cimb islamic money market fund financial statements … · cimb islamic money market fund ....

TRANSCRIPT

CIMB ISLAMIC MONEY MARKET FUND

FINANCIAL STATEMENTS

FOR THE FINANCIAL YEAR ENDED 30 NOVEMBER 2018

CIMB ISLAMIC MONEY MARKET FUND

CONTENTS PAGE(S)

INVESTORS’ LETTER 1

MANAGER’S REPORT 2 - 8

Fund Objective and Policy

Performance Data

Market Review

Fund Performance

Portfolio Structure

Market Outlook

Investment Strategy

Unit Holdings Statistics

Soft Commissions and Rebates

STATEMENT BY MANAGER 9

TRUSTEE'S REPORT 10

SHARIAH ADVISER’S REPORT 11

INDEPENDENT AUDITOR’S REPORT 12 - 15

STATEMENT OF COMPREHENSIVE INCOME 16

STATEMENT OF FINANCIAL POSITION 17

STATEMENT OF CHANGES IN EQUITY 18

STATEMENT OF CASH FLOWS 19

NOTES TO THE FINANCIAL STATEMENTS 20 - 46

DIRECTORY 47

CIMB ISLAMIC MONEY MARKET FUND

1

INVESTORS’ LETTER

Dear Valued Investor,

Thank you for your continued support and for the confidence that you have placed in us. We are pleased to share that CIMB-Principal Asset Management Berhad (“CIMB-Principal”) Malaysia has achieved RM54.02 billion in Asset under Management (“AUM”) as at September 2018.

The Edge| Thomson Reuters Lipper Malaysia Fund Awards 2018

Best Fund Over 5 Years, Equity Global - Malaysia : CIMB-Principal Global Titans Fund

Best Fund Over 5 Years, Equity Asia Pacific ex Japan - Malaysia :CIMB-Principal Asian Equity Fund

Best Fund Over 5 Years, Equity Asia Pacific ex Japan - Malaysia :CIMB Islamic Asia Pacific Equity Fund

Best Fund Over 5 Years, Equity Malaysia Diversified - Malaysia :CIMB-Principal Equity Growth & Income Fund

Best Fund Over 5 Years, Mixed Asset MYR Bal - Malaysia :CIMB-Principal Income Plus Balanced Fund

Best Fund Over 3 Years, Equity Global - Malaysia : CIMB-Principal Global Titans Fund

In addition, we received recognition from Fundsupermart.com for ‘Fund House of the Year’ award and Recommended Unit Trust 2018/2019 awards for the following funds:

CIMB-Principal Global Titans Fund

CIMB-Principal Asia Pacific Dynamic Income Fund

CIMB Islamic Asia Pacific Equity Fund

CIMB-Principal Greater China Equity Fund

CIMB-Principal PRS Plus Conservative

CIMB-Principal PRS Plus Growth

Our latest accomplishment is The Asset Triple A Private Banking, Wealth Management, Investment and Exchange-Traded Fund (“ETF”) Awards 2018 where we have been recognized for the Best Wealth Manager in Malaysia.

These prestigious awards are a celebration of the trust that you have placed in us and testament to our capability in bringing potential value to your financial goals and needs. We look forward to serving you for many years to come and to the best of our ability.

Thank you.

Yours faithfully, for CIMB-Principal Asset Management Berhad

Munirah Khairuddin Chief Executive Officer

CIMB ISLAMIC MONEY MARKET FUND

2

MANAGER’S REPORT

FUND OBJECTIVE AND POLICY

What is the investment objective of the Fund? The Fund aims to provide investors with liquidity and regular income, whilst maintaining capital stability by investing primarily in money market instruments that conform with Shariah principles.

Has the Fund achieved its objective? For the financial year under review, the Fund is in line with its stated objective.

What are the Fund investment policy and principal investment strategy? The Fund will place at least 90% of its Net Asset Value (“NAV”) in Shariah-compliant money market instruments such as Islamic Accepted Bills, Islamic Negotiable Instruments of Deposits and Islamic Repurchase Agreements (“Repo-I”) as well as in any other Shariah-compliant fixed income instruments and placements of Deposits, all of which are highly liquid and have a remaining maturity period of less than 365 days. Up to 10% of the Fund’s NAV may be invested in Shariah-compliant fixed income instruments, which have a remaining maturity period of more than 365 days but less than 732 days. The Fund will be actively managed. The strategy is to invest in liquid and low risk short-term investments for capital preservation*. The investment strategy adheres to the SC Guidelines pertaining to investments for a money market fund.

Note: *The Fund is neither a capital guaranteed fund nor a capital protected fund.

Fund category/type Money Market (Shariah-compliant)/Income

How long should you invest for? Recommended one (1) year or more

Indication of short-term risk (low, moderate, high) Low

When was the Fund launched? 17 March 2008

What was the size of the Fund as at 30 November 2018? RM578.25 million (536.26 million units)

What is the Fund’s benchmark? CIMB Islamic 1-Month Fixed Return Income Account-i (“FRIA-i”)

Note: The benchmark is customised as such to align it closer to the structure of the portfolio and the objective of the Fund.

The 1-Month FRIA-i Rate is reflective of the objective of the Fund. Thus, investors are cautioned that the risk profile of the Fund is higher than investing in Shariah-compliant deposits.

What is the Fund distribution policy? Monthly, depending on the level of income (if any) the Fund generates.

What was the net income distribution for the financial year ended 30 November 2018? The Fund distributed a total net income of RM12.94 million to unit holders for the financial year ended 30 November 2018.

CIMB ISLAMIC MONEY MARKET FUND

3

FUND OBJECTIVE AND POLICY (CONTINUED) The Fund’s NAV per unit are as follows:

Date NAV per unit

(before distribution) NAV per unit

(after distribution)

RM RM

29.12.2017 1.0835 1.0798

30.01.2018 1.0828 1.0780

28.02.2018 1.0812 1.0777

30.03.2018 1.0810 1.0773

30.04.2018 1.0800 1.0765

31.05.2018 1.0796 1.0765

29.06.2018 1.0801 1.0764

31.07.2018 1.0803 1.0765

30.08.2018 1.0803 1.0768

28.09.2018 1.0802 1.0768

31.10.2018 1.0805 1.0771

30.11.2018 1.0801 1.0782 PERFORMANCE DATA Details of portfolio composition of the Fund for the last three financial years are as follows:

30.11.2018 30.11.2017 30.11.2016

% % % Unquoted Sukuk and Islamic commercial papers 69.32 81.23 79.48

Cash and other net assets 30.68 18.77 20.52

100.00 100.00 100.00

Performance details of the Fund for the last three financial years are as follows:

30.11.2018 30.11.2017 30.11.2016

NAV (RM Million)* 578.25 250.60 170.95

Units in circulation (Million) 536.26 231.83 158.29

NAV per unit (RM)* 1.0782 1.0809 1.0799

*Ex-distribution

Highest NAV per unit (RM) 1.0835 1.0873 1.0847

Lowest NAV per unit (RM) 1.0764 1.0795 1.0761

Total return (%) 3.73 3.85 3.26

- Capital growth (%) (0.24) 0.09 0.37

- Income distribution (%) 3.99 3.75 2.87

Management Expense Ratio (“MER”) (%) ^ 0.55 0.58 0.57

Portfolio Turnover Ratio ("PTR”) (times) # 1.16 0.93 0.71 ^ The Fund’s MER for the financial year under review was lower from 0.58 times to 0.55 times

compared to the previous year’s corresponding period mainly due to the increase in NAV. # The Fund’s PTR for the financial year under review increased from 0.93 times to 1.16 times

compared to the previous year’s corresponding period due to higher number of transactions.

CIMB ISLAMIC MONEY MARKET FUND

4

PERFORMANCE DATA (CONTINUED)

Date of distribution 30.11.2018 30.11.2017 30.11.2016

Gross/Net distribution per unit (sen) Distribution on 29 December 2017 0.38 - - Distribution on 30 January 2018 0.49 - - Distribution on 28 February 2018 0.36 - - Distribution on 30 March 2018 0.38 - - Distribution on 30 April 2018 0.36 - - Distribution on 31 May 2018 0.31 - - Distribution on 29 June 2018 0.37 - - Distribution on 31 July 2018 0.37 - - Distribution on 30 August 2018 0.35 - - Distribution on 28 September 2018 0.34 - - Distribution on 31 October 2018 0.34 - - Distribution on 30 November 2018 0.19 - - Distribution on 30 December 2016 - 0.29 - Distribution on 31 January 2017 - 0.30 - Distribution on 28 February 2017 - 0.29 - Distribution on 31 March 2017 - 0.29 - Distribution on 28 April 2017 - 0.26 - Distribution on 31 May 2017 - 0.30 - Distribution on 30 June 2017 - 0.37 - Distribution on 31 July 2017 - 0.36 - Distribution on 30 August 2017 - 0.38 - Distribution on 29 September 2017 - 0.36 - Distribution on 31 October 2017 - 0.38 - Distribution on 30 November 2017 - 0.43 - Distribution on 31 December 2015 - - 0.25 Distribution on 29 January 2016 - - 0.26 Distribution on 29 February 2016 - - 0.25 Distribution on 31 March 2016 - - 0.24 Distribution on 29 April 2016 - - 0.24 Distribution on 31 May 2016 - - 0.29 Distribution on 30 June 2016 - - 0.24 Distribution on 29 July 2016 - - 0.24 Distribution on 30 August 2016 - - 0.25 Distribution on 30 September 2016 - - 0.25 Distribution on 31 October 2016 - - 0.26 Distribution on 30 November 2016 - - 0.27

30.11.2018 30.11.2017 30.11.2016 30.11.2015 30.11.2014

% % % % %

Annual total return 3.73 3.85 3.26 3.38 3.04

(Launch date: 17 March 2008)

Past performance is not necessarily indicative of future performance and that unit prices and investment returns may go down, as well as up. All performance figures for the financial year have been extracted from Lipper.

CIMB ISLAMIC MONEY MARKET FUND

5

MARKET REVIEW (1 DECEMBER 2017 TO 30 NOVEMBER 2018)

During the financial year under review, Bank Negara Malaysia’s (“BNM”) Monetary Policy Committee (“MPC”) met six times between the months of December 2017 up to the end of November 2018. The MPC kept the Overnight Policy Rate (“OPR”) at 3% throughout 2017 but commented at the last meeting of the year then that they may consider reviewing the current degree of monetary accommodation to ensure sustainability of growth prospects of the Malaysian economy. Following this, BNM raised the OPR by 25 basis points (“bps”) to 3.25% at the first MPC meeting in January 2018. There were no further changes to the OPR up to the last meeting of the year. In their November 2017 monetary policy statement, the Central Bank cited that the degree of monetary accommodativeness is consistent with the intended policy stance. However, BNM mentioned that continued volatility in international financial markets and monetary policy normalisation in some advanced economies could lead to further capital outflows and financial market adjustments in emerging economies. The MPC will continue to monitor and assess the balance of risks surrounding the outlook for domestic growth and inflation. The next upcoming MPC meeting is scheduled to be held in January 2019. In terms of inflation, headline inflation averaged at 3.7% in 2017. Overall, the Consumer Price Index (“CPI”) increased by 2.7% in January 2018 and eased lower to 1.4% between the months of February 2018 to April 2018. It spiked up slightly in May 2018 to 1.8% before settling much lower at 0.8% in June 2018. It continued to lower in August 2018 at 0.2% which was the lowest level seen since February 2015 (July 2018: 0.9%). We believe this was due to the impact of the Goods and Services tax (“GST”) zerorisation as well as lower year-on-year (“y-o-y”) fuel prices.It picked up to 0.6% y-o-y in the month of October from 0.3% yoy in September. The slight pick-up was due to higher food and beverage ("F&B) as well as transportation costs. F&B price increases accelerated to 1.2% y-o-y whilst transport cost increased at a quicker pace of 0.8% y-o-y. BNM expects the average headline inflation rate to pick up in 2019 due to the impact of the consumption tax policy but this will lapse towards the end of 2019. They believe underlying inflation will remain contained in the absence of strong demand pressures. The Malaysian economy grew 5.4% y-o-y in the first quarter ended 31 March 2018 (fourth quarter of 2017: 5.9% y-o-y) and 4.5% y-o-y in the second quarter ended 30 June 2018. It dropped to its lowest level in two years to 4.4% in the third quarter of 2018. The lower Gross Domestic Product (“GDP”) number reported was due to weaker external demand as well as ''supply shocks' for liquefied natural gas and palm oil.Private sector activity continued to be the primary driver of growth, as private consumption expanded strongly following the zerorisation of GST during the quarter. Going forward, the Malaysian economy is expected to remain on a steady growth path with private sector activity to remain as the key driver of growth amid the reprioritisation of public sector expenditure.

CIMB ISLAMIC MONEY MARKET FUND

6

FUND PERFORMANCE

1 year to 30.11.2018

3 years to 30.11.2018

5 years to 30.11.2018

Since inception to

30.11.2018

% % % %

Income 3.99 10.99 16.18 28.50

Capital (0.24) 0.22 1.98 7.83

Total Return 3.73 11.23 18.48 38.57

Benchmark 3.16 9.58 15.84 33.85

Average Total Return 3.73 3.61 3.45 3.09

As at 30 November 2018, the total return for 1 year, 3 years, and 5 years stood at 3.73%, 11.23% and 18.48% respectively which outperformed the benchmark for the respective periods. Since inception, the Fund achieved a total return of 38.57%.

CIMB ISLAMIC MONEY MARKET FUND

7

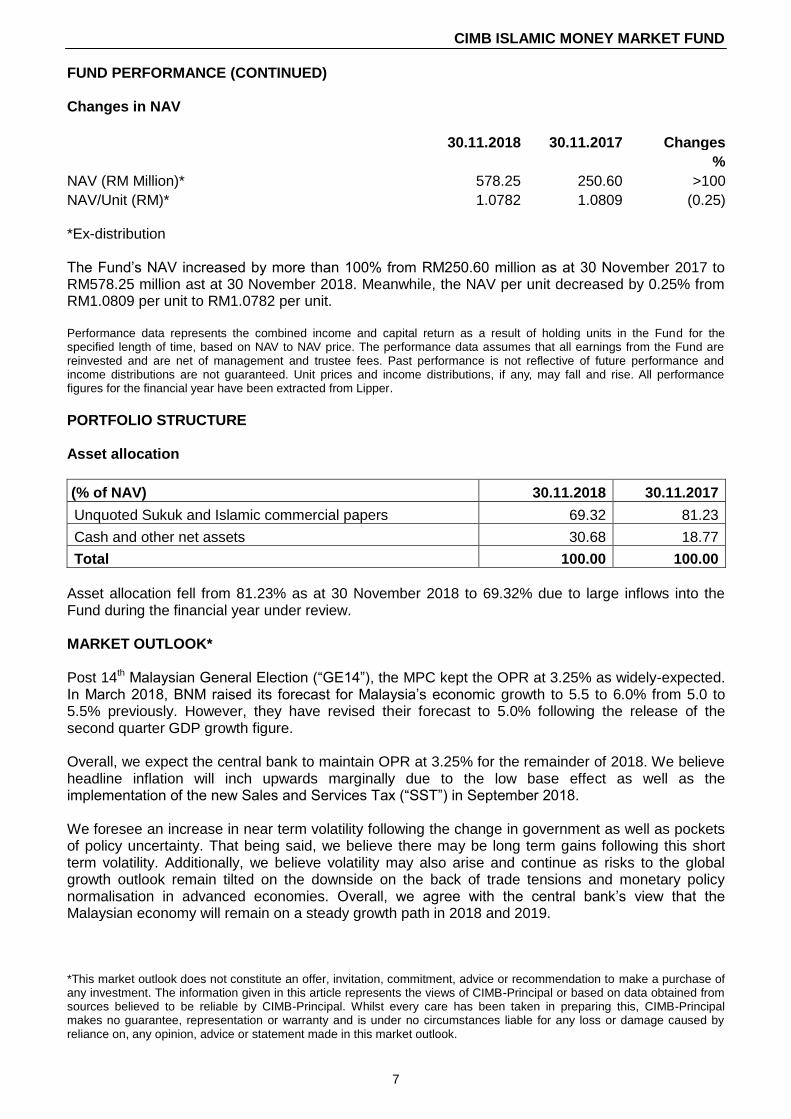

FUND PERFORMANCE (CONTINUED)

Changes in NAV

30.11.2018 30.11.2017 Changes

%

NAV (RM Million)* 578.25 250.60 >100

NAV/Unit (RM)* 1.0782 1.0809 (0.25)

*Ex-distribution

The Fund’s NAV increased by more than 100% from RM250.60 million as at 30 November 2017 to RM578.25 million ast at 30 November 2018. Meanwhile, the NAV per unit decreased by 0.25% from RM1.0809 per unit to RM1.0782 per unit.

Performance data represents the combined income and capital return as a result of holding units in the Fund for the specified length of time, based on NAV to NAV price. The performance data assumes that all earnings from the Fund are reinvested and are net of management and trustee fees. Past performance is not reflective of future performance and income distributions are not guaranteed. Unit prices and income distributions, if any, may fall and rise. All performance figures for the financial year have been extracted from Lipper.

PORTFOLIO STRUCTURE

Asset allocation

(% of NAV) 30.11.2018 30.11.2017

Unquoted Sukuk and Islamic commercial papers 69.32 81.23

Cash and other net assets 30.68 18.77

Total 100.00 100.00

Asset allocation fell from 81.23% as at 30 November 2018 to 69.32% due to large inflows into the Fund during the financial year under review.

MARKET OUTLOOK*

Post 14th Malaysian General Election (“GE14”), the MPC kept the OPR at 3.25% as widely-expected. In March 2018, BNM raised its forecast for Malaysia’s economic growth to 5.5 to 6.0% from 5.0 to 5.5% previously. However, they have revised their forecast to 5.0% following the release of the second quarter GDP growth figure.

Overall, we expect the central bank to maintain OPR at 3.25% for the remainder of 2018. We believe headline inflation will inch upwards marginally due to the low base effect as well as the implementation of the new Sales and Services Tax (“SST”) in September 2018.

We foresee an increase in near term volatility following the change in government as well as pockets of policy uncertainty. That being said, we believe there may be long term gains following this short term volatility. Additionally, we believe volatility may also arise and continue as risks to the global growth outlook remain tilted on the downside on the back of trade tensions and monetary policy normalisation in advanced economies. Overall, we agree with the central bank’s view that the Malaysian economy will remain on a steady growth path in 2018 and 2019.

*This market outlook does not constitute an offer, invitation, commitment, advice or recommendation to make a purchase ofany investment. The information given in this article represents the views of CIMB-Principal or based on data obtained from sources believed to be reliable by CIMB-Principal. Whilst every care has been taken in preparing this, CIMB-Principal makes no guarantee, representation or warranty and is under no circumstances liable for any loss or damage caused by reliance on, any opinion, advice or statement made in this market outlook.

CIMB ISLAMIC MONEY MARKET FUND

8

INVESTMENT STRATEGY

In line with the cautious investor sentiment, we continue to maintain overweight on selective corporate bonds with strong fundamentals.

UNIT HOLDINGS STATISTICS

Breakdown of unit holdings by size as at 30 November 2018 are as follows:

Size of unit holdings (units) No. of unit holders No. of units held (million)

% of units held

5,000 and below 14,901 0.04 0.01

5,001-10,000 77 0.61 0.11

10,001-50,000 1,134 27.67 5.16

50,001-500,000 410 45.49 8.48

500,001 and above 26 462.45 86.24

Total 16,548 536.26 100.00

SOFT COMMISSIONS AND REBATES

CIMB-Principal Asset Management Berhad (the “Manager”) and the Trustee will not retain any form of rebate or soft commission from, or otherwise share in any commission with, any broker in consideration for directing dealings in the investments of the Funds unless the soft commission received is retained in the form of goods and services such as financial wire services and stock quotations system incidental to investment management of the Funds. All dealings with brokers are executed on best available terms.

During the financial year under review, the Manager and the Trustee did not receive any rebates from the brokers or dealers but the Manager has retained soft commission in the form of goods and services such as financial wire services and stock quotations system incidental to investment management of the Funds.

CIMB ISLAMIC MONEY MARKET FUND

9

STATEMENT BY MANAGER TO THE UNIT HOLDERS OF CIMB ISLAMIC MONEY MARKET FUND

We, being the Directors of CIMB-Principal Asset Management Berhad (the “Manager”), do hereby state that, in the opinion of the Manager, the accompanying audited financial statements set out on pages 16 to 46 are drawn up in accordance with the provisions of the Deeds and give a true and fair view of the financial position of the Fund as at 30 November 2018 and of its financial performance, changes in equity and cash flows for the financial year then ended in accordance with the provisions of the Malaysian Financial Reporting Standards (“MFRS”) and International Financial Reporting Standards (“IFRS”).

For and on behalf of the Manager CIMB-Principal Asset Management Berhad (Company No.: 304078-K)

MUNIRAH KHAIRUDDIN ALEJANDRO ECHEGORRI Chief Executive Officer/Executive Director Executive Director

Kuala Lumpur 16 January 2019

CIMB ISLAMIC MONEY MARKET FUND

10

TRUSTEE’S REPORT TO THE UNIT HOLDERS OF CIMB ISLAMIC MONEY MARKET FUND

We, MTrustee Berhad, being the Trustee of CIMB Islamic Money Market Fund (the “Fund”), are of the opinion that CIMB-Principal Asset Management Berhad (the “Manager”), has managed the Fund for the financial year ended 30 November 2018 in accordance with the following:

(a) limitations imposed on the investment powers of the Manager under the Deeds, the Securities Commission Malaysia’s Guidelines on the Unit Trust Funds, the Capital Markets and Services Act 2007 and other applicable laws;

(b) valuation/pricing is carried out in accordance with the Deeds and relevant regulatory requirements;

(c) creation and cancellation of units is carried out in accordance with the Deeds and relevant regulatory requirements; and

(d) during the financial year, a total distribution of 4.24 sen per unit (gross) has been distributed to the unit holders of the Fund. We are of the view that the distribution is consistent with the objective of the Fund.

For and on behalf of the Trustee MTrustee Berhad

NURIZAN JALIL Chief Executive Officer

Selangor 16 January 2019

CIMB ISLAMIC MONEY MARKET FUND

11

SHARIAH ADVISER’S REPORT TO THE UNIT HOLDERS OF CIMB ISLAMIC MONEY MARKET FUND We have acted as the Shariah Adviser of CIMB Islamic Money Market Fund (the “Fund”) for the financial year ended 30 November 2018. Our responsibility is to ensure that the procedures and processes employed by CIMB-Principal Asset Management Berhad (the “Manager”) are in accordance with Shariah and Shariah Investment Guidelines. In our opinion, the Manager has managed and administered the Fund in accordance with the Shariah Investment Guidelines of the Fund and complied with applicable guidelines, rulings or decisions issued by the Securities Commission Malaysia pertaining to Shariah matters for the financial year ended 30 November 2018. In addition, we confirm that the investment portfolio of the Fund comprises securities which have been classified as Shariah-compliant by the Shariah Advisory Council of the Securities Commission Malaysia (“SACSC”) and where applicable the Shariah Advisory Council of Bank Negara Malaysia. For investments other than the abovementioned, we have reviewed the same and are of the opinion that these investments were in accordance with the Shariah Investment Guidelines of the Fund. This report is made solely to the unit holders of the Fund, as a body, and for no other purpose. We do not assume responsibility to any other person for the content of this report and we shall not be liable for any errors or non-disclosure on the part of the Manager. For and on behalf of Shariah Adviser CIMB Islamic Bank Berhad ASHRAF GOMMA ALI Director/Regional Head, Shariah & Governance/Designated Person Responsible for Shariah Advisory Kuala Lumpur 16 January 2019

CIMB ISLAMIC MONEY MARKET FUND

12

INDEPENDENT AUDITORS’ REPORT TO THE UNIT HOLDERS OF CIMB ISLAMIC MONEY MARKET FUND

REPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS

Our opinion

In our opinion, the financial statements of CIMB Islamic Money Market Fund (the “Fund”) give a true and fair view of the financial position of the Fund as at 30 November 2018, and of its financial performance and its cash flows for the year then ended in accordance with Malaysian Financial Reporting Standards and International Financial Reporting Standards.

What we have audited

We have audited the financial statements of the Fund, which comprise the statement of financial position as at 30 November 2018, and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies, as set out on pages 16 to 46.

Basis for opinion

We conducted our audit in accordance with approved standards on auditing in Malaysia and International Standards on Auditing. Our responsibilities under those standards are further described in the “Auditors’ responsibilities for the audit of the financial statements” section of our report.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Independence and other ethical responsibilities

We are independent of the Fund in accordance with the By-Laws (on Professional Ethics, Conduct and Practice) of the Malaysian Institute of Accountants (“By-Laws”) and the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants (“IESBA Code’), and we have fulfilled our other ethical responsibilities in accordance with the By-Laws and the IESBA Code.

CIMB ISLAMIC MONEY MARKET FUND

13

INDEPENDENT AUDITORS’ REPORT TO THE UNIT HOLDERS OF CIMB ISLAMIC MONEY MARKET FUND (CONTINUED) REPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS (CONTINUED)

Information other than the financial statements and auditors’ report thereon The Manager of the Fund is responsible for the other information. The other information comprises Manager’s report but does not include the financial statements of the Fund and our auditors’ report thereon. Our opinion on the financial statements of the Fund does not cover the other information and we do not express any form of assurance conclusion thereon. In connection with our audit of the financial statements of the Fund, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements of the Fund or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard. Responsibilities of the Manager for the financial statements The Manager of the Fund is responsible for the preparation of the financial statements of the Fund that give a true and fair view in accordance with Malaysian Financial Reporting Standards and International Financial Reporting Standards in Malaysia. The Manager is also responsible for such internal control as the Manager determines is necessary to enable the preparation of financial statements of the Fund that are free from material misstatement, whether due to fraud or error. In preparing the financial statements of the Fund, the Manager is responsible for assessing the Fund’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the Manager either intends to liquidate the Fund or to cease operations, or has no realistic alternative but to do so.

CIMB ISLAMIC MONEY MARKET FUND

14

INDEPENDENT AUDITORS’ REPORT TO THE UNIT HOLDERS OF CIMB ISLAMIC MONEY MARKET FUND (CONTINUED)

REPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS (CONTINUED)

Responsibilities of the Manager for the financial statements (continued)

Our objectives are to obtain reasonable assurance about whether the financial statements of the Fund as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with approved standards on auditing in Malaysia and International Standards on Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with approved standards on auditing in Malaysia and International Standards on Auditing, we exercise professional judgement and maintain professional scepticism throughout the audit. We also:

(a) Identify and assess the risks of material misstatement of the financial statements of the Fund, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

(b) Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control.

(c) Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the Manager.

(d) Conclude on the appropriateness of the Manager’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Fund’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditors’ report to the related disclosures in the financial statements of the Fund or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors’ report. However, future events or conditions may cause the Fund to cease to continue as a going concern.

(e) Evaluate the overall presentation, structure and content of the financial statements of the Fund, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

CIMB ISLAMIC MONEY MARKET FUND

15

INDEPENDENT AUDITORS’ REPORT TO THE UNIT HOLDERS OF CIMB ISLAMIC MONEY MARKET FUND (CONTINUED)

REPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS (CONTINUED)

Responsibilities of the Manager for the financial statements (continued)

We communicate with the Manager regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

OTHER MATTERS

This report is made solely to the unit holders of the Fund and for no other purpose. We do not assume responsibility to any other person for the content of this report.

PRICEWATERHOUSECOOPERS PLT LLP0014401-LCA & AF 1146 Chartered Accountants

Kuala Lumpur 16 January 2019

CIMB ISLAMIC MONEY MARKET FUND

16

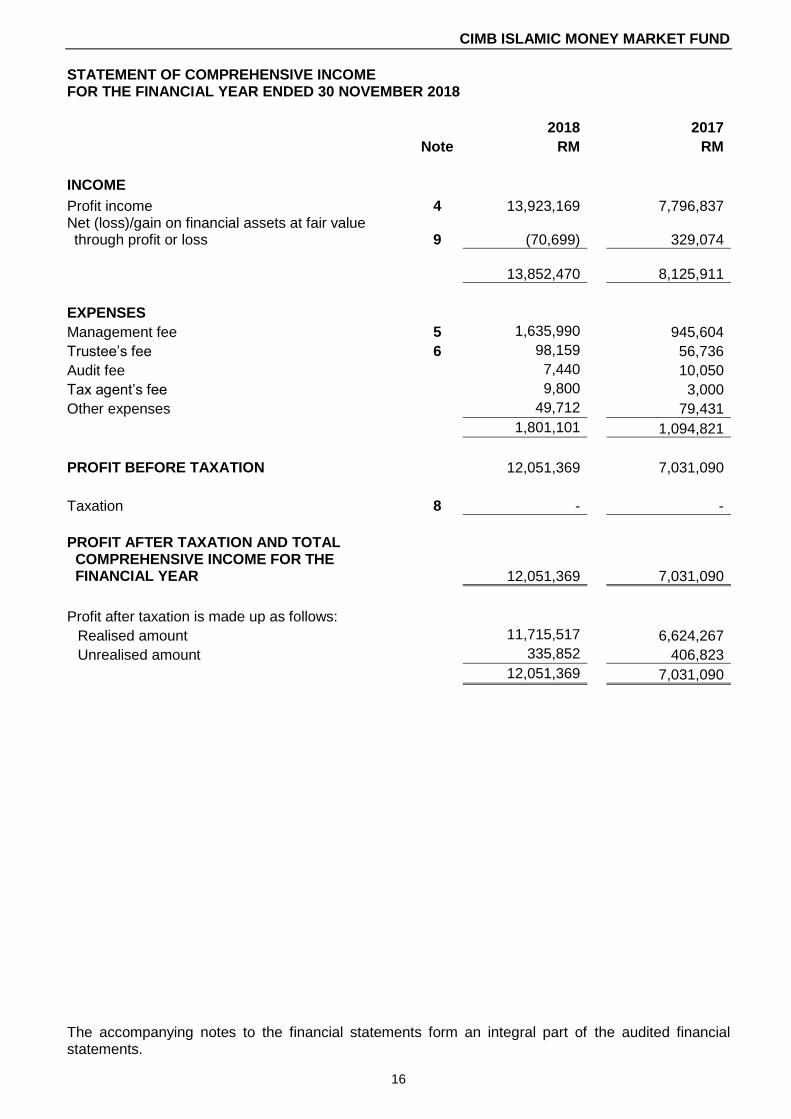

STATEMENT OF COMPREHENSIVE INCOME FOR THE FINANCIAL YEAR ENDED 30 NOVEMBER 2018

2018 2017

Note RM RM

INCOME

Profit income 4 13,923,169 7,796,837 Net (loss)/gain on financial assets at fair value through profit or loss 9 (70,699) 329,074

13,852,470 8,125,911

EXPENSES

Management fee 5 1,635,990 945,604

Trustee’s fee 6 98,159 56,736

Audit fee 7,440 10,050

Tax agent’s fee 9,800 3,000

Other expenses 49,712 79,431

1,801,101 1,094,821

PROFIT BEFORE TAXATION 12,051,369 7,031,090

Taxation 8 - -

PROFIT AFTER TAXATION AND TOTAL COMPREHENSIVE INCOME FOR THE FINANCIAL YEAR 12,051,369 7,031,090

Profit after taxation is made up as follows:

Realised amount 11,715,517 6,624,267

Unrealised amount 335,852 406,823

12,051,369 7,031,090

The accompanying notes to the financial statements form an integral part of the audited financial statements.

CIMB ISLAMIC MONEY MARKET FUND

17

STATEMENT OF FINANCIAL POSITION AS AT 30 NOVEMBER 2018

2018 2017

Note RM RM

ASSETS

Cash and cash equivalents (Shariah-compliant) 10 228,390,848 47,708,071 Financial assets at fair value through profit or loss (Shariah-compliant) 9 400,836,273 203,550,648

Amount due from Manager 189,057 241,770

TOTAL ASSETS 629,416,178 251,500,489

LIABILITIES

Amount due to dealers 50,886,255 -

Amount due to Manager 57,361 724,085

Accrued management fee 153,389 101,766

Amount due to Trustee 9,203 6,106

Distribution payable 46,610 47,042

Other payables and accruals 11,999 25,843

TOTAL LIABILITIES 51,164,817 904,842

NET ASSET VALUE OF THE FUND 578,251,361 250,595,647

EQUITY

Unit holders’ capital 553,374,270 224,826,768

Retained earnings 24,877,091 25,768,879

NET ASSETS ATTRIBUTABLE TO UNIT HOLDERS 578,251,361 250,595,647

NUMBER OF UNITS IN CIRCULATION (UNITS) 11 536,262,161 231,828,930

NET ASSET VALUE PER UNIT (RM)

(EX-DISTRIBUTION) 1.0782 1.0809

The accompanying notes to the financial statements form an integral part of the audited financial statements.

CIMB ISLAMIC MONEY MARKET FUND

18

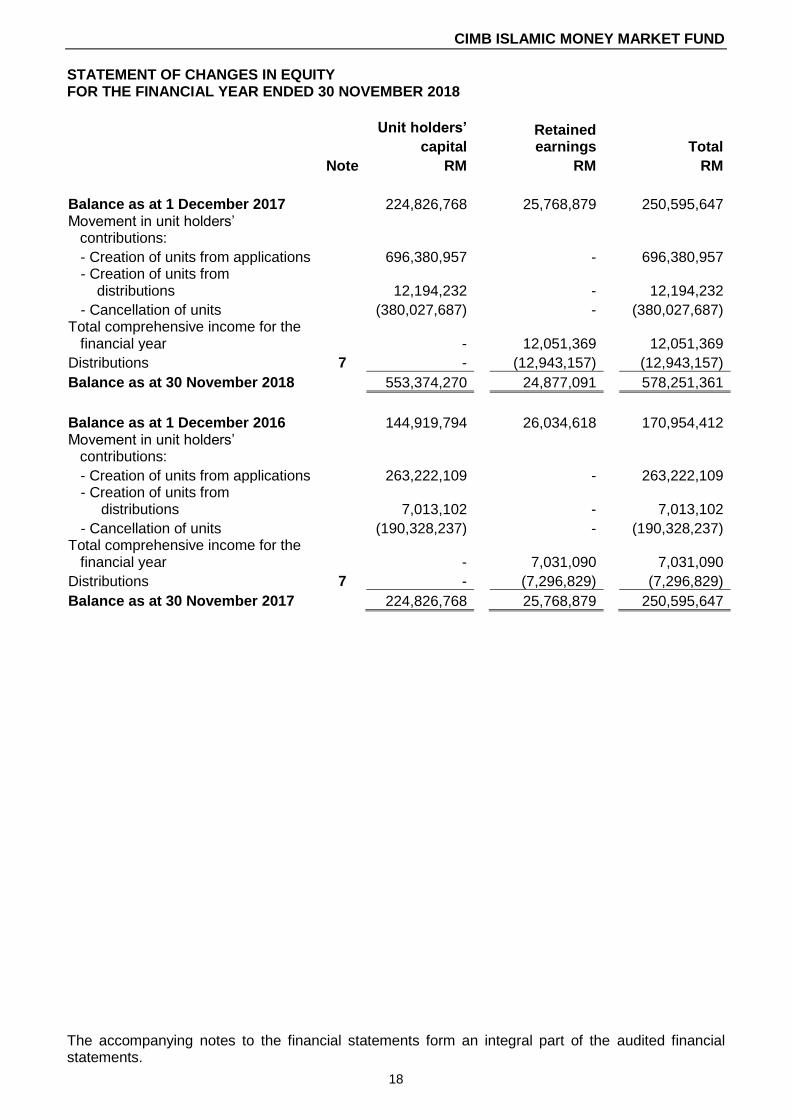

STATEMENT OF CHANGES IN EQUITY FOR THE FINANCIAL YEAR ENDED 30 NOVEMBER 2018

Unit holders’ Retained earnings Total capital

Note RM RM RM

Balance as at 1 December 2017 224,826,768 25,768,879 250,595,647 Movement in unit holders’

contributions:

- Creation of units from applications 696,380,957 - 696,380,957 - Creation of units from

distributions 12,194,232 - 12,194,232

- Cancellation of units (380,027,687) - (380,027,687) Total comprehensive income for the financial year - 12,051,369 12,051,369

Distributions 7 - (12,943,157) (12,943,157)

Balance as at 30 November 2018 553,374,270 24,877,091 578,251,361

Balance as at 1 December 2016 144,919,794 26,034,618 170,954,412 Movement in unit holders’

contributions:

- Creation of units from applications 263,222,109 - 263,222,109 - Creation of units from

distributions 7,013,102 - 7,013,102

- Cancellation of units (190,328,237) - (190,328,237) Total comprehensive income for the financial year - 7,031,090 7,031,090

Distributions 7 - (7,296,829) (7,296,829)

Balance as at 30 November 2017 224,826,768 25,768,879 250,595,647

The accompanying notes to the financial statements form an integral part of the audited financial statements.

CIMB ISLAMIC MONEY MARKET FUND

19

STATEMENT OF CASH FLOWS FOR THE FINANCIAL YEAR ENDED 30 NOVEMBER 2018

2018 2017

Note RM RM

CASH FLOWS FROM OPERATING ACTIVITIES Proceeds from disposal of unquoted Sukuk and Islamic commercial papers 155,910,330 56,490,200 Purchase of unquoted Sukuk and Islamic commercial papers (563,658,758) (296,104,779) Proceeds from redemption of unquoted Sukuk and Islamic commercial papers 259,000,000 173,500,000 Profit income received from Shariah-compliant deposits with licensed Islamic financial institutions and Hibah received 1,181,207 951,600 Profit income received from unquoted Sukuk and Islamic commercial papers 15,020,321 5,612,618

Management fee paid (1,584,367) (915,749)

Trustee’s fee paid (95,062) (54,945)

Payments for other fees and expenses (80,796) (88,927)

Net cash used in operating activities (134,307,125) (60,609,982)

CASH FLOWS FROM FINANCING ACTIVITIES

Cash proceeds from units created 696,433,670 263,327,217

Payments for cancellation of units (380,694,411) (194,913,636)

Distributions paid (749,357) (236,685)

Net cash generated from financing activities 314,989,902 68,176,896

Net increase in cash and cash equivalents 180,682,777 7,566,914 Cash and cash equivalents at the beginning of the financial year 47,708,071 40,141,157

Cash and cash equivalents at the end of the financial year 10 228,390,848 47,708,071

Cash and cash equivalents comprised of: Shariah-compliant deposits with licensed Islamic financial institutions 228,379,716 47,668,717

Bank balances 11,132 39,354

Cash and cash equivalents at the end of the financial year 10 228,390,848 47,708,071

The accompanying notes to the financial statements form an integral part of the audited financial statements.

CIMB ISLAMIC MONEY MARKET FUND

20

NOTES TO THE FINANCIAL STATEMENTS FOR THE FINANCIAL YEAR ENDED 30 NOVEMBER 2018

1. THE FUND, THE MANAGER AND ITS PRINCIPAL ACTIVITY

CIMB Islamic Money Market Fund (the “Fund’) is governed by a Master Deed dated 15 May2008, a Third Supplemental Master Deed dated 25 June 2008, a Sixth Supplemental MasterDeed dated 14 July 2008, a Seventh Supplemental Master Deed dated 19 November 2008 anda Seventeenth Supplemental Master Deed dated 25 March 2015 (collectively referred to as the“Deeds”) between CIMB-Principal Asset Management Berhad (the “Manager”) and MTrusteeBerhad (the “Trustee”).

The Fund will place at least 90% of its NAV in Shariah-compliant money market instrumentssuch as Islamic Accepted Bills, Islamic Negotiable Instruments of Deposits and Repo-i as well asin any other Shariah-compliant fixed income instruments and placements of Deposits, all ofwhich are highly liquid and have a remaining maturity period of less than 365 days. Up to 10% ofthe Fund’s NAV may be invested in Shariah-compliant fixed income instruments, which have aremaining maturity period of more than 365 days but less than 732 days. The Fund will beactively managed. The strategy is to invest in liquid and low risk short-term investments forcapital preservation. The investment strategy adheres to the SC Guidelines pertaining toinvestments for a money market fund.

All investments are subjected to the SC Guidelines on Unit Trust Funds, SC requirements, theDeeds, except where exemptions or variations have been approved by the SC, internal policiesand procedures and the Fund’s objective.

The Manager, a company incorporated in Malaysia, is jointly owned by CIMB Group Sdn Bhdand Principal International (Asia) Limited. The principal activities of the Manager are theestablishment and management of unit trust funds and fund management activities.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The following accounting policies have been used consistently in dealing with items which areconsidered material in relation to the financial statements:

(a) Basis of preparation

The financial statements have been prepared in accordance with the provisions of the MFRS and IFRS.

The financial statements have been prepared under the historical cost convention, as modified by financial assets at fair value through profit or loss.

The preparation of financial statements in conformity with MFRS and IFRS requires the use of certain critical accounting estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reported year.

It also requires the Manager to exercise their judgement in the process of applying the Fund’s accounting policies. Although these estimates and judgement are based on the Manager’s best knowledge of current events and actions, actual results may differ.

CIMB ISLAMIC MONEY MARKET FUND

21

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(a) Basis of preparation (continued)

The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in Note 2(j).

Standards, amendments to published standards and interpretations to existing standards that are effective:

The Fund has applied the following amendments for the first time for the financial period beginning 1 December 2017:

Amendments to MFRS 107 ‘‘Statement of Cash Flows - Disclosure Initiative’’introduce an additional disclosure on changes in liabilities arising from financingactivities.

The adoption of these amendments did not have any impact on the current financial period and is not likely to affect future years.

The standards, amendments to published standards and interpretations to existing standards that are applicable to the Fund but not yet effective and have not been early adopted are as follows:

(i) Financial year beginning on/after 1 December 2018

MFRS 9 “Financial Instruments” (effective from 1 January 2018) will replaceMFRS 139 “Financial Instruments: Recognition and Measurement”.

MFRS 9 retains but simplifies the mixed measurement model in MFRS 139and establishes three primary measurement categories for financial assets:amortised cost, fair value through profit or loss and fair value through othercomprehensive income (“OCI”). The basis of classification depends on theentity's business model and the contractual cash flow characteristics of thefinancial asset.

Investments in equity instruments1 are always measured at fair valuethrough profit or loss with an irrevocable option at inception to presentchanges in fair value in OCI (provided the instrument is not held for trading).A debt instrument2 is measured at amortised cost only if the entity is holdingit to collect contractual cash flows and the cash flows represent principal andinterest3.

For liabilities, the standard retains most of the MFRS 139 requirements.These include amortised cost accounting for most financial liabilities, withbifurcation of embedded derivatives1. The main changes are:

For financial liabilities classified as FVTPL, the fair calue changes dtoown credit risk should be recognised directly to OCI. There is nosubsequent recycling to profit or loss.

When a financial liability measured at amortised cost is modified withoutthis resulting in derecognition, a gain or loss, being the differencebetween the original effective interest rate, should be recognisedimmediately in profit or loss.

¹ For the purposes of the investments made by the Fund, equity instruments and derivatives refers to Shariah-compliant equity instruments and Shariah-compliant derivatives.

² For the purposes of the investments made by the Fund, debt instruments refers to Sukuk. ³ For the purposes of this Fund, interest refers to profits earned from Shariah-compliant investments

CIMB ISLAMIC MONEY MARKET FUND

22

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(a) Basis of preparation (continued)

MFRS 9 introduces an expected credit loss model (“ECL”) on impairment that replaces the incurred loss impairment model used in MFRS 139. The expected credit loss model is forward-looking and eliminates the need for a trigger event to have occurred before credit losses are recognised.

The Fund has reviewed its financial assets and liabilities and has assessed the following impact from the adoption of the new standard on 1 December 2018:

There will be no impact on the Fund’s accounting for financial assets as the Fund’s equity investments currently measured at fair value through profit or loss will continue to be measured on the same basis under MFRS 9.

There will be no impact on the Fund’s accounting for financial liabilities as the new requirements only affect the accounting for financial liabilities that are designated at fair value through profit or loss and the Fund does not have any such liabilities.

The new impairment model requires the recognition of impairment provisions based on ECL rather than only incurred credit losses as is the case under MFRS 139. It applies to financial assets classified at amortised cost. Based on the assessments undertaken to date, the Fund does not expect any loss allowance to be recognised upon adoption of MFRS 9.

(b) Financial assets and financial liabilities

Classification

Financial assets are designated at fair value through profit or loss when they are managed and their performance evaluated on a fair value basis.

Financing and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market and have been included in current assets. The Fund’s financing and receivables comprise cash and cash equivalents, amount due from stockbrokers, amount due from Manager, amount due from Manager of collective investment scheme and dividends receivable.

Financial liabilities are classified according to the substance of the contractual arrangements entered into and the definitions of a financial liability.

The Fund classifies amount due to dealer, amount due to Manager, accrued management fee, amount due to Trustee and other payables and accruals as other financial liabilities.

CIMB ISLAMIC MONEY MARKET FUND

23

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(b) Financial assets and financial liabilities (continued)

Recognition and measurement Regular purchases and sales of financial assets are recognised on the trade-date, the date on which the Fund commits to purchase or sell the asset. Shariah-compliant investments are initially recognised at fair value. Financial liabilities, within the scope of MFRS 139, are recognised in the statement of financial position when, and only when, the Fund becomes a party to the contractual provisions of the financial instrument. Financial assets are derecognised when the rights to receive cash flows from the Shariah-compliant investments have expired or have been transferred and the Fund has transferred substantially all risks and rewards of ownership. Financial liabilities are derecognised when it is extinguished, i.e. when the obligation specified in the contract is discharged or cancelled or expired. Unrealised gains or losses arising from changes in the fair value of the financial assets at fair value through profit or loss are presented in the statement of comprehensive income within net gain or loss on financial assets at fair value through profit or loss in the financial year which they arise. Unquoted Sukuk denominated in Ringgit Malaysia (“RM”) are revalued on a daily basis based on fair value prices quoted by a Bond Pricing Agency (“BPA”) registered with the SC as per the SC Guidelines on Unit Trust Funds. Refer to Note 2(j) for further explanation. Islamic commercial papers are revalued at least weekly by reference to bid and offer prices quoted by three (3) independent and reputable financial institutions of similar standing at the close of trading. Shariah-compliant deposits with licensed Islamic financial institutions are stated at cost plus accrued profit calculated on the effective profit method over the financial year from the date of placement to the date of maturity of the respective deposits. Financing and receivables and other financial liabilities are subsequently carried at amortised cost using the effective profit method.

CIMB ISLAMIC MONEY MARKET FUND

24

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(b) Financial assets and financial liabilities (continued)

Impairment on assets carried at amortised costs For assets carried at amortised cost, the Fund assesses at the end of the reporting year whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is impaired and impairment losses are incurred only if there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated. The amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective profit rate. The asset’s carrying amount is reduced and the amount of the loss is recognised in statement of comprehensive income. If ‘financing and receivables’ has a variable profit rate, the discount rate for measuring any impairment loss is the current effective profit rate determined under the contract. As a practical expedient, the Fund may measure impairment on the basis of an instrument’s fair value using an observable market price.

If, in a subsequent financial year, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised (such as an improvement in the debtor’s credit rating), the reversal of the previously recognised impairment loss is recognised in statement of comprehensive income. When an asset is uncollectible, it is written off against the related allowance account. Such assets are written off after all the necessary procedures have been completed and the amount of the loss has been determined.

(c) Income recognition

Profit income from Shariah-compliant deposits with licensed Islamic financial institutions, unquoted Sukuk and Islamic commercial papers are recognised on a time proportionate basis using the effective profit method on an accrual basis. Realised gain or loss on disposal of unquoted Sukuk and Islamic commercial papers are accounted for as the difference between the net disposal proceeds and the carrying amount of unquoted Sukuk and Islamic commercial papers, determined on cost adjusted for accretion of discount or amortisation of premium.

(d) Functional and presentation currency

Items included in the financial statements of the Fund are measured using the currency of the primary economic environment in which the Fund operates (the “functional currency”). The financial statements are presented in RM, which is the Fund’s functional and presentation currency.

CIMB ISLAMIC MONEY MARKET FUND

25

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(e) Cash and cash equivalents

For the purpose of statement of cash flows, cash and cash equivalents comprise bank balances and Shariah-compliant deposits held in highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

(f) Taxation Current tax expense is determined according to Malaysian tax laws at the current rate

based upon the taxable profit earned during the financial year. (g) Distribution

A distribution to the Fund’s unit holders is accounted for as a deduction from realised reserve. A proposed distribution is recognised as a liability in the financial year in which it is approved by the Trustee.

(h) Unit holders’ capital

The unit holders’ contributions to the Fund meet the criteria to be classified as equity instruments under MFRS 132 “Financial Instruments: Presentation”. Those criteria include: • the units entitle the holder to a proportionate share of the Fund’s NAV; • the units are the most subordinated class and class features are identical; • there is no contractual obligations to deliver cash or another financial asset

other than the obligation on the Fund to repurchase; and • the total expected cash flows from the units over its life are based substantially on

the profit or loss of the Fund. The outstanding units are carried at the redemption amount that is payable at each financial year if unit holder exercises the right to put the unit back to the Fund. Units are created and cancelled at prices based on the Fund’s NAV per unit at the time of creation or cancellation. The Fund’s NAV per unit is calculated by dividing the net assets attributable to unit holders with the total number of outstanding units.

(i) Segment information

Operating segments are reported in a manner consistent with the internal reporting used by the chief operating decision-maker. The chief operating decision-maker is responsible for allocating resources and assessing performance of the operating segments.

CIMB ISLAMIC MONEY MARKET FUND

26

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(j) Critical accounting estimates and judgements in applying accounting policies

The Fund makes estimates and assumptions concerning the future. The resulting accounting estimates will, by definition, rarely equal the related actual results. To enhance the information content of the estimates, certain key variables that are anticipated to have material impact to the Fund’s results and financial position are tested for sensitivity to changes in the underlying parameters. Estimates and judgement are continually evaluated by the Manager and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. Estimate of fair value of unquoted Sukuk and Islamic commercial papers In undertaking any of the Fund’s Shariah-compliant investment, the Manager will ensure that all assets of the Fund under management will be valued appropriately, that is at fair value and in compliance with the SC Guidelines on Unit Trust Funds. Ringgit-denominated unquoted Sukuk are valued using fair value prices quoted by a BPA. Where the Manager is of the view that the price quoted by BPA for a specific unquoted Sukuk differs from the market price by more than 20 basis points (“bps”) the Manager may use market price, provided that the Manager records its basis for using a non-BPA price, obtains necessary internal approvals to use the non-BPA price, and keeps an audit trail of all decisions and basis for adopting the use of non-BPA price. Islamic commercial papers are revalued at least weekly by reference to bid and offer prices quoted by three (3) independent and reputable financial institutions of similar standing at the close of trading.

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

Financial instruments of the Fund are as follows:

Financial assets at fair value

through profit or loss

Financing and

receivables Total

RM RM RM

2018 Cash and cash equivalents (Shariah-compliant) (Note 10) - 228,390,848 228,390,848 Unquoted Sukuk and Islamic commercial papers (Note 9) 400,836,273 - 400,836,273

Amount due from Manager - 189,057 189,057

400,836,273 228,579,905 629,416,178

2017 Cash and cash equivalents (Shariah-compliant) (Note 10) - 47,708,071 47,708,071 Unquoted Sukuk and Islamic commercial papers (Note 9) 203,550,648 - 203,550,648

Amount due from Manager - 241,770 241,770

203,550,648 47,949,841 251,500,489

All current liabilities are financial liabilities which are carried at amortised cost.

CIMB ISLAMIC MONEY MARKET FUND

27

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED) The investment objective of the Fund is to provide investors with liquidity and regular income, whilst maintaining capital stability by investing primarily in money market instruments that conform with Shariah principles. The Fund is exposed to a variety of risks which include market risk (inclusive of price risk and interest rate risk), credit risk and liquidity risk. Financial risk management is carried out through internal control process adopted by the Manager and adherence to the investment restrictions as stipulated in the Deeds and SC Guidelines on Unit Trust Funds.

(a) Market risk

(i) Price risk

This is the risk that the fair value of a Shariah-compliant investment in unquoted Sukuk and Islamic commercial papers will fluctuate because of changes in market prices (other than those arising from interest rate risk). The value of unquoted Sukuk and Islamic commercial papers may fluctuate according to the activities of individual companies, sector and overall political and economic conditions. Such fluctuation may cause the Fund’s NAV and prices of units to fall as well as rise, and income produced by the Fund may also fluctuate.

The Fund is exposed to price risk arising from interest rate fluctuation in relation to its investments of RM 400,836,273 (2017: RM 203,550,648) in unquoted Sukuk and Islamic commercial papers. The Fund’s exposure to price risk arising from interest rate fluctuation and the related sensitivity analysis are disclosed in “interest rate risk” below.

(ii) Interest rate risk In general, when profit rates rise, unquoted Sukuk and Islamic commercial papers prices will tend to fall and vice versa. Therefore, the NAV of the Fund may also tend to fall when profit rates rise or are expected to rise. However, investors should be aware that should the Fund holds an unquoted Sukuk and Islamic commercial papers till maturity, such price fluctuations would dissipate as it approaches maturity, and thus the growth of the NAV shall not be affected at maturity. In order to mitigate profit rates exposure of the Fund, the Manager will manage the duration of the portfolio via shorter or longer tenured assets depending on the view of the future profit rate trend of the Manager, which is based on its continuous fundamental research and analysis.

Investors should note that the movement in prices of unquoted Sukuk, Islamic commercial papers and Shariah-compliant money market instruments are benchmarked against profit rates. As such, the investments are exposed to the movement of the profit rates. It does not in any way suggest that this Fund will invest in conventional financial instruments. All investments carried out for the Fund including placement and deposits are in accordance with Shariah.

CIMB ISLAMIC MONEY MARKET FUND

28

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED) (a) Market risk (continued)

(ii) Interest rate risk (continued)

This risk is crucial since unquoted Sukuk and Islamic commercial papers portfolio management depends on forecasting profit rate movements. Prices of unquoted Sukuk and Islamic commercial papers move inversely to profit rate movements, therefore as profit rates rise, the prices of unquoted Sukuk and Islamic commercial papers decrease and vice versa. Furthermore, unquoted Sukuk and Islamic commercial papers with longer maturity and lower yield coupon rates are more susceptible to profit rate movements. Such investments may be subject to unanticipated rise in profit rates which may impair the ability of the issuers to meet obligation under the instrument, especially if the issuers are highly leveraged. An increase in profit rates may therefore increase the potential for default by an issuer. The table below summarises the sensitivity of the Fund’s profit or loss and NAV to movements in prices of unquoted Sukuk and Islamic commercial papers held by the Fund as a result of movement in profit rate at the end of each reporting year. The analysis is based on the assumptions that the profit rate changed by 1% with all other variables held constant. This represents management’s best estimate of a reasonable possible shift in the profit rate, having regard to the historical volatility of the profit rate.

% Change in profit rate

Impact on profit or loss/NAV 2018 2017

RM RM

+1% (77,938) (38,136)

-1% 77,978 38,156

The Fund’s exposure to interest rate risk associated with Shariah-compliant deposits with licensed Islamic financial institutions is not material as the Shariah-compliant deposits are held on short-term basis. The Fund is not exposed to cash flow interest rate risk as the Fund does not hold any financial instruments at variable profit rate.

CIMB ISLAMIC MONEY MARKET FUND

29

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED) (b) Credit risk

Credit risk refers to the risk that counterparty will default on its contractual obligation resulting in financial loss to the Fund. Investment in unquoted Sukuk and Islamic commercial papers may involve a certain degree of credit/default risk with regards to the issuers. Generally, credit risk or default risk is the risk of loss due to the issuer’s non-payment or untimely payment of the investment amount as well as the returns on investment. This will cause a decline in value of the defaulted unquoted Sukuk and Islamic commercial papers and subsequently depress the NAV of the Fund. Usually credit risk is more apparent for an investment with a longer tenure, i.e. the longer the duration, the higher the credit risk. Credit risk can be managed by performing continuous fundamental credit research and analysis to ascertain the creditworthiness of its issuer. In addition, the Manager imposes a minimum rating requirement as rated by either local and/or foreign rating agencies and manages the duration of the investment in accordance with the objective of the Fund. For this Fund, the unquoted Sukuk and Islamic commercial papers investments must satisfy a minimum rating requirement of at least “BBB3” or “P2” rating by RAM Rating Services Berhad (“RAM Ratings”) or equivalent rating by Malaysian Rating Corporation Berhad (“MARC”) or by local rating agency(ies) of the country; “BBB-” by S&P or equivalent rating by Moody’s or Fitch. The credit risk arising from placements of Shariah-compliant deposits in licensed Islamic financial institutions is managed by ensuring that the Fund will only place deposits in reputable licensed Islamic financial institutions.

CIMB ISLAMIC MONEY MARKET FUND

30

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED) (b) Credit risk (continued)

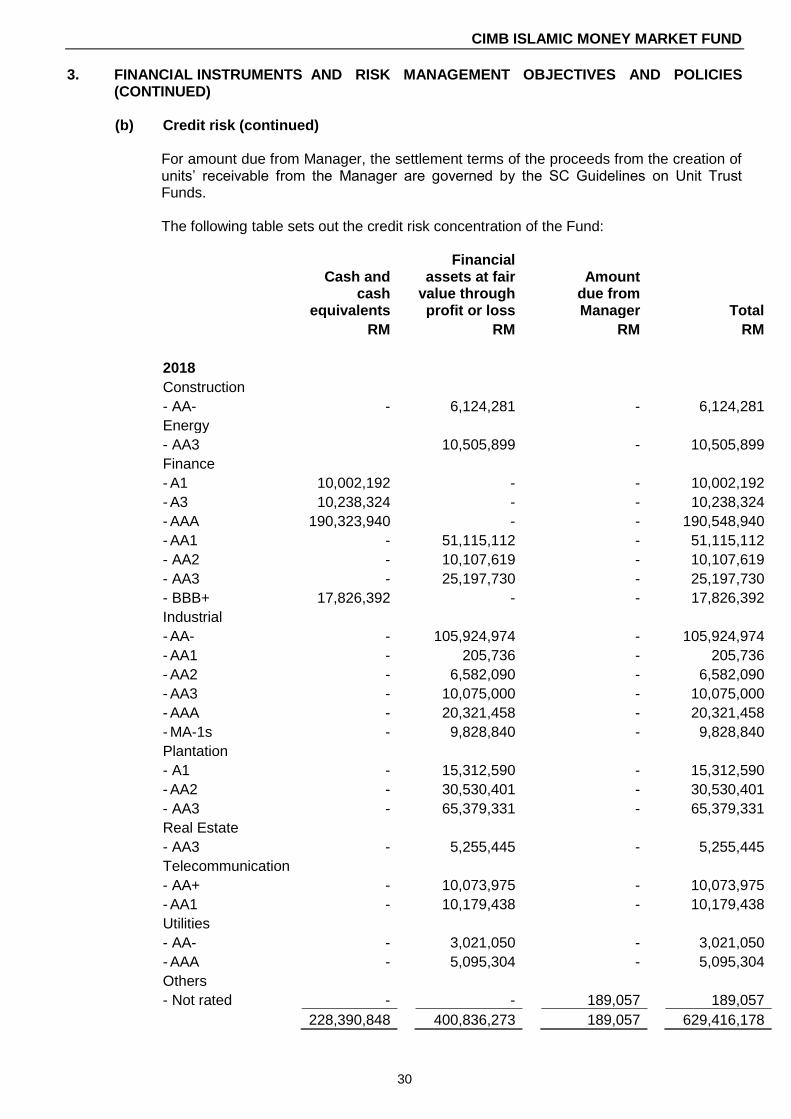

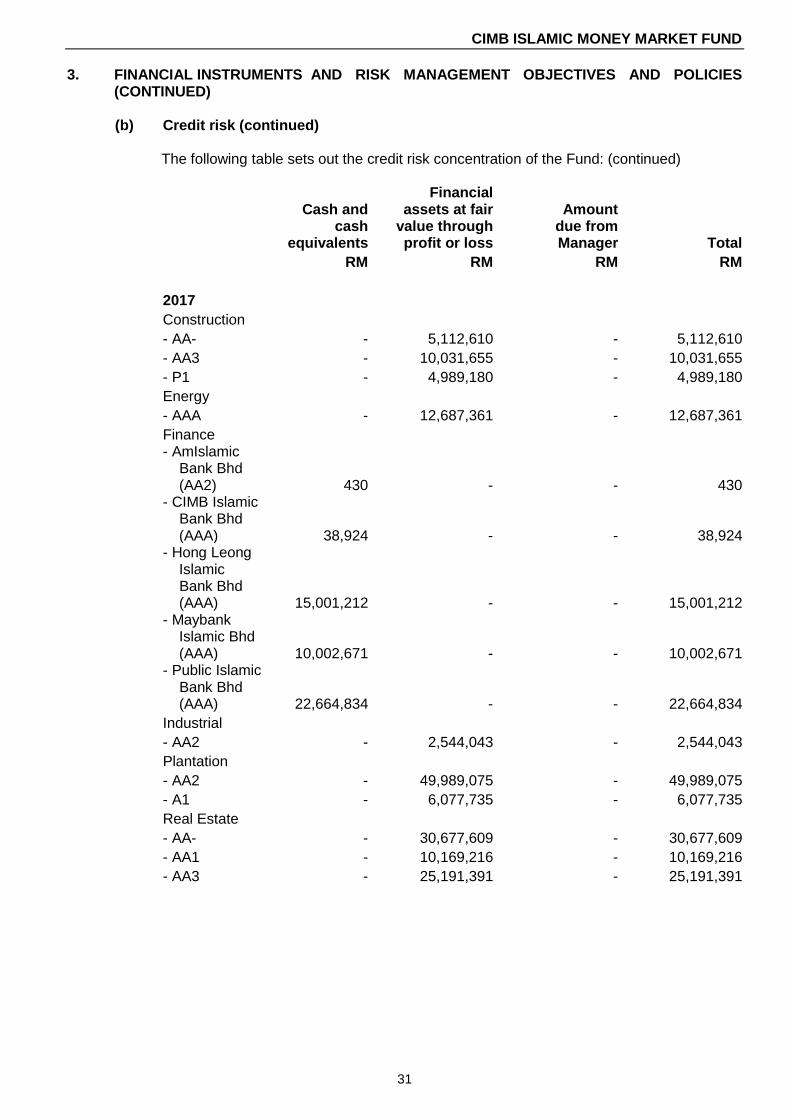

For amount due from Manager, the settlement terms of the proceeds from the creation of units’ receivable from the Manager are governed by the SC Guidelines on Unit Trust Funds. The following table sets out the credit risk concentration of the Fund:

Cash and cash

equivalents

Financial assets at fair

value through profit or loss

Amount

due from Manager Total

RM RM RM RM

2018

Construction

- AA- - 6,124,281 - 6,124,281

Energy

- AA3 10,505,899 - 10,505,899

Finance

- A1 10,002,192 - - 10,002,192

- A3 10,238,324 - - 10,238,324

- AAA 190,323,940 - - 190,548,940

- AA1 - 51,115,112 - 51,115,112

- AA2 - 10,107,619 - 10,107,619

- AA3 - 25,197,730 - 25,197,730

- BBB+ 17,826,392 - - 17,826,392

Industrial

- AA- - 105,924,974 - 105,924,974

- AA1 - 205,736 - 205,736

- AA2 - 6,582,090 - 6,582,090

- AA3 - 10,075,000 - 10,075,000

- AAA - 20,321,458 - 20,321,458

- MA-1s - 9,828,840 - 9,828,840

Plantation

- A1 - 15,312,590 - 15,312,590

- AA2 - 30,530,401 - 30,530,401

- AA3 - 65,379,331 - 65,379,331

Real Estate

- AA3 - 5,255,445 - 5,255,445

Telecommunication

- AA+ - 10,073,975 - 10,073,975

- AA1 - 10,179,438 - 10,179,438

Utilities

- AA- - 3,021,050 - 3,021,050

- AAA - 5,095,304 - 5,095,304

Others

- Not rated - - 189,057 189,057

228,390,848 400,836,273 189,057 629,416,178

CIMB ISLAMIC MONEY MARKET FUND

31

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED) (b) Credit risk (continued)

The following table sets out the credit risk concentration of the Fund: (continued)

Cash and cash

equivalents

Financial assets at fair

value through profit or loss

Amount

due from Manager Total

RM RM RM RM

2017

Construction

- AA- - 5,112,610 - 5,112,610

- AA3 - 10,031,655 - 10,031,655

- P1 - 4,989,180 - 4,989,180

Energy

- AAA - 12,687,361 - 12,687,361

Finance - AmIslamic Bank Bhd (AA2) 430 - - 430 - CIMB Islamic Bank Bhd (AAA) 38,924 - - 38,924 - Hong Leong Islamic Bank Bhd (AAA) 15,001,212 - - 15,001,212 - Maybank Islamic Bhd (AAA) 10,002,671 - - 10,002,671 - Public Islamic Bank Bhd (AAA) 22,664,834 - - 22,664,834

Industrial

- AA2 - 2,544,043 - 2,544,043

Plantation

- AA2 - 49,989,075 - 49,989,075

- A1 - 6,077,735 - 6,077,735

Real Estate

- AA- - 30,677,609 - 30,677,609

- AA1 - 10,169,216 - 10,169,216

- AA3 - 25,191,391 - 25,191,391

CIMB ISLAMIC MONEY MARKET FUND

32

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED) (b) Credit risk (continued)

The following table sets out the credit risk concentration of the Fund: (continued)

Cash and cash

equivalents

Financial assets at fair

value through profit or loss

Amount

due from Manager Total

RM RM RM RM

2017 (continued)

Utilities

- AAA - 5,093,266 - 5,093,266

- AA- - 15,320,418 - 15,320,418

- AA1 - 15,381,323 - 15,381,323

- AA3 - 10,285,766 - 10,285,766

Others

- Not rated - - 241,770 241,770

47,708,071 203,550,648 241,770 251,500,489

All financial assets of the Fund as at the end of each financial year are neither past due nor impaired.

(c) Liquidity risk

Liquidity risk is the risk that the Fund will encounter difficulty in meeting its financial obligations. The Manager manages this risk by maintaining sufficient level of liquid assets to meet anticipated payments and cancellations of the units by unit holders. Liquid assets comprise bank balances and Shariah-compliant deposits with licensed Islamic financial institutions, which are capable of being converted into cash within 7 business days. Generally, all investments are subject to a certain degree of liquidity risk depending on the nature of the investment instruments, market, sector and other factors. For the purpose of the Fund, the Manager will attempt to balance the entire portfolio by investing in a mix of assets with satisfactory trading volume and those that occasionally could encounter poor liquidity. This is expected to reduce the risks for the entire portfolio without limiting the Fund’s growth potentials.

CIMB ISLAMIC MONEY MARKET FUND

33

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED)

(c) Liquidity risk (continued) The table below summarises the Fund’s financial liabilities into relevant maturity groupings based on the remaining year as at the statement of financial position date to the contractual maturity date. The amounts in the table are the contractual undiscounted cash flows.

Between

Less than 1 month

1 month to 1 year Total

RM RM RM

2018

Amount due to dealer 50,886,255 - 50,886,255

Amount due to Manager 57,361 - 57,361

Accrued management fee 153,389 - 153,389

Amount due to Trustee 9,203 - 9,203

Distribution payable 46,610 - 46,610

Other payables and accruals - 11,999 11,999

Contractual undiscounted cash flows 51,152,818 11,999 51,164,817

2017

Amount due to Manager 724,085 - 724,085

Accrued management fee 101,766 - 101,766

Amount due to Trustee 6,106 - 6,106

Distribution payable 47,042 - 47,042

Other payables and accruals 7,281 18,562 25,843

Contractual undiscounted cash flows

886,280

18,562 904,842

(d) Capital risk management

The capital of the Fund is represented by equity consisting of unit holders’ capital of RM553,374,270 (2017: RM224,826,768) and retained earnings of RM24,877,091 (2017: RM25,768,879). The amount of capital can change significantly on a daily basis as the Fund is subject to daily subscriptions and redemptions at the discretion of unit holders. The Fund’s objective when managing capital is to safeguard the Fund’s ability to continue as a going concern in order to provide returns to unit holders and benefits for other stakeholders and to maintain a strong capital base to support the development of the investment activities of the Fund.

CIMB ISLAMIC MONEY MARKET FUND

34

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED)

(e) Fair value estimation

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e. an exit price). The fair value of financial assets traded in active markets (such as trading securities) are based on quoted market prices at the close of trading on the financial year end date. The Fund utilises the last traded market price for financial assets where the last traded price falls within the bid-ask spread. In circumstances where the last traded price is not within the bid-ask spread, the Manager will determine the point within the bid-ask spread that is most representative of the fair value. An active market is a market in which transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis. The fair value of financial assets that are not traded in an active market is determined by using valuation techniques.

(i) Fair value hierarchy

The table below analyses financial instruments carried at fair value. The different levels have been defined as follows:

Quoted prices (unadjusted) in active market for identical assets or liabilities (Level 1)

Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices) (Level 2)

Inputs for the asset and liability that are not based on observable market data (that is, unobservable inputs) (Level 3)

The level in the fair value hierarchy within which the fair value measurement is categorised in its entirety is determined on the basis of the lowest level input that is significant to the fair value measurement in its entirety. For this purpose, the significance of an input is assessed against the fair value measurement in its entirety. If a fair value measurement uses observable inputs that require significant adjustment based on unobservable inputs, that measurement is a Level 3 measurement. Assessing the significance of a particular input to the fair value measurement in its entirety requires judgement, considering factors specific to the asset or liability. The determination of what constitutes ‘observable’ requires significant judgement by the Fund. The Fund considers observable data to be that market data that is readily available, regularly distributed or updated, reliable and verifiable, not proprietary, and provided by independent sources that are actively involved in the relevant market.

CIMB ISLAMIC MONEY MARKET FUND

35

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT OBJECTIVES AND POLICIES

(CONTINUED)

(e) Fair value estimation (continued)

(i) Fair value hierarchy (continued)

Level 1 Level 2 Level 3 Total

RM RM RM RM

2018 Financial assets at fair value through profit or loss:

- Unquoted Sukuk and Islamic commercial papers - 400,836,273 - 400,836,273

2017 Financial assets at fair value through profit or loss:

- Unquoted Sukuk and Islamic commercial papers - 203,550,648 - 203,550,648

Financial instruments that trade in markets that are not considered to be active but are valued based on quoted market prices, dealer quotations or alternative pricing sources supported by observable inputs are classified within Level 2. This includes unquoted Sukuk and Islamic commercial papers. As Level 2 instruments include positions that are not traded in active markets and/or are subject to transfer restrictions, valuations may be adjusted to reflect illiquidity and/or non-transferability, which are generally based on available market information. The Fund’s policies on valuation of these financial assets are stated in Note 2(b).

(i) The carrying values of cash and cash equivalents, amount due from Manager, and all current liabilities are a reasonable approximation of their fair values due to their short term nature.

4. PROFIT INCOME

2018 2017

RM RM

Profit income from unquoted Sukuk and Islamic commercial papers 12,741,962 6,845,237 Profit income from Shariah-compliant deposits with licensed Islamic financial institutions and Hibah earned

1,181,207 951,600

13,923,169 7,796,837

CIMB ISLAMIC MONEY MARKET FUND

36

5. MANAGEMENT FEE In accordance with the Deeds, the Manager is entitled to a maximum management fee of 3.00%

per annum, calculated daily based on the NAV of the Fund. For the financial year ended 30 November 2018, the management fee is recognised at a rate of 0.50% per annum (2017: 0.50% per annum). There is no further liability to the Manager in respect of management fee other than the amount recognised above.

6. TRUSTEE’S FEE

In accordance with the Deeds, the Trustee is entitled to a maximum Trustee’s fee of 0.03% per annum calculated daily based on the NAV of the Fund. The Trustee’s fee includes the local custodian fee but excludes the foreign sub-custodian fees (if any). For the financial year ended 30 November 2018, the Trustee’s fee is recognised at a rate of 0.03% per annum (2017: 0.03% per annum). There is no further liability to the Trustee in respect of Trustee’s fee other than the amount recognised above.

7. DISTRIBUTIONS

Distributions to unit holders are derived from the following sources:

2018 2017 RM RM

Profit income 13,298,563 7,369,955 Net realised loss on disposal of unquoted Sukuk and Islamic commercial papers (117,516) (942)

13,181,047 7,369,013

Less:

Expenses (237,890) (72,184)

Net distribution amount 12,943,157 7,296,829

CIMB ISLAMIC MONEY MARKET FUND

37

7. DISTRIBUTIONS (CONTINUED)

2018 2017

Gross/Net distribution per unit (sen) Distribution on 29 December 2017 0.38 - Distribution on 30 January 2018 0.49 - Distribution on 28 February 2018 0.36 - Distribution on 30 March 2018 0.38 - Distribution on 30 April 2018 0.36 - Distribution on 31 May 2018 0.31 - Distribution on 29 June 2018 0.37 - Distribution on 31 July 2018 0.37 - Distribution on 30 August 2018 0.35 - Distribution on 28 September 2018 0.34 - Distribution on 31 October 2018 0.34 - Distribution on 30 November 2018 0.19 - Distribution on 30 December 2016 - 0.29

Distribution on 31 January 2017 - 0.30

Distribution on 28 February 2017 - 0.29

Distribution on 31 March 2017 - 0.29

Distribution on 28 April 2017 - 0.26

Distribution on 31 May 2017 - 0.30

Distribution on 30 June 2017 - 0.37

Distribution on 31 July 2017 - 0.36

Distribution on 30 August 2017 - 0.38

Distribution on 29 September 2017 - 0.36

Distribution on 31 October 2017 - 0.38

Distribution on 30 November 2017 - 0.43

4.24 4.01

Gross distribution is derived using total income less total expenses. Net distribution above is sourced from current financial year’s realised income. Gross distribution per unit is derived from gross realised income less expenses, divided by the number of units in circulation. Net distribution per unit is derived from gross realised income less expenses and taxation, divided by the number of units in circulation.

CIMB ISLAMIC MONEY MARKET FUND

38

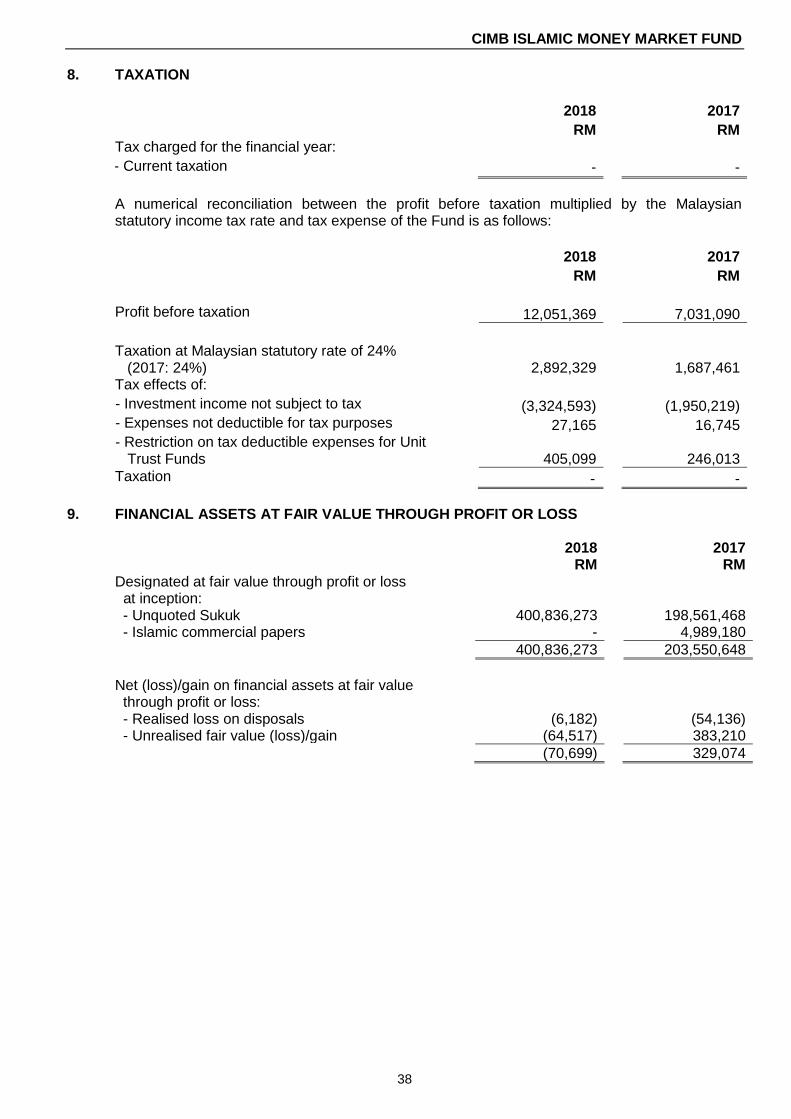

8. TAXATION

2018 2017

RM RM Tax charged for the financial year: - Current taxation - -

A numerical reconciliation between the profit before taxation multiplied by the Malaysian statutory income tax rate and tax expense of the Fund is as follows:

2018 2017

RM RM

Profit before taxation 12,051,369 7,031,090

Taxation at Malaysian statutory rate of 24% (2017: 24%) 2,892,329 1,687,461 Tax effects of:

- Investment income not subject to tax (3,324,593) (1,950,219) - Expenses not deductible for tax purposes 27,165 16,745 - Restriction on tax deductible expenses for Unit Trust Funds 405,099 246,013

Taxation - -

9. FINANCIAL ASSETS AT FAIR VALUE THROUGH PROFIT OR LOSS

2018 2017 RM RM Designated at fair value through profit or loss at inception: - Unquoted Sukuk 400,836,273 198,561,468 - Islamic commercial papers - 4,989,180

400,836,273 203,550,648

Net (loss)/gain on financial assets at fair value through profit or loss: - Realised loss on disposals (6,182) (54,136) - Unrealised fair value (loss)/gain (64,517) 383,210

(70,699) 329,074

CIMB ISLAMIC MONEY MARKET FUND

39

9. FINANCIAL ASSETS AT FAIR VALUE THROUGH PROFIT OR LOSS (CONTINUED)

Nominal Aggregate Market Percentage

Name of issuer value cost value of NAV

RM RM RM %

2018

UNQUOTED SUKUK

AmBank Islamic Bhd 5.05% 25/3/2024 (AA3)

10,000,000

10,121,209

10,120,667

1.75

Bandar Serai Development Sdn Bhd 4.62% 20/11/2019 (AA3)

10,000,000

10,045,735

10,044,858

1.74

Bumitama Agri Ltd 5.25% 18/03/2019 (AA3)

64,500,000

65,348,910

65,379,331 11.31

Celcom Networks Sdn Bhd 3.75% 29/08/2019 (AA+)

10,000,000

10,073,977

10,073,975

1.74

Encorp Systembilt Sdn Bhd 4.62% 18/11/2019 (AA1)

5,000,000

5,029,648

5,030,445

0.87

First Resources Ltd 4.35% 05/06/2020 (AA2)

10,000,000

10,210,521

10,210,421

1.77

Golden Assets International Finance Ltd 5.35% 05/08/2019 (A1)

15,000,000

15,282,257

15,312,590

2.65

Hong Leong Islamic Bank Bhd 4.80% 17/06/2024 (AA1)

5,000,000

5,118,179

5,125,758

0.89

Imtiaz Sukuk II Bhd 4.60% 22/03/2019 (AA2)

10,000,000

10,107,619

10,107,619

1.75

Jimah Energy Ventures Sdn Bhd 9.05% Due 11/12/2019 (AA3)

5,000,000

5,245,926

5,246,620

0.91

Jimah Energy Ventures Sdn Bhd 9.25% 12/11/2019 (AA3)

5,000,000

5,259,280

5,259,280

0.91

Malakoff Power Bhd 4.90% 17/12/2018 (AA-)

33,500,000

34,255,509

34,257,600

5.92

Malakoff Power Bhd 5.05% 17/12/2019 (AA-)

15,000,000

15,444,245

15,473,057

2.68

Maybank Islamic Bhd 4.75% 5/4/2019 (AA1)

10,000,000

10,088,559

10,094,974

1.75

MMC Corporation Bhd 5.20% 12/11/2020 (AA-)

3,000,000

3,021,778

3,021,051

0.52

Nur Power Sdn Bhd 4.20% 26/06/2019 (AAA)

5,000,000

5,094,084

5,095,304

0.88

Perbadanan Kemajuan Negeri Selangor 4.50% 03/12/2018 (AA3)

10,000,000

10,470,165

10,100,000

1.77

Projek Lebuhraya Usahasama Bhd 4.08% 11/01/2019 (AAA)

20,000,000

20,317,333

20,321,458

3.51

Public Islamic Bank Bhd 4.75% 07/06/2024 (AA1)

35,000,000

35,896,682

35,894,378

6.21

CIMB ISLAMIC MONEY MARKET FUND

40

9. FINANCIAL ASSETS AT FAIR VALUE THROUGH PROFIT OR LOSS (CONTINUED)

Nominal Aggregate Market Percentage

Name of issuer value cost value of NAV

RM RM RM %

2018 (CONTINUED) UNQUOTED SUKUK (CONTINUED)

RHB Islamic Bank Bhd 4.95% 15/05/2024 (AA3)

5,000,000

5,032,205

5,032,205

0.87

Tanjung Bin Power Sdn Bhd 4.54% 16/08/2019 (AA2)

20,000,000

20,303,023

20,319,981

3.51

Teknologi Tenaga Perlis 4.46% 31/07/2019 (AA1)

5,000,000

5,079,305

5,086,248

0.88

Teknologi Tenaga Perlis 4.51% 31/01/2020 (AA1)

5,000,000

5,091,541

5,093,190

0.88

UEM Edgenta Bhd 26/4/2019 (AA-)

10,000,000

9,823,445

9,828,840

1.70

UEM Sunrise Bhd 4.60% 13/12/2018 (AA-)

30,000,000

30,648,419

30,650,721

5.30

UEM Sunrise Bhd 4.72% 28/06/2019 (AA-)

25,000,000

25,549,540

25,543,596

4.42

UMW Holding Bhd 4.82% 04/10/2019 (AA2)

6,500,000

6,581,587

6,582,090

1.14

UniTapah Sdn Bhd 5.01% 12/06/2019 (AA1)

200,000

205,661

205,735

0.03

WCT Holding Bhd 4.80% 28/12/2018 (AA-)

6,000,000

6,123,623

6,124,280

1.06

TOTAL FINANCIAL ASSETS AT FAIR VALUE THROUGH PROFIT OR LOSS 393,700,000 400,844,962 400,836,273 69.32