chinabank 2004

TRANSCRIPT

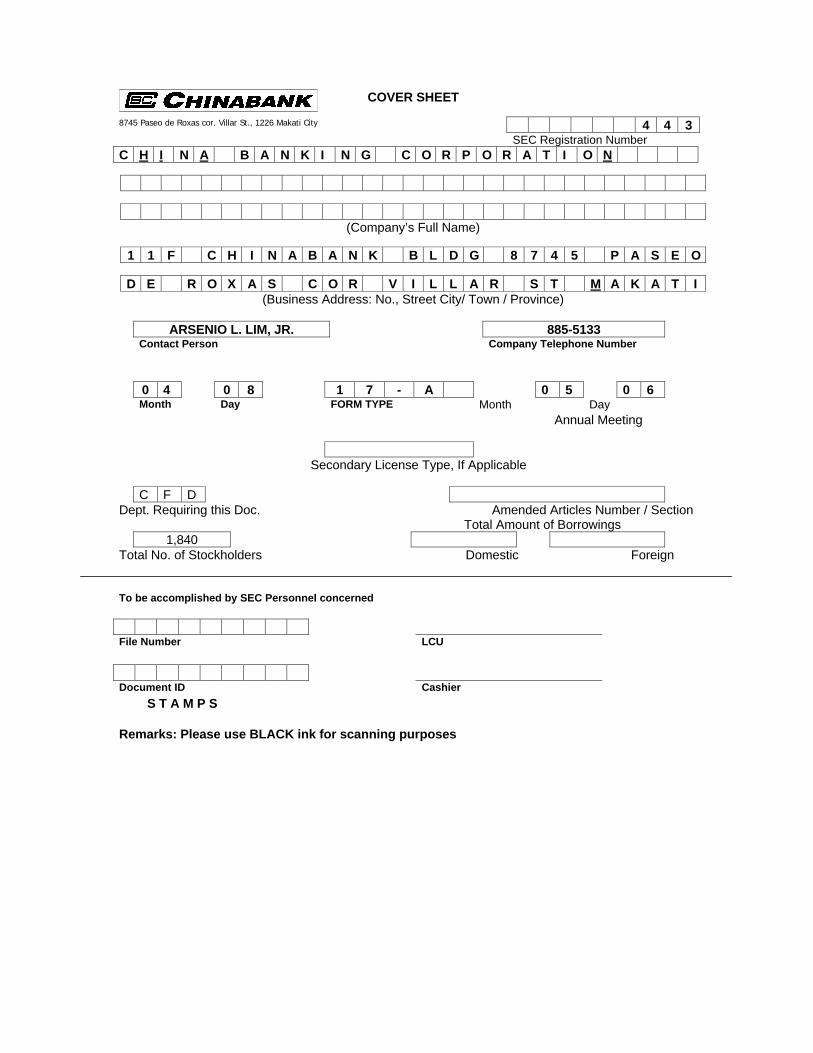

COVER SHEET

4 4 3SEC Registration Number

C H I N A B A N K I N G C O R P O R A T I O N

(Company’s Full Name)

1 1 F C H I N A B A N K B L D G 8 7 4 5 P A S E O

D E R O X A S C O R V I L L A R S T M A K A T I(Business Address: No., Street City/ Town / Province)

ARSENIO L. LIM, JR. 885-5133Contact Person Company Telephone Number

0 4 0 8 1 7 - A 0 5 0 6Month Day FORM TYPE Month Day

Annual Meeting

Secondary License Type, If Applicable

C F DDept. Requiring this Doc. Amended Articles Number / Section

Total Amount of Borrowings1,840

Total No. of Stockholders Domestic Foreign

To be accomplished by SEC Personnel concerned

File Number LCU

Document ID Cashier

S T A M P S

Remarks: Please use BLACK ink for scanning purposes

8745 Paseo de Roxas cor. Villar St., 1226 Makati City

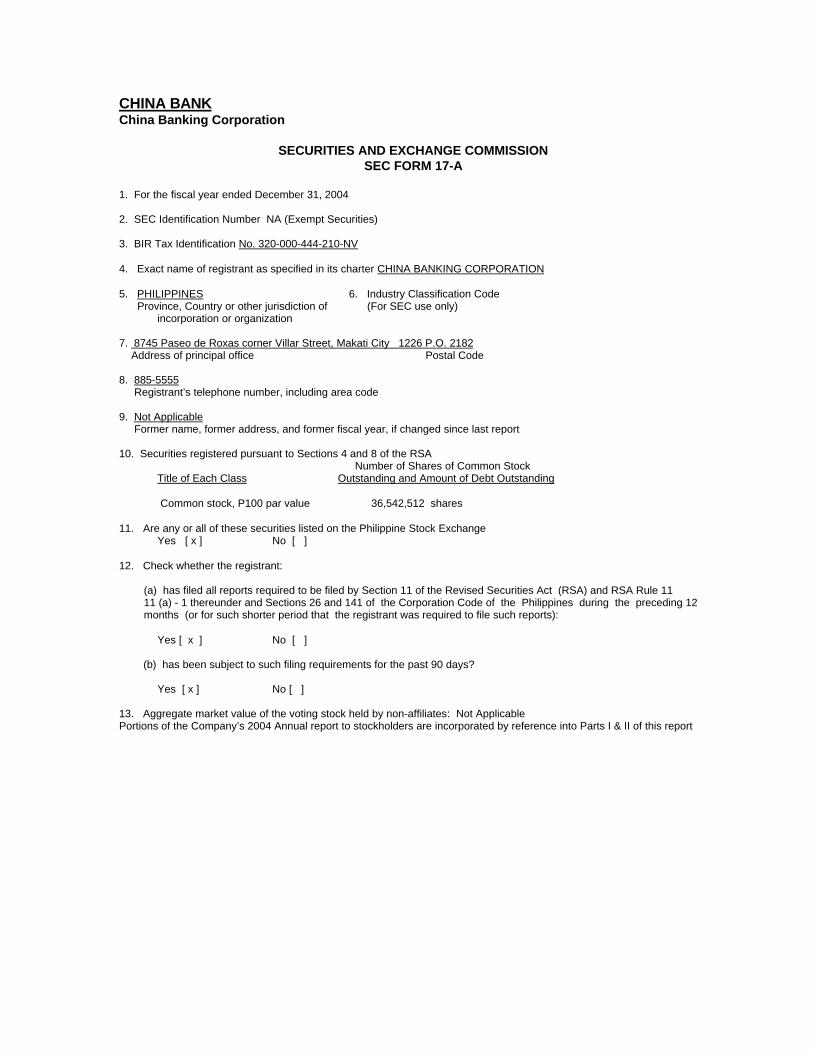

CHINA BANKChina Banking Corporation

SECURITIES AND EXCHANGE COMMISSIONSEC FORM 17-A

1. For the fiscal year ended December 31, 2004

2. SEC Identification Number NA (Exempt Securities)

3. BIR Tax Identification No. 320-000-444-210-NV

4. Exact name of registrant as specified in its charter CHINA BANKING CORPORATION

5. PHILIPPINES 6. Industry Classification Code Province, Country or other jurisdiction of (For SEC use only)

incorporation or organization

7. 8745 Paseo de Roxas corner Villar Street, Makati City 1226 P.O. 2182 Address of principal office Postal Code

8. 885-5555 Registrant’s telephone number, including area code

9. Not Applicable Former name, former address, and former fiscal year, if changed since last report

10. Securities registered pursuant to Sections 4 and 8 of the RSA Number of Shares of Common Stock

Title of Each Class Outstanding and Amount of Debt Outstanding

Common stock, P100 par value 36,542,512 shares

11. Are any or all of these securities listed on the Philippine Stock ExchangeYes [ x ] No [ ]

12. Check whether the registrant:

(a) has filed all reports required to be filed by Section 11 of the Revised Securities Act (RSA) and RSA Rule 1111 (a) - 1 thereunder and Sections 26 and 141 of the Corporation Code of the Philippines during the preceding 12months (or for such shorter period that the registrant was required to file such reports):

Yes [ x ] No [ ]

(b) has been subject to such filing requirements for the past 90 days?

Yes [ x ] No [ ]

13. Aggregate market value of the voting stock held by non-affiliates: Not ApplicablePortions of the Company’s 2004 Annual report to stockholders are incorporated by reference into Parts I & II of this report

CHINA BANKING CORPORATION SECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

PART I BUSINESS AND GENERAL INFORMATIONITEM 1. BUSINESSHistorical Background. China Bank was incorporated on July 20, 1920 and commenced business on August 16 of the sameyear as the first privately owned local commercial bank in the Philippines.

China Bank was listed on the local stock exchange in 1947 and became the first bank in Southeast Asia to process depositaccounts on-line in 1969, and the first Philippine bank to offer telephone banking in 1988. The Bank acquired its universalbanking license in 1991.

China Bank provides a wide range of domestic and international banking services and is one of the largest commercialbanks in the country in terms of assets and capital.

Business Milestones. Within a business arena dominated by intensified competition for market share, narrowing tradingmargins and regulatory pressure, in 2004, China Bank had a 3rd straight year of record income as it posted a profit after taxof P2.72 billion from P2.62 billion income in 2003. Another key financial milestone for 2004 was the P 11.9 billion increase inloans, its fastest pace in seven years. Comprehensive collection and restructuring efforts also cut past due loan level by P1.2 billion and non-performing loan ratio to 11.40% from 14.68%. CASA deposit base reached a new high of P 21.7 billion,with broader retention rates for newly acquired accounts. The launching of our CASA revival program last November shouldreinvigorate the thrust to build-up traditional funding sources. Return on owners’ equity after appraisal increment of 14.37%again surpassed industry benchmarks. Similarly, our exceptional capital adequacy ratio of 32.74% is reflective of the Bank’sstatus as one of the best capitalized banks in the industry. These indicators were among the key factors that underpinnedthe decision of credit rating agencies Fitch Ratings & Capital Intelligence to retain China Bank’s credit rating at C/D and BB-,respectively.

Despite an exigent environment, China Bank remained vigilant for fresh opportunities to improve market share andconsolidate its presence as a multi-category service provider. We clearly defined China Bank’s value to customers as theability to offer superior access to services and a selection of competitively priced fund- and fee-based products. In terms ofcustomer service delivery & profitability, the evaluation of our banking channel economics merited greater attention lastyear, as shifting clients to more convenient electronic channels would be mutually beneficial in the long-run. Given theconstraints on the opening of new branches, China Bank’s ATM network was expanded to 188 locations, while broadeningthe suite of available ATM- & Tellerphone-based services. By capturing client transactions across multiple touchpoints, ournon-traditional income streams were maximized. On the corporate banking side, our newly established cash managementunit became a significant engine for acquisition of business clients besides capturing payments flows from existingaccounts. Check warehousing was introduced in the middle of 2004 to complement our bills & tax payments services.

For retail banking, the centerpiece for 2004 was the implementation of the branch-based marketing program throughout thenetwork. By institutionalizing a set of quantifiable and consistent measures for all branches, network performance could bebetter monitored and targeted toward desired segments – maximizing the business potentials at each area. Establishmentof key metrics at all retail levels ensures that selling and cross-selling efforts become a collective responsibility. Given theconstraints on the opening of new branches, network expansion focused on in-branch and off-branch ATMs.

The Bank received recognition as “Outstanding Commercial Bank” by the Consumer Union of the Phils for 2004 and alsoby Parangal ng Bayan Foundation, Inc., National Consumer Excellence Awards for 2005. The Bank also launched thisyear its “Grateful at 85” promo in preparation for its 85th anniversary in 2005.

For improved client recall and to better highlight the affiliation with China Bank, the subsidiary company officially changed itsname from CBC Insurance Brokers, Inc. to Chinabank Insurance Brokers, Inc. Building on its strong performance from theprevious years, Chinabank Insurance Brokers, Inc. capped the year 2004 with business strategies and accomplishmentsgeared towards achieving business efficacy and customer satisfaction. The new name also signifies a new identity thatechoes the China Bank brand – “your success is our business” and “banking with principles”. The launch of the “My GreatLife Dollar Plan” paved the way for Chinabank Insurance’s first dollar denominated life insurance which is also aninvestment product.CHINA BANKING CORPORATION

SECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

This product innovation was introduced and offered in partnership with another industry leader, Great Pacific Life(GrepaLife) of the Yuchengco Group of Companies. Motor car insurance business was also reinforced by improving theclaims monitoring and service process turnaround. Their linkage with China Bank’s Consumer Banking Group Auto Loans’current computer system allows for a seamless service delivery system for motor car quotations.

Realizing the significant role technology plays in uninterrupted banking service to clients, China Bank – Properties andComputer Center, Inc. (CBC-PCCI) focused on providing the groundwork necessary to deliver effective and secure productsand services to clients and users. These are all attuned to the rapid technological changes in the industry.

For 2004, the Group implemented e-banking as China Bank’s answer to the demands of the advances in the internetbanking front. Technology Group put in place network security for Internet banking. This resulted in the certification ofexternal auditor SGV of our Bank upon passing the Network Assessment & Vulnerability Test or Ethical Hacking. TheGroup also successfully backed up the Online Clearing System accessed by unlimited users and which also links our MetroManila and provincial branches to the government institution, Philippine Clearing House. There were other significant ITprojects - Trade, Trust and Consumer which supported the overall positive performance of the Bank. Lastly, more tellerterminals in the branches were converted to Mosaic NT, the latest generation of software which allows for automaticupgrading and troubleshooting over the network.

CBC Forex Corp., another subsidiary of China Bank which handles the Bank’s business of dealing and broking in allcurrencies, registered a net income of P5.49 million in 2004.

(1) Business of Issuer

Principal Products and Services. The Bank’s products and services include deposits and related services, internationalbanking services, loans and credit facilities, trust, investment services, insurance products and other services such asacceptance of various bill payments and donations to charitable institutions. The income from these products/services aredivided into two categories, namely (1) interest income from the Bank’s deposit taking and lending/investment activitieswhich accounts for 80% of revenues and (2) other income (includes service charges, fees & commissions, trading gain,foreign exchange gain, trust fees, income from sale of acquired assets and other miscellaneous income) which account for20% of revenues.

Distribution Network. As of end 2004, China Bank distributed its products and services through its 141 branch network with79 branches in Metro Manila and 62 in the provinces. In 2004, Santiago City branch was opened in Feb. and two (2)branches were relocated namely Cebu-Banilad Branch and Cubao-Araneta Branch in order to improve network productivity,operational efficiency and customer service.

The Banks’ ATM service, known as CBC Tellercard, complements the branch network in delivering services to itscustomers. As of end 2004, there were 188 ATMs nationwide Twenty three (23) ATMs were installed this year, namely:(1) Dipolog Center Mall; (2) Gilmore IT Center; (3) Power Plant R3; (4) Market! Market! 1; (5) Medical City; (6) Pacific Mall;(7) Greenbelt 3; (8) Caltex SLX 1; (9) SM City-Marilao; (10) SM City-Batangas; (11) SM City-Baguio; (12) Malanday Branch;(13) Market! Market! 2; (14) Metropoint Mall; (15) Robinson’s Galleria; (16) Lorma Hospital; (17) Greenhills Lifestyle Center;(18) Alabang Mall; (19) Greenhills Theater Mall; (20) Gaisano Mall; (21) Glorietta 1; (22) Rockwell-Loft and (23) Shopwise-Araneta. As a founding member of the BancNet consortium, TellerCard holders have access to more than 3,000 ATMsnationwide of both BancNet and Megalink networks.

Status of New Products/Services. By 2004, China Bank offered and launched investment and cash managementproducts. The line of investment products included high-yielding instruments Money L.I.F.T. (Long-term Investment Free ofTax)-2 months and Diamond Savings Account, a term deposit product supported by a passbook. These high-yieldinginvestment options are available through its 141 branches nationwide. Consumer products such as the Contract to Sell(CTS) financing and salary loan were also offered this year. Cash management products were further boosted with thelaunching of the BIR Tax Payments (eFPs or electronic Filing and Payment system), payroll processing service, PDC’swarehousing and auto-debit arrangement.CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

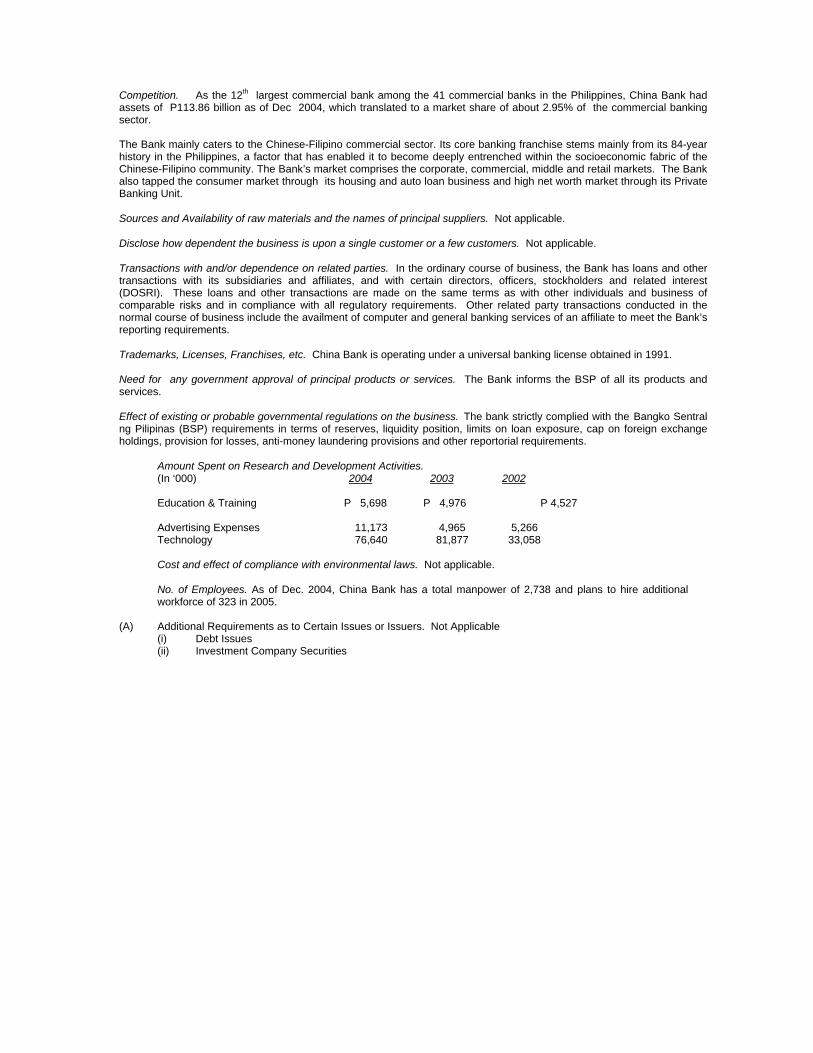

Competition. As the 12th largest commercial bank among the 41 commercial banks in the Philippines, China Bank hadassets of P113.86 billion as of Dec 2004, which translated to a market share of about 2.95% of the commercial bankingsector.

The Bank mainly caters to the Chinese-Filipino commercial sector. Its core banking franchise stems mainly from its 84-yearhistory in the Philippines, a factor that has enabled it to become deeply entrenched within the socioeconomic fabric of theChinese-Filipino community. The Bank’s market comprises the corporate, commercial, middle and retail markets. The Bankalso tapped the consumer market through its housing and auto loan business and high net worth market through its PrivateBanking Unit.

Sources and Availability of raw materials and the names of principal suppliers. Not applicable.

Disclose how dependent the business is upon a single customer or a few customers. Not applicable.

Transactions with and/or dependence on related parties. In the ordinary course of business, the Bank has loans and othertransactions with its subsidiaries and affiliates, and with certain directors, officers, stockholders and related interest(DOSRI). These loans and other transactions are made on the same terms as with other individuals and business ofcomparable risks and in compliance with all regulatory requirements. Other related party transactions conducted in thenormal course of business include the availment of computer and general banking services of an affiliate to meet the Bank’sreporting requirements.

Trademarks, Licenses, Franchises, etc. China Bank is operating under a universal banking license obtained in 1991.

Need for any government approval of principal products or services. The Bank informs the BSP of all its products andservices.

Effect of existing or probable governmental regulations on the business. The bank strictly complied with the Bangko Sentralng Pilipinas (BSP) requirements in terms of reserves, liquidity position, limits on loan exposure, cap on foreign exchangeholdings, provision for losses, anti-money laundering provisions and other reportorial requirements.

Amount Spent on Research and Development Activities.(In ‘000) 2004 2003 2002

Education & Training P 5,698 P 4,976 P 4,527

Advertising Expenses 11,173 4,965 5,266 Technology 76,640 81,877 33,058

Cost and effect of compliance with environmental laws. Not applicable.

No. of Employees. As of Dec. 2004, China Bank has a total manpower of 2,738 and plans to hire additionalworkforce of 323 in 2005.

(A) Additional Requirements as to Certain Issues or Issuers. Not Applicable(i) Debt Issues(ii) Investment Company Securities

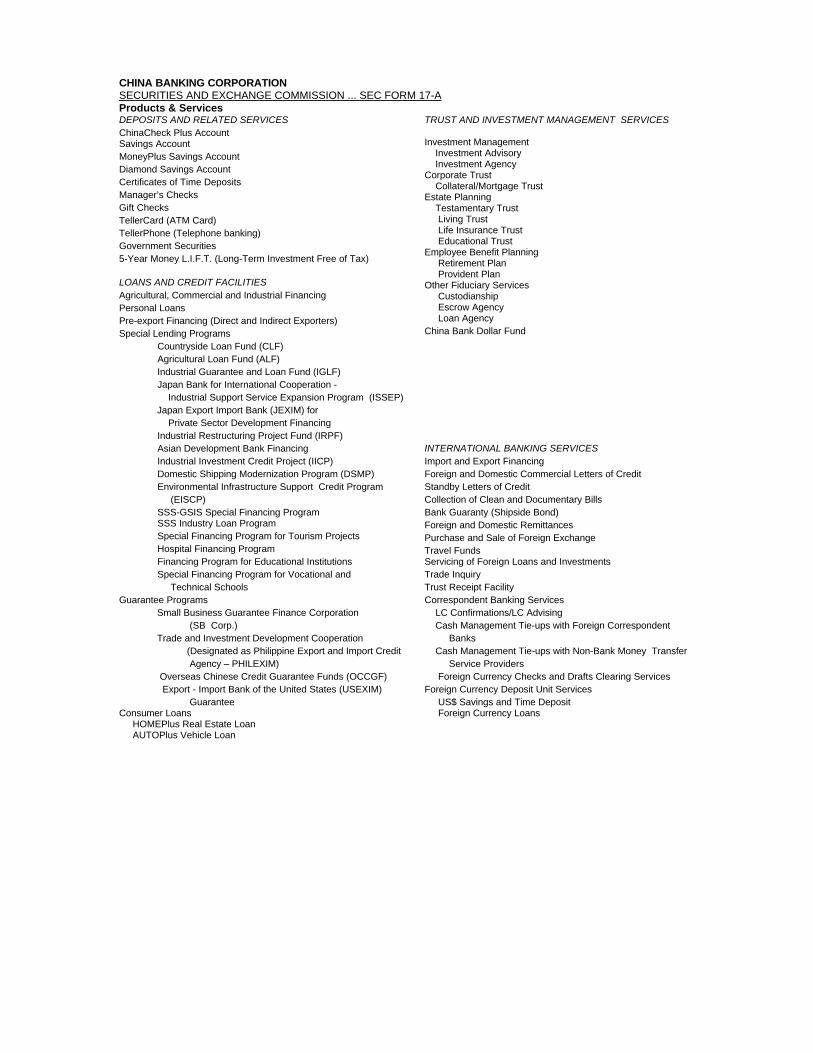

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-AProducts & ServicesDEPOSITS AND RELATED SERVICESChinaCheck Plus AccountSavings AccountMoneyPlus Savings AccountDiamond Savings AccountCertificates of Time DepositsManager’s ChecksGift ChecksTellerCard (ATM Card)TellerPhone (Telephone banking)Government Securities5-Year Money L.I.F.T. (Long-Term Investment Free of Tax)

LOANS AND CREDIT FACILITIESAgricultural, Commercial and Industrial FinancingPersonal LoansPre-export Financing (Direct and Indirect Exporters)Special Lending Programs

Countryside Loan Fund (CLF)Agricultural Loan Fund (ALF)Industrial Guarantee and Loan Fund (IGLF)Japan Bank for International Cooperation - Industrial Support Service Expansion Program (ISSEP)

Japan Export Import Bank (JEXIM) for Private Sector Development FinancingIndustrial Restructuring Project Fund (IRPF)

TRUST AND INVESTMENT MANAGEMENT SERVICES

Investment Management Investment Advisory Investment AgencyCorporate Trust Collateral/Mortgage TrustEstate Planning Testamentary Trust Living Trust Life Insurance Trust Educational TrustEmployee Benefit Planning Retirement Plan Provident PlanOther Fiduciary Services Custodianship Escrow Agency Loan AgencyChina Bank Dollar Fund

Asian Development Bank FinancingIndustrial Investment Credit Project (IICP)Domestic Shipping Modernization Program (DSMP)Environmental Infrastructure Support Credit Program

(EISCP)SSS-GSIS Special Financing ProgramSSS Industry Loan ProgramSpecial Financing Program for Tourism ProjectsHospital Financing ProgramFinancing Program for Educational InstitutionsSpecial Financing Program for Vocational and

Technical SchoolsGuarantee Programs Small Business Guarantee Finance Corporation (SB Corp.) Trade and Investment Development Cooperation (Designated as Philippine Export and Import Credit Agency – PHILEXIM) Overseas Chinese Credit Guarantee Funds (OCCGF) Export - Import Bank of the United States (USEXIM) GuaranteeConsumer Loans HOMEPlus Real Estate Loan AUTOPlus Vehicle Loan

INTERNATIONAL BANKING SERVICESImport and Export FinancingForeign and Domestic Commercial Letters of CreditStandby Letters of CreditCollection of Clean and Documentary BillsBank Guaranty (Shipside Bond)Foreign and Domestic RemittancesPurchase and Sale of Foreign ExchangeTravel Funds Servicing of Foreign Loans and InvestmentsTrade InquiryTrust Receipt FacilityCorrespondent Banking Services LC Confirmations/LC Advising Cash Management Tie-ups with Foreign Correspondent Banks Cash Management Tie-ups with Non-Bank Money Transfer Service Providers Foreign Currency Checks and Drafts Clearing ServicesForeign Currency Deposit Unit Services US$ Savings and Time Deposit Foreign Currency Loans

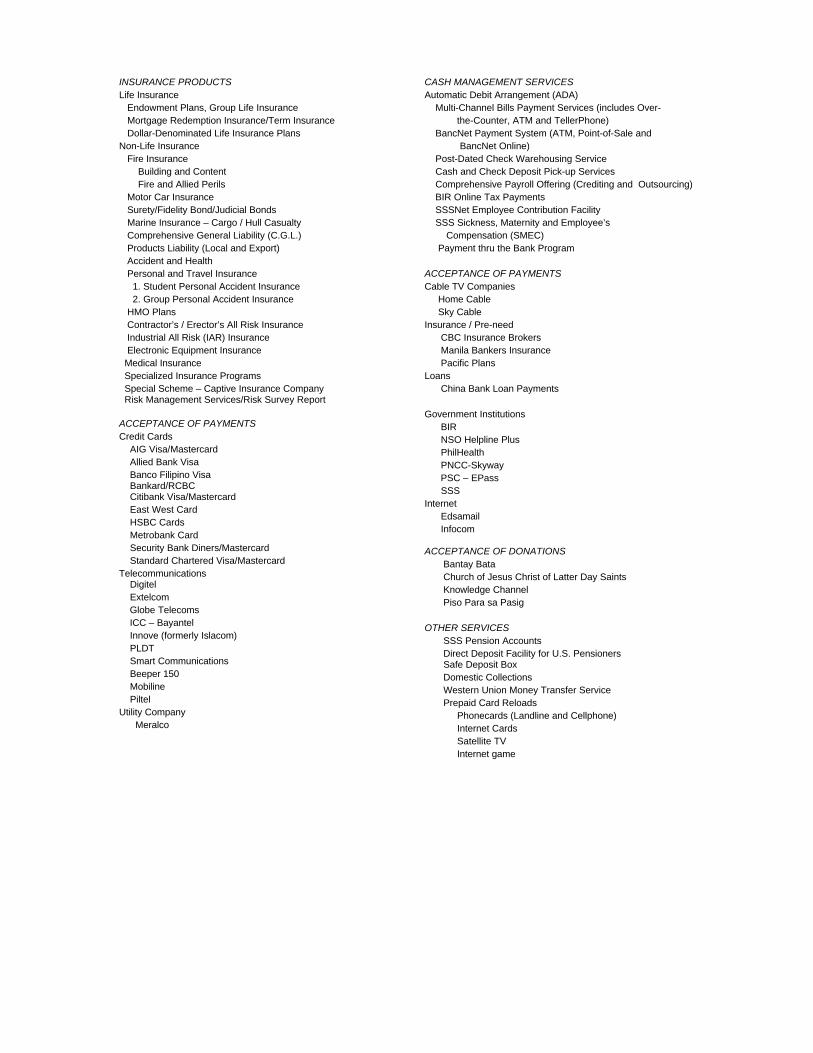

INSURANCE PRODUCTSLife Insurance Endowment Plans, Group Life Insurance Mortgage Redemption Insurance/Term Insurance Dollar-Denominated Life Insurance PlansNon-Life Insurance Fire Insurance Building and Content Fire and Allied Perils Motor Car Insurance Surety/Fidelity Bond/Judicial Bonds Marine Insurance – Cargo / Hull Casualty Comprehensive General Liability (C.G.L.) Products Liability (Local and Export) Accident and Health Personal and Travel Insurance 1. Student Personal Accident Insurance 2. Group Personal Accident Insurance HMO Plans Contractor’s / Erector’s All Risk Insurance Industrial All Risk (IAR) Insurance Electronic Equipment Insurance Medical Insurance Specialized Insurance Programs Special Scheme – Captive Insurance Company Risk Management Services/Risk Survey Report

CASH MANAGEMENT SERVICESAutomatic Debit Arrangement (ADA) Multi-Channel Bills Payment Services (includes Over- the-Counter, ATM and TellerPhone) BancNet Payment System (ATM, Point-of-Sale and BancNet Online) Post-Dated Check Warehousing Service Cash and Check Deposit Pick-up Services Comprehensive Payroll Offering (Crediting and Outsourcing) BIR Online Tax Payments SSSNet Employee Contribution Facility SSS Sickness, Maternity and Employee’s Compensation (SMEC) Payment thru the Bank Program

ACCEPTANCE OF PAYMENTSCable TV Companies Home Cable Sky CableInsurance / Pre-need CBC Insurance Brokers Manila Bankers Insurance Pacific PlansLoans China Bank Loan Payments

ACCEPTANCE OF PAYMENTSCredit Cards AIG Visa/Mastercard Allied Bank Visa Banco Filipino Visa Bankard/RCBC Citibank Visa/Mastercard East West Card HSBC Cards Metrobank Card Security Bank Diners/Mastercard Standard Chartered Visa/MastercardTelecommunications Digitel Extelcom Globe Telecoms ICC – Bayantel Innove (formerly Islacom) PLDT Smart Communications Beeper 150 Mobiline PiltelUtility Company Meralco

Government Institutions BIR NSO Helpline Plus PhilHealth PNCC-Skyway PSC – EPass SSSInternet Edsamail Infocom

ACCEPTANCE OF DONATIONSBantay BataChurch of Jesus Christ of Latter Day SaintsKnowledge ChannelPiso Para sa Pasig

OTHER SERVICESSSS Pension AccountsDirect Deposit Facility for U.S. PensionersSafe Deposit BoxDomestic CollectionsWestern Union Money Transfer ServicePrepaid Card Reloads

Phonecards (Landline and Cellphone) Internet Cards Satellite TV Internet game

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-AITEM 2. PROPERTIESThe Bank conducts its business in its Makati headquarters situated on a 2,977 square meter lot (2 parcels) with a multistorey building appraised at P1.8 BN, with business address at 8745 Paseo de Roxas cor. Villar St., Makati City. ItsBinondo operations are located at a 1,233 sq. m. lot at the corner of Dasmarinas and Juan Luna streets (4 parcels ofland with two multi-storey commercial buildings).

Other properties include land & buildings of the different branches such as1) Caloocan - 2-storey mezzanine commercial bldg situated at No. 167 Rizal Ave. Ext. and J.

Teodoro, Bgy. Calaanan, Caloocan City2) Baguio Penthouse - 3-level duplex residential building, Park Road, Baguio City

3) Davao - Phase 3 of the Ecoland Commercial Center, Matina, Davao4) San Juan - Brgy. San Pedro Cruz, Municipality of San Juan5) Cebu Bus. Park, Cebu - Samar loop cor. Panay Road, Cebu Business Park, Cebu City

6) Trece Martires, Cavite - Unnamed Road, Bo. San Agustin, Trece Martires, Cavite 7) Laguna Bel-Air - Lot 17, Blk 66, Road Lot 1-B Laguna Bel Air Subd., Sta Rosa, Laguna

8) Iloilo-Rizal Drive - Rizal cor. Gomez Sts. Brgy. Ortiz, Iloilo City9) Silang, Cavite - E. Aguinaldo Highway, Bo. Biuso, Silang, Cavite

10) Dolores, San Fernando - 460 sq.m. at Lazatin, Blvd., Dolores, San Fernando, Pampanga 11) Las Piñas - Alabang-Zapote Road cor. Aries, Pamplona, Las Piñas City12) Valenzuela - MacArthur Highway, Valenzuela City13) Rosario, Cavite - Gen. Trias Drive, Rosario, Cavite14) Imus, Cavite - Nueno Avenue, Tanzang Luma, Imus, Cavite15) Tarlac - Panganiban St., San Nicolas Tarlac City, Tarlac

16) Visayas Avenue - Visayas Ave., cor. Congressional Ext. Quezon City 17) Cabanatuan - Lot 6 Blk 3, Maharlika Highway, Dicarma, Cabanatuan City18) Libertad, Pasay City - No. 184 Libertad St., Pasay City 19) Dasmariñas, Cavite - Gen Emilio Aguinaldo Highway, Dasmariñas, Cavite20) Angeles City - 347.07 sq.m. 2 parcels of land

21) Roosevelt - # 291 Roosevelt Ave., San Francisco Del Monte, Quezon City 22) San Juan - No. 169 Blumentritt St., San Juan, Metro Manila 23) Navotas - No. 551 M. Naval St., Bankulasi, Navotas, MM 24) Cebu-Manalili - M. Velez cor. V. Rama Ave., Cebu City

25) Bacolod - Araneta St., Bacolod City26) Lapasan - C.M. Recto Ave. National Highway, Lapasan, Cagayan de Oro City

27) General Santos - 600 sq.m. lot at Bo. Lagao, Gen Santos City 28) Sorsogon - Ramon Magsaysay Ave., Sorsogon, Sorsogon 29) Zamboanga - Gov. Lim Avenue, Zamboanga City

30) Dipolog - Gen. Luna cor. G. Gonzales Sts., Dipolog City38) Davao (Recto) - C.M. Recto co. J.P. Rizal Sts., Davao City39) Cebu - Jakosalem & Magallanes St., Cebu City

40)Potrero - McArthur Highway, Potrero, Malabon City 41) West Avenue - No. 2 West Ave., Bgy. Philam, District of Diliman Quezon City 42)Talisay, Cebu - Talisay, Cebu City 43) Banilad, Cebu - Barangay of Banilad, Cebu City

44) San Fernando, Pampanga - V. Tiomico St., Sto. Rosario, San Fernando Pampanga 45) E. Rodriguez Sr. Blvd. - E. Rodriguez Sr. Ave. New Manila, Quezon City

46) Banawe - Banaue Ave., Quezon City 48) Cainta, Rizal - 415 sq.m. lot at Felix Ave., Cainta, Rizal (beside Sta Lucia East Mall) 49) Quiapo - No. 216-220 Villalobos St., Quiapo, Manila 50) Cubao-Aurora - Aurora Blvd. Cor. Miami, Cubao, Quezon City

51)San Pablo City - Rizal Ave., Poblacion, San Pablo City 52) General Santos - 500 sq.m. lot at Queennies Vill., Dadiangas Heights, Bo. Lagao, Gen. Santos

53) Cainta, Rizal - 623 sq.m. lot at Felix Ave., Cainta, Rizal (beside Sta Lucia East Mall) 54) Dolores, San Fernando - 900 sq.m. at Lazatin, Blvd., Dolores, San Fernando, Pampanga

These properties are free from any lien or encumbrance.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

Description of Property the Bank intends to acquire in the next 12 months. The Bank has no plans to acquire properties inthe next twelve (12) months.

The Bank’s schedule of Bank premises, furniture, fixtures & equipment as of Dec. 31, 2004:

Accounts Amount (In Million Pesos)Bank Premises-Land P 1,825Building under construction Bank Premises-Building 588Bank Premises-Appraisal 348Leasehold Rights & Improvements 75Furnitures, Fixtures & Equipment 1,876Less:Accumulated Depreciation-Bldg. 160Accumulated Depreciation-FFE 1,525

P 3,027

Cost of computer equipment is lodged with CBC-Properties & Computer Center, Inc.

ITEM 3. LEGAL PROCEEDINGS

• There are pending cases for and against the Bank arising from normal business activities. In the opinion of theBank’s management and legal counsel, there are no material pending legal proceedings to which the Bank orany of its subsidiaries or affiliates is a party or of which any of their property is the subject.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

• Annual Stockholders Meeting -- May 06, 2004• Directors Elected - Gilbert U. Dee, Chairman of the Board

Hans T. Sy, Vice Chairman and Chairman of the Executive CommitteePeter S. Dee, President and CEOPilar N. Liao, Independent DirectorJoaquin Dee, DirectorDy Tiong, DirectorHerbert T. Sy, Director

Henry T. Sy, Jr., DirectorHarley T. Sy, DirectorDonato T. Faylona, Independent DirectorAlberto S. Yao, Independent Director

Henry Sy, Sr., Advisor to the BoardRobert T. Dee, Jr., Advisor to the Board

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

PART II OPERATIONAL AND FINANCIAL INFORMATION

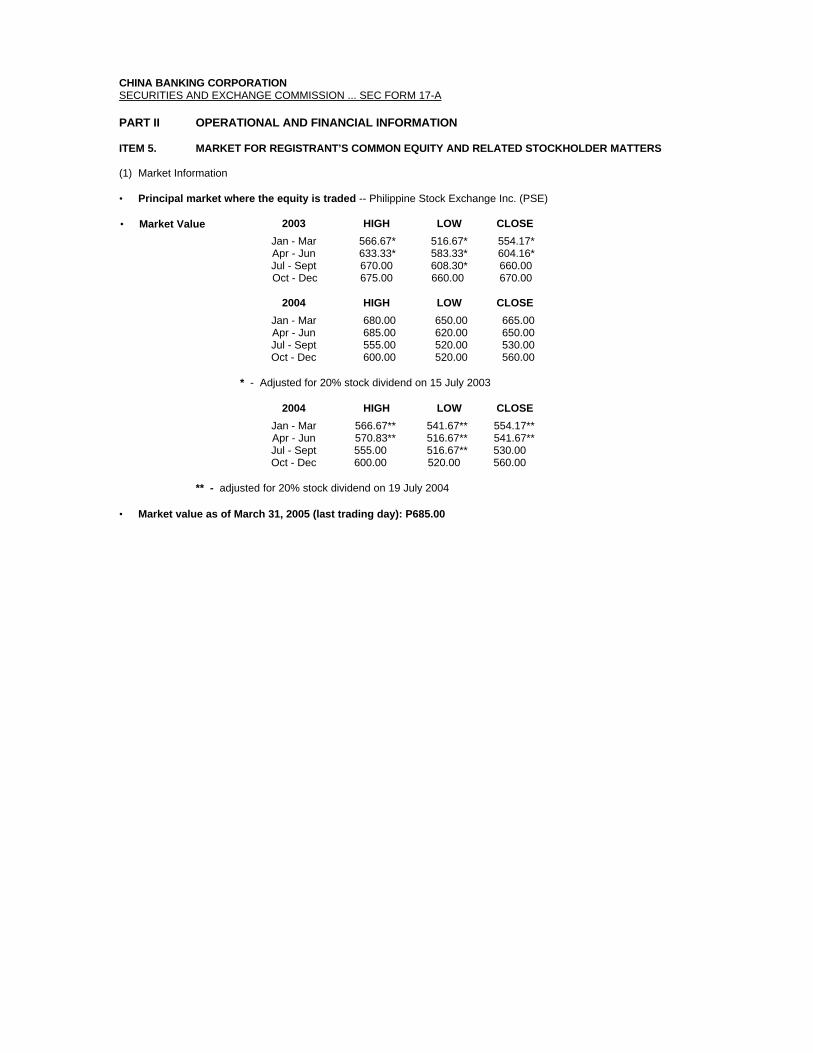

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

(1) Market Information

• Principal market where the equity is traded -- Philippine Stock Exchange Inc. (PSE)

• Market Value 2003 HIGH LOW CLOSE.

Jan - Mar 566.67* 516.67* 554.17*Apr - Jun 633.33* 583.33* 604.16*Jul - Sept 670.00 608.30* 660.00

Oct - Dec 675.00 660.00 670.00

2004 HIGH LOW CLOSE.

Jan - Mar 680.00 650.00 665.00Apr - Jun 685.00 620.00 650.00Jul - Sept 555.00 520.00 530.00Oct - Dec 600.00 520.00 560.00

* - Adjusted for 20% stock dividend on 15 July 2003

2004 HIGH LOW CLOSE.

Jan - Mar 566.67** 541.67** 554.17**Apr - Jun 570.83** 516.67** 541.67**Jul - Sept 555.00 516.67** 530.00Oct - Dec 600.00 520.00 560.00

** - adjusted for 20% stock dividend on 19 July 2004

• Market value as of March 31, 2005 (last trading day): P685.00

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

(2) Holders• Top 20 Stockholders (As of 12/31/2004)

Name of Stockholders Number of Shares Percent Share 1. Sysmart Corporation 7,457,473 20.408 2. PCD Nominee Corporation (Filipino) 5,389,793 14.749 3. SM Investments Corporation 3,509,967 9.605 4. The Int’l. Commercial Bank of China 2,952,268 8.079 5. Shoe Mart, Inc. 2,461,744 6.737 6. Henry Sy, Sr. 2,021,761 5.533 7. CBC Employees Retirement Plan 914,469 2.502 8. Joaquin Dee &/or Leticia Ty Dee 877,635 2.402 9. JJACCIS Development 716,850 1.962 10. GDSK Development Corporation 618,714 1.693 11. PCD Nominee Corporation (Non-Fil) 395,330 1.082 12. Domingo T. Dee 226,896 0.621 13. Gilbert U. Dee 214,578 0.587 14. Estate of Allen Cham 170,757 0.467 15. Regina Y. Dee 162,518 0.445 16. Hydee Management & Resource Corp. 161,187 0.441 17. SM Development Corp. 147,002 0.402 18. Kuan Yan Tan’s Charity (Phil.), Inc. 123,030 0.337 19. The First Resources Mgt. & Sec. Corp. 112,197 0.307 20. Reliance Commodities, Inc. 106,539 0.292

TOTAL 28,740,708 78.650%

Total number of shareholders (As of 12/31/2004) – 1,852

(3) DividendsChinabank’s Dividend history has been mainly in the form of stock dividends.

2004 2003 2002 2001 2000Stock Dividend 20% 20% 10% 10%Cash Dividend 5% 5% 8%

Authorized and Issued Capital Authorized Capital - P5.0 billion divided into 50 million shares Issued Shares - 36,542,512 There is no restriction that limits the ability to pay dividends other than what is required in the CorporationCode. However, any dividends declared by the Bank are subject to the approval primarily of Bangko Sentral ngPilipinas, the Philippine Stock Exchange and the Securities and Exchange Commission.

(4) Unregistered Securities

There were no unregistered securities sold by the Bank for the past three (3) years, however there were new securitiesissued resulting from the declaration of stock dividend to come from the Bank’s unissued shares which were exempt fromregistration requirement under Sec 10.1 (d) of the Securities Regulation Code.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

Compliance with leading practices on corporate governance

The Bank’s Manual on Corporate Governance has been revised to incorporate amendments introduced by variousgovernance-related circulars issued by the regulators which include among others, the creation of Corporate GovernanceCommittee, Risk Management Committee and Compensation or Remuneration Committee and the adoption ofcorresponding Committee Charter, and the PSE Revised Disclosure Rules.

Also, the Bank has an evaluation system for the Board of Directors and for the Individual Board, to determine and measurecompliance with the provisions and requirements of the Manual. This is done annually where the results are summarizedand reported to the Board of Directors by the Compliance Officer.

To enjoin compliance, a copy of the Bank’s Manual on Corporate Governance, as amended, is made available to allemployees. Also, orientation is conducted for supervisors and officers to raise the level of awareness and understanding ofthe principles, concepts and elements of good corporate governance.

ITEM 6. MANAGEMENT DISCUSSION AND ANALYSIS OR PLAN OF OPERATION

A. Management’s Discussion and Analysis (MD & A) or Plan of Operation

(1) Financial and Operating HighlightsHighlights of the balance sheet and income statement for the last three (3) fiscal years:

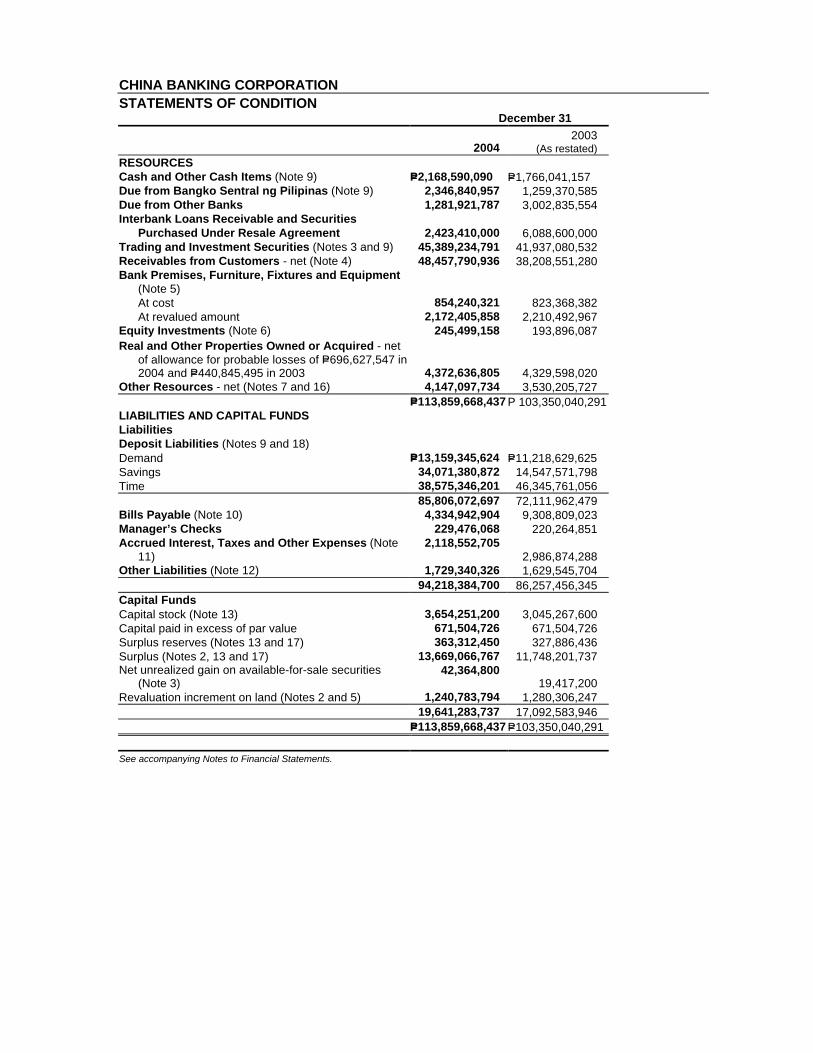

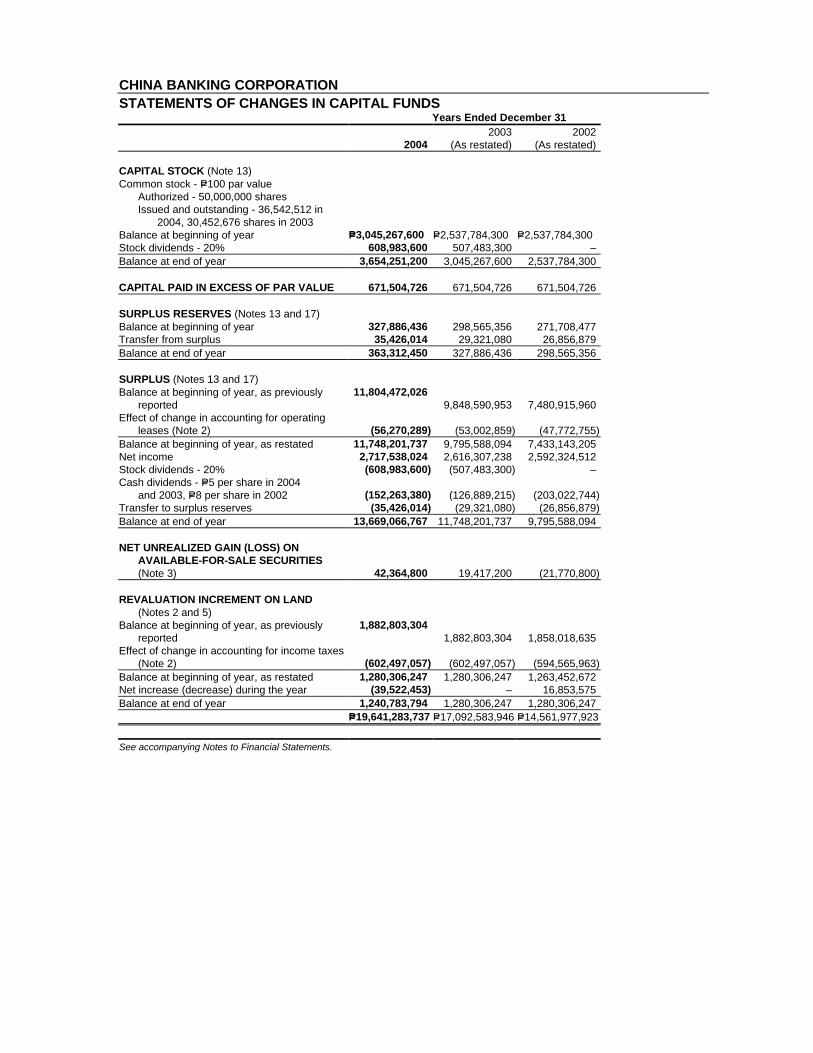

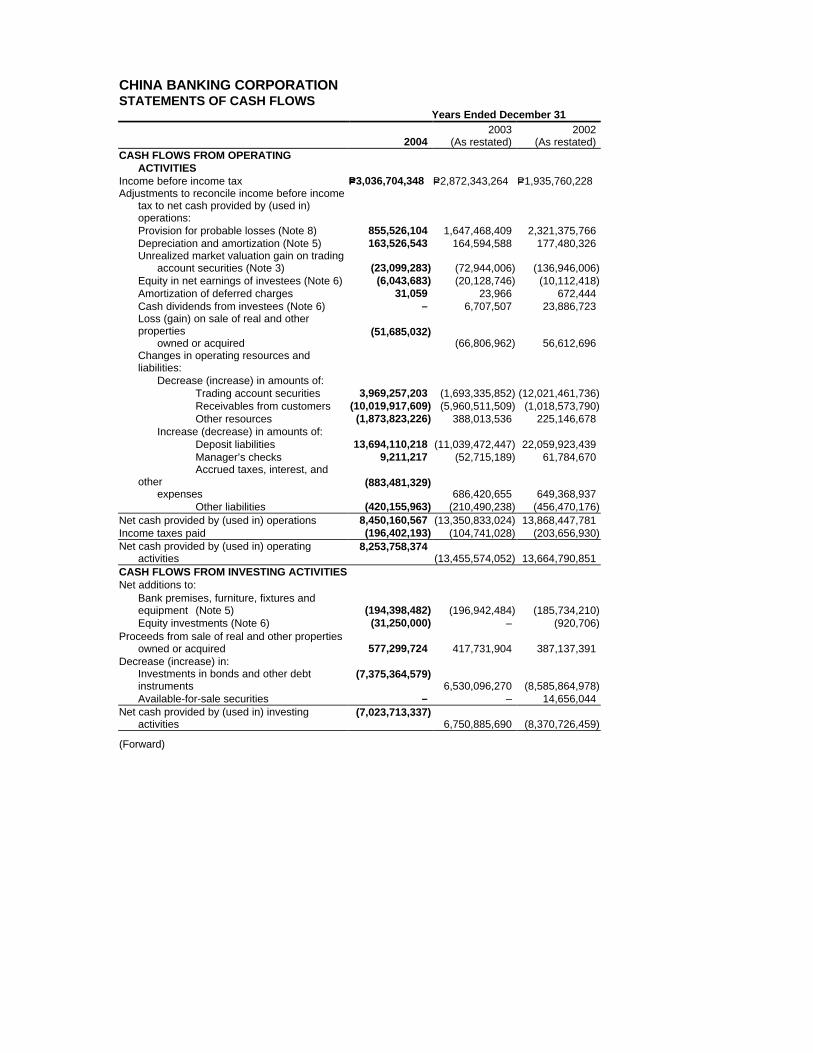

2004 2003 2002 (In Million Pesos) (As restated) (As restated)Gross Revenues 10,678 11,174 10,403 Gross Expenses 7,961 8,558 7,811 Net Income 2,717 2,616 2,592 Total Resources 113,860 103,350 107,931Loan Portfolio (Net) 48,458 38,209 34,351Total Deposits 85,806 72,112 83,151Capital Funds 19,641 17,093 14,562(In %)Return on Assets 2.46 2.57 2.73 Return on Average Equity 14.37 16.82 19.36 BIS Capital Adequacy Ratios 32.74 26.17 24.53Net Interest Margin 5.08 4.47 4.02

(2) Management’s Discussion and Analysis

The Bank posted a 3rd straight year of record income at P2.72 billion, 3.87% above 2003 figures and 4.83% from 2002figures. The resulting Return on Average Equity (ROE) of 14.37%, 16.82% and 19.36% and Return on Assets of 2.46%,2.57% and 2.73% in 2004, 2003 and 2002, respectively reflect industry best performance. Income was boosted by higherinterest margins coupled with lower provisioning at P856 million vs. P1.65 billion in 2003 and P2.32 billion in 2002.

Fund-based revenues reached P8.56 billion, expanding by 18.81% and 31.13% from 2003 and 2002 respectively, mainlyfrom interest income on loans, low-risk investment securities and IBCL. Interest expenses slightly declined by 0.52% in2004 from P3.52 billion in 2003 but was slightly up by P205 million from 2002 as a result of lower interest cost on dollardeposits and pay-offs of high yielding peso deposits such as More Than Double Your Money (MTDYM)-5 at the start of theyear. Consequently, net interest income expanded by 37.29% and 56.58% from P3.68 billion and P 3.23 billion in 2003 and2002, respectively to P5.05 billion in 2004. Net interest margin improved to 5.08% from 4.47% in 2003 and 4.02% in2002.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

Fee-based revenues dropped by 46.60% from 2003 & 45.30% from 2002 to P2.12 billion in 2004 which can be attributedto the decline in trading gains by 87.74% and 89.47% from P2.46 billion in 2003 and P2.87 billion in 2002 respectively. Thiswas expected as a substantial part of the GS inventory was sold in 2004 and 2003. On the other hand, services, fees andcommissions grew by 33.91% from P467 million in 2003 and 34.97% in 2002. Higher in-clearing service charges such asno sufficient fund (NSF) and clearing house operating memo (CHOM) boosted service and collection charges. Foreignexchange gain also increased by 14.94% in 2004 from P642 million in 2003 and by 323.67% from P174 million in 2002 asour Treasury Group maximized opportunities from the higher peso-dollar exchange rate. Miscellaneous income alsoexpanded by 9.02% to P95.5 million in 2004 from P87.6 million in 2003 and by 21.22% from P95 million in 2002 .

Despite the drop in taxes and licenses by 10.05% to P385 million and slight increase by 2.06% from 2003, operatingexpenses grew to P3.28 billion or by 4.76% in 2004 from P3.13 billion in 2003 and 18.05% from P2.85 billion in 2002.Compensation and fringe benefits grew by P195 million to P1.22 billion in 2004 from P1.02 billion in 2003 and by P276million in 2004 from P943 million in 2002 mainly due to higher salary and other fringe benefits. Miscellaneousexpenses were down by 21.09% or P150.17 million to P561.90 million from P712.16 million in 2003 and up by 1.90% orP10.50 million from 2002 as a result of reclassification of accounts.

With substantial loan loss reserves already provided in the previous 2 years, China Bank’s provision for probable lossesslowed to P856 million. The resulting loan loss coverage ratio (ratio of reserves to bad loans) of 82.19%, remainedone of the highest in the industry. This brings cumulative loan loss reserves to P6.25 billion in 2004, down by 4.5%from 2003 due to write-offs effected by end of year. NPL ratio stood at 11.40% in 2004, better than last year’s 14.68% .

Going forward, changes in market/borrowing rates, volatility of peso/dollar exchange rates and other external factors arepotential concerns.

Total resources grew by P 10.51 billion to P 113.86 billion in 2004, mainly from higher loans volume and Investment inBonds and Other Debt Instruments (IBODI). The bank’s gross loan portfolio for 2004 grew by P11.9 billion from 2003 andP17.7 billion from 2002 due to additional exposure to prime companies in telecommunications, shipping, medical services,food and agribusiness and real estate as well as higher volume of retail loans (housing & auto).

Items on the asset side such as Cash & Other Cash Items increased by 22.79% from 2003 and 36.90% from 2002 due toyear-end build-up. There was a growth in Due from BSP of 86.35% which can be attributed to an increase in BSPreserves from higher deposits . Meanwhile, Due from Other Banks dropped by 57.31% and 71.30% from 2003 and 2002,respectively as a result of lower placements with other banks. Interbank loans also declined by 60.20% to P2.42 billionfrom P6.09 billion in Dec. 2003 due to lower overnight bank placements. For 2004, IBODI increased by 27.30% to P34.39billion in 2004 from P27.02 billion in 2003 and by 2.52% from P33.55 billion in 2002 from higher investment in governmentsecurities. Trading account securities (TAS) decreased by 26.55% from 2003 and 16.60% from 2002 due toreclassification of accounts.

On the liabilities side, total deposits was up by 17.30% to P85.81 billion in 2004 from P 72.11 billion in 2003 and 3.19%from P83.15 billion in 2002 which can be attributed to higher CASA deposits and the introduction of new high yielding long-term deposits. Again, year-on-year CASA growth was one of the best ever for the Bank, and signified the eighth straightyear of over P 1 billion build-up in low-cost CASA deposits.

Interbank loans payable dropped by 87.81% to P732 million from P6.00 billion in 2003 and 70.76% from P2.50 billion in 2002 as therewas no need for additional bank borrowings. Accrued Taxes, Interest & Other Expenses declined by 29.07% from 2003 and 4.20% from2002 due to the payout of accrual interest on maturing MTDYM deposits last January. Other liabilities grew by 6.12% from 2003 due toadjustments involving reclassification to proper accounts for the whole year 2004.Total capital funds reached P19.64 billion, up by 14.91% from 2003 and 29.07% from 2002. The BIS Capital Adequacy Ratio (CAR)reached a new high of 32.74%, reflective of the Bank’s status as one of the best capitalized banks in the industry. Again, this is animprovement from the CAR of 26.17% in 2003 and 24.53% in 2002.

Changes in market rates and borrowing costs as well as movements in the peso/dollar exchange rate may affect the Bank’s liquidity.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

Despite an exigent environment, China Bank remained vigilant for fresh opportunities to hike market share and consolidateits presence as a multi-category service provider. On the corporate banking side, the Bank’s newly established CashManagement unit became a significant engine for acquisition of business clients through the launching/offering of servicessuch as BIR tax payments (electronic Filing and Payment system), payroll processing, check warehousing and auto-debitarrangements. For the retail banking, branch-based marketing program was implemented throughout the network.Consumer products were also introduced in 2004 such as the Contract to Sell (CTS) financing and salary loans. We havealso reorganized our support units such as the Centralized Operations Group which included the International Banking andLoans & Discounts. Another newly-formed group in 2004 was Credit Management, which includes Remedial Management,Securities Custodianship and Credit Division. Technology-related capital investment accounted for the bulk of the Bank’scapital expenditures for the year 2004. These include additional business applications, upgrade of computer mainframehardware (CPU and storage) for the core banking system and e-banking projects.

There were no key variable and other qualitative and quantitative factors which affected the Bank’s financial condition thatdid not arise from the Bank’s normal course of operations. Also, changes in the bank’s financial condition or operationsare due more to external factors such as interest rate movements and cost of borrowings rather than cyclical aspects.

In the normal course of the Bank’s operations, there are various outstanding commitments and contingent liabilities whichare not reflected in the accompanying financial statements. Management does not anticipate any material losses as aresult of these transactions.

The following is a summary of contingencies and commitments with their equivalent peso contractual amounts:2004 2003

Trust Department accounts P 38,184,795,281 P 33,560,644,456Forward exchange sold 7,729,720,647 13,071,690,696Unused commercial letters of credit 2,061,265,436 1,920,913,124Outstanding guarantees issued 2,637,888,695 1,342,660,084Deficiency claims receivable 779,131,078 491,142,262Late deposits/payments received 218,321,220 119,022,748Outward bills for collection 219,272,685 95,017,647Inward bills for collection 134,308,337 91,467,555Forward exchange bought 27,026,647 25,355,946Others 731,573,297 615,480,142

There are pending assessments and pre-assessments from the Bureau of Internal Revenue (BIR) pertaining to withholdingtax at source and DST for the years 1982 to 1986 and GRT for the years 1999 and 2000. In addition, the Bank has receivedtax assessments from the BIR on two industry issues. The Bank, through its tax counsel, is contesting these assessmentsand pre-assessments on the ground that the factual situations were not considered which, if considered, will not give rise tomaterial tax deficiencies. The Bank, together with other member banks of the Bankers’ Association of the Philippines (BAP), is contesting these pending assessments and pre-assessments of the BIR. Discussions are ongoing between the BAPand the BIR for the appropriate settlement and disposition of these tax issues. No provision has been made in theaccompanying financial statements for these contingencies.

Several suits and claims relating to the Bank’s lending operations and labor-related cases remain unsettled. In the opinionof management, these suits and claims, if decided adversely, will not involve sums having a material effect on the financialstatements of the Bank.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

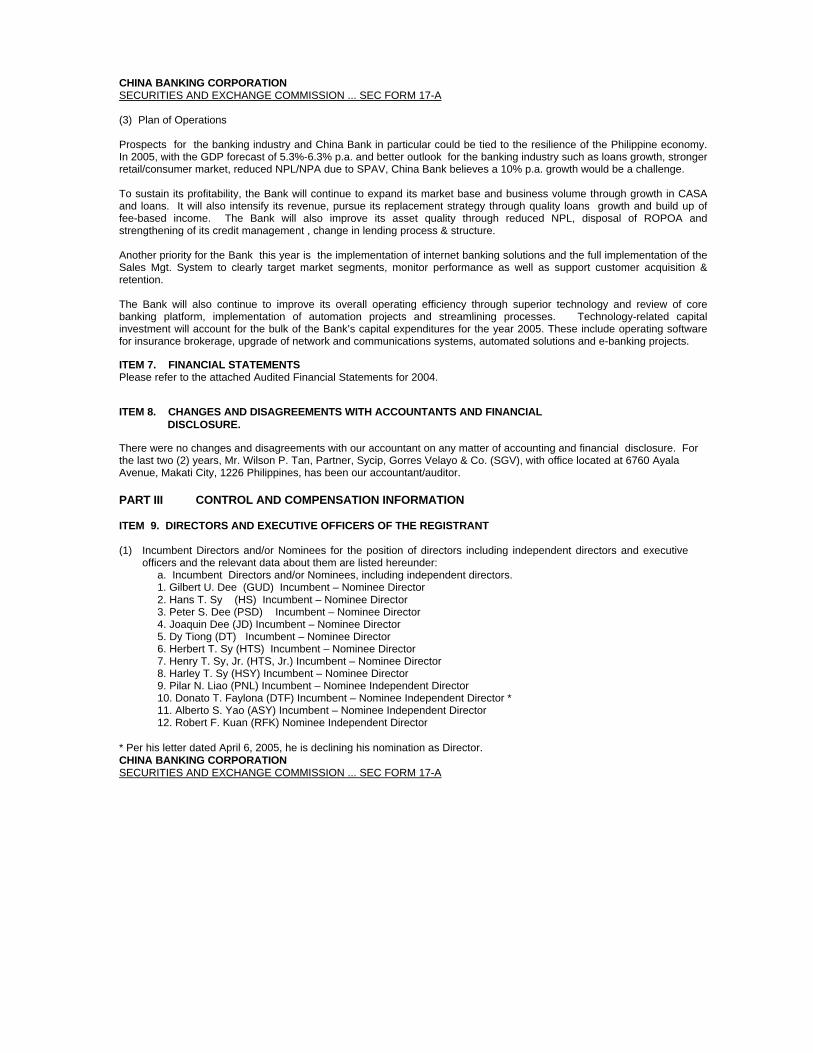

(3) Plan of Operations

Prospects for the banking industry and China Bank in particular could be tied to the resilience of the Philippine economy.In 2005, with the GDP forecast of 5.3%-6.3% p.a. and better outlook for the banking industry such as loans growth, strongerretail/consumer market, reduced NPL/NPA due to SPAV, China Bank believes a 10% p.a. growth would be a challenge.

To sustain its profitability, the Bank will continue to expand its market base and business volume through growth in CASAand loans. It will also intensify its revenue, pursue its replacement strategy through quality loans growth and build up offee-based income. The Bank will also improve its asset quality through reduced NPL, disposal of ROPOA andstrengthening of its credit management , change in lending process & structure.

Another priority for the Bank this year is the implementation of internet banking solutions and the full implementation of theSales Mgt. System to clearly target market segments, monitor performance as well as support customer acquisition &retention.

The Bank will also continue to improve its overall operating efficiency through superior technology and review of corebanking platform, implementation of automation projects and streamlining processes. Technology-related capitalinvestment will account for the bulk of the Bank’s capital expenditures for the year 2005. These include operating softwarefor insurance brokerage, upgrade of network and communications systems, automated solutions and e-banking projects.

ITEM 7. FINANCIAL STATEMENTSPlease refer to the attached Audited Financial Statements for 2004.

ITEM 8. CHANGES AND DISAGREEMENTS WITH ACCOUNTANTS AND FINANCIAL DISCLOSURE.

There were no changes and disagreements with our accountant on any matter of accounting and financial disclosure. Forthe last two (2) years, Mr. Wilson P. Tan, Partner, Sycip, Gorres Velayo & Co. (SGV), with office located at 6760 AyalaAvenue, Makati City, 1226 Philippines, has been our accountant/auditor.

PART III CONTROL AND COMPENSATION INFORMATION

ITEM 9. DIRECTORS AND EXECUTIVE OFFICERS OF THE REGISTRANT

(1) Incumbent Directors and/or Nominees for the position of directors including independent directors and executiveofficers and the relevant data about them are listed hereunder:

a. Incumbent Directors and/or Nominees, including independent directors.1. Gilbert U. Dee (GUD) Incumbent – Nominee Director

2. Hans T. Sy (HS) Incumbent – Nominee Director3. Peter S. Dee (PSD) Incumbent – Nominee Director4. Joaquin Dee (JD) Incumbent – Nominee Director5. Dy Tiong (DT) Incumbent – Nominee Director6. Herbert T. Sy (HTS) Incumbent – Nominee Director7. Henry T. Sy, Jr. (HTS, Jr.) Incumbent – Nominee Director8. Harley T. Sy (HSY) Incumbent – Nominee Director9. Pilar N. Liao (PNL) Incumbent – Nominee Independent Director10. Donato T. Faylona (DTF) Incumbent – Nominee Independent Director *11. Alberto S. Yao (ASY) Incumbent – Nominee Independent Director12. Robert F. Kuan (RFK) Nominee Independent Director

* Per his letter dated April 6, 2005, he is declining his nomination as Director.CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

Gilbert U. Dee, 69, Chairman of the Board, holds a Bachelor of Science degree in Banking from De La Salle University. He obtained hisMBA in Finance from University of Southern California in 1959. He became the Chairman of the Board in 1989 and a Director since 1969.He has been a director/officer for more than five (5) years in companies engaged in banking, finance and investment, manufacturing andauto dealership. He holds directorships in affiliates/subsidiaries and other corporations such as CBC Properties & Computer Center, Inc.(CBC-PCCI), Union Motor Corp. and Super Industrial Corp., among other corporations. GUD and PSD are related within the 5th civil degreeby consanguinity.

Hans T. Sy, 49, Vice Chairman and Chairman of the Executive Committee (ExCom), holds a Bachelor of Science degree in MechanicalEngineering from De La Salle University. He became Vice Chairman and Chairman of the ExCom since 1989 and a Director since 1986.He has been director/officer for more than five (5) years in companies engaged in banking, retailing, real estate development, malloperations, construction, cement, food and rubber manufacturing, finance and investment, insurance and entertainment. He holdsdirectorships in affiliates/subsidiaries and other corporations such as Best Rubber Corp., ACE Hardware Phils. Inc., Family EntertainmentCenter, Inc., HS Food, Inc., Land Building Corp., Market-Watch Investors Co., Inc., Shoemart, Inc., Multi-Realty Dev’t. Corp., ShoppingCenter Mgt. Corp., SM Development Corp., SM Investments Corp., Wonderfoods, Inc., among other corporations. HS, HTS, HTS, Jr. andHSY are related within the 2nd civil degree by consanguinity.

Peter S. Dee, 63, President & Chief Executive Officer (CEO), holds a Bachelor of Science degree in Commerce from De La SalleUniversity/University of the East. He became President & CEO in 1989 and has been a Director since 1977. He has been a director/officerfor more than five (5) years in companies engaged in banking, paint, food and beverage, manufacturing, real estate development, financeand insurance. He holds directorships in affiliates/subsidiaries and other corporations such as CBC Properties & Computers Center, Inc.,CBC Forex Corp., Chinabank Insurance Brokers, Inc., Cityland Dev’t. Corp., Hydee Mgt. & Resources Corp., Sinclair (Phils.), Inc., CanLacquer, Inc. and GDSK Dev’t. Corp., among other corporations. PSD and GUD are related within the 5th civil degree by consanguinity.

Joaquin Dee, 69, Director, holds a Bachelor of Arts degree in Commerce from Letran College. He has been a Director since 1984 and hasbeen a director/officer for more than five (5) years in companies engaged in banking, liquor manufacturing, flour trading and real estatedevelopment. He holds directorships in the following corporations: JJACCIS Dev’t. Corp. and Enterprise Realty Corp., among othercorporations.

Dy Tiong, 75, Director, holds a Bachelor of Science degree in Business Administration from National Jean Kuan College. He has been aDirector since 1985. He has also been a director/officer for more than five (5) years in companies engaged in banking, finance, investment,insurance and education. He holds directorships in following corporations: Panelon Phils. and Chiang Kai Shek College, among othercorporations.

Herbert T. Sy, 48, Director, holds a Bachelor of Science degree in Management from De La Salle University. He has been a Director since1993 and has been a director/officer for more than five (5) years in companies engaged in banking, food retailing, rubber manufacturing,investment, car service and car accessories, real estate development and mall operations. He holds directorships in the followingcorporations: Best Rubber Corp., SM Autoservice & Car Accessories (Phils.), Inc., Café Elysee, Inc., SM Prime Holdings, Inc. andSupervalue, Inc., among other corporations. HTS, HS, HTS, Jr. and HSY are related within the 2nd civil degree by consanguinity.

Henry T. Sy, Jr., 51, Director, holds a Bachelor of Science degree in Management from De La Salle University. He has been a Directorsince June 2000. Mr. Sy, Jr. has been a director/officer for more than five (5) years in companies engaged in banking, real estatedevelopment, construction, mall operations, cement, food & rubber manufacturing, finance and investment. He holds directorships in thefollowing corporations: SM Prime Holdings, SM Investments Corp., SM Synergy Properties Holdings Corp., Shoemart Inc., Sysmart Corp.,Highlands Prime, Inc. & SM Development Corp., among other corporations. HTS, Jr., HS, HTS and HSY are related within the 2nd civildegree by consanguinity.

Harley T. Sy, 45, Director, holds a Bachelor of Science degree in Commerce, major in Finance from De La Salle University. He became aDirector in May 2001. He has been a director/officer for more than five (5) years in companies engaged in banking, retailing, food, realestate development, finance and investment. His directorships include the following: ACE Hardware Phils., SM Investments Corp.,Shoemart, Inc. and H.S. Food, Inc., among other corporations. HSY, HTS, HS and HTS, Jr. are related within the 2nd civil degree byconsanguinity.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

Pilar N. Liao, 74, Director, holds a Bachelor’s degree in Home Economics from the College of the Holy Spirit. She becamea Director in May 1985. She has also been a director/officer for more than five (5) years in companies engaged in banking,office equipment, systems and supplies. She is also a Director of Speed Office System.

Donato T. Faylona, 57, has been engaged in the general practice of law since 1974. Presently, a partner in HerreraTeehankee Faylona & Cabrera Law Offices in-charge of litigation, a position he has held since joining the firm in 1988, hasextensively appeared in trial courts and administrative bodies such as the Securities and Exchange Commision, CivilAeronautics Board and House Land Use and Regulatory Board. Directly handled and supervised appellate practice in theCourt of Appeals and in the Supreme Court. Has likewise extensive practice in corporate law involving joint ventureagreements, mergers and acquisitions and maintenance of corporate books. His directorship include the following:Gendiesel Philippines, Inc., Dream 6750, Inc., Jadwani Int’l., Inc., VAJ Industries, Inc., VSD Realty and Dev’t. Corp., OrientWood Industrial Co., Inc., Tagum Agro-Industrial Corp., Phil-Gulf, Inc., and Casa Benita Dev’t. Corp.

Alberto S. Yao, 58, Director, holds a Bachelor of Science in Business Administration from Mapua Institute of Technology.He became a director in July 2004. He has been a director/officer for more than five (5) years in companies engaged inmanufacturing and distribution of tires, Mattel and other leading toys, infants and children’s footwear. His directorship/officership in other corporations include Richphil House, Inc., Megarich Property Ventures and Crestland Empire VentureCorporation.

Robert F. Kuan, 57, holds a Bachelor of Science degree in Business Administration from UP. He obtained his MBA fromAIM in 1975. He took up Top Management Program exclusively for company Presidents and Chief Executive Officers atBali, Indonesia in 1993. He has been the Chairman of the Board of Trustees of St. Luke’s Medical Center and Member ofBoard of Trustees of St Luke’s College of Medicine since 1996, and Brent International School of Manila since 1989. He isthe founder and the President of Chowking Food Corporation from 1985 until March 2000. He is a recipient of severalawards and citations in the field of business, such as Business Leadership Award (Pillar Category) from Aurelio Periquet,Jr. Foundation, TOFIL Awardee in the field of Business and Entrerpreneurship for the year 2003, 1999 FranchiseExcellence Awardee from the Philippine Franchise Association, 1999 Most Outstanding Professional Awardee in the field ofBusiness Administration from UP Alumni Association, among others.

GUD- Nominated by Linda Susan T. Mendoza, no relationHS-Nominated by SM Investments Corp./Shoemart, Inc./Henry Sy, Sr./Sysmart Corp.PSD – Nominated by Nancy D. Yang, sisterJD – Nominated by Christopher Dee, sonDT – Nominated by Johnny Cheng, T.K., Jr. son-in-lawHTS – Nominated by SM Investments Corp./ Shoemart, Inc./Henry Sy, Sr. / Sysmart Corp.HTS, Jr. – Nominated by SM Investments Corp./Shoemart, Inc./Henry Sy, Sr./Sysmart Corp.HSY – Nominated by SM Investments Corp./Shoemart, Inc./Henry Sy, Sr./Sysmart Corp.PNL – Nominated by Patrick Stephen Liao, sonASY – Nominated by Gregorio U. Kilayko, no relationDTF – Nominated by Regina Capital Development Corp. by Marita A. LiminganRFK – Nominated by Regina Capital Development Corp. by Marita A. Limingan

b. Principal Officers

Ricardo R. Chua, 53, Executive Vice President (EVP) and Chief Operating Officer (COO), holds a Bachelor’s Degree inCommerce, major in Accounting from the University of the East. He obtained his MBA from Asian Institute of Management(AIM) in 1975. He became the COO in December 1995. He has been involved in the banking industry for more than 5years. He is presently the President & COO of Chinabank Insurance Brokers, Inc. (CBC-IBI), Director of CBC Forex Corp.(CBC-CFC), Director and General Manager of CBC Properties and Computer Center, Inc. (CBC-PCCI).

Reynaldo L. Lao, 61, Senior Vice President (SVP) and Head of the Consumer Banking Group, holds a Bachelor’s degreein Management from University of the East. He obtained his MBA from Ateneo de Manila and graduated from the AsianInstitute of Management’s Management Development Program in 1972. He has been an SVP since 1995. He has beeninvolved in the banking industry for more than 5 years. He is a Director of Chinabank Insurance Brokers, Inc. (CBC-IBI).CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

Nancy D. Yang, 65, Senior Vice President (SVP) and Head of the Branch Banking Group, holds a Bachelor of Arts degreefrom PWU and a degree in Human Development & Child Psychology from Merill Palmer Institute, Detroit, Michigan, USA,

1960-61. She has been a SVP since 1995. She has been involved in the banking industry for more than 5 years. She is aDirector of CBC Properties & Computer Center, Inc. (CBC-PCCI) and Chinabank Insurance Brokers, Inc. (CBC-IBI). PSDand NDY are related within 2nd civil degree by consanguinity.

Samuel L. Chiong, 54, Senior Vice President (SVP), and Assistant Group Head of Branch Banking Group, holds aBachelor of Arts degree in Economics from Ateneo de Manila. He took the Advanced Bank Management Program from theAsian Institute of Management (AIM) in 1989. He has been involved in the banking industry for more than 5 years. Hebecame SVP in February 2004.

Antonio S. Espedido, Jr., 49, Senior Vice President (SVP), and Head of Treasury Group, holds a Bachelor of Science inBusiness Administration from University of San Francisco. He has been in the banking industry since 1984. He becameSVP in July 2004. He is a Director of CBC Forex Corporation (CBC-CFC).

Ramon R. Zamora, 55, Senior Vice President (SVP) and Head of the International Banking Group, holds a Bachelor of Artsdegree in Economics from Ateneo de Manila. He has been an SVP since April 2004. He has been involved in the bankingindustry for more than 5 years. He is a Director of CBC Forex Corp. (CBC-CFC).

Margarita L. San Juan, 51, First Vice President (FVP), Account Management Group, holds a B.S.B.A. Major in FinancialManagement degree from UP. She took the Advance Bank Management Program from Asian Institute Management (AIM)in 1992. She became FVP in January 1997.

Rene J. Sarmiento, 51, First Vice President (FVP) and Head of the Trust Group, holds a Bachelor of Science degree inCommerce, major in Accounting from De La Salle University. He obtained his MBA from AIM in 1978. He has been involvedin the banking industry for more than 5 years. He has been an FVP since July 2002.

Alexander C. Escucha, 48, First Vice President (FVP) and Head of Corporate Planning Division, holds a Bachelor of Artsdegree in Economics from UP. He has been involved in the banking industry for more than 5 years. He became FVP inSeptember 2002.

Rhodora Z. Canto, 55, First Vice President (FVP) and Head of Credit Management Group, holds a Bachelor of Science inBusiness Administration from University of the Philippines. She obtained her MBA from AIM in 1975. She has been in thebanking industry for more than 5 years. She became FVP in June 2004.

Note: To the best of our knowledge, no nominees for director (1) own directly/indirectly or a beneficial owner of more than 5% of the Bank’s outstandingshares (2) have any transaction with or involving the Bank or any of its subsidiaries in which a director-nominee and members of their immediate family havea direct/indirect material interest, and (3) have been involved for the past five (5) years in any legal proceeding affecting/involving themselves and/or a materialor substantial portion of their property before any court of law or administrative body in the Philippines or elsewhere, save in the usual routine cases particularlyof the Bank.

(2) Significant Employees

There is no person other than the executive officers who is expected to make a significant contribution tothe Bank.

(3) Family Relationships. (Please refer to Item 9 (1) )

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

(4) Involvement in Certain Legal Proceedings

To the knowledge and/or information of the Bank, there are no events that occurred during the past five(5) years that are material to an evaluation of the ability or integrity of any director, nominee for election asdirector, executive officer, underwriter or control person of the Bank.

Moreover, Criminal Case No. B-2003-345, RTC Branch 89, Bacoor, Cavite, formerly I.S. No. B-01-130supposedly against Mr. Harley T, Sy, among others, was considered withdrawn per Court Order dated 03August 2004 signed by Executive Judge Eduardo Israel Tanguanco, RTC, Bacoor, Cavite, signed xeroxcopy of which was furnished to OCS by Mr. Sy’s office, and which OCS, particularly, Ms. Amy De Leon andMr. Arsenio L. Lim, Jr. found to be the true xerox copy of the signed original thereof shown to them for thepurpose of comparison.

ITEM 10. EXECUTIVE COMPENSATION2005 a 2004 b 2003 b

Top 5 Senior Officers P 63,349,454.00 P 59,411,516.00 P 40,613,912.00

Regular Salaries P 20,056,416.00 P 18,570,756.00 P 17,092,752.00Regular Bonuses 3,342,736.00 3,095,126.00 23,521,160.00Profit Sharing 39,950,302.00 37,745,634.00

1. Gilbert U. Dee Chairman of the Board2. Peter S. Dee President & CEO3. Ricardo R. Chua Exec. Vice Pres. & COO4. Reynaldo L. Lao Sr. Vice Pres & Head, Consumer Banking Group5. Nancy D. Yang Sr. Vice-Pres. & Head, Branch Banking Group

Board of Directors & Officers P 485,534,627.00 P 455,876,247.00 P 349,558,479.00

Regular Salaries P 264.283,016.00 P 244,706,496.00 P 221,321,808.00Regular Bonuses 44,047,169.00 40,784,416.00 128,236,671.00Profit Sharing 177,204,442.00 170,385,335.00

a - Estimated b - Actual

Components of the 2004 Data are as follows: Components of the 2005 Data are as follows:1. Annual Salary consisting of 12 months Basic Salary 1. Annual Salary consisting of 12 months Basic Salary (December, 2004 figures) (2004 figures plus 8.0%)2. Regular Bonuses equivalent to 2 months Basic Salary 2. Regular Bonuses equivalent to 2 months Basic Salary (December, 2004 figures) (2004 figures plus 8.0%)3. Officers’ 2003 Profit Sharing (Taxable Portion) to be paid in 3. Officers’ 2004 Profit Sharing (Taxable Portion) to be paid in 2005 June 2004 (Actual 2003 PS paid in 2004, plus 10%)4. PSD/GUD’s 2003 Taxable PS (As Officer/EXCOM Member) 4. PSD/GUD’s 2004 Taxable PS (As Officer/EXCOM Member) Paid in 2004 (Actual 2003 PS paid in 2004, plus 10%)5. EXCOM Members’ 2003 Taxable PS paid in June 2004 5. EXCOM Members’ 2004 Taxable PS – actual 2003 PS paid in6. Directors’ 2003 Taxable PS paid in May 2004 2004 plus 10%

6. Directors’ 2004 PS to be paid in 2005 – same as actual 2003 PS paid in 2004

There are no compensation arrangements for members of the Board of Directors, other than four (4%) percent that isprovided under Article VIII , Sec. 1 (a) on the Distribution of Net Earnings and Five Hundred Pesos (P500.00) Per Diem perdirector per meeting attended under Article IV Sec. 11 of the Bank’s By-Laws, and there are no warrants/options held byCEO, the named executive officers, and all officers and directors as a group.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

1ITEM 11. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT(1) Security ownership of certain record & beneficial owners of more than 5%1) Title of Class 2) Name and Address

of record/beneficialOwner

3) Amount & Natureof record/beneficialownership ( indicateby “r” or “b”)

4) Percent of Class

Common Sysmart Corp.Rm. 326 Makati StockExchange Bldg., AyalaAve., Makati City

745,747,300.00 “r” 20.408

Common PCD Nominee Corp. (Fil.)G/F MSE Bldg.,6767 Ayala Avenue,Makati City

538,979,300.00 “r” 14.749

Common SM Investment Corp.Rm. 326 Makati StockExchange Bldg., AyalaAve., Makati City

350,996,700.00 “r” 9.605

Common The Int’l CommercialBank of China100 Chin Lin Road,Taipei, 10424 Taiwan,Republic of China

295,226,800.00 “r” 8.079

Common Shoemart, Inc.Rm. 326 Makati StockExchange Bldg., AyalaAve., Makati City

246,174,400.00 “r” 6.737

Common Henry Sy, Sr.Rm. 326 Makati StockExchange Bldg., AyalaAve., Makati City

202,176,100.00 “r” 5.533

HENRY SY, SR. is the record and beneficial owner of the following China Bank’s common shares as of December 31, 2004:No. ofShares

Percentageof Holdings

Direct Holdings: 2,021,761 5.53%

Indirect Holdings:1. Holdings from various brokers 80,916 .22%2. 25% ownership in SM Investment Corporation 1,488,100 4.07%3. 21.31% ownership in Shoemart, Incorporated 535,832 1.47%4. 99.98% ownership in Sysmart Corporation 7,571,377 20.72%

Total holdings direct and indirect 11,697,986 32.01%

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

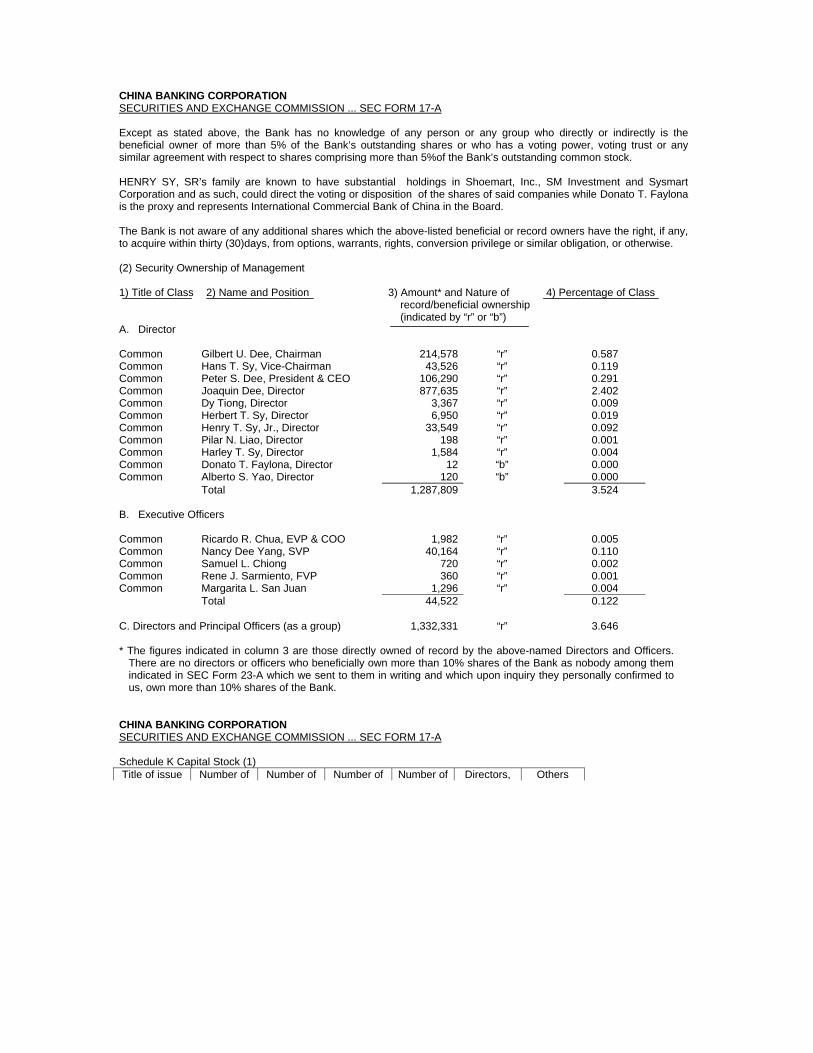

Except as stated above, the Bank has no knowledge of any person or any group who directly or indirectly is thebeneficial owner of more than 5% of the Bank’s outstanding shares or who has a voting power, voting trust or anysimilar agreement with respect to shares comprising more than 5%of the Bank’s outstanding common stock.

HENRY SY, SR’s family are known to have substantial holdings in Shoemart, Inc., SM Investment and SysmartCorporation and as such, could direct the voting or disposition of the shares of said companies while Donato T. Faylonais the proxy and represents International Commercial Bank of China in the Board.

The Bank is not aware of any additional shares which the above-listed beneficial or record owners have the right, if any,to acquire within thirty (30)days, from options, warrants, rights, conversion privilege or similar obligation, or otherwise.

(2) Security Ownership of Management

1) Title of Class 2) Name and Position 3) Amount* and Nature of record/beneficial ownership (indicated by “r” or “b”)

4) Percentage of Class

A. Director

Common Gilbert U. Dee, Chairman 214,578 “r” 0.587Common Hans T. Sy, Vice-Chairman 43,526 “r” 0.119Common Peter S. Dee, President & CEO 106,290 “r” 0.291Common Joaquin Dee, Director 877,635 “r” 2.402Common Dy Tiong, Director 3,367 “r” 0.009Common Herbert T. Sy, Director 6,950 “r” 0.019Common Henry T. Sy, Jr., Director 33,549 “r” 0.092Common Pilar N. Liao, Director 198 “r” 0.001Common Harley T. Sy, Director 1,584 “r” 0.004Common Donato T. Faylona, Director 12 “b” 0.000Common Alberto S. Yao, Director 120 “b” 0.000

Total 1,287,809 3.524

B. Executive Officers

Common Ricardo R. Chua, EVP & COO 1,982 “r” 0.005Common Nancy Dee Yang, SVP 40,164 “r” 0.110Common Samuel L. Chiong 720 “r” 0.002Common Rene J. Sarmiento, FVP 360 “r” 0.001Common Margarita L. San Juan 1,296 “r” 0.004

Total 44,522 0.122

C. Directors and Principal Officers (as a group) 1,332,331 “r” 3.646

* The figures indicated in column 3 are those directly owned of record by the above-named Directors and Officers.There are no directors or officers who beneficially own more than 10% shares of the Bank as nobody among themindicated in SEC Form 23-A which we sent to them in writing and which upon inquiry they personally confirmed tous, own more than 10% shares of the Bank.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

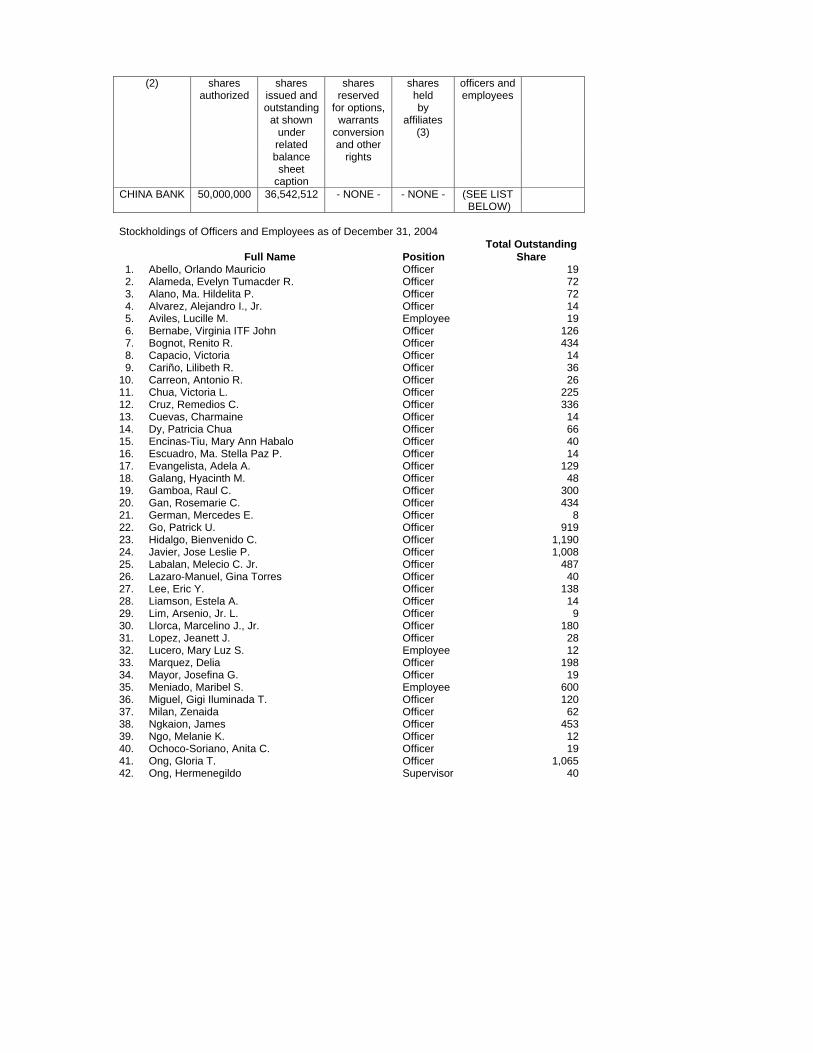

Schedule K Capital Stock (1)Title of issue Number of Number of Number of Number of Directors, Others

(2) sharesauthorized

sharesissued andoutstanding

at shownunderrelated

sharesreserved

for options,warrants

conversionand other

sharesheldby

affiliates(3)

officers andemployees

balancesheet

caption

rights

CHINA BANK 50,000,000 36,542,512 - NONE - - NONE - (SEE LIST BELOW)

Stockholdings of Officers and Employees as of December 31, 2004

Full Name PositionTotal Outstanding

Share 1. 2. 3. 4. 5.

6. 7. 8. 9.10.11.12.13.14.15.16.17.18.19.20.21.22.23.24.25.26.27.28.29.30.31.32.33.34.35.36.37.38.39.40.41.

Abello, Orlando MauricioAlameda, Evelyn Tumacder R.Alano, Ma. Hildelita P.Alvarez, Alejandro I., Jr.Aviles, Lucille M.Bernabe, Virginia ITF JohnBognot, Renito R.Capacio, VictoriaCariño, Lilibeth R.Carreon, Antonio R.Chua, Victoria L.Cruz, Remedios C.Cuevas, CharmaineDy, Patricia ChuaEncinas-Tiu, Mary Ann HabaloEscuadro, Ma. Stella Paz P.Evangelista, Adela A.Galang, Hyacinth M.Gamboa, Raul C.Gan, Rosemarie C.German, Mercedes E.Go, Patrick U.Hidalgo, Bienvenido C.Javier, Jose Leslie P.Labalan, Melecio C. Jr.Lazaro-Manuel, Gina TorresLee, Eric Y.Liamson, Estela A.Lim, Arsenio, Jr. L.Llorca, Marcelino J., Jr.Lopez, Jeanett J.Lucero, Mary Luz S.Marquez, DeliaMayor, Josefina G.Meniado, Maribel S.Miguel, Gigi Iluminada T.Milan, ZenaidaNgkaion, JamesNgo, Melanie K.Ochoco-Soriano, Anita C.Ong, Gloria T.

OfficerOfficerOfficerOfficerEmployeeOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerEmployeeOfficerOfficerEmployeeOfficerOfficerOfficerOfficerOfficerOfficer

1972721419

126434143626

2253361466

4014

12948

300434

8919

1,1901,008

48740

138149

1802812

19819

60012062

4531219

1,06542. Ong, Hermenegildo Supervisor 40

43.44.45.46.47.48.49.5051.52.53.54.55.56.57.58.59.60.61.62.63.64.65.66.67.68.69.70.71.72.73.74.75.76.77.78.

Orencia, Rafael C.Pacheco, Ma. RosarioPaggabao, Emma Z.Pajarillo, Maria Vida G.Purificacion, NoreenQua Tee, ElizabethQuintanilla, Alvin A.Ramirez, Betty ChoaRosario, Reylenita M. DelSan Diego, Nycette O.Santos, Estefania A.Say, Elizabeth C.Sia, Henry D. &/or Evelyn R. SiaSun, Antonio G.Sy, Celso M.Sy, Teresita GabaldonTam, Linda-Susan A.Tan, Annaliza M.Tan, Belenette C.Tan, Phillip M.Tan, Shirley T.Tan, William Winston O.Torralba, Edna A.Torres, Ruben M.Trinidad, Ferdinand C. &/or Salina E. TrinidadTsai, PhilipTy, Jasmin OngchanUy, Johnny L.Uy, Norberto L.Uy, Virginia YuUyquiengco, Roberto C.Virtusio, Ma. Cecilia E.Yabut, Rosario D.Yap, George C.Yong, Vivian L.Yuchenkang, Marilyn

OfficerOfficerOfficerEmployeeOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerEmployeeOfficerOfficerOfficerOfficerEmployeeOfficerOfficerEmployeeOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficerOfficer

3314141414

5481419161462

2257219

85633

216866833

2172,978

129115

721621633

5253182251322161440

318

ITEM 12. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

There is no transaction with or involving the Bank or any of its subsidiaries in which a director, executive officer, orstockholder owning five (5%) percent or more of total outstanding shares and members of their immediate family had or is tohave a direct or indirect material interest.• The Bank retains the following law firms:

• Angara Abello Concepcion Regala & Cruz Law Offices• Cruz Durian Agabin Atienza Alday & Tuazon• Lim Vigilia Alcala Dumlao & Orencia

• External auditor -- Sycip, Gorres, Velayo & CompanyCHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

PART IV EXHIBITS AND SCHEDULES

(a) Exhibits

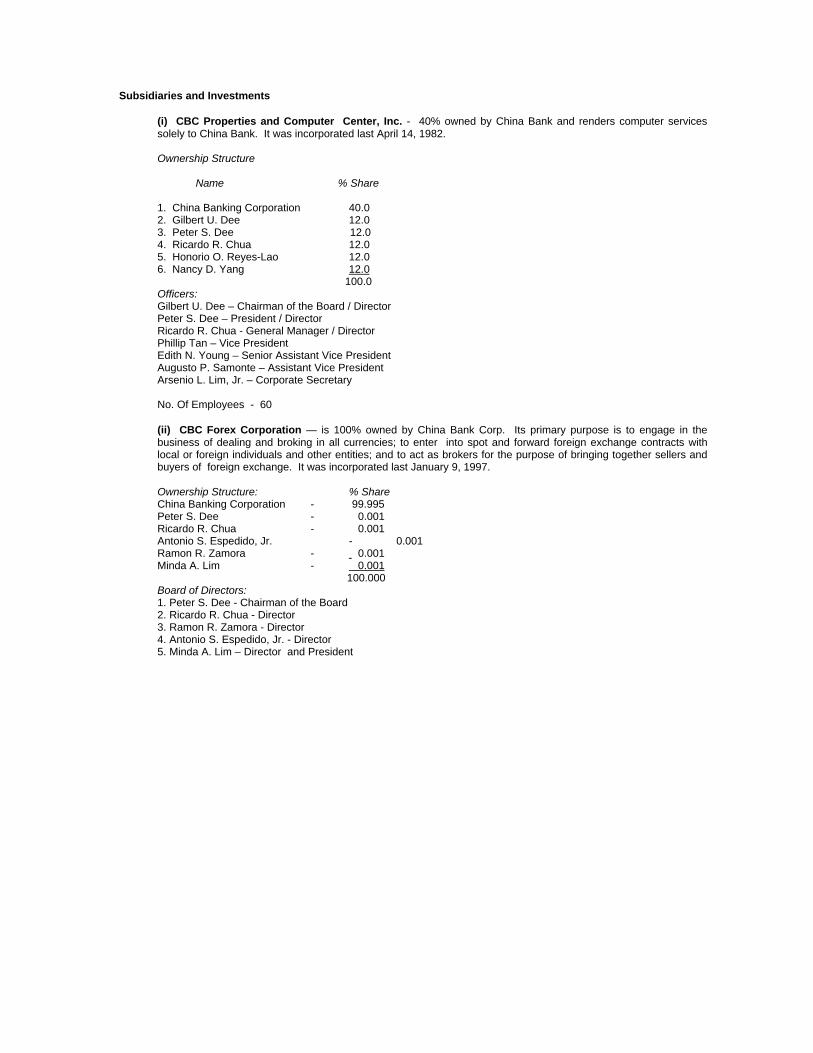

Subsidiaries and Investments

(i) CBC Properties and Computer Center, Inc. - 40% owned by China Bank and renders computer servicessolely to China Bank. It was incorporated last April 14, 1982.

Ownership Structure

Name % Share

1. China Banking Corporation 40.02. Gilbert U. Dee 12.03. Peter S. Dee 12.04. Ricardo R. Chua 12.05. Honorio O. Reyes-Lao 12.06. Nancy D. Yang 12.0

100.0Officers:Gilbert U. Dee – Chairman of the Board / DirectorPeter S. Dee – President / DirectorRicardo R. Chua - General Manager / DirectorPhillip Tan – Vice PresidentEdith N. Young – Senior Assistant Vice PresidentAugusto P. Samonte – Assistant Vice PresidentArsenio L. Lim, Jr. – Corporate Secretary

No. Of Employees - 60

(ii) CBC Forex Corporation — is 100% owned by China Bank Corp. Its primary purpose is to engage in thebusiness of dealing and broking in all currencies; to enter into spot and forward foreign exchange contracts withlocal or foreign individuals and other entities; and to act as brokers for the purpose of bringing together sellers andbuyers of foreign exchange. It was incorporated last January 9, 1997.

Ownership Structure: % ShareChina Banking Corporation - 99.995Peter S. Dee - 0.001Ricardo R. Chua - 0.001Antonio S. Espedido, Jr. - 0.001Ramon R. Zamora - 0.001Minda A. Lim - 0.001

100.000Board of Directors:1. Peter S. Dee - Chairman of the Board2. Ricardo R. Chua - Director3. Ramon R. Zamora - Director4. Antonio S. Espedido, Jr. - Director5. Minda A. Lim – Director and President

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

Officers:Peter S. Dee - Chairman of the BoardMinda A. Lim - PresidentBelenette Ching Tan - Corporate SecretaryCharis Tepoot - Chief Dealer & Treasurer

(iii) Chinabank Insurance Brokers, Inc. — is 100% owned by China Bank Corp. Its primary purpose is to act asa broker in soliciting, procuring, negotiating, receiving, managing and forwarding applications for fire, casualty, plateglass, automobiles, trucks and other motor vehicles, accident, health, burglary, rent, marine, credit, disability, lifeinsurance, and all other kinds of insurance, including reinsurance contracts or in any other manner aiding in takingout insurance, collecting payment of premiums due on such policies and doing such other business as may bedelegated to brokers or such companies in the conduct of a general insurance brokerage business. It wasincorporated last January 16, 1998.

Ownership StructureName # of Shares

1. China Banking Corporation 14,995 2. Peter S. Dee 1 3. Ricardo R. Chua 1

4. Nancy D. Yang 15. Reynaldo L. Lao 16. Ramon R. Zamora 1

15,000

OfficersPeter S. Dee - Chairman of the Board

Ricardo R. Chua - President Ramon R. Zamora - Treasurer Gerard E. Reonisto - General Manager Omar D. Vigilia - Corporate Secretary

No. of Employees - 16

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

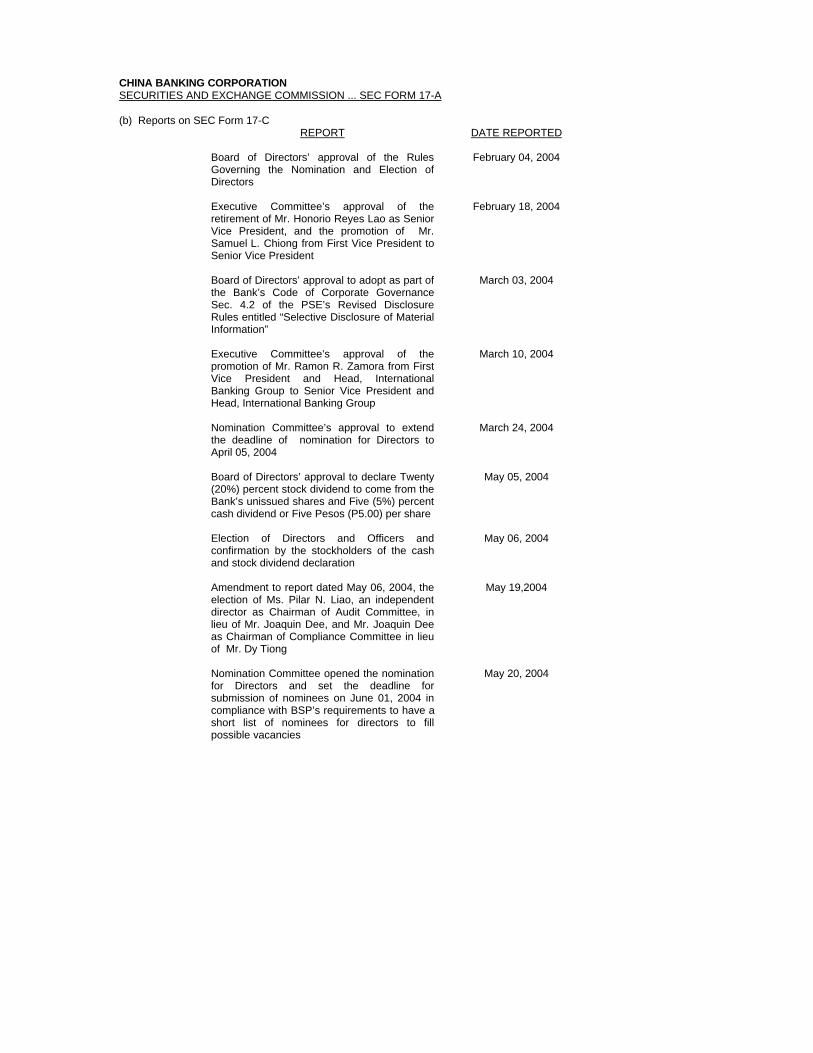

(b) Reports on SEC Form 17-CREPORT DATE REPORTED

Board of Directors’ approval of the RulesGoverning the Nomination and Election ofDirectors

February 04, 2004

Executive Committee’s approval of theretirement of Mr. Honorio Reyes Lao as SeniorVice President, and the promotion of Mr.Samuel L. Chiong from First Vice President toSenior Vice President

February 18, 2004

Board of Directors’ approval to adopt as part ofthe Bank’s Code of Corporate GovernanceSec. 4.2 of the PSE’s Revised DisclosureRules entitled “Selective Disclosure of MaterialInformation”

March 03, 2004

Executive Committee’s approval of thepromotion of Mr. Ramon R. Zamora from FirstVice President and Head, InternationalBanking Group to Senior Vice President andHead, International Banking Group

March 10, 2004

Nomination Committee’s approval to extendthe deadline of nomination for Directors toApril 05, 2004

March 24, 2004

Board of Directors’ approval to declare Twenty(20%) percent stock dividend to come from theBank’s unissued shares and Five (5%) percentcash dividend or Five Pesos (P5.00) per share

May 05, 2004

Election of Directors and Officers andconfirmation by the stockholders of the cashand stock dividend declaration

May 06, 2004

Amendment to report dated May 06, 2004, theelection of Ms. Pilar N. Liao, an independentdirector as Chairman of Audit Committee, inlieu of Mr. Joaquin Dee, and Mr. Joaquin Deeas Chairman of Compliance Committee in lieuof Mr. Dy Tiong

May 19,2004

Nomination Committee opened the nominationfor Directors and set the deadline forsubmission of nominees on June 01, 2004 incompliance with BSP’s requirements to have ashort list of nominees for directors to fillpossible vacancies

May 20, 2004

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

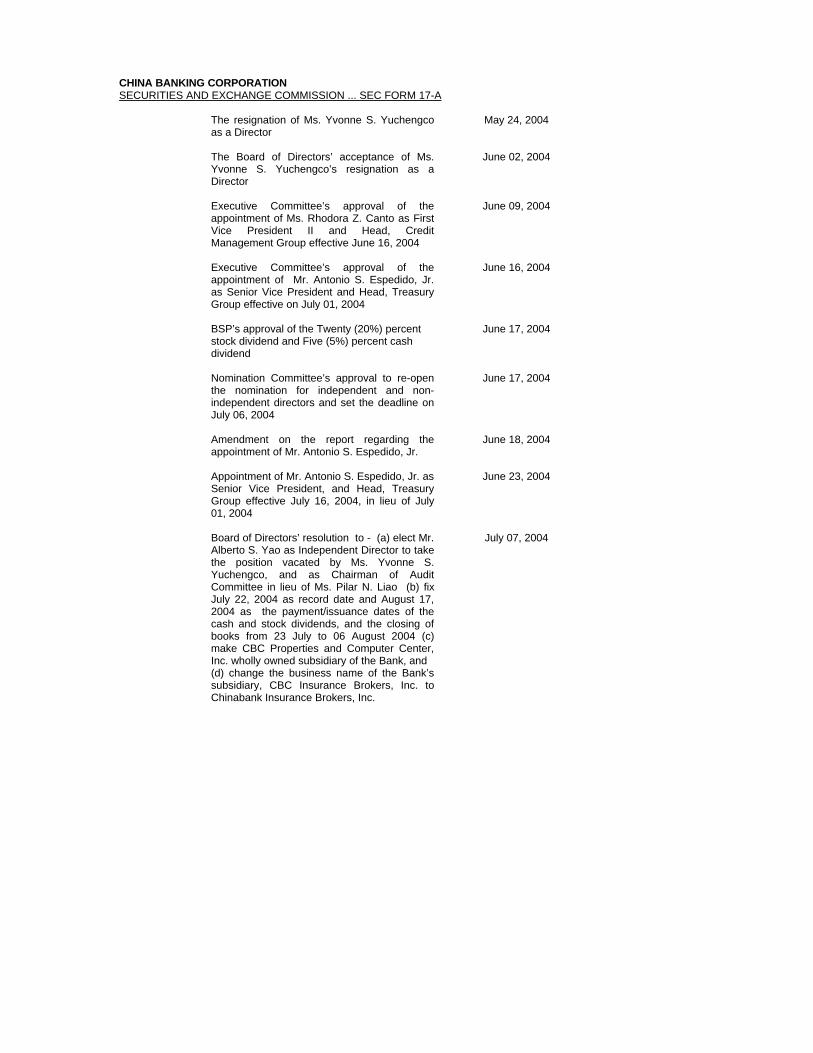

The resignation of Ms. Yvonne S. Yuchengcoas a Director

May 24, 2004

The Board of Directors’ acceptance of Ms.Yvonne S. Yuchengco’s resignation as aDirector

June 02, 2004

Executive Committee’s approval of theappointment of Ms. Rhodora Z. Canto as FirstVice President II and Head, CreditManagement Group effective June 16, 2004

June 09, 2004

Executive Committee’s approval of theappointment of Mr. Antonio S. Espedido, Jr.as Senior Vice President and Head, TreasuryGroup effective on July 01, 2004

June 16, 2004

BSP’s approval of the Twenty (20%) percentstock dividend and Five (5%) percent cashdividend

June 17, 2004

Nomination Committee’s approval to re-openthe nomination for independent and non-independent directors and set the deadline onJuly 06, 2004

June 17, 2004

Amendment on the report regarding theappointment of Mr. Antonio S. Espedido, Jr.

June 18, 2004

Appointment of Mr. Antonio S. Espedido, Jr. asSenior Vice President, and Head, TreasuryGroup effective July 16, 2004, in lieu of July01, 2004

June 23, 2004

Board of Directors’ resolution to - (a) elect Mr.Alberto S. Yao as Independent Director to takethe position vacated by Ms. Yvonne S.Yuchengco, and as Chairman of AuditCommittee in lieu of Ms. Pilar N. Liao (b) fixJuly 22, 2004 as record date and August 17,2004 as the payment/issuance dates of thecash and stock dividends, and the closing ofbooks from 23 July to 06 August 2004 (c)make CBC Properties and Computer Center,Inc. wholly owned subsidiary of the Bank, and

July 07, 2004

(d) change the business name of the Bank’ssubsidiary, CBC Insurance Brokers, Inc. toChinabank Insurance Brokers, Inc.

CHINA BANKING CORPORATIONSECURITIES AND EXCHANGE COMMISSION ... SEC FORM 17-A

PSE’s approval of the listing of the Bank’sadditional common shares to cover the 20%stock dividend

August 09, 2004

Retirement from service of Mr. Danilo A.Alcoseba, Senior Vice President and Head,Treasury Group

August 20, 2004

Board of Directors’ approval of the organizationand incorporation initially of a wholly ownedSpecial Purpose Vehicle (SPV) with authorizedcapital of P500 million and Paid –up capital ofP31,250,000.00.

September 02, 2004

Board of Directors’ approval of the creation ofRisk Management Committee, Compensationor Remuneration Committee and CorporateGovernance Committee in compliance withBSP Circular No. 456, Series of 2004

December 09, 2004

SIGNATURES

Pursuant to the requirement of Section 17 of the Code and Section 141 of the Corporation Code, this report is signed onbehalf of the issuer by the undersigned, thereunto duly authorized, in the city of Makati on this 5th day of April 2005.

By:

(SGD) PETER S. DEE (SGD) RICARDO R. CHUA Principal Executive Officer Comptroller

(SGD) RICARDO R. CHUA (SGD) ZACARIAS B. ANTONIO Principal Operating Officer Principal Accounting Officer

(SGD) ANTONIO S. ESPEDIDO, JR. (SGD) ARSENIO L. LIM, JR. Principal Financial Officer Corporate Secretary

SUBSCRIBED AND SWORN to before me this 5th day of April 2005 affiant (s) exhibiting to me their Community TaxCertificates, as follows:

NAMES COMMUNITY DATE OF PLACE OFTAX CERT. NO. ISSUE ISSUE

PETER S. DEE 13997135 02/11/05 ManilaRICARDO R. CHUA 23044331 03/11/05 MandaluyongANTONIO S. ESPEDIDO, JR. 09572840 04/01/04 MuntinlupaZACARIAS B. ANTONIO 0217392 01/20/05 ManilaARSENIO L. LIM, JR. 15189755 01/18/05 Makati

Doc. No.: 43 (SGD) FLORA DE PANO-SOLLERPage No.: 10 Notary Public for Makati CityBook No.: 43 Appl No. M-101 until 31 DecemberSeries of 2005 11th Floor China Bank Building

Paseo de Roxas, Makati CityPTR# 9441574:01-07-05; Makati CityIBP# 631501;01-03-05; Quezon CityRoll of Attorneys No. 39191

STATEMENT OF MANAGEMENT’S RESPONSIBILITYFOR

FINANCIAL STATEMENTS

The Management of China Banking Corporation is responsible for all information and representations contained in theconsolidated financial statements for the years ended December 31, 2004 and 2003. The financial statements have beenprepared in conformity with generally accepted accounting principles and reflect amounts that are based on best estimatesand informed judgment of management with an appropriate consideration of materiality.

In this regard, management maintains a system of accounting and reporting which provides for the necessary internalcontrols to ensure that transactions are properly authorized and recorded, assets are safeguarded against unauthorized useor disposition and liabilities are recognized. The management likewise discloses to the company’s audit committee and to itsexternal auditor: (i) all significant deficiencies in the design or operation of internal controls that could adversely affect itsability to record, process, and report financial data; (ii) material weaknesses in the internal controls; and (iii) any fraud thatinvolves management or other employees who exercise significant roles in internal controls.

The Board of Directors reviews the consolidated financial statements before such statements are approved and submitted tothe stockholders of the company.

Sycip, Gorres, Velayo & Co., the independent auditors appointed by the stockholders, have examined the consolidatedfinancial statements of the Company in accordance with generally accepted auditing standards and have expressed theiropinion on the fairness of presentation upon completion of such examination, in their report to stockholders.

(SGD) Ricardo R. Chua (SGD) Peter S. Dee Executive Vice President & COO President & CEO

(SGD) Gilbert U. Dee Chairman of the Board

Republic of the Philippines Makati City S.S

Subscribed and sworn to before me this 22nd day of March, 2005, affiants exhibiting to me theirCommunity Tax Certifcates Nos. as follows: