chuan-san wang 1. research question does payout policy affect investment decision ? do discretionary...

TRANSCRIPT

Chuan-San Wang

1

Research Question• Does payout policy affect investment

decision ?• Do discretionary accruals differ from

other earnings components in cash payout decisions?

• Does managers’ accounting discretion mitigate the tension between payouts and investment?

2

Motivationpayout policy can be relevantCorporate decisions can reveal

earnings qualityAccrual accounting can mitigate

competition for capital resources

3

ImportanceDividends can be value-relevant,

DeAngelo and DeAngelo (2006) Several crucial studies are based on

the irrelevance theorem, e.g., Ohlon’s (1995) valuation model

4

Contributions• It shows the causality from dividends to

investment • It quantifies the competition for capital

resources• It focuses on the impact of earnings

quality on both dividends and investments• It provides new evidence based on

actual corporate actions5

Literature #1Miller and Modigliani (1961) theoretically

propose that dividend policy is value-irrelevant because it is

made after the investment decisionThe survey evidence from Brav et al. (2005)

indicates the opposite: dividend choices are made simultaneously with

(or perhaps a bit sooner than) investment decisions

H1: The magnitude of cash dividends is simultaneously determined with that of capital expenditures.

6

Literature #2Earnings can explain the propensity to pay

dividends (Fama and French, 2001)The three earnings components are similar in

explaining dummy for dividend increase (Subramanyam, 1996)

Accrual accounting provides additional informationH2: discretionary accruals increase dividend

payouts by mitigating financial constraints.H3: the marginal propensity to pay dividends

for discretionary accruals differs from that of other earnings components

7

Research design #1Cash payout equation

2-stage regressionsSimultaneity between Y and X

variablesdiagnostic statistics

8

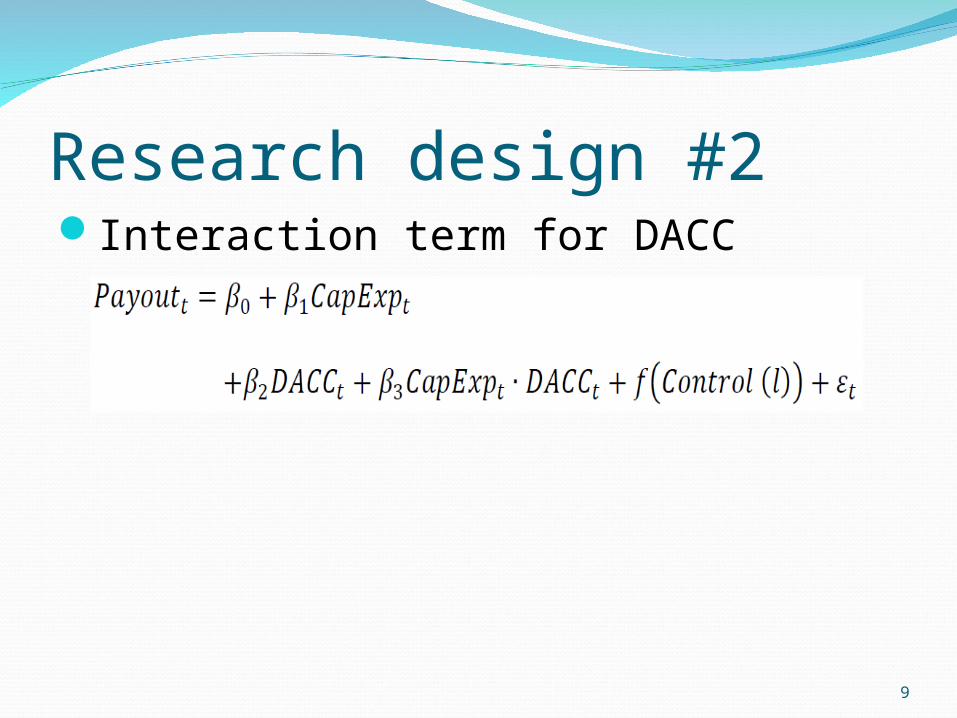

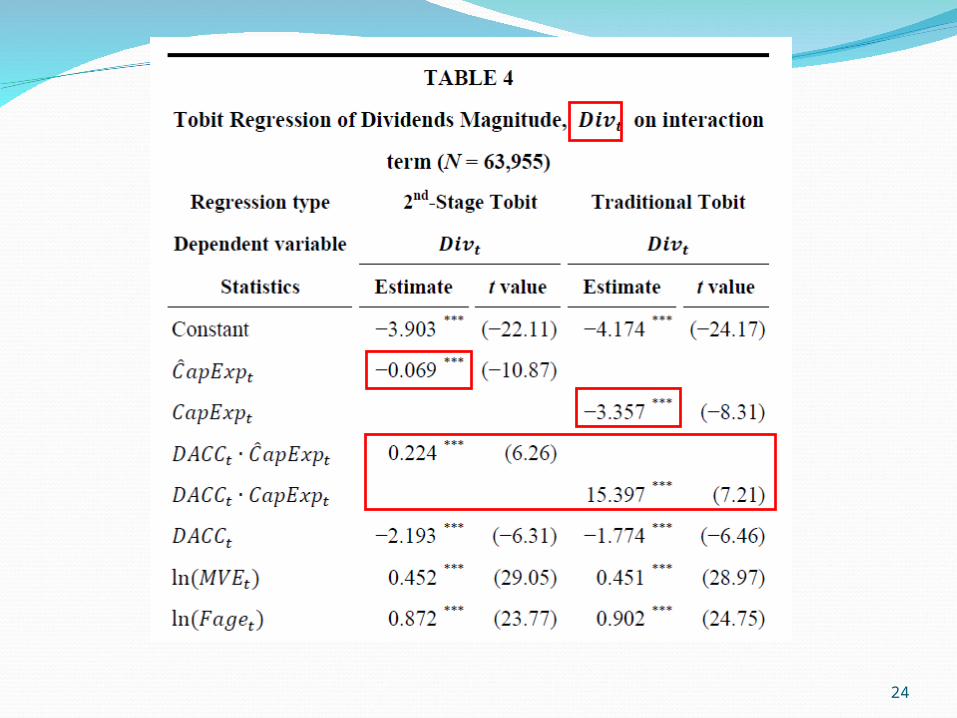

Research design #2Interaction term for DACC

9

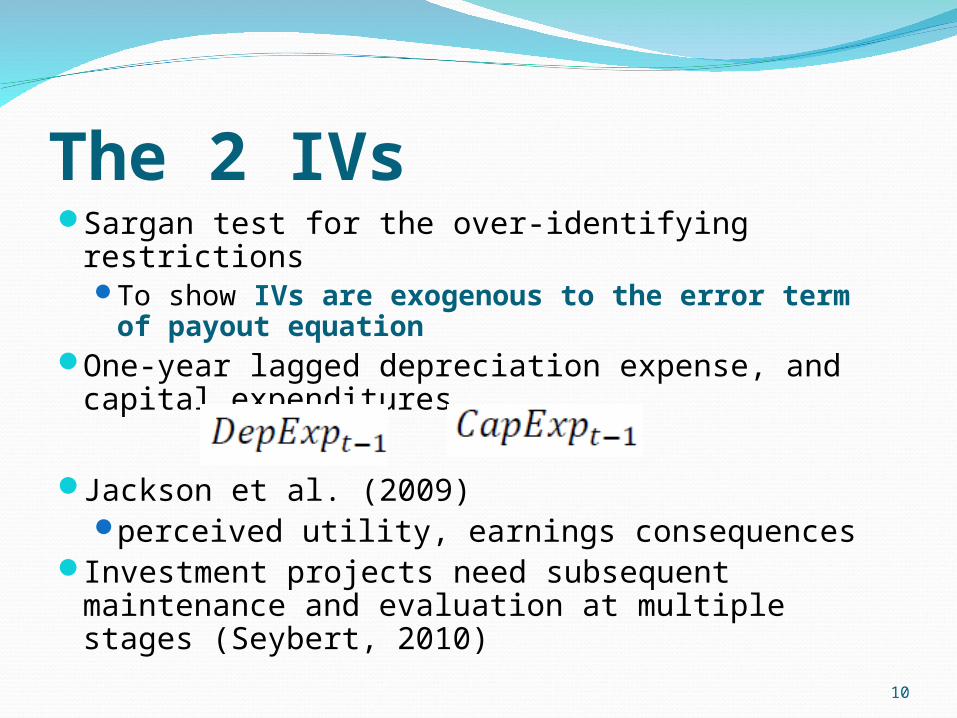

The 2 IVsSargan test for the over-identifying restrictions

To show IVs are exogenous to the error term of payout equation

One-year lagged depreciation expense, and capital expenditures

Jackson et al. (2009)perceived utility, earnings consequences

Investment projects need subsequent maintenance and evaluation at multiple stages (Seybert, 2010)

10

Discretionary Accrualscross-sectional version of the Jones modelused in Daniel et al. (2008)

11

Control Variable for Dividendslife-cycle theory

Fama and French (2001), DeAngelo et al. (2006), Chay and Suh (2009)

senior firms pay more dividends firm size, MVE firm age, Tage investment opportunities, MtB retained earnings, RE/TE cash flow uncertainty, SRVOL

12

More Control Variablesdividends persistency and financial

slackLintner (1956), Brav et al. (2005)

Past dividends

financial leverage

13

Other Control Variablefirm performance.

Fama and French (2001)value-weighted, market-adjusted buy-and-hold annual stock return, BHARt

operating cash flows, OCFtreturn on assets, ROAt

14

Sample2010 version of CompustatCRSP

1989–2008 63,955 firm–years with necessary data available

15

16

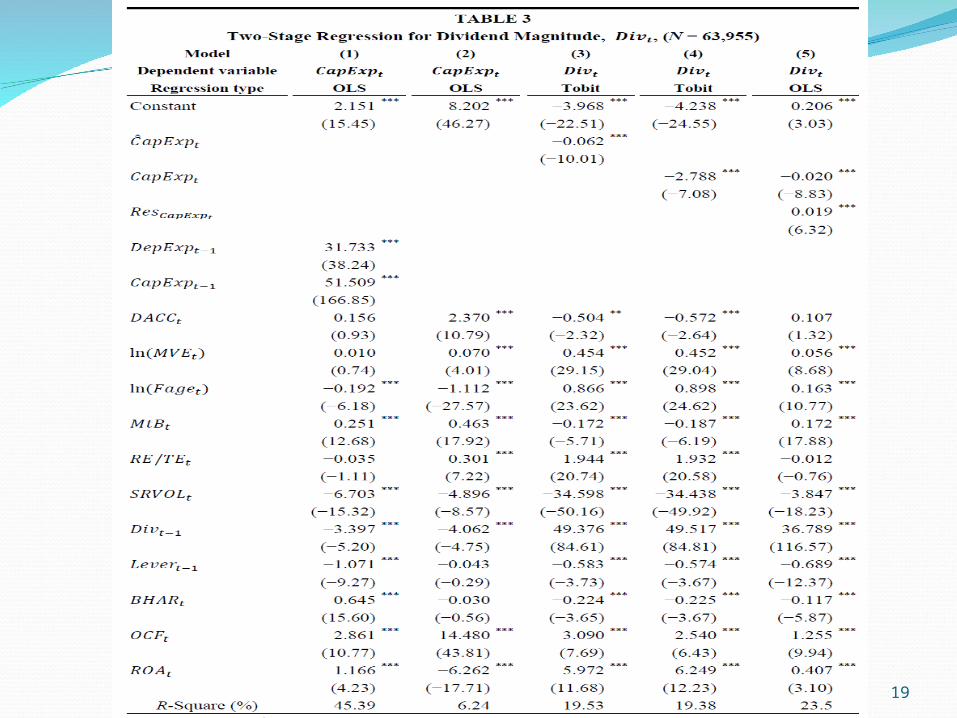

17

Baseline resultsIVs for capital expenditures are valid

and stronginvestment magnitude is determined

simultaneously with cash dividendsinvestments have a significantly

negative effect on dividendsbut the economic size is rather small

18

19

(0.4539-0.0624)/(1-0.0624)=0.4176

20

over-identifying testOLS regression of the second-stage

residuals on all exogenous variables (including the two IVs)

the R2 is 0.0000The two IVs are exogenous

21

22

23

24

25

26

27

28

RobustnessOther measures of discretionary

accrualsTeoh et al. (1998), Dechow and Dichev

(2002), and Ball and Shivakumar (2005)How to measure accruals is

independent for the dampening effect of investment on

dividendsthe endogeneity tests

29

ConclusionsDividend policy is at least simultaneously determined

with investment decisions (Brav et al 2005)The irrelevance theorem of Miller and Modigliani

(1961) may be questionable (DeAngelo and DeAngelo 2006)

The competition between dividends and investmentis small in sizecan be mitigated by managers’ use discretionary

accrualsIt is inconclusive for the propensity to pay dividends

for discretionary accruals

30