classification of quantitative trading strategies webinar ppt

TRANSCRIPT

July 11th, 2017

Radovan Vojtko, CEO - Quantpedia

A Pioneer Algo Trading Training Institute Encyclopedia of Quant Trading Strategies

MSc in Telecommunication from Slovak University of Technology. Former Portfolio Manager atTatra Asset Management (the biggest asset management company in Slovak Republic),managed over 300+mln EUR in several quantitative funds (focused on multi-asset CTA/trend-following strategies, market timing and volatility trading).

ABOUT THE SPEAKER

2

Radovan VojtkoCEO of Quantpedia.com since 2015

Who are we:

Small company, based in Slovak Republic (EU), engaged in a field of quanttrading research ...

Our mission:

We are building a database of quant trading strategies, our goal is to giveinstitutional clients opportunity to find new ideas for trading. Databasecurrently contains more than 350 strategies.

QUANTPEDIATHE ENCYCLOPEDIA OF QUANTITATIVE TRADING STRATEGIES

3

QUANTPEDIA – HOW WE DO IT

4

Academic – 10s of thousands of financial papers are published each year

Sell side research – part of the research is not publicly available (sent bybrokers/banks to their clients), however big part is freely available

Special subsection - research published by notable Asset Management companies toshow their expertise to their clients (notable examples AQR, Robeco, Cambria,Resolve etc.)

Buy side

RESEARCH IN A FIELD OF QUANT TRADING

5

ASSET CLASS FOCUS OF QUANT RESEARCHERS

6

Research on equities is totally dominant

Cheap/free data on equities, popular asset class among public

Commodities, currencies and bonds are less explored

Data from Quantpedia.com

TIMEFRAME FOCUS OF QUANT RESEARCHERS

7

Data from Quantpedia.com

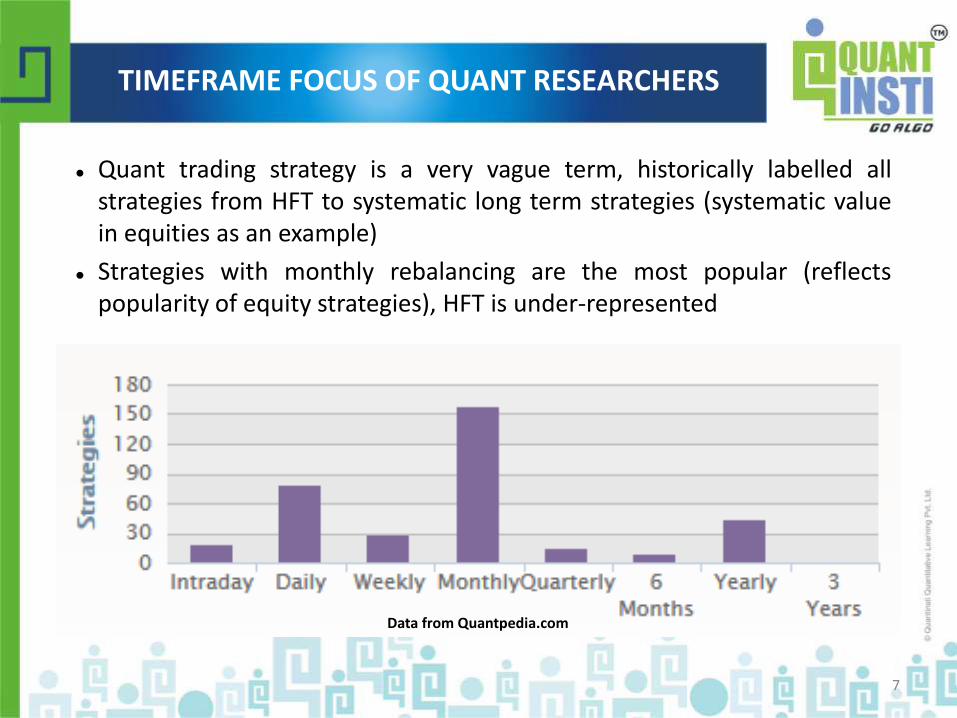

Quant trading strategy is a very vague term, historically labelled allstrategies from HFT to systematic long term strategies (systematic valuein equities as an example)

Strategies with monthly rebalancing are the most popular (reflectspopularity of equity strategies), HFT is under-represented

Again, topics/keywords reflectspopularity of equity strategies(stock picking, equity long short,momentum, market timing, value,earnings effects)

Trend following, FX strategies andarbitrage/relative tradingstrategies are also popular amongresearchers

TOPIC FOCUS OF QUANT RESEARCHERS

8

Top 20 keywords, data from Quantpedia.com

A lot of various classifications, quant strategies dynamically evolve andwhole quant-space is in a constant motion.

We will present our view of the field

Main dimensions – Timeframe, Keywords and Asset Class focus

MAIN CATEGORIES OF QUANT STRATEGIES

9

10

MULTI-ASSET CLASSIFICATION

BLIND SPOTS

11

12

EQUITY CLASSIFICATION

BLIND SPOTS

13

LESSER-KNOWN STRATEGIES

14

PAIRS TRADING WITH COMMODITIES

PRE-EARNINGS ANNOUNCEMENT DRIFT

PAIRS TRADING WITH COMMODITIES

15

Bianchi, Drew, Zhu: Pairs trading profits in commodity futures markets

http://eprints.qut.edu.au/32427/1/c32427.pdf

Trading rules: Commodity futures are divided into 5 groups with similar characteristics (energy, base

metals etc.).

A cumulative total return index is then created for each commodity.

Pairs are formed inside each commodity group over a twelve-month period (formationperiod).

The top 5 closest pairs are found by looking for the pairs of futures which minimize thesum of the squared deviations between the two normalized price series.

The top 5 pairs with the smallest historical distance measure are then traded in thetrading period (the rest of the sample).

A long-short position is opened when a pair of prices has diverged by more than twostandard deviations and the position is closed when prices have reverted.

PAIRS TRADING WITH COMMODITIES

16

Period of rebalancing – daily

Number of traded instruments – 10

Backtest period – 1990-2008

Indicative performance – 1.44% monthly for long short portfolio (~19%yearly, table III from source paper)

Estimated volatility – 11.8% yearly, estimated from t-statistic

Ertan, Karolyi, Kelly, Stoumbos: Pre-Earnings Announcement Over-Extrapolation

https://mendoza.nd.edu/assets/193974/2016_spring_finance_seminar_series_peter_kelly_paper_updated_3_22_2016.pdf

Trading rules: Investment universe – US stocks from NYSE, AMEX, NASDAQ

Stocks are divided into deciles based on the past earnings-announcementperformance (sorted based on the weighted-average of the past 8 quarterlyearnings announcement returns)

At the beginning of each trading day, the investor considers firms in the pre-earnings announcement window – 5 days before the earnings announcement date.

Then he goes long the firms within the top decile and short the firms within thebottom decile of the extrapolated return measure and holds for five days.

PRE-EARNINGS ANNOUNCEMENT DRIFT

17

Period of rebalancing – daily

Number of traded instruments – ~90 (based on the estimated samplesize)

Backtest period – 1991-2014

Indicative performance – 0.16% daily for long-short portfolio (~39%yearly, data from table 7)

Estimated volatility – ~45% yearly, estimated from t-statistic

PRE-EARNINGS ANNOUNCEMENT DRIFT

18

Alpha decay – In-sample vs. Out-of-sample performance

Post-publication performance decay

P-hacking & Replication problems

Momentum in Anomalies

COMMON ISSUES IN QUANT RESEARCH

19

McLean, Pontiff - Does Academic Research Destroy Stock ReturnPredictability? (2015)

Out-of-sample and Post-publication return-predictability of 97 variables/equityfactors, 5year horizon

Glass is half empty – return is 26% lower Out-of-sample and 58% lowerPost-publication

Glass is half full – 74% of alpha remains Out-of-sample, 42% remainsPost-publication

ALPHA DECAY

20

Hsu, Myers, Whitby: Timing Poorly: A Guide to Generating Poor ReturnsWhile Investing in Successful Strategies (2016)

Value anomaly preserves its return because most of the people who tryto invest into "value" have bad timing. In reality, investors help toincrease return of "value factor" on the contrary.

PERSISTENCE OF ANOMALIES

21

Data dredging (also data fishing, data snooping, and p-hacking) - is theuse of data mining to uncover patterns in data that can be presented asstatistically significant, without first devising a specific hypothesis as tothe underlying causality ...

Hou, Xue, Zhang: Replicating anomalies (2017) –

Abstract: „ ... data library that contains 447 anomaly variables. Withmicrocaps alleviated via New York Stock Exchange breakpoints andvalue-weighted returns, 286 anomalies (64%) are insignificant at theconventional 5% level. Imposing the cutoff t-value of three raises thenumber of insignificance to 380 (85%). „

P-HACKING

22

P-HACKING

23

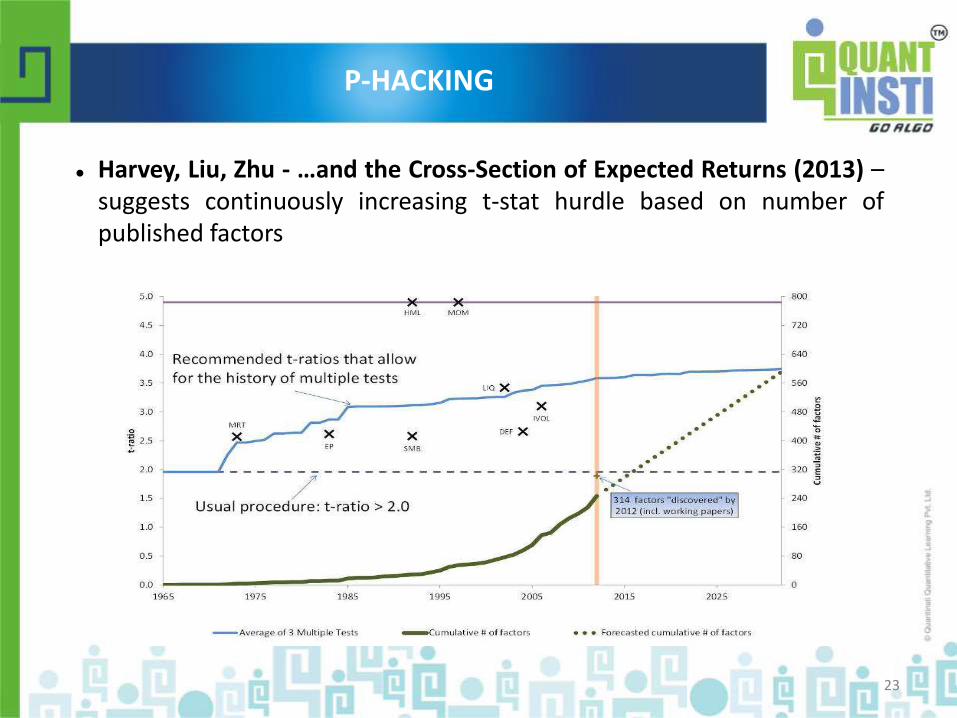

Harvey, Liu, Zhu - …and the Cross-Section of Expected Returns (2013) –suggests continuously increasing t-stat hurdle based on number ofpublished factors

MOMENTUM IN ANOMALIES – ... LET HARD DATA PICK OUT WINNERS ...

24

Huang, Huang: Real-Time Profitability of Published Anomalies (2014)

Abstract: „... each year recursively pick the best past-performer amongsuch anomalies over a given training period...“

Can we find profitable strategies in academic research? Yes.

But: Look for „blind-spots“ (assets, timeframes and instruments that are less-covered by

research).

Performance of anomalies decrease out-of-sample and post-publication (expect atleast 30-60%).

Beware of liquidity & transaction costs problems, no micro-caps (no small-caps ?), testvalue-weighted portfolios.

Increase t-stat hurdle for multiple tests.

Let the data pick out winners – momentum in anomalies/factors.

SHORT CONCLUSION

25

TAKE THE NEXT STEP WITH EPAT™

26

Over 10000 professionals from 100+ countrieshave benefited from QuantInsti’s educational initiatives.

If you want to be a successful Algorithmic Trader,then enroll for EPAT™ now!

For more information visit us on:

https://www.quantinsti.com/epat/

or Call us on

+91-22-6169-1400 / +91-9920-44-88-77

Next Batch Starts from July 29, 2017!

Success Stories

27

Before EPAT™

Fixed income Trader

Becerra Bursatil S.A

"I am very happy with the support provided by the administration team. Faculty is greatly committed at resolving queries. Having worked at one of the

leading brokerage houses, I would certainly want to get into algorithmic trading and this is where QuantInsti’s EPAT course will help me."

Marco Nicolás Dibo, Argentina

After EPAT™

Vice President

Argentina Valores S.A

Success Stories

28

V. Sankar Narayanan, India

After EPAT™

Quant Analyst

ProAlpha Systematic Capital Advisors

"I am glad that I got enrolled with EPATTM by QuantInsti™, the dilemma of getting into quant trading after 20+ years of being a database expert kept me from getting trained in algo but QuantInatiTM’s EPATTM programme gave me the much needed confidence and I was placed

within few weeks after completing my course."

Before EPAT™

Database Manager

Axis Bank

Grab the opportunity before

the next batch starts July 29,

2017!

29

PRICES TO INCREASE FROM NEXT BATCH!

Quantra™SELF PACED LEARNING COURSES

30

Recommended self-paced learning courses on trading strategies

For more information visit: www.quantra.quantinsti.com

Trading Using Options Sentiment Indicators (Free)Understand the two major emotions that drive the entire market -Fear and Greed and how we can capitalize on them to make profits.

Statistical Arbitrage TradingBuild Statistical Arbitrage strategies Step-by-Step using Excel and Python by taking this course.

Trading with Machine Learning: RegressionLearn to trade by implementing regression techniques to make predictions using Machine Learning algorithms by taking this course.

Questions?

TAKE THE NEXT STEP WITH EPAT™

32

Over 10000 professionals from 100+ countrieshave benefited from QuantInsti’s educational initiatives.

If you want to be a successful Algorithmic Trader,then enroll for EPAT™ now!

For more information visit us on:

https://www.quantinsti.com/epat/

or Call us on

+91-22-6169-1400 / +91-9920-44-88-77

Next Batch Starts from July 29, 2017!