cifuentes settles with wachovia new structure weds whole abs

TRANSCRIPT

PUBLISHED BY SOURCEMEDIA VOL. 6 / NUMBER 2 JANUARY 16, 2006

Wachovia Securities reached asettlement with its former

head of CDO research, ArturoCifuentes, who filed a Sarbanes-Oxley complaint against the bankarguing that he was improperlydismissed. The settlement, however,may not mean the end of theSecurities and ExchangeCommission’s ongoing investiga-tion into the matter.

Cifuentes contends Wachoviafired him last April after he hadrefused to sign an analyst certifica-tion on a research report stating thathis compensation was not tied to his

recommendations. He subsequentlyfiled a whistleblower complaintwith the Department of Labor’sOccupational Safety and HealthAdministration (OSHA). UnderSarbanes-Oxley, OSHA has jurisdic-tion over whistleblower complaintsin the securities industry.

As a part of the settlement,Cifuentes agreed to withdraw hiscomplaint to OSHA. But the SEC,which is automatically copied onOSHA complaints, could move for-ward with its own probe.Regulators in the SEC’s Atlanta

Cifuentes settles with WachoviaBut bank may not be out of the woods

European corporate securitizationsare poised for another slow year,

with bank lending remaining thefinancing route of choice. And vol-umes could be further pressured thisyear with a developing new trend thatcould see some ageing corporate dealsrefinished as CMBS deals in 2006.

“Traditionally, activity in this sectorhas been driven by private equity firmsusing ABS as an exit to funding ven-tures, but the banking market hasbeen so buoyant and we won’t see anincrease in issuance until banks are lessprone to issue in this area,” said AlainCarron at a Standard & Poor’s pressconference last week in London. Therelatively low interest rates and bor-rowing costs for European corporates

New structure wedswhole ABS & CMBS

In what may not come as a hugesurprise to market participants,

large CDO managers in 2005 becameeven larger — with 28 collateralmanagers representing half of theU.S. CDO market in terms of out-standing liabilities by the third quar-ter of the year, according to Standard& Poor’s. The 10 largest managerslast year comprised almost 30% ofthe CDO market.

Conversely, in 2004, 35 managersmade up 50% of the CDO market,with the 10 largest managersaccounting for 25% of the market.The rating agency found three maintrends among collateral manager par-ticipation in 2005: the largest CDOcollateral managers increased market

Big CDO managers bulk up to 3Q05

- SEE ABS & CMBS ON PAGE 16 - - SEE CDO ON PAGE 4 -

Buyout firm The Carlyle Grouphas hired Martin Glavin as an associ-ate director from Prudential M&G.The new hire plus Louis Reynolds,who came on board last Septemberfrom General Electric Co., booststo 10 Carlyle’s roster of bankers andanalysts who trade leveraged credits,including CLOs.

Dominion Bond Rating Service

- CONTINUED ON PAGE 4 -

Securitization NewsUpcoming events...............................................2

Asset-Backed:Auto tiering to shift ..........................................5Subprime defaults drop ....................................6ABS issuance predictions ................................7U.S.ABS market warms up ............................8Continued robust CLO issuance ................10BMA bond issuance forecasts ......................12

Mortgage-Backed:Strong start for MBS ......................................13Prepays to slow with housing ......................14Spread volatility in mortgages ......................15

International:New kind of German CMBS........................16U.K. smoking ban ............................................17Granite deal as benchmark ..........................18AEON card deal in the works ....................19

Data:Trade Matrix ..............................................20-21Asset-backeds ............................................22-27Mortgage-backeds ....................................28-29Ratings Watch ............................................31-35Scorecards....................................................36,38

C O N T E N T S

W H I S P E R S

- SEE CIFUENTES ON PAGE 9 -

www.asreport.com

2 - ASSET SECURITIZATION REPORT - January 16, 2006

U P C O M I N G E V E N T SAsset Securitization Report

One State Street Plaza, 27th FloorNew York, NY 10004

EDITORIALEditor-in-chief Ronald [email protected] 212.803.8722Managing Editor Karen [email protected] 212.803.8735Senior Editor/Europe Nora [email protected] (44) (0) 207.061.6487Senior Editor/Emerging Markets Felipe [email protected] 212.803.8709Associate Editor/U.S. ABS/CDOs Allison [email protected] 347.306.7848Associate Editor/U.S. ABS Grant [email protected] 212.803.8734Contributor Editor/Private Placements Hema [email protected] 212.803.8741Contributing Editor/Asian Markets Rob [email protected]

Editorial fax: 212.295.1702

SCREEN ANALYSTSCMBS Chris [email protected] 617.856.2865MBS Sally Ann [email protected] 847.579.1704Contributors: Bonnie McGeer, Chris DeReza

PUBLISHINGPublisher John Toth

212.803.6565Advertising Sales,National Account Manager David Harkey

212.803.8773Advertising Coordinator Scarlett Prado

212.803.8707Marketing Robert Han

212.803.6551Circulation Sales William Baneky

212.803.8481Director of Reprint Sales Howard Gilbert

800.367.3989

PRODUCTION & FULFILLMENT

Exec. Dir. of Creative Services Sharon PollackArt Director Yohanna WillheimAssistant Art Director Fritz LauroreExec. Dir. of Circulation John CreweExec. Dir. of Manufacturing Stacy FerraraAssoc. Production Manager Brian GoldmanDistribution Manager Mark FerraraAssistant Distribution Manager Walter HookerFulfillment Manager Lynn Sherwood

SOURCEMEDIA, INC.Chairman & CEO James M. MalkinChief Financial Officer William JohnstonChief Technology Officer Jeff ScottPresident, Publishing & Corporate Groups Bruce MorrisPresident, Securities Group Frank QuigleySenior V.P., Operations Celie BaussanV.P., Human Resources Robert DeNoiaV.P., Finance Richard AntoneckV.P., Marketing & Communications Anne O’Brien

SUBSCRIPTION INFORMATION

Phone: 800.221.1809 212.803.8333Bulk subscription US/Canada $2,195Annual Rate (48 issues) International $2,295Fax: 212.803.1592 [email protected] Securitization Report - (ISSN # 1547-3422) is published weekly exceptJanuary 3, August 28, September 4, December 25 by SourceMedia, One State StreetPlaza, 27th Floor, New York, NY 10004.Postmaster: Send address changes to Asset Securitization Report, SourceMedia,One State Street Plaza, 27th Floor, New York, NY 10004.All rights reserved. Photocopy permission is available solely through SourceMedia, OneState Street Plaza, 27th Floor, New York, NY 10004. Copying, photocopying, or dupli-cating this publication in any form other than as permitted by agreement withSourceMedia is prohibited and may constitute copyright infringement subject to lia-bility up to $100,000 per infringement (Title 17, U.S. code). For photocopy permission, back issues and bulk distribution needs, please contact Customer Service at(800) 221-1809 or e-mail: [email protected].

Asset Securitization Report is a general-circulation publication. No data herein is orshould be construed to be a recommendation for the purchase, retention or sale ofsecurities, or to provide investment advice of the companies mentioned or advertised.SourceMedia, its subsidiaries and its employees may, from time to time, purchase,own, or sell securities or other investment products of the companies discussed oradvertised in this publication.©2006 Asset Securitization Report and SourceMedia, Inc. All rights reserved.

January:Jan. 19 -20 - Princeton, N.J. - Strategic

Research Institute is hosting a confer-

ence on ‘Separating Alpha from Beta to

Enhance Portfolio Returns (From Theory

to Practice)’ at the Hyatt Regency

Princeton. For further information, or to

register, go to: www.srinstitute.com

Jan. 25-27 - Laguna Beach Calif. -

Information Management Network is

hosting the third annual Winter forum on

‘Real Estate Opportunity & Private Fund

Investing’ at the Montage Resort & Spa.

For full details, or to register, go to:

www.imn.org

Jan. 29-Feb. 1 - Las Vegas, Nev. - The

American Securitization Forum invites

you to attend its ‘ASF 2006 at the Wynn

Las Vegas Hotel. For full conference agen-

da, or to register, go to: www.ameri-

cansecuritization.com

Jan.29-Feb.1 - Scottsdale,Ariz. - Strategic

Research Institute is hosting the fourth

annual ‘Institutional Real Estate Investing

Forum’ at the Fairmont Scottsdale

Princess hotel. For further information, or

to register, go to: www.srinstitute.com

February:Feb. 5-8 - Orlando, FL. - The Mortgage

Bankers Association presents its

‘Commercial Real Estate

Finance/Multifamily Housing Convention &

Expo 2006’ at the Walt Disney Swan and

Dolphin hotel. For more information,or to

register, go to: www.mortgagebankers.org/

or call 1-800-793-6222

Feb. 7-10 - Phoenix, Ariz. - Information

Management Network presents its

eleventh annual ‘ABS West 2006’ at the

J.W. Marriott Desert Ridge Resort &

Spa. For more information, or to register,

go to: http://secure.imn.org

Feb. 7 - Las Vegas, Nev. - Strategic

Research Institute is hosting the second

annual ‘Tranche B Lending & SCIL

Finance Summit’ at the Bellagio Hotel

and Casino. For further information, or

to register, go to: www.srinstitute.com

Feb. 7-9 - Las Vegas, Nev. - Strategic

Research Institute invites you to attend

the fifth annual ‘Asset Based Lending in

the Capital Markets’ conference at the

Bellagio Hotel and Casino. For further

information, or to register, go to:

www.srinstitute.com

Feb. 14-17 - Phoenix, Ariz. - The

Mortgage Bankers Association presents

its ‘National Mortgage Servicing

Conference & Expo’ at the Phoenix

Civic Plaza. For more information, or to

register, go to:

www.mortgagebankers.org/ or call 1-

800-793-6222

Feb. 15-17 - Orlando FL - Standard &

Poor’s presents its ‘Housing Finance

2006’ conference at the Hyatt Regency

Grand Cypress Resort. For more infor-

mation, or to register, e-mail semi-

[email protected] or call

(212) 438-2800.

To include an event in the calendar please e-mail:[email protected]

4 - ASSET SECURITIZATION REPORT - January 16, 2006

share; a higher number of new man-agers entered the space — particular-ly in the ABS CDO, CLO and com-mercial real estate CDO sectors; andthe more established managers ven-tured into new asset types.

Overall, the largest CDO manag-er as of Sept. 30 was Los Angeles,CA-based Trust Company of theWest, with $22 billion in assetsunder management. The manager,which led by a substantial margin,also took the number one spot forlargest CDO of ABS manager, with$15.55 billion in assets under man-agement. TCW recently told ASR itplans to keep growing — marketpermitting — with projections fortotal structured finance CDO assetsunder management this month at$23 billion (see ASR, 12/05/05).

S&P counted total U.S. CDOissuance through Sept. 30 at $132.9billion, up 16% from the $111.6 bil-lion in volume during all of 2004.The largest contributions to thegrowth in overall CDO issuancecame from the ABS CDO and CLOmarkets, according to S&P. A littlemore than a third of the top 25 CDOmanagers across all asset types gener-ally had consistent standings withyear-end 2004 numbers.

Babson Capital Managementcame in at number two as thelargest overall CDO manager as ofSept. 30. Babson had $12.53 billionin CDO assets under management.Duke Funding Managementcame in as the third largest overallCDO manager, with $10.45 billionin assets under management, fol-lowed by Credit SuisseAlternative Capital, with $9.97billion and BlackRock FinancialManagement Inc., which came inat fifth place with $9.49 billion inCDO assets under management.

In addition, four managers thatdidn’t make the top 25 in 2004 hitthe big league by 3Q05. Bear

Stearns Asset Management placed13th, with $5.77 billion in liabili-ties; Aladdin Capital ManagementLLC made it up to 21st place with$4.28 billion in assets under man-agement; Paramax Capital Groupwas close behind at 22nd place with$4.27 billion and DeclarationManagement and Research edgedinto the 24th place spot with $4.14billion in assets under management.

Through the third quarter of lastyear, 15% of new CDO issuance washandled by managers either new tothe CDO market or new to the assettype, according to S&P. A fair portionof the new managers, however, con-sisted of seasoned professionals thathad branched off to start their ownfirms. Others, such as in the CRECDO sector, were familiar with thecollateral, but were for the first timedrawn to the securitization structureas a form of matched-term financing.

Among the largest CDO of ABSmanagers through the third quarterof 2005 were, after TCW, DukeFunding Management LLC, risingeight spots from year-end 2004 totake second place with $10.45 billionin assets under management;Brightwater Capital Management,with $9 billion; BlackRockFinancial Management, with $7.32billion; and Vanderbilt CapitalAdvisors, in fifth place with $6.57billion, according to S&P data.

Leading as the top CLO man-agers during the same time periodwere Credit Suisse AlternativeCapital, in the lead with $6.51 bil-lion; Sankaty Advisors, which rosefrom ninth place in 2004 to a sec-ond place finish as of the third quar-ter with $4.88 billion; BabsonCapital Management, with $4.62billion; Highland CapitalManagement with $4.52 billionand Ares Capital Management,rounding out the top five CLOmanagers with $3.94 billion. — AP

has appointed Jerry Marriott as asenior vice president in its Toronto-based Canadian structured financegroup. Marriott, who will be reportingto Assistant Group Managing DirectorHuston Loke, joins DBRS fromBMO Nesbitt Burns’ securitizationand structured finance group, wherehe worked on a variety of ABCP andABS deals and asset classes, includingcredit card receivables, rental carfleets, and floorplan financing. Beforejoining the securitization and struc-tured finance group, Marriot spent anumber of years in the corporatebanking and Treasury functions atBank of Montreal. Marriott receivedhis MBA from the University ofWestern Ontario and his LLB fromDalhousie University.

Law firm Loeb & Loeb has hiredJoseph Sverchek as a partner in itsNew York office. Prior to the move,he was Special Counsel atCadwalader Wickersham & Taft,which he joined in 1998. Svercheckhas experience representing spon-sors and placement agents alike instructuring ABCP in both the U.S.and European markets. On the capi-tal markets front, he has covered col-lateralized debt obligations, mediumterm notes, and structured invest-ment vehicles. Among asset classes,Svercheck has worked on tradereceivables, equipment leases, autoloans, tax liens, automobile leases,dealer floor plan receivables andothers.“Adding Joe is another step inour continuing commitment toexpand our capital markets pres-ence,” said Loeb & Loeb’s Co-ChairMichael Beck.

Australia’s Macquarie Bank isrumored to be in talks to buy major

- CONTINUED ON PAGE 6 -

- CONTINUED FROM PAGE 1 -

A S S E T - B A C K E D S

CDO CONTINUED FROM PAGE 1

www.asreport.com - January 16, 2006 - 5

Tiering in the auto sector is poisedto shift, Lehman Brothers pre-

dicts. Some nonprime and subprimeauto deals should start trading tighterrelative to prime paper, as financiallystruggling U.S. automakers forceABS investors to re-evaluate tieringin the sector.

The expected shuffle represents asignificant change in the retail autoABS market.

Traditionally, auto issuers havefallen into two distinct categories:The prime issuers tended to be largeinvestment-grade corporates, captivefinance companies or banks. Thenonprime issuers were typicallysmaller independent finance compa-nies with lower ratings, often belowinvestment grade. This less appealingcrowd also had less capitalization andfewer sources of liquidity, makingthem more reliant on the ABS mar-ket for funding.

But for the first time, the demarca-tion lines between prime and non-prime issuers are blurring. “Tieringused to be straightforward since ABSwith lower credit quality collateral wasusually issued by lower-rated seller/ser-vicers,” Lehman researchers said intheir 2006 market forecast. “This is nolonger the case.”

Both General Motors Corp. andFord Motor Co., formerly the sec-tor’s longtime benchmark issuers,saw their status in the market tumblesignificantly over the past year, withmultiple corporate downgrades fromthe rating agencies. Ford took themost recent hit, with its Jan. 5 down-grade to ‘BB-’ by Standard &Poor’s. The agency dunked GM to‘B’ in December.

At the same time, recent acquisi-tions of nonprime issuers like WFSFinancial and Onxy AcceptanceCorp. by stronger parent companies islikely to boost their stature in the mar-ket. Wachovia Corp. announced in

September that it would buyWestcorp and its subsidiary WFS,with the acquisition expected to closethis quarter. Capital One FinancialCorp. completed its purchase of Onyxin January last year.

Giving tiering another look

Citing such changes, Lehmanresearchers advise investors to re-evalu-ate the tiering framework.

Because of the resulting impact onseller/servicer risk, they anticipate aneffect on auto ABS spreads. And theybelieve this change in tiering is here tostay at least for the foreseeable future.

To illustrate the point, they offeranalysis of the CARAT and WESTOtransactions: GM’s CARAT benefitsfrom lower losses and cumulativedefaults, but also has lower creditenhancement. The WESTO transac-tions from WFS, meanwhile, are some-times wrapped. Both have a history ofstrong underwriting and stable collat-eral performance. Triple-A bonds fromboth shelves are well protected.

“However, given the corporatewoes in GM’s automotive franchise(B1/B/B+) and Wachovia’s(Aa3/A+/AA-) ownership of WFS,which bonds, CARAT or WESTO,are more susceptible to idiosyncraticseller/servicer risk?” Lehmanresearchers asked. Their answer wasCARAT.

Nonprime borrowersare more exposed toadverse macroeconomicconditions such as a slow-down in the housingmarket or a rise in unem-ployment, they wrote.

However, their analy-sis of Lehman’s propri-etary loan level databaseindicated that changes inunemployment affectborrower default ratesproportionally. They

found a 1% rise in unemploymentleads to a 20% increase in defaultsacross the borrower credit.

Subprime transactions wrapped bymonoline insurers will have even lesscredit risk, they pointed out.

Therefore, they concluded, non-prime issuers with a strong seller/ser-vicer profile and stable collateral per-formance should trade inside weakerprime auto ABS issuers.

The Lehman researchers also saidGM- and Ford-sponsored paperlagged other prime issuers by asmuch as 12 basis points in earlyMay. The two names ended the yearmore respectably, trading just 5basis points back. But theresearchers caution investors to bewary at that tighter level, and rec-ommend underweighting triple-Asfrom both automakers.

“We have few credit concernsregarding the bonds and do notexpect a flood of supply, but spreadscould widen if the news fromDetroit does not improve,” theLehman report said. “At a conces-sion of just 5 basis points in three-year GM/Ford triple-As, total returninvestors may lose more in spreadwidening than they gain in carry inthe coming months. In other words,we fear that 5 basis points is inade-quate compensation for the elevatedheadline risk.” — Bonnie McGeer

All eyes on the road ahead, as auto tiering may fishtail

A S S E T - B A C K E D S

Ford corporate rating actions by FitchDate Action Rating12/19/05 downgrade BB+07/20/05 downgrade BBB-05/19/05 downgrade BBB04/11/05 revision outlook BBB+

(to negative from stable)

GM corporate rating actions by FitchDate Action Rating11/09/05 downgrade B+

(and placed on Rating Watch Negative)

09/26/05 downgrade BB05/24/05 downgrade BB+03/16/05 downgrade BBB-

Ford corporate rating actions by Fitch

GM corporate rating actions by Fitch

6 - ASSET SECURITIZATION REPORT - January 16, 2006

Default rates among subprimeloans rose 56.5% — or 187 of

the 331 metropolitan statistical areasin October 2005 from the year-agoperiod, according to FriedmanBillings Ramsey. On average, how-ever, the default rate for subprimeloans fell to 6.16% from 6.38%.

FBR is forecasting subprime loandefault rates in 311 MSAs to rise to6.68% this October, up from the6.16% delinquency rate reached inOctober of 2005. “We attribute theincrease to the ineveitable surge indefault rates in the 10 MSAs affectedby Hurricane Katrina, to continuedweakness in the 56 MSAs, and to thenatural aging of the stock of sub-prime loans.”

The percentage of securitizedloans considered to be subprime thatwere in foreclosure in the month ofOctober rose to 2.27% from 2.25%in September, while the portion ofloans that were 90-days or moredelinquent rose to 3.15% from2.87%. The portion of loans report-ed as 60-days delinquent rose to2.76% from 2.49%, while 30-daydelinquencies rose to 7.07% from6.99%, according to FBR.

Improvements in ability to makepayments among subprime borrow-ers overall year-over-year, however,was attributed by FBR to betterlabor market conditions. Payrollemployment grew by 1.92% in

October from the previous year,while the household unemploymentrate fell by 8.8% to 4.7%. Similar totrends in delinquency rates, employ-ment did not improve in every MSA— leaving a pocket of MSAs thatcontinue to experience relativelyhigh delinquency rates.

“It is evident that a slowlyexpanding majority of MSAs is expe-riencing better labor market condi-tions, while a minority, due tochronically weak local economicactivity, is not,” FBR researcherswrote last week.

FBR identified 56 MSAs in 16states that are experiencing consis-tently high rates of default, but, thepopulation of those areas represents11% of the U.S. population, or 31.1million people. Within this MSA,subprime loans in October experi-enced a 13.82% default rate, com-pared with 2.54% for alt-A loansand 0.56% default rate for primeloans. The MSA with the highestsubprime loan default rate as ofOctober was Cleveland, Ohio, whichexperienced a 20.02% rate ofdefault. Not far after Cleveland forsubprime loan defaults wasCharleston, S.C., which experienceda 18.38% of default in October. Theworst prime borrowers among thebunch resided in Hamilton, Ohio,where 1.65% of prime loans weredelinquent in October. — AP

Subprime loan defaults,on average, fall year-over-yearshareholdings in Taiwan’s Chiang Kai

Shek International Airport andTaipei City’s public parking lots.According to local media, Macquarie— making news globally with recentacquisition activity — could paybetween NT$100 billion ($3.1 billion)and NT$200 billion for CKS Airportand up to NT$20 billion for the park-ing lots. It is speculated the assets willthen be sold into a newly-establishedreal estate asset trust, which will thensecuritize revenues earned off theback of the acquisitions, presumablyfor refinancing purposes.CKS, locatedin the manufacturing center ofTaoyan City in North West Taiwan,was the only airport of the 18 cur-rently owned by the government torecord a profit in 2005.

After reviewing the sector, theEuropean Commission confirmedlast week that it would not subjectcredit rating agencies to new legisla-tion. The commission examined rat-ing agencies, but felt the current vol-untary code was sufficient. Analystsat Royal Bank of Scotland notedthat the European Union still has sig-nificant room to penalize agenciesthrough the application of the creditquality steps in the Capital AdequacyDirective, to align risk weightingswith rating scales.

Spreads for the two FourSeasons Health Care deals, PHFSecurities and Tiara Securities,were expected to tighten on the backof claims that Allianz, the owner, hasappointed Dresdner KleinwortWasserstein to investigate refinanc-ing options.The refinancing is likely tobe based on a sale and leaseback ofthe group’s property portfolio, andcould be followed by a flotation or

- CONTINUED ON PAGE 8 -

- CONTINUED FROM PAGE 4 -

A S S E T - B A C K E D S

Breaking NewsUpdated Multiple Times Daily

www.asreport.comsubscribe today

www.asreport.com - January 16, 2006 - 7

Consensus for overall ABSissuance volumes for 2006 is

‘steady as she goes.’ Most expect thefinal tally to come in near $700 bil-lion, and close to the 2005 total,assuming shifts in volume amongclasses. In any case, the backdrop toall the sectors will be closely tied tothe consumer credit outlook. Whileconsumers remain highly leveraged,and home values are soaring to alltime highs, “both job growth andaccumulated real estate and finan-cial wealth will provide a cushion,”said Ivan Gjaja, director and headof ABS research at CitigroupGlobal Markets. “We’re unlikelyto see a sharp deterioration.”

There are also different outlooksfor the various ABS sectors, includ-ing home equities, credit cards,autos and student loans

HELs

Is there a bubble in residentialreal estate? Arguments rage on, buteither way the market will probablyrun out of steam to some extent.Slower home appreciation willtranslate into slower equitybuildups. Interest rate direction is amassive question mark, and coulddampen the sector. Gjaja foresees aflat to “modestly inverted” curve inthe second half of 2006, resulting ina compressed spread between sub-prime floating and Libor rates, assubprime lenders raise rates to playcatch up. However, HEL borrowers,who need financing, tend to be lessrate-sensitive. Gjaja adds that usual-ly higher interest rates lead to slow-er prepayments, and hence lowerissuance for the next round.

“In addition, the upward movetowards rationalization on mort-gage rates was not entirely complet-ed last year,” said Quincy Tang,senior vice president RMBS atDominion Bond Rating Service.

“As lenders continue to increasemortgage rates in the comingmonths, origination volume willinevitably slow.”

Various offsets will give comfort,and should help keep the sector rel-atively buoyant. “HELs should seerobust financing, given that a largepercentage of those borrowers holdshort, adjustable-rate products thatare due to reset in 2006,” saidPeter DiMartino, managing direc-tor at RBS Greenwich Capital.Lender sentiment also offers a ray ofhope. DiMartino notes that lendershave been suggesting some bearish-ness on volume relative to a yearago. “The housing market likelywon’t turn in 2005-type numbers,but it is still healthy despite whatyou read in the newspapers.”

DBRS’ Tang also expects down-ward pressure on issuance volumeto be partially offset by the contin-ued proliferation of certain afford-ability products, such as longerIO’s, more extended amortizationterms, and higher LTV programs.

Credit cards

Consolidation in the industrymay lead to slightly lower levels ofissuance. Last year saw a number ofmergers and acquisitions, such asBank of America’s purchase ofMBNA, and Citigroup’s digestionof Sears’ credit card portfolio.“Players who would have beenstand-alones before have nowbecome part of superbanks,” saidMark Adelson, head of structuredfinance research at NomuraSecurities. These giant acquirerswill have less need to tap the securi-tization markets. DiMartinoobserves that credit card mastertrusts headed lower, as cardholdershave grown more reliant on homeequity products. “Today’s consumersbetter understand concepts like

credit score, and try to improvetheir creditworthiness,” he said.

Autos

Ford Motor Credit Co. andGeneral Motors AcceptanceCorp. are thanking their lucky starsfor securitization markets, as theparent automakers struggle to turnprofits. Both were heavily relianton them in 2005, and will remainactive participants in ABS, assecured financing proves attractiverelative to the unsecured side.

Student loans

Getting an education costs anarm and a leg these days, and high-er tuition translates into issuance.The Deficit OmnibusReconciliation Act of 2005, legisla-tion enacted at the close of last year,should become effective by mid-2006. The bill raises annual loanlimits for first and second year stu-dents. Meanwhile, loan consolida-tion should play less of a role goingforward, as new incentives makethat route less compelling.

Other assets

The more off-the-run assetsinclude all but the kitchen sink.“Investors have become moresophisticated, and are actively seek-ing to boost returns,” said Gjaja, byturning to asset pools comprisingintellectual property, insurance,timeshares, stranded assets and tele-com cell towers.

Stranded assets should thrive nowthat political risk concerns have lift-ed. Nomura’s Adelson thinks thatthe concept may be parlayed intoother pioneer areas like pollutioncredits. Pharmaceutical royaltystreams, a close cousin to music copy-right and other intellectual property,have now proved themselves“doable,” he said. — Vanessa Drucker

2006 ABS issuance volume to keep par with last year

A S S E T - B A C K E D S

8 - ASSET SECURITIZATION REPORT - January 16, 2006

The U.S. ABS primary marketshowed its first signs of life last

week as issuance nearly doubledfrom the previous week to hitroughly $14 billion.

More than half of those deals hadyet to price as of press time, but thelargest to price was a $1.8 billionhome equity securitization fromCalifornia mortgage giant LongBeach Mortgage and led byGoldman Sachs. The first threetranches were retained, with thelargest tranche, a $536 milliontriple-A-rated one-yearoffering, pricing ninebasis points over one-month Libor. The two-year tranche priced 18basis points plus one-month Libor, while the3.25-year tranche priced24 basis points over theindex. The final triple-Atranche of the deal, atsix years in duration,priced 34 basis points over one-month Libor.

Ace Securities Corp. also put ahealthy dollop of home equity secu-rities in the market, with a $1.25billion offering arranged byDeutsche Bank. The one-yeartranche priced at seven basis pointsover one-month Libor, with the two-year tranche coming in at 15 basispoints over one-month Libor.

Also bringing a moderatelyhefty home equity offering wasCBASS, with an $828 millionoffering led by Barclays Capital.The one-year tranche of the dealpriced 29 basis points over EDSF,while the two-year tranche priced35 basis points over swaps and thefour-year tranche priced 80 basispoints over swaps. The 5.6-yeartranche ratcheted in from the four-year’s price, and finished at 62basis points over swaps.

Morgan Stanley was in the mar-ket with a $729 million home equitysecuritization that priced a one-yeartranche at eight basis points overone-month Libor, and a three-yeartranche priced at 20 basis points overone month Libor. The 6.5-yeartranche priced 33 basis points overone-month Libor.

Cendant Corp.’s Aesop Fundingtrust offered at $600 million autoloan securitization to the market viaDeutsche Bank and Merrill Lynch asjoint-leads. The single tranche, triple-

A-rated, five-year dealpriced at 22 basis pointsover one-month Libor.

Bear Stearns wasalso in the home equitymarket with a $516million offering, theone-year tranche ofwhich priced nine basispoints over one-monthLibor, the three-yeartranche priced at 22

basis points over one-month Liborand the six year tranche priced 33basis points over one-month Libor.

Of the deals that had yet to price,Irwin Home Equity had a $312million home equity deal in the mar-ket, Goldman Sachs had $490 mil-lion home equity deal circulating,and Ownit Mortgage Solutionshad a $708 million home equityoffering as well.

The student loan sector was repre-sented by GCO Education LoanFunding Corp., with a whopping,and rare, $1.14 billion student loansecuritization that had yet to price,while Barclays had a $1.218 billionhome equity securitization still onthe table and Bear Stearns had a$464 million securitization left inthe market. Goldman also had a$904 million home equity deal cir-culating in the market through itsGSAA trust. — Editorial Staff

U.S.ABS warms up with $14 billion weekauction. A number of the homesowned by Allianz are tied up in secu-ritization deals, which will likely carrya fee to have them removed andincreases the likelihood of the deals’redemption.

Residential mortgage bankerMortgageIt Holdings announcedlast Wednesday that it has cut itsnumber of branches by half. It is alsoreducing staff, with both moves aresponse to the slowdown in thesubprime lending industry. The firmcut the number of branches cateringto subprime lending to three.However, the company did not revealthe exact number of staff it intendsto let go as part of the announcedrestructuring. MortgageIt cites pres-sures on “gain on sale” margins andindustry consolidation as factorshurting fourth quarter earnings bybetween 10 and 15 cents while stat-ing that its self-originated portfolioreached roughly $4.6 billion at theend of the quarter.

Fitch Ratings’ U.S. CMBS loandelinquency index dipped eight basispoints on the month to 0.79%.According to Fitch, 2004 and 2005vintages now represent 14% and 28%of the rating agency’s index by bal-ance and continue to have low delin-quency rates. If these vintages wereremoved from the tracking universe,the delinquency index rises to 1.34%,which is equivalent to 55 basis pointsmore than its current level.The sea-soned delinquency index, whichomits deals with less than one yearseasoning, dipped nine basis pointthis month to 1.09%. Meanwhile, newKatrina-related delinquencies slowedin December to $40.3 million versus$180.5 million the previous month.

- CONTINUED ON PAGE 12 -

- CONTINUED FROM PAGE 6 -

A S S E T - B A C K E D S

The largest to price was a $1.8 billion home equity securitization

from Californiamortgage giant

Long BeachMortgage.

www.asreport.com - January 16, 2006 - 9

office began interviewing Wachoviaemployees about the alleged inci-dents in late 2005.

Cifuentes’ attorney, JeniceMalecki of Malecki Law in NewYork, confirmed that Cifuentes isnot precluded from testifying in anSEC investigation, and said herclient would comply with any SECrequests. The SEC declined to com-ment on the situation, though aspokesperson noted that “in gener-al, [the settlement] would notaffect an investigation.” It isbelieved that the settlement ismonetary in nature, as the com-plaint with OSHA was based onincome lost due to an unjust firing.The settlement is conditional upona review by the Department ofLabor, said a person familiar withwhistleblower procedures.

In the OSHA complaint,Cifuentes said he protested repeat-

edly to his superiors about pressurefrom the bank’s investment bankersto change or tailor his group’s CDOresearch. Under Sarbanes-Oxley,influence and pressure by invest-ment bankers on research analysts isstrictly prohibited. Cifuentes main-tains that when senior managementrefused to step in, he declined tocertify his group’s research reportsand was fired.

The whistleblower complaint con-tained several alleged infractions ofthe Chinese Wall that was set in placeby Sarbox and contained numerous e-mail exchanges between BrianLancaster, the head of Wachovia’sresearch group, various investmentbankers tied to structured finance atthe bank, and Cifuentes, who saidthat pressure from the investmentbankers violated polices relating toindependent research.

Yu-Ming Wang, Wachovia’s

head of structured products, isnamed repeatedly in the complaintfor allegedly pressuring the CDOgroup to produce favorable researchin conjunction with CDOs the firmwas marketing. In one exchange, itis alleged senior bankers, includingRuss Andrews and Bo Weatherly,who reported to Wang, pressuredCifuentes to write a favorable articleon CDO equity in conjunction withtheir marketing of the AXA CDOEquity fund in February 2004. Anda Feb. 3, 2005 e-mail, allegedlyfrom banker Anthony Sciacca toCifuentes, chastised Cifuentes for aJan. 31, 2005 report on the per-formance of CDO managers. The e-mail claimed the research piececontributed to the cancellation ofa meeting with Pacific InvestmentManagement Co. (Pimco) regardinga new collateralized loan obligation.— Colleen O’Connor

A S S E T - B A C K E D S

CIFUENTES CONTINUED FROM PAGE 1

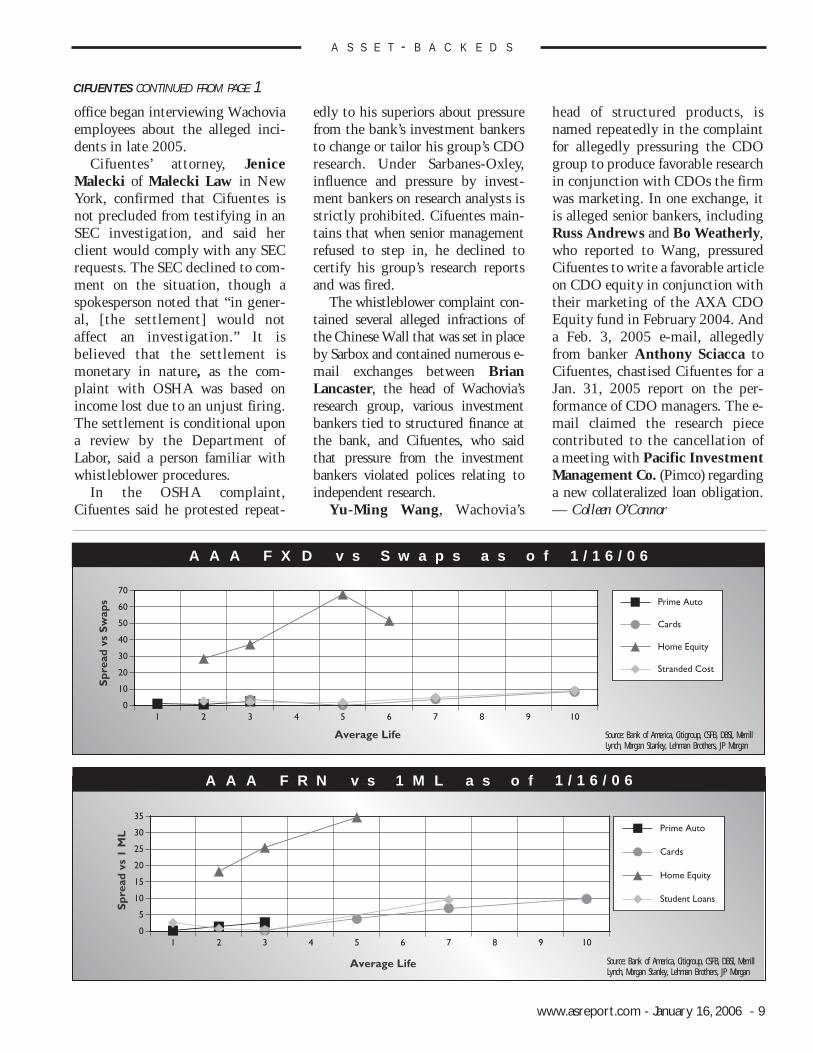

A A A F R N v s 1 M L a s o f 1 / 1 6 / 0 6

Source: Bank of America, Citigroup, CSFB, DBSI, MerrillLynch, Morgan Stanley, Lehman Brothers, JP Morgan

A A A F X D v s S w a p s a s o f 1 / 1 6 / 0 6

Source: Bank of America, Citigroup, CSFB, DBSI, MerrillLynch, Morgan Stanley, Lehman Brothers, JP Morgan

10 - ASSET SECURITIZATION REPORT - January 16, 2006

The pace of collateralized loanobligation (CLO) issuance is

expected to remain strong in 2006,as long as leveraged loan issuance,liquidity, default rates, liability andunderlying collateral spreads, andinvestor demand for CLO equityremain stable this year, according tomarket sources. The consensus isthat issuance should be at least onpar with or higher than 2005’s CLOissuance levels.

According to preliminary datareleased by Moody’s InvestorsService, more than 90 U.S. CLOswere issued in 2005, totaling about$42 billion. This compares with 57Moody’s-rated CLOs issued in 2004,totaling about $22 billion.Standard & Poor’s also reported arise in CLO issuance, according to its2005 data, which show 99 US S&P-rated CLOs issued in 2005 to totalabout $47 billion. This compareswith 66 S&P-rated CLOs issued in2004, totaling about $26 billion.

There is a very deep pipeline fornew CLOs and no slowdown inissuance is expected anytime soon,said William May, managing direc-tor at Moody’s. “Managers are ramp-ing up more deals than ever.” AndCLO equity investors from Asia,Europe and North America continueto show interest, he said.

“I think [CLO issuance in 2006]will be robust,” agreed DavidArdini, CLO portfolio manager forFranklin Templeton Investments’Franklin Floating Rate DebtGroup. “I don’t think we will see toomuch more in 2006 over 2005 thanwe saw in 2005 [compared with]2004. But we still could very well see20% growth,” he said. “Right now,there is a strong CLO pipeline and,generally speaking, the economy’soutlook is good.... The key has beenaccess to collateral, and loan issuancehas been fairly robust,” Ardini added.

Historically low default rates,despite having risen since 2004, havealso helped maintain investor allureto the leveraged loan asset class.Moody’s reported a 1.8% issuer-weighted US leveraged loan defaultrate at the end of 2005, comparedwith a 1.6% rate at the end of 2004.Meanwhile, S&P reported a 1.98%US leveraged loan default rate at theend of 2005, compared with a1.12% rate at the end of 2004. S&Pexpects loan defaults to remainbelow average this year, sliding backto 1.25% by December 2006.“Liquidity remains plentiful, and thedistress ratio —measured as the per-centage of performing loans in theUS trading at prices below 80 centson the dollar — still remains nearrecord lows, wrote S&P managingdirector Diane Vazza in a January 6default report.

CLO investors have also beenattracted to the loan market’s strongliquidity levels. “There are strongtechnicals in the [collateralized debtobligation (CDO)] marketplace....There are also many new CLO man-agers, and a lot of loan demand iscoming from the hedge funds,”Ardini said, explaining reasons whyliquidity in the loan market has beenso robust.

And the low Libor spreads onleveraged loans, which have result-ed largely because of the high com-petition for loan paper byinvestors, appears to not have hurtthe prospects for CLO issuance —at least not yet. That’s becauseCLO investors have been acceptinglow liability spreads in tandemwith lower leveraged loan spreadsover Libor.

Ardini noted that triple-A liabili-ty spreads have averaged Libor plus26 basis points or lower for aboutnine months now. “They probablywill not go tighter, but they could

stay at that level for some time into2006,” he said.

Risks remain

But despite the consensus thatstrong CLO issuance should contin-ue well into 2006, there are still sce-narios that could jeopardize issuance,market sources pointed out. Onecentral risk relates to the chance thatCLO investors might flee loans formore profitable asset classes. “Giventhe current level of returns in theCLO market, rising default rates,and other asset classes starting toperform better, [will] money andinvestor interest shift away fromCLOs?” another CLO managerasked. “Is the demand from CLOinvestors sustainable at this level?”he continued. “The returns on CLOshave been acceptable to equityinvestors only because the liabilitieshave been priced so tight that,despite the tight spreads on loan col-lateral, equity returns are still betterthan [in] many other asset classes. Ifeither of them — equity buyers orliability buyers — wants morereturn/yield and loan spreads don’twiden out commensurately, the arbi-trage [might] really shrink to anunattractive level.” He noted thatinvestors might begin to look to thestock market, for example, for high-er returns. “If liability spreads widenout and loan collateral spreads donot, the equity returns will fall to alevel where buyers probably are nolonger interested in CLO equity,which would definitely impact anissuer’s ability to get new [CLOs]done,” the CLO manager explained.

He noted that even thoughdefault rates have risen slightly, thespreads on loans have remained atall-time lows. “In a normal market,default rates rise and that leads to anatural widening of spreads. Butthat is not happening in a substan-

Robust CLO issuance likely to continue in 2006, but risks remain

A S S E T - B A C K E D S▲

www.asreport.com - January 16, 2006 - 11

tial way due to the strong technicalconditions of the market,” he said,referring to the high amount of loandemand coming from CLO man-agers and other types of institution-al investors.

The average spread on BB/BB-rated institutional loans was at Liborplus 185 bps in December 2005,while the average spread on B/B+rated loans was at Libor plus 263basis points, according to S&P’sLeveraged Commentary & Data.

That being said, loan spreads maybegin to widen out more if demandfor them decreases due to certainloan investors exiting the market formore profitable ones. For example, ifrates stabilize, some investors mayswitch to investing in bonds. “If the[Federal Reserve Board] stopsraising rates, you could see investorsmove back to bonds,” said TylerChan, director of research for theFranklin Floating Rate Debt Group.“Total return investors might startmoving away,” he explained.

In addition to concerns about loan

spreads not increasing at the samepace as liability spreads, marketplayers are also concerned about thegrowing amount of lower qualityloan paper clearing the market. IfCLO managers continue to invest ina high number of lower qualitydeals, they are increasing their port-folio’s chances of hitting troubledown the road, market sources said.

“Although deal flow is heavy, thepercentage of those deals that aremarginal credits is increasing,” saidChan. He explained that investmentbankers are filling a gap by issuingmore of these lower quality loans inorder to create enough supply tomeet investor demand. In addition,bankers are beginning to alter certaindeal structures so that loan investorsreceive a more subordinate debt posi-tion on a company’s collateral, Chansaid. For example, the $3.85 billionbank deal to back the buyout ofHertz Corp. includes bank loan debtthat is more risky because its collat-eral is Hertz’s trademark instead ofits fleet of rental cars, he said.

Increasing investments in differ-ent types of debt, such as second lienor middle market loans, could alsoraise the level of performance risk forCLOs. “It is clearly a riskier proposi-tion to buy second lien loans, highyield bonds and middle marketloans,” said Moody’s’ May. CLOsoften include buckets to invest inother forms of debt such as highyield bonds, second lien loans, mid-dle market loans and synthetics.

If CLOs do start to experiencemore trouble due to their invest-ments in riskier forms of debt, suchas middle market loans, it is the newand more inexperienced CLO man-agers that might face the most prob-lems. “It is not necessarily the casethat a [good] loan manager is goingto be a good middle market loanmanager,” said Mark Froeba, vicepresident and senior credit officer atMoody’s. “Also, a smaller shop

might not have the resources to getgood experience investing in middlemarket loans outside of a CDO,”Froeba said.

New kinds of CLOs

However, as CLO issuance contin-ues to remain strong for now, anincreasing amount of CLO managersare devising alternative types of CLOs.

For example, as issuance of mid-dle market CLOs increases, marketsources expect to see more creativemiddle market investment struc-tures. “Recently-launched middlemarket loan CDOs have also includ-ed buckets of asset-backed securitiesand loans from the broadly-syndicat-ed markets,” reported Fitch Ratingsin a December 2005 structuredfinance outlook report. “In addition,Fitch has noted a trend in middlemarket CLOs that follow more tradi-tional CLO structures and utilizeovercollateralization and interestcoverage tests.”

“With respect to middle marketCLOs, we are definitely expectingmore issuance than last year, as wellas different types of CLOs with dif-ferent assets in them,” said AllaZaydman, a director in Fitch’s cred-it products group.

Synthetic CLO issuance could alsoincrease this year, especially as an adhoc committee comprised ofinvestors and bankers moves closerto releasing proposed standard doc-umentation for synthetically refer-encing loans on credit default swapsto rating agencies, The LoanSyndications and TradingAssociation and the InternationalSwaps and DerivativesAssociation. “CLO issuance (in syn-thetic form) may accelerate in the rel-atively near future if the marketresponds favorably to the upcomingISDA templates for synthetically ref-erencing loans,” stated Moody’s in athird quarter CDO review released inDecember 2005. — Judy McDermott

A S S E T - B A C K E D S

12 - ASSET SECURITIZATION REPORT - January 16, 2006

As the U.S. economy expands andthe Federal Reserve continues

its gradual uptick on medium- tolong-term interest rates, overall bondissuance is forecasted to decline 13.3%to $3.56 trillion in 2006, compared to$4.10 trillion in 2005, according toresults from a recent Bond MarketAssociation survey. However, whileissuance is expected to fall in interestrate-sensitive sectors, it is anticipatedto either stay steady or rise in othersthat are not driven by rate fluctuations.

It is projected higher rates will havethe greatest effect on MBS issuance,according to the BMA’s 2006 creditmarket issuance outlook. Mortgage-related issuance is expected to fall20.2% to $1.68 trillion in 2006, com-pared to $2.10 recorded in 2005. Theestimate comes in light of rising mort-gage rates and a slower growth in thehousing sector.

In addition, long-term municipalissuance is predicted to total $352 bil-lion, a 13.5% decrease from the $407billion reported in 2005. ARM mort-gage-related issuance is also expectedto drop 26.7% to $633 billion due tohigher initial rates and adjustmentsrelated to higher short-term rates.Agency MBS and CMO issuance areboth slated to decrease by 17.5% to$755 billion and $260 billion, respec-tively. Non-agency MBS is expected todecrease in 2006 to $664 billion,down 23.9% from the previous year.Although a sharp fall in issuance isanticipated in the mortgage area, itwill still be the fifth highest issuance

year for the sector, according to thereport.

ABS issuance is also expected todecline for the first time since 1999. Itwill fall 12.5% to $636 billion from$727 billion issued in 2005, accordingto the survey.

“ABS will be down, but that’sbecause the largest sub-sector with-in ABS is home equity loans,” saidMichael Decker, senior vice presi-dent and head of research and poli-cy analysis at the BMA. “Homeequity loans issuance is driven to alarger extent by real estate evalua-tions. There’s an expectation thatthe run-up in home values will slowso you’ll see less home equity loanand home equity line borrowingand that’ll be reflected in lowerissuance in that area.”

Auto loan, credit card receivableand other collateral sub-sectors withinABS are expected to rise, however.

Based on the survey, cash CDOissuance is expected to increase by8.8% to $173 billion, compared to$159 billion issued in 2005.Leveraged loans will account forabout 40% of the total cash issuancein this sector with a projected $63billion in issuance, a 12.5% rise from2005, according to the report. Inaddition, synthetic CDO issuancewill be $80 billion in 2006.

Corporate bond issuance, includinginvestment grade and high yield securi-ties, is predicted to increase slightly to$719 billion, a 1.6% increment fromthe $708 issued in 2005. — HBO

Total U.S. bond issuance slated to decline in 2006 However, Fitch says it remains to be

seen whether these delinquencieshave stabilized, which would probablybe clarified later in the first quarter,the rating agency said.

Moody’s KMV announced lastTuesday that it has appointed BrianRanson, as a managing director inthe newly formed credit strategiesgroup. Ranson was most recently asenior vice president at Bank ofMontreal. Ranson’s appointmentcomes as Moody’s KMV, a providerof quantitative credit risk measure-ment and management solutions,announced the launch of the creditstrategies group and the credit riskspecialists team, both of which willfocus on providing thought leader-ship and best practices to its cus-tomers, Moody’s KMV reported in astatement. Jeffrey Bohn, managingdirector of global research and cred-it strategies, will lead the creditstrategies group, while other seniormembers will include BrianDvorak, Martha Sellers andWilliam Morokoff. The credit riskspecialists team will be led byManaging Director David Merrill inthe Americas, and managing directorGavin Style in Europe, the MiddleEast,Africa and Asia Pacific.

Last week the leaders of RBSGreenwich Capital’s debt capitalmarkets push of the past few yearssaid they are leaving the bank tostart their own hedge fund. JohnWalsh, head of credit markets, andBen Cohen, his deputy, are off tostart a credit-focused investmentvehicle. Cohen and Walsh, formerlythe global head of debt capital mar-kets at Credit Suisse, joined theUS arm of RBS in 2004.

- CONTINUED FROM PAGE 8 -

A S S E T - B A C K E D S

Subscribe to Asset Securitization Report today.

Call 888.807.8667e-mail: [email protected]

or log on to asreport.com

www.asreport.com - January 16, 2006 - 13

The strong start to the New Yearis continuing in mortgages,

though Tuesday last week did see aheavy sell-off that raised questions ofwhether the tone had shifted.Mortgage flows were strong and two-way. Monday got the week off to agood start as December paydowns —totaling over $40 billion — werereinvested. The strong gains encour-aged profit-taking as the day pro-gressed and it picked up steam onTuesday with real and fast money aswell as servicers jumping in with thestrong sell-off in Treasurys due toheavy corporate supply and mort-gage-related selling. This broughtfears that maybe the positive tone inmortgages since the start of the yearhad shifted, but the cheapening ledto active buying on Wednesday as themarket held stable, particularly fromservicers adding duration and fromoverseas. The buying was continuinginto Thursday’s session with centralbank and fast money support. Theearly year and week flows were up incoupon, but that shifted down incoupon following Tuesday’s sell-off.

Originator selling continues to beuneventful with supply averagingless than $1 billion per day. Alsosupportive for mortgages has beenthe continued low vol environment.The near- term outlook remainsfavorable. In midweek comments,JPMorgan Securities analysts areholding with their tactical over-weight due to lower vol, firmingrolls and overseas buying —whichthey believe should help support thenear-term tightening. They alsodon’t expect a turnaround beforeFebruary. UBS remains a modestoverweight on the mortgage basis.They expect foreign and crossoverbuying should offset the increase innet supply.

In their weekly MBS Strategyreport, RBS Greenwich Capital

analysts are recommending a neutralweighting. They note that January istypically a slightly positive monthfor mortgages with most of the gainearned in the first week of trading.The rest of month has traditionallyexperienced some retracement, oftenin the third week, analysts say. BearStearns is neutral to negative onexpectations of higher supply andlimited demand from banks andGSEs. Finally, Lehman Brothersincreased their mortgage short. Theydon’t believe the sector can continueto tighten on a further rally. One rea-son is the potential for increasedARM-to-fixed refinancings.

Application activity moves higher

Mortgage application activitypicked up in the first week ofJanuary. For the week ending Jan. 6,the Refinance Index rose 10% to1498, according to the MortgageBankers Association. This was in-line with expectations. As a percent-age of total application activity, refi-nancings were down slightly to42.2% from 42.7% in the previousreport. ARM share was also downslightly to 28.1% from 28.8%.

Mortgage rates declined again forthe week ending Jan.13, accordingto Freddie Mac’s latest survey.Freddie Mac’s Chief EconomistFrank Nothaft, attributed the fur-ther drop to “some economic datareleases that pointed towards moresubdued inflation in the near term.”

The 30-year fixed rate mortgagerate averaged 6.15% versus 6.21%last week. This is the lowest they’vebeen since the week ending Oct. 28,2005, when they also averaged6.15%. Since hitting a near-termhigh of 6.37% in mid-November,mortgage rates have retraced 22basis points.

Also reported, 15-year fixed rates

slipped five basis to 5.71%; 5/1hybrid ARMs were down two basispoints to 5.76%; and the one-yearARM rate was little changed at5.15% versus 5.16% previously.

With mortgage rates holdingsteady to slightly lower, expectationsare for mortgage application activityto hold around the 1500 area, andpossibly move towards 1600 in thisweek’s MBA report.

December prepaymentreports match expectations

December FNMA prepaymentreports came in pretty much asexpected with a couple of exceptions.One was 2003 4.5s and 2003 5swhich declined 13% to 14% versusexpectations of 7% to 8%. The otherwas 6.5s that declined less thanexpected. Lehman suggests the lim-ited decline in the higher couponswas due to delayed response fromborrowers to the rate backup inSeptember and October.

In comments from Bear Stearns’Senior Managing Director DaleWesthoff, he observed that theaggregate speed on FNMA collateralis at its lowest level in five years at13.8% CPR. The last time theaggregate speed was below 15 CPRwas in January 2001.

Speeds on GNMAs were a bitmore mixed with 2004 vintage 5.5sand 6s slowing just 2% to 3% versusexpectations of 14% to 20%.Meanwhile, 5.5s generally slowedless than expectations, while 6.5sdeclined more than expectations.GNMA speeds continue to be muchfaster than conventional cohorts.

Paydowns totaled around $42billion, according to JPMorgan.Net fixed rate issuance grew $21billion with 30s up $25 billion and15s declining $4 billion, analystsadd. — Sally A. Runyan/IFRMortgageData

Mortgage sell-off punctuates strong start to year

M O R T G A G E - B A C K E D S

14 - ASSET SECURITIZATION REPORT - January 16, 2006

This year’s theme in the MBS mar-ket appears to be the potential

slowing in the housing market and byextension, the resulting impact on pre-payments. While there are some signsthat housing may be slowing, a cleareridea of this isn’t likely until the spring,when housing activity tends to pick upfrom the winter doldrums.

Elevated prepayments in the lasttwo years have been due to stronghome price appreciation, the increas-ing array and use of affordability mort-gages, attractive mortgage rate levelsand the steep yield curve. Althoughnot to the level seen in the recent past,speeds on discounts are expected toremain relatively strong. AlecCrawford, managing director andhead of agency MBS strategy, expects

speeds will stay on the fast side despitea slowdown in home price growth.“There is still a fair amount of homeprice appreciation in the market,” hesaid. “Tapping home equity is still avery strong trend among borrowers.”

In a study by Merrill Lynch, ana-lysts expect speeds on current couponsto be lower than in 2004 and 2005,however, they believe speeds will behigher than in the 1994 to 1997 periodand at least as high as in 2000. Theynote in part that home prices aren’t like-ly to fall overnight, and changes in bor-rower and lender attitudes take time.

Currently, estimates for home priceappreciation for 2006 range from 3%to 8%.

Expectations are for a typical season-al slowing over the next couple of

months, before picking up again inMarch. Still, speeds in May are project-ed to be near December’s levels, whichwere essentially the slowest in 2005.

Looking nearer to January’sreports, previous estimates suggestaround a 15% decline fromDecember. In the period covering theJanuary report, mortgage rates werefairly stable, averaging 6.27% inDecember versus 6.33% inNovember. The Refinance Index wasdown modestly in December, averag-ing around 1546 versus 1633 in theprevious month. Also contributing tothe expected slowing are seasonal fac-tors. With the December data justout, firms will be revising their esti-mates over the next week or so. —Sally A. Runyan/IFR MortgageData

Prepayments expected to slow along with the housing market

M O R T G A G E - B A C K E D S

www.asreport.com - January 16, 2006 - 15

The spreads on the subordinatetranches of RMBS might have

narrowed from the wider levelsachieved in the final months of2005, but the outlook for the per-formance of the residential housingmarket is not necessarily better — orworse — than before.

According to Bear Stearns ana-lyst Gyan Sinha, it would be “hardto point out” any prior year in whichexuberant investors, unleashed fromyear-end balance sheet restrictions,tightened spreads by piling intostructured finance bonds, a phenom-enon often seen in the equities mar-ket. “The idea that investors parkmoney on the sidelines waiting todeploy it at the turn of the year is notnew, but the effect has been relative-ly muted in most years,” Sinha wrotelast week, “A confluence of eventsappears to have changed history inthis regard.”

For example, spreads on Baa1 cashRMBS bonds were at 190 basispoints, 250 basis points and 350basis points, respectively, as ofDecember 5. By January 8, spreadshad moved out to 150 basis points,190 basis points and 290 basispoints. As well, the basis betweencash and synthetic spreads on thesame bonds had moved from -50, -35 and -25 to -30, -15 and -20 fortriple-B plus, triple B, and triple-Bminus RMBS bonds, respectively.

Those events would include therecent rash of buying home equityABS credit default swap protectionfrom hedge funds and others look-ing for a new way to short the hous-ing market. The activity caused adegree of volatility within the sec-tor that hadn’t been seen in sometime. And, as Sinha pointed out, thewidening caused the return-on-equity for some ABS CDOs to reachbeyond 20%, and CDO deals withtight liability structures also

viewed the asset markets as funda-mentally cheap, he wrote.

But aside from recent tightening,Sinha and others are anticipatingthat uncertainty in regard to thehousing market’s outlook, amongother factors, will lead to spreadvolatility within the sector — atleast in the near term.

HEL performance mixed

Performance indicators so far havebeen relatively unclear, and most for-ward-looking estimates rely onfuture interest rate and gas priceestimates. The American BankersAssociation last week echoed thissentiment. While the organizationreported a 42 basis point drop — or2.33% — in home equity loan delin-quencies in the third quarter of2005, the organization warned thatshort-term interest rates could pinchconsumers’ budgets too far.Meanwhile, the ABA said that posi-tive factors such as economic growthand lower gas prices could help pushconsumers along with timely mort-gage payments. Home equity line ofcredit delinquencies were up bythree basis points, or 0.46%, accord-ing to the ABA, while propertyimprovement loan delinquencies alsosaw an uptick in the third quarter, to1.55% from 1.52%.

“The persistent interest rateincreases by the Federal Reserveand record high gas prices in thethird quarter provided a one-twopunch that continued to inflict painon personal budgets,” said JamesChessen, the ABA’s chief economist,in a statement last week. Chessenadded that the full impact ofHurricane Katrina has yet to be felt.

Agency MBS: headed toward oversupply?

On the agency side, MargaretKerins, a U.S. agency strategist

with RBS Greenwich Capital, isanticipating spreads to trade“directionally with the level ofrates and shape of the curve in2006,” she wrote last week, “Thehistorical relationship betweenspreads and rates suggests that in aflat yield curve, relatively low rateenvironment, front-end spreads arefair. Longer-end spreads are rich,but we think that is justified by thelack of supply.”

Kerins added that a worst casescenario for agency spreads wouldinclude heavy agency supply cou-pled with low Treasury supply,high headline risk and an invertedyield curve — causing spreads towiden to resist inversion. For 2006,those types of risks do not pose athreat to agency spreads. The bigrisks, instead, stem from compet-ing products; foreign demand; andcheapening of agency arbitration,which would result in portfoliogrowth, Kerins wrote.

Meanwhile, Citigroup wrote lastweek that even though seasonal pat-terns may be providing a “short-termboost for the mortgage basis,increased supply is likely to quicklyoverwhelm this positive. We recom-mend caution on the mortgage basis.”

Citi is anticipating more agencyfixed rate net supply in the first partof this year due to a combination of aflatter yield curve and greater regu-latory oversight on the so-callednontraditional mortgage products.The push toward fixed-rate origina-tion, which began in the latter end of2005, should be amplified by a pur-chase-driven atmosphere. As well,ARM prepayments should showmore of a slowdown than their fixed-rate counterparts. These, amongother factors, will increase agencysupply — causing Citi to recom-mend conservative strategies foragency MBS going forward. — AP

Mortgage market spread volatility likely to linger

M O R T G A G E - B A C K E D S

The market is ripe for the first puremultifamily residential dwelling

securitization of Eastern German prop-erties, market sources said. The deal isexpected to be Ä400 million in size.

But the transaction won’t be aloneas 2006 is expected to be another bigyear for these deals, said marketsources. “In general, CMBS will con-tinue to a big area of growth and, inparticular, multifamily home securiti-zations will drive this growth,”Nicolaus Trautwein, head of theGerman securitization team atCommerzbank, said.

Stuart Nelson from the structuredfinance team at Standard & Poor’ssaid that deals that have come to mar-ket so far have been well received. Thetrend towards privatization has seenthe government and large corpora-tions selling off sizeable chunks ofhousing stock to investors. GoldmanSachs last year acquired 65,000apartments for Ä2 billion ($2.4 bil-lion) and Deutsche Annington,which is owned by terra firma, pur-chased 152,000 apartments for Ä7billion ($8.4 billion). These portfoliosare among the larger size acquisitions

that have prepped deals for the securi-tization market. “Multifamily hous-ing has been sold in big concentra-tions to private equity firms like terrafirma who now own these huge port-folios,” Trautwein said. “It’s more effi-cient for them to look at alternativefunding sources where they only haveto deal with one or three banks asopposed to funding the deal via lots ofsmaller banks. The securitizationmarket is the only place firms with abig concentration of these assets canfind one big loan.”

Trautwein added, however, that

Multifamily transactions seize German CMBS spotlight

16 - ASSET SECURITIZATION REPORT - January 16, 2006

I N T E R N A T I O N A L

in 2005 has put the heat on alternativefinance in the secured and unsecureddebt markets. S&P said that the totalrated volume for European corporatesecuritizations slowed over the past 12months. In 2005, the agency rated 23issues for a total £7.9 billion ($13.9 bil-lion), from 20 issues totaling £12.1 bil-lion ($21.18) in 2004.

For 2006, the rating agency said itexpected the market to remain steadywith small and medium sized transac-tions outnumbering larger deals. Onekey development in 2005 that isexpected to continue thisyear has been the applica-tion of Opco Propco toassets which would previ-ously have been corporatesecuritizations, for exam-ple, Fleet Street (FourSeasons Healthcare) byGoldman Sachs andBarclays Capital andTalisman (Priory) fromABN Amro. According toMatthew Lindsay, a corporate partnerat Mishcon de Reya, theOpco/Propco structure often enables aborrower to raise additional fundscompared to a straightforward ‘bricks

and mortar’ financing, provided thetarget company has a significant num-ber of property assets with a relatedprofitable business element.

“These are single obligor specialistproperty assets securitizations,” saidPaul Geertsema at Barclays’ securiti-zation research team. “By structuringdeals as CMBS rather than as a corpo-rate securitization, issuers are achiev-ing greater leverage and higher ratingsfor essentially the same assets.”Geertsema added that he expected thistrend to result in further reductions in

corporate securitizationissuance and possibleredemptions/restructur-ings of existing corporatesecuritization transac-tions into CMBS-typestructures in 2006.

Analysts at S&P saidthat Talisman -2 (Priory)Finance Plc was the firsttransaction in Europe tobe rated with a hybrid

blend of corporate securitization andreal estate finance analysis enabling thenotes to achieve a ‘AAA’ rating with-out the benefit of explicit externalthird-party support. The transaction is

backed by a single loan supported bysingle tenant operating risk. MichelaBariletti on the structured financeteam at S&P said that while these dealsare structured on the basis of their realestate value, S&P categorizes them ascorporate securitization when they aresignificantly exposed to the borrower’sor tenant’s operating risk. “We view itas a whole business deal because whenyou compare it to a single loan CMBSdeal you see much higher exposure tothe operational risk.”

The benefits of this hybrid structureinclude a less strict package of operatingcovenants and higher rating than tradi-tional corporate securitization, saidBariletti. Another feature is bullet pay-ments with refinancing risk at theexpected maturity, although the financ-ing term is shorter than that of a classiccorporate securitization —at about sevenyears instead of 30. Other deals have beenexecuted via the private market but nowthat one market value transaction hasbeen successfully placed in the marketthe rating agency expects to receivefurther requests. Bariletti added thatother proposals have been analyzed, butwhether or not these will make it tothe market is difficult to predict. — NC

ABS & CMBS CONTINUED FROM PAGE 1

▲

“These are

single obligor

specialist property

assets securitizations.”

www.asreport.com - January 16, 2006 - 17

It is looking increasingly likelythat England will go the way of

its neighboring U.K. countriesand issue an outright ban onsmoking in public places. Howthis might affect pub securitiza-tions is still unclear, but FitchRatings analysts said that the fullsmoking ban in Scotland slated totake effect at the end of Marchshould paint a clearer picture ofwhat to expect.

The Health Bill issued inOctober last year proposed a partialban on smoking in public placesand also moved the date of intro-ducing the ban forward to summer2007 rather than the end of 2008.“By the end of last year, a Commonsselect committee had branded theproposal unfair and unworkable andhave been working to get a full banon smoking passed at the earlierdate,” said Paul Crawford, an ana-lyst at Fitch last week during a tele-conference on the sector. “We will

have to wait and see how it pans outbut the full smoking ban inScotland — where a number of pubcompanies have transac-tions with exposure toScotland — will nodoubt be used as alearning experience toget up to date one howthe ban might affecttransactions with expo-sure in England.”

The Health Bill isexpected to enter thereport stage and have itsthird reading in the Commons with-in the next two weeks. The govern-ment will allow a free vote amongLabor MPs, most of whom appear tofavor an amendment to remove theopt-out for pubs not serving food andprivate member clubs. The MPs willhave three choices to choose from: anopt-out for food pubs and privatemember clubs, opt-out for privatemember clubs, and a blanket ban for

all pubs and clubs. Health SecretaryPatricia Hewitt is believed to backthe second option.

According to theBritish Beer & PubAssociation, over20,000 private clubs areregistered in Englandand Wales. “We see anoutright ban as the bet-ter outcome for the pubindustry as it wouldcreate a level playingfield, should see a muchmore consistent effect

on all pubs, and should not result ina loss of trade to private members’clubs,” reported analysts at theRoyal Bank of Scotland. “We feelthat lower quality tenanted pubswould suffer most from such a com-promise given they are more likelyto be located close to clubs thanmanaged outlets [and] their offeringis not very different to that of a pri-vate members’ club.” — NC

Fitch, RBS explore outcome of likely smoking ban in U.K.

I N T E R N A T I O N A L

executing these larger deals takes a bitof time for structuring to work effi-ciently. Still, he expects to see more ofthe more voluminous transactions,sized between Ä3 billion ($3.6 bil-lion) and Ä4 billion ($4.8 billion), tobe part of the securitization repertoirein 2006. “I think one area that will belooked at will be multifamily homeassets in conduits which, at themoment, are being set up by severalGerman banks,” he said. S&P’sNelson estimated that between 20and 25 banks sought to provideclients with an ABS platform.“Approximately 20% of the deals wesaw this year in Germany were actual-ly refinancing activities,” he said. “Ifthis goes away then the slack willhave to fall on these lenders.”

In the past, multifamily propertycompanies were able to fund cheaply

via the Landesbanks but with thechanging environment these bankshave less incentive to provide loans atthe competitive rates they used tooffer. “I think it’s a combination of themarket speed decreasing quite signifi-cantly, while the need for funding hasincreased and all of a sudden the mar-ket has shifted to where the terms ofsecuritization seem quite attractive forthese property companies,” Trautweinsaid. Commerzbank is currently work-ing on a multifamily deal due outsometime in the 2Q06.

And NPLs?

Elsewhere in the securitizationmarketplace, skepticism is growingthat the anticipated German NPLboom (see ASR 1/10/05) will evermaterialize. Market analysts say thatits been harder to sell the benefits of

securitization and that, at themoment, it’s not likely that 2006 willoffer the boom that has been expectedsince last year. “There has been a lot oftalking and a lot of buying and sell-ing but securitization is still seen as adifficult tool,” Trautwein said. “Itseems to be also that securitization isnot as competitive as the traditionalmethod of funding because it’s per-ceived as being data administrativeheavy.” However, one source addedthat there has been talk of one bankpossibly planning a securitizationtakeout for sometime this year.S&P’s Nelson added that it hastaken awhile to make securitizationfriendly and, at the same time, it’sstill unclear whether issuers will optto come to market with large dealsor break up portfolios into smallermarket issues. — NC

How this

might affect pub

securitizations is still

unclear.

18 - ASSET SECURITIZATION REPORT - January 16, 2006

The primary pipeline in Europe isslowly gathering momentum, but

the main story remains secondary trad-ing. With only a handful of deals visi-ble on the primary so far, marketsources say trades continue to pull in.

“The beginning of the year is whatit is,” said one trader at BNP Paribas.“The market is slowly coming up tospeed with 12 deals that are supposedto be marketing on the primary thatshould bring in a total of approximate-ly Ä15.7 billion ($18.8 billion), butsome of that is smoke and mirrors orissues that may have been left overfrom last year.”

Price guidance out for Northern Rock

Price guidance came out forNorthern Rock’s Granite 2006-1,which its triple-B tranche talked 10basis point wider than current marketlevels, according to sources. The triple-A guidance was talked at Euribor plusseven to eight basis points for the europiece, 10 to 11 basis points over Liborfor the dollar tranche and 12 to 13basis points for the sterling tranche.That is in line with December’sGracechurch Mortgage Funding.

However, the triple-B rated notesare talked almost 18 basis points widerthan Gracechurch’s notes, whichpriced at 47 basis points over Libor.Market sources noted that theGracechurch deal benefited from astatic pool and increasing subordina-tion from note amortization. “The rest

of the price talk is actually somewhatless generous than usual, being flat tojust 1bp wide of secondary,” said asource on the Dresdner KleinwortWasserstein trading desk. “However,as Granite is also renowned for tight-ening price guidance more than aver-age, perhaps this situation will beavoided this time round, although wewould expect some revision for [triple-Bs], or further news flow explainingthe wide guidance.”

Toys R Us plays CMBS

Marketing is underway for VanwallFinance, a £356 million ($626.8 mil-lion) sale and leaseback CMBS forToys R Us. The properties, whichinclude 29 stores and a distributioncenter, were leased for 30 years to ToysR Us. A total of six tranches areoffered, rated from triple-A to triple-Bwith corresponding LTVs of 34.5% to70.4%. Toys R Us is currently rated‘Caa2/B-/CCC’, a weak credit standingreflected in the relatively low LTVs ofthe bonds issued in the transaction.

ABN markets 2nd covered bond

ABN Amro is marketing its sec-ond covered bond from its Ä25 bil-lion ($30 billion) Dutch program. Atotal of Ä2.5 billion ($3 billion) ofnotes are expected, with maturitydetermined by demand, bringing itstotal issuance from the program toÄ4.5 billion ($5.4 billion). The col-lateral pool consisted of Ä7.1 billion

($8.5 billion) of mortgages with a92.1% weighted average-LTV.

“These primary deals haven’t beenenough to satiate appetite and spreadson U.K. prime for example continue tocome in by .5 basis point to 1 basispoint,” said the BNP source.“Mezzanine is also coming in and weshould continue to see tightening —it’s a very good time for the market.”

Secondary still offers discounts

Analysts said that the final deals of2005 that struggled due to the over-supply in the market are now tradingat discount to par. There has been a lotof activity on Italian state side — theSCCI deal offers good value and tight-ened by a basis point but there is stillsome value on the longer end.

Traders at DrKW noted one inter-esting recent development is thedecline in demand for “high cash pre-mium” pass through amortizationproduct. Accounts and traders reluc-tance to take the inherent prepaymentrisk when there is an abundance of par-area product available has led towidening of spread differentialbetween two equivalent bonds whereone is trading at par and the other istrading at a significant cash premium.“With conservative assumptions andcorrect interpretation of CPR develop-ments in a given deal, this could leadto relative value opportunities over thecoming weeks for savvy investors,” saidtraders at the bank. — NC

Granite deal poised to set early benchmark for 2006

I N T E R N A T I O N A L

www.asreport.com - January 16, 2006 - 19

Thai consumer finance companyAEON Thana Sinsap, a sub-

sidiary of Japan’s AEON CreditService, is plotting a third raid on theABS market at the end of this month.Citigroup Global Markets willarrange the THB2.3 billion ($57.4million) credit card deal, reprising therole the bank filled for AEON’s THB2billion securitization of the same assetsin February 2005 (ASR, 2/21/05).

Roadshows will shortly take placein Bangkok for the latest four-tranche offering, with pricing duearound the Jan 27. AEON officialssaid proceeds will be used for work-ing capital requirements and newloan origination.

The transaction, issued out theEternal 3 SPV, is backed by aTHB2.8 billion pool of revolvingloans. Fitch Ratings has assignedlocal ratings of triple-A to two seniorfixed rate tranches: a THB1.5 billionthree-year piece and THB500 millionof five-year notes. Credit support willcome chiefly through two subordinat-ed five-year pieces: THB120 millionof AA-rated paper and THB160 mil-lion single-A rated tranche.Additional enhancement comes froma small cash reserve.

With Thai consumer finance com-panies no longer able to takedeposits, securitization should con-stitute a core part of their fundingstrategy going forward. One ofAEON’s domestic competitors, SiamPanich Leasing, will issue a THB5billion auto loans ABS in the firstquarter, with Standard Charteredthe appointed arranger.

Aeon’s last offering featured three-year and five-year senior notes, whichrespectively paid 70 and 85 basis pointspreads over government bonds withsimilar maturities.

Meanwhile, in the People’sRepublic of China, Huaneng PowerInternational could be the latest

high-profile entity to test the securiti-zation waters. The company has calledan extraordinary shareholder’s meetingon Jan. 18 to gain approval for aRMB15 billion ($1.86 billion) ABSprogram and RMB5 billion offering ofshort-term debentures.