city of fort mitchell, kentucky

TRANSCRIPT

CITY OF FORT MITCHELL, KENTUCKY

FINANCIAL STATEMENTS AND

INDEPENDENT AUDITOR'S REPORT

For the Year Ended June 30, 2013

Page

City Officials………………………………………………………………………………………………………………………..1

Independent Auditor's Report........................................................................…………………………………………………………………………………………………………….……..2-3

Management's Discussion and Analysis……………………………………………………………………………………………………………………………4-11

Basic Financial Statements

Government Wide Statements

Statement of Net Position……………………………………………………………………………………………………………………………………….12

Statement of Activities………………………………………………………………………………………………………………………………………13

Fund Financial Statements

Balance Sheet - Governmental Funds…………………………………………………………………………………………………………………………………….....14

Reconciliation of the Balance Sheet - Governmental

Funds to the Statement of Net Position……………………………………………………………………………………………..15

Statement of Revenues, Expenditures and Changes in

Fund Balances - Governmental Funds……………………………………………………………………………………………………………………………………16

Reconciliation of the Statement Revenues, Expenditures and Changes in

Fund Balances - Governmental Funds to the Statement of Activities………………………………………...………………..17

Notes to Financial Statements…………………………………………….…………………………………………………………………………………………………...…………….18-28

Required Supplemental Information

Budgetary Comparison Schedules - Budget to Actual:

General Fund…………………………………………………………………………………………….29

Road Tax Fund……………………………………………………………………………………………..30

Capital Projects Fund……………………………………………………………………………………….31

Municipal Road Aid Special Revenue Fund…………………………………………………………………32

Other Supplemental Information

Combining Balance Sheet - Non-Major Governmental Funds…………………………………………………………………………………………33

Combining Statement of Revenues, Expenditures, and

Changes in Fund Balance - Non-Major Governmental Funds………………………………………………………………………………………34

Budgetary Comparison Schedules - Budget to Actual:

Park Tax Special Revenue Fund………………………………………………………………………………………………………………………………………..35

Storm Sewer Contingency Special Revenue Fund………………………………………………………………………………………..36

Independent Auditor's Report on Internal Control Over Financial Reporting and on

Compliance and Other Matters Based on an Audit of Financial Statements

Performed in Accordance With Government Auditing Standards ..........................................................………………………………………………………37-38

CONTENTS

CITY OF FORT MITCHELL, KENTUCKY

FINANCIAL STATEMENTS AND

For the Year Ended June 30, 2013

INDEPENDENT AUDITOR'S REPORT

Christopher Wiest

Vicki Boerger Mary L. Burns

Ray Heist Frank Hicks

Jim Hummeldorf Kim Nachazel

Dan Rice Denny Zahler

City Administrator Chris Moriconi

Police Chief Jeff Eldridge

City Attorney Robert Ziegler

City Clerk Martha Allen

City Treasurer Amy Guenther

Fire/EMS Chief Scott McVey

Public Works Director/

Building Zoning Administrator David Noll

Department Heads

CITY OF FORT MITCHELL, KENTUCKY

LIST OF CITY OFFICIALS

For the Year Ended June 30, 2013

Mayor

Council Members

- 1 -

v.n Go.der, W. lker & Co., Inc.

INDEPENO€NT AUDITOR'S REPORT

fo ihe Honorablo l|]l.yor andMembers or the Councilcit of Fort llrlitch€ll, Kentucky

Report on lh. Fin:ncialstatemenls

We have audlted ih€ accompanying linancia slatements oi lhe governmenla aciivil es each majotfund and the aggregale remaining iund nrormaiion of the Ciiy or Fort Mlchel, Kentuckv as of and fofthe vear ended iuni:30, 2013, and the related notes to ihe rnancialstatemenls which colectvelvcomorise the clvs basicinancialstatements as Lisled n th€ t:ble of contenis

-Mana$nont's RespoEibility tor lhe Financi.l Sl€t ments

MenaaFnenr s respo- \be fo ' l e p epa cron dnd fa 'precF. r i o o ' these nan 'b l s tarere t ! ndcoracn ewrha((or l r1q p . r . p es qeneta. ly d epreo . lhe L I Fd Sla les o Ane d ts nc l -desthe d€sign, impementation, and mainlenance of interial cont.o relevant lo lhe prepa€lion and iaiforesenlatioi of financia staiements thal are iree lrom matefalmsslatemenl, whether due to fraud or

. Au d ito / s R es p o rei b i I ity

Our respons biity is to express an oplnion on lhese financlal staieme.ls based on our audt Weconducl;d our audit in accordance w(h audling slandards senera lv ac@pled n the Unlted stales oiAmerica and the standards applicable to financial audils contalned l^ Govemnent auditing standatdsissued bv lhe complroller Genera of lhe uniied slales. Those standards equi.e lhat we p an andperrorm ihe audil to oblain reasonable assuranc aboul whether the li.anca slatements a.e tree rrcm

An rudil nvolves perfoming procedures lo oblan auditevldence about lhe amounts and disclosures lntlre financia staGments. The procedures seLected depend on the auditors ludgment incudng theassessment oI lhe risks oi ma6.lal m sstatement of lhe rnanci:l slatemenls, whelher due lo lr:ud or€(or. ln making those sk assessments, the audiior cois d€rs i ernalcontro relevant lo th6 €ntlvsoreoaralion andran oresentatof ol lhe linancia sialements in o.der to design audii procedlres thal arelpproprlate n tne ciicumstances, but nol for lh€ plrpose ofexpressng an opinon on the efGcllvenessoilh; enlltys lntemal conlrol. Accordingy, we €tpress no such opinion An audl also incLudesevaluatno ihe appropdaleness ol a@ounting po icies used and the reasonableness oI signilicanlaccounriit eslimabs made by mahagemenl. as wel as evalLatns the overalpreseniallon of the

We be i€ve thatlhe audit evidence we have oblaned is sufficient a.d approprlaielo provde a bas s ror

ln our opnion ihe nnancial statefie.b efered to above present iairy h al male al.'€specls,t-fLe' a L r lporko- o f lh .go{ehnen_a a I lEso_r ' 'C \o l -on i , l r lne l {enuk lcso !J nF30 2011dd Lne ;eso-cr 'e (t:q\ { h-a ( a posrion rhereot ro rhe /ea|Tl ended r "*o da ce ^'"

accornrlns pincp es geneGlly amepred in lhe united slaies ofAmerca

Van Gorder, Walker & Co.. Inc.

-Requhed Supplemertary lnformation

Accounlins prncip es generally ac.epted nlhe United States ofAfreaca requ re lhatlhe Mar.g€r€rfsDdclssio, ,rd Aralysf on pages 4l1 be presenled to suppement lhe basc linanca stai€m€ntssuch infomaton lllhouoh nol a pad oflhe basic linancaislalements. is required by lhe GoverimentaAccounling Slandards Board who consideB il lo be an essenl a partollinancia reponn! fo.pacing thebasic fn.ncia slalements n an appropriale operalonal, economc. of hslorical contexl We lraveappied cerla n limited pro@dures lo lhe reqlired supplementary i ohaton in accordance wilh audtingslandards lenerally accepled n the Unled Slales of America, which conssted ot nqunes ofmanagedent about lhe merhods of preparinq lhe nforfraiion and comparifg lhe niormalon lorconsstency with managements responses io our nqunes. lhe basc fnanca staleffefts, an! olhefknowedg€ w€ obleined durng our audit ollhe bas c lnanca slal€menls. We do not express an op rioior polde anv assurance or lhe nlormrlion because the lmled prodedures do nol provida us wthsuliicienl evdenceto express an opinon or provide a.y asslrance

Our audlt was conducled for the pu@ose of fom ng an op n on on the basrc iinanca statements lakenas a whoe Tlre budgelary comparson schedues of pages 29-32 a.e presented ior the pupose.taddliona anaysis a.d are not a requfed parl of lhe basc fnancial slalements The budgetaryconparison schedules hrve not been sublecled lo lhe audlinq procedures applred n the audii of thebas cnnanclaLsldements and acco.d ngly. we express no opinion of it.

- supp I en entary I nfo rnati o n

Our audts were cofdlcted for lhe purpose of iorm ng an op n on on the nnancjalstatemenh as a wholeThe combinng non-major governmentaLfunds schedues and lhe bLdgetary comparson schedues ofIhe non-major governmenlal iunds on pages 33 36 are slppemenlary nformalof and are prcsenl€dJopurpos€s ol addlo.ai analysis and are not a requred paft ol the brsc fnanca slatefreiG sucfri.lormalion is the responslblity of danagen€nt and was derved from and re ates d rectly lo ti.€underLyng accounlng and olher records used lo prepare lhe llnancia staiements The informaton hasbeen sublected lo lhe audung procedures applied n the audlt oI lhe lnancial slalefren8 and cenainaddiliona procedures ncLld ng @mparing and reconclng such lnfomation d rectly lo lhe undery

"gaccounling and other records used lo prepare (he linancal sl!lemenls or lo lhe linanca slatementslhemseves, and oiher rddilona procedures n acdordance with audtna stafdards qenera y acceltedn lhe unred srates ofAmerca ln ouropifion lhe inlomation is la r y stated lna maleria.especrs iire al o. to ft€ nnancia slalemenls as a whole

other Reporting Required by Govemnent Auditing srandads

In ac.ordan.e wth Govelr, ert ,4 rdrirg Srandaids we have aso ssued olr reForl dlted Jaiuary 152014 on ourcoisderation otlhe Cly ofFon [,] Ichell Kenluckysi.lernalconlrol.verlinancalreportingand on our lesls of ils compiance wlh cenain provisions of laws, egulalons, conlracts, and granlagreemenls and other malte.s The purpose of thal reporl s 10 describe lhe scope of our lesti.g ofinl€rnalconlro over inanci.lEpofting and comp iance and rhe resulrs ol lrrat tesr nc, and noi tD piov dean opin o. on inierna convo overiinafca report ng or on complia.ce That reporl is an ille!.a padofan audt pedomed n:ccordance wth Go/errDerl, rdil;rg Slrrdards in cofsdering the ci.! of Fo.lMilchell Kentuckys nterna conlro over fina.c al repon nq and comp iance

. . / , ) n t r4L/a-*.8)4-,'.)2.-, Lr-2.^-4+ <- CE

v.n Goder, Walker, & co.,Inc.

3

CITY OF FORT MITCHELLMANAGEMENT’S DISCUSSION AND ANALYSISFOR THE FISCAL YEAR ENDED JUNE 30, 2013

- 4 -

Our discussion and analysis of City of Ft. Mitchell, Kentucky’s financial performance provides anoverview of the City’s financial activities for the fiscal year ended June 30, 2013. Please read it inconjunction with the City’s basic financial statements.

USING THIS ANNUAL REPORT

This annual report consists of a series of financial statements. The Statement of Net Position andthe Statement of Activities provide information about the activities of the City as a whole andpresent a longer-term view of the City’s finances. For governmental activities, these statementstell how these services were financed in the short term as well as what remains for futurespending. Fund financial statements also report the City’s operations in more detail than thegovernment-wide statements by providing information about the City’s financially significantfunds.

Financial Highlights

As of the close of the current and prior fiscal years, the City’s governmental funds reported fundbalances as follows:

The General Fund balance increased $357,668 due to an increase in revenues, and the currentadministration’s significant efforts at controlling costs such as equipment purchases andmaintenance and bidding of services.

The Road Tax Fund balance decreased $17,228 which is comparable to last year. Significantamounts of road work were completed on Pleasant Ridge Avenue-Phase I and Superior Drive.

The Capital Fund balance increased $224,827. All of the expenditures were offset by a transferfrom the General Fund. This fund is used for future capital purchases such as police cars, firetrucks and building renovations.

The Municipal Road State Aid increased $136,050 due to municipal road aid revenue from thestate increasing and no large projects completed out of this fund in the current fiscal year. Manyroad projects are budgeted for this fund for fiscal year 2014. However, in future years, fundingfrom the state is expected to decline.

The Storm Sewer Contingency fund was closed this fiscal year and the remaining fund balance of$68,690 was transferred to the Road Tax Fund.

The Park Tax Fund increased $43,902 due to maintenance and capital projects being deferred tothe next fiscal year.

Percentage Increase

FYE 2012 FYE 2013 Increase/ Incr/(Decr)

Funds Amount Amount (Decrease) From FYE 12

General 3,198,828$ 3,556,496$ 11.18% 357,668$

Road Tax 1,535,446 1,518,218 -1.12% (17,228)

Capital 3,476,024 3,700,851 6.47% 224,827

Municipal Road Aid 347,493 483,543 39.15% 136,050

Storm Sewer Contingency 141,342 - -100.00% (141,342)

Park Tax 158,319 202,221 27.73% 43,902

Total Fund Balance 8,857,452$ 9,461,329$ 6.82% 603,877$

CITY OF FORT MITCHELLMANAGEMENT’S DISCUSSION AND ANALYSISFOR THE FISCAL YEAR ENDED JUNE 30, 2013

(Continued)

- 5 -

OVERVIEW OF THE FINANCIAL STATEMENTS

Government-Wide Statement of Net Position and Activities

One of the most important questions asked about the City’s finances is, “Is the City as a whole ina better or worse financial position as a result of the year’s activities?” The Statement of NetPosition and the Statement of Activities report information about the City as a whole and about itsactivities in a way that helps answer this question. These statements include all assets andliabilities using the accrual basis of accounting, which is similar to the accounting used by mostprivate-sector companies. Accrual of the current year’s revenues and expenses are taken intoaccount regardless of when cash is received or paid.

These two statements report the City’s net position and changes in them. You can think of theCity’s net position as the difference between assets, what the citizens own, and liabilities, whatthe citizens owe. This is one way to measure the City’s financial health, or financial position.Over time, increases or decreases in the City’s net position are one indicator of whether itsfinancial health is improving or deteriorating. You will need to consider other factors also, such aschanges in the City’s property tax, gross receipts, payroll and insurance premium tax base, andthe condition of the City’s capital assets (roads, buildings, equipment and sidewalks) to assessthe overall health of the City.

In the Statement of Net Position and the Statement of Activities, we have listed the governmentalactivities:

Governmental activities: Most of the City’s basic services are reported here, includinggeneral government, police, fire & EMS, public works, parks and recreation. Grossreceipts and payroll license fees, insurance premium taxes, charges for services andproperty taxes, as well as government grants finance most of these activities.

Fund Financial Statements

The Governmental Fund financial statements provide detailed information about the City’s funds.Some funds are required to be established by State Statute or Municipal Ordinance (Ex. General,Road Tax, and Park Tax Funds). However, the City Council establishes a few other funds to helpit control and manage money for particular purposes (Ex. Capital Projects) or to show that it ismeeting legal responsibilities for grant funds (Ex. Municipal Aid Fund).

Governmental funds: Most of the City’s basic services are reported in governmental funds, whichfocus on how money flows into and out of those funds and the balances remaining at year-endthat are available for spending. These funds are reported using an accounting method calledmodified accrual accounting, which measures cash and all other financial assets that can readilybe converted to cash. The governmental fund statements provide a detailed short-term view ofthe City’s general government operations and the basic services it provides. Governmental fundinformation helps you determine whether there are more or fewer financial resources that can bespent in the near future to finance the City’s programs. We describe the differences between thegovernment wide net position financial statements and the governmental fund financialstatements in the reconciliations within the audited financial statements.

CITY OF FORT MITCHELLMANAGEMENT’S DISCUSSION AND ANALYSISFOR THE FISCAL YEAR ENDED JUNE 30, 2013

(Continued)

- 6 -

Government-Wide Change in Net Position

For the year ended June 30, 2013, net position for all of the changed as follows:

GovernmentalActivities

Beginning Net Position 21,833,868$Increase in Net Position 476,457

Ending Net Position 22,310,325$

Government-Wide Statement of Net Position Summary

GovernmentalActivities

2012 2013

Current Assets 7,827,819$ 9,464,962$Other Noncurrent Assets 2,009,382 736,553Capital Assets, Net 12,924,531 12,769,351

Total Assets 22,761,732 22,970,866

Current Liabilities 908,666 660,541Noncurrent Liabilities 19,198 -

Total Liabilities 927,864 660,541

Net Assets 21,833,868$ 22,310,325$

To aid in the understanding of the Statement of Activities some additional explanation is given.Of particular interest is the format that is significantly different from a typical Statement ofRevenues, Expense, and Changes in Fund Balance. You will notice that expenses are listed inthe first column with revenues from that particular program reported to the right. The result is anet (expense)/revenue. The reason for this kind of format is to highlight the relative financialburden of each of the functions on the City’s taxpayers.

CITY OF FORT MITCHELLMANAGEMENT’S DISCUSSION AND ANALYSISFOR THE FISCAL YEAR ENDED JUNE 30, 2013

(Continued)

- 7 -

FINANCIAL ANALYSIS OF THE GOVERNMENT’S FUNDS

The following schedule presents a summary of general and special revenues for all of the fundsfor the fiscal year ended June 30, 2013, and the amount and percentage of increases anddecreases in relation to the prior year.

Property tax revenue temporarily decreased $15,580 (1.1%) even though the City’s property taxrate remained same as last year. This decrease is a result of a few large commercial propertiesgoing out of business.

Payroll license fees increased by $164,973 (13.1%) and gross receipts increased $75,111(26.5%). A portion of the increase is from the 2011 St. Elizabeth Physician group moving into theCity as part of economic development effort by the current administration, and other economicdevelopment within the City, as well as the continued upswing of the economy.

Insurance premium taxes decreased $119,947 (10.4%) as a result of a few large commercialproperties temporarily not in business.

Intergovernmental revenue increased $21,569 (5.2%) mainly due to the increase in emergencyresponder incentive pay and Municipal Road Aid received from the State of Kentucky.

Charges for services decreased $17,718 (1.5%) due a $91,000 code enforcement chargecollected last year. Other charges for services such as life squad and city contract fees haveincreased due to the City provided Advanced Life Support Services (ALS).

Increase

FYE 2012 FYE 2013 Percentage (Decrease)

Revenues Amount Amount Incr(Decr) From FYE 12

Property Tax 1,436,437$ 1,420,857$ -1.1% (15,580)$

Bank Deposit Tax 63,876 71,550 12.0% 7,674

Telecommunication Tax 71,703 83,935 17.1% 12,232

Payroll License Fees 1,255,539 1,420,512 13.1% 164,973

Insurance Premium Tax 1,153,891 1,033,944 -10.4% (119,947)

Gross Receipts License Fees 283,372 358,483 26.5% 75,111

Other Licenses and Permits 80,411 79,321 -1.4% (1,090)

Intergovernmental 416,871 438,440 5.2% 21,569

Fines and Forfeitures 23,858 14,298 -40.1% (9,560)

Charges for Services 1,221,315 1,207,052 -1.2% (14,263)

Investment Income 78,818 51,519 -34.6% (27,299)

Contributions 10,033 14,927 48.8% 4,894

Sale of Surplus Property 5,073 11,955 135.7% 6,882

Miscellaneous 21,200 14,525 -31.5% (6,675)

Total Revenues 6,122,397$ 6,221,318$ 1.6% 98,921$

CITY OF FORT MITCHELLMANAGEMENT’S DISCUSSION AND ANALYSISFOR THE FISCAL YEAR ENDED JUNE 30, 2013

(Continued)

- 8 -

The following schedule presents a summary of general expenditures for all of the funds for thefiscal year ended June 30, 2013, and the amount and percentage of increases and decreases inrelation to the prior year.

Percentage IncreaseFYE 2012 FYE 2013 Increase/ (Decrease)

Expenditures Amount Amount (Decrease) From FYE 12

General Government 981,811$ 791,514$ -19.38% (190,297)$Police 1,421,649 1,540,398 8.35% 118,749Fire/EMS 1,283,856 1,395,281 8.68% 111,425Public Works 1,804,451 1,726,360 -4.33% (78,091)Recreation 89,106 83,115 -6.72% (5,991)

Parks 71,187 80,773 13.47% 9,586

Total Expenditures 5,652,060$ 5,617,441$ -0.61% (34,619)$

General expenditures decreased due to the replacement of the City parking lot in the prior fiscalyear.

Police expenditures increased due to the department filling open positions and the relatedemployee health insurance and retirement expenditures as well as grants received by thedepartment.

Fire and EMS expenditures increased since the department began provided advanced lifesupport and added three full-time medics. These expenses were partially offset by relatedrevenue.

Public works expenditures decreased due to a dump truck that was purchased in the prior fiscalyear.

Recreation expenditures decreased slightly due to certain programs not moving forward due toweather and other associated events.

Park expenditures increased due to the replacement of a slide and removal of dead trees.

CITY OF FORT MITCHELLMANAGEMENT’S DISCUSSION AND ANALYSISFOR THE FISCAL YEAR ENDED JUNE 30, 2013

(Continued)

- 9 -

CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets

The capital assets were reported for the fiscal years ended as follows:

Governmental

Activities2012 2013

Construction in Progress 1,159,259$ 160,290$Land 590,078 590,078Buildings 643,097 643,095Buildings/Land Improvements 1,187,415 1,187,415Infrastructure 17,124,686 18,805,579Equipment 1,737,635 1,734,530Furniture and Fixtures 253,062 251,774Vehicles 2,305,057 2,194,180

Totals 25,000,289$ 25,566,941$

This year's net increase of $566,562 in capital assets included:

Fire equipment 23,940$Fire vehicles 33,774Park equipment 2,860Police equipment 2,300Police vehicles 88,078Public works road and storm sewer projects 1,847,073Public works net construction in progress (998,969)Police vehicle and equipment disposals (37,366)Fire equipment and vehicle disposals (97,997)Public works infrastructure and equipment disposals (290,921)Park disposals (6,210)

566,562$

CITY OF FORT MITCHELLMANAGEMENT’S DISCUSSION AND ANALYSISFOR THE FISCAL YEAR ENDED JUNE 30, 2013

(Continued)

- 10 -

Debt

An annual payment of $19,198 is made on the mobile data terminal financing. One paymentremains.

Governmental

Activities

2012 2013

Mobile data terminal financing-Kenton Co. 38,396$ 19,198$

Totals 38,396$ 19,198$

GENERAL FUND BUDGETARY HIGHLIGHTS

Over the course of the year, the city council revised the General Fund budget once. The budgetamendment was made to increase the beginning fund balance to actual and to decreaserevenues and expenditures to more closely reflect the anticipated revenues and expenditures forthe year.

Actual revenue exceeded budgeted amounts by $170,645 (3.3%). Actual expenditures andtransfers came in under the amended budget by $185,299 (3.5%) due to significant efforts bymanagement to control costs. The City’s general fund ended the year with revenues exceedingexpenditures and transfers by $357,668.

ECONOMIC FACTORS AND NEXT YEAR’S BUDGET

General Fund Revenues

General Fund revenues are budgeted to increase approximately 6% over last year's amendedbudget numbers as the economy continues to improve, the City administration applies for grantsand new business like the Mercedes dealership move into the City. Real estate taxes arebudgeted to increase due to economic development even though the same real property tax ratewas proposed and adopted.

General Fund Expenditures

General Fund expenditures and transfers are budgeted to increase 5% from last year’s amendedbudget. 1.3% is for inflation and the remaining 3.7% is for grants that the City is applying for.Transfers to the Road and Capital Replacement Funds are budgeted at modest amounts, and, solong as the City continues to conservatively manage funding, we will amend the budget to fundtransfers in greater amount at the end of the year.

The General Government budget includes a economic plan and the purchase of benches andgarbage cans for Dixie Highway.

The police budget includes a fully staffed department of 13 officers for the City’s protection. ThePolice Department will be concentrating on many public relations projects and has budgeted forbullet proof vest, bike patrol and cruiser cameras to be paid with grant money received.

The fire and life squad department budget includes purchases of turnout gear and a new heartmonitor to be funded with grants.

The public works budget includes a seven year strategic road plan.

CITY OF FORT MITCHELLMANAGEMENT’S DISCUSSION AND ANALYSISFOR THE FISCAL YEAR ENDED JUNE 30, 2013

(Continued)

- 11 -

The recreation budget includes many great activities for the City’s citizens; however, a fewprograms were not budgeted for due to lack of participation. However, the administration haspartnered with Lakeside Park and Crestview Hills to conduct joint programming, which had theeffect of increasing programming, while achieving cost savings.

Municipal Road Aid and Road Tax Expenditures

The City has continued an aggressive schedule for road replacement and to take advantage oflow bids received by contractors, including resurfacing throughout the City and road replacementof Pleasant Ridge, Ashton, and Grace Court.

Park Fund Expenditures

The Park Fund budged includes rebuilding the soccer field.

Capital Replacement Expenditures

The Capital Replacement Fund includes engineering costs for the renovation of the city buildingand the purchase of two police cruisers and a fire pumper truck. The City has transferred annuallyto the Capital Replacement fund for future capital purchases from the general fund.

General Fund Balance

The philosophy used in preparation of the budget is to estimate the revenues and expendituresconservatively, especially in the current economy. In other words, “plan for the worst and hope forthe best.” The City has been vigilant in building up a healthy fund balance. There is a full 6 monthreserve as recommended by our auditors, as well as some additional reserve funding, so that theCity can better deal with economic down turns and unexpected expenditures. As a city, weprovide services that are of the highest quality that makes Fort Mitchell one of the most desirablecities to live in.

REQUESTS FOR INFORMATION

This financial report is designed to provide our citizens, taxpayers, customers, and creditors witha general overview of the City’s finances and to show the City’s accountability for the money itreceives. If you have questions about this report or need additional financial information, contactthe City Administrator’s Office at (859)331-1212 or 2355 Dixie Highway, Ft. Mitchell, KY 41017.

CITY OF FORT MITCHELL, KENTUCKYStatement of Net PositionJune 30, 2013

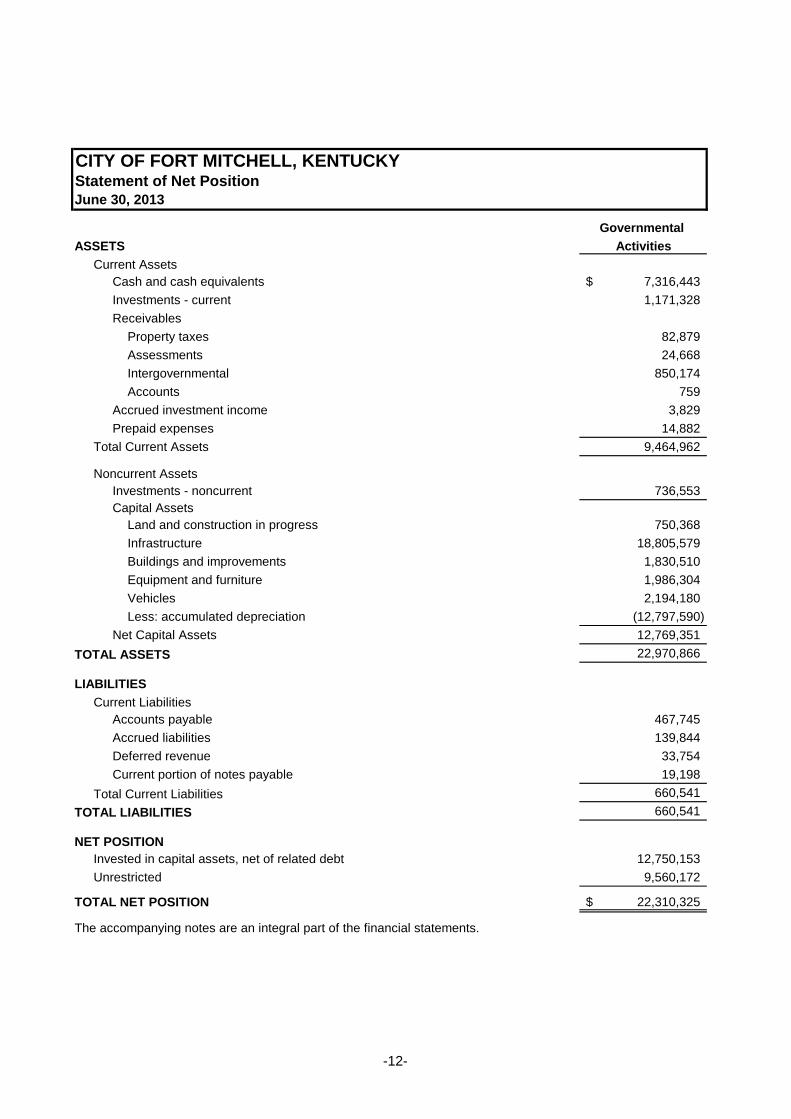

Governmental

ASSETS Activities

Current Assets

Cash and cash equivalents 7,316,443$

Investments - current 1,171,328

Receivables

Property taxes 82,879

Assessments 24,668

Intergovernmental 850,174

Accounts 759

Accrued investment income 3,829

Prepaid expenses 14,882

Total Current Assets 9,464,962

Noncurrent Assets

Investments - noncurrent 736,553

Capital Assets

Land and construction in progress 750,368

Infrastructure 18,805,579

Buildings and improvements 1,830,510

Equipment and furniture 1,986,304

Vehicles 2,194,180

Less: accumulated depreciation (12,797,590)

Net Capital Assets 12,769,351

TOTAL ASSETS 22,970,866

LIABILITIES

Current Liabilities

Accounts payable 467,745

Accrued liabilities 139,844

Deferred revenue 33,754

Current portion of notes payable 19,198

Total Current Liabilities 660,541

TOTAL LIABILITIES 660,541

NET POSITION

Invested in capital assets, net of related debt 12,750,153

Unrestricted 9,560,172

TOTAL NET POSITION 22,310,325$

The accompanying notes are an integral part of the financial statements.

-12-

CITY OF FORT MITCHELL, KENTUCKYStatement of ActivitiesFor the Year Ended June 30, 2013

Net Revenue (Expense)

and Changes inNet Position

Operating Capital TotalCharges for Grants and Grants and Governmental

Functions/Programs Expenses Services Contributions Contributions Activities

Primary GovernmentGovernmental Activities

General government 815,808$ 66,531$ 750$ -$ (748,527)$Police 1,520,583 18,804 128,217 15,418 (1,358,144)Fire and EMS 1,495,897 684,496 - 19,250 (792,151)

Public works 1,629,088 428,666 3,732 286,000 (910,690)Parks 114,000 - - - (114,000)

Recreation 83,115 5,100 - - (78,015)

Program Revenues

-13-

Recreation 83,115 5,100 - - (78,015)

Total Governmental Activities 5,658,491$ 1,203,597$ 132,699$ 320,668$ (4,001,527)

General Revenues

TaxesProperty taxes 1,429,419

Bank deposits tax 71,550Telecommunications taxes 83,935Payroll license 1,420,512Insurance premium taxes 1,033,944

Gross receipts license 358,483

Licenses and permits 79,321Investment income 51,519Miscellaneous 17,980Fines and forfeitures 14,298

Loss on disposal of capital assets (82,977)

Total general revenues 4,477,984

Change in net position 476,457

Net position, beginning 21,833,868

Net position, ending 22,310,325$

The accompanying notes are an integral part of the financial statements.

-13-

CITY OF FORT MITCHELL, KENTUCKYBalance Sheet - Governmental FundsJune 30, 2013

Capital Other Total

General Road Tax Projects Municipal Governmental Governmental

Fund Fund Fund Road Aid Funds Funds

ASSETS

Cash and cash equivalents 7,123,430$ -$ -$ -$ 193,013$ 7,316,443$

Investments 1,907,881 - - - - 1,907,881

Receivables

Property taxes 59,606 17,584 - - 5,689 82,879

Assessments 24,668 - - - - 24,668

Intergovernmental 831,680 - - 18,494 - 850,174

Accounts - 759 - - - 759

Accrued investment income 3,829 - - - - 3,829

Prepaid expenses 14,882 - - - - 14,882

Due from other funds - 1,808,405 3,700,851 482,448 16,217 6,007,921

TOTAL ASSETS 9,965,976$ 1,826,748$ 3,700,851$ 500,942$ 214,919$ 16,209,436$

LIABILITIES AND FUND BALANCES

LIABILITIES

Accounts payable 151,498$ 293,957$ -$ 17,399$ 4,891$ 467,745$

Accrued liabilities 136,722 - - - 3,122 139,844

Deferred revenue 113,339 14,573 - - 4,685 132,597

Due to other funds 6,007,921 - - - - 6,007,921

TOTAL LIABILITIES 6,409,480 308,530 - 17,399 12,698 6,748,107

FUND BALANCES

Unspendable 14,882 - - - - 14,882

Restricted - - - 483,543 202,221 685,764

Committed - 1,518,218 3,700,851 - - 5,219,069

Stabilization 2,346,195 - - - - 2,346,195

Unassigned 1,195,419 - - - - 1,195,419

TOTAL FUND BALANCES 3,556,496 1,518,218 3,700,851 483,543 202,221 9,461,329

TOTAL LIABILITIES AND

FUND BALANCES 9,965,976$ 1,826,748$ 3,700,851$ 500,942$ 214,919$ 16,209,436$

The accompanying notes are an integral part of the financial statements.

-14-

Reconciliation of the Balance Sheet - Governmental Funds

to the Statement of Net Position

Amounts reported for governmental activities in the statement of net positionare different because:

Total fund balance per balance sheet 9,461,329$

Capital assets of $25,566,941, less accumulated depreciation of ($12,797,590),used in governmental activities are not financial resources and, therefore,are not reported in the funds. 12,769,351

Deferred charges represent funds received for future projects that will notrequire current funds and therefore are reported as deferred revenues inthe governmental funds 98,843

Long-term liabilities, including leases payable, are not due and payable in the

current period and therefore are not reported as liabilities in governmental funds.

Capital lease payable (19,198)

Net position of governmental activities 22,310,325$

The accompanying notes are an integral part of the financial statements.

CITY OF FORT MITCHELL, KENTUCKY

June 30, 2013

-15-

CITY OF FORT MITCHELL, KENTUCKYStatement of Revenues, Expenditures and Changes in Fund Balances -

Governmental FundsFor the Year Ended June 30, 2013

Capital Municipal Other Total

General Road Tax Projects Road Aid Governmental Governmental

Fund Fund Fund Fund Funds Funds

Revenues

Property tax 924,445$ 372,309$ -$ -$ 124,103$ 1,420,857$

Bank deposit tax 71,550 - - - - 71,550

Telecommunications tax 83,935 - - - - 83,935

Payroll license 1,420,512 - - - - 1,420,512

Insurance premium tax 1,033,944 - - - - 1,033,944

Gross receipts license 358,483 - - - - 358,483

Other licenses and permits 79,321 - - - - 79,321

Intergovernmental 152,440 79,257 - 204,093 2,650 438,440

Fines and forfeitures 14,298 - - - - 14,298

Charges for services 1,207,052 - - - - 1,207,052

Investment income 22,373 8,631 17,849 2,094 572 51,519

Contributions 14,927 - - - - 14,927

Sale of surplus property 11,955 - - - - 11,955

Miscellaneous 14,525 - - - - 14,525

Total Revenues 5,409,760 460,197 17,849 206,187 127,325 6,221,318

Expenditures

General government 761,114 - 30,400 - - 791,514

Police 1,455,755 - 84,643 - - 1,540,398

Fire and EMS 1,367,302 - 27,979 - - 1,395,281

Public works 839,806 741,115 - 70,137 75,302 1,726,360

Parks - - - - 80,773 80,773

Recreation 83,115 - - - - 83,115

Total Expenditures 4,507,092 741,115 143,022 70,137 156,075 5,617,441

Excess (Deficit) of Revenues

Over Expenditures 902,668 (280,918) (125,173) 136,050 (28,750) 603,877

Other Financing Sources (Uses)

Operating transfers in - 263,690 350,000 - - 613,690

Operating transfers out (545,000) - - - (68,690) (613,690)

Total Other Financing Sources (Uses) (545,000) 263,690 350,000 - (68,690) -

Excess (Deficit) of Revenues and

Other Financing Sources Over

(Under) Expenditures and

Other Financing Sources (Uses) 357,668 (17,228) 224,827 136,050 (97,440) 603,877

Fund Balance, beginning 3,198,828 1,535,446 3,476,024 347,493 299,661 8,857,452

Fund Balance, ending 3,556,496$ 1,518,218$ 3,700,851$ 483,543$ 202,221$ 9,461,329$

The accompanying notes are an integral part of the financial statements.

-16-

CITY OF FORT MITCHELL, KENTUCKYReconciliation of the Statement of Revenues, Expenditures

and Changes in Fund Balances - Governmental Funds

to the Statement of ActivitiesFor the Year Ended June 30, 2013

Amounts reported for governmental activities in the statement of activitiesare different because:

Net change in fund balance - total governmental funds 603,877$

Governmental funds report the entire net sales price (proceeds) from sale of an assetas revenue because it provides current financial resources. In contrast, theStatement of Activities reports on the gain or loss on the sale of the assets. Thus,the change in net position differs from the change in fund balance by the net bookvalue of the assets sold. (94,932)

Governmental funds report capital outlays as expenditures. However, for governmental

activities those costs are shown in the Statement of Net Position and allocated over

their estimated useful lives as annual depreciation expense in the statement ofactivities. This is the amount by which depreciation exceeds capital outlays in the period.

-17-

Capital outlays 999,056$Depreciation expense (1,059,304)

(60,248)

Governmental funds do not present revenues that are not available to pay currentobligations. In contrast, such revenues are reported in the Statement of Activitieswhen earned. 8,562

Repayment of capital lease payable principal is an expenditure in the governmentalfunds, but the repayment reduces long-term liabilities in the Statement of Net Position. 19,198

Change in net position of governmental activities 476,457$

The accompanying notes are an integral part of the financial statements.

-17-

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-18-

NOTE A – ACCOUNTING POLICIES

Kentucky Revised Statutes and Ordinances of the City Council of the City of Fort Mitchell, Kentucky(City) designate the purpose, function and restrictions of the various funds. The financial statementsincluded herein consist of the General, Capital Projects, Road Tax, Municipal Road Aid, Park, andStorm Sewer Contingency Funds.

Reporting Entity

The City, for financial purposes, includes all of the funds and account groups relevant to the operationsof the City of Fort Mitchell, Kentucky.

The financial statements of the City include those of separately administered organizations that arecontrolled by or dependent on the City. Control or dependence is determined on the basis of budgetadoption, taxing authority, funding and appointment of the respective governing board.

The City of Fort Mitchell, Kentucky is a Charter City, in which citizens elect the mayor at large and eightcouncil members. The accompanying financial statements present the City’s primary government.Component units are those over which the City exercises significant influence. Significant influence oraccountability is based primarily on operational or financial relationships with the City (as distinct fromlegal relationships). The City has no component units.

NOTE B – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of certain significant accounting policies followed in the preparation of thesefinancial statements.

Basis of Presentation Government-Wide Financial Statements

The government-wide financial statements (Statement of Net Position and Activities) report informationon all activities of the City as a whole. These statements include the financial activities of the primarygovernment. The statements distinguish between those activities of the City that are governmental andthose that are considered business-type activities. The City has no business-type activities.

The statement of activities presents a comparison between direct expenses and program revenues foreach function or program of the City’s governmental activities. Direct expenses are those that arespecifically associated with a service, program or department and are therefore clearly identifiable to aparticular function. Program revenues include charges paid by the recipient of the goods or servicesoffered by the program and grants and contributions that are restricted to meeting the operational orcapital requirements of a particular program. Revenues that are not classified as program revenuesare presented as general revenues of the City, with certain limited exceptions. The comparison ofdirect expenses with program revenues identifies the extent to which each governmental function isself-financing or draws from the general revenues of the City.

Amounts paid to acquire capital assets are capitalized as assets in the government-wide financialstatements, rather than reported as expenditures. Proceeds of long-term debt are recorded as aliability in the government-wide financial statements, rather than as another financing source. Amountspaid to reduce long-term indebtedness of the reporting government are reported as a reduction of therelated liability, rather than as expenditures.

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-19-

Measurement Focus, Basis of Accounting and Financial Statement Presentation

The government-wide financial statements are reported using the economic resources measurementfocus and the accrual basis of accounting. Revenues are recorded when earned and expenses arerecorded when a liability is incurred, regardless of the timing of related cash flows. Property taxes arerecognized as revenues in the year for which they are levied. Grants and similar items are recognizedas soon as all eligibility requirements imposed by the provider have been met.

Governmental fund financial statements are reported using the current financial resourcesmeasurement focus and the modified accrual basis of accounting. Revenues are recognized as soonas they are both measurable and available. Revenues are considered to be available when they arecollectible within the current period or soon enough thereafter to pay liabilities of the current period. Forthis purpose, the government considers revenues to be available if they are collected within 60 days ofthe end of the current fiscal period. Material revenues susceptible to accrual are payroll license fees,insurance fees and grant revenues. Expenditures generally are recorded when a liability is incurred, asunder accrual accounting. However, debt service expenditures, as well as expenditures related tocompensated absences and claims and judgments, are recorded only when payment is due.

Governmental Fund Types

The City reports the following governmental funds:

(A) The General Fund is the main operating fund of the City. It accounts for financial resources usedfor general types of operations. This is a budgeted fund, and any unrestricted fund balances areconsidered as resources available for use. This is a major fund of the City.

(B) The Road Tax Fund (a special revenue fund) is used to build and repair roads. This is a major fundof the City.

(C) The Capital Projects Fund (a special revenue fund) is used to make purchases of large capitalexpenditures. This is a major fund of the City.

(D) The Municipal Road Aid Fund (a special revenue fund) is funds received from the state to build andrepair roads. This is a major fund of the City.

(E) The Park Fund and the Storm Sewer Contingency Fund, are all nonmajor special revenue funds ofthe City.

Cash and Cash Equivalents

Cash and cash equivalents include amounts in demand deposits as well as short-term investments withan initial maturity date within three months of the date acquired by the City. The City is authorized bystate statute to invest in:

Obligations of the United States and of its Agencies and Instrumentalities Certificates of Deposit Banker’s Acceptances Commercial Paper Bonds of Other State or Local Governments Mutual Funds

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-20-

Investments

In accordance with the Government Accounting Standards Board, investments held at June 30, 2013are recorded at fair value based on quoted market prices.

Property Tax Receivable

Property taxes are levied as of January 1 on property values assessed as of the same date. The taxesare billed on approximately September 1 and are due and payable on October 31. On November 1, thebill becomes delinquent and penalties and interest may be assessed by the City. A lien may be placedon the property on November 1.

Prepaid Items

Payments made to vendors for services that will benefit periods beyond June 30, 2013 are recorded asprepaid items.

Capital Assets

General capital assets are assets that generally result from expenditures in the governmental funds.These assets are reported in the governmental activities column of the government-wide statement ofnet position.

The accounting and reporting treatment applied to capital assets associated with a fund are determinedby its measurement focus. General capital assets are long-lived assets of the City as a whole. Whenpurchased, such assets are recorded as expenditures in the governmental funds and capitalized.Infrastructure, such as streets, sidewalks and storm sewers are capitalized, including infrastructureacquired prior to the implementation of GASB. The valuation basis for general capital assets ishistorical costs, or where historical cost is not available, estimated historical cost based on replacementcost. Donated capital assets are recorded at their fair market value on the date donated. Repairs andmaintenance are recorded as expenses. Renewals and betterments are capitalized. The Citymaintains a capitalization threshold of two thousand dollars with the exception of infrastructure forwhich the threshold is five thousand dollars.

Capital assets used in operations are depreciated over their estimated useful lives using the straightline method in the government-wide financial statements. Depreciation is charged as an expenseagainst operations and accumulated depreciation is reported on the respective balance sheet.

The range of useful lives used for depreciation purposes for each fixed asset class is as follows:Governmental Activities

Description Estimated Lives

Buildings 20 - 28 Years

Buildings and Land Improvements 7 - 20 Years

Public Domain Infrastructure 25 - 30 Years

Vehicles 5 - 20 Years

Equipment and Furniture 5 - 20 Years

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-21-

Budgets

Budgets are adopted on a basis consistent with generally accepted accounting principles. Annualappropriated budgets are adopted for all governmental funds. All annual appropriations continue ineffect until a new budget is adopted.

Compensated Absences

Vested or accumulated vacation leave that is expected to be liquidated with expendable availablefinancial resources is reported as expenditures and a fund liability of the governmental fund that will payit. At June 30, 2013 the liability for compensated absences is $54,773.

Accrued Liabilities and Long-term Obligations

All payables, accrued liabilities and long-term obligations are reported in the government-wide financialstatements.

Long-term debt for governmental funds is not reported as a liability in the fund financial statements.The debt proceeds are reported as revenue and payment of principal and interest reported asexpenditures.

Unearned/Deferred Revenue

In the government-wide financial statements, unearned revenue represents the amount for whichrevenue recognition criteria have not been met. In subsequent periods, when the incurrence ofqualifying expenditures has been made, the liability for the unearned revenues is removed and therevenue is recognized. In the governmental fund financial statements, revenues are deferred foramounts that are unearned or unavailable within 60 days of the fiscal year end.

Fund Equity

Net position is the difference between assets and liabilities. Assets invested in capital assets, net ofrelated debt are capital assets, less accumulated depreciation and any outstanding debt related to theacquisition, construction or improvement of those assets.

The City uses funds and account groups to report on its financial position and the result of itsoperations. Fund accounting is designed to demonstrate legal compliance and to aid financialmanagement by segregating transactions related to certain governmental functions or activities.

Nonspendable fund balances consist of amounts that are not in spendable form; the City considersprepaid expenses to be non-spendable.

Restricted fund balances are amounts that can only be used pursuant to constraints imposed byexternal sources; such as state government restrictions or the funds restricted by the will of the City’svoters. These include residual balances from the Kentucky Municipal Aid Road and Park Funds.

Committed fund balances are amounts that can only be used for specific purposes as stipulatedinternally by the City Council. These items can only be changed or lifted by the Council taking the

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-22-

same formal action that imposed the restraint. These include residual balances from the Road Tax,Capital Project, and Storm Sewer Contingency.

Assigned fund balances consists of funds that are set aside with the intent to be used for a specificpurpose by the City’s highest level of decision making authority or a body or official that has been giventhe authority to assign funds. The City has no balances that are considered to be assigned.

Stabilization fund balances are set aside by an ordinance of the City Council for the purpose ofproviding funds for an urgent event that affects the safety of the general public (e.g. flood, tornado,etc.), for unexpected revenue declines that are projected to continue for more than 2 years, forunanticipated one-time expenditures that are deemed necessary or in the City’s best interest orsignificant expenditures where the fund will be reimbursed within 12 months. Stabilization fundbalances will not be used to fund operating or regular capital expenditures that should otherwise befunded with operating revenues and reserves. The minimum and maximum level of the stabilizationfund balance is two and six months, respectively, of the most current budgeted expenditures. Allrequests for use of or an addition to the General Fund stabilization fund balance will be included in thebudget presented and approved by the City Council. Any proposed appropriation that would result inthe balance of the Stabilization Fund dropping below the established minimum fund balance must besubmitted with a plan to restore the minimum Stabilization Fund balance within two years.

Unassigned fund balances consist of all residual funds not included in nonspendable, restricted,committed, or assigned fund balances.

Operating Revenues and Expenditures

Operating revenues and expenditures are reported by fund. It also includes all revenue andexpenditures related to capital and related financing or investing activities.

Expenditures/Expenses

In the government-wide financial statements, expenses are classified by function for governmentalactivities. In the fund financial statements, governmental funds report expenditures of financialresources.

Use of Estimates

The process of preparing financial statements in conformity with U.S. generally accepted accountingprinciples requires management to make estimates and assumptions that affect reported amounts ofassets, liabilities, designated fund balances, and disclosure of contingent assets and liabilities at thedate of the financial statements, and the reported amounts of revenues and expenditures during thereporting period. Actual results could differ from those estimates.

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-23-

NOTE C – STEWARDSHIP, COMPLIANCE AND ACCOUNTABILITY

The City follows these procedures in establishing the budgetary data reflected in the financialstatements:

1) In accordance with Kentucky Revised Statutes and City ordinance, prior to May 31, the Mayorsubmits to the City Council a proposed operating budget on the modified accrual basis ofaccounting for the fiscal year commencing the following July 1. The operating budget includesproposed expenditures and the means of financing them for the upcoming year.

2) A public meeting is conducted to obtain citizen comment.

3) By July 1, the budget is legally enacted through passage of an ordinance.

4) The Mayor is required by Kentucky Revised Statutes to present a quarterly report to the CityCouncil explaining any variance from the approved budget.

5) Appropriations continue in effect until a new budget is adopted.

6) The City Council may authorize supplemental appropriations during the year.

Expenditures may not legally exceed budgeted appropriations at the function level. Any revisions to thebudget that would alter total revenues and expenditures of any fund must be approved by the Council.The Council adopted one supplementary appropriation ordinance during the year. All appropriationslapse at fiscal year end.

NOTE D – CASH, CASH EQUIVALENTS, AND INVESTMENTS

Cash and Cash Equivalents

At June 30, 2013, the City’s cash equivalents (bank deposits, money market accounts and certificatesof deposit with less than 90 days maturity and cash on hand) had a carrying amount of $7,316,444 anda bank balance of $7,423,140, the difference being items that had not cleared the bank, and petty cash,at June 30, 2013.

All of the City’s cash equivalents with the exception of petty cash are insured by the FDIC or arecollateralized with securities held by the pledging institution’s trust department in the City’s name orowned directly by the City. As of June 30, 2013, the City did not have any deposits in excess of insuredand/or collateralized amounts.

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-24-

Investments

As of June 30, 2013, the City had the following investment balances:

Unrealized Fair Market

Description Cost Gains/Losses Value

Government Securities 1,200,496$ (29,168)$ 1,171,328$

Certificates of Deposit 736,553 - 736,553

1,937,049$ (29,168)$ 1,907,881$

As of June 30, 2013, $701,734 of the City’s investment is insured by FDIC, $34,618 is collateralizedwith securities held by the pledging institutions trust department in the City’s name. The remaining$1,171,328 are government securities owned by the City.

Custodial Credit Risk and Investment Policy

It is the policy of the City to invest public funds in a manner that will provide the highest investmentreturn with the maximum security of principal while meeting the daily cash flow demands of the City andconforming to all state statutes and City regulations governing the investments of public funds.

For deposits, custodial credit risk is the risk that in the event of the failure of the counterparty, the Citywill be able to recover the value of its cash, investments or collateral securities that are in thepossession of an outside party. All deposits and investments are made in accordance with statestatutes.

The City Treasurer shall maintain a list of financial institutions authorized to provide investment servicesto the City. In addition, a list shall be maintained of approved security brokers/dealers selected bycreditworthiness who maintain an office in the Commonwealth of Kentucky.

No financial institution shall be selected as a depository of the City funds if the City funds on deposit atany time will exceed ten percent (10%) of the institution’s capital stock and surplus. The City Treasurershall evaluate the financial capacity and creditworthiness of financial institutions and broker/dealersprior to the placement of the City’s funds. The City Treasurer shall conduct an annual review of thefinancial condition and registrations of financial institutions and broker/dealers, and based on thereview, make any recommendations regarding investment policy or program changes determined to benecessary.

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-25-

NOTE E – CAPITAL ASSETS

Capital asset activity for the fiscal year ended June 30, 2013 was as follows:

Depreciation was charged to functions as follows:

Governmental Activities Amount

General Government 24,293$

Police 89,761

Fire and EMS 158,331

Public Works 750,832

Park 36,087

Total Depreciation 1,059,304$

Balance at Balance at

June 30, June 30,

2012 Additions Deletions 2013

Governmental Activities

Capital Assets not Depreciated

Land 590,078$ -$ -$ 590,078$

Construction in progress 1,159,259 73,841 (1,072,810) 160,290

Total Capital Assets Not

Being Depreciated 1,749,337 73,841 (1,072,810) 750,368

Depreciable Capital Assets

Infrastructure 17,124,686 1,847,073 (166,180) 18,805,579

Buildings 643,097 - (2) 643,095

Buildings/land improvements 1,187,415 - - 1,187,415

Equipment 1,758,420 29,100 (32,205) 1,755,315

Furniture and fixtures 232,277 - (1,288) 230,989

Vehicles 2,305,057 121,853 (232,730) 2,194,180

Total Depreciable Capital Assets 23,250,952 1,998,026 (432,405) 24,816,573

Total Capital Assets at

Historical Cost 25,000,289 2,071,867 (1,505,215) 25,566,941

Less Accumulated Depreciation

Infrastructure 7,358,423 717,578 (73,119) 8,002,882

Buildings 621,797 6,591 - 628,388

Buildings/land improvements 972,644 22,739 - 995,383

Equipment 1,411,263 136,558 (30,901) 1,516,920

Furniture and fixtures 208,964 8,091 (722) 216,333

Vehicles 1,502,667 167,747 (232,730) 1,437,684

Total Accumulated Depreciation 12,075,758 1,059,304 (337,472) 12,797,590

Depreciable Captial Assets, Net 11,175,194 938,722 (94,933) 12,018,983

Total Capital Assets, Net 12,924,531$ 1,012,563$ (1,167,743)$ 12,769,351$

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-26-

NOTE F – LONG TERM DEBT

Mobile Data Terminal Financing

Kenton County provided mobile data terminals (MDTs) for the City’s police department in July 2004.The City owns the MDTs and will pay Kenton County for them over a period of ten years in the amountof $19,198 per year. Kenton County is not charging interest on the financing of the MDTs.

Maturities

The remaining maturities on the Mobile Data Terminal Financing are as follows:

Fiscal Year

Ending June 30, Total

2014 19,198$

Total 19,198$

Summary of General Long-Term Debt

The following is a summary of the City’s long-term debt transactions for the year ended June 30, 2013:

Balance Retirements/ Balance Amounts Due

June 30, 2012 Additions Repayments June 30, 2013 Within 1 Year

MDT Financing 38,396$ -$ 19,198$ 19,198$ 19,198$

Total 38,396$ -$ 19,198$ 19,198$ 19,198$

NOTE G – EMPLOYEE’S RETIREMENT SYSTEM

County Employees Retirement System (CERS)

City employees who work at least 100 hours per month participate in the County Employees RetirementSystem (CERS). Under the provisions of the Kentucky Revised Statute 61.645, the Board of Trusteesof Kentucky Retirement Systems administers the CERS.

The plan issues separate financial statements which may be obtained by request from KentuckyRetirement Systems, 1260 Louisville Road, Frankfort, Kentucky 40601.

Plan Description – CERS is a cost-sharing multiple-employer defined benefit pension plan that coverssubstantially all regular full-time members employed in positions of each county and school board, andany additional eligible local agencies electing to participate in the System. The plan provides forretirement, disability, and death benefits to plan members. Retirement benefits may be extended tobeneficiaries of plan members under certain circumstances. Cost-of-Living Adjustments (COLA) areprovided at the discretion of the state legislature.

Non-Hazardous Contributions – For the year ended June 30, 2013, plan members were required tocontribute 5.0% of their annual creditable compensation. Employees hired after August 31, 2008 andnot already in the retirement system must contribute an extra 1%. Participating employers wererequired to contribute at an actuarially determined rate. Per Kentucky Revised Statute Section

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-27-

61.565(3), normal contribution and past service contribution rates shall be determined by the Board onthe basis of an annual valuation last proceeding the July 1 of a new biennium. The Board may amendcontribution rates as of the first day of July of the second year of a biennium, if it is determined on thebasis of a subsequent actuarial valuation that amended contribution rates necessary to satisfyrequirements determined in accordance with actuarial bases adopted by the Board. For the year endedJune 30, 2013, participating employers contributed 19.55% of each employee’s creditablecompensation. Administrative costs of CERS are financed through employer contributions andinvestment earnings.

Hazardous Contributions – For the year ended June 30, 2013, plan members were required tocontribute 8.0% of their annual creditable compensation. Employees hired after August 31, 2008 andnot already in the retirement system must contribute an additional 1%. The state was required tocontribute at an actuarially determined rate. Per Kentucky Revised Statute Section 61.565(3), normalcontribution and past service contribution rates shall be determined by the Board on the basis of anannual valuation last proceeding the July 1 of a new biennium. The Board may amend contributionrates as of the first day of July of the second year of a biennium, if it is determined on the basis of asubsequent actuarial valuation that amended contribution rates are necessary to satisfy requirementsdetermined in accordance with actuarial bases adopted by the Board. For the year ended June 30,2013, participating employers contributed 37.60% of each employee’s creditable compensation.Administrative costs of CERS are financed through employer contributions and investment earnings.

The required contribution and the actual percentage contributed by the City for the current and previousfive years are as follows:

Required Percentage

Year Contribution Contributed

2013 589,984$ 100%

2012 533,272 100%

2011 499,849 100%

2010 524,011 100%

2009 432,391 100%

2008 472,593 100%

Deferred Compensation Plan

The City also participates in 401(k) & 457 plans administered by the Kentucky Employees DeferredCompensation Authority. All payments to the Authority are payroll withheld. The City does notcontribute to the plan for any employee.

NOTE H – RISK MANAGEMENT

The City is exposed to various risks of losses related to torts; theft of, damage to, and destruction ofassets; errors and omissions; injuries to employees, and natural disasters. The City has obtainedinsurance coverage through a commercial insurance company. In addition, the City has effectivelymanaged risk through various employee education and prevention programs. All general liabilitymanagement activities are accounted for in the General Fund. Expenditures and claims are recognizedwhen probable that a loss has occurred and the amount of loss can be reasonably estimated.

CITY OF FORT MITCHELL, KENTUCKYNotes to Financial StatementsJune 30, 2013

-28-

Management estimates that the amount of actual or potential claims against the City as of June 30,2013 will not materially affect the financial condition of the City. Therefore, the General Fund containsno provision for estimated claims. No claim has exceeded insurance coverage amounts in the pastthree fiscal years.

NOTE I – CLAIMS AND JUDGMENTS

Amounts received, or receivable, from grantor agencies are subject to audit and adjustment by grantoragencies, principally the federal and state governments. Any disallowed claims, including amountsalready collected, may constitute a liability of the applicable funds. The amount, if any, of expenditureswhich may be disallowed by the grantor cannot be determined at this time although the City expectssuch amounts, if any, to be immaterial.

NOTE J – FIRE AND LIFE SQUAD PROTECTION

The Cities of Lakeside Park and Crestview Hills utilize the services of Fort Mitchell, Kentucky for fireand life squad protection. These agreements were renewed April 1, 2009 for a four year term, expiringMarch 31, 2013. Revenue to the City for these contracts totaled $324,263 for the fiscal year endedJune 30, 2013.

NOTE K – CONDUIT DEBT

The City of Fort Mitchell is participating in a program established by the Kentucky League of Cities toallow other Kentucky cities access to economical financing by issuing bonds, through the program, inthe name of the City of Fort Mitchell. The bonds are issued pursuant to a Trust Indenture and arepayable solely and secured solely by the Trust Estate and monies drawn under an irrevocable letter ofcredit from a bank. The City of Fort Mitchell has no obligation under these bonds, although the City isthe nominal issuer of the bonds. The amount of bonds outstanding at June 30, 2013 is $25,255,000.

NOTE L – INTERFUND ACTIVITY

Transfers are typically used to move unrestricted revenues collected in one fund to finance variousprograms accounted for in another fund in accordance with budgetary authorizations and to fund debtservice payments when they become due.

Tranfer From Transfer To Amount

General Road Tax 195,000$

General Capital Projects 350,000

Storm Sewer Road Tax 68,690

613,690$

NOTE M – SUBSEQUENT EVENTS

Management has evaluated events through January 15, 2014, the date on which the financialstatements were available for issue. The City did not have any events subsequent to June 30, 2013through January 15, 2014 to disclose.

CITY OF FORT MITCHELL, KENTUCKYStatement of Revenues, Expenditures and Changes in Fund Balance -

Budget and Actual (With Variances) - General FundFor the Year Ended June 30, 2013

Variance

Original Final Favorable

Budget Amendments Budget Actual (Unfavorable)

Budgetary fund balance, July 1 2,913,528$ 285,300$ 3,198,828$ 3,198,828$ -$

Resources (inflows):

Property tax 934,950 (20,824) 914,126 924,445 10,319

Bank deposit tax 63,870 7,680 71,550 71,550 -

Telecommunications tax 79,500 (2,042) 77,458 83,935 6,477

Payroll license 1,254,540 115,460 1,370,000 1,420,512 50,512

Insurance premium tax 1,264,420 (292,420) 972,000 1,033,944 61,944

Gross receipts license 272,950 27,050 300,000 358,483 58,483

Other licenses and permits 83,750 (250) 83,500 79,321 (4,179)

Intergovernmental 176,000 (25,000) 151,000 152,440 1,440

Fines and forfeitures 16,500 (1,750) 14,750 14,298 (452)

Charges for services 1,175,044 28,910 1,203,954 1,203,597 (357)

Investment income 40,000 (8,000) 32,000 22,373 (9,627)

Contributions 2,600 15,400 18,000 14,927 (3,073)

Gain on sale of capital assets 15,000 (3,045) 11,955 11,955 -

Miscellaneous 10,500 8,322 18,822 17,980 (842)

Total resources (inflows) 5,389,624 (150,509) 5,239,115 5,409,760 170,645

Amounts available for appropriation 8,303,152 134,791 8,437,943 8,608,588 170,645

Charges to appropriations (outflows):

General government 847,973 (55,484) 792,489 761,114 31,375

Police 1,652,131 (113,766) 1,538,365 1,455,755 82,610

Fire and EMS 1,444,930 (50,477) 1,394,453 1,367,302 27,151

Public works 1,039,380 (164,948) 874,432 839,806 34,626

Recreation 98,042 (5,390) 92,652 83,115 9,537

Total charges to appropriations 5,082,456 (390,065) 4,692,391 4,507,092 185,299

Interfund transfers (250,000) (295,000) (545,000) (545,000) -

Budgetary fund balance, June 30 2,970,696$ 229,856$ 3,200,552$ 3,556,496$ 355,944$

The accompanying notes are an integral part of the financial statements.

-29-

CITY OF FORT MITCHELL, KENTUCKYStatement of Revenues, Expenditures and Changes in Fund Balance -

Budget and Actual (With Variances) - Road Tax FundFor the Year Ended June 30, 2013

Variance

Original Final Favorable

Budget Amendments Budget Actual (Unfavorable)

Budgetary fund balance, July 1 1,407,905$ 127,541$ 1,535,446$ 1,535,446$ -$

Resources (inflows):

Property taxes 378,000 (8,000) 370,000 372,309 2,309

Intergovernmental - - - 79,257 79,257

Investment income 5,000 5,000 10,000 8,631 (1,369)

Total resources (inflows) 383,000 (3,000) 380,000 460,197 80,197

Amounts available for appropriation 1,790,905 124,541 1,915,446 1,995,643 80,197

Charges to appropriations (outflows):

Capital outlay

Public works 1,671,045 (858,326) 812,719 741,115 71,604

Total charges to appropriations 1,671,045 (858,326) 812,719 741,115 71,604

Interund transfers 75,000 192,658 267,658 263,690 (3,968)

Budgetary fund balance, June 30 194,860$ 1,175,525$ 1,370,385$ 1,518,218$ 147,833$

The accompanying notes are an integral part of the financial statements.

-30-

CITY OF FORT MITCHELL, KENTUCKYStatement of Revenues, Expenditures and Changes in Fund Balance -

Budget and Actual (With Variances) - Capital Projects FundFor the Year Ended June 30, 2013

Variance

Original Final Favorable

Budget Amendments Budget Actual (Unfavorable)

Budgetary fund balance, July 1 3,379,062$ 96,962$ 3,476,024$ 3,476,024$ -$

Resources (inflows):

Investment income 25,000 (5,000) 20,000 17,849 (2,151)

Total resources (inflows) 25,000 (5,000) 20,000 17,849 (2,151)

Amounts available for appropriation 3,404,062 91,962 3,496,024 3,493,873 (2,151)

Charges to appropriations (outflows):

General government 111,750 (50,757) 60,993 30,400 30,593

Police 90,000 (5,357) 84,643 84,643 -

Fire and EMS 30,000 (2,021) 27,979 27,979 -

Total charges to appropriations 231,750 (58,135) 173,615 143,022 30,593

Interund transfers 75,000 275,000 350,000 350,000 -

Budgetary fund balance, June 30 3,247,312$ 425,097$ 3,672,409$ 3,700,851$ 28,442$

The accompanying notes are an integral part of the financial statements.

-31-

CITY OF FORT MITCHELL, KENTUCKYStatement of Revenues, Expenditures and Changes in Fund Balance -

Budget and Actual (With Variances) - Municipal Road Aid FundFor the Year Ended June 30, 2013

Variance

Original Final Favorable

Budget Amendments Budget Actual (Unfavorable)

Budgetary fund balance, July 1 282,277$ 65,216$ 347,493$ 347,493$ -$

Resources (inflows):

Intergovernmental 170,000 25,000 195,000 204,093 9,093

Investment income 1,400 324 1,724 2,094 370

Total resources (inflows) 171,400 25,324 196,724 206,187 9,463

Amounts available for appropriation 453,677 90,540 544,217 553,680 9,463

Charges to appropriations (outflows):

Public works 165,300 (95,100) 70,200 70,137 63

Total charges to appropriations 165,300 (95,100) 70,200 70,137 63

Interund transfers - - - - -

Budgetary fund balance, June 30 288,377$ 185,640$ 474,017$ 483,543$ 9,526$

The accompanying notes are an integral part of the financial statements.

-32-

CITY OF FORT MITCHELL, KENTUCKYCombining Balance Sheet - Non-Major Governmental FundsJune 30, 2013

Storm Sewer Total

Contingency Park Tax Non-Major

Fund Fund Funds

ASSETS

Cash and cash equivalents -$ 193,013$ 193,013$

Accounts receivable

Property taxes - 5,689 5,689

Due from other funds - 16,217 16,217

TOTAL ASSETS -$ 214,919$ 214,919$

LIABILITIES AND FUND BALANCES

LIABILITIES

Accounts payable -$ 4,891$ 4,891$

Accrued liabilities - 3,122 3,122

Deferred revenue - 4,685 4,685

TOTAL LIABILITIES - 12,698 12,698

FUND BALANCES

Restricted - 202,221 202,221

TOTAL FUND BALANCES - 202,221 202,221

TOTAL LIABILITIES AND

FUND BALANCES -$ 214,919$ 214,919$

The accompanying notes are an integral part of the financial statements.

-33-

CITY OF FORT MITCHELL, KENTUCKYCombining Statement of Revenues, Expenditures and Changes in Fund Balance -

Non-Major Governmental FundsFor the Year Ended June 30, 2013

Storm Sewer Total

Contingency Park Tax Non-Major

Fund Fund Funds

Revenues

Property taxes -$ 124,103$ 124,103$

Intergovernmental 2,650 - 2,650

Investment income - 572 572

Total Revenues 2,650 124,675 127,325

Expenditures

Public works 75,302 - 75,302

Parks - 80,773 80,773

Total Expenditures 75,302 80,773 156,075

Excess of Revenues Over Expenditures (72,652) 43,902 (28,750)

Other Financing Sources (Uses)

Operating transfers out (68,690) - (68,690)

Total Other Financing Sources (Uses) (68,690) - (68,690)

Excess (Deficit) of Revenues and

Other Financing Sources (Uses) Over

(Under) Expenditures and Other

Financing Uses (141,342) 43,902 (97,440)

Fund Balance, beginning 141,342 158,319 299,661

Fund Balance, ending -$ 202,221$ 202,221$

The accompanying notes are an integral part of the financial statements.

-34-

CITY OF FORT MITCHELL, KENTUCKYStatement of Revenues, Expenditures and Changes in Fund Balance -

Budget and Actual (With Variances) - Park Tax Special Revenue FundFor the Year Ended June 30, 2013

Variance

Original Final Favorable

Budget Amendments Budget Actual (Unfavorable)

Budgetary fund balance, July 1 113,040$ 45,279$ 158,319$ 158,319$ -$

Resources (inflows):

Property taxes 120,000 3,500 123,500 124,103 603

Intergovernmental 35,000 (35,000) - - -

Investment income 250 (50) 200 572 372

Total resources (inflows) 155,250 (31,550) 123,700 124,675 975

Amounts available for appropriation 268,290 13,729 282,019 282,994 975

Charges to appropriations (outflows):

Parks 191,080 (94,521) 96,559 80,773 15,786

Total charges to appropriations 191,080 (94,521) 96,559 80,773 15,786

Transfers to other funds - - - - -

Budgetary fund balance, June 30 77,210$ 108,250$ 185,460$ 202,221$ 16,761$

The accompanying notes are an integral part of the financial statements.

-35-

CITY OF FORT MITCHELL, KENTUCKYStatement of Revenues, Expenditures and Changes in Fund Balance -Budget and Actual (With Variances) - Storm Sewer Contingency Special Revenue FundFor the Year Ended June 30, 2013

Variance

Original Final Favorable

Budget Amendments Budget Actual (Unfavorable)

Budgetary fund balance, July 1 10,479$ 130,863$ 141,342$ 141,342$ -$

Resources (inflows):

Intergovernmental 17,015 9,301 26,316 2,650 (23,666)

Miscellaneous 5,633 (5,633) - - -

Total resources (inflows) 22,648 3,668 26,316 2,650 (23,666)

Amounts available for appropriation 33,127 134,531 167,658 143,992 (23,666)

Charges to appropriations (outflows):

Public works 111,000 (16,000) 95,000 75,302 19,698

Total charges to appropriations 111,000 (16,000) 95,000 75,302 19,698

Transfers (to) from other funds 100,000 (172,658) (72,658) (68,690) 3,968

Budgetary fund balance, June 30 22,127$ (22,127)$ -$ -$ -$

The accompanying notes are an integral part of the financial statements.

-36-

van Gorder, Walker & Co., Inc.

IN DEPEN DENT AUDITOR'S REPORT ON INTERNALCONTROL OVER FJNANCIALREPORTING AND ON COIMPLIANCE AND OTHER IVIATTERS BASED ON AN AUDIT OF

RFORIIIED IN ACCORDANCE WIT H GOVER NMEN fAUDI|ING SIANDARDS

To the Honorable lMayor andilembers of CouncilofCity ot Forl [ritchell, Kenlucky

We have audted n accordance wth the audil nq standards ge.erely eccepled n llre UnitedSlales of America and llre slafdards app cabe lo linanca audis co.taned n GoyearerlAtdrting stand.tds ssued by the cohplrcler Gefera of lhe unted states. th€ fnan.alstalemenls of the governmenla aciivities and each najor tund of the cry of For. Milch€lKentucky as ol June 30 2013 and the re ated foles lo the fifanca slatements whichc.ll€ctvely compfse the Cly of Ft Milchel Kentuckys lifanca slalenents and have ssuedolrrepodlhereon daled JanLary 15 2014

Inlernal Conlrol over Financial Repollinq

hpannnga.dper lo rn .gouraud i tso f the inanca s ta temenls we consdered C i ly o f For rMitchel Kenllckys inlerfa con1rcl over nnancal reponng (nterna conlro)lo delermne th€aud I prccedu.€s thal aE appropfate n the cfcumslances for the purpose ol€xpressn! ouropln.ns on the liiaica sblemenls but notlorihe purpose olexpressng an opifon on ttreefieclv€ness ol City of Fon N,l tchel K€nluckys rnl€rnal contro. Accordifg y we do iolexpress an opnlon on the effecl veness of cily oJ Forr [,] rchei , Kentudky s,n1€rnarcontro]

A delicienc! in intErnal connolex sts when ihe design of operaton of a conlrot does not a owmanagemenl or empoyees n the nomal cours€ of performlng lher assqned funclions. lopretenl or del€ct and corecl misstatenents on a lmely bass A nalerdl rle.lrcss s adefcency. of combinalon of defcences n intema cantro such that there ls a reascnabt€poss bi ly lrrat a mal€rai misslal€men ol the entity s liiaic a slat€menrs wr nor be preventcd.or del€cted and corecled on a lmely bass. A stgnilicant.lehciency s a delcency or acomb nation of deficiencies, in inlernalconlrc thal s l€ss seve€ lhaf a maleralweakness, yetrmpodanl e.ough io fferil attention by rhose charged wth lov€rfance

Our consideration of nternal conlroi was for lhe imited p!rpose described n lhenrsl paragraphor th s s€cl on and was no1 des qned to denlfyaldefcefces n ntema conlrctthai miqht be

or s rgn i fcan t de l i cendes.nd there fore materaslgnncanl d€Jiciencles may exst thal were not identifed. Given rhese fiilalons dufngouraudl we did nol dentify any deliciencres in ifierna contro that we consd€r lo be mal€riaw€aknesses fiowever, nateial weaknesses may ex sl thal have not been identt€d

37 ,

. Ph ! l!s)rl rn,0

Van Gorder, Walker & Co.. Inc.

a!-!rdi3!.9scJ'!

As pan of obtaifing reasonable assuBnce about wheih€rthe Cily ol Fort l,lilchel. Kentucky siinanci.l siaiements are rtree oJ maleria misstatemed we pertormed tesls of ts cofrplancewirh €dan provisions of aws, regulaiions 6ontracls and graft asreements. noncomplancewilh whch c.uld have a drect and materialetrecl on the detemnalon or linancia stal€henlamounls. H5wever. providing an opnion on compiance with lhose provisions was nol a.obiective of our aodits, and acco.dinqy, wedo notexpress such an opinion. The resuls of ou.tesls ds.losed.o instances ofnoncompliance orolhermatlers that ae r€quired 1o be repoftedurdet Gavemnonl Auditing StandanJs.

!.u!p9s.9-9!!.9ie!sd

The Furtrose ol lh s .epod s so ely lo descrbe the scope of our lestng of nterna conlro zndcofrp iance a.d the resulls oflhat testing, a.d not to provide an opin on on lhe eifeci v€ness ollhe enlilys iniemal conlrol or on compliance. Thls repon is an irlegra parl ot an ludiperfomed in accordance wllh Govennenl Auditins Siada/ds ln conslden.s the enritysnlernaiconlmland complance. Accodingly lhis commlnicllio. is not sulabe lof a.y oih€r

{,4.-4.-A*. (,-;--^-z-* * G.. d-.^,van Gorder, Walker, & co,,Inc.