clio, michigan annual financial statements and … of contents section page 1 members ofthe board of...

TRANSCRIPT

Clio Area Schools

Clio, Michigan

Annual Financial Statementsand

Independent Auditors’ Report

June 30, 2014

Table of Contents

Section Page

1 Members of the Board of Education and Administration 1 - 1

2 Independent Auditors’ Report 2 - 1

3 Management’s Discussion and Analysis 3 - 1

4 Basic Financial Statements

District-wide Financial StatementsStatement of Net Position 4 - 1Statement of Activities 4 - 3

Fund Financial StatementsGovernmental Funds

Balance Sheet 4 - 4Reconciliation of the Balance Sheet of

Governmental Funds to the Statement of Net Position 4 - 6Statement of Revenues, Expenditures and Changes in Fund Balances 4 - 7Reconciliation of the Statement of Revenues, Expenditures and

Changes in Fund Balances of Governmental Funds to the Statement of Activities 4 - 8

Fiduciary FundsStatement of Assets and Liabilities 4 - 9

Notes to Financial Statements 4 - 10

5 Required Supplementary Information

Budgetary Comparison Schedule – General Fund 5 - 1

Section Page

6 Other Supplementary Information

Nonmajor Governmental FundsCombining Balance Sheet 6 - 1Combining Statement of Revenues, Expenditures and Changes in Fund Balance 6 - 3

Clio Area SchoolsMembers of the Board of Education and Administration

June 30, 2014

1 - 1

Members of the Board of Education

Mary Ann Dipzinski President

Eric Wood Vice President

Steve Nordstrom Secretary

Robert Gaffney Treasurer

Jeff Drayton Trustee

Henry Hatter Trustee

Tim Ranville Trustee

Administration

Fletcher Spears III Superintendent

Stephen Keskes Executive Director of Curriculumand Instruction

Jon Pechette Executive Director of Finance

Colleen Mansour Executive Director of Personnel

4468 Oak Bridge DriveFlint, MI 48532

Phone (810) 732-3000 / (800) 899-4742Fax (810) 732-6118

2 - 1

Independent Auditors’ Report

To the Board of EducationClio Area SchoolsClio, Michigan

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregateremaining fund information of Clio Area Schools, as of and for the year ended June 30, 2014, and the related notes to the financialstatements, which collectively comprise the School District’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accountingprinciples generally accepted in the United States of America; this includes the design, implementation, and maintenance of internalcontrol relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether dueto fraud or error.

Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordancewith auditing standards generally accepted in the United States of America and the standards applicable to financial audits containedin Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we planand perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. Theprocedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of thefinancial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevantto the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate inthe circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly,we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and thereasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of thefinancial statements.

2 - 2

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of thegovernmental activities, each major fund, and the aggregate remaining fund information of Clio Area Schools, as of June 30, 2014,and the respective changes in financial position for the year then ended in accordance with accounting principles generally acceptedin the United States of America.

Other Matters:

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis andbudgetary comparison information, as identified in the table of contents, be presented to supplement the basic financial statements.Such information, although not a part of the basic financial statements, is required by the Governmental Accounting StandardsBoard, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriateoperational, economic, or historical context. We have applied certain limited procedures to the required supplementary information inaccordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of managementabout the methods of preparing the information and comparing the information for consistency with management’s responses to ourinquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We donot express an opinion or provide any assurance on the information, because the limited procedures do not provide us with sufficientevidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise Clio Area Schools’basic financial statements. The list of the Members of the Board of Education and Administration and other supplementaryinformation, as identified in the table of contents, are presented for purposes of additional analysis and are not a required part of thebasic financial statements.

The other supplementary information, as identified in the table of contents, is the responsibility of management and was derived fromand relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such informationhas been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additionalprocedures, including comparing and reconciling such information directly to the underlying accounting and other records used toprepare the basic financial statements or to the basic financial statements themselves, and other additional procedures inaccordance with auditing standards generally accepted in the United States of America. In our opinion the other supplementaryinformation, as identified in the table of contents, is fairly stated, in all material respects, in relation to the basic financial statementsas a whole.

2 - 3

The list of the Members of the Board of Education and Administration has not been subjected to the auditing procedures applied inthe audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on it.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated November 6, 2014, on our considerationof Clio Area Schools’ internal control over financial reporting and on our tests of its compliance with certain provisions of laws,regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing ofinternal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internalcontrol over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with GovernmentAuditing Standards in considering Clio Area Schools’ internal control over financial reporting and compliance.

Flint, MichiganNovember 6, 2014

MANAGEMENT’S DISCUSSION AND ANALYSIS

Clio Area SchoolsWe Are Family

Fletcher Spears IIISuperintendent

Stephen KeskesExecutive Director of Curriculum and Instruction

3 - 1 Colleen MansourExecutive Director of Personnel

Jon Pechette, CPAExecutive Director of Finance

Management’s Discussion and AnalysisFor the Year Ended June 30, 2014

The Clio Area School District has chosen to implement the provisions of Governmental Accounting Standards Board Statement No. 34, BasicFinancial Statements – and Management’s Discussion and Analysis – for State and Local Governments,(GASB 34) with the enclosed financialstatements. Our discussion and analysis of Clio Area Schools’ financial performance, a GASB 34 requirement, provides an overview of theSchool District’s financial activities for the fiscal year ended June 30, 2014.

GASB 34 and generally accepted accounting principles (GAAP) require the reporting of two types of financial statements: fund financialstatements and district-wide financial statements.

Fund Financial Statements

The fund financial statements provide more detailed information about the School District’s funds, focusing on its most significant or “major”funds – not the School District as a whole. The fund-level financial statements are reported on a modified accrual basis. That is, only thoseassets that are “measurable” and “currently available” are reported, and liabilities are recognized to the extent that they are normally expectedto be paid with current financial resources. The School District has two kinds of funds:

Governmental Funds: All of the School District’s basic services are provided in governmental funds, which generally focus on (1) how cashand other financial assets that can be readily converted to cash flow in and out and (2) the balances left at year-end that are available forspending. Consequently, the governmental fund financial statements provide a detailed short-term view that helps to determine whetherthere are more or fewer financial resources that can be spent in the near future to finance the School District’s programs. Because thisinformation does not encompass the additional long-term focus of the district-wide statements, reconciliations from the fund levelstatements to the district-wide statements explain the relationship (or differences) between them. The School District’s governmental fundsinclude the General Fund, Cafeteria Special Revenue Fund, and Capital Projects Fund.

3 - 2

§ Agency Funds: The School District is the custodian for assets that belong to others in the student activities agency fund. The SchoolDistrict is responsible for ensuring that the assets reported in these funds are used only for their intended purposes and by those to whomthe assets belong. The School District excludes these activities from the district-wide financial statements because it cannot use theseassets to finance its operations.

District-wide Financial Statements

The District-wide Statement of Net Position and Statement of Activities are reported using the full accrual basis of accounting. With thismethod, all of the School District’s assets, deferred outflows of resources, liabilities, deferred inflows of resources, and current year revenuesand expenditures are reported, regardless of when cash is received or paid. These statements provide information about the activities of theSchool District as a whole, and present a long-term view of the School District’s finances. For example, the Statement of Activities details howthe School District’s services were financed in the short-term and the amount that remains for future spending. The Statement of Net Positionaggregates the School District’s restricted and unrestricted assets as well as short and long-term obligations recorded in all funds.

Financial Position and Results of Operations

The School District’s net position – the difference between assets plus deferred inflows and liabilities plus deferred outflows, as reported in theStatement of Net Position, is one way to measure the School District’s financial health, or financial position. Over time, increases or decreasesin the School District’s net position, as reported in the Statement of Activities, is one indicator of whether its financial health is improving ordeteriorating, respectively. The relationship between revenues and expenses indicates the School District’s operating results. To assess theSchool District’s overall health, it is important to consider additional non-financial factors such as the quality of educational services provided,the condition of school buildings and facilities, the safety of the schools, and other non-financial factors.

3 - 3

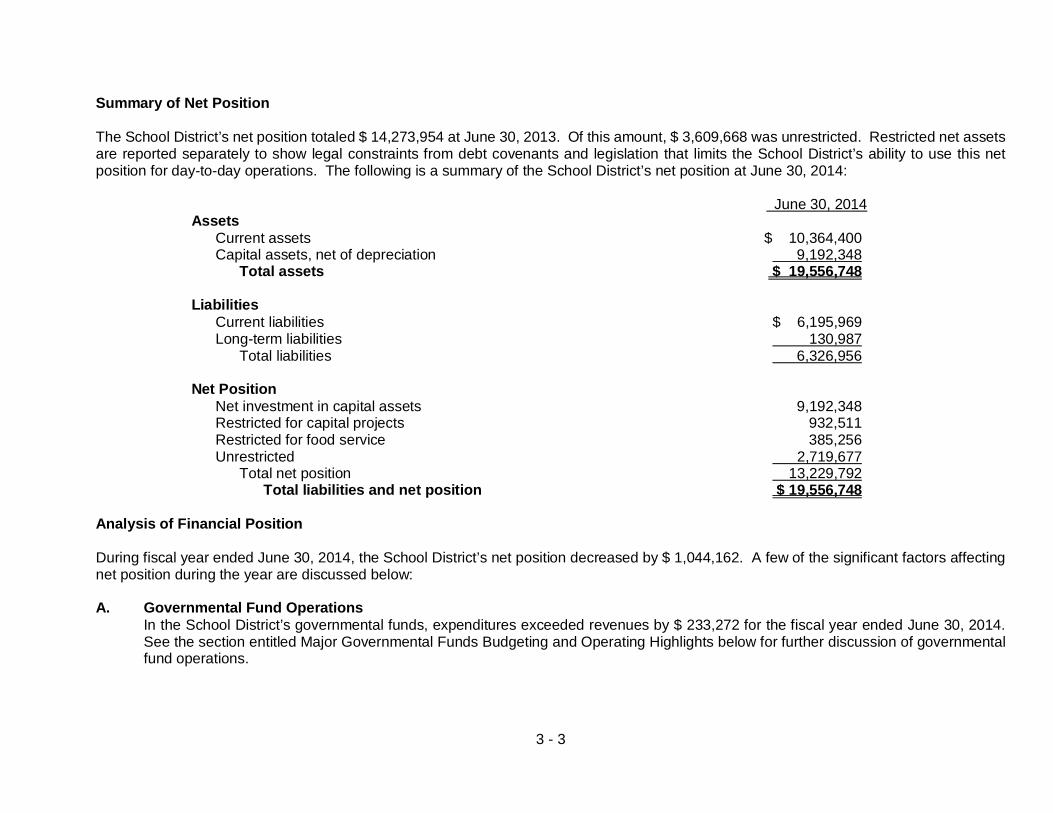

Summary of Net Position

The School District’s net position totaled $ 14,273,954 at June 30, 2013. Of this amount, $ 3,609,668 was unrestricted. Restricted net assetsare reported separately to show legal constraints from debt covenants and legislation that limits the School District’s ability to use this netposition for day-to-day operations. The following is a summary of the School District’s net position at June 30, 2014:

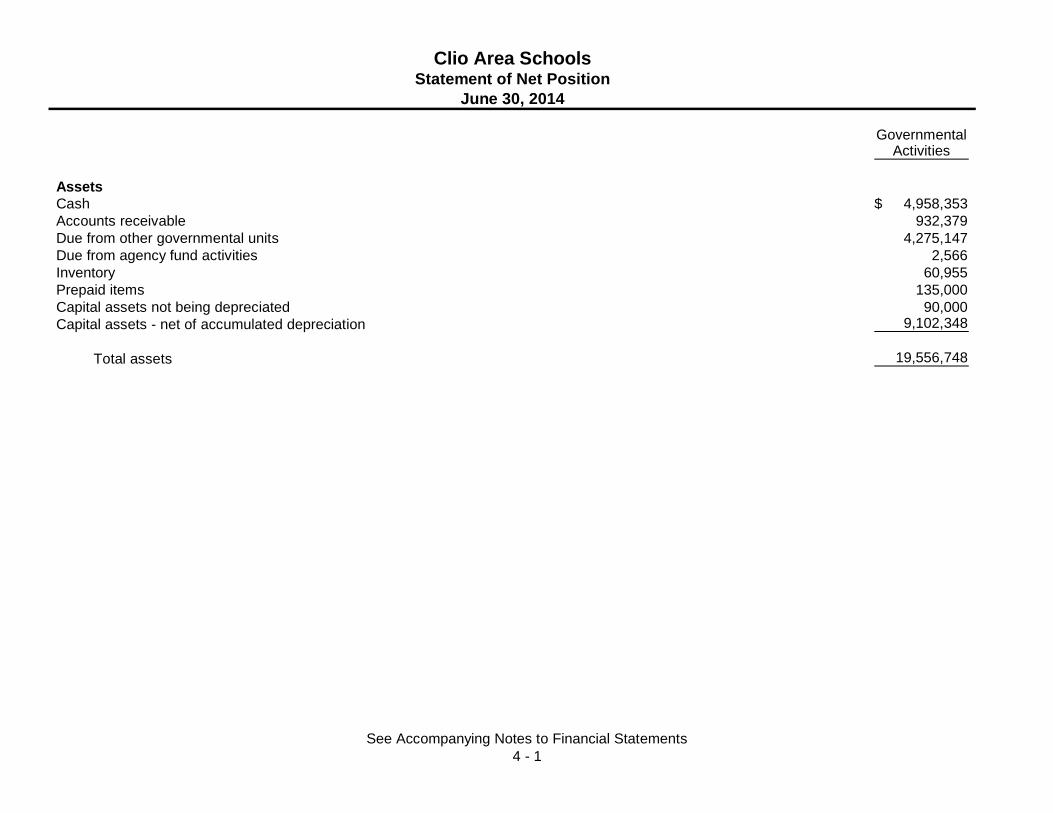

June 30, 2014Assets Current assets $ 10,364,400 Capital assets, net of depreciation 9,192,348 Total assets $ 19,556,748

Liabilities Current liabilities $ 6,195,969 Long-term liabilities 130,987 Total liabilities 6,326,956

Net Position Net investment in capital assets 9,192,348 Restricted for capital projects 932,511 Restricted for food service 385,256 Unrestricted 2,719,677 Total net position 13,229,792

Total liabilities and net position $ 19,556,748

Analysis of Financial Position

During fiscal year ended June 30, 2014, the School District’s net position decreased by $ 1,044,162. A few of the significant factors affectingnet position during the year are discussed below:

A. Governmental Fund OperationsIn the School District’s governmental funds, expenditures exceeded revenues by $ 233,272 for the fiscal year ended June 30, 2014.See the section entitled Major Governmental Funds Budgeting and Operating Highlights below for further discussion of governmentalfund operations.

3 - 4

B. Depreciation ExpenseThe provisions of GASB 34 require the School District to maintain a record of annual depreciation expense and accumulateddepreciation. The net increase in accumulated depreciation is a reduction in net position. Depreciation expense is recorded using astraight-line method over the estimated useful lives of the assets. In accordance with generally accepted accounting principles,depreciation expense is recorded based on the original cost of the asset less an estimated salvage value. For the year endedJune 30, 2014, the depreciation expense was $ 895,475.

C. Capital AcquisitionsAdditions to capital outlay for the year ended June 30, 2014, totaled $ 6,871. Capital outlay was offset by current year depreciationexpense of $ 895,475, creating a net position decrease from capital outlays of $ 888,604.

D. Claims and JudgmentsBenefit claims of $ 583,000 are shown on the district-wide statements that were not expended on the fund statements as they werenot due and payable in the current period.

3 - 5

Results of Operations

The results of this year’s operations for the School District as a whole are reported in the Statement of Activities. A summary of the district-wide results of operations for the year ended June 30, 2014 is a follows:

Revenue General revenue: Property taxes, levied for general purposes $ 2,357,845 Property taxes, levied for capital projects 855,105 State of Michigan aid, unrestricted 20,770,498 Interest and investment earnings 220 Other general revenue 230,473 Total general revenue 24,214,141

Program revenue: Charges for services 1,254,232 Operating grants and contributions 5,040,718

Total revenue 30,509,091

Expenses Instruction 18,657,809 Supporting services 11,267,836 Food services 1,241,414 Community service 386,194

Total expenses 31,553,253

Change in net position (1,044,162)

Net position – July 1, 2013 14,273,954

Net position – June 30, 2014 $ 13,229,792

3 - 6

Governmental Funds Financial Highlights

The General Fund is reported separately as a major fund in the fund financial statements. Funds reported as “Nonmajor Governmental Funds”in the fund financial statements include the Cafeteria Fund and Capital Project Fund. The annual fund financial statements provide thefollowing insights about the results of this year’s operations:

A. General FundThe General Fund experienced a decrease in fund equity of $ 967,705, or 25.3%, during the year ended June 30, 2014. Ending fundequity in the General Fund was $ 2,850,664 on June 30, 2014, which equates to 9.6% of expenditures for the year. This level wasdown from $ 3,818,369 on June 30, 2013.

B. Nonmajor Governmental FundsNonmajor governmental funds experienced an increase in fund equity of $ 734,433 during the year. The Cafeteria Special RevenueFund balance increased from the prior year. Revenues exceeded expenditures by $ 67,153, resulting in ending fund equity of $385,256,or 31.7% of expenditures for the year. Capital Projects funds experienced an increase in fund equity of $ 667,280, resulting in endingfund equity of $ 932,511.

Major Governmental Funds Budgeting and Operating Highlights

The School District’s budgets are prepared according to Michigan law and are initially adopted prior to July 1 of each year, based on facts andassumptions known at the time of the initial budget preparation. It is expected that there will be changes between the initial budget andsubsequent budgets, as many factors are not known at the time of adoption of the initial budget. Some of these factors include enrollmentfigures and resultant staffing requirements, staffing changes that take place during the year, state school aid adjustments, grant allocations,and other unforeseen items. As a matter of practice, the School District amends its budget three times during the fiscal year to adjust for thesechanges. The School District prepares budgets for the General Fund, Cafeteria Special Revenue Fund, and Capital Projects Fund.

A. General FundIn the General Fund, actual revenue was $ 28.85 million. This is below the original budget estimate of $ 29.33 million and above thefinal budgeted amount of $ 28.77 million, a variance of $74,792 or .3%. The actual expenditures of the General Fund were $ 29.81million. This is above the original budget estimate of $ 29.31 million and below the final budgeted amount of $ 29.90 million, a varianceof $ 86,600, or 0.3%.

3 - 7

The variances between the actual revenues and the original and final amended budgets in the General Fund are due primarily to thefollowing:

§ Decreased revenue from fees and services.§ Decrease in expected revenue from local property taxes.§ Decrease in revenue from state grant sources.§ Increase in revenue from federal sources.§ Increase in revenue from inter district sources.

The variances between the actual General Fund expenditures and the original and final expenditure budgets include the following:

§ Employee salary and benefit adjustments.§ Adjustments for federal and state grant expenditures.§ Decreased fuel expenses.§ Lower than expected utilities costs.§ Timing differences related to major maintenance projects.

The General fund expenditures exceeded revenues by $ 967,705 for the year ended June 30, 2014, which resulted in a 25.3% decreasein fund equity. The ending fund equity in the General Fund was $ 2,850,664 at June 30, 2014, which equates to 9.6% of expendituresfor the year. This level was down from $ 3,818,369 June 30, 2013.

B. Capital Projects FundsThe Capital Projects Funds receive revenues from property taxes and investment income. Expenditures take the form of capitalimprovement projects for major repairs and improvements to the School District’s facilities. The School District’s Capital Projects Fundsis comprised of the Sinking Fund that was passed in 2001 and reauthorized May 4, 2010.

During the year, the Capital Projects funds realized $914,601 in revenues and $ 247,321 in expenditures, resulting in a net increase infund equity of $ 667,280, for total fund equity of $ 932,511.

3 - 8

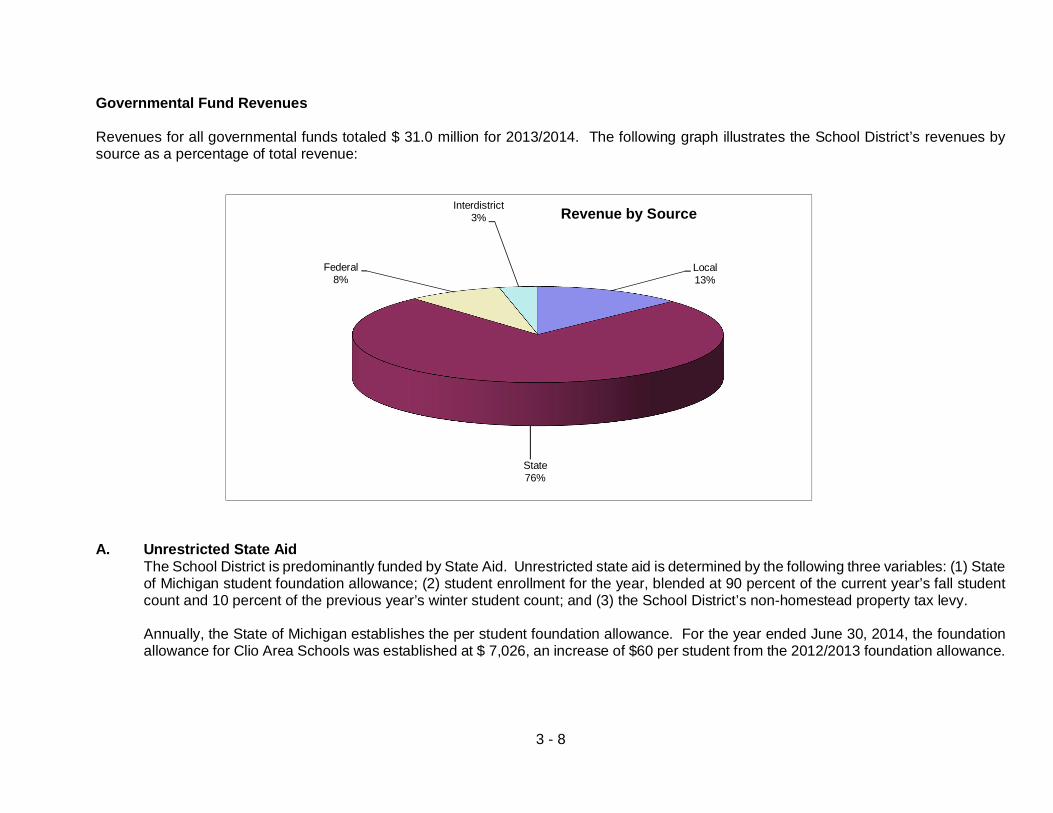

Governmental Fund Revenues

Revenues for all governmental funds totaled $ 31.0 million for 2013/2014. The following graph illustrates the School District’s revenues bysource as a percentage of total revenue:

A. Unrestricted State AidThe School District is predominantly funded by State Aid. Unrestricted state aid is determined by the following three variables: (1) Stateof Michigan student foundation allowance; (2) student enrollment for the year, blended at 90 percent of the current year’s fall studentcount and 10 percent of the previous year’s winter student count; and (3) the School District’s non-homestead property tax levy.

Annually, the State of Michigan establishes the per student foundation allowance. For the year ended June 30, 2014, the foundationallowance for Clio Area Schools was established at $ 7,026, an increase of $60 per student from the 2012/2013 foundation allowance.

Local13%

State76%

Federal8%

Interdistrict3% Revenue by Source

3 - 9

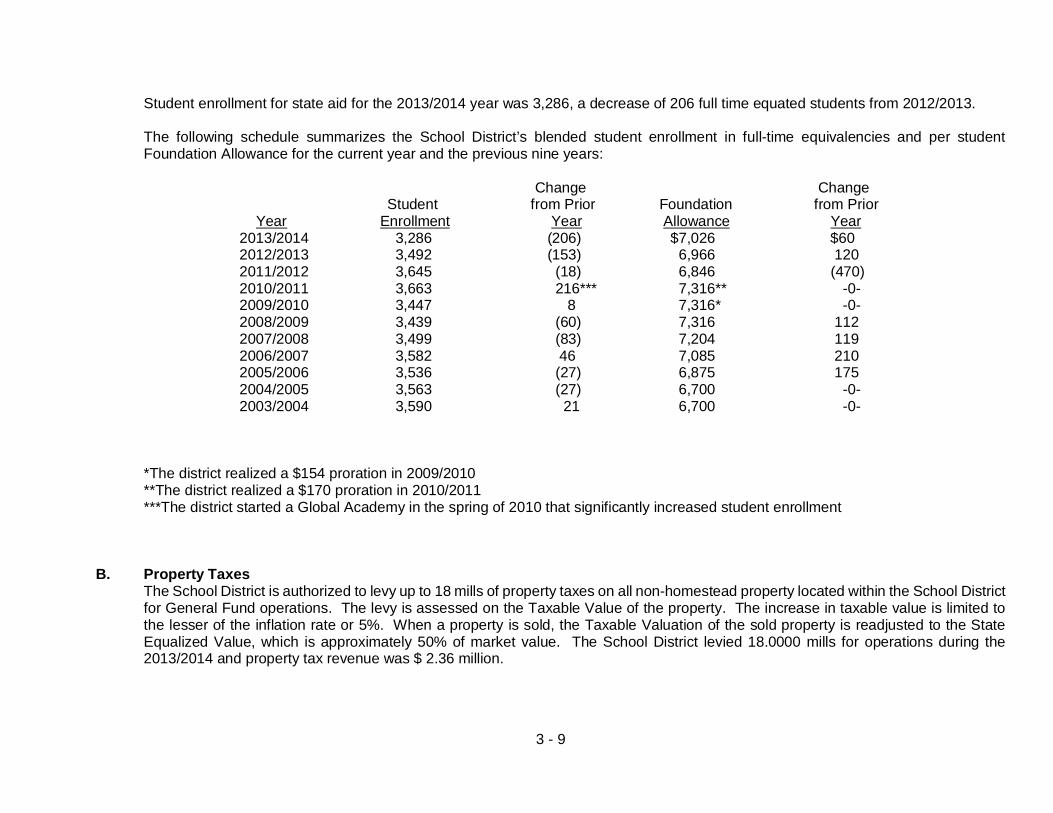

Student enrollment for state aid for the 2013/2014 year was 3,286, a decrease of 206 full time equated students from 2012/2013.

The following schedule summarizes the School District’s blended student enrollment in full-time equivalencies and per studentFoundation Allowance for the current year and the previous nine years:

Change Change Student from Prior Foundation from Prior

Year Enrollment Year Allowance Year2013/2014 3,286 (206) $7,026 $602012/2013 3,492 (153) 6,966 1202011/2012 3,645 (18) 6,846 (470)2010/2011 3,663 216*** 7,316** -0-2009/2010 3,447 8 7,316* -0-2008/2009 3,439 (60) 7,316 1122007/2008 3,499 (83) 7,204 1192006/2007 3,582 46 7,085 2102005/2006 3,536 (27) 6,875 1752004/2005 3,563 (27) 6,700 -0-2003/2004 3,590 21 6,700 -0-

*The district realized a $154 proration in 2009/2010**The district realized a $170 proration in 2010/2011***The district started a Global Academy in the spring of 2010 that significantly increased student enrollment

B. Property TaxesThe School District is authorized to levy up to 18 mills of property taxes on all non-homestead property located within the School Districtfor General Fund operations. The levy is assessed on the Taxable Value of the property. The increase in taxable value is limited tothe lesser of the inflation rate or 5%. When a property is sold, the Taxable Valuation of the sold property is readjusted to the StateEqualized Value, which is approximately 50% of market value. The School District levied 18.0000 mills for operations during the2013/2014 and property tax revenue was $ 2.36 million.

3 - 10

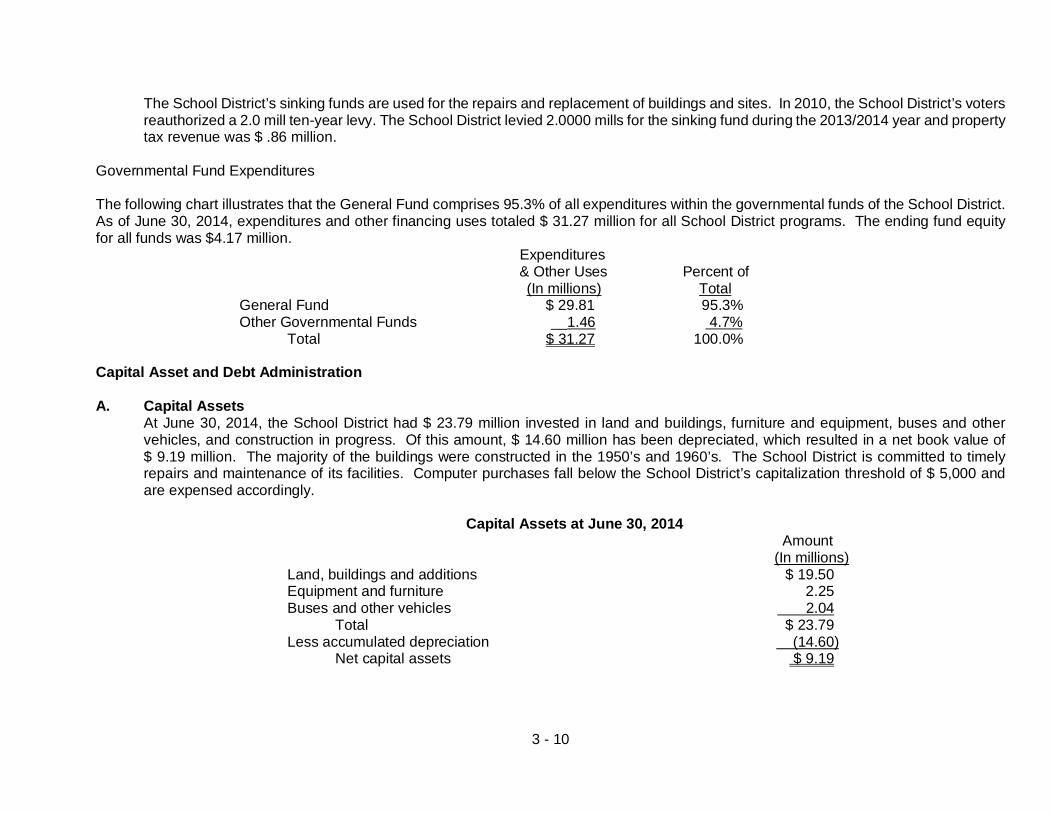

The School District’s sinking funds are used for the repairs and replacement of buildings and sites. In 2010, the School District’s votersreauthorized a 2.0 mill ten-year levy. The School District levied 2.0000 mills for the sinking fund during the 2013/2014 year and propertytax revenue was $ .86 million.

Governmental Fund Expenditures

The following chart illustrates that the General Fund comprises 95.3% of all expenditures within the governmental funds of the School District.As of June 30, 2014, expenditures and other financing uses totaled $ 31.27 million for all School District programs. The ending fund equityfor all funds was $4.17 million.

Expenditures & Other Uses Percent of

(In millions) TotalGeneral Fund $ 29.81 95.3%Other Governmental Funds __1.46 4.7%

Total $ 31.27 100.0%

Capital Asset and Debt Administration

A. Capital AssetsAt June 30, 2014, the School District had $ 23.79 million invested in land and buildings, furniture and equipment, buses and othervehicles, and construction in progress. Of this amount, $ 14.60 million has been depreciated, which resulted in a net book value of$ 9.19 million. The majority of the buildings were constructed in the 1950’s and 1960’s. The School District is committed to timelyrepairs and maintenance of its facilities. Computer purchases fall below the School District’s capitalization threshold of $ 5,000 andare expensed accordingly.

Capital Assets at June 30, 2014 Amount (In millions)

Land, buildings and additions $ 19.50Equipment and furniture 2.25Buses and other vehicles 2.04

Total $ 23.79Less accumulated depreciation (14.60)

Net capital assets $ 9.19

3 - 11

B. Long-Term DebtAt June 30, 2014, the School District had no outstanding bonded debt.

For more detailed information regarding capital assets and debt administration, please review the Notes to Financial Statements located in thefinancial section of this report.

Conditions that will Significantly Affect Financial Position and Results of Operations in Future Years

On May 4, 2010, the voters of the School District reauthorized a 2.0 mills sinking fund millage for a period of ten years. The total revenue tobe generated will be approximately $ 9.2 million dollars, down from an initial projection of $10.2 million dollars. The reduction in anticipatedrevenue is a result of the loss of tax base due to depressed property values. The funds generated from this levy are necessary to keep facilitiesin good repair and to enable the district to use more general fund monies for operations. The district also passed a restoration of the 18.0 millnon-homestead millage rate in the spring of 2007 which permits the district to collect the full levied millage. District voters will be asked torenew that millage rate during next year. The State of Michigan continues to experience high unemployment which has had a negative impacton student enrollment in Genesee County. Increases in retirement rates, per pupil funding proration’s, reductions in per pupil funding, andincreases in health care, fuel and utility rates will also have an impact on the district’s financial stability.

Contacting the District’s Financial Management

This financial report is designed to provide our citizens and taxpayers with a general overview of the School District’s finances. If you havequestions about this report or need additional information, contact Jon Pechette, CPA, Executive Director of Finance, Clio Area Schools, 430N. Mill Street, Clio, Michigan, 48420 or by telephone at 810-591-0500.

BASIC FINANCIAL STATEMENTS

GovernmentalActivities

AssetsCash 4,958,353$Accounts receivable 932,379Due from other governmental units 4,275,147Due from agency fund activities 2,566Inventory 60,955Prepaid items 135,000Capital assets not being depreciated 90,000Capital assets - net of accumulated depreciation 9,102,348

Total assets 19,556,748

Clio Area SchoolsStatement of Net Position

June 30, 2014

See Accompanying Notes to Financial Statements4 - 1

GovernmentalActivities

Clio Area SchoolsStatement of Net Position

June 30, 2014

LiabilitiesAccounts payable 601,842$State aid anticipation note payable 3,000,000Due to other governmental units 260,071Accrued salaries payable 2,079,489Unearned revenue 254,567Noncurrent liabilities

Due in more than one year 130,987

Total liabilities 6,326,956

Net PositionNet investment in capital assets 9,192,348Restricted for:

Food service 385,256Capital projects 932,511

Unrestricted 2,719,677

Total net position 13,229,792$

See Accompanying Notes to Financial Statements4 - 2

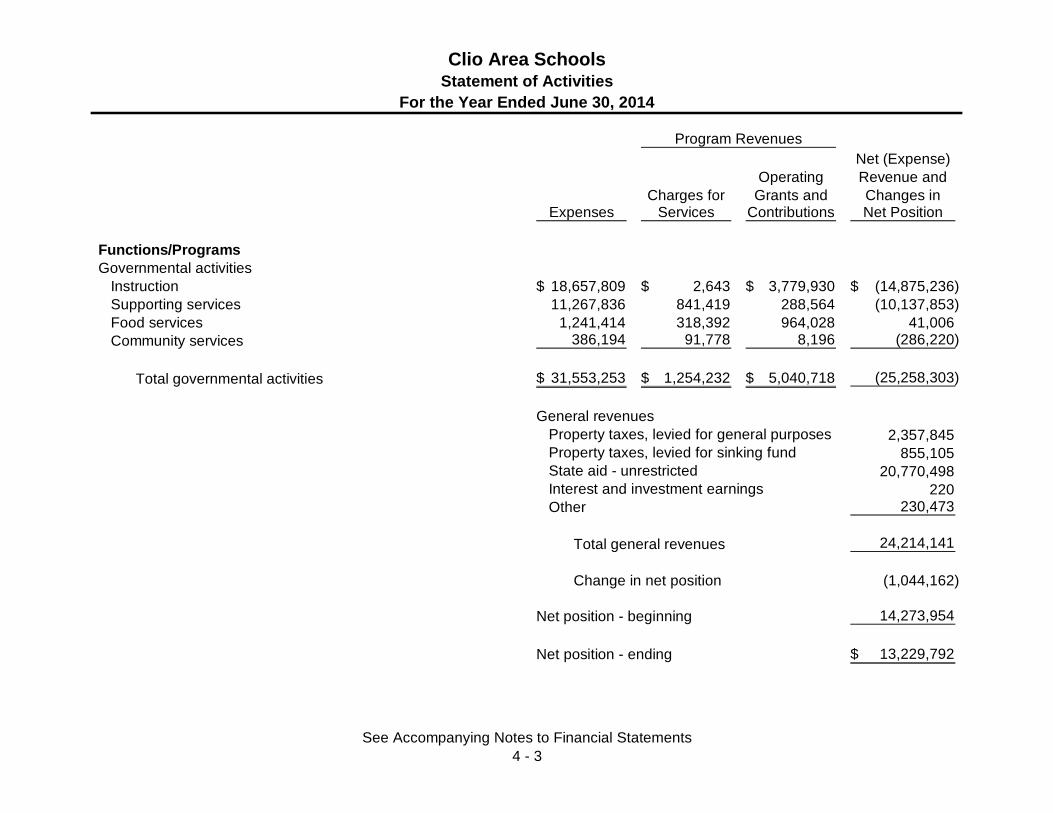

Net (Expense)Operating Revenue and

Charges for Grants and Changes inExpenses Services Contributions Net Position

Functions/ProgramsGovernmental activities

Instruction 18,657,809$ 2,643$ 3,779,930$ (14,875,236)$Supporting services 11,267,836 841,419 288,564 (10,137,853)Food services 1,241,414 318,392 964,028 41,006Community services 386,194 91,778 8,196 (286,220)

Total governmental activities 31,553,253$ 1,254,232$ 5,040,718$ (25,258,303)

2,357,845855,105

20,770,498220

230,473

Total general revenues 24,214,141

Change in net position (1,044,162)

14,273,954

13,229,792$

General revenuesProperty taxes, levied for general purposes

Program Revenues

Clio Area SchoolsStatement of Activities

For the Year Ended June 30, 2014

Property taxes, levied for sinking fund

Net position - beginning

Net position - ending

State aid - unrestrictedInterest and investment earningsOther

See Accompanying Notes to Financial Statements4 - 3

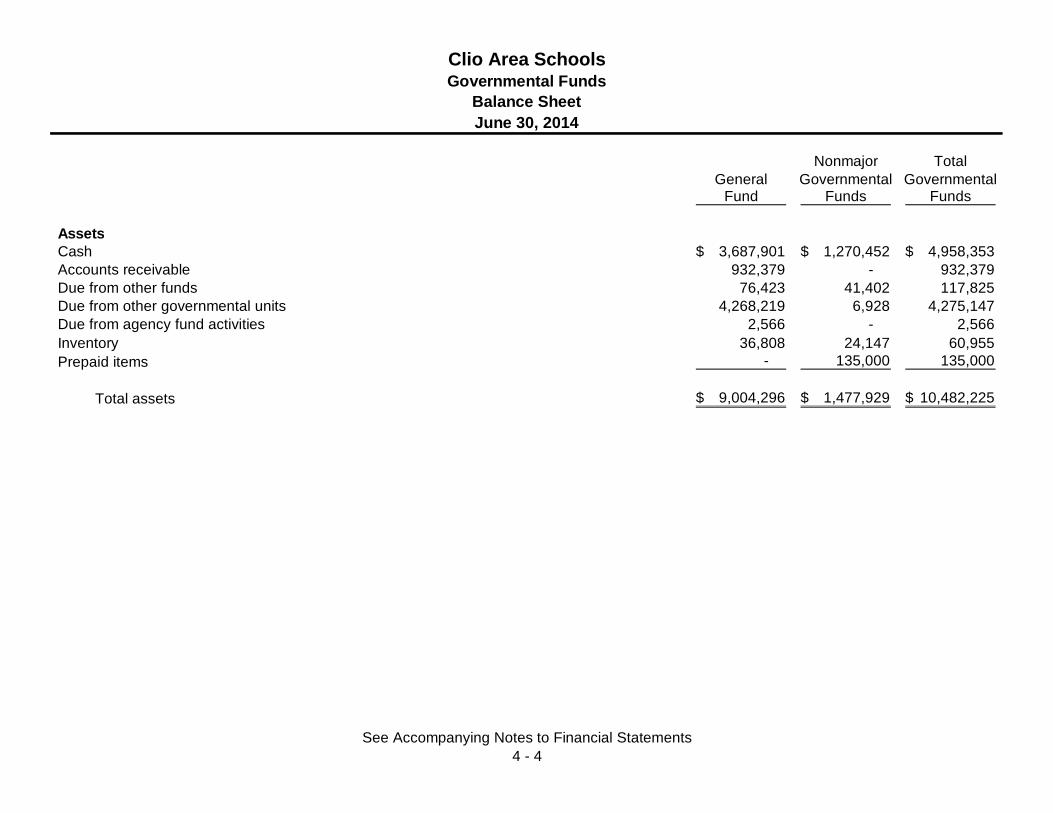

Nonmajor TotalGeneral Governmental Governmental

Fund Funds Funds

AssetsCash 3,687,901$ 1,270,452$ 4,958,353$Accounts receivable 932,379 - 932,379Due from other funds 76,423 41,402 117,825Due from other governmental units 4,268,219 6,928 4,275,147Due from agency fund activities 2,566 - 2,566Inventory 36,808 24,147 60,955Prepaid items - 135,000 135,000

Total assets 9,004,296$ 1,477,929$ 10,482,225$

Clio Area SchoolsGovernmental Funds

June 30, 2014Balance Sheet

See Accompanying Notes to Financial Statements4 - 4

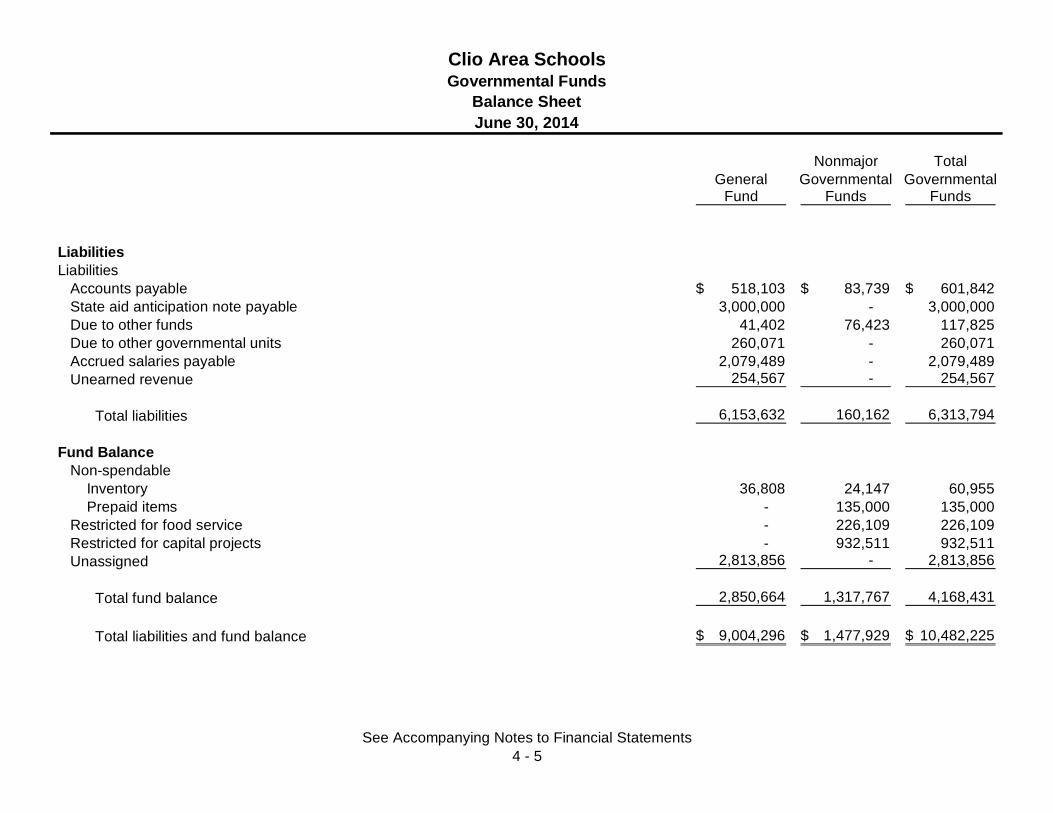

Nonmajor TotalGeneral Governmental Governmental

Fund Funds Funds

Clio Area SchoolsGovernmental Funds

June 30, 2014Balance Sheet

LiabilitiesLiabilities

Accounts payable 518,103$ 83,739$ 601,842$State aid anticipation note payable 3,000,000 - 3,000,000Due to other funds 41,402 76,423 117,825Due to other governmental units 260,071 - 260,071Accrued salaries payable 2,079,489 - 2,079,489Unearned revenue 254,567 - 254,567

Total liabilities 6,153,632 160,162 6,313,794

Fund Balance Non-spendable

Inventory 36,808 24,147 60,955 Prepaid items - 135,000 135,000Restricted for food service - 226,109 226,109Restricted for capital projects - 932,511 932,511Unassigned 2,813,856 - 2,813,856

Total fund balance 2,850,664 1,317,767 4,168,431

Total liabilities and fund balance 9,004,296$ 1,477,929$ 10,482,225$

See Accompanying Notes to Financial Statements4 - 5

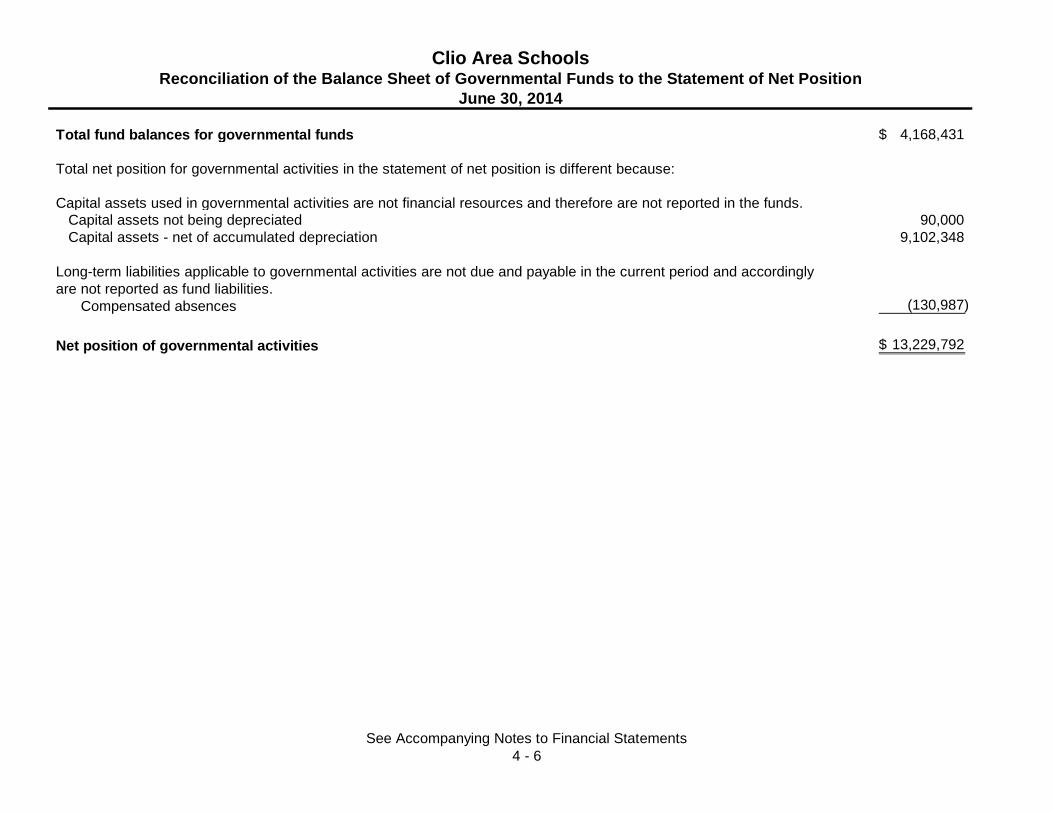

Total fund balances for governmental funds 4,168,431$

Total net position for governmental activities in the statement of net position is different because:

Capital assets used in governmental activities are not financial resources and therefore are not reported in the funds.Capital assets not being depreciated 90,000Capital assets - net of accumulated depreciation 9,102,348

Long-term liabilities applicable to governmental activities are not due and payable in the current period and accordinglyare not reported as fund liabilities.

Compensated absences (130,987)

Net position of governmental activities 13,229,792$

Clio Area SchoolsReconciliation of the Balance Sheet of Governmental Funds to the Statement of Net Position

June 30, 2014

See Accompanying Notes to Financial Statements4 - 6

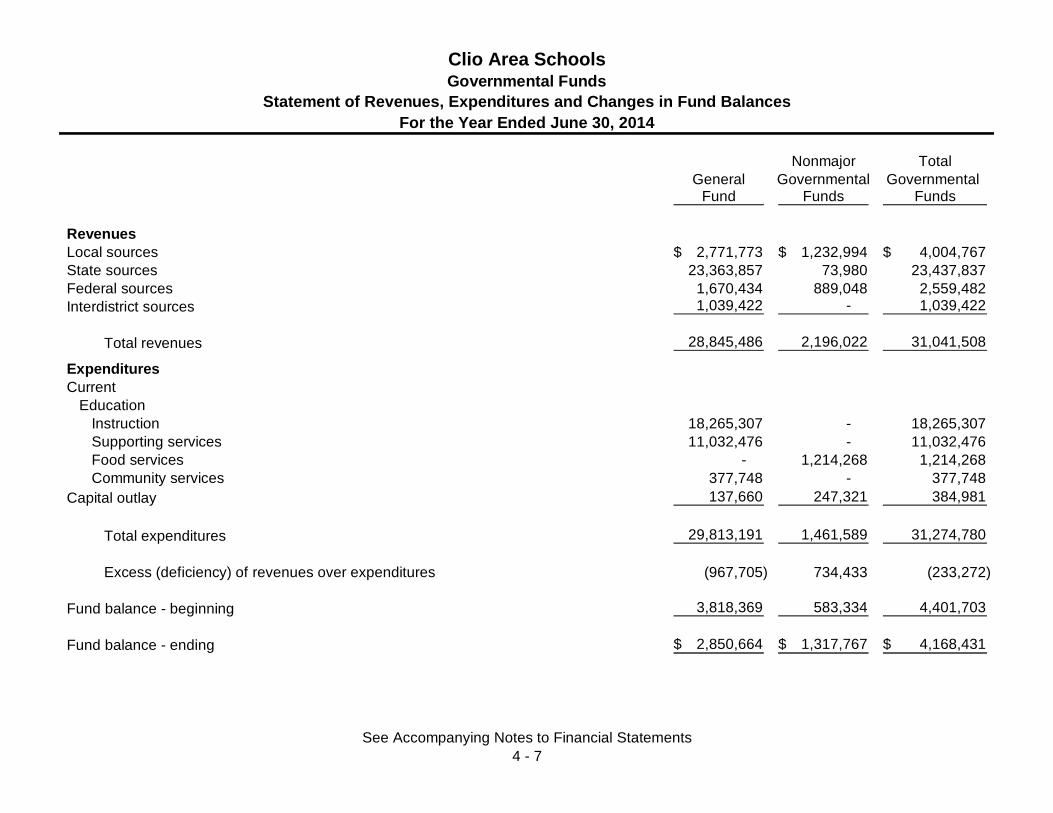

Nonmajor TotalGeneral Governmental Governmental

Fund Funds Funds

RevenuesLocal sources 2,771,773$ 1,232,994$ 4,004,767$State sources 23,363,857 73,980 23,437,837Federal sources 1,670,434 889,048 2,559,482Interdistrict sources 1,039,422 - 1,039,422

Total revenues 28,845,486 2,196,022 31,041,508

ExpendituresCurrent

EducationInstruction 18,265,307 - 18,265,307Supporting services 11,032,476 - 11,032,476Food services - 1,214,268 1,214,268Community services 377,748 - 377,748

Capital outlay 137,660 247,321 384,981

Total expenditures 29,813,191 1,461,589 31,274,780

Excess (deficiency) of revenues over expenditures (967,705) 734,433 (233,272)

Fund balance - beginning 3,818,369 583,334 4,401,703

Fund balance - ending 2,850,664$ 1,317,767$ 4,168,431$

Clio Area SchoolsGovernmental Funds

Statement of Revenues, Expenditures and Changes in Fund BalancesFor the Year Ended June 30, 2014

See Accompanying Notes to Financial Statements4 - 7

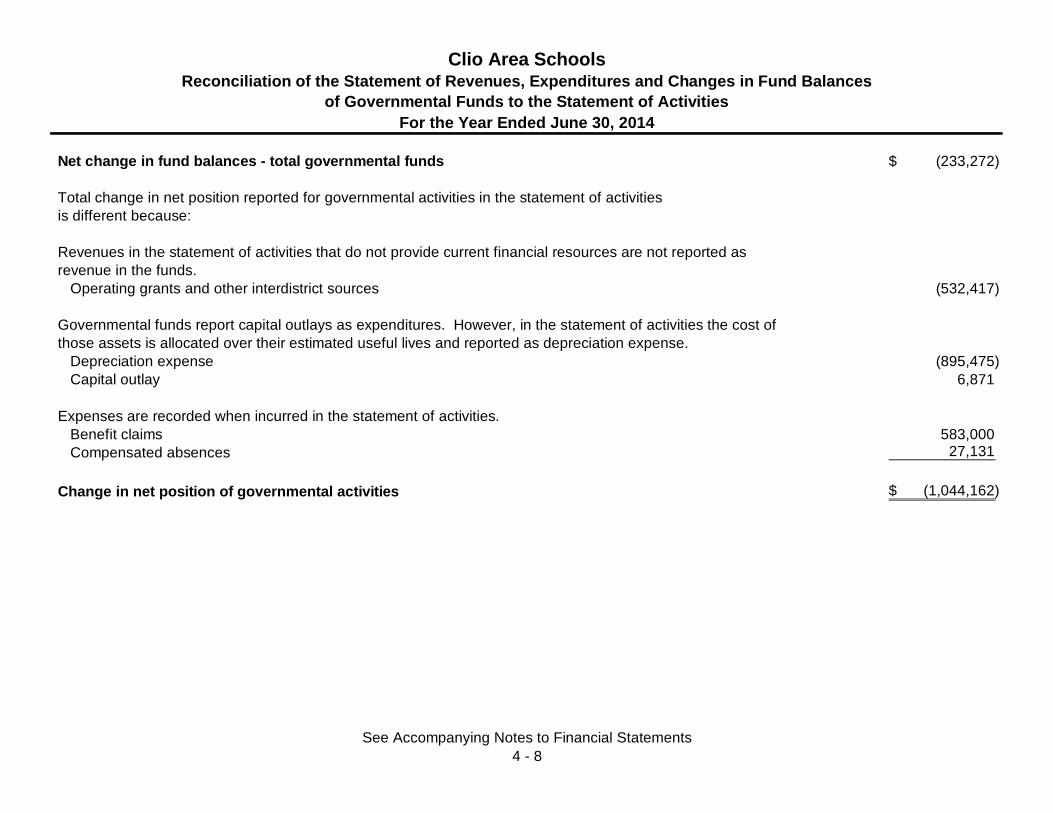

Net change in fund balances - total governmental funds (233,272)$

Total change in net position reported for governmental activities in the statement of activitiesis different because:

Revenues in the statement of activities that do not provide current financial resources are not reported asrevenue in the funds.

Operating grants and other interdistrict sources (532,417)

Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost ofthose assets is allocated over their estimated useful lives and reported as depreciation expense.

Depreciation expense (895,475)Capital outlay 6,871

Expenses are recorded when incurred in the statement of activities.Benefit claims 583,000Compensated absences 27,131

Change in net position of governmental activities (1,044,162)$

For the Year Ended June 30, 2014

Clio Area SchoolsReconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances

of Governmental Funds to the Statement of Activities

See Accompanying Notes to Financial Statements4 - 8

AgencyFund

AssetsCash 319,173$

LiabilitiesDue to other funds 2,566Due to student activities 316,607

Total liabilities 319,173$

Clio Area SchoolsFiduciary Funds

Statement of Assets and LiabilitiesJune 30, 2014

See Accompanying Notes to Financial Statements4 - 9

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 10

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accounting policies of Clio Area Schools (School District)conform to accounting principles generally accepted in the UnitedStates of America as applicable to governmental units. The followingis a summary of the School District’s significant accounting policies:

Reporting Entity

The School District is governed by an elected seven-member Boardof Education. The accompanying financial statements have beenprepared in accordance with criteria established by the GovernmentalAccounting Standards Board for determining the variousgovernmental organizations to be included in the reporting entity.These criteria include significant operational financial relationshipsthat determine which of the governmental organizations are a part ofthe School District’s reporting entity, and which organizations arelegally separate component units of the School District. The SchoolDistrict has no component units.

District-wide Financial Statements

The School District’s basic financial statements include bothdistrict-wide (reporting for the district as a whole) and fund financialstatements (reporting the School District’s major funds). Thedistrict-wide financial statements categorize all nonfiduciary activitiesas either governmental or business type. All of the School District’sactivities are classified as governmental activities.

The statement of net position presents governmental activities on aconsolidated basis, using the economic resources measurementfocus and accrual basis of accounting. This method recognizes alllong-term assets and receivables as well as long-term debt andobligations. The School District’s net position is reported in threeparts (1) net investment in capital assets, (2) restricted net position,and (3) unrestricted net position.

The statement of activities reports both the gross and net cost ofeach of the School District’s functions. The functions are alsosupported by general government revenues (property taxes andcertain intergovernmental revenues). The statement of activitiesreduces gross expenses (including depreciation) by related programrevenues, operating and capital grants. Program revenues must bedirectly associated with the function. Operating grants includeoperating-specific and discretionary (either operating or capital)grants.

The net costs (by function) are normally covered by general revenue(property taxes, state sources and federal sources, interest income,etc.). The School District does not allocate indirect costs. In creatingthe district-wide financial statements the School District haseliminated interfund transactions.

The district-wide focus is on the sustainability of the School Districtas an entity and the change in the School District’s net positionresulting from current year activities.

Fund Financial Statements

Separate financial statements are provided for governmental fundsand fiduciary funds, even though the latter are excluded from thedistrict-wide financial statements. Major individual governmentalfunds are reported as separate columns in the fund financialstatements.

Governmental fund financial statements are reported using thecurrent financial resources measurement focus and the modifiedaccrual basis of accounting. Revenue is recognized as soon as it isboth measurable and available. Revenue is considered to beavailable if it is collected within the current period or soon enoughthereafter to pay liabilities of the current period. For this purpose, theSchool District considers revenues to be available if they arecollected within 60 days of the end of the current fiscal period.

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 11

Expenditures generally are recorded when a liability is incurred, asunder accrual accounting. However, debt service expenditures, aswell as expenditures related to compensated absences and claimsand judgments, are recorded only when payment is due.

Property taxes, unrestricted state aid, intergovernmental grants, andinterest associated with the current fiscal period are all considered tobe susceptible to accrual and so have been recognized as revenue ofthe current fiscal period. All other revenue items are considered tobe available only when cash is received by the government.

Fiduciary fund statements also are reported using the economicresources measurement focus and the accrual basis of accounting.

The School District reports the following major governmental funds:

General Fund – The General Fund is used to record the generaloperations of the School District pertaining to education andthose operations not required to be provided for in other funds.

Additionally, the School District reports the following fund types:

Special Revenue Funds – Special Revenue Funds are used toaccount for the proceeds of specific revenue sources that arerestricted to expenditures for specified purposes. The SchoolDistrict’s Special Revenue Fund includes the Food Service Fund.Operating deficits generated by these activities are generallycovered by a transfer from the General Fund.

Capital Projects Fund – The Sinking Fund is used to record thesinking fund property tax levy and other revenue and thedisbursement of invoices specifically for acquiring new schoolsites, construction, additions or major replacements to schoolbuildings.

Fiduciary Funds – Fiduciary Funds are used to account for assetsheld by the School District in a trustee capacity or as an agent.The Agency Fund is custodial in nature (assets equal liabilities)and does not involve the measurement of results of operations.This fund is used to record the transactions of student groups forschool and school-related purposes.

Assets, Liabilities, and Equity

Receivables and Payables – Generally, outstanding amounts owedbetween funds are classified as “due from/to other funds”. Theseamounts are caused by transferring revenues and expenses betweenfunds to get them into the proper reporting fund. These balances arepaid back as cash flow permits.

All trade and property tax receivables are shown net of an allowancefor uncollectible amounts. The School District considers all accountsreceivable to be fully collectible; accordingly, no allowance foruncollectible amounts is recorded.

Property taxes collected are based upon the approved tax rate for theyear of levy. For the fiscal year ended June 30, 2014, the rates areas follows per $1,000 of assessed value.

General FundNon principal residence exemption 18.00000Commercial personal property 6.00000

Sinking Fund 2.00000

School property taxes are assessed and collected in accordance withenabling state legislation by cities and townships within the SchoolDistrict’s boundaries. Approximately 99% of the School District’s taxroll lies within Genesee County.

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 12

The property tax levy runs from July 1 to June 30. Property taxesbecome a lien on the first day of the levy year and are due on orbefore September 14 or February 14. Collections are forwarded tothe School District as collected by the assessing municipalities. Realproperty taxes uncollected as of March 1 are purchased by theCounties of Genesee and Saginaw and remitted to the School Districtby June 30.

Inventories and Prepaid Items – Inventories are valued at cost, on afirst-in, first-out basis. Inventories of governmental funds arerecorded as expenditures when consumed rather than whenpurchased. Certain payments to vendors reflect costs applicable tofuture fiscal years. For such payments in governmental funds theSchool District follows the consumption method, and they thereforeare capitalized as prepaid items in both district-wide and fundfinancial statements.

Capital Assets – Purchased or constructed capital assets arereported at cost or estimated historical cost. Donated capital assetsare recorded at their estimated fair market value at the date ofdonation. The School District defines capital assets as assets withan initial individual cost in excess of $ 5,000. Costs of normal repairand maintenance that do not add to the value or materially extendasset lives are not capitalized. The School District does not haveinfrastructure assets. Buildings, equipment, and vehicles aredepreciated using the straight-line method over the following usefullives:

Buildings and additions 5-50 yearsEquipment and furniture 3-20 yearsBuses and other vehicles 5-10 years

Compensated Absences – Sick days are earned by employees atvarying rates, which may accumulate from year to year, and are asfollows:

Teachers and Bus Drivers, 10 days per year; Administrators,Secretaries, and Custodians, 12 days per year.

There are some variations from group to group; normally employeeswho work only when school is in session receive 10 days per yearand employees who work the entire year receive 12 days per year.

Use of Estimates – The preparation of financial statements inconformity with accounting principles generally accepted in theUnited States of America requires management to make estimatesand assumptions that affect the reported amounts of assets andliabilities and disclosure of contingent assets and liabilities, as well asdeferred inflows and deferred outflows at the date of the financialstatements and the report amounts of revenue and expendituresduring the reporting period. Actual results could differ from thoseestimates.

Fund Equity – In the fund financial statements, governmental fundsreport fund balance in the following categories:

Non-spendable - amounts that are not available in aspendable form.

Restricted – amounts that are legally imposed or otherwiserequired by external parties to be used for a specific purpose.

Committed – amounts that have been formally set aside bythe Board of Education for specific purposes. A fund balancecommitment may be established, modified, or rescinded by aresolution of the Board of Education.

Assigned – amounts intended to be used for specificpurposes, as determined by the Board of Education. TheBoard of Education has the authority to assign funds.Residual amounts in governmental funds other than thegeneral fund are automatically assigned by their nature.

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 13

Unassigned – all other resources; the remaining fundbalances after non-spendable, restrictions, commitments andassignments.

When an expenditure is incurred for purposes for which bothrestricted and unrestricted fund balance is available, the District’spolicy is to consider restricted funds spent first.

When an expenditure is incurred for purposes for which committed,assigned, or unassigned amounts could be used, the District’s policyis to consider the funds to be spent in the following order:(1) committed, (2) assigned, (3) unassigned.

Eliminations and Reclassifications

In the process of aggregating data for the statement of net positionand the statement of activities, some amounts reported as interfundactivity and balances in the funds were eliminated or reclassified.Interfund receivables and payables were eliminated to minimize the“grossing up” effect on assets and liabilities within the governmentalactivities column.

Adoption of New Accounting Standards

Upcoming Accounting and Reporting Changes

The Government Accounting Standards Board (“The GASB”) hasissued Statements 68, Accounting and Financial Reporting forPensions, and Statement 71, Pension Transition for ContributionsMade Subsequent to the Measurement Date. Statement 68 requiresgovernments participating in public employee pension plans torecognize their portion of the long-term obligation for the pensionbenefits as a liability and to measure the annual costs of the pensionbenefits. The net pension liability will be recorded on the government-wide statements. Statement 71 amends Statement 68 to address anissue concerning transition provisions related to certain pension

contributions made to defined benefit pension plans prior toimplementation of Statement 68 by employers and non-employercontributing entities. The District is evaluating the impact thesestandards will have on its financial reporting. Statements 68 and 71are effective for the year ending June 30, 2015.

The GASB has also issued Statement 69, Government Combinationsand Disposals of Government Operations. Statement 69 providesdetailed requirements for the accounting and disclosure of varioustypes of government combinations, such as mergers, acquisitions,and transfers of operations. The guidance available previously waslimited to nongovernmental entities, and therefore did not providepractical examples for situations common in government-specificcombinations and disposals. The accounting and disclosurerequirements for these events vary based on whether a significantpayment is made, the continuation of termination of services, and thelegal structure of the new or continuing entity. Statement 69 iseffective for the year ending June 30, 2015.

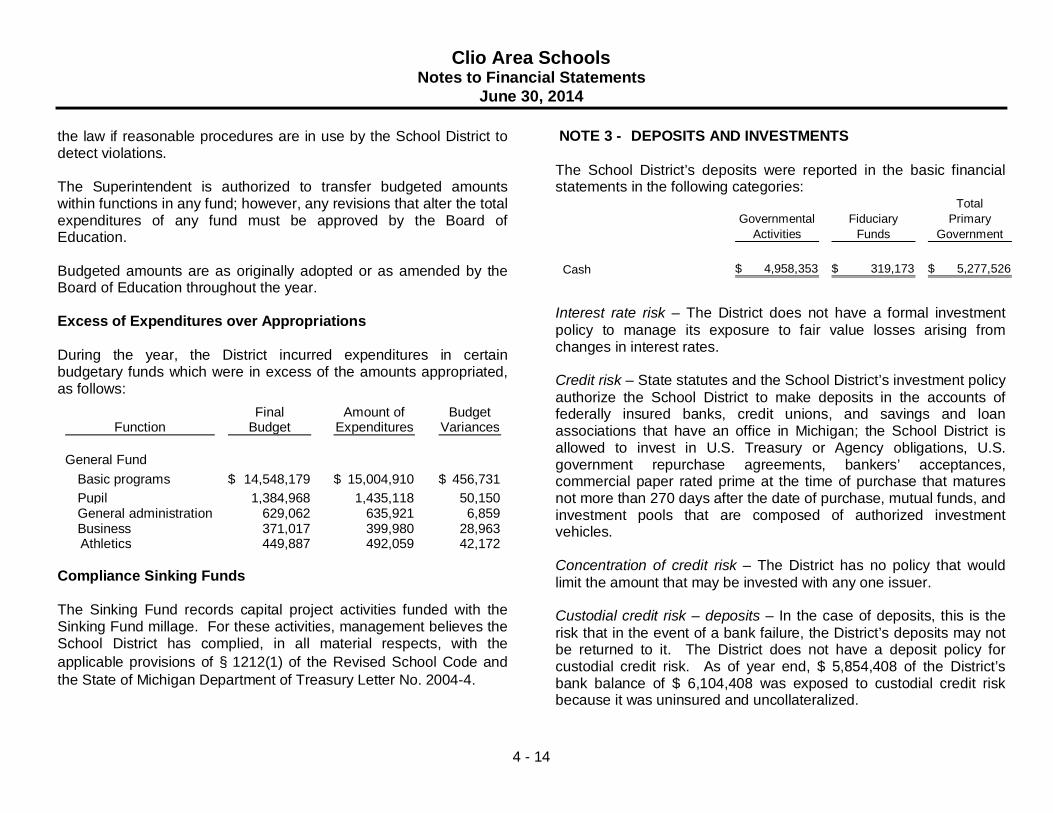

NOTE 2 - STEWARDSHIP, COMPLIANCE, ANDACCOUNTABILITY

Budgetary Information

Annual budgets are adopted on a basis consistent with accountingprinciples generally accepted in the United States of America andstate law for the General and Special Revenue Funds. All annualappropriations lapse at fiscal year end, thereby canceling allencumbrances. These appropriations are reestablished at thebeginning of the year.

The budget document presents information by fund and function.The legal level of budgetary control adopted by the governing body isthe function level. State law requires the School District to have itsbudget in place by July 1. A district is not considered in violation of

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 14

the law if reasonable procedures are in use by the School District todetect violations.

The Superintendent is authorized to transfer budgeted amountswithin functions in any fund; however, any revisions that alter the totalexpenditures of any fund must be approved by the Board ofEducation.

Budgeted amounts are as originally adopted or as amended by theBoard of Education throughout the year.

Excess of Expenditures over Appropriations

During the year, the District incurred expenditures in certainbudgetary funds which were in excess of the amounts appropriated,as follows:

Final Amount of BudgetFunction Budget Expenditures Variances

General FundBasic programs 14,548,179$ 15,004,910$ 456,731$Pupil 1,384,968 1,435,118 50,150General administration 629,062 635,921 6,859Business 371,017 399,980 28,963

Athletics 449,887 492,059 42,172

Compliance Sinking Funds

The Sinking Fund records capital project activities funded with theSinking Fund millage. For these activities, management believes theSchool District has complied, in all material respects, with theapplicable provisions of § 1212(1) of the Revised School Code andthe State of Michigan Department of Treasury Letter No. 2004-4.

NOTE 3 - DEPOSITS AND INVESTMENTS

The School District’s deposits were reported in the basic financialstatements in the following categories:

TotalGovernmental Fiduciary Primary

Activities Funds Government

Cash 4,958,353$ 319,173$ 5,277,526$

Interest rate risk – The District does not have a formal investmentpolicy to manage its exposure to fair value losses arising fromchanges in interest rates.

Credit risk – State statutes and the School District’s investment policyauthorize the School District to make deposits in the accounts offederally insured banks, credit unions, and savings and loanassociations that have an office in Michigan; the School District isallowed to invest in U.S. Treasury or Agency obligations, U.S.government repurchase agreements, bankers’ acceptances,commercial paper rated prime at the time of purchase that maturesnot more than 270 days after the date of purchase, mutual funds, andinvestment pools that are composed of authorized investmentvehicles.

Concentration of credit risk – The District has no policy that wouldlimit the amount that may be invested with any one issuer.

Custodial credit risk – deposits – In the case of deposits, this is therisk that in the event of a bank failure, the District’s deposits may notbe returned to it. The District does not have a deposit policy forcustodial credit risk. As of year end, $ 5,854,408 of the District’sbank balance of $ 6,104,408 was exposed to custodial credit riskbecause it was uninsured and uncollateralized.

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 15

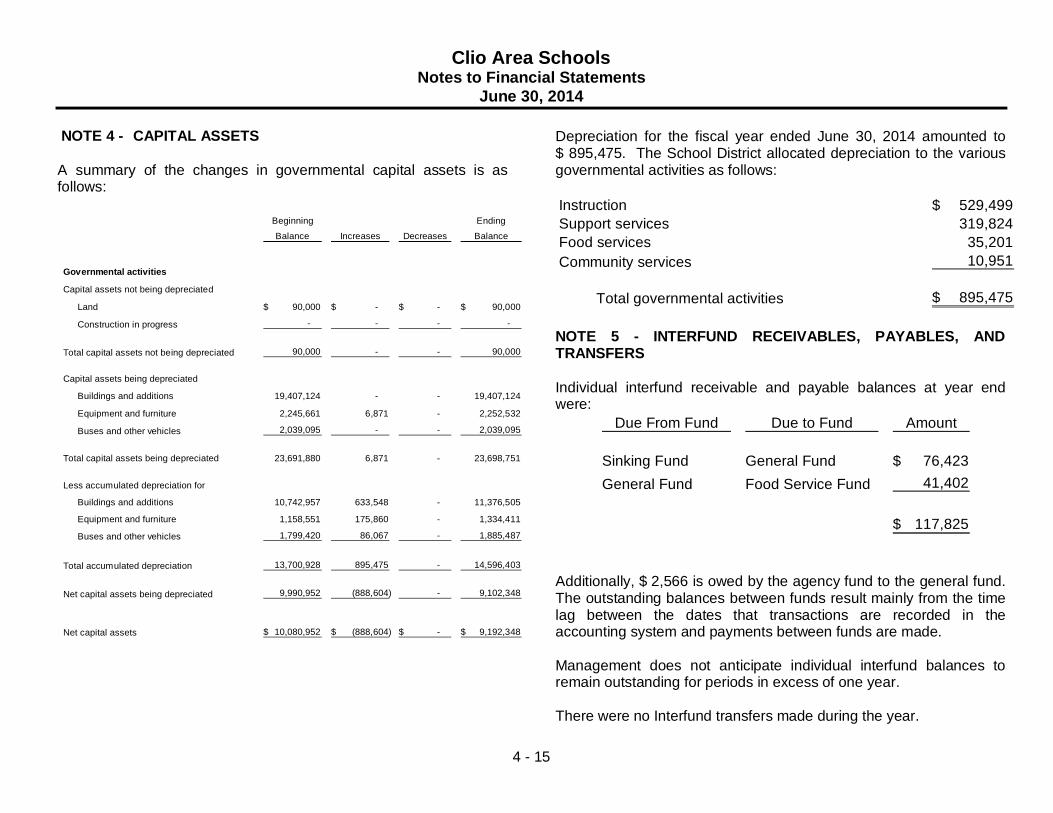

NOTE 4 - CAPITAL ASSETS

A summary of the changes in governmental capital assets is asfollows:

Beginning Ending

Balance Increases Decreases Balance

Governmental activities

Capital assets not being depreciated

Land 90,000$ -$ -$ 90,000$

Construction in progress - - - -

Total capital assets not being depreciated 90,000 - - 90,000

Capital assets being depreciated

Buildings and additions 19,407,124 - - 19,407,124

Equipment and furniture 2,245,661 6,871 - 2,252,532

Buses and other vehicles 2,039,095 - - 2,039,095

Total capital assets being depreciated 23,691,880 6,871 - 23,698,751

Less accumulated depreciation for

Buildings and additions 10,742,957 633,548 - 11,376,505

Equipment and furniture 1,158,551 175,860 - 1,334,411

Buses and other vehicles 1,799,420 86,067 - 1,885,487

Total accumulated depreciation 13,700,928 895,475 - 14,596,403

Net capital assets being depreciated 9,990,952 (888,604) - 9,102,348

Net capital assets 10,080,952$ (888,604)$ -$ 9,192,348$

Depreciation for the fiscal year ended June 30, 2014 amounted to$ 895,475. The School District allocated depreciation to the variousgovernmental activities as follows:

Instruction 529,499$Support services 319,824Food services 35,201Community services 10,951

Total governmental activities 895,475$

NOTE 5 - INTERFUND RECEIVABLES, PAYABLES, ANDTRANSFERS

Individual interfund receivable and payable balances at year endwere:

Due From Fund Due to Fund Amount

Sinking Fund General Fund 76,423$General Fund Food Service Fund 41,402

117,825$

Additionally, $ 2,566 is owed by the agency fund to the general fund.The outstanding balances between funds result mainly from the timelag between the dates that transactions are recorded in theaccounting system and payments between funds are made.

Management does not anticipate individual interfund balances toremain outstanding for periods in excess of one year.

There were no Interfund transfers made during the year.

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 16

NOTE 6 – UNEARNED REVENUE

Governmental funds report unearned revenue in connection withresources that have been received but not yet earned. At the end ofthe current fiscal year, the various components of unearned revenueare as follows:

Unearned

Monies payable to grantors due torecapture of funds 32,814$

Grant and categorical aid paymentsreceived prior to meetingall eligibility requirements 221,753

Total 254,567$

NOTE 7 - LONG-TERM DEBT

The School District issues bonds, notes, and other contractualcommitments to provide for the acquisition and construction of majorcapital facilities and the acquisition of certain equipment. Generalobligation bonds are direct obligations and pledge the full faith andcredit of the School District. Other long-term obligations includecompensated absences, claims and judgments, termination benefits,and certain risk liabilities.

Long-term obligation activity is summarized as follows:

Amount Due

Beginning Ending Within One

Balance Additions Reductions Balance Year

Accrued compensatedabsences

158,118$ -$ 27,131$ 130,987$ -$

For governmental activities, compensated absences are primarilyliquidated by the general fund.

Compensated Absences

Accrued compensated absences at year end, consists of accruedpersonal time benefits and accrued sick time benefits. The entirevested amount is considered long-term as the amount expendedeach year is expected to be offset by sick time earned for the year.

NOTE 8 – STATE AID ANTICIPATION NOTE

The School District issues state aid anticipation notes in advance ofstate aid collections, depositing the proceeds in the General Fund.These notes are necessary because the School District receivesstate aid from October through the following August for its fiscal yearending June 30th.

Short-term debt activity for the year was as follows:

Beginning EndingBalance Proceeds Repayments Balance

State aid anticipation note -$ 3,000,000$ -$ 3,000,000$

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 17

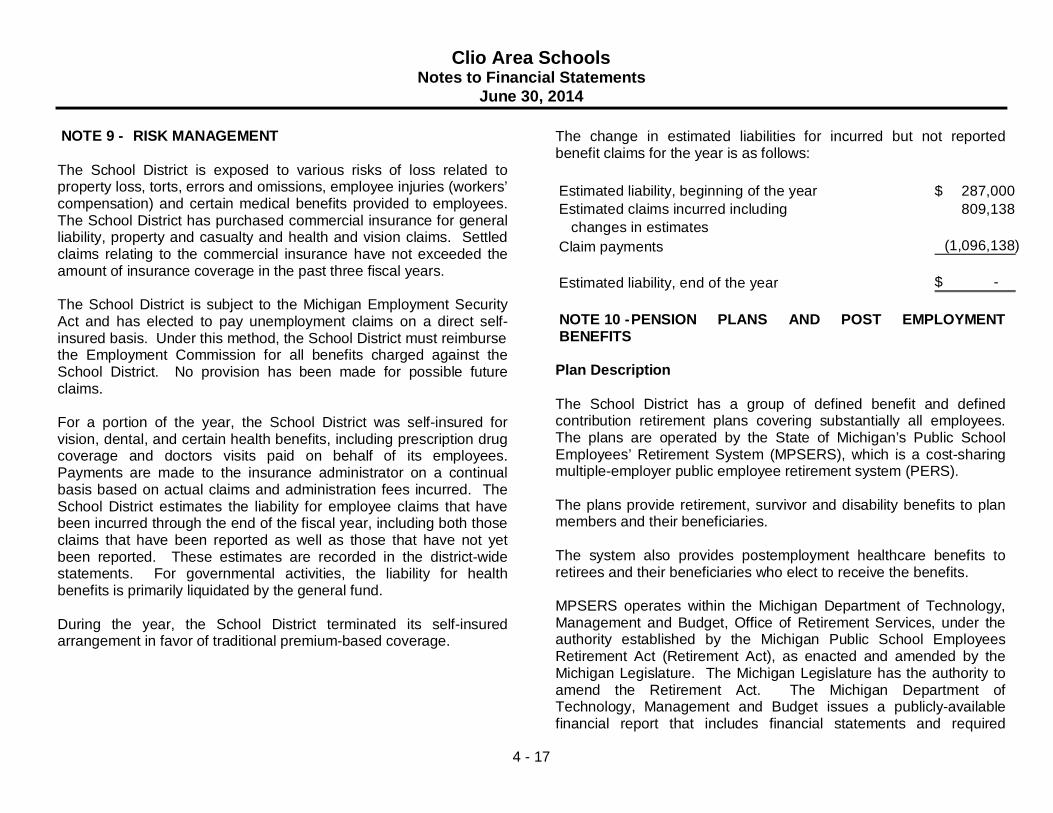

NOTE 9 - RISK MANAGEMENT

The School District is exposed to various risks of loss related toproperty loss, torts, errors and omissions, employee injuries (workers’compensation) and certain medical benefits provided to employees.The School District has purchased commercial insurance for generalliability, property and casualty and health and vision claims. Settledclaims relating to the commercial insurance have not exceeded theamount of insurance coverage in the past three fiscal years.

The School District is subject to the Michigan Employment SecurityAct and has elected to pay unemployment claims on a direct self-insured basis. Under this method, the School District must reimbursethe Employment Commission for all benefits charged against theSchool District. No provision has been made for possible futureclaims.

For a portion of the year, the School District was self-insured forvision, dental, and certain health benefits, including prescription drugcoverage and doctors visits paid on behalf of its employees.Payments are made to the insurance administrator on a continualbasis based on actual claims and administration fees incurred. TheSchool District estimates the liability for employee claims that havebeen incurred through the end of the fiscal year, including both thoseclaims that have been reported as well as those that have not yetbeen reported. These estimates are recorded in the district-widestatements. For governmental activities, the liability for healthbenefits is primarily liquidated by the general fund.

During the year, the School District terminated its self-insuredarrangement in favor of traditional premium-based coverage.

The change in estimated liabilities for incurred but not reportedbenefit claims for the year is as follows:

Estimated liability, beginning of the year 287,000$Estimated claims incurred including 809,138

changes in estimatesClaim payments (1,096,138)

Estimated liability, end of the year -$

NOTE 10 - PENSION PLANS AND POST EMPLOYMENTBENEFITS

Plan Description

The School District has a group of defined benefit and definedcontribution retirement plans covering substantially all employees.The plans are operated by the State of Michigan’s Public SchoolEmployees’ Retirement System (MPSERS), which is a cost-sharingmultiple-employer public employee retirement system (PERS).

The plans provide retirement, survivor and disability benefits to planmembers and their beneficiaries.

The system also provides postemployment healthcare benefits toretirees and their beneficiaries who elect to receive the benefits.

MPSERS operates within the Michigan Department of Technology,Management and Budget, Office of Retirement Services, under theauthority established by the Michigan Public School EmployeesRetirement Act (Retirement Act), as enacted and amended by theMichigan Legislature. The Michigan Legislature has the authority toamend the Retirement Act. The Michigan Department ofTechnology, Management and Budget issues a publicly-availablefinancial report that includes financial statements and required

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 18

supplemental information for MPSERS. The report providesinformation for the plans as a whole and information helpful forunderstanding the scale of the information presented relative to theSchool District. That report may be obtained by writing Office ofRetirement Services, P.O. Box 30171, Lansing, Michigan 48909-7671, calling 800-381-5111 or on the web athttp://www.michigan.gov/orsschools.

Full details on each of these plans are available on the MPSERSwebsite at the address provided above.

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 19

Pension Benefits

Employer contributions to MPSERS result from the applying rules and applicable changes of the School Finance Reform Act. Accordingly, eachschool district is required to contribute the full actuarial funding contribution amount to fund pension benefits. Depending on the plan selected, aplan member’s contribution may range from 0% to 7% of their gross wages. Plan members electing into the defined contribution plan are notrequired to make additional contributions.

For the period July 1, 2013 through September 30, 2013, employees had the following plan options with the corresponding employer contributionrates:

BasicMIP

PensionPlus

Pension PlusPHF (first worked

September 4,2012 or later)

Pension Plus to DCwith PHF (first

worked September 4,2012 or later)

Basic MIPDB to DCwith DBHealth

BasicMIP DBto DC

with PHF

BasicMIP with

PHF

Pension contributions 15.21% 15.02% 15.02% 12.78% 12.78% 12.78% 15.21%Health contributions 9.11% 9.11% 8.18% 8.18% 9.11% 8.18% 8.18%Defined contribution plan employer contributions:

DC 0.00% 1.00% 1.00% 3.00% 4.00% 4.00% 0.00% PHF 0.00% 0.00% 2.00% 2.00% 0.00% 2.00% 2.00%

For the period October 1, 2013 through June 30, 2014, employees had the following plan options with the corresponding employer contributionrates:

BasicMIP

PensionPlus

Pension PlusPHF (first worked

September 4,2012 or later)

Pension Plus to DCwith PHF (first

worked September 4,2012 or later)

Basic MIPDB to DCwith DBHealth

BasicMIP DBto DC

with PHF

BasicMIP with

PHF

Pension contributions 18.34% 18.11% 18.11% 15.44% 15.44% 15.44% 18.34%Health contributions 6.45% 6.45% 5.52% 5.52% 6.45% 5.52% 5.52%Defined contribution plan employer contributions:

DC 0.00% 1.00% 1.00% 3.00% 4.00% 4.00% 0.00% PHF 0.00% 0.00% 2.00% 2.00% 0.00% 2.00% 2.00%

Clio Area SchoolsNotes to Financial Statements

June 30, 2014

4 - 20

The School District’s required and actual contributions to the plansfor the years ended June 30, 2014, 2013, and 2012 wereapproximately $ 2,700,000, $ 2,440,000 and $ 2,450,000,respectively. Contributions made by the participants of the plan forthe year ended June 30, 2014 were approximately $ 18,000.

Post Employment Benefits

In addition to the pension benefits described above, state lawrequires the School District to provide post-retirement healthcarebenefits for eligible retirees and beneficiaries through the MichiganPublic School Employees Retirement System (MPSERS).

The 2012 Retirement Reform included changes to retiree healthcarebenefits. New employees hired after the effective date who elect thisbenefit are enrolled in the defined contribution Personal HealthcareFund. This establishes a portable tax-deferred account in which theparticipant contributes 2% of their salary, and receives a 2%employer match. These funds can be used to pay for healthcareexpenses in retirement.

Employees working prior to the enactment of the 2012 RetirementReform have two options: (a) the Personal Healthcare Fund, or(b) the defined benefit Premium Subsidy benefit.

Employees electing the defined benefit Premium Subsidy benefitcontribute 3% of their compensation, and the employer contributesan actuarially determined percent of payroll for all participants. Uponretirement members receive a premium subsidy towards health,dental and vision insurance. The subsidy is a percent of the premiumcost, with the percentage varying based on several factors.

For the periods July 1, 2013 through September 30, 2013, andOctober 1, 2013 through June 30, 2014, the employer contributionrate ranged from 8.18% to 9.11% and 5.52% to 6.45%, respectively.See the above two tables for rates.

The District's actual contributions match the required contributions forthe years ended June 30, 2014, 2013, and 2012 and wereapproximately $ 1,060,000, $ 1,450,000, and $ 1,390,000,respectively.

Unfunded Actuarial Accrued Liability

During the year ended June 30, 2014, the District had contributions inthe amount of $ 787,981 to the Michigan Public School EmployeeRetirement System (MPSERS). This amount represents theadditional employer contributions attributed to the unfunded actuarialaccrued liability (UAAL) rate, which was approximately 4.56% for theyear. These contributions are not included in the above tables.

NOTE 11 - CONTINGENT LIABILITIES

Amounts received or receivable from grantor agencies are subjectedto audit and adjustment by grantor agencies, principally the federalgovernment. Any disallowed claims, including amounts alreadycollected, may constitute a liability of the applicable funds. Theamount, if any, of costs which may be disallowed by the grantorcannot be determined at this time although the School Districtexpects such amounts, if any, to be immaterial. A separate report onfederal compliance has been issued for the year June 30, 2014.

The School District is a defendant in various lawsuits. In the opinionof management and the School District’s attorneys, both the outcomeand possible exposure to the District are not presently determinable.However, management believes any potential liability to the SchoolDistrict from the outcome of these lawsuits would be covered byinsurance.

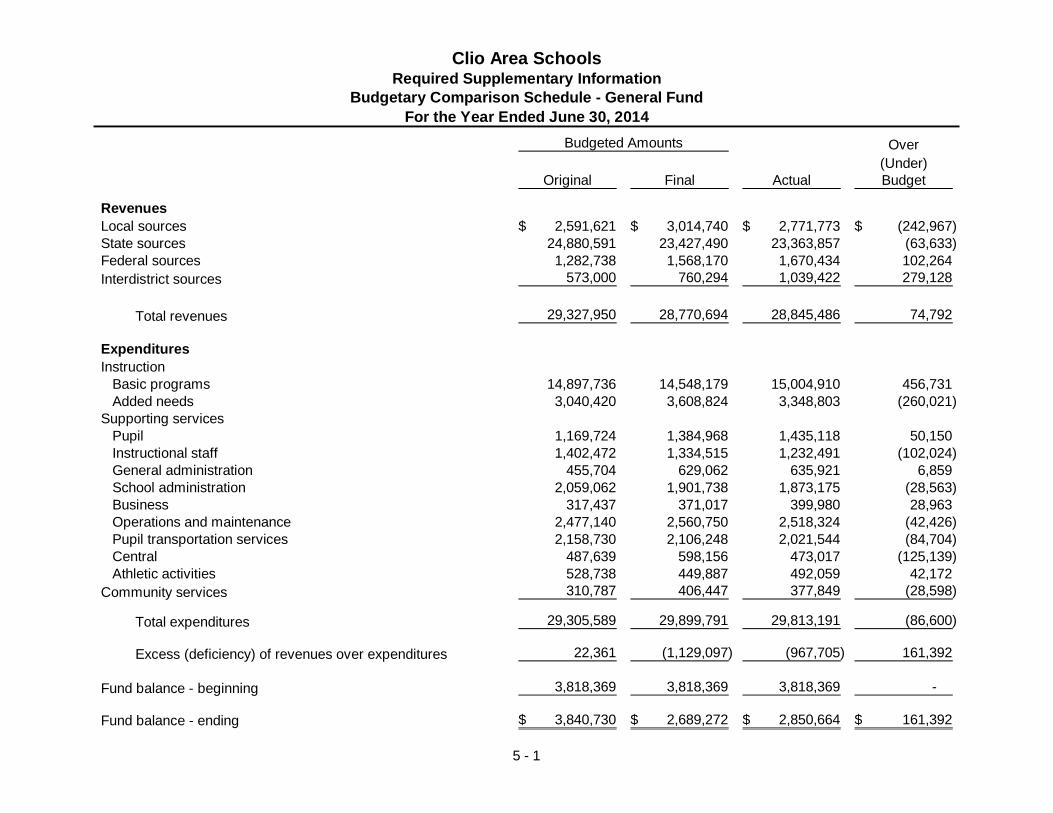

REQUIRED SUPPLEMENTARY INFORMATION

Over(Under)

Original Final Actual Budget

RevenuesLocal sources 2,591,621$ 3,014,740$ 2,771,773$ (242,967)$State sources 24,880,591 23,427,490 23,363,857 (63,633)Federal sources 1,282,738 1,568,170 1,670,434 102,264Interdistrict sources 573,000 760,294 1,039,422 279,128

Total revenues 29,327,950 28,770,694 28,845,486 74,792

ExpendituresInstruction

Basic programs 14,897,736 14,548,179 15,004,910 456,731Added needs 3,040,420 3,608,824 3,348,803 (260,021)

Supporting servicesPupil 1,169,724 1,384,968 1,435,118 50,150Instructional staff 1,402,472 1,334,515 1,232,491 (102,024)General administration 455,704 629,062 635,921 6,859School administration 2,059,062 1,901,738 1,873,175 (28,563)Business 317,437 371,017 399,980 28,963Operations and maintenance 2,477,140 2,560,750 2,518,324 (42,426)Pupil transportation services 2,158,730 2,106,248 2,021,544 (84,704)Central 487,639 598,156 473,017 (125,139)Athletic activities 528,738 449,887 492,059 42,172

Community services 310,787 406,447 377,849 (28,598)

Total expenditures 29,305,589 29,899,791 29,813,191 (86,600)

Excess (deficiency) of revenues over expenditures 22,361 (1,129,097) (967,705) 161,392

Fund balance - beginning 3,818,369 3,818,369 3,818,369 -

Fund balance - ending 3,840,730$ 2,689,272$ 2,850,664$ 161,392$

Budgeted Amounts

Clio Area SchoolsRequired Supplementary Information

Budgetary Comparison Schedule - General FundFor the Year Ended June 30, 2014

5 - 1

OTHER SUPPLEMENTARY INFORMATION

Special CapitalRevenue Projects Total

Fund Fund NonmajorGovernmental

Food Service Sinking Fund Funds

AssetsCash 251,543$ 1,018,909$ 1,270,452$Due from other funds 41,402 - 41,402Due from other governmental units 6,928 - 6,928Inventory 24,147 - 24,147Prepaid items 135,000 - 135,000

Total assets 459,020$ 1,018,909$ 1,477,929$

Nonmajor Governmental Funds

Clio Area SchoolsOther Supplementary Information

Combining Balance SheetJune 30, 2014

6 - 1

Special CapitalRevenue Projects Total

Fund Fund NonmajorGovernmental

Food Service Sinking Fund Funds

Nonmajor Governmental Funds

Clio Area SchoolsOther Supplementary Information

Combining Balance SheetJune 30, 2014

Liabilities and Fund BalanceLiabilities

Accounts payable 73,764$ 9,975$ 83,739$Due to other funds - 76,423 76,423

Total liabilities 73,764 86,398 160,162

Fund Balance Non-spendable

Inventory 24,147 - 24,147 Prepaid items 135,000 - 135,000Restricted for: Food service 226,109 - 226,109Assigned for: Capital projects - 932,511 932,511

Total fund balance 385,256 932,511 1,317,767

Total liabilities and fund balance 459,020$ 1,018,909$ 1,477,929$

6 - 2

Special CapitalRevenue Projects Total

Fund NonmajorGovernmental

Food Service Sinking Fund Funds

RevenuesLocal sources 318,393$ 914,601$ 1,232,994$State sources 73,980 - 73,980Federal sources 889,048 - 889,048

Total revenues 1,281,421 914,601 2,196,022

ExpendituresCurrent

Food services 1,214,268 - 1,214,268Capital outlay - 247,321 247,321

Total expenditures 1,214,268 247,321 1,461,589

Excess of revenues over expenditures 67,153 667,280 734,433

Fund balance - beginning 318,103 265,231 583,334

Fund balance - ending 385,256$ 932,511$ 1,317,767$

Clio Area SchoolsOther Supplementary InformationNonmajor Governmental Funds

Combining Statement of Revenues, Expenditures and Changes in Fund BalanceFor the Year Ended June 30, 2014

Fund

6 - 3