cmc case study: the prince of thieves. - ice australia case study: the prince of thieves. the...

TRANSCRIPT

CMC Case Study: The Prince of

Thieves.The Queensland Health Perspective

Luke Viney, Principal Prevention OfficerLuke Viney, Principal Prevention Officer

Ethical Standards Unit, Queensland Health

The Headlines

Fake Prince Sentenced to 14 Years for

$16.6m theft from Queensland Health

Premier Bligh Demands AnswersPremier Bligh Demands Answers

AG finds fraud risk ‘unacceptably high’

$16m fraud sparks QH overhaul

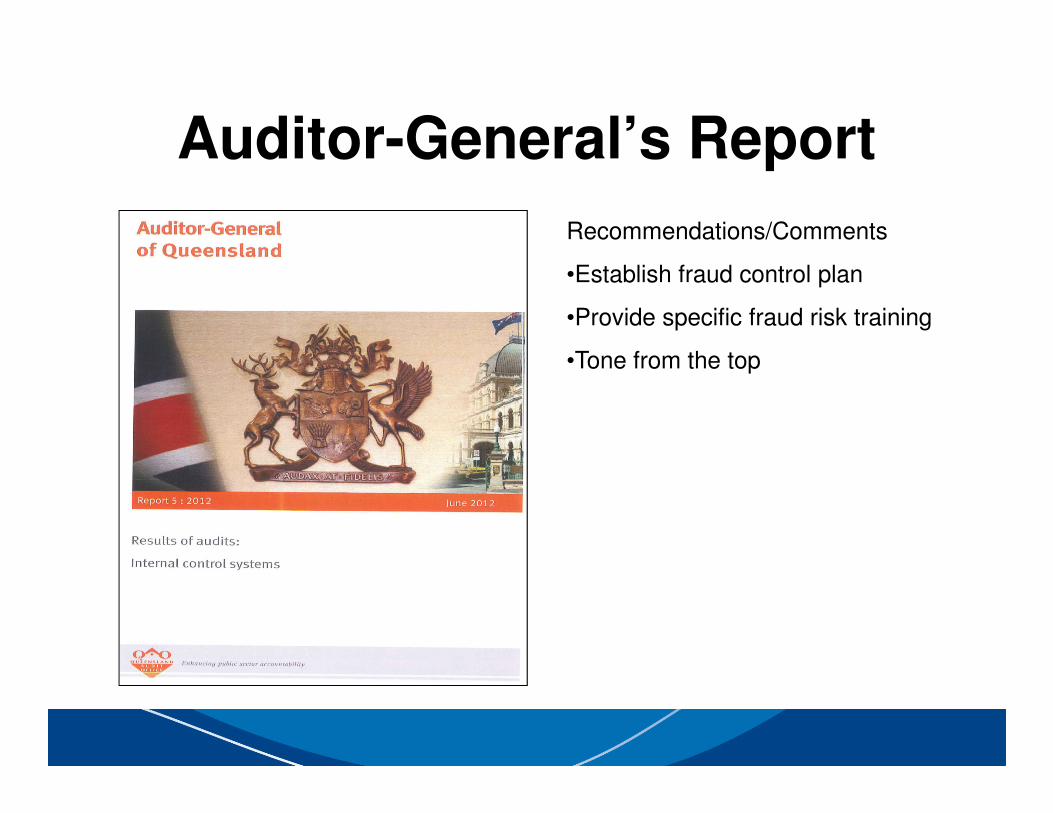

Auditor-General’s Report

Recommendations/Comments

•Establish fraud control plan

•Provide specific fraud risk training

•Tone from the top

Defining the Fraud Risk Landscape

QH Employment Streams

MedicalOperational

Trades, Artisans and General

Medical

Nursing

HP, Professional and Technical

Managerial and Clerical

Operational

Fraud Control Policy and Governance

Cultural Change: Starting at the Top

Concerns Reported Per 100 Employees

0.3

0.35

0.4

0.45

Rep

ort

s/1

00 E

mp

loyees

Complaints Per 100 Staff

Cultural Change: Starting at the Top

0

0.05

0.1

0.15

0.2

0.25

July

Aug

ust

Sep

tem

ber

Oct

ober

Nove

mbe

rD

ecem

ber

Janu

aryFeb

ruar

yM

arch

Apr

ilM

ay

June

Month

Rep

ort

s/1

00 E

mp

loyees

Complaints Per 100 Staff

11/12

Complaints Per 100 Staff

12/13

Fraud Awareness Training

• In business groups

• Core plus customised content– Fraud motivators

– Red flag behaviour

– Transactional red flags– Transactional red flags

– Reporting concerns

– Internal Controls

• Relevance

• Accessibility

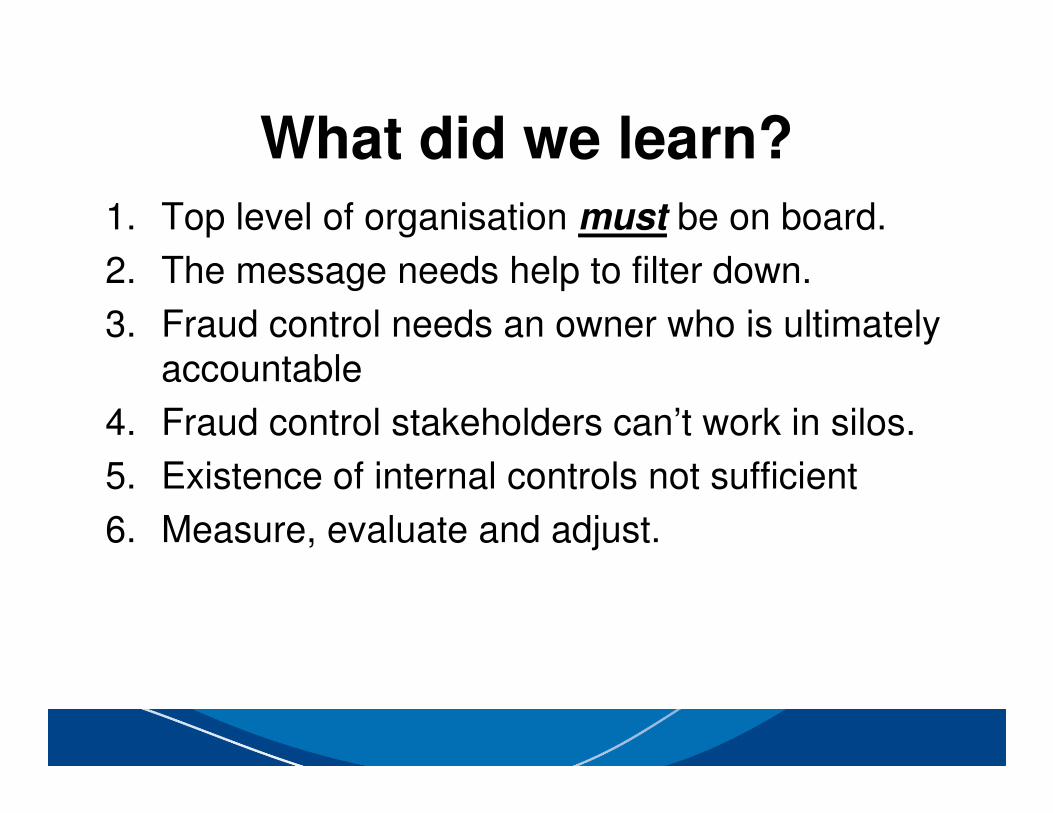

What did we learn?

1. Top level of organisation must be on board.

2. The message needs help to filter down.

3. Fraud control needs an owner who is ultimately

accountable

4. Fraud control stakeholders can’t work in silos.4. Fraud control stakeholders can’t work in silos.

5. Existence of internal controls not sufficient

6. Measure, evaluate and adjust.

Questions?Questions?