china dairy sector - jrj.com.cnpg.jrj.com.cn/acc/res/cn_res/indus/2016/8/19/4adc062e...19 august...

TRANSCRIPT

Deutsche Bank Markets Research

Asia

Hong Kong

Consumer

Industry

China dairy sector

Date

19 August 2016

Industry Update

1H16 preview: weak demand growth but improving margins

Top picks: buy Yili and sell Want Want

________________________________________________________________________________________________________________

Deutsche Bank AG/Hong Kong

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016.

Mark Yuan

Research Analyst

(+852 ) 2203 6181

Anne Ling

Research Analyst

(+852 ) 2203 6177

Key Changes

Company Target Price Rating

1117.HK 1.75 to 1.40(HKD) -

Source: Deutsche Bank

Companies Featured

Want Want China (0151.HK),HKD4.82 Sell

2015A 2016E 2017E

P/E (x) 23.4 14.3 15.1

EV/EBITDA (x) 14.4 8.7 9.4

Price/book (x) 5.3 4.1 3.7

Yili (600887.SS),CNY17.90 Buy

2015A 2016E 2017E

P/E (x) 21.6 21.1 18.1

EV/EBITDA (x) 13.8 13.6 11.6

Price/book (x) 5.0 4.9 4.4

China Mengniu Dairy (2319.HK),HKD13.12 Buy

2015A 2016E 2017E

P/E (x) 22.6 18.3 16.3

EV/EBITDA (x) 13.2 9.5 8.5

Price/book (x) 1.8 1.8 1.7

China Modern Dairy (1117.HK),HKD1.35 Hold

2015A 2016E 2017E

P/E (x) 32.2 – 13.7

EV/EBITDA (x) 16.6 – 10.7

Price/book (x) 1.1 0.9 0.8

Biostime (1112.HK),HKD22.80 Sell

2015A 2016E 2017E

P/E (x) 42.1 18.7 17.5

EV/EBITDA (x) 25.7 10.2 9.6

Price/book (x) 2.5 3.3 3.0

Source: Deutsche Bank

Major dairy companies will report their 1H16 results next week. We reiterate Yili as our top pick and expect its 1H16 earnings to be driven by mix upgrade and declining raw milk costs. We are maintaining our Buy rating on Mengniu, as we expect its sales growth to recover and margin to expand in 2016. We are maintaining our Hold rating on China Modern Dairy as we expect domestic raw milk price to remain weak in the near term. We expect Want Want’s sales to decline structurally and tailwinds from declining raw material costs to weaken from 2H16; maintaining Sell.

Demand growth remains weak, but margins improving for downstream players Industry demand for dairy products remained weak and we expect only low-single digit retail growth for liquid milk in 1H16. Yet, we believe that high-end products and declining raw milk price should be key earnings drivers for downstream players, and the trend should continue into 2H16. We forecast 8% EBIT growth for Yili and 5% for Mengniu in 1H16. We expect Want Want’ sales to decline 7% in local currency due to the sluggish demand for kids’ milk and intense competition (Figure 1).

Key focus in the results – growth of high-end products and raw milk price trend We believe that the key focus for Mengniu and Yili in the results meeting will be the growth outlook for the high-end products (UHT yoghurt, high-end milk, chilled yoghurts, etc.). Marketing spending and channel reform should be key questions for Mengniu. For China Modern Dairy, the key focus should be raw milk price trend. Investors might have low expectation for Want Want’s sales growth. We believe that the key focus will be its new product strategy.

Earnings revision for China Modern Dairy CMD has issued profit warnings and expect over Rmb400m loss in 1H16. We forecast a net loss of Rmb550m in 1H16, due mainly to the revaluation loss on biological assets and value adjustment contracts. We cut cash EBITDA (EBITDA before revaluation loss) by 22-28% to factor in a lower raw milk price forecast and lower branded milk sales growth. We cut our target price by 20% to HK$1.4 based on DCF method.

Figure 1: 1H16 estimates vs. consensus

Sales EBIT Sales EBIT Sales EBIT

Yili Buy 31-Dec I 31,236 3,588 4% 8% 3% 8%

Mengniu Buy 31-Dec I 26,556 1,545 4% 5% 3% 6%

China Modern Dairy Hold 31-Dec I 2,178 429 -11% -40% -7% N/A

Want Want Sell 31-Dec I 10,479 2,562 -7% 11% -4% 11%

Biostime* Sell 31-Dec I 2,982 936 52% 261% 59% N/A

YoY Growth_ConsensusResults

type

1H16 DB forecast YoY Growth_DBFiscal YECompany Rec

Source: Deutsche Bank; Based on pro forma basis(assuming Swisse was consolidated in 1H5), Biostime’s sales and EBIT growth was 3% and 56%, respectively.

Please also refer to: Yili 1H16 preview published on 14 July; Mengniu’s 1H16 preview published on 7 July; and Want Want’s 1H16 preview published on 27 July.

Distributed on: 08/19/2016 12:25:20GMT

19 August 2016

Consumer

China dairy sector

Page 2 Deutsche Bank AG/Hong Kong

1H16 preview: weak demand growth but improving margins

Mix-upgrade and margin expansion to be key earnings drivers for downstream names

According to the National Bureau of Statistics, the production volume of dairy

products increased 6.1% in 1H16 vs. 4.9% in 2015. Assuming industry milk

powder inventory is still increasing (more in upstream dairy farms), we expect

retail sales growth for dairy products to be in low-single digits in 1H16.

Although the sales growth has not rebounded meaningfully, we expect

downstream companies (Mengniu, Yili and Bright) to see an expansion in their

gross margins, driven by:

- Mix upgrade: UHT yoghurt, chilled yoghurt and high-end milk are the

major sales drivers for major dairy companies, while sales of low-end

products (such as milk beverage and low-end milk) is on a declining

trend. We forecast Yili’s UHT yoghurt to grow by 100%+ yoy in 1H16

and Mengniu’s UHT yoghurt by 50%+.

- Declining raw milk price: According to major large-scale farms – China

Modern Dairy, Huishan Dairy and Hosltan in China – domestic raw

milk price declined 7-10% in 1H16.

Domestic raw milk price: more stabilization in 2H16

Milk powder auction price on the Global Dairy Trade platform increased 12.5%

(compared with two weeks ago) to US$2,731/ton on 16 August. We do not

expect domestic raw milk price to have a similar rebound immediately, due to

the large price gap with international price (CIF price) and high domestic milk

powder inventory. However, we expect more price stabilization in 2H16-1H17,

helped by capacity reduction in small farms and the slowdown in large farm

expansion since 2H14. We forecast China Modern Dairy’s raw milk price to

decline 5% HoH in 2H16 to Rmb3.7/kg but recover 3% HoH to Rmb3.9/kg.

Infant milk formula – continued to be pressured by industry destocking

The China Food and Drug Administration Bureau published the detail

implementation measure for the new IMF registration regulation on 12 August.

We expect industry destocking trend to continue in 2H16 due to the new

regulations as the new regulation will reduce the number of IMF brands by

more than 60%. We believe that domestic IMF brands will be negatively

affected in the near term.

China Modern Dairy – earnings revisions

Cut net profit forecast by 36-45% in 2017-18 to factor in lower raw milk price

China Modern Dairy issued a profit warning on 13 July and expects to record

over Rmb400m in losses in 1H16. The profit warnings tracked behind our

previous annual expectations for a positive profit, mainly because of:

1) A higher-than-expected revaluation loss from biological assets due to the

declining raw milk price;

Figure 2: PRC raw milk price

2.00

2.50

3.00

3.50

4.00

4.50

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9Ju

l-0

9O

ct-0

9Ja

n-1

0A

pr-

10

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1Ju

l-1

1O

ct-1

1Ja

n-1

2A

pr-

12

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3Ju

l-1

3O

ct-1

3Ja

n-1

4A

pr-

14

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5Ju

l-1

5O

ct-1

5Ja

n-1

6A

pr-

16

Jul-

16

Rm

b/k

g

Source: agri.gov.cn

Figure 3: Fonterra average WMP and

SMP All contracts

1,000

2,000

3,000

4,000

5,000

6,000

Jul-08 Jul-09 Jul-10 Jul-11 Jul-12 Jul-13 Jul-14 Jul-15 Jul-16

WMP All Contracts SMP All Contracts

Source: GlobalDairyTrade Platform

19 August 2016

Consumer

China dairy sector

Deutsche Bank AG/Hong Kong Page 3

2) A revaluation loss arising from its value adjustment contract signed with

KKR and CDH for the acquisition of two farms in 2015 on a de-rating of

CMD’s stock price; and

3) CMD converts ~10% of its raw milk into milk powder due to the declining

demand.

We are cutting cash EBITDA (EBITDA before revaluation loss) by 23-27% in

2016-18E to factor in: 1) a lower raw milk price – new model forecasts

Rmb3.8/kg vs.Rmb4.0/kg earlier; and 2) a lower volume growth for branded

milk due to the negative impact from recent distribution channel changes.

Our new forecast also factored in a higher revaluation loss on biological assets

in 2016E and that from value adjustment contracts. We forecast CMD to report

an 11% yoy decline in sales and an Rmb550m loss in 1H16 vs. company’s

profit warning at over Rmb400m loss. We forecast a net loss of Rmb600m in

2016 as we expect less revaluation loss on value adjustment contract.

We cut net income by 36-45% in 2017-18E, mainly to factor in 1) lower raw

milk price assumption by 1-7% and 2) lower branded milk sales volume by 32-

39%.

Figure 4: Forecast change

New Old Change

2016E 2017E 2018E 2016E 2017E 2018E 2016E 2017E 2018E

Sales 4,270 4,716 5,262 5,192 6,092 6,744 -17.8% -22.6% -22.0%

Raw milk 2,978 3,146 3,501 3,078 3,396 3,552 -3.3% -7.4% -1.4%

Branded milk 1,292 1,570 1,762 2,114 2,695 3,193 -38.9% -41.7% -44.8%

volume(‘000 tons)

Raw milk 793 813 887 766 828 841 3.6% -1.8% 5.5%

Branded milk 154 182 200 227 284 326 -32.2% -36.0% -38.8%

ASP (RMB/kg)

Raw milk 3.8 3.9 3.9 4.0 4.1 4.2 -6.6% -5.7% -6.6%

Liquid milk 8.4 8.6 8.8 9.3 9.5 9.8 -9.8% -8.9% -9.8%

Gross profit 1,349 1,627 1,808 1,732 2,285 2,641 -22.1% -28.8% -31.5%

Less: SG&A (572) (655) (745) (612) (895) (1,004) -6.6% -26.8% -25.8%

Less: revaluation loss (656) (244) (216) (274) (308) (480) 139.3% -20.7% -55.1%

EBIT 121 728 847 845 1,081 1,157 -85.7% -32.7% -26.8%

Cash EBITDA* 1,115 1,324 1,429 1,441 1,711 1,959 -22.6% -22.6% -27.1%

Other gains and losses (460) - - 37 49 51 NA NA NA

Net profit (600) 446 563 580 817 885 -203.3% -45.4% -36.4% Source: Deutsche Bank estimates; Cash EBITDA refer to EBITDA before revaluation loss of biological assets.

Figure 5: 1H16 preview

1H16E 2H16E 2016E 1H16E 2H16E 2016E

YoY

Revenue 2,178 2,149 4,270 -11% -10% -10%

Gross Profit 719 628 1,349 -19% -18% -18%

SG&A (290) (282) (572) 62% 9% 9%

EBIT 429 346 777 -40% -32% -32%

Cash EBITDA 598 515 1,115 -29% -21% -21%

Net profit (550) (51) (600) -215% -67% -67% Source: Deutsche Bank

19 August 2016

Consumer

China dairy sector

Page 4 Deutsche Bank AG/Hong Kong

Valuation: new target price at HK$1.40; maintain Hold.

Our target price is based on DCF methodology, factoring in a 3.9% risk-free

rate, a 5.6% equity premium, 1.3 beta and 2% terminal growth. We cut our

target price by 20% to HK$1.40 based our new earnings forecast. Our DCF

value is sensitive to our terminal growth factor and WACC assumptions.

We maintain Hold ratings, given 1) we believe its trough valuation at 0.8x FY16

P/B has priced in 2016’s weak results; and 2) we expect stabilization of raw

milk price in next 12 months should help its earnings recovers. Upside and

downside risks: raw milk price, marketing expenses for branded milk and food

safety incidents.

Figure 7: P/B chart

0

1

2

3

4

5

6Price +2STD:3x

+1 STD:2x Avg:2x

-1 STD:1x -2 STD:1x

HK$

Source: Deutsche Bank

Want Want – changing model currency to CNY

Want Want had announced in July that it would change its presentation

currency from USD to CNY starting from the 1H16 results. We maintain our

earnings forecast, but have revised our model currency from USD to CNY. We

forecast a 7.3% yoy sales decline and 7.8% yoy earnings growth for 1H16 in

local currency. Maintaining Sell because of the aging of existing product

categories, underinvestment in new products and less tailwinds from gross

margin expansion from 2H16.

We translate the historical financials based on HKFRS as given below:

Assets and liabilities for each statement of financial position presented

are translated at the closing rate at the end of the reporting period;

Income and expenses for each income statement are translated at the

weighted average exchange rates.

Figure 6: Stock price vs. raw milk

price

0

1

2

3

4

5

6

Stock price (HKD/share) CMD_raw milk price (RMB/KG) Source: Deutsche Bank, company data

19 August 2016

Consumer

China dairy sector

Deutsche Bank AG/Hong Kong Page 5

Figure 8: 1H16 preview in USD and CNY

1H16E 2H16E 2016E 1H16E 2H16E 2016E

US$ mn CNY mn

Sales 1,603 1,402 3,004 10,479 9,801 20,279

Rice crackers 341 504 845 2,229 3,472 5,701

Snack foods 482 269 751 3,151 1,918 5,069

Beverage 773 629 1,402 5,056 4,409 9,465

Other products 6 0 6 42 1 43

Gross profit 768 661 1,429 5,022 4,626 9,648

SG&A (425) (357) (782) (2,777) (2,503) (5,280)

Operating profit 392 336 728 2,562 2,350 4,911

Net Profit 293 248 541 1,914 1,738 3,652

YoY

Turnover (USD) -11.8% -13.0% -12.4% -7.3% -6.3% -6.8%

Gross profit -0.4% -9.8% -5.0% 4.6% -2.7% 1.0%

SG&A -6.0% 0.0% -9.1% -1.1% -5.6% -3.3%

Operating profit 5.6% -6.2% -0.2% 11.0% 1.2% 6.1%

Net Profit 2.5% -3.2% -0.2% 7.8% 4.3% 6.1% Source: Deutsche Bank estimates

Biostime 1H16 preview – 52% sales growth helped by the consolidation of nutritional segment

We expect Biostime’s organic business to decline 13% yoy in 1H16 due to

intensive competition of IMF market. We forecast nutritional segment (Swisse)

to grow 36% driven by China’s growing demand. We expect investors’ key

focus should be in Swisse’s growth and margin trend.

Figure 9: Biostime 1H16 preview

(Rmb mn) 1H15 1H15 1H16E 1H16E YoY 1H16E YoY

(Pro forma)* (Pro forma)

Revenue 1,963 2,899 2,982 52% 3%

Biostime 1,963 1,963 1,710 -13% -13%

Swisse 936 1,273 n/a 36%

Cost of sales (820) (1,175) (1,085) 32% -8%

Gross profit 1,143 1,723 1,897 66% 10%

SG&A (826) (1,049) (904) 9% -14%

Other expense (57) (72) (57) 0% -21%

EBIT 259 602 936 261% 56%

Source: Deutsche Bank estimates, company data

19 August 2016

Consumer

China dairy sector

Page 6 Deutsche Bank AG/Hong Kong

Valuation comps and PE charts

Figure 10: Valuation comp

Listing Rec Mkt Capcurr US$mn Hist FY1Y FY2Y Hist FY1Y FY2Y Hist FY1Y FY2Y

1.Global dairy/IMF companies

Bright Dairy CNY Hold 2,743 53.2 39.5 36.1 4.3 3.8 3.5 1.5 0.8 0.8

Mengniu Dairy HKD Buy 6,654 22.6 18.4 16.4 1.8 1.8 1.7 1.0 1.3 1.4

Yili CNY Buy 16,283 21.6 21.3 18.3 5.0 5.0 4.5 3.1 3.2 3.7

China Huishan Dairy HKD NR 5,267 60.1 37.6 35.6 2.8 2.7 2.6 0.5 0.7 0.7

Biostime HKD Sell 1,801 42.1 18.9 17.8 2.5 3.4 3.0 0.0 2.2 2.3

Want Want HKD Sell 7,889 23.4 14.7 15.6 5.3 4.2 3.8 0.3 0.7 0.6

Almarai SAR Hold 11,679 21.6 22.8 20.9 3.6 3.3 3.0 1.6 1.6 1.8

Beingmate CNY NR 1,928 N/A N/A N/A 3.4 3.5 3.4 N/A 0.0 0.0

Danone EUR Hold 50,940 28.9 22.1 20.5 3.0 3.1 2.9 2.6 2.5 2.7

Dean Foods USD Buy 1,529 N/A N/A N/A 2.4 1.9 1.0 1.6 1.8 2.0

Fonterra NZD Buy 6,871 12.8 11.9 10.9 1.2 1.4 1.3 4.4 6.8 6.7

Mead Johnson USD Hold 15,857 26.0 24.3 22.9 N/A N/A N/A 1.8 2.2 2.3

Meiji Holdings JPY NR 14,380 24.4 23.5 20.9 3.4 3.1 2.8 1.0 1.2 1.4

Parmalat EUR NR 4,924 28.1 29.6 22.7 1.4 1.3 1.3 0.7 0.9 0.9

Saputo CAD NR 13,169 25.7 23.4 21.1 4.1 4.0 3.7 1.4 1.4 1.5

Vietnam Dairy VND NR 9,505 21.6 24.3 21.8 7.7 9.5 8.3 3.4 3.1 3.4

Whitewave USD NR 9,783 44.5 39.5 34.1 7.3 6.7 5.7 N/A 0.0 0.0

Yakult Honsha JPY NR 8,091 28.9 28.2 25.9 2.4 2.1 2.0 0.7 0.7 0.7

Average 30.3 25.0 21.4 3.6 3.6 3.2 1.6 1.7 1.8

2. A-Share F&B comp (market cap>2bn USD)

Kweichow Moutai CNY NR 57,712 23.9 22.1 19.7 5.6 5.1 4.4 2.0 2.0 2.3

Yili CNY Buy 16,283 21.6 21.3 18.3 5.0 5.0 4.5 3.1 3.2 3.7

Jiangsu Yanghe Brewery -A CNY NR 16,252 19.3 18.4 16.2 4.3 4.1 3.5 2.5 2.6 3.0

Henan Shuanghui CNY NR 12,143 18.2 17.3 15.5 5.4 4.6 4.3 3.7 4.5 4.7

Foshan Haitian CNY NR 12,955 32.2 29.1 24.9 9.9 8.6 7.3 1.9 2.1 2.1

Tsingtao Beer - A CNY NR 5,390 23.3 26.1 24.4 2.4 2.3 2.1 1.3 1.1 1.2

Yanjing Beer CNY NR 3,247 37.0 35.1 34.8 1.7 1.6 1.6 0.9 0.9 1.0

Bright Dairy CNY Hold 2,743 53.2 39.5 36.1 4.3 3.8 3.5 1.5 0.8 0.8

Changyu CNY NR 3,548 27.5 24.5 21.8 3.5 3.4 3.2 1.2 1.2 1.4

Shanxi Xinghuacun Fen Wine-A CNY NR 2,772 30.7 28.6 24.3 4.1 3.8 3.4 1.5 1.5 1.8

COFCO Tunhe CNY NR 3,807 148.6 N/A N/A 4.1 4.2 4.1 0.3 N/A N/A

Fujian Sunner Dev CNY NR 4,781 150.5 24.7 13.9 5.8 4.8 3.5 N/A 0.3 0.6

Yinjia Gongjiu CNY NR 2,947 35.4 31.4 27.2 5.4 5.1 4.8 2.0#N/A N/A#N/A N/A

Jinshiyuan CNY NR 2,622 10.2 14.9 13.0 1.7 N/A 3.1 1.2 1.4 1.8

Meihua Holdings CNY NR 2,986 41.8 25.7 20.1 2.3 2.1 2.0 1.6 1.2 1.5

Average 116.4 25.6 22.2 4.2 4.2 3.7 1.8 1.8 2.0

3. HK F&B comp (market cap>2.0bn USD)

Want Want HKD Sell 7,889 23.4 14.7 15.6 5.3 4.2 3.8 1.9 0.0 0.0

Tingyi HKD NR 5,261 25.4 25.4 20.9 1.8 1.8 1.7 2.4 2.0 2.3

WH Group HKD NR 11,638 13.8 13.0 11.3 2.0 1.8 1.6 2.0 2.4 2.9

Tsingtao Brewery-H HKD NR 5,390 18.0 21.3 20.1 1.8 1.8 1.7 1.7 1.6 1.7

Mengniu Dairy HKD Buy 6,654 22.6 18.4 16.4 1.8 1.8 1.7 1.0 1.3 1.4

China Resources HKD NR 6,527 40.5 37.8 27.0 3.2 2.4 2.4 N/A 0.7 1.0

China Huishan Dairy HKD NR 5,267 60.1 37.6 35.6 2.8 2.7 2.6 0.5 0.7 0.7

Uni-President China HKD NR 3,187 23.4 21.2 20.5 1.7 1.7 1.6 0.8 1.0 1.1

CP Pokphand HKD NR 3,136 11.4 13.0 13.0 2.7 2.0 1.9 4.5 7.7 7.7

China Modern Dairy HKD Hold 910 32.2 NA 13.2 1.1 0.8 0.8 0.0 0.0 0.0

China Agri HKD NR 1,970 N/A 29.1 16.8 0.6 0.6 0.5 N/A 0.4 0.7

Average 27.1 23.1 19.1 2.3 2.0 1.8 1.6 1.6 1.8

4.Dairy farm

China Huishan Dairy HKD NR 5,267 60.1 37.6 35.6 2.8 2.7 2.6 0.5 0.7 0.7

China Modern Dairy HKD Hold 910 17.8 32.2 NA 1.3 1.1 0.8 0.0 0.0 0.0

China Shengmu HKD NR 1,385 11.5 9.8 8.4 2.0 1.5 1.2 N/A 0.0 0.3

Yuanshengtai HKD NR 234 23.2 5.7 5.6 0.4 0.3 0.3 N/A N/A N/A

Average 28.2 21.3 16.5 1.6 1.4 1.2 0.2 0.0 0.3

PE (x) PB (x) Div Yield (%)

Source: Deutsche Bank, Bloomberg Finance LP, price as of Aug 18, 2016.

19 August 2016

Consumer

China dairy sector

Deutsche Bank AG/Hong Kong Page 7

Figure 11: Mengniu P/E chart Figure 12: Yili P/E chart

0

10

20

30

40

50

60

Mengniu 1-year forward PE band chart

Price

+2STD:67x

+1 STD:54x

Avg:42x

-1 STD:29x

-2 STD:16x

HK$

-20

0

20

40

60

80

100

120

140

160

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Yili Dairy 1-year forward PE band chart

Price

+2STD:150x

+1 STD:110x

Avg:71x

-1 STD:31x

--2 STD:9x

RMB$

Source: Deutsche Bank, Bloomberg Finance LP

Source: Deutsche Bank; Bloomberg Finance LP

Figure 13: Biostime P/E chart Figure 14: Want Want P/E chart

0

10

20

30

40

50

60

70

80

90

100

Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16

Biostime - 1-year forward PE band chartPrice

+2 STD:46x

+1 STD:34x

Avg:22x

-0.5 STD:16x

-1 STD:10x

HK$

2

4

6

8

10

12

14

16

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Price

+2STD:35x

+1 STD:31x

Avg:26x

-1 STD:21x

-2 STD:16x

HK$

Source: Deutsche Bank; Bloomberg Finance LP

Source: Deutsche Bank; Bloomberg Finance LP

The authors of this report wish to acknowledge the contribution made by Kerith

Chen, employee of Evalueserve, a third-party provider of offshore research

support services to Deutsche Bank.

19 August 2016

Consumer

China dairy sector

Page 8 Deutsche Bank AG/Hong Kong

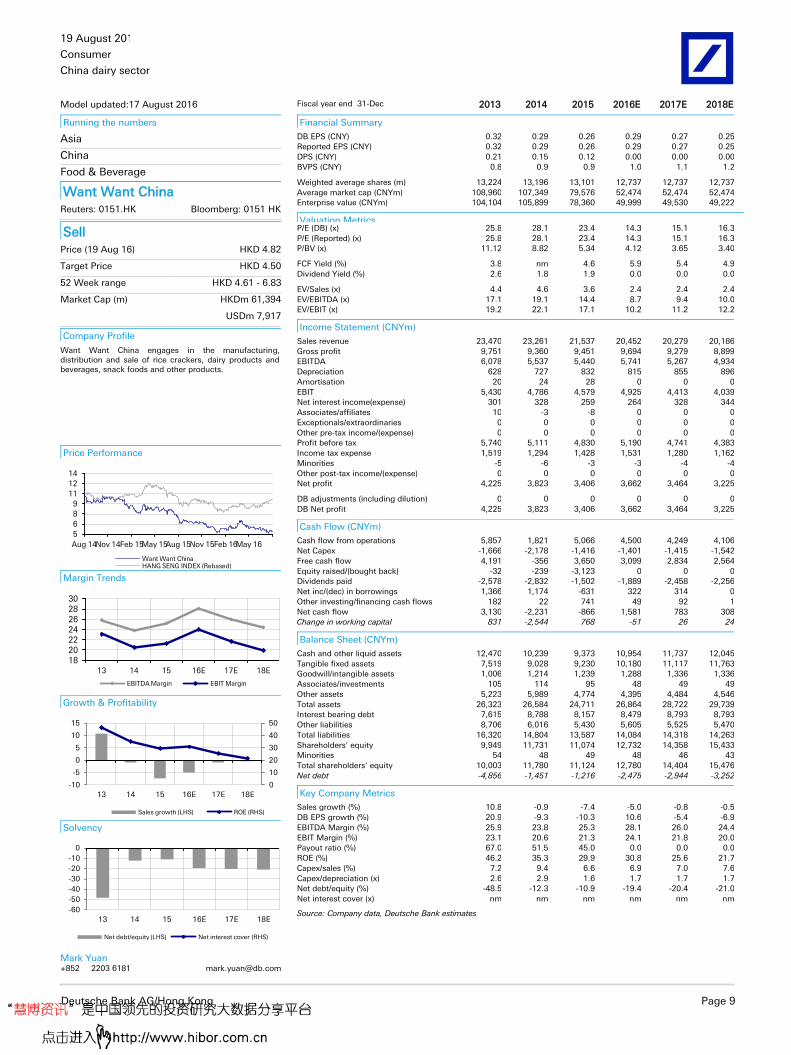

Model updated:17 August 2016

Running the numbers

Asia

China

Food & Beverage

China Modern Dairy Reuters: 1117.HK Bloomberg: 1117 HK

Hold Price (19 Aug 16) HKD 1.35

Target Price HKD 1.40

52 Week range HKD 0.99 - 2.57

Market Cap (m) HKDm 6,517

USDm 840

Company Profile

China Modern Dairy is the largest dairy farming company in China in terms of herd size and raw milk output. It sells a vast majority of raw milk to Mengniu Dairy.

Price Performance

0.0

1.0

2.0

3.0

4.0

5.0

Aug 14Nov 14Feb 15May 15Aug 15Nov 15Feb 16May 16

China Modern DairyHANG SENG INDEX (Rebased)

Margin Trends

-10

0

10

20

30

13 14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

-10

-5

0

5

10

15

-15

-10

-5

0

5

10

15

13 14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

0

1

2

3

4

5

0

20

40

60

80

100

13 14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

Mark Yuan

+852 2203 6181 [email protected]

Fiscal year end 31-Dec 2013 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (CNY) 0.13 0.15 0.06 -0.11 0.08 0.11

Reported EPS (CNY) 0.13 0.15 0.06 -0.11 0.08 0.11

DPS (CNY) 0.00 0.01 0.00 0.00 0.00 0.03

BVPS (CNY) 1.2 1.3 1.5 1.4 1.4 1.5

Weighted average shares (m) 4,813 4,827 5,042 5,305 5,305 5,305

Average market cap (CNYm) 10,893 13,051 10,405 5,570 5,570 5,570

Enterprise value (CNYm) 15,042 17,669 15,635 11,408 11,509 11,545

Valuation Metrics P/E (DB) (x) 17.4 17.8 32.2 nm 13.7 10.9

P/E (Reported) (x) 17.4 17.8 32.2 nm 13.7 10.9

P/BV (x) 2.80 1.30 1.11 0.85 0.80 0.75

FCF Yield (%) nm nm nm nm 2.7 3.8

Dividend Yield (%) 0.0 0.4 0.0 0.0 0.0 2.6

EV/Sales (x) 3.1 3.5 3.2 2.7 2.4 2.2

EV/EBITDA (x) 13.4 14.0 16.6 nm 10.7 9.5

EV/EBIT (x) 15.8 17.1 23.5 nm 15.8 13.6

Income Statement (CNYm)

Sales revenue 4,879 5,027 4,826 4,270 4,716 5,262

Gross profit 1,749 1,865 1,659 1,349 1,627 1,808

EBITDA 1,121 1,263 941 -1 1,080 1,213

Depreciation 168 227 275 338 352 366

Amortisation 0 0 0 0 0 0

EBIT 953 1,036 666 -339 728 847

Net interest income(expense) -281 -266 -315 -271 -269 -269

Associates/affiliates -1 0 5 0 0 0

Exceptionals/extraordinaries 0 0 0 0 0 0

Other pre-tax income/(expense) 0 0 0 0 0 0

Profit before tax 671 770 355 -610 459 579

Income tax expense 15 7 12 2 3 3

Minorities 26 28 22 -13 10 12

Other post-tax income/(expense) 0 0 0 0 0 0

Net profit 630 735 321 -600 446 563

DB adjustments (including dilution) 4 5 4 4 4 4

DB Net profit 634 740 325 -595 450 567

Cash Flow (CNYm)

Cash flow from operations 581 1,581 1,442 750 1,239 1,345

Net Capex -1,719 -1,728 -1,680 -1,087 -1,071 -1,112

Free cash flow -1,138 -147 -239 -337 168 233

Equity raised/(bought back) 0 0 0 0 0 0

Dividends paid 0 0 -49 0 0 0

Net inc/(dec) in borrowings -1,641 -839 -459 0 0 0

Other investing/financing cash flows -173 -322 -325 -271 -269 -269

Net cash flow -2,953 -1,308 -1,071 -608 -101 -35

Change in working capital -418 -187 -86 97 -82 -81

Balance Sheet (CNYm)

Cash and other liquid assets 800 1,170 1,017 409 308 273

Tangible fixed assets 9,987 10,989 12,968 13,061 13,536 14,066

Goodwill/intangible assets 377 375 1,562 1,562 1,562 1,562

Associates/investments 93 114 25 25 25 25

Other assets 1,237 1,469 1,936 1,744 1,890 2,110

Total assets 12,494 14,117 17,508 16,801 17,321 18,036

Interest bearing debt 4,949 5,788 6,247 6,247 6,247 6,247

Other liabilities 1,684 1,673 3,311 3,216 3,281 3,420

Total liabilities 6,633 7,461 9,558 9,463 9,528 9,668

Shareholders' equity 5,743 6,510 7,782 7,182 7,628 8,192

Minorities 118 146 168 155 165 177

Total shareholders' equity 5,861 6,656 7,950 7,337 7,793 8,369

Net debt 4,149 4,618 5,230 5,838 5,939 5,975

Key Company Metrics

Sales growth (%) nm 3.0 -4.0 -11.5 10.5 11.6

DB EPS growth (%) na 16.4 -57.8 na na 26.0

EBITDA Margin (%) 23.0 25.1 19.5 0.0 22.9 23.0

EBIT Margin (%) 19.5 20.6 13.8 -7.9 15.4 16.1

Payout ratio (%) 0.0 6.5 0.0 nm 0.0 28.6

ROE (%) 11.7 12.1 4.6 -8.0 6.1 7.2

Capex/sales (%) 41.1 43.6 43.6 38.7 34.0 31.7

Capex/depreciation (x) 11.9 9.7 7.6 4.9 4.6 4.6

Net debt/equity (%) 70.8 69.4 65.8 79.6 76.2 71.4

Net interest cover (x) 3.4 3.9 2.1 nm 2.7 3.2

Source: Company data, Deutsche Bank estimates

19 August 2016

Consumer

China dairy sector

Deutsche Bank AG/Hong Kong Page 9

Model updated:17 August 2016

Running the numbers

Asia

China

Food & Beverage

Want Want China Reuters: 0151.HK Bloomberg: 0151 HK

Sell Price (19 Aug 16) HKD 4.82

Target Price HKD 4.50

52 Week range HKD 4.61 - 6.83

Market Cap (m) HKDm 61,394

USDm 7,917

Company Profile

Want Want China engages in the manufacturing, distribution and sale of rice crackers, dairy products and beverages, snack foods and other products.

Price Performance

5

6

8

9

11

12

14

Aug 14Nov 14Feb 15May 15Aug 15Nov 15Feb 16May 16

Want Want ChinaHANG SENG INDEX (Rebased)

Margin Trends

18202224262830

13 14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

0

10

20

30

40

50

-10

-5

0

5

10

15

13 14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

-60

-50

-40

-30

-20

-10

0

13 14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

Mark Yuan

+852 2203 6181 [email protected]

Fiscal year end 31-Dec 2013 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (CNY) 0.32 0.29 0.26 0.29 0.27 0.25

Reported EPS (CNY) 0.32 0.29 0.26 0.29 0.27 0.25

DPS (CNY) 0.21 0.15 0.12 0.00 0.00 0.00

BVPS (CNY) 0.8 0.9 0.9 1.0 1.1 1.2

Weighted average shares (m) 13,224 13,196 13,101 12,737 12,737 12,737

Average market cap (CNYm) 108,960 107,349 79,576 52,474 52,474 52,474

Enterprise value (CNYm) 104,104 105,899 78,360 49,999 49,530 49,222

Valuation Metrics P/E (DB) (x) 25.8 28.1 23.4 14.3 15.1 16.3

P/E (Reported) (x) 25.8 28.1 23.4 14.3 15.1 16.3

P/BV (x) 11.12 8.82 5.34 4.12 3.65 3.40

FCF Yield (%) 3.8 nm 4.6 5.9 5.4 4.9

Dividend Yield (%) 2.6 1.8 1.9 0.0 0.0 0.0

EV/Sales (x) 4.4 4.6 3.6 2.4 2.4 2.4

EV/EBITDA (x) 17.1 19.1 14.4 8.7 9.4 10.0

EV/EBIT (x) 19.2 22.1 17.1 10.2 11.2 12.2

Income Statement (CNYm)

Sales revenue 23,470 23,261 21,537 20,452 20,279 20,186

Gross profit 9,751 9,360 9,451 9,694 9,279 8,899

EBITDA 6,078 5,537 5,440 5,741 5,267 4,934

Depreciation 628 727 832 815 855 896

Amortisation 20 24 28 0 0 0

EBIT 5,430 4,786 4,579 4,925 4,413 4,039

Net interest income(expense) 301 328 259 264 328 344

Associates/affiliates 10 -3 -8 0 0 0

Exceptionals/extraordinaries 0 0 0 0 0 0

Other pre-tax income/(expense) 0 0 0 0 0 0

Profit before tax 5,740 5,111 4,830 5,190 4,741 4,383

Income tax expense 1,519 1,294 1,428 1,531 1,280 1,162

Minorities -5 -6 -3 -3 -4 -4

Other post-tax income/(expense) 0 0 0 0 0 0

Net profit 4,225 3,823 3,406 3,662 3,464 3,225

DB adjustments (including dilution) 0 0 0 0 0 0

DB Net profit 4,225 3,823 3,406 3,662 3,464 3,225

Cash Flow (CNYm)

Cash flow from operations 5,857 1,821 5,066 4,500 4,249 4,106

Net Capex -1,666 -2,178 -1,416 -1,401 -1,415 -1,542

Free cash flow 4,191 -356 3,650 3,099 2,834 2,564

Equity raised/(bought back) -32 -239 -3,123 0 0 0

Dividends paid -2,578 -2,832 -1,502 -1,889 -2,458 -2,256

Net inc/(dec) in borrowings 1,366 1,174 -631 322 314 0

Other investing/financing cash flows 182 22 741 49 92 1

Net cash flow 3,130 -2,231 -866 1,581 783 308

Change in working capital 831 -2,544 768 -51 26 24

Balance Sheet (CNYm)

Cash and other liquid assets 12,470 10,239 9,373 10,954 11,737 12,045

Tangible fixed assets 7,519 9,028 9,230 10,180 11,117 11,763

Goodwill/intangible assets 1,006 1,214 1,239 1,288 1,336 1,336

Associates/investments 105 114 95 48 49 49

Other assets 5,223 5,989 4,774 4,395 4,484 4,546

Total assets 26,323 26,584 24,711 26,864 28,722 29,739

Interest bearing debt 7,615 8,788 8,157 8,479 8,793 8,793

Other liabilities 8,706 6,016 5,430 5,605 5,525 5,470

Total liabilities 16,320 14,804 13,587 14,084 14,318 14,263

Shareholders' equity 9,949 11,731 11,074 12,732 14,358 15,433

Minorities 54 48 49 48 46 43

Total shareholders' equity 10,003 11,780 11,124 12,780 14,404 15,476

Net debt -4,856 -1,451 -1,216 -2,475 -2,944 -3,252

Key Company Metrics

Sales growth (%) 10.8 -0.9 -7.4 -5.0 -0.8 -0.5

DB EPS growth (%) 20.9 -9.3 -10.3 10.6 -5.4 -6.9

EBITDA Margin (%) 25.9 23.8 25.3 28.1 26.0 24.4

EBIT Margin (%) 23.1 20.6 21.3 24.1 21.8 20.0

Payout ratio (%) 67.0 51.5 45.0 0.0 0.0 0.0

ROE (%) 46.2 35.3 29.9 30.8 25.6 21.7

Capex/sales (%) 7.2 9.4 6.6 6.9 7.0 7.6

Capex/depreciation (x) 2.6 2.9 1.6 1.7 1.7 1.7

Net debt/equity (%) -48.5 -12.3 -10.9 -19.4 -20.4 -21.0

Net interest cover (x) nm nm nm nm nm nm

Source: Company data, Deutsche Bank estimates

19 August 2016

Consumer

China dairy sector

Page 10 Deutsche Bank AG/Hong Kong

Appendix 1 Important Disclosures

Additional information available upon request

Disclosure checklist

Company Ticker Recent price* Disclosure

Want Want China 0151.HK 4.82 (HKD) 19 Aug 16 14,15

China Mengniu Dairy 2319.HK 13.12 (HKD) 19 Aug 16 7,14,15

Yili 600887.SS 17.90 (CNY) 19 Aug 16 NA

Biostime 1112.HK 22.80 (HKD) 19 Aug 16 1,6,7,9,14,15

China Modern Dairy 1117.HK 1.35 (HKD) 19 Aug 16 NA *Prices are current as of the end of the previous trading session unless otherwise indicated and are sourced from local exchanges via Reuters, Bloomberg and other vendors . Other information is sourced from Deutsche Bank, subject companies, and other sources. For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr.

Important Disclosures Required by U.S. Regulators

Disclosures marked with an asterisk may also be required by at least one jurisdiction in addition to the United States. See Important Disclosures Required by Non-US Regulators and Explanatory Notes.

1. Within the past year, Deutsche Bank and/or its affiliate(s) has managed or co-managed a public or private offering for this company, for which it received fees.

6. Deutsche Bank and/or its affiliate(s) owns one percent or more of any class of common equity securities of this company calculated under computational methods required by US law.

7. Deutsche Bank and/or its affiliate(s) has received compensation from this company for the provision of investment banking or financial advisory services within the past year.

14. Deutsche Bank and/or its affiliate(s) has received non-investment banking related compensation from this company within the past year.

15. This company has been a client of Deutsche Bank Securities Inc. within the past year, during which time it received non-investment banking securities-related services.

Important Disclosures Required by Non-U.S. Regulators

Please also refer to disclosures in the Important Disclosures Required by US Regulators and the Explanatory Notes.

1. Within the past year, Deutsche Bank and/or its affiliate(s) has managed or co-managed a public or private offering for this company, for which it received fees.

6. Deutsche Bank and/or its affiliate(s) owns one percent or more of any class of common equity securities of this company calculated under computational methods required by US law.

7. Deutsche Bank and/or its affiliate(s) has received compensation from this company for the provision of investment banking or financial advisory services within the past year.

9. Deutsche Bank and/or its affiliate(s) owns one percent or more of any class of common equity securities of this company calculated under computational methods required by India law.

For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr

19 August 2016

Consumer

China dairy sector

Deutsche Bank AG/Hong Kong Page 11

Analyst Certification

The views expressed in this report accurately reflect the personal views of the undersigned lead analyst about the subject issuers and the securities of those issuers. In addition, the undersigned lead analyst has not and will not receive any compensation for providing a specific recommendation or view in this report. Mark Yuan

Historical recommendations and target price: Want Want China (0151.HK) (as of 8/19/2016)

1

2

3 45

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Aug 14 Nov 14 Feb 15 May 15 Aug 15 Nov 15 Feb 16 May 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 23/04/2015: Upgrade to Hold, Target Price Change HKD8.45 Winnie Mak**

4. 15/03/2016: Hold, Target Price Change HKD5.50 Mark Yuan

2. 26/08/2015: Hold, Target Price Change HKD6.48 Winnie Mak** 5. 27/07/2016: Downgrade to Sell, Target Price Change HKD4.50 Mark Yuan

3. 07/01/2016: Hold, Target Price Change HKD5.90 Mark Yuan

19 August 2016

Consumer

China dairy sector

Page 12 Deutsche Bank AG/Hong Kong

Historical recommendations and target price: China Mengniu Dairy (2319.HK) (as of 8/19/2016)

12

3

4

5

67

8 910

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

Aug 14 Nov 14 Feb 15 May 15 Aug 15 Nov 15 Feb 16 May 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 28/08/2014: Hold, Target Price Change HKD35.60 Winnie Mak** 6. 13/10/2015: Buy, Target Price Change HKD18.00 Winnie Mak**

2. 03/11/2014: Upgrade to Buy, Target Price Change HKD37.50 Winnie Mak**

7. 03/11/2015: Buy, Target Price Change HKD16.00 Mark Yuan

3. 26/03/2015: Buy, Target Price Change HKD41.30 Winnie Mak** 8. 15/02/2016: Buy, Target Price Change HKD15.00 Mark Yuan

4. 27/08/2015: Buy, Target Price Change HKD38.00 Winnie Mak** 9. 23/03/2016: Buy, Target Price Change HKD14.10 Mark Yuan

5. 03/09/2015: Buy, Target Price Change HKD36.00 Winnie Mak** 10. 06/07/2016: Buy, Target Price Change HKD14.50 Mark Yuan

Historical recommendations and target price: Yili (600887.SS) (as of 8/19/2016)

1 2

3

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

Aug 14 Nov 14 Feb 15 May 15 Aug 15 Nov 15 Feb 16 May 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 03/11/2015: Upgrade to Buy, Target Price Change CNY18.60 Mark Yuan

3. 14/07/2016: Buy, Target Price Change CNY20.40 Mark Yuan

2. 03/04/2016: Buy, Target Price Change CNY18.40 Mark Yuan

19 August 2016

Consumer

China dairy sector

Deutsche Bank AG/Hong Kong Page 13

Historical recommendations and target price: Biostime (1112.HK) (as of 8/19/2016)

1

2 3

45

6

7

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

Aug 14 Nov 14 Feb 15 May 15 Aug 15 Nov 15 Feb 16 May 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 27/10/2014: Hold, Target Price Change HKD31.10 Winnie Mak** 5. 21/09/2015: Downgrade to Sell, Target Price Change HKD13.70 Winnie Mak**

2. 25/03/2015: Hold, Target Price Change HKD33.10 Winnie Mak** 6. 17/11/2015: Sell, Target Price Change HKD10.80 Mark Yuan

3. 04/06/2015: Hold, Target Price Change HKD30.20 Winnie Mak** 7. 03/04/2016: Sell, Target Price Change HKD16.80 Mark Yuan

4. 19/08/2015: Hold, Target Price Change HKD14.40 Winnie Mak**

Historical recommendations and target price: China Modern Dairy (1117.HK) (as of 8/19/2016)

1

2

3

4 5

6

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Aug 14 Nov 14 Feb 15 May 15 Aug 15 Nov 15 Feb 16 May 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 28/08/2014: Sell, Target Price Change HKD3.15 Winnie Mak** 4. 26/08/2015: Upgrade to Hold, HKD2.20 Winnie Mak**

2. 03/11/2014: Sell, Target Price Change HKD2.95 Winnie Mak** 5. 22/12/2015: Hold, Target Price Change HKD2.00 Mark Yuan

3. 01/12/2014: Sell, Target Price Change HKD2.20 Winnie Mak** 6. 22/03/2016: Hold, Target Price Change HKD1.75 Mark Yuan

19 August 2016

Consumer

China dairy sector

Page 14 Deutsche Bank AG/Hong Kong

Equity rating key Equity rating dispersion and banking relationships

Buy: Based on a current 12- month view of total share-holder return (TSR = percentage change in share price from current price to projected target price plus pro-jected dividend yield ) , we recommend that investors buy the stock.

Sell: Based on a current 12-month view of total share-holder return, we recommend that investors sell the stock

Hold: We take a neutral view on the stock 12-months out and, based on this time horizon, do not recommend either a Buy or Sell.

Newly issued research recommendations and target prices supersede previously published research.

52 %

37 %

10 %15 % 15 % 21 %

050

100150200250300350400450500

Buy Hold Sell

Asia-Pacific Universe

Companies Covered Cos. w/ Banking Relationship

Regulatory Disclosures

1.Important Additional Conflict Disclosures

Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the

"Disclosures Lookup" and "Legal" tabs. Investors are strongly encouraged to review this information before investing.

2.Short-Term Trade Ideas

Deutsche Bank equity research analysts sometimes have shorter-term trade ideas (known as SOLAR ideas) that are

consistent or inconsistent with Deutsche Bank's existing longer term ratings. These trade ideas can be found at the

SOLAR link at http://gm.db.com.

19 August 2016

Consumer

China dairy sector

Deutsche Bank AG/Hong Kong Page 15

Additional Information

The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively

"Deutsche Bank"). Though the information herein is believed to be reliable and has been obtained from public sources

believed to be reliable, Deutsche Bank makes no representation as to its accuracy or completeness.

If you use the services of Deutsche Bank in connection with a purchase or sale of a security that is discussed in this

report, or is included or discussed in another communication (oral or written) from a Deutsche Bank analyst, Deutsche

Bank may act as principal for its own account or as agent for another person.

Deutsche Bank may consider this report in deciding to trade as principal. It may also engage in transactions, for its own

account or with customers, in a manner inconsistent with the views taken in this research report. Others within

Deutsche Bank, including strategists, sales staff and other analysts, may take views that are inconsistent with those

taken in this research report. Deutsche Bank issues a variety of research products, including fundamental analysis,

equity-linked analysis, quantitative analysis and trade ideas. Recommendations contained in one type of communication

may differ from recommendations contained in others, whether as a result of differing time horizons, methodologies or

otherwise. Deutsche Bank and/or its affiliates may also be holding debt or equity securities of the issuers it writes on.

Analysts are paid in part based on the profitability of Deutsche Bank AG and its affiliates, which includes investment

banking revenues.

Opinions, estimates and projections constitute the current judgment of the author as of the date of this report. They do

not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank research

analysts sometimes have shorter-term trade ideas that are consistent or inconsistent with Deutsche Bank's existing

longer term ratings. These trade ideas for equities can be found at the SOLAR link at http://gm.db.com. A SOLAR idea

represents a high conviction belief by an analyst that a stock will outperform or underperform the market and/or sector

delineated over a time frame of no less than two weeks. In addition to SOLAR ideas, the analysts named in this report

may have from time to time discussed with our clients, including Deutsche Bank salespersons and traders, or may

discuss in this report or elsewhere, trading strategies or ideas that reference catalysts or events that may have a near-

term or medium-term impact on the market price of the securities discussed in this report, which impact may be

directionally counter to the analysts' current 12-month view of total return as described herein. Deutsche Bank has no

obligation to update, modify or amend this report or to otherwise notify a recipient thereof if any opinion, forecast or

estimate contained herein changes or subsequently becomes inaccurate. Coverage and the frequency of changes in

market conditions and in both general and company specific economic prospects makes it difficult to update research at

defined intervals. Updates are at the sole discretion of the coverage analyst concerned or of the Research Department

Management and as such the majority of reports are published at irregular intervals. This report is provided for

informational purposes only. It is not an offer or a solicitation of an offer to buy or sell any financial instruments or to

participate in any particular trading strategy. Target prices are inherently imprecise and a product of the analyst’s

judgment. The financial instruments discussed in this report may not be suitable for all investors and investors must

make their own informed investment decisions. Prices and availability of financial instruments are subject to change

without notice and investment transactions can lead to losses as a result of price fluctuations and other factors. If a

financial instrument is denominated in a currency other than an investor's currency, a change in exchange rates may

adversely affect the investment. Past performance is not necessarily indicative of future results. Unless otherwise

indicated, prices are current as of the end of the previous trading session, and are sourced from local exchanges via

Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank, subject companies, and in some cases,

other parties.

The Deutsche Bank Research Department is independent of other business areas divisions of the Bank. Details regarding

our organizational arrangements and information barriers we have to prevent and avoid conflicts of interest with respect

to our research is available on our website under Disclaimer found on the Legal tab.

Macroeconomic fluctuations often account for most of the risks associated with exposures to instruments that promise

to pay fixed or variable interest rates. For an investor who is long fixed rate instruments (thus receiving these cash

flows), increases in interest rates naturally lift the discount factors applied to the expected cash flows and thus cause a

19 August 2016

Consumer

China dairy sector

Page 16 Deutsche Bank AG/Hong Kong

loss. The longer the maturity of a certain cash flow and the higher the move in the discount factor, the higher will be the

loss. Upside surprises in inflation, fiscal funding needs, and FX depreciation rates are among the most common adverse

macroeconomic shocks to receivers. But counterparty exposure, issuer creditworthiness, client segmentation, regulation

(including changes in assets holding limits for different types of investors), changes in tax policies, currency

convertibility (which may constrain currency conversion, repatriation of profits and/or the liquidation of positions), and

settlement issues related to local clearing houses are also important risk factors to be considered. The sensitivity of fixed

income instruments to macroeconomic shocks may be mitigated by indexing the contracted cash flows to inflation, to

FX depreciation, or to specified interest rates – these are common in emerging markets. It is important to note that the

index fixings may -- by construction -- lag or mis-measure the actual move in the underlying variables they are intended

to track. The choice of the proper fixing (or metric) is particularly important in swaps markets, where floating coupon

rates (i.e., coupons indexed to a typically short-dated interest rate reference index) are exchanged for fixed coupons. It is

also important to acknowledge that funding in a currency that differs from the currency in which coupons are

denominated carries FX risk. Naturally, options on swaps (swaptions) also bear the risks typical to options in addition to

the risks related to rates movements.

Derivative transactions involve numerous risks including, among others, market, counterparty default and illiquidity risk.

The appropriateness or otherwise of these products for use by investors is dependent on the investors' own

circumstances including their tax position, their regulatory environment and the nature of their other assets and

liabilities, and as such, investors should take expert legal and financial advice before entering into any transaction similar

to or inspired by the contents of this publication. The risk of loss in futures trading and options, foreign or domestic, can

be substantial. As a result of the high degree of leverage obtainable in futures and options trading, losses may be

incurred that are greater than the amount of funds initially deposited. Trading in options involves risk and is not suitable

for all investors. Prior to buying or selling an option investors must review the "Characteristics and Risks of Standardized

Options”, at http://www.optionsclearing.com/about/publications/character-risks.jsp. If you are unable to access the

website please contact your Deutsche Bank representative for a copy of this important document.

Participants in foreign exchange transactions may incur risks arising from several factors, including the following: ( i)

exchange rates can be volatile and are subject to large fluctuations; ( ii) the value of currencies may be affected by

numerous market factors, including world and national economic, political and regulatory events, events in equity and

debt markets and changes in interest rates; and (iii) currencies may be subject to devaluation or government imposed

exchange controls which could affect the value of the currency. Investors in securities such as ADRs, whose values are

affected by the currency of an underlying security, effectively assume currency risk.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the

investor's home jurisdiction.

United States: Approved and/or distributed by Deutsche Bank Securities Incorporated, a member of FINRA, NFA and

SIPC. Analysts employed by non-US affiliates may not be associated persons of Deutsche Bank Securities Incorporated

and therefore not subject to FINRA regulations concerning communications with subject companies, public appearances

and securities held by analysts.

Germany: Approved and/or distributed by Deutsche Bank AG, a joint stock corporation with limited liability incorporated

in the Federal Republic of Germany with its principal office in Frankfurt am Main. Deutsche Bank AG is authorized under

German Banking Law and is subject to supervision by the European Central Bank and by BaFin, Germany’s Federal

Financial Supervisory Authority.

United Kingdom: Approved and/or distributed by Deutsche Bank AG acting through its London Branch at Winchester

House, 1 Great Winchester Street, London EC2N 2DB. Deutsche Bank AG in the United Kingdom is authorised by the

Prudential Regulation Authority and is subject to limited regulation by the Prudential Regulation Authority and Financial

Conduct Authority. Details about the extent of our authorisation and regulation are available on request.

Hong Kong: Distributed by Deutsche Bank AG, Hong Kong Branch.

India: Prepared by Deutsche Equities India Pvt Ltd, which is registered by the Securities and Exchange Board of India

(SEBI) as a stock broker. Research Analyst SEBI Registration Number is INH000001741. DEIPL may have received

19 August 2016

Consumer

China dairy sector

Deutsche Bank AG/Hong Kong Page 17

administrative warnings from the SEBI for breaches of Indian regulations.

Japan: Approved and/or distributed by Deutsche Securities Inc.(DSI). Registration number - Registered as a financial

instruments dealer by the Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA,

Type II Financial Instruments Firms Association and The Financial Futures Association of Japan. Commissions and risks

involved in stock transactions - for stock transactions, we charge stock commissions and consumption tax by

multiplying the transaction amount by the commission rate agreed with each customer. Stock transactions can lead to

losses as a result of share price fluctuations and other factors. Transactions in foreign stocks can lead to additional

losses stemming from foreign exchange fluctuations. We may also charge commissions and fees for certain categories

of investment advice, products and services. Recommended investment strategies, products and services carry the risk

of losses to principal and other losses as a result of changes in market and/or economic trends, and/or fluctuations in

market value. Before deciding on the purchase of financial products and/or services, customers should carefully read the

relevant disclosures, prospectuses and other documentation. "Moody's", "Standard & Poor's", and "Fitch" mentioned in

this report are not registered credit rating agencies in Japan unless Japan or "Nippon" is specifically designated in the

name of the entity. Reports on Japanese listed companies not written by analysts of DSI are written by Deutsche Bank

Group's analysts with the coverage companies specified by DSI. Some of the foreign securities stated on this report are

not disclosed according to the Financial Instruments and Exchange Law of Japan.

Korea: Distributed by Deutsche Securities Korea Co.

South Africa: Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch Register

Number in South Africa: 1998/003298/10).

Singapore: by Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch (One Raffles

Quay #18-00 South Tower Singapore 048583, +65 6423 8001), which may be contacted in respect of any matters

arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who

is not an accredited investor, expert investor or institutional investor (as defined in the applicable Singapore laws and

regulations), they accept legal responsibility to such person for its contents.

Taiwan: Information on securities/investments that trade in Taiwan is for your reference only. Readers should

independently evaluate investment risks and are solely responsible for their investment decisions. Deutsche Bank

research may not be distributed to the Taiwan public media or quoted or used by the Taiwan public media without

written consent. Information on securities/instruments that do not trade in Taiwan is for informational purposes only and

is not to be construed as a recommendation to trade in such securities/instruments. Deutsche Securities Asia Limited,

Taipei Branch may not execute transactions for clients in these securities/instruments.

Qatar: Deutsche Bank AG in the Qatar Financial Centre (registered no. 00032) is regulated by the Qatar Financial Centre

Regulatory Authority. Deutsche Bank AG - QFC Branch may only undertake the financial services activities that fall

within the scope of its existing QFCRA license. Principal place of business in the QFC: Qatar Financial Centre, Tower,

West Bay, Level 5, PO Box 14928, Doha, Qatar. This information has been distributed by Deutsche Bank AG. Related

financial products or services are only available to Business Customers, as defined by the Qatar Financial Centre

Regulatory Authority.

Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute,

any appraisal or evaluation activity requiring a license in the Russian Federation.

Kingdom of Saudi Arabia: Deutsche Securities Saudi Arabia LLC Company, (registered no. 07073-37) is regulated by the

Capital Market Authority. Deutsche Securities Saudi Arabia may only undertake the financial services activities that fall

within the scope of its existing CMA license. Principal place of business in Saudi Arabia: King Fahad Road, Al Olaya

District, P.O. Box 301809, Faisaliah Tower - 17th Floor, 11372 Riyadh, Saudi Arabia.

United Arab Emirates: Deutsche Bank AG in the Dubai International Financial Centre (registered no. 00045) is regulated

by the Dubai Financial Services Authority. Deutsche Bank AG - DIFC Branch may only undertake the financial services

activities that fall within the scope of its existing DFSA license. Principal place of business in the DIFC: Dubai

International Financial Centre, The Gate Village, Building 5, PO Box 504902, Dubai, U.A.E. This information has been

19 August 2016

Consumer

China dairy sector

Page 18 Deutsche Bank AG/Hong Kong

distributed by Deutsche Bank AG. Related financial products or services are only available to Professional Clients, as

defined by the Dubai Financial Services Authority.

Australia: Retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product

referred to in this report and consider the PDS before making any decision about whether to acquire the product. Please

refer to Australian specific research disclosures and related information at

https://australia.db.com/australia/content/research-information.html

Australia and New Zealand: This research, and any access to it, is intended only for "wholesale clients" within the

meaning of the Australian Corporations Act and New Zealand Financial Advisors Act respectively.

Additional information relative to securities, other financial products or issuers discussed in this report is available upon

request. This report may not be reproduced, distributed or published without Deutsche Bank's prior written consent.

Copyright © 2016 Deutsche Bank AG

David Folkerts-Landau Group Chief Economist and Global Head of Research

Raj Hindocha Global Chief Operating Officer

Research

Michael Spencer Head of APAC Research

Global Head of Economics

Steve Pollard Head of Americas Research

Global Head of Equity Research

Anthony Klarman Global Head of Debt Research

Paul Reynolds Head of EMEA

Equity Research

Dave Clark Head of APAC

Equity Research

Pam Finelli Global Head of

Equity Derivatives Research

Andreas Neubauer Head of Research - Germany

Stuart Kirk Head of Thematic Research

International locations

Deutsche Bank AG

Deutsche Bank Place

Level 16

Corner of Hunter & Phillip Streets

Sydney, NSW 2000

Australia

Tel: (61) 2 8258 1234

Deutsche Bank AG

Große Gallusstraße 10-14

60272 Frankfurt am Main

Germany

Tel: (49) 69 910 00

Deutsche Bank AG

Filiale Hongkong

International Commerce Centre,

1 Austin Road West,Kowloon,

Hong Kong

Tel: (852) 2203 8888

Deutsche Securities Inc.

2-11-1 Nagatacho

Sanno Park Tower

Chiyoda-ku, Tokyo 100-6171

Japan

Tel: (81) 3 5156 6770

Deutsche Bank AG London

1 Great Winchester Street

London EC2N 2EQ

United Kingdom

Tel: (44) 20 7545 8000

Deutsche Bank Securities Inc.

60 Wall Street

New York, NY 10005

United States of America

Tel: (1) 212 250 2500