classification of capital by asst prof. jonlen desa

TRANSCRIPT

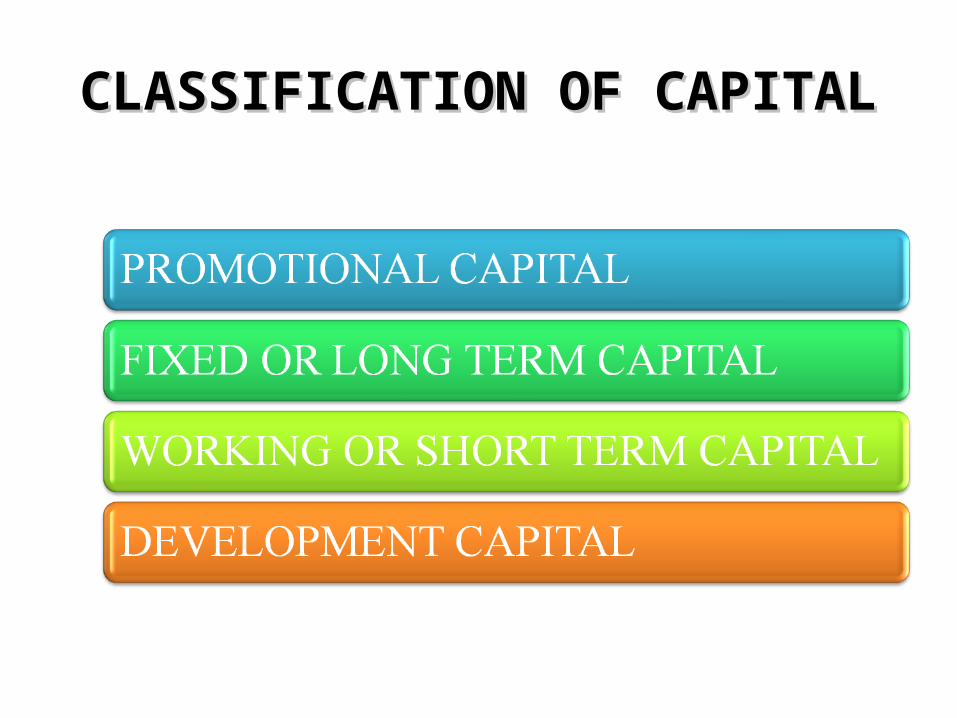

CLASSIFICATIONCLASSIFICATION OFOF CAPITALCAPITAL

ASST PROF. JONLEN DESA

CAPITALCAPITAL

Capital refers to the funds or money required by an enterprise to carry out its activities.

Capital refers to the financial resources available for use.

CLASSIFICATION OF CAPITALCLASSIFICATION OF CAPITAL

CAPITAL REQUIREMENTCAPITAL REQUIREMENT

Capital requirement refers to the amount of funds required by the company for various purposes.

The amount of capital required depends on various factors.

FACTORS DETERMINING CAPITAL REQUIREMENTS

Nature of business activity (Scale, Location, Technology)

Size of the business unit Nature of the product Technology used in manufacturing (Labour & Capital Intensive)

Miscellaneous factorsPosition of business cycle (Boom, Recession, Depression, Recovery)

Location of the company

Position of inflation

FIXED CAPITAL REQUIREMENTFIXED CAPITAL REQUIREMENT

Fixed Capital is also known as Long term capital. Fixed capital is the amount of capital required for

purchasing fixed assets. It acts a cornerstone of the capital structure of a

company. It is used for purchasing, maintaining and replacing

fixed assets. The amount of fixed capital required varies from

company to company and its requirements depend on various factors.

FIXED CAPITALFIXED CAPITAL

Fixed capital can be used for the following purposes:

Purchase of intangible assets

Long term Investment

Fixed capital is required in the initial period of manufacturing.

Additional fixed capital is also required for expansion, modernization & diversification activities.

The promoters make an estimate in advance about the amount of fixed capital required for fixed assets in the financial or capital component of the business plan.

DEFINITION

According to Hoagland, “ Fixed capital is comparatively easily defined to include land, building, machinery & other assets having a relatively permanent existence.”

FEATURES Needed for meeting long term needs Needed at the initial period Withdrawal not possible due to its permanent nature Collected from varied sources Requirement is variable Appreciation & depreciation of fixed capital is

possible. Low liquidity Needs long term planning

FACTORS AFFECTING FIXED CAPITAL REQUIREMENT

Nature of business activity Size of business unit Scale of operations Type of product manufactured Method of manufacturing (Technology used) Method of acquiring fixed assets Government subsidy

IMPORTANCE OF ADEQUATE FIXED CAPITAL.

Every business needs adequate fixed capital. Adequate means as per the needs & requirements of a

business. The fixed capital of a firm should be always adequate

and neither excess nor less. Adequate fixed capital of a business acts as a

cornerstone of the capital structure of a business firm.

Fixed capital helps the firm purchase the required fixed assets for the purpose of manufacturing activity.

It is important as it helps the firm in smooth functioning, expansion, diversification and modernization.

It brings about stability, growth and prosperity with the help of adequate fixed capital.

ADVANTAGES

Provides basic requirement of business Ensures orderly functioning Facilitates replacement of obsolete assets Supports expansion & diversification programmes Supports manufacturing activites

SOURCES OF FIXED CAPITAL

Issue of equity shares Issue of preference shares Ploughing back of profits Loans from specialized financial institutions Issue of debentures Bank loans Lease financing Right Issue Venture Capital

WORKING CAPITAL REQUIREMENTWORKING CAPITAL REQUIREMENT

In addition to fixed capital, every business firm requires working capital for meeting the day to day expenses of the firm.

Working capital is also known as short term capital. It is required to purchase current assets. Currents assets are of a temporary nature. Working capital is required for a short period of

time and it is temporary in nature.

Working capital is required for a short period of time as it is recovered form the customers when products are sold to them.

A business firm requires adequate working capital for its continuous & orderly functioning.

It raises morale of employees and ensures cordial relations with suppliers and creditors.

Working capital is also known as circulating capital and it involves a circular flow of cash.

It starts with cash paid for purchasing raw materials and ends with cash receipt after the sale of goods.

WORKING CAPITAL IS USED FOR:

Purchase of raw materials and stores Payment of wages Payment of electricity, water & telephone charges Payment of factory expenses Payment of taxes and insurance

Thus it is used for running the day to day operations of the firm smoothly.

Working capital is needed because there is a time gap between purchases & production, production & sales and sales & realization of cash

During these intervals, company requires cash to keep the business running.

Hence working capital is required as long as production and selling activities are undertaken by the business enterprise.

WORKING CAPITAL CYCLEWORKING CAPITAL CYCLE

FEATURESFEATURES

Used for meeting regular needs Needed for short period Varying amount Fluctuating in nature Easily convertible Ensures orderly working Collection from different sources Integral aspect of capital structure Concepts of working capital (Gross & Net)

FACTORS AFFECTING WORKING CAPITAL REQUIREMENT

Nature of business Size of the business Time consumed in manufacturing process Speed of turnover of circulating capital Position of business cycle Terms of purchase and sale

FACTORS AFFECTING WORKING CAPITAL REQUIREMENT

Dividend policy Cost of raw material Importance of labour in manufacturing Seasonal Variations Banking Connections Cash Requirements

SIGNIFICANCE OF ADEQUATE SIGNIFICANCE OF ADEQUATE WORKING CAPITALWORKING CAPITAL

A business unit needs adequate amount of working capital

This should be as per its requirements. There should be neither a shortage nor excess of

working capital as both affect the firm negatively. Adequate working capital is one of the pre-

requisites for continuous & orderly functioning of a business.

It acts as a source of strength and stability of a business.

SOURCES OF WORKING CAPITALSOURCES OF WORKING CAPITAL

Bank loans Issue of Debentures Public Deposits Trade Credit Advance from Customers Self financing Inter-corporate Deposits Short term loans from financial institutions Factoring

TYPES OF WORKING CAPITALTYPES OF WORKING CAPITAL

I. PERMANENT WORKING CAPITALI. PERMANENT WORKING CAPITAL

Permanent Working Capital is that part of total working capital which is used for purchasing current assets which the firm must maintain permanently in order to carry on its business operations.

Every firm must maintain a certain minimum stock, tools, spare parts and also for paying wages and meeting other expenses.

Investments in such assets will be treated as permanent working capital. It remains in the business for a long period of time & grows along with expansion of a firm.

It includes Initial & Regular Working Capital.Initial & Regular Working Capital.

A. INITIAL WORKING CAPITALA. INITIAL WORKING CAPITAL Initial working capital is required during the formation

period of a company. During the initial period, a firm’s revenue may not be

regular, credit facilities from bank may not be available, credits may be granted for sales promotion.

A firm requires initial working capital during this period to consolidate its position. It helps bring about stability.

It is needed to start the circulation of capital. This capital, should be raised by the promoters themselves. In due course, the cash position of the company will improve

and the initial working capital will not be required.

B. REGULAR WOKING CAPITALB. REGULAR WOKING CAPITAL The working capital required to keep the production

activities regular & continuous, so that business operates smoothly.

It is the excess of current assets over current liabilities. Regular working capital enables companies to

maintain minimum stock of all R/Ms, WIP & FGs, to ensure regular working of the company till new purchases are made.

Its exact amount varies from business to business and it needs to be estimated properly by the promoters and make provisions for the same.

II. VARIABLE WORKING CAPITALII. VARIABLE WORKING CAPITAL

Also termed as fluctuating working capital because of its nature.

It is used for purchasing current assets due to seasonal changes or unforeseen or abnormal circumstances.

Thus, the excess of current assets over and above the permanent working capital is termed as variable/ fluctuating working capital.

It includes Seasonal Working Capital & Special Seasonal Working Capital & Special Working Capital.Working Capital.

A. SEASONAL WORKING CAPITAL A. SEASONAL WORKING CAPITAL It refers to the working capital required during the

particular season. It is in addition to initial & regular working capital. As busy or peak season approaches, industries

increase their purchases of raw materials, more workers are employed; due to which more amount of working capital is required during busy seasons.

The same is recovered when sales increase and cash is received from the customers.

The amount of seasonal working capital varies from company to company.

B. SPECIAL WORKING B. SPECIAL WORKING CAPITALCAPITAL

A company requires extra funds to meet any unforeseen or emergency situation.

For meeting such situations, special working capital is required. It is required under the following circumstances:

Special manufacturing operations to meet sudden demand

Onset of depression

Rising prices

Unforeseen contingencies like strikes, lockouts, fire, floods etc.• The amount of special working capital depends on the situation.

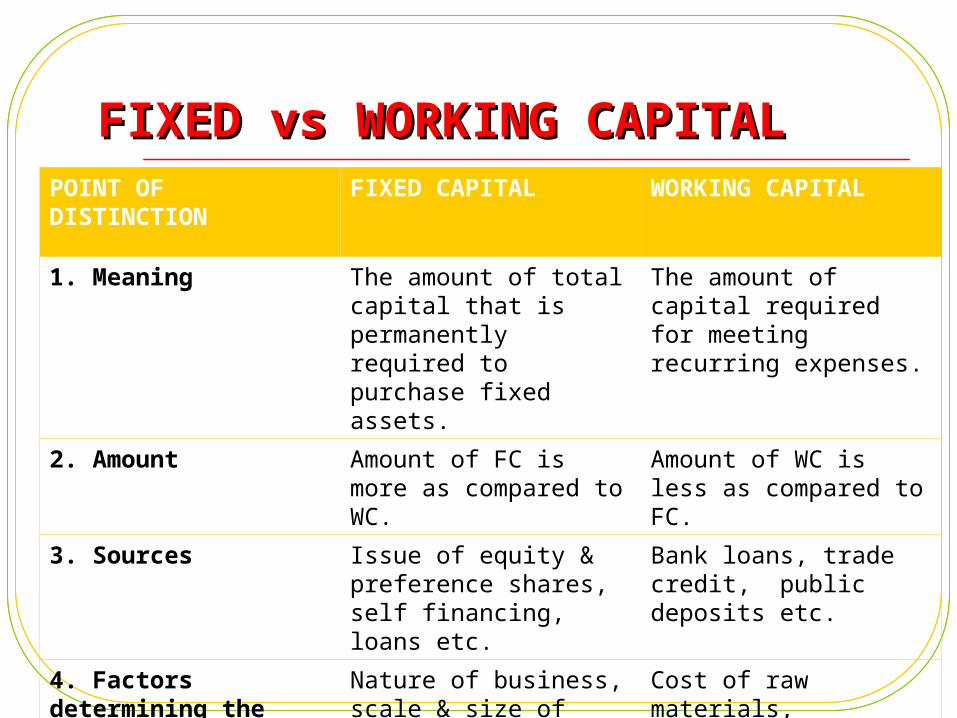

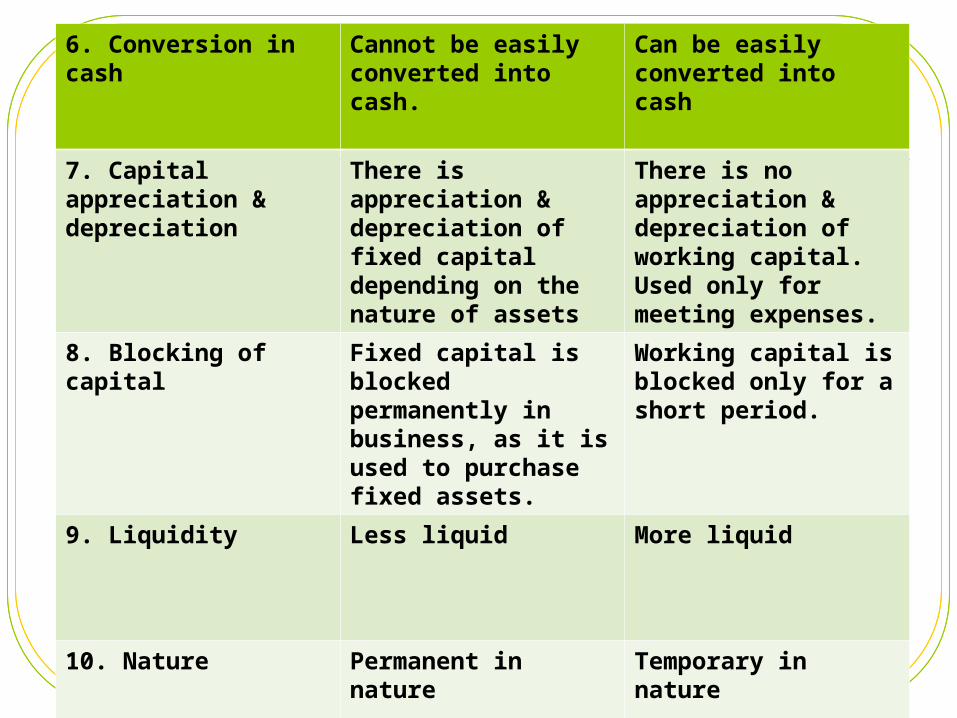

FIXED vs WORKING CAPITALFIXED vs WORKING CAPITALPOINT OF DISTINCTION

FIXED CAPITAL WORKING CAPITAL

1. Meaning The amount of total capital that is permanently required to purchase fixed assets.

The amount of capital required for meeting recurring expenses.

2. Amount Amount of FC is more as compared to WC.

Amount of WC is less as compared to FC.

3. Sources Issue of equity & preference shares, self financing, loans etc.

Bank loans, trade credit, public deposits etc.

4. Factors determining the amount

Nature of business, scale & size of operation, technology used etc.

Cost of raw materials, importance of labour, seasonal variations etc.

5. Frequency of need Needed less frequently Needed more frequently

6. Conversion in cash Cannot be easily converted into cash.

Can be easily converted into cash

7. Capital appreciation & depreciation

There is appreciation & depreciation of fixed capital depending on the nature of assets

There is no appreciation & depreciation of working capital. Used only for meeting expenses.

8. Blocking of capital Fixed capital is blocked permanently in business, as it is used to purchase fixed assets.

Working capital is blocked only for a short period.

9. Liquidity Less liquid More liquid

10. Nature Permanent in nature Temporary in nature