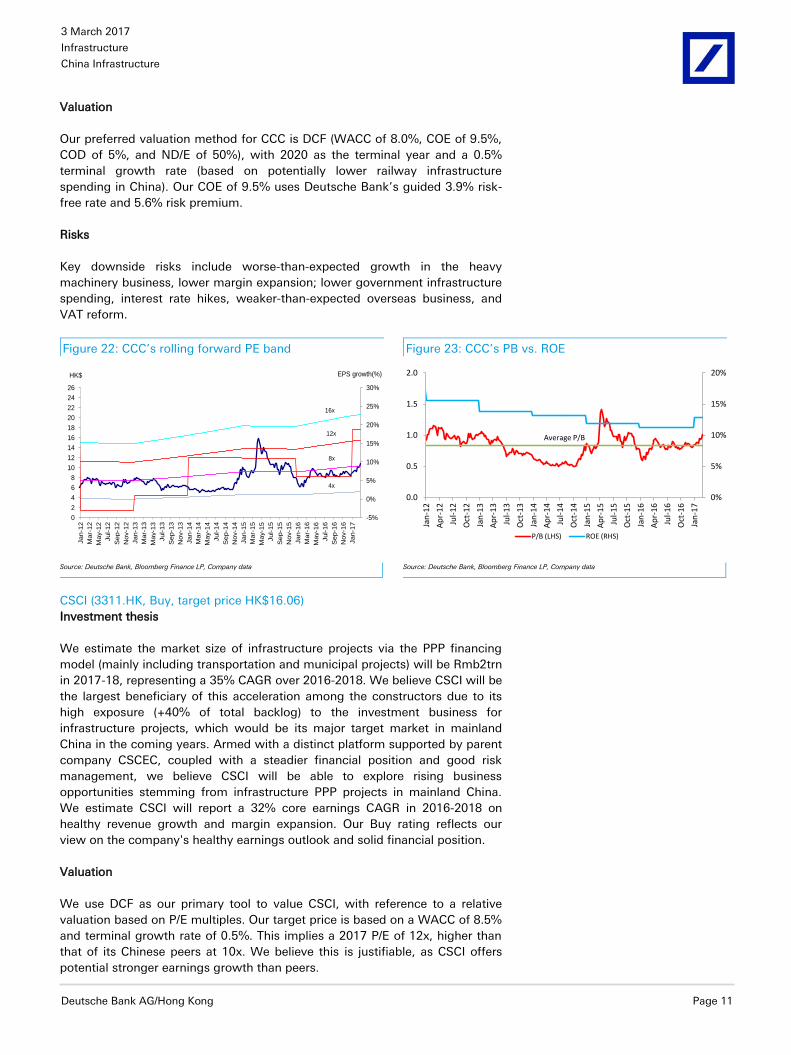

Valuation

Our preferred valuation method for CCC is DCF (WACC of 8.0%, COE of 9.5%,

COD of 5%, and ND/E of 50%), with 2020 as the terminal year and a 0.5%

terminal growth rate (based on potentially lower railway infrastructure

spending in China). Our COE of 9.5% uses Deutsche Bank’s guided 3.9% risk-

free rate and 5.6% risk premium.

Risks

Key downside risks include worse-than-expected growth in the heavy

machinery business, lower margin expansion; lower government infrastructure

spending, interest rate hikes, weaker-than-expected overseas business, and

VAT reform.

Figure 22: CCC’s rolling forward PE band Figure 23: CCC’s PB vs. ROE

-5%

0%

5%

10%

15%

20%

25%

30%

0

2

4

6

8

10

12

14

16

18

20

22

24

26

Ja

n-1

2

Mar-

12

May-1

2

Ju

l-12

Se

p-1

2

No

v-1

2

Ja

n-1

3

Mar-

13

May-1

3

Ju

l-13

Se

p-1

3

No

v-1

3

Ja

n-1

4

Mar-

14

May-1

4

Ju

l-14

Se

p-1

4

No

v-1

4

Ja

n-1

5

Mar-

15

May-1

5

Ju

l-15

Se

p-1

5

No

v-1

5

Ja

n-1

6

Mar-

16

May-1

6

Jul-16

Se

p-1

6

Nov-1

6

Ja

n-1

7

EPS growth(%)HK$

16x

8x

12x

4x

0%

5%

10%

15%

20%

0.0

0.5

1.0

1.5

2.0

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Average P/B

P/B (LHS) ROE (RHS)

Source: Deutsche Bank, Bloomberg Finance LP, Company data

Source: Deutsche Bank, Bloomberg Finance LP, Company data

CSCI (3311.HK, Buy, target price HK$16.06)

Investment thesis

We estimate the market size of infrastructure projects via the PPP financing

model (mainly including transportation and municipal projects) will be Rmb2trn

in 2017-18, representing a 35% CAGR over 2016-2018. We believe CSCI will be

the largest beneficiary of this acceleration among the constructors due to its

high exposure (+40% of total backlog) to the investment business for

infrastructure projects, which would be its major target market in mainland

China in the coming years. Armed with a distinct platform supported by parent

company CSCEC, coupled with a steadier financial position and good risk

management, we believe CSCI will be able to explore rising business

opportunities stemming from infrastructure PPP projects in mainland China.

We estimate CSCI will report a 32% core earnings CAGR in 2016-2018 on

healthy revenue growth and margin expansion. Our Buy rating reflects our

view on the company's healthy earnings outlook and solid financial position.

Valuation

We use DCF as our primary tool to value CSCI, with reference to a relative

valuation based on P/E multiples. Our target price is based on a WACC of 8.5%

and terminal growth rate of 0.5%. This implies a 2017 P/E of 12x, higher than

that of its Chinese peers at 10x. We believe this is justifiable, as CSCI offers

potential stronger earnings growth than peers.

3 March 2017

Infrastructure

China Infrastructure

Page 12 Deutsche Bank AG/Hong Kong

Risks

Key down risks include: 1) slower-than-expected promotion of PPP model; 2)

lower-government spending in public housing and infrastructure projects; 3) a

sharp increase in raw materials prices; and 4) worse-than-expected margin

performance.

Figure 24: CSCI’s rolling forward PE band Figure 25: CSCI’s PB vs. ROE

8x

4x

12x

16x

20x

-10%

0%

10%

20%

30%

40%

50%

0

5

10

15

20

25

30

35

Jan

-12

Ap

r-12

Jul-

12

Oct

-12

Jan

-13

Ap

r-13

Jul-

13

Oct

-13

Jan

-14

Ap

r-14

Jul-

14

Oct

-14

Jan

-15

Ap

r-15

Jul-

15

Oct

-15

Jan

-16

Ap

r-16

Jul-

16

Oct

-16

Jan

-17

EPS growth (%)HK$

Average P/B

0%

5%

10%

15%

20%

25%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Jan

-12

Ap

r-12

Jul-

12

Oct

-12

Jan

-13

Ap

r-13

Jul-

13

Oct

-13

Jan

-14

Ap

r-14

Jul-

14

Oct

-14

Jan

-15

Ap

r-15

Jul-

15

Oct

-15

Jan

-16

Ap

r-16

Jul-

16

Oct

-16

Jan

-17

P/B (LHS) ROE (RHS)

Source: Deutsche Bank, Bloomberg Finance LP, Company data

Source: Deutsche Bank, Bloomberg Finance LP, Company data

Other Names:

China Railway Group (0390.HK) Valuation:

Our preferred valuation method for CRG is DCF (WACC of 7.4%, COE of 9.3%, COD

of 5.0% and ND/E of 50%), with 2020 as the terminal year and 0.5% terminal

growth (average growth rate for the companies in the sector). Our COE of 9.3%

uses Deutsche Bank's guided 3.9% risk-free rate and 5.6% risk premium. Our target

price implies PEs of 10x for 2017E.

Risks:

Downside risks: rising raw material costs; slowdown in the property market;

political instability overseas; and lower margin performance.

China Rail Construction (1186.HK) Valuation

Our preferred valuation methodology for CRCC is a DCF valuation (WACC of 7.0%,

COE of 8.7%, COD of 5.0% and ND/E of 30%), with 2020 being the terminal year,

and terminal growth of 0.5% (average growth rate for the companies in the sector).

Our COE of 8.7% uses Deutsche Bank's guided 3.9% risk-free rate and 5.6% risk

premium. Our target price implies a PE of 10x for 2017E.

Risks

Downside risks: lower infrastructure capex; political instability overseas; rising raw

material costs; margin performance; weaker overseas demand; and VAT reform.

Ch

ina In

frastru

ctu

re

Infra

structu

re

3 M

arc

h 2

017

Deu

tsch

e B

an

k A

G/H

on

g K

on

g

Pag

e 1

3

Figure 26: Infrastructure construction – peer valuation

Company Name Bloomberg Curr DB rating

Price Market Cap

Avg trading

value

P/E (X) EPS Chg(%)

P/B (X) ROE (%)

March 1, 2017 Ticker (local) (US$ m) (US$ m) FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E

Chinese construction competitors

China Railway Group * 390 HK HK$ Buy 7.11 28,450 19 10.7 9.2 8.3 12% 16% 11% 1.1 1.0 0.9 11.0 11.7 11.8

China Railway Construction * 1186 HK HK$ Buy 11.36 25,225 22 9.6 8.2 7.3 7% 16% 12% 1.1 1.0 0.9 12.1 12.7 12.8

China Communications Construction * 1800 HK HK$ Buy 10.80 36,996 36 9.4 7.9 6.8 6% 19% 16% 1.1 1.0 0.9 12.5 13.9 14.3

China State Construction Int'l * 3311 HK HK$ Buy 13.20 7,632 17 13.4 10.1 8.1 -4% 34% 24% 2.0 1.8 1.5 20.2 18.6 20.2

China Machinery Engineering 1829 HK HK$ n/a 5.62 2,987 5 10.7 9.9 9.4 -15% 7% 5% 1.3 1.2 1.1 13.1 13.1 12.9

China Oilfield Services Limited 601808.SH Rmb n/a 13.43 7,585 13 n/a n/a 57.6 n/a n/a 497% 1.8 1.8 1.7 (23.1) (0.0) 3.1

Offshore Oil Engineering 600583.SH Rmb n/a 8.02 5,202 34 21.4 20.4 16.2 -51% 5% 26% 1.5 1.4 1.3 6.0 6.3 8.0

China Gezhouba Group 600068.SH Rmb n/a 11.01 7,396 114 15.4 12.4 9.9 23% 24% 25% 2.3 2.0 1.7 15.2 16.6 17.3

Sinoma International Engineering 600970.SH Rmb n/a 7.89 2,031 25 16.6 13.7 11.8 -21% 21% 16% 1.5 1.4 1.3 11.8 13.1 13.8

Shanghai Construction 600170.SH Rmb n/a 5.04 5,546 49 17.1 15.3 14.0 -5% 12% 9% 1.5 1.4 1.3 9.4 9.7 10.0

Shanghai Tunnel Engineering 600820.SH Rmb n/a 11.70 5,361 72 21.7 18.6 15.9 15% 16% 17% 2.0 1.9 1.7 9.5 10.1 10.4

Shanghai Pudong Road & Bridge Construction

600284.SH Rmb n/a 12.89 1,300 24 35.8 36.8 n/a -34% -3% n/a 1.7 1.6 1.5 8.6 9.4 9.5

Simple average for Chinese peers 16.5 14.8 15.0 -6% 15% 60% 1.6 1.4 1.3 8.9 11.3 12.0

Simple average for Chinese peers (listed on HK market)

10.7 9.1 8.0 1% 18% 14% 1.3 1.2 1.1 13.8 14.0 14.4

Regional construction competitors

Shimizu Corporation * 1803 JP JPY Hold 1,045.00 7,315 25 13.1 10.7 12.4 78% 29% -14% 1.6 1.5 1.4 12.4 15.0 11.7

KAJIMA Corporation * 1812 JP JPY Hold 738.00 6,880 39 9.2 8.6 9.3 378% 23% -7% 1.6 1.4 1.2 16.0 17.5 14.2

Hyundai Engineering&Construction 000720 KS KRW n/a 47,800.00 4,743 18 11.9 9.5 9.1 22% 25% 5% 0.9 0.8 0.7 7.6 8.7 8.6

Daewoo Engineering & Construction 047040 KS KRW n/a 6,130.00 2,250 5 21.9 7.9 7.8 -20% 177% 1% 0.9 1.0 0.9 4.2 14.4 12.4

GS E&C 006360 KS KRW n/a 29,800.00 1,900 10 64.9 9.8 7.7 26% 562% 28% 0.6 0.6 0.5 1.3 6.5 7.7

Hyundai Dev. Co. 012630 KS KRW n/a 43,800.00 2,938 13 9.5 8.0 7.9 56% 20% 1% 1.2 1.1 1.0 13.9 14.8 13.4

Samsung Eng. 028050 KS KRW n/a 12,400.00 2,219 19 33.3 16.8 13.3 n/a 98% 26% 2.2 2.1 1.8 16.8 12.7 15.5

Daelim Industrial 000210 KS KRW n/a 83,600.00 2,605 11 8.9 7.6 7.4 76% 17% 3% 0.7 0.6 0.6 7.7 8.4 8.0

Sino-Thai Engineering STEC TB THB n/a 25.50 1,123 6 37.6 28.5 22.1 -32% 32% 29% 3.9 3.5 3.2 10.9 12.7 14.9

Larsen & Toubro Ltd * LT IN INR Hold 1,469.20 20,651 34 32.4 23.5 22.9 -9% 32% 10% 2.6 2.9 2.7 10.0 12.8 12.3

BHEL * BHEL IN INR Buy 162.45 5,881 21 n/a 49.7 27.0 n/a n/a 84% 0.8 1.2 1.1 (2.7) 2.4 4.3

Gamuda GAM MK MYR n/a 4.95 2,705 4 19.7 17.6 15.7 -13% 12% 12% 1.8 1.6 1.5 9.6 10.0 10.5

IJM Corp IJM MK MYR n/a 3.35 2,734 3 19.0 19.9 17.0 -46% -5% 17% 1.3 1.3 1.2 7.5 6.7 7.6

Simple average for regional peers 23.5 16.8 13.8 47% 85% 15% 1.6 1.5 1.4 8.9 11.0 10.9

Source: Deutsche Bank estimates for companies with”*”, Bloomberg Finance LP estimates for all others

Ch

ina In

frastru

ctu

re

Infra

structu

re

3 M

arc

h 2

017

Pag

e 1

4

Deu

tsch

e B

an

k A

G/H

on

g K

on

g

Figure 27: Infrastructure construction – peer valuation (continued)

Company Name Bloomberg Curr DB rating Price Market Cap

Ave trading value

P/E (x) (F)

EPS chg

(%) (F)

P/B (x) ROE (%)

March 1, 2017 Ticker (local) (US$ m) (US$ m) FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E FY16E FY17E FY18E

Europe and US construction competitors

VINCI SA DG FP EUR n/a 68.01 43,390 99 16.5 14.8 13.7 12% 11% 8% 2.4 2.2 2.0 14.7 15.0 14.9

Bouygues SA EN FP EUR n/a 36.37 13,889 32 19.8 16.8 15.0 54% 18% 12% 1.6 1.6 1.6 5.8 9.3 10.7

EIFFAGE SA FGR FP EUR n/a 67.42 7,100 19 16.2 14.0 12.2 22% 15% 15% 1.8 1.7 1.5 11.7 12.1 12.7

ACCIONA S.A.* ANA SM EUR Buy 70.67 4,288 11 11.0 13.7 11.8 -35% 103% 16% 1.1 1.1 1.0 9.8 7.9 8.8

STRABAG SE * STR AV EUR Hold 35.10 4,222 0 16.0 15.4 15.1 29% 4% 2% 1.2 1.1 1.1 7.5 7.5 7.3

Skanska AB SKAB SS SEK n/a 215.20 10,151 27 14.5 15.9 16.9 27% -9% -6% 3.3 3.0 27.3 24.0 19.3 17.9

NCC AB NCCB SS SEK n/a 214.70 2,588 8 20.4 14.8 14.1 -46% 37% 5% 4.0 3.7 31.7 18.4 26.5 25.0

Fluor Corporation * FLR US USD Buy 55.39 7,892 81 25.3 18.5 16.5 -29% 50% 12% 2.3 2.3 2.1 9.2 12.9 13.2

Jacobs Engineering * JEC US USD Hold 56.41 6,966 54 26.1 21.1 16.2 -6% -2% 16% 1.5 1.5 1.4 4.9 7.4 9.0

Enka Insaat * ENKAI TI TRY Hold 5.64 6,633 5 12.5 12.0 11.6 1% 4% 4% 1.2 1.1 1.1 10.0 9.7 9.4

Simple average for international peers 17.8 15.7 14.3 3% 23% 8% 2.0 1.9 7.1 11.6 13.1 13.3

Overall average 19.4 15.8 14.4 15% 43% 28% 1.7 1.6 3.0 9.6 11.6 11.8

Source: Deutsche Bank estimates for companies with”*”, Bloomberg Finance LP estimates for all others

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 15

Model updated:02 March 2017

Running the numbers

Asia

China

Infrastructure

China Comms Construct Reuters: 1800.HK Bloomberg: 1800 HK

Buy Price (2 Mar 17) HKD 10.78

Target Price HKD 13.71

52 Week range HKD 7.55 - 10.80

Market Cap (m) HKDm 174,364

USDm 22,460

Company Profile

CCC is a leading state-owned company, engaged primarily in infrastructure construction (mainly ports/roads/bridges/railways), dredging, port machinery, and road/bridge/port design. CCC is the third-largest railway construction company in China and the the largest dredging company, with a 70-80% market share. It conducts a port machinery manufacturing business through SZHI, which is the largest container crane producer in the world.

Price Performance

4

8

12

16

20

Mar 15Jun 15Sep 15Dec 15Mar 16Jun 16Sep 16Dec 16

China Comms ConstructHANG SENG INDEX (Rebased)

Margin Trends

6.0

7.0

8.0

9.0

10.0

14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

1011111212131314

02468

101214

14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

01234567

0

50

100

150

14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

Phyllis Wang

- - - [email protected]

Fiscal year end 31-Dec 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (CNY) 0.86 0.96 1.02 1.21 1.40

Reported EPS (CNY) 0.86 0.96 1.02 1.21 1.40

DPS (CNY) 0.17 0.19 0.20 0.24 0.28

BVPS (CNY) 7.2 9.1 9.0 10.0 11.1

Weighted average shares (m) 16,175 16,175 16,175 16,175 16,175

Average market cap (CNYm) 76,212 138,594 154,510 154,510 154,510

Enterprise value (CNYm) 232,358 305,393 357,458 393,657 432,680

Valuation Metrics P/E (DB) (x) 5.4 8.9 9.4 7.9 6.8

P/E (Reported) (x) 5.4 8.9 9.4 7.9 6.8

P/BV (x) 1.03 0.71 1.06 0.96 0.86

FCF Yield (%) nm nm nm nm nm

Dividend Yield (%) 3.6 2.2 2.1 2.5 2.9

EV/Sales (x) 0.6 0.8 0.8 0.9 0.8

EV/EBITDA (x) 7.3 8.8 9.3 8.9 8.7

EV/EBIT (x) 9.8 11.8 12.5 11.8 11.4

Income Statement (CNYm)

Sales revenue 366,042 403,616 423,592 462,569 520,139

Gross profit 47,163 58,551 63,290 71,031 80,223

EBITDA 31,676 34,595 38,601 44,223 49,954

Depreciation 7,211 7,839 8,712 9,584 10,457

Amortisation 680 958 1,182 1,369 1,549

EBIT 23,785 25,798 28,707 33,270 37,948

Net interest income(expense) -6,520 -6,511 -4,895 -5,325 -5,968

Associates/affiliates 339 384 384 384 384

Exceptionals/extraordinaries 0 0 0 0 0

Other pre-tax income/(expense) 0 0 0 0 0

Profit before tax 17,604 19,671 24,196 28,329 32,364

Income tax expense 3,721 3,758 5,897 6,904 7,887

Minorities -102 85 98 114 131

Other post-tax income/(expense) 0 -300 -1,736 -1,736 -1,736

Net profit 13,985 15,528 16,465 19,575 22,609

DB adjustments (including dilution) 0 0 0 0 0

DB Net profit 13,985 15,528 16,465 19,575 22,609

Cash Flow (CNYm)

Cash flow from operations -6,256 18,465 3,120 4,360 2,153

Net Capex -42,255 -51,267 -34,555 -35,210 -35,210

Free cash flow -48,511 -32,802 -31,435 -30,850 -33,057

Equity raised/(bought back) 0 0 0 0 0

Dividends paid -3,116 -3,195 -3,265 -3,882 -4,483

Net inc/(dec) in borrowings 38,246 26,862 0 10,000 15,000

Other investing/financing cash flows 4,085 31,999 -1,736 -1,736 -1,736

Net cash flow -9,296 22,864 -36,436 -26,468 -24,276

Change in working capital -20,650 17,505 -24,688 -27,634 -33,945

Balance Sheet (CNYm)

Cash and other liquid assets 78,040 98,077 61,641 35,173 10,897

Tangible fixed assets 63,377 67,973 61,227 58,842 55,585

Goodwill/intangible assets 90,378 141,345 158,258 184,899 211,360

Associates/investments 9,730 12,589 12,973 13,357 13,741

Other assets 388,655 411,329 449,075 502,526 575,986

Total assets 630,180 731,313 743,173 794,798 867,570

Interest bearing debt 228,835 255,183 255,183 265,183 280,183

Other liabilities 269,733 307,124 320,181 345,998 385,514

Total liabilities 498,568 562,307 575,364 611,181 665,697

Shareholders' equity 116,531 146,724 145,429 161,122 179,248

Minorities 15,081 22,282 22,380 22,494 22,625

Total shareholders' equity 131,612 169,006 167,809 183,617 201,873

Net debt 150,795 157,106 193,542 230,010 269,286

Key Company Metrics

Sales growth (%) nm 10.3 4.9 9.2 12.4

DB EPS growth (%) na 11.0 6.0 18.9 15.5

EBITDA Margin (%) 8.7 8.6 9.1 9.6 9.6

EBIT Margin (%) 6.5 6.4 6.8 7.2 7.3

Payout ratio (%) 19.9 19.8 19.8 19.8 19.8

ROE (%) 13.2 11.8 11.3 12.8 13.3

Capex/sales (%) 11.7 12.9 8.8 7.6 6.8

Capex/depreciation (x) 5.4 5.9 3.8 3.2 2.9

Net debt/equity (%) 114.6 93.0 115.3 125.3 133.4

Net interest cover (x) 3.6 4.0 5.9 6.2 6.4

Source: Company data, Deutsche Bank estimates

3 March 2017

Infrastructure

China Infrastructure

Page 16 Deutsche Bank AG/Hong Kong

Model updated:02 March 2017

Running the numbers

Asia

China

Property

CSCI Reuters: 3311.HK Bloomberg: 3311 HK

Buy Price (2 Mar 17) HKD 13.40

Target Price HKD 16.06

52 Week range HKD 9.12 - 13.52

Market Cap (m) HKDm 60,141

USDm 7,747

Company Profile

China State Construction International Holdings Limited began operations in Hong Kong in 1979. It engages in housing/infrastructure construction and civil engineering operations as well as other peripheral operations such as foundation work, site investigation, mechanical and electrical engineering, highway and bridge construction, ready-mixed concrete, pre-cast production and infrastructure investment. China State Construction was listed on the Main Board of The Hong Kong Stock Exchange in July 2005.

Price Performance

8

9

11

12

14

15

17

Mar 15Jun 15Sep 15Dec 15Mar 16Jun 16Sep 16Dec 16

CSCI HANG SENG INDEX (Rebased)

Margin Trends

10.0

11.0

12.0

13.0

14.0

15.0

14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

18

18

19

19

20

20

21

0

5

10

15

20

25

14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

0

5

10

15

20

0

10

20

30

40

50

14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

Phyllis Wang

- - - [email protected]

Fiscal year end 31-Dec 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (HKD) 0.88 1.02 0.98 1.31 1.63

Reported EPS (HKD) 0.88 1.02 1.21 1.31 1.63

DPS (HKD) 0.26 0.33 0.36 0.39 0.49

BVPS (HKD) 4.9 5.2 6.6 7.5 8.6

Weighted average shares (m) 3,896 4,026 4,272 4,488 4,488

Average market cap (HKDm) 49,755 48,730 60,141 60,141 60,141

Enterprise value (HKDm) 51,282 50,976 57,749 59,232 60,802

Valuation Metrics P/E (DB) (x) 14.6 11.8 13.6 10.2 8.2

P/E (Reported) (x) 14.6 11.8 11.1 10.2 8.2

P/BV (x) 2.21 2.58 2.03 1.79 1.55

FCF Yield (%) nm nm 2.0 nm nm

Dividend Yield (%) 2.0 2.7 2.7 2.9 3.6

EV/Sales (x) 1.5 1.3 1.2 1.1 1.0

EV/EBITDA (x) 12.6 11.5 11.0 8.4 7.1

EV/EBIT (x) 13.7 12.4 11.8 8.9 7.4

Income Statement (HKDm)

Sales revenue 34,440 37,913 46,491 54,004 61,340

Gross profit 5,063 5,362 6,563 8,523 10,291

EBITDA 4,074 4,439 5,248 7,044 8,609

Depreciation 320 332 362 392 423

Amortisation 0 0 0 0 0

EBIT 3,754 4,107 4,886 6,652 8,186

Net interest income(expense) -301 -405 -426 -416 -467

Associates/affiliates 318 496 651 900 1,246

Exceptionals/extraordinaries 0 0 0 0 0

Other pre-tax income/(expense) 277 558 1,010 22 27

Profit before tax 4,048 4,756 6,121 7,158 8,992

Income tax expense 660 655 979 1,253 1,663

Minorities -70 -51 -13 12 15

Other post-tax income/(expense) 0 0 0 0 0

Net profit 3,457 4,153 5,155 5,894 7,314

DB adjustments (including dilution) 0 0 -953 0 0

DB Net profit 3,457 4,153 4,202 5,894 7,314

Cash Flow (HKDm)

Cash flow from operations -1,674 316 1,568 247 295

Net Capex -476 -393 -425 -425 -425

Free cash flow -2,150 -77 1,143 -178 -130

Equity raised/(bought back) 1 10 4,810 0 0

Dividends paid -901 -1,216 -1,547 -1,768 -2,194

Net inc/(dec) in borrowings 4,740 3,114 474 0 0

Other investing/financing cash flows -2,346 -1,320 -433 -425 -478

Net cash flow -656 510 4,447 -2,371 -2,802

Change in working capital -5,461 -3,958 -3,711 -5,567 -6,677

Balance Sheet (HKDm)

Cash and other liquid assets 7,452 8,015 12,462 10,092 7,290

Tangible fixed assets 2,827 2,772 2,835 2,867 2,870

Goodwill/intangible assets 0 0 0 0 0

Associates/investments 6,007 7,613 8,265 9,165 10,411

Other assets 50,292 51,664 61,534 71,997 83,554

Total assets 66,579 70,065 85,096 94,120 104,125

Interest bearing debt 14,820 17,774 18,248 18,248 18,248

Other liabilities 31,762 31,043 37,196 42,083 46,953

Total liabilities 46,581 48,818 55,444 60,331 65,201

Shareholders' equity 19,830 21,147 29,565 33,691 38,810

Minorities 168 100 87 99 114

Total shareholders' equity 19,998 21,247 29,652 33,790 38,924

Net debt 7,367 9,759 5,786 8,156 10,958

Key Company Metrics

Sales growth (%) nm 10.1 22.6 16.2 13.6

DB EPS growth (%) na 16.8 -3.8 33.5 24.1

EBITDA Margin (%) 11.8 11.7 11.3 13.0 14.0

EBIT Margin (%) 10.9 10.8 10.5 12.3 13.3

Payout ratio (%) 29.3 32.0 30.0 30.0 30.0

ROE (%) 19.2 20.3 20.3 18.6 20.2

Capex/sales (%) 1.5 1.1 0.9 0.8 0.7

Capex/depreciation (x) 1.6 1.3 1.2 1.1 1.0

Net debt/equity (%) 36.8 45.9 19.5 24.1 28.2

Net interest cover (x) 12.5 10.1 11.5 16.0 17.5

Source: Company data, Deutsche Bank estimates

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 17

Model updated:01 March 2017

Running the numbers

Asia

China

Infrastructure

China Rail Construction Reuters: 1186.HK Bloomberg: 1186 HK

Buy Price (2 Mar 17) HKD 11.20

Target Price HKD 13.36

52 Week range HKD 7.89 - 11.72

Market Cap (m) HKDm 138,180

USDm 17,800

Company Profile

CRCC is the largest railway construction company in China in terms of 2015 new contract wins. It is an integrated construction group that encompasses infrastructure construction, survey, design and consulting services, engineering equipment and component manufacturing, property development and other businesses. Its subsidiary CRCCE, with major business of manufacturing of large railway maintenance machinery, has been listed on Hong Kong Exchange since December 2015.

Price Performance

4

8

12

16

20

Mar 15Jun 15Sep 15Dec 15Mar 16Jun 16Sep 16Dec 16

China Rail ConstructionHANG SENG INDEX (Rebased)

Margin Trends

3.0

4.0

5.0

6.0

7.0

14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

11

12

12

13

13

14

14

0

2

4

6

8

10

14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

0

2

4

6

8

10

12

010203040506070

14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

Phyllis Wang

- - - [email protected]

Fiscal year end 31-Dec 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (CNY) 0.95 0.98 1.05 1.22 1.37

Reported EPS (CNY) 0.95 0.98 1.05 1.22 1.37

DPS (CNY) 0.15 0.15 0.17 0.19 0.22

BVPS (CNY) 7.5 8.2 9.1 10.1 11.3

Weighted average shares (m) 12,338 12,855 13,580 13,580 13,580

Average market cap (CNYm) 71,846 118,968 122,447 122,447 122,447

Enterprise value (CNYm) 140,729 162,101 169,205 172,871 176,028

Valuation Metrics P/E (DB) (x) 6.1 9.4 9.4 8.1 7.2

P/E (Reported) (x) 6.1 9.4 9.4 8.1 7.2

P/BV (x) 1.04 0.95 1.09 0.98 0.88

FCF Yield (%) nm 17.3 nm nm 0.6

Dividend Yield (%) 2.6 1.6 1.7 1.9 2.2

EV/Sales (x) 0.2 0.3 0.3 0.3 0.2

EV/EBITDA (x) 4.6 5.0 4.9 4.4 4.1

EV/EBIT (x) 7.1 7.6 7.4 6.6 6.1

Income Statement (CNYm)

Sales revenue 575,260 582,522 602,289 650,356 708,295

Gross profit 57,505 61,780 64,516 71,231 78,110

EBITDA 30,524 32,416 34,758 39,098 43,114

Depreciation 10,444 10,828 11,644 12,614 13,585

Amortisation 176 186 282 383 484

EBIT 19,904 21,402 22,832 26,100 29,045

Net interest income(expense) -4,460 -3,741 -2,692 -2,742 -2,786

Associates/affiliates 27 3 3 3 3

Exceptionals/extraordinaries 91 -644 -883 -918 -1,055

Other pre-tax income/(expense) -29 93 93 93 93

Profit before tax 15,532 17,113 19,354 22,537 25,300

Income tax expense 3,472 3,739 4,258 4,958 5,566

Minorities 325 729 823 958 1,076

Other post-tax income/(expense) 0 0 0 0 0

Net profit 11,735 12,645 14,273 16,620 18,659

DB adjustments (including dilution) 0 0 0 0 0

DB Net profit 11,735 12,645 14,273 16,620 18,659

Cash Flow (CNYm)

Cash flow from operations 733 46,508 23,413 23,877 24,825

Net Capex -20,467 -25,870 -24,060 -24,060 -24,060

Free cash flow -19,734 20,638 -647 -183 765

Equity raised/(bought back) 0 10,275 0 0 0

Dividends paid -2,002 -2,691 -2,251 -2,621 -2,943

Net inc/(dec) in borrowings 17,804 -2,012 0 0 0

Other investing/financing cash flows 8,555 -2,497 0 0 0

Net cash flow 4,623 23,713 -2,898 -2,804 -2,177

Change in working capital -19,407 18,178 -3,513 -6,603 -8,882

Balance Sheet (CNYm)

Cash and other liquid assets 98,407 121,934 119,036 116,232 114,055

Tangible fixed assets 44,450 45,004 42,161 38,346 33,561

Goodwill/intangible assets 17,216 30,758 45,735 60,612 75,388

Associates/investments 8,191 10,924 11,020 11,116 11,212

Other assets 455,303 487,477 504,574 543,296 591,646

Total assets 623,566 696,096 722,526 769,602 825,862

Interest bearing debt 163,065 158,837 158,837 158,837 158,837

Other liabilities 355,317 408,440 422,024 454,143 493,611

Total liabilities 518,383 567,277 580,861 612,980 652,448

Shareholders' equity 92,768 111,665 123,687 137,687 153,403

Minorities 12,415 17,154 17,977 18,935 20,011

Total shareholders' equity 105,183 128,819 141,664 156,622 173,413

Net debt 64,658 36,903 39,801 42,606 44,783

Key Company Metrics

Sales growth (%) nm 1.3 3.4 8.0 8.9

DB EPS growth (%) na 3.4 6.9 16.4 12.3

EBITDA Margin (%) 5.3 5.6 5.8 6.0 6.1

EBIT Margin (%) 3.5 3.7 3.8 4.0 4.1

Payout ratio (%) 15.8 15.2 15.8 15.8 15.8

ROE (%) 13.5 12.4 12.1 12.7 12.8

Capex/sales (%) 3.8 4.7 4.0 3.7 3.4

Capex/depreciation (x) 2.1 2.5 2.0 1.9 1.7

Net debt/equity (%) 61.5 28.6 28.1 27.2 25.8

Net interest cover (x) 4.5 5.7 8.5 9.5 10.4

Source: Company data, Deutsche Bank estimates

3 March 2017

Infrastructure

China Infrastructure

Page 18 Deutsche Bank AG/Hong Kong

Model updated:02 March 2017

Running the numbers

Asia

China

Infrastructure

China Railway Group Reuters: 0390.HK Bloomberg: 390 HK

Buy Price (2 Mar 17) HKD 7.16

Target Price HKD 7.92

52 Week range HKD 5.24 - 7.16

Market Cap (m) HKDm 152,507

USDm 19,645

Company Profile

CRG is the second largest railway construction company in China in terms of 2015 new contract value. CRG is an integrated construction group that encompasses infrastructure construction, survey, design and consulting services, engineering equipment and component manufacturing, property development and other businesses (such as mining and merchandise trading).

Price Performance

4

6

8

10

12

Mar 15Jun 15Sep 15Dec 15Mar 16Jun 16Sep 16Dec 16

China Railway GroupHANG SENG INDEX (Rebased)

Margin Trends

2.83.23.64.04.44.85.2

14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

10

11

11

12

12

0

2

4

6

8

10

14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

0

5

10

15

20

0

20

40

60

80

100

120

14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

Phyllis Wang

- - - [email protected]

Fiscal year end 31-Dec 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (CNY) 0.48 0.53 0.59 0.68 0.76

Reported EPS (CNY) 0.48 0.53 0.59 0.68 0.76

DPS (CNY) 0.08 0.09 0.10 0.11 0.12

BVPS (CNY) 4.5 5.4 5.5 6.1 6.7

Weighted average shares (m) 21,300 22,023 22,844 22,844 22,844

Average market cap (CNYm) 70,084 134,363 135,142 135,142 135,142

Enterprise value (CNYm) 173,891 218,765 222,292 226,077 228,803

Valuation Metrics P/E (DB) (x) 6.8 11.6 10.8 9.3 8.4

P/E (Reported) (x) 6.8 11.6 10.8 9.3 8.4

P/BV (x) 1.13 0.89 1.15 1.05 0.95

FCF Yield (%) 4.0 11.7 nm nm 0.3

Dividend Yield (%) 2.4 1.4 1.5 1.7 1.9

EV/Sales (x) 0.3 0.4 0.4 0.3 0.3

EV/EBITDA (x) 6.8 8.6 7.7 6.9 6.3

EV/EBIT (x) 9.3 12.1 10.7 9.4 8.6

Income Statement (CNYm)

Sales revenue 590,166 599,942 629,709 681,149 742,097

Gross profit 55,259 56,130 60,770 67,345 73,721

EBITDA 25,532 25,556 29,017 32,998 36,301

Depreciation 6,082 6,734 7,401 8,064 8,728

Amortisation 662 710 764 818 872

EBIT 18,788 18,112 20,851 24,116 26,701

Net interest income(expense) -4,275 -3,172 -1,615 -1,700 -1,792

Associates/affiliates 259 248 248 248 248

Exceptionals/extraordinaries 1,450 1,746 133 0 0

Other pre-tax income/(expense) 11 0 0 0 0

Profit before tax 16,233 15,188 19,484 22,663 25,156

Income tax expense 5,557 5,231 6,030 6,967 7,733

Minorities 414 111 128 148 164

Other post-tax income/(expense) 0 0 0 0 0

Net profit 10,262 11,592 13,459 15,549 17,259

DB adjustments (including dilution) 0 0 0 0 0

DB Net profit 10,262 11,592 13,459 15,549 17,259

Cash Flow (CNYm)

Cash flow from operations 9,600 27,385 10,494 9,835 11,204

Net Capex -6,774 -11,681 -10,802 -10,802 -10,802

Free cash flow 2,826 15,704 -308 -967 402

Equity raised/(bought back) 0 12,000 0 0 0

Dividends paid -1,406 -2,005 -2,311 -2,670 -2,964

Net inc/(dec) in borrowings -5,685 -2,492 0 -5,000 -5,000

Other investing/financing cash flows -2,714 1,418 0 0 0

Net cash flow -6,979 24,625 -2,620 -8,638 -7,562

Change in working capital -7,196 11,935 -11,011 -14,497 -15,571

Balance Sheet (CNYm)

Cash and other liquid assets 68,679 93,304 90,684 82,047 74,485

Tangible fixed assets 48,166 51,765 49,206 48,641 47,413

Goodwill/intangible assets 35,450 38,376 40,076 42,307 44,485

Associates/investments 23,852 23,654 23,654 23,654 23,654

Other assets 506,731 506,406 534,916 579,818 632,238

Total assets 682,878 713,505 738,535 776,468 822,275

Interest bearing debt 182,914 180,422 180,422 175,422 170,422

Other liabilities 391,070 393,845 410,972 441,173 477,806

Total liabilities 573,984 574,267 591,394 616,595 648,228

Shareholders' equity 95,470 118,300 126,076 138,659 152,669

Minorities 13,424 20,938 21,066 21,214 21,378

Total shareholders' equity 108,894 139,238 147,142 159,873 174,047

Net debt 114,235 87,118 89,738 93,375 95,937

Key Company Metrics

Sales growth (%) nm 1.7 5.0 8.2 8.9

DB EPS growth (%) na 9.2 11.9 15.5 11.0

EBITDA Margin (%) 4.3 4.3 4.6 4.8 4.9

EBIT Margin (%) 3.2 3.0 3.3 3.5 3.6

Payout ratio (%) 16.2 16.3 16.2 16.2 16.2

ROE (%) 11.3 10.8 11.0 11.7 11.8

Capex/sales (%) 1.3 1.9 1.7 1.6 1.5

Capex/depreciation (x) 1.1 1.6 1.3 1.2 1.1

Net debt/equity (%) 104.9 62.6 61.0 58.4 55.1

Net interest cover (x) 4.4 5.7 12.9 14.2 14.9

Source: Company data, Deutsche Bank estimates

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 19

Appendix 1

Important Disclosures

*Other information available upon request

Disclosure checklist

Company Ticker Recent price* Disclosure

China Comms Construct 1800.HK 10.78 (HKD) 2 Mar 17 6,9,13

CSCI 3311.HK 13.40 (HKD) 2 Mar 17 14,15

China Rail Construction 1186.HK 11.20 (HKD) 2 Mar 17 6,7,9,13,14,15

China Railway Group 0390.HK 7.16 (HKD) 2 Mar 17 13,14,15 Prices are current as of the end of the previous trading session unless otherwise indicated and are sourced from local exchanges via Reuters, Bloomberg and other vendors . Other information is sourced from Deutsche Bank, subject companies, and other sources. For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr. Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the "Disclosures Lookup" and "Legal" tabs. Investors are strongly encouraged to review this information before investing.

Important Disclosures Required by U.S. Regulators

Disclosures marked with an asterisk may also be required by at least one jurisdiction in addition to the United States. See Important Disclosures Required by Non-US Regulators and Explanatory Notes.

6. Deutsche Bank and/or its affiliate(s) owns one percent or more of a class of common equity securities of this company calculated under computational methods required by US law.

7. Deutsche Bank and/or its affiliate(s) has received compensation from this company for the provision of investment banking or financial advisory services within the past year.

14. Deutsche Bank and/or its affiliate(s) has received non-investment banking related compensation from this company within the past year.

15. This company has been a client of Deutsche Bank Securities Inc. within the past year, during which time it received non-investment banking securities-related services.

Important Disclosures Required by Non-U.S. Regulators

Please also refer to disclosures in the Important Disclosures Required by US Regulators and the Explanatory Notes.

6. Deutsche Bank and/or its affiliate(s) owns one percent or more of a class of common equity securities of this company calculated under computational methods required by US law.

7. Deutsche Bank and/or its affiliate(s) has received compensation from this company for the provision of investment banking or financial advisory services within the past year.

9. Deutsche Bank and/or its affiliate(s) owns one percent or more of any class of common equity securities of this company calculated under computational methods required by India law.

13. As of the end of the preceding week, Deutsche Bank and/or its affiliate(s) owns one percent or more of a class of common equity securities of this company.

For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr

3 March 2017

Infrastructure

China Infrastructure

Page 20 Deutsche Bank AG/Hong Kong

Analyst Certification

The views expressed in this report accurately reflect the personal views of the undersigned lead analyst about the subject issuers and the securities of those issuers. In addition, the undersigned lead analyst has not and will not receive any compensation for providing a specific recommendation or view in this report. Phyllis Wang

Historical recommendations and target price: China Comms Construct (1800.HK) (as of 3/2/2017)

1

2

3

4

56

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16 Dec 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 29/04/2015: Buy, Target Price Change HKD18.47 4. 04/03/2016: Buy, Target Price Change HKD10.95

2. 01/07/2015: Buy, Target Price Change HKD15.58 5. 28/04/2016: Buy, Target Price Change HKD11.97

3. 12/11/2015: Buy, Target Price Change HKD13.16 6. 14/07/2016: Buy, Target Price Change HKD12.08

Historical recommendations and target price: CSCI (3311.HK) (as of 3/2/2017)

1

2

34

5 6

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16 Dec 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 20/03/2015: Buy, Target Price Change HKD14.74 Tony Tsang** 4. 18/11/2015: Buy, Target Price Change HKD15.47 Tony Tsang**

2. 26/04/2015: Buy, Target Price Change HKD16.80 Tony Tsang** 5. 22/03/2016: Buy, Target Price Change HKD15.09 Tony Tsang**

3. 13/08/2015: Buy, Target Price Change HKD15.30 Tony Tsang** 6. 01/11/2016: Buy, Target Price Change HKD14.97

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 21

Historical recommendations and target price: China Rail Construction (1186.HK) (as of 3/2/2017)

1

23

4

5 6

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16 Dec 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 29/04/2015: Buy, Target Price Change HKD18.83 4. 04/03/2016: Upgrade to Buy, Target Price Change HKD10.14

2. 01/07/2015: Buy, Target Price Change HKD15.39 5. 28/04/2016: Buy, Target Price Change HKD11.15

3. 12/11/2015: Downgrade to Hold, Target Price Change HKD11.45 6. 14/07/2016: Buy, Target Price Change HKD11.84

Historical recommendations and target price: China Railway Group (0390.HK) (as of 3/2/2017)

1

2

3

4

56

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16 Dec 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 29/04/2015: Hold, Target Price Change HKD10.49 4. 04/03/2016: Upgrade to Buy, Target Price Change HKD6.46

2. 01/07/2015: Hold, Target Price Change HKD8.77 5. 28/04/2016: Downgrade to Hold, Target Price Change HKD6.73

3. 12/11/2015: Hold, Target Price Change HKD6.80 6. 14/07/2016: Upgrade to Buy, Target Price Change HKD6.93

3 March 2017

Infrastructure

China Infrastructure

Page 22 Deutsche Bank AG/Hong Kong

Equity rating key Equity rating dispersion and banking relationships

Buy: Based on a current 12- month view of total share-holder return (TSR = percentage change in share price from current price to projected target price plus pro-jected dividend yield ) , we recommend that investors buy the stock.

Sell: Based on a current 12-month view of total share-holder return, we recommend that investors sell the stock

Hold: We take a neutral view on the stock 12-months out and, based on this time horizon, do not recommend either a Buy or Sell.

Newly issued research recommendations and target prices supersede previously published research.

54 %

36 %

10 %18 % 18 % 18 %

050

100150200250300350400450500

Buy Hold Sell

Asia-Pacific Universe

Companies Covered Cos. w/ Banking Relationship

3 March 2017

Infrastructure

China Infrastructure

Deutsche Bank AG/Hong Kong Page 23

Additional Information

The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively

"Deutsche Bank"). Though the information herein is believed to be reliable and has been obtained from public sources

believed to be reliable, Deutsche Bank makes no representation as to its accuracy or completeness.

If you use the services of Deutsche Bank in connection with a purchase or sale of a security that is discussed in this

report, or is included or discussed in another communication (oral or written) from a Deutsche Bank analyst, Deutsche

Bank may act as principal for its own account or as agent for another person.

Deutsche Bank may consider this report in deciding to trade as principal. It may also engage in transactions, for its own

account or with customers, in a manner inconsistent with the views taken in this research report. Others within

Deutsche Bank, including strategists, sales staff and other analysts, may take views that are inconsistent with those

taken in this research report. Deutsche Bank issues a variety of research products, including fundamental analysis,

equity-linked analysis, quantitative analysis and trade ideas. Recommendations contained in one type of communication

may differ from recommendations contained in others, whether as a result of differing time horizons, methodologies or

otherwise. Deutsche Bank and/or its affiliates may also be holding debt or equity securities of the issuers it writes on.

Analysts are paid in part based on the profitability of Deutsche Bank AG and its affiliates, which includes investment

banking, trading and principal trading revenues.

Opinions, estimates and projections constitute the current judgment of the author as of the date of this report. They do

not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank provides

liquidity for buyers and sellers of securities issued by the companies it covers. Deutsche Bank research analysts

sometimes have shorter-term trade ideas that are consistent or inconsistent with Deutsche Bank's existing longer term

ratings. Trade ideas for equities can be found at the SOLAR link at http://gm.db.com. A SOLAR idea represents a high

conviction belief by an analyst that a stock will outperform or underperform the market and/or sector delineated over a

time frame of no less than two weeks. In addition to SOLAR ideas, the analysts named in this report may from time to

time discuss with our clients, Deutsche Bank salespersons and Deutsche Bank traders, trading strategies or ideas that

reference catalysts or events that may have a near-term or medium-term impact on the market price of the securities

discussed in this report, which impact may be directionally counter to the analysts' current 12-month view of total return

or investment return as described herein. Deutsche Bank has no obligation to update, modify or amend this report or to

otherwise notify a recipient thereof if any opinion, forecast or estimate contained herein changes or subsequently

becomes inaccurate. Coverage and the frequency of changes in market conditions and in both general and company

specific economic prospects make it difficult to update research at defined intervals. Updates are at the sole discretion

of the coverage analyst concerned or of the Research Department Management and as such the majority of reports are

published at irregular intervals. This report is provided for informational purposes only and does not take into account

the particular investment objectives, financial situations, or needs of individual clients. It is not an offer or a solicitation

of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Target prices are

inherently imprecise and a product of the analyst’s judgment. The financial instruments discussed in this report may not

be suitable for all investors and investors must make their own informed investment decisions. Prices and availability of

financial instruments are subject to change without notice and investment transactions can lead to losses as a result of

price fluctuations and other factors. If a financial instrument is denominated in a currency other than an investor's

currency, a change in exchange rates may adversely affect the investment. Past performance is not necessarily

indicative of future results. Unless otherwise indicated, prices are current as of the end of the previous trading session,

and are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank,

subject companies, and in some cases, other parties.

The Deutsche Bank Research Department is independent of other business areas divisions of the Bank. Details regarding

our organizational arrangements and information barriers we have to prevent and avoid conflicts of interest with respect

to our research is available on our website under Disclaimer found on the Legal tab.

Macroeconomic fluctuations often account for most of the risks associated with exposures to instruments that promise

to pay fixed or variable interest rates. For an investor who is long fixed rate instruments (thus receiving these cash

3 March 2017

Infrastructure

China Infrastructure

Page 24 Deutsche Bank AG/Hong Kong

flows), increases in interest rates naturally lift the discount factors applied to the expected cash flows and thus cause a

loss. The longer the maturity of a certain cash flow and the higher the move in the discount factor, the higher will be the

loss. Upside surprises in inflation, fiscal funding needs, and FX depreciation rates are among the most common adverse

macroeconomic shocks to receivers. But counterparty exposure, issuer creditworthiness, client segmentation, regulation

(including changes in assets holding limits for different types of investors), changes in tax policies, currency