china’s market for australian...

TRANSCRIPT

China Policy

China’s market for Australian porka window of opportunity

2

This report presents an analysis of Chinese market demand for Australian pork on the basis of survey data compiled from 33 high-volume, frequent importers of pork products. Responses are analysed and placed in context of China’s current agri-food market and policy structure, identifying key drivers of demand and indicators of growth potential, and evaluating the potential of a market access strategy. At a time of rapid development in consumer preferences and major adjustments to trade strategies in China, the report offers a snapshot of the current commercial and regulatory environment as it impacts Australia’s pork industry. The report highlights adjustment to China’s food security strategy. This has opened up market access opportunities to industry groups who position effectively with regard not just to safety and quality, but also cooperation with Chinese standards and regulatory agencies. Interest from Chinese investors and commercial partnerships is also highlighted.The report identifies domestic consumption patterns and the international importers currently serving them, and presents specific recommendations on how to position Australia’s pork industry for success in the world’s largest, fastest growing and most dynamic market for meat.

This report was funded by Australian Pork Limited. A survey was conducted by China Import and Quarantine Association and data analysis and reporting was produced by China Policy, Beijing.scope of report

3

summary: a window of opportunity for Australian pork

agei

agei

agei

most major importers surveyed welcome Australian pork

Australian pork is seen as safe, healthy, and natural

nearly half are interested in investing in Australia’s pork value chain

Eighty-five percent of importers surveyed are interested in importing Australian pork, if a protocol can be secured. Those that expressed interest cite the Australian meat industry’s strong reputation and Chinese consumers’ increasing demand for diverse and new prod-ucts, but first and foremost they cite health- and safety-related factors.

Australian pork is perceived as safe, healthy, and natural, by major importers surveyed. Some importers with concerns about price and boar taint still give high marks on these factors. Benefitting from the halo effect of Australian beef and sheepmeat producers, Aus-tralian pork already enjoys a valuable brand image among China’s importers.

Nearly half importers surveyed are interested in investment opportunities in the Australian pork industry. Companies expressing interest in investing are in most cases large, well-cap-italised, and highly credible potential partners. One such respondent, Yurun Food Group, is among China’s largest pork processors; its subsidiary Yurun Logistics is the second larg-est cold-chain logistics company. Another interested respondent, Foresun Group, bought US$75 million in beef processing and feedlot assets in Argentina last year. Investing over-seas in agricultural production does not fall under current capital account restrictions.

4

summary: a window of opportunity for Australian pork

agei

agei

agei

a new trade strategy is moving China away from ‘self sufficiency’ in food

imports will continue to grow to fill a 3+ million tonne pork supply gap in 2026

an increasingly market-based approach will advantage exporters (in the short term)

Changes in China’s food supply strategy indicate that more engagement with global mar-kets is necessary to satisfy its food needs. Domestic policies reflect an increasing departure from ‘self sufficiency’ and an explicit push to secure long-term, stable supply relationships abroad.

Demand for pork has grown beyond China’s domestic production capacity. While imports have fluctuated on the basis of volatile domestic prices, the trend line is clearly rising. Domestic pig population and pork supply data is notoriously inconsistent; however, even Chinese Academy of Agricultural Sciences projects a large and growing pork supply gap to persist through the next decade. The gap is being driven in part by China’s own move to shut down small, low quality, and environmentally damaging producers and focus on quality as well as quantity. Domestic demand is growing fastest at the top end of the mar-ket—it is uncertain whether China can manage to supply both quantity and quality.

China’s meat prices increasingly reflect the true cost of production (including expensive domestic feed grains, high labour costs and environmental impacts) and consumers’ will-ingness to pay for quality and safety assurances. As all prices move higher, there is more space in the market for Australian pork.

5

summary: a window of opportunity for Australian pork

agei

agei

agei

Australia should not wait to get a piece of the large and growing market for pork

Australia should take advantage of its ChAFTA pork victory

Australia can pursue strategic Chinese investments along the pork value chain

Competitors to Australia’s pork industry are making strategic moves to secure their long-term trade relationships in China’s market (for example Denmark’s MOU on organic mutual recognition). China’s own outbound investments into livestock production in Belt and Road countries will further expand global pork supply. If Australia wants to secure market share, now is the time to act.

ChAFTA will eliminate the current 20 percent import tariff on Australian pork in 2019, but without a protocol, pork producers will not benefit from this hard-won concession. China’s willingness to relax tariffs on pork may indicate interest in expanding international supply partnerships; with careful positioning, the 2018 round of ChAFTA negotiations may be an opportunity for progress.

With 16 major importers indicating interest in investing in the Australian pork industry, na-tional and local governments, industry associations, and pig producers have an opportunity to secure investments into farming operations, abattoirs, processors, and logistics facilities. Strategic investors on the Chinese side could help support a coordinated push on market access.

6

1 summary: a window of opportunity 3

2 survey findings: high interest from top importers 7

3 a new vision for feeding China 18

4 commercial market context 25

5 appendices 32 organisation profiles company profiles abbreviations

contents

China Policy

An eight-question survey developed by Australian Pork Limited was sent to high-volume and high-frequency importers by the China Entry-Exit Inspection and Quarantine Association (CIQA) in May and June 2017. The following data was compiled from respondents at 33 companies, running the gamut from boutique importers to China’s second largest pork processor.

Surveys were circulated and responses collected by email and Wechat, a popular Chinese social media tool. The quality and diversity of responses varied widely and indicated high quality, authentic work by CIQA. Surveys were processed and data analysed by China Policy.

survey findings: importers hungry for Australian pork

8

survey findings: overwhelming interest in Australian pork

agei agei

- eleven cite quality, safety, or health - nine cite interest in more products, more diverse prod-

ucts, or more diverse supply channels - seven name Australian meats’ high reputation - five explicitly mention Australian beef

- two cited boar taint - one left little info, but rated safety, health, and taste at 2

out of 5, suggesting possible experience with boar taint - one expressed concerns about price volatility and stabili-

ty of supply. This importer, based in Shenzhen, may have been reacting to current supply conditions (through grey channel) rather than a scenario with market access

- one may not actually be a meat importer (erroneously included)

Eighty-five percent of importers surveyed expressed interest in importing Australian pork. Of these—

Fifteen percent of respondents were not interested in importing Australian pork. Of these—

9

survey findings: top marks on safety, health, natural

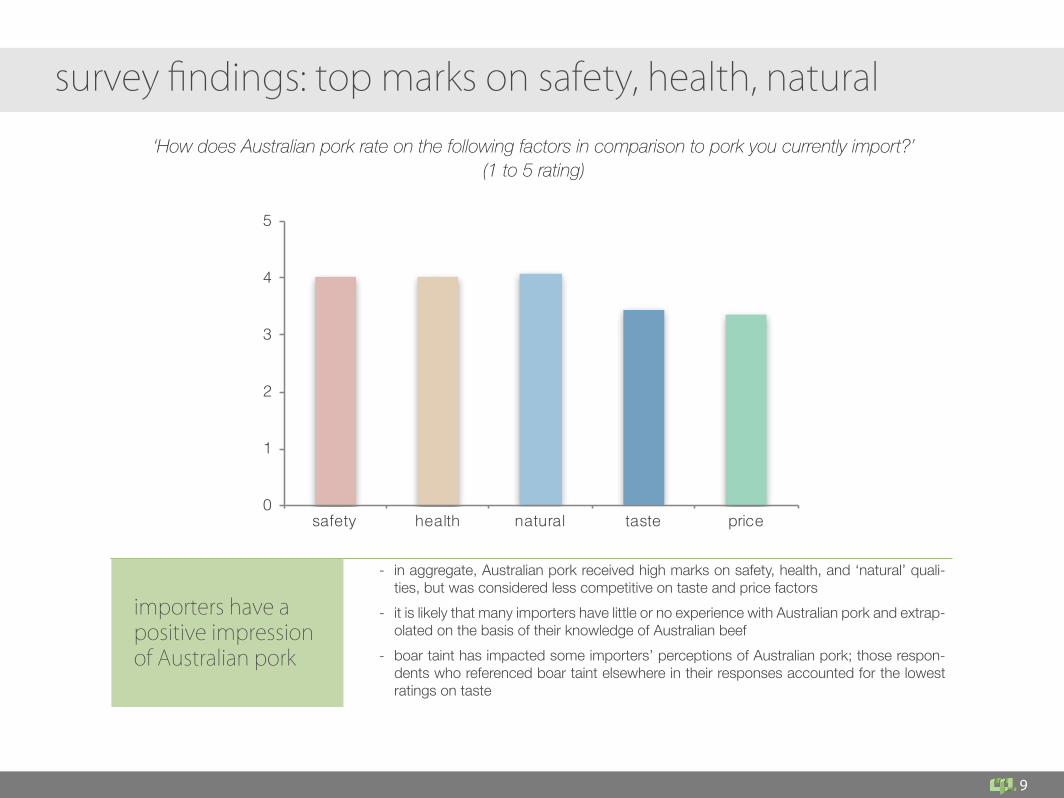

‘How does Australian pork rate on the following factors in comparison to pork you currently import?’(1 to 5 rating)

agei

importers have a positive impression of Australian pork

- in aggregate, Australian pork received high marks on safety, health, and ‘natural’ quali-ties, but was considered less competitive on taste and price factors

- it is likely that many importers have little or no experience with Australian pork and extrap-olated on the basis of their knowledge of Australian beef

- boar taint has impacted some importers’ perceptions of Australian pork; those respon-dents who referenced boar taint elsewhere in their responses accounted for the lowest ratings on taste

0

1

2

3

4

5

safety health natural taste price

10

survey findings: more attractive than many competitors

agei

Australian pork already compares favorably to many competitors

- importers overwhelmingly rated fresh chilled Australian pork as more attractive than Chi-nese produced pork

- Brazil, mired in a food safety scandal that resulted in a temporary ban on all meat imports from the country earlier this spring, provides an interesting comparison case

- the majority of importers are confident Australian pork will be more enticing to domestic consumers than Brazilian pork, but the non-reponse rate still reflects some uncertainty

- Brazilian pork is particularly competitive on price

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

China Brazil Canada USA Germany Denmark Spain

n/a ny

‘If Australian fresh (chilled) pork was air-shipped to China, would it be more attractive than pork from the following countries?’

11

survey findings: spotlight on Spain

Spanish pork enjoyed the best reputation among importers, with over 43 percent confident that it is more attractive to the Chinese market than Australian pork. Interviews with industry players suggest a number of factors are driving Spain’s success in China.

‘If Australian fresh (chilled) pork was air-shipped to China, would it be more attractive than pork from Spain?’

n/a28%

no40%

yes32%

agei

history in China’s market

- Spain has enjoyed market access since a protocol was approved in 2012

- most importers are familiar with its pork as a result

agei

number of approved processors

- Spain has 26 processors approved to export to China

- this supports higher volume and more options for importers

agei

adapting to local needs

- Spanish pork exporters have hired Chinese sales staff

- multiple sources suggest Spain’s industry has been flexible to unique needs and demands from China’s market

12

survey findings: preference for ribs and belly

‘Which cuts of Australian pork are you most interested in importing?’

agei

importers are seeking higher-end cuts from Australia

- ribs and belly cuts are the clear winners, followed by other high value cuts - these responses may be driven less by importers’ knowledge of Australian pork and

more due to perceptions that it is a higher priced or luxury product, in particular due to prior survey questions’ emphasis on chilled (rather than frozen) pork

- while only ten importers expressed interest in offal, those ten importers indicated poten-tial demand for around 200,000 tonnes of Australian pork annually

0

5

10

15

20

25

belly shoulder tenderloin loin ribs legs offal other

13

survey findings: spotlight on offal

Only ten importers indicated interest in offal; however, this list includes some of China’s largest pork processors.

agei

agei

highest volume importers demand offal

Australian offal wins on safety and health

- the ten importers interested in offal described combined demand for around 200,000 tonnes annually

- Yurun Food Group alone suggested import demand of 50,000 tonnes

- food safety risks are more likely to arise from offal than muscle cuts due to the natural function of some organs as a filter and the role of bacteria in the digestive tract

- Australia’s strong reputation for safe, natural, and healthy pork could facilitate supply relationships here

- Australian pork producers have demonstrably lower disease prevalence than US, Brazil, and other volume suppliers

14

survey findings: for gatherings, holidays, and celebrations

The majority of importers still view Australian pork as a special occasion menu item; however, that view is evolving in first tier cities.

‘Will Australian pork be a part of Chinese people’s daily diet? Or will it be a special occasion and group meal menu item?’first-tier city importer responses only

agei

30 percent of importers think Australian pork could be a staple for Chinese consumers

- notably, some of the importers producing inexpensive processed meat products did not indicate Australian pork as a daily menu item, suggesting they would not consider using Australian pork in their cheapest products

- reflects impressions of Australian pork as a pricier choice along with responses that belly, ribs, and other high value cuts might be most in demand

- consumers are increasingly choosing leaner daily menu items; this may present a market-ing opportunity for Australian pork

all importer responses

70%

30%

64%

36% special occasiondaily

15

survey findings: interest from volume importers and channels

‘Which sales channel(s) best suit Australian pork?’

agei

respondents focused on volume sales channels

- importers highlighted wholesale as the primary channel of interest for Australian pork - followed closely by retail and supermarket channels - answers to this question appear to reflect the core business of importers surveyed and

rather than the final consumer-facing sales channel for Australian pork; for further detail on ‘wholesale’ importers, see page 16

02468

101214161820

16

survey findings: spotlight on wholesale and processing

Shuanghui is China’s largest pork importer by volume, totaling over 301,000 tonnes in 2016 according to the company’s own financial reports, nearly 20 percent of all pork imports to China by volume. While Shuanghui was not a survey respondent, the company provides an indicative case of how ‘wholesale’ imports might actually reach the market.

Shuanghui use of imported pork, 2016

source: China Economic News, Shuanghui Annual Report 2016, CP analysis

agei

agei

pork sold to ‘industrial scale’ wholesale importers crosses processing, retail and e-commerce channels

WH Group (Shuanghui International)

- of over 300,000 tonnes pork imported by Shuanghui in 2016, just over 60,000 tonnes were directed towards the company’s own processed meat products - the lion’s share of imports, over 248,000 tonnes, were sold through retail channels. These include

- owned brand channels controlled by Shuanghui itself, including e-commerce channels - supermarkets and other retail channels selling Shuanghui-branded pork - retailers selling Shuanghui-imported pork under other in-house brands

Shuanghui International, renamed name WH Group in 2014, is the world’s largest pork producer and among China’s largest meat pro-cessors. The company’s acquisition of US Smithfield Foods in 2013 was the largest ever Chinese acquisition in the US at the time. The company operates pig farms across China but is primarily known as a supplier of pork and processed meat products under its flagship brand Shuanghui and a number of other labels.

processingretail

17

survey findings: potential investors

Respondents expressed a high degree of interest in investing in Australia’s pork industry. Sixteen respondents suggested they would consider investments. Some gave conditions of ‘only if the opportunity is appropriate’ or ‘interested if initial sales of Australian pork in China go well’. In one case, a respondent that rated Australian pork at the lowest possible level on taste, citing boar taint, still expressed interest in investment opportunities. Below are profiles for three enterprises that expressed interest in investing. For more context on why nearly half of major importers surveyed would consider investing, see ‘pushing agriculture to Go Global’ on page 20.

agei

China Yurun Food Group

Headquartered in Nanjing and listed on the Hong Kong Stock Exchange in 2005, Yurun Group Limited is the number two pork supplier in mainland China, and mainly operates in chilled-frozen meat and processed meat products. The company is well known for its Yurun, Furun, Wangrun, and Popular Meat Packing brands, and its nationwide production network. The company faced financial difficulties in 2015 and 2016 due in part to high pork prices on the domestic market. Still, this processor is among the largest and most credible players in China.

agei

Foresun Group

A major meat processor headquartered in Heilongjiang province in north China’s breadbasket, the company’s core business spans beef and sheepmeat in addition to pork. In 2016 the company acquired three beef abattoirs and a confinement op-eration in Argentina in a US$75 million deal with Brazil’s Margrif Global Foods. The company also operates two beef abattoirs in Australia: Tabro Meats and Moe Meat.

agei

High Hope Group

Set up in 1996 by the Jiangsu Province government with a focus on international trade, this SOE is among China’s 500 largest enterprises, with total revenue ex-ceeding C¥30 billion in 2016 and trade of over US$3 bn in goods. The company operates a meat trading subsidiary, but is primarily a cold chain logistics provider—one of five strategic focuses established during a reform in 2015. Like most large state-owned companies, High Hope is currently under pressure to ‘Go Global’ and has expressed investment interest in the Australian pork industry.

China Policy

Previously domestically oriented and geared towards self-sufficiency, trade has become a core focus of food security strategy. This is part of a strategic shift as China moves from a reactive position to take an active or even leading role in developing global rules and relationships. Moves towards marketisation have been made along the entire pork value chain with more in train, levelling the playing field for competitive international suppliers. The domestic livestock industry, meanwhile, is scrambling to address safety and environmental concerns.

a new vision for feeding China

19

Belt and Road Initiative

Initiated in 2013 and launched with a clear blueprint in 2015, the Belt and Road Initiative (BRI) is a major glo-balisation program focused on greater economic integration, political cooperation, trade, financial integra-tion, and exchange. The name refers to its two key focus areas: the Silk Road Economic Belt that connects China with the Europe via land routes through Russia, Central Asia, South Asia and the Middle East; and the 21st-Century Maritime Silk Road which links China’s coast to both Europe via the South China Sea and the Indian Ocean, and the South Pacific via the South China Sea. In 2016, President Xi Jinping suggested aligning BRI with Australia’s plan to develop its northern region, and specifically mentioned agriculture and livestock. Australia declined to sign a BRI MoU with China during Li Keqiang’s March 2017 visit.

map courtesy Lowy Institute

20

from self sufficiency to food security

agei

China is moving away from ‘self sufficiency’ in food

Changes in China’s food supply strategy indicate that more engagement with global markets is necessary to satisfy its food needs. Alongside measures to secure supply from abroad, domestic policies reflect an increasing departure from ‘self sufficiency’. China openly worries about being unable to produce enough to satisfy people’s needs as it wrestles with ecological limits. China has developed a new strategy to feed its population in the future, necessitating robust and long-term agricultural trade relationships.

agei

pushing agriculture to ‘Go Global’

After a slew of poor-performing overseas investments, China rebranded its efforts to expand internationally as ‘capacity cooperation’ in spring 2015 and set up an inter-ministerial group on agriculture foreign cooperation in summer 2015. In May 2016, State Council issued an internal document outlining principles for the new strategy on global engagement in agriculture. Many were similar to those laid out in the 5-year plan for agricultural devel-opment publicly issued in October 2016. The 5-year plan dedicates a full chapter to international agricultural co-operation, explicitly stating that ‘opening up’ must be a two-way street that conforms with the ideals of ‘win-win’ cooperation and ‘mutual development.’ Under the strategy, major agri- and food-processing enterprises are given policy and regulatory support, discounted financial services, and access to public and private funding in order to pursue international acquisitions and investments and ensure food security. Notable examples include COFCO Agri’s investment into Australian Quattro Ports and ChemChina’s acquisition of Syngenta. Agricultural investments are considered strategic. They have not, so far, been subject to the same restrictions as other more vanity-driven investments in sectors such as football, hotels and entertainment.

21

agei`

from supply to safety and sustainabilityprotecting public health

Food policy is shifting away from meeting calorie demands and towards improving health. National ‘Dietary guidelines for Chinese residents’ were revised in 2016. The recommended amount of fruit, eggs, meat, and poultry decreased slightly—at 14.6-27.4kg/year, the guidelines are not far from National Bureau of Statistics’ estimate of China’s 26.2 kg of red meat (pork, beef and mutton) and 8.4kg of poultry consumption per capita in 2016. However, the NBS estimate differs widely from international reports, such as OECD’s meat consumption estimate of 50 kg per capita in 2015.In late 2016, China’s two highest policy-making bodies issued a ‘Healthy China 2030 plan’. Topics included public health services, environmental management, the medical industry, food and pharmaceutical safety, and physical fitness. The plan targets food trade in particular, tightening management of imported food, improving safety inspection systems for foreign food, and setting up designated ports for food import.

22

agei

ensuring safety, farm to table

In response to continuing consumer concerns over food safety, China revised its Food Safety Law in late 2015, mandating a food traceability system for producers and sellers. In April 2017, China Food and Drug Administration (CFDA) published a list of food trace-ability data requirements, mandating companies keep records on procurement, processing, storage, transportation and sale. Large food processors, wholesalers and retail companies will bear the brunt of legal responsibility (and liability).Internationally, AQSIQ has passed the buck to trade partners, requiring ‘traceability to origin’ with varying degrees of success. Ministry of Commerce (MofCOM), also on the hook for traceability initiatives across a broader spectrum of products, kicked off a massive, technically intensive pilot across 58 cities in four provinces in 2016, covering meat, vegetables and liquor.

from supply to safety and sustainability

23

from supply to safety and sustainabilityagei

acknowledging environmental constraints

MoA and Ministry of Environmental Protection moved to reduce the ecological footprint of China’s livestock industry by designating areas prohibited for livestock and poultry farming in late 2016, including watersheds, conservation areas, and cities. Over ten percent of the domestic swine herd will be relocated by 2018 under the policy, according to China Animal Agriculture Association.Aimed first and foremost at addressing the environmental impacts of the livestock industry, the move has also allowed regulators a leverage point to push consolidation and relocate farms away from urban areas, towards underdeveloped provinces, and closer to sources of feed grains like corn. Perhaps unsurprisingly, livestock prohibited areas fall heavily within provinces and regions targeted for reduction by MoA’s National Hog Production Plan (2016-20).

24

from government- to market-led

agei

an increasingly market approach

With more market forces in play, China’s meat prices increasingly reflect the true cost of production (including expensive domestic feed grains, high labour costs and environmental impacts) and consumers’ willingness to pay for quality and safety assurances. Pork prices are highly sensitive for the Chinese government. They see import and use of a strategic food reserve as the most important tools to control inflation under the increasingly marketised food supply system.

agei

controlling commodities through exchange centres

As the state moves away from price controls and towards marketisation of feed grains, live hogs, and pork alike, leaders have seized upon commodities markets as a market-based alternative for predicting and controlling prices. The Dalian Commodities Exchange (DCE) launched a price index for fresh lean pork in March 2017, a move widely seen as a precursor to futures trading. DCE is actively developing futures for live hogs as well. These centres, trad-ing in RMB, are likely to open up for global trade. The Chicago Mercantile Exchange with futures denominated in USD, will be their biggest competitor.

agei

changing the game for domestic farmers and processors

Regulators, academics, and China’s largest pork processors are advocating for the launch of live hog futures markets, widely expected before year’s end. Officials believe clearer price signals will help address volatility and re-quirements to deliver on futures contracts will advantage larger-scale operations. Pig farmers and pork processors also note reduced volatility, and are keen to take advantage of risk hedging.

agei

driven by evolving consumer demand

Sales of pork fell slightly in 2015 and 2016 by volume, according to data from research firm Euromonitor. Industry analysts point to health concerns as a primary factor here and note high and rising demand for top quality and organic pork, as well as products pitching safety and traceability claims. Consumers are also making healthier choices, evidenced by rising vegetable consumption. Catering companies in first- and second-tier cities report shifting diets, with white collar workers at office cafeterias choosing around ten percent less meat and replacing it with ten percent more vegetables.

China Policy

China’s market for pork is evolving rapidly as incomes rise and diets diversify. Preferences vary widely across regions and between first tier and less developed markets, but consumers are converging on safety, health and convenience as key factors driving demand. Other trade partners are competing for a large and growing piece of the pie with a variety of strategies and selling points.

commercial market context

26

China’s pork consumption habits are highly varied

China covers a land area more than twice the size of the European Union, with comparable diversity in culinary tradition. Preferences on cuts and flavour differ widely, as does preparation technique. The wide variety of cui-sines across China, coupled with the large urban population, present unique opportunities.

Shanghai alone is home to over 24 million people—comparable to the entire Australian market. If consumers in just one province or region prefer Australian pork, or a single major processor or supermarket chain decides to procure it, that alone will provide a sizable and profitable export market.

27

China’s food market is highly regionalDiversity impacts meat preferences, with traditionally Muslim and cattle–producing regions in the north and west demanding less pork in general. While this geographic diversity must be heeded while developing a marketing strategy, it also ensures many diverse markets for Australian pork.

Developed areas of southern central China have the highest levels of meat consumption per capita. Urban coastal areas, while af-fluent, supplement their meat consumption with seafood, not included here. While there is some variance, pork still dominates the Chinese diet due to consumer preferences and as cost factors.

beefpork

lamb

China’s per capita meat consumption by province

source: china beef, sheep/goat industry report 2015

28

China’s pork market is tiered

advanced cities developing cities emerging cities lagging cities

annual income category

affluent

mainstream

value

low-income

4 3

88

67

12

6

24

71

516

2000 2010 2020

11 6 4

8886

22

5

67

7

2000 2010 2020

2515 9

7581

44

43

4

2000 2010 2020

4733

17

53

64

56

24

2000 2010 2020

China NBS 2015 data, McKinsey analysis

Rapidly rising incomes, especially in second and third tier cities, have produced a large and growing middle class. Chinese consumers spend a higher percentage of their income on food than the global average due to domestic food safety and quality concerns as well as a cultural tradition closely linking food and medicine.

affluent = >$34,000; mainstream = $16,000-34,000; value = $6,000 - $15,999; low-income = <$6,000

13 cities 27% of urban GDP 15% of urban population

80 cities 35% of urban GDP 26% of urban population

369 cities 33% urban GDP 45% of urban population

188 cities 5% of urban GDP 14% of urban population

29

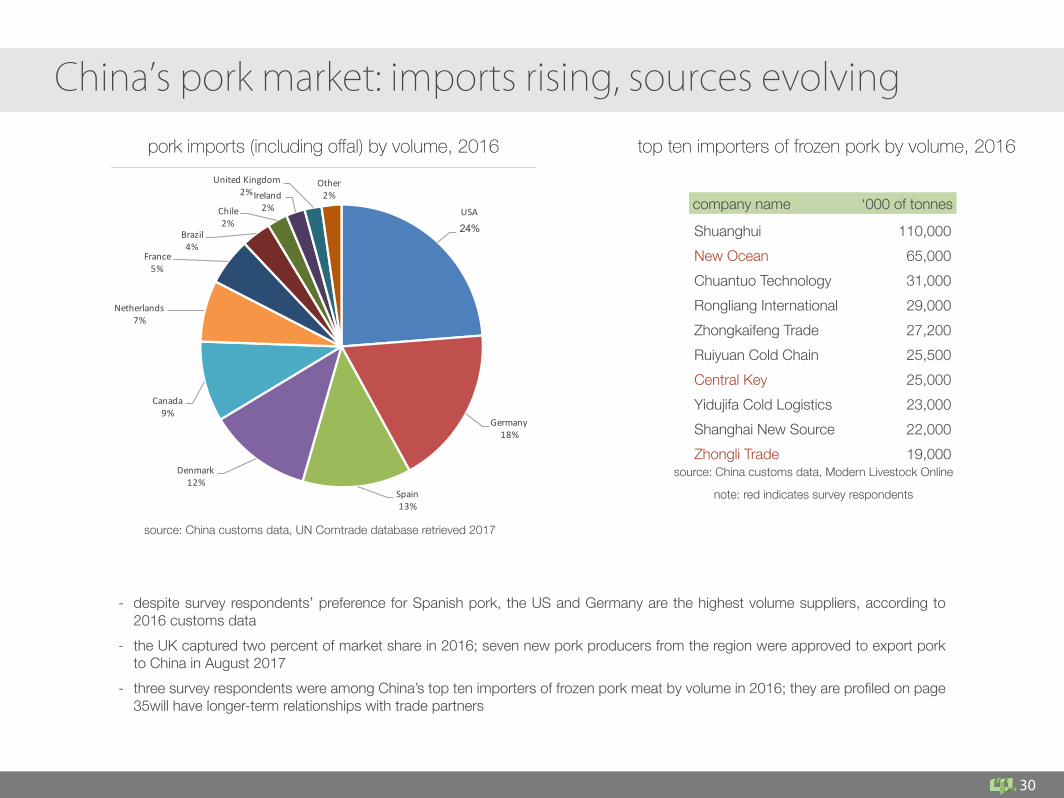

China’s pork market: imports rising, sources evolving

- imports have risen steeply over five years; market share has continued to evolve between major trade partners - who leads by volume and value varies year to year and on the basis of product mix - Spain and Germany have seen particularly steep rises in imports by value as opposed to slower growth paths from low-cost sup-

pliers like US, Canada, and Brazil - market structure is currently fluid and expanding rapidly; as growth slows, import patterns may become less flexible because im-

porters will have longer-term relationships with trade partners

2012 2013 2014 2015 2016US$0million

US$200million

US$400million

US$600million

US$800million

US$1000million

US$1200million

US$1400million

US$1600million

2012 2013 2014 2015 2016

source: China customs data, UN Comtrade database retrieved 2017

pork meat imports by value all pork imports (including offal) by value

top 10 trade partners

30

China’s pork market: imports rising, sources evolving

pork imports (including offal) by volume, 2016 top ten importers of frozen pork by volume, 2016

USA

24%

Germany18%

Spain13%

Denmark12%

Canada9%

Netherlands7%

France5%

Brazil4%

Chile2%

Ireland2%

UnitedKingdom2%

Other2%

company name ‘000 of tonnes

Shuanghui 110,000New Ocean 65,000Chuantuo Technology 31,000Rongliang International 29,000Zhongkaifeng Trade 27,200Ruiyuan Cold Chain 25,500Central Key 25,000Yidujifa Cold Logistics 23,000Shanghai New Source 22,000Zhongli Trade 19,000

note: red indicates survey respondents

source: China customs data, UN Comtrade database retrieved 2017

- despite survey respondents’ preference for Spanish pork, the US and Germany are the highest volume suppliers, according to 2016 customs data

- the UK captured two percent of market share in 2016; seven new pork producers from the region were approved to export pork to China in August 2017

- three survey respondents were among China’s top ten importers of frozen pork meat by volume in 2016; they are profiled on page 35will have longer-term relationships with trade partners

source: China customs data, Modern Livestock Online

31

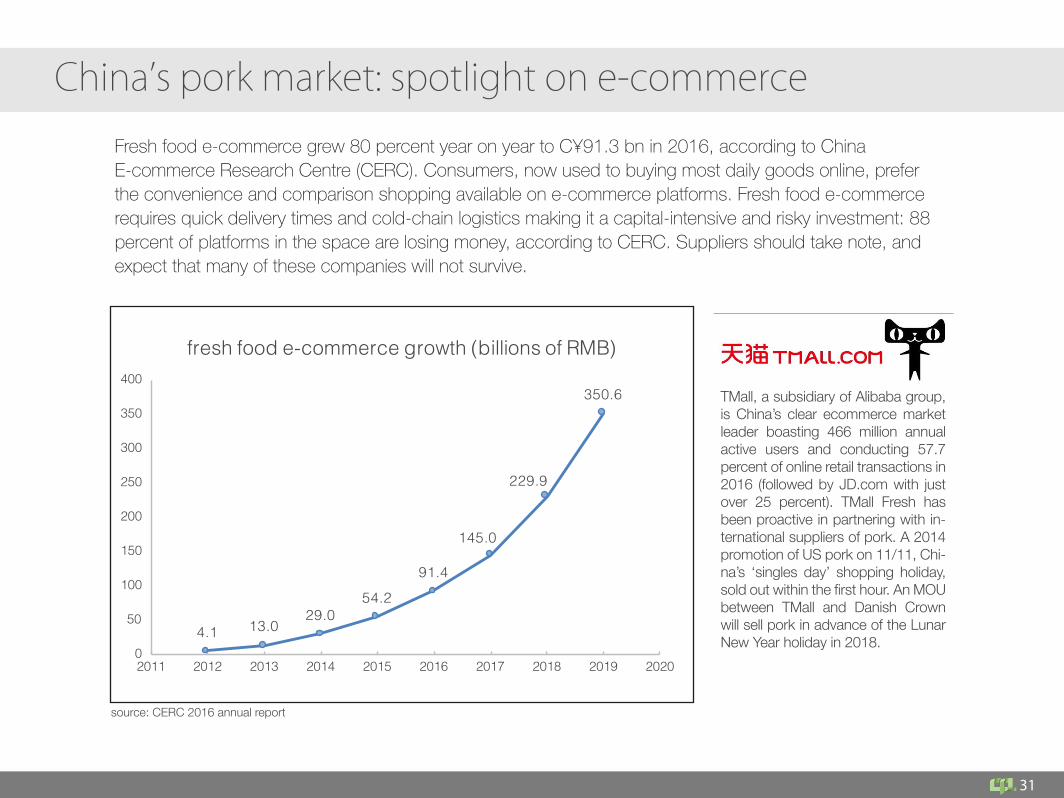

China’s pork market: spotlight on e-commerce

Fresh food e-commerce grew 80 percent year on year to C¥91.3 bn in 2016, according to China E-commerce Research Centre (CERC). Consumers, now used to buying most daily goods online, prefer the convenience and comparison shopping available on e-commerce platforms. Fresh food e-commerce requires quick delivery times and cold-chain logistics making it a capital-intensive and risky investment: 88 percent of platforms in the space are losing money, according to CERC. Suppliers should take note, and expect that many of these companies will not survive.

4.1 13.029.0

54.291.4

145.0

229.9

350.6

0

50

100

150

200

250

300

350

400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

fresh food e-commerce growth (billions of RMB)

TMall, a subsidiary of Alibaba group, is China’s clear ecommerce market leader boasting 466 million annual active users and conducting 57.7 percent of online retail transactions in 2016 (followed by JD.com with just over 25 percent). TMall Fresh has been proactive in partnering with in-ternational suppliers of pork. A 2014 promotion of US pork on 11/11, Chi-na’s ‘singles day’ shopping holiday, sold out within the first hour. An MOU between TMall and Danish Crown will sell pork in advance of the Lunar New Year holiday in 2018.

source: CERC 2016 annual report

China Policy

appendix

33

associations and organisations of note

agei

China Meat Association

Consisting of members in processed meat products, packaging ma-terials, cold chain logistics, animal feeds and machinery, CMA partici-pates in shaping food safety standards and has traditionally been su-pervised by the State-owned Assets Supervision and Administration Commission . It promotes an outward-oriented meat industry.

agei

China Entry-Exit Import and Quarantine Association (CIQA)

CIQA is a state-sponsored association that includes enterprises, institutions, individuals and other organisations involved in admin-istration of inspection and quarantine nationwide. It aims to play a bridge role between government and other entities engaged in trade to encourage safety, quality and effective economic development. The association is supervised by both the Ministry of Civil Affairs and the General Administration of Quality Supervision, Inspection and Quarantine (AQSIQ), China’s national quality regulator.

agei

China Animal Agriculture Association

A non-profit consisting of members in animal husbandry, CAAA is overseen by MoA and plays a role in product quality authentication, international cooperation and policy recommendation for govern-mental agencies. China Cattle Industry Association and China Sheep & Goat Industry Association are 2 (of 11) of its sub-chambers. They provide research and references for government policy, recommend high-quality breeding varieties, and assist in export and import work.

34

agei

leading domestic pork producers and processors

Jinluo Meat Products Co.

Among China’s largest traditional pork processors, with annual pro-cessing of over three million tonnes, the company’s products are car-ried widely across convenience stores and supermarkets. While treat-ed as a domestic player, Jinluo is technically a subsidiary of a larger conglomerate, People’s Food Holdings Ltd., registered in Bermuda and publicly listed in Singapore. Jinluo is known domestically for its ‘no starch’ packaged hams, indicating a move up the value chain from the most basic processed meat categories. In spring 2017, the com-pany was sued by Yurun over alleged copying of sausage package design.

agei

New Hope Group

Established in Sichuan by ‘Mr. Feed’ Liu Yonghao in the 1980s, New Hope Group, through its listed subsidiary Liuhe is China’s largest feed and meat processing company, primarily in pork. It has aggres-sively expanded business from feed into protein, aiming to become the global leader by 2030. Its acquisitions include Kilcoy Pastoral Company, Australia’s fourth largest beef processor. It has pledged to invest C¥17 bn in global production bases over the next three to five years targeting Australia, New Zealand, USA, Europe and South East Asia.

agei

WENS Foodstuffs Group

China’s largest livestock farming company, WENS Food Group oper-ates 239 subsidiaries across 20 provinces and regions. In 2016, the company earned C¥59.4 bn in revenue and managed a commercial swine herd of over 17 million head. The company is also among the world’s largest producers of livestock feed, with over 6 million tonnes feed produced in 2015. Net profits at WENS fell over 74 percent y-o-y in H1 2017 as pork prices fell from record highs in 2016 to four year lows in 2017. The price of feed fell simultaneously, mitigating losses at WENS and other large, vertically integrated pig farming companies.

35

agei

leading domestic pork producers and processors

Zhongli Trading

Founded in 1999, the company was China’s tenth largest importer of frozen pork in 2016, moving 19,000 tonnes into the domestic market. In addition to pork, the company trades in coconut oil, wine, cocoa, dairy, and waste paper for the recycling market. The company does not maintain a web presence, however, reflecting the degree to which major importers continue to do business based on personal relation-ships, with partnerships developed at trade shows and by word of mouth.

agei

New Ocean Logistics

Founded in 2009, Qingdao-headquartered New Ocean is primarily a meat trade logistics provider, importing meat on behalf of dozens of domestic wholesalers and processors. It was China’s second largest importer of frozen pork in 2016. In addition to maintaining current import licenses and supply relationships with hundreds of approved meat exporters, the company controls vast cold warehousing ca-pacity and provides financial services and imported meat futures contracts to domestic business partners.

agei

Central Key

China’s seventh largest frozen pork importer in 2016, Central Key also holds licenses to import technical products. Another logis-tics-focused importer, the company sources a broad range of frozen meat and poultry products from Europe, Australia and the Americas.

36

abbreviationsTermGeneral Administration of Quality Supervision, Inspection and Quarantine

billion

China-Australia Free Trade Agreement

China National Chemical Corporation

China Entry-Exit Inspection and Quarantine Association

China National Cereals, Oils and Foodstuffs Corporation

Ministry of Agriculture

memorandum of understanding

Organisation for Economic Co-operation and Development

State-owned Assets Supervision and Administration Commission of the State Council

state-owned enterprise

Belt and Road Initiative

Chicago Mercantile Exchange

China Animal Agriculture Association

China Cattle Industry Association

China E-Commerce Research Centre

China Food and Drug Administration

China Meat Association

China National Bureau of Statistics

China Sheep & Goat Industry Association

Chinese Academy of Agricultural Sciences

Dalian Commodities Exchange

European Union

Hong Kong Stock Exchange

Ministry of Civil Affairs

Ministry of Commerce

Ministry of Environmental Protection

AbbreviationAQSIQ

bn

ChAFTA

ChemChina

CIQA

COFCO

MoA

MOU

OECD

SASAC

SOE

BRI

CME

CAAA

CCIA

CERC

CFDA

CMA

NBS

CSGIA

CAAS

DCE

EU

HKSE

MCA

MofCOM

MEP