cleaning up: australia’s readiness for a low-carbon future - 2012 progress report

TRANSCRIPT

1

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

Contents

Preface 2

Executive summary 3

Introduction 6

The Australian Low-Carbon Readiness Barometer: Jan 2011-May 2012 7

Corporate sentiment towards a low-carbon future 9

Carbon pricing schemes 9

Threat or opportunity? 10

Impact on business 11

Case study: Wesfarmers 12

Corporate action for a low-carbon future 13

Modelling the impact of carbon prices 13

Reducing carbon footprints 13

Case study: Shell 14

Capitalising on opportunities in a low-carbon economy 15

Conclusion: Action without emotion 16

Appendix: Survey results 17

2

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

Preface

Cleaning up: 2012 progress report on Australia’s readiness for a low-carbon future is an Economist Intelligence Unit report, commissioned by GE. The Economist Intelligence Unit (EIU) conducted the survey and interviews independently and wrote the report. The findings and views expressed here are those of the EIU alone.

Elizabeth Fry and Sudhir Vadaketh were the authors of the report and David Line was the editor. Gaddi Tam was responsible for design and layout. The cover image is by Ivan Loh.

The quantitative findings presented in this report are based on two surveys of executives in Australia about low-carbon readiness at the firm, industry and country level. The results of these surveys, conducted in January 2011 and repeated in May 2012, have been used to determine the Australian Low-Carbon Readiness Barometer, an ongoing index of corporate sentiment about readiness for a low-carbon future.

We would like to thank the survey respondents and interviewees for their time and insights.

June 2012

3

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

Australia will begin pricing carbon in July 2012. The government announced the scheme more than a year ago, during which time corporations have had the opportunity to prepare for it. Do Australian corporations feel they are ready for a low-carbon economy? What actions have they taken to prepare for it? What are the biggest threats posed by Australia’s shift to a more sustainable model? Do corporations believe the current carbon pricing scheme is here to stay? And, crucially, have Australian firms identified opportunities for growth or alternative markets that are emerging or may emerge from a low-carbon economy? This report, based on a survey of over 130 senior executives in Australia, attempts to answer these questions.

The key findings of the research are as follows:

l Australian firms feel less prepared now than last year for a low-carbon future. Based on the overall findings from the Low-Carbon Readiness Barometer, Australian corporations today feel less ready for a low-carbon future than they did in January 2011, before the carbon pricing scheme was announced. Australia’s overall low-carbon readiness is 2.9 out of 5, down slightly from 3.1 last year (on a scale of 1 to 5, with 5 denoting excellent readiness).

There are several reasons that may explain this change in sentiment. First, executives may have

been overconfident before the carbon pricing scheme was announced and explained in detail. This year they have a much better grasp of their individual firms’ level of preparedness, and their sentiment has been tempered somewhat. Second, corporate nervousness on the eve of the introduction of the carbon pricing scheme is bound to be at its peak, as with any new piece of legislation. Third, with national business and consumer confidence down slightly this year, and given uncertain global and regional economic outlooks, corporations may be feeling more sceptical about any new costs—real and perceived—that they have to face.

l More Australian firms are taking action to prepare for carbon pricing, particularly those which will be directly affected by the carbon pricing scheme. Almost a third of Australian companies have modelled the impact of different carbon prices on their business operations, a three percentage point jump from last year (29%). Firms that will be directly affected by the carbon pricing scheme have made much more progress in improving their environmental performance, with two-thirds of them already modelling carbon’s impact. Still, that leaves a third which have yet to do so. Moreover, only 9% of companies which will be only indirectly affected by carbon pricing through higher costs have conducted such modelling.

Executive summary

4

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

That said, more than two-thirds of firms surveyed have some sort of carbon-reduction strategy in place. The primary driver for developing this strategy is the need to comply with laws and regulations. Of the firms which will be directly affected by carbon pricing, some 85% have a carbon-reduction strategy in place, with a further 6% in the midst of developing one. More than half have developed broad strategies that encompass their external partners or supply chains, in addition to their own business.

These findings indicate that Australia’s carbon pricing legislation has spurred firms to take action to reduce their carbon emissions. This will ultimately reduce the country’s overall carbon footprint. Policy clarity has given firms a much better understanding of the expected impact to their businesses, and this has allowed them to make informed investment decisions.

l Carbon pricing is here to stay, but perceived price uncertainty will be the biggest barrier to further progress on carbon reduction. Close to three-quarters of survey respondents believe that carbon pricing is here to stay, but almost half of them think that a new, better pricing regime will eventually replace the current proposed scheme (of a fixed price followed by emissions trading from 2015). This is partly due to disagreement about the optimal carbon price. Close to two-thirds of respondents believe that the A$23 per tonne starting price is too high. Still, there are a few others in favour of a higher price: almost 10% of survey respondents feel the A$23 per tonne starting price is too low. And a plurality of respondents (38%) considers uncertainty about the future price of carbon as the primary barrier to making further progress on carbon reduction in their companies.

This uncertainty may not be resolved quickly. Even in the EU, which began trading carbon emissions in 2005, there is still debate about what the optimal price should be. It is likely that Australia, which is just about to take its

first steps towards carbon pricing, will have to go through several years of discussion and trading before reaching equilibrium. More concrete action depends on greater certainty about the costs carbon pricing will impose.

l The corporate carbon agenda has shifted towards cost reduction. While respondents last year sniffed opportunities in “Developing new products and services” (47%) and “Improving relationships with customers” (47%), this year “Cost reduction” has risen to the fore. This perhaps reflects an increasing certainty about the added costs, particularly among companies directly affected by the scheme. Any potential new opportunities, however, remain relatively unexplored.

Unsurprisingly, firms that will be directly affected by the carbon pricing scheme have made more progress on this score. In particular, more than half of this group has set up dedicated roles or teams to identify greater carbon or energy efficiency measures internally. Around 30% of them have also recruited a government lobbyist, or hired an external consultant to help identify opportunities. This reflects these firms’ willingness to engage third-party help as part of a broad stakeholder engagement strategy.

Meanwhile, reflecting the current anxiety about carbon pricing, only a third of respondents believe that the opportunities created by imposing a carbon price will outweigh the risks in the long term. This is down from about one-half last year.

About the survey:The research involved surveying 136 Australia-based senior executives who are familiar with their companies’ sustainability strategy. Many of the respondents are in senior management—40% are in the C-suite or sit on the board. In terms of size, 51% work at companies with a global headcount of over 1,000 people. Some 46% of respondents work at firms with global annual revenues in excess of US$1bn.

5

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

The respondents work in a broad mix of industries—24% work in the energy and natural resources sector; 15% are in manufacturing; 12% work in construction and real estate; 12% work in the retailing sector; 10% are in IT and

technology; and the remainder work in logistics and distribution; transportation, travel and tourism; agriculture and agribusiness; consumer goods; and telecoms.

6

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

Introduction

desire to address climate change has waned. According to a recent poll by The Lowy Institute, an Australian think-tank, 57% of Australians are in favour of scrapping carbon pricing altogether—when as recently as 2006, some 68% wanted aggressive action taken to address climate change.1

Against this backdrop, the Economist Intelligence Unit (EIU) surveyed Australian corporations in May 2012, just weeks before the start of carbon pricing, to gauge their sentiment on the imminent scheme and determine what actions they had been taking to prepare for it. Our survey base is comprised of companies directly and indirectly affected by carbon pricing (see Chart 1).2 This is an update of a survey we first conducted in January 2011, before the government had announced its carbon pricing plans.

In this report we examine corporate Australia’s readiness both to face the risks and and seize the opportunities of a low-carbon future. In particular, we look at whether corporate sentiment and action has shifted over the past year.

1 “The Lowy Institute Poll”, The Lowy Institute, 2006 and 2012

2 Survey respondents are split in this way only for 2012 results

After years of debate about how to curb carbon emissions, Australia’s parliament passed legislation in 2011 that introduces a carbon pricing scheme from July 1st 2012. Under the scheme, heavy emitters will be required to purchase fixed-price permits at A$23 for each tonne of carbon they produce. The permit price will be fixed for each year but will increase annually at a pre-set rate, ahead of a full emissions-trading scheme, with a A$16 price floor, in 2015.

Despite the legislation, there is still a bit of uncertainty about Australia’s climate-change policies. Julia Gillard, the prime minister, leads a Labor Party government that depends on the support of independents and the Greens’ sole member of parliament for its slender parliamentary majority. Tony Abbott, the opposition leader, has vowed to scrap the carbon pricing scheme if he wins power (the next election must be held by November 2013).

Meanwhile, as the global economic outlook gets gloomier, and corporations, governments and consumers focus on more basic concerns, the

Chart 1Will your company be impacted under the carbon pricing legislation?(% respondents)Yes, we will be directly impacted

No, we won’t be directly impacted, but will feel the impact indirectly through higher costs

No, we won’t be directly impacted, and don’t expect to feel any indirect impact

Don’t know

38

49

7

6

7

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

The Australian Low-Carbon Readiness Barometer: Jan 2011-May 20121

Based on the survey conducted for this report, we have updated the Australian Low-Carbon Readiness Barometer, an ongoing index of perceptions of “low-carbon readiness”.

The barometer seeks to measure the degree to which companies believe Australia is prepared for the transition to a low-carbon economy, both in terms of minimising carbon emissions and seizing growth opportunities that this transition may present in terms of new markets for cleaner products and services.

The overall score is the average of three qualitative scores by senior executives on their perceptions of “low-carbon readiness” of their company, their industry, and Australia overall, on a scale of 1 to 5, with 5 denoting excellent readiness.3

In turn, perceptions of “low-carbon readiness” at the company, industry and national level are measured by averaging respondents’ scores for

two questions—“Please rate the overall readiness of each of the following for minimising their carbon footprint” (see appendix: Chart 1); and “Please rate the overall readiness of each of the following to capitalise on growth opportunities in a low-carbon economy” (see appendix: Chart 2).

Using this methodology Australia’s overall low-carbon readiness is 2.9, a small drop from 3.1 in the baseline report last year. This indicates that, on average, Australian corporations today feel slightly less ready for a low-carbon future than they did in January 2011, before the carbon pricing scheme was announced.

There are several reasons why this may be so. First, as we noted in last year’s report, executives may have been “overestimating their own firms’ readiness in relation to their competitors and the overall economy”. Last year, before the carbon pricing scheme was announced, executives would have witnessed their own firms’ efforts at improving their environmental performance—without firm national guidelines—and possibly been buoyed by what they saw. This year, with details of the carbon pricing scheme well known, they have a much better grasp of their individual firms’ level of preparedness. Hence, this year’s company score has been normalised somewhat, and brought more in line with Australia’s overall score.

2011 2012

Overall score—an average of the three scores below 3.1 2.9

Company score—low-carbon readiness of “your company” 3.6 3.2

Industry score—low-carbon readiness of “your industry” 3.0 2.9

Country score—low-carbon readiness of “the Australian economy” 2.6 2.6

3 For clarity, the scoring system in the barometer has been reversed from that used in the original survey questions (where 1=excellent). The original survey questions are reproduced in the appendix

8

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

Barometer by company sizePerceptions of low-carbon readiness also depend on the size of the company. Although all firms are feeling a little less positive, medium-sized firms are still the least upbeat. But it is large firms that have seen the sharpest drop in perceptions of low-carbon readiness. These firms typically have deep pockets and plenty of resources to commit to any carbon-reduction initiative, and hence would have been feeling extremely bullish in January 2011. However, many of them are also the heaviest emitters. As carbon pricing draws near, they perhaps have a more realistic view of the scope of change needed.

Second, corporate nervousness on the eve of the introduction of the carbon pricing scheme is bound to be at its peak, as with any new piece of legislation. In January 2011, carbon pricing must have seemed a long way off. Many firms might not have regarded it as an immediate, pressing business concern. Today, as July 1st 2012 draws near, concerns about preparedness have risen. Carbon pricing is here, and Australian firms are still unsure about its budgetary and strategic implications for their businesses.

Third, with national business and consumer confidence down slightly this year, and given the uncertain global and regional economic outlooks, corporations may feel more sceptical about any new costs they have to face. Broader economic uncertainty may be affecting their confidence about low-carbon readiness.

Barometer by industryWhen asked for their perceptions of low-carbon readiness in their own industry, executives in the agriculture and natural resources and services sectors seem slightly more upbeat than those in the construction and manufacturing sectors.

Agriculture and natural resources firms are feeling slightly more confident than last year, perhaps because they have been slowly readying themselves for carbon pricing. Export-oriented manufacturing firms, by contrast, have been going through difficult times, given the uncertain global economic outlook and the strong Australian dollar. That, along with the imminent

imposition of carbon pricing, is forcing some of them to rethink their corporate strategies; some have opted to move capacity abroad. Finally, services firms, many of which will not be directly affected by the carbon pricing scheme, may have been more relaxed about it last year, before the full details were released. Now that they better understand the actual impact of the carbon pricing scheme to their businesses, they may be feeling a little less optimistic.

2011 2012

Agriculture and natural resources4 2.9 3.0

Construction and manufacturing5 2.9 2.6

Services6 3.1 2.9

2011 2012

Small (<101 employees) 3.7 3.4

Medium (101-10,000 employees) 3.3 3.0

Large (over 10,000 employees) 3.7 3.1

4 Includes agriculture and agribusiness, energy, and natural resources sectors

5 Includes construction and real estate and manufacturing sectors

6 Includes IT and technology; logistics and distribution; retailing; telecommunications; transportation, travel and tourism; and consumer goods sectors.

9

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

Corporate sentiment towards a low-carbon future2

Carbon pricing schemes Last year, before Australia’s carbon pricing scheme was announced, there was little consensus amongst Australian executives about how to go about cutting carbon emissions: some favoured a cap-and-trade scheme, others a corporate or consumer tax, while a minority believed that carbon should not be priced at all. This year, climate change scepticism seems to have intensified. More than half of respondents believe that the impact of carbon emissions on global warming has not been sufficiently established to warrant wholesale changes in corporate strategy or behaviour, up from 40% last year.

Nevertheless, though there is still some uncertainty, a vast majority of survey respondents believe that carbon pricing is here to stay (see Chart 2). But almost half of them think that a new, better pricing regime will eventually replace the current proposed scheme.

This is partly due to disagreement about the optimal carbon price. Close to two-thirds of respondents believe that the A$23 per tonne starting price is too high. This could be because the price of publicly traded EU carbon permits has fallen steeply to around Euro6.50 (A$8.20) per tonne, making Australia’s fixed price seem very high. Looking further ahead to 2015 and the start of emissions trading in Australia, some executives may also feel that Australia’s mooted A$16 floor price is too high.

“My view has been that climate change is real and I believe it’s caused by man and probably caused by carbon dioxide,” says Mark Chellew, chief executive and managing director of Adelaide Brighton, a cement producer.7 “But Australia is going out aggressively ahead of the world. I think we’ve taken too big a first step. A carbon tax of about $10 per tonne would have been a reasonable starting point.”

7 Adelaide Brighton is initially eligible for free permits in year one of the scheme for 94.5% of its output. Its liability for the remaining 5.5% in year one is expected to be A$7m before tax and mitigation.

Chart 2Which of the following best reflects your view of the likely state of the carbon pricing mechanism in five years’ time?(% respondents)A new, better, pricing regime will eventually replace the current scheme

The proposed scheme will persist in its current form: a fixed price on carbon from mid 2012, ahead of a full emissions-trading scheme in 2015

Carbon pricing will be scrapped altogether

Don’t know

49

23

23

5

10

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

Still, there are a few others in favour of a higher price. Almost 10% of survey respondents feel the A$23 per tonne starting price is too low. David Hone, the London-based global climate change adviser at Shell, an oil and gas firm, thinks Europe’s current carbon price is undermining the region’s efforts to reduce corporate carbon footprints. “There is a growing push from businesses there to recalibrate the system so that prices rise to the sorts of levels that are being introduced in Australia,” he says, indicating that Australia’s A$16 per tonne cap-and-trade floor is suitable. “A low price doesn’t drive change. A more robust price will drive change in investment and opportunity by providing the right investment signals.”

Perhaps the salient point here is that even in the EU, which began trading carbon emissions in 2005, there is still debate about what the optimal price should be. It is likely that Australia, which is just about to take its first steps towards carbon pricing, will have to go through several years of discussion and trading before equilibrium is reached. That, in turn, should lead to more

concrete action: a plurality of respondents (38%) considers the uncertainty about the future price of carbon as the primary barrier to making further progress on carbon reduction in their companies.

Threat or opportunity?Reflecting the current anxiety about carbon pricing, only a third of respondents believe that the opportunities created by imposing a carbon price will outweigh the risks in the long term. This is down from about one-half last year. Meanwhile, while respondents last year sniffed opportunities in “Developing new products and services” (47%) and “Improving relationships with customers” (47%), this year “Cost reduction” has risen to the fore (see Chart 3). As carbon pricing draws near, firms are more focussed on how they can reduce costs rather than grow new business opportunities. This perhaps reflects the fact that there is increasing certainty about the added costs, particularly among companies directly affected by the scheme. Any potential new opportunities, however, remain relatively unexplored.

Chart 3What do you think are the biggest opportunities to your business in taking steps to reduce its carbon footprint? Select up to three.(% respondents)

Cost reduction

Improving relationships with customers

Developing new products and services

Improved employee engagement/commitment

Risk mitigation (eg, in supply chains)

Access to new markets

Improving relationships with suppliers

Other, please specify

We don’t see any opportunities in this

Don’t know

35

24

22

20

18

7

2

24

4

33

Developing new products and services

Improving relationships with customers

Risk mitigation (eg, in supply chains)

Improved employee engagement/commitment

Access to new markets

Cost reduction

Improving relationships with suppliers

47

34

26

25

22

9

47

2011 2012

11

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

Impact on businessA national carbon price will inevitably have an impact on many aspects of business. When compared to last year, respondents are generally more pessimistic about the carbon legislation’s impact across all aspects of their business. Respondents generally believe that a price on carbon will lead to higher operating costs, lower profits, and weaker competitiveness (see Chart 4). However, respondents are still confident that the carbon legislation will help improve their firms’ brand value and reputation, and

increase innovation and investment into clean technology.

Among the companies that are directly affected by the carbon pricing scheme (38%), views tend to be more polarised, with more believing that there will be a positive or negative impact on the different aspects of their businesses than those which expect no change. This suggests that these firms are—as might be expected—further ahead in their carbon reduction strategies, and hence may have a better understanding of how the carbon price will affect their firms.

Chart 4How do you think the introduction of a national corporate carbon tax will affect your company in the following areas?(All respondents)

Operating costs

Efficiency

Profits

Competitiveness within Australia

173 75 5

12 62854

245 565

5112 632

Competitiveness internationally9 1127 53

Brand value/reputation57 1019 14

Employee engagement5812 1020

Innovation/investment into clean technology43 1329 15

Risk management209 1260

Transparency1510 1362

Improve Stay the same Deteriorate Don’t know/not applicable

One reason, perhaps, for the anxiety about the imminent carbon price, is that few firms believe that they will be able to pass on any additional costs to their customers (see Chart 5). Wesfarmers, owner of Coles, Australia’s largest

supermarket chain, has said it will challenge any proposed supplier price increases and strive to avoid passing on any carbon-related costs to its customers (see case study: Wesfarmers).

Chart 5How easy or difficult will it be for your business to be able to pass along any additional costs incurred by the carbon legislation to your customers?(% respondents)

Very difficult

Somewhat difficult

Neither easy nor difficult

Reasonably easy

Very easy

38

38

1

49

7

12

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

Wesfarmers, owner of Coles, Australia’s largest supermarket chain, as well as major coal and chemicals operations, will be among the companies most heavily affected by the new carbon price scheme.

Aside from power stations, Wesfarmers is Australia’s sixth biggest carbon emitter, producing 2.7m tonnes of direct emissions. The company says it will incur a A$100m net annual cost in the first year of the scheme as a result of the initial carbon price of A$23 per tonne. (For comparison, its 2011 revenues were A$56bn).

Yet the conglomerate believes it can maintain its margins by taking steps to reduce carbon emissions and improve energy efficiency. “We invested heavily in energy efficiency a few years back when it became clear that Australia would put a price on carbon,” says Cameron Schuster, the firm’s sustainability manager. For example, Coles is installing voltage optimisation technology that reduces overall store power consumption.

Still, the carbon legislation provided some policy clarity. “While our greenhouse gas accounting, monitoring and reporting systems were purpose-built for a carbon price four years

ago, the continuous flow of regulation and policy in the past six months has necessitated a review and some tweaking,” Mr Schuster says.

Apart from the investment to improve energy efficiency, much of the group’s focus in the last year has been on intensive emissions reduction, particularly in the chemicals business. It is testing a new nitrous oxide reduction technology that could potentially cut emissions quite significantly. Meanwhile, Wesfarmers’ coal business has worked with regulators to find a way to improve the method of measuring coal-seam methane emissions.

Wesfarmers has also spent time developing internal policies to guide employees as they prepare greenhouse and energy reports and deal with customers and suppliers on issues to do with carbon pricing. Among other things, these policies deal with report verification, record keeping, carbon accounting and pricing, and the transfer of carbon permits.

Though the carbon cost is significant, Wesfarmers believes it can mitigate it to a large extent with top line growth and increased organisational efficiency.

Case study: Wesfarmers

13

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

Corporate action for a low-carbon future3

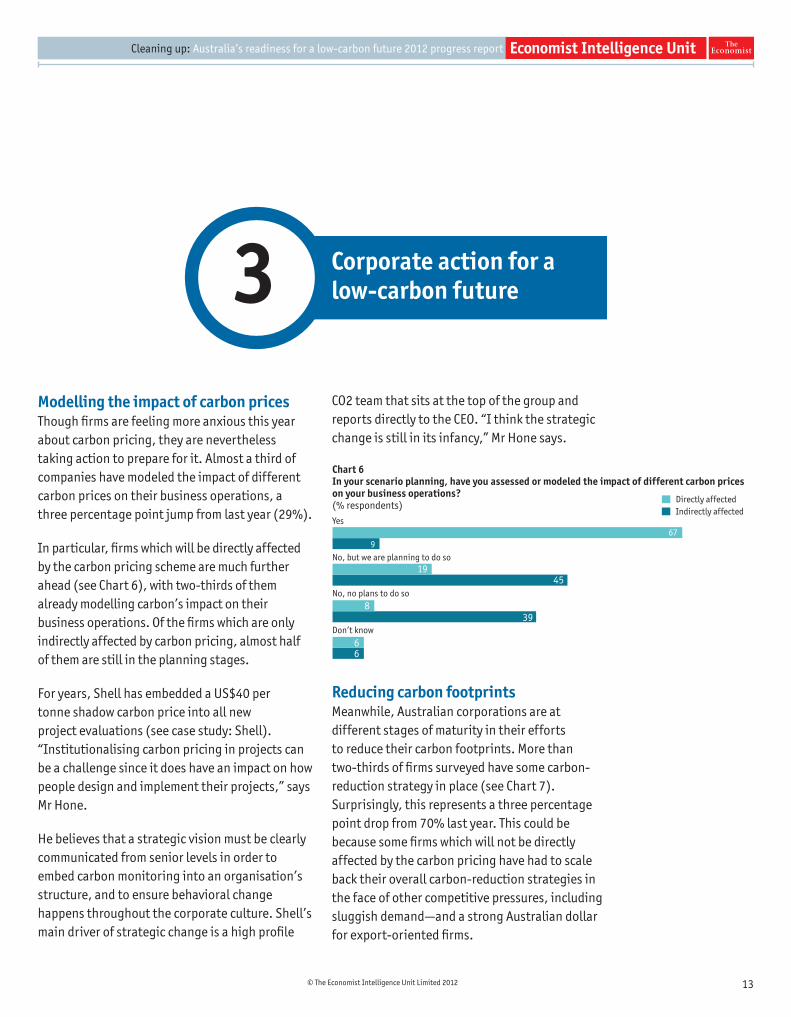

Modelling the impact of carbon prices Though firms are feeling more anxious this year about carbon pricing, they are nevertheless taking action to prepare for it. Almost a third of companies have modeled the impact of different carbon prices on their business operations, a three percentage point jump from last year (29%).

In particular, firms which will be directly affected by the carbon pricing scheme are much further ahead (see Chart 6), with two-thirds of them already modelling carbon’s impact on their business operations. Of the firms which are only indirectly affected by carbon pricing, almost half of them are still in the planning stages.

For years, Shell has embedded a US$40 per tonne shadow carbon price into all new project evaluations (see case study: Shell). “Institutionalising carbon pricing in projects can be a challenge since it does have an impact on how people design and implement their projects,” says Mr Hone.

He believes that a strategic vision must be clearly communicated from senior levels in order to embed carbon monitoring into an organisation’s structure, and to ensure behavioral change happens throughout the corporate culture. Shell’s main driver of strategic change is a high profile

CO2 team that sits at the top of the group and reports directly to the CEO. “I think the strategic change is still in its infancy,” Mr Hone says.

Chart 6In your scenario planning, have you assessed or modeled the impact of different carbon prices on your business operations?(% respondents)Yes

No, but we are planning to do so

No, no plans to do so

Don’t know

1945

679

8

66

39

5.85.8

Indirectly affectedDirectly affected

Reducing carbon footprintsMeanwhile, Australian corporations are at different stages of maturity in their efforts to reduce their carbon footprints. More than two-thirds of firms surveyed have some carbon-reduction strategy in place (see Chart 7). Surprisingly, this represents a three percentage point drop from 70% last year. This could be because some firms which will not be directly affected by the carbon pricing have had to scale back their overall carbon-reduction strategies in the face of other competitive pressures, including sluggish demand—and a strong Australian dollar for export-oriented firms.

14

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

Although the government has provided a clear outline of how Australia’s carbon-reduction policies will develop through to 2020, companies should not underestimate the organisational change required to respond, according to David Hone, the London-based global climate change adviser at Shell, an oil and gas firm.

Shell has gone through three distinct stages in its carbon management journey, which began in 1997. The first two stages occurred in parallel—recognising that carbon reduction laws would be a reality and making an early effort to influence policy so as to spur corporate investment as well as meet environmental objectives. Mr Hone claims it was a massive challenge getting all the businesses in Shell to recognise the importance of the issue and its long term impact on the company.

The second stage was building capacity within Shell. In order for carbon-reduction strategies to be effective, they need to be embedded within the organisation and underpin business procedures, practices and operations. “We had to ensure everyone understood how carbon management policies worked and their impact on the various businesses from a profit and loss

point of view,” Mr Hone says. Shell expanded on its existing trading activities to encompass carbon trading. It also implemented business processes in Europe so the refineries, exploration and production facilities would understand how to work with the new trading arm.

The third stage was elevating the issue to a highly strategic level in the organisation. Among other things, this meant embedding a US$40 per tonne shadow carbon price into all new project evaluations.

Fifteen years after the start of Shell’s carbon management strategy, Mr Hone still stresses the importance of delivering the right message within the organisation. “CO2 emissions are not like sulfur emissions where you can clean them up a bit and they go away,” he says. “CO2 is cumulative so until you go to zero emissions the problem won’t go away.”

Just like Shell, he believes Australia has made good progress, but still has a long way to go. “While reducing energy use and improving energy efficiency are both good things to do, they are just one part of the solution,” he says. “A cap-and-trade system will also bring through the right energies, in the right mix at the right time.”

Case study: Shell

As expected, firms that will be directly affected by the carbon pricing scheme are much further ahead in their efforts to implement carbon-reduction strategies: all of them either have strategies or plan to develop one (see Chart 7).

Of the firms which will be directly affected by carbon pricing, some 85% have a carbon-reduction strategy in place, with a further 6% in the midst of developing one. More than half of them have developed broad strategies that encompass their external partners or supply chains. For the firms which are not developing a strategy, the main reason is that they consider their firms too small for it to be affordable or practical.

It is a similar story in terms of specific, measurable targets to reduce carbon footprints in different

areas, from overall energy usage to green building technology and IT systems. The overall findings are similar to last year (see appendix: Chart 12), with firms that will be directly affected by carbon pricing much more advanced.

Over the years, Adelaide Brighton has already significantly reduced its carbon footprint in Australia through the use of energy-saving cement substitutes such as fly ash and slag, the use of alternative fuels and changes to cement standards. The company has also prompted changes in industry standards around ingredients, to allow for a less carbon-intensive cement mix. It is also considering closing down inefficient, carbon-intensive kilns, part of the shift in manufacturing offshore.

15

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

Chart 7Does your company have a strategy in place for reducing its carbon footprint? (% respondents)Yes, it covers the whole business, including external partners and supply chain

Yes, it covers the business, including our supply chain, but not our external partners

Yes, it covers the business, including our external partners, but not our supply chain

No, but we are currently developing one

No, and we have no plans to develop one

Don’t know

0

Yes, it covers only our own business

2712

216

6

3127

9

624

18

103

Indirectly affectedDirectly affected

“We currently import 30% of our total products and expect that within five to ten years this figure will increase to 40%,” says Mr Chellew. “We were already going to increase import flexibility rather than domestic manufacture because of the high Aussie dollar, but the carbon tax has reinforced the sense of that strategy.” In the long term, the company was going to shift its input mix towards imports anyway, because local production is carbon-intensive as a result of high electricity consumption. “There is no carbon tax on imported cement because the grinding is done offshore,” he says.

Capitalising on opportunities in a low-carbon economyAustralian firms are preparing themselves in different ways to capitalise on opportunities in a low-carbon economy. Once again, firms that are directly affected by the carbon pricing scheme have made more progress (see Chart 8). In particular, more than half of this group has set up dedicated roles or teams to identify greater carbon or energy efficiency measures internally. This perhaps reflects the most direct, pressing concern for them as carbon is priced. Around 30% of them have also recruited a government lobbyist to maximise available support, or have hired external consultants to help identify opportunities. This reflects these firms’ willingness to engage third-party help as part of a broad stakeholder engagement strategy.

Mr Hone at Shell claims that an ongoing dialogue with regulators is essential for carbon reduction and corporate performance. “It is absolutely in the interest of companies to help develop policies right from the beginning and stick with it,” he says. “That way they can fend off or dilute any threats. Companies can’t just make demands and go home again.”

To illustrate his point, he refers to the debates taking place now in Europe, as the carbon price

plunges to new lows. “If industry doesn’t work closely with Brussels to get this process to deliver, we will suffer a backlash,” he says. “At that point the policy makers will do something else and you can bet the something else will be mandated, less flexible, less easy to manage and more challenging,” he says.

Chart 8What steps has your company taken to make the most of these opportunities? Select all that apply. (% respondents)Dedicated roles/teams to identify greater carbon/energy efficiency measures internally

Dedicated roles/teams to identify 'green' markets

Dedicated roles/teams to identify 'green' products or services

Government lobbyist/liaison to maximise available support or subsidies

Hired external consultants to help identify opportunities31

Customer/client focus groups to identify level of demand for 'green' products/services

2521

5636

27

2123

27

2720

12

Indirectly affectedDirectly affected

16

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

Conclusion

Action without emotionThis suggests that further research and analysis into the carbon pricing scheme is needed, in particular into its impact on corporate and environmental performance. The Australian government needs to keep up a broad-based communication and dialogue in order to secure buy-in from Australian corporations and society. Shell’s experience in Europe underscores the importance of a regular dialogue on carbon-reduction policies between corporations and regulators. By building a broader consensus behind its carbon pricing policies, the government will be able to attract more low-carbon investment into the country, and drive clean-product innovation within local firms. This will position Australian companies for success in low-carbon economies around the world.

Australia’s carbon pricing legislation has spurred firms to take action to reduce their carbon emissions. This will ultimately reduce the country’s overall carbon footprint. Greater policy clarity has given firms a much better understanding of the expected impact to their businesses, and this has allowed them to make informed investment decisions.

Nevertheless, this is only the first step in a long journey, as Australia prepares itself for a low-carbon future. Though the carbon legislation has undoubtedly had an impact on firms’ behaviour, corporate sentiment towards climate change and carbon reduction is still uncertain, as shown by the small drop in Australia’s low-carbon readiness score.

17

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

Appendix:Survey results

Note: Percentages may not total 100 due to rounding or the ability of respondents to choose multiple responses

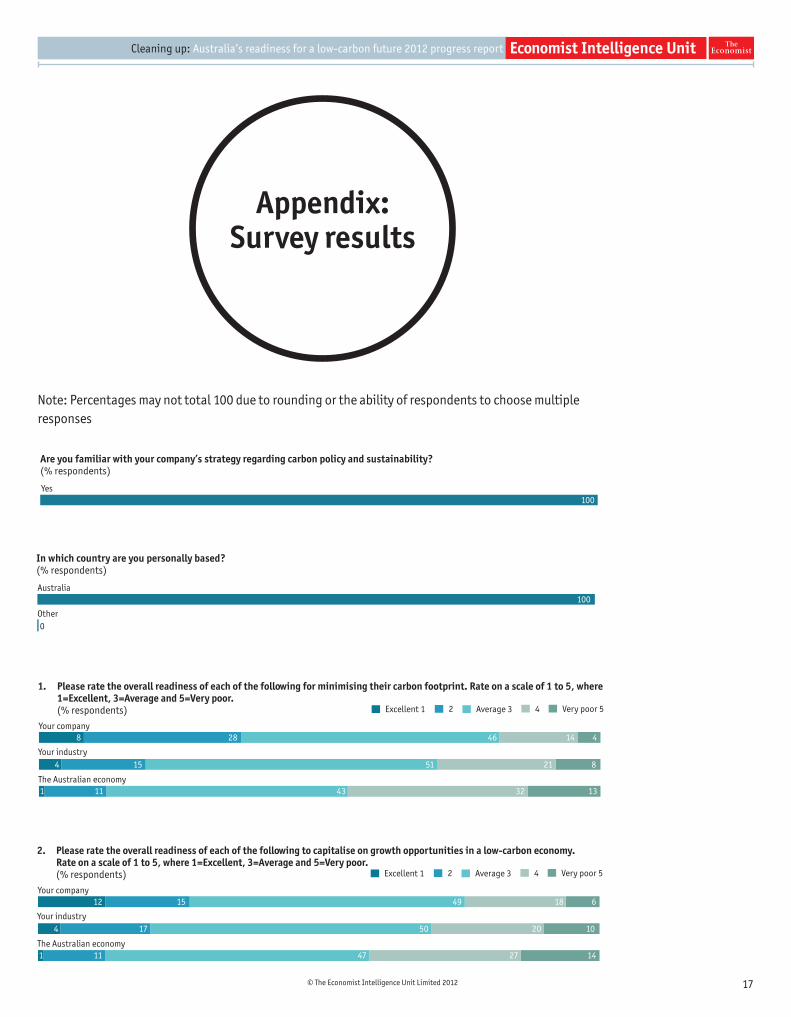

Are you familiar with your company’s strategy regarding carbon policy and sustainability?(% respondents)

Yes100

37

In which country are you personally based?(% respondents)

Australia

Other

100

0

1. Please rate the overall readiness of each of the following for minimising their carbon footprint. Rate on a scale of 1 to 5, where 1=Excellent, 3=Average and 5=Very poor. (% respondents)

Your company

Your industry

The Australian economy

46288 14 4

154 82151

111 133243

Excellent 1 2 Average 3 4 Very poor 5

2. Please rate the overall readiness of each of the following to capitalise on growth opportunities in a low-carbon economy. Rate on a scale of 1 to 5, where 1=Excellent, 3=Average and 5=Very poor. (% respondents)

Your company

Your industry

The Australian economy

491512 18 6

174 102050

111 142747

Excellent 1 2 Average 3 4 Very poor 5

18

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

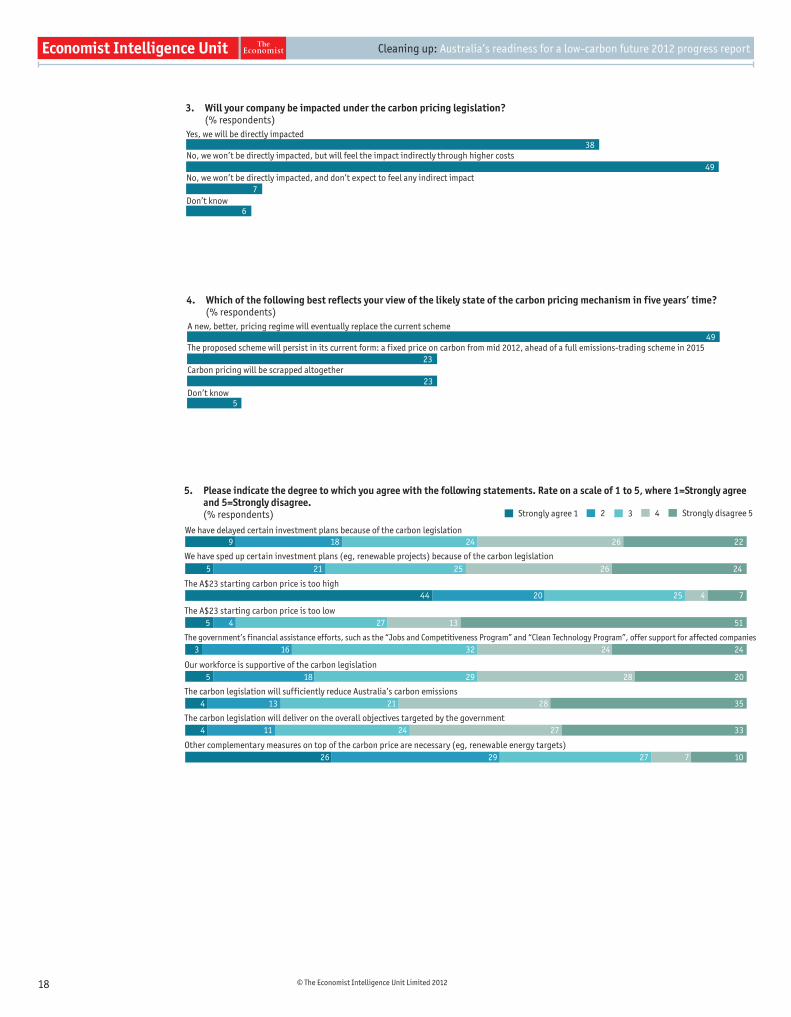

3. Will your company be impacted under the carbon pricing legislation? (% respondents)Yes, we will be directly impacted

No, we won’t be directly impacted, but will feel the impact indirectly through higher costs

No, we won’t be directly impacted, and don’t expect to feel any indirect impact

Don’t know

38

49

7

6

4. Which of the following best reflects your view of the likely state of the carbon pricing mechanism in five years’ time? (% respondents)A new, better, pricing regime will eventually replace the current scheme

The proposed scheme will persist in its current form: a fixed price on carbon from mid 2012, ahead of a full emissions-trading scheme in 2015

Carbon pricing will be scrapped altogether

Don’t know

49

23

23

5

5. Please indicate the degree to which you agree with the following statements. Rate on a scale of 1 to 5, where 1=Strongly agree and 5=Strongly disagree. (% respondents)

We have delayed certain investment plans because of the carbon legislation

We have sped up certain investment plans (eg, renewable projects) because of the carbon legislation

The A$23 starting carbon price is too high

The A$23 starting carbon price is too low

24189 26 22

215 242625

2044 7425

275 514 13

The government’s financial assistance efforts, such as the “Jobs and Competitiveness Program” and “Clean Technology Program”, offer support for affected companies323 2416 24

Our workforce is supportive of the carbon legislation295 2018 28

The carbon legislation will sufficiently reduce Australia’s carbon emissions214 3513 28

The carbon legislation will deliver on the overall objectives targeted by the government244 3311 27

Other complementary measures on top of the carbon price are necessary (eg, renewable energy targets)2726 1029 7

Strongly agree 1 2 3 4 Strongly disagree 5

19

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

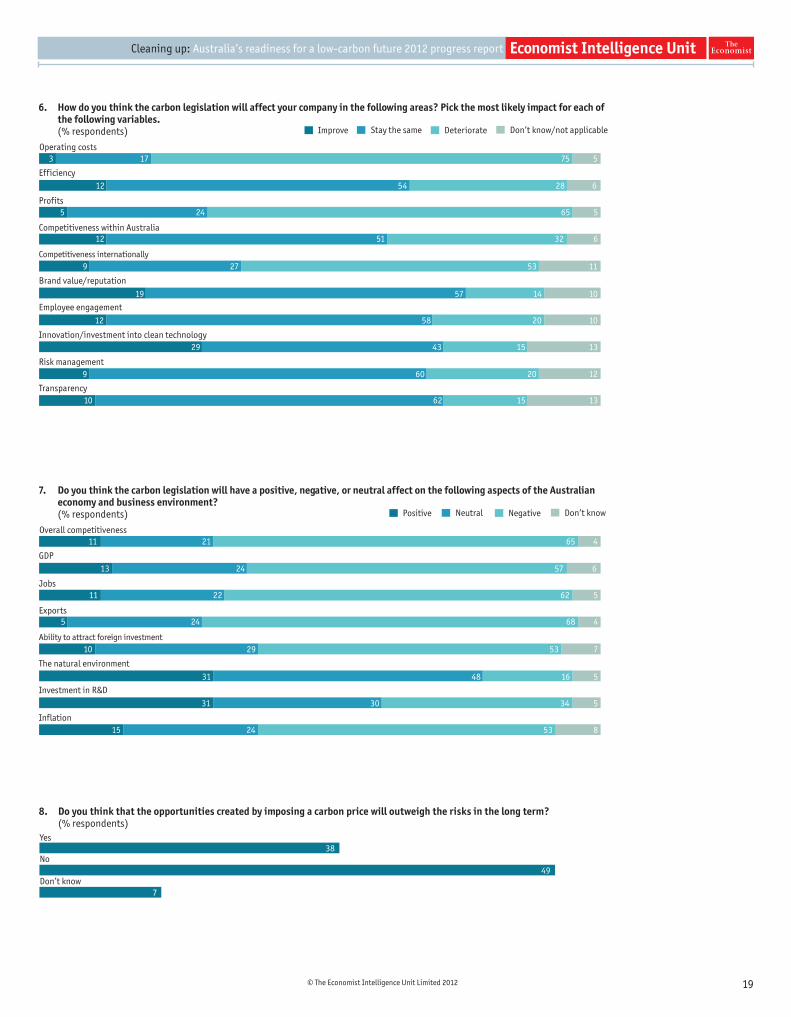

6. How do you think the carbon legislation will affect your company in the following areas? Pick the most likely impact for each of the following variables. (% respondents)

Operating costs

Efficiency

Profits

Competitiveness within Australia

173 75 5

12 62854

245 565

5112 632

Competitiveness internationally9 1127 53

Brand value/reputation57 1019 14

Employee engagement5812 1020

Innovation/investment into clean technology43 1329 15

Risk management209 1260

Transparency1510 1362

Improve Stay the same Deteriorate Don’t know/not applicable

7. Do you think the carbon legislation will have a positive, negative, or neutral affect on the following aspects of the Australian economy and business environment? (% respondents)

Overall competitiveness

GDP

Jobs

Exports

2111 65 4

13 65724

2211 562

245 468

Ability to attract foreign investment10 729 53

The natural environment48 531 16

Investment in R&D3031 534

Inflation24 815 53

Positive Neutral Negative Don’t know

8. Do you think that the opportunities created by imposing a carbon price will outweigh the risks in the long term? (% respondents)Yes

No

Don’t know

38

49

7

20

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

9. How easy or difficult will it be for your business to be able to pass along any additional costs incurred by the carbon legislation to your customers? (% respondents)

Very difficult

Somewhat difficult

Neither easy nor difficult

Reasonably easy

Very easy

38

38

1

49

7

10. In your scenario planning, have you assessed or modelled the impact of different carbon prices on your business operations? (% respondents)

Yes

No, but we are planning to do so

No, no plans to do so

Don’t know

32

9

32

27

11. Does your company have a strategy in place for reducing its carbon footprint? (% respondents)Yes, it covers the whole business, including external partners and supply chain

Yes, it covers the business, including our supply chain, but not our external partners

Yes, it covers only our own business

No, and we have no plans to develop one

Don’t know

Yes, it covers the business, including our external partners, but not our supply chain

41

32

31

No, but we are currently developing one28

27

23

35

21

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

11a. What have been the primary drivers for developing this strategy? Select up to three. (% respondents)Complying with laws and regulations

Desire to do the right thing ethically

It is a part of ongoing corporate risk management

Upgrading the company’s image

Improving the bottom line

Desire to discover new markets

Meeting demands of customers

Other, please specify

Responding to criticism in the media

Supporting recruitment and retention of employees

Responding to pressure from NGOs and citizen lobby groups

64

35

26

19

14

13

6

2

2

5

43

11b. What are the primary reasons why your company is not developing a strategy for reducing its carbon footprint? (% respondents)My company is too small for it to be affordable or practical

My company should focus on making money, not saving the environment

My company does not consider it as necessary

The cost involved is too high

Our competitors have yet to, so we see no need

There has been insufficient support for such a strategy at senior management level

Other, please specify

46

23

15

8

0

0

31

12. Does your firm have specific, measurable targets for reducing its carbon footprint in the following areas? (% respondents)

Overall energy usage

Green building technology (eg, lighting)

IT systems (eg, data centres)

Staff practices (eg, commuting, recycling)

2960 5

56 836

4940 10

3857 5

Core products and services49 1339

Suppliers64 1620

Partners6018 21

Customers60 1624

New investments42 1246

Yes No Not applicable

22

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

13. Do you agree or disagree with the following statements? (% respondents)

All senior executives in my company are aware of our sustainability agenda

The board should lead initiatives to cut carbon emissions

Carbon reduction will become increasingly crucial to all aspects of corporate strategy

Carbon reduction is a short-term concern

2469 7

68 1121

3262 6

6826 5

The impact of carbon emissions on global warming hasn’t been sufficiently established to warrant wholesale changes in corporate strategy or behaviour51 741

Yes No Not applicable

14. Has your organisation implemented the following measures? (% respondents)

Employee incentives to encourage “green” process innovation

Employee education and training on ways to improve carbon efficiency

Means to track and analyse efficiency of resource usage

Clearly defined carbon reduction programme (internal)

6331 6

47 647

3854 7

5242 6

Clearly defined carbon reduction programme (supply chain)17 776

Renewable energy use targets27 766

Transparency with regard to carbon cost of business operations (internal disclosure)39 754

Transparency with regard to publication of carbon footprint (eg, in annual report)35 1154

Climate change risk management: Insurance against potential impacts21 1168

Yes No Not applicable

15. To what extent do you see Australia’s shift to a more environmentally sustainable economy as a threat or an opportunity to your business? Drag the slider button to choose a relevant percentage split that reflects how each option should be weighted. (% respondents)

Opportunity7154 6 7 5 13 16 13 9 4

100:0 90:10 80:20 70:30 60:40 50:50 40:60 30:70 20:80 10:90 0:100

16. Please indicate the degree to which you agree with the following statements. Rate on a scale of 1 to 5, where 1=Strongly agree and 5=Strongly disagree. (% respondents)

Is a driver of process innovation

Is an opportunity to gain a competitive advantage by creating new, or more marketable, products/services

Is an opportunity to find new clients in Australia

Is an opportunity to find new clients internationally

252513 15 18 3

2410 415 2126

10 329 52421

15289 616 26

Is an opportunity to gain a competitive advantage in terms of cost reduction267 420 19 25

Is a necessity driven by government regulation2427 332 6 8

Is a necessity driven by customer and other stakeholder demands/need to maintain reputation20157 632 20

Is a necessity because of the climate risks from emissions3211 520 16 16

Strongly agree 1 2 3 4 Strongly disagree 5 Don’t know

23

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

17. What do you think are the biggest opportunities to your business in taking steps to reduce its carbon footprint? Select up to three. (% respondents)Cost reduction

Improving relationships with customers

Developing new products and services

Improved employee engagement/commitment

Risk mitigation (eg, in supply chains)

Access to new markets

Improving relationships with suppliers

Other, please specify

We don’t see any opportunities in this

Don’t know

35

24

22

20

18

7

2

24

4

33

18. What steps has your company taken to make the most of these opportunities? Select all that apply. (% respondents)Dedicated roles/teams to identify greater carbon/energy efficiency measures internally

Dedicated roles/teams to identify ‘green’ products or services

Government lobbyist/liaison to maximise available support or subsidies

Dedicated roles/teams to identify ‘green’ markets

Customer/client focus groups to identify level of demand for ‘green’ products/services

Hired external consultants to help identify opportunities

Other, please specify

44

21

21

21

20

18

29

19. Which of the following have been the primary drivers for the development of new “green” products/services in your business? (% respondents)Increased regulatory demands that are likely to come into place

A belief that relevant innovation in this area will be crucial to our ongoing business success

A desire to be first to market with a new product/service in our industry

The need to keep up with our industry competitors

Increased customer demand (or belief that there is pent-up demand) for “green” products/services that use less carbon emissions in their creation

Increased customer demand (or belief that there is pent-up demand) for new “green” products/services that help cut users’ carbon emissions

Increased regulatory demands already in place

A belief that 'green' products/services can improve your company’s productivity

Other, please specify

Not applicable—we don’t currently provide “green” products/services

16

9

7

10

6

6

4

2

26

15

24

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012 © The Economist Intelligence Unit Limited 2012

20. What are the primary barriers to making further progress on carbon reduction in your company? Select up to three. (% respondents)Uncertainty about the future price of carbon

Availability at acceptable cost of relevant technologies

Lack of international standards (eg, an agreed method of calculating carbon emissions)

Unclear regulatory environment

Risk that environmental practices will raise your costs in comparison to competitors

Difficulty in developing relevant targets and measures

Lack of systems and tools to monitor and enforce compliance with the company’s environmental policies

Lack of client engagement/ demand

Difficulty in funding environmental efforts

Lack of buy in and commitment from senior management

Lack of employee engagement

Other, please specify

There are no barriers to making further progress

38

21

20

27

14

13

11

11

9

7

4

12

26

32

21. What do you think are the most crucial policies the federal government should pursue to encourage the reduction of carbon emissions? Select up to three. (% respondents)Mandating a gradual shift in the country’s energy supply towards cleaner sources

Subsidies for clean technology investments by companies

Establishment of incentives for green corporate behaviour

The current carbon pricing scheme

Establishment of environmental reporting standards

Subsidies for clean technology usage by consumers

Establishment of national carbon emission reduction goals

Provision of education on green practices for consumers

Provision of information on sustainable practices for companies

Establishment of penalties for lack of compliance by consumers

Establishment of penalties for lack of compliance by companies

Other, please specify

None of the above: government can help most by doing nothing and letting the market come up with solutions

42

22

18

26

17

14

14

10

8

4

2

15

34

25

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

© The Economist Intelligence Unit Limited 2012

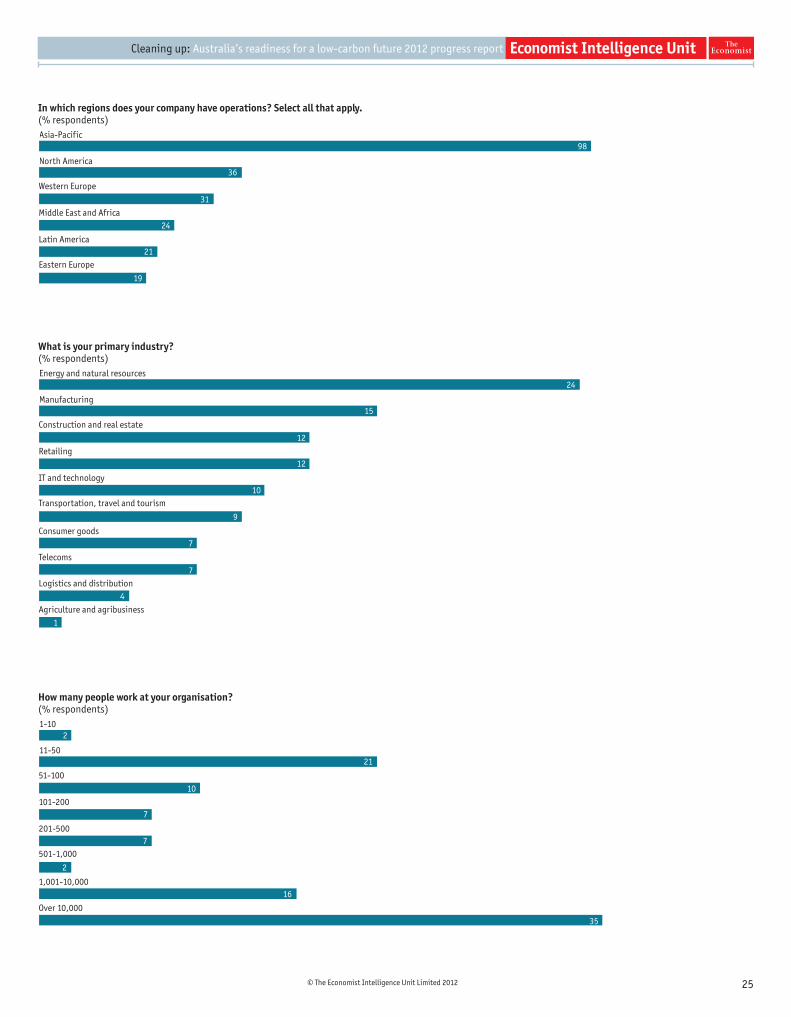

In which regions does your company have operations? Select all that apply.(% respondents)Asia-Pacific

North America

Western Europe

Middle East and Africa

Latin America

Eastern Europe

98

24

21

31

19

36

What is your primary industry?(% respondents)Energy and natural resources

Manufacturing

Construction and real estate

Retailing

IT and technology

Transportation, travel and tourism

Consumer goods

Telecoms

Logistics and distribution

Agriculture and agribusiness

24

10

12

12

9

7

7

4

1

15

How many people work at your organisation?(% respondents)1-10

11-50

51-100

101-200

201-500

501-1,000

1,001-10,000

Over 10,000

2

7

10

7

2

16

35

21

Cleaning up: Australia’s readiness for a low-carbon future 2012 progress report

26 © The Economist Intelligence Unit Limited 2012

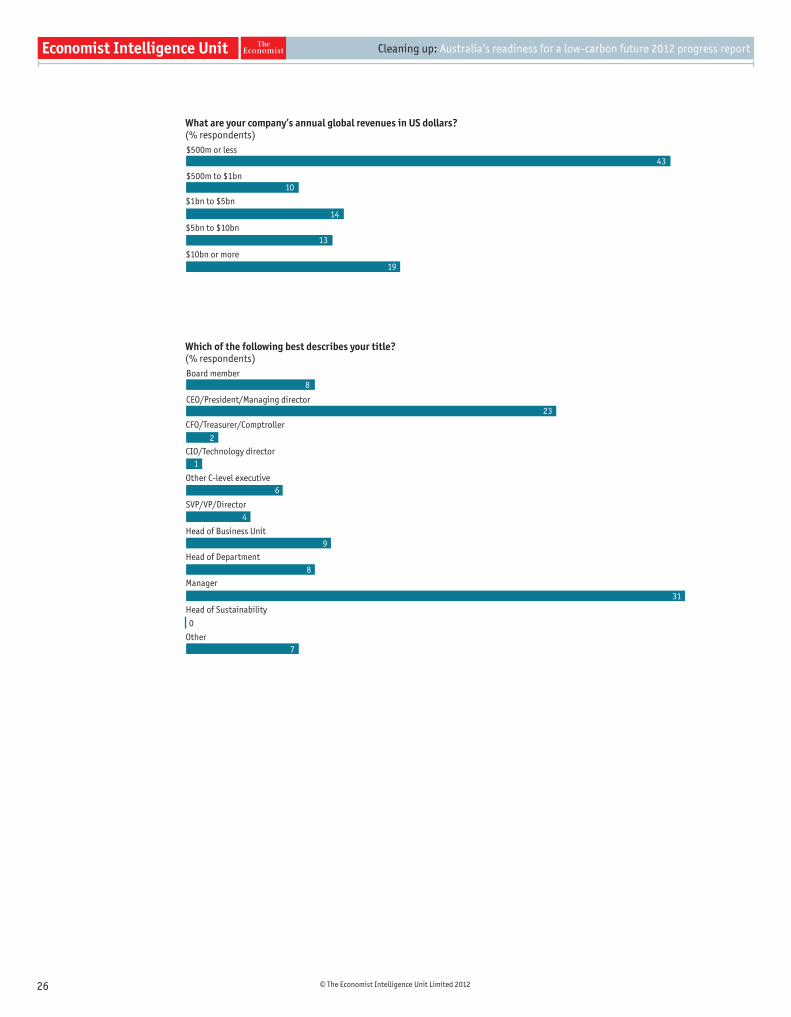

What are your company’s annual global revenues in US dollars?(% respondents)$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

43

19

14

13

10

Which of the following best describes your title?(% respondents)Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Head of Sustainability

Other

8

6

4

9

8

31

7

0

2

1

23

Whilst every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsor of this report can accept any responsibility or liability for reliance by any person on this report or any of the information, opinions or conclusions set out herein.

Cover image - Ivan Loh

LONDON26 Red Lion SquareLondonWC1R 4HQUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8500E-mail: [email protected]

NEW YORK750 Third Avenue5th FloorNew YorkNY 10017, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

HONG KONG6001, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

GENEVABoulevard des Tranchées 161206 GenevaSwitzerlandTel: (41) 22 566 2470Fax: (41) 22 346 9347E-mail: [email protected]