cleardebt group limited - britdaq group limited annual report... · cleardebt group limited report...

TRANSCRIPT

ClearDebt Group Limited

REPORT AND FINANCIAL STATEMENTS

for the year ended 30 June 2015

Registration Number 02441375

ClearDebt Group Limited CONTENTS

Page

Financial highlights 1

Directors and advisers 2

Chairman’s statement 3

Chief Executive’s statement 4-6

Directors’ report 7-10

Strategic review 11-12

Corporate governance 13-14

Directors’ remuneration report 15-16

Accounts

Independent Auditor’s report to the members of ClearDebt Group Limited 17-18

Consolidated statement of comprehensive income 19

Consolidated statement of financial position 20

Consolidated statement of changes in equity 21

Consolidated statement of cash flows 22

Notes to the consolidated financial statements 23-44

Company balance sheet 45

Notes to the company financial statements 46-51

Shareholder information 52

ClearDebt Group Limited FINANCIAL HIGHLIGHTS For the year ended 30 June 2015

1

2015 2014

£ £

Revenue 7,837,962 8,674,436

Gross profit 2,807,803 3,029,715

Loss before interest, tax, depreciation and amortisation (360,570) (255,067)

Loss from operations (820,100) (901,322)

Loss before taxation (841,559) (1,195,763)

Loss after taxation (852,591) (1,661,399)

Cash generated by operations 1,307,219 78,626

Since 1 July 2014 (2014: 1 July 2013), the following numbers of new Individual Voluntary Arrangements (IVA’s)

have been arranged through ClearDebt: -

Year ended Year ended

30 June 2015 30 June 2014

First quarter 477 669

Second quarter 393 608

Third quarter 231 620

Fourth quarter 296 733

_____ _____

1,397 2,630

_____ _____

As at 30 June 2015 the total number of active IVA’s and Protected Trust Deeds (“PTD’s”) was 9,516 (2014:

10,028). No new IVA or PTD cases were acquired during the year.

As at 30 June 2015 the total number of Debt Management Plans (“DMP’s”) under management was 627 (2014:

205).

ClearDebt Group Limited DIRECTORS AND ADVISERS

2

DIRECTORS

G Carey FCIB

D E M Mond FCA FCCA

D M Shalom ACA

A F Smith

A J Leon FCA

S Lee

SECRETARY

D E M Mond FCA FCCA

REGISTERED OFFICE

Nelson House

Park Road

Timperley

Altrincham

Cheshire

WA14 5BZ

AUDITORS

UHY Hacker Young Manchester LLP

Chartered Accountants

St James Buildings

79 Oxford Street

Manchester

M1 6HT

REGISTRARS

Britdaq Limited

Richmond House

Eastbourne Road

Blindley Heath

Lingfield

Surrey

RH7 6JX

BANKERS

The Royal Bank of Scotland PLC

P O Box 5429 Macclesfield & Stockport CRT

3rd Floor

38 Mosley Street Manchester M61 OHW

SOLICITORS DAC Beachcroft LLP

3 Hardman Street

Manchester

M3 3HF

DWF LLP

1 Scott Place

2 Hardman Street

Manchester

M3 3AA

ClearDebt Group Limited CHAIRMAN’S STATEMENT

3

I present the Group’s financial statements for the year ended 30 June 2015.

Group revenue was £7,837,962 (2014: £8,674,436) and gross profit was £2,807,803 (2014: £3,029,715). Earnings

before interest, tax, depreciation and amortisation resulted in a loss of £360,570 (2014: £255,067) after taking into

account a further exceptional profit of £76,321 (2014: £2,280,455) relating to further monies due on disposal of

the majority of the Group’s debt management book in 2014 and a further goodwill impairment of £938,927 (2014:

£3,463,353). After accounting for the above the Group made a loss after taxation of £852,591 (2014: £1,661,399)

after reduced net finance charges of £21,459 (2014: £294,441) and depreciation and amortisation charges of

£459,530 (2014: £646,255).

At the year end the Group’s net assets decreased to £3,233,861 (2014: £4,079,286). Cash flow remained positive

and cash balances increased to £969,791 (2014: £338,970) after the repayment of some £100,000 of loans leaving

the Group with a remaining debt of only £103,165 (2014: £203,750)

During the year our advice and debt management subsidiary Abacus (Financial Consultants) Limited (“Abacus”)

applied for authorisation by the Financial Conduct Authority (“FCA”) and is currently going through the approval

process but continues to operate under its interim permission with the FCA. Prices for DMP back books have

fallen substantially with the uncertainty of the FCA process and many industry buyers have now paused

acquisition of these books at any price until the FCA landscape becomes clearer.

Our Individual Voluntary Arrangement (“IVA”) subsidiary ClearDebt Limited has given up its FCA Interim

Permission as at 31 December 2014 and has not applied for a full FCA licence as it only deals with insolvency

cases. It has therefore taken advantage of the exclusion from the requirement for an FCA licence where the

Insolvency Practitioner is acting in reasonable contemplation of an Insolvency appointment.

In terms of numbers of new IVAs passed, the Group passed 1,397 new IVAs compared to 2,630 in 2014. The

numbers of IVAs in the marketplace peaked at the end of the June 2014 quarter and have been falling quarter on

quarter since. We believe this has occurred both as a result of the economic recovery, as well as the introduction

of the FCA regime in April 2014 which has led to large reductions in the number of referral organisations – who

have been unwilling or unable to comply with the new FCA requirements on debt advice.

We have had another successful year in recovering compensation for IVA clients who have often been mis-sold

Payment Protection Insurance (PPI). This continues to generate good additional supervisory income as mis-sold

PPI claims monies are paid into the IVA estate of our customers for the benefit of creditors. The majority of these

claims have however now been realised and we expect this income stream to drop off in the coming financial

year.

We continue to reduce our overheads wherever possible to enable us to continue to trade profitably going forward

without the benefit of the related supervisory income from PPI mis-sales. We anticipate a tough year ahead with

the increased costs of FCA regulation and the reduced IVA numbers in the marketplace although any anticipated

rises in UK interest rates may provide a boost to demand for our services.

We also intend to further tidy up our balance sheet by the cancellation of the deferred share capital and to facilitate

this we sought and received on 27 October 2015 shareholders’ approval to change our plc status back to that of a

private limited company. Hence, we are proposing at the forthcoming Annual General Meeting in December to

cancel the deferred share capital. The private limited company status will not affect the ability for shareholders to

trade our shares on the matched bargain facility provided by Britdaq.

Gerald Carey FCIB

Chairman

25 November 2015

ClearDebt Group Limited CHIEF EXECUTIVE’S STATEMENT

4

The Group has recorded a loss of £841,559 before taxation in the year.

Our debt management and advice subsidiary Abacus (Financial Consultants) Limited (“Abacus”) applied for its

full FCA authorisation on 19 December 2014 and is going through the approval process presently. We expect to

be granted full authorisation by the end of this calendar year and in the meantime Abacus continues to operate

under its interim permission.

The decision to sell the bulk of the debt management book and our timing in the latter part of the last financial

year appears to have been astute with prices falling substantially since then as the implications of the FCA regime

have been now fully understood by the market. Indeed, many buyers have paused or withdrawn from the industry

whilst they re-assess the value of such books given the substantial extra work the FCA require any purchasers to

do in reviewing the quality of the advice given to customers by the vendor. Invariably the books that are available

have become available due to vendor compliance issues with the FCA meaning substantial work needs to be

undertaken in both due diligence and in ensuring post acquisition in a short timescale that all plans acquired are

still appropriate for the customer’s current needs.

Abacus did however complete a purchase of a small back book of approximately 100 DMP’s in May 2015 for

some £39,000.

Substantial management time continues to be taken up with the FCA approval process for Abacus as the continual

requests for further information by the FCA is dealt with.

We have made substantial improvements to our systems and processes over the year and whilst time consuming,

it has enabled us to generate substantial management information to understand our business and customer needs

more clearly.

Following a review of the IVA business it was determined that it did not require FCA authorisation as it could

rely on the statutory Insolvency exclusion granted to licensed insolvency practitioners as ClearDebt Limited

(“ClearDebt”) only deals with insolvency cases. We therefore surrendered our interim permission on 31 December

2014 in respect of the ClearDebt business and did not seek FCA authorisation. IVAs remain the focus of the Group

although we continue to run a small debt management book to service customers who are not suitable for an IVA

and to whom a debt management plan is the most appropriate solution for them.

OPERATIONAL REVIEW

ClearDebt – IVA Division

The numbers of new IVA’s passed dropped markedly in the year reducing by 47% to 1,397 (2014: 2,630). The

insolvency statistics show that IVA numbers have been falling throughout the period and we continue to be

disciplined in our costs of acquisition in the face of many of our competitors who still appear to us to be paying

unsustainable rates for the provision of information required to put forward new cases.

No new IVA books were acquired during the year and as at 30 June 2015 we had a total of 9,516 (2014: 10,028)

IVA’s and PTD’s generating income. In April 2015 we completed the approval of a mass variation to our IVA

book with the agreement of creditors which enabled us to close large numbers of cases where the payments by the

customer were complete but the case had remained open solely pending the completion of PPI mis-selling

investigations.

The division made a loss before taxation of £632,208 (2014: £1,610,317) after Group recharges during the year

and after a goodwill write down of £938,927 (2014: £1,942,059). This represents a small decrease in profitability

when compared to last year where, excluding the goodwill write down, the division made a profit of £306,719

(2014: £331,742). Supervisory fees relating to PPI mis-selling redress once again made a good contribution to

profitability although we expect this to now tail off as the majority of the mis-sold PPI claims have now been

processed.

ClearDebt Group Limited CHIEF EXECUTIVE’S STATEMENT

5

The Board monitors (on a monthly basis) several key performance indicators (“KPIs”) for the business and

continues to monitor the number of cases passed, the cost per case acquired and the staff heads to caseload

numbers. We continue to only adopt referral and marketing relationships where the cost of acquisition is in our

view economic to make a profit over the life of a case as well as focusing on the compliance of lead introducers.

Where we find evidence of non–compliant selling with any of our partners we continue to insist on immediate

changes to ensure compliance or have terminate relationships. This has resulted in lower numbers of cases being

passed although encouraging new lead sources are starting to reverse that trend in recent months.

Abacus– Debt Management Division

The division made a loss before tax of £209,351 (2014: profit £414,554) after Group recharges. The profit last

year however included a net gain of £759,161 from the sale of the back book less goodwill write downs. The main

role of the division continues to be to provide debt advice although we have started to rebuild our debt management

book to service customers whose most appropriate solution is a debt management plan. As at 30 June 2015, the

total number of active DMP’s was 627 (2014: 205). We also received a further £76,321 of deferred consideration

in respect of the prior year sale of the back book.

The Board has KPIs to monitor the number of active income generating plans as well as the value of monthly

contributions made by debtors. The costs of acquisition of cases and plans are also monitored closely. IVA plans

remain our focus and we will only grow the book where customers unsuitable for an IVA require a DMP.

ClearCash – prepaid MasterCard

The division was sold just prior to the year end as we decided to focus on our core activities. We achieved a small

profit on the sale of the shares of the subsidiary ClearCash Limited although this was after the write down of the

start-up costs of the division of some £253,000 from the previous financial years.

The division made a small profit before taxation in the year, to the date of disposal, of £16,443 (2014: loss £27,837)

but the level of profitability and potential of the business was felt to be insufficient to justify the management time

going forward.

FINANCIAL REVIEW

Group turnover reduced to £7,837,962 (2014: £8,674,436) reflecting the reduced numbers of new IVAs passed.

Gross profit however declined by 7% to £2,807,803 (2014: £3,029,715) reflecting the continuing pressure on fees

and the costs of new customer acquisition. Losses before interest, tax, depreciation and amortisation amounted to

£360,570 (2014: £255,067) which included some £76,321 of deferred consideration in respect of the DMP back

book sales in 2014 and a further impairment of £938,927 against the carrying value of goodwill related to the

insolvency business (2014: £3,463,353). Finance costs decreased as expected to £21,962 (2014: £295,877)

following the repayment of the majority of the debt of the Group in 2014.

Cash resources increased during the year and at the year-end amounted to £969,791 (2014: £338,970). This is

pleasing especially after the payment of some £500,000 in taxation liabilities due in respect of the year ended 30

June 2014.

Operational cash flow remains satisfactory from the IVA casebook backed by our royalty income and PPI mis-

selling claims related supervisory income.

ClearDebt Group Limited CHIEF EXECUTIVE’S STATEMENT

6

GOING CONCERN

As part of the Groups going concern review the Board has followed the guidelines published by the Financial

Reporting Council entitled “Going Concern and Liquidity Risk: Guidance for UK Companies 2009”. The Board

has prepared detailed financial forecasts and cash flows for the two years to 30 June 2017 and in drawing up these

forecasts the Board has assumed that its application for Full Permission will be granted by the FCA to enable it

to continue to trade. The forecast assumptions are based upon its view of the current and future economic

conditions in the UK that will prevail over the forecasted period - given that the business is likely to be solely

focused on the UK market for the foreseeable future. We have produced sensitivities to these forecasts to test our

ability to trade as a going concern for at least the following 12 months. In addition, D E M Mond has provided

the Board with an undertaking of financial support in the event that the Group should require additional finance.

The Board believes that the use of the going concern basis of accounting is appropriate based upon a review of

these forecasts and the finance available to the Group.

FUTURE OUTLOOK

The IVA market is holding steady at similar levels to the past few years and whilst we have been increasing market

share the declining disposable incomes of indebted consumers continue to impact on IVA fees and our margins.

Profitability remains favourable although this is mainly due to the contribution from mis-sold PPI related

supervisory receipts which are expected to reduce over the next 12 months.

We continue to reduce our cost base wherever possible and we are carefully monitoring the cost of referrals and

marketing spend to ensure that new cases are acquired at an affordable level to achieve sustainable profitability

once mis-sold PPI claims related contributions reduce.

I would like to take this opportunity to thank all our employees for their dedication and hard work during the year

in providing our customers with the fair and sustainable solutions they require appropriate to their circumstances.

I would also especially like to thank all the staff for their efforts in documenting our systems and processes to

further enforce the high level principles of the FCA throughout our business and ensure that the customer’s best

interests remain at the heart of all we do.

Finally, the Board continues to look for ways in which value can be realised for shareholders although this is

proving difficult to achieve at present whilst the new FCA regime is currently being rolled out. We anticipate that

many participants and referrers in the industry may lose their licences to trade or take on new business in the next

few months making it hard to plan for until we know who the winners and losers under the new FCA regime will

be.

David Emanuel Merton Mond FCA FCCA

Chief Executive Officer

25 November 2015

ClearDebt Group Limited DIRECTORS’ REPORT

7

The Directors present their report and the financial statements of the Group for the year ended 30 June 2015.

ClearDebt Group Limited is a parent company, incorporated and domiciled in England.

Principal Activities and Review of the Business

The principal activity of the Group is the provision of financial advice and appropriate solutions to individuals

experiencing personal debt problems.

The principal activity of the Company is that of a holding company.

A review of the Group’s activities and its future prospects is detailed in the Chairman’s Statement on page 3 and

the Chief Executive’s Statement on pages 4 to 6.

Results and Dividends

The trading results for the year and the Group’s financial position at the end of the year are set out in the attached

financial statements.

The Directors do not recommend payment of a dividend (2014: nil).

Share Capital

The Company is aware of the following substantial interests in the ordinary share capital as at 25 November 2015:

Number of shares held % of Total

D E M Mond 119,054,616 38.61

O Mond 17,459,800 5.66

A Mond 15,373,733 4.99

S Mond 15,232,602 4.94

D Murray 11,921,125 3.87

Mrs M Rose 11,328,466 3.67

The Directors are not aware of any other person who is beneficially interested in 3% or more of the issued share

capital.

Directors who held office during the year The Directors of the Company who held office during the year are as follows:

G Carey FCIB (Non-Executive Chairman)

D E M Mond FCA FCCA

A F Smith

D M Shalom ACA

S Lee

A J Leon FCA (Non-Executive)

Payment of Creditors

It is the Group’s policy to consider the terms of payment with suppliers when agreeing the terms of the transaction,

to ensure that suppliers are aware of these terms and abide by them. Trade creditor days for the Group at 30 June

2015, were 10 days (2014: 13 days). This represents the ratio, expressed in days, between the amounts invoiced

to the Group in the period by its suppliers and the amounts due, at the year end, to trade creditors falling due for

payment within one year.

Employee Involvement The Group recognises and seeks to encourage the involvement of its employees, with the aim being the

recruitment, motivation and retention of quality employees throughout the Group.

The Group’s employment policies, including the commitment to equal opportunity, are designed to attract, retain

and motivate employees regardless of sex, race, religion or disability. The Group is committed to ensuring and

communicating the requirements for a safe and healthy working environment for all employees, consistent with

health and safety legislation and, wherever practicable, gives full consideration to applications for employment

from disabled persons.

Principal Risks and Uncertainties

ClearDebt Group Limited DIRECTORS’ REPORT

8

All businesses face a range of risks and uncertainties, being subject to risk factors from internal and external

sources. The Board considers the likelihood and significance of risk factors when putting in place risk management

procedures to ensure risk mitigation.

The following are considered to be the key risks facing the Group: -

1. Compliance – the industry is adapting to a strict new compliance regime regulated by the FCA. Businesses

and their referral partners have to apply for the first time for Full Permission from the FCA to continue to

trade. The licence application made by Abacus (Financial Consultants) Limited was submitted by the 31

December 2014 deadline and we expect to receive Full Permission before the end of 2015. There are

therefore risks that Full Permission may not be received or restrictions are placed upon our activities. In

addition, there are risks that some of our key referral partners may not achieve licence approval. We continue

to invest heavily in our compliance regime and we are also providing advice and assistance to those referral

partners we have carefully selected to help them meet the standards required by the FCA.

2. Competition - the market for debt resolution solutions remains highly competitive. The Group seeks to

manage the risk of losing referrers through providing innovative solutions supported by high quality delivery.

The Group’s main marketing channel is through referrals and the internet and the Group monitors closely

the strategies of competitors and the prices paid in the market place and reacts appropriately where necessary.

3. Credit risk – the Group’s credit risk is attributable to its trade receivables and is managed by daily monitoring

of customer’s payments into their programmes versus agreed contracted terms.

4. Funding arrangements – the Group monitors cash flow as part of its normal activities. Cash flow positions

are discussed with the Board on a monthly basis to ensure that all possible treasury benefits are being taken

and facilities are available if necessary. Advertising and marketing spend is monitored closely as it is a key

component of funding requirements.

5. Royalty income - substantial revenue has been earned from royalty income from a third party which provides

outsourced services to ClearDebt Limited and other companies which manage IVA’s and Protected Trust

Deeds (PTD’s). These services are provided to and paid for by, the estates of the respective IVA’s and PTD’s.

Calculation of the amount of revenue due to ClearDebt Limited is based on the revenue invoiced by the third

party. Should these services cease to be chargeable to the estates then the reduction in royalty income would

significantly affect the reported revenues and profits of ClearDebt Limited and the Group.

6. Economic environment – the current economic climate remains favourable as the market for indebted

consumers is likely to continue to grow in the next few years although the amount of disposable income that

consumers have available for solutions remains depressed - leading to pressure on margins.

7. Creditor Pressure – Creditors can restrict the market for personal debt resolutions by refusing to agree to

proposals which they do not deem acceptable. This can have the effect of restricting approvals and therefore

the timing of fees or the receipt of any fees at all. The Group is actively involved in talking to creditors both

independently and through its Trade Association, Debt Resolution Forum constantly to ensure that all Group

products are in line with creditor approval criteria as much as possible.

Risks associated with financial instruments entered into by the Group are detailed in note 20.

ClearDebt Group Limited DIRECTORS’ REPORT

9

Directors’ Responsibilities The directors are responsible for preparing the Annual Report and the financial statements in accordance with

applicable laws and regulations.

Company law requires the directors to prepare such financial statements for each financial year. Under that law

the directors have chosen to prepare group financial statements in accordance with International Financial

Reporting Standards (IFRSs) as adopted by the European Union and have chosen to prepare the parent company

financial statements under in accordance with United Kingdom Generally Accepted Accounting Practice (United

Kingdom Accounting Standards and applicable law). Under company law the directors must not approve the

accounts unless they are satisfied that they give a true and fair view of the state of affairs of the Company and of

the profit or loss of the company for that period.

In preparing the parent company financial statement, the directors are required to:

- select suitable accounting policies and apply them consistently;

- make judgements and accounting estimates that are reasonable and prudent;

- state whether UK Accounting Standards have been followed, subject to any material departures disclosed

and explained in the financial statements; and

- prepare the financial statements on the going concern basis unless it is inappropriate to presume that the

company will continue in business.

In preparing the group financial statements, International Accounting Standard 1 requires that the directors:

- properly select and apply accounting policies;

- present information, including accounting policies, in a manner that provides relevant, reliable, comparable

and understandable information;

- provide additional disclosures when compliance with the specific requirements in IFRS are insufficient to

enable users to understand the impact of particular transactions, other events and conditions on the entity's

financial position and financial performance; and

- make an assessment of the Company's ability to continue as a going concern.

The directors are responsible for keeping adequate accounting records that are sufficient to show and explain the

company’s transactions and disclose with reasonable accuracy at any time the financial position of the company

and enable them to ensure that the financial statements comply with the Companies Act 2006. They are also

responsible for safeguarding the assets of the Company and hence for taking reasonable steps for the prevention

and detection of fraud and other irregularities.

The directors are also responsible for the maintenance and integrity of the corporate and financial information

included on the company’s website. Legislation in the United Kingdom governing the preparation and

dissemination of financial statements may differ from legislation in other jurisdictions.

We confirm that to the best of our knowledge:

1. the financial statements, prepared in accordance with the relevant financial reporting framework, give a true

and fair view of the assets, liabilities, financial position and profit or loss of the company and the undertakings

included in the consolidation taken as a whole; and

2. the strategic review, includes a fair review of the development and performance of the business and the position

of the company and the undertakings included in the consolidation taken as a whole, together with a description

of the principal risks and uncertainties that they face.

Statement as to Disclosure of Information to Auditors

The directors who were in office on the date of approval of these financial statements have confirmed, as far as

they are aware, that there is no relevant audit information of which the auditors are unaware. Each of the directors

has confirmed that they have taken all the steps that they ought to have taken as directors in order to make

themselves aware of any relevant audit information and to establish that it has been communicated to the auditor.

ClearDebt Group Limited DIRECTORS’ REPORT

10

Auditors UHY Hacker Young Manchester LLP, Chartered Accountants has indicated its willingness to continue in office

and a resolution that they should be re-appointed as auditors will be put to the members at the annual general

meeting.

By order of the Board

D E M Mond

Company Secretary

25 November 2015

ClearDebt Group Limited STRATEGIC REVIEW

11

The Companies Act 2006 requires the Board of Directors to regularly review its operations against its strategic

objectives and to report on an annual strategic review. The following section summaries the Board’s review for

the financial year of this report.

Activities and status

The principal activity of the Group is the provision of financial advice and appropriate solutions to individuals

experiencing personal debt problems. In addition to this review statement the Chairman’s and Chief Executives’

Statements on pages 3 - 6 and the financial report give a review of developments during the year and of future

prospects.

The directors consider that the Company was not at any time up to the date of this report a close company within

the meaning of Section 414 of the Act.

Our Strategic Approach

Our strategy remains to provide the highest standard of debt advice to indebted consumers in the UK ensuring

that they receive the solution most appropriate for their circumstances. We listen to our customers and take a

collaborative working approach to map out a bespoke solution for their specific requirements. By treating our

customers fairly and providing successful outcomes we aim to build a trusted partner relationship which may be

used to provide additional services once their debt solution has been completed.

As we build our brand so the costs of customer acquisition and the costs of failed solutions will reduce and ensure

we can produce sustainable long term profits to our shareholders.

Our Strategy is driven by our Values At the core of our vision – satisfactory returns for our shareholders through sustainable long term profits - three

values guide how we conduct our business. We work to be:

a. Ethical and responsible

i. For people - our shareholders and the public

ii. For standards in business practice

iii. For the environment

b. Open

iv. Having honest relationships with our customers and shareholders

c. Transparent

v. In our approach to all so that we can take responsibility for all we do and be held to account for our

advice and solutions at all times.

Business Objectives - A Partner of Choice

Our vision is to create long term sustainable returns for our shareholders by being the partner of choice for both

our customers and referrers.

Principal risks and uncertainties

The principal risks and uncertainties facing the Group are set out in page 8 of the director’s report.

Environmental matters and our business in Society

a. Our Commitment to the Community

We believe that as a responsible business working in the community we should support those organisations

we can to help improve the world in which we live. In 2015 we have supported several local charities and

have made donations to a locally based charity to enable free debt advice to indebted individuals to be

provided both locally and across the country.

ClearDebt Group Limited STRATEGIC REVIEW

12

b. Our Environment

We are committed to improving the environment and minimising any negative impact our activities may have

upon it. We encourage our partners to make similar commitments.

We are committed to energy efficiency and to reducing our carbon footprint. We will select, configure and

use any vehicles we acquire to ensure the maximum efficiency. We encourage the use of public transport

whenever possible. We will encourage energy efficient lighting, heating and air-conditioning systems and

practice building energy management.

c. People

We believe we can only become better at what we do and more successful as a business by encouraging and

supporting our people to discover their talents and make the most of their capabilities.

We are committed to invest time and resources to ensuring that all of our people at every level in our own

company and in those of our partners are equipped with the necessary skills to meet current and future

business needs and to aid their own professional and personal development. We believe in structured

continuing professional development is the key to personal fulfilment and to delivering better services

competitively.

Health and safety is of paramount importance to us all and we encourage both our partners and our own

management to pursue the highest possible standards meeting all regulatory requirements.

d. Business Ethics

Trust is important today more than ever and building and maintaining our reputation is absolutely the key to

us.

The long term trusted relationships we build with our partners are rooted in our open, trusting and positive

values.

We recognise the vital importance that clarity, open communication and delivery to expectation have in

building confidence and trust.

Key performance indicators

The financial key performance indicators are set out in the operational review of the Chief Executive on pages 4

and 5.

Financial Instruments

Information in respect of the Group’s policies on financial risk management objectives including policies to

manage credit risk, liquidity risk and foreign currency risk are given in note 20 to the financial statements.

By order of the Board

D E M Mond

Director

25 November 2015

ClearDebt Group Limited CORPORATE GOVERNANCE

13

Principles of Corporate Governance The Group’s Board appreciates the value of good corporate governance not only in the areas of accountability and

risk management but also as a positive contribution to business prosperity. It believes that corporate governance

involves more than a simple “box ticking” approach to establish whether a company has met the principles

(including those set out in the corporate governance guidelines for AIM companies published by the Quoted

Companies Alliance in September 2010) of a number of specific rules and regulations. Rather the issue is one of

applying corporate governance in a sensible and pragmatic fashion having regard to the individual circumstances

of a particular company’s business. The key objective is to enhance and protect shareholder value.

Board Structure

The Board is responsible to shareholders for the proper management of the Group. A statement of Directors’

responsibilities in respect of the accounts is set out in the directors’ report.

The Non-Executive Directors have a particular responsibility to ensure that the strategies proposed by the

Executive Directors are fully considered.

To enable the Board to discharge its duties, all Directors have full and timely access to all relevant information

and there is a procedure for all Directors, in furtherance of their duties, to take independent professional advice,

if necessary, at the expense of the Group. The Board has a formal schedule of matters reserved to it and meets

monthly. It is responsible for overall group strategy, approval of major capital expenditure projects and

consideration of significant financing matters.

The following Committees have been set up, which have written terms of reference and deal with specific aspects

of the Group’s affairs.

1. The Remuneration Committee, which includes D E M Mond and the two Non-Executive Directors, is

responsible for making recommendations to the Board on the Company’s framework of executive

remuneration and its cost. The Committee determines the contract terms, remuneration and other benefits

for each of the Executive Directors, including pension rights and compensation payments. The Board itself

determines the remuneration of D E M Mond and the Non-Executive Directors. The Committee meets as

required.

2. The Audit Committee includes the two Non-Executive Directors. Its prime tasks are to review the scope of

the external audit, to review reports from the auditors and to review the half-yearly and annual accounts

before they are presented to the Board, focusing in particular on accounting policies and areas of

management judgment and estimation. The Committee is responsible for monitoring the controls, which are

in force to ensure the integrity of the information reported to the shareholders. The Committee acts as a

forum for discussion of internal control issues and contribute to the Board’s review of the effectiveness of

the Group’s internal control and risk management systems and processes. It advises the Board on the

appointment of external auditors and on their remuneration for both audit and non-audit work and discusses

the nature and scope of the audit with the external auditors. It reviews and monitors the independence of the

auditors especially with regard to non-audit work. It meets at least twice a year including immediately before

the submission of the annual and interim financial statements to the Board.

Any new Non-Executive Directors will be asked to join both Committees.

No formal nomination Committee exists in view of the stage of development of the Group. Instead appointments

to the Board by the Chief Executive and other Executive Directors are discussed with the Non-Executive

Chairman. Appointments are made after an evaluation of the skills, knowledge, and expertise required ensuring

that the Board as a whole has the ability to ensure that the Group can continue to compete effectively in its market

place.

Internal Control

The Directors are responsible for the Group’s system of internal control and for reviewing its effectiveness. The

Board has designed the Group’s system of internal control in order to provide the Directors with reasonable

assurance that its assets are safeguarded, that transactions are authorised and properly recorded and that material

errors and irregularities are either prevented or would be detected within a timely period. However, no system of

internal control can eliminate the risk of failure to achieve business objectives or provide absolute assurance

against material misstatement or loss. The key elements of the control system in operation are:

ClearDebt Group Limited CORPORATE GOVERNANCE

14

a. The Board meets regularly with a formal schedule of matters reserved to it for decision and has put in place

an organisational structure with clear lines of responsibility defined and with appropriate delegation of

authority;

b. There are procedures for planning, approval and monitoring of capital expenditure and information systems

for monitoring the Group’s financial performance against approved budgets and projections;

The process adopted by the Group accords with the guidance contained in the document “Internal Control

Guidance for Directors on the Combined Code” issued by the Institute of Chartered Accountants in England and

Wales.

The Audit Committee receives reports from the external auditors on a regular basis and from Executive Directors

of the Group. The Board has considered whether the Group’s internal controls processes would be significantly

enhanced by an internal audit function and has taken the view that at the Group’s current stage of development,

this is not required. The Board will continue to review this matter each year. The Board receives periodic reports

from all Committees.

There are no significant issues disclosed in the financial statements for the period ended 30 June 2015 and up to

the date of approval of the report and financial statements that have required the Board to deal with any related

material internal control issues.

Relations with Shareholders The Group values its dialogue with both institutional and private investors. Effective two-way communication

with fund managers, institutional investors and analysts is pursued and this encompasses issues such as

performance, policy and strategy. During the year the Directors have not had any meetings with analysts and

institutions, though have had discussions with a number of shareholders when requested.

There is also an opportunity, at the Company’s Annual General Meeting for individual shareholders to raise

general business matters with the full Board and notice of the Company’s Annual General Meeting is circulated

to all shareholders at least 20 working days before such meeting. The Chairman of the Audit and Remuneration

Committee will be available at the Annual General Meeting to answer questions.

ClearDebt Group Limited DIRECTORS’ REMUNERATION REPORT

15

The Board’s Remuneration Committee, which currently comprises Gerald Carey (Non-Executive Chairman),

Anthony Leon (Non-executive director) and David Mond (Chief Executive Officer), makes recommendations to

the Board within agreed terms of reference in determining specific remuneration packages for each of the

Directors, including pension rights.

Members of the Committee who have a personal financial interest in the matters to be decided are not involved in

decisions. In arriving at its recommendations, the Committee has access to professional advice from both within

and outside the Company.

Remuneration Policy

Each remuneration package is reviewed against a background of published comparative information on the

remuneration of Executive Directors in similar positions, taking into account the industry, the region of

employment, the type of work and the size of the Company. The extent to which the recommended remuneration

is above or below average takes account of the Director’s qualifications and length of service with the Company,

the Director’s actual performance and the performance of the Company. This will remain the policy for

forthcoming years.

Directors’ Emoluments The emoluments of the Directors from the date of their appointment during the financial year ended 30 June 2015

were as follows:

2015 2014

2015 Total Total

Salary & 2015 Salary & Salary &

Benefits Pensions Benefits Benefits

£’000 £’000 £’000 £’000

Executive Directors

David Mond (Chief Executive Officer) 273 - 273 195

David Shalom (Finance Director) 223 - 223 146

Andrew Smith (Marketing & External Affairs Director) 52 - 52 51

Simon Lee (Chief Operating Officer) 200 - 200 120

Non-Executive Directors Gerald Carey (Chairman) 23 - 23 23

Anthony Leon 15 - 15 15

___ ___ ___ ___

Aggregate remuneration 786 - 786 550

___ ___ ___ ___

On 1 August 2014, in line with UK legislation on pensions, the executive directors and employees of the Group

were auto enrolled into a defined contribution pension scheme set up to satisfy the legislation. David Shalom opted

out of the scheme. The 3 remaining executive directors received less than £500 each in payments made on their

behalf by the Group in accordance with the scheme rules.

Under the terms of the scheme those members of staff that did not opt out had 1% of their gross salary deducted

and paid into the scheme on their behalf whilst the employing company paid in a further 1% into the scheme on

their behalf. The level of contributions and company funding will increase in line with the present statutory

requirements under the legislation.

Directors’ Options

Options have been granted to directors under an EMI scheme. The granting of options ensures that the holders are

incentivised to concentrate on growing shareholder value. No share options were granted during the year leaving

options outstanding over 5,500,000 ordinary shares at a weighted average exercise price of 1.82p per ordinary

share.

Directors’ Service Agreements

Anthony Leon, Gerald Carey and David Mond all have agreements subject to 6 months’ notice. David Shalom,

Andrew Smith and Simon Lee all have service agreements subject to 12 months’ notice.

ClearDebt Group Limited DIRECTORS’ REMUNERATION REPORT

16

Directors’ Interests The interests of the Directors in the ordinary shares of the Company were as follows:

Ordinary Shares

At 0.5p each At 0.5p each

At 30 June At 30 June

2015 2014

David Mond 119,054,616 119,054,616

Andrew Smith 6,750,000 6,750,000

David Shalom 2,150,000 2,150,000

Gerald Carey 1,020,000 1,020,000

Anthony Leon 500,000 500,000

The directors held the following interests in share options as at 30 June 2015 and 25 November 2015.

At 30 June At 30 June Option Date Expiry

Scheme 2015 2014 Price Exercisable Date

David Mond EMI 375,000 375,000 2.00p 07.10.12 07.10.19

David Mond EMI 500,000 500,000 1.75p 21.09.13 21.09.20

David Mond EMI 750,000 750,000 1.75p 31.10.14 31.10.21

Andrew Smith EMI 375,000 375,000 2.00p 07.10.12 07.10.19

Andrew Smith EMI 750,000 750,000 1.75p 31.10.14 31.10.21

David Shalom EMI 375,000 375,000 2.00p 07.10.12 07.10.19

David Shalom EMI 500,000 500,000 1.75p 21.09.13 21.09.20

David Shalom EMI 750,000 750,000 1.75p 31.10.14 31.10.21

Simon Lee EMI 375,000 375,000 2.00p 07.10.12 07.10.19

Simon Lee EMI 750,000 750,000 1.75p 31.10.14 31.10.21

INDEPENDENT AUDITOR’S REPORT

TO THE MEMBERS OF CLEARDEBT GROUP LIMITED

17

We have audited the Group and Parent Company financial statements which comprise the Consolidated Statement

of Comprehensive Income, Consolidated Statement of Financial Position, the Company Balance Sheet, the

Consolidated Statement of Cash Flows, the Consolidated Statement of Changes in Equity and the related notes.

The financial reporting framework that has been applied in the preparation of the Group financial statements is

applicable law and International Financial Reporting Standards (IFRSs) as adopted by the European Union. The

financial reporting framework that has been applied in the preparation of the Parent Company financial statements

is applicable law and United Kingdom Accounting Standards (United Kingdom Generally Accepted Accounting

Practice).

This report is made solely to the Company’s members, as a body, in accordance with Chapter 3 of Part 16 of the

Companies Act 2006. Our audit work has been undertaken so that we might state to the Company’s members

those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent

permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s

members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of directors and auditors As more fully explained in the Directors’ Responsibilities Statement, the directors are responsible for the

preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility

is to audit and express an opinion on the financial statements in accordance with applicable law and International

Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s

(APB’s) Ethical Standards for Auditors.

Scope of the audit of the financial statements An audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to

give reasonable assurance that the financial statements are free from material misstatement, whether caused by

fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the company's

circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant

accounting estimates made by the directors; and the overall presentation of the financial statements. In addition,

we read all the financial and non-financial information in the annual report to identify material inconsistencies with

the audited financial statements and to identify any information that is apparently materially incorrect based on, or

materially inconsistent with, the knowledge acquired by us in the course of performing the audit. If we become

aware of any apparent material misstatements or inconsistencies we consider the implications for our report.

Opinion on the financial statements

In our opinion the financial statements:

- the financial statements give a true and fair view of the state of the Group’s and of the Parent Company’s

affairs as at 30 June 2015 and of the Group’s loss for the year then ended;

- the Group financial statements have been properly prepared in accordance with IFRSs as adopted by the

European Union;

- the Parent Company financial statements have been properly prepared in accordance with United Kingdom

Generally Accepted Accounting Practice; and

- the financial statements have been prepared in accordance with the requirements of the Companies Act 2006.

Opinion on other matters prescribed by the Companies Act 2006

In our opinion the information given in the Directors’ Report for the financial year for which the financial

statements are prepared is consistent with the financial statements.

INDEPENDENT AUDITOR’S REPORT

TO THE MEMBERS OF CLEARDEBT GROUP LIMITED

18

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report

to you if, in our opinion:

- adequate accounting records had been kept; or

- returns adequate for our audit have not been received from branches not visited by us; or

- the Parent Company financial statements are not in agreement with the accounting records and returns; or

- certain disclosures of directors’ remuneration specified by law are not made.

- we have not received all the information and explanations that we considered necessary for the purpose of

our audit.

Michael D Wasinski

(Senior Statutory Auditor)

For and on behalf of

UHY HACKER YOUNG MANCHESTER LLP

Chartered Accountants and Statutory Auditor

25 November 2015

St James Building

79 Oxford Street

Manchester

M1 6HT

ClearDebt Group Limited CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

For the year ended 30 June 2015

19

2015 2014

Notes £ £

Revenue 3 7,837,962 8,674,436

Cost of sales (5,030,159) (5,644,721)

_________ _________

Gross profit 2,807,803 3,029,715

Administrative expenses (2,303,090) (2,071,919)

Profit on disposal of debt management books 76,321 2,280,455

Profit on disposal of subsidiary 6 4,489 -

Goodwill impairment 10 (938,927) (3,463,353)

Share based payment 17 (7,166) (29,965)

_________ _________

Loss before interest, tax,

depreciation and amortisation (360,570) (255,067)

Depreciation 11 (182,431) (193,118)

Amortisation 10 (277,099) (453,137)

Gain on bargain purchase - -

_________ _________

Loss from operations 4 (820,100) (901,322)

Finance costs 5 (21,962) (295,877)

Finance income 503 1,436

_________ _________

Loss before taxation (841,559) (1,195,763)

Taxation 8 (11,032) (465,636)

_________ _________

Loss after taxation and total comprehensive

loss for year (852,591) (1,661,399)

_________ _________

Amount attributable to:

Owners of the parent (852,591) (1,661,399)

_________ _________

Loss per ordinary share - basic (pence) 9 (0.28p) (0.54p)

Loss per ordinary share - diluted (pence) 9 n/a n/a

_________ _________

ClearDebt Group Limited CONSOLIDATED STATEMENT OF FINANCIAL POSITION

As At 30 June 2015 Company Number 02441375

20

2015 2014

Notes £ £

Assets

Non-current assets Intangible assets 10 91,209 1,264,758

Property, plant and equipment 11 241,676 337,899

Deferred taxation 15 20,349 19,918

__________ _________

353,234 1,622,575

Current asset

Trade and other receivables 12 2,870,754 4,123,800

Cash and cash equivalents 969,791 338,970

__________ _________

3,840,545 4,462,770

__________ _________

Total assets 4,193,779 6,085,345

__________ _________

Equity and liabilities

Equity Issued capital 16 6,166,812 6,166,812

Share premium 279,948 279,948

Share based compensation 376,484 369,318

Retained losses (3,589,383) (2,736,792)

__________ _________

Total equity attributable to the owners of the parent 3,233,861 4,079,286

__________ _________

Current liabilities Trade and other payables 13 847,141 1,301,457

Corporation tax payable 13 9,612 500,852

Current financial liabilities 13 103,165 150,000

__________ _________

959,918 1,952,309

Non-current liabilities Financial liabilities 14 - 53,750

__________ _________

Total liabilities 959,918 2,006,059

__________ _________

Total equity and liabilities 4,193,779 6,085,345

__________ _________

The financial statements were approved by the Board of Directors and authorised for issue on 25 November 2015

and are signed on its behalf by:

D E M Mond

Director

ClearDebt Group Limited CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

For the year ended 30 June 2015

21

Issued Share Share Share Based Other Retained Total

Capital Premium Compensation Reserves Losses Equity

£ £ £ £ £ £

Balance as at 30 June 2013 6,166,812 279,948 339,353 - (1,075,393) 5,710,720

Share based compensation - - 29,965 - - 29,965

Total comprehensive loss - - - - (1,661,399) (1,661,399)

for the year

________ ________ ________ _______ _________ ________

Balance as at 30 June 2014 6,166,812 279,948 369,318 - (2,736,792) 4,079,286

Share based compensation - - 7,166 - - 7,166

Total comprehensive loss - - - - (852,591) (852,591)

for the year

________ ________ ________ _______ ________ ________

Balance as at 30 June 2015 6,166,812 279,948 376,484 - (3,589,383) 3,233,861 ________ ________ ________ _______ _________ ________

Share capital

Share capital has arisen on the issue of shares and represents the nominal value of shares issued.

Share premium

The share premium account arose from the issue of equity shares above the nominal value less share issue costs.

Share based compensation

This reserve is the result of the Company’s grant of equity settled share options and warrants and measured in

accordance with IFRS2 share-based payment.

Retained losses

The retained losses reflect losses incurred to date.

ClearDebt Group Limited CONSOLIDATED STATEMENT OF CASH FLOWS

For the year ended 30 June 2015

22

2015 2014

£ £

Cash flow from continuing operating activities

Loss before taxation (841,559) (1,195,763)

Depreciation of property, plant and equipment 182,431 193,118

Amortisation of intangible assets 277,099 453,137

Profit on sale of subsidiary (4,489) -

Profit on disposal of debt management books (76,321) (2,280,455)

Goodwill impairment 938,927 3,463,353

Loss on disposal of fixed assets 2,339 101,246

Share based payment 7,166 29,965

Decrease/ (increase) in trade and other receivables 1,254,483 (1,166,260)

Finance costs 21,962 295,877

Finance income (503) (1,436)

(Decrease)/ increase in trade and other payables (454,316) 185,844

_________ _________ Cash generated by operations 1,307,219 78,626

Corporation tax (paid)/ refund (500,151) 52,832

Interest on loans (21,962) (295,877)

_________ _________

Net cash generated by/ (used in) operating activities 785,106 (164,419)

Investing activities Acquisition of intangibles (42,542) (288,690)

Acquisition of property, plant and equipment (88,482) (66,467)

Disposal of intangible assets 76,321 2,819,035

Sale of subsidiary 500 -

Finance income 503 1,436

_________ _________

Net cash (used in) /generated by investing activities (53,700) 2,465,314

Financing activities Repayment of existing loans (200,585) (2,250,000)

Proceeds from new loans advanced 100,000 200,000

_________ _________

Cash used by financing activities (100,585) (2,050,000)

Increase in cash and cash equivalents 630,821 250,895

Opening cash and cash equivalents 338,970 88,075

_________ _________

Closing cash and cash equivalents 969,791 338,970

_________ _________

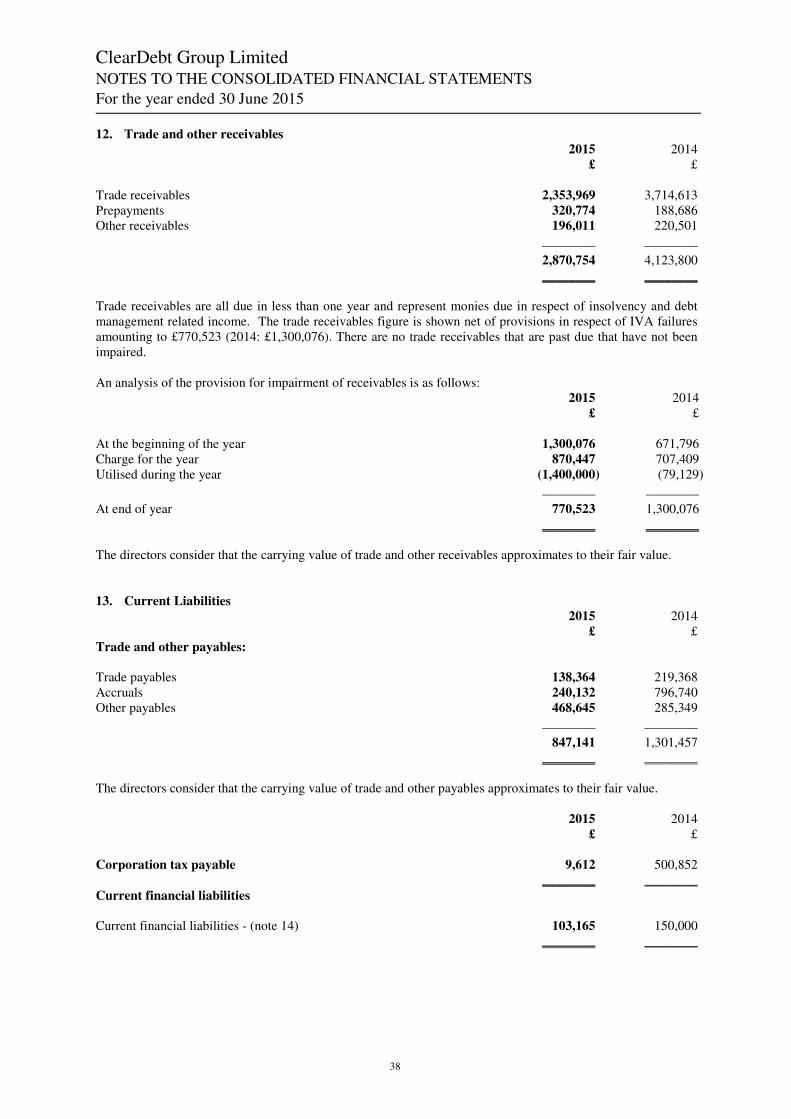

ClearDebt Group Limited NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 30 June 2015

23

1. General information

ClearDebt Group Limited is a company incorporated and domiciled in the United Kingdom under the Companies

Act 2006. The Group’s functional and presentational currency is £ sterling.

Interpretations of standards The following accounting standards, interpretations and amendments have been adopted by the Company since 1

July 2014 with no significant impact on its results or financial position:

IAS 27 “Separate Financial Statements (2011)

IAS 28 “Investments in Associates and Joint Ventures”

IAS 32 “Offsetting Financial Assets and Financial Liabilities”

IFRS10 “Consolidated Financial Statements”

IFRS 11 “Joint Arrangements”

IFRS 12 “Disclosures of Interest in Other Entities”

The following standards, interpretations and amendments to existing standards have been published and are

mandatory for the Company’s accounting periods beginning on or after 1 July 2015 or later periods, but which

have not been adopted by the Company:

Annual improvements to IFRSs 2010-2012 cycle and 2011-2013 Cycle.

IAS 16 and IAS 38 - Clarification of Acceptable Methods of Depreciation and Amortisation effective from 1

January 2016

IFRS 7 Amendment related to transition to IFRS is effective from 1 January 2016

IFRS 9 “Financial Instruments” is effective from 1 January 2018.

The Directors anticipate that the adoption of these standards and interpretations in future periods will have no

material impact on the financial statements of the Group.

2. Significant Accounting Policies

Basis of Preparation The financial statements have been prepared in accordance with International Financial Reporting Standards and

IFRIC interpretations as endorsed by the European Union (IFRS) and the requirements of the Companies Act 2006

applicable to companies reporting under IFRS.

The financial statements have been prepared on the historic cost basis. The principal accounting policies adopted

are set out below.

Going concern As part of the Groups going concern review the Board has followed the guidelines published by the Financial

Reporting Council entitled “Going Concern and Liquidity Risk: Guidance for UK Companies 2009”. The Board

has prepared detailed financial forecasts and cash flows for the two years to 30 June 2016 and in drawing up these

forecasts the Board has assumed that its application for Full Permission will be granted by the FCA to enable it to

continue to trade. The forecast assumptions are based upon its view of the current and future economic conditions

in the UK that will prevail over the forecasted period - given that the business is likely to be solely focused on the

UK market for the foreseeable future. We have produced sensitivities to these forecasts to test our ability to trade

as a going concern for at least the following 12 months. In addition, D E M Mond has provided the Board with an

undertaking of financial support in the event that the Group should require additional finance.

The Board believes that the use of the going concern basis of accounting is appropriate based upon a review of

these forecasts and the finance available to the Group.

ClearDebt Group Limited NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 30 June 2015

24

2. Significant Accounting Policies (continued)

Critical Accounting Estimates and Judgements

The preparation of the financial information in conformity with IFRS requires management to make judgements,

estimates and assumptions that affect the application of policies and the reported amounts of assets and liabilities,

income and expenses. The estimates and associated assumptions are based on historical experience and various

other factors that are believed to be reasonable under the circumstances, the results of which form the basis of

making the judgements about carrying values of assets and liabilities. Actual results may differ from these

estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting

estimates are recognised in the period in which the estimate is revised if the revision affects only that period or in

the period of the revision and future periods if the revision affects both current and future periods.

The principal balances that have been estimated relate to: -

- estimates as to the recoverability of goodwill. The Group is required to review, on an annual basis, whether

goodwill has suffered any impairment. The recoverable amount is determined based on value in use

calculations. The use of this method requires the estimation of future cash flows and the choice of a discount

rate in order to calculate present value - actual outcomes may vary. The carrying amount of goodwill at the

balance sheet date was £nil after impairment losses of £938,927 identified during the year.

- estimates relating to provisions required for uncollectable debtor balances (see note 12).

Basis of Consolidation

Where the company has the power, either directly or indirectly, to govern the financial and operating policies of

another entity or business so as to obtain benefits from its activities, it is classified as a subsidiary. The

consolidated financial statements present the results of the company and its subsidiaries (“the Group”) as if they

formed a single entity. Inter-company transactions are therefore eliminated in full.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring the accounting policies

used in line with those used by the Group.

Business Combinations The consolidated financial statements incorporate the results of business combinations using the purchase method.

In the consolidated statement of financial position, the acquiree’s identifiable assets, liabilities and contingent

liabilities are initially recognised at their fair values at the acquisition date. The results of acquired operations are

included in the consolidated income statement from the date on which control is obtained.

Goodwill represents the excess of the cost of a business combination over the interest in the fair value of

identifiable assets, liabilities and contingent liabilities acquired. Cost comprises the fair values of assets given,

liabilities assumed and equity instruments issued.

Goodwill Goodwill arising on acquisition of subsidiaries or business is recognised as a separate asset on the statement of

financial position after the recognition at fair value of any other intangible assets identified at the time of

acquisition.

Goodwill is capitalised as an intangible asset. Where the fair value of identifiable assets, liabilities and contingent

liabilities exceeds the fair value of consideration paid, the excess is credited in full to the Group income statement

on the acquisition date. The Group carries out annual impairment tests for goodwill. Impairment losses in respect

of goodwill are recognised immediately in the income statement and are not reversed.

ClearDebt Group Limited NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 30 June 2015

25

2. Significant Accounting Policies (continued)

Impairment

At each reporting date, the Group reviews the carrying amounts of its intangibles and property, plant and

equipment to determine whether there is any indication that those assets have suffered an impairment loss. If any

such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the

impairment loss (if any). Where the asset does not generate cash flows that are independent of other assets, the

Group estimates the recoverable amount of the cash-generating unit to which the asset belongs.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the

estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current

market assessments of the time value of money and the risks specific to the asset for which the estimates of future

cash flows have been adjusted.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the

carrying amount of the asset (cash-generating unit) is reduced to its recoverable amount, in which case the

impairment loss is treated as expenses in the consolidated income statement.

Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit) is

increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not

exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset

(cash-generating unit) in prior years. A reversal of an impairment loss is recognised as income immediately.

Other Intangible Assets Internal and externally acquired intangible assets are initially recognised at cost and subsequently amortised over

their useful economic lives. The amortisation expense is shown separately on the face of the Consolidated Income

Statement. The significant intangibles recognised by the Group, their useful economic lives and the methods used

to determine the cost of intangibles acquired in a business combination are as follows: -

Software and other development costs - 4 years’ straight line

Intangible assets - Debt management back books - 12 months’ straight line

Intangible assets - Insolvency back books - 3-4 years’ straight line

Expenditure arising from the Group’s development costs and software development is recognised only if all of the

following conditions are met:

- an asset is created that can be identified;

- it is probable that the asset created will generate future economic benefits;

- the development cost of the asset can be measured reliably;

- the Group has the intention to complete the asset and the ability and intention to use or sell it;

- sufficient resources are available to complete the development and to either sell or use the asset.

Where the criteria have not been achieved, software development expenditure is recognised as an expense in the

period in which it is incurred.

Segmental Reporting Management determines its operating segments by identifying components:

a) that engage in business activities that earn revenues and incur expenses (including revenues and expenses

relating to transactions with other components of the Group),

b) whose operating results are regularly reviewed by the entity’s chief operating decision maker, the board of

directors of ClearDebt Group Limited, to make decisions about resources to be allocated to the segment, and

c) for which discrete financial information is available.

ClearDebt Group Limited NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 30 June 2015

26

2. Significant Accounting Policies (continued)

Revenue

Revenue is recognised at the fair value of amounts receivable or received in relation to a range of services provided

to customers as follows:

Individual Voluntary Arrangements (IVA’s)

Fees are earned for arranging and administering IVA’s on behalf of individuals experiencing debt problems.

Generally, revenue is accrued based upon the stage of completion of specific customer contracts where the

outcome can be assessed with reasonable certainty and the value for that service has been agreed between the

Group and the customer.

Nominee fees

Nominee fees are recognised upon the approval of an IVA proposal at a creditors meeting.

Supervisory fees

Supervisory fees are accrued on a monthly basis over the duration of the arrangement as the service is provided.

Protected Trust Deeds (PTD’s)

Fees earned in respect of PTD’s are recognised when received.

Debt Management Services

Fees are receivable for the management of debts on behalf of customers experiencing financial difficulties. Fees

are recognised upon receipt of customer payments on the basis that these arrangements are informal and there is

no certainty that economic benefits will accrue until a payment is received.

Commissions and Payment Protection Mis-selling Claims Income

The Group also receives commission income from the referral of loans and other products as well as fees in respect

of non IVA claims for mis-sold payment protection products. Commissions are recorded as they are received.

Royalty Income

Revenue from royalty income is accrued in accordance with contractual agreements in place. Revenue is calculated

as a proportion of the revenue invoiced by that third party.

Prepayment Card Services

The Group receives a revenue share from the issue and usage charges in respect of the ClearCash prepaid

MasterCard. Income and charges are recognised in the period in which they were incurred by the card user.

Property, Plant and Equipment All property, plant and equipment are initially recorded at cost. Depreciation is provided at rates calculated to

write off the cost less residual value of each asset over its expected useful life, as follows:

Leasehold improvements - 25% straight line

Fixtures and fittings - 25% straight line

Residual value and estimated remaining lives are reviewed annually.

Provisions

Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of a past event

where it is probable that it will result in an outflow of economic benefits that can be reliably estimated. If the

effect of time value of money is material, provisions are determined by discounting the expected future cash flows

at a pre-tax rate that reflects current market assessments of the time value of money.

ClearDebt Group Limited NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 30 June 2015

27

2. Significant Accounting Policies (continued)

Share-based Compensation

Equity-settled share-based payments are measured at the fair value of services received in exchange for the grant

of options or warrants. The fair value determined is recognised as an expense if it relates to trading activities or

in the share premium account if it relates to the issue of equity instruments. The total amount to be expensed over

the vesting period is determined by reference to the fair value of the options or warrants granted, excluding the

impact of any non-market vesting conditions (for example, profitability and growth targets). Non-market vesting

conditions are included in the assumptions about the number of options or warrants that are expected to become

exercisable.

At each reporting date, the Group revises its estimates of the number of options or warrants that are expected to

become exercisable. It recognises the impact of the revision of original estimates, if any, in the income statement,

and a corresponding adjustment to reserves over the remaining vesting period.

The proceeds received net of any attributed transaction costs are credited to share capital (nominal value) and

share premium when the options or warrants are exercised. Non vesting conditions which are not satisfied during

the vesting period are treated as cancellations and any remaining expense is accelerated in the period of failure.

Fair value is measured by use of the Black-Scholes model. The expected life used in the model has been adjusted,

based on management’s best estimate, for the effect of non-transferability, exercise restrictions and behavioural

considerations.

Leasing Rentals payable under operating leases are charged to income on a straight-line basis over the term of the relevant

lease.

Financial Instruments Financial assets and financial liabilities are recognised in the statement of financial position when the Group has

become a party to the contractual provisions of the instrument.

Trade and other receivables

Trade receivables are classified as loans and other receivables in accordance with IAS 39, measured on initial

recognition at fair value, and are subsequently measured at amortised cost using the effective interest rate method.

Appropriate allowances for estimated irrecoverable amounts are recognised in the consolidated income statement

when there is objective evidence that the asset is impaired. The allowance recognised is measured as the difference

between the asset’s carrying amount and the present value of estimated future cash flows discounted at the

effective interest rate computed at initial recognition.

Cash and cash equivalents

Cash and cash equivalents comprise cash at bank and in hand, deposits held at call with banks and other short-

term highly liquid investments with original maturities of three months or less and are classified as other loans

and receivables in accordance with IAS 39.

For the purposes of the Statement of Cash Flows, cash and cash equivalents consist of amounts as defined above.

Financial liabilities

Financial liabilities are classified according to the substance of the contractual arrangements entered into. An

instrument will be classified as a financial liability when there is a contractual obligation to deliver cash or another

financial asset to another enterprise.

Trade and other payables

Trade payables are initially recognised at fair value and subsequently at amortised cost using the effective interest

method. They are classified as “Other liabilities” in accordance with IAS 39.

ClearDebt Group Limited NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 30 June 2015

28

2. Significant Accounting Policies (continued)

Borrowings

Interest-bearing bank loans and overdrafts are classified as “other liabilities” in accordance with IAS 39. They

are initially recorded at their fair value, net of any transaction costs associated with borrowings. Borrowings are

subsequently stated at amortised cost.

Finance charges, including premiums payable on settlement or redemption, are expensed to the income statement

over the term of the instrument using an effective rate of interest and are added to the carrying amount of the

instrument to the extent that they are not settled in the period in which they arise. Borrowings are classified as

current liabilities unless the Group has an unconditional right to defer settlement of the liability for at least 12

months after the reporting date.

Taxation

The tax expense represents the sum of the current tax expense and deferred tax expense. Taxable profits differ

from net profit as reported in the Statement of Comprehensive Income because it excludes items of income or

expense that are taxable or deductible in other years and it further excludes items that are not taxable or deductible.

The Group’s liability for current tax is calculated by using tax rates that have been enacted or substantively enacted

by the reporting date.

Deferred tax is the tax expected to be payable or recoverable on differences between the carrying amount of assets