cimbt 05

DESCRIPTION

CIMBT_2005 CIMB THAI BANK PCL Annual Report 2005TRANSCRIPT

1

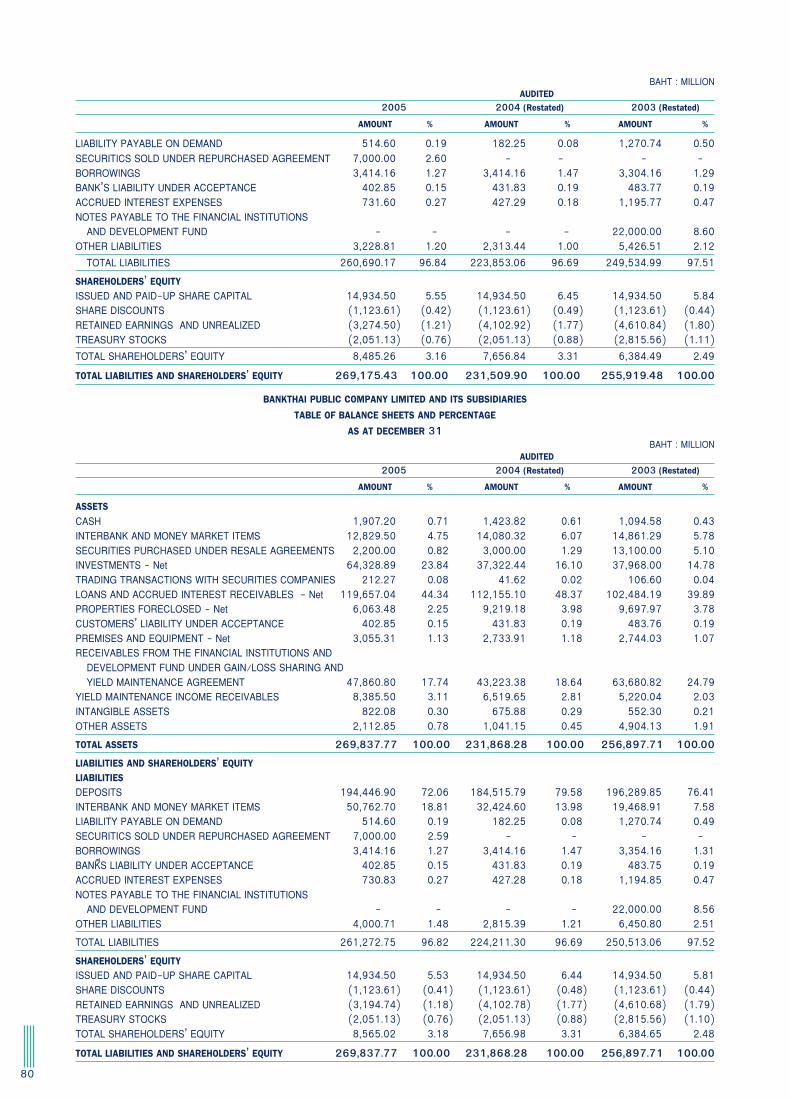

THE BANK’S SUMMARY OF FINANCIAL INFORMATIONBANKTHAI PUBLIC COMPANY LIMITED

(Million Baht)Consolidated The Bank only

At Year End 2005 2004 2003 2005 2004 2003

(Restated) (Restated) (Restated)

TOTAL ASSETS 269,838 231,868 256,870 269,175 231,510 255,919

Lendings (net) 119,657 112,155 102,484 119,219 111,535 101,393

Liabilities 261,273 224,211 250,513 260,690 223,853 249,535

Deposits 194,447 184,516 196,290 194,573 184,559 196,323

Shareholders’ equity 8,565 7,657 6,357 8,485 7,657 6,384

Total interest and dividend income 8,839 6,418 7,937 8,725 6,438 7,970

Total Income 10,420 8,105 9,532 9,925 7,642 8,942

Net earnings (losses) for the year 611 587 (3,936) 611 587 (3,936)

Basic earnings (losses) per share (Baht) 0.48 0.47 (3.22) 0.48 0.47 (3.22)

Book value (Baht) 6.96 6.37 5.99 6.96 6.37 6.01

RATIOS

Return on Assets (%) 0.24 0.24 (1.49) 0.24 0.24 (1.49)

Return on Equity (%) 7.53 8.38 (45.81) 7.57 8.36 (45.86)

Net Profit (%) 5.86 7.24 (41.29) 6.16 7.68 (44.01)

BIS Ratios (%) 8.56 10.99 14.19 8.56 10.99 14.19

Note : Restated financial Statements

22

MESSAGE FROM THE CHAIRMAN

After growing at a rate of 6.1 per cent in 2004, the economy of Thailand slowed to 4.5 per centin 2005. Notwithstanding the deceleration, the performance in 2005 was satisfactory consideringadverse developments that might have at first glance appeared to impinge negatively on the country.These range from the tsunami disaster that struck the coastal areas in the Andaman Sea in December2004 resulting in a sharp decline in the number of tourist arrivals, prolonged drought, second outbreakof avian influenza and persistent unrest in the three southernmost provinces. In addition, large increasein oil prices prompted the Government to abolish diesel subsidies, as consumer price index edged higher.Apart from this, positive contributions to economic growth came from the stable outlook for Thailand’smajor trading partners, a stimulus to exports, higher employment rates and a short-term economicstimulus package introduced by the Government.

A closer examination of economic growth in 2005 shows that an upward trajectory of retailoil prices particularly towards the end of the year sent inflation climbing from 2.7 per cent in 2004 to 4.5per cent in 2005. The trade balance deficit reached US$8,578 million as imports grew by 26.0 per cent,while exports slowed. As a result of these trends, the country’s current account deficit widened to US$3,714million. Notwithstanding this, Thailand’s total international reserves stood at a comfortable level ofUS$52,100 million.

In 2006, the political tension coupled with an upward trend in interest rates and oil prices will likelyhamper the growth prospects of Thailand, dampening private consumption as well as public and privateinvestment. Despite these factors, the stable outlook for Thailand’s major trading partners and the bilateralfree trade agreements between Thailand and various countries as well as the healthy revival of the tourismindustry will be the main growth drivers. Steadier oil prices will also contribute towards fostering economicstability while higher interest rates will help rein in inflation to the 3.5-5.0 per cent range.

I am pleased to say that BankThai succeeded in achieving its business goals in 2005. The annualoperating income totaled Baht 9,925.4 million, growing by Baht 2,283.4 million or 29.9 per centcompared to 2004, as a result of higher interest income and investment returns. Operating expensestotaled Baht 9,099.1 million, increasing by Baht 2,044.0 million or 29.0 per cent over 2004, due tohigher interest expenses on deposit accounts and borrowings as money market interest rates began to

3

move upwards. In addition to this, the Bank set aside provision for bad debt and doubtful accounts in theamount of Baht 215.0 million. As a result, the Bank registered a net profit of Baht 611.3 million, increasingfrom Baht 586.8 million in 2004.

A review of the Bank’s financial position shows that, as of 31 December 2005, the Bank’s totalassets amounted to Baht 269,175.4 million, increasing by 16.3 per cent compared with 2004. At thesame time, total net loans (less allowance for doubtful debts and interest receivables) stood at Baht114,842.8 million, growing by 8.2 per cent, while the total deposits (excluding interbank and moneymarket items) rose by 5.4 per cent to Baht 194,573.3 million.

During the year we continued to ensure that we operate with a growing commitment to goodcorporate governance which is a key ingredient for sustainable growth. Achievements of the Bank werereflected in recognition and awards such as Best Corporate Governance Report Awards from the SETAwards 2005. We constantly strive for improvements in all facets of our operation with a view to reinforcingour future competitiveness by expanding the range and reach of our products and services and deliveringlong-term value to our customers. To support and complement these efforts, the year saw the Bank’snetwork expanding to 112 branches across the country. Furthermore, the retail sales team and all thebranch offices are placing a new and tighter focus on strengthening the Bank’s retail activities. Continuedattention is given to upgrading the quality of our human resources which, in 2005, involved the commissionof a consultancy firm to conduct a special study directed at ensuring the overall effectiveness of theBank’s performance appraisal system. Other initiatives in train include organizing activities for customersand promoting public understanding of various issues of interest. This included, in 2005, the “Proud to beThai with BankThai Tour” and the “MBA World Forum”.

In 2006, the Bank intends to take a more aggressive approach to enhancing our ability to deliver auniversal banking platform to customers once the obligations related to the management of impaired assetsare fulfilled. We will remain committed to introducing changes to our organizational structure in such a waythat will enhance customer satisfaction, ensure the delivery of quality demand-driven products andservices, and address the changing needs of our growing customer base. Continued focus will be given tostrengthening our retail banking activities and expanding our outreach efforts by employing a variety ofchannels, including our business centres and branch offices.

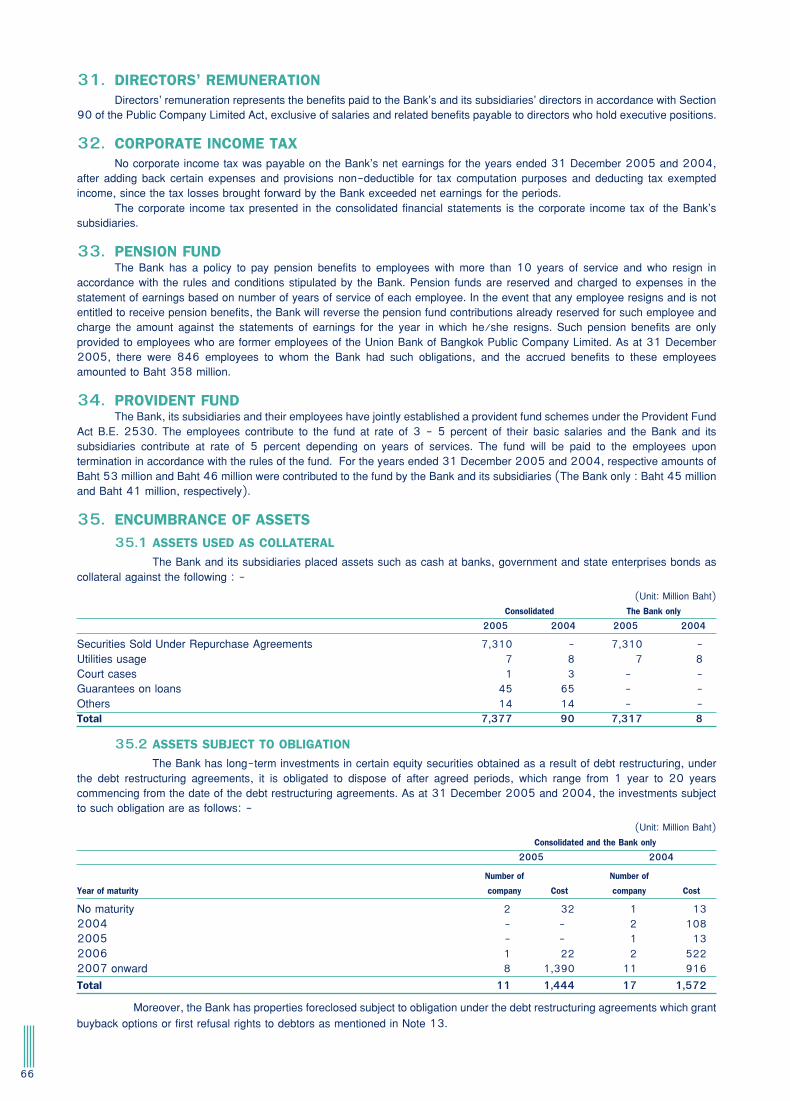

On behalf of the Board of Directors, I wish to record our gratitude to our customers andshareholders, Financial Institutions Development Fund (FIDF), Ministry of Finance, Bank of Thailand,other entities and financial institutions, both at home and abroad, for their continued patronage and supportduring the year. My thanks and appreciation are also due to our staff whose cooperation and dedicationhave contributed meaningfully to the achievement of our goals.

Last but not least, let me assure you that BankThai remains firmly committed to a path ofcontinual improvement as we strive to respond more effectively and efficiently to the needs of ourcustomers. Looking forward, it is my earnest hope that we will continue to enjoy the support andcooperation of our customers, shareholders, the competent authorities and financial institutions, whilebuilding on the dedication of our staff.

Tawee ButsunthornChairman of the Board of Directors

44

BOARD OF DIRECTORS

Mr. Tawee ButsuntornChairman

Mr. Pramon SutivongAdvisor to the Board Of Directors

Dr. Sarasin VirapholIndependent Director

Mr. Dharin DivariIndependent Director

Mr. Techapit SangsingkeoDirector

Mrs. Saowanee SuwannacheepDirector

5

Mr. Phirasilp SubhapholsiriPresident

Dr. Piboon LimprapatIndependent Director

Mr. Pongpanu SvetarundraDirector

Mr. Preecha OonchittiDirector

Mr. Luen KrisnakriDirector

Mr. Thaphop KleesuwanSecretary to the Board of Directors

66

MANAGEMENT COMMITTEE

Mr. Phirasilp SubhapholsiriPresident

Mr. Ekajai TivutanondSenior Executive Vice President

Mr. Surin PremamornkitSenior Executive Vice President

Mr. Phongsuree BunnagExecutive Vice President

Mr. Prasert WangrattanapraneeExecutive Vice President

7

Mrs. Duangphorn SucharittanuwatSenior Executive Vice President

Mr. Manit JeeraditSenior Executive Vice President

Mr. Surachai ChitratseneeSenior Executive Vice President

Mr. Chamnarn WangtalSenior Executive Vice President

Mr. Thaphop KleesuwanSecretary to the Management Committee

88

LIST OF EXECUTIVE OFFICERS

Corporate Banking Group 1Corporate Banking Division 1/1Mr. Chit ChittivaranonEVP. Corporate Banking Division

1/1 Head

Miss Chatsaral AnantakoolFVP. Corporate Banking

Mrs. Siriluch IntuluckVP. Corporate Banking

Mrs. Sananuch PramsanehVP. Corporate Banking

Corporate Banking Division 2/1Mr. Somkiat SethasompopeSVP. Corporate Banking Division

2/1 Head

Miss Sirintip TantiyanoneVP. Corporate Banking

Miss Wanida BuranasajjaVP. Corporate Banking

Mr. Suvat HiminkoolVP. Credit Analysis Section Head

Corporate Banking Division 3/1Mr. Kraisorn PongpunEVP. Corporate Banking Division

3/1 Head

Mrs. Wanida SupanantaroekSVP. Corporate Banking

Mr. Amorn ChulaluksananukulFVP. Corporate Banking

Mr. Chairerk ThongphasookVP. Corporate Banking

Mr. Kanachai WiwatwithayaVP. Corporate Banking

Mr. Boonrat ChuenurajitVP. Credit Analysis Section Head

Corporate Banking Division 4/1Mr. Wiwat VetayanukulEVP. Corporate Banking Division

4/1 Head

Mr. Takashi KusumotoEVP. Japanese Business

Development

Miss Ong-Orn PruthikositFVP. Corporate Banking

(Japanese BusinessDevelopment)

Miss Suteewan SirisawatFVP. Corporate Banking

Mr. Somchai ToemtrisnaFVP. Corporate Banking

Miss Oraphan PhanpairojVP. Corporate Banking

Mr. Somboon KasemsomboonchaiVP. Corporate Banking

Mrs. Supaporn KhuntawichitVP. Credit Analysis Section Head

Corporate Banking Division 5/1Mrs. Wirongrong SukyingEVP. Corporate Banking Division

5/1 Head

Miss Noppamas TamkaongarmFVP. Corporate Banking

Mr. Narong OngartmaneerutFVP. Corporate Banking

Mr. Hasadin ProthienVP. Corporate Banking

Mr. Watson ChansajchaVP. Corporate Banking

Mrs. Pornpilai BurasaiVP. Corporate Banking

Corporate Banking Group 2Corporate Banking Division 1/2Mr. Witchayarat UsuparatSVP. Corporate Banking Division

1/2 Head

Mr. Chamnan NgampojanavongSVP. Corporate Banking

Mr. Pornchai ShardweeFVP. Corporate Banking

Mrs. Orarach IsarangkoonNa Ayudhaya

VP. Corporate Banking

Mr. Wichien JongpanichkulthornVP. Corporate Banking

Mrs. Hathaikorn WichairatanaVP. Credit Analysis Section Head

Corporate Banking Division 2/2Mr. Suwat SummashipvitsavakulEVP. Corporate Banking Division

2/2 Head

Mr. Munin ThampornpipatFVP. Corporate Banking

Dr. Neramit PanchangkakulFVP. Corporate Banking

Mr. Weera PrushyapornsriVP. Corporate Banking

Mr. Vivat ChaijirapornVP. Corporate Banking

Mr. Chamroen AocharoenyingVP. Corporate Banking

Mr. Prasert SuparattanapinantVP. Corporate Banking

Corporate Banking Division 3/2Mr. Samchai BenchapathomrongEVP. Corporate Banking Division

3/2 Head

Mrs. Suchada Na BangchangFVP. Corporate Banking

Mr. Kusol SripaorayaVP. Corporate Banking

Mr. Samran UmasangthongkulVP. Corporate Banking

Mr. Sumrit NuntawadeepisarnVP. Corporate Banking

Corporate Banking Division 4/2Mr. Vorakan DhepchalermEVP. Corporate Banking Division

4/2 Head

Mr. Tara RatanaphiphobSVP. Corporate Banking

Mr. Vongpat BhuncharoenFVP. Corporate Banking

Miss Manussa LertdumrongluckVP. Corporate Banking

Mr. Sorasri SrisumaVP. Corporate Banking

Corporate Banking Division 5/2Mr. Wongkasem KarnthanatSVP. Corporate Banking Division

5/2 Head

Mr. Chalor TaerungreungFVP. Corporate Banking

Mr. Narongchai IndrasuksriVP. Corporate Banking

Mr. Sombat SunantapongsakVP. Corporate Banking

Mr. Sakchai WongchaisuriyaVP. Corporate Banking

Institutional Banking GroupTreasury & Trading DivisionMr. Sutee LosoponkulEVP. Treasury & Trading

Division Head

Treasury Sales DivisionMr. Padej PiroonsitEVP. Treasury Sales

Division Head

Capital Market and TradeDivisionMr. Chamnan WangtalSEVP. (Acting) Capital Market

and Trade Division Head

Structured Credit DivisionMr. Chaiwat MetevelungsunSVP. Structured Credit

Division Head

Privileged Banking DivisionMrs. Duangchai ValaisathienEVP. Privileged Banking

Division Head

International Business andInvestor Services DepartmentMrs. Boonyapak WanichpanSVP. International Business and

Investor Services DepartmentHead

Mrs. Mukda TechakasemVP. International Trade and

Foreign Remittance ServicesSection Head

Miss Srivipa TiradnakornVP. Branch Services

Development Section Head

Mrs. Orauma ShayyaVP. Investor Services Operations

Section Head

Treasury TeamMrs. Kanyaparnch BoonbandarnVP. Treasury Team Head

Mr. Thanyakhet VisavakulVP. Treasury

Trading TeamMiss Veeravan TantiprasutFVP. Trading Team Head

Mr. Apichat SuratanasurangVP. Trading

Mr. Wintu PanpanichVP. Trading

Mr. Sakul JirapanathornVP. Trading

9

Institutional Banking TeamMr. Prawat RakpatapeesuwanFVP. Institutional Banking

Team Head

Mrs. Saisamorn DuangmaneeFVP. Institutional Banking

Team Head

Treasury Product Developmentand Investment Analysis TeamMr. Thawatchai PrommapornVP. Treasury Product

Development andInvestment Analysis

Foreign Exchange Sales TeamMrs. Chalairat SorasuchartFVP. Foreign Exchange Sales

Team Head

Mrs. Kanda HarnprasitthadaVP. Foreign Exchange Sales

Mrs. Chalida PhatcharoenVP. Foreign Exchange Sales

Institutional & DerivativeSales TeamMr. Adisorn ChanpongVP. Institutional & Derivative

Sales Team Head

Miss Sarinthorn SureeVP. Institutional & Derivative

Sales

International Trade Sales TeamMrs. Rujiporn PromchaiVP. International Trade Sales

Team Head

Privileged Banking ProductDevelopment TeamMrs. Janchai AngsamapornFVP. Privileged Banking

Product Development TeamHead

Capital Market TeamMiss Sumalee Boon-A-NanCapital Market Team Head

Privileged Banking Team 1Miss Ladda Somjit

VP. Privileged BankingTeam 1 Head

Privileged Banking Team 2Mrs. Orawan PatimaprakornVP. Privileged Banking

Team 2 Head

Retail Banking GroupRetail Banking DivisionMr. Tada CharukitpaisarnEVP. Retail Banking

Division Head

Miss Amornrat HovatanapibulFVP. Unsecured Loans

Management Section Head

Mr. Wanchai RujipipatvongVP. Unsecured Loans

Management

Mr. Charlee RittimanomaiVP. Business Data Analysis

Miss Areeya PatarabunluaphobVP. Secured Loans Management

Section Head

Branch Services andOperations DivisionMr. Patom AmorndechawatEVP. Branch Services and

Operations Division Head

Retail Credit Operations andE-Banking DivisionMr. Nuekruk BaingernEVP. Retail Credit Operations

and E-Banking Division Head

Domestic Banking OperationsDepartmentMr. Chanin VeerawanFVP. Domestic Banking

Operations Department Head

Mr. Prasartporn LukkanakulVP. Domestic Bill Collection &

Cheque Operations SectionHead

Mr. Wiboon SuphanurakVP. Cash Control & Domestic

Remittance Services SectionHead

Mr. Virat AuppathumpsirikulVP. Branch Operations & A.T.M.

Support Section Head

Electronic Banking ServiceDepartmentMr. Tawich VirangkurSVP. Electronic Banking

Service Department Head

Miss Pimjai KijkongkhajornVP. Cash Management Product

Development Section Head

Mr. Pnickpong ChuntakettaVP. BTiBank & Phone Banking

Channel ManagementSection Head

Mr. Sittichai PrinyanusornVP. ATM & SST Channel

Management Section Head

Retail Credit Operations &Collection DepartmentMr. Surin PakavaleetornSVP. Retail Credit Operations &

Collection Department Head

Mr. Wipach PredawutVP. Retail Loans Operations

Section Head

Mrs. Chadarat PainVP. Retail Collection Section

Business Planning & AnalysisTeamMr. Sutee TantanaFVP. Business Planning &

AnalysisTeam Head

Retail Products ManagementTeamMrs. Pimonporn PoolnapolSVP. Retail Products

Management Team Head

Retail Deposit ManagementTeamMr. Parames PrombureeFVP. Retail Deposit Management

Team Head

Direct Sales Management TeamMr. Khomkit MaromFVP. Direct Sales Management

Team Head

Bangkok Metropolitan BranchManagement TeamMr. Chanon ChotevijitFVP. Bangkok Metropolitan

Branch Management TeamManager

Provincial Branch ManagementTeamMrs. Hathaitip HengtakulFVP. Provincial Branch

Management Team Manager

Branch Service TeamMr. Udomsak LehleakbhaiFVP. Branch Service Team Head

Retail Credit ApplicationProcessing TeamMrs. Kanyika sukhavatFVP. Retail Credit Application

Processing Team Head

Mrs. Jinida LakanathampichitVP. Secured Credit Application

Processing Section Head

Mrs. Juruayporn SuwanasakornVP. Unsecured Credit

Application Processing SectionHead

Fraud Control and InvestigationTeamMr. Wiroj MongkolmahalarpVP. Fraud Control and

Investigation Team Head

Business Support GroupTechnology DivisionPol. Capt. Danai KhaophaisarnEVP. Technology Division Head

Miss Prapaporn TungsaroteFVP. Technology Division

Legal DivisionMr. Paraadorn PhakaphatEVP. Legal Division Head

Asset Management DivisionMr. Songwud BuakhemEVP. Asset Management

Division Head

Technology DevelopmentDepartmentMiss Suree MongkolnchaiarunyaSVP. Technology Development

Department Head

Miss Yupa PipatkornkulFVP. Data Warehouse Section

Head

Mrs. Wilaiporn KasempannaraiVP. Deposit System Section

Head

Mr. Paiboon SiriprasertkulVP. Loans System Section Head

Mrs. Nattaya NipatkusolkitVP. Information System Section

Head

Miss Suwanna NimitsurachartVP. Trade Finance & Treasury

System Section Head

Mr. Prathuang YammontaVP. Delivery Channels System

Section Head

Technology ProductionsDepartmentMr. Paiboon SirichuchninFVP. Technology Productions

Department Head

Mr. Weerarat RatanamungmekarVP. IT Support and Helpdesk

Section Head

Mr. Bundit SirisathienVP. Network Communications

and Security System SectionHead

10

Mr. Chanchai NouyenpolVP. Operating System and

Database DevelopmentSection Head

Mr. Tawee RatanawilaiwanVP. Data Center Operations

Section Head

Credit Operations DepartmentMr. Thiti SupamaneeSVP. Credit Operations

Department Head

Mr. Chookiat YongsomboonVP. Non-Revolving Credit &

Contingent Liability SectionHead

Miss Sutasinee ChuennaitumVP. Revolving Credit,

Restructured Loans & DebtCollections Section Head

Network and OfficeManagement DepartmentMr. Somkeart SrisuwanSVP. Network and Office

Management Department Head

Mr. Manoon TumsanVP. Office Administration

Section Head

Mr. Tanoo WongthanyakornVP. General Administration

Section Head

Mrs. Benjawan SidhibhlakornVP. Branch Network

Section Head

Credit AdministrationDepartmentMr. Suchart ChandsongsangSVP. Credit Administration

Department Head

Mrs. Bulan NitsayanFVP. Credit Facility Contract

Section Head

Mr. Somchai SanaephanVP. Mortgage Registration

Section

Mr. Sanya KichpechrVP. Collateral Appraisal Section

Project Management OfficeMr. Prachawan PraimaneeFVP. Project Management

Office Head

Mr. Padet ChumasaratulVP. Project Coordination and

Application ChangeManagement Section 1 Head

Miss Krittika ChansityanonVP. Project Management

Section 1 Head

Mr. Angkul PaleewongseVP. Project Management

Section 2 Head

Information Security TeamMr. Krisda SribunnakFVP. Information Security

Team Head

Metropolitan Case MonitoringTeamMiss Suvimon PhoponvattanakornVP. Metropolitan Case

Monitoring Team Head

Provincial Case Monitoring TeamMr. Sayan AngsusinghaVP. Provincial Case Monitoring

Team Head

Legal Execution TeamMr. Pongdej WongpoomFVP. Legal Execution Team

Head

Mr. Chalong ViseshomVP. Legal Execution Section 1

Head

Mrs. Vimolrat PattichartVP. Legal Execution Section 2

Head

Miss Rapeeporn VanasantVP. Legal Execution Section 3

Head

Legal Consultant TeamMr. Kitti NetprasatVP. Legal Consultant

Miss Panita ChaowpetVP. Legal Consultant

Non-Performing LoanManagement TeamMr. Boripat KulchartchaiSVP. Non-Performing Loan

Management Team Head

Mr. Sonthit ChukateFVP. Non-Performing Loan

Management Team Head

Mr. Chalermpol DecharitFVP. Non-Performing Loan

Management Team Head

Mr. Suchart TanakulrungsonFVP. Non-Performing Loan

Management Team Head

Mr. Sathien KasettratadFVP. Non-Performing Loan

Management Team Head

Mr. Suwat K.SrisuwanFVP. Non-Performing Loan

Management Team Head

Mr. Sarnanda LekhyanandaFVP. Non-Perfroming Loan

Management Team Head

Mrs. Krongkarn PichayakulVP. Debt Restructuring

Miss Siriluck WongthaiVP. Debt Restructuring

Mrs.Chanyakorn ApiratanapimolchaiVP. Debt Restructuring

Mr. Teerarat NgampatipatpongVP. Debt Restructuring

Non-Performing Assets SalesTeamMr. Thaphop KleesuwanSVP. (Acting) Non-Performing

Assets Sales Team Head

Mr. Arnon LimmongkolVP. Investment

Mrs. Saovanee SiriveshvaravudhVP. Administration

Risk Management and StaffCredit GroupMrs. Panute Na ChiangmaiEVP. Risk Management and

Staff Credit Deputy Group Head

Mr. Somsak ChaiyadejSVP. Risk Management Division

Head

Mr. Anuchat PrakartchaiVP. Credit Risk Portfolio

Management

Market Risk Management TeamMr. Ekachai LokcharoenlarbFVP. Market Risk Management

Team Head

Mrs. Suchada NukornnavaratVP. Market Risk Management

Mr. Narest SatityapongVP. Liquidity Risk Management

Operational Risk ManagementTeamMr. Tawat JitkraisornVP. Operational Risk

Management Team Head

Mrs. Tippawan SrikaewVP. Risk Information

Management

Staff Credit TeamMr. Somchai VongpiyasatitSVP. Staff Credit Team Head

Miss Siriporn SirisinghaFVP. Staff Credit

Mr. Voraphong PattanapibulVP. Staff Credit

Credit Policy TeamMrs. Kampoo VisuthipholFVP. Credit Policy Team Head

Miss Marayat SawetkitithamVP. Credit Policy

Miss Supalak SasalaksananonVP. Credit Policy

Credit Committee SecretaryTeamMr. Damrong BoonmalisonVP. Credit Committee SecretaryTeam Head

Research OfficeMr. Aongarj DivahutaVP. Industry Research &

Corporate Analysis SectionHead

Financial Control DivisionMr. Prasert WangrattanapraneeEVP. Financial Control Division

Head

Financial Accounting andBudgeting DepartmentMiss Pensri PhabhapoteFVP. Financial Accounting and

Budgeting Department Head

Mrs. Vilaiwan TiasiriVP. Assets, Liabilities

Accounting Control SectionHead

Miss Ratana VatanapukdeeVP. Budgeting and Finance

Management Section Head

Management Accounting andInformation DepartmentMr. Kamol RuangmanamongkolFVP. Management Accounting

and Information DepartmentHead

Miss Rattana BenjatachahVP. Management Accounting

Section Head

Mr. Wacharapong SujaridchaiVP. Management Information

Section Head

Mrs. Napaporn PrapapunsiriVP. Data Warehouse Section

Head

11

SOP Management and InternalControl TeamMr. Chaikajohn ThampratheepFVP. SOP Management and

Internal Control Team Head

Tax Management TeamMiss Kanlaya AnochaFVP. Tax Management Team

Head

Finance Core Banking TeamMrs. Teeraporn RatanopasVP. Finance Core Banking Team

Head

Corporate Affairs DivisionOffice of the PresidentMr. Thaphop KleesuwanSVP. Office of the President

Head

Public Relations OfficeMrs. Thapthim SinghaseniSVP. Public Relations Office

Head

Planning OfficeMiss Uthaiwan AnuchitanukulFVP. Planning Office Head

Human Resources ManagementDivisionMr. Phongsuree BunnagEVP. Human Resources

Management Division Head

BUHR Team - Business GroupMr. Pachurn SubhasatienpongFVP. BUHR Team Head -

Business Group

Mr. Suthichai VongrachitVP. BUHR - Business Group

BUHR Team - Operations &Support GroupMrs. Nuntawan SudsatayaFVP. BUHR Team Head -

Operations & Support Group

Mrs. Maliwan WongphoomVP. BUHR - Operations &

Support Group

Human Resources DevelopmentTeamMiss Metta AngtrakoonFVP. Human Resources

Development Team Head

Miss Phailin KomalamisraVP. Human Resources

Development Section Head -Operations & Support Group

Employee Relations TeamMr. Saroj KijjanontFVP. Employee Relations Team

Head

Mr. Sakda PhoomphanVP. Employee Relations

HR Tools Development TeamMrs. Phanit WongphaetFVP. HR Tools Development

Team Head

Internal Audit DepartmentMr. Suthanai PrasertsanSVP. Internal Audit Department

Head

Mrs. Malini ApiwatananontFVP. Internal Audit Section Head

Mrs. Yuphadee IntharakasetVP. Head Office Audit Unit Head

Mr. Somkiat JitvutthichodVP. Credit Audit Unit Head

Mr. Santiporn WongpanchalertVP. Subsidiaries Audit Unit Head

Mr. Boonkiat EkwanichVP. Information Technology and

Risk Management SystemAudit Section Head

Mrs. Nantiya MesookVP. Risk Management System

Audit Unit Head

Compliance and Credit ReviewTeam

Mr. Pattanasak ChermchansophonFVP. Compliance and Credit

Review Team Head

Miss Dussadee PhothongVP. Credit Review Section Head

Mr. Parkpoom BunchasakVP. Compliance Section Head

Business CenterCorporate Banking Group 1Business Center - SathonMr. Pakorn PrechapornManager

Business Center - ChonburiMr. Preecha KaroonvattanaManager

Business Center - LadpraoMrs. Laval SinghamanyManager

Business Center - JawaradMr. Parkpoom HemarakshaManager

Business Center - RajadamnernMr. Suriyon ManawapatManager

Business Center - YannawaMr. Sunk SapphansaenManager

Business Center - Bangna-TradMr. Passapol SirikulbodeeManager

Business Center - BangnaMr. Kraiwut DoltadaManager

Business Center - New PhetburiMr. Chaowalert PunjawasaruchManager

Business Center - HueykwangMr. Sakolpat WongchartluangManager

Business CenterCorporate Banking Group 2Business Center - BangbonMiss Kandate KanchanomaiManager

Business Center - NongkhaemMr. Chaiyan ArunrungsawatManager

Business Center - RangsitMr. Bunjhob SiriratanakumwongManager

Business Center - NgamwongwanMr. Suphavich DeewongphaibulManager

Business Center -CharansnitwongseMr. Wittaya NuntankkomManager

Business Center - SamutsakornMrs. Duangporn WiwattanawarangManager

Business Center - SuratthaniMr. Cheerapat PrawatManager

Business Center - HatyaiMr. Thongchai WassanarungruengsukManager

Business Center - PhuketMr. Songwuth ThephabutrManager

Business Center - PhetburiMr. Pradit LimsawatManager

Business Center - Chiang MaiMr. Sakchai WongchaisuriyaManager

Business Center - NakhonsawanMr. Somphop PhuangphongManager

Business Center - KhonkaenMr. Uthai HomwantaManager

Business Center - Nakhon RatchasimaMr. Thanadej KanokyurapanManager

Business Center - Ubon RatchathaniMr. Veerachai PuranasuthemmongkolManager

Business Center - Pra KakhonSi AyutthayaMr. Anugul PhinijnaiManager

1212

MANAGEMENT’S DISCUSSION AND ANALYSISOF THE YEAR’S RESULTS

1. RESULTS OF OPERATIONOVERVIEW OF RESULTSFor the year ended 31 December 2005, the Bank reported a net profit of Baht 611 million or Baht 0.48 per share, compared

with a net profit of Baht 587 million or Baht 0.47 per share in 2004. The Bank attributed this increase to the growth in lending,debt investments, leaseholds and finance leases, as well as higher yield maintenance income.

(a) A SUMMARY OF THE BANK’S INCOMEAs reflected in the consolidated financial statements as at 31 December 2005, the Bank’s income amounted to Baht

10,420 million, increasing by Baht 2,316 million or 28.57 per cent over the comparable figure of the previous year. Meanwhile,the Bank-only financial statements showed that as at 31 December 2005, the Bank’s income stood at Baht 9,925 million,growing by Baht 2,283 million or 29.88 per cent compared with 2004. The particulars are as follows:

The Bank’s income consists principally of interest and dividend income (including the yields generated under theGain/Loss Sharing and Yield Maintenance Agreement), as well as non-interest income. In accordance with the consolidatedfinancial statements as at 31 December 2005, interest and dividend income accounted for 84.83 per cent of the Bank’s totalincome. Specifically, for the years 2005 and 2004, the Bank’s interest and dividend income amounted to Baht 8,839 million andBaht 6,419 million respectively. As a result, the Bank’s interest and dividend income increased by Baht 2,421 million or 37.72per cent in 2005 compared with the previous year.

The Bank-only financial statements showed that for the year ended 31 December 2005, interest and dividend incomerepresented 87.90 per cent of the total income. Specifically, for the years 2005 and 2004, the Bank’s interest and dividendincome amounted to Baht 8,725 million and Baht 6,438 million respectively. As a result, in 2005, the Bank posted an increasein interest and dividend income at Baht 2,287 million or 35.52 per cent compared with a year earlier.

In the consolidated financial statements, the Bank’s non-interest income for the year ended 31 December 2005accounted for 15.17 per cent of the total income. Specifically, for the years 2005 and 2004, the Bank’s non-interest incomeamounted to Baht 1,581 million and Baht 1,686 million respectively. As a result, the Bank’s non-interest income decreased byBaht 105 million or 6.24 per cent from the corresponding period one year earlier, due to a decline in profit from currencyexchange transactions.

The Bank-only financial statements showed that for the year ended 31 December 2005, the Bank’s non-interest incomerepresented 12.10 per cent of the total income. Specifically, for the years 2005 and 2004, the Bank’s non-interest incomeamounted to Baht 1,201 million and Baht 1,204 million respectively. This reflected a drop in non-interest income of Baht3 million or 0.26 per cent in 2005 compared with 2004.

(b) SUMMARY OF CAPITAL FUNDS AND OPERATING EXPENSESIn the consolidated financial statements, the Bank’s capital funds and operating expenses (incorporating loss and doubtful

loans, corporate income tax and minority interests) as at 31 December 2005 amounted to Baht 9,809 million, increasing byBaht 2,291 million or 30.48 per cent over a year earlier. By the same token, the Bank-only financial statements showed that,in 2005, the Bank’s capital funds and operating expenses stood at Baht 9,314 million, growing by Baht 2,259 million or 32.02per cent compared with 2004. The particulars are as follows:

The Bank’s capital funds structure and operating expenses (incorporating loss and doubtful loans, corporate income taxand minorty interests) comprise both interest and non-interest expenses, with interest expenses representing the largest share.In the consolidated financial statements for the year ended 31 December 2005, the Bank’s interest expenses accounted for51.20 per cent of the total expenses. Specifically, for the years 2005 and 2004, the Bank’s interest expenses amounted to Baht5,022 million and Baht 3,744 million respectively. As a result, the Bank’s interest expenses grew by Baht 1,278 million or34.15 per cent in 2005, as a result of an increase in interest-bearing deposits and borrowings.

The Bank-only financial statements showed that for the year ended 31 December 2005, the Bank’s interest expensesaccounted for 53.91 per cent of the total expenses. Specifically, for the years 2005 and 2004, the Bank’s interest expensestotaled Baht 5,022 million and Baht 3,745 million respectively. As a result, the Bank reported an increase of Baht 1,277 millionor 34.09 per cent in interest expenses in 2005 compared with a year earlier.

In the consolidated financial statements, the Bank’s non-interest expenses (incorporating loss and doubtful loans,corporate income tax and minority interests) as at 31 December 2005 accounted for 48.80 per cent of the total expenses.Specifically, for the years 2005 and 2004, the Bank’s non-interest expenses amounted to Baht 4,787 million and Baht 3,774million respectively. As a result, the Bank posted an increase of Baht 1,013 million or 26.84 per cent in 2005 compared withthe corresponding period a year earlier due to an increase in lending and the expanded scope of related services, as well asloan-loss provisioning.

The Bank-only financial statements showed that for the year ended 31 December 2005, the Bank’s non-interestexpenses (incorporating loss and doubtful loans, corporate income tax and minority interests) represented 46.09 per cent of thetotal expenses. Specifically, for the years 2005 and 2004, the Bank’s non-interest expenses amounted to Baht 4,292 millionand Baht 3,310 million respectively. As a result, the Bank posted an increase of Baht 982 million or 29.67 per cent in 2005compared with the corresponding period a year earlier.

13

(c) NET PROFIT (LOSS)

The Bank’s audited operating results showed that for the years ended 31 December 2005 and 2004, the Bank’s netoperating profit amounted to Baht 611 million and Baht 587 million respectively. The growth in net profit in 2005 mainly stemmedfrom an increase in lending, debt investments, hire purchase and financial lease contracts, while an increase in capital fundsresulted from deposits, borrowings, loan-loss provisioning and expenses incurred in extending the range of lending products andservices.

(d) RATE OF RETURNS TO SHAREHOLDERS

In 2005, the Bank did not make any dividend payments due to its previous accumulated loss. In accordance with thePublic Company Limited Act B.E. 2535 (AD 1992) and the Bank Charter, dividend distribution depends primarily on the Bank’soverall profitability without accumulating any losses. Furthermore, the Bank of Thailand requires the Bank to write off all worthlessor irrecoverable assets from the accounts before paying dividends. For the year ended 31 December 2005, the Bank registeredsome operating profit but posted accumulated loss of Baht 2,849 million.

2. THE BANK’S FINANCIAL POSITIONASSETSThe Bank’s business profitability depends primarily on its interest-earning assets, principally loans (loans and interest

receivables), interbank and money market items, investments and securities purchased under resale agreements.According to the Bank-only financial statements as at 31 December 2005, the Bank’s loans increased by Baht 7,400 million

or 5.69 per cent to Baht 137,449 million, while interbank and money market items declined by Baht 1,403 million or 9.93per cent to Baht 12,726 million. At the same time, the Bank’s securities purchased under resale agreements decreased byBaht 800 million or 26.67 per cent to Baht 2,200 million, while investments grew by Baht 27,499 million or 72.98 per cent toBaht 65,179 million. As a result, the Bank’s total assets amounted to Baht 269,175 million, increasing by Baht 37,666 millionor 16.27 per cent.

The consolidated financial statements showed that, as at 31 December 2005, the Bank’s loans increased by Baht7,185 million or 5.40 per cent to Baht 140,167 million. At the same time, interbank and money market items declined by Baht1,251 million or 8.88 per cent to Baht 12,829 million, while securities purchased under resale agreements dropped by Baht800 million or 26.67 per cent to Baht 2,200 million, and investments increased by Baht 27,006 million or 72.36 per cent toBaht 64,329 million. As a result, the Bank’s total assets amounted to Baht 269,838 million, increasing by Baht 37,969 millionor 16.38 per cent.

ASSET QUALITY

(a) LOANSCONCENTRATION OF LOANS

As at 31 December 2005, top beneficiaries of the Bank’s loans were from the sectors of manufacturing with a 30.19per cent share of the total portfolio, followed by commercial business, 18.98 per cent, and real estate, 18.27 per cent. In thisrespect, loans extended to the manufacturing sector amounted to Baht 41,788 million, increasing by Baht 3,547 million or 9.28per cent compared with the corresponding period a year earlier. Loans extended to commercial business totaled Baht26,271, declining by Baht 1,479 million or 5.33 per cent, followed by real estate at Baht 25,292 million, dropping by Baht 281million or 1.10 per cent compared with the corresponding period a year earlier.

In pursuance of its lending policy, the Bank continues its commitment to distribute loans among diverse sectors with a viewto avoiding over-concentration and emphasizing lending to priority economic sectors with good growth trends and potential,particularly large, medium, small and retail enterprises.

The majority of loans carried maturities of more than one year, accounting for Baht 100,068 million or 72.28 per cent ofthe total portfolio, of which loans exceeding Baht 10 million accounted for Baht 117,415 or 84.82 per cent.

(b) OUTSTANDING LOANS

As at 31 December 2005, the Bank’s outstanding loans (excluding accrued interest receivable, including loans tocommercial banks) amounted to Baht 138,436 million. Of this, loans to juristic persons accounted for Baht 113,279 million or81.83 per cent of the outstanding portfolio, while personal loans represented Baht 26,157 million or 18.17 per cent.

As at 31 December 2005, loans extended to the top ten borrowers represented Baht 11,248 million or 8.13 per centof the outstanding portfolio, with none of them accounting for more than 10 per cent. This has contributed towards limiting theBank’s exposure to credit risk as no one borrower could have a major effect on the Bank’s financial position in the event of default.

(c) CLASSIFICATION OF ASSETS

As at 31 December 2005, the Bank’s classified assets (including accrued interest receivable, excluding financialinstitutions) amounted to Baht 141,825 million, of which loan-loss provisions accounted for Baht 22,425 million. As a result,the Bank-only financial statements showed that, as at 31 December 2005, the ratio of the Bank’s loan-loss provisions (includingaccrued interest receivable, excluding financial institutions) accounted for 15.81 per cent compared with 17.48 per cent in 2004.By the same token, according to the consolidated financial statements as at 31 December 2005, the ratio of the Bank’s loan-lossprovisions (including accrued interest receivable, excluding financial institutions) accounted for 17.14 per cent compared with18.81 per cent in 2004.

14

As at 31 December 2005, the Bank’s substandard loans collectively classified as Non-Covered Assets Pool (NON CAP)amounted to Baht 91,614 million, including accrued interest receivable, excluding financial institutions. In this respect, the Bankset aside Baht 4,701 million in loan-loss provisions as required by the Bank of Thailand. At the same time, substandard loanscollectively classified as Covered Assets Pool (CAP), including accrued interest receivable, excluding financial institutions,accounted for Baht 50,211 million while loan-loss provisions amounted to Baht 17,724 million. The particulars are presentedin the table below.

Loans and accrued Loan valuation after Provisioning rate Book valueinterest receivable deduction of security on the basis of BOT’s (millions(millions of baht) (millions of baht) requirement (per cent) of baht)

Non-Covered Assets Pool (NON CAP):Classified as passed 83,130 37,097 1 357Classified as special mention 1,063 350 2 7Classified as substandard 803 273 20 240Classified as doubtful 1,745 779 50 592Classified as loss 4,873 2,699 100 3,112

Total 91,614 41,198 4,308General allowance for potentially irrecoverable loans 393

Loan-loss provisions for NON CAP 4,701Loans classified as CAP (1) 50,211 37,282 17,724

Total 141,825 78,480 22,425(1) Such loans did not call for any classification or additional provisions for loss, as they fell within the scope of the Gain/Loss Sharing and Yield

Maintenance Agreement.

In order to effectively monitor and control debt service payments by customers, the Bank maintains a database of debtinformation which is updated at the end of every month. The database records payment schedules and can be used to retrieveinformation on debt-service obligations. In this connection, delinquent loans are grouped under four main categories, namely:(a) 1-3 months past due; (b) 3-6 months past due; (c) 6-12 months past due; and (d) more than 12 months past due. Thedatabase also provides a tool for classifying loans and predicting trends in NPLs.

(d) NON-PERFORMING LOANS (SUBSTANDARD LOANS)

As at 31 December 2005, the Bank’s non-performing loans collectively classified as NON-CAP accounted for Baht7,011 million or 5.06 per cent of outstanding portfolio (comprising the principal plus financial institutions). The classificationembodied in the Bank of Thailand’s notification of 16 January 2003 defines non-performing loans as substandard, doubtful andloss, and includes doubtful loans that have been written off then transferred back to the account.

(e) CRITERIA FOR RECOGNIZING REVENUEINTEREST AND DISCOUNT ON LOANSRevenue recognized as having been earned consists principally of accrual basis revenue based on the outstanding

principal amount. With respect to defaulted loan which payment of principal or interest is more than three months in arrears,interest is not recorded as income on an accrual basis but on a cash basis. In pursuance of the directive of the Bank of Thailand,interest accruing on such defaulted loan and reported as income is transferred out of the account.

Interest on restructured loans is also recognised on an accrual basis except when the loan has yet to comply with therestructuring requirements. In this respect, interest is recorded as income on a cash basis until compliance has been demonstratedfor at least three consecutive months or by three consecutive installments, whichever is longer.

LIABILITIES AND SHAREHOLDERS’ EQUITYIn the Bank-only financial statements, the Bank’s liabilities as at 31 December 2005 amounted to Baht 260,690 million,

increasing by Baht 36,837 million or 16.46 per cent over the corresponding period a year earlier. Meanwhile, the consolidatedfinancial statements showed that, as at 31 December 2005, the Bank’s liabilities stood at Baht 261,273 million, growing by Baht37,061 million or 16.53 per cent.

As reflected in the Bank-only financial statements, shareholders’ equity as at 31 December 2005 amounted to Baht8,485 million, growing by Baht 828 million or 10.82 per cent compared with 2004. This was attributable to an increase in netprofit of Baht 611 million as well as higher gain on revaluation of securities of Baht 217 million. At the same time, in theconsolidated financial statements, shareholders’ equity stood at Baht 8,565 million, increasing by Baht 908 million or 11.86per cent compared with 2004.

The consolidated financial statements and the Bank-only financial statements both showed that, as at 31 December2005, the Bank’s off-balance-sheet commitments totaled Baht 349,759 million, increasing by Baht 217,630 million or 164.71per cent over the corresponding period a year earlier, as a result of an increase in derivatives activities.

15

3. LIQUIDITYAs presented in the consolidated as well as the Bank-only financial statements, the Bank’s cash flow for the year 2005 was

as follows:The Bank’s net cash flow received from (or expended for) its operations amounted to Baht 26,677 million and Baht 27,142

million, increasing by Baht 27,578 million and Baht 27,410 million respectively compared with 2004, as a result of an increasein deposits.

Similarly, the Bank’s net cash flow received from (or expended for) its investment activities totaled Baht (26,093) million andBaht (26,660) million respectively, growing by Baht 26,610 million and Baht 27,148 million compared with 2004, due to anincrease in investment securities.

At the same time, the Bank’s net cash flow received from (or expended for) its fund-raising activities amounted to Baht (100)million and Baht (0) million respectively, declining by Baht 815 million and Baht 110 million compared with 2004.

Against that background, the difference between the Bank’s net cash flow received from (or expended for) its operations andthe net cash flow received from (or expended for) its fund-raising activities and investment securities did not have any materialimpact on the Bank’s cash-in-hand and liquidity situation at the end of the accounting period. As a result, the Bank was able tomeet the minimum requirement prescribed by the Bank of Thailand.

RELATIONSHIP BETWEEN SOURCES AND USES OF FUNDSThe Bank derives its funds from two major sources, namely deposits and borrowings while credits make up the bulk of the

Bank’s expenditure. As at 31 December 2005, the Bank’s deposits totaled Baht 1,108 million, its borrowings, Baht 24,390million, and its credit, Baht 135,251 million. This may be divided into maturity periods as presented in the table below.

(millions of baht)Maturity Period Credit a/ % Deposits a/ % Borrowings a/ %

Payment demanded - - 51,501 24.85 7,748 18.64Up to one year 38,368 27.72 145,296 70.11 28,357 68.21Greater than one year 100,068 72.28 10,440 5.04 5,470 13.15Total 138,436 100.00 207,237 100.00 41,575 100.00a/ Including interbank and money market items.

A closer look at the above table reveals a mismatch between the Bank’s sources and uses of funds. This was primarily dueto the action taken by the Bank from end-2001 to end-2005 to transfer impaired assets in the amount of Baht 98,126 millionto the Thai Asset Management Corporation (TAMC). In this respect, the Thai Asset Management Corporation Decree B.E. 2544(AD 2001) requires all financial institutions to transfer impaired assets as well as any other rights over the property being held ascollateral for debt repayments with respect to such impaired assets to the TAMC within the prescribed conditions and time-limit.Notwithstanding this, the Bank was able to achieve higher growth in lending and debt investments which contributed towardsgenerating revenue and, at the same time, minimizing the mismatch between sources and uses of funds.

The Bank derives its funds from customer deposits which may be categorized as follows:(millions of baht)

2005 2004 2003

Categories of Deposit Amount % Amount % Amount %Current and savings deposits 51,501 24.85 57,686 29.42 45,158 22.06Long-term deposits 155,737 75.15 138,422 70.58 159,506 77.94Total 207,238 100.00 196,108 100.00 204,664 100.00

Over the past three years, efforts have been exerted by the Bank to reduce deposit expense by lessening the share oflong-term deposits and increasing the share of current and savings deposits.

MAINTENANCE RATIOSCAPITAL TO RISK ASSETS RATIOAs at 31 December 2005, the Bank’s capital to risk assets ratio amounted to 8.56 per cent, declining by 10.99 per cent from

2004. Notwithstanding this, the Bank was able to satisfy the regulatory minimum set by the Bank of Thailand at 8.5 per cent.

LIQUID ASSETS RATIOThe Bank of Thailand requires all commercial banks to maintain the minimum liquid assets ratio at not less than 6 per cent of

total deposits and offshore borrowings with less than one-year maturity. At end-2005, the Bank’s total liquid assets amountedto Baht 25,034 million while its loan-to-deposit ratio stood at 66.80 per cent. At the same time, the ratio of liquid assets to totalassets amounted to 9.30 per cent while the ratio of liquid assets to total deposits stood at 11.37 per cent, thereby satisfying theregulatory minimum.

INVESTMENT COSTIn 2005, the Bank invested 18,010,000 million shares from BT WorldLease Co. Ltd. at a total cost of Baht 247,637,500.

The acquisition of 75 per cent of the issued and paid-up share capital of BT WorldLease converted the Company into one of theBank’s subsidiary companies. In addition, the Bank invested 2,499,993 ordinary shares at Baht 10 par each from Sathorn AssetManagement Co. Ltd., thereby acquiring 100 per cent of the Company’s issued and paid-up share capital. This policy measuremarked an important milestone in consolidating the Bank’s presence in the asset management market. Besides those alreadymentioned, the Bank has no further plans or policy measures aimed at increasing investment. Instead, the Bank will continue todirect its efforts towards converting debt into equity through the restructuring process.

16

SOURCES OF CAPITALCapital structureThe Bank’s capital structure consists of 83.29 per cent deposits and 16.71 per cent borrowings as well as domestic and

foreign bonds.

THAILAND’S ECONOMIC CONDITIONS AND OUTLOOKOVERVIEW

After growing at a rate of 6.1 per cent in 2004, the economy of Thailand slowed to 4.5 per cent in 2005. At least four factorscontributed to the slowdown. The tsunami disaster that struck six southern provinces in December 2004 resulting in tourismslump, persistent unrest in the three southernmost provinces, recurrent outbreak of avian influenza, and prolonged drought.External factors contributing to the downturn included steeply rising oil prices which subsequently prompted the Government toabolish diesel subsidies. However, the stable outlook for Thailand’s major trading partners combined with a stimulus to exportsenabled export growth to gather some momentum. In addition to this, an economic stimulus package was introduced by theGovernment to mitigate the adverse impact on growth.

A closer examination of economic growth in 2005 shows that an upward trajectory of oil prices nudged inflation up from 2.8per cent in 2004 to 4.5 per cent in 2005. Imports grew at a relatively high rate while exports slowed. As a result of these trends,the country’s trade deficit widened and the current account turned negative following several years of positive balance.

PRIVATE CONSUMPTION GROWTHGrowth in private consumption tapered off slightly from 5.9 per cent in 2004 to 4.6 per cent in 2005, as the prices of certain

consumer goods and services edged higher due to an upward trend in oil prices and interest rates, particularly towards the end ofthe year, in combination with household debt burdens. Notwithstanding this, private consumption growth has been sustained bythree broad factors: higher employment, an increase in farm income and a short-term economic stimulus package introduced bythe Government.

INVESTMENTIn 2005, investment slowed in tandem with weakening business confidence and a drastic increase in investment costs.

Despite the slowdown, growth in public and private investment was held at 10.8 per cent compared with 13.8 per cent in 2004,primarily as a result of high capacity utilization particularly in certain industries, leading to production growth. Other contributoryfactors included continued expansion of the Thai economy and growth in public investment, resulting from the expedited release ofbudgetary allocations to stimulate the economy.

EXTERNAL SECTORIn 2005, Thailand’s trade deficit widened to US$8,578 million compared with a trade surplus of US$1,460 million in 2004.

As a result, trade balance turned negative for the first time in eight years, occasioned primarily by steep increases in oil priceswhich, in turn, led to a significant rise in the import growth rate of 26.0 per cent. Exports began to strengthen towards the latterpart of the year but still registered a slowdown in 2005. In the face of trade deficit and tourism slump induced by the tsunamidisaster, the country’s current account posted a deficit of US$3,714 million. Notwithstanding this, Thailand’s balance of paymentsrecorded a surplus of US$5,422 million, as a result of inflows of foreign direct investment and the country’s international reserveswhich held steady at US$52,100 million.

MONETARY SECTORCommercial bank interest rates readjusted upwards during the second half of 2005. The four major commercial banks raised

the fixed deposit rates for terms ranging between 3 and 24 months by another 1.75-2.25 per cent and the loan rate was up byanother 0.75-1.25 per cent, in accordance with the monetary policy of the Bank of Thailand (BOT) to raise the 14-dayrepurchase rate and issue BOT bonds, as a means of absorbing liquidity. Meanwhile, bank credits expanded by 8.1 per cent whiledeposits increased by 8.4 per cent.

OUTLOOK FOR 2006Despite the stable outlook for Thailand’s major trading partners and bilateral free trade agreements between Thailand and

various countries as well as the healthy revival of the tourism industry, adverse developments in the political arena will impingeupon the growth in private consumption and public & private investment. In addition, an upward trajectory of interest rates and oilprices is expected to continue into 2006.

Economic stability is likely to improve, primarily as a result of steadier oil prices, with tight monetary policy expected to rein ininflation to the 3.5-5.0 per cent range in 2006 compared with 4.5 per cent in 2005.

Interest rates are largely on an upward path with commercial banks expected to raise the rates further by another 1.0-1.5percentage points in response to both external and domestic pressures, including further interest-rate increases imposed by theUS Federal Reserve. In addition, the 14-day repurchase rate is forecast to adjust further upward while reduction in liquidity in thebanking system is expected.

17

BANKTHAI’S MISSION, VALUE AND VISIONTHE BANK’S POLICY AND OVERVIEW OF DEVELOPMENTS IN 2005

In 2005, the Bank continued with the thrust on expanding the scope, reach and effectiveness of its business operations witha view to enhancing its ability to deliver a universal banking platform to customers. As an important step in that direction, the Bankintroduced changes to its organizational structure and business processes, with focus on strengthening retail banking activities andensuring the delivery of a full range of quality demand-driven products and services. Many of the initiatives to support theBank’s expansion and competitiveness are already in train and included, in 2005, the following highlights:

a) Life and non-life insurance. BT Insurance Co. Ltd., a subsidiary of the Bank, offers both life and non-life insuranceproducts. As part of the strategy to reinforce its market presence in the insurance arena, the Bank signed a Memorandum ofUnderstanding with Millea Life Insurance (Thailand) Public Co. Ltd., a subsidiary of Millea Asia Pte. Ltd., a leading player inthe Japanese insurance market. In this process, Millea Asia acquired 5 per cent of BankThai shares with BankThai, in turn,purchasing 30 per cent of Millea Life ordinary shares. This alliance marked an important milestone in the Bank’s efforts to betterserve its customers, while generating income and enlisting the support of a strategic shareholder.

b) A new and tighter focus is being given to extend retail banking activities, involving the introduction of new products such asPersonalCash - a multi-purpose term loan with no collateral or personal guarantee, repayable in installments, and carries intereston a reducing balance basis.

c) A fuller range of products and services has been put in place to increase business efficiency and capturing revenue. Thisincludes offering a wide spectrum of investor services that best meet customer needs by serving as bondholders’ representative,custodian, trustee, registrar and paying agent.

d) In this era of digital convergence, emphasis continues to be given to address customer needs by extending the rangeof cash management options and services that optimize the use of information and communication technology. This involvesupgrading the existing products and services, extending service delivery channels and introducing new electronic banking productsand services, including:

1) “Power Pay” enables a client to manage his/her accounts payable efficiently through, for example, the issuance ofBankThai cheques, instant online fund transfer, payroll services, delivery of shareholder returns, and loan repayment. Power Paycomes with the following array of features and benefits:

ë “Pay in Pack” can help fulfill nationwide banking needs of customers. It allows for safe and efficient electronic fundtransfers between banks including BankThai, within a secured environment.

ë “Smart Cheque” is ideal for clients preferring to pay by cheques. It allows for instant BankThai cheque issuance andonward delivery within a secure electronic environment, meaning savings in time and efforts.

ë The Bank and PCC Processing Group Co. Ltd as well as its member banks, namely, Bangkok Bank Public Co. Ltd.,Kasikornbank Public Co. Ltd. and Thai Military Bank Public Co. Ltd., have teamed up to offer real-time electronic payment servicethrough “ePAY”. With the support of “ePAY”, customers are provided with the platform to transfer funds online into the account ofbeneficiaries from anywhere in the world, within a secure PKI environment. In 2005, the Bank reached an agreement with anumber of government offices, namely Customs Department (to facilitate the payment of customs duty) and Industrial EstateAuthority of Thailand, in addition to the existing arrangement with the Revenue Department (to facilitate electronic/online taxpayment by business operators).

ë Wire@Wish allows for instant over-the-counter transfer of cash between any branch of BankThai and any branch ofBangkok Bank Public Co. Ltd., Kasikornbank Public Co. Ltd. and Thai Military Bank Public Co. Ltd. at lower costs. Wire@Wishprovides real-time results and is available to account holders as well as the general public.

ë BAHTNET is an ideal way of transferring large sums of money between banks and making payments to governmentauthorities; it provides real-time results.

2) “Power Collect” facilitates the collection of payment for goods and services, as well as cheque clearance. It has thefollowing two options:

ë “Cheque in Time” provides for fast and efficient cheque clearance, and also allows for the acceptance of post-datedcheques, or PDC. Cleared funds are deposited into the receiving account within three business days of the due date.

In 2005, the Bank extended the coverage of such service to allow juristic persons to deposit post-dated cheques into theirbank account on the date shown on the cheque to avoid clearing delays. Clearing results are transmitted electronically to customerto facilitate the monitoring of their cash flows.

ë “Direct Debit” offers a convenient payment method for both service providers or vendors and consumers. At theinstruction of the customer, the amount is debited from the account for the payment of, for example, utility bill, mobile phone bill,instalment, insurance premium, etc.

ë “Bill Payment” enables customers to pay their bills or their suppliers; it comes with the following options:“Counter Payment” - payment can be made over-the-counter at any branch of BankThai nationwide.“BT Phone Banking” - payment can be made round the clock by dialing 0-2626-7777.“ATM” - payment can be made round the clock through the ATM.“BTiBank” is a facility that allows customers to make payments via the Internet.

18

3) The Bank offers the following electronic means of communication and information exchange within a secure environment:ë “BTiBank” provides customers with cost-effective Internet banking solutions via www.btibank.com or www.btibank.co.th.

To enjoy the options provided by “BTiBank” the customer will need an account with BankThai and an assigned User ID and PIN.“BTiBank” features account access, fund transfers between different accounts or between banks via, for example, “Pay in Pack”,Wire@Wish and “BAHTNET”. It also facilitates the payment for goods and services such as the payment of credit card debt,mobile phone bill, instalment and utility bill. Once the transaction is complete, the information is sent back to the customer viae-mail. Other banking transactions available on “BTiBank” include reordering cheque books, tracking cheque status and stoppingcheque payment, including statement request and balance inquiry. SSL protocol is used to provide security and privacy overthe Internet. “BTiBank” has been designed to handle complex financial transactions and, therefore, is an ideal tool for largecorporations. Specifically, it allows for the electronic integration of a range of services, from approval of financial transactions tomanaging subsidiaries. The Help Desk which is set up at BankThai Care Centre, ISO 9001:2000-certified, can be reached ontelephone No. 0-2626-7777 and enter - 0 -.

ë “BT Speed Link” offers customers the following options: “Pay in Pack”, “Smart Cheque” and “Direct Debit”. It facilitatesa high speed link directly between customers and the Bank within a secure electronic environment and represents an ideal tool forjuristic persons having to deal with complex approval processes.

e) Organizational Structure and Human Resources DevelopmentIn 2005, the Bank commissioned a consultancy firm to study the Bank’s performance appraisal system with a view to

identifying Key Performance Indicators (KPIs) that can function as benchmarks that the Bank can use to align staff performanceand organizational goals, while creating a culture of rewarding staff for excellence in performance. Another important undertakingduring the year was the revision of the remuneration structure for the Bank and its subsidiaries, as well as the development of astandard welfare package for the staff of new subsidiary companies that reflect prevailing labour market conditions.

During the fourth quarter of 2005, the Bank restructured its organization into two distinct functions - business functionsand support functions. Business functions are clustered according to customer types (corporation/institution/retailer) and type ofbusiness (product management/sales/service channel/operation). The goal is to strengthen the Bank’s capability to develop andput in place products and services that satisfy the diverse and changing needs of customers.

As at 31 December 2005, total personnel in the Bank numbered 2,479. Of that figure, 940 are stationed at variousbranch offices and 1,539 at head offices. In terms of recruitment, the selection process seeks to draw candidates from a varietyof backgrounds embodying various disciplines which are required for the Bank’s functions, taking into account the candidate’sknowledge, skills, experience and competence.

f) Research and Development ActivitiesThe Research Office remains fully committed to extend and underpin its research and analytical capabilities to address the

evolving needs of the Bank’s own offices, customers and subsidiary companies. Continued focus is on enhancing the publicationof technical and research materials related to the economy, business and other issues of interest, as well as on producingand disseminating economic indicators regularly via various channels. Furthermore, the Research Office continues to play acomplementary role in generating revenue for the Bank by producing research papers for sale to outside parties. This initiativecontinues to capture the interest of various organizations and the general public.

In 2005, the Research Office teamed up with subsidiary companies to publish a journal entitled @ Money Corner.The journal features articles related to the economy, finance and investment deemed to be of interest to the Bank’s own customersand those of its subsidiary companies as well as other interested parties. In addition, the Research Office released its annualpublication, highlighting ways of reviewing and readjusting strategy and turning challenge into opportunity in the face of steeplyrising oil prices and an upward trend in interest rates. The publication has been disseminated to the Bank’s own offices andcustomers as well as the customers of its subsidiary companies and other interested parties.

g) Corporate ImageThe Bank continues to seek out and take tangible steps to enhance its corporate image and maximize customer outreach.

In this process, a wide range of undertakings is tailored to address the needs of specific customer groups, with event marketinghaving been cost-effectively integrated into the Bank’s strategic marketing programmes. The events are built around the theme“Proud to be Thai”, a theme which directly reflects the stance and image of BankThai. As a Thai commercial bank, BankThaiconstantly looks for opportunities to build up our national identity and pride. In 2005, the following two events were organized:

1. The Fifth “Bankthai...Proud to be Thai” Charity Concert was held at Thailand Cultural Centre on 23 August 2005, aspart of the Bank’s tradition of preserving Thai culture, including music and art. The concert which was performed by BangkokSymphony Orchestra (BSO) offered an opportunity for the Thai people from different generations to appreciate Thai classical andcontemporary music that is blended with orchestral instruments. Overall, it was a display of musical grandeur with a touch ofmodernness, yet laced with the wonderful gentleness and subtleties of Thai music. An overwhelming success, the concertbrought together famous artists from different generations such as Charin Nantanakorn, Ruangtong Tonguntom, Setha Sirachaya,Soontaree Vechanont, Nantida Kaewbuasai, Yuenyong Opakul, Rudklao Amratisha, Saovanit Navapan, Thitima Suttasoontorn,Haruthai Maungboonsri and Anuwat Sa-nguansakpakdee (Boy Peacemaker). The total net proceeds of Baht 1,535,610went to the Narcotics Control Foundation.

19

2. The Second “Proud to be Thai with Bankthai” Tour took the participants to Lopburi Province. This exclusive range ofcultural tours is dedicated not only to enhancing the knowledge and appreciation of Thai culture and traditions, but also topromoting pride in Thailand’s rich cultural heritage. This customer appreciation event also presents an avenue to promote businessopportunities, while affording the participants the chance to capitalize on the knowledge of Ajarn Pao-thong Thongchua, arenowned cultural expert and guide. So far, 8 tours have been organized with the participation of 700 people, and have receivedoverwhelmingly positive feedback.

In addition to the above, a wide range of activities is designed to target different customer groups. This includes, forexample, academic-related activities which are handled specifically by the Educational Counseling Office. In 2005, theOffice teamed up with the Office of Public Relations to organize the Third “MBA World Forum”, which was attended by over1,500 participants and provided a forum for young people and prospective MBA students to obtain guidance and informationfrom business schools both at home and abroad. In 2005, two events were organized: one in Bangkok and another in Chiang Mai,with the latter designed to reach out to young people living in provincial towns.

In addition, “Improve Your English” programme is designed to create opportunities for young people and others to improvetheir English language proficiency. The programme continues to receive support from a number of leading English languageschools both at home and abroad, and focuses on specific topics. In 2005, it saw the participation of about 500 people.

The Bank continues to focus its efforts on organizing seminars on various business-related issues of concern and interestto the customers, entailing collaboration with other entities. For example, in 2005, the Bank teamed up with Thailand TextileInstitute to organize a seminar entitled “Still Hope for the Thai Textile and Thai Garment Industry” for its loan customers.In addition, the Bank organized a number of other events, including a special talk for a group of Japanese customers on thesubject of “Post-Election Political and Economic Trends in Thailand”. The guest speakers were Dr. Virabongsa Ramangkura,Mr. Viset choopiban and Mr. Sondhi Limthongkul. Other seminars related to privileged banking etc. were also organized.

On health-promotion issues, the Bank continues to extend support to a large number of related academic institutions,organizations, associations and foundations. This includes Anti-Tuberculosis Drugs Research Fund within Siriraj Foundation underthe Royal Patronage of Her Royal Highness Princess Galayani Vadhana Princess Narathivas, National Council of Women ofThailand under Royal Patronage, Saijai-Thai Foundation, Thailand Association of the Blind, Office of the National CultureCommission, and Foundation for the Mentally Retarded of Thailand. In addition, the Bank teamed up with Caraboa TawandangCo. Ltd. to produce a CD, “Sub Narmta Andaman”, the proceeds from which went towards alleviating the plight of students atBaan Kalim School and Rajaprachanukroh School 36 (Baan Kamala School) in the tsunami-struck Phuket Province. Donationsalso went to the Rajaprachanukroh Foundation under Royal Patronage to help the victims of the tsunami.

BUSINESS DIRECTION IN 2006In 2006, the Bank intends to take a more aggressive approach to enhancing its ability to deliver a universal banking platform

to customers once its obligations related to the management of impaired assets for the FIDF (from 2001 to 2005) under theGain/Loss Sharing and Yield Maintenance Agreement are fulfilled. Appropriate changes will continue to be introduced to itsorganizational structure with a view to strengthening focus on each customer group and customer service, while keeping pace withan ever-growing customer base. Focus of attention will continue to be given to enrich the support of SMEs and personal bankingcustomers.

The organizational structure that is in place provides two well-defined functions, namely business functions and supportfunctions. This includes finance, human resources, legal affairs etc. The business functions are clustered according to thecorresponding customer and business types. The goal is to continue the Bank’s efforts to improve and develop products andservices that satisfy the diverse and changing needs of customers. The operation of the Bank is currently divided into the followinggroups:

1. Corporate Banking Group 1 and Group 22. Institutional Banking Group3. Retail Banking Group4. Business Support Group5. Risk Management and Staff Credit Group

The work is supported by the following divisions:1. Financial Control Division2. Corporate Affairs Division3. Human Resources Management Division4. Core Banking (Core Banking Project Office)

The Bank together with its group of companies remain firmly committed to positioning itself as a full service banking group thatoffers customers as wide a range of products and services as possible. Priority attention continues to be given to strengthening theBank’s competitive position by improving profit margins in every facet of its business, including corporate banking, institutionalbanking, retail banking, and through its subsidiary companies. Focus is also on increasing revenue raised through fees andcharges as a means of improving operational results and stability.

20

In addition to providing the right products and services, the Bank continues to give priority attention to understanding thecomplete relationship with a customer, including service channel preferences. As an important step in that direction, strategicmoves are being taken to boost the capacity of business centers and electronic channels, including self-service kiosks such asATMs (Automated Teller Machines), CDMs (Cash Deposit Machines) and PUMs (Passbook Update Machines). Currently, thereare 619 of such machines in operation. In this respect, appropriate action will be taken between 2006 and 2007 to increase thenumber and efficiency of such machines with a view to providing existing customers with an easier access to the Bank’s productsand services while attracting new customers.

The Bank will continue its thrust on employing the highest standards of risk management with a view to complying with thedirective of the Bank of Thailand and becoming BASEL II accord. Constant attention will be given to evaluating the suitability ofbusiness and developing processes initiated in 2005, especially those in operation units and support units. A balanced mix ofpolicy initiatives will enable the Bank to implement a more aggressive business strategy while managing its human resourceseffectively. In this respect, policy attention will be given to ascertain that staff sizes are commensurate with the volume of business,as well as to evaluate performance reliably and fairly and to ensure that the levels of pay and benefits reflect adequately therelevant labour market supply and demand factors. Further initiatives will also be taken to develop staff skills and knowledge witha view to enhancing the quality of the Bank’s stock of human capital.

HUMAN RESOURCES MANAGEMENT, TRAINING AND DEVELOPMENTThe Bank remains fully committed to enhancing the quality of its stock of human capital which it recognizes as one of the most

important ingredients for success. An important milestone in 2005 was the commissioning of a consultancy firm to help the Bankmove away from the current MBO (Management-by-Objectives) system and move to the BSC (Balanced Score Card) systemthat uses a clear set of Key Performance Indicators (KPI). The rationale behind this policy move is to more effectively measureperformance of staff against the Bank’s set goals and objectives, and to provide a legitimate basis for recommending the paymentof bonuses as a means of rewarding special services or personal performance.

In addition, the Bank plans to review its list of core professional competencies and determine functional competencies requiredfor all positions, to be used in the recruitment process as well as in upgrading the quality of its stock of human capital whilefostering the corporate culture in the long run.

Furthermore, the human resources development programme will focus on the implementation of a management traineeprogramme as well as talent assessment and career planning, to be used as a tool for executive succession planning andrecruitment of professionally qualified and/or experienced specialists to fill specific vacancies.

TRAINING COURSESThe Bank is committed to providing staff with the highest possible quality of training. This involves organizing courses on

specific topics and exhibiting a direct link between learning and the Bank’s overall business strategy and policy. For that purpose,the core training programme has been developed taking account of training needs of each position and/or function identifiedthrough a survey. In 2005, the Bank organized 184 training courses, of which 43 were organized by the Bank and 141 byoutside parties. This represented 6.18 days of training per staff member, costing to the tune of Baht 6.16 million.

POLICY GOVERNING THE BANK’S SUBSIDIARY AND ASSOCIATE COMPANIESA company is deemed to be a subsidiary of the Bank if the Bank has the power to determine that company’s financial and

business policies in such a way as to be in their best interest. It is a company in which the Bank owns, directly or indirectly, morethan 50 per cent of that company’s issued and paid-up share capital.

A company is deemed to be an associate of the Bank if the Bank has the right to participate in the formulation of its financialand business policies. It is a company in which the Bank owns, directly or indirectly, more than 20 per cent of its issued andpaid-up share capital.

The Bank’s policy governing its subsidiary and associate companies involves appointing the Bank’s executives to theirrespective boards of directors. The executives concerned are required to report on the developments and progress achieved by thecompanies to the meeting of BankThai Board of Directors once a week. In addition, the Bank’s Audit Committee is assigned toprovide audit services to the companies concerned.

Essentially in all cases, the subsidiary and associate companies are engaged in activities that are contributing, directly orindirectly, to promoting the Bank’s business. The Bank’s policy is to continue working simultaneously and on parallel paths withthe companies concerned with a view to promoting its own business and those of its subsidiary and associate companies.Significantly, effective cross selling between the Bank and the companies concerned has the potential to contribute towardsoptimizing customer satisfaction through one-stop service offerings. From this perspective, customers can take advantage ofthe service offered by the Bank concurrently with its subsidiaries, say, BT Consultancy Co. Ltd., BT Insurance Co. Ltd. andBT Securities Co. Ltd. to facilitate their business dealings and identify new avenues for doing business or raising funds. Forinstance, BT Consultancy Co. Ltd. can give technical advice to customers and help them identify suitable sources of fund. If thestock exchange should open up the avenue for such fund-raising, then BT Securities Co. Ltd. can step in to help with the relatedformalities and arrangements.

21

RESPONSIBILITY OF THE BOARD OF DIRECTORS FORFINANCIAL STATEMENTS

The Board of Directors is responsible for the financial statements of BankThai Public Company Limitedand its subsidiaries, and the financial disclosures presented in the annual report. The financial statements havebeen prepared in accordance with accounting principles generally accepted in Thailand and suitable accountingpolicies, consistently applied and supported by prudent judgment. Essential data and information have beendisclosed in the notes to the financial statements, with consideration given to the directives prescribed by theBank of Thailand as well as the regulations of the Securities Exchange Commission and the Stock Exchange ofThailand.

The Board continues to give priority attention to enhancing the effectiveness of the Bank’s system ofinternal control to provide reasonable assurance that the system is contributing towards achieving reliability offinancial reporting, thereby protecting the Bank’s assets while preventing malfeasance or irregularity.